august-2013 - national power training institute · a seminar presentation of the training report...

TRANSCRIPT

SUMMER TRAINING REPORT

on

REC MECHANISM & REGULATORY FRAMEWORK IN INDIA

Vis-à-vis DEVELOPED COUNTRIES

(COMPARATIVE STUDY AND FUTURE PERSPECTIVE)

At

LARSEN & TOUBRO Ltd., CHENNAI

(Water & Renewable IC)

AUGUST-2013

Under the guidance of :

Mr.S.K.CHOUDHARY

Principal Director,

CAMPS, NPTI

Mr.RAJEEV B. AGARWAL

Business Acquisition Head-L&T

Integrated Mega Solar PV farms

Prepared by

ABHINAV AGRAWAL

MBA - Power Management, Class: 2012-14

Centre for Advanced Management and Power Studies (CAMPS)

NATIONAL POWER TRAINING INSTITUTE (NPTI), Faridabad

Submitted to

MAHARISHI DAYANAND UNIVERSITY, ROHTAK

i

DECLARATION

I, Abhinav Agrawal, student of MBA-Power Management (2012-14) at National Power Training

Institute, Faridabad hereby declare that the Summer Training Report entitled

“REC MECHANISM & REGULATORY FRAMEWORK IN INDIA

Vis-à-vis DEVELOPED COUNTRIES”

(COMPARATIVE STUDY AND FUTURE PERSPECTIVE)

is an original work and the same has not been submitted to any other institute for the award of any

other degree.

A seminar presentation of the Training Report was made on and the

suggestions approved by the faculty were duly incorporated.

Presentation Incharge Signature of Candidate

COUNTER SIGNED PRINCIPAL/DIRECTOR

OF INSTITUE

ii

CERTIFCATE

iii

ACKNOWLEDGEMENT

I have no words to express my sincere gratitude to all the people who had been associated with

me in some way or the other and helped me avail this opportunity for my summer Internship on

the topic “A COMPARITIVE STUDY OF REC MECHANISM & REGULATORY FRAMEWORK IN

INDIA Vis-à-vis DEVELOPED COUNTRIES”.

I express my heartily thanks to Mr. Milan Kumar (Sr. G.M., EDRC) for providing me the

opportunity to work on such an insightful project.

I acknowledge with gratitude and humanity my indebtedness to my Summer Internship guide

Mr. Rajeev Agarwal (Business Acquis i t ion Head -Solar PV) for providing me

excellent guidance and motivation under whom I completed my summer internship.

I would like to take the opportunity to thanks Mr. Prateek (Asst.Manager), Mr.Vineet

(Sr.Engg.), Mr. Dinesh (Sr.Engg.), Mr.Dhruva Ballal (Sr.Engg.) for their guidance and support

throughout the course of my project.

This project would have been quite difficult without the suggestions and guidance of my college

senior at L&T Mr. Gurudutt Bhatt, I would express my sincere thanks to him.

I would like to thank my Project In-charge Mr. S.K.Choudhary (Principal Director, CAMPS)

and Mr. J.S.S. Rao (Principal Director, CP&M, NPTI) Faridabad for his support and guidance

throughout the course of summer internship.

A special thanks to Manju Mam (Director) and Mrs. Indu Maheswari (Dy. Director) for their

guidance throughout my summer internship. I am highly grateful to Dr. Rohit Verma (Dy.

Director) and Dr. K.P.S. Parmar (Asst. Director) and all faculty members for arranging my

internship at L&T (W&R IC) and being a constant source of motivation and guidance

throughout the course of my internship.

Thank you for all for being there for me always.

Abhinav Agrawal

iv

EXECUTIVE SUMMARY India’s expeditiously growing economy and expanding grandiloquent urban population is

catalyzing the appetite of country’s electricity requirement enormously. IEA predicts that by

2020 country will need 327 GW of power generation capacity implying addition of 16 GW per

year. This increase in electricity needs with slower than expected increase in domestic fuel

production has lead country to import of fossil fuels like oil with almost 75% of dependency and

estimated 30% of coal dependency by 2017 on global fuel supply market which is getting

costlier and volatile due to global competition to get access over the scarce resources. This

clearly signifies that for one of the biggest economies of world like India for addressing all issues

like booming economy, energy requirements, climate change, health issues, environmental

commitments made at Kyoto protocol relying on only one sources of energy is not enough and

diversifying the energy security by integrating the renewable by adopting the global schemes like

CDM/JI will be a wise option. Estimations of MNRE and some key consultants say that India

has got a potential of almost 50 GW of wind potential, 18 GW of biomass potential, 15.4 GW of

small hydro power potential and almost near around 67 GW of solar potential till 2017. The

initiatives for promoting RE began back in 1994 with schemes like “Small Wind &Hybrid

Systems” but because of incentive scarce schemes with lesser support the Renewable market

didn’t picked up in the country. Until recently the most effective tool has been „The Electricity

Act 2003 with a clause which required SERC’s to set a Renewable Portfolio Standard within

their states and MNRE also issued guidelines to create an attractive environment for promoting

various technologies in Renewable. The prime minister’s NAPCC released in June 2008,

mandated to meet 15% of power requirements via Renewable by 2020. In the process of

supporting the above target, Jawaharlal Nehru National Solar Mission (JNNSM) targeting 22

GW of solar generations till 2022 was launched in 2009. Taking concern of vibrant-risk taking

entrepreneurial culture of country MNRE announced schemes like Generation Based Incentive

(GBI) and Accelerated Depreciation (AD) in 2008 and 2009 respectively to attract the

developers and various tax/levy deduction-exemption policies for manufacturers in the market.

Almost 21 states have come up with their state level Renewable Policies with attractive Feed in

tariffs (FIT‟s) for RE generators and almost a bunch of benefits for attracting Captive RE

generators as well. Moreover REC mechanism already operational in the market is also expected

to play a revolutionary role in development of India’s Renewable sector. Thus with ample of

natural resources like sunlight, wind, biomass, bagasse, etc available and with the best of the

enabling and supporting environment provided to financial institutions and entrepreneurs by the

central government with some of the smartest policies arsenals today India has come a long way

from just 2% in 1995 to almost 10.9% of renewable mix of installed generations in country and

we believe to lead the renewable market globally in near future but there are some prominent

issues backstabbing this success journey and international learning to improve REC markets.

v

LIST OF ABBREVIATION

AD Accelerated Depreciation

BHEL Bharat Heavy Electricals Limited

CDM Clean Development Mechanism

CEA Central Electricity Authority

CPP Captive Power Plant

CFA Central Finance Assistance

CERC Central Electricity Regulatory Commission

DMRPS Dynamic Minimum Renewable Purchase Standard

DORA Date Of Receiving Application

GHG Green House Gas

GBI Generation Based Incentive

GW Giga Watt

GOI Government of India

IEA International Energy Agency

IPP Independent Power Producer

JI Just Implementation

JNNSM Jawaharlal Nehru National Solar Mission

MW Mega Watt

MWh Mega Watt Hour

MOEF Ministry Of Environment And Forest

MOP Ministry Of Power

MEP Market Equilibrium Price

vi

MU Million Units

NTPC National Thermal Power Corporation

NHPC National Hydro Power Corporation

NEEPCO North Eastern Electric Power Corporation Limited.

NLDC National Load Dispatch Centre

NAPCC National Action Plan for Climate Change

PLF Plant Load Factor

PFC Power Finance Corporation

REC Renewable Energy Certificates

RO Renewable Obligation

ROC Renewable Obligation Certificate

RPO Renewable Purchase Obligation

SEB State Electricity Board

SNA State Nodal Agency

SHP Small Hydro Plant

vii

LIST OF FIGURE AND CHARTS

Figure 1: Electricity Demand and Supply Curve Between 2003 T0 2010 ..................................... 1

Figure 2: Installed Capacity in India (in GW) ................................................................................ 4

Figure 3: Electricity Demand projection in billion units from 2010 till 2020 ................................ 4

Figure 4: RE Installed Capacity ...................................................................................................... 5

Figure 5: Eligibiltiy For Availing REC Benefit ........................................................................... 29

Figure 6: Process Of Issuance Of Roc In U.K. ............................................................................. 43

Figure 7: Large Scale Generation Certificate Trading Procedure ................................................ 58

Figure 8: Small Scale Technology Certificates Trading Procedure .............................................. 59

LIST OF TABLES AND ANNEXURE

Table 1: RE Projects, capital cost and levellised tariff for FY 2013-14 (lakh/MW) by CERC ...... 7

Table 2:Potential of RE technologies (Source: MNRE, 30/JUNE/2013) ..................................... 11

Table 3: Preferential Tariff ........................................................................................................... 22

