exxonmobil “the outlook for energy a view to 2030”

TRANSCRIPT

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 1/42

Outlook for Energy

A View to 2030

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 2/42IFC1 exxonmobil.com

Table o Contents

Transition to modern energy/technology 2

Our key energy challenges 6

Growing global demand 13

Global transportation demand 15

A single-cell oil well? 16

Improving today’s vehicle 18

Thinking outside the tank 20

Global industrial demand 21

Managing emissions 22

Global energy demand and supply 25

The importance o natural gas 27

Options or carbon policy 31

CO2 emissions 32

Integrated energy solutions 34

Key indings 36

Glossary 37

This publication includes orward-looking statements. Actual uture

conditions (including economic conditions, energy demand, and

energy supply) could dier materially due to changes in technology,

the development o new supply sources, political events, demographic

changes, and other actors discussed herein (and in Item 1 o

ExxonMobil’s latest report on Form 10-K). This material is not to be

reproduced without the permission o Exxon Mobil Corporation.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 3/42The Outlook for Energy: A View to 2030 1

The Outlook or Energy:

A View to 2030

The Outlook for Energy: A View to 2030 1

In our Outlook or Energy – A View to 2030, we see many

hopeul things – economic recovery and growth, improved

living standards and a reduction in poverty, and promising

new energy technologies.

But we also see a tremendous challenge: how to meet the

world’s growing energy needs while also reducing the impact

o energy use on the environment.

As the Outlook shows, ExxonMobil expects that global energy

demand in 2030 will be almost 35 percent higher than in

2005, even accounting or the recession that dampened

energy demand in 2009. Other key ndings include:

• Growthwillbeledbyrapidexpansioninnon-OECD

countries such as China and India, where energy usage will

rise by about 65 percent.

• Demandwillbeparticularlyintenseforelectricpower

generation, which will comprise 40 percent o global energy

demand by 2030.

• Oilandnaturalgaswillremainessential,butothersources

including nuclear and renewables (e.g., wind, solar and

biouels) will play an expanded role.

The uture o energy is directly linked to the uture well-being

and prosperity o the world’s people.

Today, about 1.5 billion people – a quarter o the world’s

population – lack access to electricity. Even more lack modern

cooking and heating uels. Expanding access to energy – and

the opportunities it aords – should be a shared global goal.

Our energy and environmental challenges are intertwined and

their scale is enormous. Today, energy use per person around

the world varies dramatically but equates to an average o

200,000 British thermal units (BTUs) a day. Globally, that

translates to 15 billion BTUs every second.

ExxonMobil believes that meeting uture energy needs while

also reducing environmental risk will require an integrated set

o solutions that includes:

• Acceleratingenergyefciency,whichtempersdemandand

saves emissions

• Expandingall economic energy sources, including oil and

natural gas

• Mitigatingemissionsthroughtheuseofnewtechnologies

and cleaner-burning uels such as natural gas, nuclear and

other renewable sources.

This multidimensional approach will need trillions o dollars

in investment, and an unwavering commitment to innovation

and technology that evolves over years and decades. It will

require sound, stable government policies that enable access

to resources and encourage long-term investments and

technological development. And it will require the global

energy industry to operate on a scale even larger than today.

Updated each year, The Outlook or Energy is a comprehensive

look at long-term trends in energy demand, supply, emissions

and technology. The report is built upon detailed analysis o

data rom about 100 countries, incorporating publicly available

inormation as well as in-house expertise.

ExxonMobil uses the Outlook to guide its long-term investment

decisions. We share it publicly to encourage a better

understanding o our company, our industry and the global

energy challenges that we all have a vested interest in meeting.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 4/42

Transition to modern energy/technology

2 exxonmobil.com

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 5/42The Outlook for Energy: A View to 2030 3

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 6/42

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 7/42

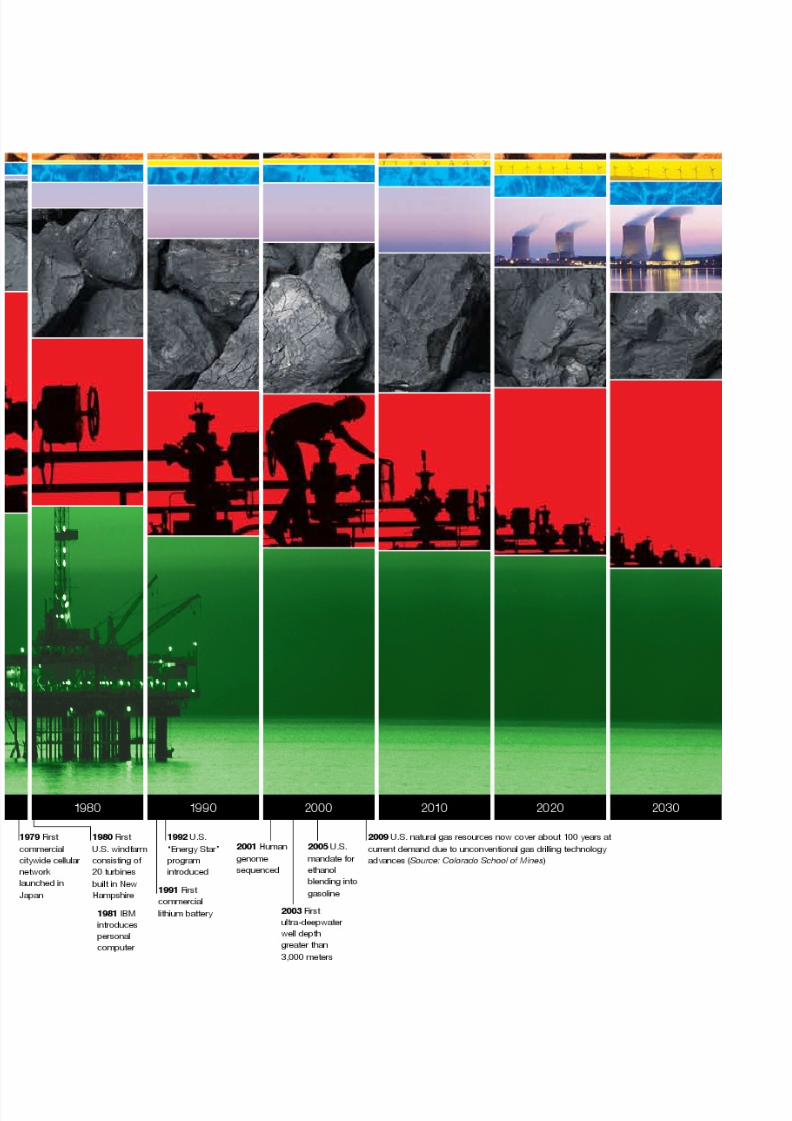

Energy sources and technology evolve

over time – and each infuences the

other. By understanding the history o

energy and technology, we can betterunderstand the uture course o the

energy challenge.

As an example, the history o energy

use in the United States over the last

150 years illustrates the way energy use

and technologies develop over time.

In the United States in 1850, wood

was the biggest energy source. But by

1900, coal had become predominant. Technology played a role in this trend, as

mining evolved and coal ed the newly

industrialized nation. America’s access to

energy enabled its growth as an industrial

economy; in turn, industrial growth and

the wealth it created expanded U.S.

energy demand. It is important to note

that it took about 40 years or coal to

achieve its substantial share.

By 1950, oil was overtaking coal, asmore Americans owned cars and rail

transport shited rom coal to diesel.

The growth o cars and trucks, as

well as the birth o the commercial

airline industry, meant a new need or

transportation uels. Improvements in

oil-exploration technologies helped keep

pace with this growing uel demand.

Also by 1950, hydroelectric power came

into use. And natural gas, considerednearly worthless a generation earlier, grew

as a uel to meet the growing heating and

industrial needs o an increasingly wealthy

nation. Coal remained signicant and

helped meet growing electricity demand.

From 1950 to 2000, we saw the

introduction and growth o nuclear energy

and the rst meaningul appearance o

modern renewable uels. Natural gas also

continued to grow and was now ueling

power generators as well.

Looking out to 2030, we see gradual

shits in energy and technology

continuing. Both the U.S. and world

energy mix continue to grow morediverse, which strengthens energy

security by reducing the risk rom

disruption to any single supply source.

We will need to expand all these

sources – and develop new ones –

to meet uture demand. New energy

technologies will open up new energy

sources, and new end-use technologies

will reshape demand patterns, just

as they have or the last 150 years. It

is important to remember, however,that these shits happen slowly, over

the course o decades. Free markets,

open trade, and stable legal, regulatory

and tax rameworks will acilitate these

positive transormations.

Change in energy use and technology

development is an evolutionary

process, but one that oten has

revolutionary impacts.

Evolution o energy and technology

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 8/42The Outlook for Energy: A View to 2030 4

Importance o energy

Beore considering the many energy demand, supply and

emissions trends that consti tute the world’s energy outlook

through 2030, it is worth refecting on the importance o

energy to all aspects o our lives.

Fundamentally, the energy outlook is about people – bil lions

o people and their amilies using energy to improve their

daily lives.

At a national and international level, it is the lieblood

o modern economies. For developed nations, reliable

energy uels the technologies and services that enrich and

extend lie. Energy powers advanced computers, improved

transportation, expanded communications, cutting-edge

medical equipment and procedures, and much more.

For developing nations, expanding reliable and aordable

supplies o energy supports and even accelerates changes

that improve and save lives. Reliable energy means

expanded industry, modern agriculture, increased trade

and improved transportation. These are building blocks

o economic growth that create the jobs that help people

escape poverty and create better lives or their children.

For these reasons and more, energy issues are vitally

important and demand our understanding.

4 exxonmobil.com

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 9/42

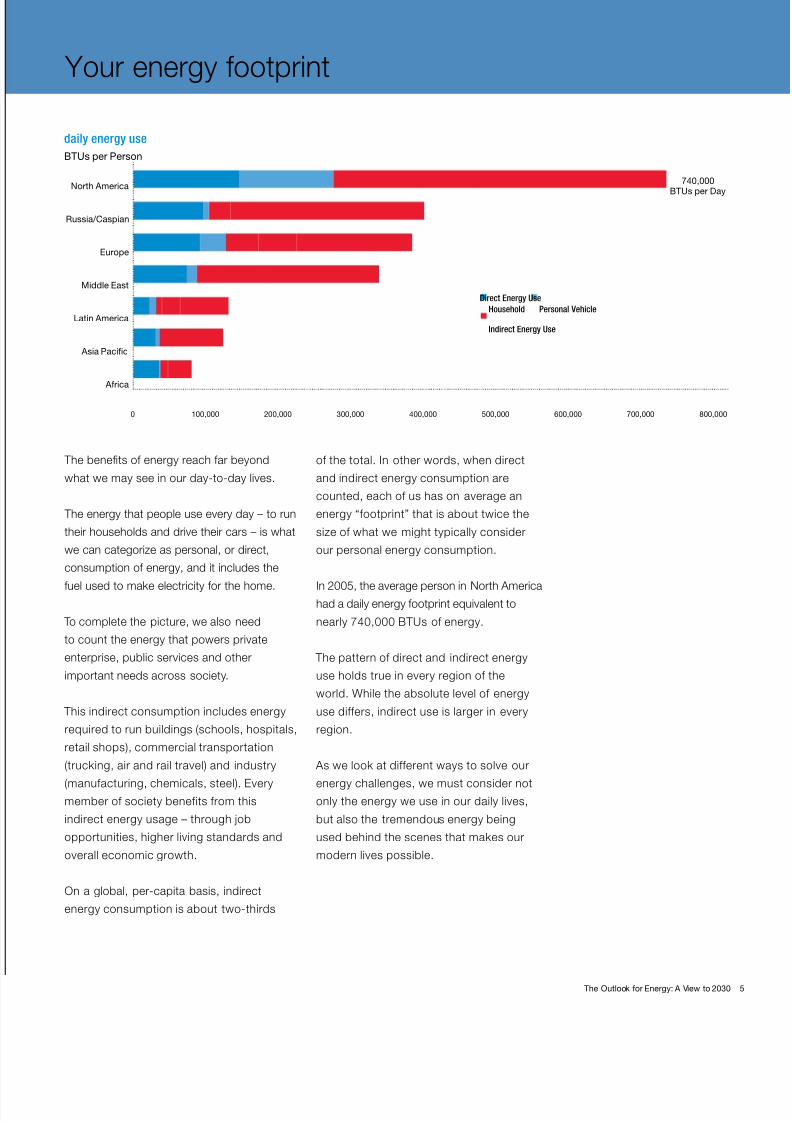

The benets o energy reach ar beyond

what we may see in our day-to-day lives.

The energy that people use every day – to run

their households and drive their cars – is what

we can categorize as personal, or direct,

consumption o energy, and it includes the

uel used to make electricity or the home.

To complete the picture, we also need

to count the energy that powers private

enterprise, public services and other

important needs across society.

