shongweni lap regional economic assessment june 2010 draft

TRANSCRIPT

SHONGWENI LOCAL AREA PLAN

REGIONAL ECONOMIC ASSESSMENT

JUNE 2010

ETHEKWINI MUNICIPALITY

SHONGWENI LOCAL AREA PLAN

REGIONAL ECONOMIC ASSESSMENT

JUNE 2010

PREPARED FOR:

PHILANI CELE / HENRY MASINGA

Linda Masinga & Associates

PO Box 70036

Overport

4067

Tel: 031 202 0573/4

e-mail: [email protected]

PREPARED BY:

TINDALL KRUGER

Strategic Planning Resources

Postnet Suite 75

Private Bag X03

Westville

3630

Tel: 031 – 262 7014

e-mail: [email protected]

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

i

TABLE OF CONTENTS

1. INTRODUCTION ..........................................................................................................................1

1.1. PURPOSE OF THE ASSESSMENT............................................................................................1

1.2. BACKGROUND TO THE SHONGWENI LOCAL AREA ................................................................1

1.3. CURRENT PLANNING PROPOSALS ........................................................................................3

2. THE ETHEKWINI ECONOMIC DEVELOPMENT CONTEXT...............................................................4

2.1. INTRODUCTION ...................................................................................................................4

2.2. OVERVIEW OF THE ETHEKWINI ECONOMY...........................................................................4

2.3. SPATIAL DISTRIBUTION OF ETHEKWINI ECONOMIC ACTIVITY ...............................................5

2.4. RECENT TRENDS IN SPATIAL ECONOMIC DEVELOPMENT .....................................................8

3. RETAIL SECTOR ...........................................................................................................................9

3.1. INTRODUCTION ...................................................................................................................9

3.2. TRENDS IN RETAIL SECTOR ...................................................................................................9

3.3. REGIONAL RETAIL OFFERING ............................................................................................. 12

3.4. POTENTIAL RETAIL CATCHMENTS ...................................................................................... 21

3.5. SHOPPING CENTRE STANDARDS ........................................................................................ 26

3.6. GAP ANALYSIS ................................................................................................................... 28

3.7. SUMMARY RECOMMENDATIONS: RETAIL DEVELOPMENT IN SHONGWENI ........................ 34

4. COMMERCIAL / OFFICE SECTOR ............................................................................................... 35

4.1. GLOBAL TRENDS IN THE COMMERCIAL PROPERTY SECTOR ................................................ 35

4.2. CURRENT OFFICE PROPERTY ECONOMIC TRENDS .............................................................. 35

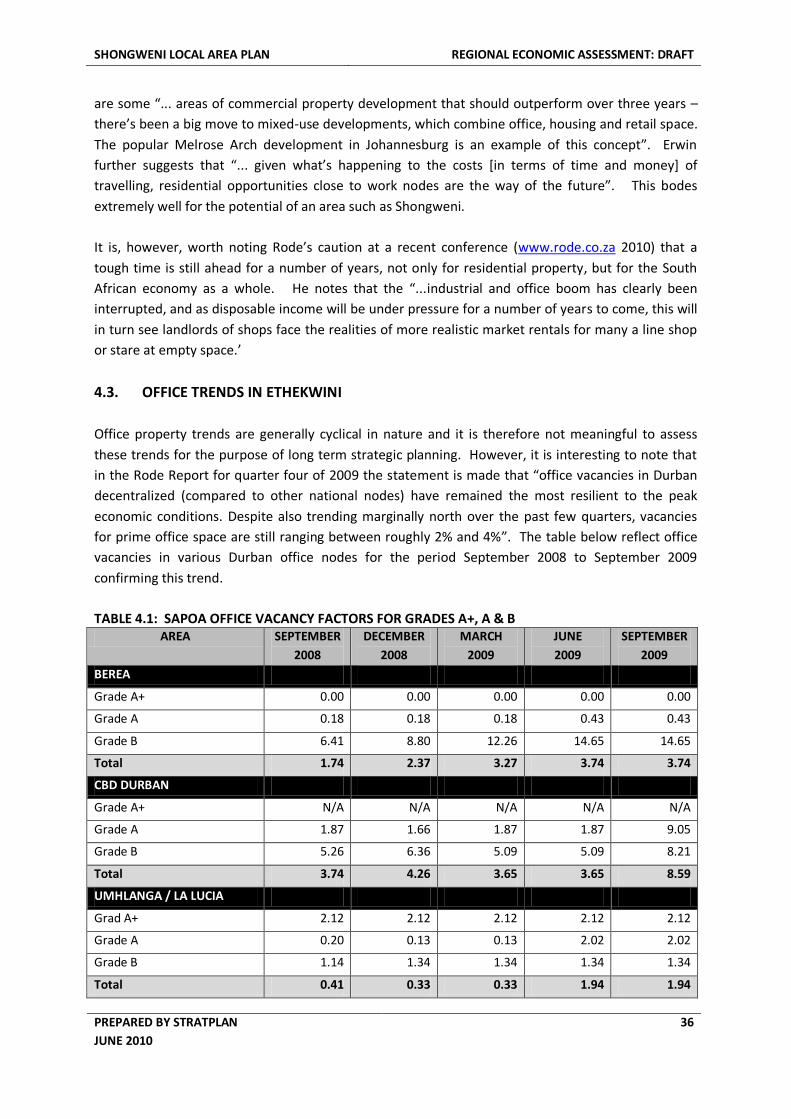

4.3. OFFICE TRENDS IN ETHEKWINI ........................................................................................... 36

4.4. CONSIDERING SUPPLY IN WESTERN AREAS ........................................................................ 37

4.5. OPPORTUNITIES FOR ESTABLISHMENT OF COMMERCIAL SECTOR...................................... 37

4.6. BASIC RECOMMENDATIONS: OFFICE / COMMERCIAL DEVELOPMENT ............................... 37

5. MANUFACTURING SECTOR ....................................................................................................... 38

5.1. INTRODUCTION ................................................................................................................. 38

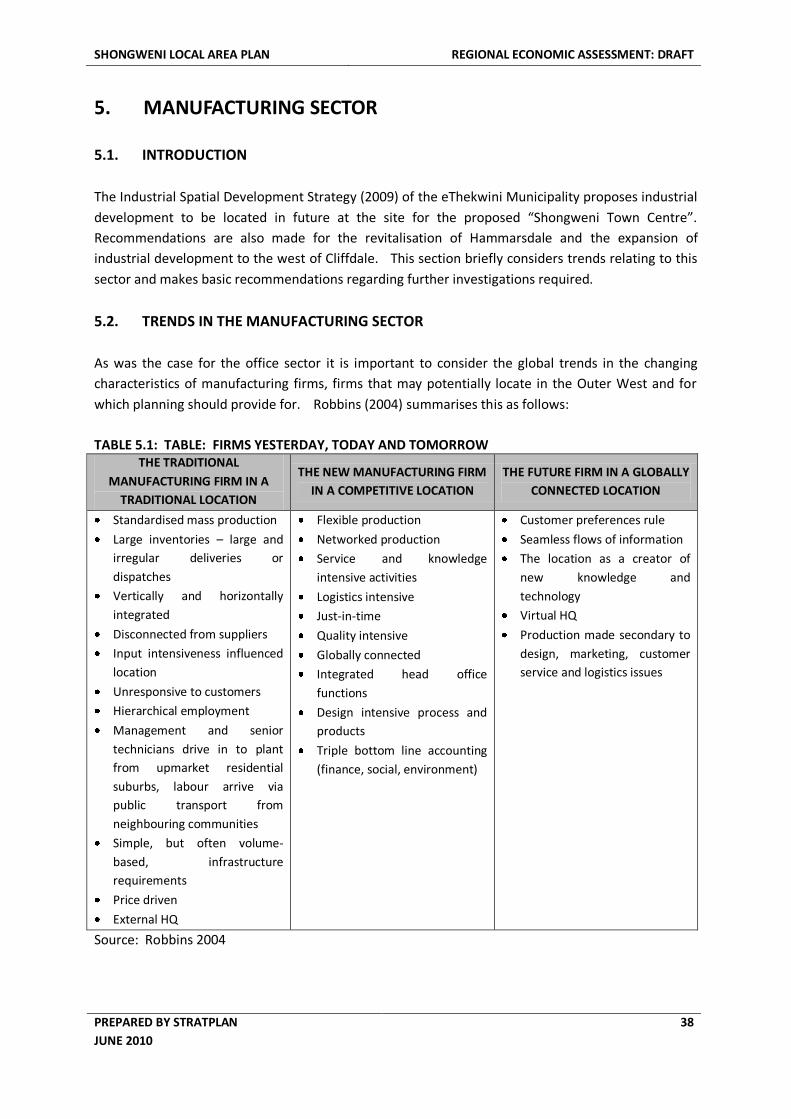

5.2. TRENDS IN THE MANUFACTURING SECTOR ........................................................................ 38

5.3. TRENDS IN THE INDUSTRIAL PROPERTY SECTOR ................................................................ 39

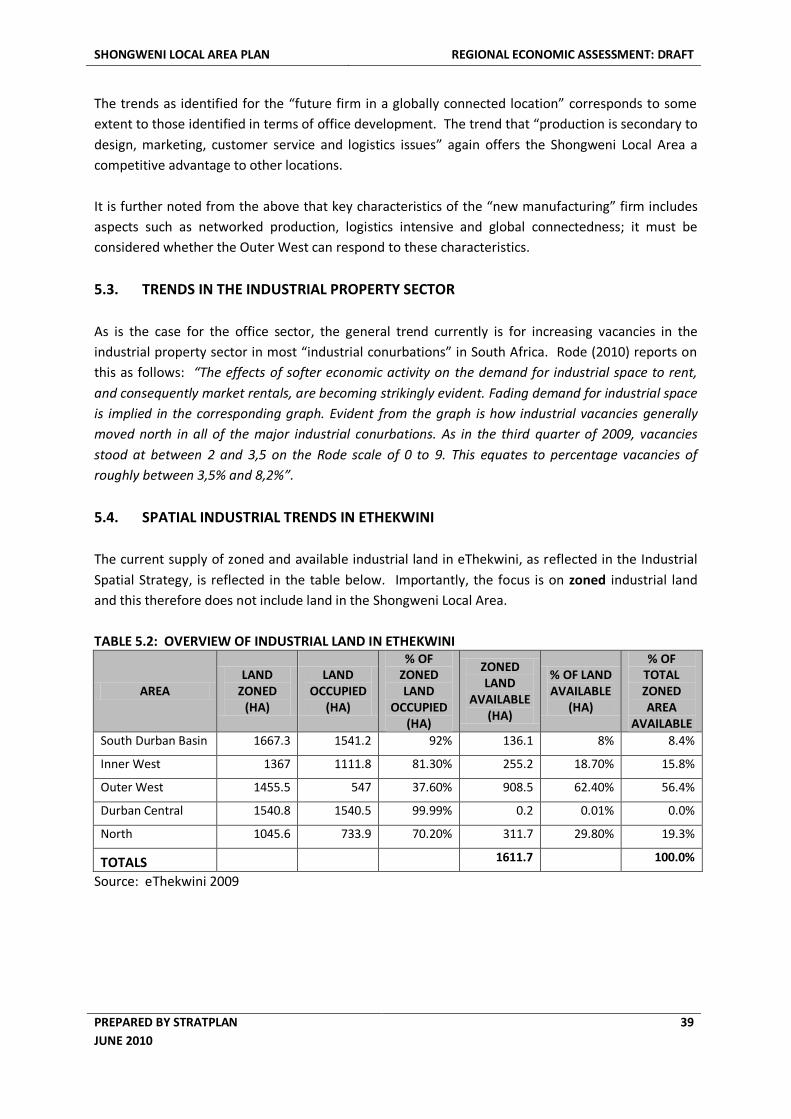

5.4. SPATIAL INDUSTRIAL TRENDS IN ETHEKWINI ..................................................................... 39

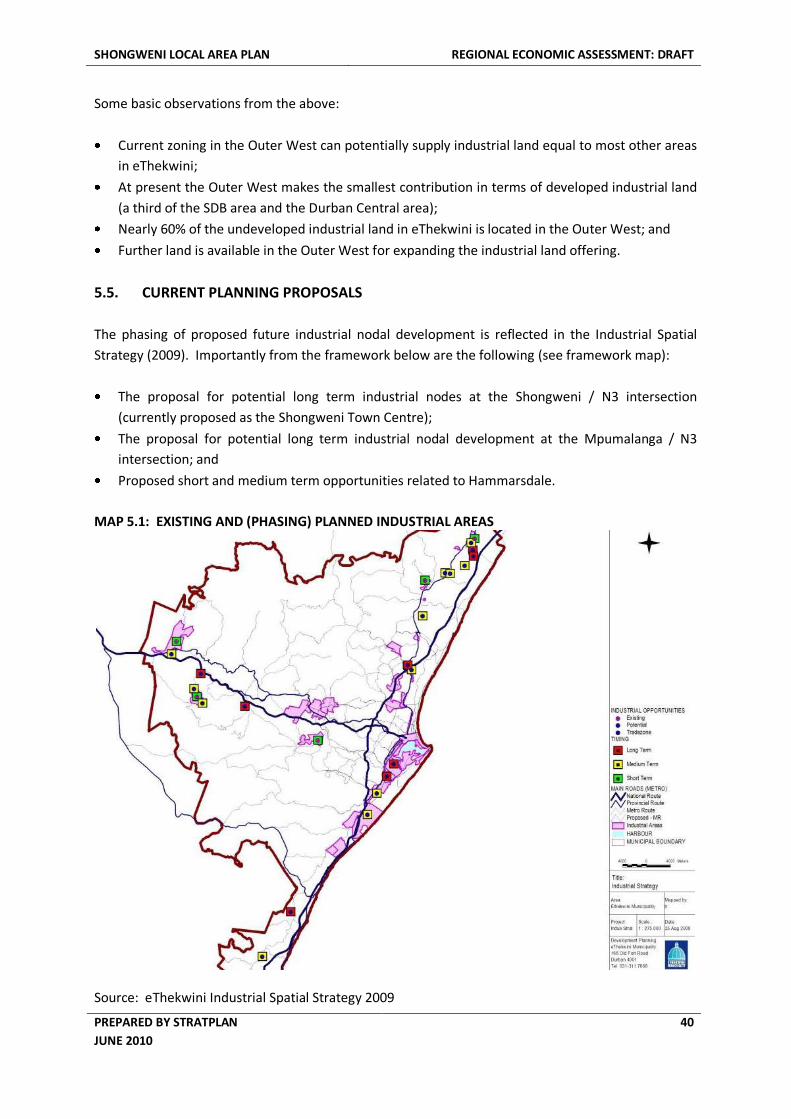

5.5. CURRENT PLANNING PROPOSALS ...................................................................................... 40

5.6. RECOMMENDATIONS ........................................................................................................ 42

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

ii

6. ALTERNATIVE OPPORTUNITIES ................................................................................................. 43

6.1. THE AGRIBUSINESS SECTOR ............................................................................................... 43

7. SUMMARY RECOMMENDATION ............................................................................................... 44

7.1. GENERAL RECOMMENDATIONS ......................................................................................... 44

7.2. MIDDLE TO HIGH INCOME RETAIL RECOMMENDATIONS ................................................... 44

7.3. LOW INCOME RETAIL RECOMMENDATIONS ...................................................................... 45

7.4. OFFICE / COMMERCIAL DEVELOPMENT RECOMMENDATIONS ........................................... 45

7.5. MANUFACTURING SECTOR DEVELOPMENT RECOMMENDATIONS ..................................... 45

LIST OF FIGURES:

FIGURE 2.1: GROSS DOMESTIC PRODUCT CONTRIBUTION BY SECTOR FOR 2005 ............................................... 5

FIGURE 3.1: THE STATUS OF TRADITIONAL VS ORGANISED RETAILING ............................................................ 10

FIGURE 3.2: PERCENTAGE HOUSEHOLD EXPENDITURE PER POPULATION GROUP 1993 TO 2008 ..................... 11

LIST OF MAPS:

MAP 3.1: DIAGRAM: PROPOSED NODAL DEVELOPMENT IN THE OUTER WEST ............................................... 32

MAP 5.1: EXISTING AND (PHASING) PLANNED INDUSTRIAL AREAS .................................................................. 40

MAP 5.2: PROPOSED FOCUS AREAS ................................................................................................................ 41

LIST OF TABLES:

TABLE 1.1: PRELIMINARY (NOT FINAL) LAND USE TABLE FOR THE SHONGWENI LOCAL AREA PLAN ................... 3

TABLE 2.1: THE SPREAD OF EMPLOYMENT ACROSS ETHEKWINI BY TYPE AND NUMBER OF JOBS, 2001 ............. 6

TABLE 3.1: OVERVIEW OF FORMAL RETAIL IN THE OUTER WEST ..................................................................... 14

