global vehicle remarketing 2002images.adesainc.com/publicweb/analytserv/gvr/2002/gvr_2002.pdfthe...

TRANSCRIPT

GLOBAL VEHICLE REMARKETING 2002U.S. & CANADIAN MARKETS

ADESA ANALYTICAL SERVICES

ADESA Corporation’s Chief Economist, Tom Kontos leads the company’s effort to provide value-added

analytical services to ADESA customers, the media, and the investment community. These services range

from ADESA’s award-winning publication series, Global Vehicle Remarketing to custom analysis of whole-

sale price trends for ADESA’s remarketing clients.

In January 2001, ADESA introduced Global Vehicle Remarketing: U.S. & Canadian Markets (GVR). As

shown in the opening section of that report, the U.S. and Canadian markets represent over one-third of the

world’s vehicle population. Coverage of the $78 billion vehicle remarketing industry in these two critical

markets, in which ADESA Corporation is a leading player, will continue on an annual basis in GVR.

In June 2001, ADESA introduced Pulse, which provides a quarterly review and outlook of economic

indicators pertinent to the industry. In addition to GVR and Pulse, ADESA Analytical Services plans

to periodically issue other reports in the Global Vehicle Remarketing series, on topics including:

• Vehicle remarketing in Europe and other world markets.

• Comprehensive coverage of ancillary remarketing services such as dealer financing, transportation and

marshalling, reconditioning and certification, repossession, title processing, vehicle importation, etc.

• The salvage market.

• The role of Internet technology in vehicle remarketing.

ADESA provides these valuable reports on a complimentary basis to its key clients and industry contacts.

For information concerning subscription to this report series, please call 317/249-4251, or visit our web

corner at www.adesa.com under “The Industry’s Pulse.”

Other Analytical Services available to ADESA clients include:

• Custom analysis of remarketing clients’ vehicle sales at auction.

• Presentations at client meetings.

• Production of auction dealer surveys and other targeted surveys.

To learn more about these services, please contact Tom Kontos, Vice President, Industry Relations

& Analytical Services, at 317/249-4235 or [email protected].

Welcome to the second edition of Global Vehicle Remarketing: U.S.& Canadian Markets (GVR). This annual

edition focuses on the United States and Canadian vehicle markets, where over one-third of the world’s

vehicles operate.

ADESA Corporation has a unique vantage point from which to explore this industry – both in terms

of the broad scope of the company’s remarketing services and its leading position in both the U.S. and

Canada. In the U.S., ADESA is the second largest and fastest growing vehicle auction provider, and

in Canada, the largest. ADESA is also the third largest provider of “total loss” vehicle recovery (salvage

auction) services in the two countries. The company is also allied with several other automotive services

affiliates of parent company, ALLETE, a uniquely diversified, publicly held corporation (see “About ADESA

Corporation and ALLETE Automotive Services” on page 65). These combined operations and capabilities

make ADESA the broadest-based vehicle remarketing services network in North America.

Since the inaugural edition of this report in January 2001, ADESA Analytical Services (described on the

inside front cover) has launched Global Vehicle Remarketing’s Pulse, a quarterly update of vehicle remar-

keting industry economic indicators. With the industry uncertainty caused by events following the horrors

of September 11, ADESA Analytical Services issued a “White Paper” on “The Impact of War and Recession

on Vehicle Remarketing” between the summer and winter editions of Pulse. Future reports in the Global

Vehicle Remarketing (GVR) series will continue to expand both the breadth and depth of coverage to

include key vehicle remarketing markets throughout the world and selected topics within specific market

segments. Look for this and other timely information relating to vehicle remarketing on ADESA’s

website (see link below).

We hope you will find new insights in this second edition, and we welcome your opinions and suggestions.

Tom Kontos

Vice President, Industry Relations

& Analytical Services

ADESA Corporation

January 2002

www.adesa.com/kontoskorner

PREFACE

Tom Kontos

TABLE OF CONTENTS

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Summary and Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

New and Used Vehicle Sales in the U.S. & Canada . . . . . . . . . . . . . . . .7

2001 at a Glance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

Historical Volume Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

Automotive Finance Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

Used Vehicle Sales Volume Projections . . . . . . . . . . . . . . . . . . . . . .17

The Vehicle Remarketing Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

Vehicle Remarketing Defined . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Vehicle Flows in the U.S. . . . . . . . . . . . . . . . . . . . . . . . . . . .26

The Vehicle Remarketing Value Chain . . . . . . . . . . . . . . . . .28

A Remarketer’s Checklist . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Vehicle Suppliers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

Automotive Finance Companies . . . . . . . . . . . . . . . . . . . . . .36

Rental Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38

Commercial Fleets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

Dealers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42

Auction Sales Volume Projections . . . . . . . . . . . . . . . . . . . . . . . . . .51

Wholesale Market Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .53

Analysis of AuctionNet Database . . . . . . . . . . . . . . . . . . . . . . . . . . .54

Analysis of ADESA Database . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60

Wholesale Market Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .62

About the Author . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64

About ADESA and ALLETE Automotive Services . . . . . . . . . . . . . . . .65

4

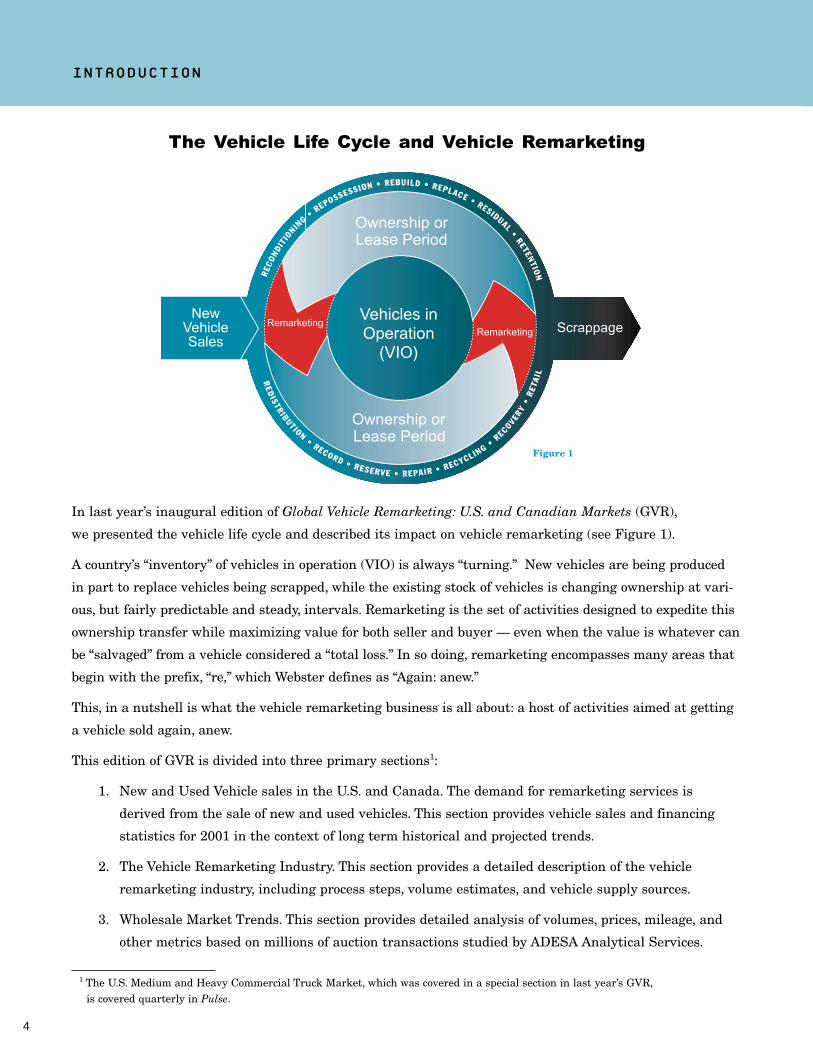

INTRODUCTION

New Vehicle Sales

Scrappage

Ownership or Lease Period

Ownership or Lease Period

RemarketingVehicles in Operation

(VIO)

The Vehicle Life Cycle and Vehicle Remarketing

Remarketing

REC

ONDI

TIONIN

G• REPOSSESSION • REBUILD • REPLACE • RESIDUAL

•RETEN

TION

RED

ISTR IBUT ION•

RECORD • RESERVE • REPAIR • RECYCLING•

RECOVERY

•R

ETA

IL

Figure 1

In last year’s inaugural edition of Global Vehicle Remarketing: U.S. and Canadian Markets (GVR),

we presented the vehicle life cycle and described its impact on vehicle remarketing (see Figure 1).

A country’s “inventory” of vehicles in operation (VIO) is always “turning.” New vehicles are being produced

in part to replace vehicles being scrapped, while the existing stock of vehicles is changing ownership at vari-

ous, but fairly predictable and steady, intervals. Remarketing is the set of activities designed to expedite this

ownership transfer while maximizing value for both seller and buyer — even when the value is whatever can

be “salvaged” from a vehicle considered a “total loss.” In so doing, remarketing encompasses many areas that

begin with the prefix, “re,” which Webster defines as “Again: anew.”

This, in a nutshell is what the vehicle remarketing business is all about: a host of activities aimed at getting

a vehicle sold again, anew.

This edition of GVR is divided into three primary sections1:

1. New and Used Vehicle sales in the U.S. and Canada. The demand for remarketing services is

derived from the sale of new and used vehicles. This section provides vehicle sales and financing

statistics for 2001 in the context of long term historical and projected trends.

2. The Vehicle Remarketing Industry. This section provides a detailed description of the vehicle

remarketing industry, including process steps, volume estimates, and vehicle supply sources.

3. Wholesale Market Trends. This section provides detailed analysis of volumes, prices, mileage, and

other metrics based on millions of auction transactions studied by ADESA Analytical Services.

1 The U.S. Medium and Heavy Commercial Truck Market, which was covered in a special section in last year’s GVR,is covered quarterly in Pulse.

5

The first part of this report focuses on new and used vehicle sales in the U.S. and Canada upon which

the vehicle remarketing industry in these two countries depends. Fortunately, new and used vehicle sales

volumes were at or near record levels in both countries during 2001. New light vehicle sales reached a

near-record 17.2 million units in the U.S. and a record 1.6 million units in Canada, for a total of 18.7 mil-

lion units in the two countries combined. Used vehicle sales topped 42.6 million units in the U.S. (matching

ADESA Analytical Services’ projection in last year’s GVR) and reached 2.1 million units in Canada, yield-

ing a total of 44.7 million units for both countries combined. Total used vehicle sales in the U.S. in 2001

broke the record set in 1995 by 866,000 units.

Zero-percent financing was the key factor leading to 2001’s emergence as the second best new vehicle sales

year ever. Coupled with more conservative residual values, and therefore higher monthly payments, on

automotive leases, zero-percent financing furthered the trend towards declining lease penetration (leases as

a percent of total retail sales). Although consumer leasing continues to play an important role in both the

new and used vehicle markets, and has helped propel both to record sales, lease penetration has dropped

from over 30% to under 25% in the U.S., and from over 45% to under 35% in Canada.

Zero-percent financing and other low-APR programs also made new vehicle purchases more attractive to

consumers visiting franchised dealership lots in 2001, and this led to a modest drop in used vehicle sales

by franchised dealers both in the U.S. and in Canada.

Residual value losses on off-lease vehicles in the U.S. averaged $987 in 2000 (the latest year for which data

is available), but a smaller percentage of leased vehicles went full-term and were returned to the lessor.

This is good news for automotive finance companies looking for signs that the worst of the residual value

crisis may be over.

Vehicles in operation (VIO) in the U.S. climbed from 213.3 million in 2000 to 216.7 million in 2001, and

from 17.6 million in 1998 to 19.2 million in 1999 (the latest year for which data is available) in Canada.

This growth in VIO is the basis for our five-year projections of used vehicle sales by vehicle age. ADESA

Analytical Services conservatively projects used vehicle sales in the U.S. to grow from 42.6 million units in

2001 to 46.5 million units in 2006 – an increase of nearly four million units (9%). This is a milder projection

than the projection in last year’s report because of an anticipated correction in new vehicle sales (which

represent additions to VIO) back to long-term trend levels over the next several years, after record new

SUMMARY AND OUTLOOK

6

GLOBAL VEHICLE REMARKETING

auto sales in 1999 through 2001. The forecast also shows a decline in vehicles three years old or less for

the same reason, as well as from declining off-lease volumes due to lower lease penetration. With improved

vehicle durability, more older used vehicles will be sold in the years to come.

