the brazilian healthcare sector - business sweden · confidential for internal use within client...

TRANSCRIPT

CONFIDENTIAL

FOR INTERNAL USE WITHIN CLIENT COMPANY ONLY

THE BRAZILIAN

HEALTHCARE SECTOR

GREAT OPPORTUNITIES ON LATIN AMERICA’S LARGEST HEALTH CARE MARKET

São Paulo, Brazil

August 2015

9,7% of GDP

BRL 470bn spent on Healthcare... … comparable to many European countries.

However, annual health expenses per capita is still

relatively low in Brazil (USD 1109, 2012).

BUSINESS SWEDEN 28 OCTOBER, 2015 2

THE BRAZILIAN HEALTHCARE MARKET IS THE LARGEST

IN LATIN AMERICA AND GROWING RAPIDLY

SOURCE: WORLD DATA BANK, BRAZILIAN INSTITUTE OF

GEOGRAPHY AND STATISTICS (IBGE), WHO

Development

of a middle

class

Welfare

diseases

increasing

Upcoming

growth of

the Brazilian

healthcare

market

Aging

population

BUSINESS SWEDEN 28 OCTOBER, 2015 3

THE BRAZILIAN CONSTITUTION PROVIDES UNIVERSAL

HEALTHCARE..

SOURCE: BMI: BRAZIL PHARMACEUTICALS & HEALTHCARE REPORT Q4 2012, ECONOMIST INTELLIGENCE UNIT: BROADENING HEALTHCARE ACCESS IN BRAZIL THROUGH INNOVATION, WHO, FOLHA DE SAO PAULO, THE

LANCET

The government has to provide free universal healthcare as a constitutional right for 200 million Brazilians, an

important democratization movement in the 1988 constitution

The SUS is one of the largest public health care system in the world. The SUS operates though both

public and private participation as it also finances the private sector performing complementary tasks not being taken on by the public

sector

PUBLIC HEALTHCARE REACHES 100% OF POPULATION BUT ANYONE WHO CAN AFFORD HAVE A PRIVATE HEALTH INSURANCE

SUS - UNIFIED HEALTH SYSTEM

Autonomy of federal units

SUS Mixed

Provided by

public or private

Free

universal access

Theoretically, the SUS reaches 100% of the population.

However it is estimated that today there are approx. 150

million people that depend exclusively on SUS and 49

million people (or 25%) having private

health insurances but that can also access to

SUS

Brazil’s medical system is to a significant extent

decentralized, giving autonomy to states and

municipalities

BUSINESS SWEDEN 28/10/2015 4

..YET THE PRIVATE SECTOR REPRESENTED 53% OF

TOTAL HEALTH EXPENDITURES IN 2014

47% BRL 221 bn

53% BRL 249 bn

PRIVATE PUBLIC

TOTAL HEALTH EXPENDITURES BY SECTOR The Brazilian governments’ share of total expenditure amounted

to 47% in 2014. As a comparison, the Swedish government’s

share represents 82% of total health expenditures

The public system in Brazil has since the start been

underfunded and the expenditures fall far behind the OECD average

of 70%. People often have to wait for months for exam results and critical

procedures

Governments’ share on expenditures in Brazil are relatively low when

compared to Sweden but absolute values are significant

BRL 221 bn for the public sector

BRL 249 bn for the private sector

The Brazilian Congress has approved that 25% of government

revenue from oil findings will go to fund public healthcare.

