session 02

TRANSCRIPT

Stakeholder Relationships, Social Responsibility and

Corporate Governance Chapter 3

A stakeholder is somebody or something with direct interest

In a business context, customers, investors and shareholders, employees, suppliers, government agencies, communities, and many others who have a “stake” or claim in some aspects of the company’s products, operations, markets, industry, and outcomes are known as stakeholders

Primary stakeholders are those whose continued association is absolutely necessary for the firm’s survival; these include employees , customers, investors, and shareholders as well as the governments and communities that provide the infrastructure.

Identifying stakeholders

Secondary Stakeholders do not typically engage in transactions with the company and thus are not essential for its survival; these include the media, trade associations, and special interest groups.

the American Association of Retired People, is a special interest groups, work to support retirees’ rights such as health care benefits.

Social Responsibility

Being Socially Responsible means that people and organizations must behave ethically and with sensitivity toward social, cultural, economic and environmental issues.

Striving for social responsibility helps

individuals, organizations and governments have a positive impact on development, business and society with a positive contribution to bottom-line results.

The term corporate citizenship is often

used to express the extent to which businesses strategically meet the economic, legal, ethical, and philanthropic responsibilities placed on them by their various stakeholders.

Economic; maximizing stakeholder’s wealth order and/or value.

Legal; abiding by all laws and government regulations

Ethical; following standards of acceptable behavior as judged by stakeholders.

Philanthropic; “giving back” to society.

Reputation is one of an organization’s greatest intangible assets with tangible value. CSR is the major influencer of reputation;

40% of reputation is driven by citizenship, governance and workplace perception.

Positive CSR perception leads to recommendation;

65% of the general public will “Definitely Recommend” the top 20 CSR U.S. companies vs. 26% for bottom 20 CSR companies

Corporate governance is a set of relationships between a company's directors, its shareholders and other stakeholders.

It provides structure through which the objectives of the company are set, and the means of obtaining these objectives and monitoring performance are determined.

In short, corporate governance is a system by which an organization is controlled.

wiki.answers.com

A well-defined and enforced corporate governance provides a structure that, at least in theory, works for the benefit of everyone concerned by ensuring that the enterprise adheres to accepted ethical standards and best practices as well as to formal laws. To that end, organizations have been formed at the regional, national, and global levels.

In recent years, corporate governance has received increased attention because of high-profile scandals involving abuse of corporate power and, in some cases, alleged criminal activity by corporate officers.

An integral part of an effective corporate governance regime includes provisions for civil or criminal prosecution of individuals who conduct unethical or illegal acts in the name of the enterprise.

Financial security.techtarget.com

The whole of corporate gamut lies in

concepts like transparency, accountability, merit, ethics, fairness and responsibility in the following terms;

Transparency; through checks and balance

like auditing committees, external and internal audit system, which are free of interference by decision makers.

Accountability; All who have enjoyed power through a strong set of rules are answerable to sponsors as well as society.

Mapping Responsibility; Both vertical and horizontal, so that responsibility is taken by those who make the decisions.

Disclosure; In a company nothing should be hidden for long and without reason. Once a decision has been made, it should be known to all.

Highlights of basic tools for sound corporate governance

Appointment of key personnel after ensuring that they are fit and proper for their jobs; Board of Directors.

Promotion of corporate values, ethics, codes of conduct for appropriate behavior and institution of a system to ensure compliance with them; Business Ethics, code of conduct.

Articulation of corporate strategy against which success of overall enterprise and the contribution of individuals can be measured;

Management System.

Assignment of clear-cut responsibilities and decision-making authorities and outlining chain of required approvals from individuals to the board of directors; Management System.

Institution of a forum interfacing the board of directors, senior management and the auditors; Corporate Governance Rating.

Putting in place sound internal control system, including internal and external audit functions, risk management functions, independent of business lines; Audit and Audit Committee.

