dr, reddy - betapharm

DESCRIPTION

Dr, Reddy - BetapharmTRANSCRIPT

Dr. Reddy - Betapharm

Deal Ya No Deal – Team 1

Pre- Deal

Deal

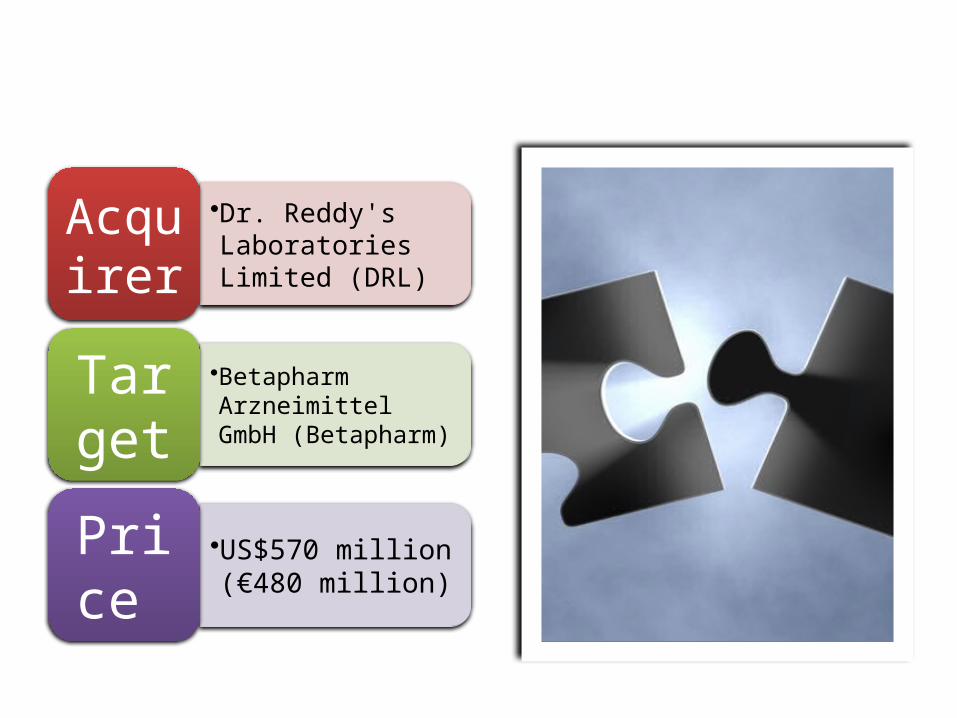

•Dr. Reddy's Laboratories Limited (DRL)

Acquirer

•Betapharm Arzneimittel GmbH (Betapharm)

Target

•US$570 million (€480 million)

Price

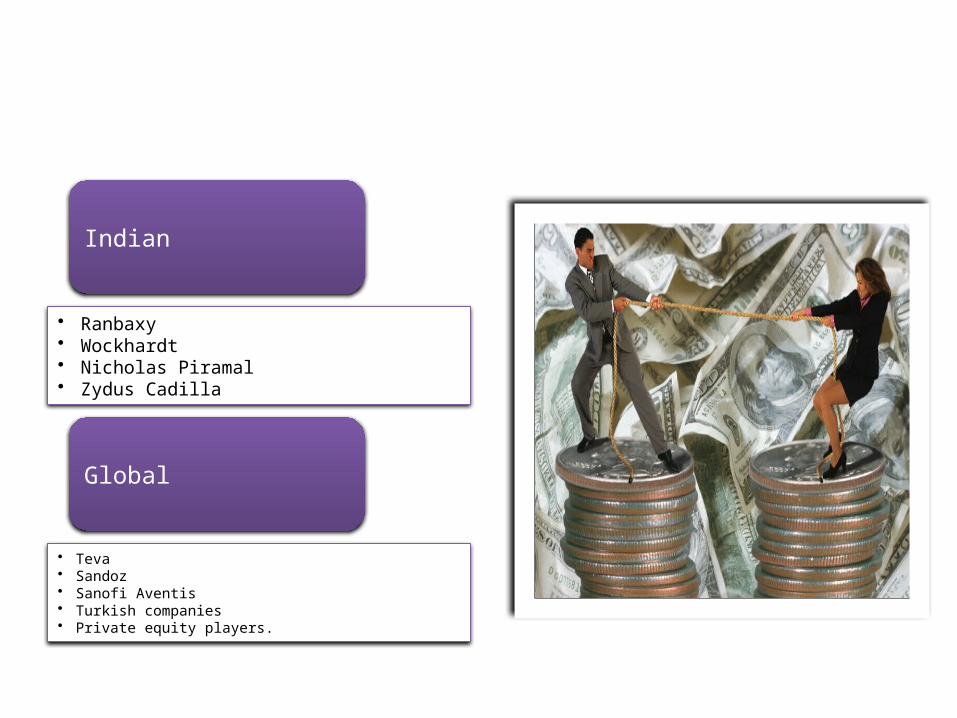

Other Bidders

Indian

• Ranbaxy• Wockhardt• Nicholas Piramal• Zydus Cadilla

Global

• Teva• Sandoz• Sanofi Aventis• Turkish companies• Private equity players.