TABLE 3.2: SUMMARY OF CURRENT REGIONAL RETAIL OFFERING ................................................................... 16

TABLE 3.3: OUTER WEST GROSS LETTABLE RETAIL PER RETAIL CENTRE TYPE ................................................... 16

TABLE 3.4: DISTRIBUTION OF RETAIL IN HILLCREST BY TYPE OF CENTRE .......................................................... 17

TABLE 3.5: BUSINESS CATEGORIES IN THE BOTHA'S HILL COMMERCIAL NODE ................................................ 20

TABLE 3.6: CATCHMENT AREAS IN TERMS OF PLANNING UNIT ....................................................................... 22

TABLE 3.7: SUMMARY OVERVIEW OF CURRENT AND FUTURE POPULATION IN SHONGWENI CATCHMENTS .... 25

TABLE 3.8: MONTHLY AVERAGE HOUSEHOLD INCOME PER LSM CATEGORY ................................................... 27

TABLE 3.9: WARRANTED SPACE (IN SQUARE METER) PER PERSON ACCORDING TO LSM GROUPS ................... 27

TABLE 3.10: SUGGESTED HIERARCHY OF SHOPPING FACILITIES ....................................................................... 28

TABLE 3.11: RETAIL SPACE REQUIREMENTS BASED ON CURRENT POPULATION AND NATURAL GROWTH ........ 29

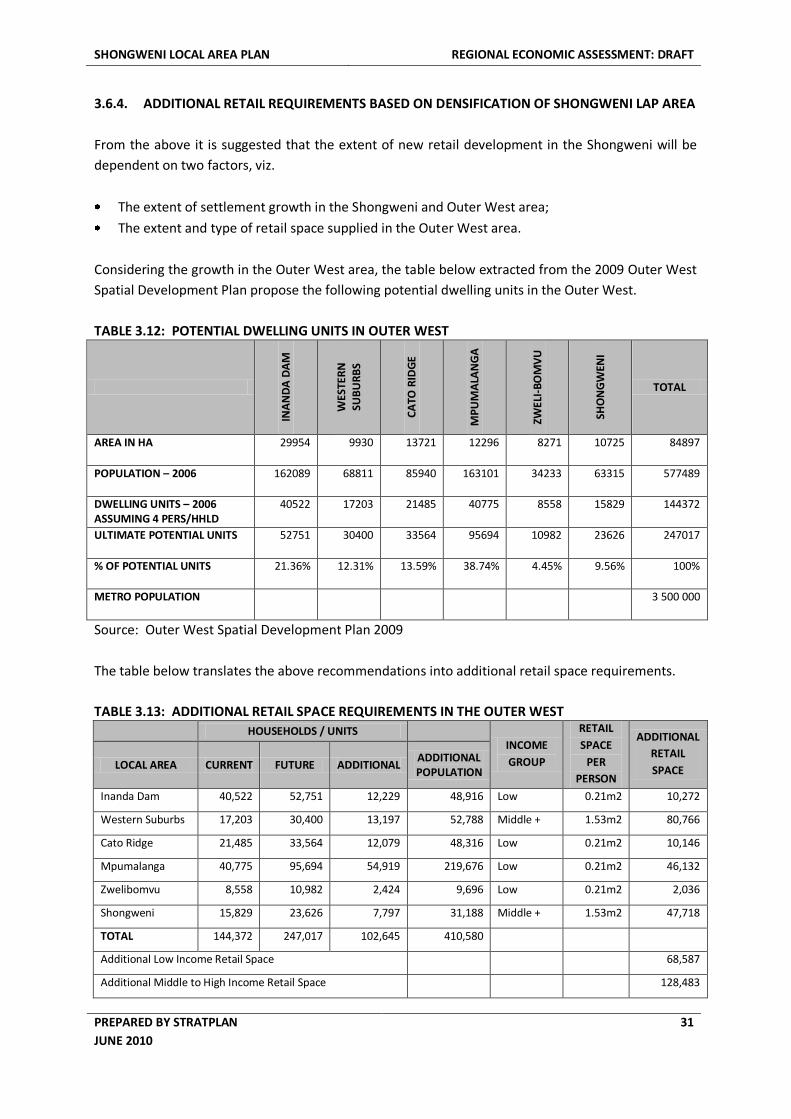

TABLE 3.12: POTENTIAL DWELLING UNITS IN OUTER WEST ............................................................................. 31

TABLE 3.13: ADDITIONAL RETAIL SPACE REQUIREMENTS IN THE OUTER WEST ............................................... 31

TABLE 4.1: SAPOA OFFICE VACANCY FACTORS FOR GRADES A+, A & B ............................................................ 36

TABLE 5.1: TABLE: FIRMS YESTERDAY, TODAY AND TOMORROW ................................................................... 38

TABLE 5.2: OVERVIEW OF INDUSTRIAL LAND IN ETHEKWINI ........................................................................... 39

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

1

1. INTRODUCTION

1.1. PURPOSE OF THE ASSESSMENT

This assessment is an extension to the economic development brief for the Shongweni Local Area

Plan. It is intended to develop a better regional perspective of specifically the retail sector with a

view to guiding future land use planning in the Shongweni area. The commercial/office and

manufacturing sectors are, however, also commented on. The specific focus is on identifying

appropriate uses for future developments in identified development nodes. The report therefore

presents a basic assessment of the retail, commercial/office and manufacturing sector trends in the

eThekwini Municipality and more specifically the western sections of the Municipality.

1.2. BACKGROUND TO THE SHONGWENI LOCAL AREA

1.2.1. DEFINING THE AREA

The Shongweni Area is located to the west of Pinetown and is bordered to the north by the Valley of

the 1000 Hills, to the west by Inchanga and Hammarsdale / Mpumalanga and to the south by various

traditional council areas including Zwelibomvu.

The Study Area includes the following Planning Units as defined by the eThekwini Municipality:

Alverstone

Assagay

Botha’s Hill

Bux Farm

Cliffdale

Clifton Canyon

Drummond

Monteseel

Peacevale

Pinetown Rural

Salem Community

Shongweni Resource Reserve

Summerveld

1.2.2. THE SHONGWENI AREA – STATUS QUO FINDINGS

The Study Area is characterized by substantial differences in socio-economic conditions and the local

communities have different expectations and requirements for development. The residents of the

more affluent areas such as Assagay, Alverstone and Summerveld have vastly different expectations

and priorities than those residing in areas such as Cliffdale, Bux Farm, Salem and Pinetown Rural.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

2

Further impacting on this is the economic needs and expectations of those residing in predominantly

traditional and informal settlement areas bordering on the Study Area.

There is a general lack of bulk infrastructure and basic services such as schools and health facilities in

parts of the Shongweni Area, especially in the Planning Units to the south west of the N3. In these

Units there are also insufficient employment opportunities, limited economic activities and a weak

economic base. Settlement patterns are fragmented and dispersed and this forms a major constraint

as the development and services provision of these settlements will be not only difficult but also

costly.

The Shongweni Area contains portions of steep fragmented topography and unusual landform and

these unique landscapes contribute to the tourism potential of the Study Area. However, this also

poses a challenge for the provision of infrastructure in large portions of the Study Area.

There are numerous registered conservancies within the Study Area, such as the entire Assagay

valley that is registered as the Assagay Conservancy. Again these conservancies contribute to the

tourism potential of the Study Area, but will also limit future development.

The Shongweni Resource Reserve once was the premier destination for nature lovers and extreme

sport enthusiasts in the City. The future of this Reserve is however now unclear due to the successful

land claim by the Zwelibomvu community. The vision that the land claimants have for the area needs

to be established and they will need support if they want to ensure that the Reserve continues to be

a premier destination for nature lovers and extreme sport enthusiasts in eThekwini and for people

from further afield.

Employment opportunities and the provision of income-generating activities are the two most

important development needs within the Salem, Shongweni and Cliffdale areas. On the other hand

Summerveld, the upper portions of Shongweni Resource Reserve, Assagay and Alverstone view

nature conservation, wildlife and equestrian related activities as important needs.

Although economic activities are varied within the Study Area they do not provide sufficient

employment opportunities for the large concentration of people that are living in especially the

settlements to the west of the N3. The development of a strong economic sector in these Planning

Units could potentially help to alleviate the current weak economic base of these settlements.

Whilst there are a substantial number of small businesses operating in the Planning Units to the west

of the N3, many of these are associated with agriculture and quarrying and are not large employers.

They have limited capacity to grow and are not able to provide meaningful levels of employment

within these Planning Units and in the Outer West in general.

It can be concluded economic development challenges faced by the different Planning Units differ

substantially, but that the challenges that will be faced in Planning Units with similar characteristics

can be clearly identified. The key challenges for economic development would then be:

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

3

Lack of land available for development should densification of existing areas not be considered;

Uncontrolled and unplanned development impacting on the building of specifically the tourism

industry in the area (i.e. conflict between different land uses);

Proximity to eThekwini may be perceived as both a challenge and an opportunity (i.e.

competition for businesses in metropolitan areas is much more significant); and

Low levels of infrastructure and services available in the Study Area.

This current study attempts to address and make recommendations regarding all of the above, by

providing guidance as to development opportunities in the various nodes.

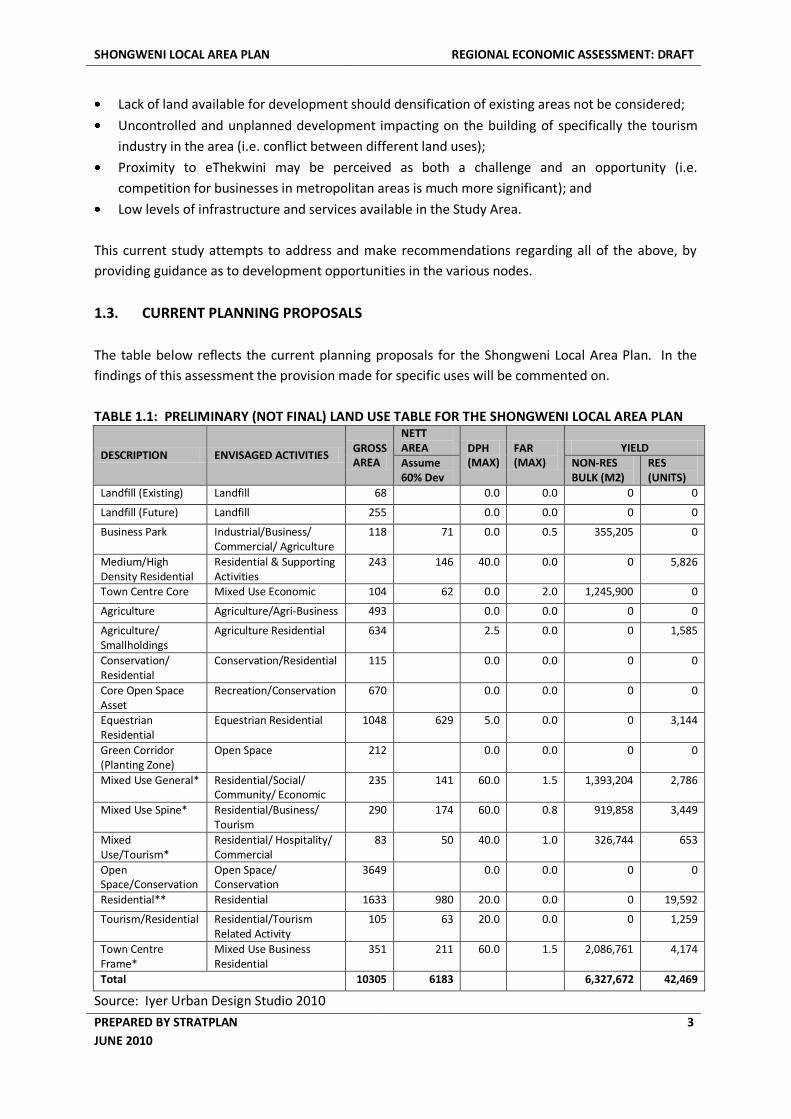

1.3. CURRENT PLANNING PROPOSALS

The table below reflects the current planning proposals for the Shongweni Local Area Plan. In the

findings of this assessment the provision made for specific uses will be commented on.

TABLE 1.1: PRELIMINARY (NOT FINAL) LAND USE TABLE FOR THE SHONGWENI LOCAL AREA PLAN

DESCRIPTION ENVISAGED ACTIVITIES GROSS AREA

NETT AREA DPH

(MAX) FAR (MAX)

YIELD Assume 60% Dev

NON-RES BULK (M2)

RES (UNITS)

Landfill (Existing) Landfill 68 0.0 0.0 0 0

Landfill (Future) Landfill 255 0.0 0.0 0 0

Business Park Industrial/Business/ Commercial/ Agriculture

118 71 0.0 0.5 355,205 0

Medium/High Density Residential

Residential & Supporting Activities

243 146 40.0 0.0 0 5,826

Town Centre Core Mixed Use Economic 104 62 0.0 2.0 1,245,900 0

Agriculture Agriculture/Agri-Business 493 0.0 0.0 0 0

Agriculture/ Smallholdings

Agriculture Residential 634 2.5 0.0 0 1,585

Conservation/ Residential

Conservation/Residential 115 0.0 0.0 0 0

Core Open Space Asset

Recreation/Conservation 670 0.0 0.0 0 0

Equestrian Residential

Equestrian Residential 1048 629 5.0 0.0 0 3,144

Green Corridor (Planting Zone)

Open Space 212 0.0 0.0 0 0

Mixed Use General* Residential/Social/ Community/ Economic

235 141 60.0 1.5 1,393,204 2,786

Mixed Use Spine* Residential/Business/ Tourism

290 174 60.0 0.8 919,858 3,449

Mixed Use/Tourism*

Residential/ Hospitality/ Commercial

83 50 40.0 1.0 326,744 653

Open Space/Conservation

Open Space/ Conservation

3649 0.0 0.0 0 0

Residential** Residential 1633 980 20.0 0.0 0 19,592

Tourism/Residential Residential/Tourism Related Activity

105 63 20.0 0.0 0 1,259

Town Centre Frame*

Mixed Use Business Residential

351 211 60.0 1.5 2,086,761 4,174

Total 10305 6183 6,327,672 42,469

Source: Iyer Urban Design Studio 2010

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

4

2. THE ETHEKWINI ECONOMIC DEVELOPMENT CONTEXT

2.1. INTRODUCTION

The eThekwini Municipal area has experienced significant changes in its spatial economic

development over the past decade and these changes will also direct / guide future economic

development to the west of eThekwini. With a view to this, this section of the report provides a

brief overview of economic and spatial economic development in eThekwini based on available

information.

An overview of the eThekwini economy, extracted from a 2006/7 review prepared for eThekwini, is

presented with a view to understanding the contribution of and trends in the key economic sectors.

2.2. OVERVIEW OF THE ETHEKWINI ECONOMY

(Extracted from eThekwini Municipality Economic Review 2006/7 prepared by Graham Muller

Associates)

The economy of the eThekwini Municipality is the driving force behind economic growth in the region

and gross domestic product (GDP) in the metropolitan economy has grown at an average annual rate

of 3.65 % over the period from 1995-2005. This compares favourably with the rest of KwaZulu-Natal

province, which grew at a rate of 2.3% for the period from 1995 to 2004. The combined rate of GDP

growth for the province from 1995-2004 was 2.9%. The metropolitan area has consistently shown

strong positive GDP growth over the last ten years at a level which has been fairly similar to the

growth experienced in Cape Town (3.52 %) and the City of Tswane (3.23 %) but somewhat lagging

behind GDP growth for Johannesburg which has averaged 4.29% since 1996. More recent growth

trends suggest that eThekwini metropolitan area has been lagging in GDP growth with the other

three cities mentioned experiencing growth at 4% or higher for the 2001- 2004 period and the

eThekwini metropolitan area averaging a more modest 3.15% over the same period.

The single largest contributor to GDP in the eThekwini metropolitan area is the manufacturing sector

which contributes to a quarter of total GDP. The importance of this sector in the metropolitan area

and the province as a whole cannot be understated as its total contribution to provincial GDP in 2004

was nearly 15%. After manufacturing the next largest sector is finance and business services, and 72%

of the contribution to the provincial finance and business services sector’s GDP is generated in the

metropolitan area.