The second part of this report provides a detailed description of the vehicle remarketing industry, includ-

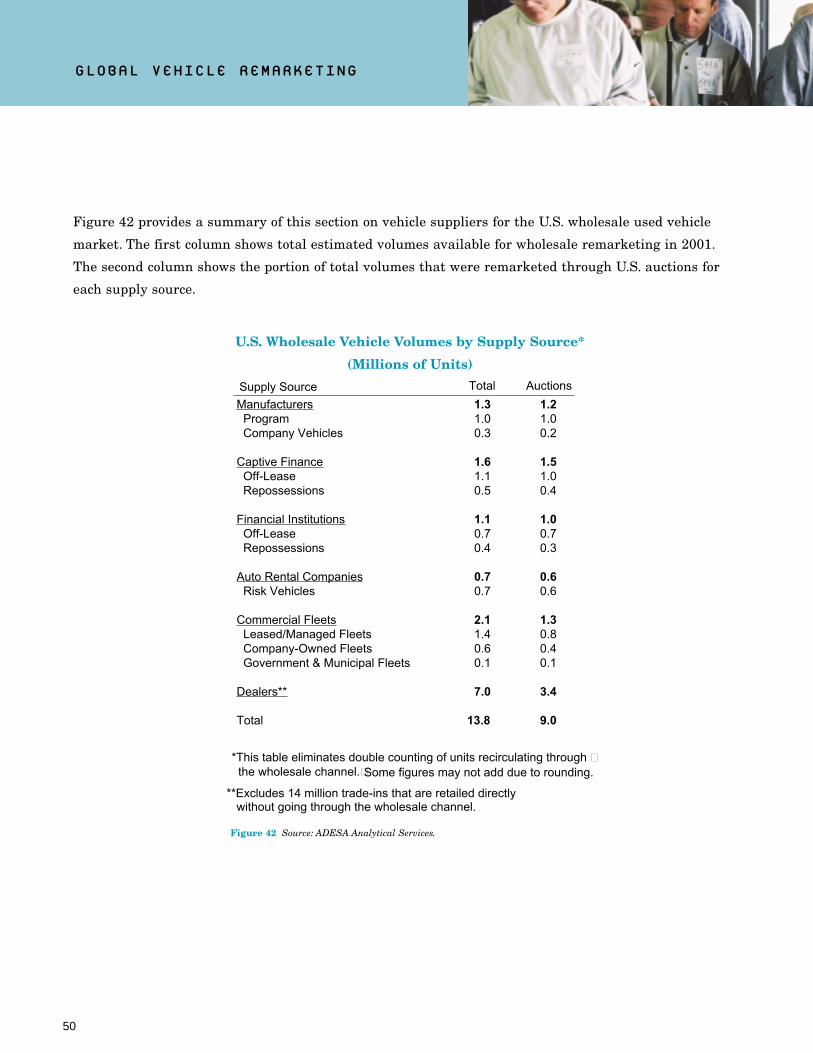

ing process steps, volume estimates, and vehicle supply sources. Making use of available industry data,

ADESA Analytical Services estimates that the vehicle remarketing industry in the U.S. and Canada chan-

neled net sales of 9.6 million units into the retail used vehicle market in 2001. These vehicles came from

a number of sources including dealers, manufacturers, automotive finance companies, rental companies

and commercial fleets. Key vehicle types examined in this report include program and rental “risk”

vehicles, off-lease vehicles, repossessions, and commercial fleet vehicles. Volumes from these sources are

summarized in Figure 42 on page 50 of this report.

Using our projections of used vehicle sales, along with an analysis of historical trends in auction sales by

model age, ADESA Analytical Services projects U.S. and Canada auction sales volumes to grow from 9.6

million units in 2001 to nearly 10.0 million units in 2003. Volumes are projected to taper modestly there-

after to 9.9 million units annually, primarily due to declining off-lease volumes.

The third part of this report provides an analysis of wholesale market trends and a market outlook for 2002

and beyond. The analysis shows that auction prices in late 2001 had significantly declined, primarily due to:

1. zero-percent financing incentives on new vehicles,

2. rental fleet downsizing in the aftermath of September 11, and

3. continued high volumes of off-lease units.

These general price trends vary by vehicle age, model class, and market segment and are amply covered

in this report and in the recently released Winter 2001 issue of Pulse.

Another important market barometer is sold volume as a percent of offered volume (conversion rate).

Conversion rates were also down during most of 2001 as evidenced by the ADESA Auction Dealer

Optimism Index. A positive sign is that this index, which shows the year-on-year variance in dealer con-

signment conversion rates, turned positive in November and December, which bodes well for the wholesale

market outlook in 2002 (see page 62 and the Winter 2001 edition of Pulse for further details).

New and UsedVehicle Sales in the U.S. &

Canada

7

GLOBAL VEHICLE REMARKETING

8

2001 at a Glance

Figure 2 succinctly shows the strength of new and used vehicle sales in the U.S. and Canada during 2001.

U.S. Canada TotalNew Vehicle Sales 17,177 1,568 18,745

Used Vehicle Sales 42,624 2,090 44,714 Franchised Dealers 15,945 929 16,874 Independent Dealers 14,416 377 14,793 Private Individuals 12,263 784 13,047

Total Vehicle Sales 59,801 3,658 63,459

Light Vehicle Sales in the U.S. and Canada in 2001

(000s of Units Sold)

Figure 2 Source: Automotive News Data Center, CNW Marketing/Research,

DesRosiers Automotive Consultants, and ADESA Analytical Services.

* CNW data for U.S. franchised dealer used vehicle sales includes sales at affiliated

used car lots operated by the franchised dealer under a different name than its new car

stores. CNW also includes off-lease vehicles purchased by lessees. These factors combine

to make CNW’s figures higher than those reported by the National Automobile Dealers

Association (NADA).

As the table shows, the two markets combined for 63.5 million total vehicle sales, of which 44.7 million

(70%) were used vehicles and 18.7 million (30%) were new vehicles. The U.S. had the second best new

vehicle sales year ever behind 2000’s 17.4 million units, while Canada had a new record year.

On the used vehicle side, the U.S. came in at 42.6 million units for 2001, essentially matching the projection

we made in last year’s GVR, and exceeding the 2000 sales total by more than one million units. This

represents a new record, breaking the old record set in 1995 by 866,000 units. Canadian used vehicle sales

in 2001 were essentially flat compared to 2000. Figure 3 shows new and used vehicle sales for 2001

compared to 2000.

*

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

9

United States 2001 2000 Amount Percent

New Vehicle Sales 17,177 17,410 (233) -1.3%

Used Vehicle Sales 42,624 41,620 1,003 2.4% Franchised Dealers 15,945 16,178 (232) -1.4% Independent Dealers 14,416 13,559 856 6.3% Private Individuals 12,263 11,883 379 3.2%

Total Vehicle Sales 59,801 59,030 770 1.3%

Canada 2001 2000 Amount Percent

New Vehicle Sales 1,568 1,545 23 1.5%

Used Vehicle Sales 2,090 2,123 (33) -1.6% Franchised Dealers 929 934 (5) -0.5% Independent Dealers 377 371 6 1.6% Private Individuals 784 818 (34) -4.2%

Total Vehicle Sales 3,658 3,668 (10) -0.3%

Increase/(Decrease)

Increase/(Decrease)

Figure 3 Source: Automotive News Data Center, CNW Marketing/Research DesRosiers Automotive

Consultants, and ADESA Analytical Services.

Light Vehicle Sales in the U.S. and Canada — 2001 vs 2000

(000s of Units Sold)

Considering the impact of the recession that began in March 2001 and the shocking events of September

11, vehicle sales in 2001 exceeded most analysts’ expectations.1 Franchised dealers in both the U.S. and

Canada sold fewer used vehicles in 2001 than in 2000, as zero-percent financing and other incentives drove

more store traffic to their new car departments. Independent dealers in both countries more than offset the

lost used auto sales of franchised dealers.

1 For a detailed discussion of the impacts of war and recession on vehicle remarketing see ADESA’s Winter 2001 Pulsereport and http://www.adesa.com/KontosKorner/WarAndRecession.htm.

10

Figure 4 combines sales volumes with average price data to arrive at the total value of new and used

vehicle sales transactions in the U.S. and Canada. As the table shows, the value of used vehicle sales

almost matched that of new vehicles, even in a near-record new-car sales year.

Memo:2001 2000

Volume Average Value AverageUnited States (000s) Price ($Billions) Price

New Vehicle Sales 17,177 $21,850

Used Vehicle Sales 42,624 $8,578 Franchised Dealers 15,945 12,132 Independent Dealers 14,416 8,071 Private Individuals 12,263 4,319

Total Vehicle Sales 59,801 $12,493

Memo:2001 2000

Volume Average Value* AverageCanada (000s) Price* ($Billions) Price*

New Vehicle Sales 1,568 $24,000 $38 $24,477

Used Vehicle Sales 2,090 $9,479 $20 $9,678 Franchised Dealers 929 13,000 $12 13,334 Independent Dealers 377 7,000 $3 7,153 Private Individuals 784 6,500 $5 6,654

Total Vehicle Sales 3,658 $15,704 $57 $15,911

* In Canadian dollars. 2001 Figures are preliminary estimates.

$21,507

$8,61812,2388,2754,316

$12,321

$369

$36719511953

$737

Light Vehicle Sales Transactions in the U.S. and Canada

Figure 4 Source: Automotive News Data Center, CNW Marketing/Research and ADESA Analytical Services.

GLOBAL VEHICLE REMARKETING

11

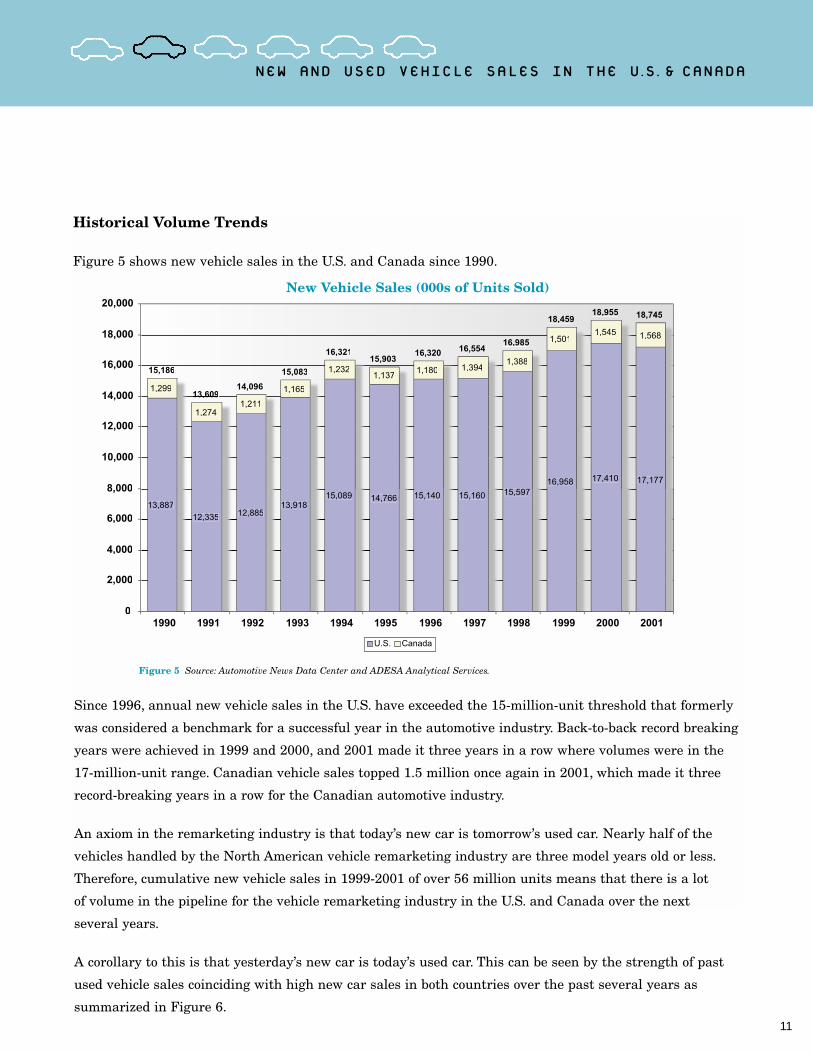

Historical Volume Trends

Figure 5 shows new vehicle sales in the U.S. and Canada since 1990.

