restructuring the brazilian metallurgical sector - bndes

TRANSCRIPT

RESTRUCTURING THE BRAZILIAN METALLURGICAL SECTOR Maria Lúcia Amarante de Andrade Luiz Maurício da Silva Cunha Guilherme Tavares Gandra* * Respectively, manager, economist and engineer of the BNDES’ Mining and Metallurgy Department. The authors thank Eliane Figueredo Costa de Oliveira for her collaboration.

- 2 -

Abstract The restructuring process of the Brazilian metallurgical sector has been characterized by the activity of a set of forces that obscure the roles of cause and effect, but which, in an independent fashion, have been driving the metallurgical sector market towards a new temperament. In this study, we seek to show how these various interlinked factors have determined the modifications which have been observed in the metallurgical market over the past 10 years. For this, we begin by making evident those determining elements that are necessary for unraveling the restructuring process through a description of the history of the preceding period. Following this, each of the principal forces related to the restructuring process are analyzed, among them the privatization process, the specialization and concentration of production, and technological development. The current structure of the Brazilian metallurgical sector is presented along with recent changes, including the role of the BNDES as financier of the development of the country’s metallurgical sector. At the end, we will outline the likely direction that the metallurgical market will take as a result of these tendencies.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 3 -

Introduction After a situation of great stagnation during the decade of the 1980s, the Brazilian metallurgical industry, due to diverse factors, reacquired its dynamism, and in the last 10 years has experienced a complete transformation of its international scenario. Through the rationalization of investments, cost reductions, modernization of production processes and the taking advantage of synergies, great improvements were aggregated in the quality/competitiveness/productivity triad. The many privatizations in the sector, initiated in 1988, marked the beginning of the current phase of restructuring. Associated with this, and also very relevant, technological innovations for products and processes contributed to changing the concepts and decisions fundamental to the development of the companies. Currently, the metallurgical sector faces a new reality of adapting to the norms imposed by the globalization of markets and by the recent international crises. In this way, the metallurgical environment has been acquiring new features: more international, less labor-intensive, more concentrated, more adaptive to new environmental questions, with investments being targeted toward smaller and more versatile industrial complexes and with corporations holding increasingly greater shares of production. History To understand the true revolution that has occurred in the metallurgical world over the last 10 years, it is necessary to quickly review the situation of the sector before its restructuring. From the Postwar to the Decade of the 1970s The postwar period was marked by an enormous development in Brazilian metallurgical production (Graph 1), in the same way that occurred in other industries. Between 1945 and 1979, the average annual rate growth for world production of crude steel was about 5%. The reconstruction of a world destroyed by war helped industrial activity, favoring some countries in the rapid development of their economies. Graph 1 Evolution of World Production of Crude Steel - 1945/97 Source: International Iron and Steel Institute (IISI). The United States has always been characterized by exclusively private activity in the metallurgical industry. Actually, in the entire history of its metallurgical sector no state company was ever formed, a fact that is justified by the very dynamic nature of the North American private sector. Its strong culture, the size and structure of its capital markets, in addition to the frequent mergers and acquisitions which occurred, favored the formation of great corporations – holding companies that acted diversely in several economic sectors, and strong enough not to need state intervention.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 4 -

The four largest producers of steel in United States (US Steel, Nucor, Bethlehem Steel and LTV) were formed from the metallurgical divisions of these diversified groups. LTV is a good example which, according to Gazeta Mercantil’s “Panorama Sectorial”, started from a series of stockholders’ movements in the 1950s and 1960s, as can be observed in the following events: • 1956: Ling Eletric acquires L.M. Eletronics; • 1959: Ling Eletric acquires Altec Eletronics; • 1960: Ling Eletric founds Temco (electronics and missiles); • 1961: Ling-Temco acquires control of Chance Vought (producer of flat steel for the

Navy), forming LTV (Ling-Temco-Vought); and • 1964: LTV becomes a holding, divided into three companies: LTV Aerospace, LTV Ling

Altec and LTV Electrosystems.

Japan, which had its metallurgical sector controlled by the State, financially strengthened its steel plants, privatizing them with great stock participation on the part of banks. After the end of the Second World War, Japan Iron & Steel (state controlled) was dissolved, giving origin to Iwata Iron & Steel and Fuji Iron & Steel. The latter, after the mergers and acquisitions wave of the 1960s, eventually created Nippon Steel (today the world’s largest producer). The countries of Western Europe, for the most part, sought to nationalize in order to increase the efficiency of their industries, which were fragmented and didn't have the minimum scale necessary for the business. In this way, for example, appeared Usinor-Sacilor (in France), British Steel (in the United Kingdom) and Cockerill-Sambre (in Belgium). These nationalizations were founded on structures that already existed, objectified by the need to eliminate the risk of bankruptcies (and consequent mass dismissals) and to later adjust their optimal scale for the market. Known as the industrialized countries, they reached a period of maturation in their metallurgical industries in the beginning of the 1980s, due to the deceleration growth in their economies. In Eastern Europe, the decision for nationalization was primarily political. Recognizing the strategic position of metallurgical production for the sustaining of development, the so-called developing economies in regions like Latin America, Asia, Africa and Middle East, invested (through the State) in the construction of metallurgical parks, with emphasis on the creation of capacity. The main reasons for these nationalization were, besides political questions, the fragility of the private sector, the knowledge of the importance of scale and the need for intervention in order to accelerate a late industrialization. Moreover, they possessed a character that was different to the European nationalizations, where the majority of state ownerships occurred with the objective of restructuring. Besides this, another aspect which shows the difference between these two movements is the fact that, in the developing countries, the state-run companies were not just controlled (as occurred in most of the European countries), but were also built by the national governments. The process of nationalization was, therefore, another salient factor of the postwar period (Table 1). It can be observed that some countries of Europe like Italy, Austria and Spain, also accompanied this movement, while in the developing countries the incipient metallurgical base, even though outdated and state-run, was fundamental to the

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 5 -

development of their internal industrial sectors. This also impeded the industrialized countries expanding their growth through exports. Table 1 Creation of the Nationalized Steel plants

Decades Countries 20s and 30s Italy, South Africa 40s and 50s Mexico, Brazil, Argentina, Austria, Spain, Egypt 60s Finland, Venezuela, South Korea 70s Taiwan, Indonesia, Iran, Saudi Arabia 80s Malaysia

Source: Germano Mendes de Paula, Privatização e Estrutura de Mercado na Indústria Siderúrgica Mundial. In Brazil, the creation of state-run steel plants was part of the import substitution model whose objective was to decrease dependency on manufactured products from the industrialized countries (Table 2). Among these, the main formation was the Companhia Siderúrgica Nacional (CSN), which also had the first integrated coke-fired steel plant in the country, located in the municipal district of Volta Redonda (RJ), with an annual capacity of 270,000 t of steel (about 6% of its current capacity). Table 2 Metallurgical companies established by the Brazilian Government

Creation/ Foundation

Initiation of Operation

Company

1939 1959 Cia. Siderúrgica do Nordeste (Cosinor) 1941 1946 Cia. Siderúrgica Nacional (CSN) 1942 1942 Cia. Ferro e Aço de Vitória (Cofavi) n.a. 1944 Cia. Siderúrgica de Mogi das Cruzes (Cosim)

1944 1949 Aços Especiais Itabira (Acesita) 1953 1963 Cia. Siderúrgica Paulista (Cosipa) 1956 1962 Mills Siderúrgicas de Minas Gerais (Usiminas) 1961 1973 Aços Finos Piratini 1963 1973 Mill Siderúrgica da Bahia (Usiba)

1963/75 1985 Aço Minas Gerais (Açominas) 1976 1983 Cia. Siderúrgica de Tubarão (CST)

Source: IBS, Empresas Siderúrgicas do Brasil (1991). Obs.: Aparecida and Cimetal have not been included since were not founded by the State.

In the decade of the 1950s, the construction of Cosipa and Usiminas was initiated, which were responsible for a great expansion in the production of flat steel. In the midst of the growth of the Brazilian industrial park, demand and production increased rapidly, causing imports to decrease considerably. In 1966, Brazil became the largest producer of steel in Latin America. In 1973, Siderbrás, a state holding company responsible for controlling and coordinating national metallurgical production, was created. In the 1970s, the Brazilian government sought foreign financing to invest in increasing domestic capacity and technological development, mainly in order to attend to the growing demand for flat steel. It worth emphasizing that the long steel segment, which allows smaller scales for initial operation, was supplied mainly through private companies.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 6 -

Before the Restructuring (1980s) In the middle of the 1980s, world steel production stabilized at the average level of 710 million t/year, indicating a phase of maturity of the metallurgical industry. That stabilization was due mainly to the deceleration of growth in the developed economies, and the threat of steel substitute materials such as plastic, aluminum and ceramics. The maturity of the industry due to the stability of internal demand is shown below (Graph 2). Metallurgical products, whose demand possesses a strong correlation with the degree of economic development of a society, constitute a basic input for the development of the market. Graph 2 Visible Per Capita Consumption of Steel: Industrialized countries - 1982/87 Source: IISI. The world metallurgical market has been characterized by a strong government participation through state companies, which controlled about 70% of world capacity and were concentrated mainly in Western European countries, those still developing, and those with centralized economies. Japan and United States, without nationalized steel plants, began efforts to overcome the obstacles presented by the stagnation of their consumer markets. In a general way, the metallurgical industry has always been globally recognized for its importance in the economic development of nations, for supplying input for the development of infrastructure, and for supplying the construction, production, and consumer goods industries, especially the automotive industry. The sector is also characterized by responding to a substantial portion of GDP, and for the generation of employment. With respect to equity, the metallurgical sector has had its activity mostly controlled by domestic capital, be it private or state. Metallurgical companies, in general, produced just enough for their domestic markets, and restricted their operation in foreign markets to the exporting of goods and technology. This was justified by the high costs of building the plants, which, in their great majority, were integrated. The presence of multinational investments in the metallurgical sector was not significant. More specifically in Brazil, throughout the 1980s, the so-called “lost” decade, the country’s foreign debt crisis provoked a decline in the internal demand for steel. The excess of