Table 4: RPO Targets Set By SERC’s (2013) In Accordance With NAPCC Target ................... 24

Table 5: ROC Trading Price U.K. - 2013 ..................................................................................... 44

Table 6: Band Allocation to Different RE Technologies.............................................................. 49

Table 7: LRET Annual Target ...................................................................................................... 56

Table 8: Schedule of Solar Credits Multipliers (Source: ORER) ................................................. 62

Table 9: Solar Credits Calculation ................................................................................................ 62

1

TABLE OF CONTENT

DECLARATION ............................................................................................................................. i

CERTIFCATE ................................................................................................................................ ii

ACKNOWLEDGEMENT ............................................................................................................. iii

EXECUTIVE SUMMARY ........................................................................................................... iv

1 Introduction ............................................................................................................................. 1

1.1 Current Scenario ............................................................................................................... 2

1.2 Indian Power Sector: Demand, Capacity And Projection ................................................ 3

1.3 Role Of Renewable Energy In The In The Power Sector ................................................ 5

1.3.1 Off Grid Renewable Energy ..................................................................................... 6

1.4 Renewable Energy Costs .................................................................................................. 6

1.5 Key Drivers Of Renewable Energy .................................................................................. 8

1.5.1 Accelerated Depreciation: ......................................................................................... 8

1.5.2 Generation Based Incentives: ................................................................................... 8

1.5.3 National Solar Mission: ............................................................................................ 8

1.5.4 Income Tax Holiday: ................................................................................................ 9

1.5.5 Feed-In-Tariff: .......................................................................................................... 9

1.6 Need Of Renewable Energy ........................................................................................... 10

1.6.1 Coal Deficit ............................................................................................................. 10

1.6.2 Greenhouse Gas Emissions ..................................................................................... 10

1.6.3 Clean Development Mechanism And Carbon Markets .......................................... 10

1.6.4 Enormous Renewable Potential .............................................................................. 10

1.6.5 Energy Security ....................................................................................................... 11

1.7 Objective ........................................................................................................................ 12

1.8 Scope Of Work ............................................................................................................... 12

1.9 About The Organization ................................................................................................. 12

2 Literature Review And Research Methodology .................................................................... 15

Literature Review.................................................................................................................... 15

2

2.1 National And International Experience With RECs ...................................................... 15

2.1.1 Rec Implementation In Australia ............................................................................ 15

2.1.2 Rec Implementation In United Kingdom ................................................................ 15

2.1.3 Rec Implementation In Usa .................................................................................... 15

2.1.4 Rec Implementation In India .................................................................................. 16

2.2 Research Methodology ................................................................................................... 21

3 Regulatory Framework For RE deployment ......................................................................... 22

3.1 Feed In Tariffs (Fit) ........................................................................................................ 22

3.2 Renewable Purchase Obligations (RPO)........................................................................ 23

3.3 Renewable Energy Certificates (REC) ........................................................................... 26

4 REC Mechanism .................................................................................................................... 27

4.1 Basics Of REC Mechanism ............................................................................................ 27

4.2 REC Objective: .............................................................................................................. 28

4.3 Pre-Requisites Of Eligible Entity ................................................................................... 29

4.4 Procedure For Implementation Of REC Mechanism .................................................... 31

4.4.1 Procedure For Accreditation (Through State Nodal Agency) ................................ 31

4.4.2 Procedure For Registration ..................................................................................... 32

4.4.3 Procedure For Issuance ........................................................................................... 32

4.4.4 Procedure For Trading And Redemption ................................................................ 33

4.4.5 Trading (Through PXs) ........................................................................................... 33

4.4.6 Redemption (Through PXs) .................................................................................... 34

4.4.7 Compliance Reporting: ........................................................................................... 34

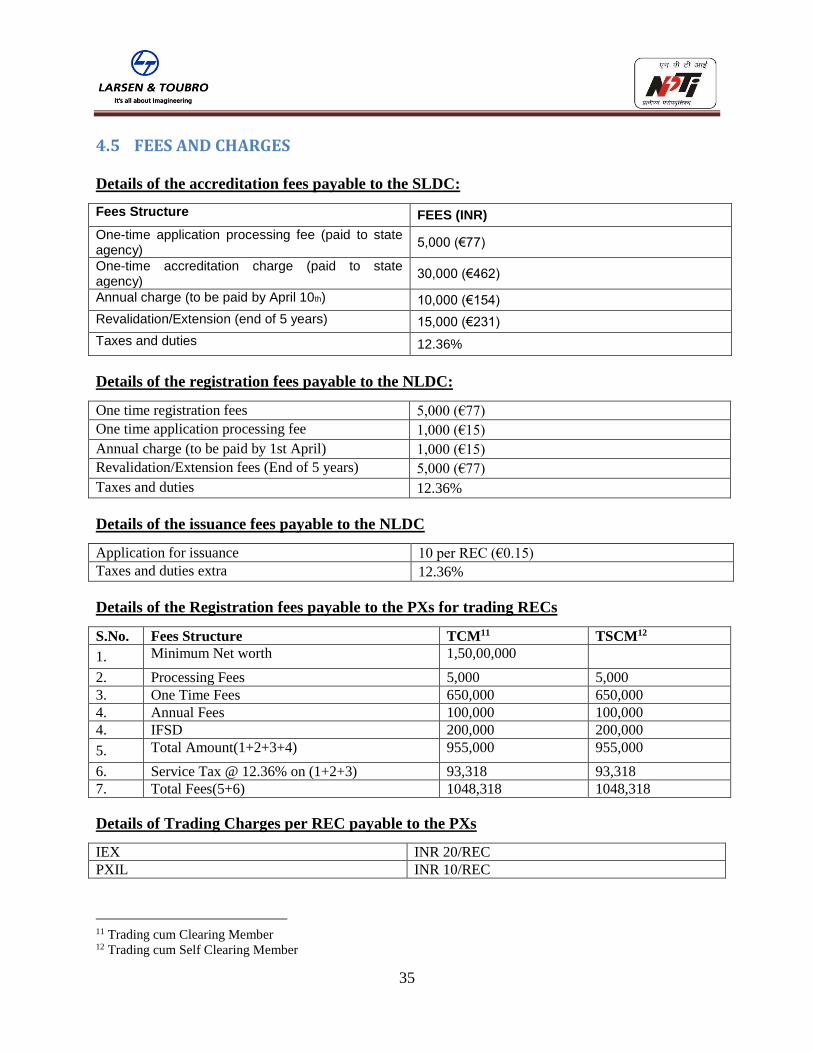

4.5 Fees And Charges........................................................................................................... 35

4.6 Pricing Of Certificate: .................................................................................................... 36

4.7 Recent Amendmnets In Rec Mechanism ....................................................................... 38

5 REC INTERNATIONAL LEARNING ................................................................................ 40

5.1 United Kingdom ............................................................................................................. 40

5.1.1 Introduction ............................................................................................................. 40

5.1.2 Technology Banding of Renewable Obligation ...................................................... 41

3

5.1.3 Implementation Authority:...................................................................................... 42

5.1.4 Issuance Of ROCs ................................................................................................... 43

5.1.5 How the value of a ROC is determined .................................................................. 44

5.1.6 Setting the obligation level ..................................................................................... 45

5.1.7 Recent Amendment In Ro Banding (2013-2017) ................................................... 45

5.1.8 Band Allocation for RE Technologies .................................................................... 46

5.1.9 Renewable Obligation:............................................................................................ 51

5.1.10 Future of the Renewables Obligation in UK........................................................... 52

5.2 AUSTRALIA ................................................................................................................. 53

5.2.1 Introduction ............................................................................................................. 54

5.2.2 Regulatory Authorities ............................................................................................ 54

5.2.3 Small-scale Renewable Energy Scheme (SRES) .................................................... 54

5.2.4 Large-scale Renewable Energy Target ................................................................... 55

5.2.5 Types of Renewable Energy Certificates (RECs): .................................................. 57

5.2.6 Failed Certificates ................................................................................................... 63

Renewable Obligation ............................................................................................. 63

6 CONCLUSION AND RECOMMENDATION ................................................................... 66

6.1 Conclusion: .................................................................................................................... 66

6.2 Recommendation:........................................................................................................... 67

6.3 Bibliography .................................................................................................................. 68

6.4 Annexure ........................................................................................................................ 69

1

1 INTRODUCTION

The Indian energy sector is grappling with new challenges, a result of rapid economic growth,

which has become a hallmark of the development agenda of the country. In the last decade, the

Indian economy has experienced growth at 7-8%, transforming the country into the ninth largest

economy in the world. However, in the last couple of years, there has been a slow-down, with

growth rates having dropped to around 5% in FY 2012-13. In the past few years industrial

production has dipped, and with a concurrent lack of quality service delivery, growth rates have

flattened.

