the digital shelf the opportunity for search in packaged goods yahoo! search marketing proprietary...

TRANSCRIPT

THE DIGITAL SHELFTHE OPPORTUNITY FOR SEARCH INPACKAGED GOODS

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Presented By:James Lamberti, SVP, comScoreMatt Wilburn, Sr. Director, Yahoo!

October 2007

2

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

THE ROLE OF SEARCH Marketing the Motivation

LONGEVITY CONTINUUM

MOTIVATION CONTINUUM

“I suffer from

allergies”

“I bought a new home”

“I have a new baby”

Occasion Based

Lifestage

Lifestyle

PermanentTemporaryImmediate

“I stained

my carpet”

3

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

THE OPPORTUNITY FOR BRAND Understanding the Motivation

LONGEVITY CONTINUUM

MOTIVATION CONTINUUM

Occasion Based

Lifestage

Lifestyle

PermanentTemporaryImmediate

Future: Huge Opportunity

is here!(e.g. branding, need

states)

Current CPG view - search as

direct marketing

(e.g. transactional)

4

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

• To understand how consumers use search to find information about consumer packaged goods

• To understand the marketing opportunity available in search for packaged goods companies

• To quantify the value of packaged goods searchers both demographically and attitudinally

THE DIGITAL SHELF Study Objectives

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

5

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Survey Attitudes of Searchers and Non-Searchers Category Engaged (n = 2,800) across 4 categories:

• Household • Baby Products• Personal Care• Packaged Foods

Survey Fielded: June and July 2007

Behavioral What are they doing online?

Clickstream Behavior Observed: February – April 2007 on comScore 1 million+ panel

BACKGROUND & METHODOLOGY

THE CONSUMERSizing and Search Marketing Opportunity

THE MOTIVATIONUnderstanding Their Needs

THE VALUEComparing Searchers & Non-Searchers

THE OPPORTUNITYQuantifying the $$ Opportunity for Search Marketing

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

6

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

BACKGROUND & METHODOLOGY

2 million PanelAttitudinal(20-min survey)

What do they think?

Behavioral (Click Stream)

What are they doing?

Population Visitors to CPG Related Sites in past 30 days

Total US Internet Population Visitors to CPG Related Sites or

Searched on CPG Related Terms

Time Period June – July 2007 3 Months Ending April 2007

Sample Size

n = 2,800; 700 per category,

500 Searchers, 200 Non-Searchers

Over 1MM Panelists

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

7

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

CPG CATEGORIES ANALYZED

PACKAGED FOOD

PRODUCTS

PACKAGED FOOD

PRODUCTS

BABY CARE

BABY CARE

PERSONAL CARE

PERSONAL CARE

HOME CARE

HOME CARE

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Who are searchers?

Sizing the Opportunity

9

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

THE SEARCH MARKETING OPPORTUNITYAll CategoriesNearly half of Internet Users search on CPG related terms or visit CPG related sites.

USING SEARCH

Source: comScore Marketing Solutions; 3 Months Ending April 2007 – Total U.S.

Food

Baby

Personal Care

Household

93.7MM 43.8MM

26.0MM 15.7MM

35.9MM 9.8MM

7.3MM 1.7MM

% INTERNET REACH

UNIQUE VISITORS

UVs USESEARCH

10

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

SIZING THE SEARCH MARKETING OPPORTUNITYBaby Products Example

1 U.S. Internet Population 203 Million

2 Monthly Site Category Penetration

13%

3 Category Involved Consumers

26.0 Million

4 % Using Search 60%

5 Search Marketing Opportunity

15.6 Million

11

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

SEARCHERSU.S.

POPULATION

Average Income $63.3k $45K

Average Age 40.6 46.2

Female 78% 50%

4 yr. College or Better Education 45% 22%

Demographic & Life Stage Questions: Base: Searcher (n = 2,011); Non – Searcher (n= 803) = Significant difference at 95% confidence

Demographic Profile

Searchers are more affluent, younger, and more likely to be female

12

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

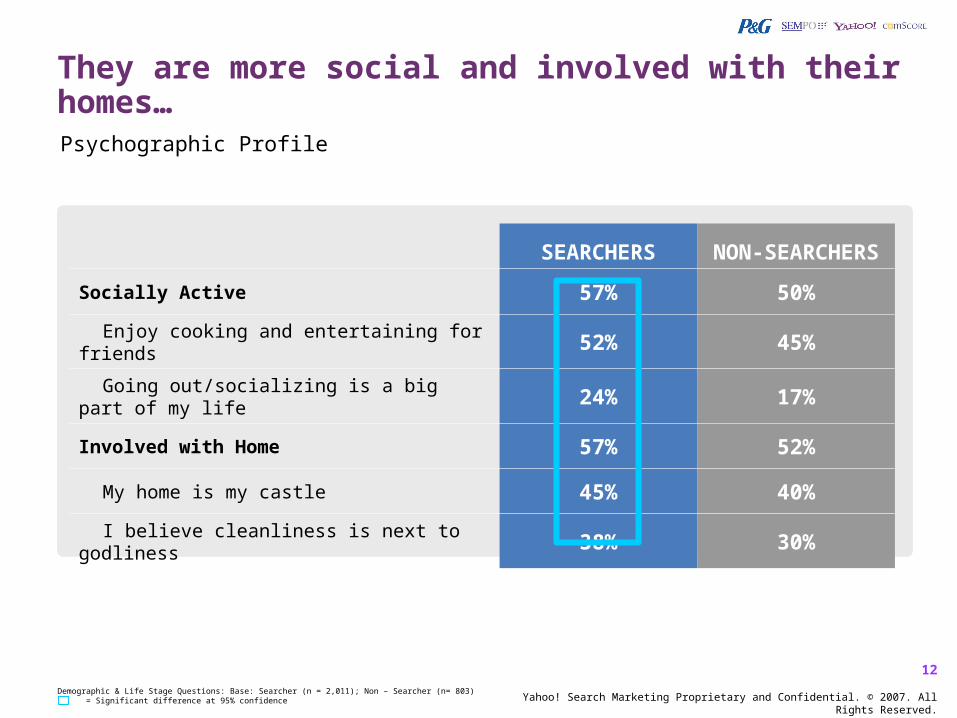

They are more social and involved with their homes…Psychographic Profile

Demographic & Life Stage Questions: Base: Searcher (n = 2,011); Non – Searcher (n= 803) = Significant difference at 95% confidence

SEARCHERSNON-

SEARCHERS

Socially Active 57% 50%

Enjoy cooking and entertaining for friends 52% 45%

Going out/socializing is a big part of my life 24% 17%

Involved with Home 57% 52%

My home is my castle 45% 40%

I believe cleanliness is next to godliness 38% 30%

13

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

39%

35%

27%

28%

23%

13%

Q6: Besides search engines, what other sources, if any, did you use the last time you got information for the following categories? Please check all that apply. Searcher (n = 2,011); Non – Searcher (n= 803))

= Significant difference at 95% confidence, * Significant difference at 90% Confidence.

