ecap asean power grid.ppt

TRANSCRIPT

ASEAN Power GridASEAN Power Grid by

Mr.Kornphat SrisupingSystem Planning DivisionSystem Planning Division

Electricity Generating Authority Of Thailand

Expert Group Meeting on Conceptualizing the Asian Energy HighWay

Electricity Generating Authority of Thailand

Urumqi, China, 3-5 September 2013

1

Electricity Generating Authority of ThailandPower for Thai Happiness

ASEAN Energy CooperationASEAN Energy Cooperation

AMEM: ASEAN Ministers on Energy Meeting (once a year)

SOME: Senior Officials Meeting on Energy (once a year)SOME: Senior Officials Meeting on Energy (once a year)

ACE: ASEAN Centre for Energy (accelerate the integration of energy strategies within ASEAN by providing information technology and expertise)strategies within ASEAN by providing information, technology and expertise)

AFOC: ASEAN Forum on Coal

EE&C-SSN: Energy Efficiency and Conservation Subsector Network

NRSE-SSN: New and Renewable Sources of Energy Subsector Network

ASCOPE: ASEAN Council on Petroleum

HAPUA: Heads of ASEAN Power Utilities/AuthoritiesHAPUA: Heads of ASEAN Power Utilities/Authorities

AERN: ASEAN Energy Regulatory Network (TOR being prepared)

2

HAPUA & AIMS BackgroundHAPUA & AIMS Background

Dec 1997 : Heads of ASEAN governments committed to jointly develop ASEAN Power Grid (APG) and Trans-ASEAN Gas Pipeline as a part of the ASEAN Vision 2020 [Th 2 d ASEAN I f l S it i K l L M l i ]ASEAN Vision 2020 [The 2nd ASEAN Informal Summit in Kuala Lumpur, Malaysia]

Jul 1999 : HAPUA was assigned to materialized APG through ASEAN Interconnection Master Plan Study (AIMS) [The 17th AMEM in Bangkok, Th il d]Thailand]

Apr 2000 : AIMS Working Group was established [The 16th Meeting of HAPUA in Chiang Rai, Thailand]

Jul 2003 : AIMS Final Report was endorsed [The 21st AMEM in Langkawi, Malaysia]

May 2004 : HAPUA Structure was re-organized

Feb 2006 : TOR and Work Plan of AIMS II was adopted and the study startedFeb 2006 : TOR and Work Plan of AIMS-II was adopted and the study started [The 1st Meeting of Power Interconnection Sub Working Group (PI SWG) in Krabi, Thailand]

Jul 2011 : AIMS-II Final Report was endorsed [The 27th Meeting of HAPUA in Danang,Jul 2011 : AIMS II Final Report was endorsed [The 27 Meeting of HAPUA in Danang, Vietnam]

Jun 2012 : HAPUA Structure was re-organized

3

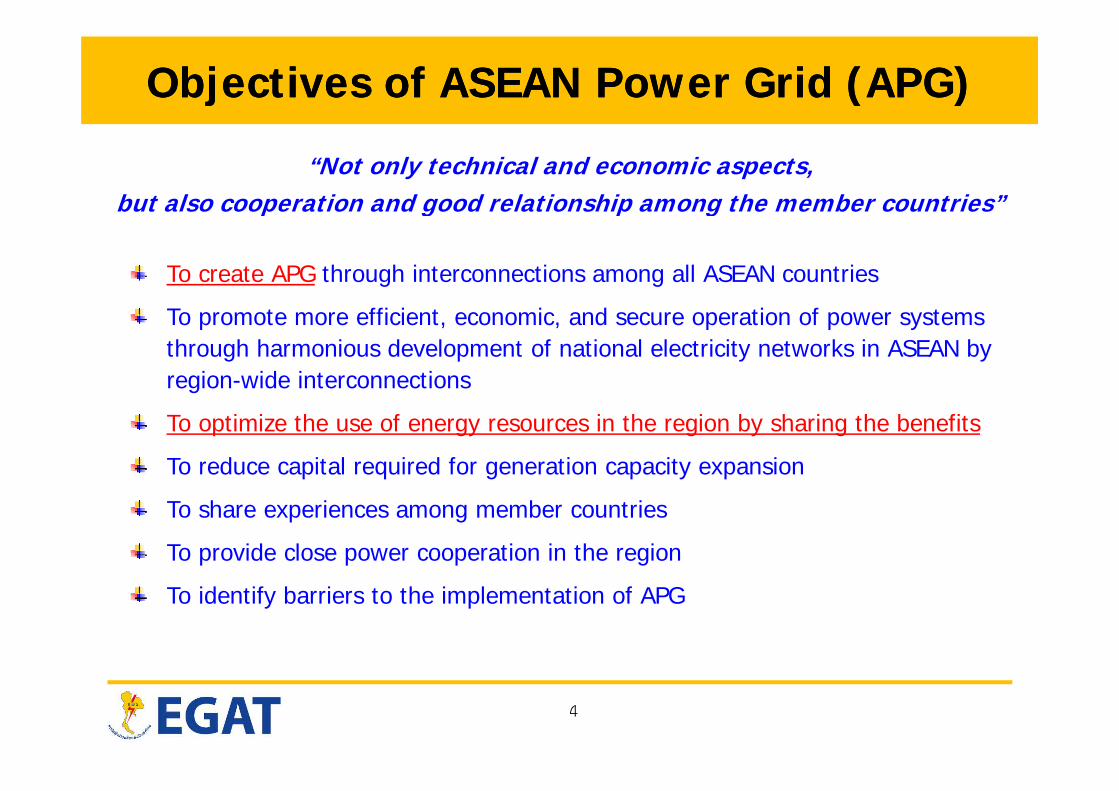

Objectives of ASEAN Power Grid (APG)Objectives of ASEAN Power Grid (APG)

“Not only technical and economic aspects, but also cooperation and good relationship among the member countries”p g p g

To create APG through interconnections among all ASEAN countries

To promote more efficient, economic, and secure operation of power systems through harmonious development of national electricity networks in ASEAN by region-wide interconnections