The struggling Indian power sector has much to do with this situation. With a perpetual power

deficit of 8-10% for a decade, electricity available for industry and business has been

insufficient. In order to sustain their production, they have resorted to inefficient diesel-fuelled

back-up power. At the same time around 300 million people in rural India wait for a modern

electricity connection in their homes. India’s energy planning, which is based on the twin

objectives of high economic growth and providing electricity to all, is failing to meet either.

India’s domestic power demand in 2012 was 918 billion units and is expected to reach 1,640

billion units by 2020 at 9.8% annual growth. At this count, India will have to almost double its

current installed capacity of210 gigawatts (GW) to 390 GW in the next eight years. This seems

highly unlikely, given the over-dependence on conventional sources for electricity generation,

and the apathetic view taken towards alternative renewable energy sources by the country’s

energy planners.

There is growing energy inequity between rural and urban areas and also between the developed

and developing states. As stated, 300 million rural citizens are yet to benefit from electricity,

there being a profound injustice in delivery through the centralized system. While the urban-rural

divide in energy supply could be reduced through decentralized systems running on renewable

energy, it is more difficult to bridge the widening gap between developed and not so-developed

states. Thus, to take an example, on one hand, Delhi and Punjab has a per capita electricity

consumption which is more than double the national average, while in Bihar, the per capita

consumption is still rooted at one-fifth the national average.

Figure 1: Electricity Demand and Supply Curve Between 2003 T0 2010

2

1.1 CURRENT SCENARIO

India’s current Centralized energy planning, which tilts heavily on coal and fossil fuel sources,

quixotically leave most of the homes in these coal-bearing and forested regions in darkness. This

fossil fuel addition also tends to be expensive, pushing fiscal deficits to dangerous levels. Thus,

the main concern arises on how to protect our last reserves of forests, their dependent indigenous

communities from destructive coal mining and yet ensure energy security.

Decentralized renewable energy systems are the proverbial silver lining in the Indian power

sector’s dark cloud. This sector is witnessing unprecedented growth, both in terms of capacity

addition and cost reduction, domestically and globally. In 2009-10, renewable energy provided

25% of the country’s gross energy consumption. In the last decade, installed capacity of

renewable energy has grown from just 3%in 2002 to 12% in 2012, largely dominated by wind

energy. Electricity generated from renewable energy sources have also become affordable,

making it highly competitive with conventional sources. With wind having reached grid parity,

the point at which subsidies or government support can be trimmed, and solar expected to reach

that point in the next two to three years, positive market conditions have developed in

Favor of renewable energy in the country.

The threat of climate change, caused by rising global temperatures, has also had it’s its impact on

India’s energy planning. India has pledged to reduce its economy’s greenhouse gas (GHG)

intensity by 20-25%by 2020 from 2005 levels, and promised that its per capita emissions will not

exceed those of developed nations. Further in this direction, the National Action Plan on Climate

Change (NAPCC) was released in2008 by the Government of India, which has set a target of

15% electricity to be generated from renewable energy sources by 2020. However this target is

highly conservative and lacks realism, viewed in conjunction with existing potential, current cost

reduction and past record on installed capacity. In light of growth within the renewable energy

sector, and the gaps in power generation in context of India’s needs, suggests that new targets

need to be set beyond 2020.

In the past few years, the Government of India has introduced some specific regulations and

schemes to boost the renewable energy sector in order to achieve its NAPCC targets and fulfill

its climate pledge to the international community. Of these, the Jawaharlal Nehru National Solar

Mission (JNNSM) is the most significant. A specific target of 20 GW by2022 under JNNSM has

improved market conditions for solar energy technologies which should create rapid diffusion of

these technologies across the country. The JNNSM has already led to decrease in tariffs and

overall project costs. There is growing expectation that the JNNSM’s and corresponding state

solar purchase obligation (SPO) targets will encourage the development of manufacturing

capabilities in solar technology and equipment.

Another important government regulation in this context is the Renewable Purchase Obligation

(RPO) whereby state electricity regulatory commissions (SERCs) are obligated by law to buy a

certain percentage of electricity from renewable energy sources. The guidelines issued in 2010

by Central Electricity Regulatory Commission (CERC) had recommended a standardized RPO

target of 5% in every state with linear increase of 1% annually till2020 to achieve the NAPCC

target of 15%.

3

Introduction of the Renewable Energy Certificate(REC) mechanism by Government of India,

which is a market based mechanism to facilitate the compliance of RPO’s across states of the

country and provides an alternative to obligated entities to fulfill their targets by purchasing

REC’s that are traded on the Indian energy exchanges. This was seen by many as possible

redemption for RPO implementation but with many sellers lined up and hardly any buyers, the

Riches not been able to take a big flight and has failed miserably on the ground.

In reality, the corresponding RPO targets across the different states range between 1 and 20%,

the states having failed in achieving their objective. The current RPO regulation does not have a

clear rationale for the formulation of RPO targets for the respective states. It only factors the

capacity addition from locally available renewable energy resources and overlooks two

important factors that govern power demand – the consumption pattern according to the

consumer profile and purchasing capability of the respective states. The existing RPO regulation

also lacks the presence of an abiding compliance mechanism for achieving its targets. With state

regulators’ hands tied with the lack of an effective penal mechanism and power utilities citing

bad financial conditions as an excuse, there is hardly any compliance to the RPO regulation.

Although the business opportunities that lie in massive shift towards renewable energy is well

understood, the sector faces numerous critical barriers towards its development & deployment,

largely regulatory in nature, perception related, and technology biased and political. To

overcome these challenges, appropriate policy reforms at both the regulatory and market levels

must be ensured.

1.2 INDIAN POWER SECTOR: DEMAND, CAPACITY AND PROJECTION

India, which has to build up its energy infrastructure to keep pace with the economic and social

changes, faces a formidable challenge. Energy and electricity requirements have risen sharply in

recent years, and this trend is likely to continue in the foreseeable future. As on 30 June 20131,

India has a total installed capacity of 225.793 GW, with coal being the principal source of

electricity, followed by large-scale hydroelectric power. Renewable energy takes third place

at 12%, having jumped nearly four times in the last decade2. Of the total installed capacity,

around 30%has been added by the private sector while over40% is controlled or owned by state

governments, the remaining coming under the ambit of the central power sector.

It is expected that by 2020, India’s peak power demand will rise to 1,640 billion units with close

to 8% growth rate, which means that in the next eight years India’s peak power demand will

almost double. With peak power deficit ranging between8-10% and annual power demand

growing at 9%, it will be a giant challenge for India to build its energy infrastructure fast enough

to meet its twin objectives of sustaining a high economic growth rate in the range of 8-9 % for a

longer period of time, while at the same time ensuring all of its citizens have access

to modern electricity supply.

1 CEA Monthly Report – JUNE 2013 2 India’s performance in renewable energy, Energetica India, November-December, 2012

4

Figure 2: Installed Capacity in India (in GW)

Figure 3: Electricity Demand projection in billion units from 2010 till 2020

There are various estimates on capacity addition in the Indian power sector in order to meet

rising power demand as well as reducing the growing power deficit. While Greenpeace, the

European Renewable Energy Council (EREC) and Global Wind Energy Council (GWEC)

estimate that India needs390 GW of installed capacity by 2020, Germany’s GiZ, the US

department of energy and the renewable energy policy network, REN 21 predicts that the

requirement will be 415-440 GW by 2017.3 The Union power ministry has proposed an addition

of 76 GW in the current 12thfive-year plan (2012-17) and another 93 GW in the13thfive-year plan

(2017-22). However, in the 11thfive-year plan, the Government of India missed its revised

installed capacity target of 10 GW which is being carried forward to the current plan period

COAL, 132.288

GAS, 20.359

DIESEL, 1.19

NUCLEAR, 4.78

HYDRO, 39.623

RES, 27.541

5

1.3 ROLE OF RENEWABLE ENERGY IN THE IN THE POWER SECTOR

In 2002, renewable energy accounted for only 3% of the country’s installed capacity at 3,497

MW, in the last 10 years; it has risen to 12%. In 2009, renewable energy provided 25% of India’s

total energy consumption, which clearly shows that it can deliver at economies of scale and

become India’s principal source of energy with the necessary policy, fiscal and regulatory

support in place. Amongst renewable energy technologies, wind is the most dominant with 70%

of the share followed by small-hydro power with 13%. Most of the country’s grid-connected

installed renewable energy capacity– over 91% – exists across just eight states, Tamil Nadu,

Gujarat, Karnataka, Maharashtra, Rajasthan, Andhra Pradesh, Uttar Pradesh and Himachal

Pradesh. (See Annexure 1 for technology-wise installed capacity of renewable energy).

