vat training module

TRANSCRIPT

ZCTA ZIMBABWE ADVAVCED TAXATION

VALUE ADDED TAX

STUDY GUIDE

1

Index

Part Topic Page

Self assessment

1 History & background to VAT2 Interpretation of law3 Outline of VAT in Zimbabwe4 Definitions/ Interpretation5 Registration6 Tax periods7 Accounting basis for VAT8 Deemed supplies9 Time of supply10 Value of supply11 Zero rated supplies12 Exempt supplies13 Importation of goods14 Imported services15 Input tax16 Calculation of VAT payable17 Tax invoices18 Credit and debit notes19 Record keeping20 Refunds21 Penalties and interest22 Assessments23 Objections & appeals24 Offences and penalties

2

1. HISTORY & BACKGROUND TO VAT

1.1WHAT IS VAT?

Value Added Tax (more commonly known by its abbreviation VAT) is an indirect tax levied on the supply of goods or services.

It is also levied on the importation of goods and, under some circumstances, on the importation of services.

It is levied and accounted for at the prescribed rates and is borne by the final consumers of goods and services. For some goods and services a special zero rate of 0% is applied, while a limited range of goods and services are exempted from the tax. Because the tax is borne by the final consumer, it can be called a consumption tax as the amount of tax you pay is directly related to the purchases you make.

The Zimbabwe Revenue Authority is responsible for the administration of the VAT system.

1.2 INDIRECT VS. DIRECT TAXATION

Indirect tax is levied on transactions rather than on persons. Value-added Tax, being a consumption tax is an example of an indirect tax. This tax is recovered when transactions relating to goods and services are entered into.

Direct tax is levied on persons as defined in the Act, based on their ability to pay and the level of income. An indirect tax does not rely on these criteria.

Everyone pays VAT at the same rate irrespective of the level of income. Naturally, persons with higher income will have more money to spend and consequently they will spend more on tax than another person with limited disposable income.

3

.1.3 GENERAL OPERATIONAL ASPECTS OF VAT - Section 6

Value-added tax is levied under the Value-added Ax Act. The tax is not charged on commodities as such, but rather on the supply of commodities and is imposed at the prescribed rates on the following: -

The supply of any goods and services in Zimbabwe by a registered operator in the course of furtherance of an enterprise (trade).

Goods imported into Zimbabwe in certain circumstances, and Services imported into Zimbabwe in certain circumstances.

The Zimbabwe Government chose to introduce a destination type VAT i.e. the tax will be levied in the country where the goods or services are consumed. Therefore, VAT is payable on imports of goods (whether or not the importer is a registered operator), and certain services for the domestic market.

Importers who are registered operators are entitled to claim credit for tax paid on imports in the same manner as for tax invoiced to them on domestic supplies. Direct exports of goods from Zimbabwe to other countries pay VAT at a special rate known as the zero (0%) and therefore do not effectively pay any tax on such supplies. This is a fundamental principle of a value-added tax system.

Exporters who are registered operators will be entitled to claim an input tax credit for supplies invoiced to them (or paid on importation), in respect of the inputs acquired for their export sales. Certain other goods and services which are either difficult to tax, or, which are politically sensitive are also subject to the zero rate (e.g. certain basic foodstuffs) or are exempted such as financial services and passenger transport.

As previously mentioned, a supply must occur before VAT may be charged. It is therefore imperative to determine the nature, time, and value of the supply. The tax element of most goods and services supplied will be determined by applying the tax fraction, which is expressed as follows: -

Tax Fraction r

100 + r

Where r = the rate (percentage) of tax chargeable

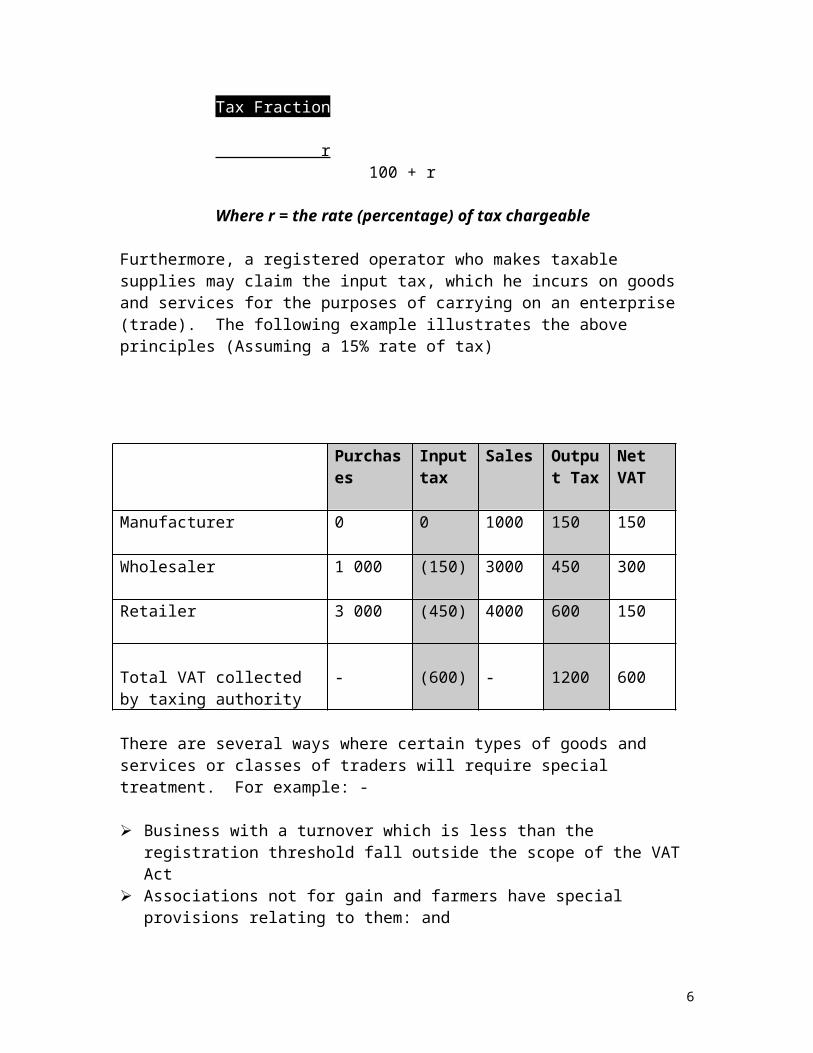

Furthermore, a registered operator who makes taxable supplies may claim the input tax, which he incurs on goods and services for the purposes of carrying on an enterprise

4

(trade). The following example illustrates the above principles (Assuming a 15% rate of tax)

Purchases Input tax

Sales Output Tax

Net VAT

Manufacturer 0 0 1000 150 150

Wholesaler 1 000 (150) 3000 450 300

Retailer 3 000 (450) 4000 600 150

Total VAT collected by taxing authority

- (600) - 1200 600

There are several ways where certain types of goods and services or classes of traders will require special treatment. For example: -

Business with a turnover which is less than the registration threshold fall outside the scope of the VAT Act

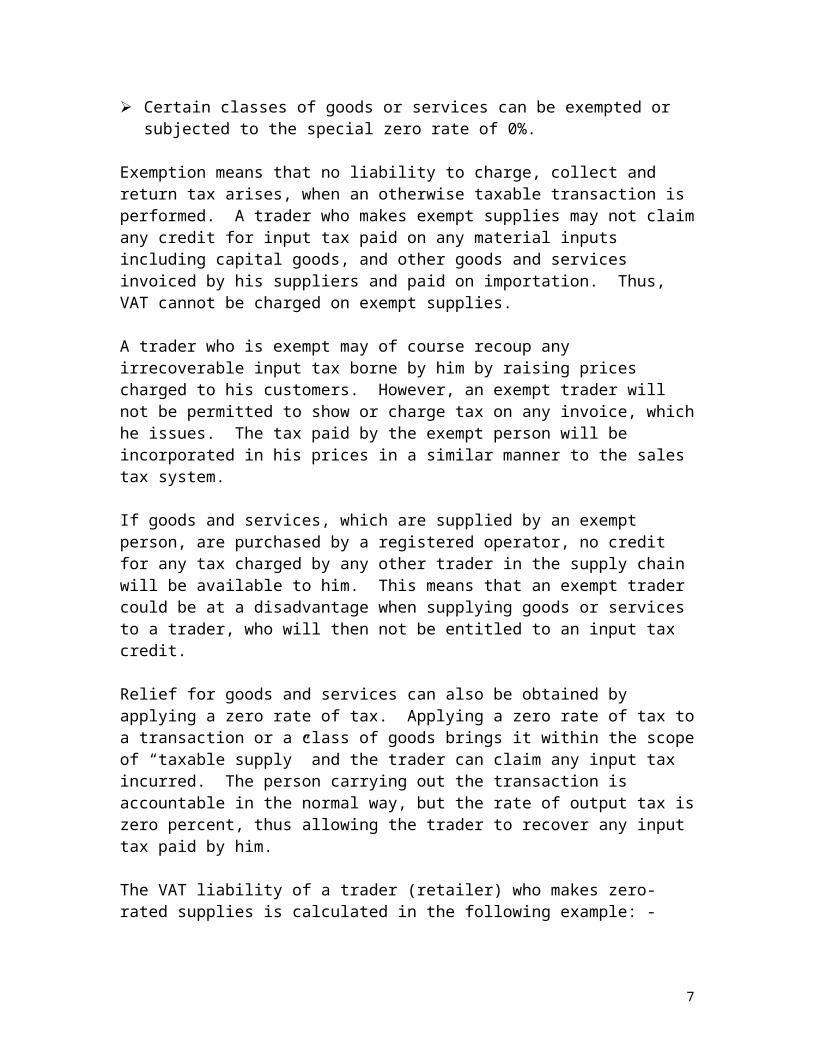

Associations not for gain and farmers have special provisions relating to them: and Certain classes of goods or services can be exempted or subjected to the special zero

rate of 0%.

Exemption means that no liability to charge, collect and return tax arises, when an otherwise taxable transaction is performed. A trader who makes exempt supplies may not claim any credit for input tax paid on any material inputs including capital goods, and other goods and services invoiced by his suppliers and paid on importation. Thus, VAT cannot be charged on exempt supplies.

A trader who is exempt may of course recoup any irrecoverable input tax borne by him by raising prices charged to his customers. However, an exempt trader will not be permitted to show or charge tax on any invoice, which he issues. The tax paid by the exempt person will be incorporated in his prices in a similar manner to the sales tax system.

If goods and services, which are supplied by an exempt person, are purchased by a registered operator, no credit for any tax charged by any other trader in the supply chain will be available to him. This means that an exempt trader could be at a disadvantage when supplying goods or services to a trader, who will then not be entitled to an input tax credit.

5

Relief for goods and services can also be obtained by applying a zero rate of tax. Applying a zero rate of tax to a transaction or a class of goods brings it within the scope of “taxable supply” and the trader can claim any input tax incurred. The person carrying out the transaction is accountable in the normal way, but the rate of output tax is zero percent, thus allowing the trader to recover any input tax paid by him.

The VAT liability of a trader (retailer) who makes zero-rated supplies is calculated in the following example: -

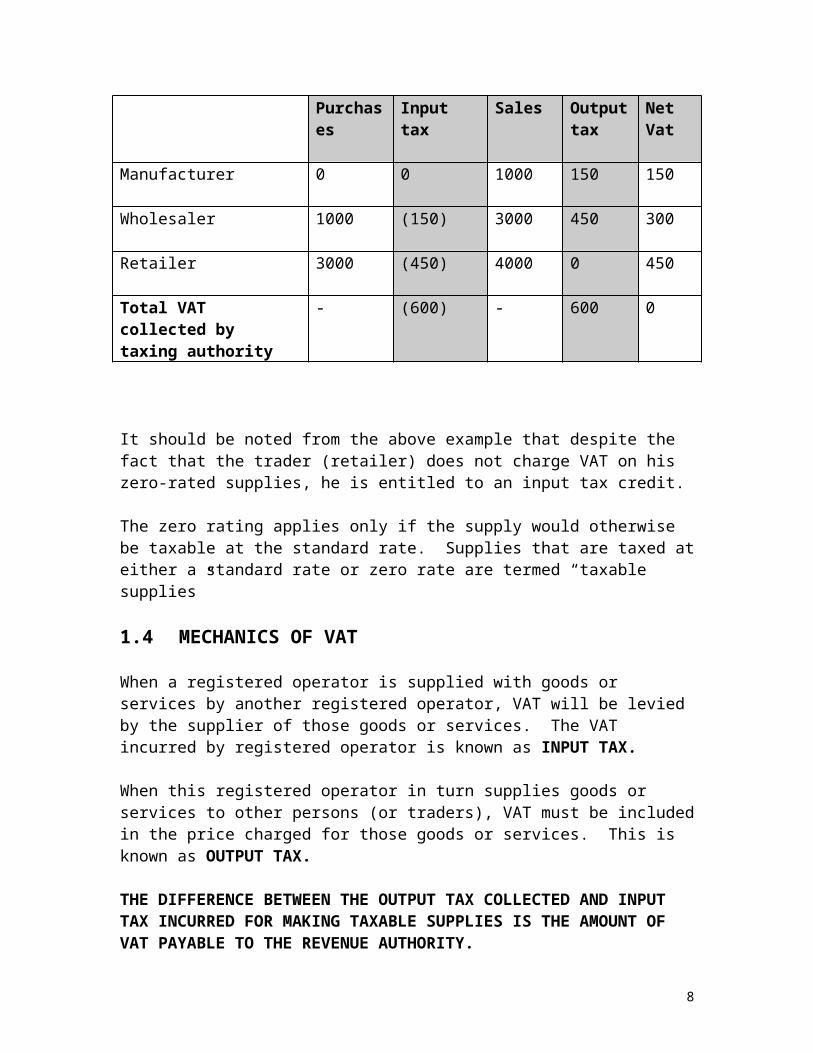

Purchases Input tax Sales Output tax

Net Vat

Manufacturer 0 0 1000 150 150

Wholesaler 1000 (150) 3000 450 300

Retailer 3000 (450) 4000 0 450

Total VAT collected by taxing authority

- (600) - 600 0

It should be noted from the above example that despite the fact that the trader (retailer) does not charge VAT on his zero-rated supplies, he is entitled to an input tax credit.

