weatherford international ltd. - iis windows...

TRANSCRIPT

© 2009 Weatherford. All rights reserved.

Weatherford International Ltd.

Howard Weil 37th Annual Energy Conference

March 24, 2009

© 2009 Weatherford. All rights reserved. 2Full year 2008

Revenue $ 9,601

EBITDA $ 2,750

Operating Income $ 2,018

Income from Continuing Operations $ 1,399

Capital Expenditures $ 2,300

Vital Statistics

Financial Operational

Product Lines 10

Number of Countries 100+

Employees 49,600

% of Employees outside US 74%

Service Bases 809

Manufacturing Facilities 128

($ in millions)

© 2009 Weatherford. All rights reserved. 3

Revenue

International 54%

North America46%

Geographic Overview

Eastern Hemisphere 41%

Latin America 13%

Full year 2008

© 2009 Weatherford. All rights reserved. 4

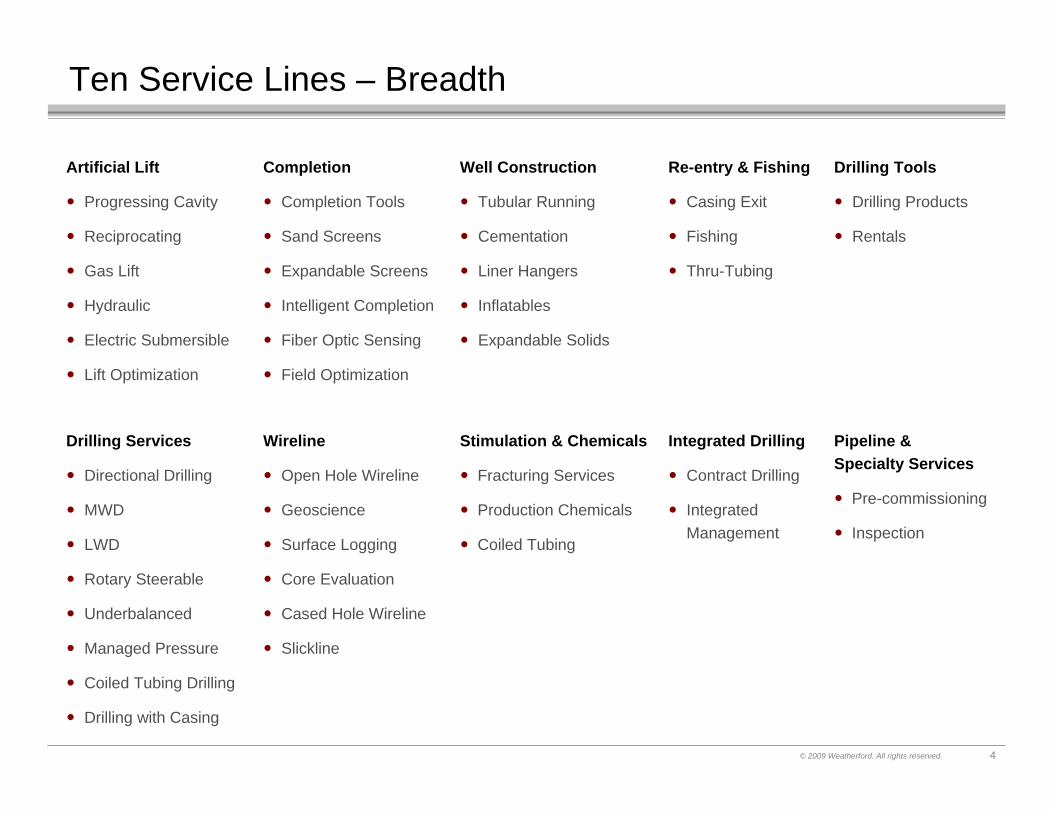

Drilling Services

Directional Drilling

MWD

LWD

Rotary Steerable

Underbalanced

Managed Pressure

Coiled Tubing Drilling

Drilling with Casing

Wireline

Open Hole Wireline

Geoscience

Surface Logging

Core Evaluation

Cased Hole Wireline

Slickline

Well Construction

Tubular Running

Cementation

Liner Hangers

Inflatables

Expandable Solids

Re-entry & Fishing

Casing Exit

Fishing

Thru-Tubing

Drilling Tools

Drilling Products

Rentals

Integrated Drilling

Contract Drilling

Integrated Management

Completion

Completion Tools

Sand Screens

Expandable Screens

Intelligent Completion

Fiber Optic Sensing

Field Optimization

Stimulation & Chemicals

Fracturing Services

Production Chemicals

Coiled Tubing

Pipeline & Specialty Services

Pre-commissioning

Inspection

Artificial Lift

Progressing Cavity

Reciprocating

Gas Lift