In 2012, actual electricity generation from different renewable energy technologies stood at

46.04 billion units, accounting for 5.76% of the total electricity generation, half of this generated

from wind energy. Among the states, Tamil Nadu, Karnataka, Maharashtra, Gujarat and

Rajasthan account for nearly80% of the total electricity generation from renewable energy

technologies.

Figure 4: RE Installed Capacity

In 2012 WIND energy contributed 2% of the total electricity generated, in the country. The real

potential of wind energy is yet to be realized. It can meet up to 25% of the country’s future

electricity demand by 2020. Wind energy potential in India ranges between 543 GW and 2006

GW at 80meter hub height with turbine density of 9 MW/sq. km5, more than 95% of this in the

five southern and western states of Tamil Nadu, Karnataka, Maharashtra, Gujarat and Andhra

Pradesh. Of this, just one state, Tamil Nadu already provides 40%quite typically, government

estimates wind energy potential conservatively at 103 GW at 80 meter hub height and 50 GW at

WIND68%

SMALL HYDRO13%

SOLAR PV6%

BIOMASS5%

BAGASSE COGEN8%WASTE TO POWER

0%

Renewable Installed Capacity (GW)

6

50 meter hub height6, which indicates that there is still a huge potential available to the

Government of India to exploit.

Among other renewable energy technologies, SOLAR power has the greatest potential and a

long way to go, given the abundance of incident radiation on the Indian mainland. Currently,

solar energy accounts for only 4% of the total renewable energy installed, with the Government

of India under JNNSM seeking to increase capacity addition up to 20 GW by 2022. Now it

seems

that this target is highly conservative, given the current price churning in the Indian solar energy

sector, with costs of solar energy having dropped to 40% of 2008summer prices, and expected to

reduce further. India will add nearly 34 GW of solar energy by 2020 particularly through

massive deployment of solar photovoltaic (PV)and solar rooftop applications, taking solar

energy’s share to 8% of the installed capacity, according to the Greenpeace report, Energy

[R]evolution India.

Other renewable energy technologies are also expected to play a vital role in the future growth of

this sector, with small hydro-power (< 25 MW) tagged at a potential of around 25 GW. This will

mostly be driven by private investments and by 2020 India will have added at least 5 GW of

small hydro-power, even by the most conservative scenarios. Biomass-based electricity

generation, on continuous flow of economical raw material is expected to hold a minimum

potential of 24GW, largely from non-productive agricultural residues and farm product wastes.

1.3.1 OFF GRID RENEWABLE ENERGY

Although there is no clear and explicit assessment of the true potential of off-grid and grid-

interactive distributed renewable energy, It is conservatively estimated that over 4 billion units of

electricity is being generated from different off-grid applications since the period 2011-12 and it

is expected that by2020, this generation, even on an incremental basis will come up to around 27

billion units. Even though electricity generation from off-grid and grid-interactive distributed

renewable energy systems are lacking in quantity, its real impact can be observed by the positive

changes it has brought about in the lives and livelihood of the millions in remote villages of the

country, where centralized electricity schemes like the Rajiv Gandhi Gramin Vidyutikaran

Yojana (RGGVY) have failed to deliver quality electricity supply. A form of small-scale energy

revolution, based on decentralized, distributed and application oriented renewable energy

solutions can be witnessed in some developing but energy-poor states like Uttar Pradesh, Bihar,

West Bengal and Madhya Pradesh. They have not only brought lights to the villages but

transformed the entire village economy.

1.4 RENEWABLE ENERGY COSTS Renewable energy technologies are not just on the verge of being deemed mature technologies

but also, the price for exploring these technologies is falling rapidly, as is evident from the

proposed tariffs by CERC.

Renewable energy technologies fare decently well on learning rate standards, the cost of a

technology which has a learning rate of 0.90 is expected to fall by 10% every time the

cumulative output from the technology doubles. For solar PV this rate stands at 0.8 for the past

30 years and for wind it varies between 0.75-0.94.8 In real market terms the price of PV modules

7

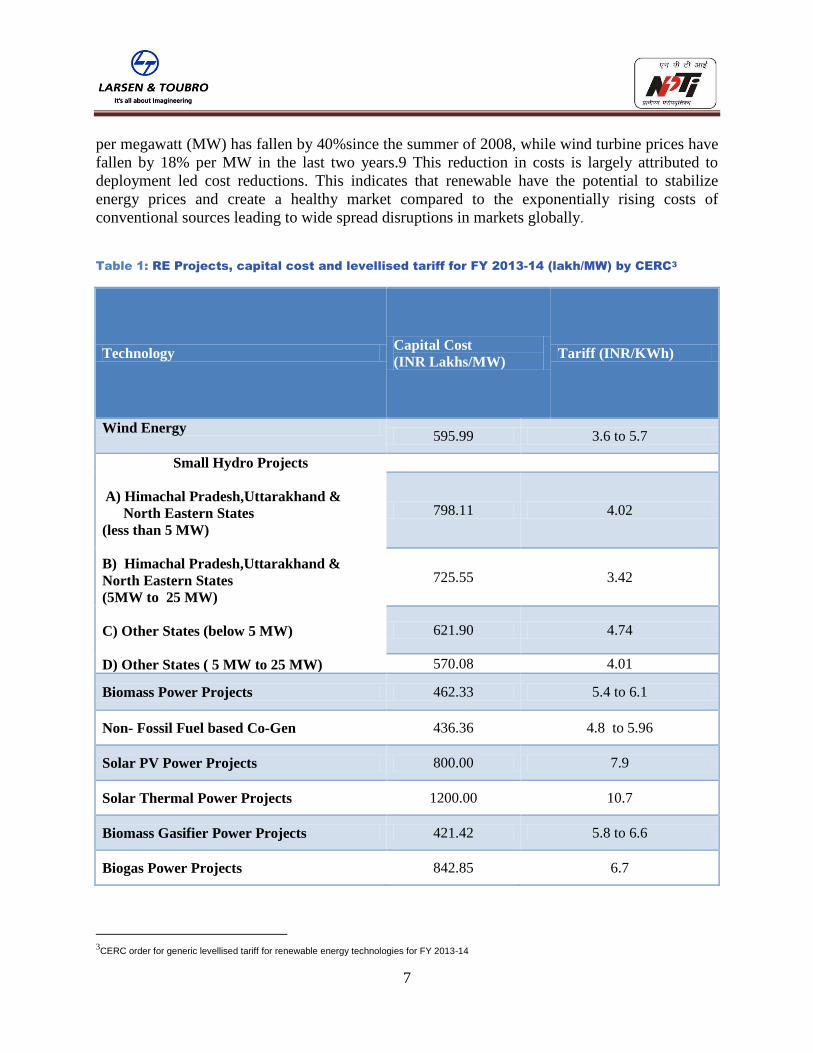

per megawatt (MW) has fallen by 40%since the summer of 2008, while wind turbine prices have

fallen by 18% per MW in the last two years.9 This reduction in costs is largely attributed to

deployment led cost reductions. This indicates that renewable have the potential to stabilize

energy prices and create a healthy market compared to the exponentially rising costs of

conventional sources leading to wide spread disruptions in markets globally.

Table 1: RE Projects, capital cost and levellised tariff for FY 2013-14 (lakh/MW) by CERC3

Technology Capital Cost

(INR Lakhs/MW) Tariff (INR/KWh)

Wind Energy 595.99 3.6 to 5.7

Small Hydro Projects

A) Himachal Pradesh,Uttarakhand &

North Eastern States

(less than 5 MW)

B) Himachal Pradesh,Uttarakhand &

North Eastern States

(5MW to 25 MW)

C) Other States (below 5 MW)

D) Other States ( 5 MW to 25 MW)

798.11 4.02

725.55 3.42

621.90 4.74

570.08 4.01

Biomass Power Projects 462.33 5.4 to 6.1

Non- Fossil Fuel based Co-Gen 436.36 4.8 to 5.96

Solar PV Power Projects 800.00 7.9

Solar Thermal Power Projects 1200.00 10.7

Biomass Gasifier Power Projects 421.42 5.8 to 6.6

Biogas Power Projects 842.85 6.7

3CERC order for generic levellised tariff for renewable energy technologies for FY 2013-14

8

1.5 KEY DRIVERS OF RENEWABLE ENERGY

The growth of RE in India has been catalyzed by several Acts, policies and institutional

measures that have been implemented over the past few years especially post EA 2003.