To optimize the use of energy resources in the region by sharing the benefits

To reduce capital required for generation capacity expansion

To share experiences among member countries

To provide close power cooperation in the region

To identify barriers to the implementation of APG

4

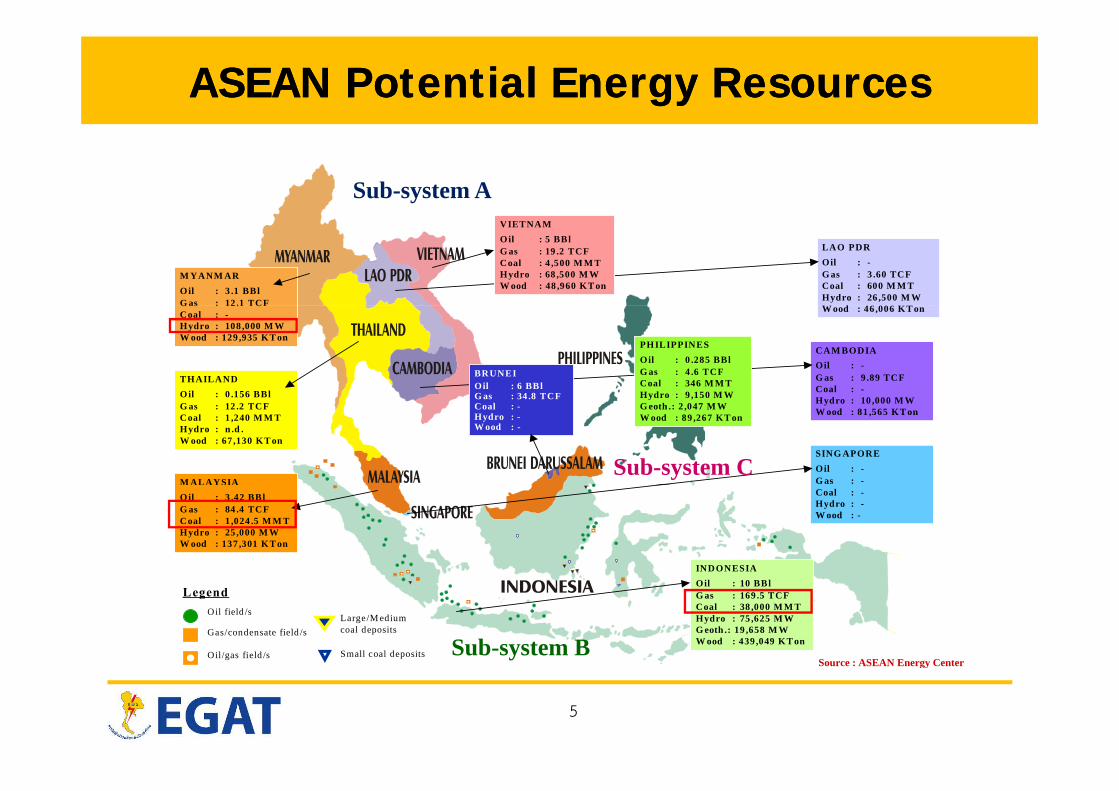

ASEAN Potential Energy ResourcesASEAN Potential Energy Resources

Sub-system A

M YANM AROil : 3 .1 BBl G as : 12 .1 TCF

LAO PDROil : -G as : 3 .60 TCFCoal : 600 M M THydro : 26 ,500 M WW d 46 006 KT

VIETNAMOil : 5 BBl G as : 19 .2 TCFCoal : 4 ,500 M M THydro : 68 ,500 M WW ood : 48 ,960 KT on

G as : 12 .1 TCFCoal : -Hydro : 108 ,000 M WW ood : 129 ,935 KT on

THAILANDOil : 0 156 BBl

W ood : 46 ,006 KT on

CAM BODIAOil : -G as : 9 .89 TCFCoal : -

BRUNEIOil : 6 BBlG as : 34 8 TCF

PHILIPPINESOil : 0 .285 BBl G as : 4 .6 TCFCoal : 346 M M THydro : 9 150 M WOil : 0 .156 BBl

G as : 12 .2 TCFCoal : 1 ,240 M M THydro : n .d .W ood : 67 ,130 KT on

M ALAYSIA

Hydro : 10 ,000 M WW ood : 81 ,565 KT on

SING APOREOil : -G as : -

G as : 34 .8 TCFCoal : -Hydro : -W ood : -

Hydro : 9 ,150 M WG eoth .: 2 ,047 M WW ood : 89 ,267 KT on

Sub-system C

INDONESIA

Oil : 3 .42 BBl G as : 84 .4 TCFCoal : 1 ,024 .5 M M THydro : 25 ,000 M WW ood : 137 ,301 KT on

Coal : -Hydro : -W ood : -

LegendOil field /s

Gas/condensate field /s

Oil/gas field /s

Large/M edium coal deposits

Small coal deposits

Oil : 10 BBlG as : 169 .5 TCFCoal : 38 ,000 M M THydro : 75 ,625 M WG eoth .: 19 ,658 M WW ood : 439 ,049 KT on

Source : ASEAN Energy CenterSub-system B

5

Source : ASEAN Energy Center

CurrentCurrent HAPUA StructureHAPUA Structure

R ti Li

AMEMASEANReporting Line

Consultation LineASEAN

Secretariat

SOME

HAPUA Council

HAPUASecretariat

HAPUA Working Committee(Country Coordinator)

ASEAN Power Grid Consultative Committee

(APGCC)

Working Group #3Distribution &

Power Reliability d Q lit

Working Group #4Policy &

Commercial D l t

Working Group #5

Human Resource

Working Group #1

Generation

Working Group #2

Transmissionand Quality

Chair : SingaporeVice Chair : Myanmar

Development

Chair : PhilippinesVice Chair : Cambodia

Chair : MalaysiaVice Chair : Brunei

Chair : IndonesiaVice Chair : Lao PDR

Chair : ThailandVice Chair : Vietnam

6Restructured due to the approval of the 15th Meeting of HAPUA Committee

and endorsement of the 28th Meeting of HAPUA Council (6th June 2012).