New Vehicle Sales (000s of Units Sold)

Figure 5 Source: Automotive News Data Center and ADESA Analytical Services.

13,88712,335 12,885

13,91815,089 14,766 15,140 15,160 15,597

16,958 17,410 17,177

1,299

1,2741,211

1,165

1,2321,137

1,180 1,3941,388

1,5011,545 1,568

15,186

13,60913,60914,096

15,083

16,32115,903

16,320 16,55416,985

18,45918,955 18,745

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

U.S. Canada

Since 1996, annual new vehicle sales in the U.S. have exceeded the 15-million-unit threshold that formerly

was considered a benchmark for a successful year in the automotive industry. Back-to-back record breaking

years were achieved in 1999 and 2000, and 2001 made it three years in a row where volumes were in the

17-million-unit range. Canadian vehicle sales topped 1.5 million once again in 2001, which made it three

record-breaking years in a row for the Canadian automotive industry.

An axiom in the remarketing industry is that today’s new car is tomorrow’s used car. Nearly half of the

vehicles handled by the North American vehicle remarketing industry are three model years old or less.

Therefore, cumulative new vehicle sales in 1999-2001 of over 56 million units means that there is a lot

of volume in the pipeline for the vehicle remarketing industry in the U.S. and Canada over the next

several years.

A corollary to this is that yesterday’s new car is today’s used car. This can be seen by the strength of past

used vehicle sales coinciding with high new car sales in both countries over the past several years as

summarized in Figure 6.

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

12

U.S. Used Vehicle Sales (000s of Units Sold)

Canada Used Vehicle Sales (000s of Units Sold)

1,025 970872

984848 934 929

434319

321

361

283

371 377

1,134

1,0061,001

1,050

765

818 784

2,593

2,2952,194

2,395

1,896

2,123 2,090

0

500

1,000

1,500

2,000

2,500

3,000

1995 1996 1997 1998 1999 2000 2001

Franchised Dealers Independent Dealers Private Individuals

Figure 6 Source: CNW Marketing/Research, DesRosiers Automotive Consultants, and ADESA Analytical Services.

GLOBAL VEHICLE REMARKETING

13

Even with new vehicle sales at 17-million-unit levels, franchised dealers in the U.S. continue to sell around

16-million used units annually. In fact, franchised dealers have sold more used vehicles than new vehicles

on a cumulative basis since 1990 (185 million used versus 180 million new). Along with strong and steady

sales by independent used car dealers, this is testimony to the ability of the used vehicle market and

remarketing industry to process the trade-ins and other vehicles cycling back from many years of strong

new vehicle sales. This is a pattern that can be expected to continue.

Automotive Finance Trends 1

In the automotive industry, 2001 will be remembered as the year of the zero-percent financing program

that represented automakers’ response to the events of September 11 combined with dismal economic news.

The program was the major factor contributing to record new vehicle sales in October, and as we’ve said

elsewhere, made Detroit look better than Washington in terms of stimulating the economy. However, this

program and other low-APR financing incentives, combined with more conservative lease residual value-

setting, has caused a shift in consumer automotive financing from loans to leases that has important conse-

quences for the vehicle remarketing industry.

As stated in last year’s GVR, consumer leasing has been the most important market trend affecting the vehicle

remarketing industry over the last decade. With more companies exiting the leasing business, and with greater

use of installment loan financing, many industry observers are wondering whether leasing has run its course

and whether the industry should be poised for a reversal of the volume gains from which it has benefited.

Some perspective on this issue can be gained from looking at leasing’s growth since 1990 as shown in Figure 7.

Whether one looks at units leased (per data from CNW Marketing/Research) or Federal Reserve data on

the dollar value of outstanding leases, it is clear that leasing grew significantly throughout the 1990s,

plateaued in 2000, and began decreasing in 2001.

The decline in leasing since 2000 can also be seen in Figure 8, which shows monthly lease penetration (the

percentage of total new vehicle retail sales represented by lease financing) over the last two years.

Lease penetration has fallen almost five percentage points over the past two years, from 30.5% of new light

vehicle retail sales (i.e., excluding fleet sales) to 24.8%. This decline in lease penetration has important

ramifications for off-lease volumes destined for the vehicle remarketing industry over the next few years,

as discussed on page 37.

1 Although this section focuses on automotive finance trends in the U.S., similar trends in new car financing have been seen in Canada. Leasing, which

had grown to over 45% of retail auto sales during the 1990s, contracted at rates similar to those in the U.S., starting in 2000 as low-rate financing made

inroads on lease penetration rates. ADESA Analytical Services estimates that lease penetration in Canada now stands at less than 35% of retail sales.

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

14

Lease Penetration

(Leases as a Percent of Total New Vehicle Retail Sales)

Figure 8 Source: CNW Marketing/Research and ADESA Analytical Services.

24.8%%

30.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Jan-

00

Feb

-00

Mar

-00

Apr

-00

May

-00

Jun-

00

Jul-0

0

Aug

-00

Sep

-00

Oct

-00

Nov

-00

Dec

-00

Jan-

01

Feb

-01

Mar

-01

Apr

-01

May

-01

Jun-

01

Jul-0

1

Aug

-01

Sep

-01

Oct

-01

Nov

-01

Dec

-01

Growth of Consumer Leasing

Figure 7 Source: Federal Reserve Board, CNW Marketing/Research, and ADESA Analytical Services.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

CNW Consumer Leases (Units) Federal Reserve Board Consumer Leases Outstanding ($Millions)

Jan-

90

May

-90

Sep

-90

Jan-

91

May

-91

Sep

-91

Jan-

92

May

-92

Sep

-92

Jan-

93

May

-93

Sep

-93

Jan-

94

May

-94

Sep

-94

Jan-

95

May

-95

Sep

-95

Jan-

96

May

-96

Sep

-96

Jan-

97

May

-97

Sep

-97

Jan-

98

May

-98

Sep

-98

Jan-

99

May

-99

Sep

-99

Jan-

00

May

-00

Sep

-00

Jan-

01

May

-01

Sep

-01

GLOBAL VEHICLE REMARKETING

15

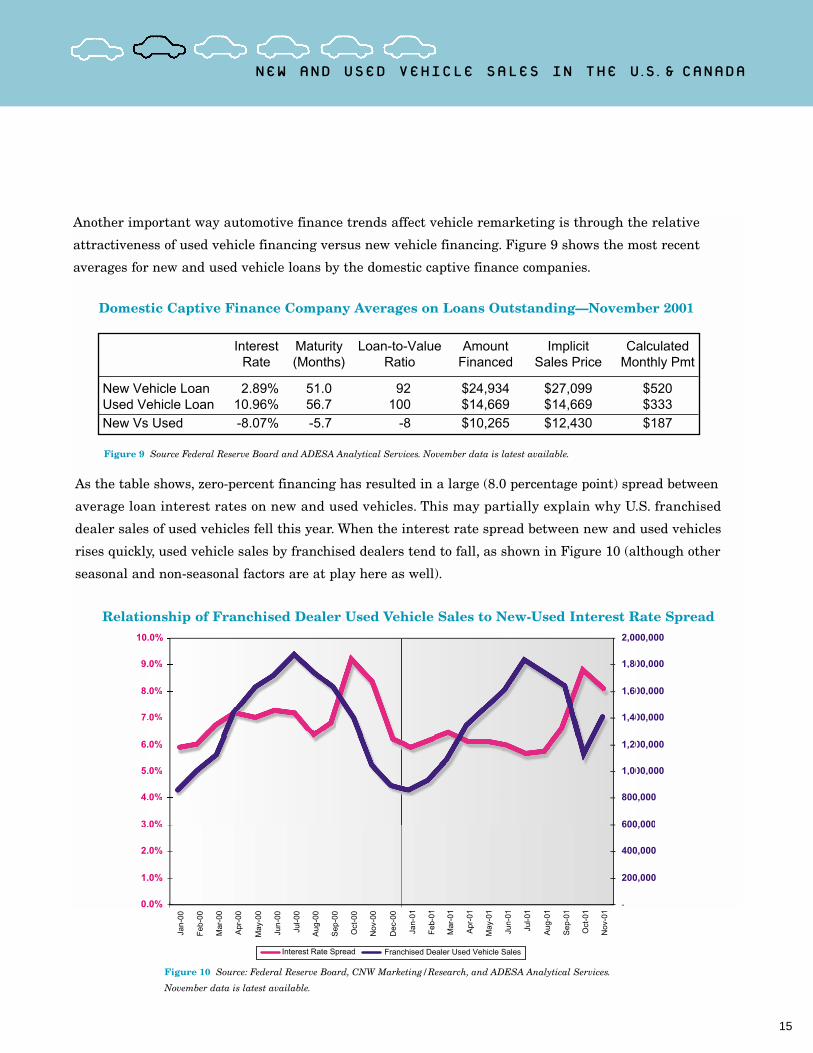

Another important way automotive finance trends affect vehicle remarketing is through the relative

attractiveness of used vehicle financing versus new vehicle financing. Figure 9 shows the most recent

averages for new and used vehicle loans by the domestic captive finance companies.

Domestic Captive Finance Company Averages on Loans Outstanding—November 2001

Figure 9 Source Federal Reserve Board and ADESA Analytical Services. November data is latest available.

Interest Maturity Loan-to-Value Amount Implicit CalculatedRate (Months) Ratio Financed Sales Price Monthly Pmt

New Vehicle Loan 2.89% 51.0 92 $24,934 $27,099 $520Used Vehicle Loan 10.96% 56.7 100 $14,669 $14,669 $333New Vs Used -8.07% -5.7 -8 $10,265 $12,430 $187

Relationship of Franchised Dealer Used Vehicle Sales to New-Used Interest Rate Spread

0.0%

1.0%

2.0%

3.0%0%

4..0%

5..0%

6..0%

7..0%

8..0%

9..0%

10..0%

Jan-

00

Feb

-00

Mar

-00

Apr

-00

May

-00

Jun-

00

Jul-0

0

Aug

-00

Sep

-00

Oct

-00

Nov

-00

Dec

-00

Jan-

01

Feb

-01

Mar

-01

Apr

-01

May

-01

Jun-

01

Jul-0

1

Aug

-01

Sep

-01

Oct

-01

Nov

-01

200,000

400,000

600,000600

0,000800

00,0001,00

00,0001,20

00,0001,40

00,0001,60

00,0001,80

00,0002,00

Interest Rate Spread Franchised Dealer Used Vehicle Sales

Figure 10 Source: Federal Reserve Board, CNW Marketing/Research, and ADESA Analytical Services.

November data is latest available.

As the table shows, zero-percent financing has resulted in a large (8.0 percentage point) spread between

average loan interest rates on new and used vehicles. This may partially explain why U.S. franchised

dealer sales of used vehicles fell this year. When the interest rate spread between new and used vehicles

rises quickly, used vehicle sales by franchised dealers tend to fall, as shown in Figure 10 (although other

seasonal and non-seasonal factors are at play here as well).