This indirect consumption includes energy

required to run buildings (schools, hospitals,

retail shops), commercial transportation

(trucking, air and rail travel) and industry

(manuacturing, chemicals, steel). Everymember o society beneits rom this

indirect energy usage – through job

opportunities, higher living standards and

overall economic growth.

On a global, per-capita basis, indirect

energy consumption is about two-thirds

o the total. In other words, when direct

and indirect energy consumption are

counted, each o us has on average an

energy “ootprint” that is about twice the

size o what we might typically consider

our personal energy consumption.

In 2005, the average person in North Americahad a daily energy ootprint equivalent to

nearly 740,000 BTUs o energy.

The pattern o direct and indirect energy

use holds true in every region o the

world. While the absolute level o energy

use diers, indirect use is larger in every

region.

As we look at dierent ways to solve our

energy challenges, we must consider notonly the energy we use in our daily lives,

but also the tremendous energy being

used behind the scenes that makes our

modern lives possible.

Your energy ootprint

North America

Latin America

Europe

Middle East

Asia Pacific

Africa

Russia/Caspian

740,000

BTUs per Day

Direct Energy Use

Household

Indirect Energy Use

Personal Vehicle

daily energy use

BTUs per Person

200,000 300,000 500,000 600,000 700,000400,000 800,0000 100,000

The Outlook for Energy: A View to 2030

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 10/426 exxonmobil.com

As we survey the global energy landscape to

2030, we see several interlocking challenges.

One o the biggest jobs through 2030 will be

to reduce poverty and raise living standards

around the world. An important actor in

achieving this goal will be to continue meeting

the world’s energy needs saely, reliably andaordably, even as population and economic

growth – particularly in developing countries –

pushes global demand higher by almost 35

percent compared to 2005.

By providing reliable and aordable energy,

we will also help revitalize economies and

enable broad economic gains around the

world. Meeting this demand will not be

easy, especially considering that the world’s

energy resources are increasingly ound indicult or hard-to-reach places. And it will

require the global energy industry to operate

on a scale even larger than it does today.

At the same time, because we want to

ensure that today’s progress does not come

at the expense o uture generations, we

need to manage the risks to our climate

and environment. That includes taking

meaningul steps to curb carbon dioxide

(CO2) emissions, while at the same time

utilizing local resources to help maintain

secure supplies.

We can meet these interlockingchallenges. To do it, we will need an

integrated set o solutions that includes

expanding all economic energy sources,

improving efciency and mitigating

emissions through the use o cleaner-

burning uels such as natural gas.

These solutions must be supported

by trillions o dollars in new energy

investment, a long-term ocus and constant

technological innovation.

ExxonMobil is committed to pursuing each

o these integrated solutions.

Our key energy challenges

Globally, about 2.5 billion people rely

on traditional uels such as wood and

dung or heating and cooking.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 11/42

Over the past 150 years, the evolution o

modern energy and technology has enabled

people in developed countries to achieve

a liestyle in which access to energy – at

home, at work and on the road – is largely

taken or granted. In many o these places,

the challenge today is largely one o securing

enough reliable, aordable energy tocontinue meeting these existing needs.

But in some parts o the world, the challenge

is ar more basic. Today, globally, about

1.5 billion people lack access to electricity.

Even more live without modern uels or

cooking and heating. Instead, these

2.5 billion people – nearly 40 percent o the

world’s population – rely on burning wood,

dung or other traditional biomass uels,which can be dangerous to people’s health

and harmul to ai r quality.

Gaining access to energy represents

hope and opportunity. It means improved

transportation, increased commerce,

expanded industry and greater access to

health care and other social services – all o

which create jobs that help people escape

poverty. For nations with widespread

poverty, aordable and reliable energy also

is vital to building homes, schools, hospitals

and sanitation systems that can improve

and save lives.

As we consider the energy outlook to 2030,

it is important to keep in mind this “energygap,” and energy’s potential to lit lives and

improve communities in developed and

developing nations alike.

Challenge: meeting basic needsGlobally,

about

1.5billion people

lack access

to electricity.

A satellite image o the Earth

at night shows electricity

usage by region.

Photo courtesy o NASA

electricity modern cooking and heating fuels

Available Available

About1.5 Billion Peoplewith No Electricity

About2.5 Billion Peoplewith No Modern

Cooking or Heating Fuels

The Outlook for Energy: A View to 2030 7

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 12/428 exxonmobil.com

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 13/42The Outlook for Energy: A View to 2030 9

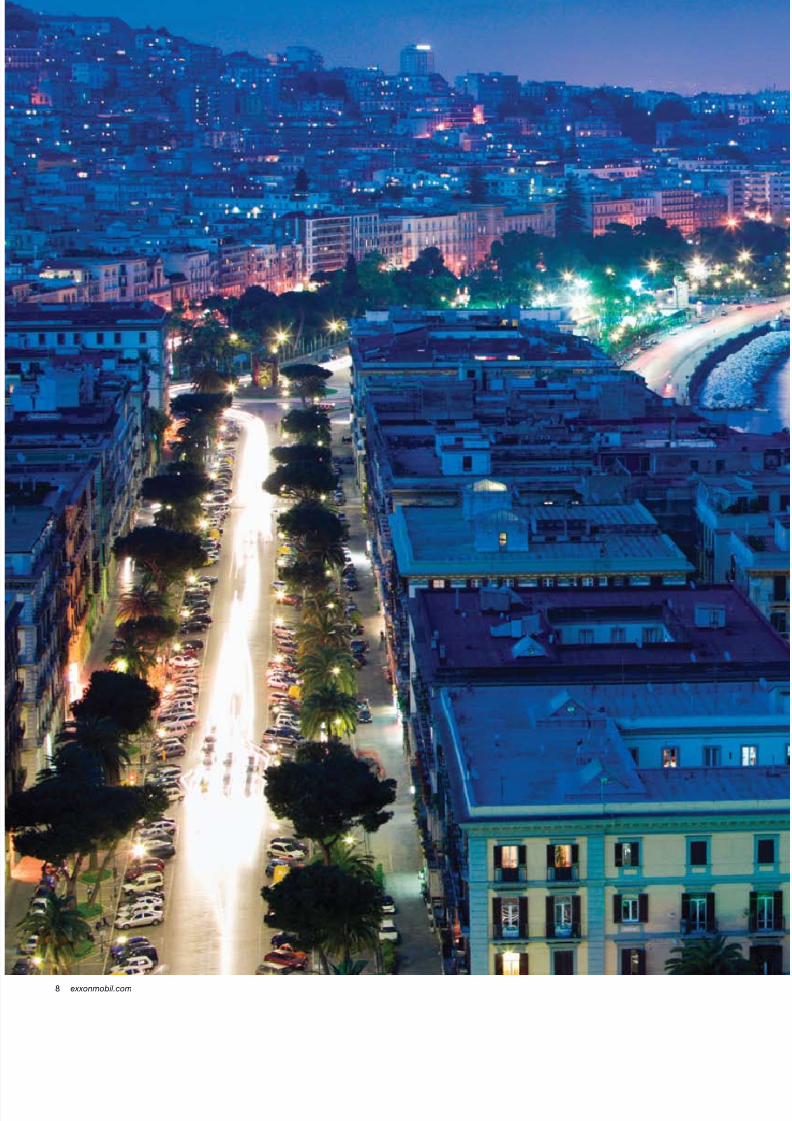

On average, a city o 1 million peoplein the OECD:

Needs 6 million BTUs of energy every second

Consumes over 1,000 gallons of oil per minute

Uses 150 tons of coal each hour

Requires two world-scale power plants

Drives 500,000 cars that use over 500,000

gallons of petroleum every day

Naples, Italy, population 1,004,500

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 14/4210 exxonmobil.com

When ExxonMobil prepares its Outlook or

Energy each year, we start with the world’s

economic outlook, because economic

activity – along with population growth – is

a undamental driver o energy demand.

The economic trend, globally, is the same,

and it’s encouraging.

While the recession is expected to produce a

2percentcontractioninglobalGDPin2009,

economic growth will return, and return

to a pre-recession rate. In act, rom 2005

through2030,weseeglobalGDPexpanding

at an average annual rate o 2.7 percent.

At the same time, the world’s population

is expected to rise rom 6.7 billion today to

almost 8 billion. As we noted earlier, risingpopulations not only create new demands or

energy or personal needs such as uels or

cars and electricity or homes, but also energy

that is consumed “indirectly” – the energy that

serves the broader society and economy.

Together, population and economic growth

through 2030 will continue to drive global

energy demand higher.

ExxonMobil expects that global energy

demand will rise by an average annual

rate o 1.2 percent a year through 2030,

when the world will be using almost 35

percent more energy than it did in 2005.

The composition o the world’s energy will

continue to evolve through 2030, as we

will discuss later in the Outlook .

It’s important to note that while economic

growth drives energy demand, bec aus e

o expected gains in energy eciency, our

projected rate o energy-demand growth

(1.2 percent) is less than hal the rate

ofglobalGDPgrowth(2.7percent)

through 2030.

Energy demand to grow signicantly

In the United States and other OECD

countries, energy demand will be

essentially at and CO 2 emissions

will decline through 2030 even as

economies and populations grow.

Energy efciency will play a key role.

1980 20302005

0.9% Average Growth per Year

2005 – 2030

1980 20302005

2.7% Average Growth per Year

2005 – 2030

1980 20302005

1.2% Average Growth per Year

2005 – 2030

Quadrillion BTUs

700

600

500

400

300

200

100

0

energy demand

Trillions in 2005 Dollars

100

80

60

40

20

0

GDP

Billions

10

8

6

4

2

0

population

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 15/42The Outlook for Energy: A View to 2030 11

Economic growth drives energy demand

The world uses 15 billion BTUs

o energy every second. As more

countries move up the economic

ladder, more energy will be required.

GDP

1980 20302005

Trillions in 2005 Dollars

OECD

OECD

Non-OECD

Non-OECD

60

50

40

30

20

10

0

energy demand

1980 20302005

Quadrillion BTUs

400

300

200

100

0

Global

energy demand

will be almost

35%higher in 2030

than it was

in 2005.

While global energy demand is expected

to rise by almost 35 percent through 2030,

to ully understand the energy outlook in

coming decades, we need to examine what’s

going on in developed Organization or

EconomicCo-operationandDevelopment

(OECD)countries(liketheUnitedStatesand

Europeannations)andnon-OECDnations(such as China and India), because the trends

in these two groups can be starkly dierent.

Through2030,theeconomiesofnon-OECD

countries, while still relatively smaller, will grow

atamuchfasterratethanthoseoftheOECD.

By 2030, these developing economies will

havereachedcloseto60percentofOECD

economic output.

Innon-OECDcountries,rapideconomicgrowth is expected to produce a steep climb

in energy demand. In act, we expect

that between 2005 and 2030, non-OECD

energy demand will grow by about

65 percent. However, even with this rapid

growth, per-capita energy demand in non-

OECDcountriesstillwillbemuchsmaller

thaninOECDcountries.

By contrast, in OECD countries, energy

demand is expected to actually be

slightly lower in 2030 versus 2005, even

though their economies will be more

than 50 percent larger on average.

How is this possible? The main reason is

eciency. ExxonMobil continues to projectsubstantialimprovementsinefciencyinOECD

countries.Innon-OECDcountries,wealsosee

efciencyimproving,butfastergrowthinGDP

and personal incomes will continue to drive

demand higher there.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 16/4212 exxonmobil.com

Our world continues to become more energy

eicient. From 1980 to 2000, the energy it

tooktoproduceoneunitofGDPfellbyan

average 1.2 percent a year. This occurred

or a number o reasons, including the use

o new, energy-saving technologies.

We expect eiciency gains to acceleratebetween 2005 and 2030 versus historical

trends,withenergy-per-GDPfallingatan

average global rate o 1.5 percent a year.

This aster pace will be driven by higher energy

costs, government mandates and regulations,

technology advances and expected CO2

emissionscostsinOECDcountries.

Improving eiciency at this rate will save a

signiicant amount o energy.

Through 2030, ExxonMobil expects global

energy demand to grow by an average

1.2 percent. To see how energy eiciency

works to curb energy-demand growth,

imagine i the world’s economies grew as

projected through 2030, but eiciency

was held lat at 2005 levels. In that case,

global energy demand in 2030 would not

be almost 35 percent higher than in 2005,

as we currently project; it would be about

95percenthigher.Putanotherway,gains

in energy eciency through 2030 will curb

energy-demand growth through 2030 by

about 65 percent.

In this respect, the greatest source o energy

in the uture is nding ways to use energy

more eciently.

Eciency: reducing demand growth

energy per GDP

energy demand

1980 2030

Millions of BTUs per Thousand of Dollars

of Gross Domestic Product (2005 Dollars)Quadrillion BTUs

1.2% Average Growth per Year

2005 – 2030

1.2% Average Efficiency Gain

per Year1980 – 2000

1.5% Average Efficiency Gain

per Year2005 – 2030

15

10

5

01980 2030

1000

600

500

400

300

800

700

900

200

100

02005

What demand would bewithout efficiency gains

Constant 2005 Level

2005

~300Quads

Through 2030, the amount o

energy saved through improved

efciency will be greater than the

energy consumed rom any single

supply source.

