f2-final test.pdf

DESCRIPTION

acca f2 MOCK EXAMTRANSCRIPT

ACCA FINAL ASSESSMENT

Management Accounting

QUESTION PAPER

Time allowed 2 hours

All 50 questions are compulsory and must be attempted

Formulae Sheet is on page 3

Do not open this paper until instructed by the supervisor

This question paper must not be removed from the examination hall

JUNE 2011

Kaplan Publishing/Kaplan Financial

Pape

r F2

ACCA F2 MANAGEMENT ACCOUNTING

2 KAPLAN PUBLISHING

© Kaplan Financial Limited, 2010

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials.

All rights reserved. No part of this examination may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without prior permission from Kaplan Publishing.

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 3

Formulae Sheet

Linear regression

r = ]y)(-y[n ]x)(-x[n

yx-xyn2222 ∑∑∑∑

∑∑∑

If y = a + bx,

b = 22 x)(-xnyx-xyn

∑∑

∑∑∑ and a =

ny∑

- bnx∑

Economic order quantity

Economic order quantity = H

O

CD2C

Economic batch quantity = ⎟⎠⎞

⎜⎝⎛

RD-1C

D2C

H

O

ACCA F2 MANAGEMENT ACCOUNTING

4 KAPLAN PUBLISHING

All 50 questions are compulsory and must be attempted

1 A Ltd manufactures a single product which it sells for $9 per unit. Fixed costs are $54,000 per month and the product has a variable cost of $6 per unit.

In Period 1, actual sales amounted to $180,000. What was A Ltd’s margin of safety?

units (2 marks)

2 The following details are available for a company:

Budget labour hours 8,500

Budgeted overheads $148,750

Actual labour hours 7,928

Actual overheads $146,200

Based on the data given above, what is the amount of overhead under/over absorbed?

A $2,550 under-absorbed

B $2,529 over-absorbed

C $2,550 over-absorbed

D $7,460 under-absorbed (2 marks)

3 Over the last two months the following production costs were incurred by Department Z:

Level of activity

Production cost

May 5,269 units $36,614

June 4,821 units $33,926

In July budgeted production was 2,560 units. The budgeted production cost would be:

A $20,360

B $15,740

C $18,880

D $14,552 (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 5

4 The annual demand for an item produced by Fish Ltd is 10,000 units. The cost of placing an order is $320 and the cost of holding an item in stock for one year is $60. What is the economic order quantity to the nearest unit?

A 325

B 330

C 327

D 337 (2 marks)

The following information is to be used for questions 5 and 6.

During the month of June a manufacturing process incurs material costs of $8,000 and conversion costs of $4,500. 2,000 kg of material was input. There is a normal loss of 10% and all losses have a scrap value of $1.75 per kg. During the period 1,700 kg were output to finished goods. Opening and closing stocks in the process were nil.

5 What was the cost per kg output in the period?

$ (2 marks)

6 What was the value of the abnormal loss written off in the profit and loss account?

$ (2 marks)

7 The following information is available about a product a company sells:

Direct material (per unit) $12

Direct labour (per unit) $23

Variable overheads (total) $30,000

Fixed overheads (total) $50,000

Production (units) 10,000

What is the prime cost per unit?

A $15

B $38

C $43

D $35 (2 marks)

ACCA F2 MANAGEMENT ACCOUNTING

6 KAPLAN PUBLISHING

8 A company has recorded the following results:

March April May

Units 2,800 3,000 2,700

Production costs $29,200 $30,000 $28,800

In June, the budgeted output is 3,250 units. The budgeted production costs should be:

A $13,000

B $31,000

C $31,250

D $32,500 (2 marks)

9 A company uses process costing in calculating output cost. The following details are available for a particular department in June 20X2. All materials are added at the start of the process.

Opening work in progress Nil units

Units started 10,000 units

Closing work in progress 1,000 units

100% complete for materials

75% complete for conversion

Normal loss 200 units

Units completed 8,000 units

If all losses occur at the start of the process, then how many equivalent units should be included for materials?

A 7,750

B 8,750

C 8,800

D 9,800 (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 7

10 A company makes three products as follows:

Chairs Tables Cupboards

Wood @ $5 per m2 $20 $40 $60

Labour @ $6 per hour $12 $24 $48

Fixed costs absorbed $10 $20 $40

Profit $4 $6 $10

Selling price $46 $90 $158

Maximum demand for each product is 1,000 units, however supplies of wood are limited to 30,000 m2 and the labour force will only work 6,000 hours.