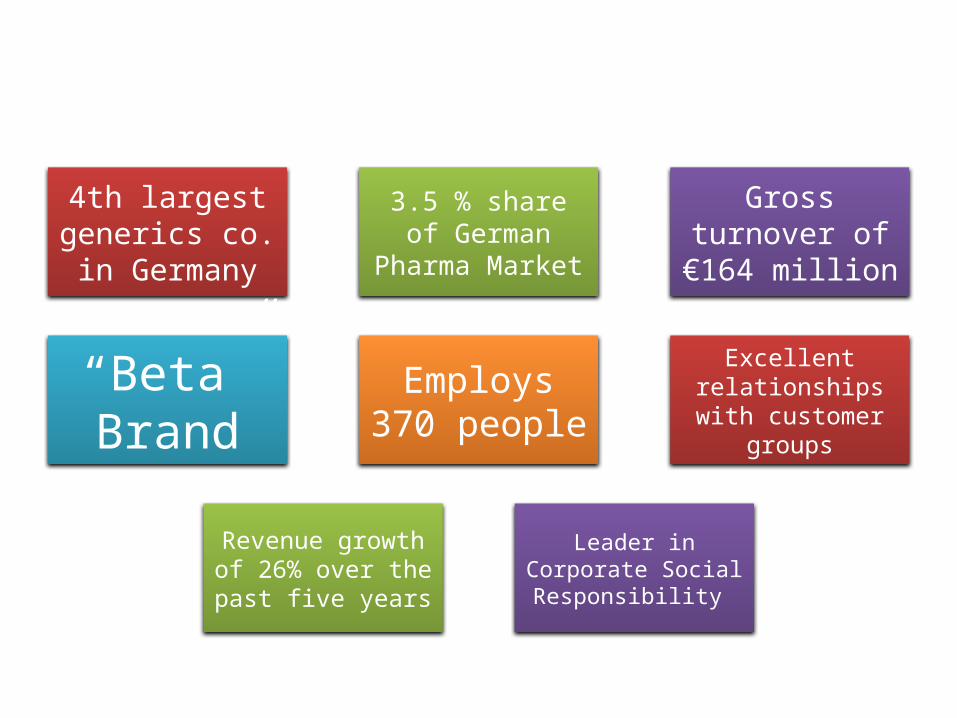

Betapharm

4th largest generics co. in Germany

3.5 % share of German

Pharma Market

Gross turnover of €164 million

“Beta” Brand

Employs 370 people

Excellent relationships

with customer groups

Revenue growth of 26% over the past five years

Leader in Corporate Social Responsibility

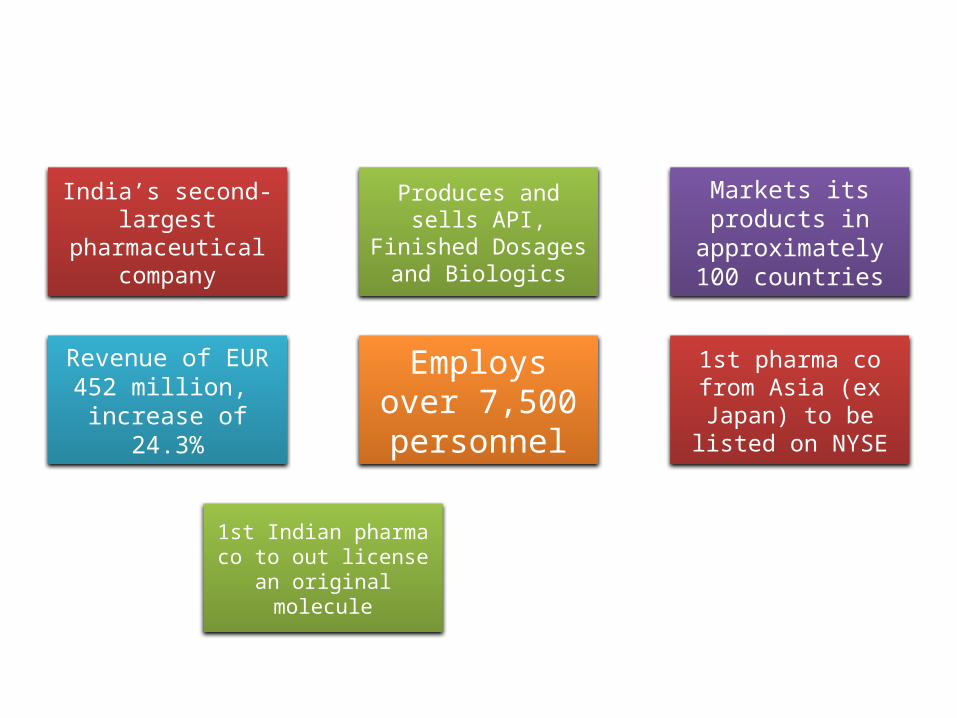

Dr. Reddy Labs

India’s second-largest

pharmaceutical company

Produces and sells API, Finished

Dosages and Biologics

Markets its products in

approximately 100 countries

Revenue of EUR 452 million, increase of

24.3%

Employs over 7,500 personnel

1st pharma co from Asia (ex Japan) to be

listed on NYSE

1st Indian pharma co to out

license an original molecule

Perfect Pharma Acquisition

Rationale

Limitations in India

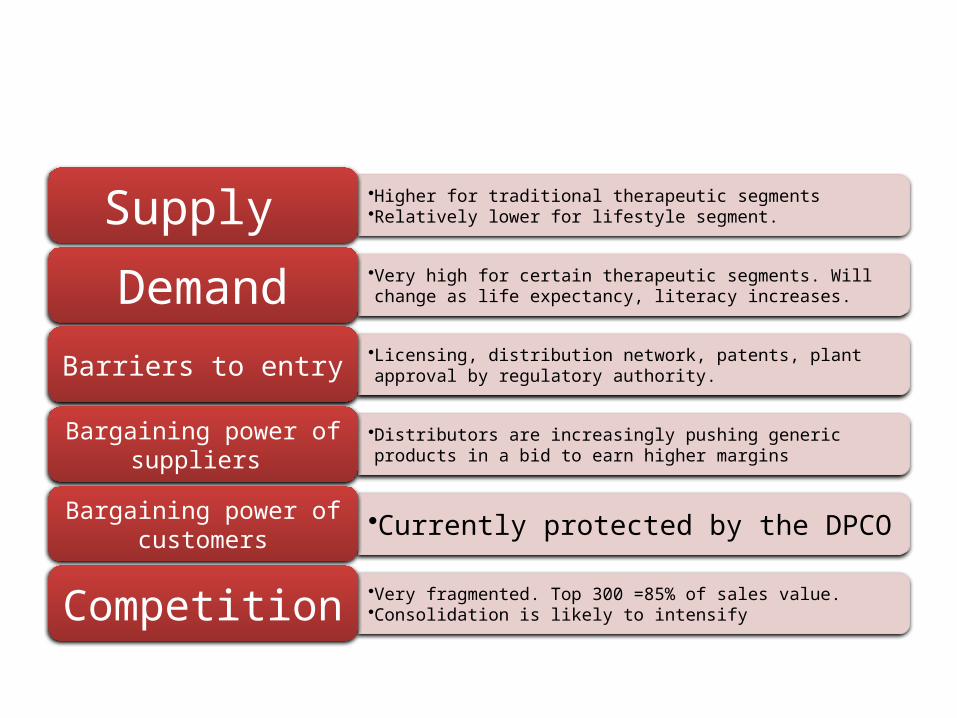

•Higher for traditional therapeutic segments•Relatively lower for lifestyle segment.Supply •Very high for certain therapeutic segments. Will change as life expectancy, literacy increases.Demand•Licensing, distribution network, patents, plant approval by regulatory authority.Barriers to entry