Taking sensible steps to improve

energy efciency is a “triple win” –

it saves money, reduces energy

demand and curbs CO 2 emissions.

Gains in energy

eciency through

2030 will

reduce globalenergy-demand

growth by

approximately

65%

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 17/42The Outlook for Energy: A View to 2030 13

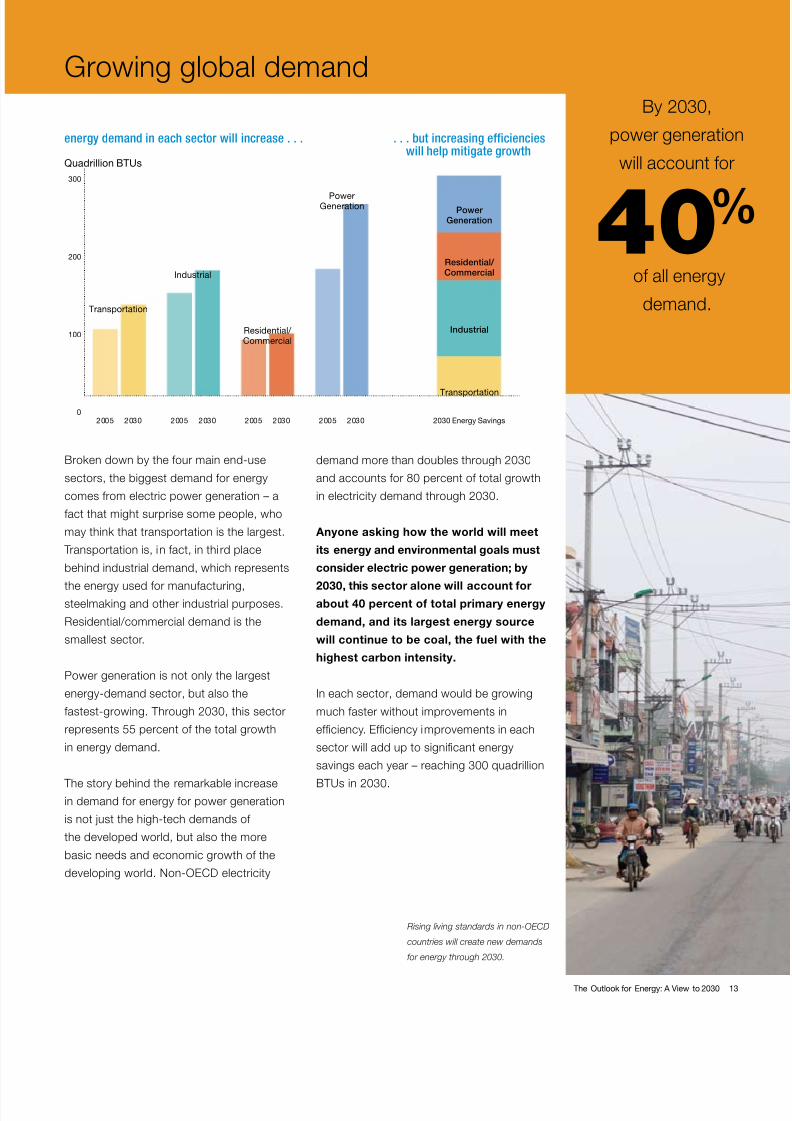

Broken down by the our main end-use

sectors, the biggest demand or energy

comes rom electric power generation – a

act that might surprise some people, who

may think that transportation is the largest.

Transportation is, in act, in thi rd place

behind industrial demand, which represents

the energy used or manuacturing,steelmaking and other industrial purposes.

Residential/commercial demand is the

smallest sector.

Powergenerationisnotonlythelargest

energy-demand sector, but also the

astest-growing. Through 2030, this sector

represents 55 percent o the total growth

in energy demand.

The story behind the remarkable increasein demand or energy or power generation

is not just the high-tech demands o

the developed world, but also the more

basic needs and economic growth o the

developingworld.Non-OECDelectricity

demand more than doubles through 2030

and accounts or 80 percent o total growth

in electricity demand through 2030.

Anyone asking how the world will meet

its energy and environmental goals must

consider electric power generation; by

2030, this sector alone will account orabout 40 percent o total primary energy

demand, and its largest energy source

will continue to be coal, the uel with the

highest carbon intensity.

In each sector, demand would be growing

much aster without improvements in

eciency. Eciency improvements in each

sector will add up to signicant energy

savings each year – reaching 300 quadrillion

BTUs in 2030.

Growing global demand

2005 2030

Transportation

2005 2030

PowerGeneration

2005 2030

Residential/ Commercial

2005 2030

Industrial

2030 Energy Savings

Quadrillion BTUs

energy demand in each sector will increase . . . . . . but increasing efficiencieswill help mitigate growth

300

200

100

0

Transportation

Power

Generation

Residential/

Commercial

Industrial

Rising living standards in non-OECD

countries will create new demands

or energy through 2030.

By 2030,

power generation

will account or

40%o all energy

demand.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 18/4214 exxonmobil.com

In the residential/commercial sector –

the energy we use in our homes and

businesses – residential demand dominates,

at about three times bigger than commercial.

This trend continues as demand in this

sector grows through 2030.

Residential energy demand is tied closelyto the total number o households in the

world. Through 2030, we see the number o

households rising by 900 million, with nearly

90 percent o that growth occurring

innon-OECDcountries.

OECDcountriestodayusesubstantially

moreenergyperhouseholdthannon-OECD

countries. While that remains true in 2030,

all around the world, households are growing

more ecient in their use o energy. Through2030, the steepest decline in energy-per-

householdwillcomefromOECDcountries,

with more modest rates o improvement in

non-OECDnations.

A diverse mix o energy is used to meet

residential/commercial demand. Natural

gas and electricity account or most o the

growth in this sector through 2030. But

biomass – uels like wood and dung – will

retain a substantial share o supply, mainly in

thenon-OECD.

Note: In each sector, we have included

“electricity” in the breakdown o demand by

uel. Electricity, o course, is not a uel in itsel –

it must be generated by other energy sources such as coal and natural gas. But it is important

to recognize the share o total electricity that is

consumed by each end-use sector.

Residential/commercial demand

2005 2030 2005 20302005 2030 2005 2030

by sector

Residential

Non-OECD

OECD

Commercial

Quadrillion BTUs

120

100

80

60

40

20

0

residential

1980 20302005

Billion Households

3.0

2.5

0

2.0

1.5

0.5

1.0

residential energy use

Non-OECD

OECD

Millions of BTUs per Household

80

70

60

50

40

30

20

10

0

There will be 900 million more households

in the world by 2030 – and they will need

energy or heating, cooking and appliances.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 19/42The Outlook for Energy: A View to 2030 15

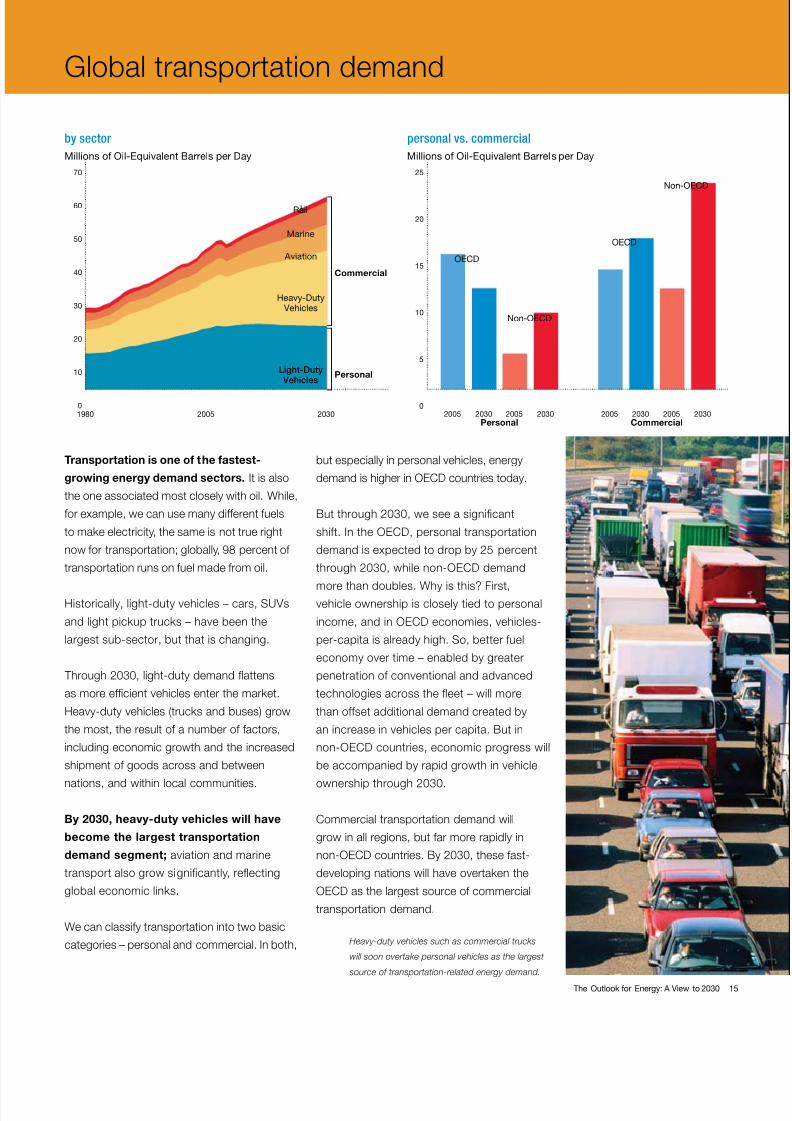

Transportation is one o the astest-

growing energy demand sectors. It is also

the one associated most closely with oil. While,

or example, we can use many dierent uels

to make electricity, the same is not true right

now or transportation; globally, 98 percent o

transportation runs on uel made rom oil.

Historically, light-duty vehicles – cars, SUVs

and light pickup trucks – have been the

largest sub-sector, but that is changing.

Through 2030, light-duty demand fattens

as more ecient vehicles enter the market.

Heavy-duty vehicles (trucks and buses) grow

the most, the result o a number o actors,

including economic growth and the increased

shipment o goods across and between

nations, and within local communities.

By 2030, heavy-duty vehicles will have

become the largest transportation

demand segment; aviation and marine

transport also grow signicantly, refecting

global economic links.

We can classiy transportation into two basic

categories – personal and commercial. In both,

but especially in personal vehicles, energy

demandishigherinOECDcountriestoday.

But through 2030, we see a signicant

shift.IntheOECD,personaltransportation

demand is expected to drop by 25 percent

through2030,whilenon-OECDdemand

more than doubles. Why is this? First,vehicle ownership is closely tied to personal

income,andinOECDeconomies,vehicles-

per-capita is already high. So, better uel

economy over time – enabled by greater

penetration o conventional and advanced

technologies across the feet – will more

than oset additional demand created by

an increase in vehicles per capita. But in

non-OECDcountries,economicprogresswill

be accompanied by rapid growth in vehicle

ownership through 2030.

Commercial transportation demand will

grow in all regions, but ar more rapidly in

non-OECDcountries.By2030,thesefast-

developing nations will have overtaken the

OECDasthelargestsourceofcommercial

transportation demand.

Global transportation demand

2005 20052030 2030 2005 2030 2005 2030Personal Commercial

PersonalLight-Duty Vehicles

Heavy-Duty Vehicles

Aviation

Marine

Rail

Commercial

OECD

Non-OECD

OECD

Non-OECD

by sector

personal vs. commercial

1980 2030

Millions of Oil-Equivalent Barrels per Day Millions of Oil-Equivalent Barrels per Day

70

60

50

40

30

20

10

0

25

20

15

10

5

02005

Heavy-duty vehicles such as commercial trucks

will soon overtake personal vehicles as the largest

source o transportation-related energy demand.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 20/4216 exxonmobil.com

ExxonMobil believes that biouels rom photosynthetic

algae could someday play an important role in meeting the

world’s growing need or transportation uels, while also

reducing CO2 emissions.

In July 2009, we announced a signicant new project to research

and develop algae biouels. Our partner is Synthetic Genomics

Inc (SGI), a Caliornia-based biotech rm ounded by genome

researchpioneerDr.J.CraigVenter.Thegoaloftheprogram:to

produce a commercially scalable, renewable algae-based

uel compatible with today’s gasoline, diesel and jet uel.

• Why algae? Scientists already know that certain algae

naturally produce oils similar to the petroleum products we

use today. I commercial quantities o these algae-based oils

could be developed, they could avoid the need to build the

extensive new delivery inrastructure that some other alternative

transportation uels might require.

• Algae-based biouels have potential environmental

advantages. Through photosynthesis, algae absorb CO2 –

the main greenhouse gas – and convert it to useul products,

like oils and oxygen. As a result, uels made rom algae could

reduce greenhouse gas emissions.