The zero rating applies only if the supply would otherwise be taxable at the standard rate. Supplies that are taxed at either a standard rate or zero rate are termed “taxable supplies”

1.4 MECHANICS OF VAT

When a registered operator is supplied with goods or services by another registered operator, VAT will be levied by the supplier of those goods or services. The VAT incurred by registered operator is known as INPUT TAX.

When this registered operator in turn supplies goods or services to other persons (or traders), VAT must be included in the price charged for those goods or services. This is known as OUTPUT TAX.

THE DIFFERENCE BETWEEN THE OUTPUT TAX COLLECTED AND INPUT TAX INCURRED FOR MAKING TAXABLE SUPPLIES IS THE AMOUNT OF VAT PAYABLE TO THE REVENUE AUTHORITY.

WHERE INPUT TAX EXCEEDS OUTPUT TAX A REFUND WILL BE MADE.

6

1.5 THE VAT REGISTRATION NUMBER

All registered operators are issued with a VAT Registration number, which should be recorded on all tax documents. The registration number will be computer generated.

2. INTERPRETATION OF LAW

2.1 INTENTION OF THE LEGISLATURE

A study of tax cases shows that in the interpretation of a taxation statute, the intention of the legislature is sought. The courts are not prepared to depart from a literal interpretation where there is doubt as to the legislature’s intention, but where the intention is clear the courts will give effect to that intention, as is the case of all other Acts.

2.2 CONTRA FISCUM RULE

Should a provision of a taxing statute be ambiguous, the contra fiscum principle must be applied. In other words, where a section of the act is reasonably capable of two constructions, the court must allow the lesser imposition, or give the taxpayer charged the benefit of the doubt.

This rule has often been applied by our courts. The judgement of Milner J in the Badnehorst case should also be noted in this respect:

“Where there is an ambiguity which is manifest without resorting to considerations of inequity, supposed or real, the court will, no doubt, interpret a taxing statute, as it did with others favorably to the subject and so, contra fiscum”

2.3 DEFINITIONS OF WORDS

Like most Zimbabwe statutes, the VAT Act contains a general interpretation section, where the meanings that certain words and phrases are intended to bear for the purposes of the Act are to be found.

The definitions contained are therefore of particular importance. As in all such interpretation sections, it is expressly provided that the meaning attributed to particular

7

words and phrases must be those given in the definition section unless the context otherwise indicates. Thus, the meaning given to the word or phrase in the definition section

In determining whether or not the context otherwise indicates, the whole of the Act must be considered, since other parts thereof may shed light upon the intention of the legislature and may serve to show that the particular provision ought not to be construed as it would be if considered alone and apart from the rest of the Act.

2.4 “MEANS” AND “INCLUDES”

The definition in the VAT Act often provides that a word or phrase “means” something. In other cases it is stated that a word or phrase “includes” something, and in other cases, it is stated that a word or phrase “means and includes”

Generally, when a definition states that a word or phrase “means” something, such definition is exhaustive and the word or phrase can have no other meaning than that which appears in the definition. However, this is always subject to the proviso that a contrary intention may appear in the statute.

On the other hand, the word ‘includes’ is normally used to enlarge the meaning of words or phrases occurring in a statute, but in some cases it may also be exhaustive and be equivalent to “means and includes”

2.5 “NOTWITHSTANDING ANYTHING…”

When the words “notwithstanding anything contained in this Act” appears in a section or subsection of statute, the effect thereof is that such section or subsection must be interpreted as if the rest of the Act is excluded.

In some cases the words may be in a subsection “notwithstanding anything in this section contained”, and in such case the effect is that the subsection must be considered as if the rest of the section were excluded. In addition, the word “notwithstanding” has been held to mean “even if”

2.6 “SHALL” AND “MAY”

The word “shall” is normally used as being equivalent to “must”. In other words it is imperative or peremptory, while the word “may” is usually used in a permissive sense. In general, in the more modern statures, the word “shall” is used to create a duty. Where,

8

however, the expression “it shall be lawful” appears in a stature, it usually confers a discretionary power.

On the other hand the word “may “ is sometimes construed as imperative, or in other words “may” can be equivalent to “must”. However, in the absence of proof that the legislature intended that the word “may” is to be interpreted as “must”, such word is given its natural meaning, that is a permissive and not an obligatory use.

2.7“AND” AND “OR”

It is important to take note of the words at the end of (and sometimes within the same) sentences, which indicate several criteria or conditions, which need to be evident before a particular section (or part thereof) can be applied in any situation. When using “and” this normally indicates a link between several conditions, all of which need to be evident. When using “or” this indicates an option between two or more conditions, where, if either one is evident, the law will or can apply.

Pay special attention to sections of the Act which have a combination of “and” and “or” linking conditions, as these sections will be more difficult to interpret.

9

3. OUTLINE OF VAT IN ZIMBABWE

Value-added tax brings within its scope the widest range of goods and services supplied by registered operators in Zimbabwe. Value-added tax is collected at each stage in the production and distribution chain. The liability to charge VAT will arise every time a transaction (supply) is carried out by registered operators and will not depend on the profitability or outcome of the transaction, as VAT is not a tax on business profits or turnover. The tax invoice to a registered operator is deducted from the tax charged and invoiced by the supplier (registered operator) to arrive at the net tax liability.

Although VAT will be the legal liability of the registered operator, it will ultimately be passed onto the final consumer. This is because each time a registered operator invoices a customer, the registered operator has claimed a credit for the VAT previously invoiced to him. The VAT paid is deducted from the amount of tax charged and the registered operator is liable only for the difference between his output and his input tax. The effect of this crediting mechanism is that the tax rolls forward at each intermediate transaction until the point of sale to the final consumer. The following example serves to illustrate the credit offset mechanism, which is fundamental to the operation of VAT.

10

Transaction Amount VAT

11

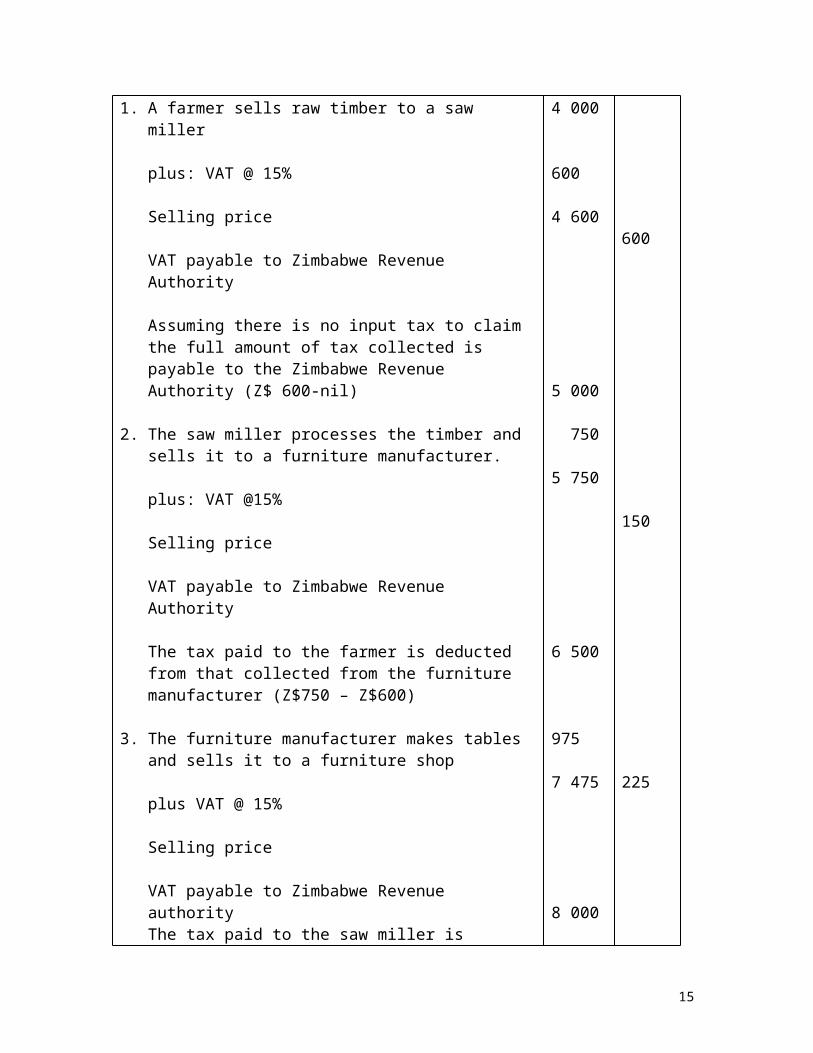

1. A farmer sells raw timber to a saw miller

plus: VAT @ 15%

Selling price

VAT payable to Zimbabwe Revenue Authority

Assuming there is no input tax to claim the full amount of tax collected is payable to the Zimbabwe Revenue Authority (Z$ 600-nil)

2. The saw miller processes the timber and sells it to a furniture manufacturer.

plus: VAT @15%

Selling price

VAT payable to Zimbabwe Revenue Authority

The tax paid to the farmer is deducted from that collected from the furniture manufacturer (Z$750 – Z$600)

3. The furniture manufacturer makes tables and sells it to a furniture shop

plus VAT @ 15%

Selling price

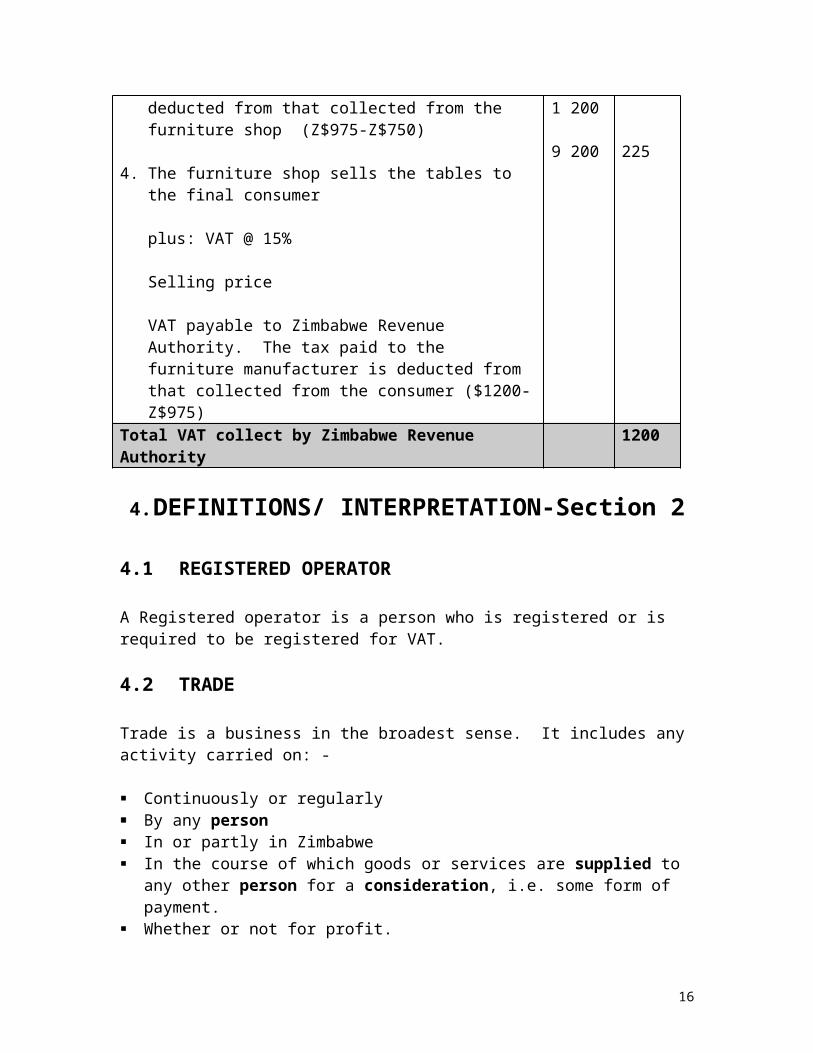

VAT payable to Zimbabwe Revenue authorityThe tax paid to the saw miller is deducted from that collected from the furniture shop (Z$975-Z$750)

4. The furniture shop sells the tables to the final consumer

plus: VAT @ 15%

Selling price

VAT payable to Zimbabwe Revenue Authority. The tax paid to the furniture manufacturer is deducted from that collected from the consumer ($1200-Z$975)

4 000

600

4 600

5 000

750

5 750

6 500

975

7 475

8 000

1 200

9 200

600

150

225

225

Total VAT collect by Zimbabwe Revenue Authority 1200

12

4. DEFINITIONS/ INTERPRETATION-Section 2

4.1 REGISTERED OPERATOR

A Registered operator is a person who is registered or is required to be registered for VAT.

4.2 TRADE

Trade is a business in the broadest sense. It includes any activity carried on: -

Continuously or regularly By any person In or partly in Zimbabwe In the course of which goods or services are supplied to any other person for a

consideration, i.e. some form of payment. Whether or not for profit.

It therefore includes

Business transactions to start or close down business Ordinary businesses-manufacturers, traders, auctioneers, lessors, contractors etc Trades and professions – builders, electricians, plumbers, doctors, lawyers,

accountants, etc Non profit organizations- sporting/ social clubs, charitable organizations

As well as the following special inclusions: -

Public authorities – government departments, provincial authorities Local authorities Charitable organizations

A number of activities are excluded from the definition of “trade”, namely: -

Services rendered by an employee (who earns remuneration) to his employer or by the holder of any office in performing the duties of office, e.g. salary/wage earners or a company director. A private independent contractor does not fall within this exclusion.

The supply of goods or services by a concern from a branch or main business which is permanently located at premises outside Zimbabwe if the branch or main business can be separately identified and maintains its won system of accounting.

Private or recreational pursuits or hobbies (unless structured like a business) Private occasional transactions, e.g. occasional sale of domestic/household goods,

personal effects or private motor vehicle Any activities to the extent that they are of exempt supplies.