The following are major drivers of growth of renewable energy in India.

1.5.1 Accelerated Depreciation:

The GoI allowed renewable energy based power producers to claim accelerated depreciation

(AD) at the rate of up to 80% in the first year on a written-down value (WDV) basis under

Section 32, Rule 5 of the Income Tax Act. This was the most significant driver of renewable

energy capacity addition in the past. However, this has resulted, to some extent, in mushrooming

of players with the purpose of off-setting income from other business to claim tax benefits rather

than actual production of electricity. However, AD for wind power projects has been withdrawn

recently to attract attention from more serious players for development of Renewable Energy.

1.5.2 Generation based incentives:

The GoI along with Indian Renewable Energy Development Agency (IREDA) as the nodal

agency, had introduced a scheme for grid interactive wind power projects which provided an

incentive of Rs 0.50 per kilowatt-hour (kWh), with a cap of Rs. 15 lakh per MW per year,

totaling Rs. 62.5 lakh per MW to be availed for a minimum of four years and maximum of 10

years. The scheme was however limited to a capacity of first 4,000 MW commissioned through

GBI on or before 31 March, 2013. Recently the central government withdrew AD benefit for

wind projects. This has slowed down wind energy capacity addition by almost 50% on year-on-

year basis. However, there is a possibility of reinstatement of GBI to attract investments in wind

sector. Subsidy in equipment imports: Some technologies like small hydro, biomass and solar PV

(off grid) systems are provided support through capital subsidy based on installed capacity. For

example, Ministry of New and Renewable Energy (MNRE) provides a capital subsidy of 30%

for off-grid and decentralized solar photovoltaic (SPV) applications.

1.5.3 National Solar Mission:

The Mission has set an overall target of 20,000 MW in three phases: First phase up to 2012/13,

second phase from 2013 to 2017, and the third phase from 2017 to 2022. The mission targets

capacity of grid-connected solar power generation to 1,000 MW by 2013 and 4,000 MW by

2017. It is further envisioned that the solar capacity addition could reach 10,000 MW by 2017

and 20,000 MW by 2022. JNNSM targets, including grid connected, off-grid application and for

solar collectors.

9

1.5.4 Income Tax Holiday:

Section 80 IA of the Income Tax Act offers a 10-year consecutive tax holiday period within a

block of first 15 years during the life cycle of all infrastructure projects which also includes

renewable energy power generation projects.

1.5.5 Feed-in-tariff:

Central and state electricity regulatory commissions (CERCs and SERCs) have notified wind-

specific feed-in-tariff for electricity generated from wind. Also, state-specific tariff for solar

energy in states such as Rajasthan, Gujarat, Madhya Pradesh, and Karnataka have been

announced. Such preferential tariffs have provided attractive returns to investors leading them to

set up projects in various states.

All the above policy measures that have been largely driven by fiscal incentives and subsidies

have resulted in growth of RE supply. However, such measures do not help in large scale

development of RE. For development of renewable energy markets it is important to create

demand pull as well which will result in better pricing of power from RE. Hence, market creation

remains the overwhelming emphasis of the policy makers. In this regard, mechanisms such as

Renewable Purchase Obligation (RPO)4 and Renewable Energy Certificates (REC)5 have been

introduced through policies and regulations.

4 Discussed in Section 3.2 5 Discussed in Section 3.3

10

1.6 NEED OF RENEWABLE ENERGY

1.6.1 Coal Deficit India has got 250 billion tons of coal reserves, but due to poor quality of coal whole of the reserves available can’t be procured and put to use. Annual report of FY 10 of Ministry of Coal clearly states that the maximum amount of coal allocated in country is to the power industry, despite of the above fact CEA has announced that out of the 85 operating thermal power plants (TPP‟s) 7 plants are running at critical stock (coal) level of less than 7 days and 9 stations are running at super critical stock levels of less than 4 days whereas the ideal stock level for pithead plants is 15 days and for other TPP‟s it varies from 20 to 30 days

1.6.2 Greenhouse Gas Emissions

As per the latest CEA report dated 30th June 2013 the overall generation capacity of India is

225.793 GW and almost more than 75 % of installed generation in India comes from thermal

sources which include fossil fuels like coal, diesel and natural gas. But this heavy reliability with

increasing global competition for access of scarce resources and the need for designing the boiler

of plants to soot for the imported coal in the plants. The most important of all is the increasing

greenhouse gas emissions from the plants, presently the India stands at 5th place globally in terms

of greenhouse gas emitters. An overview of GHG inventory for energy sector under Ministry of

Environment and Forest (MOEF) shows the consumption trends of fossil fuels depicting the

rampant increase in the use of fossil fuels in the past decade resulting in a CO2 emissions

increasing at CAGR of almost 4.8% for 1994 to 2006.

1.6.3 Clean Development Mechanism and Carbon Markets The increasing concerns for environment across the world lead to Kyoto Protocol which

ultimately resulted in flexible mechanisms like Clean Development Mechanism (CDM) and Just

Implementation (JI). These have created the path for developing countries like India to

participate in carbon credit markets. Carbon credits can be exchanged between organizations in

international markets at the current market prices. In 2009 when the global GDP declined the

carbon markets grew 6%. Industrial governments of various countries have started working in

this field by implementing domestic policies and regulations. Experience shows that cost of

reducing greenhouse gases in developing countries costs around US$ 1 to 4 as compared to

developed countries where it costs around US$15 to 100 because of various opportunities

available in developing country. Presently India is on 2nd no. behind China for the amount CDM

projects approved across the world.

1.6.4 Enormous Renewable Potential

India’s demographic location makes it a resource rich country as far as renewable are concerned.

There is long coastline of 7517 km facilitating sufficient wind energy potential in states like

11

Tamil Nadu, Karnataka and Gujarat and the country also receives an annual radiations of 5000

trillion KWh/year with an average isolation of 4KWh/day to 7 KWh/day, country also

experiences almost 300 sunny days/year. Biomass has also got a high energy potential in the

country with resources such as firewood, agro-residues and animal wastes, which are mainly

used by rural population also there lies a tremendous off grid renewable power potential to

places where it is costly to extend the grid. Northern and North eastern regions are also having

high potentials in SHPs and currently installation of about 300 MW/year is being achieved in

SHPs. Summary of the renewable potential of different RE technologies and their respective

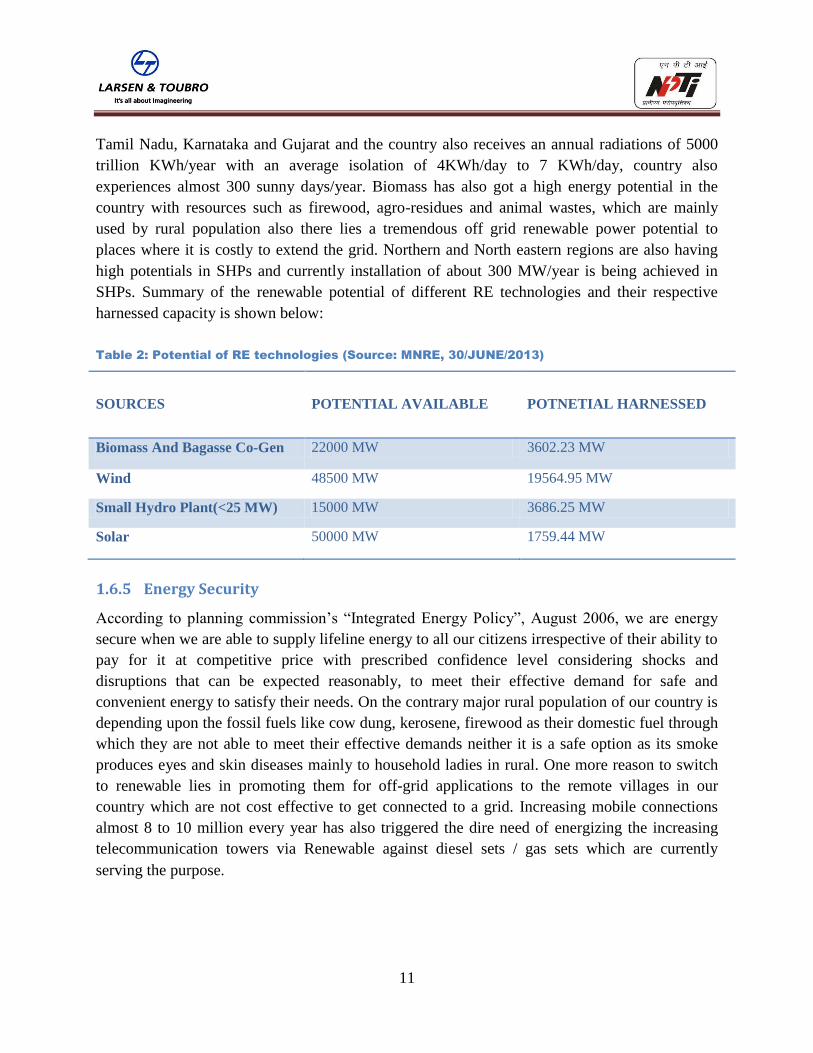

harnessed capacity is shown below:

