china: opportunities and challenges for latin america luis miguel castilla chief economist...

TRANSCRIPT

China: Opportunities and challenges for Latin America

Luis Miguel Castilla

Chief EconomistCorporación Andina de Fomento

Punta del Este, March 30 2006

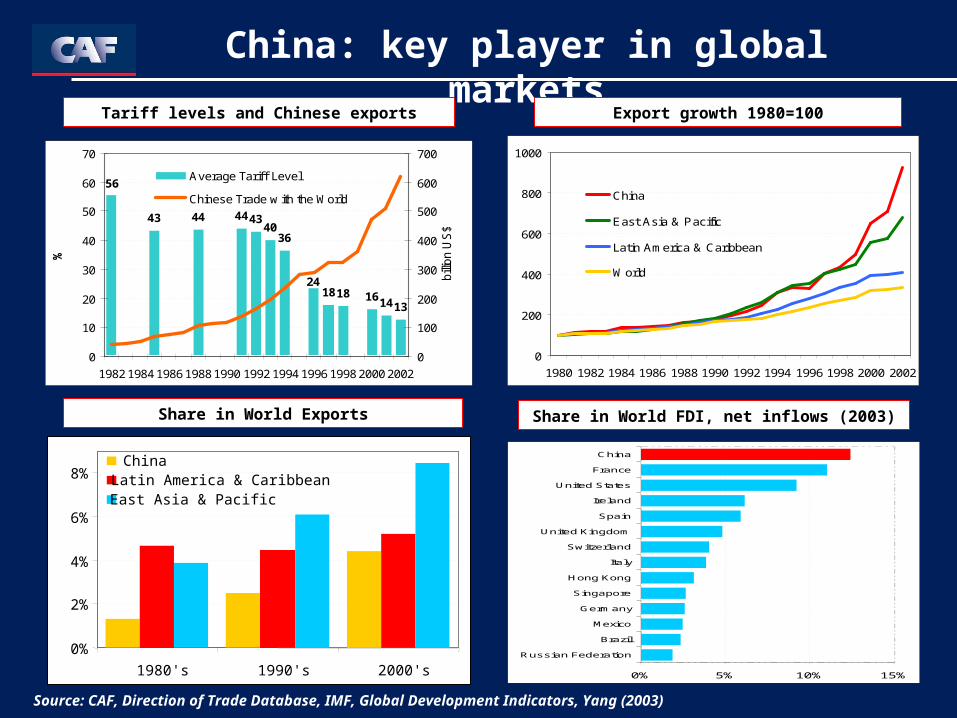

China: key player in global markets

0

200

400

600

800

1000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

China

East Asia & Pacific

Latin America & Caribbean

World

Export growth 1980=100

Share in World FDI, net inflows (2003)

Tariff levels and Chinese exports

Share in World Exports

Source: CAF, Direction of Trade Database, IMF, Global Development Indicators, Yang (2003)