•Distributors are increasingly pushing generic products in a bid to earn higher margins

Bargaining power of suppliers

•Currently protected by the DPCOBargaining power of customers

•Very fragmented. Top 300 =85% of sales value. •Consolidation is likely to intensifyCompetition

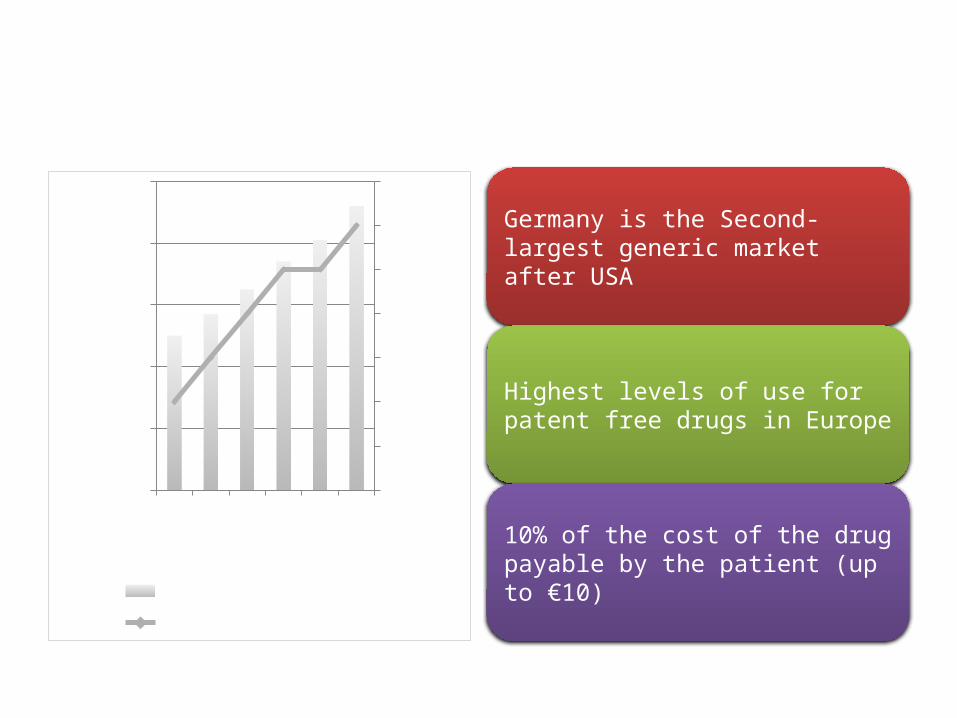

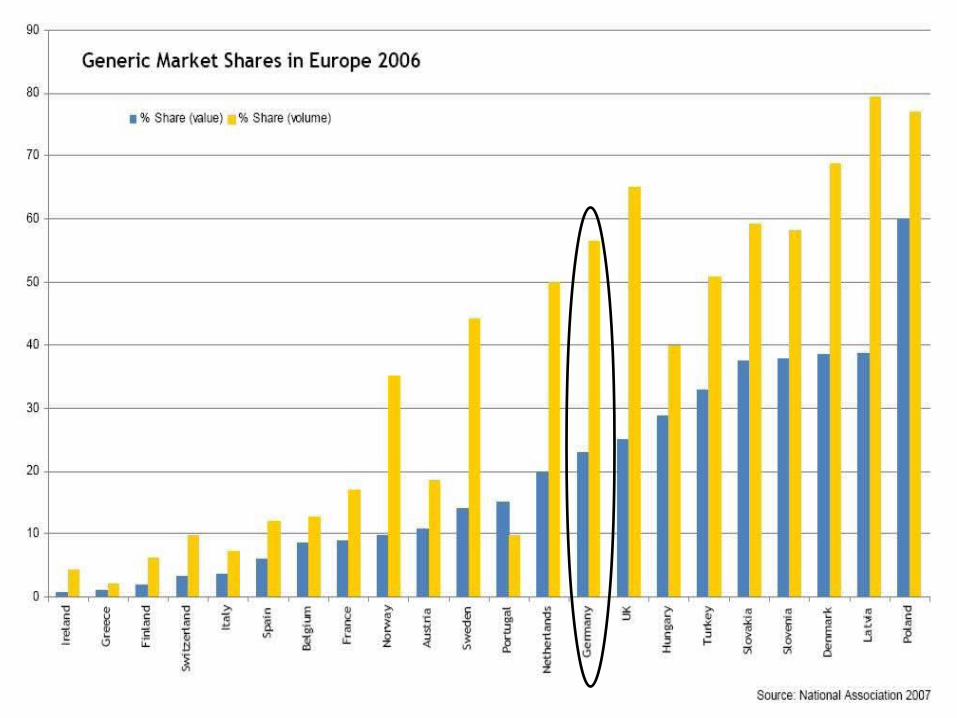

Access to the German Generics

Germany is the Second-largest generic market after USA

Highest levels of use for patent free drugs in Europe

10% of the cost of the drug payable by the patient (up to €10)