In-Store

Offline Media

Friends and family

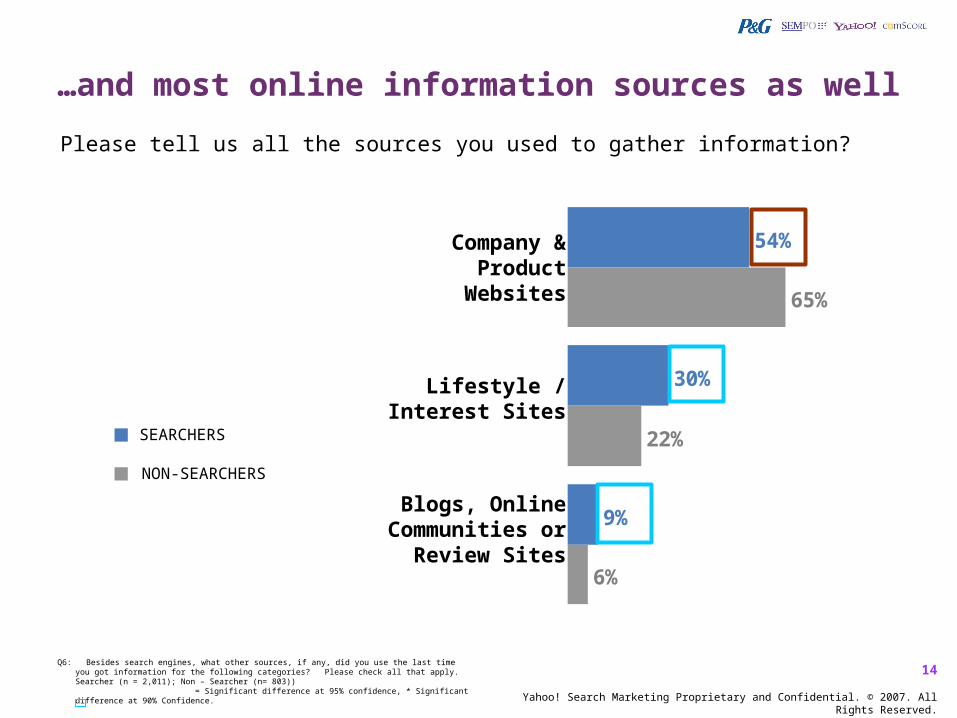

…and they are hyper engaged, leveraging a larger number of offline sources to gather information…Please tell us all the sources you used to gather information?

SEARCHERS

NON-SEARCHERS

14

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

54%

30%

9%

65%

22%

6%

Q6: Besides search engines, what other sources, if any, did you use the last time you got information for the following categories? Please check all that apply. Searcher (n = 2,011); Non – Searcher (n= 803))

= Significant difference at 95% confidence, * Significant difference at 90% Confidence.

Company & Product

Websites

Lifestyle / Interest Sites

Blogs, Online Communities or

Review Sites

…and most online information sources as well

Please tell us all the sources you used to gather information?

SEARCHERS

NON-SEARCHERS

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

What are customers

looking for?

16

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

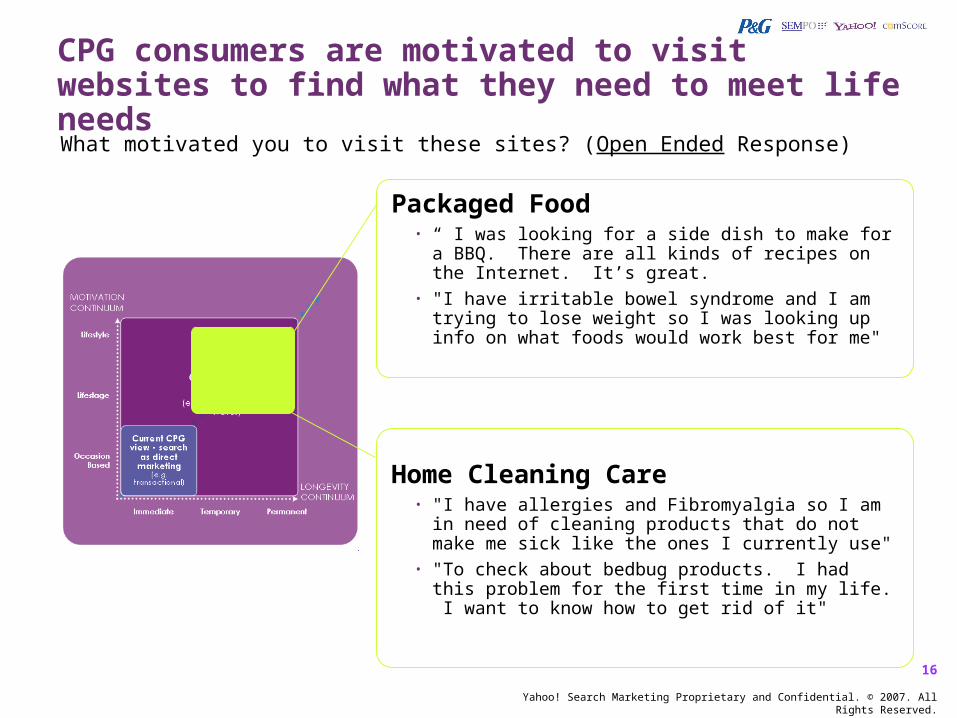

Packaged Food• “ I was looking for a side dish to make for a BBQ.

There are all kinds of recipes on the Internet. It’s great.