Transport and communication is also a significant contributor to the economy in the eThekwini

metropolitan area. This is unsurprising given that the metropolitan area is home to the Port of

Durban, Africa’s busiest port and a major transportation hub. The transport and communication

sector is the fastest growing sector in the municipality, recording average annual growth of 6.45 %

for the 2001-2005 period.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

5

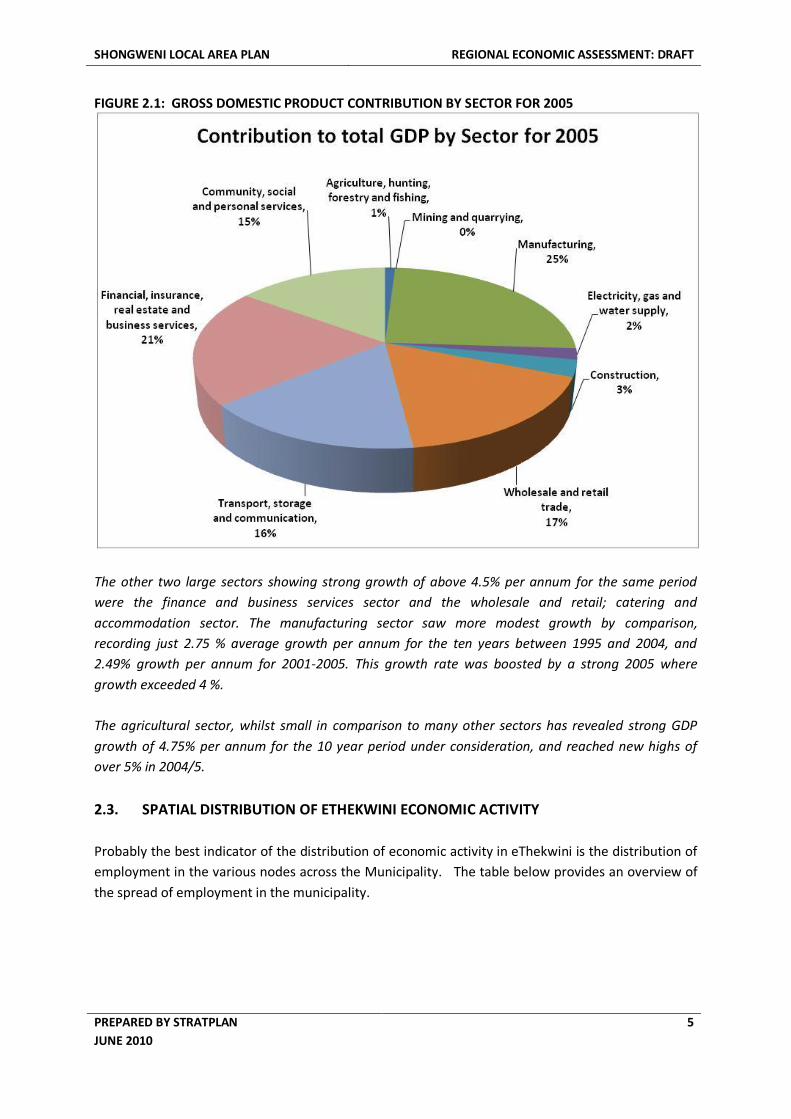

FIGURE 2.1: GROSS DOMESTIC PRODUCT CONTRIBUTION BY SECTOR FOR 2005

The other two large sectors showing strong growth of above 4.5% per annum for the same period

were the finance and business services sector and the wholesale and retail; catering and

accommodation sector. The manufacturing sector saw more modest growth by comparison,

recording just 2.75 % average growth per annum for the ten years between 1995 and 2004, and

2.49% growth per annum for 2001-2005. This growth rate was boosted by a strong 2005 where

growth exceeded 4 %.

The agricultural sector, whilst small in comparison to many other sectors has revealed strong GDP

growth of 4.75% per annum for the 10 year period under consideration, and reached new highs of

over 5% in 2004/5.

2.3. SPATIAL DISTRIBUTION OF ETHEKWINI ECONOMIC ACTIVITY

Probably the best indicator of the distribution of economic activity in eThekwini is the distribution of

employment in the various nodes across the Municipality. The table below provides an overview of

the spread of employment in the municipality.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

6

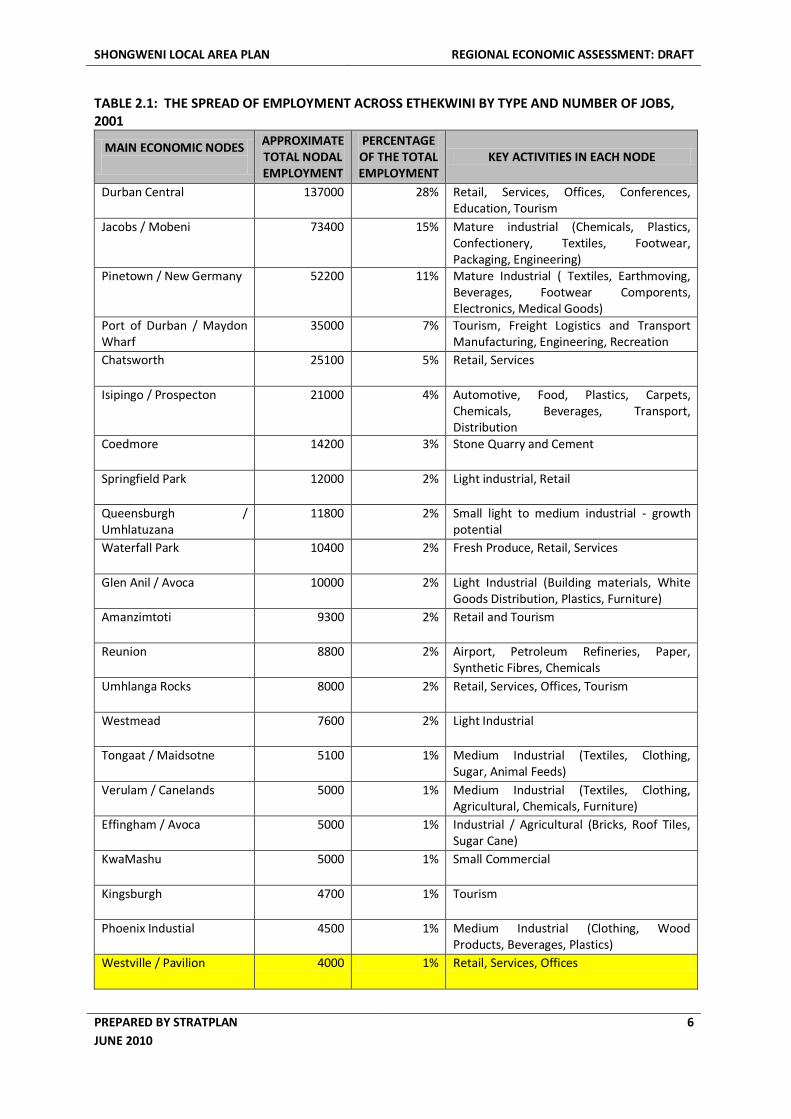

TABLE 2.1: THE SPREAD OF EMPLOYMENT ACROSS ETHEKWINI BY TYPE AND NUMBER OF JOBS, 2001

MAIN ECONOMIC NODES

APPROXIMATE TOTAL NODAL EMPLOYMENT

PERCENTAGE OF THE TOTAL EMPLOYMENT

KEY ACTIVITIES IN EACH NODE

Durban Central 137000 28% Retail, Services, Offices, Conferences, Education, Tourism

Jacobs / Mobeni 73400 15% Mature industrial (Chemicals, Plastics, Confectionery, Textiles, Footwear, Packaging, Engineering)

Pinetown / New Germany 52200 11% Mature Industrial ( Textiles, Earthmoving, Beverages, Footwear Comporents, Electronics, Medical Goods)

Port of Durban / Maydon Wharf

35000 7% Tourism, Freight Logistics and Transport Manufacturing, Engineering, Recreation

Chatsworth 25100 5% Retail, Services

Isipingo / Prospecton 21000 4% Automotive, Food, Plastics, Carpets, Chemicals, Beverages, Transport, Distribution

Coedmore 14200 3% Stone Quarry and Cement

Springfield Park 12000 2% Light industrial, Retail

Queensburgh / Umhlatuzana

11800 2% Small light to medium industrial - growth potential

Waterfall Park 10400 2% Fresh Produce, Retail, Services

Glen Anil / Avoca 10000 2% Light Industrial (Building materials, White Goods Distribution, Plastics, Furniture)

Amanzimtoti 9300 2% Retail and Tourism

Reunion 8800 2% Airport, Petroleum Refineries, Paper, Synthetic Fibres, Chemicals

Umhlanga Rocks 8000 2% Retail, Services, Offices, Tourism

Westmead 7600 2% Light Industrial

Tongaat / Maidsotne 5100 1% Medium Industrial (Textiles, Clothing, Sugar, Animal Feeds)

Verulam / Canelands 5000 1% Medium Industrial (Textiles, Clothing, Agricultural, Chemicals, Furniture)

Effingham / Avoca 5000 1% Industrial / Agricultural (Bricks, Roof Tiles, Sugar Cane)

KwaMashu 5000 1% Small Commercial

Kingsburgh 4700 1% Tourism

Phoenix Industial 4500 1% Medium Industrial (Clothing, Wood Products, Beverages, Plastics)

Westville / Pavilion 4000 1% Retail, Services, Offices

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

7

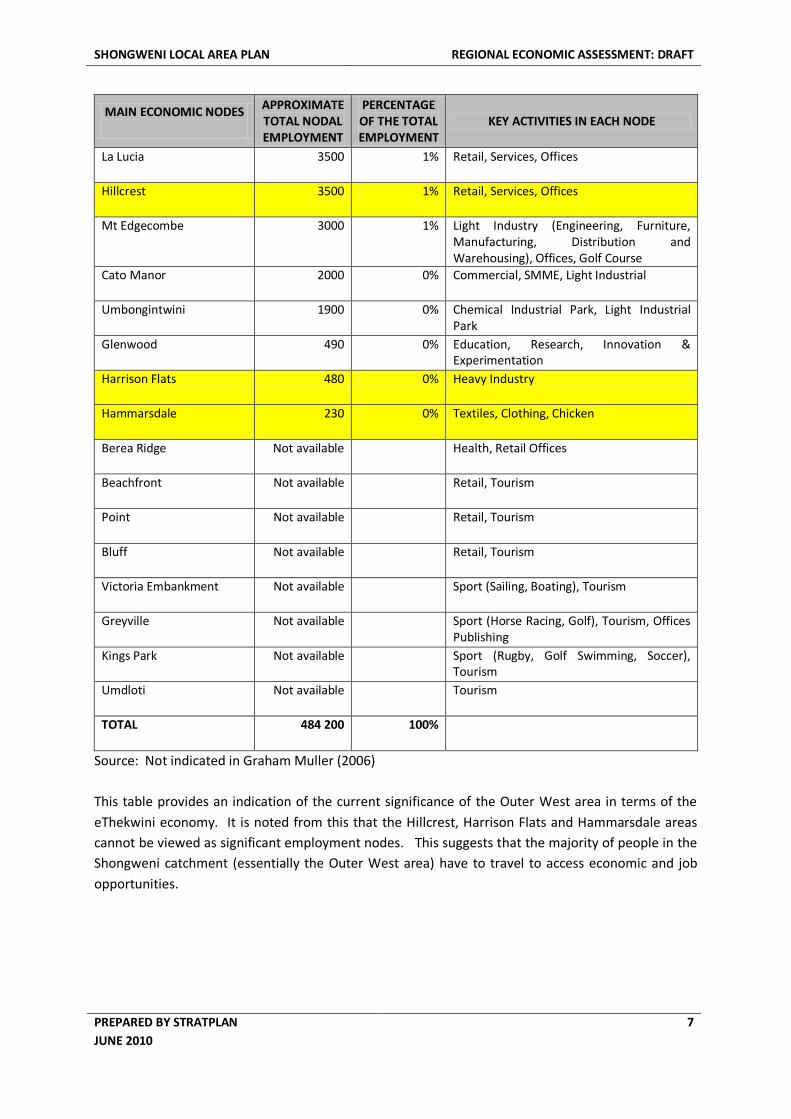

MAIN ECONOMIC NODES

APPROXIMATE TOTAL NODAL EMPLOYMENT

PERCENTAGE OF THE TOTAL EMPLOYMENT

KEY ACTIVITIES IN EACH NODE

La Lucia 3500 1% Retail, Services, Offices

Hillcrest 3500 1% Retail, Services, Offices

Mt Edgecombe 3000 1% Light Industry (Engineering, Furniture, Manufacturing, Distribution and Warehousing), Offices, Golf Course

Cato Manor 2000 0% Commercial, SMME, Light Industrial

Umbongintwini 1900 0% Chemical Industrial Park, Light Industrial Park

Glenwood 490 0% Education, Research, Innovation & Experimentation

Harrison Flats 480 0% Heavy Industry

Hammarsdale 230 0% Textiles, Clothing, Chicken

Berea Ridge Not available Health, Retail Offices

Beachfront Not available Retail, Tourism

Point Not available Retail, Tourism

Bluff Not available Retail, Tourism

Victoria Embankment Not available Sport (Sailing, Boating), Tourism

Greyville Not available Sport (Horse Racing, Golf), Tourism, Offices Publishing

Kings Park Not available Sport (Rugby, Golf Swimming, Soccer), Tourism

Umdloti Not available Tourism

TOTAL 484 200 100%

Source: Not indicated in Graham Muller (2006)

This table provides an indication of the current significance of the Outer West area in terms of the

eThekwini economy. It is noted from this that the Hillcrest, Harrison Flats and Hammarsdale areas

cannot be viewed as significant employment nodes. This suggests that the majority of people in the

Shongweni catchment (essentially the Outer West area) have to travel to access economic and job

opportunities.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

8

2.4. RECENT TRENDS IN SPATIAL ECONOMIC DEVELOPMENT

Over the past decade the most visible spatial economic development trend was expansion and

consolidation of development to the north of Durban. This development is attributed primarily to

the pro-active approach taken by one major landowner in the area and a fully integrated

development approach taken. This integrated development approach supported residential, retail,

industrial, entertainment and public infrastructure developments. The most notable examples of

these types of development are:

Residential (Edgeview, Somerset Park, Mount Edgecombe, Itala Ridge, La Lucia Ridge,

Broadlands, Izinga Ridge);

Retail (Gateway and surroundings);

Industrial (River Horse Valley and developments around Ballito and King Shaka Airport);

Entertainment (Sibaya Casino and other); and

Public infrastructure (most notably the King Shaka Airport, the Umhlanga Rocks Promenade and

Pier etc).

Planning for future development in the Conurbia and Sibaya areas will further add substantially to

the number of residents in the area. Previous studies (StratPlan 2007) illustrated that at least a 10

fold increase in the population of the Umhlanga Ridge catchment is anticipated, not considering the

continued densification and population growth in existing settlement areas.

Other significant development areas in eThekwini over the past decade include the Point Waterfront

development, the Durban sports precinct including the Moses Mabhida Stadium, expansion of the

vehicle manufacturing industry in Prospecton, the Galleria and related retail developments to the

south of Durban.

Considered within the above context the Outer West area has received limited attention in terms of

development in the same period, with new comparatively small retail developments in Hillcrest, and

some upmarket housing estates in the Botha’s Hill and Water Fall areas, being the only

developments of any significance. These developments, however, do not compete in any way with

the developments in northern, central and southern areas of eThekwini.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

9

3. RETAIL SECTOR

3.1. INTRODUCTION

Historic and current planning for the Shongweni Local Area proposes the establishment of a Town

Centre and several supporting nodes. It is anticipated that in both the proposed Town Centre and

other smaller nodes a strong emphasis will be placed on retail development. This section therefore

explores retail development opportunities in Shongweni, considering specifically the future demand

for such development in the context of current supply.