2001

2002

2003

2004

2005

2006

0

2

4

6

8

10

25

26

27

28

29

30

31

32

Gernerics (USD Bn)Penetration %

Gen

eri

cs

Pen

etr

ati

on

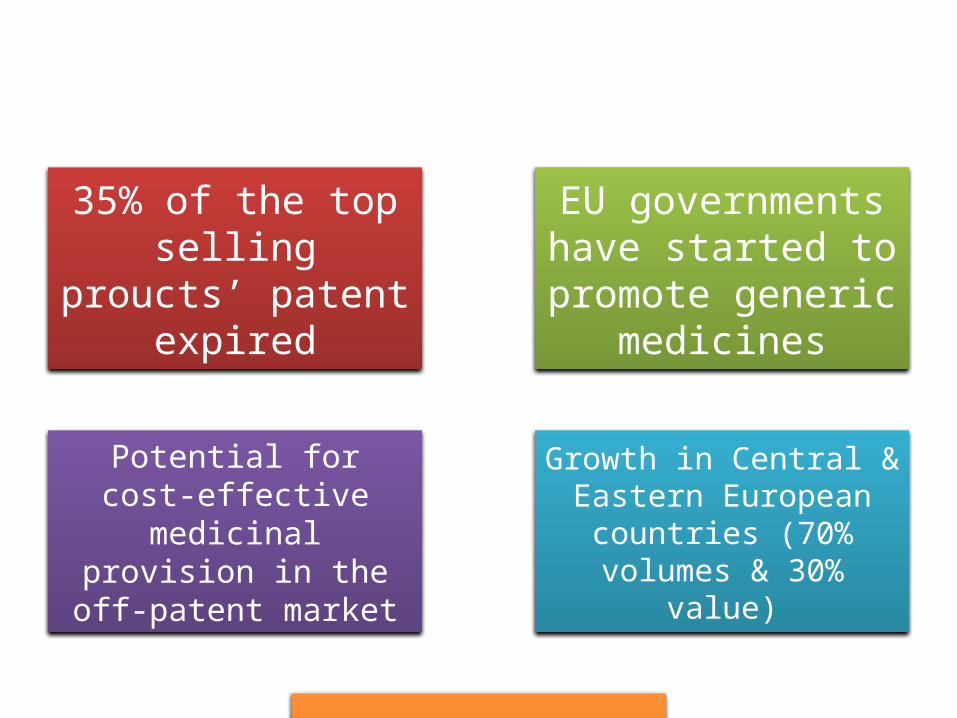

Strategic presence in the Europe

35% of the top selling proucts’ patent expired

EU governments have started to promote generic

medicines

Potential for cost-effective medicinal

provision in the off-patent market

Growth in Central & Eastern European

countries (70% volumes & 30%

value)

