is japan really a “buy”? the corporate governance...

TRANSCRIPT

Is Japan really a “Buy”? The corporate governance, cash holdings, and economic performance of Japanese companies

Kazuo Kato [email protected]

Meng Li

Douglas J. Skinner [email protected]

April 2016

Abstract

We investigate whether Japan’s much touted governance reforms improve its firms’ management of cash, economic performance, and valuation. Consistent with an improvement in governance since 2000, Japanese firms hold less cash and increase payouts to shareholders. Improvements in performance are associated with reductions in (excess) cash, reductions in the influence of the banks that traditionally sit at the center of horizontal keiretsu, and increases in the holdings of management and foreign investors. The market valuation of Japanese firms’ cash holdings was lower than for US firms during the 1990s but increases to levels closer to those of US firms in the 2000s. Collectively, the evidence suggests that performance improves in those Japanese companies that reform their governance practices. These findings have implications for other Asian economies, such as China, India, and Korea, where there are ongoing discussions of whether improved governance can increase firm performance and valuation.

__________________________________________________ Kato is from the Osaka University of Economics; Li is from Jindal School of Management, UT-Dallas; Skinner is from University of Chicago, Booth School of Business. We appreciate comments from Julian Franks (NBER discussant), Yasushi Hamao, Akihiro Noguchi, Ronan Powell (JBFA editor), Akinobu Shuto, Dan Simunic, Tomomi Takada, Arnt Verriest, two anonymous referees, and workshop participants at Arkansas, Boston College, Harvard Business School (IMO conference), Melbourne, Minnesota Empirical Conference, Nagoya, NBER Japan Project, Southern Methodist University, Tilburg, and USC. Kato acknowledges financial support from the Japanese Society for the Promotion of Science, Granted-in-Aid for Science Research C21530485.

1

1. Introduction

In the weeks after Japan’s 2011 earthquake and tsunami and the ensuing negative

shock to equity prices, a great deal of attention focused on whether Japanese equities were

cheap.1 This is not a new perspective. At least since French and Poterba (1991), it has been

clear that common valuation metrics for Japanese firms often differ systematically from

those of firms in other countries. At the time French and Poterba first wrote their paper,

Japanese equity prices seemed too high based on P/E multiples. Since the “bubble” in

Japanese real estate and equity prices burst in 1990, Japanese equities have looked cheap by

conventional measures. Over the last two decades, price-to-book multiples for Japanese

firms have often been well below those of U.S. firms, with many below 1.2

Japanese firms are known for holding high levels of cash. Rajan and Zingales (1995)

examine cash holdings of companies across the G7, and find that Japanese firms held

substantially more cash than their G7 counterparts. Because large holdings of cash are

generally viewed as symptomatic of poor governance, this evidence is consistent with the

more general view that Japanese companies are poorly governed.

Japan’s corporate governance problems have received a great deal of attention. 3

Some argue that Japan’s poor governance was responsible for its economic performance

during the “lost decade” (Morck and Nakamura, 2001) and helps explain the low relative

valuations of its public companies. As Japan’s economic problems deepened during the mid

1 See, for example, “Buffett casts vote of confidence on Japan,” Financial Times, March 21, 2011. Buffett is quoted as saying that “(i)t will take some time to rebuild but it will not change the economic future of Japan…If I owned Japanese stocks, I would certainly not be selling them ... (f)requently, something out of the blue like this, an extraordinary event, really creates a buying opportunity.” 2 Milhaupt (2006) cites data showing that in 2000, approximately 13% of 779 non-financial firms on the Tokyo Stock Exchange were trading below their “bust up” values (measured as cash and cash equivalents plus investment securities minus debt). 3 The recent debacle at Olympus has again focused international attention on the governance practices of Japanese companies (for example, see “Pressure on Japan to probe Olympus,” Financial Times, October 25, 2011, as well as Michael Woodford’s book, “Exposure,” which describes the scandal in detail and relates it to governance problems in Japan (Woodford, 2012)).

2

to late 1990s, its government made a series of changes designed to remake its corporate

sector and financial system, including corporate governance reforms, which we describe

further in Section 2. The jury is still out on whether these reforms have led to substantive

changes in Japan’s corporate governance practices and the performance of its corporate

sector. While in some ways things have improved—the importance of the banks and the

keiretsu system generally have declined—in other ways it seems that the old ways of doing

business in Japan remain firmly in place.4 Corporate governance reform continues to be

discussed as part of Prime Minister Abe’s economic policies for pulling Japan out of its

ongoing economic problems.5

Our paper investigates whether there has been any progress in reforming the

governance of Japanese companies and, if so, whether this translates into improvements in

economic performance. There is little systematic evidence on these questions. They are

important not just in Japan, but in other markets that have adopted or are considering

Western-style governance practices—including China, Korea, and India—with the

expectation that this will improve the performance of the corporate sector and boost

economic growth. To do this, we examine whether Japanese companies increased their

payouts and reduced their cash holdings, whether this results in improved performance and

valuations, and whether these effects are related to firm characteristics likely to be associated

with governance, such as the nature of firms’ shareholders.

This approach has a number of advantages in assessing the effectiveness of

corporate governance reforms in Japan. First, our use of cash holdings and payout policy

4 Milhaupt (2006, p. 3) writes that “(o)ver the past decade, the formal institutional environment for Japanese corporate governance has been reformed significantly and at an accelerated pace…Yet, despite substantial legal reform and decade after Japan’s economic problems emerged, there has been no sea change in Japanese corporate governance practices.” 5 See, for example, “Shinzo Abe, shareholder activist,” The Economist, June 6, 2015.

3

provides a relatively direct way of assessing corporate governance reform in Japan.

Although one can measure corporate governance using various metrics and indices, these

measures generally have limitations because, first, corporate governance is multi-dimensional

and so not subject to direct measurement and, second, different corporate governance

structures are likely to be optimal for different firms (e.g., Larcker et al., 2007). This is

especially true in Japan, which allows firms to adopt either a western-style model or a more

traditional Japanese model, as we discuss further in Section 2.

Second, the management of cash has become a flashpoint for disagreements between

corporate managers and investors. As we discuss further in Section 2, the corporate finance

literature (e.g., Jensen, 1986; LaPorta et al., 2000) views managers’ tendency to hold excessive

levels of cash in the companies they manage as an important agency problem, and evidence

shows that high levels of cash are more likely in countries with weaker investor protection,

and that this has consequences for valuations. Activist investors frequently cite firms’ cash

balances as an example of poor governance, and engage with firms to force increased cash

payouts (Klein and Zur, 2009). The management of cash has become a common focus of

battles between external, activist investors and management over the last decade in Japan.6

We provide evidence that Japanese companies, on average and in aggregate, reduce

their cash holdings and increase their payouts after 2000, but that there is a good deal of

cross-sectional variation in these trends. Japanese firms still retain a lot of cash. The median

Japanese non-financial firm held about 15% of assets as cash in 2011, similar to the numbers

for the early 1990s (the median is 13% over 1990-1992). However, using regressions that

control for the effect of firm characteristics on cash holdings, we find that Japanese

managers have, on average, reduced their holdings of cash since 2000, by 3%-4% of assets. 6 See “A Clash over Cash,” The Economist, May 16, 2002. For a more extensive discussion of activist investing in Japan, see Buchanan et al. (2012), Hamao et al. (2011), and Uchida and Xu (2008).

4

To provide a benchmark for assessing the Japanese experience, we also report on the

cash holdings of US firms. US firms increased their cash holdings substantially over the last

two decades (Dittmar and Mahrt-Smith, 2007; Bates et al., 2009; Pinkowitz et al., 2016).

Consequently, although Japanese firms have historically held high levels of cash compared to

firms in other countries, Japanese and U.S. firms now hold roughly comparable levels of

cash, with the median U.S. firm holding cash of around 10-11% of assets over 2003 to 2008

(the number stays at around 11% over 2009-2011).7

Consistent with the idea that governance improves in Japan, Japanese managers now

manage cash more like their western counterparts: empirical models of cash holdings that

explain cash for U.S. firms are increasingly useful for Japanese firms. We find adjusted R-

squareds of around 30% for U.S. firms in the 1990s and 2000s; for Japanese firms, the

adjusted R-squared increases from 17% in the 1990s to around 32% in the 2000s.

Coefficient signs and magnitudes are similar for U.S. and Japanese firms in the 2000s; this is

not the case in the 1990s. This suggests that cash holdings for Japanese firms now depend

on largely the same economic factors that drive cash holdings for US firms, consistent with

similarly effective governance (Dittmar et al., 2003).

When we use these regressions to control for the effect of firm characteristics that

vary through time and across firms, we find that Japanese firms still hold more cash than

U.S. firms. A Japan dummy in the cash holdings regressions is consistently positive and

significant, and implies that, after conditioning on firm characteristics, Japanese firms hold

around 13%-14% more cash (as a fraction of assets) than similar U.S. firms over 2004-2007,

a result that is not greatly affected by the financial crisis.

7 Our conclusions are robust to different treatments of marketable securities, including excluding marketable securities from “cash” for Japanese firms and including them for US firms. US firms’ holdings of marketable securities increase significantly since the early 1990s while Japanese firms’ holdings of marketable securities, significant in the 1990s, essentially disappear around 2001.

5

Japanese firms have very different dividend policies from those of firms in most

other countries. While the fraction of dividend payers in major western economies declines

over the last 25 years (Fama and French, 2001, DeAngelo et al., 2008; Denis and Osobov,

2008; Floyd et al., 2015), over 80% of Japanese industrials continue to pay dividends.

However, these dividends are small compared to those of U.S. dividend payers. Our

evidence shows that the median Japanese dividend-payer pays out dividends that represent

0.6% of assets over the sample period compared to 1.8% for the typical U.S. firm.

Similar to what has occurred in the U.S. and elsewhere, stock repurchases have

become an important way for Japanese firms to return cash to stockholders. Japanese firms

have been able to make stock repurchases since the mid-1990s, a practice that was effectively

prohibited under the Commercial Code and securities exchange laws prior to this time. We

find that beginning around 1997, a substantial minority of Japanese firms (in the 10% to

30% range over 1999 to 2011) makes repurchases, and that the large majority of these firms

also pay dividends (as in the US, few firms only repurchase).

Repurchases contribute to strong growth in aggregate real payouts for Japanese

firms, from around ¥3 trillion in 1999 to around ¥10 trillion in 2008 (1991 real yen)

although dividends play a bigger role in the growth of payouts (of these totals, aggregate

dividends grow from ¥2.4 trillion to ¥6.5 trillion, or at a compound annual real rate of

11.7%). Firms that repurchase and pay dividends account for the bulk of this growth, and

tend to be the largest firms. As a fraction of assets or earnings, these firms pay out roughly

two to three times as much cash as firms that only pay dividends, suggesting a bifurcation of

payout policy (and perhaps capital management more generally) across firms.

We use residuals from regression models that explain cash holdings to measure

Japanese firms’ excess cash. For three non-overlapping periods (1994-2001, 2001-2007, and

6

2007-2011), we sort firms into deciles based on this excess cash measure. We then report

transition matrices which show how firms’ excess cash changes over these periods, and

analyze the relation between these changes and firm performance, measured using ROA and

Tobin’s Q. For the period most likely to benefit from reform, 2001-2007, changes in excess

cash are inversely related to changes in performance (this result also holds in 2007-2011, but

only for Q).

For these same periods, we estimate regressions that explain changes in firm

performance using both changes in excess cash and changes in cash payouts. For both

2001-2007 and 2007-2011, changes in performance are negatively related to changes in

excess cash and positively related to changes in cash payouts; these results are both

economically and statistically significant. These findings are consistent with the idea that

improved governance, as manifested in improved management of cash, is associated with

improved corporate performance.