0%

2%

4%

6%

8%

1980's 1990's 2000's

ChinaLatin America & CaribbeanEast Asia & Pacific

43 44 444340

36

1818 161413

24

56

0

10

20

30

40

50

60

70

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

%

0

100

200

300

400

500

600

700

billio

n U

S$

Average Tariff Level

Chinese Trade w ith the World

0% 5% 10% 15%

Russian Federation

Brazil

Mexico

Germany

Singapore

Hong Kong

Italy

Switzerland

United Kingdom

Spain

Ireland

United States

France

China

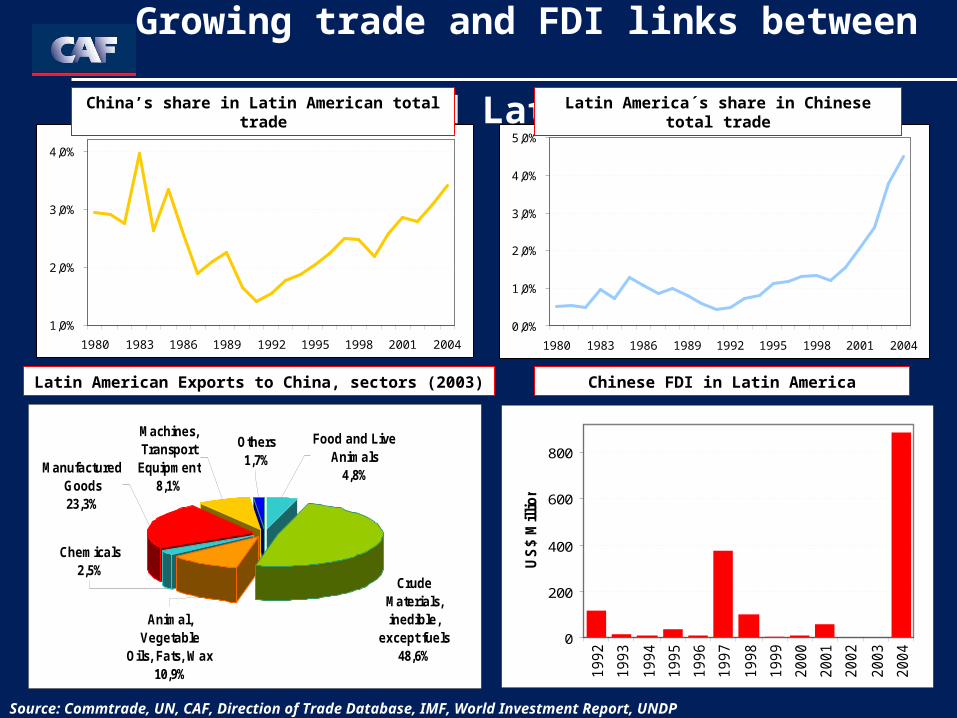

Growing trade and FDI links between China and Latin America

Chinese FDI in Latin AmericaLatin American Exports to China, sectors (2003)

Source: Commtrade, UN, CAF, Direction of Trade Database, IMF, World Investment Report, UNDP

Fuente:

1,0%

2,0%

3,0%

4,0%

1980 1983 1986 1989 1992 1995 1998 2001 2004

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

1980 1983 1986 1989 1992 1995 1998 2001 2004

Latin America´s share in Chinese total tradeChina’s share in Latin American total trade