HAPUAHAPUA MembersMembers

Department of Electrical ServicesBrunei Darussalam

Electricité du CambodgeKingdom of Cambodia

PT. PLN (Persero)Republic of Indonesia

Electricité du LaosLao PDRRepublic of Indonesia Lao PDR

Tenaga Nasional BerhadM l i

Department of Electric Power of MyanmarU i f MMalaysia Union of Myanmar

National Power Corporation Singapore Power LTD

Electricity of Vietnam

pRepublic of the Philippines

g pRepublic of Singapore

Electricity Generating Authority of Thailand Electricity of VietnamSocialist Republic of Viet Nam

Electricity Generating Authority of ThailandKingdom of Thailand

7

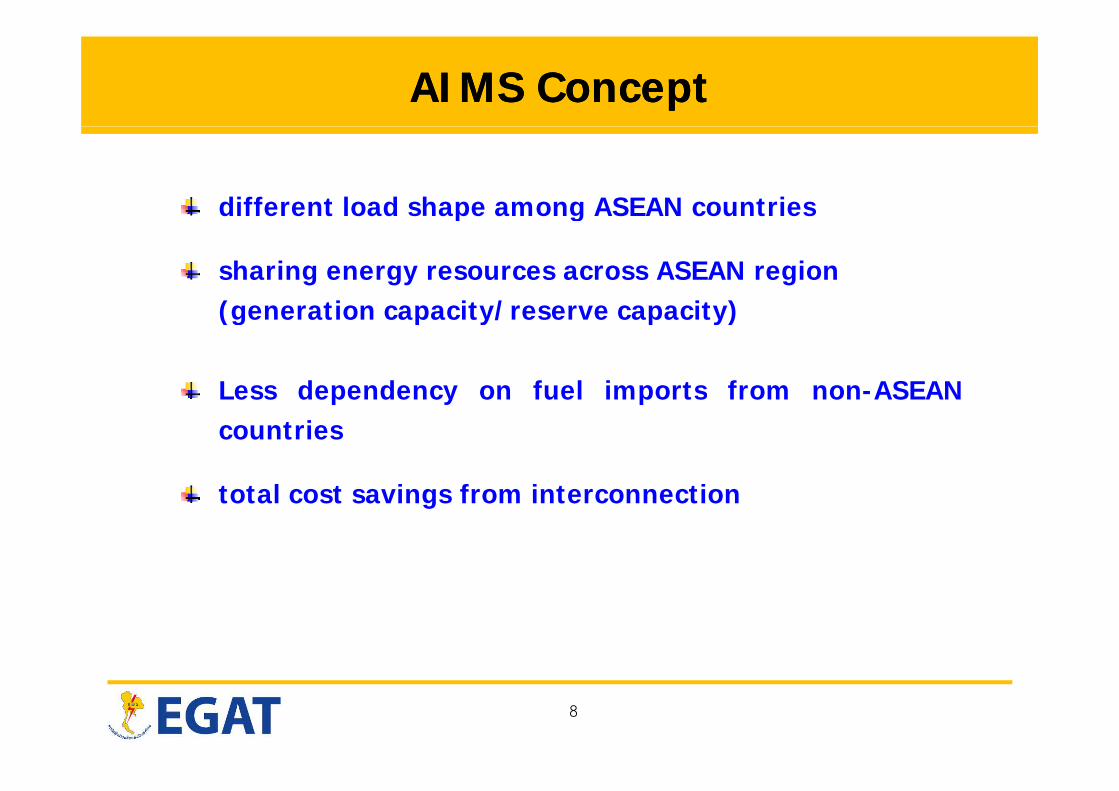

AIMS ConceptAIMS Concept

different load shape among ASEAN countriesd e e t oad s ape a o g S cou t es

sharing energy resources across ASEAN region(generation capacity/reserve capacity)(generation capacity/reserve capacity)

Less dependency on fuel imports from non-ASEANLess dependency on fuel imports from non ASEANcountries

t t l t i f i t titotal cost savings from interconnection

8

MethodologyMethodology

Assumption and criteria of each system

Data collection (Generation and Transmission)

Formulation of least cost generation capacity and

transmission expansion planning of each systemp p g y

Formulation of least cost generation capacity and

transmission expansion planning of interconnection

Determination of total cost savingsDetermination of total cost savings

9

Demand 2 696 MW

Demand & Gen Supply in Demand & Gen Supply in 2025 2025 (individual)(individual)

Demand 74,277 MWi

Non Co-in Demand 213,804 MWCo-in Demand 189,098 MWTotal Gen Cap 254,992 MW

Demand 4,212 MWDomestic 6,632 MWImport - MWEE - MW

Demand 2,696 MWDomestic 4,653 MWImport - MWEE - MW

Domestic 82,874 MWImport: Ca, La, Cn

2,863 MWEE - MW

EE MW

Demand 19,649 MW

Demand 4,301 MWDomestic 4,738 MWImport: La, Vn 300 MW (from Grid)EE - MW

Demand 54,588 MWDomestic 57,494 MWImport: La 3,141 MW

Demand 1,132 MWDomestic 1,539 MW

,Domestic 24,719 MWImport - MWEE - MW

EE: PM 300 MW

Demand 21,752 MWDomestic 25,728 MW

Demand 2,208 MWDomestic 2,573 MW

Domestic 1,539 MWImport - MWEE 200 MW

,Import - MWEE: Th 300 MW

Demand 9,837 MWDomestic 12 798 MW

Domestic 2,573 MWImport - MWEE - MW

Domestic 12,798 MWImport - MWEE - MW

Demand 13,329 MW Demand 1,237 MW

Demand 4,586 MWDomestic 5,990 MWImport MW

10

,Domestic 17,634 MWImport - MWEE - MW

Domestic 1,617 MWImport - MWEE 200 MW

Import - MWEE 400 MW

Note:1) Peak demand of individual systems2) Domestic capacity includes existing, committed and generic projects 3) Import and EE capacity includes existing and committed projects only