To tie these results more closely to governance, we show that changes in

performance, changes in excess cash, and changes in cash payouts are related to changes in

ownership characteristics in ways consistent with improvements in governance helping to

explain the changes. We find that ownership characteristics likely to be associated with good

governance (foreign ownership, management ownership, ownership by financial institutions)

tend to be related to decreases in excess cash and increases in payout, while the opposite is

true of bank loans, which is likely to proxy for the influence of banks, and so associated with

poor governance. Further, these ownership characteristics are directly related to changes in

firm performance in ways consistent with our expectations (changes in foreign ownership,

management ownership, and financial ownership are positively related to improvements in

performance, while changes in bank loans are negatively related). During the 2001-2007

7

period most likely to benefit from reform, we find an economically significant relation

between improvements in performance and declines in excess cash. We also show that

performance improves more in firms for which the influence of banks (as measured by bank

ownership and loans) declines and the ownership of foreign investors and managers

increases. These results support the idea that governance reforms lead to improved capital

management and performance for firms that adopt them.

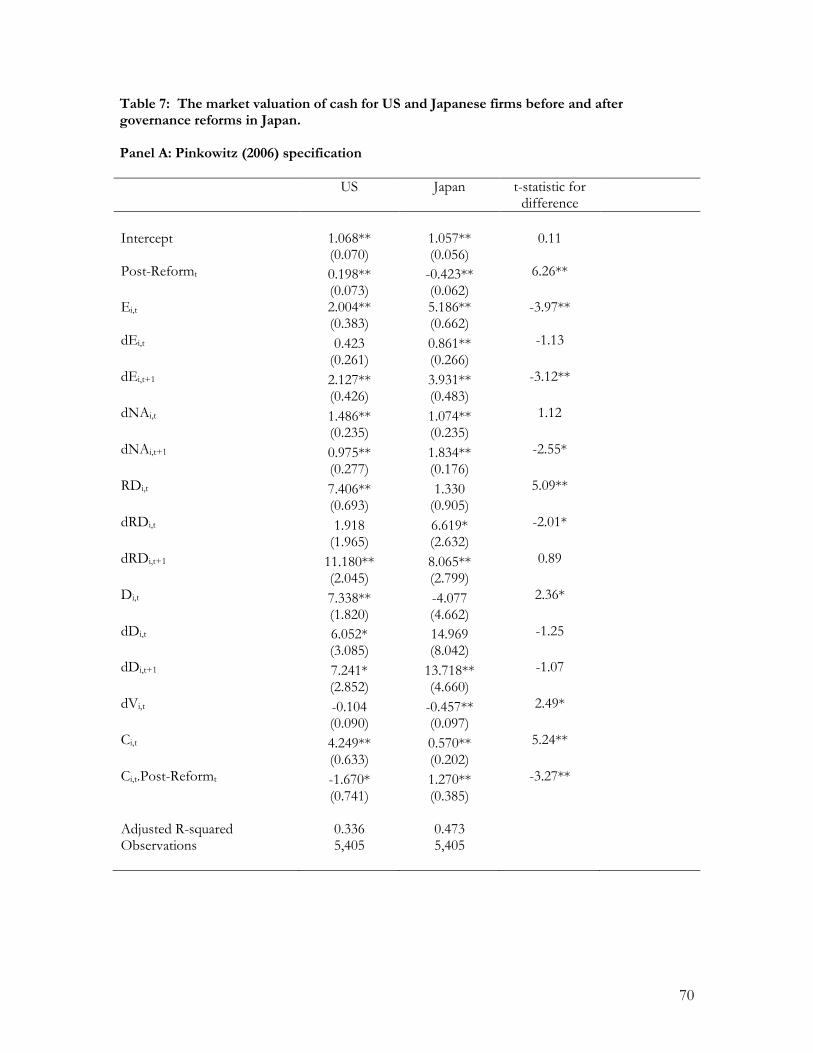

Following previous work on governance (Dittmar and Mahrt-Smith, 2007; Pinkowitz

et al., 2006) we also provide evidence on differences between the market valuation of cash

for US and Japanese firms. The market valuation of cash for Japanese firms is lower than

for US firms in the 1990s, consistent with poorer governance in Japan, but increases to

comparable levels during the 2000s, consistent with improved governance.

Our analysis is inherently cross-sectional, which makes it hard to make strong causal

statements about the relations between firms’ ownership characteristics, cash holdings,

payout policies, and performance. Nevertheless, to date there is virtually no evidence on

whether the reforms that have been widely discussed in the wake of Japan’s long-standing

economic problems have actually had any effect. While Japanese firms are known to have

different dividend policies from firms in other major countries (Dewenter and Warther,

1998), there is little evidence on the extent to which Japanese firms repurchase or on the

overall level of payouts by Japanese firms. We present evidence of a relationship between

changes in cash holdings, payout policy, and firm performance, as well as of a relation

between these changes and changes in ownership characteristics that capture elements of

Japan’s unusual keiretsu (“main bank”) corporate system that is often blamed for its

economic problems. As such, our evidence sheds light on the important questions of

8

whether corporate Japan has actually reformed and whether such reforms improve

performance.

Our research has implications that go beyond Japan. We ask whether western-style

governance is effective in economies with underlying institutions that differ from those of

western economies such as the U.S. and U.K. Japan has certain “institutional rigidities,”

such as a powerful business lobby (Keidanren) and a judiciary that opposes shareholder rights,

which impede the ability of reforms to achieve their goals.8 Similar institutional rigidities

exist in other Asian economies. In China, the prevalence of state-owned enterprises makes it

difficult for shareholder-based governance to be effective; in Korea, the prevalence and

influence of the large corporate groups (chaebol) are a powerful force that resists change; in

India, there are similar issues with “pyramidal” business groups.9 Our evidence indicates

that reforms in governance can improve performance in spite of these rigidities.

Section 2 provides a summary of the governance literature as it pertains to the

management of cash, discusses governance reform in Japan, and presents our empirical

predictions. Section 3 details our sample and data. Section 4 presents our evidence on the

relation between Japanese firms’ cash holdings, payout policy, and governance. As an

alternative approach to assessing governance reform, Section 5 provides the evidence on

whether the valuation of cash holdings improves for Japanese firms. Section 6 concludes.

8 For evidence on how these rigidities have hindered western-style investor activism in Japan, see Buchanan et al. (2012) and Hamao et al. (2011). Keidanren is an organization that represents the interests of the Japanese corporate sector and that has representation from over 1,300 Japanese companies as well as industry and local economic associations, with the self-stated goal of supporting the “self-sustaining development of the Japanese economy and improvement in the quality of life for the Japanese people” (http://www.keidanren.or.jp/en/profile/pro001.html last accessed April 27, 2016). It is widely seen as being resistant to governance reform. In discussing recent efforts to reform Japanese corporate governance, the Economist wrote “Past efforts at reform have been stonewalled by Keidanren, Japan’s big-business lobby,” see “Corporate governance in Japan: A revolution in the making,” The Economist, May 3, 2014. 9 See, for example, Nakamura and Fruin (2012) on China, and Khanna and Palepu (2000) and Bertrand et al. (2002) on India. Nakamura and Fruin discuss the implications of the Japanese experience for governance in China and other emerging Asian economies. On the similarity of these problems in Japan and Korea, see for example, “Corporate savings in Asia: A $2.5 trillion problem,” The Economist, September 27, 2014.

9

2. Theory and empirical predictions

2.1 Cash holdings and corporate governance

“Corporate governance deals with the ways in which suppliers of finance to

corporations assure themselves of getting a return on their investment. How do the

suppliers of finance get managers to return some of the profits to them?” (Shleifer and

Vishny (1997, p. 737). A large literature points to managers’ tendency to hold excessive cash

in their firms as an important agency problem. Jensen (1986) and La Porta et al. (2000),

among others, argue that managers have incentives to over-retain cash to divert resources

for pet projects, engage in empire building, or otherwise benefit themselves at the expense of

outside shareholders. As Myers and Rajan (1998) point out, high levels of corporate liquidity

(relative to other types of investment such as assets in place) make shareholders especially

vulnerable to managers’ tendency to waste corporate resources, which makes governance

especially important for firms with large cash holdings.

Dittmar et al. (2003) report that firms in countries with poor shareholder protection

hold up to twice as much cash as those in countries where shareholders are better protected.

Kalcheva and Lins (2007) and Lee and Powell (2011) report similar evidence. Pinkowitz et

al. (2006) and Kalcheva and Lins (2007) show that the value of cash holdings is lower in

countries with poorer investor protection relative to those with stronger protection and,

conversely, that the value of dividends is higher in these countries. Dittmar and Mahrt-

Smith (2007) show that the market valuation of cash holdings is lower for firms with poor

governance and that poorly governed firms waste cash and exhibit weaker operating

performance. Chen et al. (2012) provide evidence that the cash holdings of Chinese

companies declined after an exogenous shock that improved governance.

There is consistent evidence that activist investors, especially hedge funds, target

10

firms that have agency problems related to excess cash. Brav et al. (2008) report that

activists increase value by taking various actions, including increasing payouts. Brav et al.

(2010) focus on hedge fund activists, and show that these investors focus on ‘value’ firms

with low relative valuations, sound operating cash flows, and low dividend payouts; that is,

on “cash cows” that suffer from agency costs of free cash flow. Klein and Zur (2009) show

that hedge fund activists target firms with agency problems related to cash, and that they

achieve sustainable improvements in performance by forcing these firms to increase payouts.

Becht et al. (2015) report evidence on shareholder activism around the world,

including the US, Europe, and Asia. Their Asian subsample includes mostly Japanese firms.

Their evidence shows that while successful activist campaigns generate positive returns

around the world, activists in Asia are much less likely to succeed compared to those in

Europe and the US. This is generally consistent with the evidence from Japan. Hamao et al.

(2011) and Uchida and Xu (2008) focus on activism in Japan, and show that activists target

firms with high cash balances and low payouts to shareholders, with limited success. This

evidence is consistent with the idea that institutional rigidities in Asia make it difficult for

activists to effect change in the firms they target.

The arguments and evidence summarized above make it clear that high levels of cash

holdings (and low levels of shareholder payouts) are generally associated with managerial

agency problems and poor governance.10 As we discuss next, Japanese firms are well known

for high cash holdings, poor financial performance, and poor governance, which explains

why the Japanese Government and its regulators have consistently pushed for improvements

in governance. This also motivates our focus on Japan, which we see as a useful setting for

10 This is not to say that all firms with high cash balances perform poorly. As Pinkowitz et al. (2016) discuss, US multinationals, including prominent technology firms such as Apple, Google, and Microsoft, are known to hold high levels of cash, in part for tax reasons. Apple has been subject to activist pressure to reduce its cash holdings (for example, see “Einhorn squeezes Apple for its cash,” Wall Street Journal, February 11, 2013).

11

examining the link between governance and cash holdings, payout policy, and firm

performance.

2.2 Corporate governance reform in Japan

The Japanese economy has performed persistently poorly over the last two decades.

One of the alleged culprits has been Japan’s unusual and (some argue) ineffective corporate

governance. Fukao (2003) blames the lost decade on weak governance of Japanese banks

and insurance companies, while Hoshi and Kashyap (2001) discuss the Japanese financial

system and its link to economic performance, especially during the 1990s. Morck and

Nakamura (2001) argue that Japanese corporate governance helps explain the poor

economic performance of its corporate sector.

An important distinguishing feature of the Japanese system is the role of the “main

bank” system and the related keiretsu structure (Aoki et al., 1994; Hoshi and Kashyap, 2001;

Morck and Nakamura, 2004). Under this system, creditors, especially banks, play an

important role in governance, employees (including management) are seen as an important

stakeholders, and shareholders’ rights are relatively less important than in western

economies.

A large number of authors discuss and analyze corporate governance reforms in

Japan. These reforms are complex and multifaceted, and span the mid-1990s through the

early 2000s. Some of these reforms occur organically as a result of other changes in the

economy. The crisis in the banking sector in the mid-1990s, which was due mainly to the

bursting of the bubble in stock and real estate prices that occurred earlier in the decade and

that resulted in a very substantial non-performing loan problem, led the government to inject

capital into the banks and force them to divest their large holdings of shares in non-financial

public companies (Hoshi and Kashyap, 2001; Nakamura, 2006). This led, in turn, to an

12

increase in the share holdings of individual and institutional investors, both domestic and

foreign. Because of the increase in shares held by outsiders, managers of non-financial firms

faced pressure to improve their disclosures and governance practices (Nakamura, 2006).