3.2. TRENDS IN RETAIL SECTOR

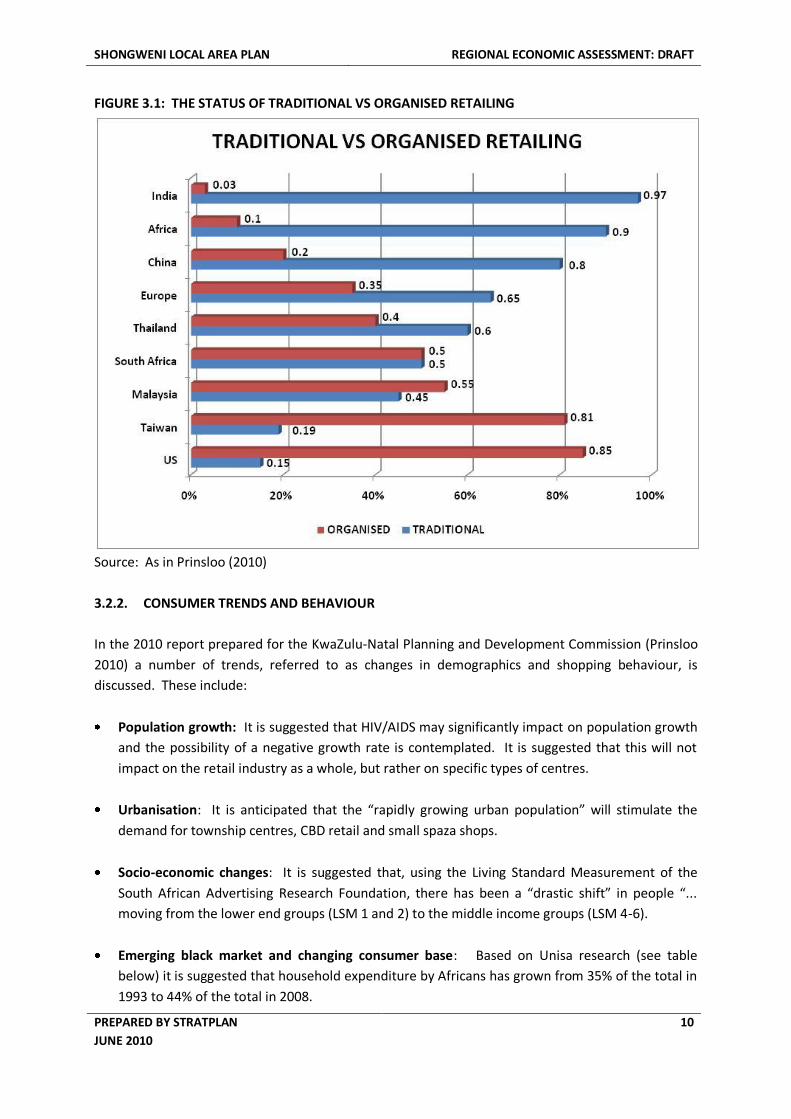

3.2.1. TRADITIONAL VS ORGANISED RETAILING

The retail sector is a significant sector in the economy of any urban area and do not only provide

services to local residents, but is often also a magnet for visitors and investors, as well as a creator of

employment. Prinsloo (2010) notes that over the past four years phenomenal growth has been

experienced specifically in shopping centre space and that growth of 8% per annum in retail space

over the past 15 years have been recorded. Shopping centre space in South Africa now totals 18

million square metres or +/- 50% of all retail sector space.

Prinsloo (2010) distinguishes between traditional retailing, focusing mainly on market areas, street

retailing and retail along specific major roads and strips, also referred to as unplanned retail

development and organised / planned retailing. As indicated above in South Africa the ratio between

traditional and planned retailing is 50/50. This ratio, however, differs substantially across the world

as illustrated in the table below.

From the table it appears as if South Africa is attempting to emulate the United States and that the

ratio of traditional versus organised retailing is more in line with highly developed economies than

that of other developing countries in Africa and countries such as India. Prinsloo (2010) in his

assessment of trends suggests that in South Africa the focus will be on “... planned/organised mall

development, as well as the redevelopment of town centres as is currently happening in the UK”. It

is suggested that the jury is still out on the success of lifestyle centres in South Africa.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

10

FIGURE 3.1: THE STATUS OF TRADITIONAL VS ORGANISED RETAILING

Source: As in Prinsloo (2010)

3.2.2. CONSUMER TRENDS AND BEHAVIOUR

In the 2010 report prepared for the KwaZulu-Natal Planning and Development Commission (Prinsloo

2010) a number of trends, referred to as changes in demographics and shopping behaviour, is

discussed. These include:

Population growth: It is suggested that HIV/AIDS may significantly impact on population growth

and the possibility of a negative growth rate is contemplated. It is suggested that this will not

impact on the retail industry as a whole, but rather on specific types of centres.

Urbanisation: It is anticipated that the “rapidly growing urban population” will stimulate the

demand for township centres, CBD retail and small spaza shops.

Socio-economic changes: It is suggested that, using the Living Standard Measurement of the

South African Advertising Research Foundation, there has been a “drastic shift” in people “...

moving from the lower end groups (LSM 1 and 2) to the middle income groups (LSM 4-6).

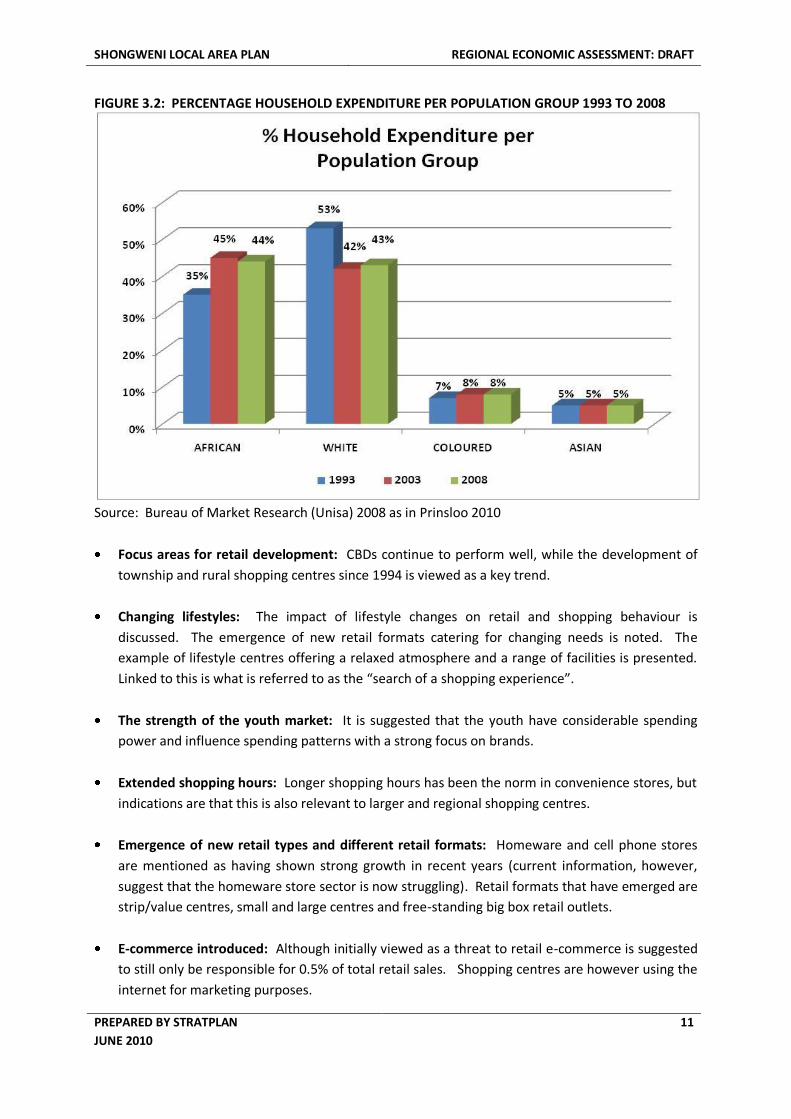

Emerging black market and changing consumer base: Based on Unisa research (see table

below) it is suggested that household expenditure by Africans has grown from 35% of the total in

1993 to 44% of the total in 2008.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

11

FIGURE 3.2: PERCENTAGE HOUSEHOLD EXPENDITURE PER POPULATION GROUP 1993 TO 2008

Source: Bureau of Market Research (Unisa) 2008 as in Prinsloo 2010

Focus areas for retail development: CBDs continue to perform well, while the development of

township and rural shopping centres since 1994 is viewed as a key trend.

Changing lifestyles: The impact of lifestyle changes on retail and shopping behaviour is

discussed. The emergence of new retail formats catering for changing needs is noted. The

example of lifestyle centres offering a relaxed atmosphere and a range of facilities is presented.

Linked to this is what is referred to as the “search of a shopping experience”.

The strength of the youth market: It is suggested that the youth have considerable spending

power and influence spending patterns with a strong focus on brands.

Extended shopping hours: Longer shopping hours has been the norm in convenience stores, but

indications are that this is also relevant to larger and regional shopping centres.

Emergence of new retail types and different retail formats: Homeware and cell phone stores

are mentioned as having shown strong growth in recent years (current information, however,

suggest that the homeware store sector is now struggling). Retail formats that have emerged are

strip/value centres, small and large centres and free-standing big box retail outlets.

E-commerce introduced: Although initially viewed as a threat to retail e-commerce is suggested

to still only be responsible for 0.5% of total retail sales. Shopping centres are however using the

internet for marketing purposes.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

12

3.2.3. SHOPPING CENTRE RELATED TRENDS

Trends more related to the shopping centres themselves highlighted by Prinsloo (2010) include:

Renewal of centres: Reference is made specifically to first generation centres in need of “total

revamps and re-tenanting”.

Increasing shopping centre size: Once established and successful shopping centres attract

additional investment for expansion, e.g. Boardwalk in Richards Bay and the Midlands Mall in

Pietermaritzburg.

Cannibalisation: Prinsloo (2010) describes the process of cannibalisation as occurring when “...

there is an oversupply of retail facilities in a certain area ... the market share of each facility will

then automatically be reduced and outdated facilities will further deteriorate”. This is viewed as

one of the most serious threats for retailers in South Africa.

3.3. REGIONAL RETAIL OFFERING

3.3.1. INTRODUCTION

In order to understand the future demand for retail that may be experienced within the Shongweni

Local Plan area it is necessary to understand current supply. Although no regional or sub-regional

centres exists within close proximity to the area a number of retail areas / centres located outside of

the local area plan area may in future impact on retail development.

This discussion will provide a brief overview of the following concentrations of retail development

and the potential impact thereof on retail development in the study area:

Hillcrest

Kloof

Pinetown

Pavilion (Westville)

Mpumalanga

Camperdown / Cato Ridge

Botha’s Hill

This is followed with a summary of the impact of these developments on future development in the

Shongweni node.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

13

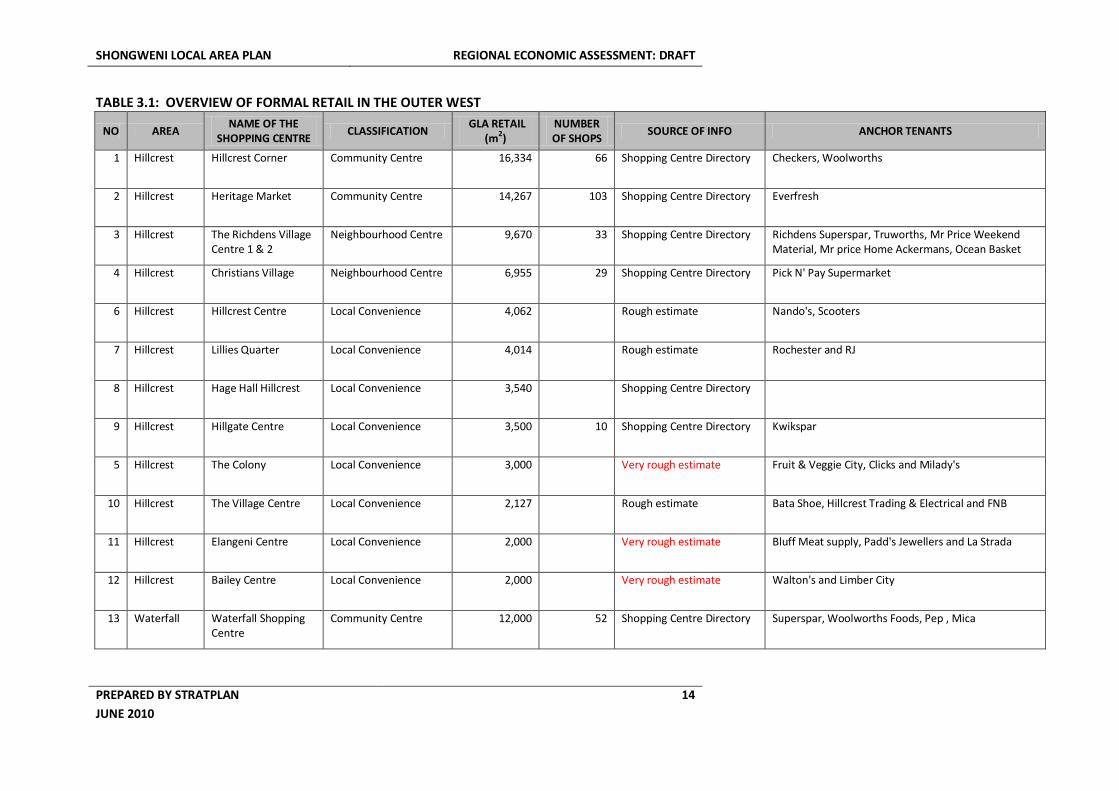

3.3.2. THE CURRENT RETAIL OFFERING

For the purpose of this assessment the StratPlan Team developed a database of retail offerings in the

Outer West area of the eThekwini Municipality. The database was developed using information for

the South African Shopping Centre Directory (2009/10) as a basis and augmenting this with

information from Google surveys, site visits and personal knowledge of the area.

The table below lists the various shopping centres and concentrations of shopping activity currently

in the Outer West area and provides basic information relating to these. The Pinetown area (only

representing the organised retail space) and the Pavilion Shopping Centre are included as these areas

currently have a major impact on retailing trends in the Outer West.

With the inclusion of major Pinetown Shopping Centres and the Pavilion the current retail offering is

around 300 000 m2, with the Pavilion contributing 120 000 m2 of this.

TABLE 3.1 FOLLOW OVERLEAF

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

14

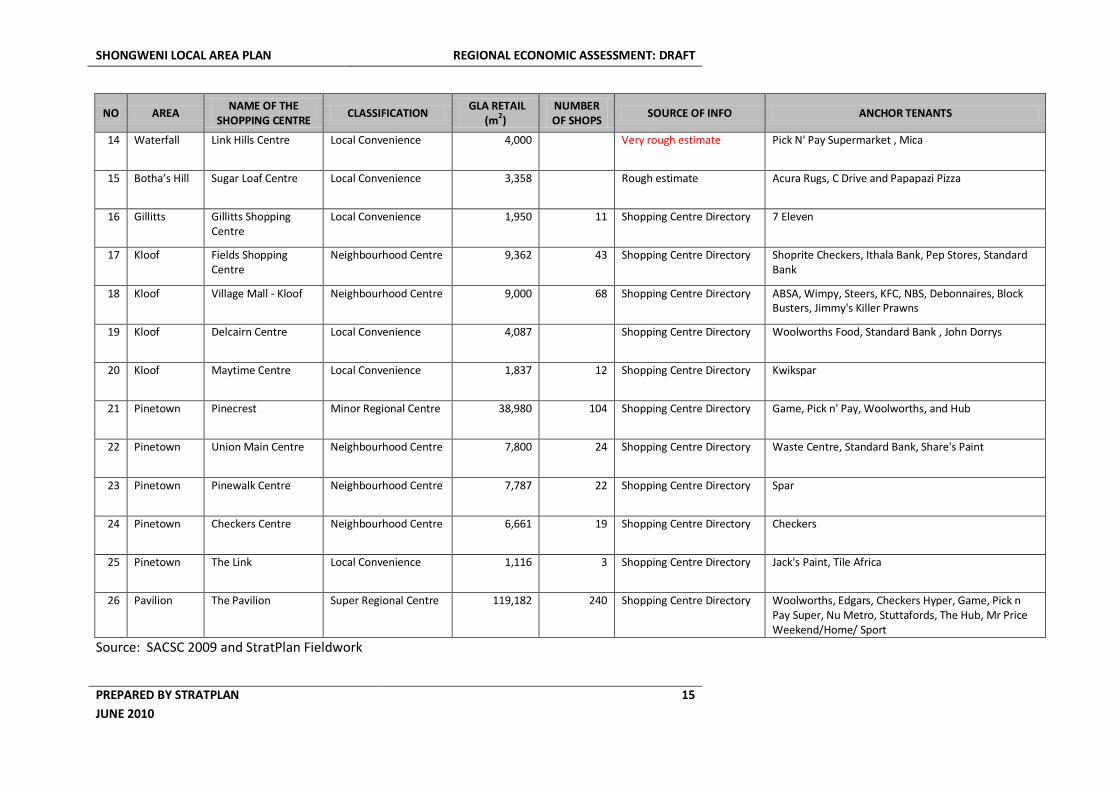

TABLE 3.1: OVERVIEW OF FORMAL RETAIL IN THE OUTER WEST

NO AREA NAME OF THE

SHOPPING CENTRE CLASSIFICATION

GLA RETAIL (m2)

NUMBER OF SHOPS

SOURCE OF INFO ANCHOR TENANTS

1 Hillcrest Hillcrest Corner Community Centre 16,334 66 Shopping Centre Directory Checkers, Woolworths

2 Hillcrest Heritage Market Community Centre 14,267 103 Shopping Centre Directory Everfresh

3 Hillcrest The Richdens Village Centre 1 & 2

Neighbourhood Centre 9,670 33 Shopping Centre Directory Richdens Superspar, Truworths, Mr Price Weekend Material, Mr price Home Ackermans, Ocean Basket