Demand 2 696 MW

Demand & Gen Supply in Demand & Gen Supply in 2025 2025 (interconnected)(interconnected)

Demand 74,277 MWi

Demand 4,212 MWDomestic 6,632 MWImport - MWEE - MW

Demand 2,696 MWDomestic 4,653 MWImport - MWEE: Th 600 MW

Co-in Demand 189,098 MWTotal Gen Cap 252,979 MWReduced Gen Cap 2,013 MW

Domestic 81,874 MWImport: Ca, La, Cn

3,585 MWEE - MW

EE MWDemand 4,301 MWDomestic 4,438 MWImport: La, Vn 300 MW (from grid)EE: Th 300 MW

Demand 19,649 MW

Demand 54,588 MWDomestic 50,294 MWImport: Ca, La, Mm

10,591 MWDemand 1,132 MWDomestic 1,539 MW

,Domestic 24,419 MWImport - MWEE 500 MW

,EE: Ca, La, PM 1,500MW

Demand 21,752 MWDomestic 21,848 MW

Demand 2,208 MWDomestic 2,473 MW

Domestic 1,539 MWImport - MWEE 200 MW

,Import: Sw 3,200 MWEE: Th, Sm 1,200 MW

Demand 9,837 MWDomestic 11 003 MW

Domestic 2,473 MWImport: Sw 100 MWEE 500 MW

Domestic 11,003 MWImport: Bt, PM, Sm

1,800 MWEE - MW

Demand 13,329 MW Demand 1,237 MW

Demand 4,586 MWDomestic 6,040 MWImport MW

11

,Domestic 17,034 MWImport - MWEE: PM 600 MW

Domestic 1,457 MWImport - MWEE 200 MW

Import - MWEE 400 MW

Note:1) Peak demand of individual systems2) Domestic, import and EE capacity includes existing, committed and generic projects

L V

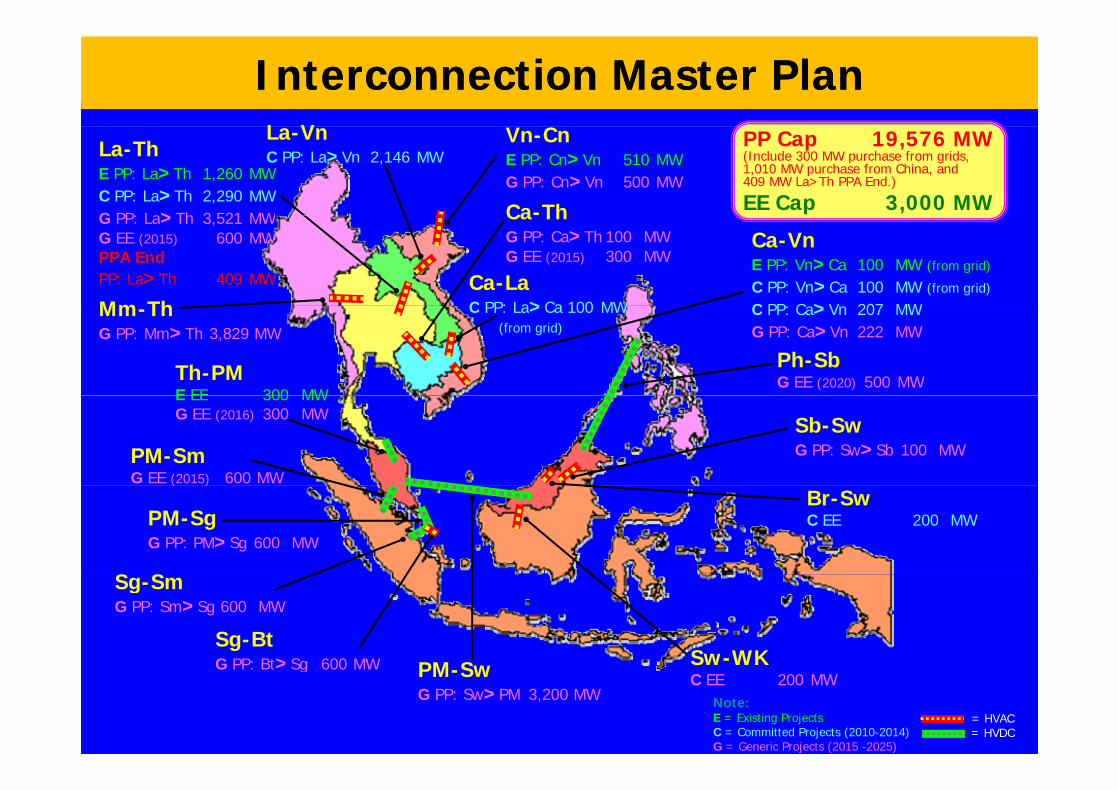

Interconnection Master PlanInterconnection Master PlanPP Cap 19,576 MW(Include 300 MW purchase from grids,1,010 MW purchase from China, and 409 MW La>Th PPA End.)

EE Cap 3,000 MWCa-Th

La-VnC PP: La>Vn 2,146 MWLa-Th

E PP: La>Th 1,260 MWC PP: La>Th 2,290 MWG PP: La>Th 3 521 MW

Vn-CnE PP: Cn>Vn 510 MWG PP: Cn>Vn 500 MW

Ca-VnE PP: Vn>Ca 100 MW (from grid)

C PP: Vn>Ca 100 MW (from grid)

C PP C >V 207 MW

Ca ThG PP: Ca>Th 100 MWG EE (2015) 300 MW

G PP: La>Th 3,521 MWG EE (2015) 600 MWPPA EndPP: La>Th 409 MW

Mm ThCa-LaC PP: La>Ca 100 MW C PP: Ca>Vn 207 MW

G PP: Ca>Vn 222 MWMm-ThG PP: Mm>Th 3,829 MW

Th-PME EE 300 MW

Ph-SbG EE (2020) 500 MW

C PP: La>Ca 100 MW(from grid)