In addition, as discussed by Hoshi and Kashyap (2001, Ch. 7), the period from the

end of the ‘high growth’ period in Japan in the early 1970s through to the “Big Bang” in

1996, can be characterized as a period of deregulation (also known as liberalization) of the

financial sector. They describe how changes during this period changed the nature of

Japanese corporate governance, mainly due to reduced importance of bank loans in

financing companies (changes in the Commercial Code liberalized industrial companies’

ability to access debt markets and issue bonds) and more generally in weakening the strong

links between banks and industrial companies that were a hallmark of the keiretsu structures

that had hitherto dominated Japanese corporate finance.11

The Japanese Government made a series of changes in the Commercial Code (CC)

from 1993 to 2002 that brought regulation of the capital markets closer to the Western

model and were designed to improve the governance of Japanese companies.12 The most

important of these changes are as follows:

• Beginning in 1997, the CC formally authorized the issuance of stock options.

Milhaupt (2006) cites survey evidence, which shows that the number of companies issuing

stock options to employees or managers increased from 0 in 1997 to 463 in 2001.

11 Hoshi and Kashyap (2001, pp. 289-290) indicate that the Japanese Big Bang “... should be viewed as the last stage of a gradual deregulation that started in the late 1970s” that “completed the transformation of the Japanese financial system from a heavily regulated bank-centered system…to a liberalized, market-based system.” The stated goal of the Big Bang was to make the markets “fair, free, and global.” 12 The discussion that follows draws on discussions of Japanese corporate governance reform in Araki (2005), Gilson and Milhaupt (2005), Patrick (2004), Milhaupt (2006), and Shishido (2001).

13

• As described in detail in Appendix B, a sequence of legal changes during the 1990s

and early 2000s removed restrictions on share repurchases. As we show below, this has

resulted in a very significant increase in the use of repurchases by Japanese firms.

• In 2000, the Civil Rehabilitation Act, modeled loosely on the U.S. Chapter 11

process, was passed, which allowed for more flexible and efficient corporate reorganizations.

This law introduced a debtor-in-possession system and allowed ‘pre-packaged’ bankruptcies

for the first time.

• In 1997, merger procedures were liberalized and in 1999, the CC was further revised

to allow share-for-share exchanges and to eliminate the prohibition on the use of holding

company structures. A further change in 2000 provided enhanced flexibility for separating

business units from parent companies. These changes opened the door for an increase in

M&A activity (prior to these changes, M&A generally, and especially hostile M&A

transactions, were essentially precluded under Japanese law). These changes also promoted

the use of spin-offs, divestitures, and other forms of corporate restructuring. Milhaupt

(2006) discusses the fact that Japan saw one of the first hostile M&A bids in 2000, and

presents data that show a large increase in M&A activity from 1997 to 2000.

• The costs of filing derivative lawsuits brought by shareholders against the

management of companies was substantially reduced, which increased the number of such

lawsuits significantly.

• There were several reforms to the statutory auditor system, which had the effect of

strengthening their role in governance (the role of statutory auditors, as is also true under the

traditional German governance model, is to monitor the board’s compliance with the law

and certificate of incorporation). These included extensions in the term of the auditors,

14

expansion of their responsibilities, and increases in the number and required qualifications of

these auditors. By 2005, at least half of the board of auditors must be outside auditors.13

• A major change in the CC in 2002 allowed firms to opt out of the traditional

statutory auditor board model in favor of a US-style committee system of board governance.

In lieu of statutory auditors, firms establish board committees for audit, nomination, and

compensation, each of which must have more than three members, the majority of whom

must be external, non-employee directors. Milhaupt (2006) cites survey evidence, which

shows a large increase in the number of firms that reduce board size (number of directors)

to less than ten and which add outside directors.

• Over the period from around 1997 to the early 2000s, accounting standards and

disclosure requirements were significantly revised to bring them into line with international

standards, including requiring cash flow statements, the introduction of deferred tax

accounting, consolidated financial statements, mark-to-market accounting for marketable

securities, the reporting of pension obligations on balance sheets, quarterly reporting, among

other changes (e.g., Urasaki, 2014). Japan instituted the Accounting Standards Board of

Japan, a private standard-setter modeled on the US FASB, in 2001. Legislation in 2003

enhanced the ability of the Financial Supervisory Agency (FSA) to oversee the accounting

and auditing industry.

At least three conclusions are evident from this discussion. First, changes in

Japanese corporate governance were relatively slow moving and were linked to other

changes, such as overall liberalization of the financial system and the banking crisis that

began around 1997. Second, many of these changes, most notably the fact that companies

13 These auditors are not to be confused with external auditors, such as the Big 4 audit firms. The external audit process functions in Japan in much the same way as it does elsewhere in the world, including in the US and UK, although there are some differences (Skinner and Srinivasan, 2012).

15

could ‘opt in’ to a western-style governance model, meant that there was likely to be

considerable variation in the extent to which companies adopted governance reforms as well

as the nature of the changes that they made.14 Third, the changing nature of the financial

system likely induced certain changes in the governance model, the most obvious example

being the declining influence of the banks in governance of industrial companies.

These points help justify our focus on cash holdings and payout policy as measures

of governance. Because there is no single preferred or required governance model, and

because firms endogenously choose different models best suited to their characteristics, it

would be hard to create a measure of governance that adequately captures governance

quality or to use such a measure to gauge how governance changes over this period. Nor is

it possible to identify a single point in time when these reforms occur. Moreover, as

discussed in Section 2.1 above, there is a substantial body of theory and evidence that

supports a relation between the management of cash holdings and corporate governance.

2.3 Empirical predictions

In spite of the large literature on the effectiveness of governance reforms in Japan,

there is little empirical evidence on whether Japan’s governance reforms improve corporate

performance and increase returns to stockholders, although some recent work provides

evidence on investor activism in Japan. Hamao et al. (2011) report mixed evidence on the

ability of activist investors to reform Japanese companies between 1998 and 2009, and

widespread adoption of poison pills since 2006; see also Uchida and Xu (2008) and

Buchanan et al. (2012).

14 Patrick (2004, p. 27) concludes his discussion of Japanese corporate governance reform by stating that “…there is no monolithic Japanese corporate governance system today and there will not be one in the future. Different firms will have different corporate governance systems, depending on their histories, ownership patterns, and leaders,” and that “…the variance of corporate governance arrangements will be substantially wider than in the past (emphasis added).”

16

Our main empirical prediction is that the reforms of the late 1990s had two

observable effects on Japanese companies: (1) to improve capital management practices by

lowering excess cash and increasing payouts to shareholders, and (2) to improve operating

performance. Notice that the mechanism we posit is that reforms lead to improvements in

both capital management and operating performance; we are not arguing that the channel is

from governance to capital management to performance.15 These are essentially the same

arguments that form the basis for investor activism, as described above. Because most

reforms were not mandatory, there is likely to be variation in the extent to which they are

adopted by firms, which allows us to exploit cross-sectional as well as time-series variation.

We use the approach of Opler et al. (1999) to model cash holdings,. Dittmar et al.

(2003) use the extent to which this type of cash holdings model fits the data as a measure of

governance—because this model captures how cash holdings vary with the economic forces

(such as investment opportunities and precautionary demand for cash) that affect cash, the

fit of the model can be used to assess governance quality. Following this approach, we

expect that this model will work better for Japanese firms in the period after governance

reform.

Based on these arguments, we expect an inverse relation between changes in excess

cash holdings and firm performance in the 2001-2007 period when reforms are most likely

to take effect. Because we posit that this inverse relation is due to governance reform, we do

not expect to observe this relation in other periods (Japanese firms in the 1990s) or settings

(for US firms). Our use of cash holdings as a measure of governance quality for Japanese

companies is supported by recent evidence in Aoyagi and Ganelli (2014). These authors

15 In other words, the reforms have separate effects on capital management and operating performance. However, under the Jensen (1986) free cash flow argument, forcing managers to disgorge excess cash limits their ability to engage in value-destroying investments, which improves performance.

17

show that the cash holdings of Japanese firms are inversely related to the “Proprietary

Bloomberg Score,” which they describe as a comprehensive governance index applicable to

Japanese companies.16

We also test predictions about how these effects are likely to vary across firms as a

function of ownership structure. Based on previous research on the keiretsu structure of

Japanese firms (Weinstein and Yafeh, 1998; Morck and Nakamura, 1999; Pinkowitz and

Williamson, 2001), we expect that firms more strongly aligned with these corporate groups

are more likely to improve their capital management policies and firm performance when the

influence of the banks that sit at the center of these groups declines.

We also report results from tests of whether the market’s valuation of cash improves

for Japanese firms in the post-reform period. Following Pinkowitz et al. (2006) and Dittmar

and Mahrt-Smith (2007), we estimate cross-sectional regressions of firm value on various

determinants, including cash holdings. These authors argue that lower coefficients on cash

in these regressions are indicative of poorer governance. We investigate whether coefficients

on cash are lower for Japanese firms relative to US firms in the period before reform, and

whether this coefficient increases after the reforms are in place.

3. Sample and data

We first compare the cash holdings of Japanese and US firms. The US is often held

out as a model for Japanese governance (Nakamura, 2011) and is commonly used as a

benchmark in cross-country governance studies (Doidge et al., 2004; Aggarwal et al., 2008).

Our data are from WorldScope, collected via Thomson Reuters DataStream (Japanese and

US firms), and from Nikkei Financial Quest and Nikkei Quick (Japanese firms).17 The sample

16 This index includes measures of board size, percentage of outside directors, disclosure quality.

18

includes Japanese firms listed on the Tokyo Stock Exchange and JASDAQ, and US firms

listed on the NYSE, AMEX, and NASDAQ from 1990 to 2011. This period includes the

bursting of the bubble in Japan, which began its economic malaise and so is a suitable

starting point for our study. We drop observations with missing total assets and exclude

utilities, transportation, and financial firms. Data for Japanese repurchases comes from

Nikkei Quest, supplemented with data drawn directly from financial statements.

Bates et al. (2009) define cash as the sum of cash and marketable securities in their

study of the cash holdings of US firms. Because of possible differences in Japanese firms’

use of marketable securities, we exclude marketable securities and measure cash holdings

simply as cash divided by total assets.18 To be consistent, we do the same for US firms. We

replicate all of our analyses using the sum of cash and marketable securities in place of cash

and discuss substantive differences below; our main inferences are not sensitive to the

treatment of marketable securities. In the next section we discuss how Japanese firms’

holdings of marketable securities change over our sample period.

We define keiretsu firms as those that belong to one of the largest six large horizontal

keiretsu, also known as enterprise groups (Dewenter and Warther, 1998). We obtain these

data from Industrial Groupings in Japan (IGJ, 2001), a standard source of these data, and

classify firms as keiretsu firms if they are classified in IGJ as horizontal keiretsu firms with

inclination scores of 2-4. Our results are robust to variations of this definition.