Oil and gas royalties reached BRL18,5 bn in 2014

ALTHOUGH UNDERFUNDED, THE PUBLIC SECTOR IS AN HIGHLY INTERESTING CLIENT SEGMENT ONLY BY ITS MERE SIZE

BUSINESS SWEDEN 28 OCTOBER, 2015 5

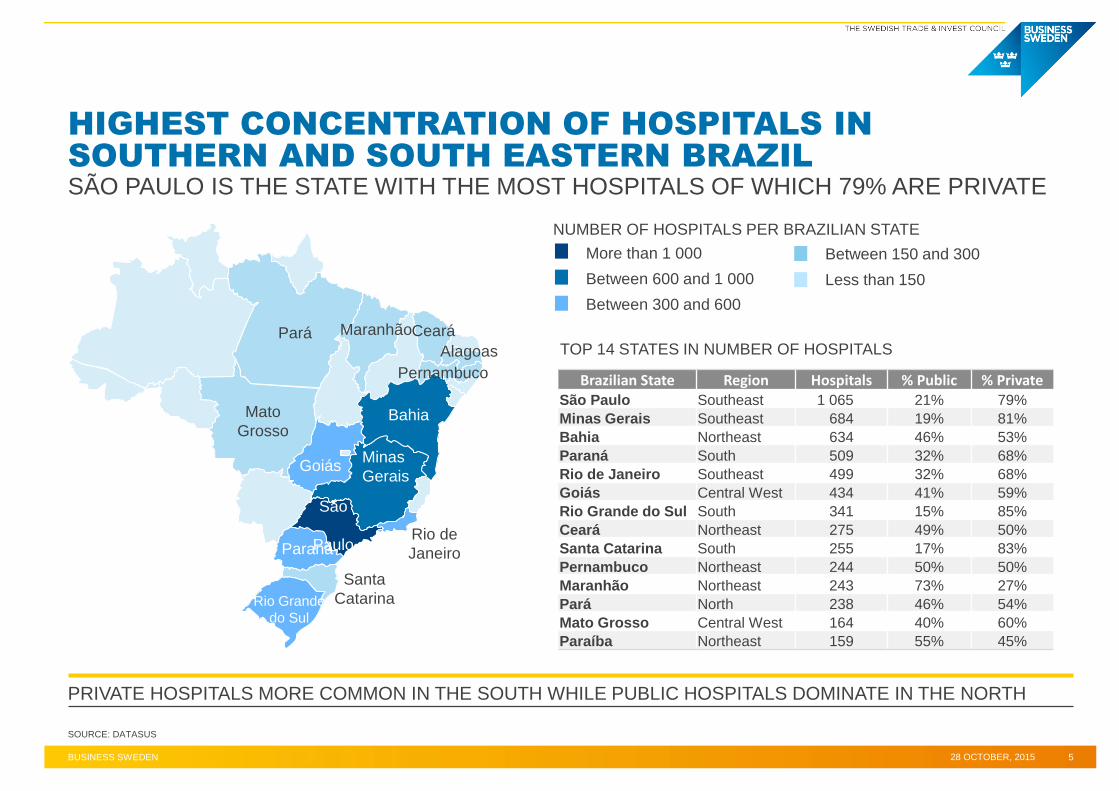

HIGHEST CONCENTRATION OF HOSPITALS IN

SOUTHERN AND SOUTH EASTERN BRAZIL

SOURCE: DATASUS

PRIVATE HOSPITALS MORE COMMON IN THE SOUTH WHILE PUBLIC HOSPITALS DOMINATE IN THE NORTH

Brazilian State Region Hospitals % Public % Private São Paulo Southeast 1 065 21% 79%

Minas Gerais Southeast 684 19% 81%

Bahia Northeast 634 46% 53%

Paraná South 509 32% 68%

Rio de Janeiro Southeast 499 32% 68%

Goiás Central West 434 41% 59%

Rio Grande do Sul South 341 15% 85%

Ceará Northeast 275 49% 50%

Santa Catarina South 255 17% 83%

Pernambuco Northeast 244 50% 50%

Maranhão Northeast 243 73% 27%

Pará North 238 46% 54%

Mato Grosso Central West 164 40% 60%

Paraíba Northeast 159 55% 45%

More than 1 000

Between 600 and 1 000

Between 300 and 600

NUMBER OF HOSPITALS PER BRAZILIAN STATE

Rio Grande

do Sul

Paraná

São

Paulo Rio de

Janeiro

Minas

Gerais

Bahia

Goiás

Ceará

Santa

Catarina

Pernambuco

Maranhão Pará

Mato

Grosso

Alagoas

Between 150 and 300

Less than 150

TOP 14 STATES IN NUMBER OF HOSPITALS

SÃO PAULO IS THE STATE WITH THE MOST HOSPITALS OF WHICH 79% ARE PRIVATE

PRIVATE PUBLIC

BUSINESS SWEDEN 28 OCTOBER, 2015 6

BRAZIL’S LEADING HOSPITALS ARE PRIVATE

PHILANTHROPIC INSTITUTIONS

SOURCE: MINISTRY OF HEALTH (MS), DATASUS, LEGISLATION

General Hospitals

Specialist Hospitals

Day Hospitals

(partial hospitalization)

Research/University

Hospitals

HOSPITALS

PRIVATE AND PHILANTHROPIC HOSPITALS GENERALLY MORE INCLINED TO PURCHASE HIGH-END PRODUCTS

Federal

State

Municipal

Philanthropic Managed by the federal government

Mostly general hospitals

100 hospitals

Managed by the state governments

Large share of specialist hospitals

610 hospitals

Example: Hospital das Clínicas (SP)