Availability of affordable generic medicines is major budgetary factor

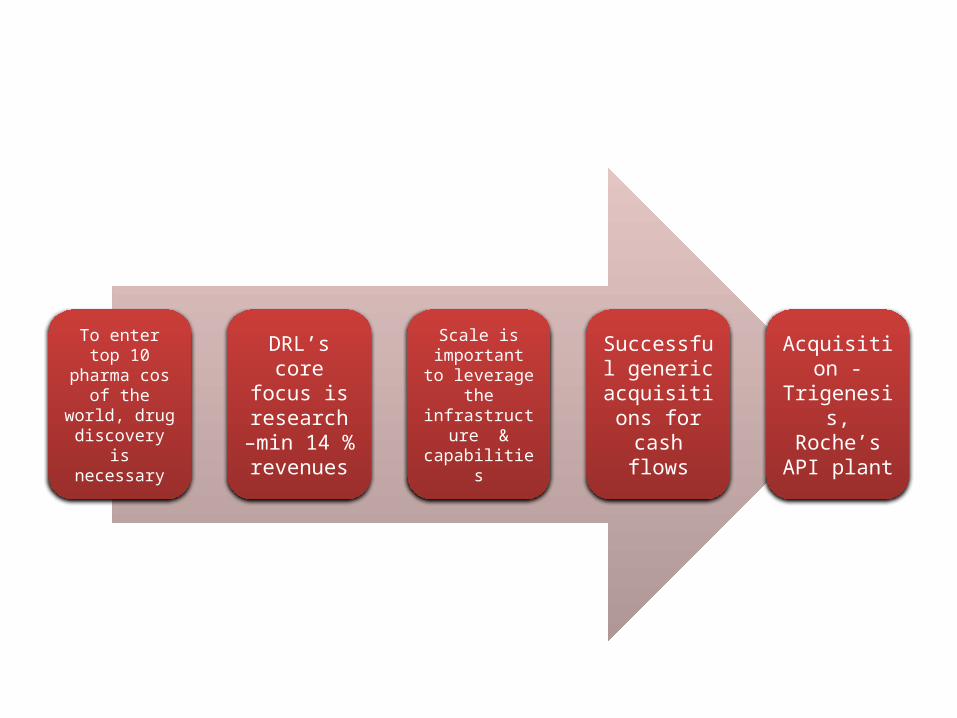

De Risking Drug discovery

To enter top 10 pharma cos of the

world, drug discovery is necessary

DRL’s core focus is

research –min 14 % revenues

Scale is important

to leverage the

infrastructure &

capabilities

Successful generic acquisitio

ns for cash flows

Acquisition -

Trigenesis,

Roche’s API plant

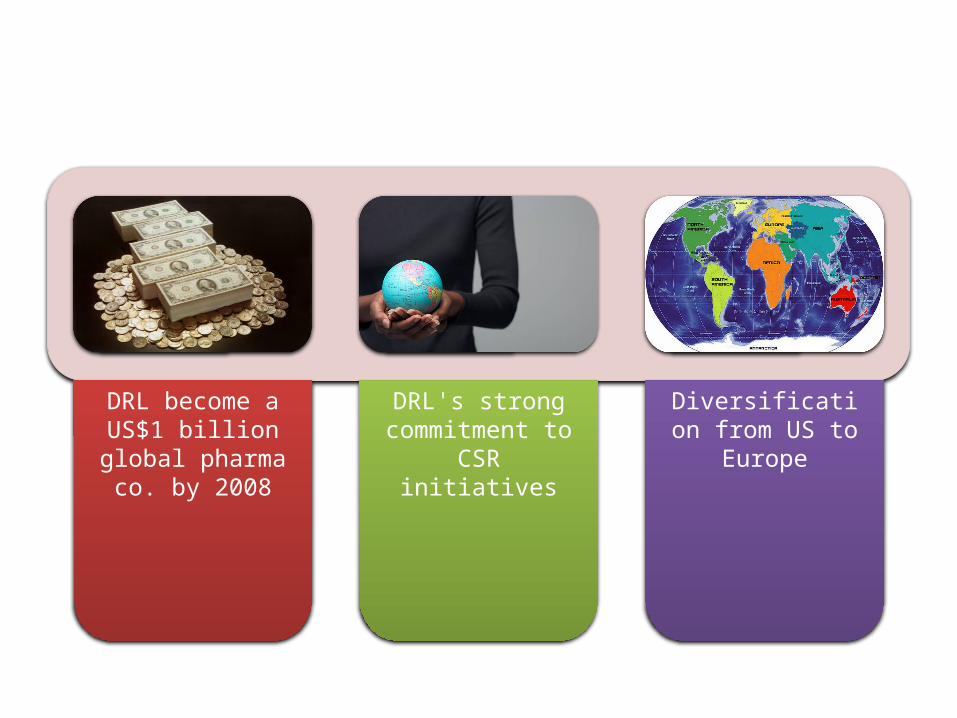

Miscellaneous

DRL become a US$1 billion

global pharma co. by 2008

DRL's strong commitment to CSR initiatives

Diversification from US to

Europe

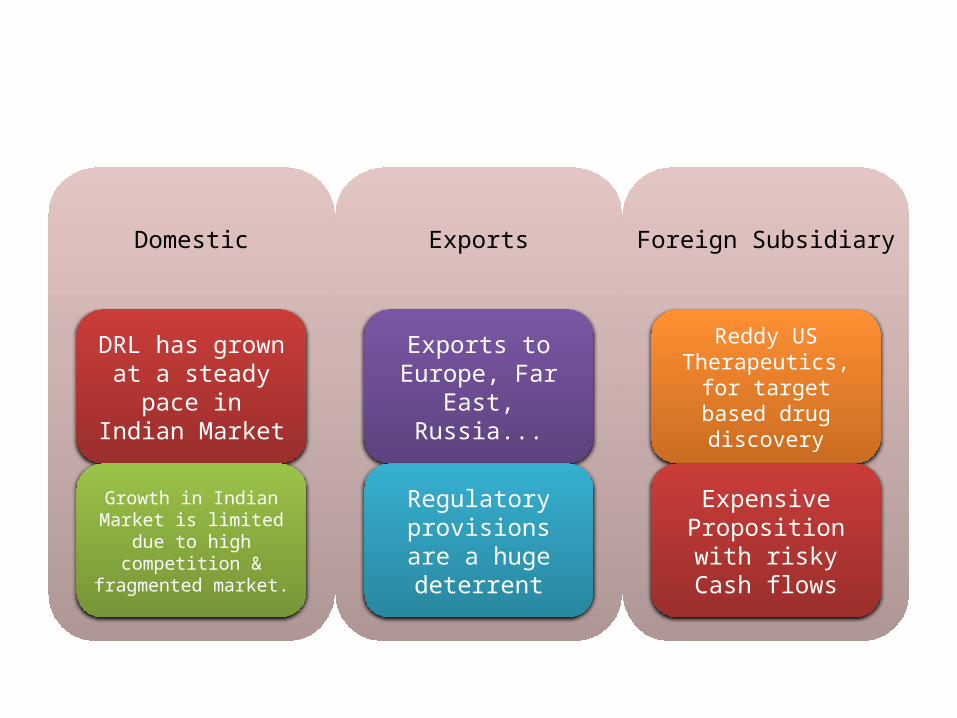

Options

Organic

Domestic

DRL has grown at a steady

pace in Indian Market

Growth in Indian Market is limited

due to high competition &

fragmented market.

Exports

Exports to Europe, Far

East, Russia...

Regulatory provisions are a huge deterrent

Foreign Subsidiary

Reddy US Therapeutics,

for target based drug discovery

Expensive Proposition with risky Cash flows

Inorganic

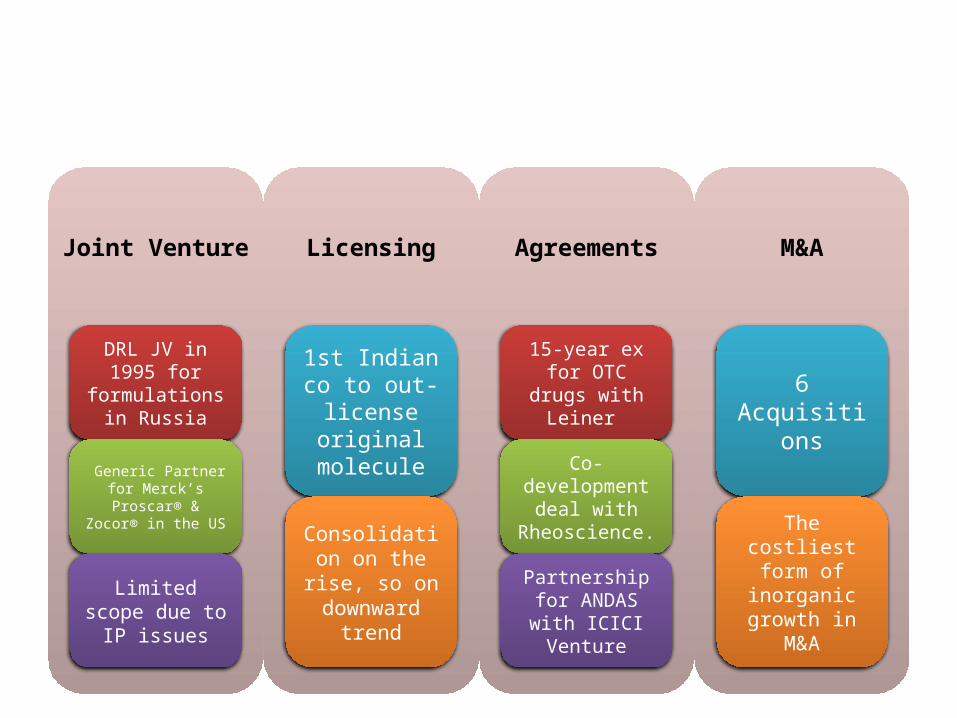

Joint Venture

DRL JV in 1995 for

formulations in Russia

Generic Partner for Merck’s Proscar® &

Zocor® in the US

Limited scope due to IP issues

Licensing

1st Indian co to out-

license original

molecule

Consolidation on the rise, so on downward

trend

Agreements

15-year ex for OTC drugs with Leiner

Co-development

deal with Rheoscience.