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 7 -

current capacity therefore forced the steel plants to export their products with a smaller return, in such a way as to guarantee their placement in the international market and the maintenance of national production. Profits and investments suffered a significant decline due to low prices, foreign as much as internal (caused by government policy price controls for combating inflation), and to less availability of foreign credit. Thus, the crisis of the Brazilian government prevented investments from being made in the modernization of the national industrial park, distancing it more and more from international standards of quality, productivity and competitiveness. The national metallurgical industry had a very fragmented production, but one which operated on a self-sufficient basis for all products, and at any cost. In this way it had a certain vulnerability, considering that the process of opening the economy had also began, not to mention as the globalization of the world market. Table 3 Indicators of the Brazilian Metallurgical Sector - 1980s

1980 1982 1984 1986 1988 1990 Production (Millions of t) 15.34 13.00 18.39 21.23 24.66 20.57 % Production in Latin America 53.2 48.7 55.3 56.7 58.2 53.8 Internal sales (Millions of t) 10.71 8.84 9.33 12.52 11.08 8.61 Exports (Millions of t) 1.50 2.39 6.46 6.14 10.92 9.00 Revenues (US$ Millions) n.a. n.a. 6,081 7,069 9,905 10,627 Investments (US$ Millions) 2,713 2,224 509 548 496 494 Productivity (Base 1980) 100 75 118 118 131 122 Number of Employees (000s) 135.0 127.5 137.9 151.3 151.8 132.7 Source: IBS. As much in Brazil as on the world level, if state participation was fundamental in the beginning, it didn’t have the conditions to complete the capacity cycle of the industry because it presented its own obstacles to development. Influenced by political decisions, state control reduced the responsiveness and freedom of companies to react to the demands of the market and changes in the environment. In a general way, the investments in research for new products and technological processes were insufficient. The companies became slow, out-of-date or even technologically obsolete, not well rationalized, and very cost inefficient, because they were often protected by closed markets. The opening of the markets and the modernization of the metallurgical sector became imperative, since the sector appeared to be entering a stagnation process. A conjunction of forces impelled the world metallurgical industry to be restructured, among which the following deserve mention: * the stagnation of demand in the developed economies; * the growth in the use of material substitutes; * the need for privatization; * the provocation of competition due to globalization; and * the consequent fall in prices and profitability resulting from excess capacity.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 8 -

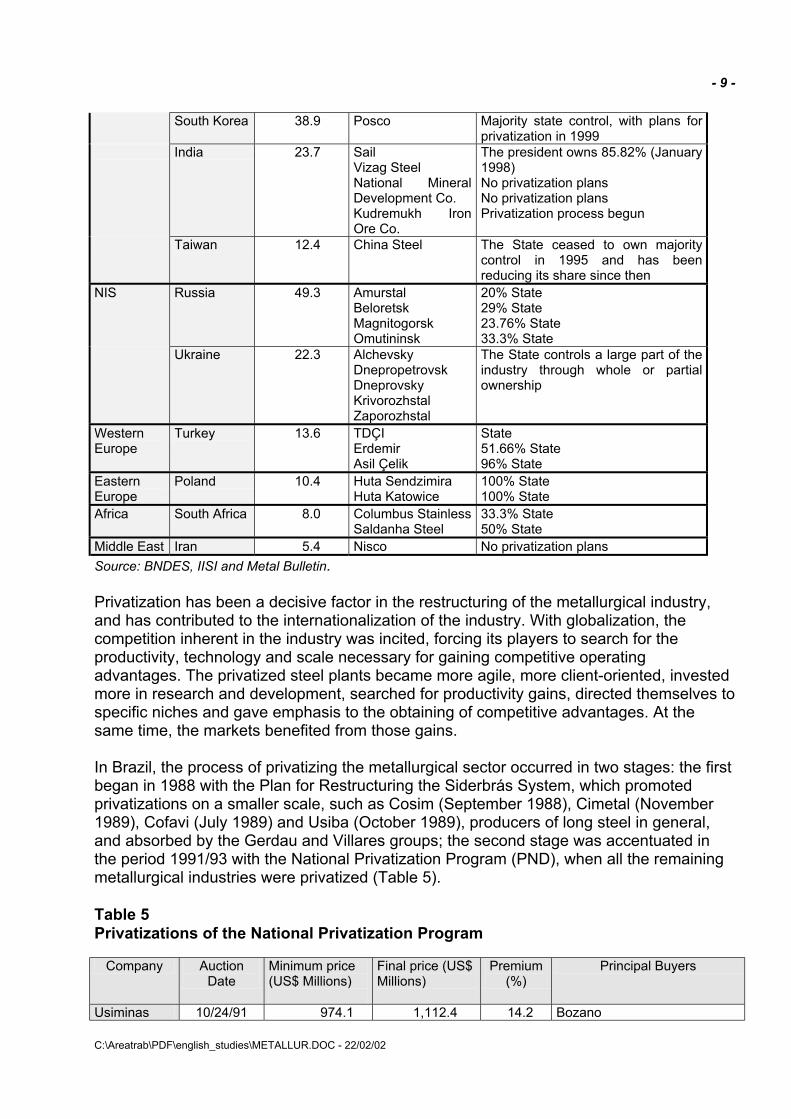

Restructuring the World Metallurgical Sector Privatization Driven by the idea of the opening and globalization of markets, a great process of privatization began in the world metallurgical industry in 1988, characterizing a new stage in the continual and profound transformation of the sector. The predominance of state-run companies generated a certain immobility in the market, besides the fact that they provided low investment in technological research and less speed in the reformulation of productive processes and the consequent obtaining of productivity gains. In such a context, the companies often acted according to political interests, and contrary to a commercial focus. These markets therefore possessed serious obstacles to development. The privatization movement, which can be considered the “fuse” for the restructuring process, has been occurring along the entire decade of the 1990s in a constant and very intense way. To have an idea of this evolution, in 1990 state ownership was 60% of world production, in 1994 it fell to 40%, and today less than 20% remains in the hands of the state. The most relevant privatizations occurred in Western Europe and in Latin America. In 1986, state companies controlled more than half the production of steel in 10 European countries (Austria, Belgium, Spain, Finland, France, Italy, Norway, Portugal, United Kingdom and Sweden). By the end of 1997, there remained only one state-run steel plant, Belgium’s Cockerill-Sambre, which in October of 1998 was acquired by Usinor (stock share of 53%), the fourth-largest manufacturer of steel in Europe, for US$ 770 million. Another important event was the acquisition in 1997 of the Spanish state-owned Companhia Siderúrgica Integral (CSI) by Arbed of Luxembourg. In 1990, about 50% of steel production in Latin America corresponded to state-run companies. By the end of 1997, the sector had already been completely privatized. The last company to be privatized was the Venezuelan Siderúrgica del Orinoco (Sidor), completely acquired for US$ 1.78 billion by a Latin-American consortium formed by Mexican Hylsamex (30%) and Tamsa (17,5%), Argentina’s Siderar (17,5%) and Techint (5%), Brazil’s Usiminas (10%), and Venezuela’s Sivensa (20%). The remaining state-owned companies in the world are located primarily in the Asian countries, Eastern Europe, the Middle East, and Africa (Table 4). Table 4 State Share in the World’s Principal Countries, By Region

Region Country Production (Millions of t)

in 1996

Main Companies with State Share

Situation

Asia China 100.0 Shougang, Baoshan Maanshan, Anshan

Total state control over industry

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 9 -

South Korea 38.9 Posco Majority state control, with plans for privatization in 1999

India 23.7 Sail Vizag Steel National Mineral Development Co. Kudremukh Iron Ore Co.

The president owns 85.82% (January 1998) No privatization plans No privatization plans Privatization process begun

Taiwan 12.4 China Steel The State ceased to own majority control in 1995 and has been reducing its share since then

NIS Russia 49.3 Amurstal Beloretsk Magnitogorsk Omutininsk

20% State 29% State 23.76% State 33.3% State

Ukraine 22.3 Alchevsky Dnepropetrovsk Dneprovsky Krivorozhstal Zaporozhstal

The State controls a large part of the industry through whole or partial ownership