• Algae-based biouels likely would not impact the global

ood supply. While biouels made rom plants l ike corn and

sugar cane are an expanding energy source, they require

ertile land and resh water; algae can be grown using land

and water unsuitable or plant or ood production. Algae also

could yield between three and eight times more biouel per

acre compared to other biouel sources.

Getting these algae uels rom the lab to broad, commercial

scale at the local gas station will be a tremendous

undertaking – and could require decades o work.

It is an exciting project that brings together SGI’s expertise in

genomics, synthetic biology, microbiology and biochemistry;

and ExxonMobil’s expertise in transportation uels and the

development o technologies and systems needed to increase

scale rom concept phase to large-scale manuacturing.

ExxonMobil expects to spend more than $600 million on

this project i research and development milestones are met.

ExxonMobil’s investment in algae-based uels is just one part

o our commitment to the breakthrough technologies and

integrated solutions that will be needed to address rising

demand or transportation uels and other long-term challenges

illustrated in our Outlook or Energy .

A single-cell

oil well?

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 21/42The Outlook for Energy: A View to 2030 17

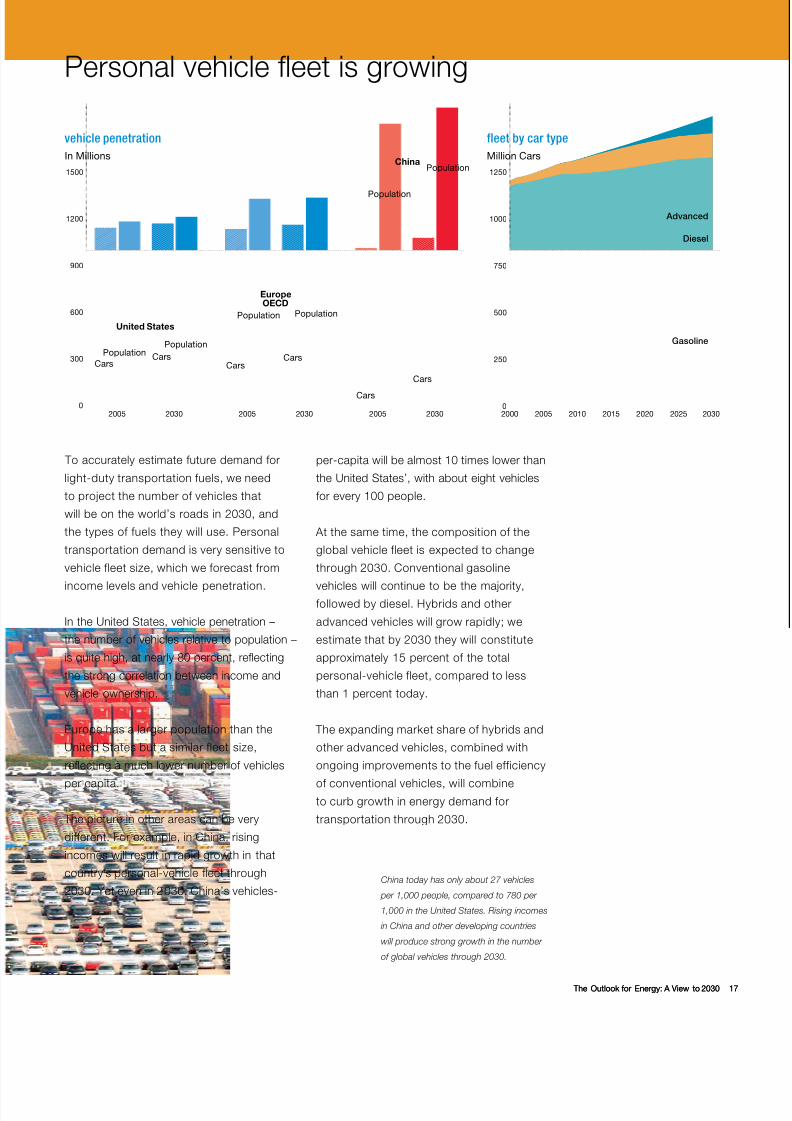

To accurately estimate uture demand or

light-duty transportation uels, we need

to project the number o vehicles that

will be on the world’s roads in 2030, and

thetypesoffuelstheywilluse.Personal

transportation demand is very sensitive to

vehicle leet size, which we orecast rom

income levels and vehicle penetration.

In the United States, vehicle penetration –

the number o vehicles relative to population –

is quite high, at nearly 80 percent, refecting

the strong correlation between income and

vehicle ownership.

Europe has a larger population than the

United States but a similar leet size,

refecting a much lower number o vehicles

per capita.

The picture in other areas can be very

dierent. For example, in China, rising

incomes will result in rapid growth in that

country’s personal-vehicle feet through

2030. Yet even in 2030, China’s vehicles-

per-capita will be almost 10 times lower than

the United States’, with about eight vehicles

or every 100 people.

At the same time, the composition o the

global vehicle leet is expected to change

through 2030. Conventional gasoline

vehicles will continue to be the majority,ollowed by diesel. Hybrids and other

advanced vehicles will grow rapidly; we

estimate that by 2030 they will constitute

approximately 15 percent o the total

personal-vehicle leet, compared to less

than 1 percent today.

The expanding market share o hybrids and

other advanced vehicles, combined with

ongoing improvements to the uel eiciency

o conventional vehicles, will combineto curb growth in energy demand or

transportation through 2030.

Personalvehicleeetisgrowing

2005 2030

United States

CarsCars

PopulationPopulation

2005 2030

CarsCars

Population Population

EuropeOECD

2005 2030

Cars

Cars

Population

vehicle penetration

In Millions

1500

1200

900

600

300

0

fleet by car type

Million Cars

Gasoline

Diesel

Advanced

1250

1000

750

500

250

02000 20302015 2020 20252005 2010

PopulationChina

China today has only about 27 vehicles

per 1,000 people, compared to 780 per

1,000 in the United States. Rising incomes

in China and other developing countries

will produce strong growth in the number

o global vehicles through 2030.

The Outlook for Energy: A View to 2030 17

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 22/4218 exxonmobil.com

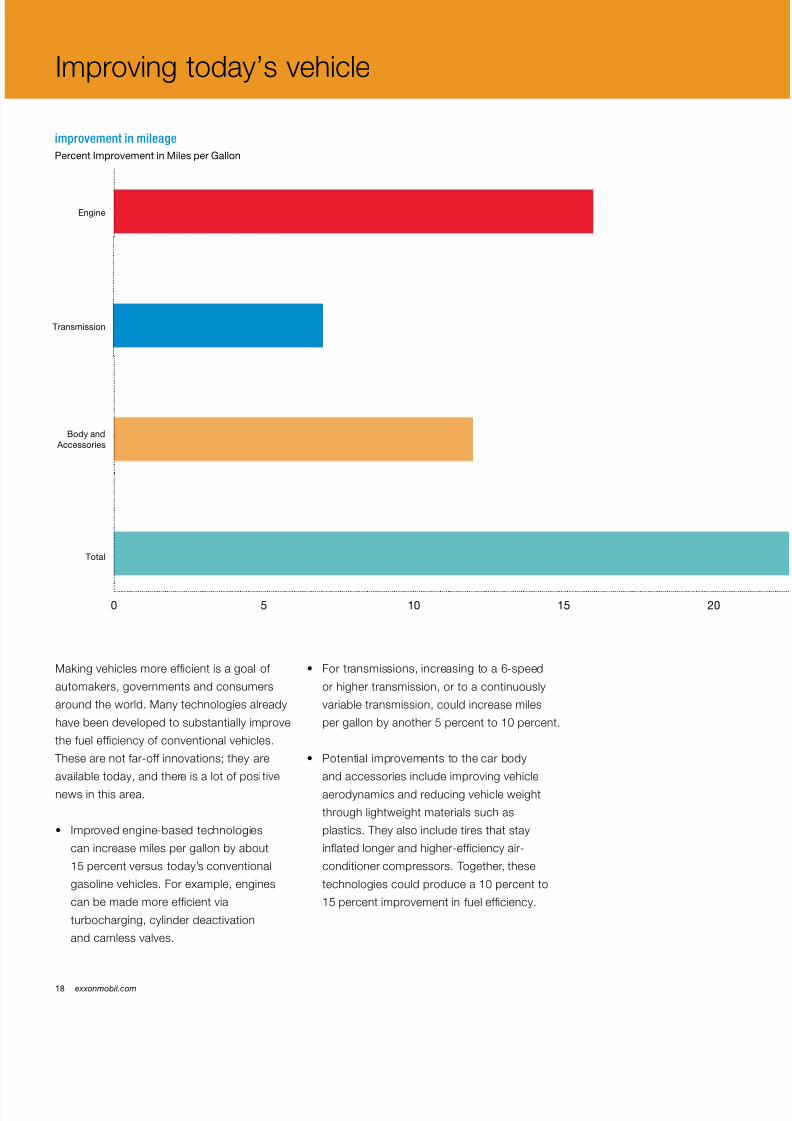

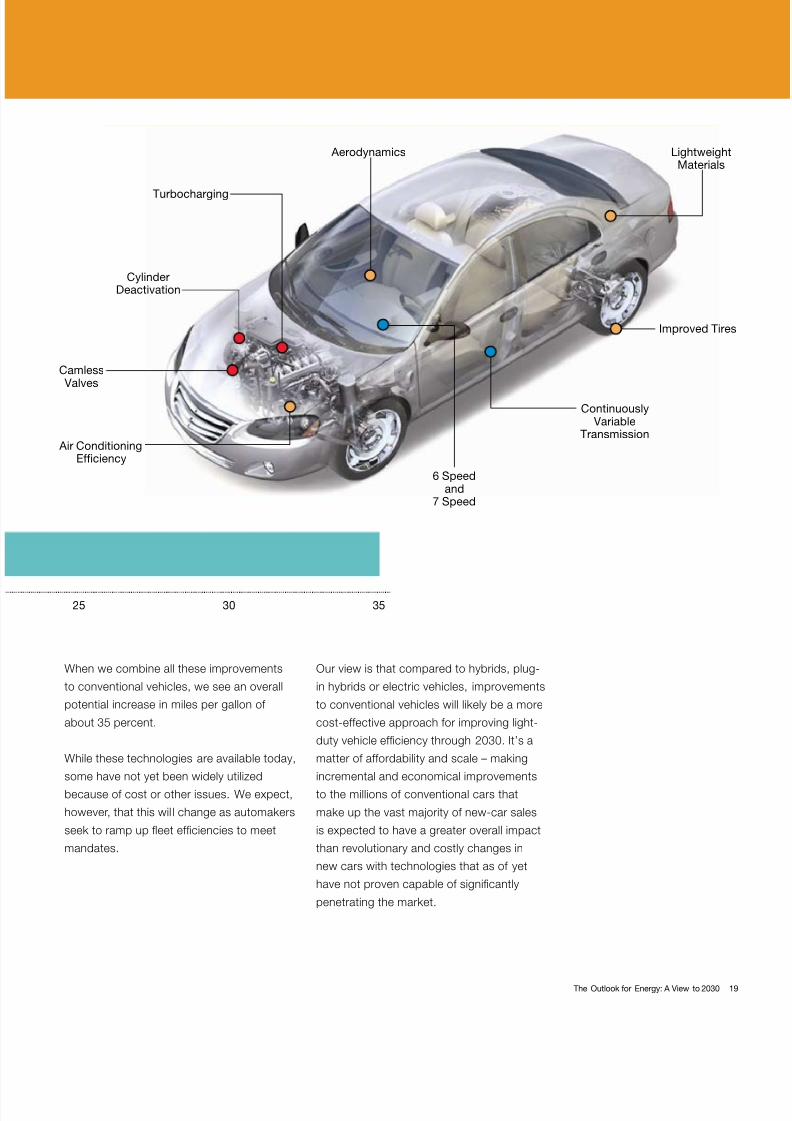

Making vehicles more ecient is a goal o

automakers, governments and consumers

around the world. Many technologies already

have been developed to substantially improve

the uel eciency o conventional vehicles.

These are not ar-o innovations; they are

available today, and there is a lot o posi tive

news in this area.

• Improvedengine-basedtechnologies

can increase miles per gallon by about

15 percent versus today’s conventional

gasoline vehicles. For example, engines

can be made more ecient via

turbocharging, cylinder deactivation

and camless valves.

• Fortransmissions,increasingtoa6-speed

or higher transmission, or to a continuously

variable transmission, could increase miles

per gallon by another 5 percent to 10 percent.

• Potentialimprovementstothecarbody

and accessories include improving vehicle

aerodynamics and reducing vehicle weight

through lightweight materials such as

plastics. They also include tires that stay

infated longer and higher-eciency air-

conditioner compressors. Together, these

technologies could produce a 10 percent to

15 percent improvement in uel eciency.