• "I have irritable bowel syndrome and I am trying to lose weight so I was looking up info on what foods would work best for me"

Home Cleaning Care• "I have allergies and Fibromyalgia so I am in

need of cleaning products that do not make me sick like the ones I currently use"

• "To check about bedbug products. I had this problem for the first time in my life. I want to know how to get rid of it"

CPG consumers are motivated to visit websites to find what they need to meet life needsWhat motivated you to visit these sites? (Open Ended Response)

17

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Personal Beauty • "I am always trying to find something new to combat

aging, acne, and to cover up these issues. I like to research what will work best on my skin"

• "I've been wanting information about a problem I'm having with hair loss"

• "My skin is rather dry and I sometimes do not get enough sleep, so I was looking for products that would reduce lack of sleep signs that can show around the eyes"

Baby Products• "I have a daughter that has accidents at night and I

wanted to find the best product for her to use"

• "Wanted to find out what kind of disposable training pants to buy and the different types of pull ups that were available"

This is consistent across categories

What motivated you to visit these sites? (Open Ended Response)

18

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

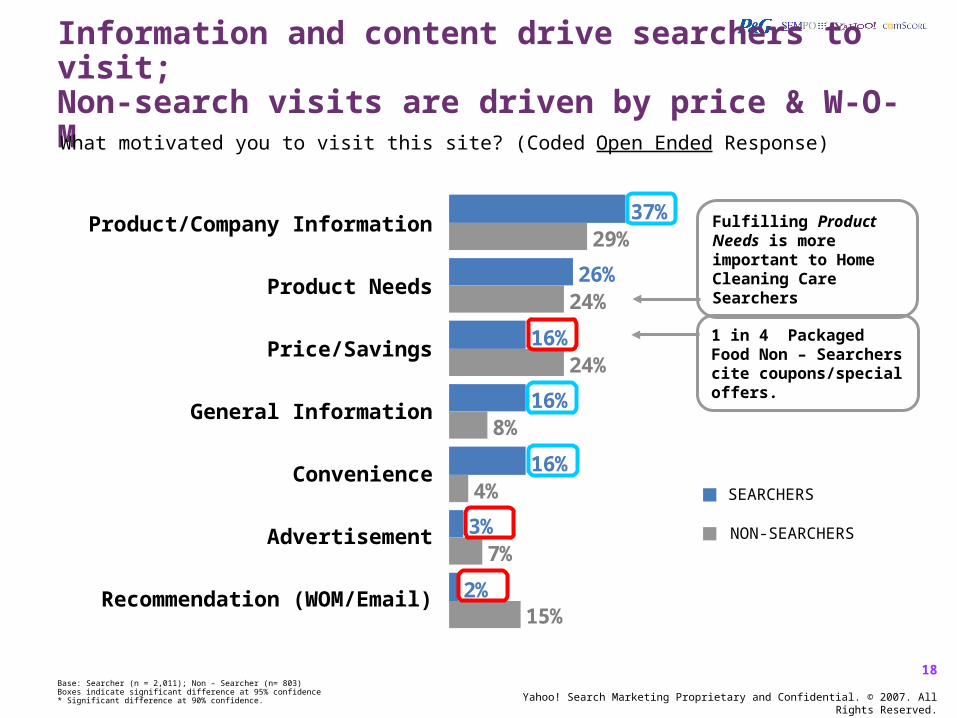

Information and content drive searchers to visit; Non-search visits are driven by price & W-O-MWhat motivated you to visit this site? (Coded Open Ended Response)

Product/Company Information

Product Needs

Price/Savings

General Information

Convenience

Advertisement

Recommendation (WOM/Email)

37%

26%

16%

16%

16%

3%

2%

29%

24%

24%

8%

4%

7%

15%

SEARCHERS

NON-SEARCHERS

Fulfilling Product Needs is more important to Home Cleaning Care Searchers

1 in 4 Packaged Food Non – Searchers cite coupons/special offers.

Base: Searcher (n = 2,011); Non – Searcher (n= 803) Boxes indicate significant difference at 95% confidence* Significant difference at 90% confidence.

19

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

48%

44%

40%

40%

36%

31%

29%

26%

21%

36%

38%

28%

47%

23%

15%

22%

10%

10%

… and they go to great lengths to get it, exhibiting significantly deeper category engagementWhat motivated you to visit this site? (Select as many that apply)

Find more information products

Learn about new products

Help me make a purchase decision

Find out about special offers

Get/compare product prices

Find where to buy/local places

See official company website

Compare competitive products

Consumer and professional reviews

Q3: Thinking about each category separately, what made you want to go online the last time you were looking for information about each? You may have various reasons so feel free to check as many as apply.

Base: Searcher (n = 2,011); Non – Searcher (n= 803) = Significant difference at 95% confidence, * Significant difference at 90% Confidence.

SEARCHERS

NON-SEARCHERS

20

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

SEARCHERS

NON-SEARCHERS

73%

64%

47%

29%

58%

44%

59%

22%

Information & Help

Purchase Decision

Promotion

Company Website

Q3: Thinking about each category separately, what made you want to go online the last time you were looking for information about each? You may have various reasons so feel free to check as many as apply.

Base: Searcher (n = 2,011); Non – Searcher (n= 803) = Significant difference at 95% confidence, * Significant difference at 90% Confidence.

Searchers want product information and help making a purchase decision…What motivated you to visit this site? (Select as many that apply)