Western Europe

Turkey 13.6 TDÇI Erdemir Asil Çelik

State 51.66% State 96% State

Eastern Europe

Poland 10.4 Huta Sendzimira Huta Katowice

100% State 100% State

Africa South Africa 8.0 Columbus Stainless Saldanha Steel

33.3% State 50% State

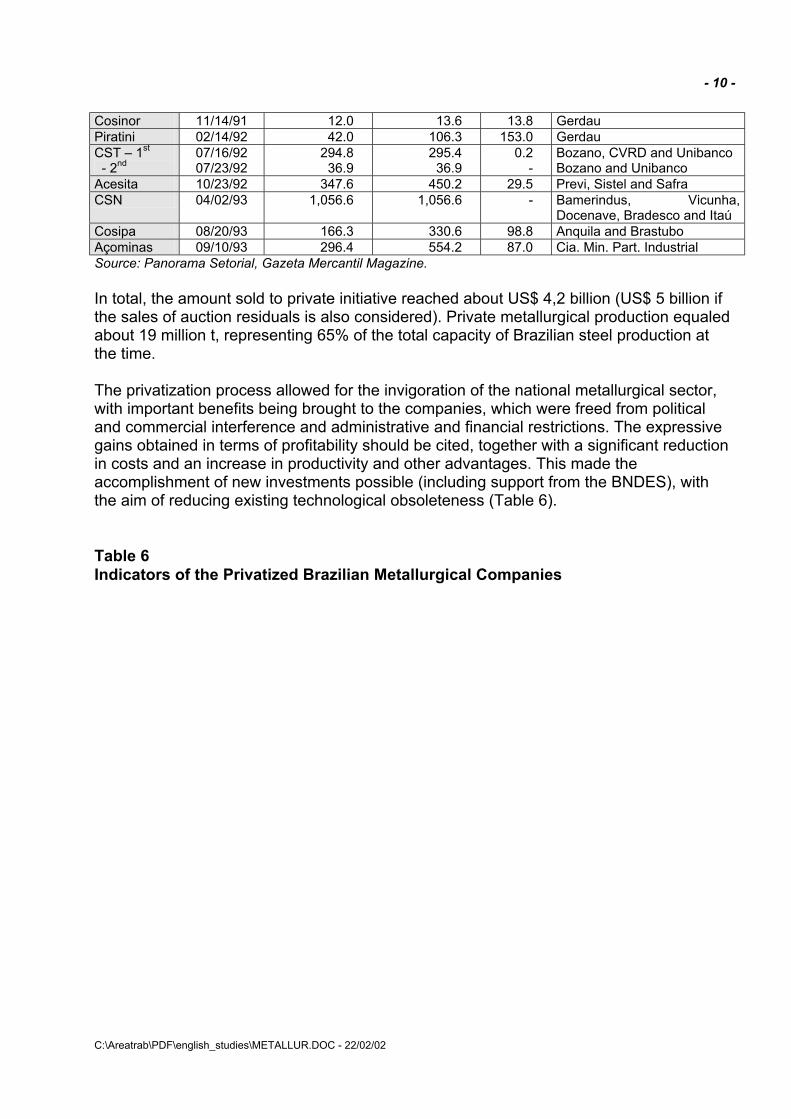

Middle East Iran 5.4 Nisco No privatization plans Source: BNDES, IISI and Metal Bulletin. Privatization has been a decisive factor in the restructuring of the metallurgical industry, and has contributed to the internationalization of the industry. With globalization, the competition inherent in the industry was incited, forcing its players to search for the productivity, technology and scale necessary for gaining competitive operating advantages. The privatized steel plants became more agile, more client-oriented, invested more in research and development, searched for productivity gains, directed themselves to specific niches and gave emphasis to the obtaining of competitive advantages. At the same time, the markets benefited from those gains. In Brazil, the process of privatizing the metallurgical sector occurred in two stages: the first began in 1988 with the Plan for Restructuring the Siderbrás System, which promoted privatizations on a smaller scale, such as Cosim (September 1988), Cimetal (November 1989), Cofavi (July 1989) and Usiba (October 1989), producers of long steel in general, and absorbed by the Gerdau and Villares groups; the second stage was accentuated in the period 1991/93 with the National Privatization Program (PND), when all the remaining metallurgical industries were privatized (Table 5). Table 5 Privatizations of the National Privatization Program

Company Auction Date

Minimum price (US$ Millions)

Final price (US$ Millions)

Premium (%)

Principal Buyers

Usiminas 10/24/91 974.1 1,112.4 14.2 Bozano

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 10 -

Cosinor 11/14/91 12.0 13.6 13.8 Gerdau Piratini 02/14/92 42.0 106.3 153.0 Gerdau CST – 1st - 2nd

07/16/92 07/23/92

294.8 36.9

295.4 36.9

0.2 -

Bozano, CVRD and Unibanco Bozano and Unibanco

Acesita 10/23/92 347.6 450.2 29.5 Previ, Sistel and Safra CSN 04/02/93 1,056.6 1,056.6 - Bamerindus, Vicunha,

Docenave, Bradesco and Itaú Cosipa 08/20/93 166.3 330.6 98.8 Anquila and Brastubo Açominas 09/10/93 296.4 554.2 87.0 Cia. Min. Part. Industrial Source: Panorama Setorial, Gazeta Mercantil Magazine. In total, the amount sold to private initiative reached about US$ 4,2 billion (US$ 5 billion if the sales of auction residuals is also considered). Private metallurgical production equaled about 19 million t, representing 65% of the total capacity of Brazilian steel production at the time. The privatization process allowed for the invigoration of the national metallurgical sector, with important benefits being brought to the companies, which were freed from political and commercial interference and administrative and financial restrictions. The expressive gains obtained in terms of profitability should be cited, together with a significant reduction in costs and an increase in productivity and other advantages. This made the accomplishment of new investments possible (including support from the BNDES), with the aim of reducing existing technological obsoleteness (Table 6). Table 6 Indicators of the Privatized Brazilian Metallurgical Companies

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 11 -

Company Year Crude Steel Production (Thousands

of t)

Revenues (US$

millions)

Net Profit (US$

millions)

Net Equity (US$

millions)

Return on Net Equity

(%)

Number of Employeesa

Productivity per (t/Many

Year)

Acesita 1992 700 397 (100) 428 - 7,462 94 1993 768 463 31 499 6.2 5,584 138

1995 612 678 32 1,064 3.0 4,996 123 1997 632 523 3 1,051 0.3 4,247 149

Açominas 1992 2,127 394 38 2,567 1.5 6,479 328 1993 2,375 430 55 2,852 1.9 6,261 379 1995 2,435 678 35 2,244 1.6 5,060 481 1997 2,376 571 (37) 1,718 - 3,906 608

Cosipa 1992 2,960 863 (297) 793 - 16,757 177 1993 2,952 799 (579) 1,351 - 13,544 218 1995 3,598 1,222 74 2,059 3.6 9,182 391 1997 3,791 1,178 (109) 1,456 - 7,681 494

CSN 1992 4,363 1,516 125 4,136 3.0 18,162 240 1993 4,337 1,604 22 3,937 0.6 17,904 242 1995 4,340 2,206 110 5,905 1.9 13,900 312 1997 4,796 2,290 403 3,942 10.2 9,400 510

CST 1992 3,179 546 (149) 1,972 - 4,892 650 1993 3,571 617 33 1,923 1.7 5,085 702 1995 3,739 931 190 3,129 6.1 4,350 859 1997 3,714 876 113 2,778 4.1 3,622 1,025

Usiminas 1992 4,033 1,256 123 1,395 8.8 12,144 301 1993 4,132 1,212 246 1,557 15.8 10,944 362 1995 4,160 1,740 336 2,813 11.9 9,890 375 1997 3,930 1,618 325 2,699 12.1 8,436 466

Sources: Economática, IBS, periodicals, companies, and the BNDES. a Some figures are estimates. With respect to the financial aspect of the industry, it should be emphasized that the restructuring plan was important for the recovery of these companies, which underwent alterations in their debt structure before they were transferred to the private sector. The efforts of the State in the financial restructuring of the steel plants is worth mentioning in this regard. It should also be pointed out that these privatized companies started to destine the greater part of their production to the internal market, at better prices than those sold for exports. The controlling of prices had already ceased to exist prior to the privatization process. These efforts should not be forgotten when the current financial-accounting situation is analyzed. Another important result was the professionalization of the company administrations brought about by the new controllers, and their reorientation towards the obtaining of results with a wider business vision, including: • new corporate strategies; • the strengthening of companies into managerial groups that were compatible with the

new economic opening; • participation in new investments, including abroad; and • the taking advantage of operational synergies.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 12 -

Commercialization strategies also became more aggressive, such as the providing of services in partnership with customers, the acquisition of steel distribution companies, promotional campaigns in the media, and the creation of distribution channels abroad. Parallel to privatization, the process of opening the sector began, with a reduction of the government’s price controls as well as the beginning of economic liberalization. Import quotas for metallurgical and technological products, as well as non-tariff barriers, were reduced. In addition to this, the “Modernization Program” of the Brazilian metallurgical sector began in earnest after 1994, with investment plans totaling an estimated R$ 10.4 billion to be applied over the period 1994/2000. These factors have also influenced the evolution of the sector in a positive manner. Growth of the Developing Countries The beginning of the maturation of the metallurgical industry was identified with a certain delay on the part of the industrialized countries. Japan and Europe invested strongly in capacity increases even though domestic consumption was no longer providing significant growth. In the attempt to sustain growth through exports, the industrialized countries “collided with” those that were still developing, which had installed capacities that were sufficient to not only supply their internal markets, but also to market their surpluses abroad. While for the industrialized countries in general, production levels have remained stable during the 1990s, for developing countries a boom in the production of steel has been verified. This occurred due to two main reasons: • the demand for metallurgical products is greater during the full growth period of a

country, when the efforts to implement economic infrastructure and expand the industrial sector become more intense; and

• there was already production capacity in these countries that had been built with strong government support and from the importation of technological processes, in general from Japan and of Germany.

The greatest growth in steel production growth over the period 1988/96 came from the Asian countries. In China, production developed at an annual average rate of 6.7%, and in Korea, 9.3%, while in Japan it stayed practically stable, with even a small drop. It is also worth mentioning that over the same period the metallurgical productions of India and of Mexico grew at annual average rates of 6.5% and 6.8%, respectively. Graph 3 Share of Blocs of Countries in World Production and Exports - 1987 and 1996 (In %)