Chemicals2,5%

Manufactured Goods23,3%

Food and Live Animals

4,8%

Crude Materials, inedible,

except fuels48,6%

Animal, Vegetable

Oils, Fats, Wax10,9%

Machines, Transport

Equipment8,1%

Others1,7%

0

200

400

600

800

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

US

$ M

illio

n

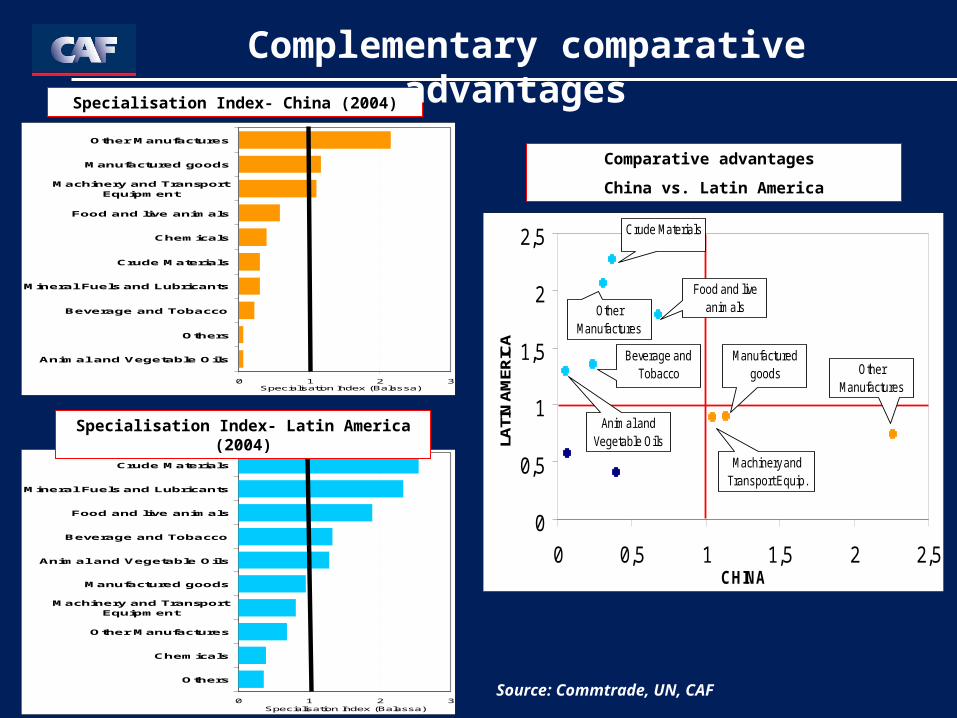

0 1 2 3

Animal and Vegetable Oils

Others

Beverage and Tobacco

Mineral Fuels and Lubricants

Crude Materials

Chemicals

Food and live animals

Machinery and TransportEquipment

Manufactured goods

Other Manufactures

Specialisation Index (Balassa)

0 1 2 3

Others

Chemicals

Other Manufactures

Machinery and TransportEquipment

Manufactured goods

Animal and Vegetable Oils

Beverage and Tobacco

Food and live animals

Mineral Fuels and Lubricants

Crude Materials

Specialisation Index (Balassa)

0

0,5

1

1,5

2

2,5

0 0,5 1 1,5 2 2,5CHINA

LATI

N A

MER

ICA

Manufactured goods

Machinery and Transport Equip.

Other Manufactures

Crude Materials

Other Manufactures

Food and live animals

Beverage and Tobacco

Animal and Vegetable Oils

Specialisation Index- China (2004)

Specialisation Index- Latin America (2004)

Complementary comparative advantages

Comparative advantages

China vs. Latin America

Source: Commtrade, UN, CAF

1. China as a competitor

2. China as an opportunity

3. Major obstacles limiting Latin American trade with China

China as a competitor

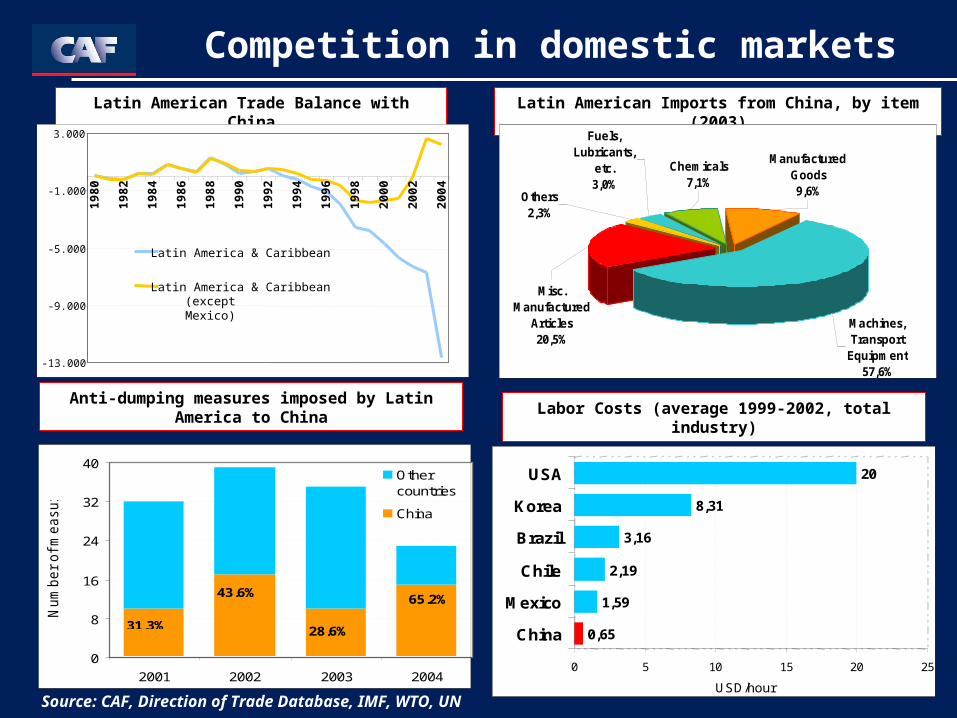

Competition in domestic marketsLatin American Imports from China, by item (2003)