4 Hillcrest Christians Village Neighbourhood Centre 6,955 29 Shopping Centre Directory Pick N' Pay Supermarket

6 Hillcrest Hillcrest Centre Local Convenience 4,062 Rough estimate Nando's, Scooters

7 Hillcrest Lillies Quarter Local Convenience 4,014 Rough estimate Rochester and RJ

8 Hillcrest Hage Hall Hillcrest Local Convenience 3,540 Shopping Centre Directory

9 Hillcrest Hillgate Centre Local Convenience 3,500 10 Shopping Centre Directory Kwikspar

5 Hillcrest The Colony Local Convenience 3,000 Very rough estimate Fruit & Veggie City, Clicks and Milady's

10 Hillcrest The Village Centre Local Convenience 2,127 Rough estimate Bata Shoe, Hillcrest Trading & Electrical and FNB

11 Hillcrest Elangeni Centre Local Convenience 2,000 Very rough estimate Bluff Meat supply, Padd's Jewellers and La Strada

12 Hillcrest Bailey Centre Local Convenience 2,000 Very rough estimate Walton's and Limber City

13 Waterfall Waterfall Shopping Centre

Community Centre 12,000 52 Shopping Centre Directory Superspar, Woolworths Foods, Pep , Mica

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

15

NO AREA NAME OF THE

SHOPPING CENTRE CLASSIFICATION

GLA RETAIL (m

2)

NUMBER OF SHOPS

SOURCE OF INFO ANCHOR TENANTS

14 Waterfall Link Hills Centre Local Convenience 4,000 Very rough estimate Pick N' Pay Supermarket , Mica

15 Botha’s Hill Sugar Loaf Centre Local Convenience 3,358 Rough estimate Acura Rugs, C Drive and Papapazi Pizza

16 Gillitts Gillitts Shopping Centre

Local Convenience 1,950 11 Shopping Centre Directory 7 Eleven

17 Kloof Fields Shopping Centre

Neighbourhood Centre 9,362 43 Shopping Centre Directory Shoprite Checkers, Ithala Bank, Pep Stores, Standard Bank

18 Kloof Village Mall - Kloof Neighbourhood Centre 9,000 68 Shopping Centre Directory ABSA, Wimpy, Steers, KFC, NBS, Debonnaires, Block Busters, Jimmy's Killer Prawns

19 Kloof Delcairn Centre Local Convenience 4,087 Shopping Centre Directory Woolworths Food, Standard Bank , John Dorrys

20 Kloof Maytime Centre Local Convenience 1,837 12 Shopping Centre Directory Kwikspar

21 Pinetown Pinecrest Minor Regional Centre 38,980 104 Shopping Centre Directory Game, Pick n' Pay, Woolworths, and Hub

22 Pinetown Union Main Centre Neighbourhood Centre 7,800 24 Shopping Centre Directory Waste Centre, Standard Bank, Share's Paint

23 Pinetown Pinewalk Centre Neighbourhood Centre 7,787 22 Shopping Centre Directory Spar

24 Pinetown Checkers Centre Neighbourhood Centre 6,661 19 Shopping Centre Directory Checkers

25 Pinetown The Link Local Convenience 1,116 3 Shopping Centre Directory Jack's Paint, Tile Africa

26 Pavilion The Pavilion Super Regional Centre 119,182 240 Shopping Centre Directory Woolworths, Edgars, Checkers Hyper, Game, Pick n Pay Super, Nu Metro, Stuttafords, The Hub, Mr Price Weekend/Home/ Sport

Source: SACSC 2009 and StratPlan Fieldwork

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

16

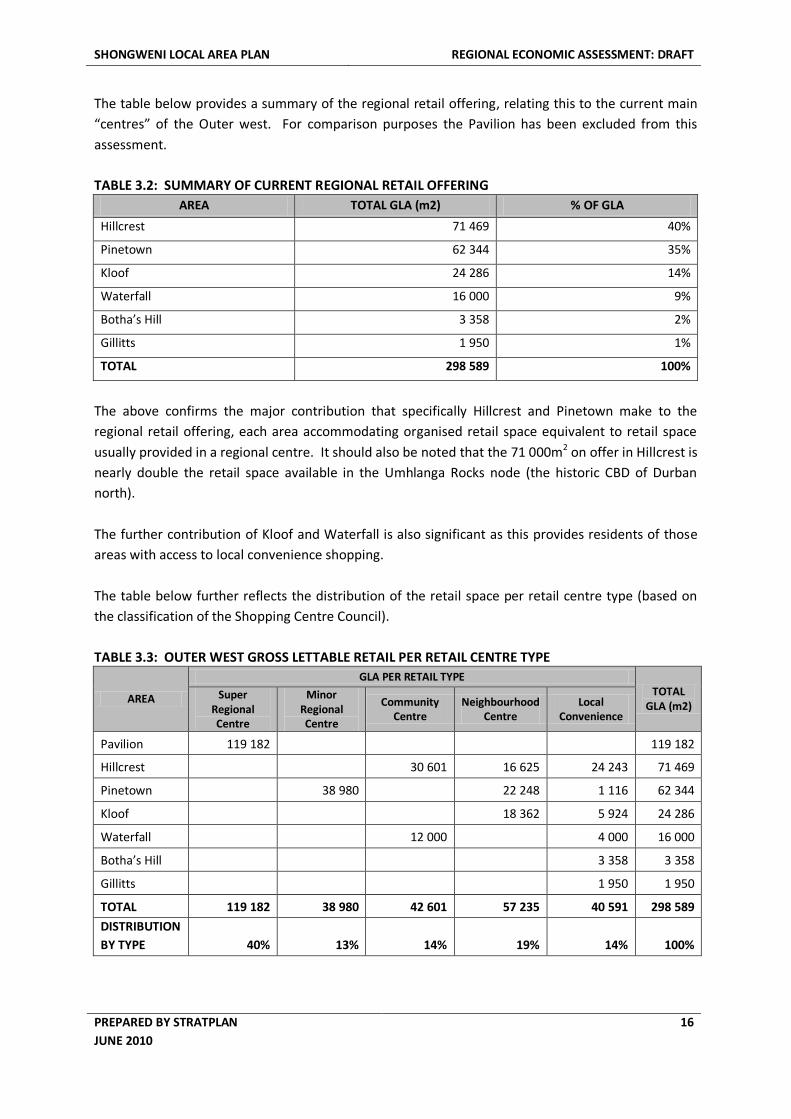

The table below provides a summary of the regional retail offering, relating this to the current main

“centres” of the Outer west. For comparison purposes the Pavilion has been excluded from this

assessment.

TABLE 3.2: SUMMARY OF CURRENT REGIONAL RETAIL OFFERING

AREA TOTAL GLA (m2) % OF GLA

Hillcrest 71 469 40%

Pinetown 62 344 35%

Kloof 24 286 14%

Waterfall 16 000 9%

Botha’s Hill 3 358 2%

Gillitts 1 950 1%

TOTAL 298 589 100%

The above confirms the major contribution that specifically Hillcrest and Pinetown make to the

regional retail offering, each area accommodating organised retail space equivalent to retail space

usually provided in a regional centre. It should also be noted that the 71 000m2 on offer in Hillcrest is

nearly double the retail space available in the Umhlanga Rocks node (the historic CBD of Durban

north).

The further contribution of Kloof and Waterfall is also significant as this provides residents of those

areas with access to local convenience shopping.

The table below further reflects the distribution of the retail space per retail centre type (based on

the classification of the Shopping Centre Council).

TABLE 3.3: OUTER WEST GROSS LETTABLE RETAIL PER RETAIL CENTRE TYPE

AREA

GLA PER RETAIL TYPE TOTAL

GLA (m2) Super

Regional Centre

Minor Regional Centre

Community Centre

Neighbourhood Centre

Local Convenience

Pavilion 119 182

119 182

Hillcrest

30 601 16 625 24 243 71 469

Pinetown

38 980

22 248 1 116 62 344

Kloof

18 362 5 924 24 286

Waterfall

12 000 4 000 16 000

Botha’s Hill

3 358 3 358

Gillitts

1 950 1 950

TOTAL 119 182 38 980 42 601 57 235 40 591 298 589

DISTRIBUTION

BY TYPE 40% 13% 14% 19% 14% 100%

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

17

Following from the above, the sections that follow provide a brief discussion of the retail situation in

each of the key retail nodes. The areas where retail is currently limited, such as Mpumalanga and

Cato Ridge, is also considered.

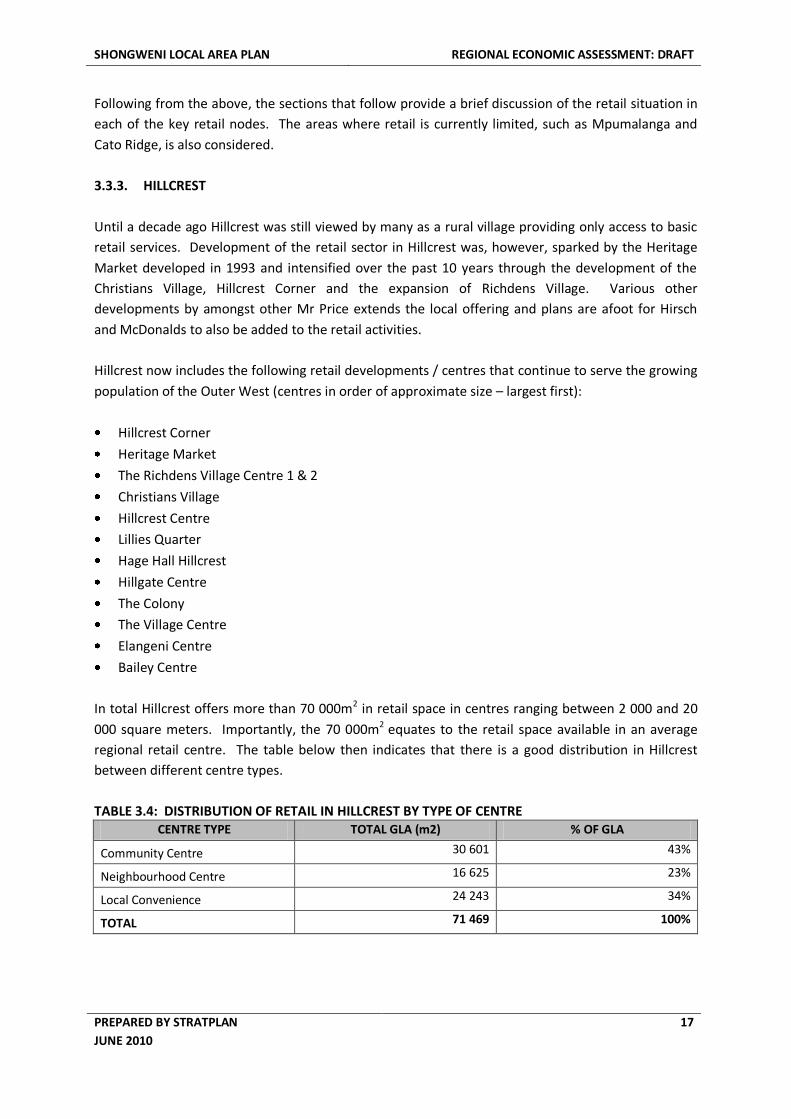

3.3.3. HILLCREST

Until a decade ago Hillcrest was still viewed by many as a rural village providing only access to basic

retail services. Development of the retail sector in Hillcrest was, however, sparked by the Heritage

Market developed in 1993 and intensified over the past 10 years through the development of the

Christians Village, Hillcrest Corner and the expansion of Richdens Village. Various other

developments by amongst other Mr Price extends the local offering and plans are afoot for Hirsch

and McDonalds to also be added to the retail activities.

Hillcrest now includes the following retail developments / centres that continue to serve the growing

population of the Outer West (centres in order of approximate size – largest first):

Hillcrest Corner

Heritage Market

The Richdens Village Centre 1 & 2

Christians Village

Hillcrest Centre

Lillies Quarter

Hage Hall Hillcrest

Hillgate Centre

The Colony

The Village Centre

Elangeni Centre

Bailey Centre

In total Hillcrest offers more than 70 000m2 in retail space in centres ranging between 2 000 and 20

000 square meters. Importantly, the 70 000m2 equates to the retail space available in an average

regional retail centre. The table below then indicates that there is a good distribution in Hillcrest

between different centre types.

TABLE 3.4: DISTRIBUTION OF RETAIL IN HILLCREST BY TYPE OF CENTRE CENTRE TYPE TOTAL GLA (m2) % OF GLA

Community Centre 30 601 43%

Neighbourhood Centre 16 625 23%

Local Convenience 24 243 34%

TOTAL 71 469 100%

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

18

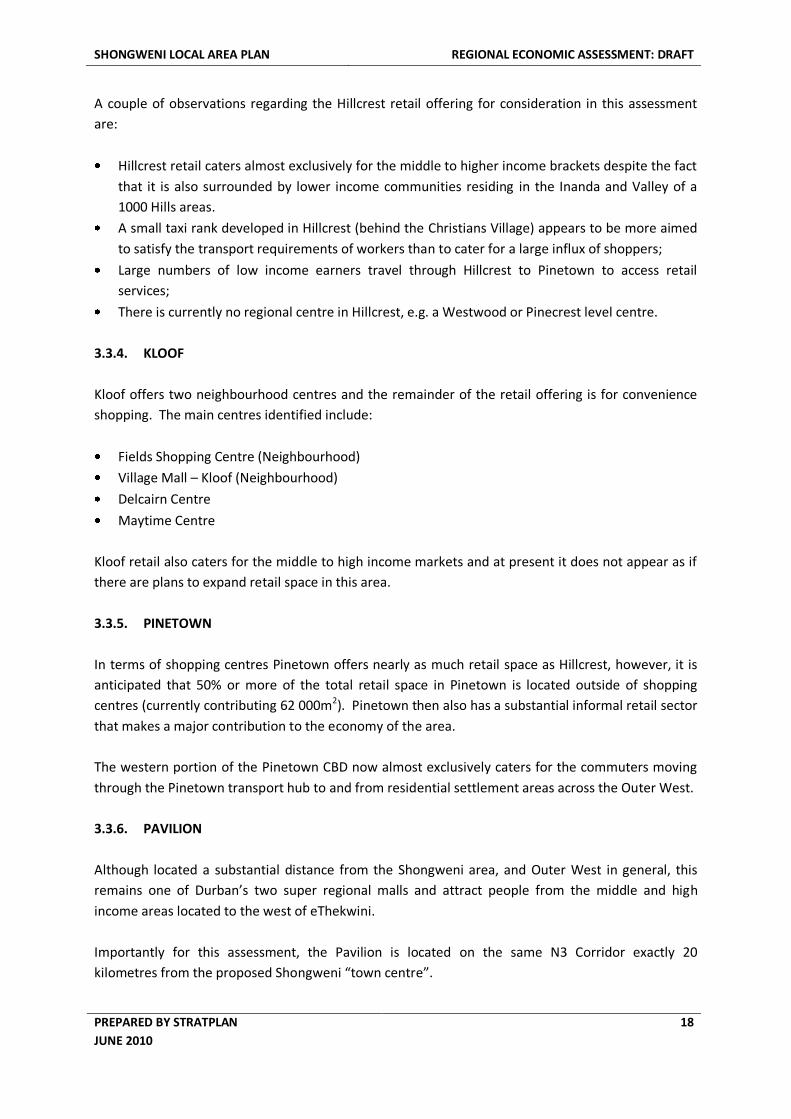

A couple of observations regarding the Hillcrest retail offering for consideration in this assessment

are:

Hillcrest retail caters almost exclusively for the middle to higher income brackets despite the fact

that it is also surrounded by lower income communities residing in the Inanda and Valley of a

1000 Hills areas.

A small taxi rank developed in Hillcrest (behind the Christians Village) appears to be more aimed

to satisfy the transport requirements of workers than to cater for a large influx of shoppers;

Large numbers of low income earners travel through Hillcrest to Pinetown to access retail

services;

There is currently no regional centre in Hillcrest, e.g. a Westwood or Pinecrest level centre.

3.3.4. KLOOF

Kloof offers two neighbourhood centres and the remainder of the retail offering is for convenience

shopping. The main centres identified include:

Fields Shopping Centre (Neighbourhood)

Village Mall – Kloof (Neighbourhood)

Delcairn Centre

Maytime Centre

Kloof retail also caters for the middle to high income markets and at present it does not appear as if

there are plans to expand retail space in this area.