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 13 -

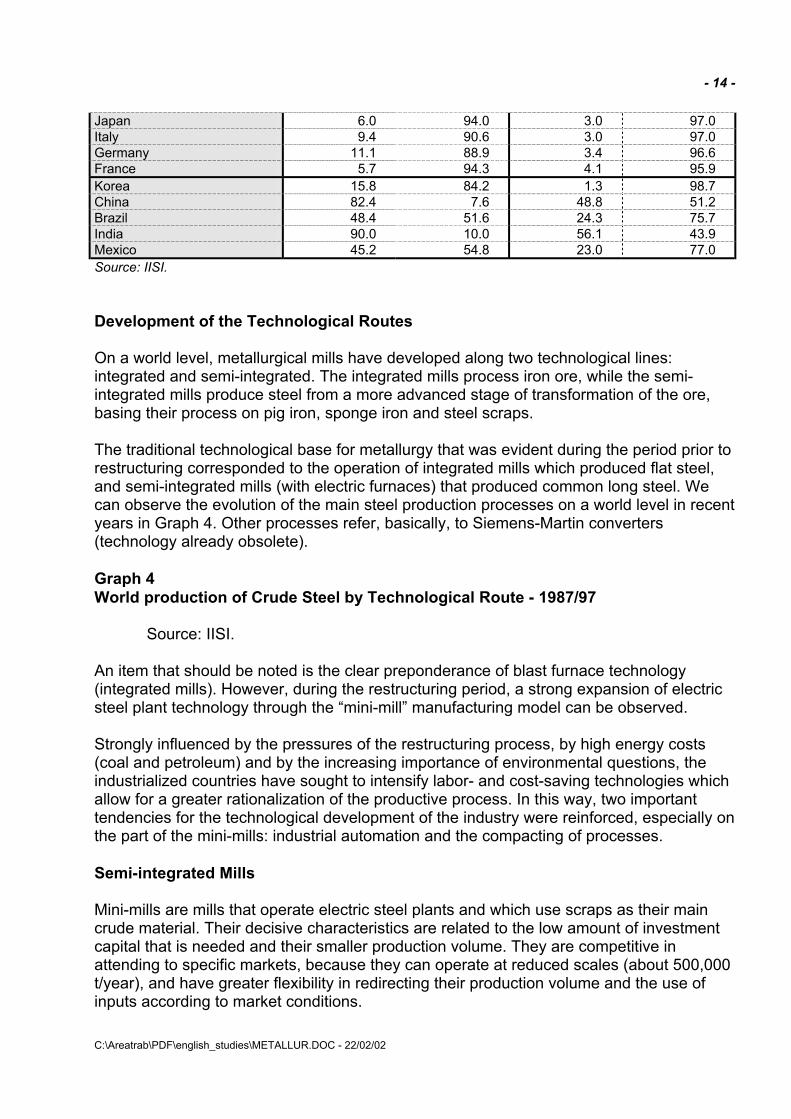

Source: IISI. The average annual rate growth for the production of crude steel in Latin America in the period 1988/96 reached 1. 9%, greater, moreover, than Brazil’s, which corresponded to a growth of 0.2%. This provoked a change in the relative participation of countries in the world production of steel (Graph 3). The share of the developing countries grew from 4.3% (1973) to 18.1% (1994) in production, and from 2.3% (1970) to 16.1% (1994) in exports. The New International Division of Production In immediate response to the structural excess of supply and the evolution of the developing countries, the industrialized countries restructured their steel plants in the sense of rationalizing production, developing new technological processes, and increasing the mix of products. In such a way, several other tendencies which also characterize this restructuring period were determined. Among them, reduction units were deactivated or simply not built, since they required investments with a smaller economic return and involved high energy consumption and pollution generation. They concentrated instead on building rolling units. Besides this, the industrialized countries intensified their focus on differentiated products with a higher aggregate value (such as coated and special steel), which provide a greater financial return through higher prices. In spite of having large steel production plants, the developing countries didn't make significant technological progress. Their growing production volumes were concentrated in more simple products and by-products, that is to say, with lower aggregate value. Thus a new international division of metallurgical production was established. The developing world concentrated more on the production and exportation of mainly semi-finished steel, steel plates and coiled hot-rolled strips, becoming potential suppliers to the industrialized world, which, in turn, began to give more emphasis to the so-called finishing facilities, preparing special products with a higher aggregate value (Table 7). Table 7 Share of Metallurgical Products in the Production of Selected Countries - 1987 and 1996 (In % of Crude Steel Production) 1987 1996

COUNTRY Semi-Finished Rolled Semi-Finished Rolled United States 40.2 59.8 6.7 93.3

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 14 -

Japan 6.0 94.0 3.0 97.0 Italy 9.4 90.6 3.0 97.0 Germany 11.1 88.9 3.4 96.6 France 5.7 94.3 4.1 95.9 Korea 15.8 84.2 1.3 98.7 China 82.4 7.6 48.8 51.2 Brazil 48.4 51.6 24.3 75.7 India 90.0 10.0 56.1 43.9 Mexico 45.2 54.8 23.0 77.0 Source: IISI. Development of the Technological Routes On a world level, metallurgical mills have developed along two technological lines: integrated and semi-integrated. The integrated mills process iron ore, while the semi-integrated mills produce steel from a more advanced stage of transformation of the ore, basing their process on pig iron, sponge iron and steel scraps. The traditional technological base for metallurgy that was evident during the period prior to restructuring corresponded to the operation of integrated mills which produced flat steel, and semi-integrated mills (with electric furnaces) that produced common long steel. We can observe the evolution of the main steel production processes on a world level in recent years in Graph 4. Other processes refer, basically, to Siemens-Martin converters (technology already obsolete). Graph 4 World production of Crude Steel by Technological Route - 1987/97 Source: IISI. An item that should be noted is the clear preponderance of blast furnace technology (integrated mills). However, during the restructuring period, a strong expansion of electric steel plant technology through the “mini-mill” manufacturing model can be observed. Strongly influenced by the pressures of the restructuring process, by high energy costs (coal and petroleum) and by the increasing importance of environmental questions, the industrialized countries have sought to intensify labor- and cost-saving technologies which allow for a greater rationalization of the productive process. In this way, two important tendencies for the technological development of the industry were reinforced, especially on the part of the mini-mills: industrial automation and the compacting of processes. Semi-integrated Mills Mini-mills are mills that operate electric steel plants and which use scraps as their main crude material. Their decisive characteristics are related to the low amount of investment capital that is needed and their smaller production volume. They are competitive in attending to specific markets, because they can operate at reduced scales (about 500,000 t/year), and have greater flexibility in redirecting their production volume and the use of inputs according to market conditions.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 15 -

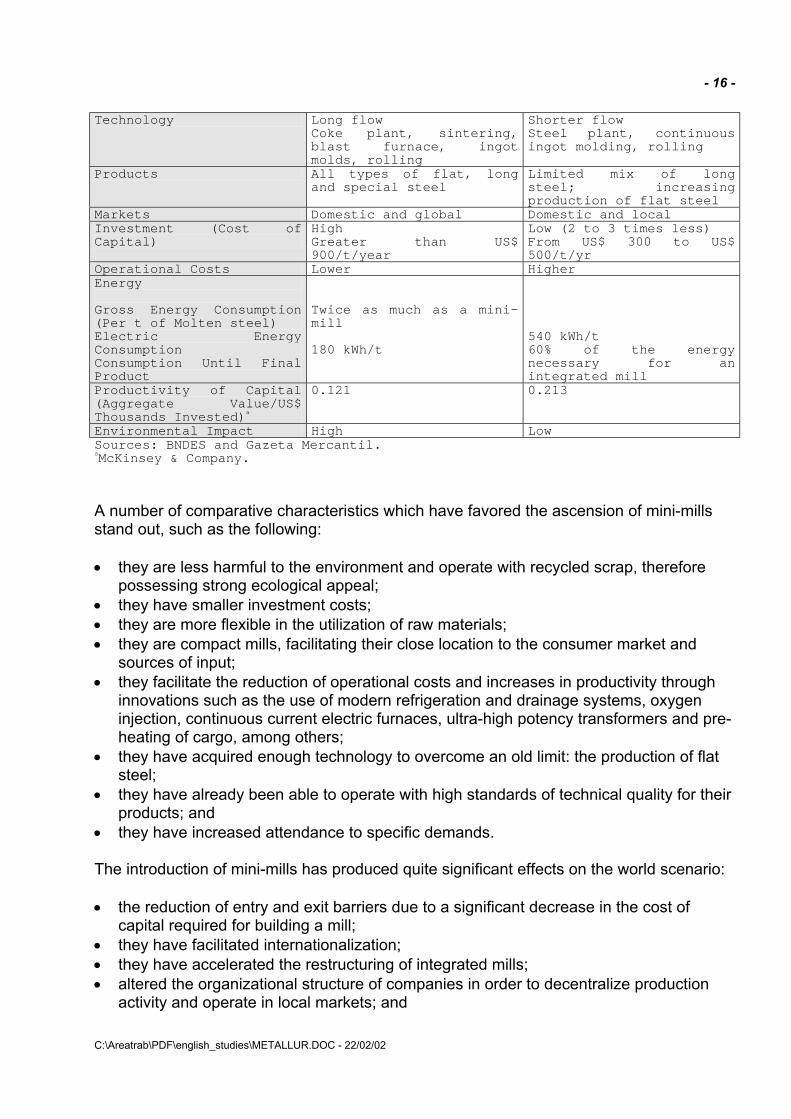

Properly said, the term mini-mill refers to the technological route (electric-arc furnace + continuous ingot molding) used in the manufacturing process, and not to the size of the mill (or company). Mini-mills are characterized by their name because they reduce the minimum optimum scale of operation for a mill. Some North American companies like Northwestern and Chaparral use larger scale mini-mills (1,5 million t), but they are exceptions. Most produce quantities varying between 350,000 and 500,000 t/year in multiple plants (for example, the US’ Nucor and Oregon). Mini-mills date back to the decade of the 1930s, when the United States’ Northwestern Steel and Wire Company began to use electric furnaces to produce steel. However, it was during the restructuring process that the mini-mill won definitive acceptance, because its consolidation is related to the development of equipment (mainly continuous ingot molding) that allows for reducing their minimum optimum scale. The substitution of conventional molding for continuous ingot molding facilitated revenue and productivity increases with the elimination of stages, such as conventional ingot molds, pit furnaces, and primary rolling. Besides this, continuous ingot molding, a much simpler operation, consumed less energy and facilitated the reduction of at least 50% of the labor required for production. This process, which has benefited all metallurgical production, became fundamental to the selection of the mini-mill technological route. Used as an indicator of technological modernization, it reached 77.6% of the world production of crude steel in 1996. In Brazil, it grew 39% over the period 1992/97, passing from 58% to 74% of steel production. The countries that currently stand out in the use of the mini-mills technological route are the United States, Japan and Korea (Graph 5). Graph 5 Production of Crude Steel, by Process, for Selected Countries - 1996 Source: IISI. In 1996, Nucor (the largest of the mini-mills), reached the position of fourth-largest steel mill in North America, narrowly exceeded by only US Steel, Bethlehem and LTV. During the restructuring process, the building of new large integrated mill projects has been losing competitiveness in relation to the mini-mills (Table 8). It is important to stress that the technological process used in a certain area is very dependent on logistical questions, involving the availability and cost of primary inputs, transportation and investment costs, and finally, costs inherent to the peculiarities of each area. Table 8 Comparison of the Technological Routes Integrated Mini-Mills Inputs Iron ore, coke or

charcoal Scraps, sponge iron, pellets, pig iron

Production capacity Large scale 2 million to 10 million t/year

Small scale 100,000 to 1 million t/year

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 16 -

Technology Long flow Coke plant, sintering, blast furnace, ingot molds, rolling

Shorter flow Steel plant, continuous ingot molding, rolling

Products All types of flat, long and special steel

Limited mix of long steel; increasing production of flat steel

Markets Domestic and global Domestic and local Investment (Cost of Capital)