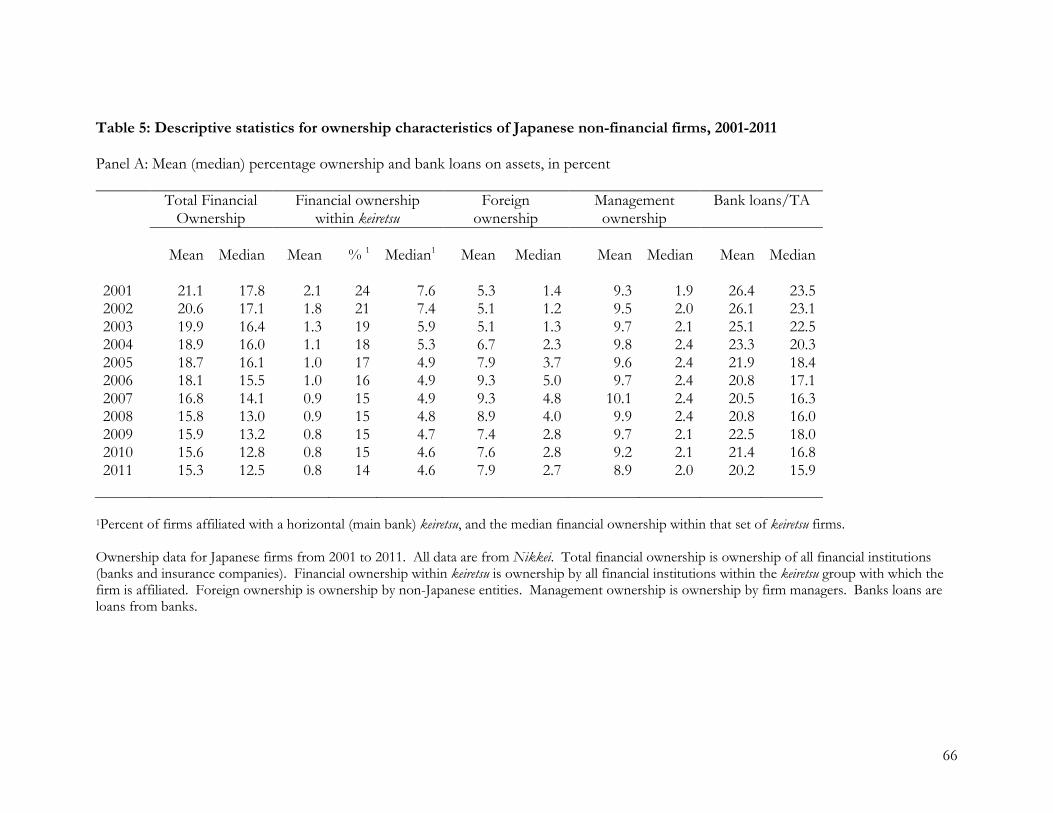

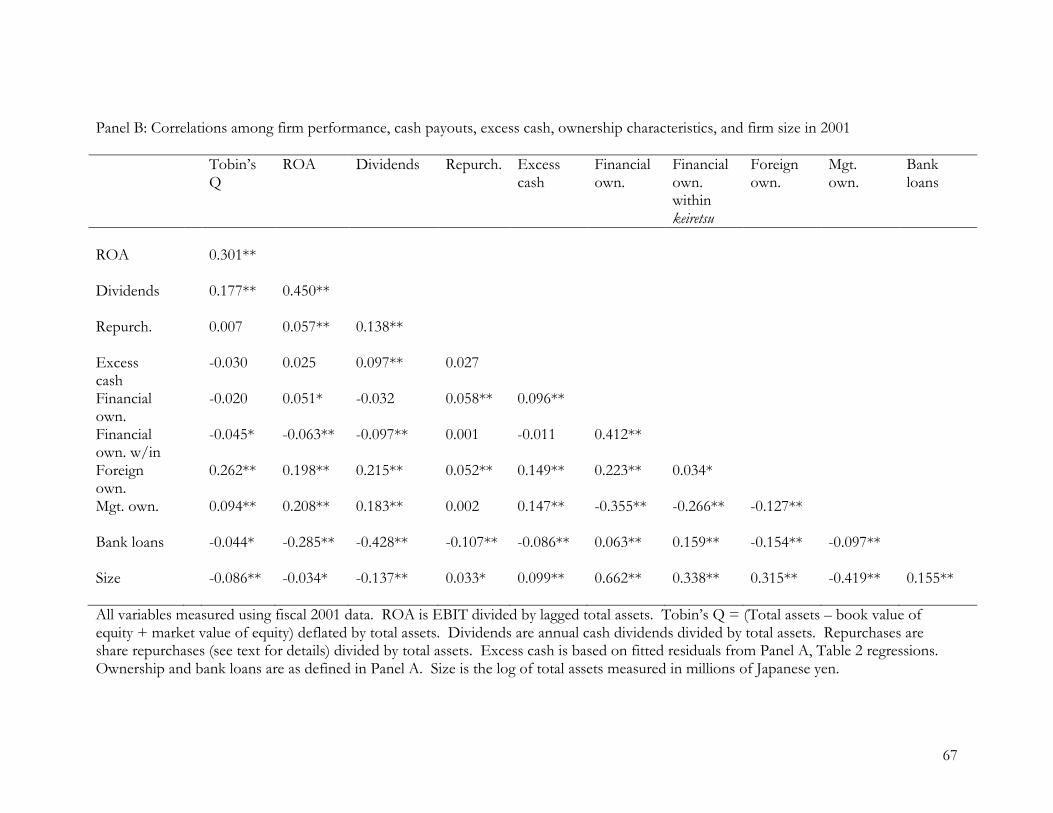

We also obtain data on the ownership characteristics of Japanese firms. We measure

the fractional holdings of financial institutions (both total and within the firm’s keiretsu),

17 We also compute certain variables for the US firms using Compustat as a robustness check. For the cash holdings variable, we obtain larger sample sizes using Compustat for US firms and Nikkei for Japanese firms than are available on WorldScope. Our inferences are not affected by the source of the data. 18 Pinkowitz and Williamson (2001) also exclude marketable securities to measure cash for Japanese firms.

19

foreign ownership, and management ownership. These data are from Nikkei beginning in

2001.

4. Evidence

4.1 Differences between Japanese and US industrial firms, 1990-2011

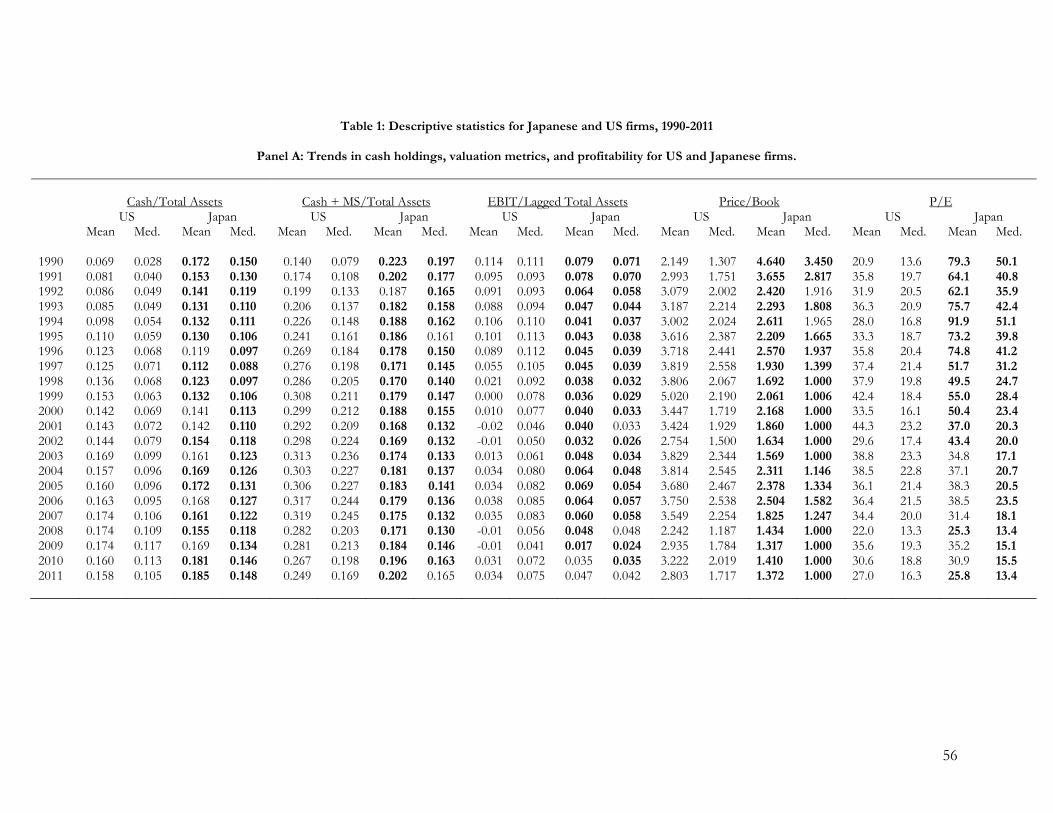

We begin by comparing the cash holdings, profitability, and valuation of Japanese

and US companies since 1990. Table 1, Panel A reports means and medians for cash

deflated by total assets, cash and marketable securities deflated by total assets, profitability

(EBIT/lagged TA), price-to-book ratios, and price-earnings ratios by country and year.19

For Japanese firms, the mean ratio of cash/assets is 17.2% (median 15.0%) in 1990,

substantially higher than for US firms for which the mean is 6.9% (median 2.8%), consistent

with Rajan and Zingales (1995). The cash holdings of Japanese companies decline through

1997, when the average reaches 11.2% (median 8.8%). After this, average cash holdings

increase to 17.2% (median 13.1%) in 2005, higher than for US firms but by a smaller margin

(the mean for US firms in 2005 is 16.0% and the median is 9.6%). The numbers then

fluctuate before increasing to 18% (15%) in 2010 and 2011.20 So Japanese firms still hold

more cash than US firms but the differences are smaller than in the early 1990s, due largely

to an increase in the holdings of US firms (Aoyagi and Ganelli (2014), provide evidence that

Japanese firms hold more cash than their G7 counterparts over 2004-2012). We revisit this

conclusion below, however, using regressions that control for the effect of firm

characteristics.

19 Cash deflated by total assets and (cash + marketable securities) deflated by total assets are winsorized at 0 and 1, ROA at -1 and 1, price-to-book ratios at 0 and 30, and P/E ratios at the 1% and 99% percentiles. Bold numbers for Japanese firms indicate significant differences from the corresponding number for US firms at the 1% level or better under two-tailed tests. 20 Median cash ratios of Japanese are significantly higher than those for US firms (at the 1% level, two tailed) for the full time period. Mean cash ratios are not significantly different from those of US firms in 1996, 2000-2003, 2006, and 2009 but are significantly higher in all other years.

20

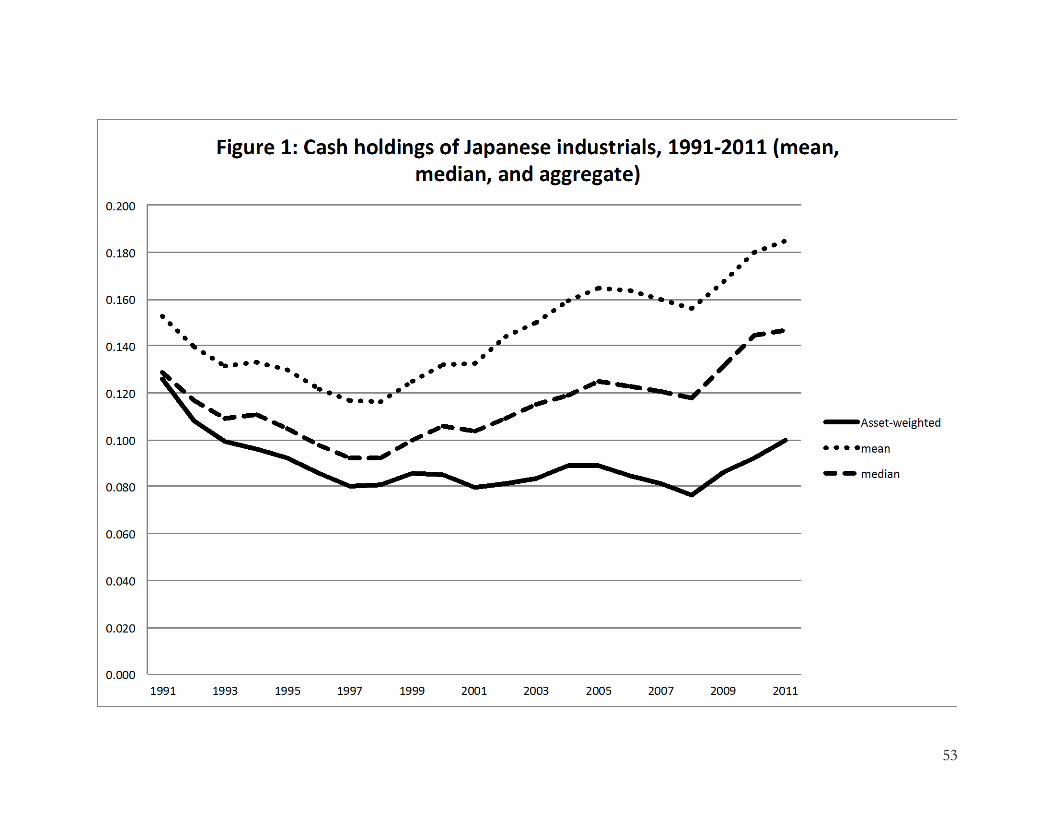

Figure 1 plots mean and median ratios of cash/total assets for Japanese firms as well

as the asset-weighted ratio (aggregate cash divided by aggregate assets). The asset-weighted

ratio is consistently below the mean and median, indicating lower cash holdings for the

largest Japanese firms. The increasing divergence of the three series in Figure 1 reflects a

substantial increase in the dispersion of cash holdings across Japanese firms after 2000. This

approximately coincides with the introduction of the governance reforms, consistent with

our argument that the reforms increased the cross-sectional dispersion of governance.