Labor Costs (average 1999-2002, total industry)Anti-dumping measures imposed by Latin America

to China

Latin American Trade Balance with China

Source: CAF, Direction of Trade Database, IMF, WTO, UN

-13.000

-9.000

-5.000

-1.000

3.000

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

Latin America & Caribbean

Latin America & Caribbean(except Mexico)

0,65

1,59

2,19

3,16

8,31

20

0 5 10 15 20 25

China

Mexico

Chile

Brazil

Korea

USA

USD/hour

Others2,3%

Manufactured Goods9,6%

Chemicals7,1%

Fuels, Lubricants,

etc.3,0%

Misc. Manufactured

Articles20,5%

Machines, Transport

Equipment57,6%

0

8

16

24

32

40

2001 2002 2003 2004

Num

ber

of m

easure

s

Othercountries

China

65,2%

28,6%

43,6%

31,3%

China as an opportunity

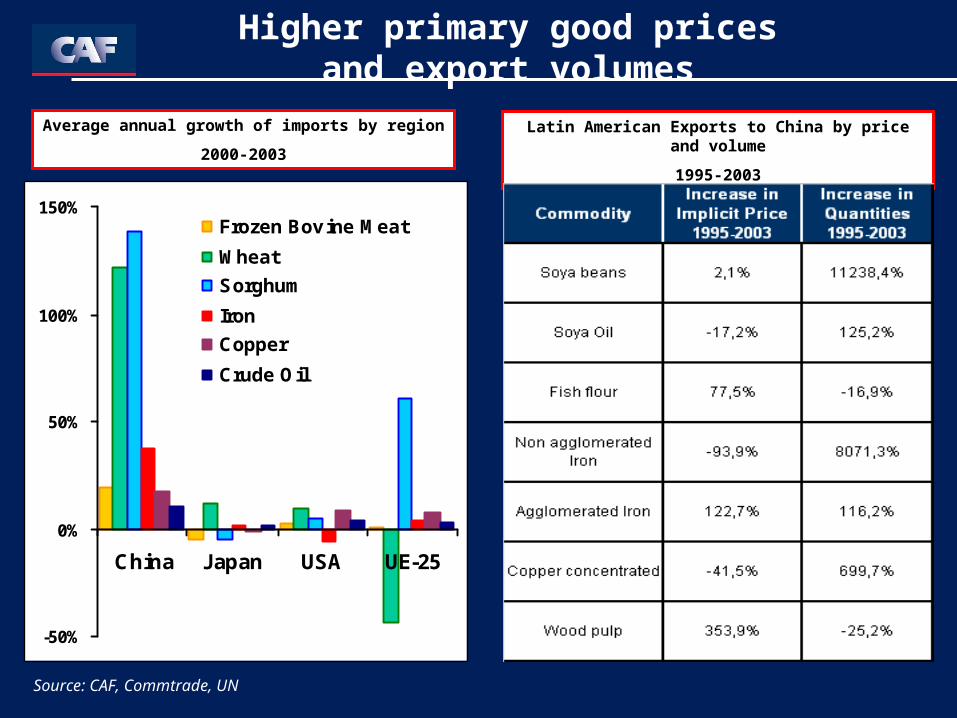

Higher primary good prices and export volumes

Source: CAF, Commtrade, UN

-50%

0%

50%

100%

150%

China Japan USA UE-25

Frozen Bov ine Meat

Wheat

Sorghum

Iron

Copper

Crude Oil

Average annual growth of imports by region

2000-2003

Latin American Exports to China by price and volume

1995-2003

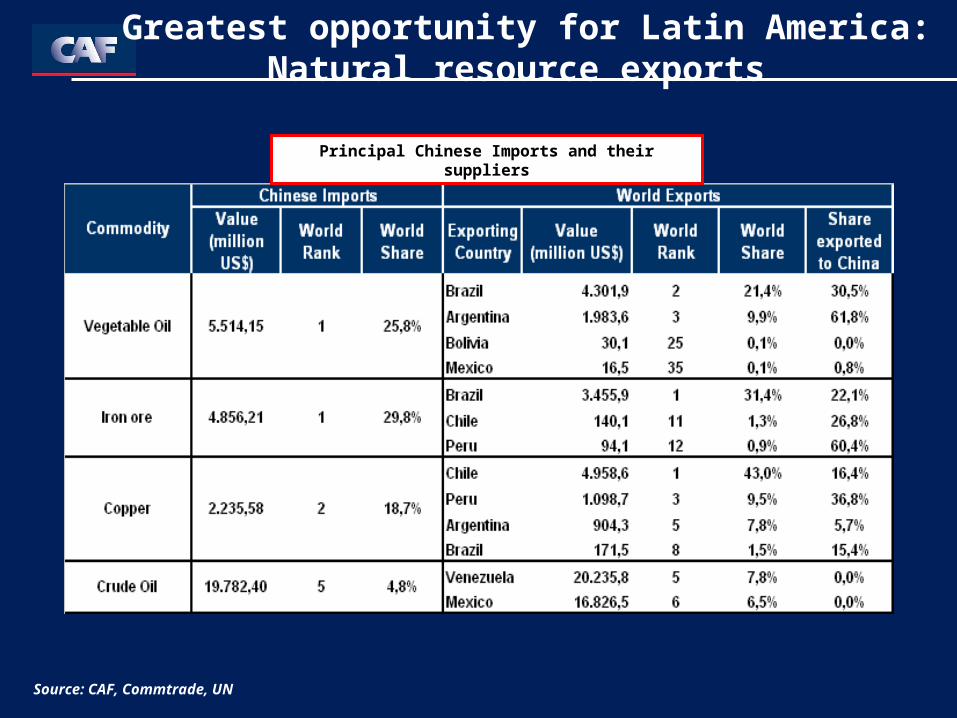

Greatest opportunity for Latin America:Natural resource exports

Source: CAF, Commtrade, UN

Principal Chinese Imports and their suppliers

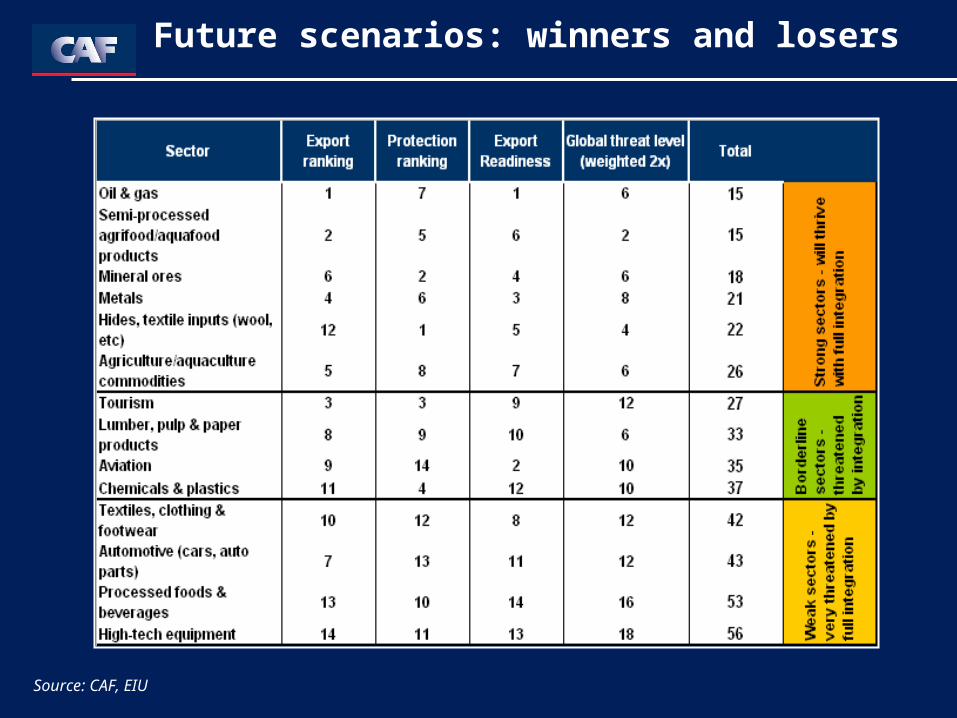

Future scenarios: winners and losers

Source: CAF, EIU

Major obstacles faced by Latin American winning sectors :