High Greater than US$ 900/t/year

Low (2 to 3 times less) From US$ 300 to US$ 500/t/yr

Operational Costs Lower Higher Energy Gross Energy Consumption (Per t of Molten steel) Electric Energy Consumption Consumption Until Final Product

Twice as much as a mini-mill 180 kWh/t

540 kWh/t 60% of the energy necessary for an integrated mill

Productivity of Capital (Aggregate Value/US$ Thousands Invested)a

0.121 0.213

Environmental Impact High Low Sources: BNDES and Gazeta Mercantil. aMcKinsey & Company. A number of comparative characteristics which have favored the ascension of mini-mills stand out, such as the following: • they are less harmful to the environment and operate with recycled scrap, therefore

possessing strong ecological appeal; • they have smaller investment costs; • they are more flexible in the utilization of raw materials; • they are compact mills, facilitating their close location to the consumer market and

sources of input; • they facilitate the reduction of operational costs and increases in productivity through

innovations such as the use of modern refrigeration and drainage systems, oxygen injection, continuous current electric furnaces, ultra-high potency transformers and pre-heating of cargo, among others;

• they have acquired enough technology to overcome an old limit: the production of flat steel;

• they have already been able to operate with high standards of technical quality for their products; and

• they have increased attendance to specific demands. The introduction of mini-mills has produced quite significant effects on the world scenario: • the reduction of entry and exit barriers due to a significant decrease in the cost of

capital required for building a mill; • they have facilitated internationalization; • they have accelerated the restructuring of integrated mills; • altered the organizational structure of companies in order to decentralize production

activity and operate in local markets; and

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 17 -

• restructured company logistics, with a consequent reduction in transportation costs. Integrated Mills The technological trajectory of the integrated mills has always moved in the direction of increasingly greater economies of scale. The evolution of the efficient minimum scale was dictated by the need for economies in the blast furnaces. During the restructuring process, the growth of mini-mills forced a search for larger productivity gains on the part of the integrated mills. The blast furnace/LD converter technological route still presents certain small growth opportunities in the developing countries, although it is expected to remain stationary in the industrialized countries. Specialists from the sector estimate that the blast furnace will still be the most important reduction process for metallurgical production over at least the next 20 years. Some factors that contribute to the defense of the integrated mills are: • once the crisis has passed, the largest growth in the production of steel in the world

should continue to occur in Southeast Asia: on one hand, China, whose metallurgy is primarily integrated with blast furnaces, is expected to contribute to the continuity of the region’s leadership in this process; and, on other, Korea and Taiwan are expected to continue in the direction of the direct electric/steel plant reduction process in order to decrease their dependence on scrap;

• in the case of more elaborated and special steel, scale and specialization are

fundamental, restricting the number of manufacturers for these types of steel in order to reduce overall costs; and

• depending on the characteristics of the products and their aggregate value, logistical

questions involving access to crude materials and the transportation of the final product are focussed on the global market, where the great integrated mills are more competitive.

A good example is Brazil, where the mini-mills are less viable because the low cost of iron ore and the high price of electrical energy result in great competitive advantage for the integrated mills. However, the tendency is not to construct any new integrated mills but instead a better utilization of existing facilities. Even on the national level, this use can be optimized. According to a study by McKinsey & Company, the minimum efficient scale is reached with a capacity of 5 million t, a level where practically no gain is obtained on the cost of equipment per ton of steel. While the average capacity of Brazilian integrated mills is 4.5 million t, in Korea it has reached 10 million t. Graph 6 Share of the Technological Routes in Brazilian Production - 1997

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 18 -

Source: IISI. In 1997, integrated mills represented 86.3% of Brazilian production, which, according to the steel plant process, have their configuration presented in Graph 6. However, in order to survive, the integrated mills adopted emerging technologies that enabled them to improve their cost structures involving the refining of products. An important point is related to the coke plant stage, questioned for its environmental problems and its operating and building costs, but which still doesn’t have any substitute for great production volumes. A tendency that is worth mentioning in the Brazilian case refers to the installation of mini-coke plants that substitute charcoal for coke, for economic reasons. As a comparison, the costs for producing pig iron are US$ 130/t and US$ 65/t for coal and coke, respectively. In this case, the mini-coke or coke plant centers (for supplying several companies) present much lower investment needs than traditional coke plants, which require an associated thermoelectric unit. In this way, in spite of their not producing sub-products, the tendency has been for increasing usage of mini-coke plants. Other Emerging Technologies Other technologies have come to provide significant gains in metallurgy. The main ones, listed below, reinforce the trajectory of process compaction: • injection of fine coal - Powder Cooled Injection (PCI) -, whose advantages are the

reduction of operational costs, the least environmental impact, and increasing the useful life of the blast furnace;

• alternative reduction processes for transforming iron ore into primary metal that will

substitute the blast furnace, and whose advantages are the reduction of damage to the environment, increasing labor productivity, and providing the greatest operational flexibility; examples: Corex, Direct Iron Ore Smelting (Dios), Romelt, Hismelt, Aisi-Doe, Cyclone Converter Furnace (CCF), Tecnored (Brazilian) and Ausmelt; and

• the molding of fine plates (thin-slab casting), seeking to substitute the hot strip roller,

and whose advantages are low investment, quick installation, low operating costs and the lowest labor needs. According to Germano Mendes de Paula:

"The first industrial plant using thin-slab casting technology entered into operation in July of 1989. It is Nucor Steel’s Crawfordsville (Indiana, United States) mill, with an installed capacity of 820,000 tons. It required investments of US$ 375 million and employed 402 workers initially. The low level of labor incorporation brought about a substantial compaction of the process. The great revolution caused by the thin-slab casting technology is due to the possibility of producing plane products starting from an electric steel plant... The future diffusion of thin-slab casting technology will imply an

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 19 -

eventual reversion of the modus operandi of the sector: smaller mills will be able to assist regional markets to the detriment of the current structure that involves great integrated coke mills which supply markets at the national and international level.”

In the two basic technological routes referred to above, other technological developments have been promoted in recent years, such as, for example, high oxygen injection, combined blasting (integrated mills), treatment and continuous pre-heating of scrap, UHP electric-arc furnaces and greater utilization of pot-furnace refining. Another process, still in its pioneer stages, refers to the obtaining of iron carbide as the main prime material of an electric steel plant. The process is being tested by Nucor at its facilities in Trinidad and Tobago, in partnership with Samitri, subsidiary of the Companhia Siderúrgica Belgo Mineira. The iron carbide would be an alternative source of metal material, as would be sponge iron. In the face of the tendency, before the crisis, of rising scrap prices and the difficulty in obtaining good quality material (clean scrap)—indispensable for the production of plane steel—, metallurgical companies began investing in research in order to develop alternative sources of metals. Product Refining Over the last 10 years, the markets and the steel consuming industries have become more and more demanding. Thus, the search for product quality became an essential factor for competition in the new globalized environment. Constant efforts were made in the attempt to recover and aggregate special properties and differentiating characteristics for steel, thereby preventing its substitution. In this way, one of the tendencies which intensified in the restructuring period was the refining of metallurgical products. There was a growth in the production of steel with higher aggregate value, exemplified here by the increase in the amount of galvanized plates used in rolling production (Graph 7), whose demand was leveraged mainly by its wide use in the automobile industry. Other good example is the evolution of stainless steel consumption. In the plane segment, which represents more than 70% of the world consumption of stainless steel, there was a constant growth of 5% per annum on average over the period 1985/95. Graph 7 Share of Galvanized Plates in Total Rolling Production - 1980/96 Source: Germano Mendes de Paula. Made possible by technological advances, the process of metallurgical product refining was dictated initially by the industrialized countries, but in recent years companies from the developing countries have also begun making this a part of their goals. This has been largely due to the internationalization of the steel consuming industries (automobile, white line products), which have installed production units in the developing countries and