Improving today’s vehicle

0 10 20155

improvement in mileage

Engine

Transmission

Body and

Accessories

Total

Percent Improvement in Miles per Gallon

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 23/42The Outlook for Energy: A View to 2030 19

When we combine all these improvements

to conventional vehicles, we see an overall

potential increase in miles per gallon o

about 35 percent.

While these technologies are available today,

some have not yet been widely utilized

because o cost or other issues. We expect,

however, that this wil l change as automakers

seek to ramp up feet eciencies to meet

mandates.

Our view is that compared to hybrids, plug-

in hybrids or electric vehicles, improvements

to conventional vehicles will likely be a more

cost-eective approach or improving light-

duty vehicle eciency through 2030. It’s a

matter o aordability and scale – making

incremental and economical improvements

to the millions o conventional cars that

make up the vast majority o new-car sales

is expected to have a greater overall impact

than revolutionary and costly changes in

new cars with technologies that as o yet

have not proven capable o signicantly

penetrating the market.

3025 35

Aerodynamics

Turbocharging

LightweightMaterials

CylinderDeactivation

Camless Valves

Air ConditioningEfficiency

6 Speedand

7 Speed

Continuously Variable

Transmission

Improved Tires

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 24/4220 exxonmobil.com

ExxonMobil’s interest in cars and trucks goes ar beyond the

uel tank. Using our expertise not only in uels and lubricants,

but also in chemicals and plastics, we are advancing new

technologies to make vehicles more uel efcient.

Conventional vehicle eciency improvements will be a key in

reducing the demand or personal transportation uel demand

intheOECDby2030.

Some o our technologies are already on the road. For example:

• Workingwithmajortiremanufacturers,ExxonMobil

developed a new tire-lining technology that uses up to 80

percent less material in the manuacturing process, making tires

lighter and keeping them properly infated. A car with under-

infated tires burns up to an extra tank o gasoline every year.

• ExxonMobilhasdevelopedlightweight plastics or car

parts such as bumpers and uel tanks. Lighter vehicles use

less uel; or every 10 percent drop in vehicle weight, uel

economy improves by 7 percent. ExxonMobil is a leading

supplier o polyoleinic polymers used in the manuacture o

plastic car parts.

• WeintroducedMobil 1 Advanced Fuel Economy, a

lower-viscosity synthetic motor oil. Lower viscosity means less

energy is required to circulate the oil in the engine. Mobil AFE

can improve uel economy by up to 2 percent versus motor oils

most commonly used.

These ExxonMobil technologies may not get much notice rom

drivers, but they can add up to signifcant uel savings. For

example, i all vehicle tires on the road in the United States retained

air pressure as well as tires made with our new technology, it

would save more than 700 million gallons o uel annually.

By enabling cars and trucks to travel arther on a gallon o uel,

drivers not only spend less money per mile, they also emit

less CO2 per mile.

Reducing emissions associated with transportation is one o the

key long-term challenges outlined in The Outlook or Energy . In

the United States, transportation accounted or 33 percent o all

energy-related CO2 emissions in 2008, second only to electric

powergeneration,accordingtotheDepartmentofEnergy.

In addition to technologies available today, ExxonMobil

also is researching advanced engine technologies that

could make the internal-combustion engine more ecient,

and developing innovations that could advance hybrid and

hydrogen-powered vehicles.

Thinking outside

the tank

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 25/42The Outlook for Energy: A View to 2030 21

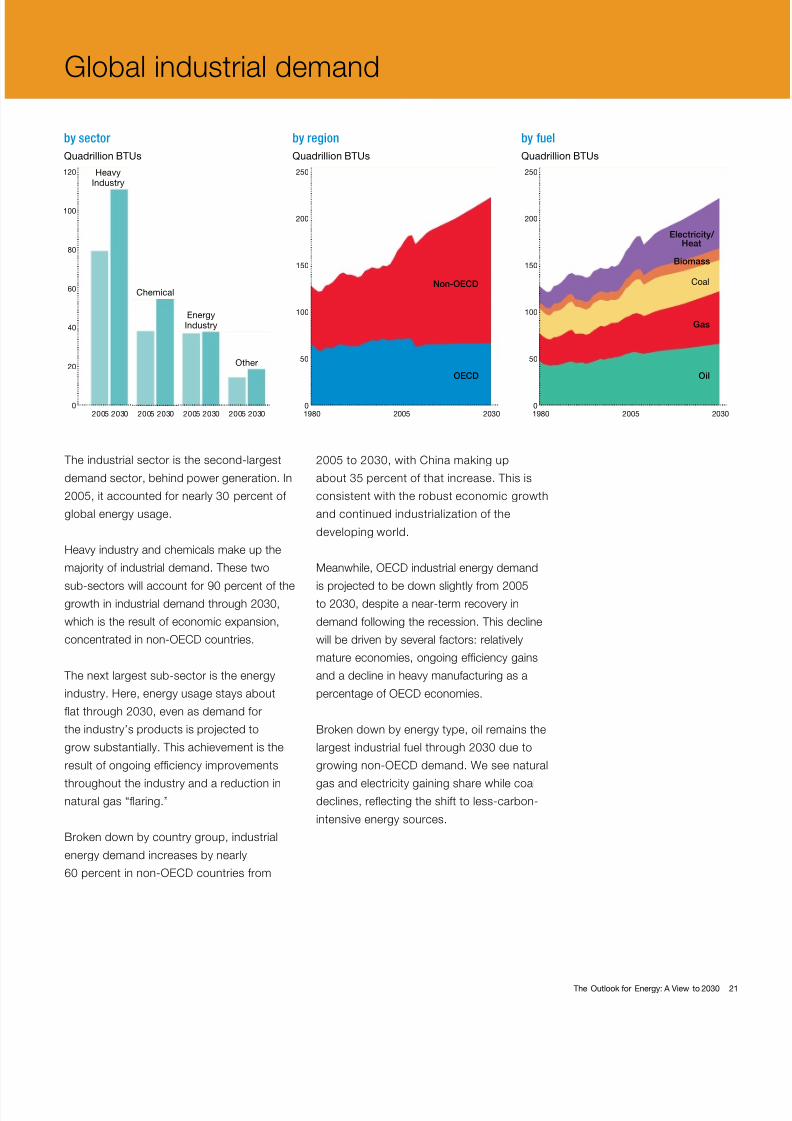

The industrial sector is the second-largest

demand sector, behind power generation. In

2005, it accounted or nearly 30 percent o

global energy usage.

Heavy industry and chemicals make up the

majority o industrial demand. These two

sub-sectors will account or 90 percent o thegrowth in industrial demand through 2030,

which is the result o economic expansion,

concentratedinnon-OECDcountries.

The next largest sub-sector is the energy

industry. Here, energy usage stays about

fat through 2030, even as demand or

the industry’s products is projected to

grow substantially. This achievement is the

result o ongoing eciency improvements

throughout the industry and a reduction innatural gas “faring.”

Broken down by country group, industrial

energy demand increases by nearly

60percentinnon-OECDcountriesfrom

2005 to 2030, with China making up

about 35 percent o that increase. This is

consistent with the robust economic growth

and continued industrialization o the

developing world.

Meanwhile,OECDindustrialenergydemand

is projected to be down slightly rom 2005to 2030, despite a near-term recovery in

demand ollowing the recession. This decline

will be driven by several actors: relatively

mature economies, ongoing eciency gains

and a decline in heavy manuacturing as a

percentageofOECDeconomies.

Broken down by energy type, oil remains the

largest industrial uel through 2030 due to

growingnon-OECDdemand.Weseenatural

gas and electricity gaining share while coaldeclines, refecting the shit to less-carbon-

intensive energy sources.

Global industrial demand

2005 2030

HeavyIndustry

2005 2030

Chemical

2005 2030

EnergyIndustry

2005 2030

Other

by sector

Quadrillion BTUs

120

100

80

60

40

20

0

Oil

Gas

Coal

Biomass

Electricity/ Heat

by fuel

Quadrillion BTUs

250

200

150

100

50

01980 20302005

OECD

Non-OECD

by region

Quadrillion BTUs

250

200

150

100

50

01980 20302005

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 26/4222 exxonmobil.com

ExxonMobil is successully reducing emissions rom its

own operations. In 2008, we achieved a global reduction o

10 million metric tonnes o greenhouse gas emissions – about

a 7 percent decline rom 2007.

We reduce emissions by increasing eciency in our day-to-

day operations, using new energy eciency technologies and

reducing faring.

• Efciency. Since the launch o our Global Energy

Management System in 2000, ExxonMobil has identied

opportunities to improve eciency by 15 percent to 20 percent at

our reneries and chemical plants. We have already implemented

about 60 percent o these. Over the past several years, eciency

at our rening and chemicals operations has improved at a rate

two to three times aster than the industry average.

• Cogeneration. ExxonMobil continues to expand its use o

cogeneration – a process in which we produce electricity to

power our operations while also capturing heat to make steam

needed to transorm raw materials into consumer products.

ExxonMobil is an industry leader in this highly ecient orm

o energy production, with interest in about 100 cogeneration

acilities in more than 30 locations worldwide. In 2008, we

added 125 megawatts o power capacity, with the startup

o new acilities at our renery in Antwerp, Belgium. With

new acilities under construction, we expect to increase our

cogeneration capacity to more than 5 gigawatts by 2011.

• Flare Reduction. Across our operations, we are working

to reduce laring o gas that has no economic outlet as

well as gas that is lared as a result o maintenance or

unexpected operating events. In 2008, we reduced upstream

laring by about 30 percent, and we plan urther reductions

o more than 20 percent over the next several years

compared to 2008 levels.

Since 2004, we have invested more than $1.5 billion in

activities to increase eciency and reduce emissions. We plan

to spend at least $500 million more over the next ew years.

ExxonMobil believes that energy eciency is the most powerul

tool or meeting the central challenge outlined in The Outlook

or Energy : how to meet rising demand or energy while also

reducing the impact o energy use on the environment.

In addition to improving eciency and reducing emissions

at our own operations, ExxonMobil also is developing

technologies to help consumers do the same. This is

important because while about 10 percent o petroleum-

related greenhouse gas emissions are rom industry

operations, 90 percent are rom consumer use o petroleum.

Managing

emissions

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 27/42The Outlook for Energy: A View to 2030 23

Growing demand or electricity, and the uels

used or power generation, is a major trend

o the last 25 years, and will remain so or the

next 25 years as living standards continue

to improve worldwide and more people gain

access to electricity.

Powergenerationisthelargestenergy-demandsector and the astest-growing – rising at an

average o approximately 1.7 percent a year –

and will account or about 40 percent o all

energy demand, up rom 36 percent in 2005

and 26 percent in 1980. This will support

strong increases in global electricity demand,

which will be about our times higher than 1980.

Electricity demand rises at a much aster rate

innon-OECDcountries,reectingtheirfaster

economic growth and relatively low electricitypenetration to date.

What uels will be used to generate this

electricity? Through 2030, there is a shit

away rom coal toward natural gas, as well

as to nuclear and renewable uels. This will

be driven by environmental policies, including

ones that seek to reduce emissions by

putting a cost on carbon emissions.

By 2030, we expect that 40 percent o the

world’s electricity will be generated by

nuclear and renewable uels.

Projectingthefuturemixoffuelsforpowergeneration is a complex task with many

variables. As part o this process, we must

consider how these uels will compete

economically, because these are the real-lie

actors that utilities and power generators

look at when considering which uels to use

or what types o new power plants to build.

Electricity use is growing rapidly

by sector

Residential

Commercial

HeavyIndustry

OtherIndustry

Transportation

Thousands of Terrawatt Hours

30

25

20

15

10

5

01980 20302005

40%

by generation

Thousands of Terrawatt Hours

1980 20302005

30

25

20

15

10

5

0

Renewables

Nuclear

Oil

Coal

Gas

Thousands of Terrawatt Hours

30

25

20

15

10

5

0

by region

1980 20302005

United States

Europe

Asia Pacific

OECD

China

Other Asia Pacific

Other

Non-OECDOther

By 2030, about 40 percent o the

world’s electricity will be generated

by nuclear and renewable uels.

The Outlook for Energy: A View to 2030 23

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 28/4224 exxonmobil.com

In the United States, absent any policies

that impose a cost on CO2 emissions, we

would expect coal and natural gas to be the

lowest-cost options or uture, new-build

power plants.

But policies that impose a cost on carbon

would sway these economics. Coal, beingthe most carbon-intensive uel, would

increase in price more than natural gas.

At $30 per ton o CO2, natural gas would

become the most economic alternative or

new-build power plants. This is where we

expect CO2 costs may evolve over the

next 10 years.

As the CO2 price increases, we would expect

to see uel switching rom coal to natural

gas. This will happen by running existingnatural gas plants at higher load actors, as

well as by building new natural gas plants

and retiring old coal plants.

At $60 per ton, natural gas is still very

competitive. In addition, nuclear and wind are

now competitive, which is why we include

strong growth or both in our Outlook .