13

The definition of trade is one of the most important definitions in the VAT Act and every person who is required to register or who applies for voluntary registration must meet the criteria in the definition.

4.3 PERSON

The term “person” includes: -

Sole proprietor, i.e. an individual carrying on business in his own name or under a trade name

A company A partnership or joint venture A deceased estate or insolvent estate Trusts Incorporated body of persons e.g. an entity established under its own enabling act of

parliament Unincorporated body of persons, e.g. club, society or association with its own

constitution. Local and public authorities

4.4 SUPPLY

The definition is very wide and includes all forms of supply irrespective of where the supply is effected, (even including things that happen by law e.g. expropriation) and any derivative of supply shall be construed accordingly

4.5 CONSIDERATION

This term refers to that which is given in return to the supplier as payment for the supply. Normally the consideration is in money but it also includes barter transactions where other goods are given or services rendered to the supplier as payment. Any act of forbearance whether voluntary or not for the inducement of a supply of goods or services will constitute consideration, but it does not include any donation made as an unconditional gift to an association not for gain. Also excluded is a “deposit” which is lodged to secure a future supply of goods or services. However, a “deposit” paid on a returnable container does constitute consideration

14

4.6. GOODS

The term “goods “includes

Corporeal (tangible) movable things, goods in the ordinary sense Any real right in those corporeal movable things Fixed property, land & buildings Any real right in such fixed property e.g. servitudes, mineral rights, notarial leases

e.t.c. Sectional title units (inc. timeshare)- get title deeds to a share of flats Shares in a share block company- no title deeds but you own shares Postage stamps

The term “goods” excludes: -

Money i.e. notes, coins, cheques, bills of exchange e.t.c. (Except when sold as a collectors item)

Value cards, revenue stamps etc which are used to pay taxes (except when sold as a collectors item)

Any right under a mortgage bond Farm land

4.7 SERVICES

Services means anything done or to be done.

The term “services” includes: - Granting, assignment, cession, surrender of any right Making available of any facility or advantage Certain acts which are deemed to be services i.t.o. Section 7

The term “services “excludes

A supply of “goods” Money Any stamp, form or card which falls into the definition of goods

Examples of services: -

Commercial services- electricians, plumbers, builders Professional services- doctors, accountants, lawyers Advertising agencies Intellectual property rights- patents, trade marks, copy rights, know-how

15

Personal right- restraints of trade Provision of cover under an insurance contract.

4.8 COMMERCIAL RENTAL ESTABLISHMENT

There are four distinct classes of commercial rental establishments

Hotels, motels, inns, boarding houses, hostels or similar establishments where lodging is normally provided to five or more persons at a daily, weekly, monthly or other periodic charge.

Accommodation units such as houses, flats apartments, rooms e.t.c. which are let or normally held for letting in the normal course of a business undertaking conforming to certain requirements. To qualify under this class, the person must let the units regularly for continuous periods not exceeding 45 days and the receipts from that letting must be at least the amount specified by the Ministry per annum for each unit. This applies where the person has less than five houses, flats apartments, rooms, etc

A house, flat, apartment room etc which constitutes an asset (including a leased asset) of an undertaking which does not form part of a hotel, motel, boarding house, etc mentioned above which is let or held for letting for continuous periods not exceeding 45 days and the total receipts from such letting at least an amount as prescribed by the Minister per annum. This applies where the person has 5 or more houses, flats apartments, rooms, etc.

4.9 CONNECTED PERSON

There are six different relationships between different persons incorporated in the definition of connected person in the VAT Act. The term is important because if two persons are connected in terms of the definition, it may be necessary to apply a special value of supply rule which will force the supplier to charge VAT on the open market value of the supply, rather than on the amount of consideration received.

Examples of connected persons: -

A company and it’s Directors Parents and their children A Trust and a beneficiary of that Trust Separately registered branches of a registered operator.

4.10 INPUT TAX

This is the tax paid by the recipient of the supply of any goods or services to the supplier. Input tax may be deducted by the recipient where the supply of such goods and/or services are acquired by a registered operator for the purposes of making taxable supplies in the following circumstances: -

16

Where the supplier (being a registered operator) has charged tax on the supply and has provided the recipient with a tax invoice as required.

Where the importer (being a registered operator) has paid VAT on the importation of goods or services and is in possession of a bill of entry as required.

Where second-hand goods have been purchased from a non-registered operator, and the recipient has paid for the supply and has kept the necessary details of the supplier and the transaction in terms of the prescribed documentary requirements. This is sometimes called a “notional input” and is calculated by multiplying the tax fraction (15/115) by the amount paid. There are special rules where the second-hand goods constitute fixed property. In this case the input tax is limited to the stamp duty. If 6% stamp has been paid on the fixed property (from a non-registered operator) notional input tax is limited to the stamp duty paid. It is not the notional VAT that should be granted.

Where goods are repossessed from a debtor (non-registered operator) by the supplier of goods under an installment credit agreement (e.g. a bank). This is calculated by multiplying the tax fraction at the time the supply was originally made by the balance of the cash value still owing to the supplier.

Where goods or services were acquired only partly for taxable supplies and partly for some other purpose, a fair and reasonable portion may be claimed. Furthermore, the amount of input tax claimable in any tax period will depend on whether the registered operator is registered on the invoice or the payments basis.

4.11 INSTALMENT CREDIT AGREEMENT

An agreement for the supply of goods under an instalment sale or financial lease which are normally subject to some suspensive condition as to the passing of ownership. These may be referred to as “hire purchase” agreements. The agreement will normally provide for the payment of the purchase price including finance charges at a fixed or determinable instalment and the recipient accepts the risks attached to those goods insofar as loss or damage are concerned. In the case of a financial lease the term of the agreement must be at least 12 months. This type of agreement must be distinguished from a rental agreement where the recipient does not become the owner of the goods at any stage.

4.12 OUTPUT TAX

This is the tax charged by a registered operator on a supply of goods or services.

17

4.13 SECOND –HAND GOODS

These are goods, which have been previously owned and used (excludes animals and certain gold coins)

4.14 TAXABLE SUPPLY

A supply (including a zero rated supply), which is chargeable with tax under the VAT Act.

4.15 FARM LAND

This is land, which is used for agricultural and pastoral activities

The term excludes:

Communal land i.t.o. Section 3 of the Communal Land Act Land, which is in a municipal town or local government area as defined in the Urban

Councils Act. A town ward of a rural district that has been declared a specified area i.t.o. the Rural

Districts Councils Act Land in the area of any township as defined in the Land Survey Act, and State land, the layout of which has been approved i.t.o. Section 43 of the Regional,

Town and Country Planning Act Chapter 29:1.

14.16 FIXED PROPERTY

Means land, together with improvements affixed thereto, any share in a company, which confers a right to, or an interest in the use of immovable property. It does not include farmland.

18

5 REGISTRATION- Section 23

5.1 INTRODUCTION

Any person who

Carries on or intends to carry on any trade (s) and Whose taxable value of supplies exceed the prescribed limit and In the course of which taxable supplies (includes zero-rated supplies) are made, must

register for VAT

NOTEIt is the person not the trade, who is registered for VAT. A person is only registered once for all the trades/divisions/branches carried on, unless permission is granted to register them separately.

5.2 LIABILITY FOR REGISTRATION

A person is liable to register if: - At the end of any month the total value of supplies of goods or services (turnover) has

exceeded the prescribed amount in the preceding period of 12 months, or There are reasonable grounds for believing that the total value of supplies of goods

and services, which will be made in the following 12 months, will exceed the prescribed amount.

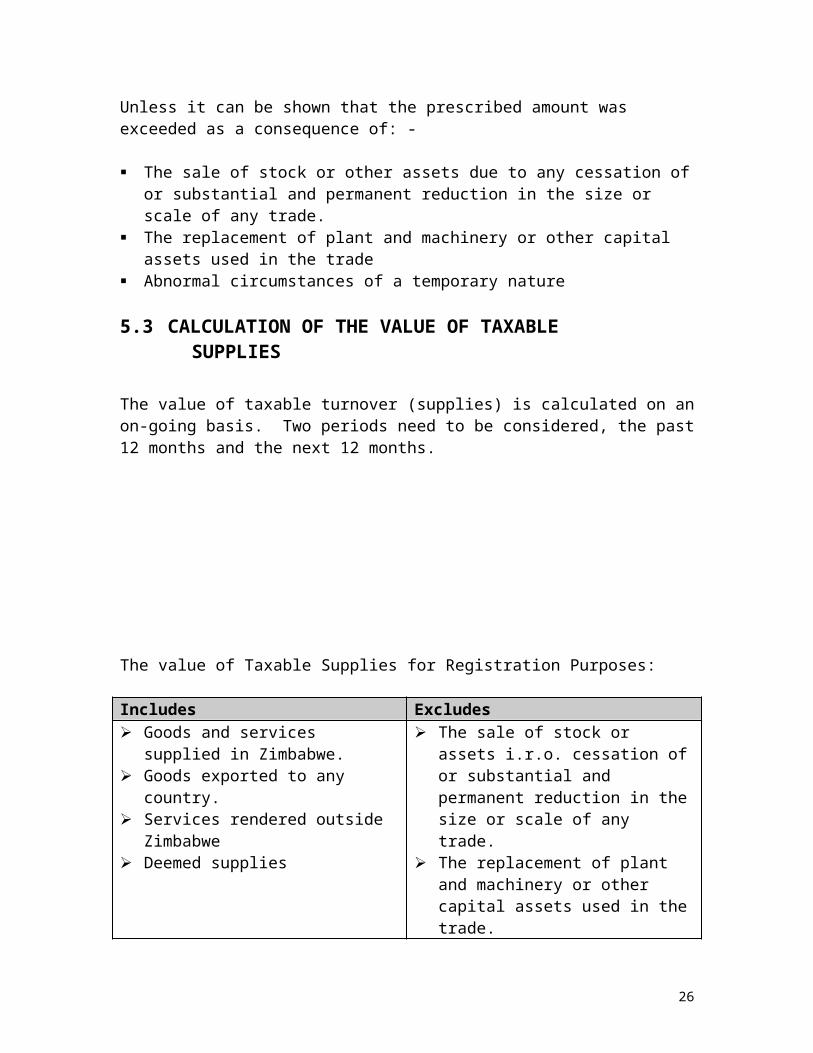

Unless it can be shown that the prescribed amount was exceeded as a consequence of: -

The sale of stock or other assets due to any cessation of or substantial and permanent reduction in the size or scale of any trade.

The replacement of plant and machinery or other capital assets used in the trade Abnormal circumstances of a temporary nature

5.3 CALCULATION OF THE VALUE OF TAXABLE SUPPLIES

19

The value of taxable turnover (supplies) is calculated on an on-going basis. Two periods need to be considered, the past 12 months and the next 12 months.

The value of Taxable Supplies for Registration Purposes:

Includes Excludes Goods and services supplied in

Zimbabwe. Goods exported to any country. Services rendered outside Zimbabwe Deemed supplies

The sale of stock or assets i.r.o. cessation of or substantial and permanent reduction in the size or scale of any trade.

The replacement of plant and machinery or other capital assets used in the trade.

Exempt supplies. Unconditional gifts received by

associations not for gain and charitable orgnisations

VAT

5.4 VOLUNTARY REGISTRATION

A person can apply for voluntary registration even if the total value of taxable supplies is less than the prescribed amount per annum. As a general rule of thumb, it will be advantageous for a person to register if they supply goods or services mainly to other registered operators. The person must satisfy the Commissioner that they are carrying on trade.

5.5 REGISTRATION PROCEDURE

Application for compulsory and voluntary registration must be made on the prescribed registration form together with any other documents, which the Commissioner may require from time to time (i.e.. company registration particulars, bank details, etc) For compulsory registration, this must be completed not later than 30 days from the date of liability.

5.6 REFUSAL TO VOLUNTARILY REGISTER A PERSON

20

The Commissioner may refuse to register a person for voluntary registration if any one of the following criteria are not met: -

Has no fixed place of abode or business Does not keep proper accounting records Has not opened a banking account Has previously been registered as a registered operator under VAT or i.t.o. the

repealed Act (Sales Tax) and failed to perform his duties under either Act.

Such refusal must be given to the applicant in writing.

5.7 SEPARATE REGISTRATION

A registered operator may register separately any trades, branches or divisions carried on by him for VAT purposes. This means that it is possible for a registered operator to have more than one VAT registration number if he carries on his trade in branches or divisions.

It is important to note that if a person who operates several trades or who operates any trade in branches or divisions (other than an association not for gain) cannot avoid the liability to register for VAT by considering the turnover of each branch or division individually. In such cases, the turnover of all his trades/divisions/branches must be aggregated to determine the total value of the supplies.

There are two conditions under which separate registration can be granted, namely: -

It must maintain an independent system of accounting for each trade/division/branch, and

It must be capable of being separately identified (i.e. nature of the activities or the location)

The implication of separate registration is that each separately registered trade/division/branch is treated as a registered operator in its own right. It will have to: -

Retain the same tax period as the representative branch (except for farmers) and Retain the same accounting basis as the parent body Remain registered until cancelled by the parent body or until the parent body’s

registration is cancelled.

Transfers of taxable goods or services between any separately registered trades/divisions or branches must be accounted for on the prescribed return covering that period. Tax invoices are to be issued to these trades/divisions/branches and each trade/division/branch has to: -

Keep its own accounting records Submit returns and

21

Account for VAT to the Zimbabwe Revenue Authority

A separate application form (as prescribed) must be completed for each such trade/division/branch for which a separate registration is required. The person who applied for separate registration of any trade/division/branch will be held responsible in the event of any default under the VAT Act by such trade/division/branch.

NOTE 1

A subsidiary company cannot be a branch or division of a holding company, even if it carries on business as a branch under the same trading name as it is a separate legal entity. For example if each of Edgars` branches are registered in separate companies, then they do not constitute a “branch” for VAT purposes. However, if all the branches are registered under one company, each of the different stores can be registered as a branch of the Head Office.

NOTE 2

There are special concessions for associations not for gain in that it’s activities can be divided into separate trades/divisions/branches without being aggregated to establish the registration threshold if the association so elects. The effect of this is that one identifiable activity may be registered and another not.