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 20 -

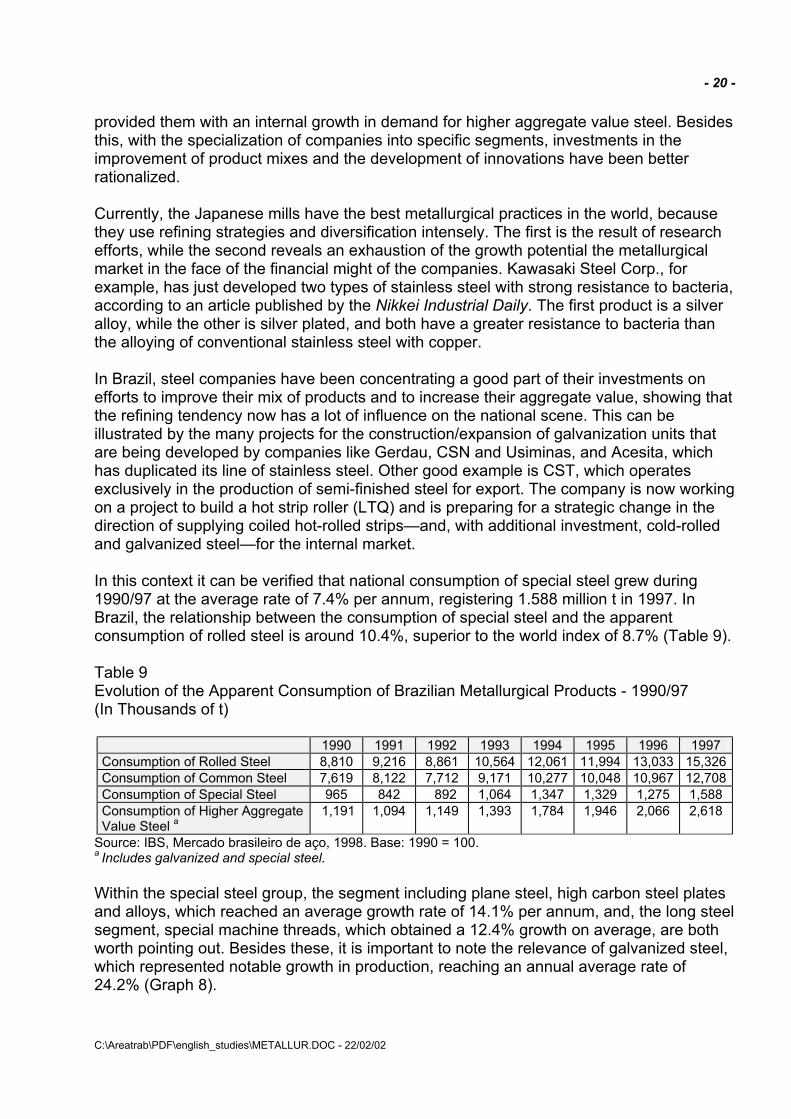

provided them with an internal growth in demand for higher aggregate value steel. Besides this, with the specialization of companies into specific segments, investments in the improvement of product mixes and the development of innovations have been better rationalized. Currently, the Japanese mills have the best metallurgical practices in the world, because they use refining strategies and diversification intensely. The first is the result of research efforts, while the second reveals an exhaustion of the growth potential the metallurgical market in the face of the financial might of the companies. Kawasaki Steel Corp., for example, has just developed two types of stainless steel with strong resistance to bacteria, according to an article published by the Nikkei Industrial Daily. The first product is a silver alloy, while the other is silver plated, and both have a greater resistance to bacteria than the alloying of conventional stainless steel with copper. In Brazil, steel companies have been concentrating a good part of their investments on efforts to improve their mix of products and to increase their aggregate value, showing that the refining tendency now has a lot of influence on the national scene. This can be illustrated by the many projects for the construction/expansion of galvanization units that are being developed by companies like Gerdau, CSN and Usiminas, and Acesita, which has duplicated its line of stainless steel. Other good example is CST, which operates exclusively in the production of semi-finished steel for export. The company is now working on a project to build a hot strip roller (LTQ) and is preparing for a strategic change in the direction of supplying coiled hot-rolled strips—and, with additional investment, cold-rolled and galvanized steel—for the internal market. In this context it can be verified that national consumption of special steel grew during 1990/97 at the average rate of 7.4% per annum, registering 1.588 million t in 1997. In Brazil, the relationship between the consumption of special steel and the apparent consumption of rolled steel is around 10.4%, superior to the world index of 8.7% (Table 9). Table 9 Evolution of the Apparent Consumption of Brazilian Metallurgical Products - 1990/97 (In Thousands of t)

1990 1991 1992 1993 1994 1995 1996 1997 Consumption of Rolled Steel 8,810 9,216 8,861 10,564 12,061 11,994 13,033 15,326 Consumption of Common Steel 7,619 8,122 7,712 9,171 10,277 10,048 10,967 12,708 Consumption of Special Steel 965 842 892 1,064 1,347 1,329 1,275 1,588 Consumption of Higher Aggregate Value Steel a

1,191 1,094 1,149 1,393 1,784 1,946 2,066 2,618

Source: IBS, Mercado brasileiro de aço, 1998. Base: 1990 = 100. a Includes galvanized and special steel. Within the special steel group, the segment including plane steel, high carbon steel plates and alloys, which reached an average growth rate of 14.1% per annum, and, the long steel segment, special machine threads, which obtained a 12.4% growth on average, are both worth pointing out. Besides these, it is important to note the relevance of galvanized steel, which represented notable growth in production, reaching an annual average rate of 24.2% (Graph 8).

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 21 -

Graph 8 Growth Index of Apparent Consumption of Brazilian Metallurgical Products - 1990/97 Source: BNDES. Internationalization Internationalization can be analyzed in two ways: the flow of international trade and the internationalization of productive capital—that is to say, the performance of companies in countries that are not their origin. Before the restructuring period, multinational investments in metallurgy were not very representative. The metallurgical companies, in general, produced for their internal markets. Internationalization was limited to the export of goods and technology. International trade Graph 9 World exports of Plane and Long Steel - 1987/96 Source: IISI.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 22 -

In this respect, it can be noticed that growth in international steel trade resumed again over the period in question, in spite of the expected fall for the next few years. The share of world exports of plane and long steel in global production grew from 28.7% to 42.3% over the period 1987/96 (Graph 9). We can observe that this increase didn't occur in the same way among the other segments, with a greater dynamism being shown for rolled plane segment in relation to long steel. In spite of the significant volume of international trade, the very nature of metallurgy creates cost advantages and logistics for local suppliers, establishing a type of barrier or natural protection. This is truer for the long steel segment, which has a lower aggregate value line (burdened with higher transportation costs) and a largest number of producing countries. It should also be pointed out that, in spite of the growth in the volume of international trade, the flow continues to be for the most part intra-regional. To have an idea, in 1995 about 26.5% of all international trade took place among the 15 countries that form the European Union. In Asia, 52.9% of imports came from its own regional area. The same occurred in North America with 48.9%. In Latin America, intra-regional trade grew from 10% (1990) to 33.8% (1995). In 1997 Brazil sent about 59% of its exports to the countries of the Americas (with 25% going to the United States alone). In relation to imports, 34% came from the American continents. In line with this tendency, specialists expect a reduction in transoceanic trade due to some basic points: • lower import levels of products with lower aggregate value on the part of the United

States, Japan and China; • less international trade involving semi-finished products and steel commodities,

represented in terms of volume, with attention going back to regional markets; • the negative impact of the collapse of NIS, and the Asian crisis; • large investments in traditionally importing countries like China, India, Korea and other

Asian countries; and • the cooling of the market, generating an increase in international competition and,

consequently, an intensification of protectionism. The growth in international steel trade during recent years has not been only the result of globalization. Factors such as the increase in exports from the former USSR due to the collapse of its internal market, and the strong expansion of the Southeast Asian economy, mainly through the substantial increase in Chinese imports, also contributed to a greater commercialization of steel. At the beginning of the restructuring period, with its oversupply, stagnation of demand and the growth in the developing countries, a proliferation of para-tariff protection mechanisms sprang up in several countries in order to protect national industries (such as voluntary export restriction accords).

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 23 -

The protectionist position of United States stands out in particular, in that it has maintained an over-taxation posture with respect to Brazilian, Japanese and Russian hot-rolled strips since the middle of 1998, alleging dumping practices and subsidies as its reasons. The relaxing of protectionism and antidumping measures, allied to the contraction of internal demand, has placed Brazilian companies in a delicate position. The United States has also adopted the practice of negotiating voluntary export restrictions of certain products with exporting countries. Due to this new scenario, investment strategies in the 1990s have tended to benefit the formation of joint ventures that seek to overcome protectionist barriers, with emphasis mainly on the installation of finishing facilities in the consuming countries. The Internationalization of Capital The tendency towards the internationalization of capital has been reinforced in this manner, growing significantly in relationship to the other preponderant factor in the restructuring process: the industrial concentration of production. In the past, the main restrictions to the growth of capital internationalization in the metallurgical sector were the great investments necessary to build an integrated coke mill. The restructuring process accelerated internationalization mainly in the following ways:

• technological - mini-mills reduced the large minimum scale needed for the sector; • market-related - the tendency towards the refining of products opened up investment

opportunities in finishing mills; and • political-institutional - privatization made the acquisition of already-operating companies

possible.

One of the most important movements was represented by a group of Japanese companies that invested in the North American market. The following was accomplished: • acquisitions of stock shares in the integrated mills (for example, 13% of Inland Steel by

Nippon Steel, and 70% of National Steel by NKK Corp.); • joint-ventures in the building of finishing facilities (for example, LSE II-Electro-

galvanization with Sumitomo and LTV, and Protect Coating with Kobe and USX); and • the construction of new mini-mills (for example, Florida Steel with Kyoei Steel and

Sumitomo, and Coperweld Steel with Daido Steel and Usinor). In December 1994, US-based LTV Corp., Japanese Sumitomo Metals and British Steel formed a joint-venture in order to found Trico Steel, a mill located in Alabama using thin-slab-casting technology, with output capacity of 2.2 million t. In Europe, a number of joint-ventures were established among companies from several countries. In November 1992, British Steel and Avesta (Sweden) unified their stainless steel divisions, forming Avesta Sheffield. In 1994, DMV Stainless was created from an association of the Dalmine (Italy), Mannesmann (Germany) and Vallourec (France) companies. In Asia, Japanese and South Korean investments expanded into another countries in the region. In spite of the internationalization process being led by companies from the industrialized countries, good examples already exist in companies from another origins. The case of Argentinean Techint comes to mind, with its acquisition seamless steel tube mills in