Managed by the municipal Government

Mostly general hospitals

1685 hospitals

Attend mainly to private insurance plans

Are generally high quality

Less than a half attend SUS

2860 hospitals

Private, non-profit oriented hospitals

At least 60% of beds must be reserved

for SUS patients. In return, the hospital

gets exemption from taxes

6 of the best Brazilian hospitals are

philantropic, considered Excellence

Hospitals by the government

1444 hospitals

Private and philanthropic hospitals are

generally more inclined to purchase

high-end medical devices and

equipment.

Purchase prices are in general also

higher in the private sector.

Attend mostly to SUS patients

Many are working with overcapacity

Although there are good quality

hospitals, most are in bad conditions

Private

MOST PRIVATE HEALTH PLAN BENEFICIARIES LIVE IN THE SOUTH AND SOUTH EAST

BUSINESS SWEDEN 28 OCTOBER, 2015 7

THE STATE OF SÃO PAULO ALONE HAS 19 MILLION

PRIVATE INSURANCE BENEFICIARIES

SOURCE: MINISTRY OF HEALTH - CNES, NATIONAL AGENCY FOR SUPPLEMENTARY HEALTH SERVICES (ANS)

More than 7 million

Between 2 and 7 million

Between 0,7 and 2 million

Between 0,4 and 0,7 million

Less than 0,4

NR OF PRIVATE INSURANCE PLAN BENEFICIARIES

MORE THAN 80% OF PRIVATELY INSURED BENEFIT FROM A HEALTH PLAN THROUGH THEIR EMPLOYMENT CONTRACT

Brazilian State Region Number of

Beneficiaries % Individual or Familiar

% Collective (Company)

São Paulo Southeast 18 805 870 19% 80%

Rio de Janeiro Southeast 6 059 970 19% 80%

Minas Gerais Southeast 5 380 330 15% 84%

Paraná South 2 900 763 26% 74%

Rio Grande do Sul South 2 789 899 14% 85%

Bahia Northeast 1 678 221 17% 83%

Santa Catarina South 1 517 826 12% 87%

Pernambuco Northeast 1 434 487 28% 72%

Ceará Northeast 1 278 580 31% 68%

Espírito Santo Southeast 1 130 645 13% 86%

Goiás Central West 1 109 992 23% 76%

Federal District (DF) Central West 952 797 4% 96%

Pará North 891 646 34% 66%

TOP 13 STATES - NR OF PRIVATE INSURANCE BENEFICIARIES

Rio Grande

do Sul

Paraná

São

Paulo Rio de

Janeiro

Minas

Gerais

Bahia

Goiás

Ceará

Santa

Catarina

Pernambuco

Pará

DF

Espírito

Santo

BUSINESS SWEDEN 28 OCTOBER, 2015 8

RECENT REGULATION OPENS UP FOR FOREIGN

OWNERSHIP OF HOSPITALS AND CLINICS IN BRAZIL

BRAZILIAN’S FEDERAL

CONSTITUTION FEDERAL LAW NO 8.080

Creates an universal public

healthcare system

Article 199 of the Federal

Constitution (CF-1988) states that

health care is open to private

enterprise. However paragraph 3

(§ 3º) declares the following:

§ 3º It is forbidden the direct or

indirect participation of foreign

companies or foreign capital

in healthcare in the country, except

in cases provided by law

AS FROM JANUARY 2015 IT IS NOW POSSIBLE FOR SWEDISH INVESTORS TO FULLY ENTER THE BRAZILIAN HEALTHCARE MARKET

FEDERAL LAW NO 13.097

The exceptions were

presented by the Federal Law

No 8.080: international

insurance companies,

laboratories,

pharmacies, diagnostic

companies, donations,

all authorized in the country in

1990

Law No 13.097, which amended

the Federal Law No 8.080

opened up additional areas where foreign capital is now

allowed for investments in

clinics and hospitals

1988

1990

2015

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

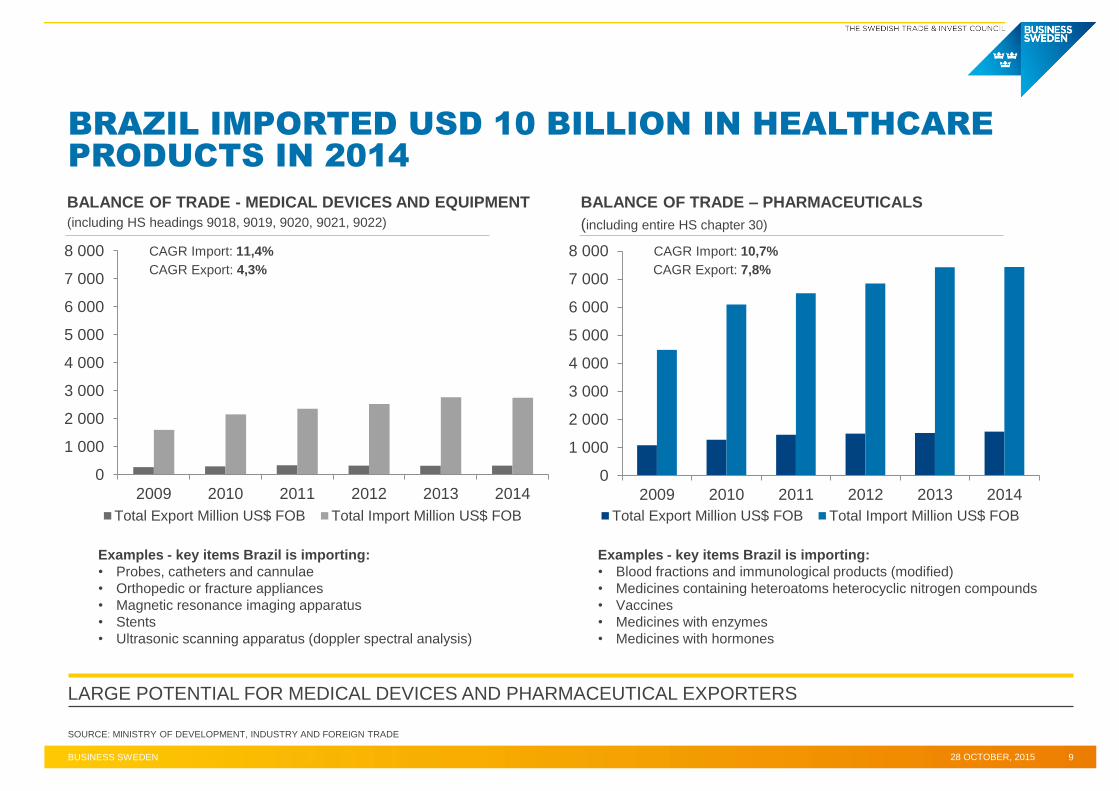

2009 2010 2011 2012 2013 2014

Total Export Million US$ FOB Total Import Million US$ FOB

BUSINESS SWEDEN 28 OCTOBER, 2015 9

BRAZIL IMPORTED USD 10 BILLION IN HEALTHCARE

PRODUCTS IN 2014

SOURCE: MINISTRY OF DEVELOPMENT, INDUSTRY AND FOREIGN TRADE

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2009 2010 2011 2012 2013 2014

Total Export Million US$ FOB Total Import Million US$ FOB

BALANCE OF TRADE - MEDICAL DEVICES AND EQUIPMENT

(including HS headings 9018, 9019, 9020, 9021, 9022)

BALANCE OF TRADE – PHARMACEUTICALS

(including entire HS chapter 30)

CAGR Export: 7,8%

CAGR Import: 10,7%

CAGR Export: 4,3%

CAGR Import: 11,4%

LARGE POTENTIAL FOR MEDICAL DEVICES AND PHARMACEUTICAL EXPORTERS

Examples - key items Brazil is importing:

• Probes, catheters and cannulae

• Orthopedic or fracture appliances

• Magnetic resonance imaging apparatus

• Stents

• Ultrasonic scanning apparatus (doppler spectral analysis)

Examples - key items Brazil is importing:

• Blood fractions and immunological products (modified)

• Medicines containing heteroatoms heterocyclic nitrogen compounds

• Vaccines

• Medicines with enzymes

• Medicines with hormones

Documentation

Required* Class I Class II Class III Class IV

Cadaster

(ANVISA)

Register

(ANVISA)

For register within ANVISA, products are framed in the following risk

classes:

Class I – low risk for individuals and public health;

Class II – medium risk for individuals and/or low risk for public health;

Class III – high risk for individuals and/or medium risk for public health;

Class IV – high risk for individuals and public health.

In accordance with ANVISA, Class III and Class IV products need

mandatory registration within ANVISA, while only some Class II products

need registration, such as medical equipment, due to special risks. Other

Class II products and all of the products Class I need a cadaster*.