When we include marketable securities along with cash (Panel A, Table 1) the

conclusions change, largely because of differential trends in holdings of marketable

securities. US firms increase their holdings of marketable securities from 1998 to 2007 to a

mean (median) of 15% (5%) of assets after which they fall to 10% (1%) by 2011 (not

reported in tables). In contrast, Japanese firms hold around 5% (3%) of assets as marketable

securities through 1997 after which there is a sharp decline to around 1% (0%) in 2001, with

little subsequent change.21

The increase in US firms’ holdings of marketable securities for most of our sample

period means that conclusions about the level of cash holdings reverse when we include

marketable securities. Beginning in the mid to late 1990s, US firms’ holdings of cash and

marketable securities exceed those of Japanese firms by increasingly large amounts and

continue to do so through most of the rest of the period. US firms’ mean (median) holdings

of cash and marketable securities are consistently around 30% (21%-25%) over 2000-2007

compared to 17%-18% (13%) for Japanese firms. One possibility is that while US firms

21 There are two non-mutually exclusive explanations for the decline in Japanese firms’ holdings of marketable securities from 1997 to the early 2000s. First, the decline reflects the general unwinding of corporate cross-holdings that begins in the mid-1990s (Miyajima and Kuroki, 2007). Second, the decline in 2001 could reflect Japanese firms’ response to the introduction of mark-to-market accounting for these securities: many Japanese firms reclassified their equity holdings as long-term in this year, apparently to avoid mark-to-market treatment that became effective for 2001 fiscal year-ends (Urasaki, 2014).

21

treat marketable securities as being akin to cash and short-term liquidity, Japanese firms’

holdings were more strategic, including the cross-holdings that form part of the keiretsu

structures. If this is the case, it seems appropriate to exclude marketable securities for

Japanese firms (this choice doesn’t matter very much after 2001, when most Japanese firms

hold essentially no marketable securities). This logic also implies that the appropriate

comparison is between cash holdings for Japanese firms and cash and marketable securities

for US firms, in which case we would conclude that US firms hold more short-term liquidity

than Japanese firms in every year except 1990 and 1991. In any event, these univariate

comparisons are not very meaningful, as discussed below. We conduct all of our primary

analyses of the relation between changes in excess cash and firm performance (reported

below) including and excluding marketable securities for Japanese firms, without any

meaningful changes in inferences.

We use accounting profitability (ROA = EBIT on lagged total assets) to compare the

performance of Japanese and US firms. Japanese firms are substantially less profitable than

US firms for most of this period. Median ROA is significantly lower for Japanese firms in all

years except 2001, 2008, and 2011 when the differences are not significant. Mean ROA is

also significantly lower for most of the 1990s, although ROA becomes more volatile for US

firms during the 1990s due to increasing left-skewness in the earnings cross-section, a trend

that continues during the 2000s.22 Japanese firms do not display the tendency of US firms to

22 This increasing left skewness is due to at least two related phenomenon. First, as discussed by Fama and French (2004), there has been a systematic shift in the nature of US publicly-traded firms, with firms tending to go public earlier in their life cycles. Second, US firms are reporting losses at an increasing rate (Hayn, 1995; Klein and Marquardt, 2006), and these losses tend to increase in size over time.

22

report large write-downs and losses, and generally show much less cross-sectional dispersion

in profitability.23

To try and hold size and sample composition roughly constant, we also compare the

profitability of the largest 1,500 US and Japanese firms (not reported in tables). Large US

firms are about twice as profitable as Japanese firms, with mean (and median) ROA of about

10% compared to 4.7% (4.2%) for Japanese firms. These differences are fairly consistent

during the full period of our study.

To get a sense for whether Japanese firms are “cheap” in terms of conventional

benchmarks, we also compare price-to-book (P/B) and price-earnings (P/E) ratios for

Japanese and US firms. P/B ratios are persistently lower for Japanese firms. During the

1990s, P/B ratios for US firms average 3.40 (median 2.13) while those for Japanese firms

average 2.36 (median 1.86). [The decade-by-decade numbers are not shown in tables.]

During the 2000s the differences widen to 3.50 (2.09) for US firms versus 1.84 (1.00) for

Japanese firms.

After reaching a peak in 1994, when the mean (median) P/E ratio was 92 (51)—the

phenomenon that French and Poterba (1991) study—P/E ratios for Japanese firms decline.

While partly due to a decline in Japanese equity prices, this is also due to a consistent

increase in Japanese firms’ EPS, in part due to the fact that Japanese accounting rules

changed significantly over this period.24 P/E ratios for US firms show little trend, with the

median varying in a tight range around 20 and the mean varying between approximately 30

and 40. P/E ratios for Japanese and US companies are similar over 2003 through 2011.

23 Some argue that earnings management (particularly to avoid losses and earnings decreases) is more prevalent in Japan (e.g., Suda and Shuto, 2005). 24 French and Poterba (1991) discuss the fact that the high P/E ratios they observed in the 1980s for Japanese companies were partly driven by differences in accounting pushing down EPS numbers, including the fact that most financial statements in Japan were not consolidated. These accounting differences had largely disappeared by the early 2000s, which could explain at least part of the upward trend in Japanese P/E ratios.

23

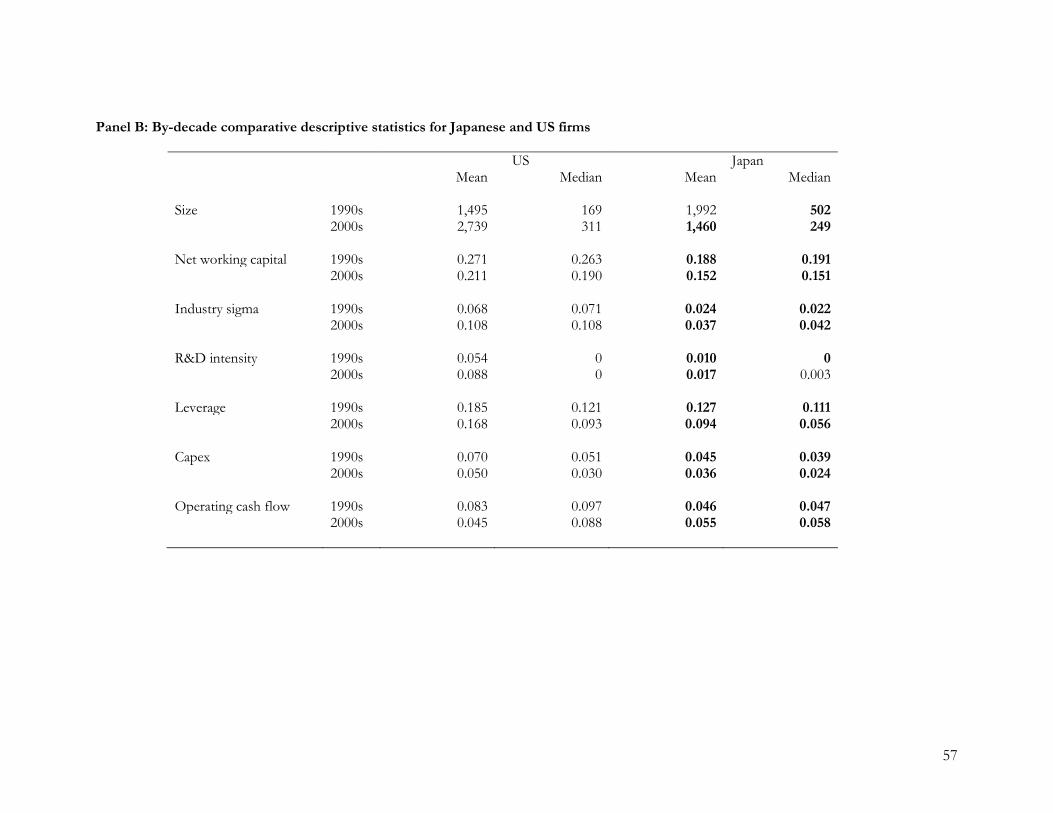

In Panel B of Table 1 we compare net working capital (excluding cash), industry

sigma, R&D intensity, leverage, capital expenditures, and operating cash flows. Along with

P/B ratios, these are the important determinants of cash holdings (Opler et al., 1999; Bates

et al., 2009). To economize on space, we report means and medians for each set of firms by

decade (1990s and 2000-2011); we provide variable definitions in Appendix A.25

Japanese and US firms differ in a number of respects likely to affect cash. First,

Japanese firms have lower P/B ratios (above) and R&D intensity throughout most of the

sample period. While median R&D intensity is always close to zero, means are 5.4% and

8.8% for US firms versus 1.0% and 1.7% for Japanese firms over the 1990s and 2000s,

respectively. (All differences across countries are statistically significant at the 5% level or

better.) Second, Japanese firms are considerably less volatile than US firms: median industry

sigma is 7.1% and 10.8% for US firms compared to only 2.2% and 4.2% for Japanese firms,

with similar inferences for means. Other things equal, these differences imply that Japanese

firms would hold less cash than US firms (growth opportunities and volatility tend to be

positively associated with cash holdings).26

Third, Japanese firms generally are less levered and have lower operating cash flows,

lower capital expenditures, and less working capital than US firms. (Mean leverage for US

firms is 0.185 and 0.168 versus 0.127 and 0.094 for Japanese firms across the two decades,

respectively, with similar inferences for medians; median operating cash flows are 0.097 and

0.088 for US firms versus 0.047 and 0.058 for Japanese firms, with slightly different

inferences for means; mean capex for US firms is 0.070 and 0.050 versus 0.045 and 0.036 for

25 For each decade we report medians of the annual means and medians. 26 Statements about the relation between firm characteristics and cash holdings are based on previous research on cash holdings; for example, see Bates et al. (2009), Pinkowitz et al. (2016) or Opler et al. (1999). Pinkowitz et al. (2016) estimate this model using a large sample of firms drawn from a large cross-section of countries and find that cash holdings are positively related to industry volatility, P/B, and R&D and negatively related to firm size, capital expenditures, cash flows, net working capital, and leverage.

24

Japanese firms, with similar inferences for medians; mean net working capital is 0.271 and

0.211 for US firms versus 0.188 and 0.152 for Japanese firms, with similar inferences for

medians.) Because these characteristics are generally negatively related to cash holdings, they

help explain why Japanese firms hold more cash than US firms.

To compare the cash holdings of Japanese and US firms conditional on firm

characteristics, we use variants of the model from Opler et al. (1999). Based on the

transactions costs and precautionary demands for cash, Opler et al. model cash holdings as a

function of firm size, a dividend-payer dummy, leverage, price-to-book, industry sigma, net

working capitals, R&D intensity, capital expenditures, and cash flow, to which we add

profitability and a loss dummy. We use fitted residuals from these regressions later in the

paper to measure Japanese firms’ excess cash holdings, a key variable in our analysis.