Special monitoring of situations where conflict of interest arises, including business relationships with borrowers affiliated with the bank, large shareholders, senior management, or key decision-makers within the firm; Financial Reporting.

Offer of incentives (monetary and otherwise) to management (senior, business line) and employees in the form of compensation, promotion and other recognition; Rewards.

Channeling flow of information both

within and outside the organization (the public).

State Bank of Pakistan Hand Book

Pakistan announced that they were going to adopt IAS, International Accounting Standards, in 1974, shortly after it was created.

In the first stage of compliance, since Pakistan did not have their own accounting regulations, they made it voluntary for all companies in the country to adopt international accounting standards.

(Ashraf & Ghani 2007, page 183)

Auditing and Financial Reporting

Chapter 4

Internationally known by the older name of International Accounting Standards (IAS). IAS were issued between 1973 and 2001 by the Board of the International Accounting Standards Committee (IASC).

On April 1, 2001, the new IASB took over from the IASC the responsibility for setting International Accounting Standards. International Accounting Standards Board.

During its first meeting the new Board adopted existing IAS and Standing Interpretations Committee standards (SICs).

The IASB has continued to develop standards calling the new standards International Financial Reporting Standards (IFRS)

Introduction to Financial Statements Purpose of Financial Statements

Financial statements are a structured representation of the financial position (Balance Sheet) and financial performance (Income Statement) of an entity.

The objective of financial statements is to provide information about the financial position, financial performance and cash flows of an entity that is useful to a wide range of users in making economic decisions.

Financial statements also show the results of management’s stewardship of the resources entrusted to it. To meet this objective, financial statements provide information about an entity’s

(a) assets (b) liabilities (c) equity (d) income and expenses, including gains

and losses (e) other changes in equity; and (f) cash flows

Component of Financial Statements

Components of Financial Statements:

A complete set of financial statements comprises: a balance sheet; an income statement; a statement of changes in equity showing

either:◦ all changes in equity, or◦ changes in equity other than those arising from

transactions with equity holders acting in their capacity as equity holders;

a cash flow statement; and notes, comprising a summary of significant

accounting policies and other explanatory notes.