To maximise its profits, the company should produce:

A 1,000 chairs

B 1,000 chairs and 1,000 tables

C 1,000 cupboards

D 333 chairs, 333 tables, 333 cupboards (2 marks)

11 A company uses a predetermined overhead absorption rate based on machine hours. The budgeted factory overhead for one year was $68,000, but the actual overhead incurred was $72,000. In the period, 17,500 machine hours were worked and overheads were over-absorbed by $2,375.

The budgeted level of machine hours was:

A 16,530

B 16,000

C 17,090

D 16,520 (2 marks)

12 If ∑x = 440, ∑y = 330, ∑x2 = 17,986, ∑y2 = 10,366, ∑xy =13,467 and n = 11.

The value of r, the co-efficient of correlation, to two decimal places, is:

(2 marks)

ACCA F2 MANAGEMENT ACCOUNTING

8 KAPLAN PUBLISHING

13 A product requires 3 kilos of raw material per unit. The standard cost of each kilo is $2. During the last period, 5,000 units were produced, 16,000 kilos were purchased and used costing a total of $30,400.

The materials price and usage variances were:

Price Usage

A $1,600 F $2,000 A

B $1,600 A $2,000 F

C $65,600 F $84,000 A

D $65,500 A $84,000 F (2 marks)

14 When accounting for the outputs of a chemical manufacturing process, costs incurred in the process are shared between the main product and its by-products.

The above statement is:

A True

B False (1 mark)

15 Jones Inc is considering undertaking a project requiring 350 skilled labour hours. Jones Inc have a workforce of 25 skilled workers who are currently not fully employed. They are on annual contracts and the number of spare hours currently available for this project is 275. Any hours in excess of this will have to be paid at time and a quarter. The normal hourly rate is $25.

The relevant cost of skilled labour in the contract is:

A $1,875.00

B $2,343.75

C $8,593.75

D $8,750.00 (2 marks)

16 Depreciation of equipment is usually classified in the cost accounts as a:

A production overhead

B administration overhead

C direct expense

D selling overhead (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 9

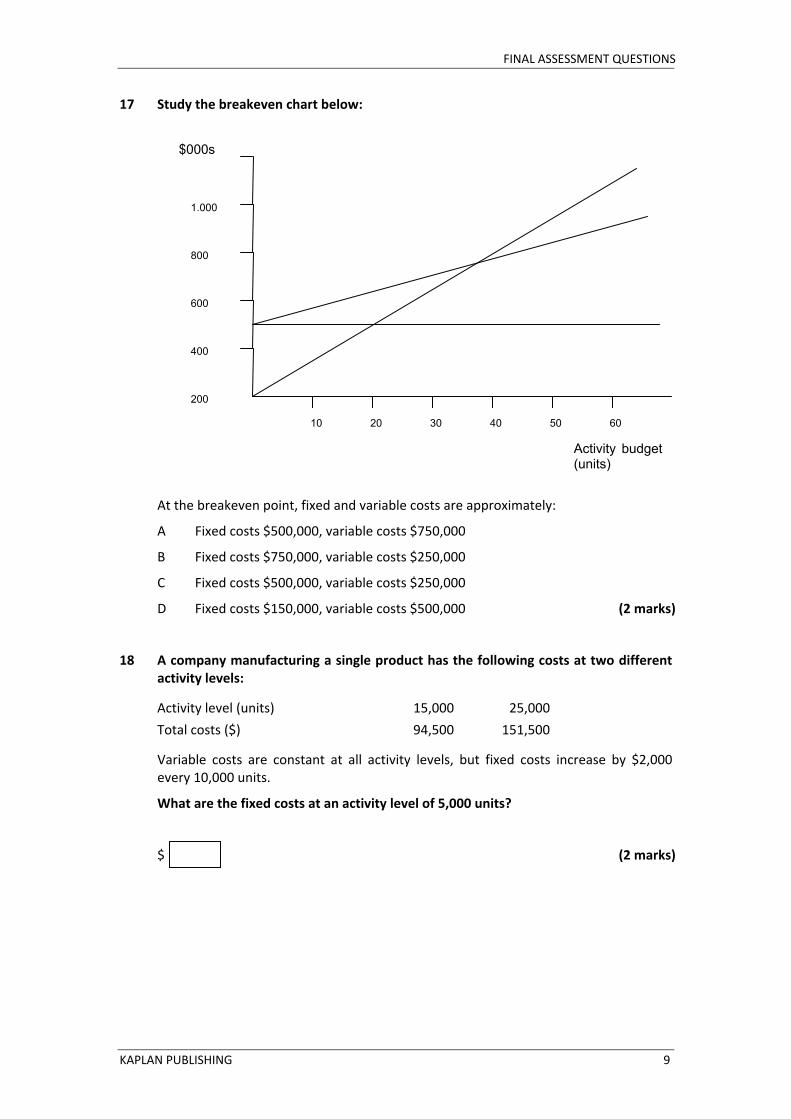

17 Study the breakeven chart below:

At the breakeven point, fixed and variable costs are approximately:

A Fixed costs $500,000, variable costs $750,000

B Fixed costs $750,000, variable costs $250,000

C Fixed costs $500,000, variable costs $250,000

D Fixed costs $150,000, variable costs $500,000 (2 marks)

18 A company manufacturing a single product has the following costs at two different activity levels:

Activity level (units) 15,000 25,000

Total costs ($) 94,500 151,500

Variable costs are constant at all activity levels, but fixed costs increase by $2,000 every 10,000 units.

What are the fixed costs at an activity level of 5,000 units?

$ (2 marks)

10 20 30 40 50 60

400

200

600

800

1,000

$000s

Activity budget (units)

ACCA F2 MANAGEMENT ACCOUNTING

10 KAPLAN PUBLISHING

19 Overheads for maintenance department S1 are apportioned 45%, 40% and 15% among the manufacturing departments M1, M2 and M3.

What will be the overhead apportioned to M2 if the service department’s overheads total $74,425?

A $11,163

B $29,770

C $33,491

D $44,655 (2 marks)

20 A company is trying to decide whether to sell or keep a machine which was purchased four years ago. Which of the following should be ignored in making the decision?

(1) The written down value of the machine

(2) The sale proceeds

(3) The original cost of the machine

A (1) and (2)

B (1) and (3)

C None of the above (1 mark)

21 150 hours of skilled labour are needed for a contract. There is no idle time at the moment and the workers would have to be taken off production of a different product in order to work on the contract. The details of the other product are shown below.

per unit

Selling price $100

Direct materials $12

Direct labour 2.5 hours @ $20/hour

Variable overheads $15

Fixed overheads $17

The skilled workers’ pay rate would not change, regardless of which product they worked on.

The relevant cost of the skilled labour on the contract is:

A $10,950

B $4,380

C $3,900

D $1,380 (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 11

22 When more than one limiting factor (apart from sales demand) constrains the activities of an organisation, the optimal production plan can be found by ranking products in order of contribution per unit of limiting factor.

This statement is:

A True

B False (1 mark)

23 The following data relate to a product manufactured by White Rabbit Inc for the last year:

Actual sales 2,000 units at $450 each

Budgeted output and sales for the year 1,750

Standard selling price $475

Budgeted profit per unit $125

Budgeted contribution per unit $175

The sales volume variance under marginal costing is:

A $31,250 (F)

B $31,250 (A)

C $43,750 (F)

D $50,000 (F) (2 marks)

24 Workwear Inc supplies shirts embroidered with the customer’s logo to a number of large companies. The following information has been estimated for a typical batch of 100 of the most popular cotton shirt:

Design of logo $50

Setting up of embroidery machine 2 hours @ $25 per hour

Shirts $130 for 50

Thread and consumables $20

Embroiderer’s wages 5 hours @ $11 per hour

The marginal cost of sales for a batch of 200 shirts is:

A $750

B $770

C $820

D $870 (2 marks)

ACCA F2 MANAGEMENT ACCOUNTING

12 KAPLAN PUBLISHING

25 Which of the following is most likely to be used as a cost unit for a hospital ward?

A Meals served

B Patient days

C Operations undertaken (1 mark)

26 A paint company has recorded the following information for a process for the last month:

$

Raw materials (350 litres) 4,250

Labour and overheads 2,495

Actual output 325 litres

Normal output is expected to be 95 litres for every 100 litres of raw material.

What is the average cost per unit of completed output?

$ (2 marks)

27 A continuous budget is:

A the budget for the factor which limits the activities of the organisation and on which other budgets are based

B a budget which is designed to change as the volume of activity changes

C a budget which is updated regularly by adding a further accounting period when the first accounting period expires (1 mark)

28 Which of the following statements are true?

(1) The sales volume variance will be higher in marginal costing than in absorption costing.