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

16

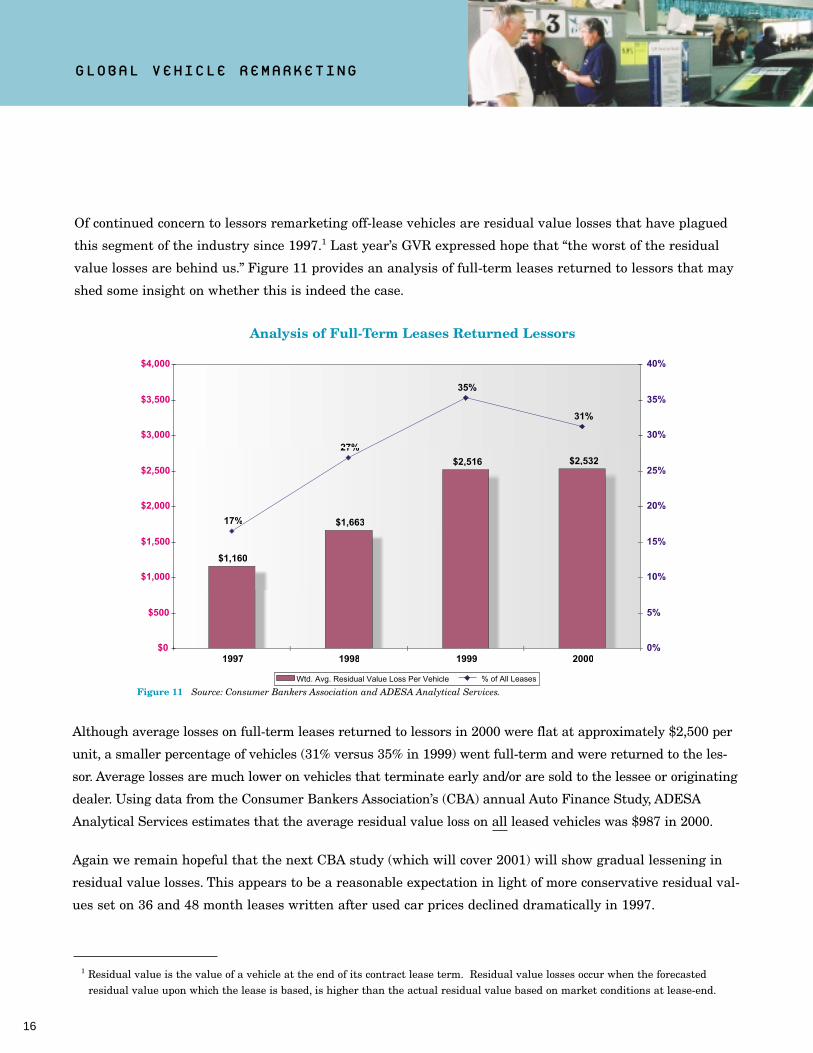

Analysis of Full-Term Leases Returned Lessors

Figure 11 Source: Consumer Bankers Association and ADESA Analytical Services.

$1,160

$1,663

$2,516 $2,532

17%%

27%27%

35%

31%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

1997 1998 1999 20000%

5%

10%

15%

20%

25%

30%

35%

40%

Wtd. Avg. Residual Value Loss Per Vehicle % of All Leases

Of continued concern to lessors remarketing off-lease vehicles are residual value losses that have plagued

this segment of the industry since 1997.1 Last year’s GVR expressed hope that “the worst of the residual

value losses are behind us.” Figure 11 provides an analysis of full-term leases returned to lessors that may

shed some insight on whether this is indeed the case.

1 Residual value is the value of a vehicle at the end of its contract lease term. Residual value losses occur when the forecasted residual value upon which the lease is based, is higher than the actual residual value based on market conditions at lease-end.

Although average losses on full-term leases returned to lessors in 2000 were flat at approximately $2,500 per

unit, a smaller percentage of vehicles (31% versus 35% in 1999) went full-term and were returned to the les-

sor. Average losses are much lower on vehicles that terminate early and/or are sold to the lessee or originating

dealer. Using data from the Consumer Bankers Association’s (CBA) annual Auto Finance Study, ADESA

Analytical Services estimates that the average residual value loss on all leased vehicles was $987 in 2000.

Again we remain hopeful that the next CBA study (which will cover 2001) will show gradual lessening in

residual value losses. This appears to be a reasonable expectation in light of more conservative residual val-

ues set on 36 and 48 month leases written after used car prices declined dramatically in 1997.

GLOBAL VEHICLE REMARKETING

17

Used Vehicle Sales Volume Projections

In last year’s GVR, ADESA Analytical Services presented a five-year projection of used vehicle sales in the U.S.

using a methodology based on “parc turn,” that is, used vehicle sales as a percent of the existing stock of vehi-

cles in operation (VIO).1 Historical parc turns were calculated by vehicle age and applied to projections of VIO

to arrive at projected used vehicle sales. Last year this methodology yielded a 2001 used vehicle sales projection

of 42,665,000 which was 41,084 units (0.1%) higher than actual 2001 U.S. sales of 42,623,916.

Figure 12 shows total vehicles in operation in the U.S. by vehicle age.

Total U.S. Vehicles in Operation by Vehicle Age Thru July 1 of each year

000s Vehicles

Figure 12 Source: R.L. Polk & Co., Goldman, Sachs & Co., and ADESA Analytical Services.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

10+ years old8-9 years old6-7 years old4-5 years old2-3 years old0-1 years old*

History Projection

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

0-1 years old* 8,872 8,480 8,048 8,627 9,561 10,132 10,651 10,246 10,649 12,172 13,104 12,396 10,515 10,934 11,249 11,584 11,725

2-3 years old 29,104 26,931 24,924 24,570 25,423 27,641 29,447 28,854 27,708 28,942 30,188 32,455 31,182 28,301 27,341 28,227 28,571

4-5 years old 28,993 28,891 28,758 26,670 24,552 23,957 24,587 26,522 28,562 27,854 26,932 27,922 29,308 31,175 30,225 27,386 27,719

6-7 years old 26,676 28,056 28,262 28,248 27,971 25,761 23,611 23,022 23,854 25,573 27,327 26,588 25,955 27,002 28,184 29,955 30,320

8-9 years old 17,000 21,146 25,127 26,692 26,844 26,480 26,378 24,442 22,603 21,923 22,553 24,081 26,078 25,473 24,816 25,825 26,140

10+ years old 64,707 63,949 65,955 70,949 74,365 79,470 83,620 87,985 91,667 93,045 93,196 93,241 95,719 98,083 101,762 103,632 104,894

175,352 177,454 181,074 185,756 188,717 193,441 198,294 201,071 205,043 209,509 213,300 216,683 218,758 220,967 223,577 226,609 229,368

* Excludes current and one year old vehicle registrations (net of scrappage) that occur after July 1 of each year.

1 Vehicles in operation (VIO) refers to the number of registered vehicles in a given geography. Typically, VIO is used in reference to acountry’s vehicle population. VIO is also called “parc” by some analysts; the latter is an international term and is not misspelled.

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

18

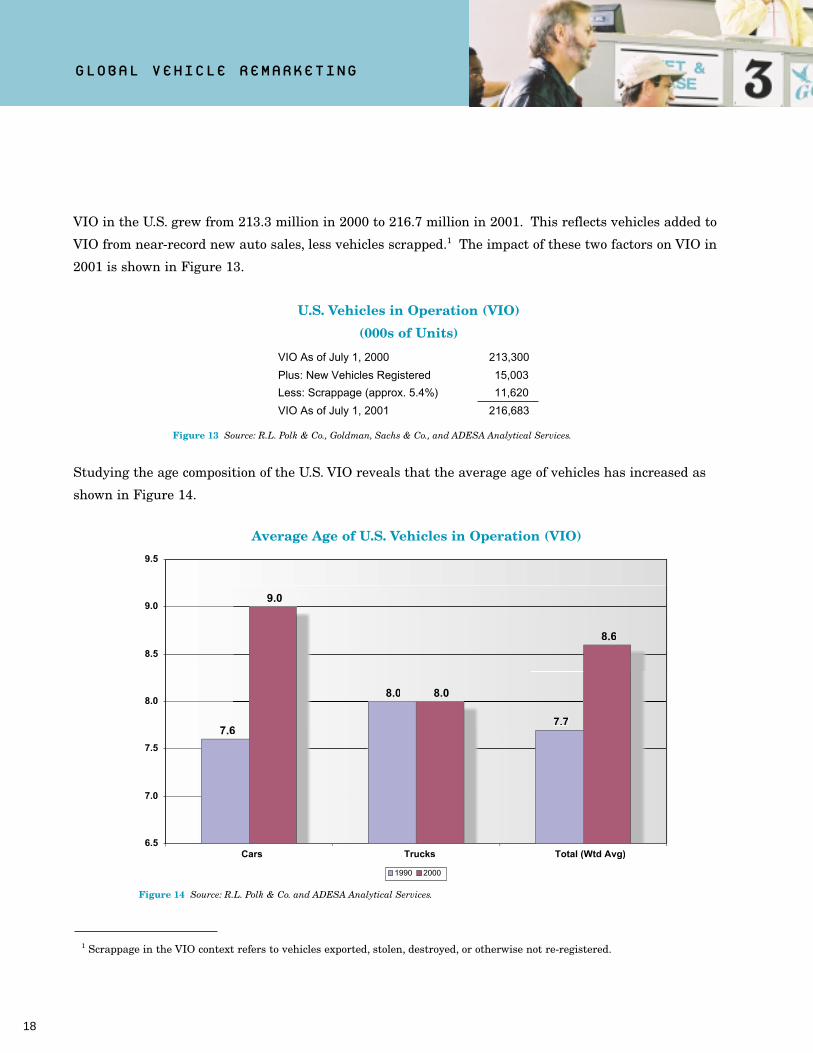

VIO in the U.S. grew from 213.3 million in 2000 to 216.7 million in 2001. This reflects vehicles added to

VIO from near-record new auto sales, less vehicles scrapped.1 The impact of these two factors on VIO in

2001 is shown in Figure 13.

1 Scrappage in the VIO context refers to vehicles exported, stolen, destroyed, or otherwise not re-registered.

U.S. Vehicles in Operation (VIO)

(000s of Units)

Figure 13 Source: R.L. Polk & Co., Goldman, Sachs & Co., and ADESA Analytical Services.

VIO As of July 1, 2000 213,300

Plus: New Vehicles Registered 15,003

Less: Scrappage (approx. 5.4%) 11,620

VIO As of July 1, 2001 216,683

Average Age of U.S. Vehicles in Operation (VIO)

Figure 14 Source: R.L. Polk & Co. and ADESA Analytical Services.

7.66

8.0

7.7

9.0

8.0

8.6

6.5

7.0

7.5

8.0

8.5

9.0

9.5

Cars Trucks Total (Wtd Avg)

1990 2000

Studying the age composition of the U.S. VIO reveals that the average age of vehicles has increased as

shown in Figure 14.

GLOBAL VEHICLE REMARKETING

19

This is primarily due to quality improvements that allow vehicles to stay in operation longer.1 Survival

rates for vehicles (determined by calculating the period of time required for half the vehicles originally reg-

istered in a given year to still be in the VIO) have been variously estimated at 13 to 16 years. For the vehi-

cle remarketing industry, quality improvements continue to extend the potential life of a vehicle between

owners, but they also extend the vehicle’s life overall. On balance, this is positive for the industry because

each longer-lasting vehicle in the VIO still has the potential to change hands three to four times during its

lifetime, even if the time between ownership-changes grows.

As stated in last year’s GVR, there is about a one-in-five chance that a vehicle in operation will be sold in the

used vehicle market during any year, although this average varies greatly by age of vehicle. Applying the same

methodology used in last year’s GVR projections, i.e., calculating parc turn rates by vehicle age, yields the five-

year used vehicle sales projections (along with a breakout of sales by age) summarized in Figure 15.

It should be noted that the expected growth in VIO as forecast this year by Goldman, Sachs & Co. is lower

than projected last year. This is because new vehicle sales in 2001 greatly exceeded most analysts’ (includ-

ing Goldman, Sachs’) expectations. The anticipated correction in new vehicle sales back to long-term trend

levels has been, in effect, delayed by one year. Therefore, the resulting forecast for used vehicle sales reach-

es 46.5 million units by 2006 in this year’s forecast, rather than in 2005 as in last year’s version. Neverthe-

less, used vehicle volumes are projected to be healthy throughout the forecast period, growing at a 1.7%

compound annual growth rate (CAGR).

1 The lack of growth in the average age of trucks is not due to lack of improvements in truck quality and durability. Rather, it isdue to the greatly increased sales of minivans, SUVs, pickups and other trucks in recent years. With more people buying newtrucks, the average age of the truck population is younger than it otherwise would be.

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

20

The forecast also shows a decline in sales of used vehicles that are three years old or less. This reflects expecta-

tions that both new vehicle sales and leasing will decline in the coming years, making fewer nearly-new units

available in the used vehicle market. Nevertheless, record new vehicle sales and leasing in 1999 through 2001

will result in excellent availability and sale of late-model (especially five-year-old) units throughout the

forecast period. In addition, the improved durability discussed previously in this section will result in

improved availability and sale of older units (greater than seven model years old), which are typically

sold by independent dealers and the public.