Table 2: Potential of RE technologies (Source: MNRE, 30/JUNE/2013)

SOURCES POTENTIAL AVAILABLE POTNETIAL HARNESSED

Biomass And Bagasse Co-Gen 22000 MW 3602.23 MW

Wind 48500 MW 19564.95 MW

Small Hydro Plant(<25 MW) 15000 MW 3686.25 MW

Solar 50000 MW 1759.44 MW

1.6.5 Energy Security

According to planning commission’s “Integrated Energy Policy”, August 2006, we are energy

secure when we are able to supply lifeline energy to all our citizens irrespective of their ability to

pay for it at competitive price with prescribed confidence level considering shocks and

disruptions that can be expected reasonably, to meet their effective demand for safe and

convenient energy to satisfy their needs. On the contrary major rural population of our country is

depending upon the fossil fuels like cow dung, kerosene, firewood as their domestic fuel through

which they are not able to meet their effective demands neither it is a safe option as its smoke

produces eyes and skin diseases mainly to household ladies in rural. One more reason to switch

to renewable lies in promoting them for off-grid applications to the remote villages in our

country which are not cost effective to get connected to a grid. Increasing mobile connections

almost 8 to 10 million every year has also triggered the dire need of energizing the increasing

telecommunication towers via Renewable against diesel sets / gas sets which are currently

serving the purpose.

12

1.7 OBJECTIVE

The main objective of the project is to review and compare the mechanism of implementation of

Renewable Energy Certificate in India and suggesting L&T what are the changes that can be

encountered for sustainability of REC mechanism in India. The objective entails the following

points:

Study of REC Mechanism implementation in different countries

Need based analysis and cost benefit analysis

Study and compare the role of Renewable Obligation in various countries.

Study the various methods of REC implementation in various countries.

To explore India‘s REC market opportunities

Analyzing the future of RECs in various countries and factors that will replace REC

mechanism.

Recommendations and Conclusion

1.8 SCOPE OF WORK

Based on the study of Renewable Energy Certificate Mechanism implementation in various

countries it can be suggested that various ‘Technology Bands’ and ‘Certificate Multiplier

Scheme’ along with enforcement of the Renewable Purchase Obligation (RPO) can be

implemented in India too in coming years by Central Electricity Regulatory Commissions. REC

market in India is in its earlier stages so REC market opportunities can be more in future if some

changes like above suggested are notified in its regulatory framework.

The report provides the various suggestions for the L&T to frame its marketing strategy

accordingly and focus on ‘Off-Grid’ renewable solution as it will beneficial from RECs

prospective too.

1.9 ABOUT THE ORGANIZATION

LARSEN & TOUBRO LIMITED

Larsen & Toubro is a USD 14 billion technology, engineering, construction, manufacturing and

financial services conglomerate, with global operations. It is ranked 4thin the global list of Green

Companies in the industrial sector by the reputed international magazine Newsweek, and ranked

the world’s 9th Most Innovative Company by Forbes International. L&T is one of the largest and

most respected companies in India’s private sector. A strong, customer–focused approach and

the constant quest for top-class quality have enabled L&T to attain and sustain leadership in its

major lines of business over seven decades.

L&T Construction- Larsen & Toubro’s Construction Group

L&T Construction is India’s largest construction organization with over 70 years of experience

and expertise in the field. L&T Construction figures among the World’s top contractors and

13

ranks 35thamong top global contractors and ranks 60thamong international contractors as per the

survey conducted by Engineering News Record magazine, USA. To add to our credentials here,

L&T Construction is the 1stand the only Indian EPC among the top 100 in the above survey, to

be featured ahead of globally renowned contractors such as Technip, Samsung, Hyundai, Foster

Wheeler etc.

Many of the country’s prized landmarks – its exquisite buildings, tallest structures, largest

airports/ industrial projects, longest flyovers, highest via-ducts, longest pipelines including many

other benchmark projects have been built by L&T Construction. L&T Construction’s leading

edge capabilities cover every discipline of construction: civil, mechanical, electrical and

instrumentation engineering and these services are extended to all core sector industries and

infrastructure projects.

To specifically cite our landmarks in power plant construction, L&T has constructed many large

scale utility power plants with full compliance to international standards. L&T has a track record

of 50,000MW plant capacities being executed through 134 projects done globally. In

transmission line projects, L&T has executed 9,700 km national and 1200 odd km international

projects. L&T has also executed 218 air insulated and 36 gas insulated substations in the range of

33kV to 400kV globally.

These landmark projects testify that L&T Construction is equipped with the requisite expertise

and wide-ranging experience to undertake Engineering Procurement and Construction (EPC)

projects with single source responsibility. Contracts are executed using state of the art design

tools and project management techniques from concept to commissioning.

L&T Construction today is organized into six Independent Companies to allow for more in-depth

technology and business development as well as to improve focus on domestic and international

project execution. Each Independent Company is further split into different Business Units (BU)

to take care of the specific needs of various customers under each market segment.

L&T Construction, with its recent foray into turnkey EPC solutions under the Water & Renewable Energy

IC for the Solar Industry, is also making a strong statement about L&T’s commitment to the welfare of

the nature.L&T Construction is a brand of Larsen & Toubro Ltd.

The Independent Companies (ICs) are:

1. Water & Renewable Energy

2. Power Transmission & Distribution

3. Buildings & Factories

4. Infrastructure

5 .Metallurgical & Material Handling Projects

6. Transportation & Infrastructure

14

L&T Solar Business- Solar Business arm of Water & Renewable Energy Independent Company

L&T Solar Business within the Water & Renewable Energy IC belongs to the L&T

Conglomerate’s Construction arm; which designs, constructs and facilitate developers with

finances for Utility Scale Solar power plants in India and abroad including Photovoltaic and CSP

Technologies and also, EPC Solutions for Rooftop Solar Systems.

L&T Solar Business ranks 11thfor the year 2012 among Global Solar EPC Companies declared

by IMS Research. L&T Solar Business is the Only Indian Solar EPC figured among Top 15

Globally.

The Solar Business operates out of the L&T Construction group (erstwhile ECC) headquarters

located in the south of India at Chennai, Tamil Nadu. With its branch offices and project setups

operating across key solar intensive regions in India, it has more than 330 employees with further

planned expansion of manpower to cater the upcoming projects in pipelines.

L&T Solar Business is an Accredited MNRE Channel Partner and supports the customer for

obtaining MNRE subsidy for their solar systems. It has been awarded “SP 1A” grading by CARE

for Highest Performance Capability and High financial Strength.

Our strengths are solar PV power project design, fast and cost effective solar PV power plant

construction without compromising on quality, and our ability to bring in financial assistance for

developers of utility scale photovoltaic power plants in India. Thanks to the combination of our

many decades of power plant EPC experience in India, constant innovation/adaptation to new

ideas within the solar industry as well as our extensive networks with the financing communities,

given our conglomerate image, we are today emerging as one of the most reliable EPCs for

turnkey construction of Solar PV power plants in the country, we are someone trusted by various

government agencies, investors and well respected by both: the private & public sector

companies in India for pioneering work in the green energy area.

Over the past year, the annual growth of our turnkey Solar EPC business ranks well over the

industry average in India– we already commissioned 114 MWp of utility scale solar PV plants

across India (most of it in record time) in the FY12 and in FY13, we commissioned 41 MWp

solar PV power projects. Together totaling to 177MWp of solar PV power plants. In the CSP

segment, 125 MW Solar Thermal Power Plant is under construction, on commissioning this will

be the largest CSP plant in Asia.

Apart from our India focus, internationalizing our business activities is also on the anvil along

with our plan to build further plants in the country over the next few years; an expansion to

countries synergetic with L&T’s skill and expertise is also well planned.

15

2 LITERATURE REVIEW AND RESEARCH METHODOLOGY

LITERATURE REVIEW

2.1 National and International Experience with RECs

2.1.1 REC Implementation in Australia

The Government of Australia enacted The Renewable Energy (Electricity) Act 2000 for

the establishment and administration of a scheme to encourage additional electricity generation

from renewable energy sources. This is done through the issuing of certificates for the

generation of electricity using eligible renewable energy sources and requiring certain

purchasers (called liable entities) to surrender a specified number of certificates for the electricity

that they acquire during a year. Where a liable entity does not have enough certificates to

surrender, the liable entity will have to pay renewable energy shortfall charge. It was implemented

in the year 2001.