3.3.5. PINETOWN

In terms of shopping centres Pinetown offers nearly as much retail space as Hillcrest, however, it is

anticipated that 50% or more of the total retail space in Pinetown is located outside of shopping

centres (currently contributing 62 000m2). Pinetown then also has a substantial informal retail sector

that makes a major contribution to the economy of the area.

The western portion of the Pinetown CBD now almost exclusively caters for the commuters moving

through the Pinetown transport hub to and from residential settlement areas across the Outer West.

3.3.6. PAVILION

Although located a substantial distance from the Shongweni area, and Outer West in general, this

remains one of Durban’s two super regional malls and attract people from the middle and high

income areas located to the west of eThekwini.

Importantly for this assessment, the Pavilion is located on the same N3 Corridor exactly 20

kilometres from the proposed Shongweni “town centre”.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

19

3.3.7. MPUMALANGA

Mpumalanga is a major residential area located to the immediate west of the Shongweni Local Area.

Historically Mpumalanga residents have been dependent on accessing commercial and social services

in a number of areas, most notably Pinetown, but also Pietermaritzburg and Cato Ridge.

Recently, the eThekwini Municipality facilitated the establishment of a multi-use development in

Mpumalanga described as follows in a press release:

“Phase One consisting of R30m bulk infrastructure to unlock land in the town centre commenced in

earnest in January 2010. This will allow for various mixed use developments to follow. The 36 week

project, the funding for which comes from the Neighbourhood Development Partnership Grant

(NDPG), will lay the foundation for the R200m investment by Eris Property Group towards the

provision of a 18000 sqm retail shopping centre, which will be the first facility to be established in the

towncentre.”

“The retail shopping centre is to be provisionally known as the Mpumalanga Mall and will comprise a

mix of both national and local retailers. It will substantially increase the much needed retail offering

in the Mpumalanga and Hammarsdale communities, who in the past have had to travel to

Pietermaritzburg, Pinetown or Durban for their household and retail shopping needs.”

It is anticipated that the following public investment will occur subject to completion of negotiations

and business plans with respective government departments:

1. New Metro Police Station

2. Municipal Customer Care Centre (Sizakala) which will accommodate various government

service departments, including a library

3. Social welfare centre

4. Public park with sport and recreational facilities

5. New railway station integrated with nodal transport interchange

6. Health facilities

7. Small trader facilities

It is suggested that the new shopping centre will serve people from the Mpumalanga Township,

Shongweni, Georgedale, Sankhontshe, Mophela, Malangeni, mini Town and Hammarsdale industrial.

It is then anticipated that, considering the proposed 18 000m2 the centre will also fulfil a more

regional function drawing also people residing to the north of the N3.

3.3.8. CATO RIDGE

Dunbar’s Centre in Cato Ridge is essentially a Spar Centre, accommodating a Super Spar, a Tops

Liquor Store and a Build It Hardware Store. Other facilities also available at the centre include:

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

20

First National Bank;

Standard Bank and Nedbank ATMs;

Cato Ridge Post Office;

A Pharmacy;

A Surgery; and

A number of smaller stores (e.g. furniture etc).

A total of approximately 3 600m2 of floor space is available in this development. A surfaced parking

area and small “taxi shed” is also on the site.

Although a relatively small centre this caters for a much larger community.

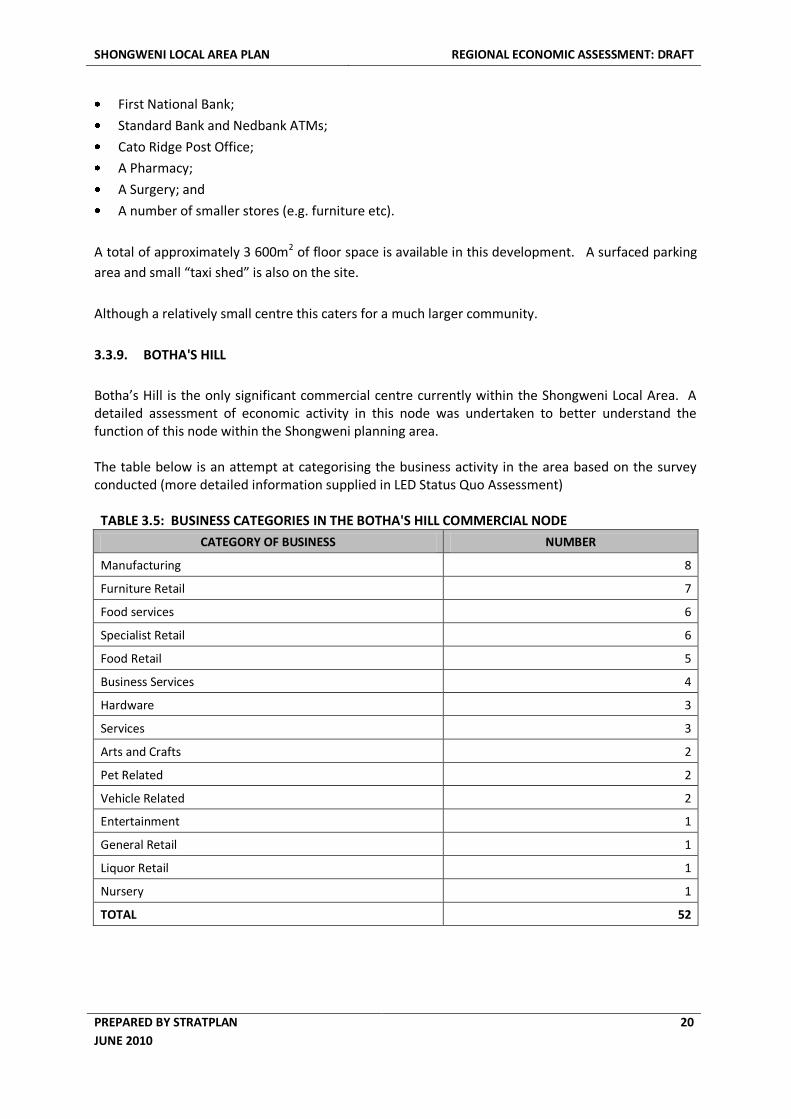

3.3.9. BOTHA'S HILL

Botha’s Hill is the only significant commercial centre currently within the Shongweni Local Area. A detailed assessment of economic activity in this node was undertaken to better understand the function of this node within the Shongweni planning area. The table below is an attempt at categorising the business activity in the area based on the survey conducted (more detailed information supplied in LED Status Quo Assessment) TABLE 3.5: BUSINESS CATEGORIES IN THE BOTHA'S HILL COMMERCIAL NODE

CATEGORY OF BUSINESS NUMBER

Manufacturing 8

Furniture Retail 7

Food services 6

Specialist Retail 6

Food Retail 5

Business Services 4

Hardware 3

Services 3

Arts and Crafts 2

Pet Related 2

Vehicle Related 2

Entertainment 1

General Retail 1

Liquor Retail 1

Nursery 1

TOTAL 52

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

21

The above table confirms that there is not a specific focus of business activity in the node, but that the area is home to a range of economic activities ranging from manufacturing to specialist retail. It is interesting to note the number of furniture retailers identified, specifically considering that these establishments service a vastly different market (higher income) from that served by for instance the larger food and hardware retailers (lower income). The area also includes four smaller groupings of businesses (centres) where more specialised business and retail services are offered. From the above and visits to the area it is concluded that the Botha’s Hill node serves vastly different markets that can potentially be divided into three categories:

The lower income population residing in the Valley of a 1000 Hills;

The local residents in settlements mainly along the R103; and

Visitors or tourists visiting the area. Importantly, the Botha’s Hill area serves as a commercial node for only a limited portion of the Shongweni Local Area.

3.4. POTENTIAL RETAIL CATCHMENTS

3.4.1. INTRODUCTION

At the outset of this section it must be indicated that a comprehensive model identifying the most

appropriate locations for retail development in the eThekwini Municipality should be developed and

should guide future decision-making regarding retail development. As this is not within the scope of

this assessment this section takes a preliminary look at potential retail catchments specifically for the

Shongweni LAP area. The potential catchment for the Shongweni LAP area covers a major part of the

Outer West area of the eThekwini Municipality.

3.4.2. OVERVIEW OF THE CATCHMENTS

For the purpose of this assessment three catchment zones were identified. The three zones are

defined as follows:

Local Area Plan (LAP) Core: The LAP core area includes all the planning units forming part of the

Shongweni Local Area Plan.

Expanded Core: The expanded area identifies those planning units where, should a suitably

attractive / relevant retail facility be established in the Shongweni Area, the majority of people

will potentially make use of such a facility.

Edge: The edge represents those areas where people may potentially make use of facilities in

Shongweni, but for whom other options may also be available.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

22

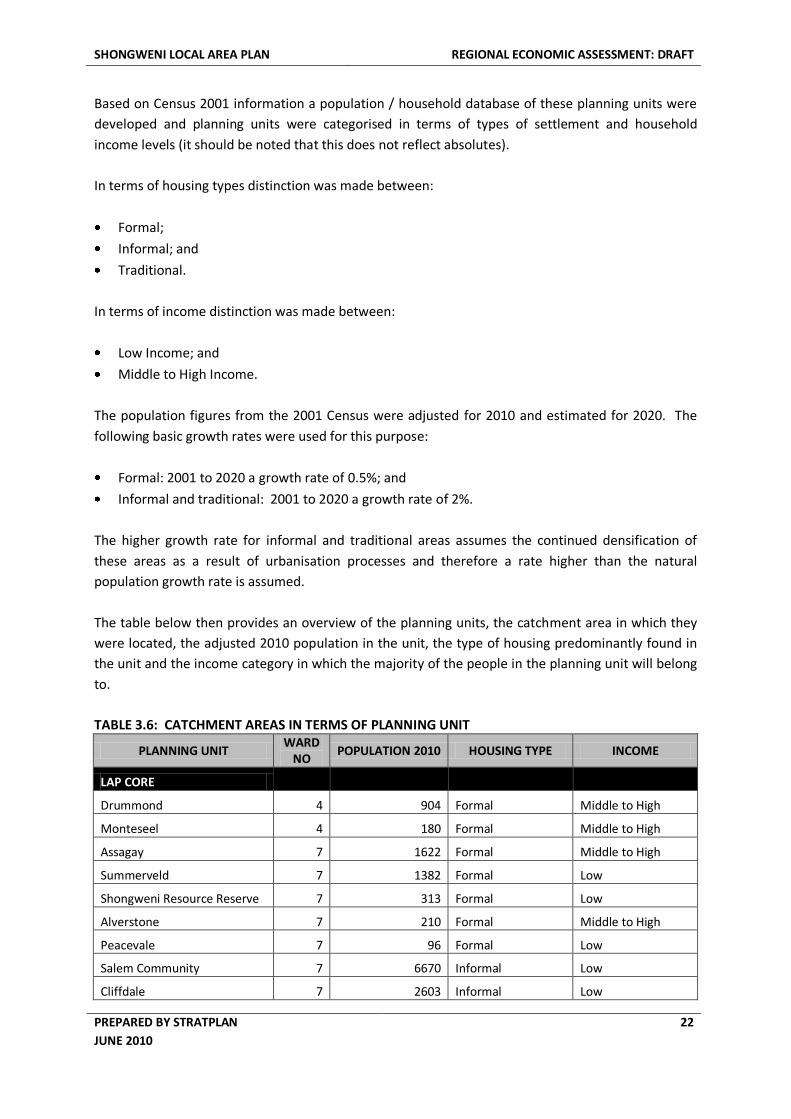

Based on Census 2001 information a population / household database of these planning units were

developed and planning units were categorised in terms of types of settlement and household

income levels (it should be noted that this does not reflect absolutes).

In terms of housing types distinction was made between:

Formal;

Informal; and

Traditional.

In terms of income distinction was made between:

Low Income; and

Middle to High Income.

The population figures from the 2001 Census were adjusted for 2010 and estimated for 2020. The

following basic growth rates were used for this purpose:

Formal: 2001 to 2020 a growth rate of 0.5%; and

Informal and traditional: 2001 to 2020 a growth rate of 2%.

The higher growth rate for informal and traditional areas assumes the continued densification of

these areas as a result of urbanisation processes and therefore a rate higher than the natural

population growth rate is assumed.

The table below then provides an overview of the planning units, the catchment area in which they

were located, the adjusted 2010 population in the unit, the type of housing predominantly found in

the unit and the income category in which the majority of the people in the planning unit will belong

to.