2001-2006Vehicle age up to: 2001 2002 2003 2004 2005 2006 CAGR*One-Year 848 757 727 751 773 782 -1.6%Two-Year 1,478 1,525 1,390 1,254 1,299 1,315 -2.3%Three-Year 2,215 2,439 2,515 2,291 2,065 2,090 -1.2%

Four-Year 3,873 3,828 4,211 4,342 3,953 4,001 0.7%Five-Year 4,078 4,484 4,430 4,870 5,020 5,081 4.5%Six-Year 5,325 4,591 5,047 4,984 5,477 5,544 0.8%Seven-Year 5,149 5,690 4,907 5,396 5,330 5,395 0.9%Eight-Year 5,650 5,919 6,551 5,655 6,221 6,297 2.2%

Nine-Year 4,102 4,532 4,756 5,275 4,563 4,619 2.4%Ten-Year 2,755 2,688 2,979 3,134 3,489 3,531 5.1%

Eleven-Year+ 7,151 7,234 7,306 7,482 7,711 7,805 1.8%

Total 42,624 43,688 44,819 45,434 45,901 46,460 1.7%

Projected U.S. Used Vehicle Sales Volumes (000s)

*Compound annual growth rate.

Projected Used Vehicle Sales Volumes (000s)

— By Vehicle Age —

Figure 15 Source: ADESA Analytical Services.

GLOBAL VEHICLE REMARKETING

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

20012001 20022002 20032003 20042004 20052005 20062006

Eleven-Year+Ten-YearNine-YearEight-YearSeven-YearSix-YearFive-YearFour-YearThree-YearTwo-YearOne-Year

21

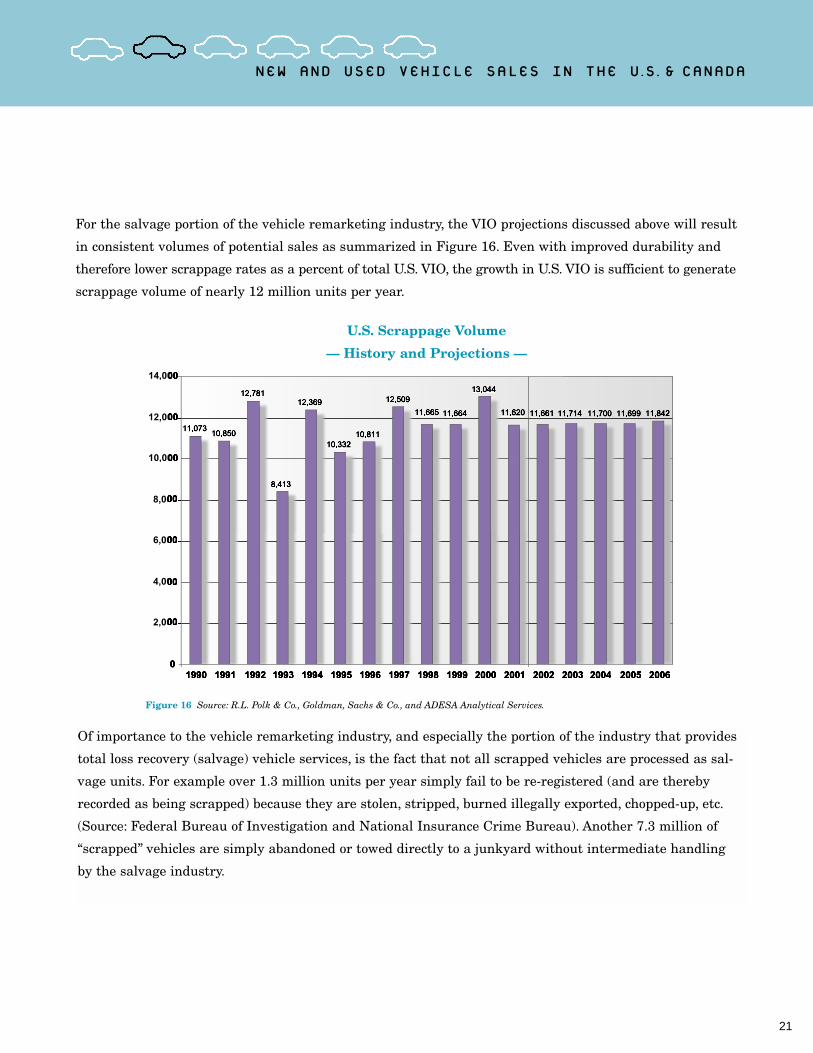

Of importance to the vehicle remarketing industry, and especially the portion of the industry that provides

total loss recovery (salvage) vehicle services, is the fact that not all scrapped vehicles are processed as sal-

vage units. For example over 1.3 million units per year simply fail to be re-registered (and are thereby

recorded as being scrapped) because they are stolen, stripped, burned illegally exported, chopped-up, etc.

(Source: Federal Bureau of Investigation and National Insurance Crime Bureau). Another 7.3 million of

“scrapped” vehicles are simply abandoned or towed directly to a junkyard without intermediate handling

by the salvage industry.

For the salvage portion of the vehicle remarketing industry, the VIO projections discussed above will result

in consistent volumes of potential sales as summarized in Figure 16. Even with improved durability and

therefore lower scrappage rates as a percent of total U.S. VIO, the growth in U.S. VIO is sufficient to generate

scrappage volume of nearly 12 million units per year.

U.S. Scrappage Volume

— History and Projections —

Figure 16 Source: R.L. Polk & Co., Goldman, Sachs & Co., and ADESA Analytical Services.

2,00

4,00

6,00

8,00

10,00

12,00

14,000

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

22

ADESA Analytical Services estimates that approximately 2.7-3.0 million units of the 11.7 million units

of annual scrappage are processed through the salvage vehicle remarketing industry. However, the portion

of total scrappage handled by this industry is expected to grow by 3-5% per year, which, along with the

stability of projected scrappage volumes, assures a steady growth to this industry.

In Canada, VIO has grown significantly as shown in Figure 17.

1 Last year’s GVR showed an estimate of used vehicle sales also performed by DesRosiers that was based on parc turn.That methodology yielded an estimate of annual Canadian used vehicle sales of 3.0 million units.

Total Vehicles in Operation — Canada

Figure 17 Source: Ward’s Communications and ADESA Analytical Services. 1999 data is latest available.

16,66816,86116 861

17,078

17,581

19,217

15,000

15,500

16,000

16,500

17,000

17,500

18,000

18,500

19,000

19,500

1995 1996 1997 1998 1999

GLOBAL VEHICLE REMARKETING

Despite the growth in VIO, current estimates of used vehicle sales in Canada put forth by DesRosiers

Automotive Consultants conservatively project 2002 used vehicle sales to be flat with 2001 at 2.1 million

units. (Figure 18 shows the DesRosiers estimate by seller type.) Also, the DesRosiers estimates show a

decline in used vehicle sales from 2.6 million units in 1995 to 2.1 million units in 2000 and 2001.1

23

It is possible that the discrepancy between Canadian VIO growth and used vehicle sales is due in part to

exports of wholesale used vehicles out of Canada. This has been prompted by comparatively low Canadian

used vehicle prices and a weak Canadian dollar relative to the U.S. dollar. ADESA Analytical Services

believes Canadian used vehicle exports will diminish over time, and the growth in VIO shown in Figure 17

would indicate that future used vehicle sales beyond 2002 should grow towards the 3.0 million-unit level

presented in last year’s GVR.

Projected 2002 Used Vehicle Sales in Canada (000s of Units Sold)

Figure 18 Source: DesRosiers Automotive Consultants.

938938(45.4%)

379(18.4%)

747747(336.2%)

Franchised Dealers Independent Dealers Private Individuals

Total Sales Volume = 2.1 million units

NEW AND USED VEHICLE SALES IN THE U.S.& CANADA

Based on ADESA Analytical Services projections presented in this section, the combined U.S. and Canadian

used vehicle markets will represent nearly 50 million units in annual sales by 2006 -- up over 11% from the

45 million units sold in the two countries in 2001.

The Vehicle Remarketing

Industry

25

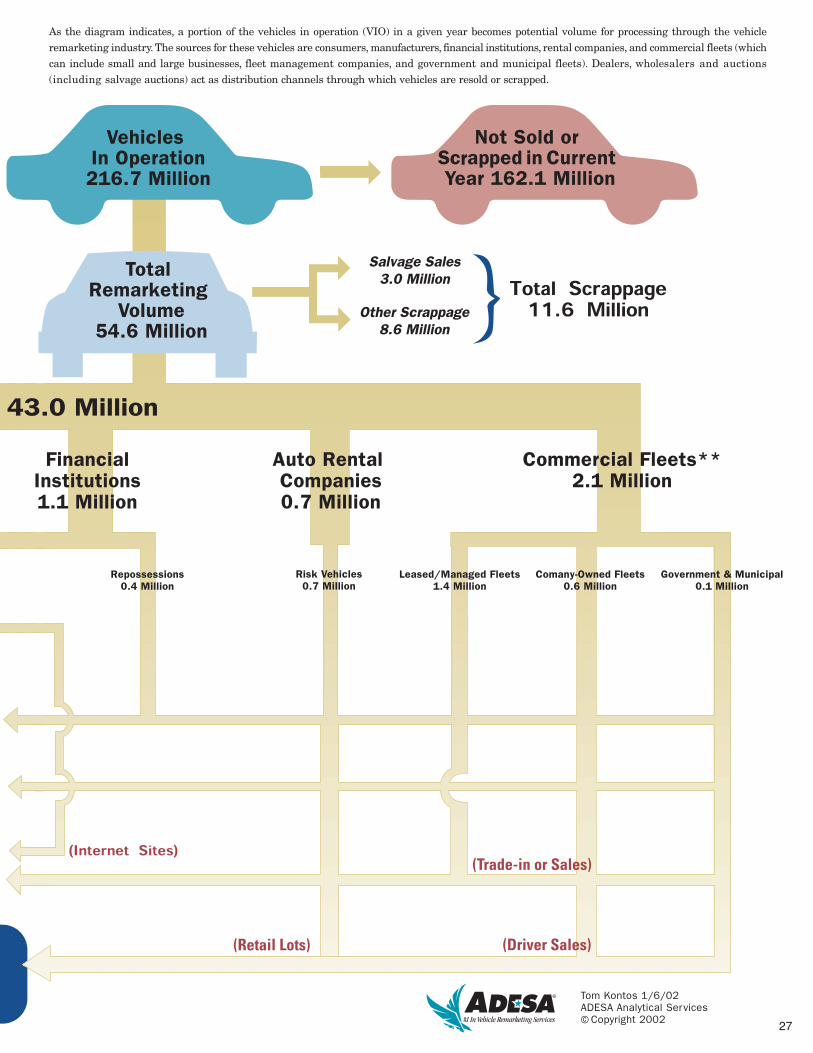

26

* Based on estimated volumes (in units) for 2001 and best available data for cross-reference. No estimates are provided where information is insufficient.** Includes approximately 0.3 million units of medium and heavy duty commercial trucks.*** See Figure 42, page 50 for details on auction volume sources.

***

Vehicle Remarketing Defined

This year’s GVR again includes

this diagram showing the flow

of used vehicles through the

remarketing process, along

with updated volume

estimates for the U.S.

27

As the diagram indicates, a portion of the vehicles in operation (VIO) in a given year becomes potential volume for processing through the vehicle remarketing industry. The sources for these vehicles are consumers, manufacturers, financial institutions, rental companies, and commercial fleets (whichcan include small and large businesses, fleet management companies, and government and municipal fleets). Dealers, wholesalers and auctions(including salvage auctions) act as distribution channels through which vehicles are resold or scrapped.

Tom Kontos 1/6/02ADESA Analytical Services Copyright 2002

Customer contact& notification;

lease termination

Economiesof ScaleNational

DistributionChannel

TechnologyDevelopment

and Web-based Services

HumanResources

and CustomerService

Orientation

Customizedinternetreporting

capabilities

In-housetrucking fleet

Affiliatedtransport

companies

Strategicallylocated

transportterminalsOUTBOUND

LOGISTICS

Customizedconsultativeanalysis of

results

Title search& processingcapabilities;

paymentprocessing

Skip tracing,collateral

recovery & otherrepossesion-

related services

Search, preview,post vehicles

on-line

Market Reports and Analytical

Services

Vehicletracking

Pick up& delivery to

central strategiclocation

SERVICE

Figure 19 depicts the vehicle

remarketing process in the form

of a value chain that involves

logistics, vehicle reconditioning

operations, promotional activities,

and other services. A checklist

has also been provided on page

31, to help individuals charged

with maximizing returns on

vehicles being remarketed, as a

reminder of the multitude of

services that the remarketing

industry can provide.