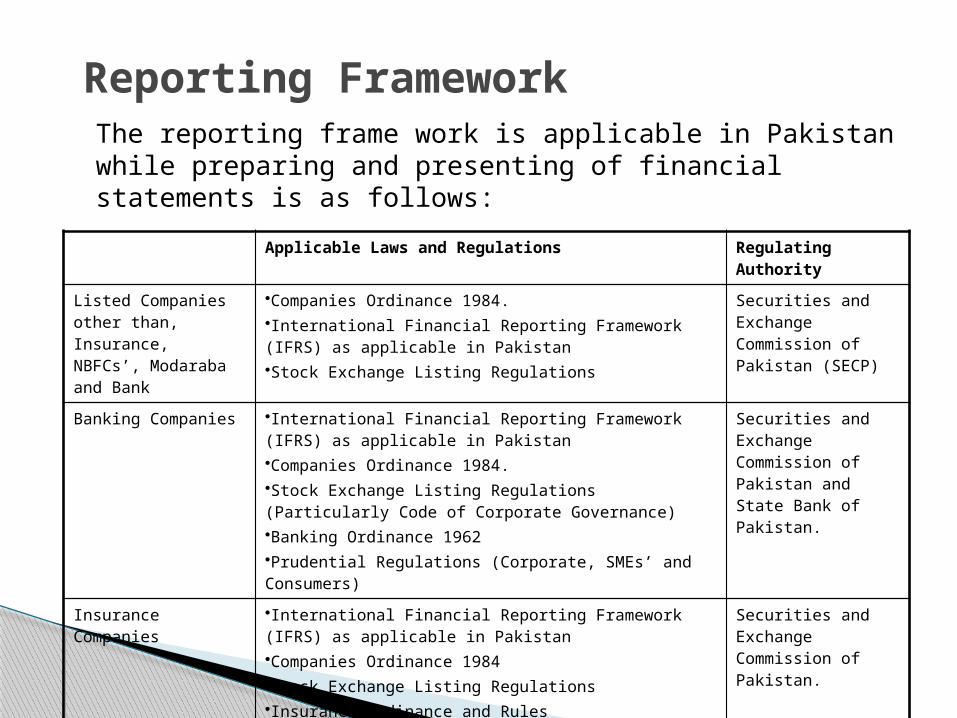

Reporting Framework The reporting frame work is applicable in Pakistan while preparing and presenting of financial statements is as follows:

Applicable Laws and Regulations Regulating Authority

Listed Companies other than, Insurance, NBFCs’, Modaraba and Bank

•Companies Ordinance 1984.•International Financial Reporting Framework (IFRS) as applicable in Pakistan•Stock Exchange Listing Regulations

Securities and Exchange Commission of Pakistan (SECP)

Banking Companies •International Financial Reporting Framework (IFRS) as applicable in Pakistan•Companies Ordinance 1984.•Stock Exchange Listing Regulations (Particularly Code of Corporate Governance)•Banking Ordinance 1962•Prudential Regulations (Corporate, SMEs’ and Consumers)

Securities and Exchange Commission of Pakistan and State Bank of Pakistan.

Insurance Companies •International Financial Reporting Framework (IFRS) as applicable in Pakistan•Companies Ordinance 1984•Stock Exchange Listing Regulations •Insurance Ordinance and Rules

Securities and Exchange Commission of Pakistan.

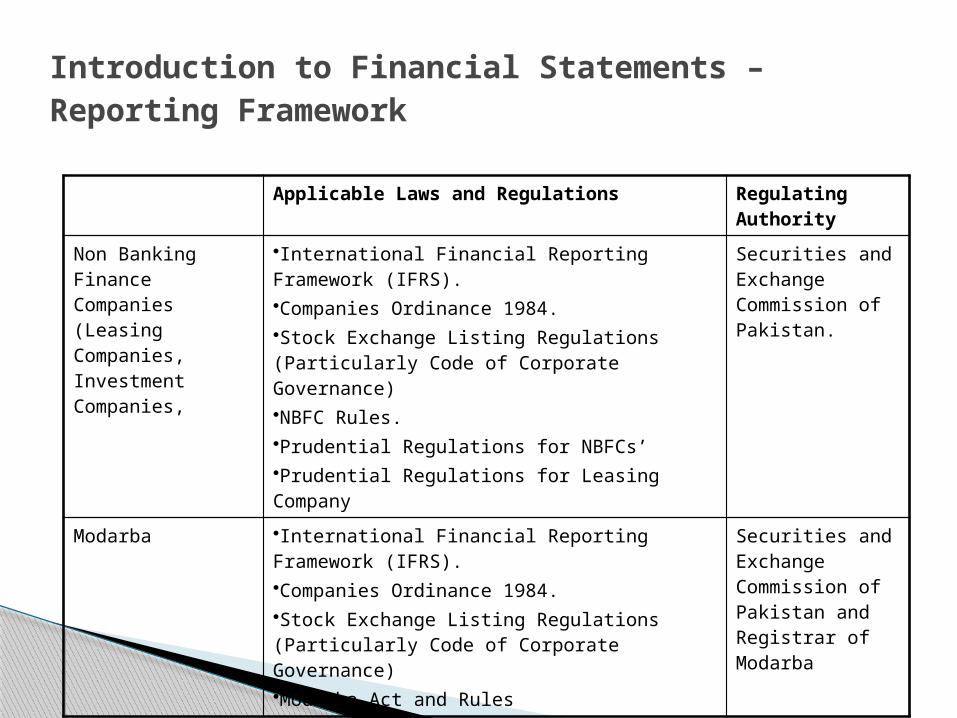

Introduction to Financial Statements – Reporting Framework

Applicable Laws and Regulations Regulating Authority

Non Banking Finance Companies (Leasing Companies, Investment Companies,

•International Financial Reporting Framework (IFRS).•Companies Ordinance 1984.•Stock Exchange Listing Regulations (Particularly Code of Corporate Governance)•NBFC Rules.•Prudential Regulations for NBFCs’•Prudential Regulations for Leasing Company

Securities and Exchange Commission of Pakistan.