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 24 -

Mexico (Tamsa), Italy (Dalmine) and Venezuela (Sidor). Currently, the group controls a 29% share of the international trade of seamless steel tubes, eclipsing giants like US Steel, Mannesmann from Germany, and the Japanese Sumitomo Heavy Industries. In Brazil, internationalization is also intensifying, both with the increasing of market share by foreign groups like Nippon and Kawasaki, among others, as well as the creation of foreign subsidiaries on the part of some national groups/companies like Gerdau, which now has mills in Uruguay, Argentina, Chile and Canada. Brazilian companies have been trying to act in a synergetic manner with foreign multinationals, looking for partnerships that will attract the best practices and technologies. In this sense, CSN, for example, is currently in the process of developing two joint-venture projects: Cisa, in partnership with Mexican Imsa, for the construction of a coated steel mill in Araucaria (PR) with the capacity to produce 440,000 t/year of products destined basically for the production of metallic structures for civil construction, the automotive industries, and appliances; and Galvasud, a joint-venture with Thyssen Krupp Stahl, that will invest about US$ 260 million in the construction of cut, solder and galvanization lines in the Rio de Janeiro-São Paulo axis, with the main objective of supplying the automobile industry. However, the incursion of foreign companies into the Brazilian steel market can be considered mild, limiting itself to minority shares. Not even the process of privatization was capable of attracting significant investments. A more important movement occurred recently with the entrance of French Usinor, which acquired 27.68% of the total capital of Acesita, and 38.94% of its voting capital, in what represented the company’s effective entry (with its own operating strategies) into the Brazilian metallurgical market. Concentration The complex conjuncture that characterized the beginning of the restructuring process (excess installed capacity and products offered, high exit costs, markups reduced by the fall in international prices, increased competitiveness) transformed the search for cost reduction and optimization in the obtaining and use of productive/financial resources into fundamental factors for survival. This favored the expansion of business scales significantly. The size of the company aggregated competitive gains to the extent that it optimized the following factors:

• use of financial assets; • coordination of investments; • transfer of the best operational practices; • optimization of distribution channel use; • investments in research and development; and • relationships with multinational clients. Besides this, only large companies would have a volume of capital sufficient enough to support high investments in the face of competitors. Therefore, within the restructuring

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 25 -

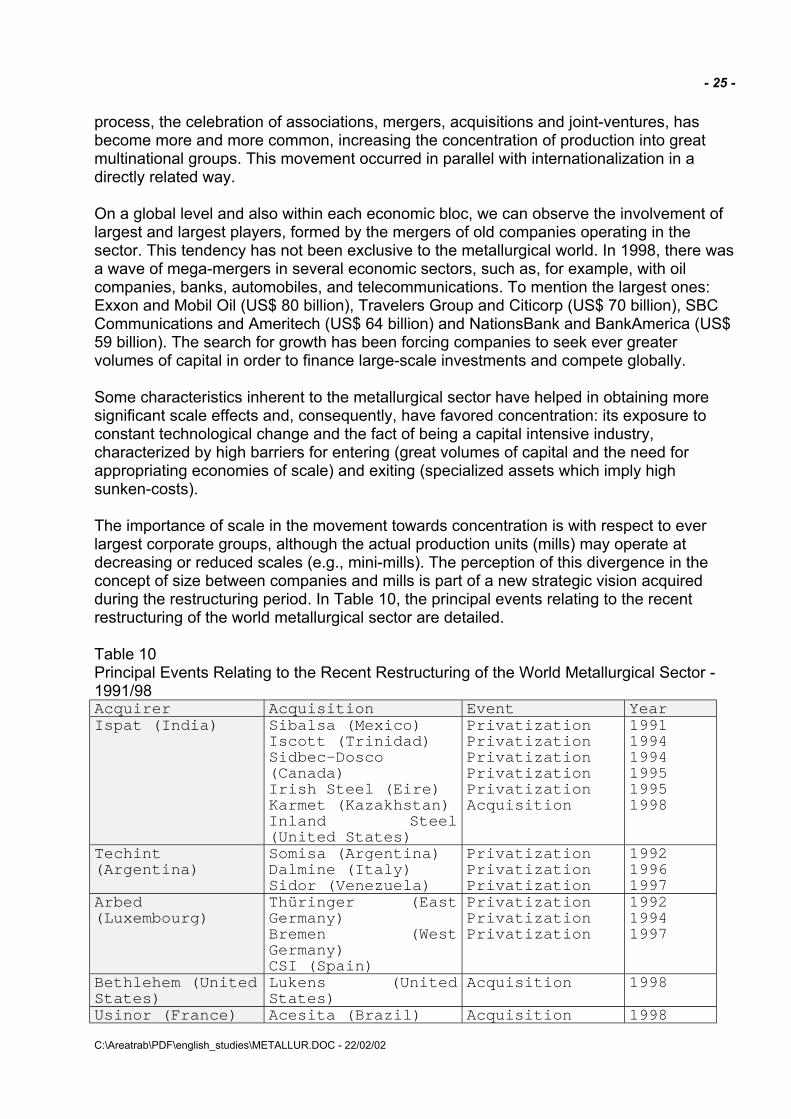

process, the celebration of associations, mergers, acquisitions and joint-ventures, has become more and more common, increasing the concentration of production into great multinational groups. This movement occurred in parallel with internationalization in a directly related way. On a global level and also within each economic bloc, we can observe the involvement of largest and largest players, formed by the mergers of old companies operating in the sector. This tendency has not been exclusive to the metallurgical world. In 1998, there was a wave of mega-mergers in several economic sectors, such as, for example, with oil companies, banks, automobiles, and telecommunications. To mention the largest ones: Exxon and Mobil Oil (US$ 80 billion), Travelers Group and Citicorp (US$ 70 billion), SBC Communications and Ameritech (US$ 64 billion) and NationsBank and BankAmerica (US$ 59 billion). The search for growth has been forcing companies to seek ever greater volumes of capital in order to finance large-scale investments and compete globally. Some characteristics inherent to the metallurgical sector have helped in obtaining more significant scale effects and, consequently, have favored concentration: its exposure to constant technological change and the fact of being a capital intensive industry, characterized by high barriers for entering (great volumes of capital and the need for appropriating economies of scale) and exiting (specialized assets which imply high sunken-costs). The importance of scale in the movement towards concentration is with respect to ever largest corporate groups, although the actual production units (mills) may operate at decreasing or reduced scales (e.g., mini-mills). The perception of this divergence in the concept of size between companies and mills is part of a new strategic vision acquired during the restructuring period. In Table 10, the principal events relating to the recent restructuring of the world metallurgical sector are detailed. Table 10 Principal Events Relating to the Recent Restructuring of the World Metallurgical Sector - 1991/98 Acquirer Acquisition Event Year Ispat (India) Sibalsa (Mexico)

Iscott (Trinidad) Sidbec-Dosco (Canada) Irish Steel (Eire) Karmet (Kazakhstan) Inland Steel (United States)

Privatization Privatization Privatization Privatization Privatization Acquisition

1991 1994 1994 1995 1995 1998

Techint (Argentina)

Somisa (Argentina) Dalmine (Italy) Sidor (Venezuela)

Privatization Privatization Privatization

1992 1996 1997

Arbed (Luxembourg)

Thüringer (East Germany) Bremen (West Germany) CSI (Spain)

Privatization Privatization Privatization

1992 1994 1997

Bethlehem (United States)

Lukens (United States)

Acquisition 1998

Usinor (France) Acesita (Brazil) Acquisition 1998

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 26 -

Cockerill-Sambre (Belgium) Finaverdi (Italy)

Acquisition Acquisition

1998 1998

Thyssen (Germany) Krupp (Germany) Merger 1997 Sources: Germano Mendes de Paula, BNDES. Europe has been the stage for two of the most recent events, the merger of the two largest German companies (Thyssen and Krupp Hoesch) and the purchase of Belgium’s Cockerill-Sambre by French Usinor, creating Europe’s largest steel company. The concentration indexes have been constantly increasing, verified by the fact that five large groups now dominate the metallurgical sector in Europe: Usinor, Thyssen-Krupp, British Steel, Arbed and Riva. In Japan, concentration has also been intense, with the production from the four largest mills reaching 59.3 million t of crude steel in 1997, equal, approximately, to 60% of total Japanese national production. Besides this, the Japanese sector is characterized by a special peculiarity, where the integrated coke mills own shares in the semi-integrated mills, so that the loss of market in one is compensated by the growth of the other. In Graph 10, the ranking of the 20 largest metallurgical groups in 1997 is illustrated. Graph 10 Ranking of the 20 Largest Metallurgical Groups in the World a - 1997 Source: Metal Bulletin, March 1998. a The LNM Group includes Ispat International, Ispat Karmet and Ispat Indo. The dynamism of this equity restructuring process has been so intense that some very important events took place in 1998, with consequences that are not shown in Graph 10. Therefore, in relation to what is illustrated in the graph, the following considerations should be taken into account: • Thyssen Krupp Stahl excludes Krupp Thyssen Stainless, which produced 1,9 million t

in 1997; • Arbed does not include Aceralia/Aristrain (CSI), which, if included, would increase the

company’s production to 18 million t; • Usinor’s production should be added to the Acesita/CST/Villares Group and Cockerill-

Sambre, elevating the groups to the position of third-largest world producer and largest producer in Europe (in addition to this, Usinor also acquired Italian Arvedi); and

• The LNM Group’s position should increase considerably due to its acquisition of the United States’ Inland Steel.

In observing the concentration phenomenon in the metallurgical industry, the case of the United States also stands out, where the degree of industrial concentration has been decreasing, an exception to the world trend. The index measuring the share of the four largest companies in that country’s national production (C4) suffered a sharp fall, dropping from about 53% (in 1985) to 37% (in 1997).