Hydraulic

Electric Submersible

Lift Optimization

Ten Service Lines – Breadth

© 2009 Weatherford. All rights reserved. 5Based on revenues for full year 2008

1. Artificial Lift 17%

2. Drilling Services 16%

3. Well Construction 15%

4. Drilling Tools 11%

5. Completion 10%

6. Wireline 8%

7. Re-Entry & Fishing 7%

8. Stimulation & Chemicals 7%

9. Integrated Drilling 6%

10. Pipeline & Specialty Services 3%

Ten Service Lines – Relative Size

© 2009 Weatherford. All rights reserved. 6

• Trailing Eight Quarters:

– 42% revenue growth 72% from international markets

– 30% EBIT growth all from international markets

($ in millions, except EPS)

Historical Operating Results

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08

Total Revenue 1,852 1,816 1,972 2,192 2,196 2,229 2,541 2,635

North America 1,006 883 995 1,053 1,090 1,012 1,180 1,178

Middle East/North Africa/Asia 395 435 456 538 522 556 638 676

Europe/West Africa/CIS 245 291 308 345 348 390 409 392

Latin America 206 207 213 256 236 271 314 389

Net Operating Income 420 341 423 471 490 433 548 547

North America 300 192 264 257 292 224 313 296

Middle East/North Africa/Asia 83 97 104 132 121 131 146 163

Europe/West Africa/CIS 56 70 78 90 93 99 102 89

Latin America 49 46 45 63 60 58 70 89

Research & Development (41) (41) (43) (44) (43) (44) (52) (54)

Corporate (27) (23) (25) (27) (33) (35) (31) (36)

Income from Continuing Operations 286 235 298 345 351 300 384 364

Diluted EPS from Continuing Operations 0.41 0.34 0.43 0.49 0.50 0.43 0.55 0.53

© 2009 Weatherford. All rights reserved. 7

Net Debt / Capitalization

~ 40%

Repurchased 35.3 million

SharesSince

March 2006

($ in millions)