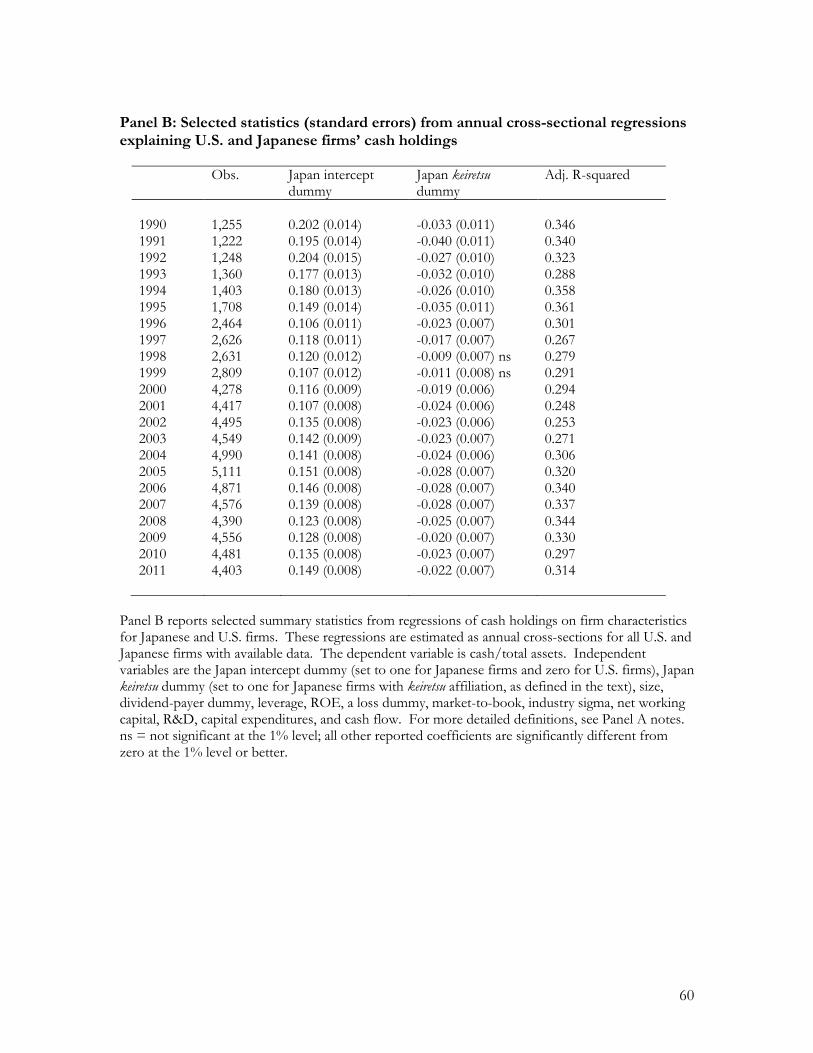

We first estimate panel regressions for each country, both for the full period (1990-

2011) and by decade (1990-1999 and 2000-2011), and report the results in Table 2, Panel A.

This allows us to assess whether the economic determinants of cash differ across Japanese

and US firms, as well as how these determinants change over time in each country. If

Japanese firms’ governance improves after the reforms, we expect to see improvements in

their management of cash in the 2000s, in which case the regressors should do a better job

of explaining cash (Dittmar et al., 2003). When we estimate the regressions for the full time

period we include dummies for 2001-2007 and 2008-2011 to see how cash holdings change

after 2000 after conditioning on firm characteristics (and separating the crisis period).

Second, we estimate cross-sectional regressions that pool US and Japanese firms

each year, and report the results in Table 2, Panel B. These regressions include a Japan

dummy to assess whether the cash holdings of Japanese companies differ from those of US

companies conditional on the other variables, and a dummy for Japanese keiretsu firms. We

25

also estimate these regressions using cash and marketable securities instead of cash as the

dependent variable (not reported in tables) and discuss those results when different.27

Table 2 Panel A reports the first set of regressions. For US firms, the adjusted R-

squareds are 32% for 1990-1999, 33% for 2000-2011, and 34% for the overall period.

Consistent with prior research, cash holdings are positively related to industry sigma, market-

to-book, and R&D intensity, and negatively related to size, dividend payment, leverage, net

working capital, capital expenditures, and cash flow. The significance and magnitude of

regression coefficients are mostly consistent across sub-periods. The time dummies are

insignificant for US firms, indicating that cash holdings for these firms do not change in the

2000s once we account for changes in firm characteristics (consistent with Bates et al., 2009).

When we estimate the US firm regressions using cash and marketable securities as the

dependent variable (not reported in tables), explanatory power increases, with R-squareds

close to 50%. Coefficients on key variables increase in absolute value. The fact that these

models work better for cash and marketable securities than cash suggests that US firms view

marketable securities as part of short-term liquidity and manage the sum of these amounts.28

The opposite is true for Japanese firms, as discussed next.

For Japanese firms the time dummies are reliably negative for both periods, with

coefficients of -3.4% for 2001-2007 and 2008-2011. This indicates that, on average,

Japanese firms reduce cash holdings after 2000 once we condition on firm characteristics,

consistent with governance reforms having some effect.

27 We estimate these regressions in a number of other ways as well, including requiring that firms have observations for all years in the relevant subperiod as well as requiring that they have observations for at least three years in the relevant subperiod. Results are not sensitive to these sampling requirements and are available upon request. We cluster standard errors by firm and year. 28 This is also consistent with how the financial press portrays the cash holdings of US firms. For example, the press refers to the more than $200 billion of cash and marketable securities on Apple’s balance sheet (including long-term marketable securities) simply as “cash.”

26

The model does not explain cash as well for Japanese firms in the 1990s. For 1990-

1999, the adjusted R-squared is 17%, about half that for US firms in the same period. The

industry sigma variable, which is important for US firms, does not load for Japanese firms.29

In the 2000s, the adjusted R-squared for Japanese firms nearly doubles, to 32%, essentially

the same as for US firms, with industry sigma strongly significant in the expected direction.

This shift suggests that Japanese firms manage cash in a more disciplined way (or at least

more like US firms) in the post reform period, consistent with improved governance.30

When we instead estimate these regressions using cash and marketable securities for

Japanese firms (not reported in tables), the R-squareds decline, opposite to what we observe

for US firms, to 23% (versus 29%) for the full period and to 10% (versus 16%) for the 1990s

and 27% (32%) for the 2000s. This suggests that cash is the more relevant variable for

Japanese firms.

Table 2, Panel B reports the annual cross-sectional regressions that include both US

and Japanese firms as well as intercept dummies for Japanese and Japanese keiretsu firms.

The idea is to compare the cash holdings of Japanese firms in general, as well as keiretsu firms

in particular, to those of US firms conditional on firm characteristics. For brevity we only

tabulate coefficients on the Japan and keiretsu intercept dummies along with number of

29 In addition, the coefficient on the dividend payer dummy is positive for Japanese firms in the 1990s (t = 4.5), opposite to the result for US firms, for which the coefficient is strongly and consistently negative. Because dividends paid by Japanese firms are typically much smaller than those of US firms (see next section), this suggests that while dividends help mitigate free cash flow problems in US firms, they do not do so for Japanese firms, instead serving a more perfunctory role. 30 To ensure these results are not due to underlying differences between US and Japanese firms, we also estimate these regressions for a sample of matched-pairs of US and Japanese firms. To implement this, in each year we match a Japanese firm with a US counterpart in the same industry, within 10% of size, and with the closest ROA. The overall results are similar to those reported: for US firms, the cash holdings regression R-squares are 35.2% and 29.8% in the 1990s and 2000s, respectively; for Japanese firms, the R-squares are 19.0% and 42.8%, respectively. Thus, results for the Japanese firms are more strongly consistent with relatively weak governance in the 1990s and improved governance in the 2000s.

27

observations and R-squareds.31

The coefficient on the Japan intercept is large and reliably positive in all years,

indicating that Japanese firms hold more cash than US firms after conditioning on firm

characteristics. The differences are large in the early 1990s, ranging from 17% to 20% of

assets over 1990-1994. The differences are less pronounced over 1995 to 2001 but remain in

the 10% to 14% range. The differences remain in the 12% to 15% range for the rest of the

sample period, indicating that Japanese firms consistently hold more cash than US firms

after conditioning on firm characteristics. The coefficient on the keiretsu dummy is reliably

negative in all years except 1998 and 1999, which indicates that these firms hold 2% to 3%

less cash than other Japanese firms over most of the period (Pinkowitz and Williamson,

2001, report a similar finding).

We have also estimated these regressions using cash and marketable securities as the

dependent variable (not reported in tables). 32 Because US firms have larger holdings of

marketable securities for most of the sample period (Table 1), differences are smaller but

remain significant: Japanese firms still hold more liquidity. A more appropriate specification

may be to use cash for Japanese firms and cash and marketable securities for US firms,

which biases against finding that Japanese firms hold more liquidity. The results from this

specification (not reported in tables) show that, conditional on firm characteristics, Japanese

firms still hold significantly more liquidity than US firms in all years except 1996, 1997, and

1999. The differences are around 12%-15% in the early 1990s and increase from 5% in 2000

31 Pinkowitz et al. (2016) use a similar approach to compare the cash holdings of US and non-US firms. In most cases, the sign and significance of the coefficients is consistent with that for the regressions reported in Panel A, although for those variables where there was some inconsistency between the results for the US and Japanese firms, the coefficients are less significant. 32 As another robustness analysis, we estimate these regressions using the matched pairs of US and Japanese firms described earlier. The results of this analysis show consistent results for the Japanese intercept dummy (which displays coefficient values very similar to those reported in Table 2) but smaller and less significant negative coefficients on the keiretsu intercept dummy.

28

and 2001 to 9% in 2007 and 13% in 2010 and 2011. Thus, the conclusion that Japanese

firms typically hold more cash than US firms is robust to the treatment of marketable

securities, and holds up even when we stack the deck by including marketable securities for

US but not Japanese firms. This finding is consistent with the evidence in Aoyagi and

Ganelli (2014), who also report that Japanese firms hold more cash than firms in other G7

countries.

4.2 Payout policy for Japanese firms

To analyze the payout policy of Japanese firms in a meaningful way it is necessary to

consider both dividends and repurchases. Restrictions on repurchases in Japan were

gradually lifted beginning in the mid-1990s, as discussed in more detail in Appendix B.

There is little systematic evidence on stock repurchases for Japanese firms.

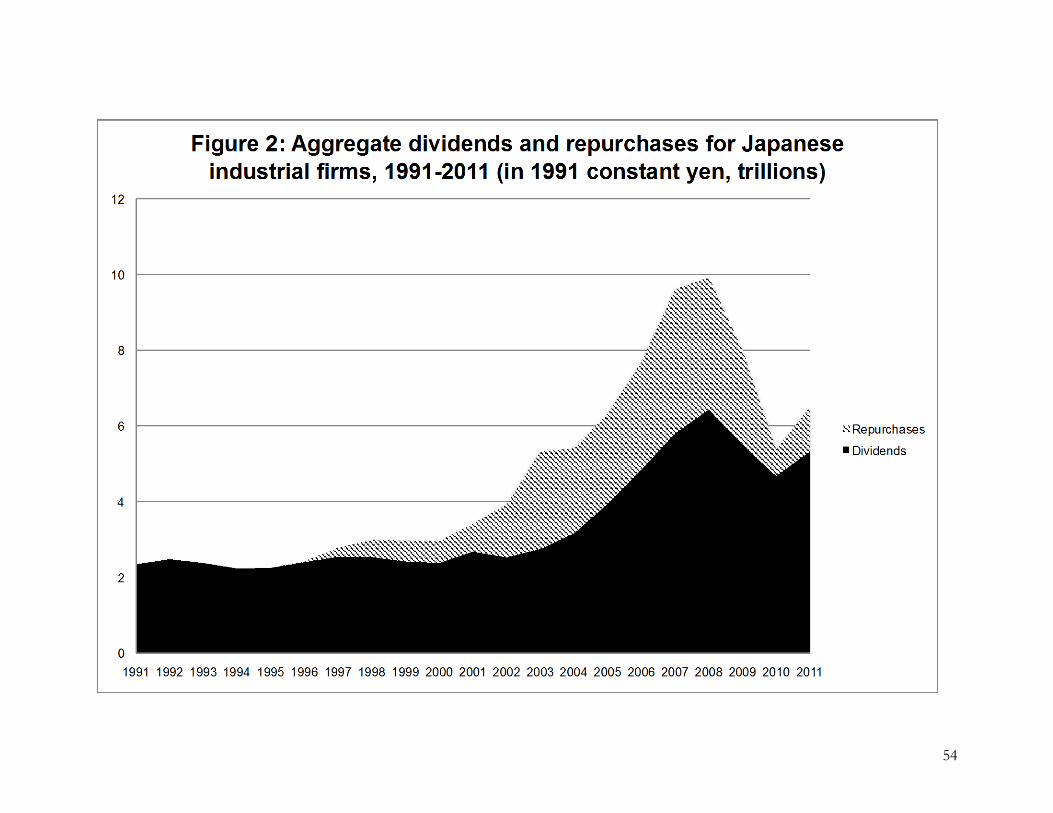

Figure 2 shows aggregate dividends and repurchases by Japanese firms, measured in

constant 1991 yen. Payouts are stagnant during the 1990s but increase strongly after 2000,

consistent with improved overall governance. Repurchases for Japanese firms begin at ¥33

billion in 1996 and grow quickly to ¥739 billion in 2001, ¥1.4 trillion in 2002, ¥2.6 trillion in

2003, and reach ¥3.8 trillion in 2007. Dividends are largely flat over 1991 to 2000, varying

between ¥2.2 trillion and ¥2.5 trillion with no obvious trend. However, over 2001 to 2008

they grow strongly, from ¥2.7 trillion to ¥6.4 trillion, before declining with the crisis. Total

payouts triple over this period, from ¥3.0 trillion in 2000 to ¥9.9 trillion in 2008, with

dividends accounting for 58% of the increase.