28

Managementand

Sales Expertise

Securedstorage

Vehicle historyand electronic

condition reports

Certificationdiagnosis &mechanical

reconditioning

Reconditioning& vehicle

enhancementrecommendations

Body & paintwork;

vehicleenhancementand detailing

Databasemarketing to

targeted buyersfor traditional or

on-line sales

Nationaladvertising inautomotive

industrypublications

Education &training to

expand dealerawareness anduse of auctions

Customizedpromotional

campaigns such asspecial sales events and buyer incentives

MARKETING& SALES

OPERATIONS

INBOUNDLOGISTICS

Vehicle conditionreport andequipment/option listing

Auction LocationsBody & Paint Facilities

Mechanical ShopsDetailing CentersTransport Trucks

etc.

Figure 19

29

31

A REMARKETER’S CHECKLIST FOR MAXIMIZING VALUE*

Logistical Services:______ Pick-up______ Collateral Recovery______ Marshalling______ Secured Storage______ Delivery

Reconditioning Services:Inspection Services:______ Vehicle history check (odometer, theft, title,

frame damage, flood or hail damage, salvage)______ Condition report (paper)______ Electronic Condition Report______ Digital photos______ Lease-end inspections______ Lot inventory audits

Detail Services:______ Car Wash (Automated or hand wash)______ Wash and Vacuum______ Full Detailing______ Enhanced Detailing (includes clay bar

treatment and three-step buffing)

Body & Paint Services:______ Paintless Dent Repair (PDR)______ Air brush service______ Complete body repair and paint refinishing______ Upholstery repair______ Glass repair______ Glass replacement______ Appearance enhancements (e.g., stripes)

Mechanical Services:______ Mechanical inspection services - pre-auction sale______ Certification-Level Inspection and Diagnosis______ Selected mechanical services performed

by certified technicians______ Complete mechanical repair services______ Tire replacement______ Mechanical inspection services - post-auction sale

Marketing Services:______ Database marketing research______ Advertising (Auction-level)______ Advertising (National-level)______ Telemarketing______ Broadcast fax and e-mail______ Direct mail______ Promotions

Web-based Services:______ Locate auctions of interest______ Review auction schedules______ Preview auction inventory______ Preview online inventory______ Online searches for specific vehicles______ Review auction market reports______ Post vehicles on-line______ Track vehicles being remarketed______ Purchase vehicles at set prices online______ Bid on vehicles online (Live)______ Bid on vehicles online (Set timeframe)______ Dealership management software tools______ Used parts locator

Administrative Services:______ Title processing______ Auction market reports______ Specialized reports to client's specs______ Check processing______ Electronic funds transfer______ Dealer Financing______ Retail Financing

Outsourced Services:______ Coordinated national remarketing______ Repossession services______ Lease-end services______ Title services

Analytical Services:______ Reports on industry trends______ Custom analysis based on client needs______ Presentations______ Surveys

* This worksheet can be used as a handy reference. These services may also be tailored as needed to meet the specific needs of medium and heavy commercial vehicle remarketers and insurance companies remarketing salvage vehicles. To inquire about any of the services listed on this page, please call ADESA Corporation at 317/249-4265.

THE VEHICLE REMARKETING INDUSTRY

33

The survey also confirms the scale of the industry in terms of acreage for storing and processing vehicles,

with the average auction located on 65 acres and operating seven lanes. The largest auctions have as many

as 339 acres and 27 lanes. The breadth of services offered at a typical auction – including auto detailing,

mechanical repair, body and paint repair, transportation, and dealer financing – require an average of 255

full and part-time employees.

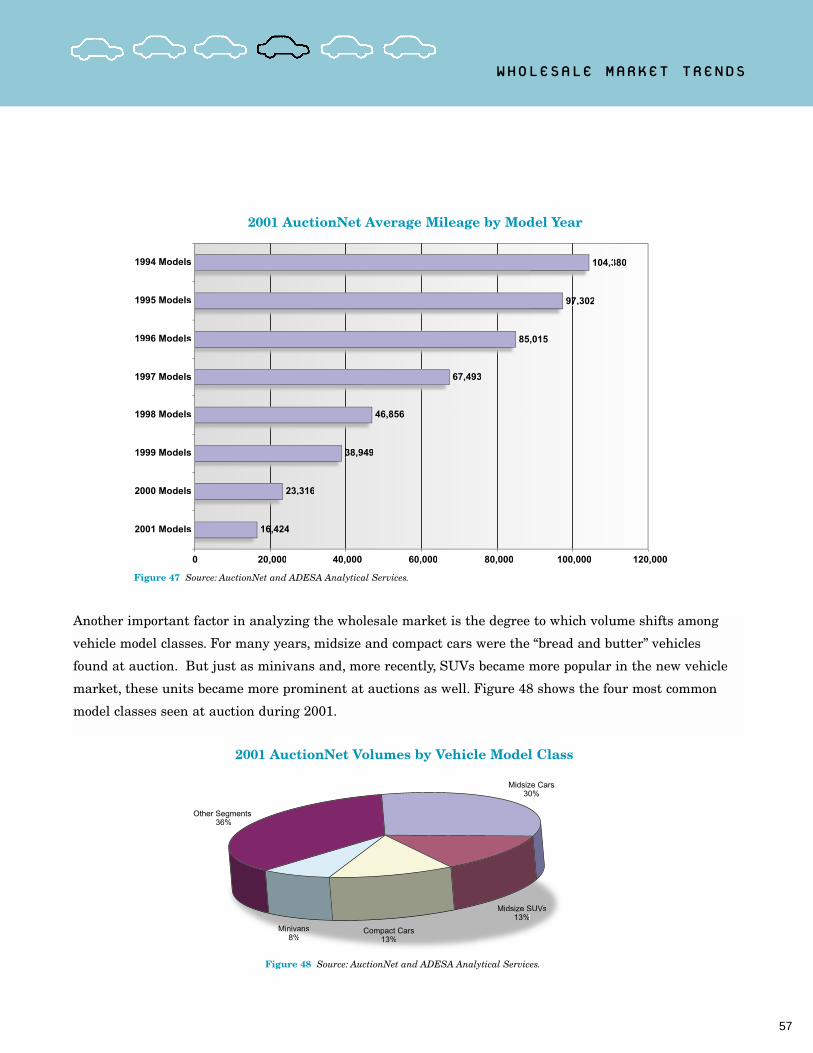

Figure 21 shows historical trends in auction vehicle sales per the NAAA survey plus ADESA Analytical

Services’ estimate for 2001.

U.S. and Canada Auction Vehicle Sales by Source

Figure 21 Source: National Auto Auction Association (NAAA) and ADESA Analytical Services.

3,428(36%)

3,762(41%)

3,963(43%)

3,857(45%)

3,991(42%)

3,398(37%)

3,293(36%)2,945

(34%)

1,945(20%)1,797

(19%)1,739(19%)1,723

(20%)

207(2%)324

(3%)233(2%)138

(1%)

0

2,000

4,000

6,000

8,000

10,000

12,000

1998 1999 2000 2001

Dealers Fleets and Leasing Companies Manufacturers Other

Total = 8,662 Total = 9,228 Total = 9,280 Total = 9,571

North American Auction Industry Sales Transactions

Figure 20 Source: National Auto Auction Association, and ADESA Analytical Services.

1997 1998 1999 2000

Gross Value of Vehicles Sold ($Billions) $56.6 $66.7 $76.5 $77.6

Units Sold (000s) 7,354 8,662 9,228 9,280

Average Price/Unit $7,693 $7,700 $8,288 $8,361

Sitting squarely in the middle of the remarketing process are the 285-plus wholesale auctions in the U.S.

and Canada that are members of the National Auto Auction Association (NAAA). Since 1997, NAAA has

been conducting a member survey, which shows that the value of wholesale transactions had reached

$77.6 billion in 2000 as shown in Figure 20.

GLOBAL VEHICLE REMARKETING

34

As these figures show, auction industry volumes in the U.S. and Canada have grown from 7.4 million units

in 1997 to an estimated 9.6 million units in 2001, with 9.1 million units being sold in the U.S. and 500,000

in Canada. Volumes from dealers have dropped from 45% of total sales to 36%, and have also dropped in

absolute terms from 3.9 to 3.4 million units annually. However, these volumes have been more than offset

by volumes coming from institutional consignors such as automobile manufacturers and their finance arms,

banks, auto rental companies and commercial fleets. To a great degree, this trend reflects the rapid growth

of leasing that results in more vehicles being handled by automotive finance companies off-lease rather

than as trade-ins to dealers. In addition, this trend towards greater auction use by major corporations con-

firms the efficiency and value of the auction-centered services provided by the vehicle remarketing industry.

Estimated 2001 Auction Volumes by Major Supply Source

(000’s of Units)

Figure 22 Source: ADESA Analytical Services.

Source of Vehicles Entered Sold % Sold Entered SoldDealers 8,204 3,290 40% 52% 36%Fleets and Leasing Companies* 5,343 3,793 71% 34% 42%Manufacturers** 2,228 1,850 83% 14% 20%Other*** 143 119 84% 1% 1%Total 15,917 9,053 57% 100% 100%

Source of Vehicles Entered Sold % Sold Entered SoldDealers 345 138 40% 43% 27%Fleets and Leasing Companies* 262 198 76% 33% 38%Manufacturers** 96 94 99% 12% 18%Other*** 101 88 87% 13% 17%Total 804 518 64% 100% 100%

Source of Vehicles Entered Sold % Sold Entered SoldDealers 8,549 3,428 40% 51% 36%Fleets and Leasing Companies* 5,605 3,991 71% 34% 42%Manufacturers** 2,323 1,945 84% 14% 20%Other*** 244 207 85% 1% 2%Total 16,722 9,571 57% 100% 100%

Units % of Total

United StatesUnits % of Total

CanadaUnits % of Total

Total United States and Canada

* Includes off-lease vehicles sold in “open” auction sales.** Includes off-lease vehicles sold in “closed,” “factory” auction sales.

*** Includes salvage units sold by insurance companies and other consignment sales.

ADESA Analytical Services also developed a breakout of 2001 sales for the U.S. and Canada based on the

NAAA survey (see Figure 22).

Vehicle Suppliers

The following sections provide details on the major suppliers of vehicles to the vehicle remarketing industry.

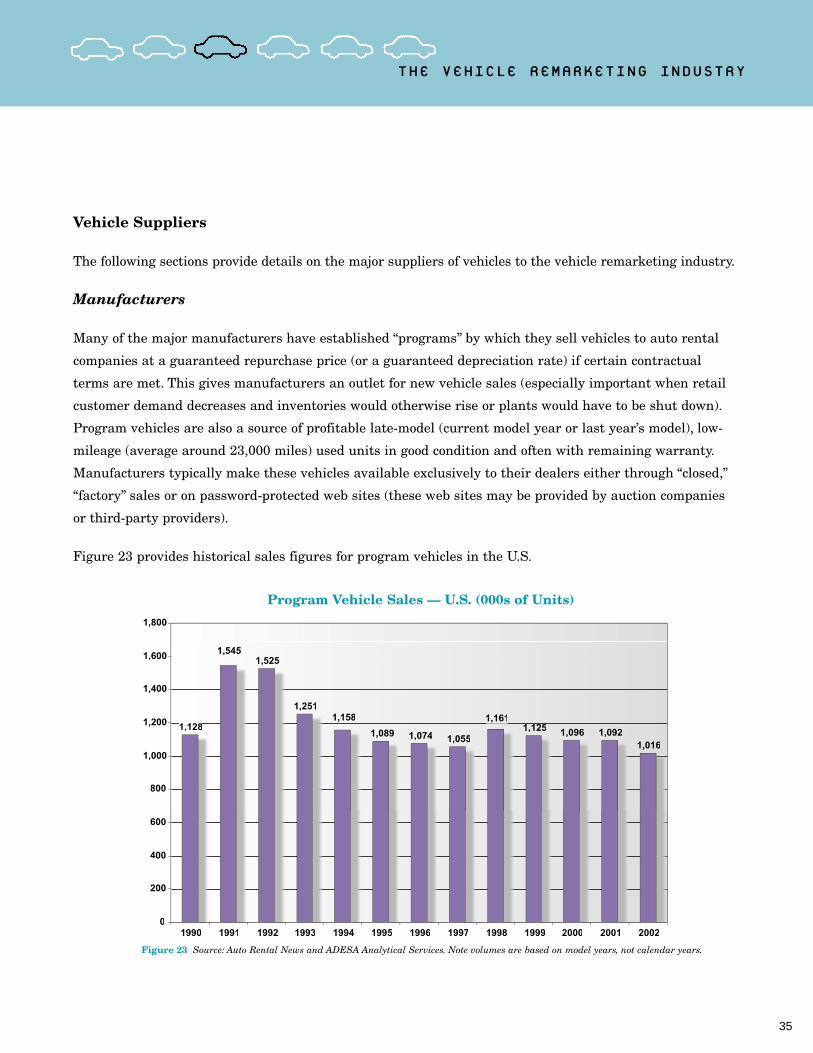

Manufacturers

Many of the major manufacturers have established “programs” by which they sell vehicles to auto rental

companies at a guaranteed repurchase price (or a guaranteed depreciation rate) if certain contractual

terms are met. This gives manufacturers an outlet for new vehicle sales (especially important when retail

customer demand decreases and inventories would otherwise rise or plants would have to be shut down).