E EE 300 MW G EE (2016) 300 MW

PM-SmG EE (2015) 600 MW

Sb-SwG PP: Sw>Sb 100 MW

( )

PM-SgG PP: PM>Sg 600 MW

S S

Br-SwC EE 200 MW

Sg-SmG PP: Sm>Sg 600 MW

Sg-BtG PP: Bt>Sg 600 MW PM S Sw-WK

12 Note:E = Existing Projects C = Committed Projects (2010-2014)G = Generic Projects (2015 -2025)

= HVAC= HVDC

G PP: Bt>Sg 600 MW PM-SwG PP: Sw>PM 3,200 MW

SC EE 200 MW

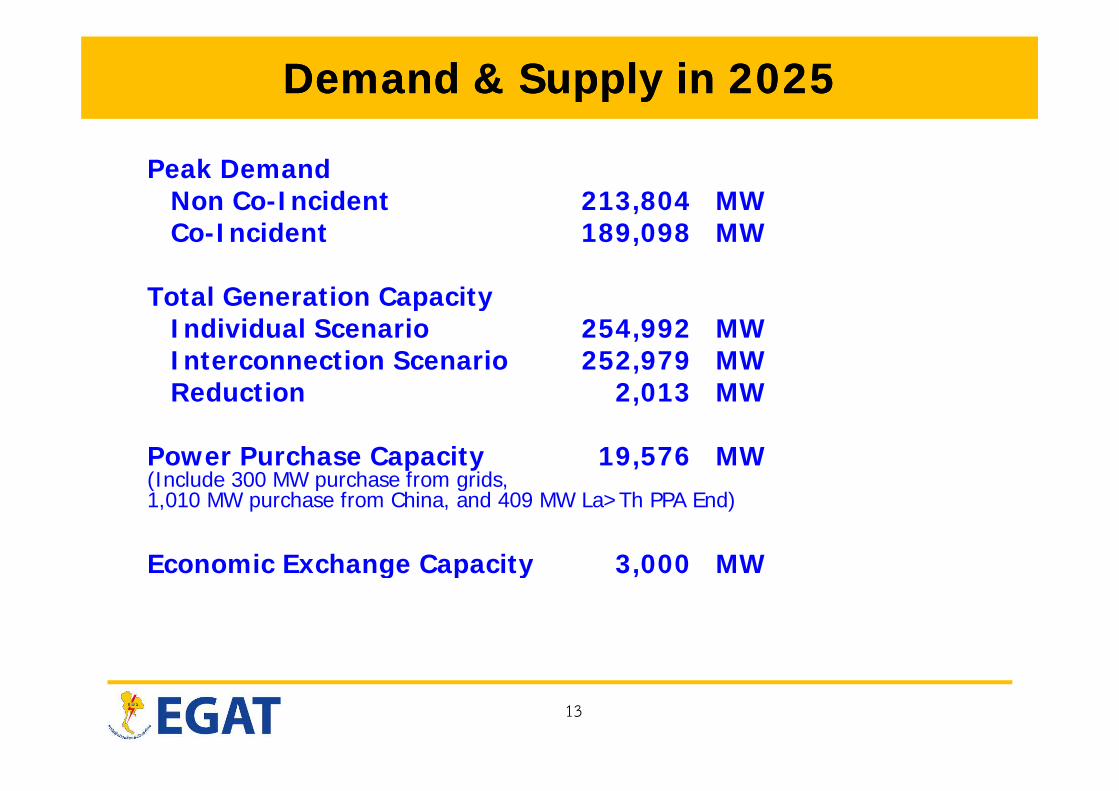

Demand & Supply in Demand & Supply in 20252025

Peak DemandNon Co-Incident 213,804 MWCo-Incident 189,098 MW

Total Generation Capacity ota Ge e at o Capac tyIndividual Scenario 254,992 MWInterconnection Scenario 252,979 MWReduction 2 013 MWReduction 2,013 MW

Power Purchase Capacity 19,576 MW(Include 300 MW purchase from grids,(Include 300 MW purchase from grids, 1,010 MW purchase from China, and 409 MW La>Th PPA End)