Balance Sheet

Dec 07 Mar 08 Jun 08 Sep 08 Dec 08

Assets

Cash 171 626 268 337 234

Accounts Receivable 1,962 2,105 2,111 2,426 2,443

Inventories 1,608 1,768 1,909 2,022 2,088

Other Current Assets 731 602 639 722 700

Total Current Assets 4,472 5,101 4,927 5,507 5,465

Fixed Assets 4,154 4,583 4,980 5,515 5,924

Goodwill 3,358 3,455 3,511 3,813 3,534

Other Assets 1,207 1,345 1,379 1,364 1,509

Total Assets 13,191 14,484 14,797 16,199 16,432

Liabilities & Shareholders' Equity

Short-Term Debt 774 193 50 1,074 1,256

Other Current Liabilities 1,428 1,468 1,399 1,566 1,723

Long-Term Debt 3,066 4,564 4,540 4,544 4,564

Other Long-Term Liabilities 516 568 639 632 573

Shareholders' Equity 7,407 7,691 8,169 8,383 8,316

Total Liabilities/Shareholders' Equity 13,191 14,484 14,797 16,199 16,432

© 2009 Weatherford. All rights reserved. 8Based on revenues for full year 2008

Cash $ 234

Short-Term Debt, including Current Portion of Long-Term Debt $ 6

Long-Term Debt $ 5,814

Shareholder’s Equity $ 8,316

Net Debt/Net Capitalization 40.2%

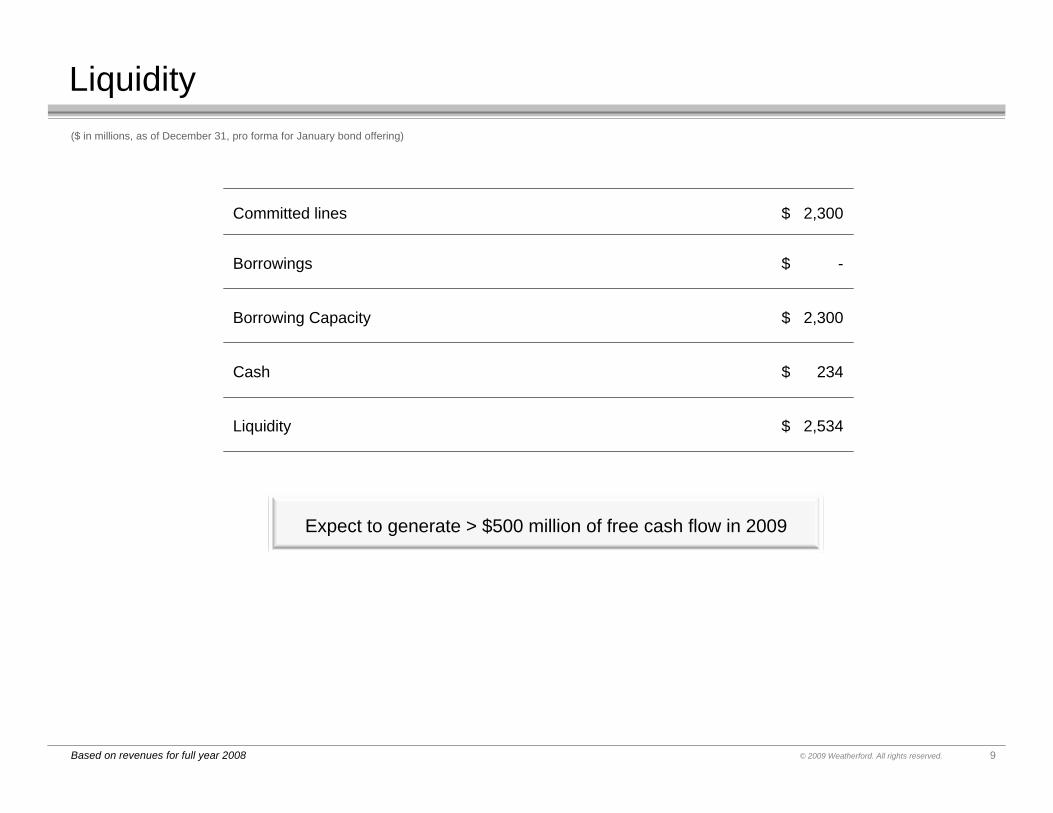

Capital Structure($ in millions, as of December 31, pro forma for January bond offering)

• Nearest dated maturity is $350 million due November 2011

• Average weighted maturity is over 13 years with ~ 30% in ~ 30 years

• Average weighted interest rate is 6.9%

© 2009 Weatherford. All rights reserved. 9Based on revenues for full year 2008

Committed lines $ 2,300

Borrowings $ -

Borrowing Capacity $ 2,300

Cash $ 234

Liquidity $ 2,534

Liquidity($ in millions, as of December 31, pro forma for January bond offering)

Expect to generate > $500 million of free cash flow in 2009

© 2009 Weatherford. All rights reserved. 10

Historical View

© 2009 Weatherford. All rights reserved. 11

Industry Expansion – Customer Spending

Source: Barclays Capital

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

North America International

1999 – 2008: International 12.9% CAGR2003 – 2008: International 13.3% CAGR1999 – 2008: International 12.9% CAGR2003 – 2008: International 13.3% CAGR

1999 – 2008: Overall 10.5% CAGR

2003 – 2008: Overall 11.2% CAGR

($ in

mill

ions

)

© 2009 Weatherford. All rights reserved. 12

Industry Expansion – Rig Count

Rig

Cou

nt Global 10% CAGR

1999 – 2008: International 8% CAGR2003 – 2008: International 9% CAGR1999 – 2008: International 8% CAGR2003 – 2008: International 9% CAGR

Global 10% CAGR

WFT International Rig CountWFT NAM Rig Count

© 2009 Weatherford. All rights reserved. 13

Weatherford Performance – Revenue

26% CAGR

30% CAGR

($ in

mill

ions

)

1999 – 2008: International 31% CAGR2003 – 2008: International 32% CAGR1999 – 2008: International 31% CAGR2003 – 2008: International 32% CAGR