5.8 CANCELLATION OF REGISTRATION- Section 24

A registered operator may be deregistered if: -

If the value of his taxable supplies falls below the registration threshhold He ceases to carry on any trade and will not carry on any trade within 12 months after

that date Where he has applied for registration in anticipation of commencing a trade and has

not commenced that trade. A registered operator has successfully applied for voluntary registration and it

subsequently appears that he has not complied with the requirements.

Cancellation of registration, with the approval of the Zimbabwe Revenue Authority will take effect from the last day of the tax period on which the application is made.

A person who ceases to be registered remains responsible for any duties or obligations under the Act while he was registered.

22

A registered operator’s separately registered trades/division/branches may be cancelled if:

The registered operator being the parent body applies in writing to the Zimbabwe Revenue Authority.

When for any reason, the main (parent body) registration is cancelled. It appears to the Commissioner that the duties under the VAT Act have not been

carried out by the separately registered trades/divisions/branches.

The effect of the cancellation is that all duties under the Vat Act revert to the registered operator (parent body). A separately registered trade/division/branch may become the main branch if it continues to trade after the main branch has deregistered (see notes above)

6. TAX PERIODS – Section 27

6.1 SUBMISSION OR RETURNS & PAYMENTS

All registered operators are required to submit returns and account for VAT to the Zimbabwe Revenue Authority at regular intervals. These intervals are called tax periods.

A registered operator`s first tax period will commence on:

The commencement date of VAT, or The date on which he became a registered operator, if he was not liable or carrying on

any trade at the commencement date of VAT.

A VAT return in the prescribed form must be submitted to the Authority for each tax period. The VAT return must reach the authority on or before the 20th of the month after the end of a tax period, or where such day falls on a public holiday or a weekend, the last business day before that date.

The month in which a registered operator`s tax period ends will be determined by the Zimbabwe Revenue Authority. Tax periods do not all end at the same time for all registered operators.

These are as follows: -

Category A & B =2 months (i.e. every 2 months) Category C=1 month (i.e. monthly) Category D= Any other tax period

The VAT return form is completed to show the taxable supplies made and received as well as any tax adjustments for the period. A return will be sent to each registered

23

operator prior to the end of his tax period. The form (whether there is an amount payable or a refund claimed) is to be completed and returned to the Zimbabwe Revenue Authority within the period allowed.

A special return for sales in execution (i.t.o. Section 7 (1)) to be made within 30 days from date of sale. Such sales to be excluded from ordinary Return.

6.2 TWO-MONTH TAX PERIOD (CATEGORY A OR B)

Most registered operators will be allocated a “standard tax period” of 2 months unless otherwise requested, but such persons can elect to be on Category C (monthly). Registered operators may choose between the 2 categories, but if no choice is elected the Authority will allocate them either category A or B automatically. The tax periods end as follows, subject to the 10 day rule which will be discussed under paragraph 6.6: -

Category A: The last day of: - Jan, May, March, July, Sept & NovemberCategory B: The last day of: - Feb, Apr, June, Aug, Oct & December

6.3 ONE-MONTH TAX PERIOD (CATEGORY C)

Larger enterprises whose taxable supplies exceed amount prescribed will be required to submit returns on a monthly basis.

Other trades such as those who expect regular refunds of VAT (e.g. exporters and charitable organisations) may also, on application, be allowed to adopt a one-month tax period.

Where a person operates more than one trade or a trade in branches or divisions, it is necessary that all the taxable supplies be aggregated to ascertain the total turnover. This applies whether or not the separate trades/divisions/branches are registered as separate registered operators.

The Authority may allocate a one-month tax period to a registered operator who repeatedly defaults in performing his duties as a registered operator.

Any other registered operator may on application in writing also be allocated Category C. The one-month period will be effective from a date determined by the Zimbabwe Revenue Authority.

6.4 ANY OTHER TAX PERIOD (CATEGORY D)

Registered operators will qualify for any other tax period if: -

The registered operator’s trade consists solely of farming activities; or

24

The registered operator whose separately registered trade, branch or division consists sorely of farming activities, provided any other trades, branches or division carried on by that registered operator do not consist of farming activities; and

The total turnover from all farming activities must not exceed the prescribed amount

This tax period is not available to any registered operator who has been allocated a Category C tax period

*Note

Pay attention to the bolded words “and” and “or” and the interpretation thereof.See Chapter 2 of this document for more details

6.5 CHANGE OF TAX PERIODS

The Zimbabwe Revenue Authority may, on application by the registered operator, approve a change of tax period from either one of the two-month tax period to the other (that is from Category A to B, or vice versa) or from Category D to Category A, B, or C. The first return after the change should not include any period for which a return has previously been made. The effect of this is that an irregular period for the return is made for the change over period.

Example 1: Change from Category A to Category B

A registered operator wishes, or is required to change from Category A to Category B. A return is furnished on 25 April for the 2 months ended 31 March. In May the Zimbabwe Revenue Authority advises that the registered operator is allocated Category B with effect from 1 June. He should submit a return for the period:

1 April to 31 May 1 June to 30 June (1 month)

And thereafter for the 2 monthly tax period.

Example 2: Change from Category B to Category A

A farmer with a 2-month tax period submits a return on 18 May for the period 1 March to 30 April and applies to change to a 6-month period ending in November and May. Approval is granted with effect from 1 July. He should submit a return for the period:

25

1 May to 30 June 1 July to 30 November (5 months)

And thereafter for the new 6 months

6.6 THE 10-DAY RULE

Whilst the tax period normally ends on the last day of the month, there is provision for registered operators to adopt a date ending on a day other than the end of the month.

If a registered operator has an accounting cut-off or closing date within 10 days before or after the end of the month in which the tax period ends, the registered operator may use that date as the last day for the tax period. It should be noted that this rule can be used by registered operators to manipulate the accounting for transactions in specific tax periods to their advantage.

Regardless of when the registered operator closes off the tax period, the return must still be submitted by the prescribed dates.

If, a date other than the last day of the month has been used by the registered operator to close off his books, then the next tax period commences on the day immediately thereafter.

26

7. ACCOUNTING BASIS – Section 14

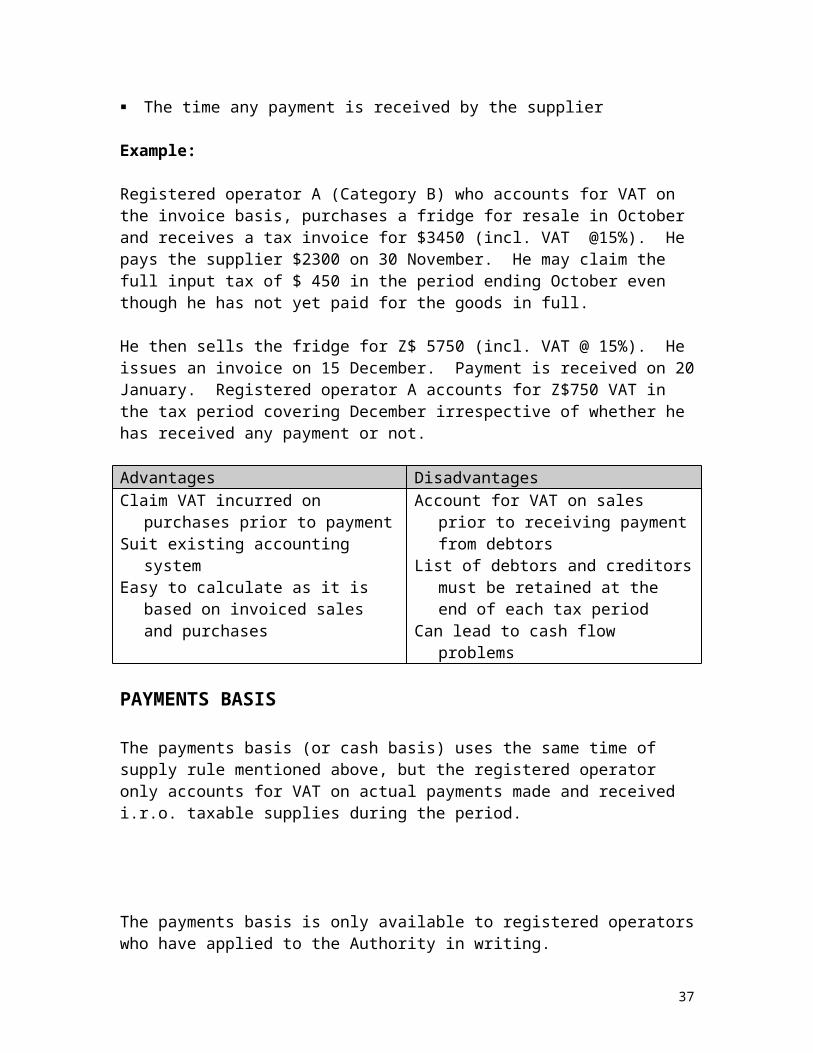

7.1 INVOICE BASIS

The invoice (or accrual) basis of accounting is that registered operators must account for both cash and credit sales and cash and credit purchases. Since VAT is an invoice-based tax, all registered operators must account for VAT on the invoice basis unless application has been made and permission granted from the Commissioner to use some other basis (i.e. payments basis)

The general time of supply rule is that registered operators will account for VAT at the earlier of: -

That time an invoice is issued, or The time any payment is received by the supplier

Example:

Registered operator A (Category B) who accounts for VAT on the invoice basis, purchases a fridge for resale in October and receives a tax invoice for $3450 (incl. VAT @15%). He pays the supplier $2300 on 30 November. He may claim the full input tax of $ 450 in the period ending October even though he has not yet paid for the goods in full.

He then sells the fridge for Z$ 5750 (incl. VAT @ 15%). He issues an invoice on 15 December. Payment is received on 20 January. Registered operator A accounts for Z$750 VAT in the tax period covering December irrespective of whether he has received any payment or not.

Advantages DisadvantagesClaim VAT incurred on purchases prior to

paymentSuit existing accounting systemEasy to calculate as it is based on invoiced

Account for VAT on sales prior to receiving payment from debtors

List of debtors and creditors must be retained at the end of each tax period

27

sales and purchases Can lead to cash flow problems

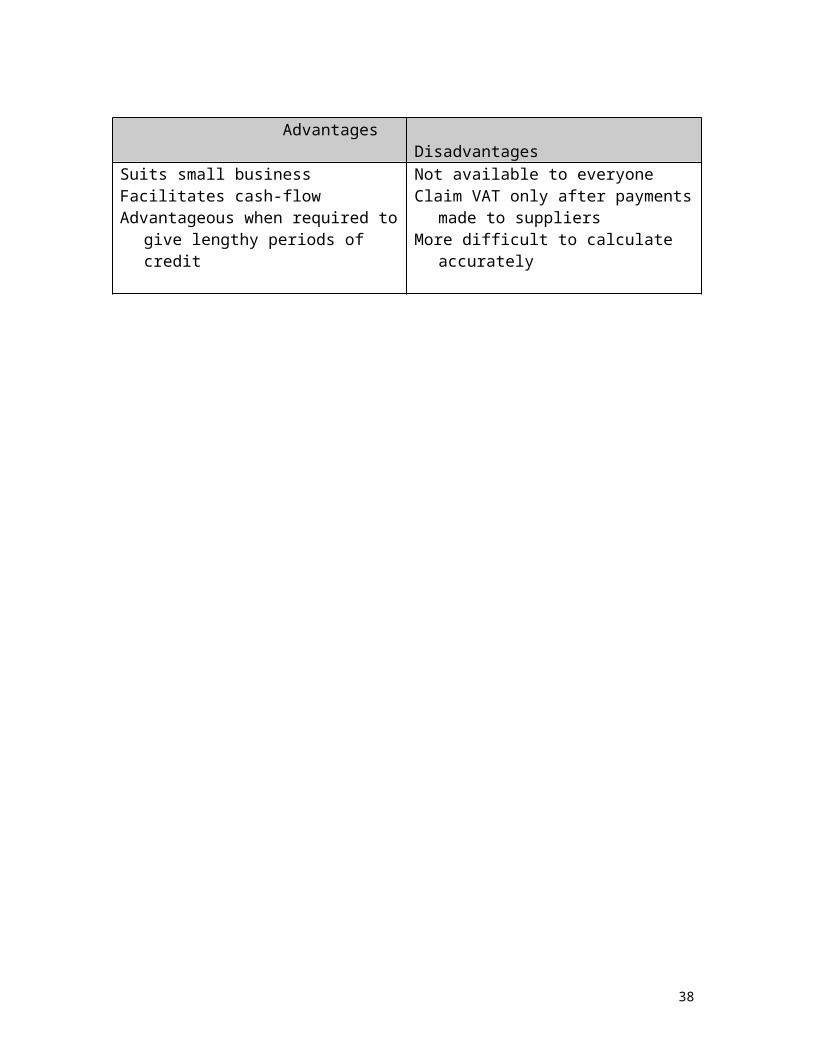

PAYMENTS BASIS

The payments basis (or cash basis) uses the same time of supply rule mentioned above, but the registered operator only accounts for VAT on actual payments made and received i.r.o. taxable supplies during the period.

The payments basis is only available to registered operators who have applied to the Authority in writing.