Economic Exchange Capacity 3,000 MWg p y ,

13

Fuel MixFuel Mix

3 5 6 7

90%

100%

3

29

2

29 29 29 3032 37 40 41 41 42 43 43

4343 42 42

70%

80%

Renew&Others

Geothermal3 2 2

60%

Geothermal

Uranium

Lignite&Coal

Heavy Oil

Diesel

56 53 51 47 4544

4139 38 38 37 36 36 34

33 33 33

40%

50% Diesel

Gas

Hydro&Pump

20%

30%

12 14 17 19 21 20 20 19 20 19 19 19 19 19 18 18 18

0%

10%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

14

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

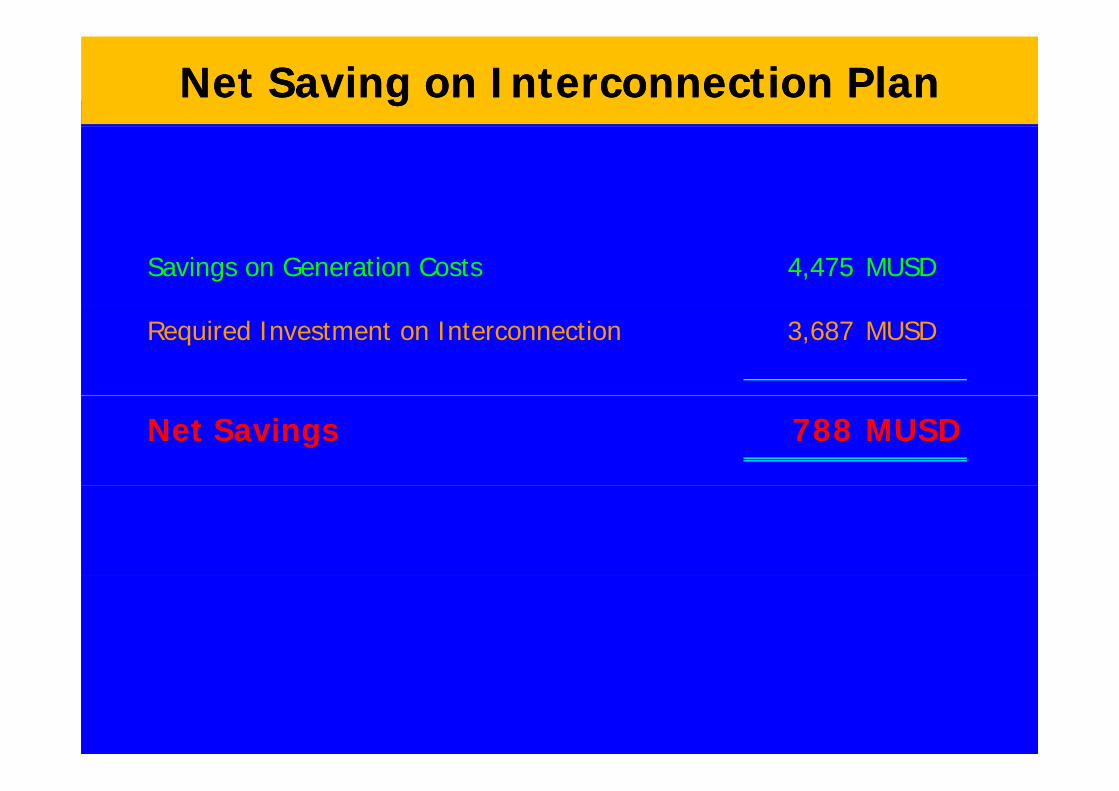

Net Saving on Interconnection PlanNet Saving on Interconnection Plan

Savings on Generation Costs 4,475 MUSD

Required Investment on Interconnection 3,687 MUSD

Net Savings 788 MUSD

15

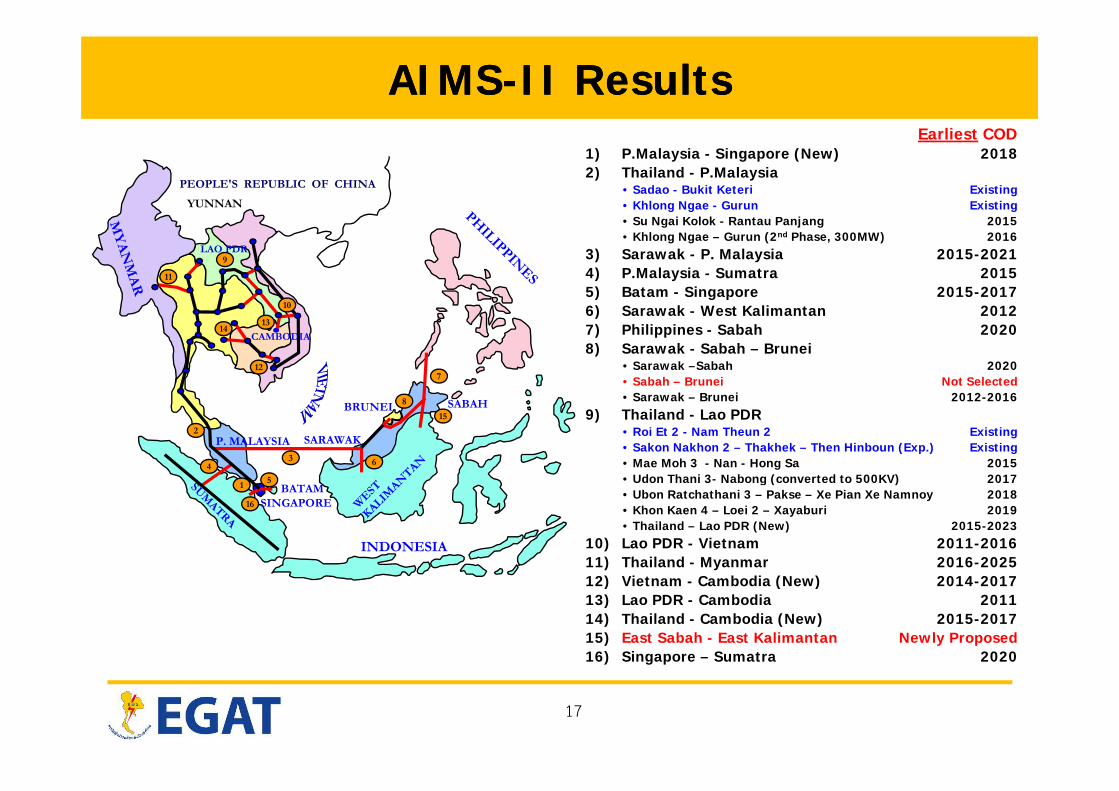

AIMSAIMS--II FindingsII Findings

Benefit : Sharing energy resources among ASEAN Countries to optimize the utilization of ASEAN resources for highestoptimize the utilization of ASEAN resources for highest efficiency

Results:

By 2025, there will be up to 19,576 MW of cross-border powerpurchase and 3 000 MW of economic exchange through thepurchase and 3,000 MW of economic exchange through thecross border interconnections

The integration of ASEAN Network resulted in a net saving ofThe integration of ASEAN Network resulted in a net saving of788 MUSD and a reduction in installed capacity by 2,013 MW

1616

AIMSAIMS--II ResultsII Results

PEOPLE'S REPUBLIC OF CHINA

YUNNAN

Earliest COD1) P.Malaysia - Singapore (New) 20182) Thailand - P.Malaysia

• Sadao - Bukit Keteri Existing• Khlong Ngae - Gurun Existing

11

10

9LAO PDR

• Su Ngai Kolok - Rantau Panjang 2015• Khlong Ngae – Gurun (2nd Phase, 300MW) 2016

3) Sarawak - P. Malaysia 2015-20214) P.Malaysia - Sumatra 20155) Batam - Singapore 2015-20176) S k W t K li t 2012