21

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

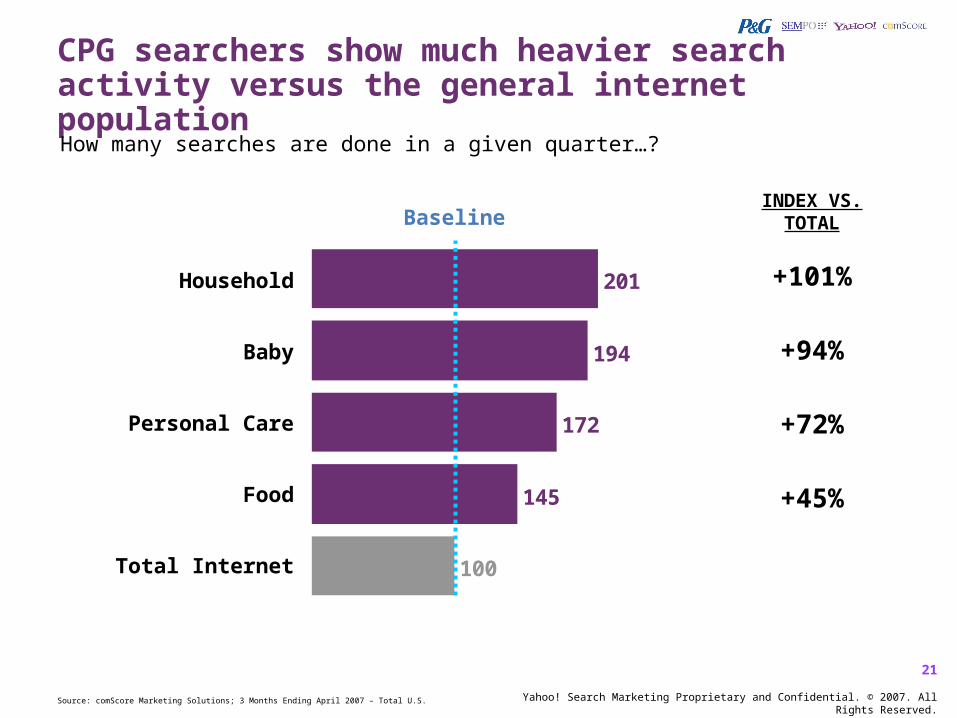

145

172

194

201

100

CPG searchers show much heavier search activity versus the general internet populationHow many searches are done in a given quarter…?

BaselineINDEX VS.

TOTAL

+101%

+94%

+72%

+45%

Household

Baby

Personal Care

Food

Total Internet

Source: comScore Marketing Solutions; 3 Months Ending April 2007 – Total U.S.

22

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

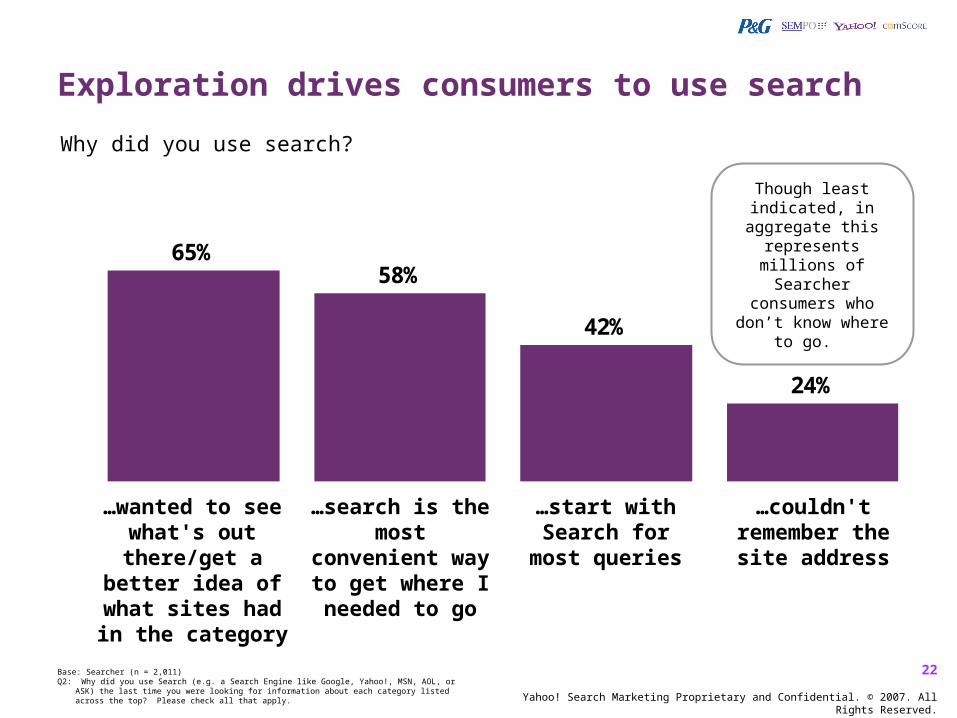

65%58%

42%

24%

Though least indicated, in

aggregate this represents millions

of Searcher consumers who

don’t know where to go.

Exploration drives consumers to use search

Why did you use search?

Base: Searcher (n = 2,011)Q2: Why did you use Search (e.g. a Search Engine like Google, Yahoo!, MSN, AOL, or ASK) the last

time you were looking for information about each category listed across the top? Please check all that apply.

…wanted to see what's out there/get a

better idea of what sites had in the category

…search is the most

convenient way to get

where I needed to go

…start with Search for

most queries

…couldn't remember the site address

23

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

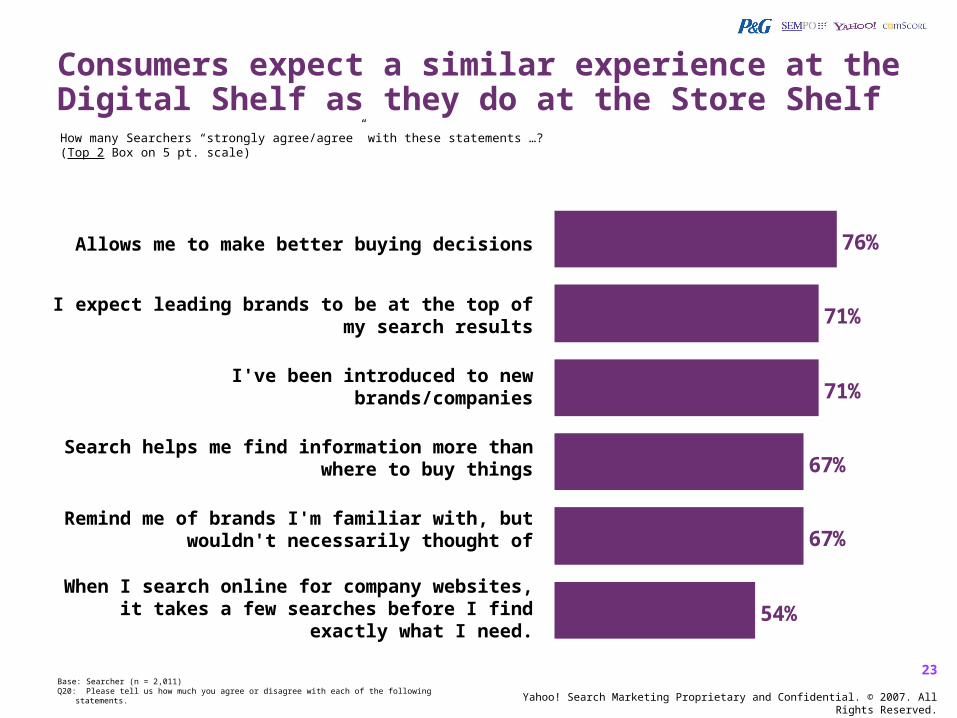

76%

71%

71%

67%

67%

54%

Base: Searcher (n = 2,011)Q20: Please tell us how much you agree or disagree with each of the following statements.