Advantages DisadvantagesSuits small businessFacilitates cash-flowAdvantageous when required to give

lengthy periods of credit

Not available to everyoneClaim VAT only after payments made to

suppliersMore difficult to calculate accurately

28

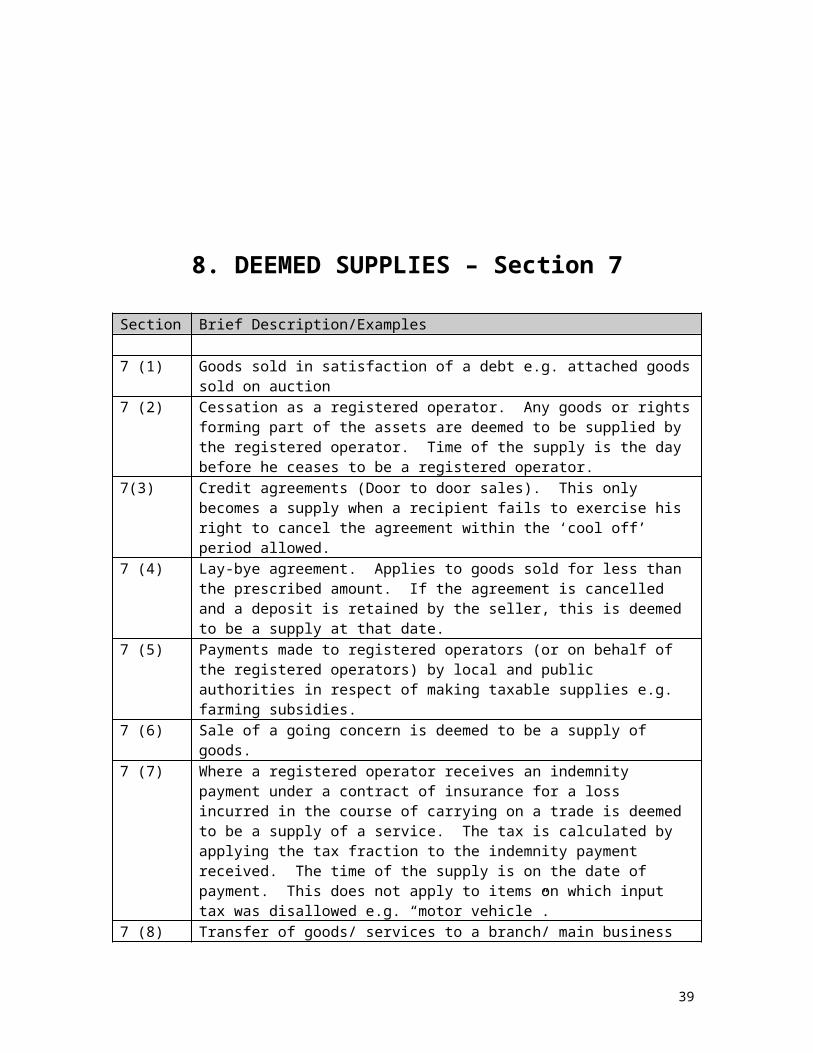

8. DEEMED SUPPLIES – Section 7

Section Brief Description/Examples

7 (1) Goods sold in satisfaction of a debt e.g. attached goods sold on auction7 (2) Cessation as a registered operator. Any goods or rights forming part of the assets

are deemed to be supplied by the registered operator. Time of the supply is the day before he ceases to be a registered operator.

7(3) Credit agreements (Door to door sales). This only becomes a supply when a recipient fails to exercise his right to cancel the agreement within the ‘cool off’ period allowed.

7 (4) Lay-bye agreement. Applies to goods sold for less than the prescribed amount. If the agreement is cancelled and a deposit is retained by the seller, this is deemed to be a supply at that date.

7 (5) Payments made to registered operators (or on behalf of the registered operators) by local and public authorities in respect of making taxable supplies e.g. farming subsidies.

7 (6) Sale of a going concern is deemed to be a supply of goods.7 (7) Where a registered operator receives an indemnity payment under a contract of

insurance for a loss incurred in the course of carrying on a trade is deemed to be a supply of a service. The tax is calculated by applying the tax fraction to the indemnity payment received. The time of the supply is on the date of payment. This does not apply to items on which input tax was disallowed e.g. “motor vehicle”.

7 (8) Transfer of goods/ services to a branch/ main business situated outside Zimbabwe and which is separately identifiable and maintains its own accounting system.

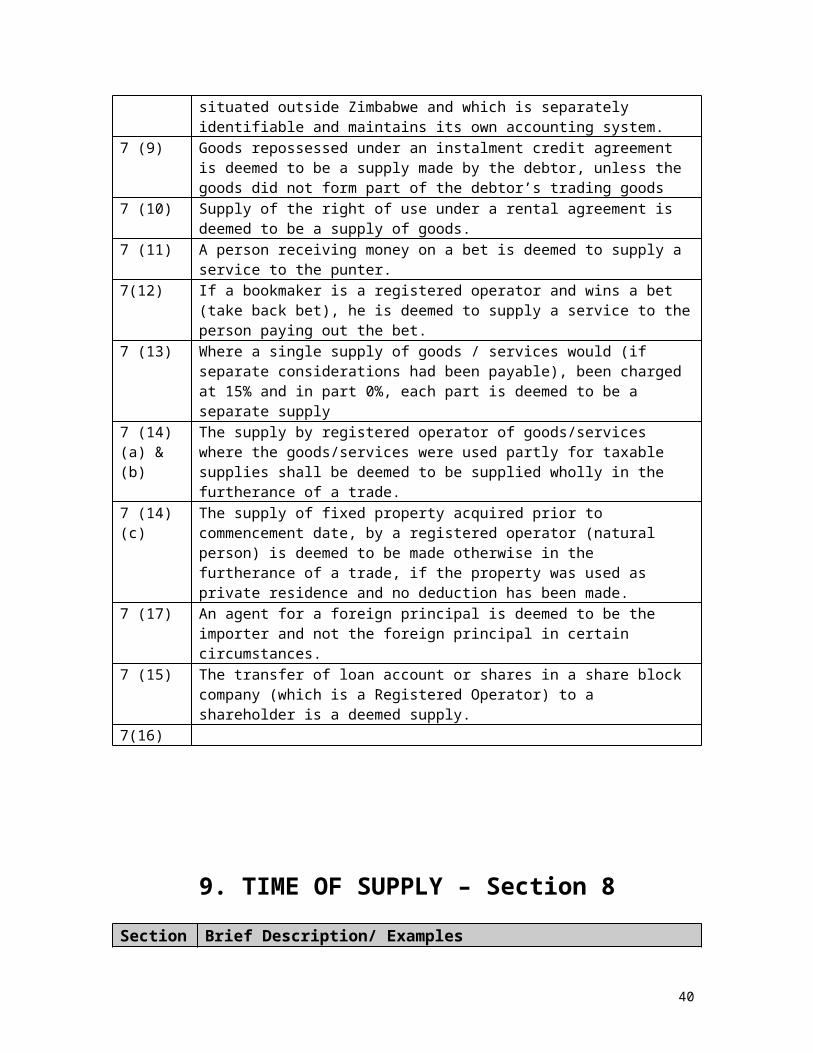

7 (9) Goods repossessed under an instalment credit agreement is deemed to be a supply made by the debtor, unless the goods did not form part of the debtor’s trading goods

7 (10) Supply of the right of use under a rental agreement is deemed to be a supply of goods.

7 (11) A person receiving money on a bet is deemed to supply a service to the punter.7(12) If a bookmaker is a registered operator and wins a bet (take back bet), he is deemed

to supply a service to the person paying out the bet.7 (13) Where a single supply of goods / services would (if separate considerations had

been payable), been charged at 15% and in part 0%, each part is deemed to be a separate supply

29

7 (14) (a) & (b)

The supply by registered operator of goods/services where the goods/services were used partly for taxable supplies shall be deemed to be supplied wholly in the furtherance of a trade.

7 (14) (c) The supply of fixed property acquired prior to commencement date, by a registered operator (natural person) is deemed to be made otherwise in the furtherance of a trade, if the property was used as private residence and no deduction has been made.

7 (17) An agent for a foreign principal is deemed to be the importer and not the foreign principal in certain circumstances.

7 (15) The transfer of loan account or shares in a share block company (which is a Registered Operator) to a shareholder is a deemed supply.

7(16)

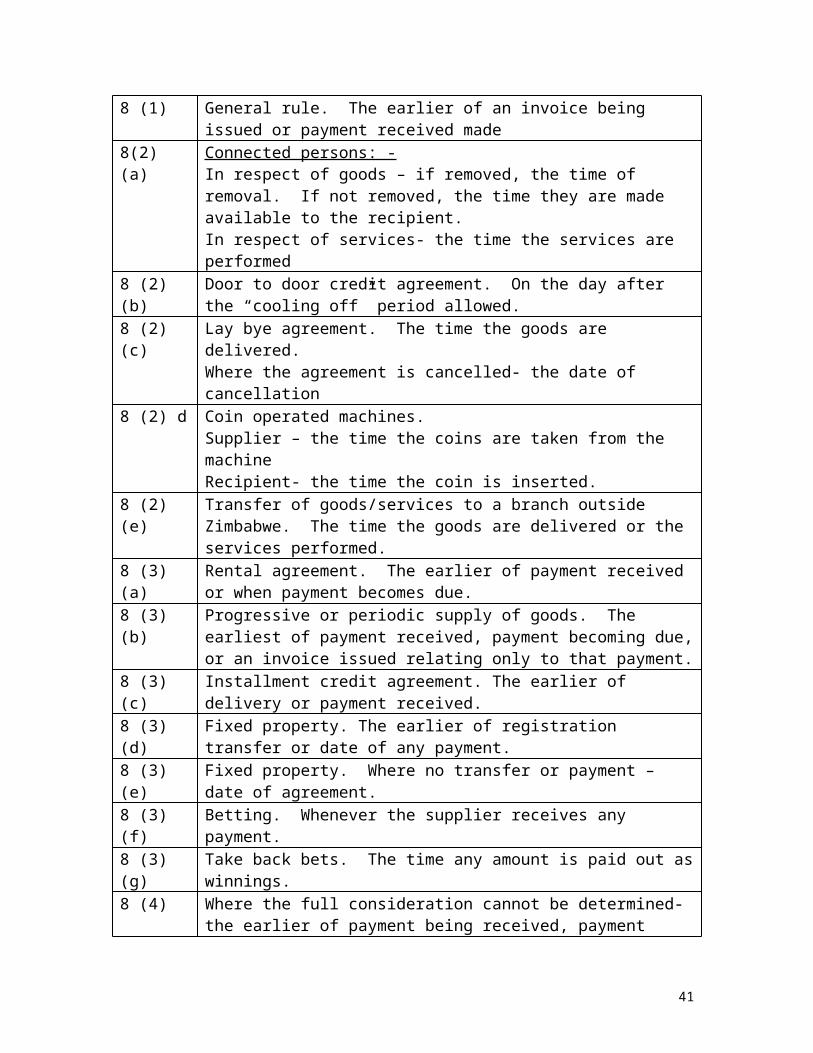

9. TIME OF SUPPLY – Section 8

Section Brief Description/ Examples8 (1) General rule. The earlier of an invoice being issued or payment received

made8(2) (a) Connected persons: -

In respect of goods – if removed, the time of removal. If not removed, the time they are made available to the recipient.In respect of services- the time the services are performed

8 (2) (b) Door to door credit agreement. On the day after the “cooling off” period allowed.

8 (2) (c) Lay bye agreement. The time the goods are delivered.Where the agreement is cancelled- the date of cancellation

8 (2) d Coin operated machines.Supplier – the time the coins are taken from the machineRecipient- the time the coin is inserted.

8 (2) (e) Transfer of goods/services to a branch outside Zimbabwe. The time the goods are delivered or the services performed.

8 (3) (a) Rental agreement. The earlier of payment received or when payment becomes due.

8 (3) (b) Progressive or periodic supply of goods. The earliest of payment received, payment becoming due, or an invoice issued relating only to that payment.

8 (3) (c) Installment credit agreement. The earlier of delivery or payment received.8 (3)(d) Fixed property. The earlier of registration transfer or date of any payment.8 (3) (e) Fixed property. Where no transfer or payment – date of agreement.8 (3) (f) Betting. Whenever the supplier receives any payment.8 (3) (g) Take back bets. The time any amount is paid out as winnings.8 (4) Where the full consideration cannot be determined- the earlier of payment

being received, payment being due, or an invoice is issued. (appropriated

30

goods)8 (5) Cessation of trade by a registered operator. The day before ceasing to be a

registered operator.8 (6) Section 17(1) adjustments i.r.o. change in use of assets in the trade from

taxable to non-taxable use- the time the goods are so applied.8 (7) Fringe benefits. At the end of each month where the cash equivalent is

required to be included in remuneration, or where not required to be so included, at the end of the year of assessment.

8(8) Repossessed goods. The day the goods are repossessed or the day after the last day where the debtor may be reinstated.

8 (9) Deemed importation by agent for a foreign principal. The time that the agent pays the VAT on importation.