• Infrastructure and logistics

• Competitiveness

• Business environment

• Trade barriers

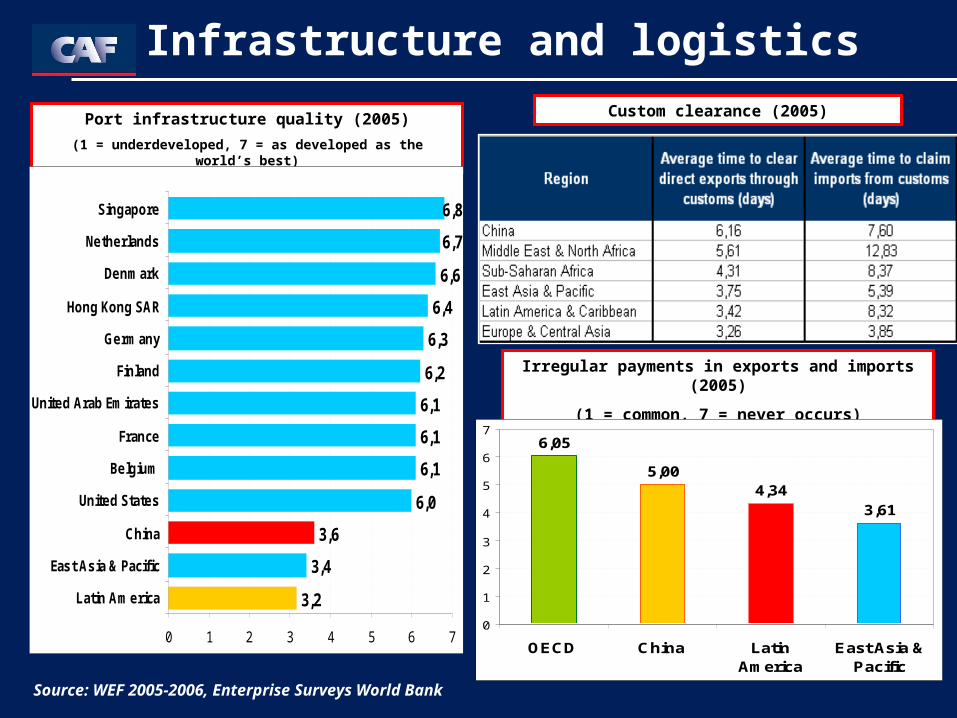

Infrastructure and logistics

Port infrastructure quality (2005)

(1 = underdeveloped, 7 = as developed as the world’s best)

Custom clearance (2005)

Irregular payments in exports and imports (2005)

(1 = common, 7 = never occurs)