WFT International RevenueWFT NAM Revenue

© 2009 Weatherford. All rights reserved. 14

Weatherford Performance – Revenue per Rig

Rev

enue

/Rig

($)

14% CAGR

19% C

AGR

1999 – 2008: International 21% CAGR2003 – 2008: International 22% CAGR1999 – 2008: International 21% CAGR2003 – 2008: International 22% CAGR

WFT NAM Revenue / Rig (millions)WFT International Revenue / Rig (millions)WFT Revenue / Rig (millions)

© 2009 Weatherford. All rights reserved. 15

Weatherford Performance – EBITDA

31% CAGR

38% CAGR

($ in

mill

ions

)

WFT EBITDA

© 2009 Weatherford. All rights reserved. 16

Weatherford Performance – EBIT

45% CAGR

48% CAGR

($ in

mill

ions

)

WFT EBIT

© 2009 Weatherford. All rights reserved.

Weatherford Investments in Expansion

17

1999 – 2008:

R&D Working Capital

Acquisitions Capex Total

2003 – 2008:

R&D Working Capital

Acquisitions Capex Total

($ in

mill

ions

)($

in m

illio

ns)

$17,089

$13,896

© 2009 Weatherford. All rights reserved. 18

Drilling Services

Directional Drilling

MWD

LWD

Rotary Steerable

Underbalanced

Managed Pressure

Coiled Tubing Drilling

Drilling with Casing

Wireline

Open Hole Wireline

Geoscience

Surface Logging

Core Evaluation

Cased Hole Wireline

Slickline

Well Construction

Tubular Running

Cementation

Liner Hangers

Inflatables

Expandable Solids

Re-entry & Fishing

Casing Exit

Fishing

Thru-Tubing

Drilling Tools

Drilling Products

Rentals

Integrated Drilling

Contract Drilling

Integrated Management

Completion

Completion Tools

Sand Screens

Expandable Screens

Intelligent Completion

Fiber Optic Sensing

Field Optimization

Stimulation & Chemicals

Fracturing Services

Production Chemicals

Coiled Tubing

Pipeline & Specialty Services

Pre-commissioning

Inspection

Artificial Lift

Progressing Cavity

Reciprocating

Gas Lift

Hydraulic

Electric Submersible

Lift Optimization

Ten Service Lines – Breadth

© 2009 Weatherford. All rights reserved. 19

North America50664

34%

Service LocationsManufacturing Facilitiesof Employees

Latin America108

718%

Service LocationsManufacturing Facilitiesof Employees

Asia5932

9%

Service LocationsManufacturing Facilitiesof Employees

Middle East/ North Africa554

20%

Service LocationsManufacturing Facilitiesof Employees

Europe / W Africa81 21

19%

Service LocationsManufacturing Facilitiesof Employees

International303 Service Locations64 Manufacturing Facilities

International303 Service Locations64 Manufacturing Facilities

Weatherford locationsRegional officesCorporate headquarters

Infrastructure

Additions 2008-200917 Service Locations3 R&D Facilities5 Training Facilities

Additions 2008-200917 Service Locations3 R&D Facilities5 Training Facilities

© 2009 Weatherford. All rights reserved. 20

Depth – Technology Additions

• Across all Product and Service Lines

• Examples shown from:

– MWD/LWD

– RSS

– Directional Motors

– Open-hole Wireline

– Cased-hole Wireline

• Examples focus on:

– Adding more sensing capabilities on “new” directional & wireline platforms

– Pushing the performance envelope

© 2009 Weatherford. All rights reserved. 21

MWD/LWD – Technology Developments

• 4 ¾” MFR-Ultra 80” – Q4 2007 (MENAP)

– Deep reading resistivity in geosteering applications

– 165°C

– 30,000 psi

• Azimuthal (“Focused”) MFR – Q4 2008 (US)

– Azimuthal resistivity used in geosteering applications

– 165°C

– 30,000 psi

• Resistivity Imaging Sensor – Q2 2009 (MENAP)

– Unique to Weatherford

– Electric imaging tool providing 3-D image of borehole

– Designed to work in water and oil based muds

– Competition’s tools only work in water based mud

• 6 ¾” SAGR – Q1 2008 (MENAP)