2.1.2 REC Implementation in United Kingdom

The tradable RE certificate in UK is called as Renewable Obligation Certificate (ROC).The

“Renewable Obligation (RO)” implemented in UK in April, 2002 in UK, and the “Renewable

Obligation Scotland” and the “Northern Ireland Renewable Obligation” are designed to incentivize

renewable generation into the electricity generation market. These schemes were introduced by the

Department of Trade and Industry, the Scottish Executive and the Department of Enterprise, Trade

and Investment respectively and are administered by the Gas and Electricity Markets Authority of

Great Britain. In UK, Renewable Obligation (RO) was introduced through Renewable Obligation

Order (ROO) in April 2002 and was enforced under the terms of Section 32 of the Electricity Act,

1989. RO has been made the main support scheme for renewable electricity in the UK. Through

ROO 2002, the targets for RO were defined for period up-to March 31, 2011. However, during the

review of RO in 2009 target for FY 2020 was revised to 15 % and the ROC mechanism was

extended to year 2037 from earlier 2027.

2.1.3 REC Implementation in USA

In USA, 29 states plus the districts of Columbia have adopted RPS with varying target values,

ranging from 1% to 30% within an implementation schedule varying from 5 to 25 years.

Eligible renewable resources also vary from state to state. Texas was the first state to

implement a renewable energy certificates trading program. Amongst several RPS systems

that allow REC trading, Texas’s RES system has often been referred to as well design RPS

system. It was implemented in January 2002. There are two categories of certificates in the Texas

REC Program: Renewable Energy Credits (RECs) and REC Offsets.

16

2.1.4 REC Implementation in India

2.1.4.1 The Electricity Act, 2003

An Act to consolidate the laws relating to generation, transmission, distribution, trading and use

of electricity and generally for taking measures conducive to development of electricity

industry, promoting competition therein, protecting interest of consumers and supply of

electricity to all areas, rationalization of electricity tariff, ensuring transparent policies

regarding subsidies, promotion of efficient and environmentally benign policies, constitution

of CEA, Regulatory Commissions and establishment of Appellate Tribunal and for matters

connected therewith or incidental thereto.

Further, the Electricity Act, 2003 entrusts on the appropriate Commission the responsibility of

promotion of co-generation and generation based on renewable energy sources. The policy

framework of the GOI also stresses on the encouragement of renewable energy sources keeping in

view the need for energy security of the country. Relevant provisions of the Act are reproduced as

below:

Section 86(1)(e): The State Commission shall promote cogeneration and generation of electricity

from renewable sources of energy by providing suitable measures for connectivity with the grid and

sale of electricity to any person, and also specify, for purchase of electricity from such sources, a

percentage of the total consumption of electricity in the area of a distribution licensee.

Section 61(h): The Appropriate Commission shall, subject to the provisions of the Act, specify the

terms and conditions for the determination of tariff, and in doing so, shall be guided by the

promotion of co-generation and generation of electricity from renewable sources of energy.

Section 86(1)(b): The SERCs shall discharge the function to regulate electricity purchase and

procurement process of distribution licensees including the price at which electricity shall be

procured from the generating companies or licensees or from other sources through agreements

for purchase of power for distribution and supply within the State.

Section 3(1): The Central Government shall, from time to time, prepare the National

Electricity Policy and tariff policy, in consultation with the State Governments and the

Authority for development of the power systems based on optimal utilization of resources such

as coal, natural gas, nuclear substances or materials, hydro and renewable sources of energy.

Section 3(3): The Central government may, from time to time in consultation with the

State governments, and the Authority review or revise, the National Electricity Policy and tariff

policy referred to in section 3(1).

Section 79(k): CERC shall discharge the functions assigned under the Act.

17

Section 66: The Appropriate Commission shall endeavor to promote the development of a market

(including trading) in power in such manner as may be specified and shall be guided by the

National Electricity Policy referred in Section 3 in this regard.

2.1.4.2 National Electricity Policy, 2005

National Electricity Policy was notified by Central Government in February 2005 as per provisions

of Section 3 of EA 2003. The Clause 5.12 of NEP outlines several conditions in respect of

promotion and harnessing of renewable energy sources. The salient features of the said provisions

of NEP are as follows.

• Non-conventional sources of energy being the most environment friendly there is an urgent need

to promote generation of electricity based on such sources of energy. For this purpose, efforts need

to be made to reduce the capital cost of projects based on non-conventional and renewable sources

of energy. Cost of energy can also be reduced by promoting competition within such projects. At

the same time, adequate promotional measures would also have to be taken for development of

technologies and a sustained growth of these sources.

• The Electricity Act 2003 provides that co-generation and generation of electricity from non-

conventional sources would be promoted by the SERCs by providing suitable measures for

connectivity with grid and sale of electricity to any person and also by specifying, for purchase of

electricity from such sources, a percentage of the total consumption of electricity in the area of a

distribution licensee. Such percentage for purchase of power from non-conventional sources should

be made applicable for the tariffs to be determined by the SERCs at the earliest. Progressively the

share of electricity from non-conventional sources would need to be increased as prescribed by

SERCs. Such purchase by distribution companies shall be through competitive bidding process.

Considering the fact that it will take some time before non-conventional technologies compete,

in terms of cost, with conventional sources, the Commission may determine an appropriate

differential in prices to promote these technologies.

• Industries in which both process heat and electricity are needed are well suited for cogeneration of

electricity. A significant potential for cogeneration exists in the country, particularly in the sugar

industry. SERCs may promote arrangements between the co-generator and the concerned

distribution licensee for purchase of surplus power from such plants. Cogeneration system also

needs to be encouraged in the overall interest of energy efficiency and also grid stability."

2.1.4.3 Tariff Policy, 2006

National Electricity Policy was notified by Central Government during January 2006 as per

provisions of Section 3 of EA 2003. Tariff Policy (TP) has further elaborated the role of regulatory

commissions, mechanism for promoting harnessing of renewable energy and timeframe for

18

implementation etc. The Clause 4 of the TP addresses various aspects associated with promotion

and harnessing of renewable energy sources. The salient features of the said provisions of TP are as

under:

• Pursuant to provisions of section 86(1)(e) of the Act, the Appropriate Commission shall fix a

minimum percentage for purchase of energy from such sources taking into account availability of

such resources in the region and its impact on retail tariffs. Such percentage for purchase of energy

should be made applicable for the tariffs to be determined by the SERCs latest by April 1, 2006.

It will take some time before non-conventional technologies can compete with conventional

sources in terms of cost of electricity. Therefore, procurement by distribution companies shall be

done at preferential tariffs determined by the Appropriate Commission.

• Such procurement by Distribution Licensees for future requirements shall be done, as far as

possible, through competitive bidding process under Section 63 of the Act within suppliers offering

energy from same type of nonconventional sources. In the long-term, these technologies would

need to compete with other sources in terms of full costs.

• The Central Commission should lay down guidelines within three months for pricing non-firm

power, especially from non-conventional sources, to be followed in cases where such

procurement is not through competitive bidding.

2.1.4.4 Rural Electricity Policy, 2006

Rural Electricity Policy also envisaged the need for non-conventional sources of energy with

the provision of institutional arrangements and technical support by the State Governments in

order to achieve cost effective and sustainable energy. The salient features of the Clause 3.3 and

Clause 8.9 of REP are as under:

Non-conventional sources of energy could be utilized even where grid connectivity exists provided

it is found to be cost effective.

• Institutional arrangements for back-up services and technical support to systems based on

nonconventional sources of energy will have to be created by the State Governments. Such

services would be provided on cost basis so as to make the arrangements sustainable.

2.1.4.5 National Action Plan for Climate Change, 2008

On June 30, 2008 Hon„ Prime Minister of India announced National Action Plan for Climate

Change(NAPCC) which delineated India’s strategy to tackle menace of global warming without

jeopardizing prospects of economic growth. The Technical Document annexed to NAPCC

includes following provisions for mainstreaming the RE based resources in India’s power

sector. In particular the document solicits use of REC mechanism. The provisions listed under

section 4.2.2 of NAPCC on Grid Connected Systems, are as follows:

19

• Dynamic Minimum Renewable Purchase Standard (DMRPS) may be set, with escalation each

year till a pre-defined level is reached, at which time the requirements may be revisited. It is

suggested that starting 2009-10, the national renewable standard (excluding hydropower with

storage capacity in excess of daily peaking capacity, or based on agriculture based renewable

sources that are used for human food) may be set at 5% of total grids purchase, to increase by 1%

each year for 10 years, SERCs may set higher percentages than this minimum at each point in

time.