Source: WEF 2005-2006, Enterprise Surveys World Bank

3,2

3,4

3,6

6,0

6,1

6,1

6,1

6,2

6,3

6,4

6,6

6,7

6,8

0 1 2 3 4 5 6 7

Latin America

East Asia & Pacific

China

United States

Belgium

France

United Arab Emirates

Finland

Germany

Hong Kong SAR

Denmark

Netherlands

Singapore

6,05

5,004,34

3,61

0

1

2

3

4

5

6

7

OECD China LatinAmerica

East Asia &Pacific

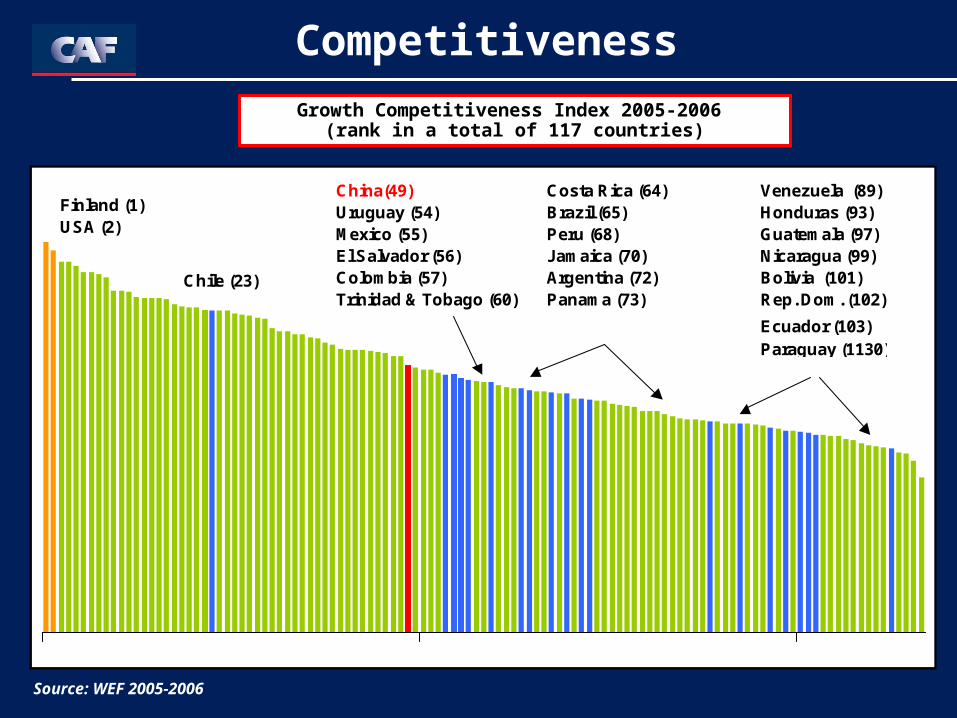

Competitiveness

Chile (23)

Uruguay (54)Mexico (55)El Salvador (56)Colombia (57)Trinidad & Tobago (60)

Costa Rica (64)Brazil (65)Peru (68)Jamaica (70)Argentina (72)Panama (73)

Venezuela (89)Honduras (93)Guatemala (97)Nicaragua (99)Bolivia (101)Rep. Dom. (102)

Ecuador (103)Paraguay (1130)

Finland (1)USA (2)

China(49)

Source: WEF 2005-2006

Growth Competitiveness Index 2005-2006 (rank in a total of 117 countries)