Modarba •International Financial Reporting Framework (IFRS).•Companies Ordinance 1984.•Stock Exchange Listing Regulations (Particularly Code of Corporate Governance)•Modarba Act and Rules

Securities and Exchange Commission of Pakistan and Registrar of Modarba

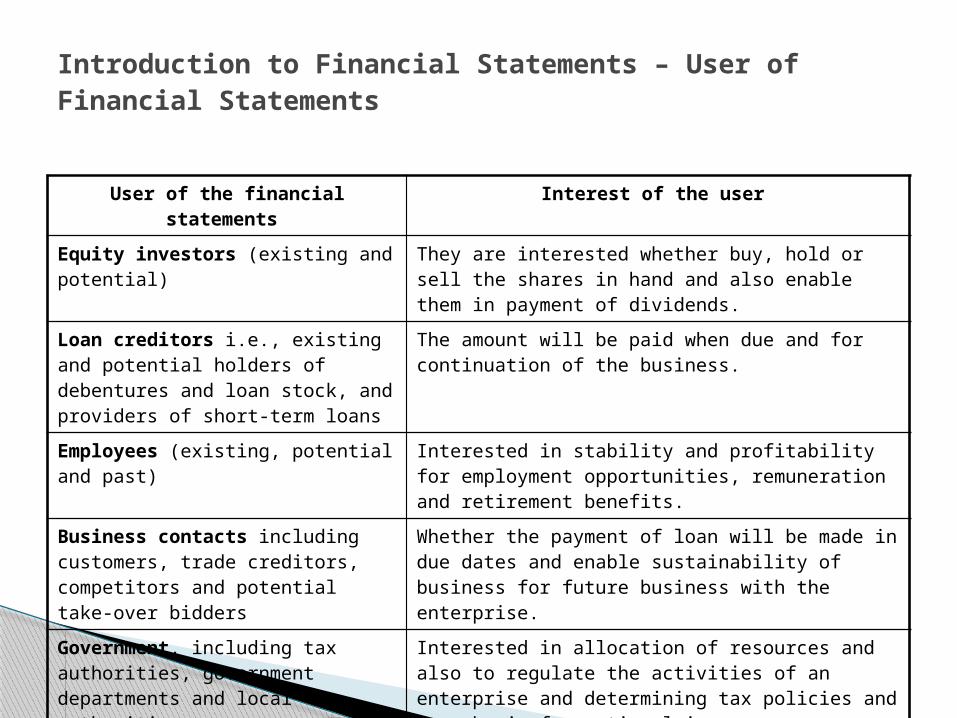

Introduction to Financial Statements – User of Financial Statements

User of the financial statements Interest of the user

Equity investors (existing and potential) They are interested whether buy, hold or sell the shares in hand and also enable them in payment of dividends.

Loan creditors i.e., existing and potential holders of debentures and loan stock, and providers of short-term loans

The amount will be paid when due and for continuation of the business.

Employees (existing, potential and past) Interested in stability and profitability for employment opportunities, remuneration and retirement benefits.

Business contacts including customers, trade creditors, competitors and potential take-over bidders

Whether the payment of loan will be made in due dates and enable sustainability of business for future business with the enterprise.

Government, including tax authorities, government departments and local authorities

Interested in allocation of resources and also to regulate the activities of an enterprise and determining tax policies and as a basis for national income.

Public, including tax payers, ratepayers and environmental groups

Trends and recent development in the prosperity of the entity and range of it’s activities.