Carbon capture and storage (CCS), a

process in which CO2 emissions are

captured beore they can enter the

atmosphere, holds promise in the uture.

However, even with CO2 emissions priced

at $60 per ton, new-build plants with CCS

remain challenged and very expensive –

meaning a less aordable source o electricity or consumers. This high cost,

combined with the need to build a regulatory

ramework or CO2 storage, presents

signicant challenges or its use over the

next two decades beyond government-

subsidized demonstration projects.

Likewise, solar energy aces signiicant

hurdles to becoming economically

competitive in this time rame. The cost o

capturing solar energy in photovoltaic cells orconcentrators remains generally unaordable

or large, commercial applications.

Electricity generation cost

Baseload plants are electric power plants that run continuously to meet minimum electricity demand requirements, while peaking power plantsrun intermittently to meet seasonal and daily peak electricity demand.

* Wind and solar exclude additional costs for intermittency and transmission investments ** With carbon capture and storage technology

U.S. baseload plants, startup 2025

Coal Gas Nuclear Wind* Coal/ CCS**

Gas/ CCS**

Solar*

No CO2

Cost

Coal Gas Nuclear Wind* Coal/ CCS**

Gas/ CCS**

Solar*

At $30 per Ton

Coal Gas Nuclear Wind* Coal/ CCS**

Gas/ CCS**

Solar*

At $60 per Ton

Cost per Kilowatt Hour in 2009 Cents

20

15

10

5

0

20

15

10

5

0

20

15

10

5

0

Climate policies that put a “cost”

on CO 2 emissions will shit the

economics o uels used or power

generation. Natural gas, nuclear

and wind stand to beneft.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 29/42The Outlook for Energy: A View to 2030 25

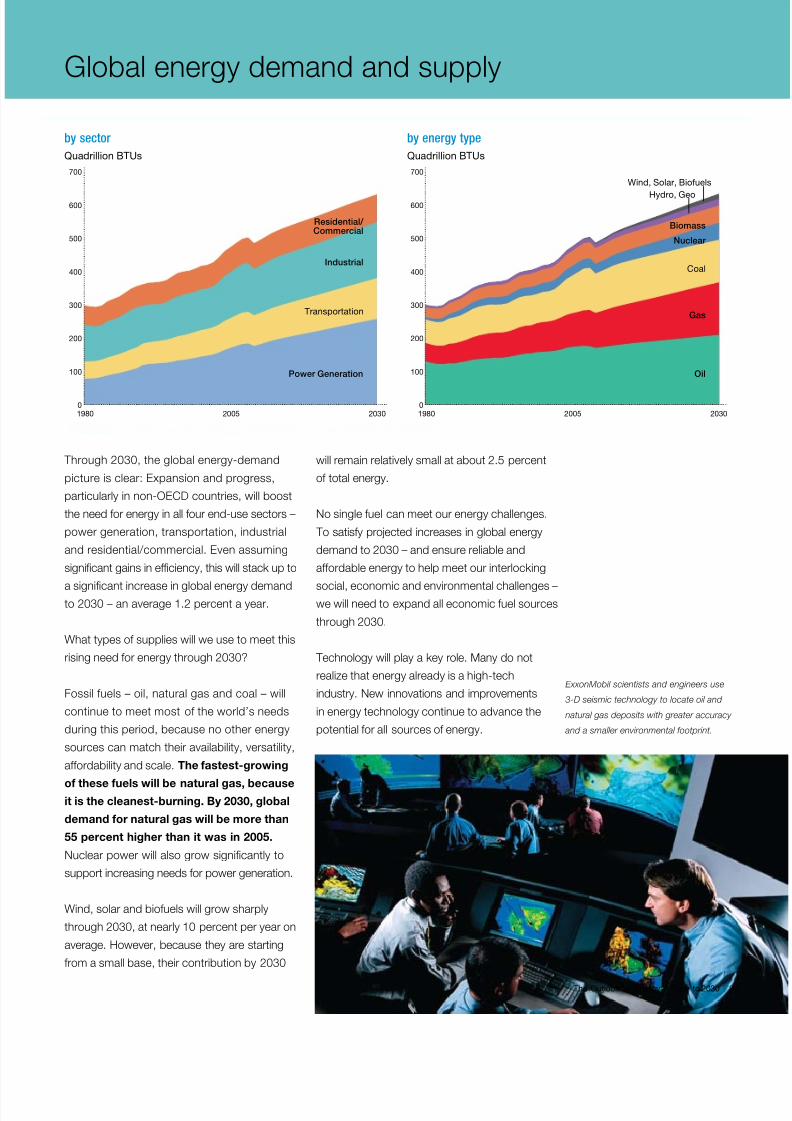

Through 2030, the global energy-demand

picture is clear: Expansion and progress,

particularlyinnon-OECDcountries,willboost

the need or energy in all our end-use sectors –

power generation, transportation, industrial

and residential/commercial. Even assuming

signicant gains in eciency, this will stack up to

a signicant increase in global energy demandto 2030 – an average 1.2 percent a year.

What types o supplies will we use to meet this

rising need or energy through 2030?

Fossil uels – oil, natural gas and coal – will

continue to meet most o the world’s needs

during this period, because no other energy

sources can match their availability, versatility,

aordability and scale. The astest-growing

o these uels will be natural gas, becauseit is the cleanest-burning. By 2030, global

demand or natural gas will be more than

55 percent higher than it was in 2005.

Nuclear power will also grow signicantly to

support increasing needs or power generation.

Wind, solar and biouels will grow sharply

through 2030, at nearly 10 percent per year on

average. However, because they are starting

rom a small base, their contribution by 2030

will remain relatively small at about 2.5 percent

o total energy.

No single uel can meet our energy challenges.

To satisy projected increases in global energy

demand to 2030 – and ensure reliable and

aordable energy to help meet our interlocking

social, economic and environmental challenges –we will need to expand all economic uel sources

through 2030.

Technology will play a key role. Many do not

realize that energy already is a high-tech

industry. New innovations and improvements

in energy technology continue to advance the

potential or all sources o energy.

Global energy demand and supply

Industrial

Transportation

Oil

Gas

Coal

Nuclear

Biomass

Hydro, Geo

Wind, Solar, Biofuels

Power Generation

Residential/

Commercial

by sector

by energy type

1980 2030

Quadrillion BTUs Quadrillion BTUs

700

600

500

400

300

200

100

0

700

600

500

400

300

200

100

02005 1980 20302005

ExxonMobil scientists and engineers use

3-D seismic technology to locate oil and

natural gas deposits with greater accuracy

and a smaller environmental ootprint.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 30/4226 exxonmobil.com

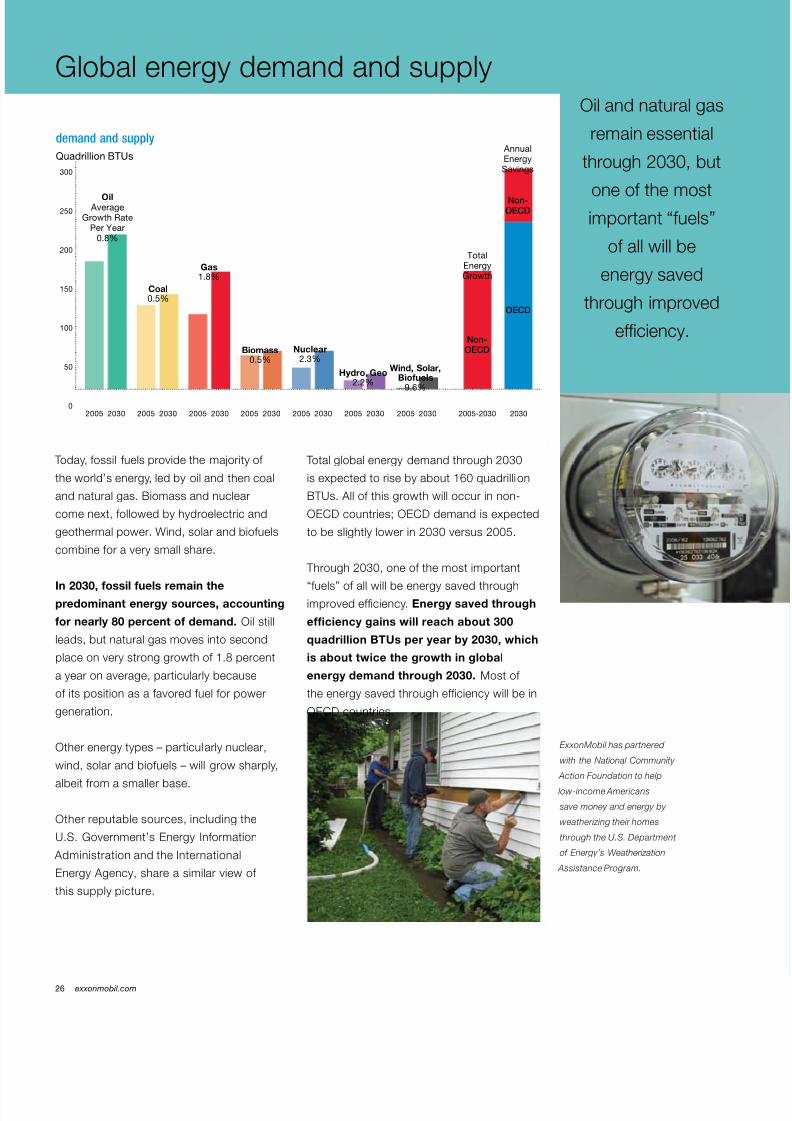

Today, ossil uels provide the majority o

the world’s energy, led by oil and then coal

and natural gas. Biomass and nuclear

come next, ollowed by hydroelectric and

geothermal power. Wind, solar and biouels

combine or a very small share.

In 2030, ossil uels remain thepredominant energy sources, accounting

or nearly 80 percent o demand. Oil still

leads, but natural gas moves into second

place on very strong growth o 1.8 percent

a year on average, particularly because

o its position as a avored uel or power

generation.

Other energy types – particularly nuclear,

wind, solar and biouels – will grow sharply,

albeit rom a smaller base.

Other reputable sources, including the

U.S. Government’s Energy Inormation

Administration and the International

Energy Agency, share a similar view o

this supply picture.

Total global energy demand through 2030

is expected to rise by about 160 quadrillion

BTUs. All o this growth will occur in non-

OECDcountries;OECDdemandisexpected

to be slightly lower in 2030 versus 2005.

Through 2030, one o the most important

“uels” o all will be energy saved throughimproved eciency. Energy saved through

efciency gains will reach about 300

quadrillion BTUs per year by 2030, which

is about twice the growth in global

energy demand through 2030. Most o

the energy saved through eciency will be in

OECDcountries.

Global energy demand and supplyOil and natural gas

remain essential

through 2030, but

one o the mostimportant “uels”

o all will be

energy saved

through improved

eciency.

2005 2030

Oil Average

Growth RatePer Year

0.8%

2005-2030

TotalEnergyGrowth

AnnualEnergySavings

Non-

OECD

Non-

OECD

OECD

20302005 2030

Gas1.8%

2005 2030

Quadrillion BTUs

demand and supply

300

250

200

150

100

50

02005 2030

Nuclear2.3%

2005 2030

Hydro, Geo2.2%

2005 2030

Wind, Solar,Biofuels

9.6%

2005 2030

Biomass0.5%

Coal0.5%

ExxonMobil has partnered

with the National Community

Action Foundation to help

low-income Americans

save money and energy by

weatherizing their homes

through the U.S. Department

o Energy’s Weatherization

Assistance Program.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 31/42The Outlook for Energy: A View to 2030 27

Natural gas will provide a growing share o the world’s energy

through 2030. Aordable and abundant, natural gas can help

provide the energy needed or economic and social progress.

And because it burns cleaner than oil and much cleaner

than coal, natural gas is a powerul tool or reducing the

environmental impact o energy use.

ExxonMobil produces more natural gas than any other public

company in the world. We also develop breakthrough

natural gas technologies that make more o this cleaner-burning uel available to consumers around the world.

In the United States, ExxonMobil technologies have unlocked

vast new resources o natural gas that previously were

trapped in dense rock ormations, as well as other types o

so-called “unconventional” natural gas. These technologies

have resulted in a signifcant upswing in U.S. natural gas

production, and may have similar applications in other parts

o the world.

• OurMulti-Zone Stimulation Technology (MZST) allowsoperators to create ractures in reservoir rock at a more rapid

rate than conventional technology so gas can fow more

easily.UsingMZSTandourFastDrillProcess,ExxonMobil

is increasing recovery and production rates while reducing

development costs and our environmental ootprint.

• ExxonMobilhasjoinedwithQatarPetroleumandother

partnerstofurtherdevelopQatar’sNorthField, the largest

non-associated natural gas feld in the world. There, we

plan to develop natural gas resources exceeding 150 trillion

cubic eet, which will serve a global customer base.