• Central and State Governments may set up a verification mechanism to ensure that the

renewable based power is actually procured as per the applicable standard (DMRPS or SERC

specified). Appropriate authorities may also issue certificates that procure renewable based

power in excess of the national standard. Such certificates may be tradable, to enable utilities falling

short to meet their renewable standard obligations. In the event of some utilities still falling short,

penalties as may be allowed under the Electricity Act 2003 and rules there under may be

considered.

• Procurement of renewable based power by the State Electricity Boards/other power utilities

should, in so far as the applicable renewable standard (DMRPS or SERC specified) is concerned,

be based on competitive bidding, without regard to scheduling, or the tariffs of conventional power

(however determined).

• Renewable based power may, over and above the applicable renewable standards, be enabled to

compete with conventional generation on equal basis (whether bid tariffs or cost-plus tariffs),

without regard to scheduling (i.e.) renewable based power supply above the renewable standard

should be considered as displacing the marginal conventional peaking capacity). All else being

equal, in such cases, the renewable based power should be preferred to the competing conventional

power.

2.1.4.6 Forum of Regulators Recommendations

Forum of Regulators (FOR) established under Section 166 of the Electricity Act is an association of

Chairpersons of all electricity regulators. Chairperson of the Central Electricity Regulatory

Commission is ex-officio Chairperson of the FOR. The primary responsibility of the FOR is to

harmonize the regulatory policies in the country. The FOR has established various Working Groups

to look into different aspects of the electricity sector. The FOR has published a report Policies on

Renewables in 2008, with the objective of evolving a common approach for the promotion of RES

in the country. The report recommends that each State Commission may specify a minimum RPO

in line with the NAPCC and emphasizes to develop REC mechanism for achieving RPO targets.

FOR came out with Model Regulations on Renewable Purchase Obligation and its compliance

for SERCs in October, 2009 to evolve a framework for implementation of REC mechanism

20

which necessitated both Central Commission and State Commissions to frame suitable

regulations for giving effect to the REC framework. The framework of REC is expected to give

push to renewable energy capacity addition in the country. Some suggested outlines are:

• Need for inter-State exchange of RE power. Inter-State exchange of RE power is desirable from

National perspective and the same should be promoted.

• Mechanism for appropriate treatment for inter-State RE exchange through Regional Energy

Account needs to be developed.

2.1.4.7 CERC Guidelines, 2010

In exercise of the mandate in section 66 of the Act, the Central Commission has notified CERC

(Terms and Conditions for recognition and issuance of REC for RE Generation) Regulations, 2010

to facilitate development of renewable energy market at national level. The salient features of the

CERC guidelines are:

• CERC to designate any agency as Central Agency. Functions of Central agency shall include

registration, maintaining account, repository settlement and such other functions as designated by

CERC. Detailed procedures, bye laws to be prepared by Central Agency and shall be approved by

CERC.

• Power exchanges approved by CERC shall be eligible exchange platforms for REC exchange.

Fees and charges payable under this mechanism shall be specified by CERC.

• Two categories of certificates one for electricity generation from solar technologies called solar

certificates and another for electricity from other renewable energy technologies called non-solar

certificates. Both these certificates are mutually exclusive and cannot be exchanged. The

certificates will be valid for 365 days after issuance. CERC determine forbearance price and floor

price within which REC can be exchanged.

2.1.4.8 Provision for Compliance Auditing

Under Section 4.5 of order (Notice no. L-1/12/2010-CERC) “Detailed Procedure for Issuance of

Renewable Energy Certificate to the Eligible Entity by Central Agency” CAs have to monitor the

compliance of duties and obligation as specified by CERC by undertaking detailed

investigation/audit and submit the report on revocation of Registration of the Eligible Entity, if

necessary, to the Central Agency/Central Commission. Remuneration charges payable to

such auditors shall be met by Central Agency.

21

2.2 RESEARCH METHODOLOGY

With the broad objective of meeting the NAPCC target of 15% RE by 2020, MNRE projection

of renewable capacity addition in the 12th five year plan were considered keeping in mind the

availability and commercial potential of each RE resource in India. Secondary data about state

level future RE capacity addition, state wise RPO targets, energy requirement & availability status

of various states etc. has been collected from various sources. The historical annual energy

scenario over the past decade, as well as in the recent past, has also been studied before

projecting future demand. The analysis of statement of reason of RECs –II amendment sent to

CERC by L&T is done by going through various regulatory drafts and various concerned reports.

The study of regulatory support for renewable energy generation by mandating renewable

obligation fulfillment and various renewable obligation certificates of three countries has been done

by going through various regulatory drafts and various concerned reports of respective countries.

Energy requirement & RE Potential from auhentic sources are taken.

REC Mechanism in India (Collection of regulatory Information ,policy framework,etc)

International market of UK & Australia are covered & various operating & regulatory issues

were analysed

Various statements of reason sent by L&T to CERC for 2nd amendement were analysed

Analysis and Conclusion

22

3 REGULATORY FRAMEWORK FOR REDEPLOYMENT

3.1 Feed in Tariffs (FIT)

Under section 61(h) EA2003 empowered the CERC to specify terms and conditions for the tariff

determination for promotion of co-generation of electricity from renewable sources of energy

and section 86(1) (b) empowered the SERCs to regulate electricity purchase and procurement

process of Discoms including the price at which electricity is procured. Tariff policy notified by

central government has a clause 4 saying non-conventional sources of electricity will take time to

compete with conventional sources of electricity and so procurement by distribution companies

should be done on the basis of preferential tariff which should be set by SERCs latest by 1st April

2006, it also mandated the CERC to lay down guidelines for preferential tariff of non-firm power

within 3 months of TP notification. FIT is a preferential tariff set by different SERCs based on

the guidelines of CERC in their respective states for encouraging the developers to participate in

developing Renewable based generation power plants. FIT helps the developers to recover their

investments in RE technologies at a fast pace and hence reducing the burden of heavy debt

interests on developers. Table 3 shows the preferential tariffs for different renewable

technologies by SERCs.

Table 3: Preferential Tariff

STATE

BIOMASS BAGASSE MUNICIPAL

WASTE

SHP

(upto1MW,1MW

-5MW,

5MW-25MW)

SOLAR

PV

WIND(ZONE:

1,2,3,4)

ANDHRA

PRADESH - - - - 17.91 3.50

ASSAM 4 3.28 - 2.03 11 -

BIHAR 3.33 3.20 4.40 3.20 17.91 -

CHATTIS

-GARH 4 3.51 - - 15.5 -

GUJRAT 4.40 4.55 - - 15 3.56

HARYANA 5.26 - 3.67 15.96 13.77

HIMACHA

L PRADESH - - - 2.87 14,87 -

23

3.2 RENEWABLE PURCHASE OBLIGATIONS (RPO)

Under Section 86 (1) (e) of the EA2003, State commission are empowered to promote

cogeneration and generation of electricity from renewable sources of energy for connectivity

with the grid and specifying a certain percentage of the total consumption of electricity from

such sources. Following this most of the SERCs have issued Orders/Regulations specifying such

percentages. This percentage is referred to as “Renewable Purchase Obligation (RPO)”. These

orders will mandate the Discoms and other obligated entities in the order to buy a minimum

percentage of power from the renewable energy sources. CERC have taken out guidelines for

RPO obligations but the each of the state’s RPO obligation order differs from each other. If the

obligated entity fails to fulfill its RPO obligations it will be directed by the respective SERC to

deposit a certain amount in to a separate fund which will be further used in promoting the

Renewable. Table 4 shows the various states RPOs as per their respective latest orders.

RPOs are enforced on three categories of power consumers:

a) Distribution licensees

b) Open Access consumers

c) Captive consumers of electricity generated from conventional sources of energy.

They can meet this RPO obligation by:

1. Purchasing the required quantity of solar power directly from producers at Preferential Tariff.

2. Buying Renewable Energy Certificates (RECs)6 from Power Exchange.

3. Self or Captive Generation of Renewable Energy.

No RPO is fulfilled by:

1) Discom’s purchasing power at APPC.

2) Purchase of power at mutually agreed price at Power Exchanges by captive consumers and

open access consumers.

The obligations are driven by the National Action Plan on Climate Change (NAPCC) that aims

at 15% renewable energy in the overall energy mix of India by 2020.

There are two categories of RPOs:

i) Solar RPO (Solar Purchase Obligation i.e. SPO)

ii) Non-Solar RPO

6 Discussed in Section 3.3

24

States in India are free to set their own RPOs in line with the recommendations from their State