– Spectral, Azimuthal, Gamma Ray

– Unique to Weatherford

– Reads chemical content of shale formation

– Provides rock description

© 2009 Weatherford. All rights reserved. 22

MWD/LWD – Technology Developments

• New Generation Ranging Method – Q3 2009 (NAM)

– SAGD applications (steer well parallel to existing well)

– New generation ranging tool

– Key in heavy oil

– Improved accuracy

• Intelli-Pipe Interface – Q2 2008 (LAO)

– Continuous real-time communications

• GABIS II – At Bit Sensors – Q3 2008 (NAM)

– Gamma and inclination measurements below the mud motor (speed of sight)

– Key in unconventional resources (CBM)

• TVM – 3-axis vibration sensor – Q1 2008 (MENA / EWACIS)

– Drilling efficiency measurement

– Provides measurements ranging from 0 – 200 g’s and downhole RPM

© 2009 Weatherford. All rights reserved. 23

MWD/LWD – Technology Developments

• Pe (AZD) Evaluation – Q4 2007 (MENAP)

– Photo-electric measurement in density tool

– Log evaluation measurement

• Sonic – Q4 2008 (US / EH)

– Improved data correlation and measurement quality

• Formation Pressure Tester – Q2 2009

© 2009 Weatherford. All rights reserved. 24

• Automated Drilling Mode (“cruise control”) – Q3 2008

– Automatic maintenance of inclination and azimuth

• Integrated ERT motor power section – Q3 2008

– Runs rotary steerable with power section

• Vertical Drilling System – Q4 2007

– Standalone point the bit system (No MWD required) – Q1 2008

– Standalone push the bit system (No MWD required) – Q4 2008

• New (industry first) HPHT RSS System – (US / EH)

– 175°C and 30,000 psi

– Highest pressure and temperature ratings in industry

• Next generation rotary steerable system – 2009

RSS – Technology Developments

© 2009 Weatherford. All rights reserved. 25

RSS – Technology Developments

• Dual Pulser – Q3 2008 (US / MENAP)

– Can run two pulses in BHA; can run RSS & LWD pulsing; removes problem of hard wired motor

– To allow incorporation of a mud motor in the RSS BHA with full control

▪ Improved reliability vs. wired motor, EM short hop or acoustic

▪ Increased data rates

• Torque Mitigator – Q4 2008 (US / EH)

– Provides the ability to operate under extreme drilling conditions where stick slip is an issue

• EM HEL RSS underbalanced application – 2007 (Global)

– Unique to WFT

© 2009 Weatherford. All rights reserved. 26

Motor Technology Developments

• Mechanical Vertical Drilling Tool – Q4 2009 (NAM)

– Eliminates need for RSS

• Continuous Coil Tubing Orientator System – Q1 2009 (NAM)

– Provides a means of continuously orienting the bend in the motor to steer the well in 3 dimensions

• 11 ¼” Performance Motors – Q1 2008

– Significantly improved drilling performance

• 4 Degree Bent Housing Motor – Field Proven, Best in Class

– For short-radius directional work

• ERT Power Sections – Field Proven, Best in Class

– Improved rate of penetration

© 2009 Weatherford. All rights reserved. 27

• Compact Micro Imager – Q2 2008 (2.4” pads in Q1 2009)

– Real Time and Memory

– Acquires excellent formation images to be obtained in broad range of boreholes

• Oil Based Mud Imager – Q3 2008

– Real Time only

– Allows excellent formation images to be obtained in OBM wellbores

• Ultrasonic Micro Imager – Q2 2008

– Real Time only

– Provides another method for acquiring formation images

– Reduces drilling risk by providing geomechanical, wellbore stability and stress analysis

Open-Hole – Technology Developments

© 2009 Weatherford. All rights reserved. 28

• Array Induction – Advanced Formation Density – Q2 2009

– Real Time only

– Resistivity / Density / Neutron Platform for basic log evaluation

– Multiple depth of investigation, improved resolution with deeper reading for resistivity

• Reservoir Evaluation System (RES) – Q2 2009

– Real Time only

– Provides direct measurement of formation and fluid properties of the reservoir

– Improved accuracy of formation properties for permeability, fluid gradients

– Down-hole lab analysis for fluid properties evaluation (unique)

– Mini DST / Interference testing

• Compact Dipole Sonic – Q3 2009

– Real Time and Memory

– Complete geophysical, petrophysical, and mechanical properties evaluation service