Program vehicles are also a source of profitable late-model (current model year or last year’s model), low-

mileage (average around 23,000 miles) used units in good condition and often with remaining warranty.

Manufacturers typically make these vehicles available exclusively to their dealers either through “closed,”

“factory” sales or on password-protected web sites (these web sites may be provided by auction companies

or third-party providers).

Figure 23 provides historical sales figures for program vehicles in the U.S.

35

THE VEHICLE REMARKETING INDUSTRY

Program Vehicle Sales — U.S. (000s of Units)

1,128

1,5451,525

1,2511,158

1,089 1,074 1,055

1,161,1,125 1,096 1,092

1,016

00

200

400

600

800

1,0000

1,2000

1,4000

1,6000

1,800

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Figure 23 Source: Auto Rental News and ADESA Analytical Services. Note volumes are based on model years, not calendar years.

36

Program vehicle sales have declined by about 500,000 units since their peak in 1991. At that time, manu-

facturers used program vehicles as a “lever” to keep plant utilization high during the 1990-91 recession.

In this year’s recession, manufacturers primarily used zero-percent financing and other retail incentives

rather than increased program vehicle sales to accomplish the same goal. ADESA Analytical Services

expects program vehicle supply to the U.S. vehicle remarketing industry to remain at the one-million-unit

level for the foreseeable future.

From discussions with the remarketing departments of the major manufacturers in Canada, ADESA

Analytical Services expects approximately 150,000 program units annually to be sold through auctions

and auction-owned websites for the foreseeable future. This represents 30% of total annual Canadian

remarketing industry volume.

Automotive Finance Companies

A second major source of vehicles to the remarketing industry are captive (i.e., the finance arms of the

major automobile manufacturers) and non-captive (e.g., banks, credit unions, etc.) automotive finance

companies. In years past, these companies furnished mostly repossessed vehicles to auctions, amounting

to approximately one million units annually.1 Since the early 1990s, however, the bulk of units remarketed

by these companies are off-lease vehicles.

To determine projected off-lease volumes returning for wholesale remarketing in the U.S., the estimates

shown in Figure 24 were utilized.

Estimates of Lease Termination Outcomes

Figure 24 Source: ADESA Analytical Services using data as noted.

Latest Research Results

Termination Outcome NADA CNW M/R CBA** Average 2001 2002

Lessee Takes Possession 16% 25% 26% 22% 711 689

Dealer Takes Possession 20% 32% 15% 22% 711 689

Lessor Takes Possession* 64% 43% 59% 56% 1,810 1,753

Total 100% 100% 100% 100% 3,233 3,130

*** Includes month-to-month, lease conversions, repossession, insurance loss, etc.*** Consumer Bankers Association. Weighted average of early- and full-term leases.*** Based on CNW Marketing/Research totals (000s of units).

Off-Lease Volumes***

1 During recessions, loan default rates and therefore repossessions rise. This is one of several factors that provide stability to vehicleremarketing volumes despite cyclical fluctuations in the general economy and in the automotive industry.

GLOBAL VEHICLE REMARKETING

37

With projected declines in lease volumes (discussed on pages 13-14), ADESA Analytical Services projects

off-lease volumes in the U.S. to decrease significantly over the next five years as shown in Figure 25.

Despite these declines, off-lease volumes available for wholesale remarketing will remain at historically

high levels over the next five years.

Off-Lease Volumes Returning for Wholesale Remarketing (000s of Units)

Figure 25 Source: CNW Marketing/Research and ADESA Analytical Services.

200250

500588

662

848907

1,198

1,582

1,9181,856

1,810 1,753

1,672

1,523

1,3091,248

0

2000

4000

6000

8000

1,0000

1,2000

1,4000

1,6000

1,8000

2,0000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

History Projections

In Canada, around 40% of retail sales in 1999 and 2000 were leases (although lease penetration in 2001

dropped due to attractive loan financing availability), and around 41% of off-lease vehicles return to the

lessor (per DesRosiers Automotive Consultants). As a result, off-lease volumes available for wholesale

remarketing are expected to average around 250,000 units annually over the next two years. Beyond

2003, ADESA Analytical Services expects a similar tapering in off-lease volumes as that projected for

the U.S., to an ultimate volume of approximately 175,000 units by 2006.

THE VEHICLE REMARKETING INDUSTRY

Trends in Consumer Leasing 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

New Light Vehicle SalesVolumes (000s)

13,887 12,335 12,885 13,918 15,089 14,766 15,140 15,160 15,597 16,958 17,410 17,177 15,750 15,570 16,051 16,568 16,750Consumer Leases 574 743 1,203 1,852 2,519 2,648 2,963 3,424 3,587 4,146 4,162 3,607 3,348 3,181 3,278 3,314 3,350Off-Lease Returns 400 500 1,000 1,591 1,688 2,186 2,846 3,261 3,302 3,366 3,437 3,233 3,130 3,040 2,820 2,470 2,400Off-Lease Volumes Returning for Wholesale Remarketing 200 250 500 588 662 848 907 1,198 1,582 1,918 1,856 1,810 1,753 1,672 1,523 1,309 1,248

Consumer Leases as a Percent of New Light Vehicle Sales 4% 6% 9% 13% 17% 18% 20% 23% 23% 24% 24% 21% 21% 20% 20% 20% 20%Remarketing Volumes as a Percent of Off-Lease Returns 50% 50% 50% 37% 39% 39% 32% 37% 48% 57% 54% 56% 56% 55% 54% 53% 52%

History Projections

38

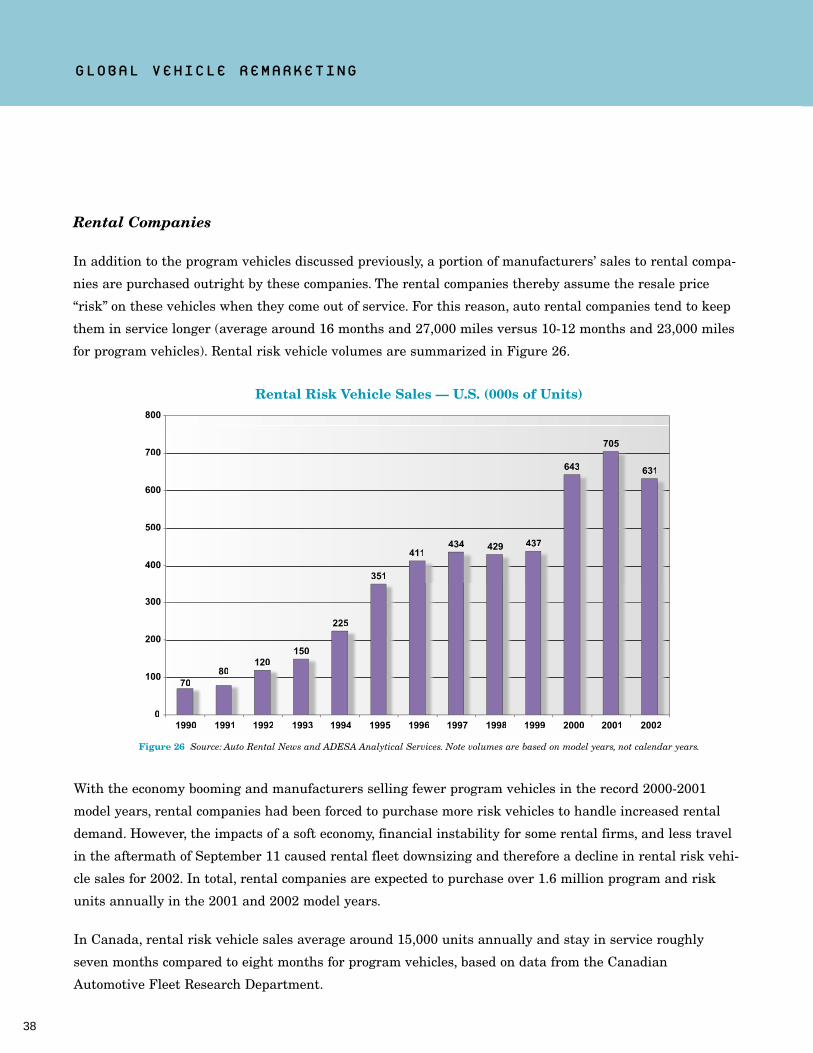

Rental Companies

In addition to the program vehicles discussed previously, a portion of manufacturers’ sales to rental compa-

nies are purchased outright by these companies. The rental companies thereby assume the resale price

“risk” on these vehicles when they come out of service. For this reason, auto rental companies tend to keep

them in service longer (average around 16 months and 27,000 miles versus 10-12 months and 23,000 miles

for program vehicles). Rental risk vehicle volumes are summarized in Figure 26.

Rental Risk Vehicle Sales — U.S. (000s of Units)

7080

120150

225

351

411434 429 437

643

705

631

0

1000

2000

3000

4000

5000

6000

7000

800

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

With the economy booming and manufacturers selling fewer program vehicles in the record 2000-2001

model years, rental companies had been forced to purchase more risk vehicles to handle increased rental

demand. However, the impacts of a soft economy, financial instability for some rental firms, and less travel

in the aftermath of September 11 caused rental fleet downsizing and therefore a decline in rental risk vehi-

cle sales for 2002. In total, rental companies are expected to purchase over 1.6 million program and risk

units annually in the 2001 and 2002 model years.

In Canada, rental risk vehicle sales average around 15,000 units annually and stay in service roughly

seven months compared to eight months for program vehicles, based on data from the Canadian

Automotive Fleet Research Department.

GLOBAL VEHICLE REMARKETING

Figure 26 Source: Auto Rental News and ADESA Analytical Services. Note volumes are based on model years, not calendar years.

39

Commercial Fleets

Another important source of vehicle remarketing supply is commercial fleets.1 There are 15.2 million

commercial fleet vehicles in the U.S. – or seven percent of the nation’s 216.7 million-unit vehicle population.

Figure 27 breaks out commercial fleet vehicle volumes by fleet type.

Total Fleet Vehicles in Service by Fleet Type

Total Vehicles = 15.2 millions

Figure 27 Source: Automotive Fleet and ADESA Analytical Services. Fleet size based on 2000 vehicle

registrations (latest available).

Businesses (10 or more units)

39.3%

Businesses (4-10 units)18.7%

Government21.7%

Rental12.0%

Utilities5.4%

Other Municipal*3.0%

* Includdes police, taxi, etc.

000s Units

Segment Cars Trucks Total % of Total

Businesses (4-10 units) 1,173 1,662 2,835 18.7%

Businesses (10 or more units) 2,950 3,026 5,976 39.3%

Subtotal Businesses 4,123 4,688 8,811 58.0%

Government 883 2,408 3,291 21.7%

Utilities 317 498 815 5.4%

Other Municipal* 442 8 450 3.0%

Subtotal Government/Municipal 1,642 2,914 4,556 30.0%

Rental 1,581 248 1,829 12.0%

Total 7,346 7,850 15,196 100.0%

Memo:

Vehicle Type Percent 48.3% 51.7% 100.0%

* Includes police, taxi, etc.