Partnership for ANDAS with ICICI Venture

M&A

6 Acquisition

s

The costliest form of

inorganic growth in

M&A

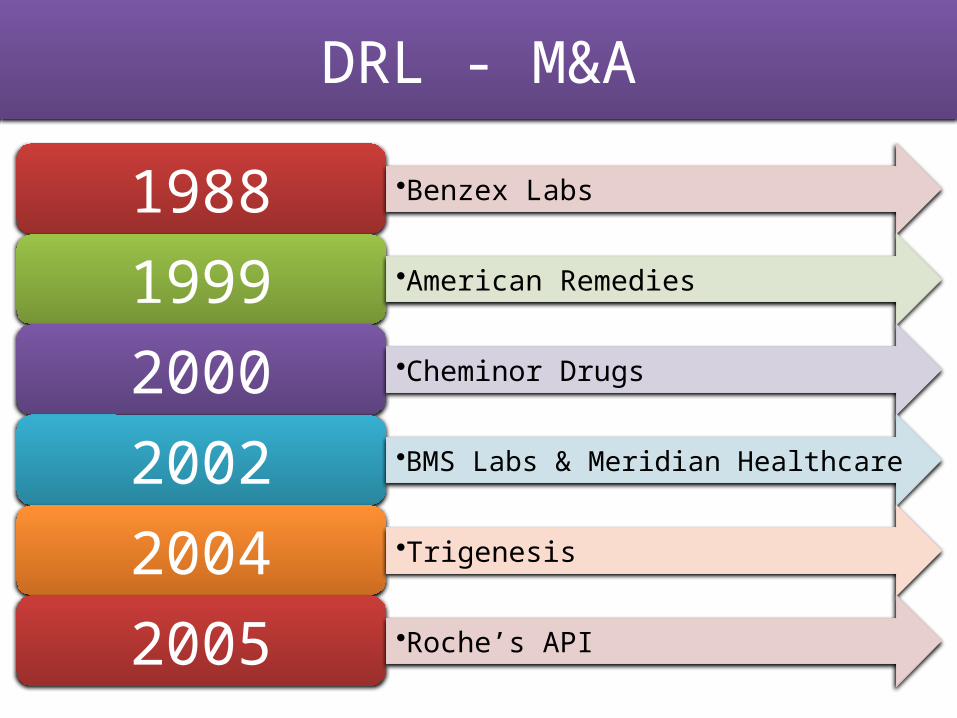

DRL - M&A

1988 •Benzex Labs

1999 •American Remedies

2000 •Cheminor Drugs

2002 •BMS Labs & Meridian Healthcare

2004 •Trigenesis

2005 •Roche’s API

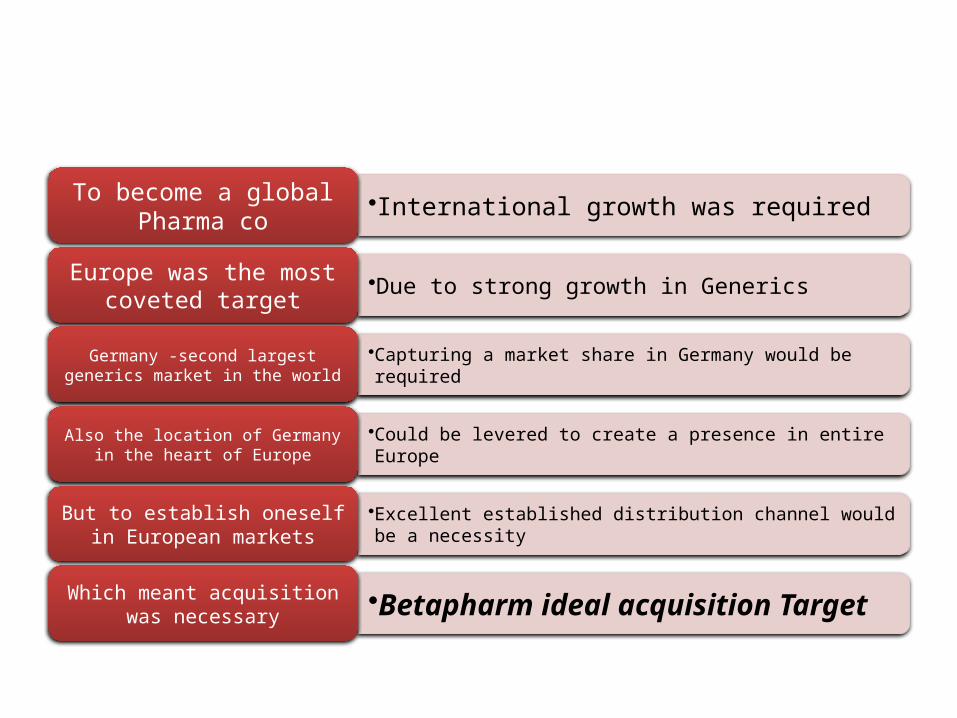

Betapharm – Ideal Acquisition

•International growth was requiredTo become a global Pharma co

•Due to strong growth in GenericsEurope was the most coveted target

•Capturing a market share in Germany would be required

Germany -second largest generics market in the world

•Could be levered to create a presence in entire EuropeAlso the location of Germany