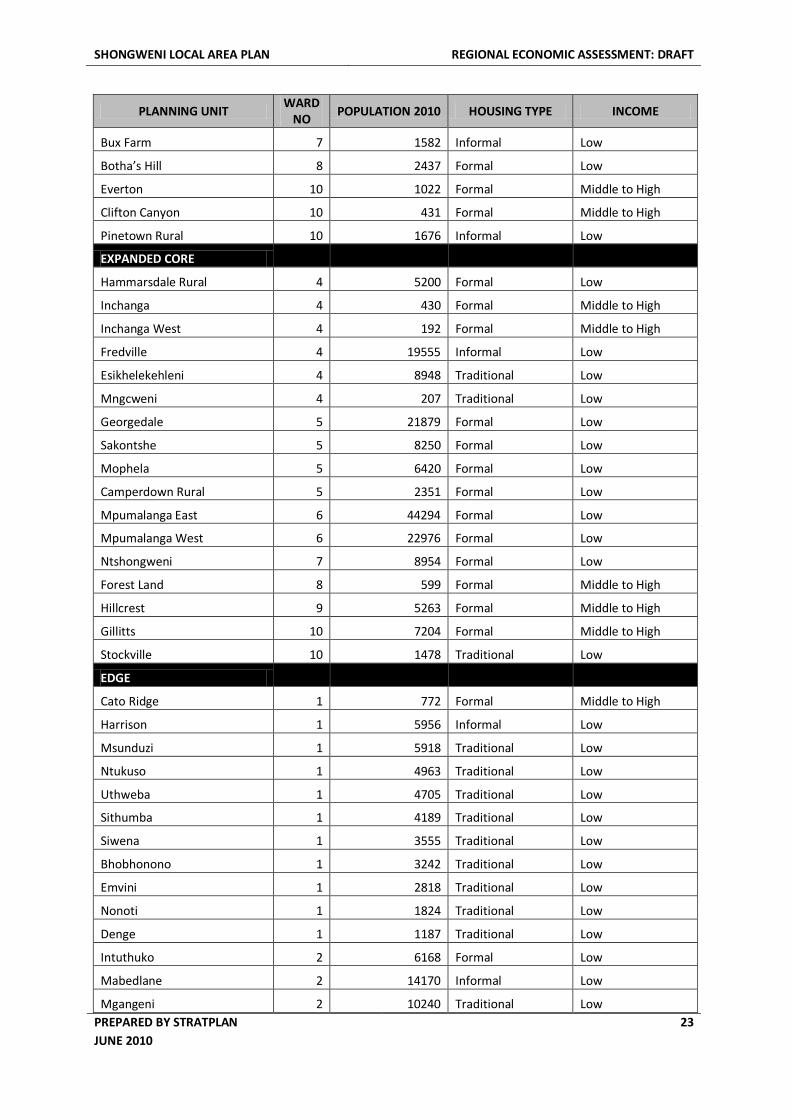

TABLE 3.6: CATCHMENT AREAS IN TERMS OF PLANNING UNIT

PLANNING UNIT WARD

NO POPULATION 2010 HOUSING TYPE INCOME

LAP CORE

Drummond 4 904 Formal Middle to High

Monteseel 4 180 Formal Middle to High

Assagay 7 1622 Formal Middle to High

Summerveld 7 1382 Formal Low

Shongweni Resource Reserve 7 313 Formal Low

Alverstone 7 210 Formal Middle to High

Peacevale 7 96 Formal Low

Salem Community 7 6670 Informal Low

Cliffdale 7 2603 Informal Low

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

23

PLANNING UNIT WARD

NO POPULATION 2010 HOUSING TYPE INCOME

Bux Farm 7 1582 Informal Low

Botha’s Hill 8 2437 Formal Low

Everton 10 1022 Formal Middle to High

Clifton Canyon 10 431 Formal Middle to High

Pinetown Rural 10 1676 Informal Low

EXPANDED CORE

Hammarsdale Rural 4 5200 Formal Low

Inchanga 4 430 Formal Middle to High

Inchanga West 4 192 Formal Middle to High

Fredville 4 19555 Informal Low

Esikhelekehleni 4 8948 Traditional Low

Mngcweni 4 207 Traditional Low

Georgedale 5 21879 Formal Low

Sakontshe 5 8250 Formal Low

Mophela 5 6420 Formal Low

Camperdown Rural 5 2351 Formal Low

Mpumalanga East 6 44294 Formal Low

Mpumalanga West 6 22976 Formal Low

Ntshongweni 7 8954 Formal Low

Forest Land 8 599 Formal Middle to High

Hillcrest 9 5263 Formal Middle to High

Gillitts 10 7204 Formal Middle to High

Stockville 10 1478 Traditional Low

EDGE

Cato Ridge 1 772 Formal Middle to High

Harrison 1 5956 Informal Low

Msunduzi 1 5918 Traditional Low

Ntukuso 1 4963 Traditional Low

Uthweba 1 4705 Traditional Low

Sithumba 1 4189 Traditional Low

Siwena 1 3555 Traditional Low

Bhobhonono 1 3242 Traditional Low

Emvini 1 2818 Traditional Low

Nonoti 1 1824 Traditional Low

Denge 1 1187 Traditional Low

Intuthuko 2 6168 Formal Low

Mabedlane 2 14170 Informal Low

Mgangeni 2 10240 Traditional Low

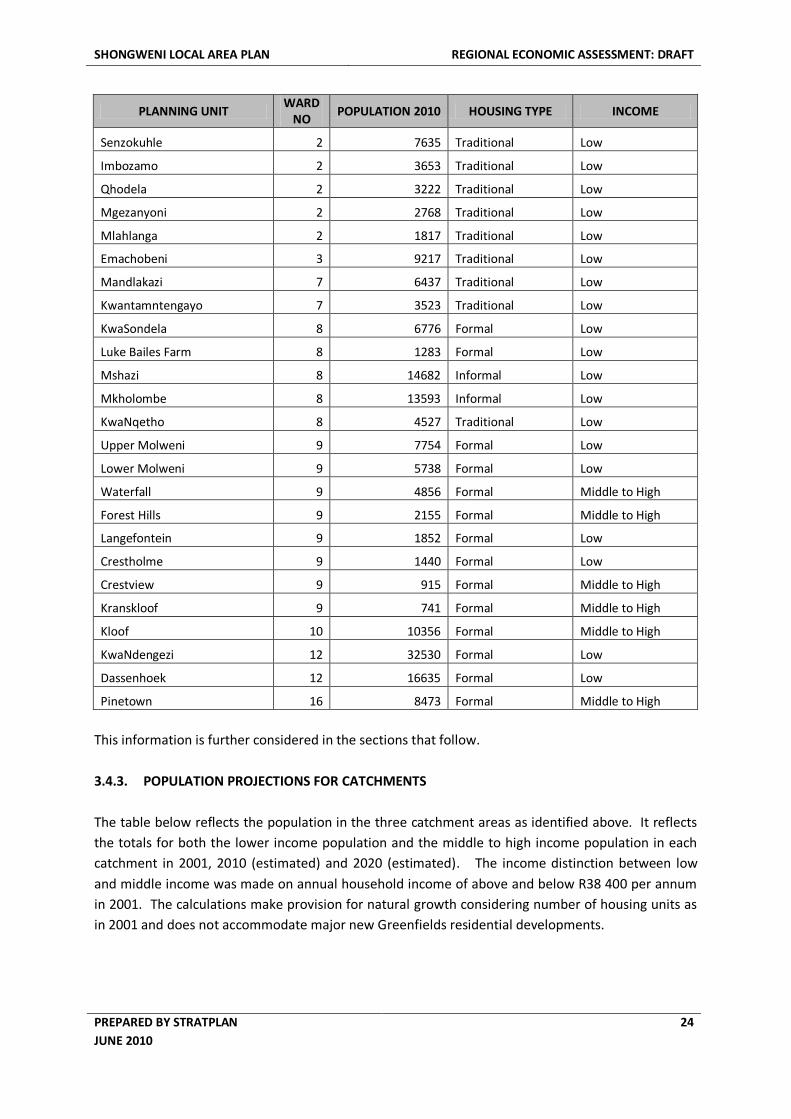

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

24

PLANNING UNIT WARD

NO POPULATION 2010 HOUSING TYPE INCOME

Senzokuhle 2 7635 Traditional Low

Imbozamo 2 3653 Traditional Low

Qhodela 2 3222 Traditional Low

Mgezanyoni 2 2768 Traditional Low

Mlahlanga 2 1817 Traditional Low

Emachobeni 3 9217 Traditional Low

Mandlakazi 7 6437 Traditional Low

Kwantamntengayo 7 3523 Traditional Low

KwaSondela 8 6776 Formal Low

Luke Bailes Farm 8 1283 Formal Low

Mshazi 8 14682 Informal Low

Mkholombe 8 13593 Informal Low

KwaNqetho 8 4527 Traditional Low

Upper Molweni 9 7754 Formal Low

Lower Molweni 9 5738 Formal Low

Waterfall 9 4856 Formal Middle to High

Forest Hills 9 2155 Formal Middle to High

Langefontein 9 1852 Formal Low

Crestholme 9 1440 Formal Low

Crestview 9 915 Formal Middle to High

Kranskloof 9 741 Formal Middle to High

Kloof 10 10356 Formal Middle to High

KwaNdengezi 12 32530 Formal Low

Dassenhoek 12 16635 Formal Low

Pinetown 16 8473 Formal Middle to High

This information is further considered in the sections that follow.

3.4.3. POPULATION PROJECTIONS FOR CATCHMENTS

The table below reflects the population in the three catchment areas as identified above. It reflects

the totals for both the lower income population and the middle to high income population in each

catchment in 2001, 2010 (estimated) and 2020 (estimated). The income distinction between low

and middle income was made on annual household income of above and below R38 400 per annum

in 2001. The calculations make provision for natural growth considering number of housing units as

in 2001 and does not accommodate major new Greenfields residential developments.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

25

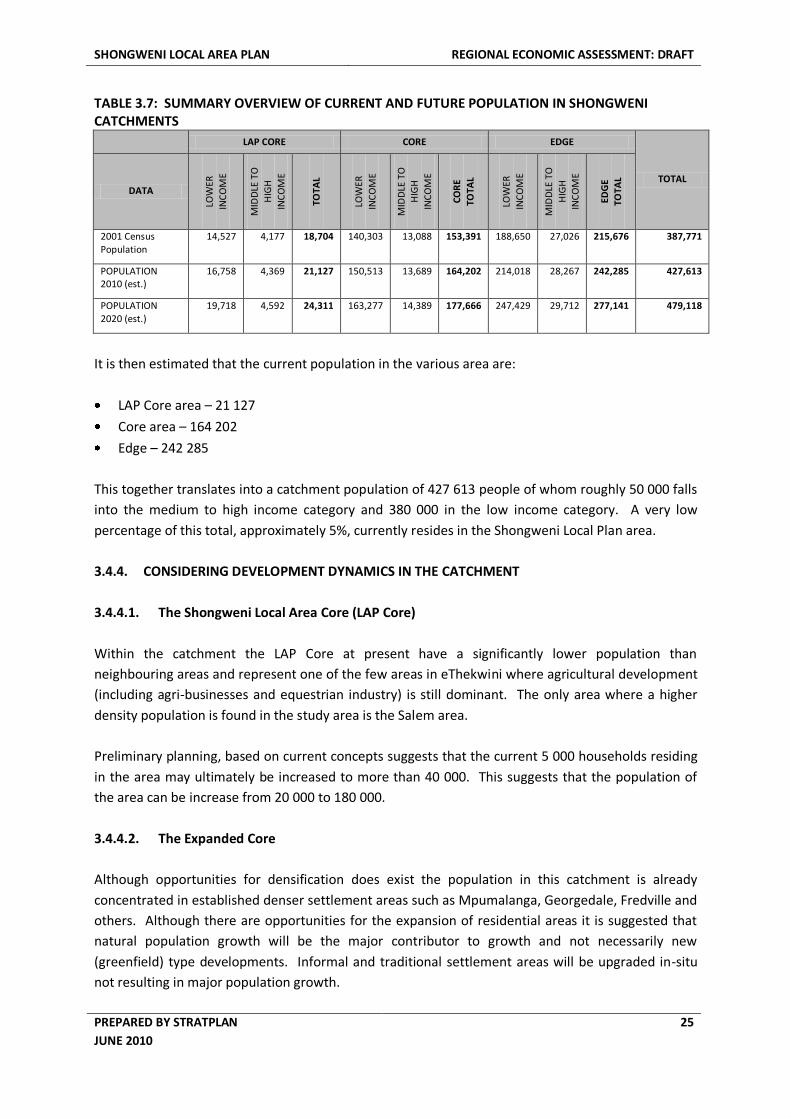

TABLE 3.7: SUMMARY OVERVIEW OF CURRENT AND FUTURE POPULATION IN SHONGWENI CATCHMENTS

LAP CORE CORE EDGE

TOTAL DATA

LOW

ER

INC

OM

E

MID

DLE

TO

HIG

H

INC

OM

E

TOTA

L

LOW

ER

INC

OM

E

MID

DLE

TO

H

IGH

INC

OM

E

CO

RE

TOTA

L

LOW

ER

INC

OM

E

MID

DLE

TO

HIG

H

INC

OM

E

EDG

E

TOTA

L

2001 Census Population

14,527 4,177 18,704 140,303 13,088 153,391 188,650 27,026 215,676 387,771

POPULATION 2010 (est.)

16,758 4,369 21,127 150,513 13,689 164,202 214,018 28,267 242,285 427,613

POPULATION 2020 (est.)

19,718 4,592 24,311 163,277 14,389 177,666 247,429 29,712 277,141 479,118

It is then estimated that the current population in the various area are:

LAP Core area – 21 127

Core area – 164 202

Edge – 242 285

This together translates into a catchment population of 427 613 people of whom roughly 50 000 falls

into the medium to high income category and 380 000 in the low income category. A very low

percentage of this total, approximately 5%, currently resides in the Shongweni Local Plan area.

3.4.4. CONSIDERING DEVELOPMENT DYNAMICS IN THE CATCHMENT

3.4.4.1. The Shongweni Local Area Core (LAP Core)

Within the catchment the LAP Core at present have a significantly lower population than

neighbouring areas and represent one of the few areas in eThekwini where agricultural development

(including agri-businesses and equestrian industry) is still dominant. The only area where a higher

density population is found in the study area is the Salem area.

Preliminary planning, based on current concepts suggests that the current 5 000 households residing

in the area may ultimately be increased to more than 40 000. This suggests that the population of

the area can be increase from 20 000 to 180 000.

3.4.4.2. The Expanded Core

Although opportunities for densification does exist the population in this catchment is already

concentrated in established denser settlement areas such as Mpumalanga, Georgedale, Fredville and

others. Although there are opportunities for the expansion of residential areas it is suggested that

natural population growth will be the major contributor to growth and not necessarily new

(greenfield) type developments. Informal and traditional settlement areas will be upgraded in-situ

not resulting in major population growth.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

26

3.4.4.3. The Edge

The majority of the informal and traditional areas included in the “edge” are located outside of the

urban edge of the Municipality and will in all likelihood not attract new Greenfields development.

Provision will, however, be made for the in-situ upgrading of housing and the provision of services.

3.4.5. THE PASSING TRAFFIC

The Shongweni area is the gateway through which all traffic between not only Durban and

Pietermaritzburg, but also the rest of the country, generally moves. The fact that the Shongweni

area can be accessed from both the N3 and the M13 further enhances accessibility. Despite this the

impact of passing traffic on retail potential in an area such as Shongweni is difficult to establish. No

meaningful standards in this regard exist and examples of similarly located retail centres are limited.

Future studies regarding the impact of passing traffic on the Liberty Mall in Pietermaritzburg, the

Pavilion Shopping Centre, the Canal Walk Centre in Cape Town and others in Gauteng should be

considered.

Potentially substantial passing traffic can be attracted to retail at in the Shongweni node, however,

the extent to which this is successful will depend on the nature of the development. Passing traffic

would generally be attracted to retail areas that offer easily accessible retail space. This may not be

in line with the requirements of the regional residential market.

3.5. SHOPPING CENTRE STANDARDS

3.5.1. INTRODUCTION

Shopping centre potential assessments, specifically in the South African rural context, is not a science

(at least not yet), and is often directly influenced by the “gut feel” of the developer for whom the

assessment is being made. Prinsloo (2010) suggests that one technique that is useful is “per capita

retail space warranted per annum”. It is, however, acknowledged that it is “... difficult if there is a

lot of cross shopping between different areas, and if the retail supply is not fully known”. He further

indicates that these techniques have in recent years been supplemented by “major advances in data

availability and processing, and in computerised functionality”.

The standards, i.e. number of persons to be served by a specific type/size of centre, can merely be

used as indicative of where an opportunity may potentially exist. Whether the actual development

will be successful will ultimately depend on the facility or conglomeration of facilities having the

correct market focus, including consideration of price, product range, quality etc.

This section takes a brief look at the general approach taken in determining retail potential and

indicates how this will be applied to the Shongweni Local Area.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

27

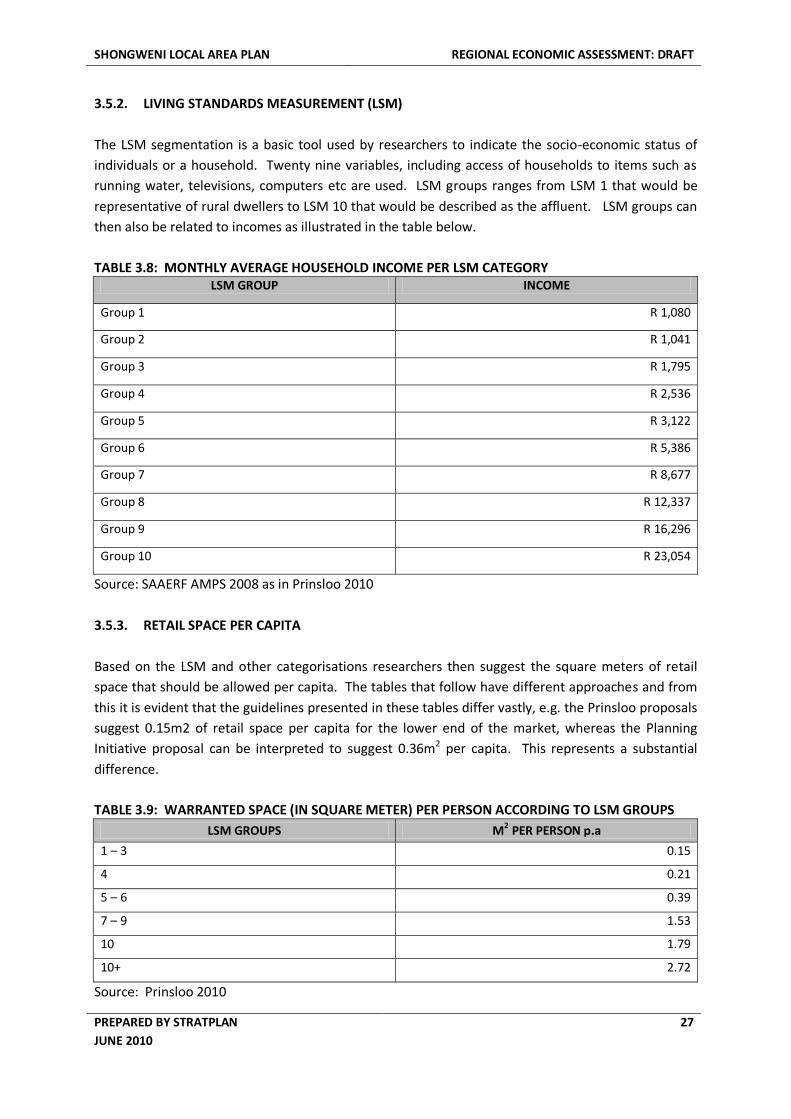

3.5.2. LIVING STANDARDS MEASUREMENT (LSM)

The LSM segmentation is a basic tool used by researchers to indicate the socio-economic status of

individuals or a household. Twenty nine variables, including access of households to items such as

running water, televisions, computers etc are used. LSM groups ranges from LSM 1 that would be

representative of rural dwellers to LSM 10 that would be described as the affluent. LSM groups can

then also be related to incomes as illustrated in the table below.