Open-Hole – Technology Developments

© 2009 Weatherford. All rights reserved. 29

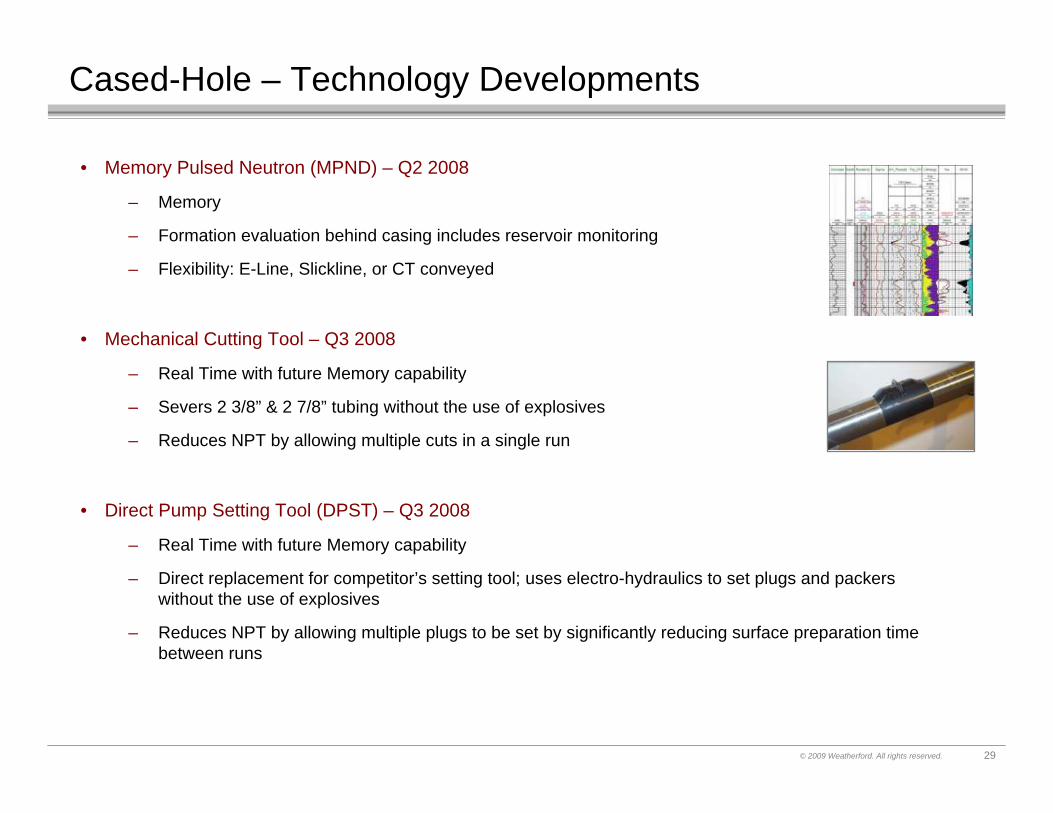

• Memory Pulsed Neutron (MPND) – Q2 2008

– Memory

– Formation evaluation behind casing includes reservoir monitoring

– Flexibility: E-Line, Slickline, or CT conveyed

• Mechanical Cutting Tool – Q3 2008

– Real Time with future Memory capability

– Severs 2 3/8” & 2 7/8” tubing without the use of explosives

– Reduces NPT by allowing multiple cuts in a single run

• Direct Pump Setting Tool (DPST) – Q3 2008

– Real Time with future Memory capability

– Direct replacement for competitor’s setting tool; uses electro-hydraulics to set plugs and packers without the use of explosives

– Reduces NPT by allowing multiple plugs to be set by significantly reducing surface preparation time between runs

Cased-Hole – Technology Developments

© 2009 Weatherford. All rights reserved. 30

• Mechanical Cutting Tool – Q1 2009

– Real Time with future Memory capability

– Severs 3 ½”, 4 ½” & 5 ½” tubing without the use of explosives

– Reduces NPT by allowing multiple cuts in a single run

– Reduces HSE risk by eliminating dangerous explosives and chemicals normally used to sever down hole tubulars

• Cased Reservoir Evaluation (CRE) – Q2 2009

– Real Time

– Advanced formation evaluation behind casing

– 5 detector configuration provides enhanced measurement for formation evaluation

– Water saturation analysis, C/O analysis, density analysis, sigma analysis

– Enhanced gas analysis for unconventional reservoirs

Cased-Hole – Technology Developments

© 2009 Weatherford. All rights reserved. 31

Forward View

© 2009 Weatherford. All rights reserved.