Liquefed Natural Gas (LNG): ExxonMobil is a global leader in

developing and delivering advanced LNG technologies. These

breakthroughs are creating a “global gas market” that can link

theworld’slargestnaturalgasreserves,suchasthoseinQatar,

with consumers who need them.

• ExxonMobilhelpedpioneeranew class o LNG carriers.

Theseships,calledQ-Max,cancarryupto80percentmore

cargo than conventional LNG carriers, reducing transportation

costs while improving eciency and reducing emissions.

• Wearebuildingstate-of-the-artLNGreceivingterminalsin

the United States and Europe. In 2009, o the coast o Italy, we

opened the world’s frst oshore gravity-based structure or unloading, storage and re-gasication o LNG. The terminal’s

main structure rests on the seabed in 95 eet o water, about 10

miles oshore, and out o sight o land.

• ExxonMobil,togetherwithitspartners,isproducingnearly

35 million tons per year o LNG. We anticipate increasing our

joint production to almost 65 million tons per year by 2010. And

beyond 2010, we expect this to go up to around 100 million

tons per year.

The most signicant single use o natural gas is as a uel tomake electricity. As The Outlook or Energy shows, the world’s

need or electricity – and the uels used to produce it – will grow

substantially over the coming decades. Natural gas can help

meet this growing need or electricity.

Natural gas used or electricity can reduce CO2 emissions by

up to 60 percent versus coal, which today is the most popular

uel or power generation. It also has ewer emissions o sulur

oxides and nitrogen oxides.

The importance o

natural gas

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 32/4228 exxonmobil.com

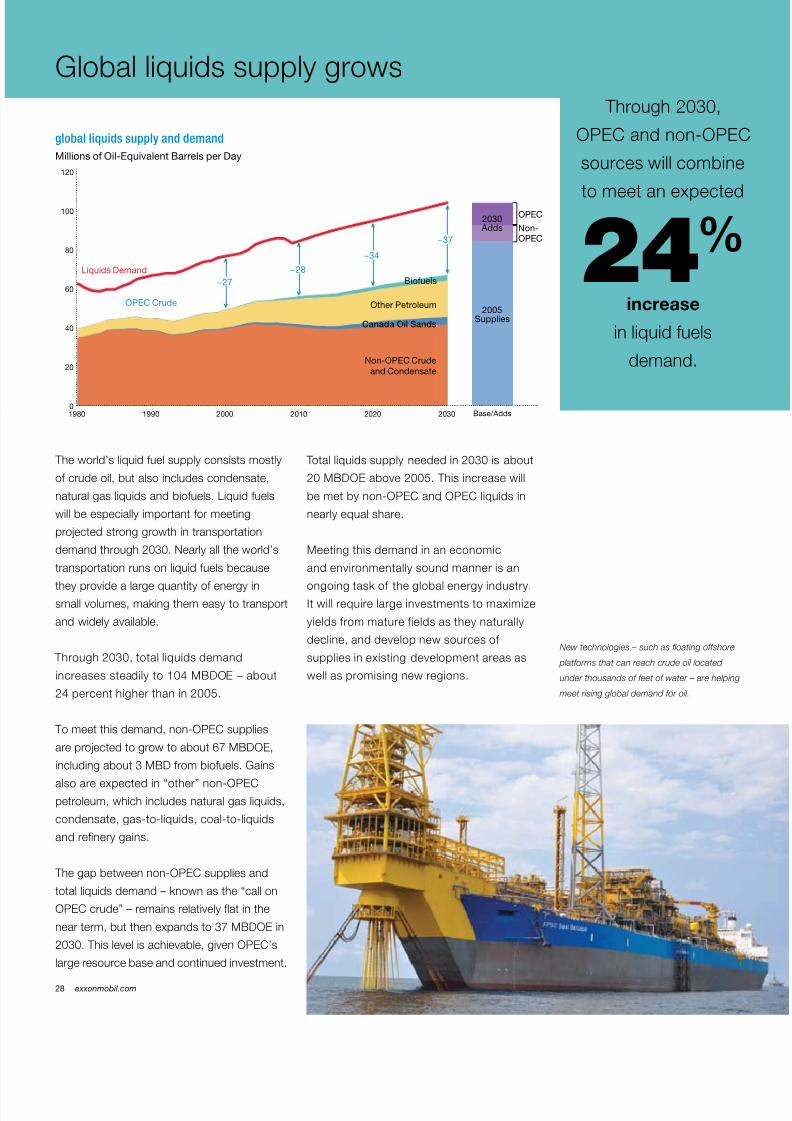

The world’s liquid uel supply consists mostly

o crude oil, but also includes condensate,

natural gas liquids and biouels. Liquid uels

will be especially important or meeting

projected strong growth in transportation

demand through 2030. Nearly all the world’s

transportation runs on liquid uels because

they provide a large quantity o energy insmall volumes, making them easy to transport

and widely available.

Through 2030, total liquids demand

increasessteadilyto104MBDOE–about

24 percent higher than in 2005.

Tomeetthisdemand,non-OPECsupplies

areprojectedtogrowtoabout67MBDOE,

includingabout3MBDfrombiofuels.Gains

alsoareexpectedin“other”non-OPECpetroleum, which includes natural gas liquids,

condensate, gas-to-liquids, coal-to-liquids

and renery gains.

Thegapbetweennon-OPECsuppliesand

total liquids demand – known as the “call on

OPECcrude”–remainsrelativelyatinthe

nearterm,butthenexpandsto37MBDOEin

2030.Thislevelisachievable,givenOPEC’s

large resource base and continued investment.

Total liquids supply needed in 2030 is about

20MBDOEabove2005.Thisincreasewill

bemetbynon-OPECandOPECliquidsin

nearly equal share.

Meeting this demand in an economic

and environmentally sound manner is an

ongoing task o the global energy industry.It will require large investments to maximize

yields rom mature ields as they naturally

decline, and develop new sources o

supplies in existing development areas as

well as promising new regions.

Global liquids supply grows

2005Supplies

2030 Adds Non-

OPEC

Base/Adds

OPEC

global liquids supply and demand

Millions of Oil-Equivalent Barrels per Day

Non-OPEC Crude

and Condensate

Canada Oil Sands

Other Petroleum

Biofuels

Liquids Demand

OPEC Crude

120

100

80

60

40

20

01980 20302010 20201990 2000

~27

~28

~34

~37

New technologies – such as oating oshore

platorms that can reach crude oil located

under thousands o eet o water – are helping

meet rising global demand or oil.

Through 2030,

OPECandnon-OPEC

sources will combine

to meet an expected

24%increase

in liquid uels

demand.

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 33/42The Outlook for Energy: A View to 2030 29

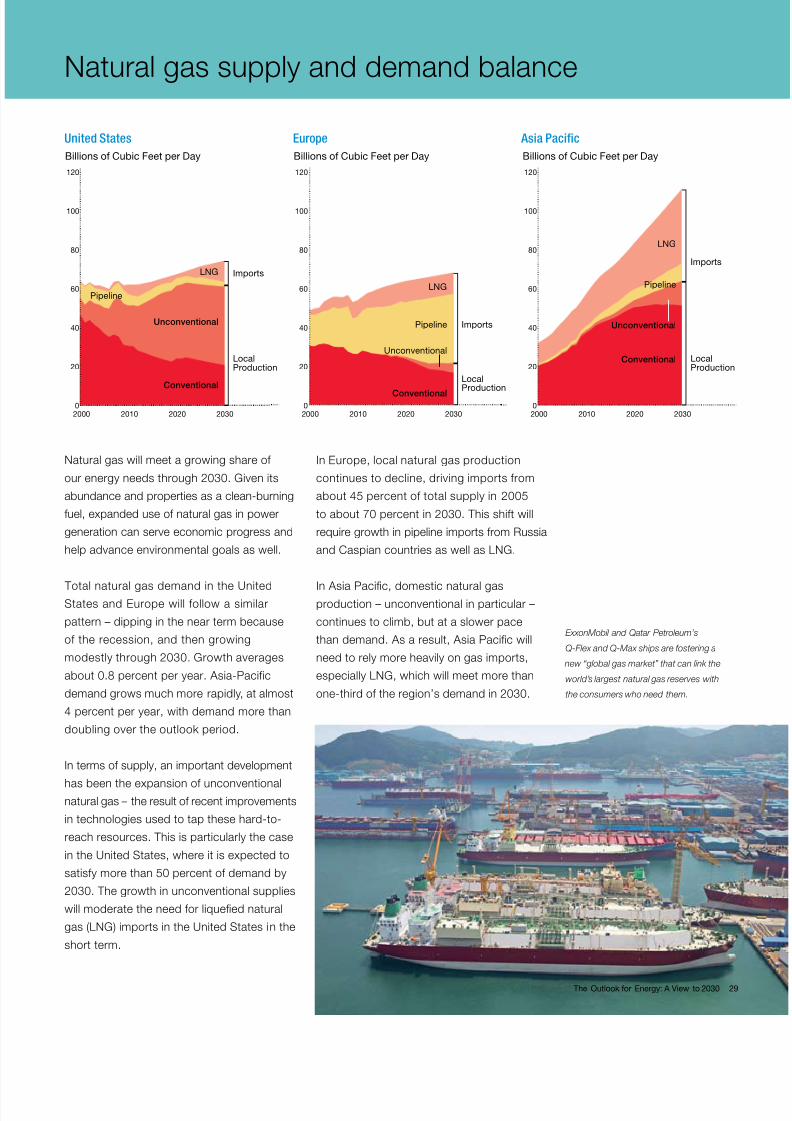

Natural gas will meet a growing share o

our energy needs through 2030. Given its

abundance and properties as a clean-burning

uel, expanded use o natural gas in power

generation can serve economic progress and

help advance environmental goals as well.

Total natural gas demand in the UnitedStates and Europe will ollow a similar

pattern – dipping in the near term because

o the recession, and then growing

modestly through 2030. Growth averages

about0.8percentperyear.Asia-Pacific

demand grows much more rapidly, at almost

4 percent per year, with demand more than

doubling over the outlook period.

In terms o supply, an important development

has been the expansion o unconventionalnatural gas – the result o recent improvements

in technologies used to tap these hard-to-

reach resources. This is particularly the case

in the United States, where it is expected to

satisy more than 50 percent o demand by

2030. The growth in unconventional supplies

will moderate the need or liqueed natural

gas (LNG) imports in the United States in the

short term.

In Europe, local natural gas production

continues to decline, driving imports rom

about 45 percent o total supply in 2005

to about 70 percent in 2030. This shit will

require growth in pipeline imports rom Russia

and Caspian countries as well as LNG.

InAsiaPacic,domesticnaturalgasproduction – unconventional in particular –

continues to climb, but at a slower pace

thandemand.Asaresult,AsiaPacicwill

need to rely more heavily on gas imports,

especially LNG, which will meet more than

one-third o the region’s demand in 2030.

Natural gas supply and demand balance

LocalProduction

Imports

LNG

Pipeline

Unconventional

Conventional

Billions of Cubic Feet per Day

120

100

80

60

40

20

0

Asia Pacific

2000 203020202010

Local

Production

Imports

LNG

Pipeline

Unconventional

Conventional

Billions of Cubic Feet per Day

120

100

80

60

40

20

0

Europe

2000 203020202010

LocalProduction

ImportsLNG

Pipeline

Unconventional

Conventional

Billions of Cubic Feet per Day

120

100

80

60

40

20

0

United States

2000 203020202010

ExxonMobil and Qatar Petroleum’s

Q-Flex and Q-Max ships are ostering a

new “global gas market” that can link the

world’s largest natural gas reserves with

the consumers who need them.