Allows me to make better buying decisions

I expect leading brands to be at the top of my search results

I've been introduced to new brands/companies

Search helps me find information more than where to buy things

Remind me of brands I'm familiar with, but wouldn't necessarily thought of

When I search online for company websites, it takes a few searches before I find exactly

what I need.

Consumers expect a similar experience at the Digital Shelf as they do at the Store ShelfHow many Searchers “strongly agree/agree” with these statements …? (Top 2 Box on 5 pt. scale)

24

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Searchers can be influenced to switch brands based on factors other than priceThinking about your last purchase, did you switch brands? Why did you switch?

29%36%

Searchers Non-Searchers

QA14/11a: Did you switch to another brand? Base: Searchers (n = 1,893); Non-Searchers (n = 751) QA15/12a: Why did you switch? Base: Searchers (n = 625); Non-Searchers (n = 208) = Significant difference at 90% confidence.

Price (Main Reason for

Switching)

• Searchers 27%• Non- Searchers

38%

25

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

SEARCHERS

NON-SEARCHERS

26%21%

17%

7% 5%

21%26%

13%

3% 2%

Cross-media messaging creates demand for more informationDid any of the following compel you to look for information?

Q5: Still thinking about the last time you got information online about each category, which, if any, of the following compelled you to get more information? Please check all that apply.

Base: Searcher (n = 1,960); Non – Searcher (n= 709). = Significant difference at 95% confidence

TV Ad Online/ website Ad

Print ad Radio Ad Billboard

26

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

SEARCHERS

NON-SEARCHERS

73%

52%36% 28%35%

58%

29% 22%

Search is critical both for content and product sitesHow do you usually get to these websites…?

Use a Search Engine

Type in address

Linked from a

Lifestyle/Interest site

Have these sites

bookmarked

56%

33%47%

36%34% 31%47% 39%

COMPANYPRODUCTWEBSITES

LIFESTYLEWEBSITES

Q24: How do you usually get to these types of sites? Base: For Lifestyle Websites Searcher (n = 661); Non – Searcher (n= 135). For Company Product

Websites Searcher (n = 1,737); Non – Searcher (n = 700). = Significant difference at 95% confidence

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

The Value of

Searchers

28

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Searchers spend 20% more in the category than non-searchers…

THE VALUE OF SEARCHERS Category Spending

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

SEARCHERS NON – SEARCHER

Packaged Food Products $51.91 $41.69

Home Cleaning Care Products $40.30 $32.34

Personal Beauty $52.19 $46.36

Baby Products $62.56 $52.09

QD2: In the past 30 days, how much have you spent in total on <INSERT PRODUCT CATEGORY ASSIGNED>? (Your best estimate is fine.) Base: Searcher (n = 2,011); Non – Searcher (n= 803) = Significant difference at 95% confidence.

29

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

1. Go out of my way to recommend good products and brands

2. Social and well-connected

3. Others look to me for advice when it comes to technology

4. I am a natural leader; people always listen to my opinions

5. A good brand is worth talking about

6. I tend to be one of the first among my friends to try new products

7. I often tell friends about products that interest me

52% of CPG searchers are also brand advocates… and this defines a Brand AdvocateUsing segmentation we separate buyers into two groups

Source: Engaging Advocates with Search and Social Media | December 2006Across 4 Verticals: Auto, Consumer Electronics, Home Loans, and Hotel BookingsFindings Derived from Segmentation Using over 30 Psychographic Attributes

30

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

More open to influence, considering more brands prior to making a purchase

However, once they make their purchase, they are more loyal to the brands they buy

50%+ write about their purchases online, with the large majority writing something positive (90%)

A 2-to-1 rate of converting someone to make the exact same purchase

Why are brand advocates important

Using segmentation we separate buyers into two groups

Source: Engaging Advocates with Search and Social Media | December 2006Across 4 Verticals: Auto, Consumer Electronics, Home Loans, and Hotel BookingsFindings Derived from Segmentation Using over 30 Psychographic Attributes

31

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

CPG searchers are significantly more likely to be brand advocates and convince friends to purchaseUsing segmentation we separate buyers into two groups

QA18/15a: How likely are you to recommend the brand to friend, family member, or colleague? Base: Searchers who recall brand (n = 1,952); Non-Searchers who recall brand (n = 769)

QA19/16a: Did you convince or persuade at least one friend or family member to buy the brand? Base: Searchers who recall brand (n = 1,768); Non-Searchers (n = 683) = Significant difference at 95% confidence, * and = Significant difference at 90% confidence.

SearchersNon-

Searchers

Brand Advocate 52% 38%

Did you convince someone to purchase the same [CPG category] brand/product?