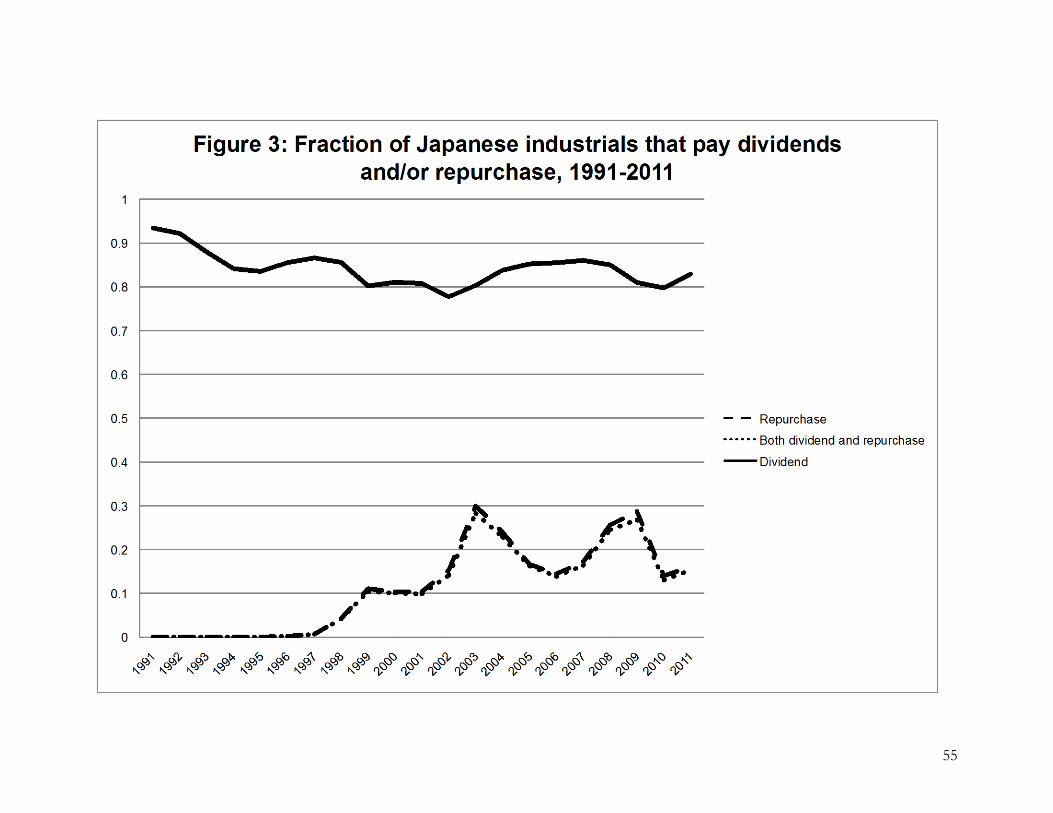

Figure 3 reports the fraction of Japanese firms that pay dividends, repurchase, and

that both pay dividends and repurchase by year. The fraction of dividend-payers is above

90% in 1991 but drifts downward over the 1990s, falling to just less than 80% by 2002.

After this, the fraction of dividend-payers fluctuates around 80%. This fraction is much

29

higher than in other major economies, including the US (Denis and Osobov, 2008; Floyd et

al., 2015). However, dividends paid by Japanese firms are smaller than those paid in other

countries. Our data (not reported) show that annual dividends for the median Japanese firm

represent about 0.6% of assets compared to 1.8% of assets for US firms (these amounts do

not vary greatly across the sample period).

Figure 3 also shows that the fraction of Japanese firms that repurchase increases

from close to 0 in 1997 to around 10% from 1999 to 2001 and then fluctuates between 14%

and 30% over 2002 to 2011. Few firms repurchase without also paying dividends. Similar to

the concentration in payouts in the US (DeAngelo et al., 2004), the growth in payouts

evident in Figure 2 is concentrated in firms that both pay dividends and repurchase, which

tend to be the largest firms.33 Overall, Figures 2 and 3 show that Japanese firms increased

payouts substantially during the 2000s, both through increases in dividends and through the

introduction of repurchases. This increase is mainly driven by larger firms, consistent with

the view that improved governance is not uniform.

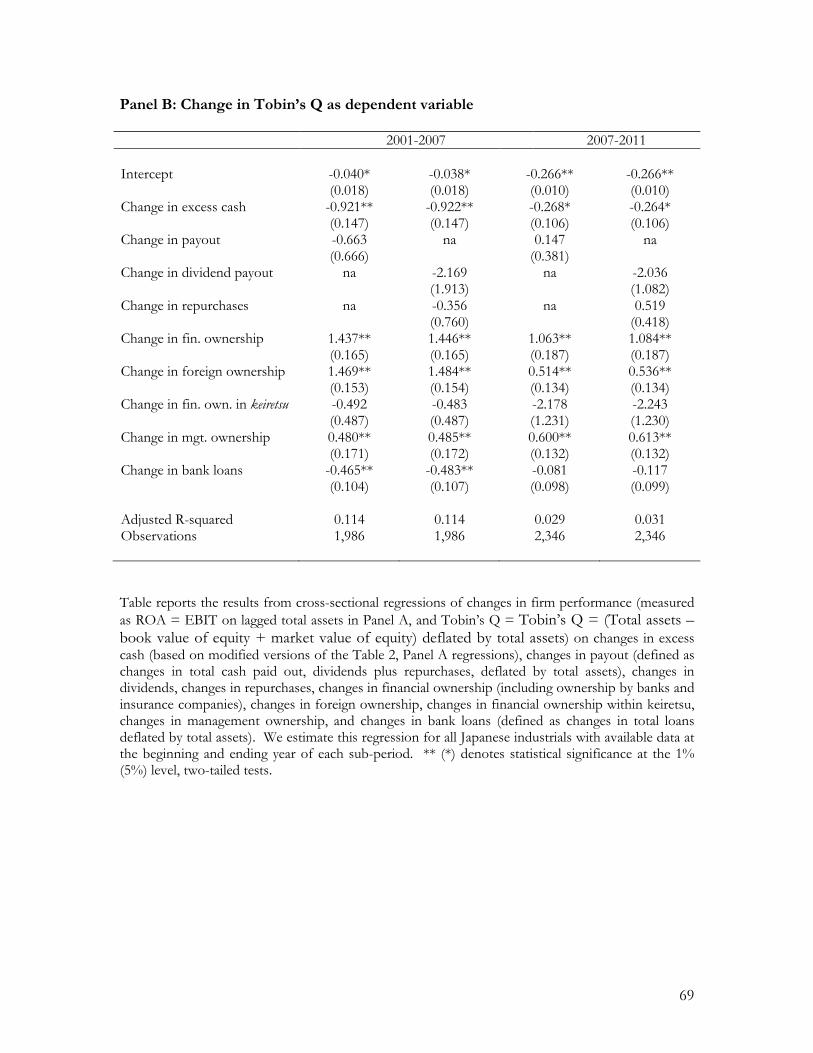

4.3 The relation between excess cash, payout policy, and firm performance

We next provide evidence on whether reductions in (excess) cash holdings translate

into improved performance. We first use the cash holdings regressions to sort sample firms

into excess cash deciles. To do this, we use the fitted residuals from the Table 2, Panel A

regressions, estimated separately for the 1990s and 2000s, to measure excess cash. We use

decile ranks based on this measure to investigate whether changes in excess cash are

associated with changes in firm performance, measured using both ROA and Tobin’s Q.34

33 Firms that both repurchase and pay dividends are larger than those that only pay dividends, which in turn are substantially larger than non-payers. These data not reported in tables. 34 To avoid the possibility of a mechanical relation between changes in excess cash and ROA we use total assets at the beginning of the period as the denominator for ROA, so it is not affected by changes in cash during the period. We also use return on equity (ROE) to measure performance, with similar results, as well as replicating

30

We predict that declines (increases) in excess cash are associated with improved (worsened)

performance in the post reform period.

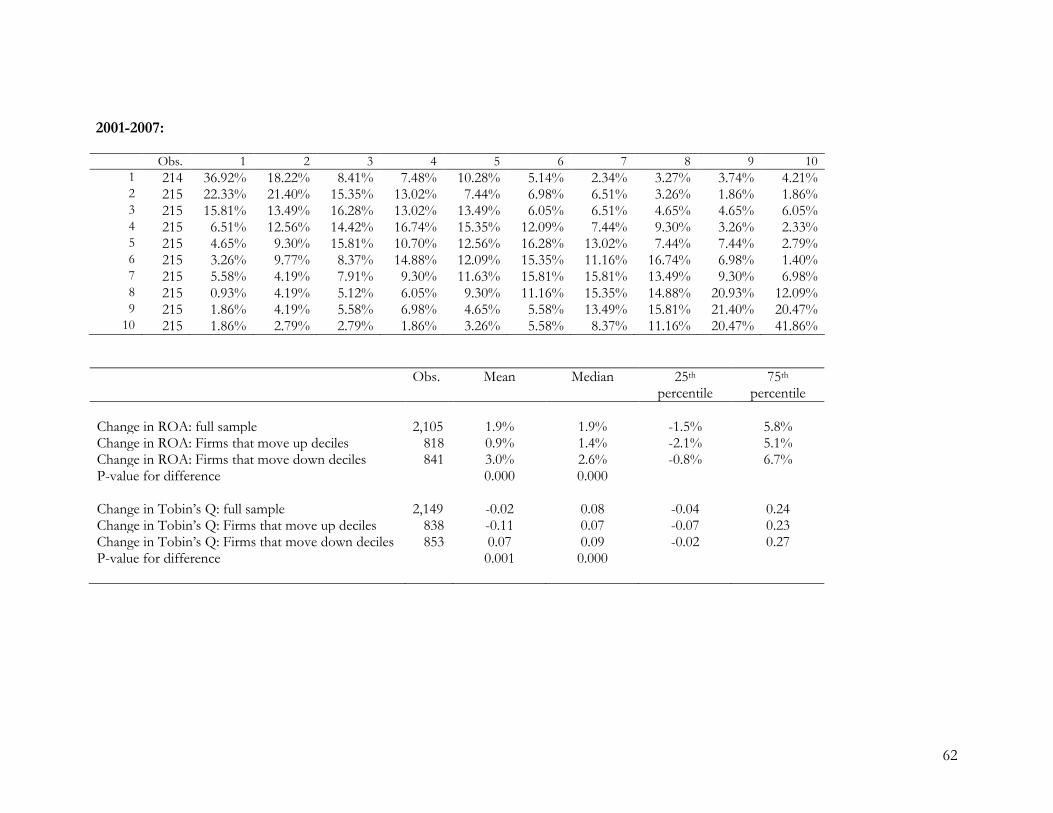

We report the results of this analysis in Table 3. We analyze transitions in excess

cash over three periods. For each period, we sort firms into excess cash deciles in the initial

year and then re-sort in the final year, and report transition matrices for 1994-2001, 2001-

2007, and 2007-2011. Although time period choices are inevitably arbitrary, we view 2001 as

representing the transition to the post-reform period of the 2000s (2001 also coincides with

the availability of data on the ownership structure of Japanese firms, which we utilize in the

next subsection). We expect our prediction—that changes in excess cash and performance

are inversely related—will hold in 2001-2007 (when the results of reform should be evident)

but not in 1994-2001 (the heart of the economic malaise). Because 2007-2011 is also a post-

reform period, there may be a negative relation in this period as well although the relation is

likely clouded by the effects of the global financial crisis.