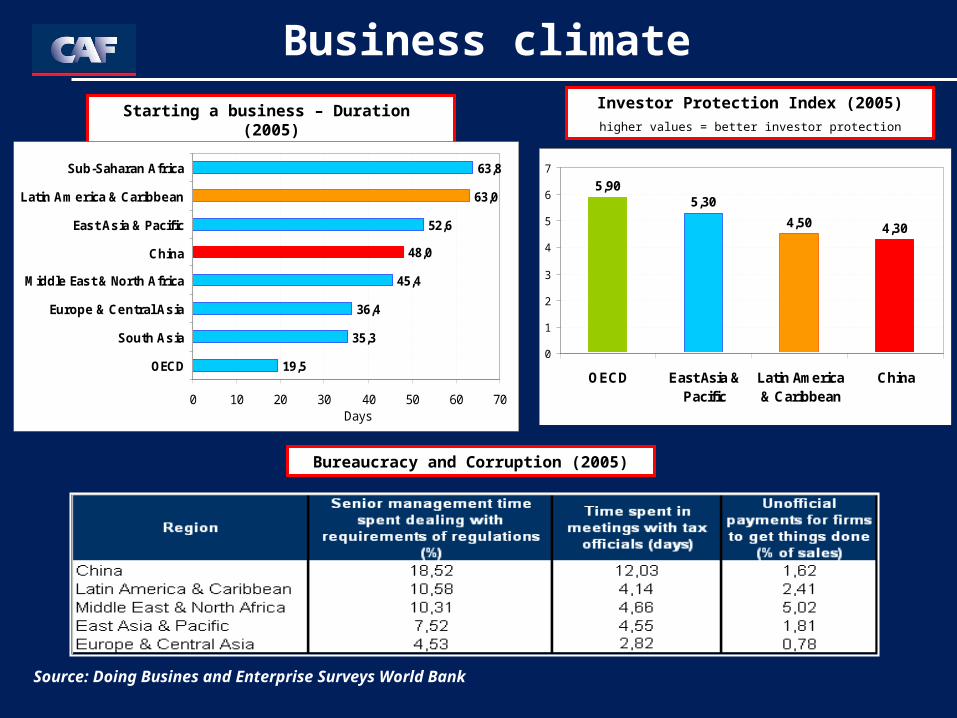

Bureaucracy and Corruption (2005)

Business climate

Starting a business – Duration (2005) Investor Protection Index (2005)

higher values = better investor protection

Source: Doing Busines and Enterprise Surveys World Bank

19,5

35,3

36,4

45,4

48,0

52,6

63,0

63,8

0 10 20 30 40 50 60 70

OECD

South Asia

Europe & Central Asia

Middle East & North Africa

China

East Asia & Pacific

Latin America & Caribbean

Sub-Saharan Africa

Days

5,905,30

4,50 4,30

0

1

2

3

4

5

6

7

OECD East Asia &Pacific

Latin America& Caribbean

China

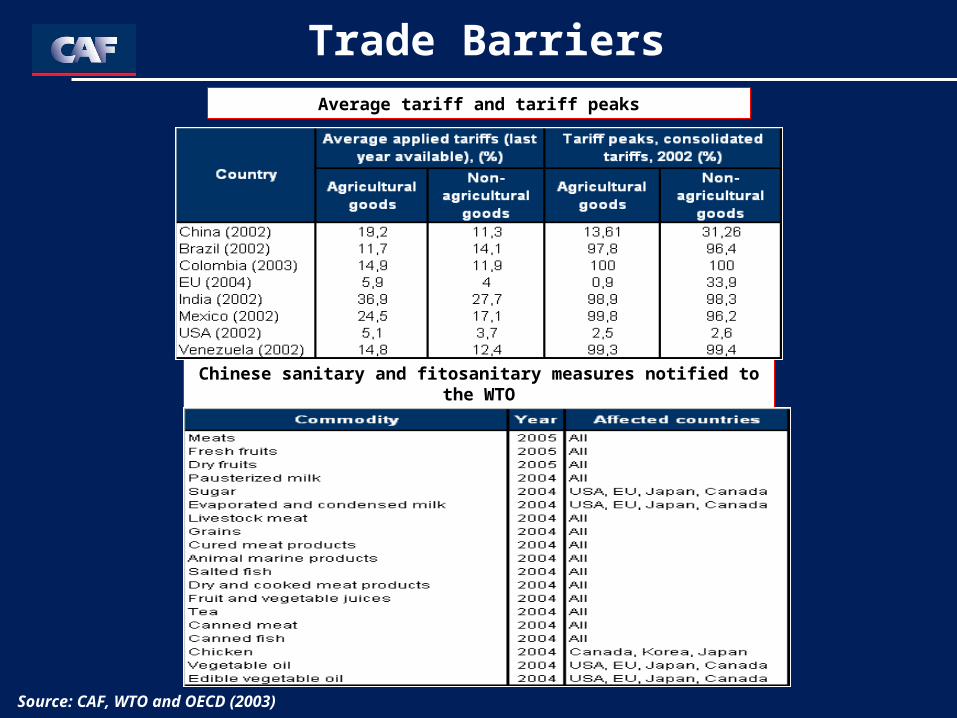

Trade Barriers

Chinese sanitary and fitosanitary measures notified to the WTO

Average tariff and tariff peaks

Source: CAF, WTO and OECD (2003)

Latin American strategy towards China:

• For sensitive sectors, generating greater value added and product differentiation

• Overcoming barriers:- Investment in infrastructure- Trade facilitation (customs) - Business climate

• Eliminating trading barriers that limit bilateral trade

• FDI attraction and technological upgrade

In summary...

www.caf.com