Plan to Purchase 22% 16%

Already Purchased

41% 33%

32

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

* Market = Visited CPG related website in the category in past month

Advocacy extends the reach potential of search marketing dramatically

21.9MM12.2MM2.3MM58.4MMExtended Reach Estimate

SearcherSearcherSearcherSearcher

2.4MM

55%

4.4MM

45%

9.8MM

Personal Beauty Products

14.6MM

64%

22.8MM

52%

43.8MM

Packaged Food Products

.6MM

64%

.9MM

51%

1.7MM

Home Cleaning Care Products

6.2MMAdvocacy Impact

69%Conversion Rate

8.9MMUnique Searchers Who Advocate

57%

15.7MM

Baby Products

Unique Searchers

% Brand Advocates

+ 33% + 35% + 24% + 39%

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Key Searcher

Segments

34

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Predictive Factors Examined 100+ variables from the questionnaireFrom this, 13 factors identified as predictive

• Interact with site • Help make decision• Product information• What others say• Environment/safety• Company info• Save money• Use new media• Search to brands• Search for info• Brand advocate• Influencer• Leader/expert

SEGMENTATION METHODOLOGY

4-STEP STATISTICAL PROCESS(1) Identified key concepts in data using multiple iteratively applied statistical processes

(2) Employed 3-stage cluster analysis

(3) Used discriminate analysis to assess the reliability of the cluster solutions and identify ways that the clusters differed from each other

(4) Repeated steps 2 and 3 until a stable and business relevant solution emerged – which turned out to be a 7 cluster solution

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

35

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Brand AdvocatesInterested & Engaged

Value Conscious Consumers

Curious, strongly motivated, brand conscious in search activities, most receptive to visiting CPG related websites with product related information, benefits, and incentives

Normal or somewhat higher on most measures, motivated by product features

Younger, higher income families, enjoy cooking/entertaining

Motivated by product features, curious

Motivated by product/company information, search to fulfill personal needs,

Single, older, lower income

Low motivation, media has little impact

Least likely to switch brands/switch on price, lowest spenders

Stay-at-home, older, lower income

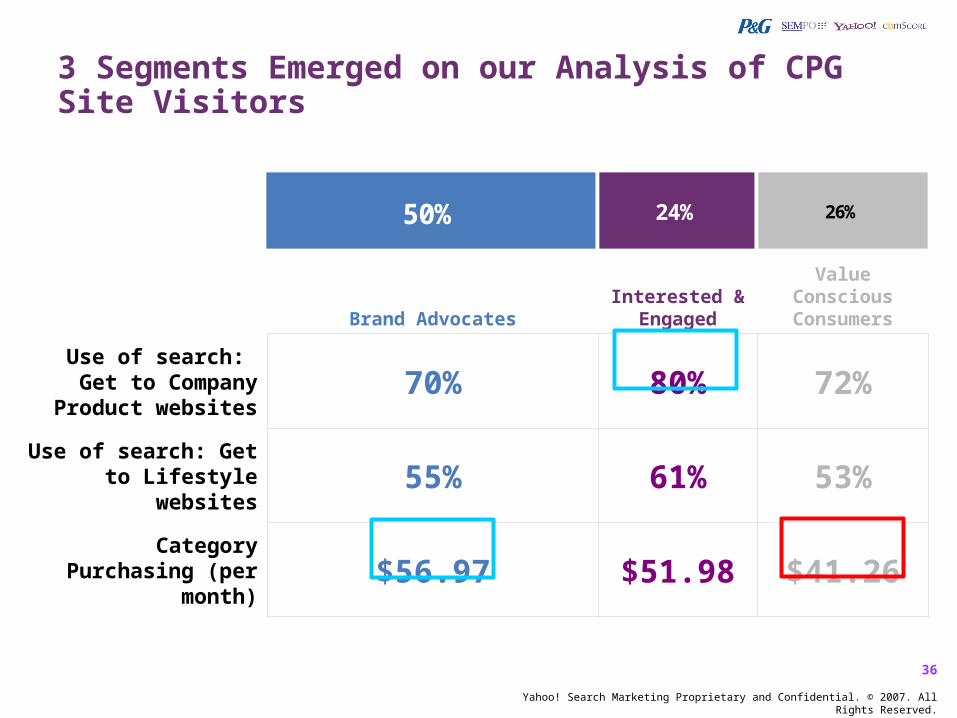

3 Segments Emerged on our Analysis of CPG Site Visitors

24% 26%50%

36

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

3 Segments Emerged on our Analysis of CPG Site Visitors

24% 26%50%

Brand Advocates

Interested & Engaged

Value Conscious Consumers

Use of search: Get to Company

Product websites70% 80% 72%

Use of search: Get to Lifestyle

websites55% 61% 53%

Category Purchasing (per

month)$56.97 $51.98 $41.26

37

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Brand Advocates

Media influence on search• Similar to Information Seekers

• Billboard: 7%

Overall Attitudes and behaviors• Very strong band advocates: 73%• Persuasive – already purchased brand:

64%• Switched brands: 40%

• On product features: 54%• On price: 23%

• Vocal, post online reviews: 34% past 3 months

• Active researchers, compare products online weekly or more often: 47%

Search: Motivations for using and attitudes

• Brand focused• Expect leading brands to be at the

top of my search results: 42%• Reminds me of familiar brands: 32%

• More intense searches• Takes a few searches before I find

exactly what I need: 27%

Motivations for CPG site visitation• Generally higher than Low Value Consumers

but mostly lower than Information Seekers• But, more responsive to incentives to visit

company/product websites• Product prices: 49%• Contests to win prizes: 44%• Opportunity to learn about new

products: 47%• Ability to compare competitive

products: 43%

Search Usage

Category Spending

Advocacy & LeadershipSegment Size

(35.5MM Users)

50%

Demographic profile• 77% female• Average age: 39.7 years• Average income: $65.8K• 4 year college or greater: 46%• Married with kids at home: 42%• Single: 21%