CAMBODIA14

10

127

136) Sarawak - West Kalimantan 20127) Philippines - Sabah 20208) Sarawak - Sabah – Brunei

• Sarawak –Sabah 2020• Sabah – Brunei Not Selected• Sarawak Brunei 2012 2016

SARAWAK

BRUNEI

P. MALAYSIA

BATAM

8

643

1

2

5

15SABAH • Sarawak – Brunei 2012-2016

9) Thailand - Lao PDR• Roi Et 2 - Nam Theun 2 Existing• Sakon Nakhon 2 – Thakhek – Then Hinboun (Exp.) Existing• Mae Moh 3 - Nan - Hong Sa 2015• Udon Thani 3- Nabong (converted to 500KV) 2017

INDONESIA

BATAMSINGAPORE

1

16• Ubon Ratchathani 3 – Pakse – Xe Pian Xe Namnoy 2018• Khon Kaen 4 – Loei 2 – Xayaburi 2019• Thailand – Lao PDR (New) 2015-2023

10) Lao PDR - Vietnam 2011-201611) Thailand - Myanmar 2016-2025

) i b di ( )12) Vietnam - Cambodia (New) 2014-201713) Lao PDR - Cambodia 201114) Thailand - Cambodia (New) 2015-201715) East Sabah - East Kalimantan Newly Proposed16) Singapore – Sumatra 2020

17

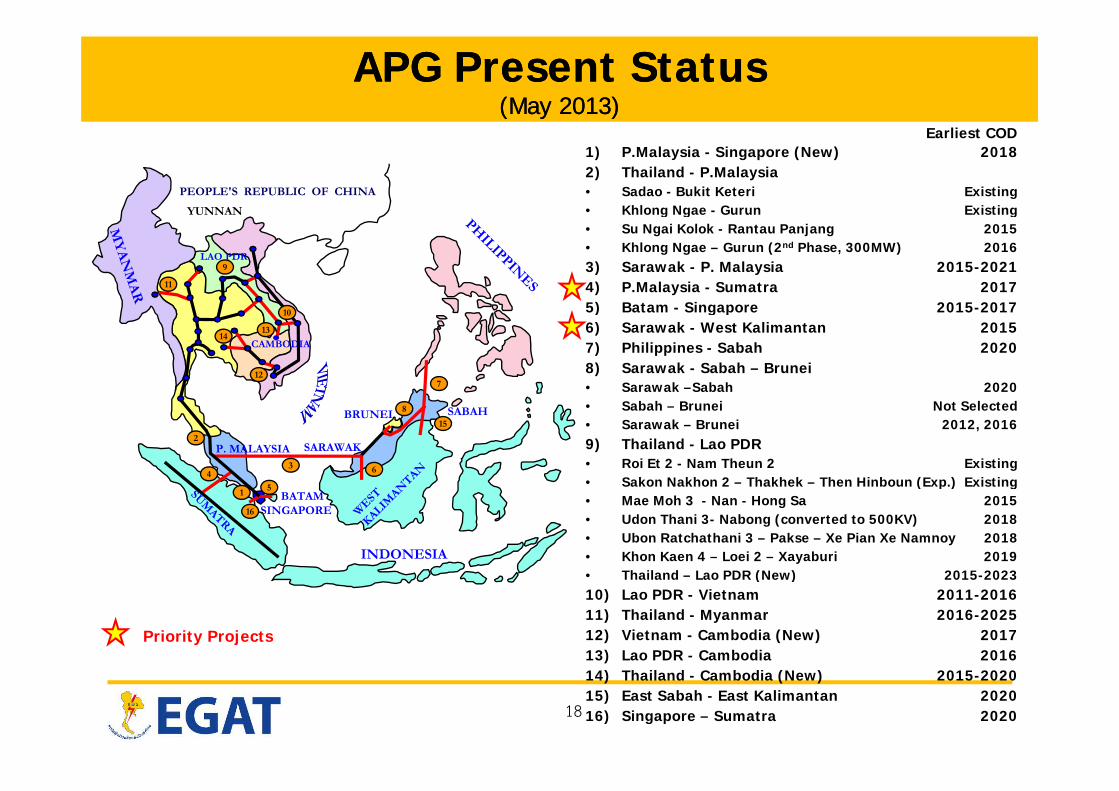

APG Present Status APG Present Status (May (May 20132013))

PEOPLE'S REPUBLIC OF CHINA

YUNNAN

Earliest COD1) P.Malaysia - Singapore (New) 20182) Thailand - P.Malaysia• Sadao - Bukit Keteri Existing• Khlong Ngae - Gurun Existing

11

9LAO PDR

g g g• Su Ngai Kolok - Rantau Panjang 2015• Khlong Ngae – Gurun (2nd Phase, 300MW) 20163) Sarawak - P. Malaysia 2015-20214) P.Malaysia - Sumatra 20175) Batam Singapore 2015 2017

CAMBODIA14

10

127

13

5) Batam - Singapore 2015-20176) Sarawak - West Kalimantan 20157) Philippines - Sabah 20208) Sarawak - Sabah – Brunei• Sarawak –Sabah 2020

SARAWAK

BRUNEI

P. MALAYSIA

8

643

2

5

15SABAH • Sabah – Brunei Not Selected

• Sarawak – Brunei 2012, 20169) Thailand - Lao PDR• Roi Et 2 - Nam Theun 2 Existing• Sakon Nakhon 2 – Thakhek – Then Hinboun (Exp.) Existing

INDONESIA

BATAMSINGAPORE

1 5

16

Sakon Nakhon 2 Thakhek Then Hinboun (Exp.) Existing• Mae Moh 3 - Nan - Hong Sa 2015• Udon Thani 3- Nabong (converted to 500KV) 2018• Ubon Ratchathani 3 – Pakse – Xe Pian Xe Namnoy 2018• Khon Kaen 4 – Loei 2 – Xayaburi 2019• Thailand – Lao PDR (New) 2015-2023

Priority Projects

• Thailand – Lao PDR (New) 2015-202310) Lao PDR - Vietnam 2011-201611) Thailand - Myanmar 2016-202512) Vietnam - Cambodia (New) 201713) Lao PDR - Cambodia 2016