1 For excellent sources of detailed information on commercial vehicle fleets in the U.S. and Canada, see the annual “Fact Book”editions of Automotive Fleet and Canadian Automotive Fleet magazines, published by Bobit Publishing Company.

THE VEHICLE REMARKETING INDUSTRY

40

These fleets can be owned outright by the business, government, and municipal organizations that operate

the vehicles, or they can be leased from, and managed by, fleet management companies as summarized in

Figure 28.

Company-Owned Fleet Vehicles in Service

Figure 28 Source: Automotive Fleet and ADESA Analytical Services. Fleet size based on 2000 vehicle registrations

(latest available).

634 738 1,372 14.0%1,218 1,456 2,674 27.3%

1,852 2,194 4,046 41.3%

752 2,010 2,762 28.2%

281 445 726 7.4%430 7 437 4.5%

1,463 2,462 3,925 40.1%

1,569 248 1,817 18.6%

4,884 4,904 9,788 100.0%

49.9% 50.1% 100.0%

539 924 1,463 27.1%1,732 1,570 3,302 61.1%

2,271 2,494 4,765 88.1%

131 398 529 9.8%

36 53 89 1.6%12 1 13 0.2%

179 452 631 11.7%

12 0 12 0.2%

2,462 2,946 5,408 100.0%

45.5% 54.5% 100.0%

000s Units

Segment Cars Trucks Total % of Total

Businesses (4-10 units)

Businesses (10 or more units)

Subtotal Businesses

Government

Utilities

Other Municipal*

Subtotal Government/Municipal

Rental

Total

Memo:

Vehicle Type Percent

000s Units

Segment Cars Trucks Total % of Total

Businesses (4-10 units)

Businesses (10 or more units)

Subtotal Businesses

Government

Utilities

Other Municipal*

Subtotal Government/Municipal

Rental

Total

Memo:

Vehicle Type Percent

Leased/Managed Fleet Vehicles in Service

GLOBAL VEHICLE REMARKETING

41

All of this volume represents auction market potential – either traditional or Internet-based. However, fleet

management companies and large company-owned fleets (including rental companies discussed previously)

are the groups within these categories that most favor auctions for their vehicle remarketing.

Commercial fleet vehicle remarketing volumes also tend to be stable throughout the business cycle because

fleet managers use and replace these vehicles based on fairly consistent policies. Figure 29 shows average

turnback mileage and prices for commercial fleet vehicles.

Average Turnback Mileage and Prices for Commercial Fleet Vehicles — 2001

Figure 29 Source: Automotive Fleet and ADESA Analytical Services.

Average Mileage Average Price

Average Average Service Average Average AverageMonthly Life in Turnback Capitalized Depreciation Turnback

Segment Miles Months Mileage Cost Per Month Price

Compact Cars 2,034.00 21.07 42,856 $14,524 $276.63 $8,695

Intermediate Cars 1,967.67 25.80 50,766 $17,751 $345.14 $8,847

Minivans 2,160.00 27.10 58,536 $20,092 $381.70 $9,748

SUVs 2,104.67 25.07 52,764 $24,962 $475.00 $13,054

Full-Size Vans 1,901.33 29.43 55,956 $18,448 $308.22 $9,377

Light Trucks 2,321.00 30.43 70,628 $20,012 $347.22 $9,446

Figure 30 Source: Canadian Automotive Fleet, Automotive Fleet, and ADESA Analytical Services.

Fleet as aRetailCountry Fleet Total % of Total

Canada 1,298,923 293,232 1,592,155 18.4%

U.S. 14,269,650 2,734,915 17,004,565 16.1%

2000 New Registrations

Commercial fleet vehicle sales in Canada make up a slightly higher percentage of total new vehicle sales

than in the U.S., as seen in Figure 30.

ADESA Analytical Services estimates annual Canadian commercial fleet vehicle sales available for

wholesale remarketing to be approximately 85,000 units.

THE VEHICLE REMARKETING INDUSTRY

42

Dealers

There are 22,150 franchised (new vehicle) dealerships and 54,150 independent (non-franchised dealers

selling used vehicles only) in the U.S. In Canada, there are an estimated 3,550 franchised dealers, and

estimates of the number of independent dealers range from 11,400 to 21,750. These retailers combine to

sell 30.3 million used units in the U.S. and 1.3 million units in Canada. Figure 31 shows the decline in

franchised dealerships in the U.S. and Canada. In both countries, the number of franchised dealerships

declined by 11% from 1990 through 2001.

Number of Franchised Dealerships in the U.S. and Canada

Figure 31 Source: NADA, DesRosiers Automotive Consultants, and ADESA Analytical Services.

20,500

21,000

21,5000

22,0000

22,5000

U.S

.

Can

ada

23,0000

23,5000

24,0000

24,5000

25,0000

25,500

3,3003,300

3,4003,400

5005003,53,5

6006003,63,6

7007003,73,7

8008003,83,8

9009003,93,9

0000004,04,0

4,1004,100

U.S. 24,825 24,200 23,500 22,950 22,850 22,800 22,750 22,700 22,600 22,400 22,250 22,150

Canada 4,000 3,964 3,966 3,872 3,855 3,819 3,714 3,608 3,543 3,535 3,569 3,550

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

This is part of a consolidation trend that is amplified by the growth of publicly held dealership groups,

most of which fall into the top 100 dealership groups in the U.S. Figure 32 captures the consolidation trend

by examining the share of several measures of total franchised dealership activity accounted for by the top

100 dealer groups.

GLOBAL VEHICLE REMARKETING

43

Although the top 100 dealer groups now represent 15% of total dealership revenue, their share of used

vehicle sales volume remains relatively low – especially when sales by independent dealers are included.

Dealers earn a substantial amount of profit from selling used vehicles. For franchised dealers, who sell

both new and used vehicles, average gross profits from used vehicles match those of new vehicles, even

though the used vehicle ties up almost 50% less capital. Independent dealers generally sell a lower priced

and older vehicle, but their profitability is even better on a per-unit basis. Buy-Here/Pay-Here dealers tend

to sell the least expensive vehicle of all dealer types, and yet their profitability is the highest on a per-unit

basis (especially when finance profits are added in). These observations are supported by the data in Figure 33.

Top 100 Dealer Groups Share of Total Franchised Dealerships

Figure 32 Source: Automotive News Data Center and ADESA Analytical Services. 2000 data is latest available.

4.3%

8.0%

4.6%

7.0%

9.8%

4.8%

8.6%

5.0%

7.5%

10.6%

5.7%

10.1%

5.8%

8.8%

12.2%

6.33%

11.2%

5.6%%%

9.2%

14.1%

7.6%

12.4%

6.7%

10.5%

14.8%

7.8%

13.6%

6.6%

10.9%

14.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Total # of Dealerships Total New Vehicles Sold Total Used Vehicles Sold Total All Vehicles Sold Total Group Revenue

1995 1996 1997 1998 1999 2000

THE VEHICLE REMARKETING INDUSTRY

Dealers have choices in the means by which they source their used vehicle inventory. Obviously, dealers can

obtain used vehicles through trade-ins. This involves negotiation between dealer and customer and overlaps

into the negotiations taking place on the vehicle the dealer is trying to sell. Dealer experience in favorably

negotiating new car trades results in a modest gross profit advantage for new car trade-ins versus some

auction-sourced units (see Figure 34). However, dealers recently have been generating their greatest prof-

its on vehicles (often off-lease units) they purchase at auction from finance companies in fleet/lease sales.

$1,509

$1,532

$1,541

$1,556

$1,631

$1,686

61$2,0

$0 $500 $1,000 $1,500 $2,000 $2,500

Street Purrcchase

Used Vehicle TTrade

Auctions - Closed “Faccctory”

Auctions - Open “OOOther”

Wholesssalers

New Vehicle TTrade

Auctions - Open “Fleet/LLeease”

44

Gross Profit by Source of Vehicles Retailed by Franchised Dealers

Figure 34 Source: NADA Dealer Academy and ADESA Analytical Services. Based on 2001 data for franchised dealers..

U.S. Dealer Profitability (All data is on a per-vehicle basis)

Buy Here/Independent Pay Here

New Used Dealers** DealersAverage Retail Sales Price $25,632 $13,882 $10,942 $6,721

Average Gross Profit $1,539 $1,534 $1,722 $3,471***Gross Profit % 6.0% 11.1% 15.7% 51.6%

* Per NADA. Represents 2001 year-to-date data through November (latest available).** Per NIADA. Based on 2000 data (latest available).*** Includes finance income.

Franchised Dealers*

Figure 33 Source: NADA, National Independent Automobile Dealers Association (NIADA) and ADESA Analytical Services.

GLOBAL VEHICLE REMARKETING

45

Although dealers also make good margins on vehicles purchased from wholesalers1, they often lose money

on vehicles they sell to wholesalers (referred to as “wholesaling”). Figure 35 shows the range of gross profits

on vehicles wholesaled.

18

46)

7)

($200)

($150)

($100)

($50)

$0

$50

$100

$150

High

Average

Low

$188

$69

-$49

-$222

-$436

-$546

-$923$92-$1,000

-$800

-$600

-$400

-$200

$0

$200

$400

1 to 10 11 to 20 21 to 30 31 to 45 46 to 60 61 to 90 Over 90

Gross Profit Per Used Vehicle Wholesaled by Franchised DealersOverall Average at Various Dealerships By Days in Inventory

1 Wholesalers (also called brokers) buy used vehicles from dealers and corporate fleets (including rental and government fleets),and sell to other dealers, often via auction. Wholesalers profit from “arbitraging” the difference in price.

2 ADESA Analytical Services has performed detailed analysis that confirms this. Interested dealers may call Tom Kontos (317) 249-4235 for details.

3 AuctionNet prices reflect wholesale prices for both franchised and independent dealers and therefore should not be compareddirectly with the NADA retail prices, which are for franchised dealers only, to attempt to calculate used vehicle gross profit margins. Also, NADA average retail prices include sales of vehicles not sourced at auction. Wholesale price trends are discussed at length in the third part of this report.

Figure 35 Source: NADA Dealer Academy and ADESA Analytical Services. Based on 2001 data for franchised dealers.

ADESA Analytical Services estimates that more than half the trade-ins that U.S. franchised dealers

wholesale (a total of seven million units), or roughly 3.6 million units, are sold to wholesalers and the rest

(3.4 million units) are wholesaled via auction. The competitive bidding environment of auctions versus the

arbitrage profit motivation of wholesalers will often result in higher gross margins for vehicles wholesaled

by franchised dealers at auction.2

At the net profit level, auction-sourced vehicles may generate more F&I (Finance and Insurance) income

because of their often-superior condition and higher value. In addition, auction prices appear to have been rising

more slowly than retail used vehicle prices for franchised dealers, as shown in Figure 36.3 This is an indication

that gross profits on used vehicles sourced at auction have been increasing for franchised dealers in the U.S.

THE VEHICLE REMARKETING INDUSTRY

46

Gross Profit by Days in Inventory

Figure 37 Source: NADA Dealer Academy and ADESA Analytical Services. Based on 2001 data for franchised dealers.

Another important factor in determining dealer profitability on used vehicles is quickness of inventory

turnover. Figure 37 shows that dealers generate considerably more gross profit (and not coincidentally,

often incur lower reconditioning costs) on vehicles that sell within 45 days.

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01

NADA Avg Retail Price AuctionNet Wholesale

Wholesale and Retail Price Trends

Figure 36 Source: NADA, AuctionNet and ADESA Analytical Services.

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

%0%

%5%

%10%

%15%

%20%

%25%

%30%

%35%

$ Per Unit $1,717 $1,862 $1,840 $1,715 $1,554 $1,308 $829Margin % 33% 18% 12% 11% 7% 9% 9%

1 to 10 11 to 20 21 to 30 31 to 45 46 to 60 61 to 90 Over 90

$337

$473$485 $505

$456

$499

$465

$0

$100

$200

$300

$400

$500

$600

1 to 10 11 to 20 21 to 30 31 to 45 46 to 60 61 to 90 Over 90

GLOBAL VEHICLE REMARKETING

Reconditioning Investment by Days in Inventory

($ Per Unit Retailed)

47

By using auctions to proactively obtain used vehicles that are targeted to a specific market and clientele,