TABLE 3.8: MONTHLY AVERAGE HOUSEHOLD INCOME PER LSM CATEGORY LSM GROUP INCOME

Group 1 R 1,080

Group 2 R 1,041

Group 3 R 1,795

Group 4 R 2,536

Group 5 R 3,122

Group 6 R 5,386

Group 7 R 8,677

Group 8 R 12,337

Group 9 R 16,296

Group 10 R 23,054

Source: SAAERF AMPS 2008 as in Prinsloo 2010

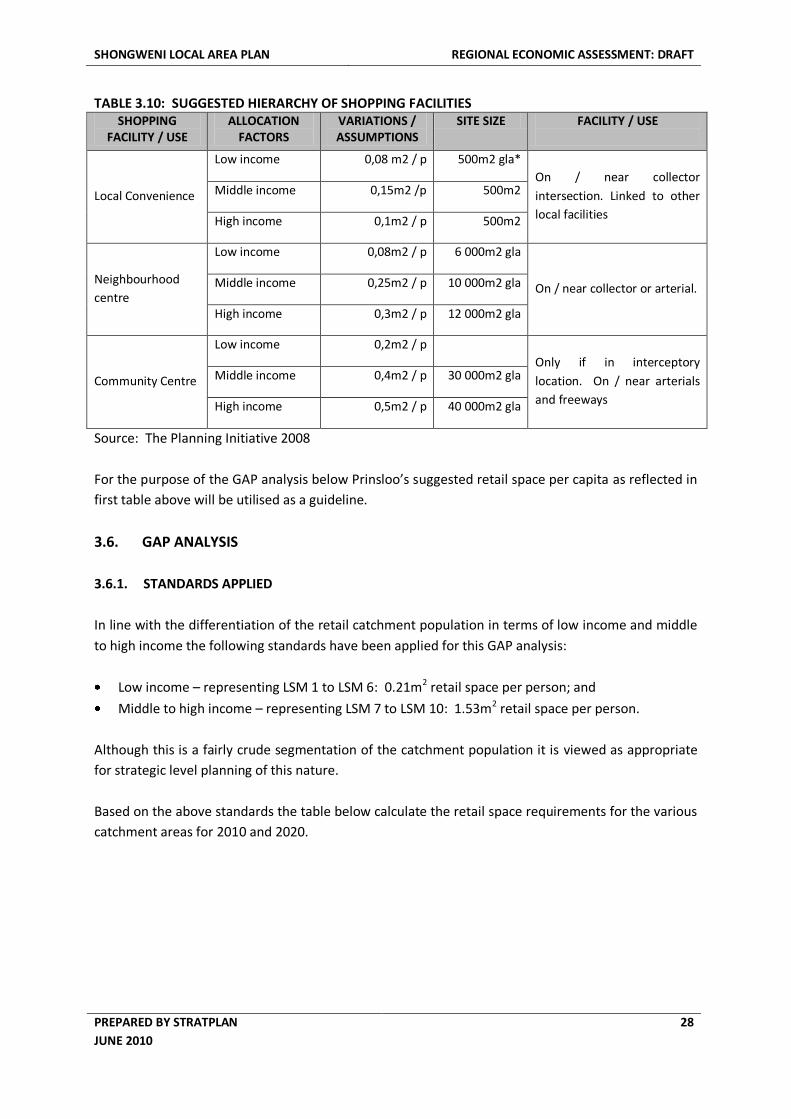

3.5.3. RETAIL SPACE PER CAPITA

Based on the LSM and other categorisations researchers then suggest the square meters of retail

space that should be allowed per capita. The tables that follow have different approaches and from

this it is evident that the guidelines presented in these tables differ vastly, e.g. the Prinsloo proposals

suggest 0.15m2 of retail space per capita for the lower end of the market, whereas the Planning

Initiative proposal can be interpreted to suggest 0.36m2 per capita. This represents a substantial

difference.

TABLE 3.9: WARRANTED SPACE (IN SQUARE METER) PER PERSON ACCORDING TO LSM GROUPS

LSM GROUPS M2 PER PERSON p.a

1 – 3 0.15

4 0.21

5 – 6 0.39

7 – 9 1.53

10 1.79

10+ 2.72

Source: Prinsloo 2010

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

28

TABLE 3.10: SUGGESTED HIERARCHY OF SHOPPING FACILITIES SHOPPING

FACILITY / USE ALLOCATION

FACTORS VARIATIONS / ASSUMPTIONS

SITE SIZE FACILITY / USE

Local Convenience

Low income 0,08 m2 / p 500m2 gla*

On / near collector

intersection. Linked to other

local facilities

Middle income 0,15m2 /p 500m2

High income 0,1m2 / p 500m2

Neighbourhood

centre

Low income 0,08m2 / p 6 000m2 gla

On / near collector or arterial. Middle income 0,25m2 / p 10 000m2 gla

High income 0,3m2 / p 12 000m2 gla

Community Centre

Low income 0,2m2 / p

Only if in interceptory

location. On / near arterials

and freeways

Middle income 0,4m2 / p 30 000m2 gla

High income 0,5m2 / p 40 000m2 gla

Source: The Planning Initiative 2008

For the purpose of the GAP analysis below Prinsloo’s suggested retail space per capita as reflected in

first table above will be utilised as a guideline.

3.6. GAP ANALYSIS

3.6.1. STANDARDS APPLIED

In line with the differentiation of the retail catchment population in terms of low income and middle

to high income the following standards have been applied for this GAP analysis:

Low income – representing LSM 1 to LSM 6: 0.21m2 retail space per person; and

Middle to high income – representing LSM 7 to LSM 10: 1.53m2 retail space per person.

Although this is a fairly crude segmentation of the catchment population it is viewed as appropriate

for strategic level planning of this nature.

Based on the above standards the table below calculate the retail space requirements for the various

catchment areas for 2010 and 2020.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

29

TABLE 3.11: RETAIL SPACE REQUIREMENTS BASED ON CURRENT POPULATION AND NATURAL GROWTH

CATCHMENT AREA

2010 2020

LOW INCOME MEDIUM TO HIGH

INCOME LOW INCOME

MEDIUM TO HIGH INCOME

Est number

of people

Retail space at 0.21m2

per person

Est number

of people

Retail space at 1.53m2

per person

Est number

of people

Retail space at 0.21m2

per person

Est number

of people

Retail space at 1.53m2

per person

LAP Core 16,572 3,480 4,535 6,939 19,280 4,049 5,010 7,665

Core 141,175 29,647 22,946 35,107 153,077 32,146 24,503 37,489

Edge 204,346 42,913 38,641 59,121 235,732 49,504 42,137 64,469

TOTAL PEOPLE 362,093 66,122 408,089 71,649

RETAIL AREA JUSTIFIED

76,040 101,167 85,699 109,623

The retail space requirements for the LAP core is low and will not be considered separately. The low

income and middle to high income retail space requirements is dealt with in more detail below.

3.6.2. LOW INCOME RETAIL SPACE REQUIREMENTS

The 2010 retail space requirement for the low income group is as follows (not including additional

green field development):

LAP Core and Core = 33,127m2

Edge = 42,913m2

Total = approx. 76 000m2 (increases by 10 000m2 in 2020)

Considering that it is estimated that Pinetown alone provides in excess of 120 000m2 of retail space it

can be suggested that this market is well catered for in terms of retail. The reality, however, is that

Pinetown is not well located for a large section of the catchment population and that the available

retail space is also shared with other income groups and residents of areas such as Clermont and

further afield.

It is therefore suggested that the 18 000m2 retail development under construction in Mpumalanga

will go a long way, specifically in terms of location, in addressing the current requirements of the LAP

Core and Core catchments, as defined above. Further future retail development around Cato Ridge

and Camperdown will further address some of the shopping needs of the low income families

residing to the north west of the Shongweni LAP area.

It is further proposed that opportunities for the establishment of more local retail nodes in rural /

traditional low income areas should be identified and the development thereof should be facilitated

by provincial and local government. This will reduce the need for costly transport and increase the

disposable income of households.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

30

With regard to low income retail space it is therefore concluded that the current offering in regional

nodes is sufficient and that the focus should rather be on the development of existing regional nodes

such as Mpumalanga and more local retail nodes within walking distance or residents of low income

areas.

The additional 10 000m2 required by 2020 could in all likelihood be accommodated in existing

regional and local nodes.

3.6.3. MIDDLE TO HIGH INCOME RETAIL SPACE REQUIREMENTS

The 2010 retail space requirement for the middle to high income group is as follows (not including

additional Greenfield development and densification):

LAP Core and Core = 42,046m2

Edge = 59,121 m2

Total = approx. 101 000m2 (increases by 9 000m2 in 2020)

Considering that the current offering in terms of retail space in Hillcrest, Kloof and Waterfall

(shopping centres only) totals 111 755 m2, it is suggested that, based on the standards used, the area

is currently oversupplied in terms of retail. It should further be noted that this does not consider

utilisation of the space available in Pinetown and the Pavilion by the middle to high income groups in

the Shongweni catchments.

The extent of new upmarket residential development that came on line in the larger Hillcrest region

is difficult to establish and it is accepted that this would have contributed to a substantial increase in

the retail space requirements for the area. Further investigation and quantification of this growth

relevant to the Census 2001 figures should be undertaken.

The following statement in the 2009 Outer West Spatial Development Plan should perhaps be

considered in this regard:

The Retail Sector is influenced by the performance of shopping centres and the buying power of the

nodal catchment. The biggest growth in the form of new developments over the last 5 years has

occurred in Hillcrest and Waterfall. Some of the existing shopping areas on Old Main Road display

minimal shopping activities during the day which may imply that the buying power has either moved

out of Hillcrest or that there is an oversupply of shopping centres. Trends are not very clear as

developers still pursue development in this area despite resistance from the public. Traffic congestion

and lack of waste water disposal options act as deterrents to new development.

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

31

3.6.4. ADDITIONAL RETAIL REQUIREMENTS BASED ON DENSIFICATION OF SHONGWENI LAP AREA

From the above it is suggested that the extent of new retail development in the Shongweni will be

dependent on two factors, viz.

The extent of settlement growth in the Shongweni and Outer West area;

The extent and type of retail space supplied in the Outer West area.

Considering the growth in the Outer West area, the table below extracted from the 2009 Outer West

Spatial Development Plan propose the following potential dwelling units in the Outer West.

TABLE 3.12: POTENTIAL DWELLING UNITS IN OUTER WEST

INA

ND

A D

AM

WES

TER

N

SUB

UR

BS

CA

TO R

IDG

E

MP

UM

ALA

NG

A

ZWEL

I-B

OM

VU

SHO

NG

WEN

I

TOTAL

AREA IN HA 29954 9930 13721 12296 8271 10725 84897

POPULATION – 2006 162089 68811 85940 163101 34233 63315 577489

DWELLING UNITS – 2006 ASSUMING 4 PERS/HHLD

40522 17203 21485 40775 8558 15829 144372

ULTIMATE POTENTIAL UNITS 52751 30400 33564 95694 10982 23626 247017

% OF POTENTIAL UNITS 21.36% 12.31% 13.59% 38.74% 4.45% 9.56% 100%

METRO POPULATION 3 500 000

Source: Outer West Spatial Development Plan 2009

The table below translates the above recommendations into additional retail space requirements.

TABLE 3.13: ADDITIONAL RETAIL SPACE REQUIREMENTS IN THE OUTER WEST

HOUSEHOLDS / UNITS

INCOME

GROUP

RETAIL

SPACE

PER

PERSON

ADDITIONAL

RETAIL

SPACE LOCAL AREA CURRENT FUTURE ADDITIONAL ADDITIONAL POPULATION

Inanda Dam 40,522 52,751 12,229 48,916 Low 0.21m2 10,272

Western Suburbs 17,203 30,400 13,197 52,788 Middle + 1.53m2 80,766

Cato Ridge 21,485 33,564 12,079 48,316 Low 0.21m2 10,146

Mpumalanga 40,775 95,694 54,919 219,676 Low 0.21m2 46,132

Zwelibomvu 8,558 10,982 2,424 9,696 Low 0.21m2 2,036

Shongweni 15,829 23,626 7,797 31,188 Middle + 1.53m2 47,718

TOTAL 144,372 247,017 102,645 410,580

Additional Low Income Retail Space 68,587

Additional Middle to High Income Retail Space 128,483

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

32

The rate of future urban growth in the Outer West will depend on a number of factors, but

importantly access to job opportunities and the availability of alternative housing closer to the CBD /

SDB / Pinetown areas of employment will have a major impact on this growth rate. It is highly

possible that the above numbers of units will only be achieved in a 50 year timescale.

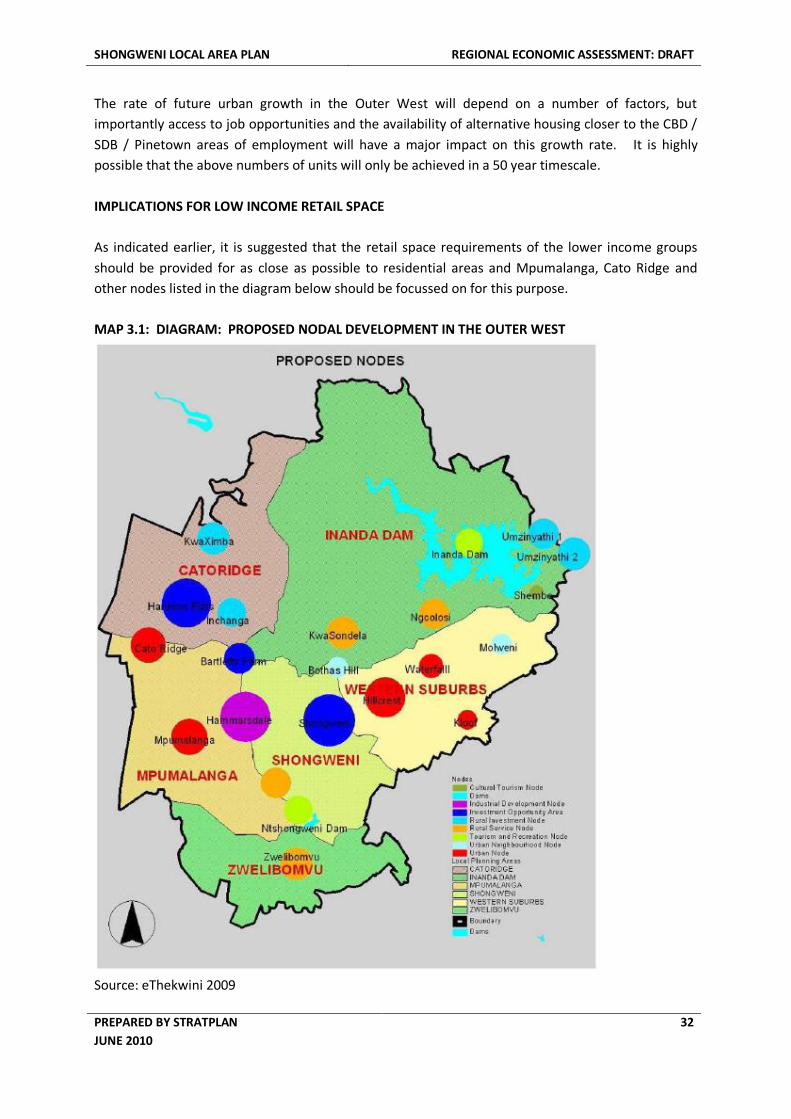

IMPLICATIONS FOR LOW INCOME RETAIL SPACE

As indicated earlier, it is suggested that the retail space requirements of the lower income groups

should be provided for as close as possible to residential areas and Mpumalanga, Cato Ridge and

other nodes listed in the diagram below should be focussed on for this purpose.

MAP 3.1: DIAGRAM: PROPOSED NODAL DEVELOPMENT IN THE OUTER WEST

Source: eThekwini 2009

SHONGWENI LOCAL AREA PLAN REGIONAL ECONOMIC ASSESSMENT: DRAFT

PREPARED BY STRATPLAN

JUNE 2010

33

Further to this, it is suggested that the above projected retail space requirements for the low income

groups may be found to be to low in future due to changing retail needs and patterns of this group.

Also, it is hoped that employment and income patterns in the low income areas improve over time

allowing for a greater proportion of the low income group to be accommodated in the middle to high

income groups.

IMPLICATIONS FOR MIDDLE TO HIGH INCOME RETAIL SPACE

Accommodating future retail space growth for the middle to high income groups is much more

complex. The above calculations suggest additional provision for 128 000 m2 to be made (different

scenarios regarding this could be explored in future) should household / unit densities reflected in

the OWSDP be considered. Current local area planning for Shongweni suggest that at least 60 000

m2 more retail space may be required (assuming 10 000 [current proposals suggest 20 000] more

middle to high income households accommodated in Shongweni than anticipated in Outer West

Spatial Planning). This suggest a requirement for at least an additional 190 000 m2 of retail space for

the middle to high income population of the Outer West once proposed densities have been

achieved. Considering that the area may well be overtraded at present by 30 000 m2, this

requirement can be reduced to 160 000m2.

The challenge will then be to determine where this space will be developed in the longer term, and

again it is assumed that this will be achieved over a 50 year timescale. It is suggested that the

following nodes will attract some of this space:

Giba Gorge area (currently proposals for commercial / retail development in this area);

Kloof;

Hillcrest;

Waterfall;

Botha’s Hill;

Shongweni Town Centre.

In nodes such as Kloof and Hillcrest additional space will relate to the redevelopment of existing