18

14) Thailand - Cambodia (New) 2015-202015) East Sabah - East Kalimantan 202016) Singapore – Sumatra 2020

Existing APG Projects Existing APG Projects (May (May 20132013))

Project No. Interconnected Systems Capacity

(MW)

1 P.Malaysia – Singapore 450y g p

2 Thailand – P.Malaysia 380- Sadao – Bukit Keteri 80

- Khlong Ngae – Gurun 300

9 Thailand – Lao PDR 2,105- Nakhon Phanom - Thakhek - Theun Hinboun 214Nakhon Phanom Thakhek Theun Hinboun 214

- Ubon Ratchathani 2 – Houay Ho 126

- Roi Et 2 – Nam Theun 2 948

- Udon Thani 3 – Nabong – Nam Ngum 2 597

- Nakhon Phanom 2 - Thakhek - Theun Hinboun (Exp) 220

10 Lao PDR - Vietnam 24810 Lao PDR Vietnam 248

12 Vietnam – Cambodia 170

14 Thailand Cambodia 100

19

14 Thailand – Cambodia 100

APG Priority ProjectsAPG Priority Projects(May (May 20132013))

Project No. Interconnected Systems Capacity

(MW)

4 P.Malaysia – Sumatra (2017) 600- Melaka – Pekan Baru

6 West Kalimantan Sarawak (2015) 2306 West Kalimantan – Sarawak (2015) 230

20

ChallengesChallenges

Harmonization of common technical standards codes or guidelines in the areas of Planning and Design, System Operation and Maintenanceg g , y p

Harmonization of legal and regulatory framework for bilateral and cross-border power interconnection and trade

Functional area knowledge (skills, experiences)

Financing Modalities for funding sources to APG realizationg g

National Policy

Cooperation among ASEAN Energy Agency such as HAPUA ASCOPE AFOCCooperation among ASEAN Energy Agency such as HAPUA, ASCOPE, AFOC

High penetration of intermittent renewable energy sources

F el s bsidia (p ice disto tion)Fuel subsidiary (price distortion)

21

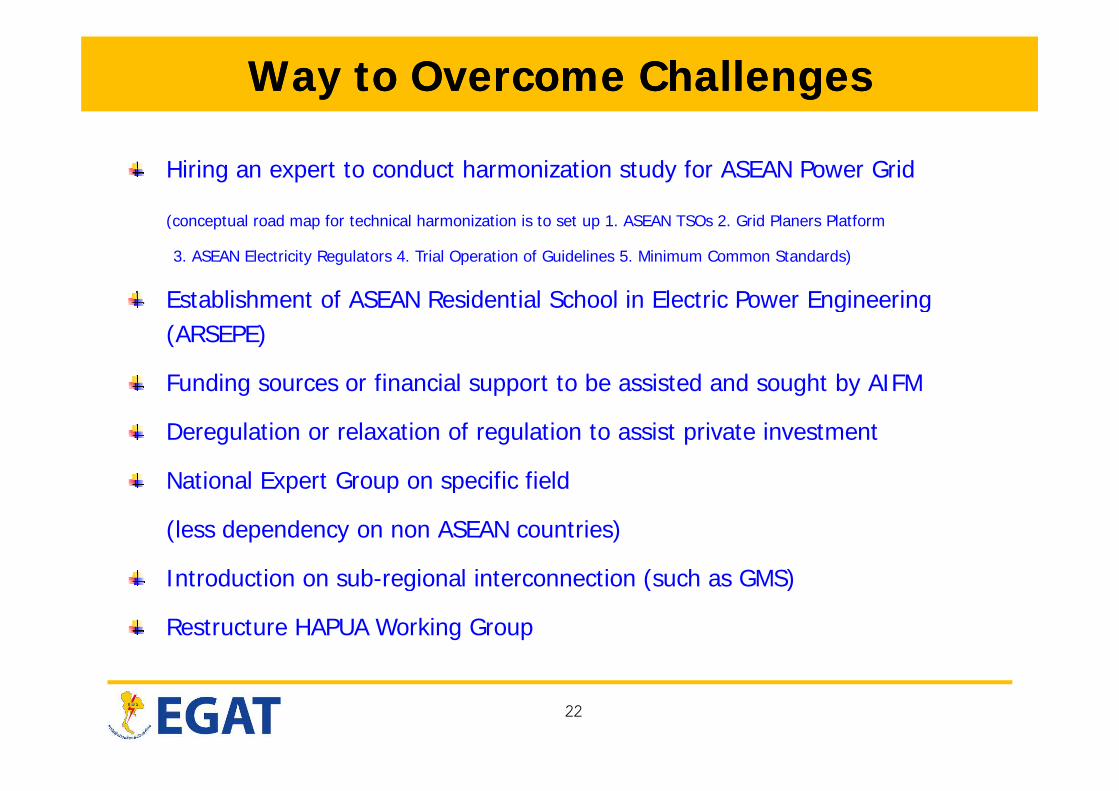

Way to Overcome ChallengesWay to Overcome Challenges

Hiring an expert to conduct harmonization study for ASEAN Power Grid

( t l d f t h i l h i ti i t t 1 ASEAN TSO 2 G id Pl Pl tf(conceptual road map for technical harmonization is to set up 1. ASEAN TSOs 2. Grid Planers Platform

3. ASEAN Electricity Regulators 4. Trial Operation of Guidelines 5. Minimum Common Standards)

Establishment of ASEAN Residential School in Electric Power EngineeringEstablishment of ASEAN Residential School in Electric Power Engineering (ARSEPE)

Funding sources or financial support to be assisted and sought by AIFM g pp g y

Deregulation or relaxation of regulation to assist private investment

National Expert Group on specific fieldNational Expert Group on specific field

(less dependency on non ASEAN countries)

Introduction on sub regional interconnection (such as GMS)Introduction on sub-regional interconnection (such as GMS)

Restructure HAPUA Working Group

22

2323กฟผ.