38

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

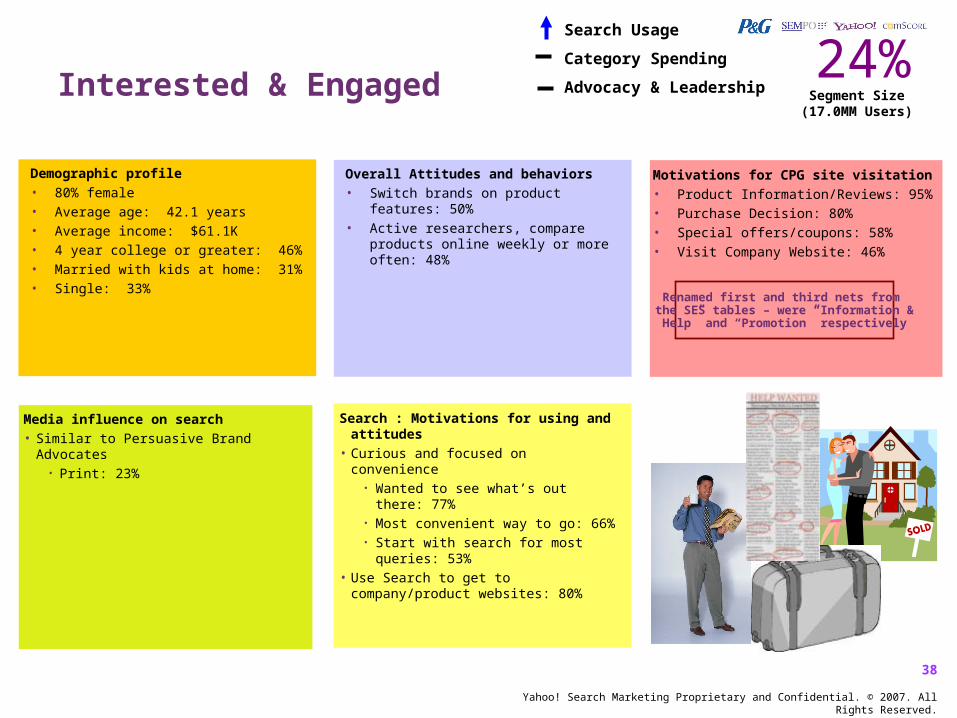

Search Usage

Category Spending

Advocacy & LeadershipInterested & Engaged

Media influence on search• Similar to Persuasive Brand Advocates

• Print: 23%

Overall Attitudes and behaviors• Switch brands on product features:

50%• Active researchers, compare products

online weekly or more often: 48%

Search : Motivations for using and attitudes

• Curious and focused on convenience• Wanted to see what’s out there:

77%• Most convenient way to go: 66%• Start with search for most queries:

53%• Use Search to get to company/product

websites: 80%

Motivations for CPG site visitation• Product Information/Reviews: 95%• Purchase Decision: 80%• Special offers/coupons: 58%• Visit Company Website: 46%

Demographic profile• 80% female• Average age: 42.1 years• Average income: $61.1K• 4 year college or greater: 46%• Married with kids at home: 31%• Single: 33%

Segment Size(17.0MM Users)

24%

Renamed first and third nets from the SES tables – were “Information &Help” and “Promotion” respectively

39

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Search Usage

Category Spending

Advocacy & LeadershipValue Conscious Consumers

Media influence on search• Very low impact

Attitudes and behaviors• Lower scores than other segments

nearly across the board• Less active socially: 43%• Low Involvement with their

home: 43%• Brand Advocacy is very low:

14%• Motivated more by price than other

segments when switching brands: 39%

Search : Motivations for using and attitudes

• More limited in all areas

Motivations for CPG site visitation• Least motivated across the board

Demographic profile• 79% female• Average age: 41.0 years• Average income: $60.6K• 4 year college or greater: 42%• Married with kids at home: 39%• Single: 25%

Segment Size(18.5MM Users)

26%

40

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

REACH

• Nearly half of internet users searched using CPG keywords and/or visited a CPG-related site during the past 90 days.

• Nearly half of CPG site traffic originates with search– this is higher than most categories. Search is the starting point for both consumers and brands.

• CPG Searchers use search 2X as much as the general internet population. In aggregate they represent scalable audiences with considerable spending power and influence.

RELEVANCE

• Demographic, attitudinal and behavioral data about CPG searchers reveals a profile of a more affluent, younger, female and more media-savvy consumer.

• CPG searchers say they are seeking information to help with purchase decisions and to find relevant CPG content. Their search activity demonstrates active interest and openness to influence.

• You’re competing with other brands and ‘non-brand’ site for their attention.

Research Highlights

41

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

RESULTS

• CPG searchers link their search activity with purchase intent and skew away from price as the reason to switch brands. Active, responsive.

• CPG Searchers report spending 20% more money in store, in-category, during the 30 days around their search activity.

• They are much more likely to be ‘brand advocates’ and share their recommendations with friends and family. Multiplier effect.

IMPLICATIONS

• These insights challenge the notion that search “doesn’t fit” for CPG brands: It scales, it reaches a valuable and engaged consumer. It is a more efficient and personal message delivery vehicle than other media.

• CPG advertisers should treat the search results page like a retail store shelf: is the brand present? Is it easy to find? Is it packaged to sell?

• Position your brand through search to reinforce and extend association with key brand equities. Ladder up! (Temporary –> Lifestage -> Lifestyle).

Research Highlights

42

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

The result of over 50 years of Olay

research, Olay

spent millions on positioning

Regenerist as a premium and revolutionary

new product for anti-aging

skincare

THE MISSED OPPORTUNITY The Digital Shelf

anti aging skin care

Neutrogena is advertising to engaged category consumers at a critical brand-building moment…at the digital shelf, Olay is out-of-stock.

43

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

THE MISSED OPPORTUNITY The Digital Shelf

Iams is spending

millions on launching

Healthy Naturals dog food…

natural dog food

…but a competitor is outbidding them (by less than $1!), resulting in poor placement

44

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

THE MISSED OPPORTUNITY The Digital Shelf - Even Digital Leaders Can Improve

Kellogg’s spent millions on

packaging and advertising to link “Organic”

to their brands…

organic cereal

Kellogg’s Organic products don’t appear on the “digital shelf” – but its competitor does with wholegrainnation.com. This is a missed opportunity with an engaged consumer.

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

THANK

YOU

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Why search should matter to P&G

47

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Search is more important to P&G brand switchers who are engaged in the categoryHow important is Search….”? (Top Box & Top 2 Box on 5 pt. scale)

Q17: How important was using Search (e.g. a Search Engine like Google, Yahoo!, MSN, AOL, or ASK) in helping you make your purchase of < INSERT BRAND FROM Q11. IF Q11 = “Don’t know / Can’t recall” INSERT “the brand you most recently purchased” >. Base sizes vary by usage. = Significant difference at 95% confidence, = Significant difference at 90% confidence.

40%

29%

Veryimportant

Somewhatimportant40% 44% 39% 36% 35%

29% 27%28% 33%

18%

69% 71% 67% 69%

53%

Any 3 P&G

Home Cleanin

g

Personal

Beauty

Baby Product

s

Did Not Switch

36% 37% 37% 44%

32%18% 22%

34%

68%

55%59%

77%

Visited All 3

Visited Any 2

Visited Any 1

1st Time Baby

Products

Search is especially important to point of

entry buyers.