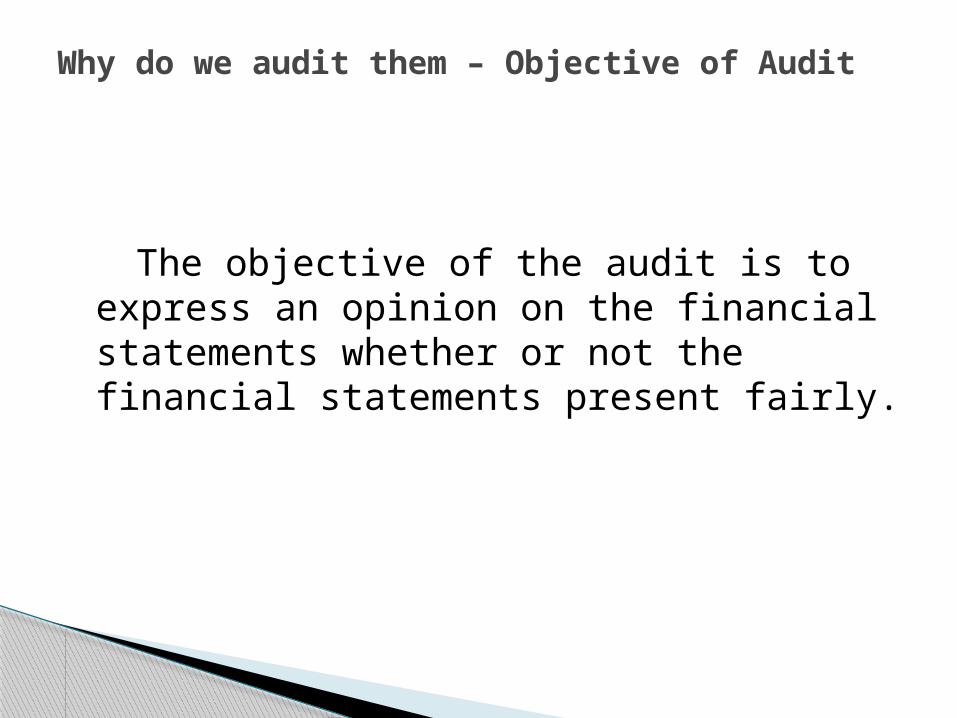

Why do we audit them – Objective of Audit

The objective of the audit is to express an opinion on the financial statements whether or not the financial statements present fairly.