The Outlook for Energy: A View to 2030 29

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 34/4230 exxonmobil.com

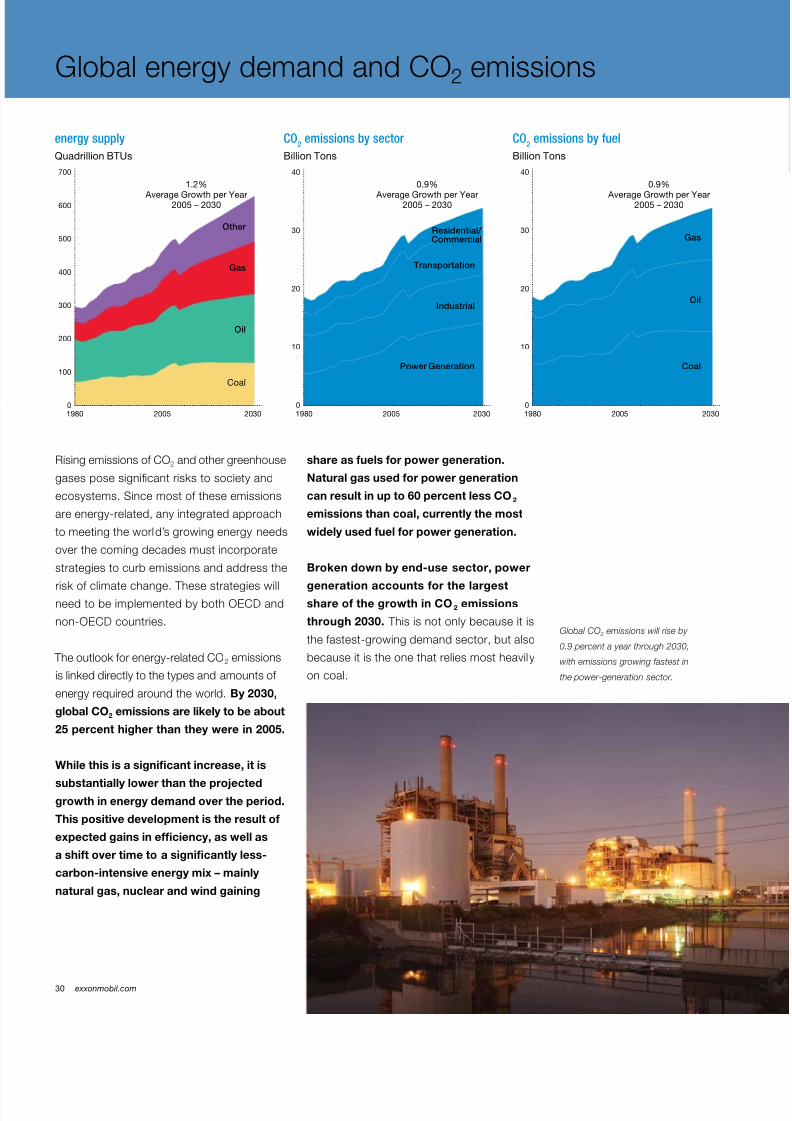

Rising emissions o CO2 and other greenhouse

gases pose signicant risks to society and

ecosystems. Since most o these emissions

are energy-related, any integrated approach

to meeting the world’s growing energy needs

over the coming decades must incorporate

strategies to curb emissions and address the

risk o climate change. These strategies willneedtobeimplementedbybothOECDand

non-OECDcountries.

The outlook or energy-related CO2 emissions

is linked directly to the types and amounts o

energy required around the world. By 2030,

global CO2 emissions are likely to be about

25 percent higher than they were in 2005.

While this is a signifcant increase, it is

substantially lower than the projectedgrowth in energy demand over the period.

This positive development is the result o

expected gains in efciency, as well as

a shit over time to a signifcantly less-

carbon-intensive energy mix – mainly

natural gas, nuclear and wind gaining

share as uels or power generation.

Natural gas used or power generation

can result in up to 60 percent less CO2

emissions than coal, currently the most

widely used uel or power generation.

Broken down by end-use sector, power

generation accounts or the largestshare o the growth in CO2 emissions

through 2030. This is not only because it is

the astest-growing demand sector, but also

because it is the one that relies most heavily

on coal.

Global energy demand and CO2 emissions

Global CO 2 emissions will rise by

0.9 percent a year through 2030,

with emissions growing astest in

the power-generation sector.

Gas

Oil

Coal

1.2%

Average Growth per Year2005 – 2030

Other

energy supply

1980 2030

Quadrillion BTUs

700

600

500

400

300

200

100

02005

Gas

Oil

Coal

0.9%

Average Growth per Year2005 – 2030

CO2

emissions by fuel

1980 2030

Billion Tons

40

30

20

10

02005

Transportation

Industrial

Power Generation

0.9%

Average Growth per Year2005 – 2030

CO2

emissions by sector

1980 2030

Billion Tons

40

30

20

10

02005

Residential/ Commercial

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 35/42The Outlook for Energy: A View to 2030 31

ExxonMobil believes that the broad objective o actions

to address climate change should be to reduce the risk o

serious impacts on society and the environment, while not

harming the contribution o energy to economic development

and expanded prosperity around the world.

As a company with 125 years o experience developing the

technology and inrastructure that delivers the world’s energy,

we believe we have a unique perspective on what types

o conditions are necessary to successully tackle such a

complex global energy challenge.

Above all, companies, consumers and investors will need a

market environment that provides clear signals to encourage

sensible and broad-based investment in the two most

powerul emissions-ghting tools: improvements to energy

eciency and the expanded use o lower-carbon uels such

as natural gas. Continued progress on these ronts will require

trillions o dollars in new investment, and steadast work on

the creation o new technologies.

Some governments are considering policies that would

impose a “cost” on CO2 emissions. In these cases,

ExxonMobil believes that a revenue-neutral carbon tax

has many advantages over a cap-and-trade system in terms

o achieving our society’s shared goal o reducing emissions

over the long term:

• Acarbontaxcancreate a clear and uniorm cost or

emissions in all economic decisions. This price stability

encourages companies to invest in advanced technologies,

and provides a clear incentive or all consumers to increase

eciency and reduce emissions.

• Acarbontaxavoids the costs and complexity o having

to build a new market or emissions allowances or the need

or new layers o regulators and administrators to manage

this market. It also does not open up signicant opportunities

or market manipulation, or require complex and costly

compliance and enorcement systems.

• A carbon tax can be made revenue-neutral. Returning

the tax revenue to consumers through reductions in other

taxes – payroll taxes or a simple dividend – reduces the

burden on the economy, and ensures that government

policy is specically ocused on reducing emissions, not on

becoming a revenue stream or other purposes.

• Becauseglobalparticipationissoimportanttocontrolling

emissions, a carbon tax may be a more viable ramework or

engaging participation by other nations.

As The Outlook or Energy shows, curbing greenhouse gas

emissions while also meeting rising energy demand will

require a tremendous global eort, sustained over decades.

Compared with a cap-and-trade system, a carbon tax – by being

predictable, transparent, and comparatively simple to understand

and implement – is a more eective approach or creating the

conditions necessary to achieve emissions-reduction goals.

Options or

carbon policy

The Outlook for Energy: A View to 2030 31

8/7/2019 ExxonMobil “The Outlook for Energy A View to 2030”

http://slidepdf.com/reader/full/exxonmobil-the-outlook-for-energy-a-view-to-2030 36/4232 exxonmobil.com

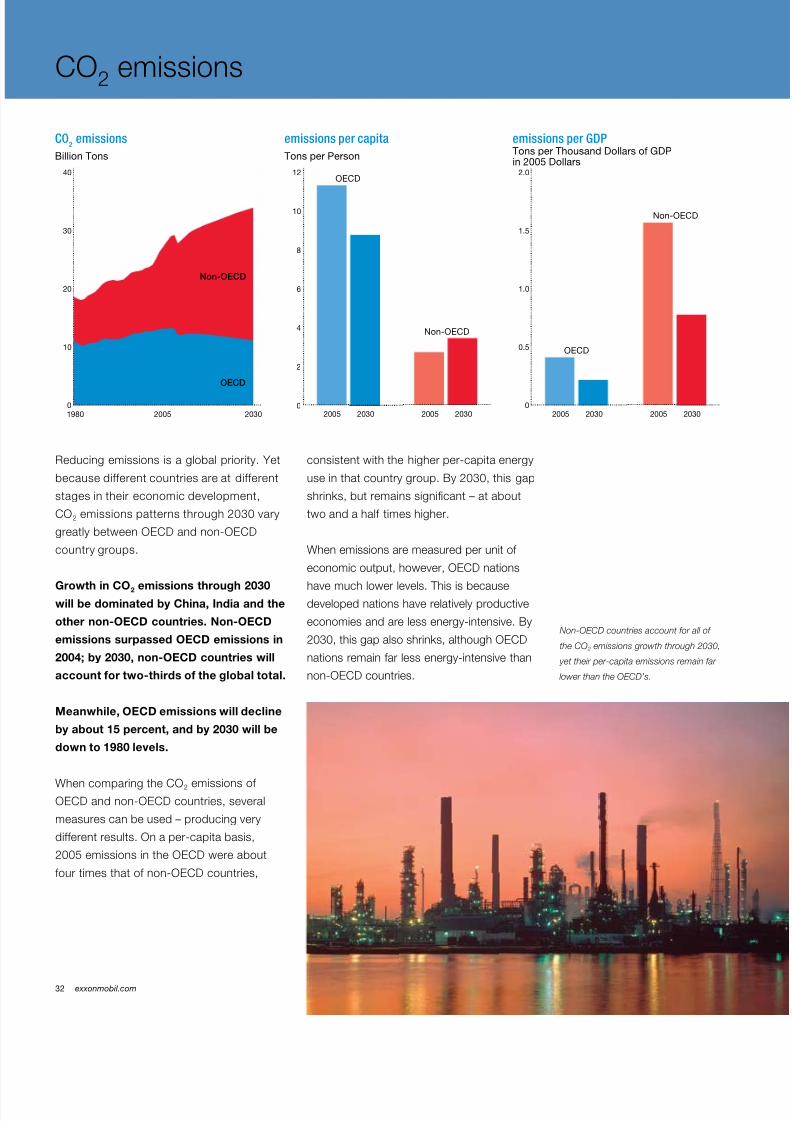

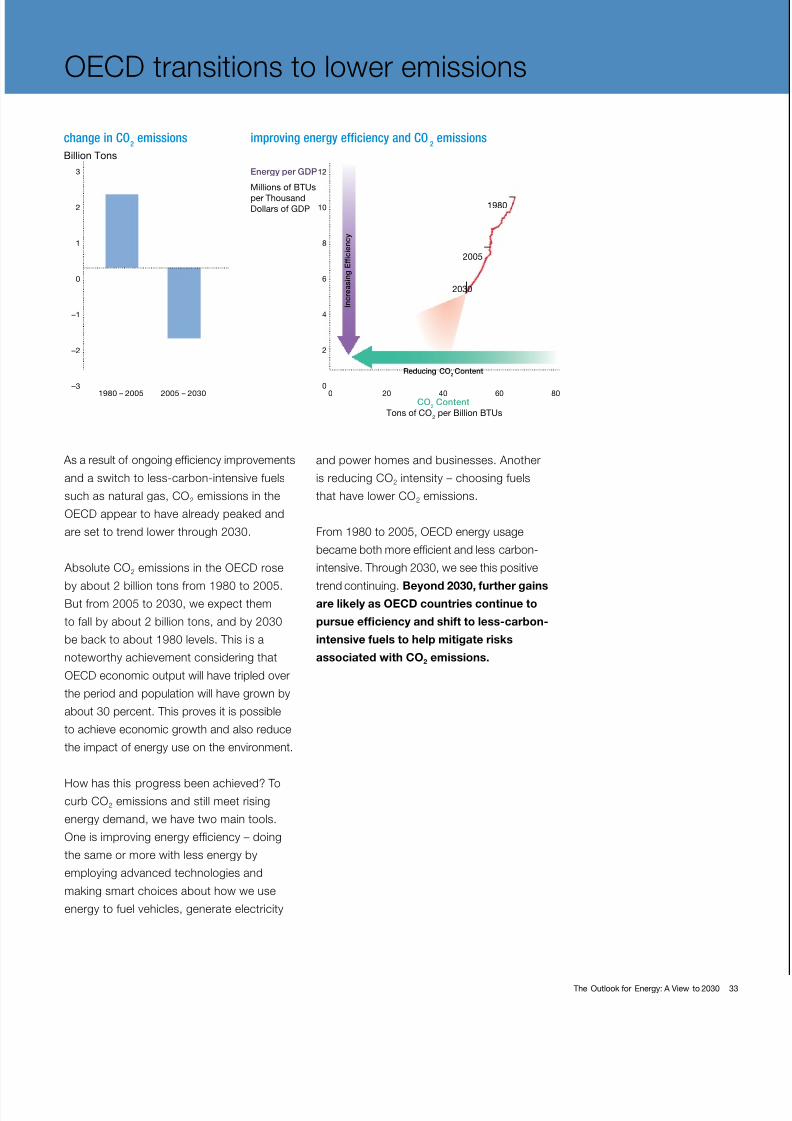

Reducing emissions is a global priority. Yet

because dierent countries are at dierent

stages in their economic development,

CO2 emissions patterns through 2030 vary

greatlybetweenOECDandnon-OECD

country groups.

Growth in CO2 emissions through 2030will be dominated by China, India and the

other non-OECD countries. Non-OECD

emissions surpassed OECD emissions in

2004; by 2030, non-OECD countries will

account or two-thirds o the global total.

Meanwhile, OECD emissions will decline

by about 15 percent, and by 2030 will be

down to 1980 levels.

When comparing the CO2 emissions o OECDandnon-OECDcountries,several

measures can be used – producing very

dierent results. On a per-capita basis,

2005emissionsintheOECDwereabout

fourtimesthatofnon-OECDcountries,

consistent with the higher per-capita energy

use in that country group. By 2030, this gap

shrinks, but remains signicant – at about

two and a hal times higher.

When emissions are measured per unit o

economicoutput,however,OECDnations

have much lower levels. This is becausedeveloped nations have relatively productive

economies and are less energy-intensive. By

2030,thisgapalsoshrinks,althoughOECD

nations remain ar less energy-intensive than

non-OECDcountries.

CO2 emissions