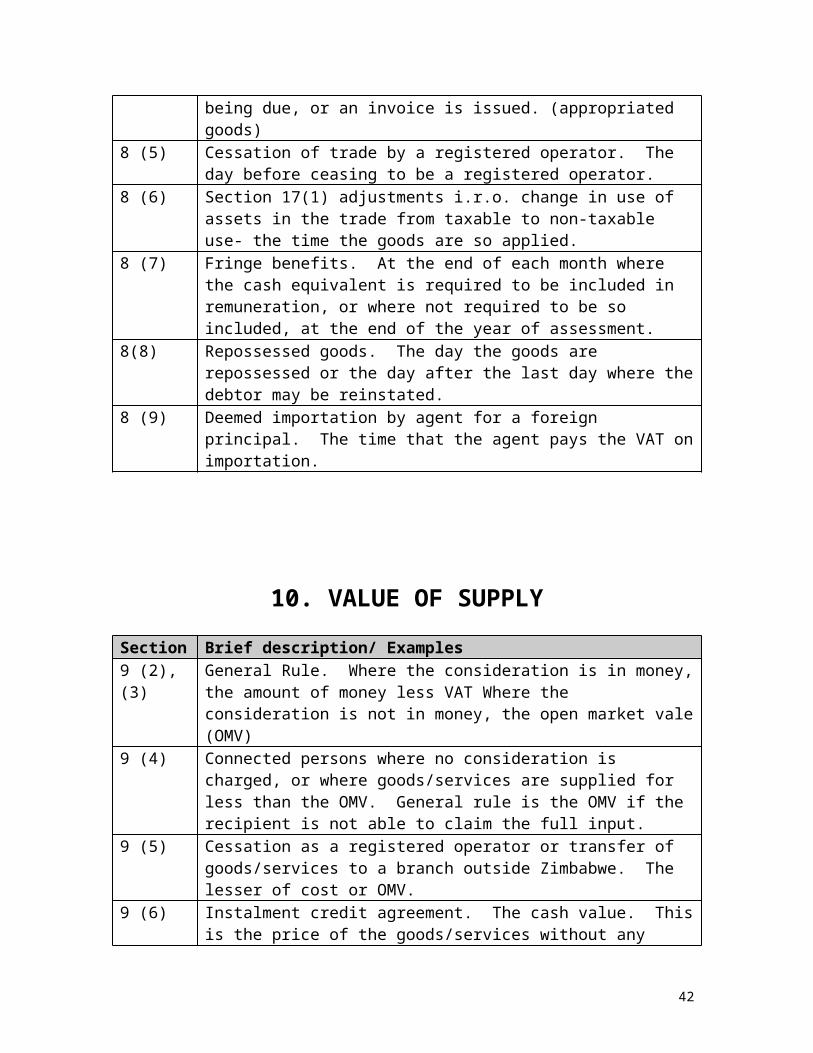

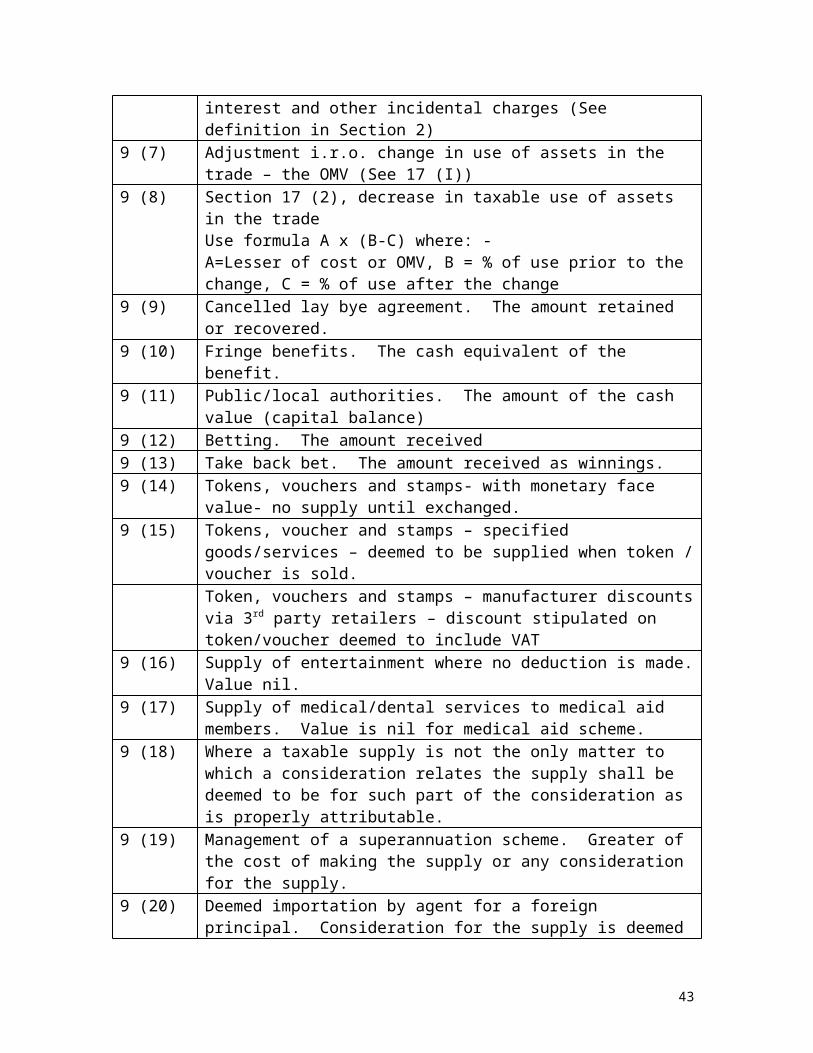

10. VALUE OF SUPPLY

Section Brief description/ Examples9 (2), (3) General Rule. Where the consideration is in money, the amount of money

less VAT Where the consideration is not in money, the open market vale (OMV)

9 (4) Connected persons where no consideration is charged, or where goods/services are supplied for less than the OMV. General rule is the OMV if the recipient is not able to claim the full input.

9 (5) Cessation as a registered operator or transfer of goods/services to a branch outside Zimbabwe. The lesser of cost or OMV.

9 (6) Instalment credit agreement. The cash value. This is the price of the goods/services without any interest and other incidental charges (See definition in Section 2)

9 (7) Adjustment i.r.o. change in use of assets in the trade – the OMV (See 17 (I))9 (8) Section 17 (2), decrease in taxable use of assets in the trade

Use formula A x (B-C) where: -A=Lesser of cost or OMV, B = % of use prior to the change, C = % of use after the change

9 (9) Cancelled lay bye agreement. The amount retained or recovered.9 (10) Fringe benefits. The cash equivalent of the benefit.9 (11) Public/local authorities. The amount of the cash value (capital balance)9 (12) Betting. The amount received9 (13) Take back bet. The amount received as winnings.9 (14) Tokens, vouchers and stamps- with monetary face value- no supply until

exchanged.9 (15) Tokens, voucher and stamps – specified goods/services – deemed to be

supplied when token / voucher is sold.

31

Token, vouchers and stamps – manufacturer discounts via 3rd party retailers – discount stipulated on token/voucher deemed to include VAT

9 (16) Supply of entertainment where no deduction is made. Value nil.9 (17) Supply of medical/dental services to medical aid members. Value is nil for

medical aid scheme.9 (18) Where a taxable supply is not the only matter to which a consideration

relates the supply shall be deemed to be for such part of the consideration as is properly attributable.

9 (19) Management of a superannuation scheme. Greater of the cost of making the supply or any consideration for the supply.

9 (20) Deemed importation by agent for a foreign principal. Consideration for the supply is deemed to be the value for purposes of the importation plus any tax levied on importation.

9 (21) Where any supply is made for no consideration, the value is nil. Different rules may apply for connected persons.

11. ZERO RATED SUPPLIES

Section 10 (1) – Goodsa) Goods exported to an address in an export countryb) Goods (including consumables) supplied to repair goods temporarily admitted into

Zimbabwe.c) Goods supplied under a rental agreement if used exclusively in an export country.d) Goods supplied under a rental agreement if used in or paid for from an export country. Only

applies to foreign registered businesses.e) Supply of business as a going concern.f) Gold supplied to the Reserve Bank or any other registered banks.g) Regular inputs supplied to farmers for farming e.g. herbicides, fodder and insecticide.

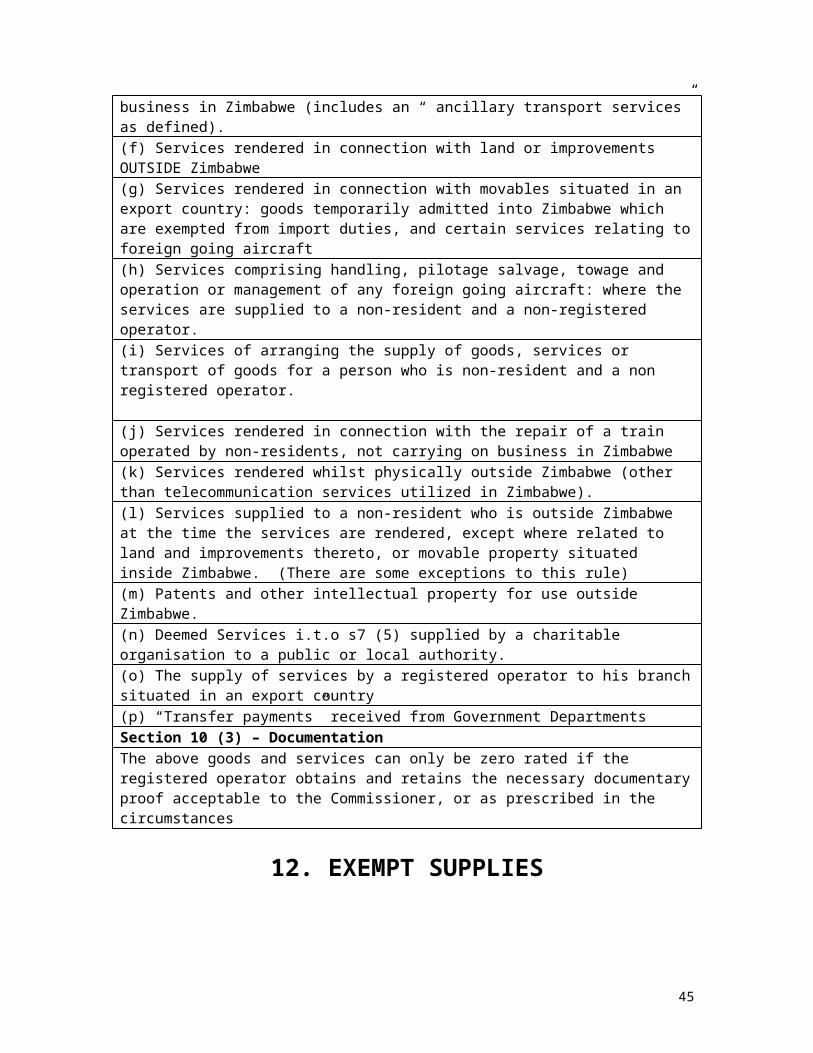

Certain food stuffs e.g. Milk, raw meat, bread. Goods for disabled persons.h) Goods supplied to an independent branch in an export country.i) Supply of gold coins issued by the Reserve Bank Drugs as defined in the Medicines & Allied Substances control Act.Section 10 (2) – Services(a) Transport PASSENGERS or GOODS to, from and outside Zimbabwe.(b) Transportation of PASSENGERS from one place to another place in Zimbabwe by aircraft to the extent that the travel constitutes “international carriage”(c) Transport and ancillary transport services supplied within Zimbabwe i.r.o. imports and exports of GOODS, if supplied by the same supplier responsible for the international transport of those goods.(d) Insuring arranging of the transport and arranging of insurance of PASSENGERS or GOODS i.r.o. international transport(e) Transportation services for the movement of goods through Zimbabwe from one export country to another, when provided to a non-resident (non-registered operator), who does not carry on a business in Zimbabwe (includes an “ ancillary transport services” as defined).(f) Services rendered in connection with land or improvements OUTSIDE Zimbabwe(g) Services rendered in connection with movables situated in an export country: goods temporarily admitted into Zimbabwe which are exempted from import duties, and certain services

32

relating to foreign going aircraft(h) Services comprising handling, pilotage salvage, towage and operation or management of any foreign going aircraft: where the services are supplied to a non-resident and a non-registered operator.(i) Services of arranging the supply of goods, services or transport of goods for a person who is non-resident and a non registered operator.

(j) Services rendered in connection with the repair of a train operated by non-residents, not carrying on business in Zimbabwe(k) Services rendered whilst physically outside Zimbabwe (other than telecommunication services utilized in Zimbabwe).(l) Services supplied to a non-resident who is outside Zimbabwe at the time the services are rendered, except where related to land and improvements thereto, or movable property situated inside Zimbabwe. (There are some exceptions to this rule)(m) Patents and other intellectual property for use outside Zimbabwe.(n) Deemed Services i.t.o s7 (5) supplied by a charitable organisation to a public or local authority.(o) The supply of services by a registered operator to his branch situated in an export country(p) “Transfer payments” received from Government DepartmentsSection 10 (3) – DocumentationThe above goods and services can only be zero rated if the registered operator obtains and retains the necessary documentary proof acceptable to the Commissioner, or as prescribed in the circumstances

12. EXEMPT SUPPLIES

Types of Exempt Supplies

a) Supply of certain Financial Services (excluding financial services charged at the zero rate).

b) The supply by an association not for gain of any donated goods or services OR where the association manufactures goods, if at least 80% of the value of the materials used consist of donated goods.

c) The supply of residential accommodation in a dwelling under a lease or hire agreement OR, where an employer permits his employee to occupy the accommodation as a fringe benefit for the duration of the employment.

d) The supply of leasehold land used to erect dwellings and for existing dwellingse) Sale or letting of land outside Zimbabwe. Note that any SERVICES relating to such

land is zero-rated. S10(2) (f)f) The supply of public road and railway transport to fare paying passengers and their

luggage. Note that the transport of passengers to an export country is zero-rated and this will override the exemption.

g) Any educational services for pre-school, primary, secondary, tertiary and technical education and the education or training of physically/ mentally handicapped persons at any institution, which meets the requirements of the Ministry responsible for education or higher education.

h) Medical services supplied by any person. This includes incidental and subordinate

33

services in respect thereof.i) The supply of goods and services by an employee organisation to any of its members

to the extent that the consideration for the supply consists of membership contributions.

j) The supply of piped water, rates charged by a local authority and domestic electricity

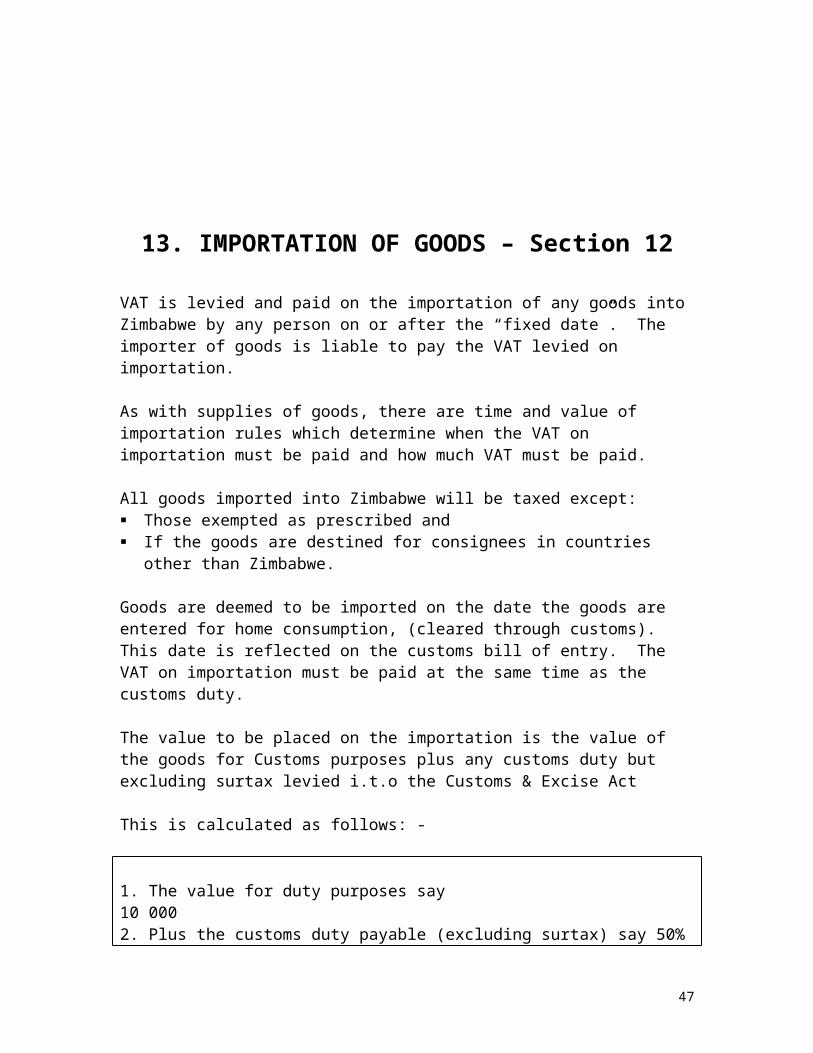

13. IMPORTATION OF GOODS – Section 12

VAT is levied and paid on the importation of any goods into Zimbabwe by any person on or after the “fixed date”. The importer of goods is liable to pay the VAT levied on importation.