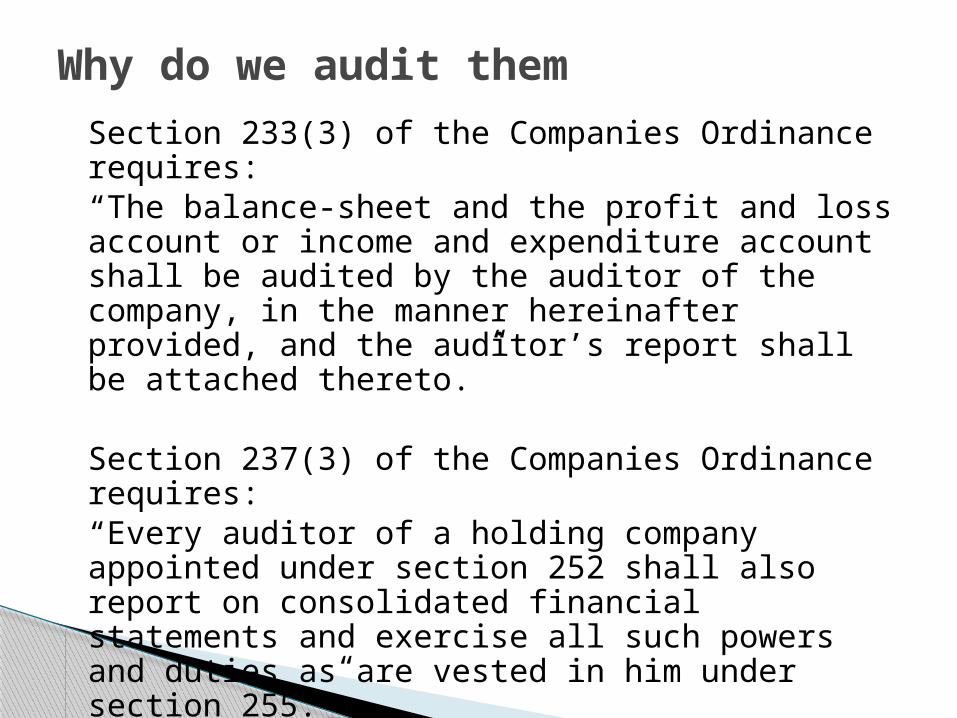

Why do we audit themSection 233(3) of the Companies Ordinance requires:“The balance-sheet and the profit and loss account or income and expenditure account shall be audited by the auditor of the company, in the manner hereinafter provided, and the auditor’s report shall be attached thereto.”

Section 237(3) of the Companies Ordinance requires:“Every auditor of a holding company appointed under section 252 shall also report on consolidated financial statements and exercise all such powers and duties as are vested in him under section 255.”

Section 252(1) of the Companies Ordinance requires:“Every company shall at each annual general meeting appoint an auditor or auditors to hold office from the conclusion of that meeting until the conclusion of the next annual general meeting.”

Why do we audit them

Required by the Section 35 (1) of the Banking Ordinance 1962.“The balance sheet and profit and loss account prepared in accordance with section 34 (Accounts and balance-sheet) of shall be audited by a person who is duly qualified, under the Chartered Accountants Ordinance, 1961 (X of 1961), or any other law for the time being in force, to be an auditor of companies and is borne on the panel of auditors maintained by the State Bank for the purposes of audit of banking companies.”

Basic Accounting Principles

Over all considerations of preparing and presenting financial statements

◦ Fair Presentation and Compliance with IFRS.◦ Going Concern◦ Accrual Basis of Accounting ◦ Consistency of Presentation◦ Materiality and Aggregation◦ Off setting◦ Comparative Information

Basic Accounting PrinciplesFair Presentation and Compliance with IFRS.

Financial statements shall present fairly the financial position, financial performance and cash flows of an entity.

Fair presentation requires the faithful representation of the effects of transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Framework.

The application of IFRSs, with additional disclosure when necessary, is presumed to result in financial statements that achieve a fair presentation.

Basic Accounting Principles

Accrual Basis of Accounting An entity shall prepare its financial statements, except for cash flow information, using the accrual basis of accounting.

Consistency of Presentation The presentation and classification of

items in the financial statements shall be retained from one period to the next unless:

it is apparent, following a significant change in the nature of the entity’s operations or a review of its financial statements, that another presentation or classification would be more appropriate having regard to the criteria for the selection and application of accounting policies in IAS 8; or

a Standard or an Interpretation requires a change in presentation.

Materiality and Aggregation Each material class of similar items

shall be presented separately in the financial statements. Items of a dissimilar nature or function shall be presented separately unless they are immaterial.

Off setting Assets and liabilities, and income and

expenses, shall not be offset unless required or permitted by a Standard or an Interpretation.

Comparative Information

Except when a Standard or an Interpretation permits or requires otherwise, comparative information shall be disclosed in respect of the previous period for all amounts reported in the financial statements. Comparative information shall be included for narrative and descriptive information when it is relevant to an understanding of the current period’s financial statements.

Institute of Chartered Accountants of Pakistan

Conclusion

In order to protect the stakeholders’ interest it is necessary to have an appropriate auditing system and accurate Financial Reporting in the organization.

In the past many power holding people of organization have done frauds which damaged all the stakeholders’ interest.

Case study Financial Dilemma