trx investor presentation - iis windows...

TRANSCRIPT

TRX Investor PresentationSunTrust Robinson Humphrey Business Services Conference

November 8, 2005

Safe Harbor

Certain statements in this presentation may constitute “forward-looking” statements as defined in Section 27A of the Securities Act of 1933 (the “Securities Act”), Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”), or in releases made by the Securities and Exchange Commission, all as may be amended from time to time.

Statements contained in this presentation that are not historical facts may be forward-looking statements within the meaning of the PSLRA. Any such forward-looking statements reflect our beliefs and assumptions and are based on information currently available to us and are subject to risks and uncertainties that could cause actual results to differ materially, including but not limited to, the loss of key clients, volatility in the number of transactions we service, failure or interruptions of our software, hardware and other systems, industry declines, competitive pressures and other risks.

Forward-looking statements are predictions and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise. These cautionary statements are being made pursuant to the Securities Act, the Exchange Act and the PSLRA with the intention of obtaining the benefits of the “safe harbor” provisions of such laws. TRX, Inc. cautions investors that any forward-looking statements we make are not guarantees or indicative of future performance.

TRX Business Model: Transaction Processing & Data Integration

World’s largest transaction markets – travel and financial services

Rapid and fundamental market changes working in our favor

Significant transaction volume and scale for multiple clients

1

Multiple touches with TRX hosted technology solutions

TRX Investment Highlights: Powering Travel Distribution Transformation

Leading market position in transaction processing and data integration

Established relationships with global travel industry leaders

Independent, objective and unbiased technology provider

Core end-to-end travel processing infrastructure

Strong financial model with revenue and margin growth opportunity

Disciplined management team

2

Source: TRX Estimates

Global Growth of 4% CAGR

US $200 Billion

Rest of the World$615 Billion

2004 Global Gross Travel Sales

Source: PhoCusWright

Total U.S. Travel and Online PenetrationIn Billions

Online Growth Driving Change

75%

25%

2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6

Total TravelOnline Penetration

$186.0 $189.8$195.4

$203.6$213.8

23%31%

39%

48%54%

2002 2003 2004 2005 20062 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6

Total TravelOnline Penetration

$186.0 $189.8$195.4

$203.6$213.8

23%31%

39%

48%54%

2002 2003 2004 2005 20062 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6

Total TravelOnline Penetration

$186.0 $189.8$195.4

$203.6$213.8

23%31%

39%

48%54%

2002 2003 2004 2005 2006

Travel: Growing, Massive Industry & Largest eCommerce Category

3

% o

f Mar

ket

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2001 2002 2003 2004 2005 2006

29%

CAGR

11%

5%

(16)%

% o

f Mar

ket

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2001 2002 2003 2004 2005 2006

29%

CAGR

11%

5%

(16)%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2001 2002 2003 2004 2005 2006

29%

CAGR

11%

5%

(16)%

Trends Favor Low-Cost Providers

Declining Agency Commissions

Declining Average Air Fares

Source: Airlines Reporting Corporation, TRX

Dramatic Concentration

Source: Runzheimer International

Travel: Concentrating Distribution & Changing Economics

Source: TRX Estimates Based on PhoCusWright and Forrester Research

Travel Segments - CAGR (2001-2006)

Top 15 Sellers of Travel2001 = 50%2006 = 75%

$400

$420

$440

$460

$480

$500

2001 2002 2003 2004 2005

$500

$458$448

$440

$411

Q1$400

$420

$440

$460

$480

$500

2001 2002 2003 2004 2005

$500

$458$448

$440

$411

Q1

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002+

10.1%9.1% 8.7%

8.0%

6.8%5.8%

4.0% 3.5%

0.0%0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002+

10.1%9.1% 8.7%

8.0%

6.8%5.8%

4.0% 3.5%

0.0%

Online Agencies

Suppliers

Large Agencies

Other Agencies

4

CFO Mandates & Growth of Credit Card Usage

Changing Procurement of T&E

Source: “Expense Management: Driving Savings Through Better Information and Spending Policies,” American Express, 2005

“59% of CFOs report their companies use a

corporate card system, but many want more readily

available and easily accessedspending data…”

Source: The Nilson Report, December 2004

Growth of Electronic Payment

US Payment Transactions (1998-2008)