BUSINESS SWEDEN 28 OCTOBER, 2015 10

ANVISA IS THE NATIONAL SURVEILLANCE AGENCY FOR

PHARMACEUTICALS AND MEDICAL DEVICES

COMPLYING WITH ANVISA STANDARDS ESSENTIAL FOR ENTERING BRAZILIAN MARKET

SOURCE: BUSINESS SWEDEN DESK RESEARCH AND INTERVIEWS WITH ANVISA *DEPENDING OF CLASSIFICATION PRODUCT WILL NEEDED A CADASTER (STANDARD REGISTRATION) OR GO THROUGH A COMPLETE

REGISTRATION, INVOLVING A SIGNIFICANTLY MORE RIGOROUS EVALUATION PROCESS.

= yes, need approval = no, do not need approval

= only certain products need approval

Formulating rules

Establishing controlling mechanisms

Assessing risks and adverse events regarding

health provision in hospitals, clinics, and health posts

Enforcing rules

Nationwide health

surveillance

services

ANVISA

NATIONAL HEALTH SURVEILLANCE AGENCY (ANVISA)

BUSINESS SWEDEN 28 OCTOBER, 2015 11

BRAZIL’S HEALTH CARE MARKET IS CHALLENGING BUT

OFFERS GREAT BUSINESS OPPORTUNITIES

Which

opportunities

make Brazil

interesting?

What

challenges

should companies

be ready to face?

High production costs

Excessive bureaucracy for registration of products

Complex tax system

Current economic crisis

Complex SUS funding

system

Precarious situation in

healthcare public institutions

Complex public hospital

purchase process

High future investments

Oil royalties will increase public health expenditure

New opening for foreign capital in clinics and hospitals

Aging population, increase of welfare diseases

Increasing imports of healthcare products

Large market of 200 million people, with 100% public

health insurance coverage and strong private sector

Investments

Stakeholders

Market

Investments

Business in Brazil

Public System Presence of top quality

hospitals

High number of

healthcare institutions

Developing pharma

industry

Public health system is historically underfunded

Most of health expenditure comes from the private sector

Total healthcare expenditure per capita is low

SIGNIFICANT BUSINESS POTENTIAL ON LARGE AND GROWING BUT COMPLEX HEALTH CARE MARKET

BUSINESS SWEDEN OFFERS A FULL SERVICE

PORTFOLIO FOR EFFICIENT MARKET ENTRY

* BSO SERVICES INCLUDE: OFFICE PLACE & SERVICE, ADMINISTRATION, COMPANY ESTABLISHMENT (INCL

LEGAL ADRESS) , DELEGATE MANAGER AND FINANCIAL ANALYSIS

28 OCTOBER, 2015 BUSINESS SWEDEN 12

ICT

OUR INDUSTRY FOCUS

HEALTH CARE

& LIFE

SCIENCE

MATERIALS &

MANUFACTU

RING

SECURITY CREATIVE

INDUSTRIES

ENERGY &

ENVIRONMENT

TRANSPORT

SYSTEMS

OUR CUSTOMERS

SWEDISH COMPANIES EXPANDING

INTO BRAZIL LOCAL SUBSIDIARIES OF

SWEDISH COMPANIES SWEDISH GOVERNMENT

OUR MARKET OFFERING

MARKET ENTRY

STRATEGY

OUR STRENGTH

PARTNER

SEARCH STAKEHOLDER

MANAGEMENT

IMPORT

ANALYSIS

SOURCING

ANALYSIS ACQUISITION

SUPPORT

MARKET

ANALYSIS

BUSINESS

SUPPORT

OFFICE *

RECRUITING

EXPERIENCED

TEAM WITH

INDUSTRY FOCUS

UNIQUE OWNERSHIP PROVIDE

ACCESS TO THE SWEDISH

GOVERNM.& FUNDING STRUCTURE

GLOBAL

PRESENCE

LOCAL& SWEDISH

PERSPECTIVE TO BUSINESS

OPPORTUNITIES

ACCESS TO HIGH LEVEL

AUTHORITIES & BUSINESS

NETWORKS IN BRAZIL

CONTACT US

BUSINESS SWEDEN IN BRAZIL

Rua Joaquim Floriano, 466 – cj 1908 – Ed. Office

BR 04534-002 – São Paulo - Brazil

Phone: +55 11 2137 4400

Fax: +55 11 2137 4425