As with supplies of goods, there are time and value of importation rules which determine when the VAT on importation must be paid and how much VAT must be paid.

All goods imported into Zimbabwe will be taxed except: Those exempted as prescribed and If the goods are destined for consignees in countries other than Zimbabwe.

Goods are deemed to be imported on the date the goods are entered for home consumption, (cleared through customs). This date is reflected on the customs bill of entry. The VAT on importation must be paid at the same time as the customs duty.

The value to be placed on the importation is the value of the goods for Customs purposes plus any customs duty but excluding surtax levied i.t.o the Customs & Excise Act

This is calculated as follows: -

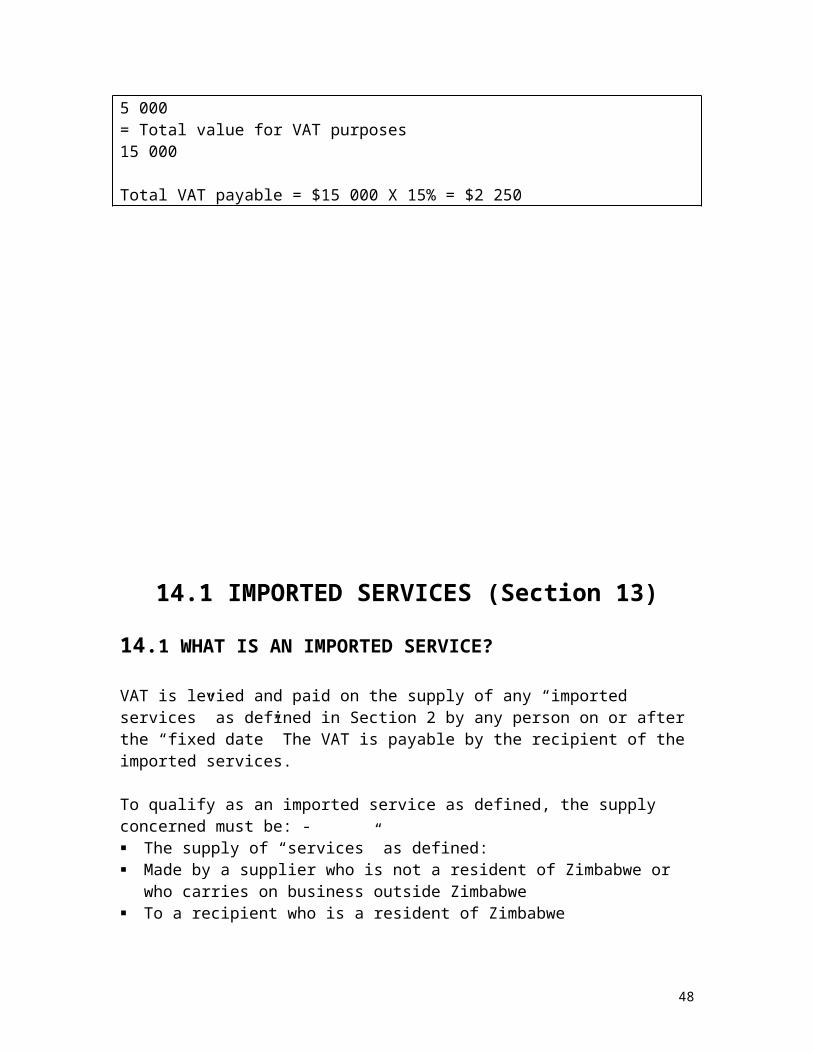

1. The value for duty purposes say 10 0002. Plus the customs duty payable (excluding surtax) say 50% 5 000= Total value for VAT purposes 15 000

Total VAT payable = $15 000 X 15% = $2 250

34

14.1 IMPORTED SERVICES (Section 13)

14.1 WHAT IS AN IMPORTED SERVICE?

VAT is levied and paid on the supply of any “imported services” as defined in Section 2 by any person on or after the “fixed date” The VAT is payable by the recipient of the imported services.

To qualify as an imported service as defined, the supply concerned must be: - The supply of “services” as defined: Made by a supplier who is not a resident of Zimbabwe or who carries on business

outside Zimbabwe To a recipient who is a resident of Zimbabwe Utilised or consumed in Zimbabwe otherwise than for making taxable supplies

The definition also states that it applies “to the extent that such services are utilised or consumed in Zimbabwe otherwise than for the purpose of making taxable supplies”. This means that the service concerned might be partially taxable. This will apply for example where the services are used partially for taxable supplies and partially for private purposes or exempt supplies.

The definition implies that VAT need only be paid on services which are imported by a person who: -

Is not registered as a registered operator: or Is a registered operator but utilisting the services wholly or partially for exempt

supplies: or Is a registered operator utilising the services for private purposes (i.e. not for taxable

supplies)

35

Example 1

Registered operator A, who manufactures widgets, pays a technical license fee to a UK based company for the right to manufacture the widgets in Zimbabwe and for know-how. Although the service, in respect of which the technical license fee is paid, is supplied by a supplier who is resident outside Zimbabwe to a recipient who is resident in Zimbabwe, the services supplied do not fall within the definition of “imported services” as they are consumed in the course of registered operator A`s taxable activity of manufacturing and selling widgets. VAT would therefore not be payable in this situation as the services do not meet the definition of imported services in Section 2 of the VAT Act.

Example 2

Company B, a life insurer, employs a UK based advertising agency to run an advertising campaign for a new life policy, which it intends marketing. VAT will be payable in this situation as the services are consumed by company B in the course of an exempt activity, i.e. the provision of life insurance.

14.2 WHEN MUST VAT ON IMPORTED SERVICE BE PAID (Sec 14)

The recipient of the services, must within 30 days of the time of importation, declare and pay the VAT to the Zimbabwe Revenue Authority on the prescribed form.

14.3 TIME OF SUPPLY

The time of supply of imported services is the earlier of: - The time that an invoice in respect of the supply is issued by the supplier or recipient;

or The time that any payment is made by the recipient in respect of the supply

Whichever event occurs first.

14.4 VALUE OF SUPPLY

The value of the supply is either: - The amount of the consideration (less VAT) for the supply: or The open market value of the supply

Whichever is the greater

36

14.6 EXEMPTIONS

VAT is not payable on imported services if: - The supply would be exempt from VAT or zero-rated if supplied in Zimbabwe: or The supply of the service is subject to VAT at the standard rate of 15% in Zimbabwe

15. INPUT TAX (Section 15 & 16)

15.1 WHAT WILL QUALIFY AS INPUT TAX?

Any VAT charged to a registered operator on the supply to him or importation by him on any goods or services where those goods or services are acquired wholly or partly for the purpose of consumption, use or supply in the course of making taxable supplies, will qualify as input tax

Input tax may therefore apply to acquisitions of: -

Trading stock Raw materials Manufacturing overheads Administrative overheads Marketing expenditure Fixed assets Cleaning and security services Accounting services Consultation services

To qualify as input tax, two requirements have to be met, namely: -

The goods or services must be acquired by the registered operator wholly or partly for the purpose of consumption, use or supply in the course of making taxable supplies.

The goods supplied must have been subject to VAT at the standard rate or the goods must qualify as “second hand goods” (previously owned and used) as defined in section 2 which have been acquired from a non-registered operator.

Where goods or services are acquired for a purpose other than making taxable supplies, the VAT will not qualify as input tax.

A deduction of input tax can be made in respect of a supply only if the registered operator (or his authorised agent) is in possession of: -

37

A valid tax invoice which has been issued to him by the supplier (being a registered operator)

Sufficient records in respect of any non-taxable supply of second-hand goods purchased or

A customs bill of entry or other prescribed customs document for any importation of goods or services on which tax has been paid.

15.2 DETERMINING THE AMOUNT OF INPUT TAX

Below are 2 examples of how to calculate or determine the amount of input tax, which a registered operator can claim: -

Example 1: Goods acquired wholly for making taxable supplies:

Registered operator purchases a cash register for use in his retail clothing shop. The cash register costs him $115 000 (includes $15 000 VAT). Registered operator A`s activities consist solely of selling clothes. As he purchased the cash register wholly for the making of taxable supplies, the full amount of $15 000 VAT incurred may be claimed as input tax.

Example 2: Goods acquired partly for making taxable supplies

Registered operator B purchases a personal computer to use in his insurance brooking business. He derives 60% of his income from the life insurance side of his business, and 40% from the short-term insurance side. The computer is used in processing information relating to both. The computer costs Registered operator B an amount of Z$230 000 (includes $30 000 VAT). As the computer is acquired only partly for use in the making of taxable supplies, registered operator B is required to apportion the full amount of VAT charged to determine input tax based on the turnover. The input tax is determined by applying the percentage of the intended use of the making of taxable supplies to the full amount of VAT payable.

i.e.: 40% x Z$30000 = Z$12000

15.3 DENIAL OF INPUT TAX

There are certain circumstances under which the input tax payable cannot be deducted by the registered operator, namely: -

Goods or services acquired for purposes of entertainment Membership fees or subscriptions of clubs, associations or societies of a sporting,

social or recreational nature

38

Medical services provided to persons under medical aid (i.e. the medical scheme cannot claim an input on the medical services provided to it’s members) and

The acquisition of non-commercial motor vehicle by a registered operator

15.3.1 Entertainment

Common place examples are as follows: - Staff refreshments such as tea, coffee and other beverages and snacks Food and other ingredients purchased in order to provide meals to staff, clients and

business associates Catering services acquired for staff canteens and dining rooms Equipment and utensils used in kitchens Furniture and other equipment and utensils used in canteens and dining rooms Christmas lunches and parties, including the hire of venues Gold days for customers and clients Beverages, meals, other hospitality and entertainment supplied to customers and

clients at product launches and other promotional events Entertainment of customers and clients in restaurants, theatres and night clubs Capital goods such as holiday houses, yachts and private aircraft used for

entertainment

N.B. The above list is not exhaustive

The VAT Act does, however, provide for certain exceptions to this rule. These exceptions are listed below: -

Registered operators in the business of supplying entertainment at a charge that at least covers the direct and indirect costs of providing the entertainment

Personal subsistence of employees only where employees incur expenditure on personal subsistence on behalf of their employer, and the actual expenditure is reimbursed. It is a condition for the claim that the employee must be away on business overnight from his/her normal place of work and residence. Where an allowance is paid to the employee for this expense, no input tax credit will be allowed. Furthermore any expenses relating to recreation or amusement such as theatre or movie tickets will not qualify for the deduction

Meals or refreshments supplied by operators of taxable passenger transport services (e.g. air transport where meals are provided)

Meals or refreshments supplied by organisers of seminars and similar events (once again, subject to the costs being covered by the entrance fees)

39

Sport or recreational facilities provided by local authorities and Charitable organisations

15.3.2 Goods or services acquired by medical schemes or benefit funds

The implication of this rule is that medical and other benefit schemes are not registered for VAT insofar as the provision of these benefits are concerned to their members. Consequently, no input tax may be claimed by these schemes on any medical and dental services incurred by the members, which are in turn submitted to the scheme/fund for payment

15.3.3 Motor Vehicles

A deduction of input tax may not be claimed by a registered operator in respect of the acquisition by him of a non-commercial motor vehicle, whether that acquisition was by way of purchase, importation, leasing, operating rental or casual hire.

Even if the vehicle is used exclusively for taxable supplies the VAT paid may still not be claimed as input tax.

Exceptions

Registered operators who are motor vehicle dealers or operate a vehicle rental trade (e.g. Avis, Hertz, Budget, etc) for the exclusive purpose of making direct taxable supplies of those motor vehicles in the ordinary course of their trade

Modification and installation costs after delivery of the vehicle (e.g. canopy modification for a light delivery van (LDV) or installation of mobile phone kites, etc)

Repairs and maintenance / general running costs of the motor vehicle acquired for making taxable supplies such as tyres, servicing etc and

Insurance

Converted vehicles

Where a motor vehicle is modified or converted prior to delivery and the final product is supplied to the purchase in that state, no input tax at all can be claimed. If the purchaser takes delivery of the motor vehicle and subsequently modifies or converts it, the VAT paid on such modification or conversion may be claimed. Provided that the modified motor vehicle is used for making taxable supplies.

The VAT paid on the vehicle itself will, however, still be denied.

Demonstration vehicles

The VAT paid on demonstration vehicles used by motor vehicle dealer to display and demonstrate will be allowed.

40

15.3.4 Club subscriptions of a recreational nature

No input tax may be claimed on VAT paid i.r.o. any membership fees to sporting and recreational clubs e.g. Harare Country Club, Lake Kariba Diving Club, etc.