1 9 9 8 2 0 0 3 2 0 0 8

Electronic& Card

Check& Cash

24% 50%36%

1 9 9 8 2 0 0 3 2 0 0 8

Electronic& Card

Check& Cash

1 9 9 8 2 0 0 3 2 0 0 8

Electronic& Card

Check& Cash

24% 50%36%

5

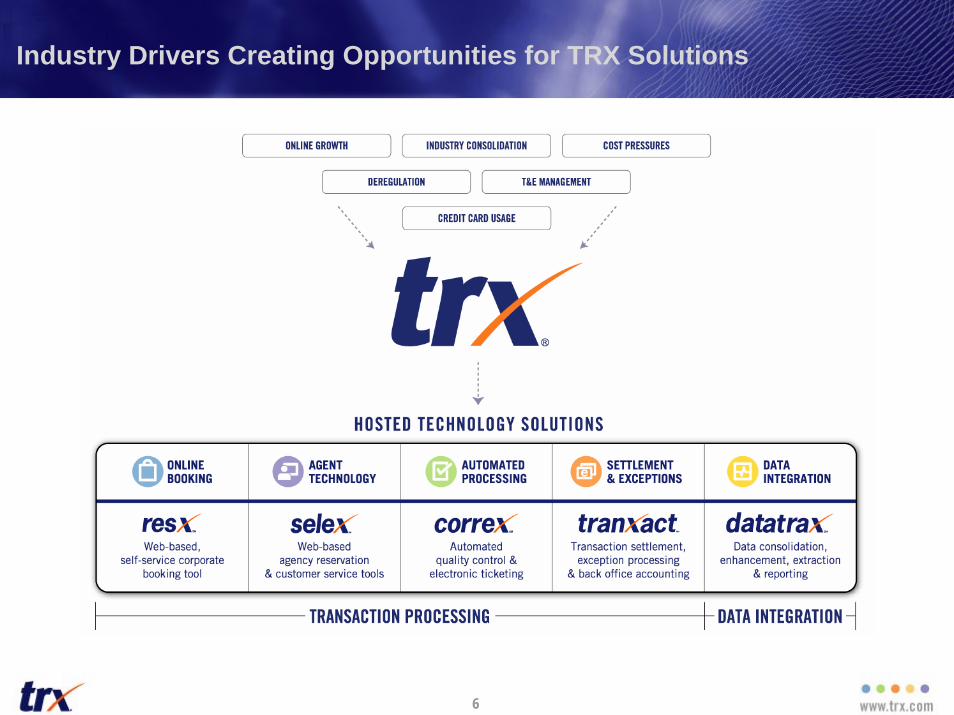

Industry Drivers Creating Opportunities for TRX Solutions

6

Covering the Transaction Lifecycle

Refunds, Voids, & Exchanges Paper Tickets Settlement

Global Data Feeds Normalization Enhancement Actionable Information

Reservation Improvement & Auto-Ticketing

Self-Service

Agent-Assisted Workflow Management Ticket Tracking Audit & Research

7

Automation & Process Re-Engineering Reduce Costs

Labor

Downtime

Processing

Errors

Training

$$$$

Development

Processing Infrastructure

Redundancy

Data Security

$

Traditional Agency Processing & Ticketing Model vs. TRX Model

12-24 months

8

85% Cost Reduction

Powering Travel Distribution Transformation & Global Market Leaders

9

Competitive Advantages

Switching Costs

Transaction Scale

Strategic Relationships

Industry Expertise

10

Disciplined Strategy with Multiple Sources of Growth

Capitalize on the migration to online travel

Grow revenues from traditional travel agencies

Continue to enhance our technology offerings

Expand use of our data integration capabilities

Pursue strategic relationships and acquisition opportunities

11

Management Team with Experience & Discipline

Shane HammondExecutive Vice President, Sales & Client Services,

North America

Peter GroverExecutive Vice President, Sales & Client Services,

Europe

Charlie CrissmanExecutive Vice President,

StrategicPlanning

David CathcartVice President,

Finance &Controller

Helen PorterVice President,

Solutions Management & Application Development

Tim SevertExecutive

Vice President,Administration

Vic PynnChief

OperatingOfficer

Lindsey SykesChief

Financial Officer

12

2005 Revenue Sources

Growth with Expanding Margins

Transaction-Based Revenue Model

4%Project

95%Transaction

1%Implementation

& Other

Strong Financial Model

• Attractive growth rates

• Improving revenue mix

• Cost structure leverage

• Shared scale

• Strong cash generation

13

2000 2001 2002 2003 2004

Rapid Growth in Core Service Offerings

58% CAGR

(15)% U.S. CAGR

Transaction Processing Revenue Data Integration Revenue

Customer Care Revenue

US

Europe

In Millions

In Millions

(1) CAGR excludes impact of 2004 European joint ventures acquisitions.