Table 3 reports the transition matrices (the percentages are based on rows, and so

sum to 100 across rows). Each row comprises observations in a given excess cash decile for

the initial year, from 1 to 10, where 1 denotes the lowest excess cash decile and 10 the

highest excess cash decile. The columns comprise deciles defined in the same way for the

last year. Observations on the diagonal thus represent firms in the same excess cash decile

in the first and last years (no change). Observations above the diagonal represent firms for

which excess cash holdings increase in relative terms, so that firms move up deciles, and

all of the analysis in this sub-section using cash and marketable securities in place of cash, once again with similar results. In addition, as a robustness check we have estimated the cash holdings regressions used to generate the excess cash measure after excluding the cash flow and ROE which measure performance (this avoids any possible relationship between variables used to predict cash holdings and the outcome measure used in these tests).

31

conversely for observations below the diagonal. This analysis requires firms to have data in

the first and last years of each period and we lose observations accordingly.

If membership in excess cash deciles were independent over time, we would see 10%

in all cells. Instead, Table 3 shows clustering in cells on the diagonal and just off the

diagonal and particularly in the extremes, indicating that firms’ levels of excess cash holdings

are persistent over time, consistent with excess cash levels being a relatively “sticky”

characteristic that reflects firm governance.

The key test links changes in excess cash to changes in firm performance. For each

period, we divide firms into those for which excess cash worsens (improves), as indicated by

increases (decreases) in decile membership over the period. Table 3 reports the results of

this analysis—we compare the change in performance (ROA and Tobin’s Q) over each

transition period for firms with increases and decreases in excess cash.35

For 1994-2001, there is little evidence of a relation between changes in excess cash

holdings and firm performance. The mean (median) change in ROA is -0.6% (0.1%) for

firms with increases in excess cash and -0.9% (-0.7%) for firms with decreases in excess cash,

numbers that are not different at conventional significance levels. The mean (median)

change in Tobin’s Q is -0.17 (-0.18) for firms with increases in excess cash and -0.30 (-0.26)

for firms with decreases in excess cash; the differences in means is not statistically significant

while the difference in medians is significant, but in the wrong direction (firms with lower

excess cash experience a larger decrease in performance).

Consistent with our predictions, we find a negative relation between changes in

excess cash and performance over 2001-2007. For this period, there is an overall

improvement in performance, with a mean (median) increase in ROA of 1.9% (1.9%). For 35 The changes in ROA and Tobin’s Q exhibit correlations of 0.49, 0.36, and 0.29 for the three periods, respectively.

32

firms for which excess cash declines, the mean (median) change in ROA is 3.0% (2.6%),

compared to 0.9% (1.4%) for firms for which excess cash holdings increase, with differences

significant at better than 1%. The results for Tobin’s Q are similar: firms with lower excess

cash experience a mean (median) increase in Q of 0.07 (0.09) compared to changes in Q of -

0.11 (0.07) for firms with higher excess cash, differences that are also significant at 1%.

There is weaker evidence of a negative relation over 2007-2011, as expected. For the

sample as a whole, mean (median) ROA declines by -1.9% (-1.7%) due to the effects of the

global financial crisis. The mean (median) change in ROA is -2.0% (-1.7%) for firms with

increases in excess cash versus -1.2% (-1.2%) for firms with decreases in excess cash,

differences that are statistically significant in the predicted direction but only at the 10% level

(two-tailed).36 Results are stronger when we use Tobin’s Q. As for ROA, there is an overall

decline in Q. But this decline is smaller for firms that reduce excess cash (the mean and

median declines are -0.28 and -0.18, respectively) compared to those that increase excess

cash (the mean and median declines are -0.33 and -0.22); the mean difference is significant at

the 10% level while the median difference is significant at the 1% level.

Another way of assessing the relation between changes in excess cash and changes in

performance is to use continuous measures of both variables, and to include changes in

payouts in the analysis. To do this, for each period we regress changes in ROA (and Tobin’s

Q) on changes in excess cash and changes in payout, where the latter is measured as the

change in total cash payout (deflated by total assets) from the initial year to the final year.

This tests our prediction that declines in excess cash and increases in cash payouts are

associated with improved performance. Because dividends represent a stronger

36 When we replicate this analysis using cash and marketable securities rather than cash, the differences in changes in ROA are again highly significant for 2001-2007 and significant at the 5% level over 2007-2011. Results are generally slightly stronger if we use ROE in place of ROA.

33

commitment than repurchases (e.g., Brav et al., 2005; Grullon and Michaely, 2002; Skinner,

2008), we separate changes in dividends and repurchases.

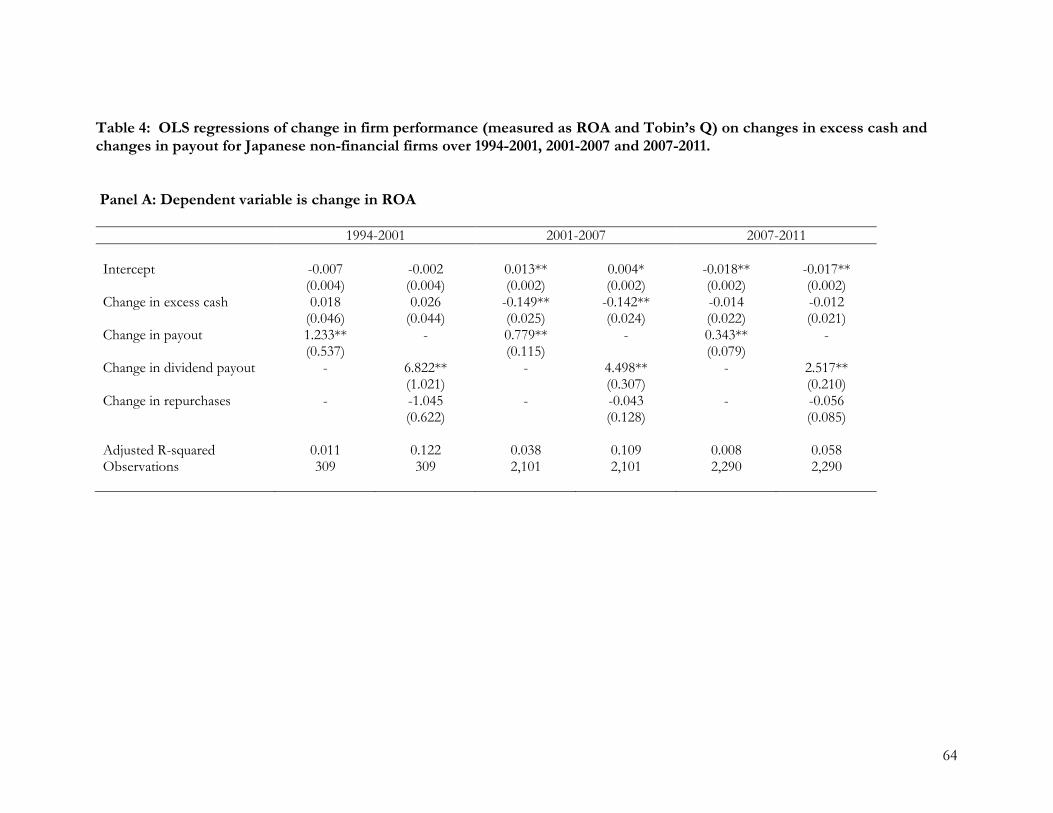

The results are in Table 4. For ROA in the first sub-period, the coefficient on the

change in excess cash is not significant, as expected in the absence of reform (and consistent

with the results in Table 3). The change in payout is positive and significant (1.23, t = 2.30),

which implies that higher profitability is associated with higher payouts. The overall R-

squared is 1.1%. When we separate payouts into dividends and repurchases, the coefficient

on dividends is large and highly significant (6.82, t = 6.68) while that on repurchases is not

significant; the R-squared increases to 12.2%. This tells us that, on average, managers of

Japanese firms increase dividends when earnings increase, as expected under conventional

models of dividend policy (e.g., Fama and Babiak, 1968).

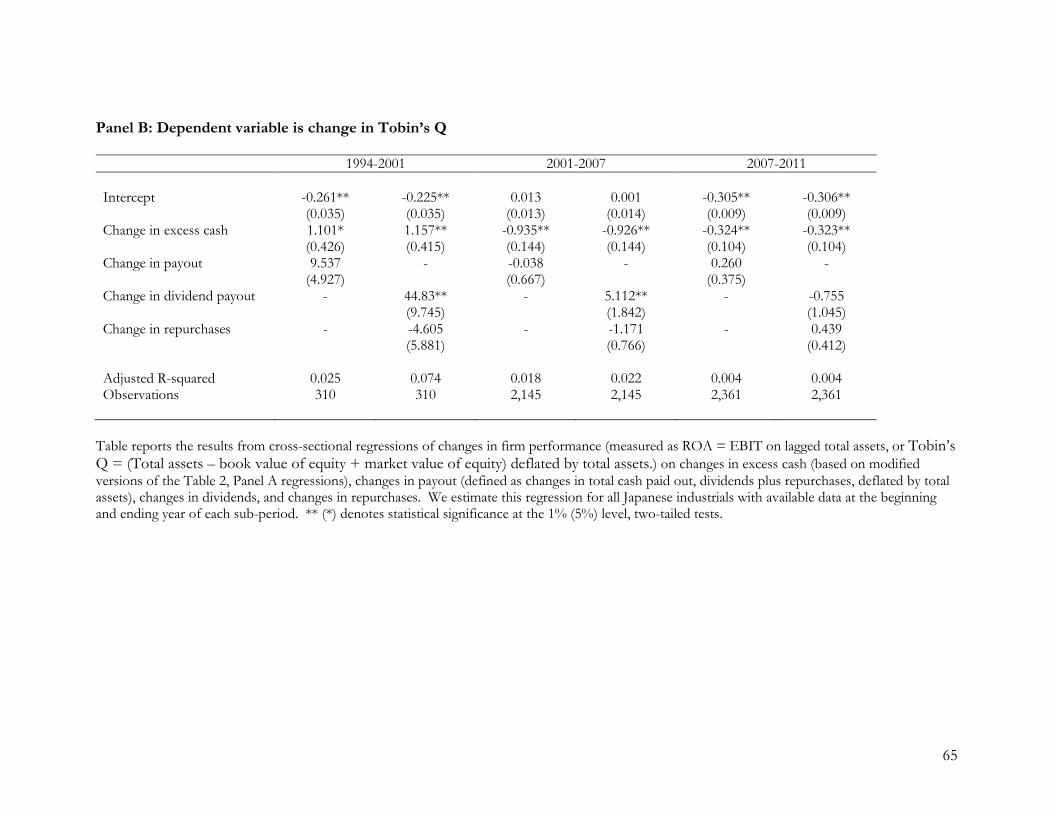

The results for Tobin’s Q in the first period indicate that changes in excess cash are

positively related to performance, with the coefficient on excess cash positive and strongly

significant. This is opposite to what we expect under the governance story but could reflect

the fact that better performing firms built cash reserves during this period. As with ROA,

the change in Q is positively related to dividends, suggesting again that better performance is

associated with increased dividends. The adjusted R squared is 7.4%.

The results for 2001 to 2007 are consistent with what we expect if the governance

reforms are effective for some firms over this period. For ROA in this period, the

coefficient on the change in excess cash is -0.15 (t = -5.86) while that on the change in

payouts is 0.78 (t = 6.75), indicating that improved performance is associated with lower

excess cash and increased payouts. The R-squared is 3.8%. The coefficient on excess cash

implies that a decline in excess cash of 2% of assets (close to the median) is associated with

an increase in profitability of around 30 basis points, which we view as a plausible

34

magnitude. When we separate payout into dividends and repurchases, the R-squared

increases to 10.9%. The coefficient on dividends of 4.50 (t = 14.6) implies a payout ratio of

0.22, while that on repurchases is again insignificant. The coefficient on excess cash remains

negative and highly significant, with a coefficient of -0.14 (t = -5.83).37

The results for Tobin’s Q over 2001 to 2007 also support our prediction that

changes in excess cash are negatively related to changes in performance. For both

specifications, the coefficient on the change in excess cash is negative and highly significant