in the heart of Europe

•Excellent established distribution channel would be a necessity

But to establish oneself in European markets

•Betapharm ideal acquisition TargetWhich meant acquisition

was necessary

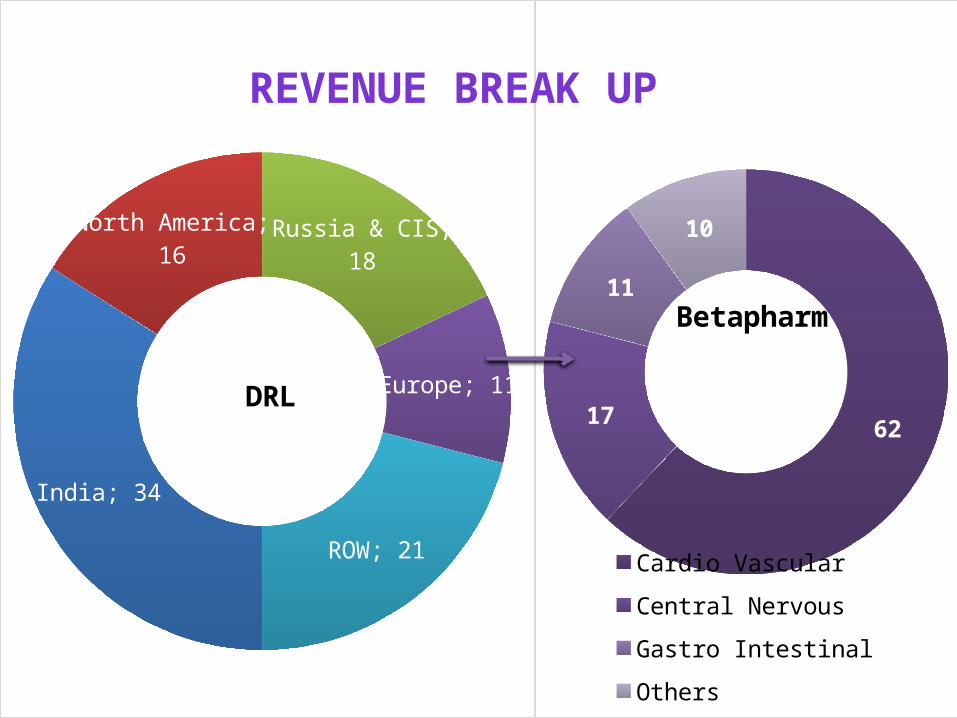

India; 34

North America; 16

Russia & CIS; 18

Europe; 11

ROW; 21

DRL6217

11

10

Betapharm

Cardio Vascular

Central Nervous

Gastro Intestinal

Others

REVENUE BREAK UP

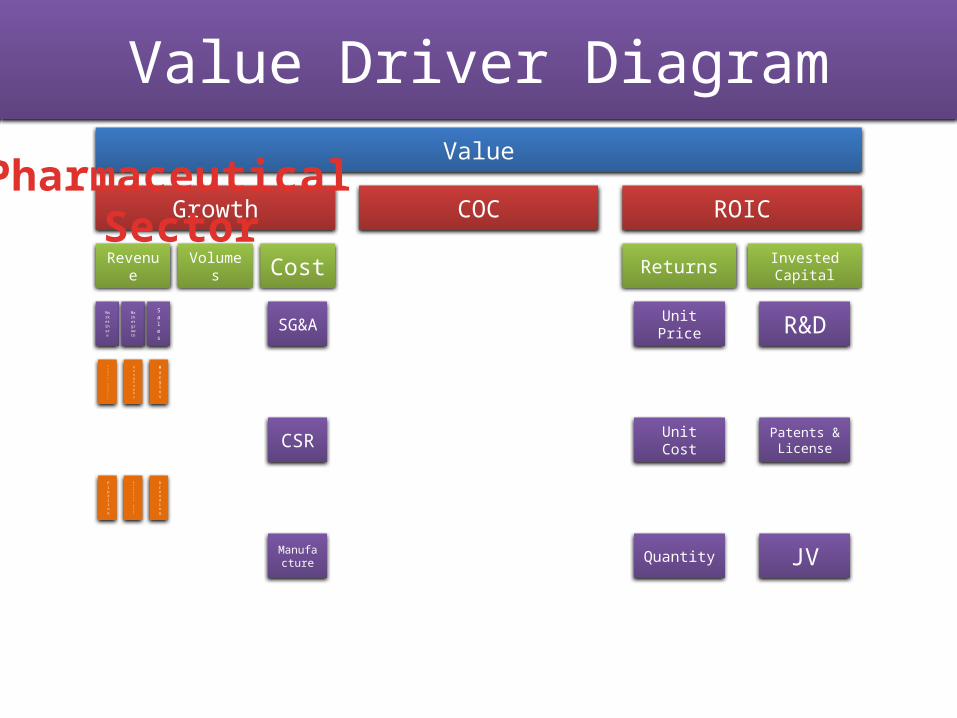

Value Driver DiagramValue

Growth

Revenue

Market Share

Product Quality

Pipeline

Market growth

Geography

Business Unit

Sales

Margins

Branding

Volumes Cost

SG&A

CSR

Manufacture

COC ROIC

Returns

Unit Price

Unit Cost

Quantity

Invested Capital

R&D

Patents & License

JV

Pharmaceutical Sector

Valuation

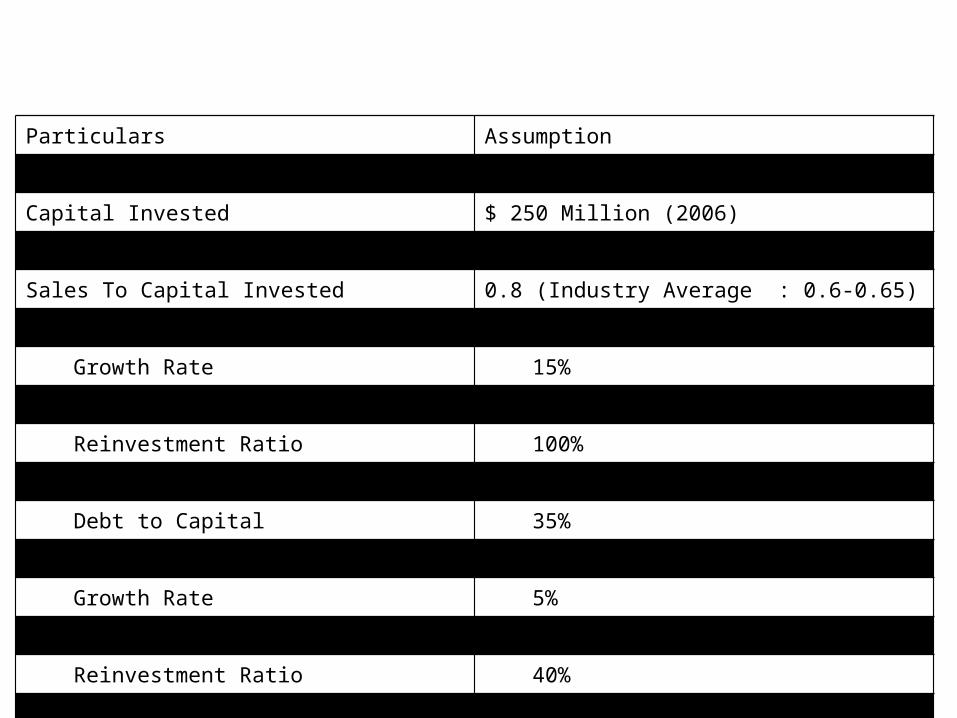

DCF Valuation - Base CaseParticulars Assumption

Revenue $ 200 Million (2006)