(2) There is no fixed overhead volume variance in marginal costing

(3) An adverse materials price variance means that the actual cost of the material was more than the standard cost

A (1) and (2)

B (1) and (3)

C (2) and (3)

D All three statements are correct (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 13

29 A company makes three products, Red, Green and Yellow. The following data are available for the next year:

Red Green Yellow

Planned sales (units) 450 375 550

Planned selling price ($) 1.20 0.95 1.35

What is the total sales budget for the next year?

A $896.25

B $1,583.75

C $1,601.25

D $1,638.75 (2 marks)

30 Attainable cost standards are based on efficient operating conditions and include an allowance for fatigue.

This statement is:

A True

B False (1 mark)

31 Process Inc uses process costing to value its product at each stage of production. The following information is available from process 1:

$

Materials $3,750 500 kg

Labour $3,000 100 hours

Overheads $1,125 −

Output − 425 kg

The normal loss is 10% of the inputs and cannot be sold. There is no opening or closing work-in-progress.

What is the value of the output to process 2?

A $6,500.00

B $6,693.75

C $7,437.50

D $7,500.00 (2 marks)

ACCA F2 MANAGEMENT ACCOUNTING

14 KAPLAN PUBLISHING

32 DEF Inc uses standard costing. The fixed overhead capacity variance for the last period is a favourable variance of $435.

The details for the last period are as follows:

Budget

Fixed production overheads ($) 15,950

Budgeted production (units) 550

Standard time to produce unit (hours) 4

Actual

Fixed production overheads ($) 17,545

Units 560

The actual hours worked for the period are:

A 2,055

B 2,123

C 2,140

D 2,260 (2 marks)

33 Calc Ltd wishes to establish a daily sales forecast. The following historic sales data has been gathered over the last 20 days:

Daily sales Number of days

$200 3

$250 6

$300 8

$350 3

What is the expected daily sales to the nearest whole $?

A $1,720

B $278

C $285

D $1,715 (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 15

The following information is to be used for questions 34 and 35:

The following information relates to product Delta which is manufactured by Alpha Beta Inc.

Alpha Beta uses absorption costing.

Extract from cost card:

$ per unit

Direct materials 5.30

Direct labour 5.20

Variable overhead 3.80

Fixed overhead 2.90 _____

17.20 _____

The fixed overhead charged to each unit of the product is based on a monthly production level for product Delta of 1,000 units.

In the last month, actual production was 1,150 units and the costs incurred were as follows:

$

Direct materials 6,250

Direct labour 5,870

Variable overhead 5,230

Fixed overhead 3,230 ______

20,580 ______

34 The flexed budget for direct materials and labour at 1,150 units is:

A Materials $6,095, labour $5,980

B Materials $5,980, labour $6,095

C Materials $7,188, labour $6,751

D Materials $5,300, labour $5,200 (2 marks)

35 The total variance for fixed expenditure and the variable overheads expenditure variance are:

A Fixed overheads $105 (A), variable overheads $860 (F)

B Fixed overheads $105 (F), variable overheads $860 (A)

C Fixed overheads $105 (A), variable overheads $860 (A)

D Fixed overheads $105 (F), variable overheads $860 (F) (2 marks)

36 The coefficient of determination, r2, always falls within the range 0 to 1.

A True B False (1 mark)

ACCA F2 MANAGEMENT ACCOUNTING

16 KAPLAN PUBLISHING

37 In a forecasting model based on y = a + bx, the intercept is £234. If the value of y is £491 and x is 20, then the value of the slope, to two decimal places, is:

A –24.55

B –12.85

C 12.85

D 24.85 (2 marks)

38 Animal Farm Inc manufactures two products, Bull and Cow. The raw material used in the manufacture of these products is Grass. The expected production levels for the products for next year are as follows:

Production (units) Grass – requirements per unit (kg)

Bull 3,000 5

Cow 4,500 6

The expected price of Grass for the next year is $1.50 per kg. The opening inventory is 2,500 kg. The company has a target to halve inventory levels by the end of the year.

The value for next year of the material purchases budget for Grass is:

$ (2 marks)

39 Which of the following is not true of service industries?

A The output should be carefully inspected before being received and accepted

B The standard of the service is variable due to high human input

C The output is intangible (1 mark)

40 An electronics company producing hard drives has a favourable variable overhead efficiency variance. This could be caused by:

A An increase in the cost of electricity

B A change in the quality of supervision

C An increase in the demand for computer components (1 mark)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 17

41 The following graph has been plotted to solve a linear programming to find an optimum production plan.

The area OABCD is:

A the feasible region

B the optimum production plan

C the area of maximum contribution (1 mark)

42 A company is considering a job that requires 500kg of raw material. The material is used within the company for various products. The current inventory is 2,500kg, of which 1,000 kg was purchased at a price of $3 per kg and 1,500 kg was purchased at $3.15 per kg. The current price for new material is $3.50 per kg. What is the relevant cost of material for the job?