26% CAGR

US

Europe

In Millions

(1)

2000 2001 2002 2003 2004

2000 2001 2002 2003 2004

2000 2001 2002 2003 2004$0 -

$2 -

$4 -

$6 -

$8 -

$10 -

$12 -

$0

$5

$10

$15

$20

$25

$30

$35

$0 -

$10 -

$20 -

$30 -

$40 -

$50 -

$60 -

$70 -

14

Revenue Mix

2000

TransactionProcessing (63%)

CustomerCare (24%)

DataIntegration (13%)

2001 2002 2003 2004 2005YTD

100%

80%

60%

40%

20%

0%

Adjusted EBITDA excl. non-cash stock comp

Summary Financial Performance

2005 YTD

Adjusted EBITDAAdd: Non-cash stock compensation

($ in millions)2002 2003 2004 '02 - '04 CAGR

Revenue (1)

Transaction Processing $40.1 $49.1 $66.4 $55.7 28.7%Data Integration 3.2 6.0 10.5 11.9 82.5Customer Care 22.0 17.7 32.5 21.7 21.4

Total Revenue 65.3 72.8 109.4 89.3 29.5

Recurring Cash ExpensesOperating 41.3 43.7 73.2 57.2 33.2Selling, General & Administrative 16.2 16.0 19.9 14.7 11.5Technology Development 5.1 6.4 13.5 8.9 63.2

Total Recurring Cash Expenses 62.5 66.1 106.6 80.8 30.81.9 5.7 2.8 8.5

Operating Income (EBIT) (5.2) (1.6) (7.1) 0.6Net Income ($9.4) ($4.4) ($11.2) ($7.0)

(1) Excludes client reimbursements(2) Excludes IPO incentive payments of $0.5 million in 2005(3) Excludes non-recurring IPO and restructuring costs

3.9% 8.8% 2.9% 9.6%Margin

0.7 0.7 0.4 0.12.6 6.4 3.2 8.6

Other DataCash provided by operations $5.4 $13.1 $2.6 $6.5Capital expenditures 4.9 7.5 9.4 6.7

(2)

(3)

15

Proven Operating Leverage

2000 2001 2002 2003 2004 2005YTD

0%

20%

40%

60%

80%

Margin Expansion Scaleable Cost Structure

Expenses

Customer Care Mix

Adjusted EBITDA (Excludes non-cash stock compensation)

(1) Includes equity method losses 2000-2003

(2) Excludes non-cash stock compensation

59%

64%

72%

(1)Operating %

SG&A%

Tech Dev %

26%

21% 17%

10%11% 10%

(2)

16

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

(8%)

(2%)

4%

9%

3%

9%

2000 2001 2002 2003 2004 2005YTD

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

(8%)

(2%)

4%

9%

3%

9%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

(8%)

(2%)

4%

9%

3%

9%

2000 2001 2002 2003 2004 2005YTD

Cash and Cash Equivalents $29.7

($ in millions)September 30, 2005 September 30, 2005

Assets Liabilities

Current Assets Current LiabilitiesAccounts Payable and Accrued Liabilities $28.0

Trade Accounts Receivable, net 9.0 Customer Deposits and Deferred Revenue 13.8Prepaids and Other 2.3 Current Portion of Long-Term Debt 3.4

Total Current Assets 41.1 Total Current Liabilities 45.2

Property and Equipment 18.2 Long-Term Debt, less current portion 1.9

Other Noncurrent Assets

Convertible Notes 1.4

Goodwill 21.5Other Assets 0.6

Shareholders’ Equity

Total Noncurrent Assets 22.1

Common Stock & APIC 90.1Treasury Stock (2.3)Deferred Compensation (0.1)Cumulative Translation Adjustment 0.5Accumulated Deficit (56.1)

Total Stockholders’ Equity 32.2

Total Assets $81.4 Total Liabilities and Stockholders’ Equity $81.4

Clean Balance Sheet

Other long-term liabilities 0.7

17

6.7

Long-Term Growth Targets

CATEGORY FY 2004 2005 YTD TARGET

35%768350

3%

(7)%

(9)%

10%81

(16)7

9%

1%

(2)%

Revenue Growth (Y-o-Y)Transaction ProcessingData IntegrationCustomer Care

Total

20 – 25%25 – 35%

$10 – 20 million base20 – 30%

Adjusted EBITDA Margin 18 – 23%

Operating Income Margin 12 – 18%

Net Income Margin 7 – 11%

(1) Impacted by U.S. Airways termination in May 2004 and long-term extensions of European contracts.

(2) Excludes stock compensation associated with the adoption of SFAS 123R.

(3) Excludes non-recurring IPO and restructuring costs.

(2)

(1)

(3)

(3)

18

TRX Investment Highlights: Powering Travel Distribution Transformation

Leading market position in transaction processing and data integration

Established relationships with global travel industry leaders

Independent, objective and unbiased technology provider

Core end-to-end travel processing infrastructure

Strong financial model with revenue and margin growth opportunity

Disciplined management team

19