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 27 -

The old integrated coke producers (US Steel, Bethlehem, LTV Corp., Inland, National and Armco) experienced the impact of the restructuring process more intensely and reduced their overall production from 84.1 million t (1972) to 42.8 million t (1996), favoring the semi-integrated groups as a whole. In the following Graph 11, concentration in the world metallurgical industry is shown. Graph 11 Concentration of the World Metallurgical Industry - 1997 Sources: IISI, BA&H analysis, and BNDES It is important to consider the production level of each country when making a concentration analysis. Without taking into account production scales, the tendency would be to compare countries such as the United Kingdom and Japan directly, when these countries have completely different production levels (approximately 17 t and 100 million t, respectively). Thus we can observe that the larger producing countries like Japan, the United States and China, have a consequently smaller concentration, without suggesting that their companies are necessarily smaller in scale. Nevertheless, it is possible to conclude that China’s sector is quite dispersed. It is also important to emphasize the positions of two countries in Graph 11: Korea, which has the largest degree of concentration within its group, in spite of its high production volume (about 39 million t), due to the output of Posco, the second-largest producer in the world which alone is responsible for producing 68% of national production (the second-largest Korean company is Inchon Steel, 55th in the world ranking, producing just 3.57 million t or 14% of Posco’s production); and Russia, which produced about 70 million t in 1992 and therefore has an installed capacity and concentration sufficient to be part of the group of large producers, but which, affected by its internal crisis, suffered a drastic reduction in production volume and still needs to pass through a necessary restructuring in order to adjust and rationalize its industry. The Brazilian metallurgical sector, after its own process of restructuring and privatization, has reduced the number of companies operating in its sector from 30 to 11, but still appears very dispersed, as can be seen in Graph 11. The sector doesn't still have a corporate scale sufficient to be considered one of the great international players. The largest Brazilian company (CSN) fell only 38th in the ranking of world producers in 1997, with 4.8 million t of steel produced. Considering the combined production of Cosipa and Usiminas, the joint company is only in 11th position. In spite of being the world’s seventh-largest producer of crude steel in 1997, total Brazilian production is still less than Nippon Steel, the largest metallurgical company in the world. Specialization Pressured by the need to rationalize investments, reduce industrial costs and acquire/maintain consumer markets, metallurgical companies increasingly sought to specialize their production processes over the restructuring period, which implied a return to specific and very defined lines of operation. In this way, they have traced strategies,

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 28 -

defined objectives, targeted investments and rationalized their assets, always based on their performance in a specific niche. It is possible to notice this tendency even in the nature of the recent mergers and acquisitions that have taken place. In contrast with other periods, when corporate groups diversified their investment portfolios into various types of business activities, in recent years the groups involved in buying and selling operations have generally restricted them to metallurgical activity. With this, we can observe that the specialization of production on the part of the companies has been occurring in way that is highly correlated with other restructuring events, mainly in order to the increase corporate scale (concentration) and internationalization. A clear example of this specialization is the special steels segment, which is characterized by the high necessary operating investments required for constant technological improvement, yet having to count, on the other hand, on reduced market volume. Therefore, in order to operate within the maximum scale compatible with the size of the market, the tendency of these companies has been to give emphasis to those products which produce gains in competitiveness, reducing the production of lines with lesser competitive strength. In this way, this industry has suffered a wide restructuring process, continuing even today in its search for the optimization of capital, scale and distribution channels. It is a segment with a high degree of concentration and specialization, where a few powerful competitors engage in the international commercialization of high added value products. In a general way, it can be affirmed that specialization assumes a globalized and extremely competitive focus on positioning strategy in the international environment (Table 11). Table 11 Globalization Strategies of the Metallurgical Companies Specialization Focus Description Companies (Example) Product The company searches for a

product for which it can become a global supplier (or even a dominant supplier), with industrial plants located in various parts of the world

The Techint group from Argentina, which has plants in Argentina, Mexico and Italy

Process The company seeks to focus on the construction of an international operational network which uses the same industrial process

The Indian Ispat company owns or manages direct reduction integrated mills in India, Canada, Mexico, Trinidad, and Germany

Global Market The company endeavors to attend to a select group of global consumers in the place where they are located

Investments by Japanese metallurgical companies (plane steel) in the United States

Local Markets The company seeks to attend to many local market consumers (fragmented)

Australia’s BHP Steel and Gerdau (investments in various rolling mills in order to attend to local civil construction markets)

General Regionalism The company searches to become a major supplier of multiple products in various market segments with a specific

Posco, South Korea (investments in Australia, China, and Vietnam)

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 29 -

geographical area Source: Germano Mendes de Paula. In Brazil, due to the form that its metallurgical industry developed, local companies have opted for operations focussed in one of the following segments, by product type: semi-finished, long, plane and special steel. Long steel has been produced since the beginning produced by private companies, because they demanded smaller scale and investments for operation. At that time the government built specialized plane steel mills to make up for production deficiency, and in order to attend to demand. After that, and taking advantage of the favorable world configuration and internal export policy, other mills were built that manufactured semi-finished products directed to the foreign markets. Soon after the privatization of the metallurgical sector, companies began to concentrate on programs which increased production and reduced costs, but by the end of 1994 the tendency towards specialization already dominated corporate strategies. This movement was more visible in the case of special steel, which was characterized by the production of an enormous range of products, often without competitiveness but protected by local markets. These companies had to adapt to new market conditions through a profound restructuring process, focussing on specialization. Currently, the restructuring process in course in national steel sector demonstrates the intention of strengthening domestic competitiveness both in the more open, internal market, as well as abroad, with products of greater quality and at more competitive prices being offered. The configuration observed today in the Brazilian metallurgical sector will be analyzed in more detail in the section to follow. However, by virtue of the expected restructuring of companies’ equity, Brazilian companies may undergo strategic changes that will alter their current position. Current Structure of the Brazilian Metallurgical Market The restructuring of the Brazilian metallurgical sector has also been a dynamic process, significantly reducing the number of companies in the country—consistent with the world tendency, and coinciding with the privatization of the national sector. At the end of the decade of the 1980s, the sector was composed of more than 30 companies/groups which operated in a market environment protected by high import quotas and government price controls. Companies controlled by the federal government represented about 71% of the sector’s installed capacity, and were characterized mainly by the following attributes: • the sector was highly in debt; • industrial park relatively out-of-date; • investment limitations; • bureaucratic and/or political administration; • commercial limitations; • low planning and strategy autonomy; • high environmental liabilities; and • production costs incompatible with international standards. At the beginning of the nineties, with the privatization program (already described in the section entitled “Privatization,” p. ?) and economic liberalization under way, a restructuring process began in the sense of increasing the competitiveness of the sector.

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 30 -

During recent years, with the privatization process having been completed, a stock restructuring process has been occurring, begun with the exit of the banks Bozano Simonsen, Bamerindus, Econômico and Unibanco from their control of some of the main privatized Brazilian steel companies, like Usiminas, Cosipa and CST. The banks exercised a fundamental role in the privatization of the companies, reaping large profits from the business. However, their main motivation was the exchanging of “privatization currency” (government junk bonds) for real assets. The intensification of globalization and the need for obtaining larger scales of production, together with the realization of new investments with lower returns, has led banks to gradually leave the sector, with control being passed on to a few private groups which are directly or indirectly linked to the sector, including a significant participation on the part of pension funds. Another important factor in the evolution of the stockholder composition of Brazilian metallurgical comps refers to the privatization of the Companhia Vale do Rio Doce (CVRD) on May 6, 1997, which owned large stock holdings in several companies in the sector. The Brazil Consortium, led by CSN (25.55%) and contributed to by pension funds (39.29%), Investvale + BNDESPAR (9.47%), Banco Opportunity (16.73%) and NationsBank (8.97%), acquired Valepar, a holding company retaining 41.73% of CVRD’s voting capital, for the value of R$ 3.33 billion. The privatization, in which CSN acquired 25.5% of control, strongly contributed to an increase in crossed stock holdings in the sector and in this way reinforced the positions of CSN and the pension funds, especially Banco do Brasil’s pension fund (Previ), as can be observed in Table 12. In such a way, the Brazilian metallurgical industry has established a very particular situation in relation to its current stockholder composition, characterized by a high level of crossed holdings (Graph 12). Table 12 Share of the CVRD and Pension Funds in the Privatization of the Metallurgical Sector: Total capital - 1997 CVRD PREVI Other Funds CSN 9.57 13.42 13.42 Usiminas 7.74 8.09 11.92 CST 22.69 9.30 34.40 Açominas 4.84 - - Acesita - 23.84 26.50 Source: BNDES. Graph 12 Stock Participation in the Brazilian Metallurgical Sector - Voting Capital - 1998 Source: BNDES. It is important to emphasize that the complexity of stock ownership networks not only presents internal obstacles, it also inhibits foreign investor participation and affects the competitiveness of the Brazilian metallurgical sector. In this sense, the need to continue the restructuring process in order to develop the sector is essential, since, from a market

C:\Areatrab\PDF\english_studies\METALLUR.DOC - 22/02/02

- 31 -

aspect, it is very concentrated, with two to three producers for each of the major segments (Table 13). This contributes to the small level of competition in the internal market. Table 13 The Brazilian Metallurgical sector Products Companies (Location)

Semi-Finished Steel Açominas (MG), CST (ES) Special Steel Acesita (MG), Mannesmann (MG) Rolled Plane Steel Cosipa (SP), CSN (RJ), Usiminas (MG)

Integrated mills

Rolled Long Steel Belgo Mineira (MG), Gerdau (MG) Special Steel Aços Villares (SP), Villares Metals (SP), Gerdau (RS) Semi-Integrated

mills Rolled Long Steel Gerdau (CE, PE, BA, RJ, PR, RS), Mendes Jr. – BMP (MG), Barra Mansa (RJ), Belgo Mineira (SP), Itaunense (MG)

Source: BNDES Eleven companies are currently responsible for 98% of Brazil’s production (Graph 13). However, during the restructuring period, the sector evolved towards the consolidation of production into five operational blocks, responsible for 96% of national output (Table 14), considering that: Graph 13 The Major Brazilian Metallurgical Companies (In % of Crude Steel Production) Source: BNDES. • Usiminas and Cosipa are currently in a joint process of restructuring in preparation for