A $1,500

B $1,575

C $1,750

D $2,500 (2 marks)

10 20 30 40 50 60

200

0

400

800

1,000

y

X

Labour constraint

Materials constraint

Sales constraint

A B

C

D

ACCA F2 MANAGEMENT ACCOUNTING

18 KAPLAN PUBLISHING

43 Zed Inc makes 2 products, X and Y. The products go through two departments, Assembly and Finishing.

The following has been estimated:

Assembly Finishing

Product X – labour hours 5 2

Product Y – labour hours 7 3

Overheads ($) 250,000 175,000

Production is expected to be 3,000 units of X and 5,000 of Y

Calculate overhead absorption rates for the two departments.

A Assembly = $8.33 per hour, Finishing = $5 per hour

B Assembly = $5 per hour, Finishing = $8.33 per hour

C Assembly = $11.90 per hour, Finishing = $3.50 per hour

D Assembly = $3.50 per hour, Finishing = $11.90 per hour (2 marks)

44 The following data relate to RP Ltd’s production process:

Opening work in process Nil

Goods completed in the period 19,000

Closing work in process 4,000

The closing work in process was 100% complete with respect to materials, but only 70% complete with respect to conversion cost. The conversion cost for the period was $118,810.

Therefore the conversion cost per equivalent unit was:

A $5.50

B $5.00

C $5.21

D $5.45 (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 19

45 Gold Ltd makes two products: A and B. Both products require two production processes which are carried out in two separate production departments. In each of the two production departments, the labour available for the forthcoming period is 200 hours.

Information about A and B is as follows:

A B

Contribution per unit $50 $30

Labour required, department 1 2 hours 0.5 hours

Labour required, department 2 1 hour 0.8 hours

Maximum demand for the period 100 units 100 units

To maximise contribution, which production plan should be followed?

Units of A produced Units of B produced

A 75 100

B 100 100

C 37 50

D 50 50 (2 marks)

46 Subwoofer Ltd can either make or buy component Q. The purchase cost is $28.75. If the company makes the component, it will incur the following costs per unit:

$

Materials 3.75

Labour 7.50

Variable overheads 12.50

Fixed overheads 8.75 ____

32.50 ____

Which of the following is true?

A If the fixed costs have to be paid anyway, the company should buy the component

B If the fixed costs have to be paid anyway, the company should make the component

C If the fixed costs are a relevant cost, the company should still make the component

D None of the above is true (2 marks)

ACCA F2 MANAGEMENT ACCOUNTING

20 KAPLAN PUBLISHING

47 Epsilon Inc manufactures two products, Theta and Omega. Data relating to the next year are given below:

The expected production levels for the products for next year and labour hours are as follows:

Production (units) Direct labour hours (per unit)

Theta 300 15

Omega 450 20

The standard rate for labour hours is $8.50 per hour.

The value of the direct labour budget for the next year is:

A $13,500

B $70,125

C $114,750

D $127,500 (2 marks)

48 In a period, there was a favourable variable overhead efficiency variance of $6,750. The standard variable overhead absorption rate per hour was $3 and 15 hours were allowed for each unit as standard. The actual hours worked were 21,750. The number of units actually produced was:

A 150

B 1,300

C 1,450

D 1,600 (2 marks)

49 The following is a graph of cost against volume of output:

To which of the following costs does the graph correspond?

A Electricity bills made up of a standing charge and a variable charge

B Bonus payments to employees when production reaches a certain level

C Sales commission payable per unit up to a maximum amount of commission

D Bulk discounts on purchases, the discount being given on all units purchased (2 marks)

FINAL ASSESSMENT QUESTIONS

KAPLAN PUBLISHING 21

50 The following information relates to Job 1234, which is being carried out by XY Limited to meet a customer’s order.

Department A Department B

Direct materials consumed $10,000 $6,000

Direct labour hours 800 hours 400 hours

Direct labour rate per hour $4 $5

Production overhead per direct labour hour $4 $4

Administration and other overheads 20% of full production cost

What is the cost to the customer for Job 1234?

A $20,800

B $26,000

C $30,720

D $31,200 (2 marks)

(Total: 90 marks)

ACCA F2 MANAGEMENT ACCOUNTING

22 KAPLAN PUBLISHING