The VAT on subscriptions to magazines and trade journals which are related in some direct manner to the nature of the trade carried on by the registered operator may be claimed.

If the fees or subscriptions are payable to professional organisations such as: -

A professional accounting body Medical and dental council, or Law society of Zimbabwe

Input tax may be claimed if it is a condition of employment that such fees are to be paid by the employer for the employee (s) concerned.

15.5 PRE-INCORPORATION EXPENSES – Section 19

If the company reimburses the person for the costs and purchases, it is deemed to be the recipient of the goods or services and to have paid any VAT component. Accordingly the company can deduct that VAT as input tax. This is the case if the person: -

Was reimbursed by the company for the whole amount paid, andAcquired the goods or services for the purpose of trade to be carried on by the company.

The company may claim such input tax in the tax period during which the reimbursement is made

The company may not, however, claim the deduction under section 19 of the Act where: -The supply of the goods or services by the person to the company is a taxable supply, or

is a supply of second-hand goods not being a taxable supplyThe goods or services were acquired more than six months before the date of

incorporation, or

41

The company does not hold sufficient records (in this case no input tax can be claimed at all under any section of the VAT Act)

16. CALCULATIONS OF VAT

Below is an overview of the calculation of VAT payable or refundable for any particular period. Note that the timing of transactions and the amount of tax payable depends on whether the registered operator is on the invoice or payments basis.

42

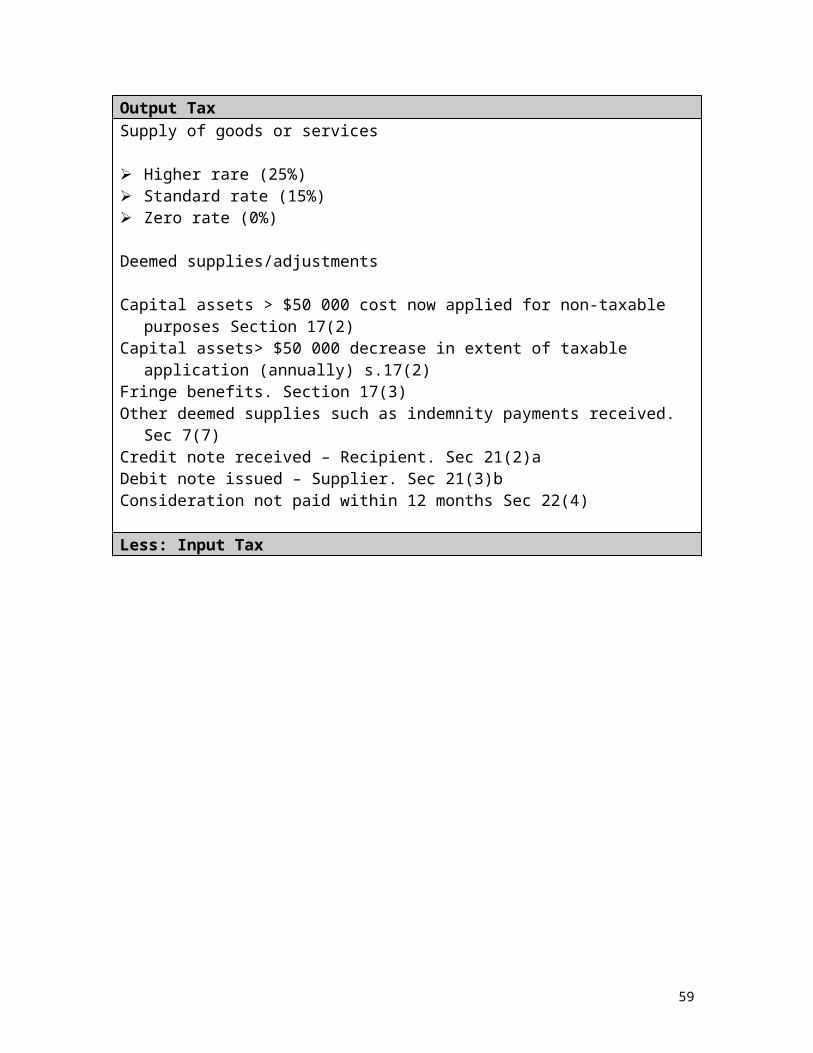

Output TaxSupply of goods or services

Higher rare (25%) Standard rate (15%) Zero rate (0%)

Deemed supplies/adjustments

Capital assets > $50 000 cost now applied for non-taxable purposes Section 17(2)Capital assets> $50 000 decrease in extent of taxable application (annually) s.17(2)Fringe benefits. Section 17(3)Other deemed supplies such as indemnity payments received. Sec 7(7)Credit note received – Recipient. Sec 21(2)aDebit note issued – Supplier. Sec 21(3)bConsideration not paid within 12 months Sec 22(4)

Less: Input Tax

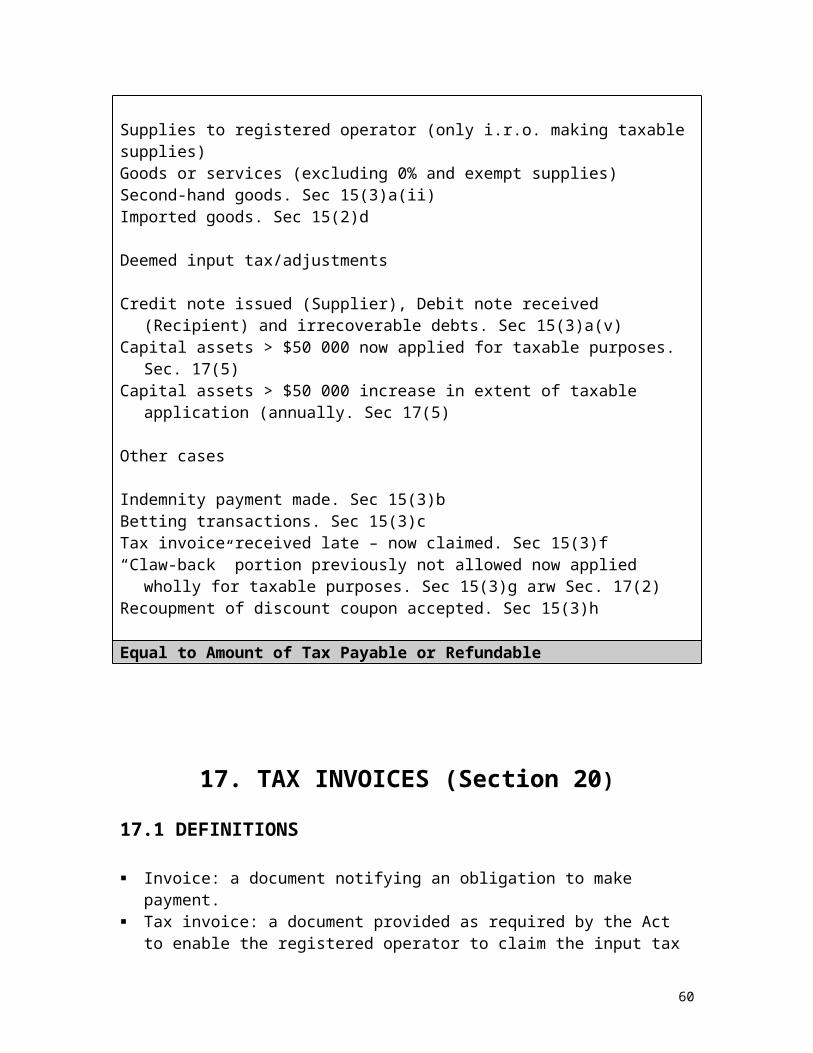

Supplies to registered operator (only i.r.o. making taxable supplies)Goods or services (excluding 0% and exempt supplies)Second-hand goods. Sec 15(3)a(ii)Imported goods. Sec 15(2)d

Deemed input tax/adjustments

Credit note issued (Supplier), Debit note received (Recipient) and irrecoverable debts. Sec 15(3)a(v)

Capital assets > $50 000 now applied for taxable purposes. Sec. 17(5)Capital assets > $50 000 increase in extent of taxable application (annually. Sec 17(5)

Other cases

Indemnity payment made. Sec 15(3)bBetting transactions. Sec 15(3)cTax invoice received late – now claimed. Sec 15(3)f“Claw-back” portion previously not allowed now applied wholly for taxable purposes.

Sec 15(3)g arw Sec. 17(2) Recoupment of discount coupon accepted. Sec 15(3)h

Equal to Amount of Tax Payable or Refundable

43

17. TAX INVOICES (Section 20)

17.1 DEFINITIONS

Invoice: a document notifying an obligation to make payment. Tax invoice: a document provided as required by the Act to enable the registered

operator to claim the input tax

17.2 WHAT ARE THE REQUIREMENTS FOR TAX INVOICE?

A normal invoice is a document that notifies of an obligation to pay. In practice, a registered operator will normally only issue a tax invoice which will satisfy the requirements of the Zimbabwe Revenue Authority and the requirements of the contracting parties.

A registered operator is required to issue a tax invoice within 30 days from the date of supply, but if the consideration in money does not exceed $100 a tax invoice is not required. However, in such cases, some type of source document is required in order to claim input tax e.g. till slip, petty cash slip. e.t.c. A tax invoice as described in section20(4) must be issued on transactions exceeding $100.

A tax invoice is a special tax document and certain details about the taxable supply to which it relates must be stated on the tax invoice. (See below for details). A tax invoice should also be in Zimbabwean currency. If the tax invoice is issued in a foreign currency, then the exchange rate ruling at the time of supply as determined i.t.o. Section 8 of the VAT Act for the supply should be used.

Requirements: tax invoice {Section 20 (4)}The words “TAX INVOICE” in a prominent placeName, address and VAT registration number of the supplierName and address of recipientIndividual serialised number and date of issueDescription of goods and /or servicesQuantity or volume of goods or services suppliedPrice & VAT **

** There are 3 methods allowed for reflecting the price & VAT as follows: -

Method 1 Method 2 Method 3The amount excluding VAT, plus the VAT charged and the amount including VAT

Where VAT is included in the final price, the consideration, together with a statement that VAT is included and the rate of tax.

Where VAT is included in the final price, the amount charged including VAT and the amount of VAT charged

44

EXAMPLE OF A TAX INVOICE

TAX INVOICEDragon Associates (Pvt) LimitedSuite 4, 1st Floor Nehanda House80 Chimurenga AvenueHarare

Tax Invoice No: 89624 VAT Registration No: 4545884937 Our Ref: TD/mb/06715/T

Date: 30 May 2002

To: Perplex (Pvt ) Limited 8 Horror Street, Granitesite

Harare

DATE DESCRIPTION OF GOODS

QUANTITY Z$

30/11/2002 Widgets 300 x 200Nuts 39 x 60 x 48Bolts 4 x 9

VAT @ 15%

4 000 870 200

2 00013003400

67001005

7705

45

TAX INVOICES PREPARED BY THE RECIPIENT

In some instances the consideration for a supply is determined by the recipient of the goods/services rather than by the supplier. In appropriate cases the Authority may permit the recipient to create a tax invoice and in which case, the document issued is deemed to be a tax invoice

The conditions are as follows: - Sec 20(2)

Both the recipient and supplier must be registered operators The Authority must have granted prior approval for the issue of the tax invoice by the

recipient The supplier and the recipient must agree that the supplier will not also issue a tax

invoice; and The tax invoice must be provided to the supplier and a copy retained by the recipient

In the case of goods being repossessed from a registered operator as contemplated i.t.o. Section 7 (9) and section 20(3) the person repossessing the goods (a registered operator -–normally a bank) is required to create and furnish the defaulting debtor with a tax invoice.

SPECIAL CASES

Although the general rule is that a registered operator must have a tax invoice before he will be allowed to claim any input tax in relation to the supply, there are a few exceptions to the rule.

17.4.1. Second hand goods as defined

Where registered operator purchases second hand goods from a non-registered operator, to support his claim for input tax, the purchaser has to record the following:

Name address and I.D. no. of the supplier (I.D. no. of the representative person if it is a company)

Date of acquisition Quantity or volume of goods Consideration for the supply Recipient must verify the person’s I.D. no. or passport number Where the amount of the supply is $1 000 or more, the recipient must obtain and

retain a copy of the person’s I.D., and, in the case of a company, a business letterhead or similar document is also required which shows the name and registration number allocated by the relevant authority.

46

Where the goods concerned have been repossessed from a non-registered operator, the person (registered operator) exercising his right of repossession is required to keep details as mentioned above.

17.4.2. Other cases

Where the purchase price is less than Z$100 and the total consideration is in money, no tax invoice is required.

Where the Zimbabwe Revenue Authority is satisfied that there will be sufficient records and that it will be impractical for a tax invoice to be issued, he may grant permission for tax invoices not to be issued.

No tax invoice need be issued where a supply is exempted from VAT. Where a tax invoice is issued which includes zero rated, exempt, standard rated, and

higher rates supplies, the document must clearly distinguish between the various supplies. The relevant values of each supply must be indicated separately.

COPIES OF TAX INVOICES

If a tax invoice is lost for a particular supply received a copy may be obtained from the supplier provided the duplicate is clearly marked “ copy only” by the supplier. A facsimile of a tax invoice is not acceptable in any circumstances

A copy sent by e-mail is also not acceptable.

18. CREDIT AND DEBIT NOTES- Sec 21

Credit notes are often issued by a supplier when the consideration for a supply is reduced.

Debit notes are also issued by the supplier when the consideration is subsequently increased.

The issue of a debit note or credit note when a tax invoice has previously been issued is generally used to show the increase or decrease in tax (as the case may be) on the supply. This is to be done whether or not the supplier accounts for tax on an invoice or payments basis. The issue of a credit note is not required when a prompt payment (settlement) discount is the reason for the reduction in the consideration, provided the terms of that discount are clearly shown on the tax invoice.

18.1 REQUIREMENTS FOR CREDIT AND DEBIT NOTES

Credit and debit notes are required to be issued in one or more of the following circumstances: -

The cancellation of a supply of goods or services The nature of that supply of goods or services has been fundamentally varied or

altered

47

The previously agreed consideration for the supply of the goods or services being altered by agreement with the recipient (including a discount)