Switched to P&G Brand

# of P&G Category Sites Visited & Point of Entry

48

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Searchers are more successful in converting their friends to buy P&G productsHow likely are you to recommend your P&G brand…? Did they purchase or do they plan to purchase the P&G brand…?

Q18: How likely are you to recommend <INSERT BRAND CHECKED IN Q11 IF CODES = 1 – X OR “VERBATIM COMMENT” IF “Other (Please specify)”> to friend, family member, or colleague? Base: Searchers who recall P&G brand bought (n = 1,059); Non-Searchers who recall P&G brand bought (n = 374) Q19: Did you convince or persuade at least one friend or family member to buy the brand? Base: Searchers who recall brand (n = 966); Non-Searchers (n = 333 ) = Significant difference at 95% confidence, = Significant difference at 90% confidence.

Searchers

Definitely Recommend Purchase

51%

67%

Plan to Purchase

18%

Purchased

49%

Non-Searchers

Definitely Recommend Purchase

56%

52%

Plan to Purchase

15%

Purchased

37%

10.1MMpeople

11.4MMpeople

Personal Beauty &

Baby Products

Personal Beauty &

Baby Products

49

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

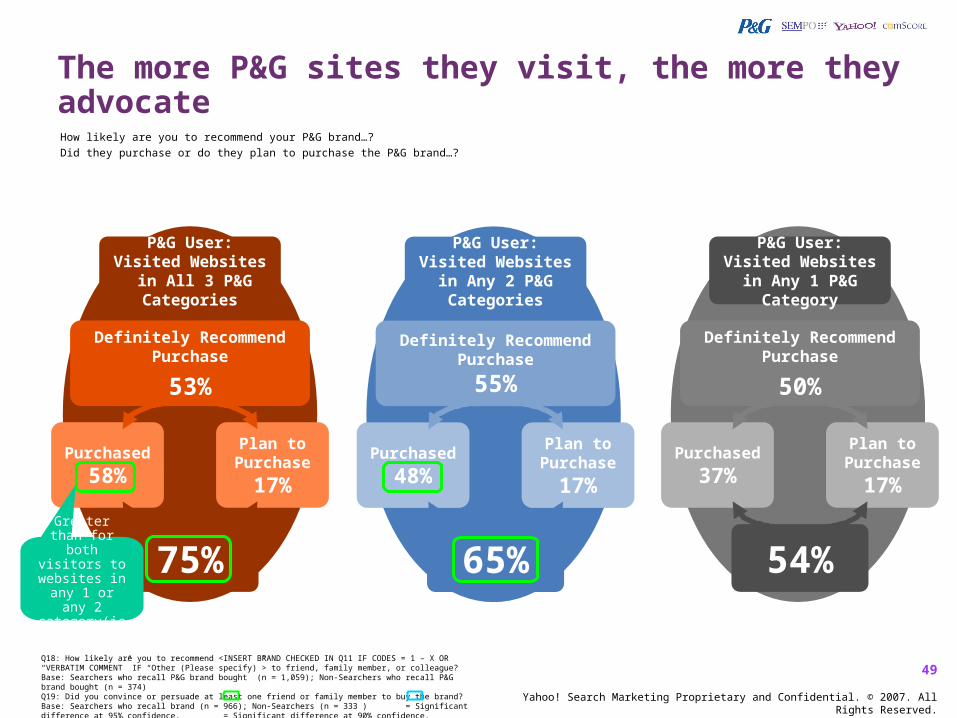

The more P&G sites they visit, the more they advocateHow likely are you to recommend your P&G brand…? Did they purchase or do they plan to purchase the P&G brand…?

Q18: How likely are you to recommend <INSERT BRAND CHECKED IN Q11 IF CODES = 1 – X OR “VERBATIM COMMENT” IF “Other (Please specify)”> to friend, family member, or colleague? Base: Searchers who recall P&G brand bought (n = 1,059); Non-Searchers who recall P&G brand bought (n = 374) Q19: Did you convince or persuade at least one friend or family member to buy the brand? Base: Searchers who recall brand (n = 966); Non-Searchers (n = 333 ) = Significant difference at 95% confidence, = Significant difference at 90% confidence.

P&G User: Visited Websites

in All 3 P&G Categories

Definitely Recommend Purchase

53%

75%

Plan to Purchase

17%

Purchased

58%

P&G User: Visited Websites

in Any 1 P&G Category

Definitely Recommend Purchase

50%

54%

Plan to Purchase

17%

Purchased

37%

P&G User: Visited Websites

in Any 2 P&G Categories

Definitely Recommend Purchase

55%

65%

Plan to Purchase

17%

Purchased

48%

Greater than for both

visitors to websites in

any 1 or any 2

category(ies)

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Alternative Key Findings Slides

51

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

• Customers view CPG website as the digital shelf extension of the shopping experience. Nearly half of all Internet users have visited a CPG related site in the past quarter

IMPLICATION: Consumers are looking for your company, your brands and your products online. Develop a robust strategy to reach and engage with your customers where they’re at -- online

• Searchers are your most engaged consumers, thirsty for information and ripe for influence. Search queries are predominantly informational, not conversion based

IMPLICATION: Searchers represent significant opportunity for marketers seeking to engage customers at a deeper level by providing exactly what they need and want – product information, opportunities to learn more about whole product lines, customer reviews, and a desire to “pre-shop” online before purchase

• Search is the most widely utilized starting point for arriving at lifestyle and company branded websites. Over 43% of CPG site visitors arrived via search

IMPLICATION: Search marketing is a reach vehicle – potentially influencing millions of “in-market” consumers

Executive Summary

52

Yahoo! Search Marketing Proprietary and Confidential. © 2007. All Rights Reserved.

Executive Summary

• Offline media often ignites searchers to follow-up with product research, seek more information, and/or find deals.

IMPLICATION: Search marketing needs to be integrated with your overall brand strategy to maximize the impact of your cross media campaigns.

• The segmentation underscores the motivations driving search behavior – a quest for knowledge, the need to be empowerment – all a convenient mouse click away.

IMPLICATION: The best search marketing strategy will link to good content - ultimately “building brand” in the process.

• Searchers are among your most valuable customers. They spend more, have desirable demos, and advocate for the brands they love.

IMPLICATION: Engage with searchers not only for their value alone, but for their potential to reach and influence a wider sphere of prospects.