• Volatility

– Shale production

– Decline curves

– LNG deliveries

– Industrial demand

– Average rig count ~800 in U.S. and ~250 in Canada

• Efficiency

– $150 million reduction in fixed and variable costs

– Headcount

– Infrastructure

– Supply Chain

32

North America Outlook – Near-Term

© 2009 Weatherford. All rights reserved. 33

North America Outlook – Long-Term

• Secular forces in the market

– Shale

– Heavy Oil

– Deepwater

• Mid-single digit annual market growth

• Weatherford should grow above the market rate

– Young technologies

– Strong in shale (directional, evaluation, completion, stimulation)

– Strong in heavy oil (directional, completion, artificial lift)

– Strong in deepwater

▪ Legacy (tubular running, cementation, line hangers, fishing, proprietary drilling tools)

▪ Higher end technologies (directional, wireline, completion)

© 2009 Weatherford. All rights reserved.

• Severe Pullback

– North Sea

– Russia

– Central Europe

– Venezuela

– Argentina

• Weak Markets

– Saudi

– West Africa

– Asia Pacific

• Steady Markets

– Middle East ex Saudi

– North Africa

– Mexico

– Brazil

– China

34

International Outlook – Near-Term

© 2009 Weatherford. All rights reserved. 35

International Outlook – Long-Term

• Secular forces in the market

– Emergence of heavy oil

– Emergence of gas

– More challenging reservoirs

• Low double-digit annual market growth

• Weatherford should grow well above the market rate

– Required breadth, depth and reach

– Young technologies with immature global share (high local share)

– Strong in heavy oil (directional, completion, artificial lift)

© 2009 Weatherford. All rights reserved. 36

E&P Spending**WFT*

*Full year 2008

International – Most Growth Opportunities

North America46%

Latin America13%

Eastern Hemisphere41%

North America30%

Latin America12%

Eastern Hemisphere58%

* * Barclays Capital – 2008 Survey

© 2009 Weatherford. All rights reserved. 37

International Competitive Requirements

• Breadth = Client Relevance, Economies of Scale and Solutions

• Depth = Technology

• Infrastructure = Reach

© 2009 Weatherford. All rights reserved. 38

Implications for the Future

• Shift in geographic exposure

• Shift in product and service mix

• Margin and return expansion

© 2009 Weatherford. All rights reserved. 39

TargetedCurrent Revenue*

*Full year 2008

Geographic Shift

North America46%

Latin America13%

Eastern Hemisphere41%

North America25%

Latin America25%

Eastern Hemisphere50%

2008 2013

© 2009 Weatherford. All rights reserved. 40

Service Line Shift

• Artificial Lift

• Well Construction

• Drilling Services

• Drilling Tools

• Completion

• Wireline

• Re-Entry & Fishing

• Stimulation & Chemicals

• Integrated Drilling

• Pipeline & Specialty Services

• Drilling Services

• Well Construction

• Artificial Lift

• Completion

• Integrated Drilling

• Wireline

• Stimulation & Chemicals

• Re-Entry & Fishing

• Drilling Tools

• Pipeline & Specialty Services

20132007

© 2009 Weatherford. All rights reserved. 41

Margin and Return Expansion

• Technology intensity

• Economies of scale

• Efficiencies at delivery point

– Evaluation

– Drilling

– Intervention

– Production

• Best in class growth

© 2009 Weatherford. All rights reserved. 42

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 concerning, among other things, the prospects for Weatherford’s operations which are subject to certain risks, uncertainties andassumptions. These risks and uncertainties, which are more fully described in Weatherford International Ltd.’s reports and registration statements filed with the SEC, include the impact of oil and natural gas prices and worldwide economic conditions on drilling activity, the demand for and pricing of Weatherford's products and services and domestic and international economic and regulatory conditions. Should one or more of these risks or uncertainties materialize, or should the assumptions prove incorrect, actual results may vary in material aspects from those currently anticipated.