Capital Invested $ 250 Million (2006)

German Corporate Tax Rate 30% (Marginal)

Sales To Capital Invested 0.8 (Industry Average : 0.6-0.65)

High Growth Period 5 years

Growth Rate 15%

EBIT Margin 25%

Reinvestment Ratio 100%

ROIC 15%

Debt to Capital 35%

Stable Period Perpetuity

Growth Rate 5%

EBIT Margin 18%

Reinvestment Ratio 40%

ROIC 12%

Debt to Capital 35%

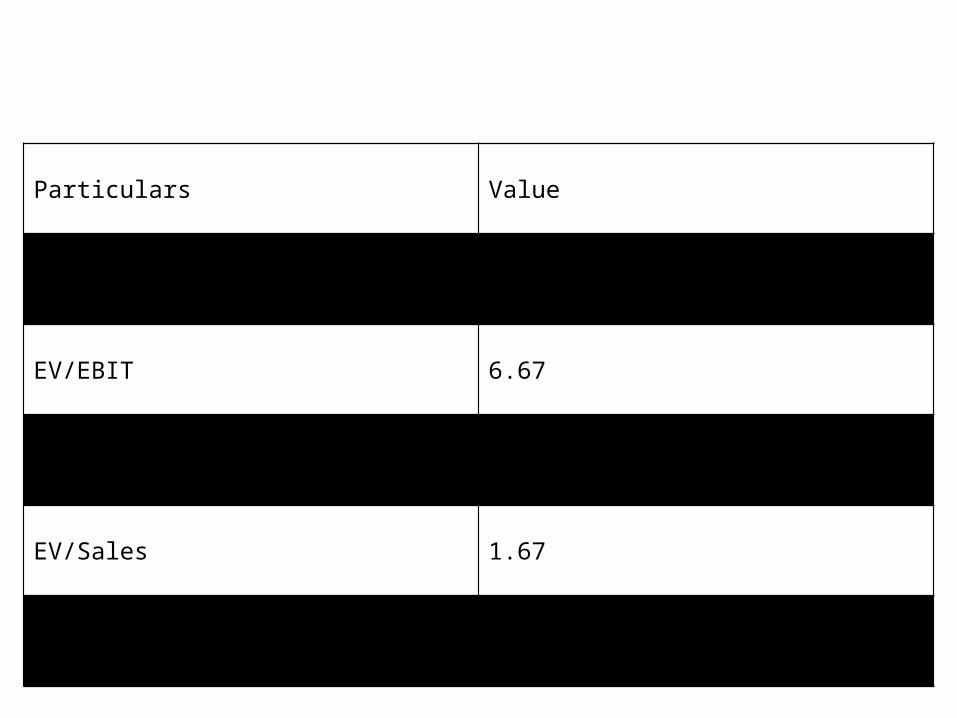

Valuation - Base Case

Particulars Value

Enterprise Value (EV) $ 333.52 Million

EV/EBIT 6.67

EV/EBIT(1-t) 9.53

EV/Sales 1.67

EV/Capital Invested 1.33

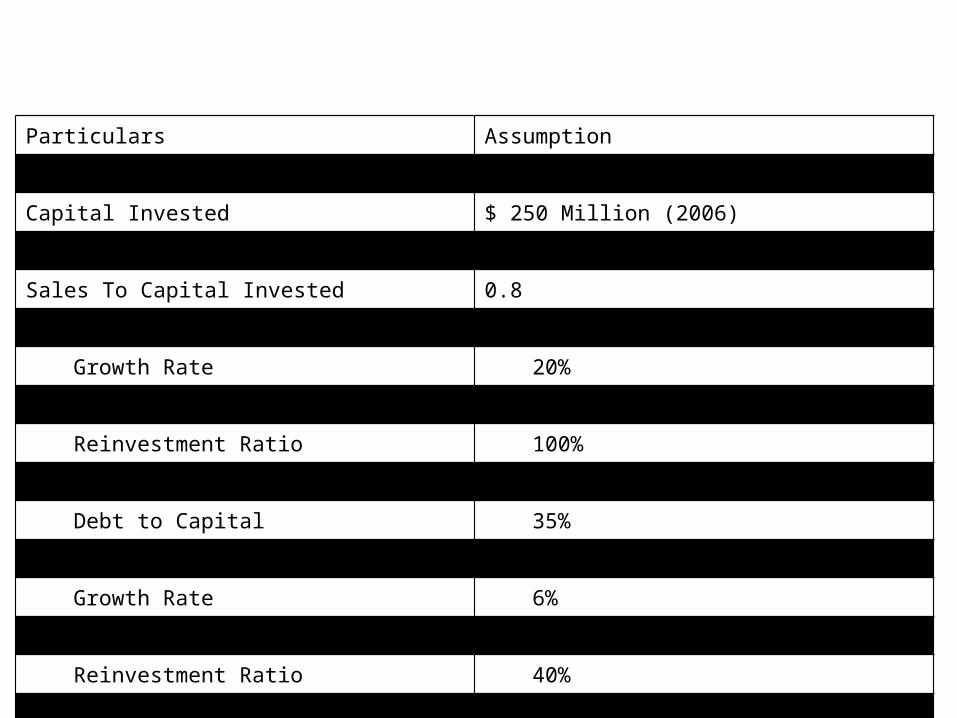

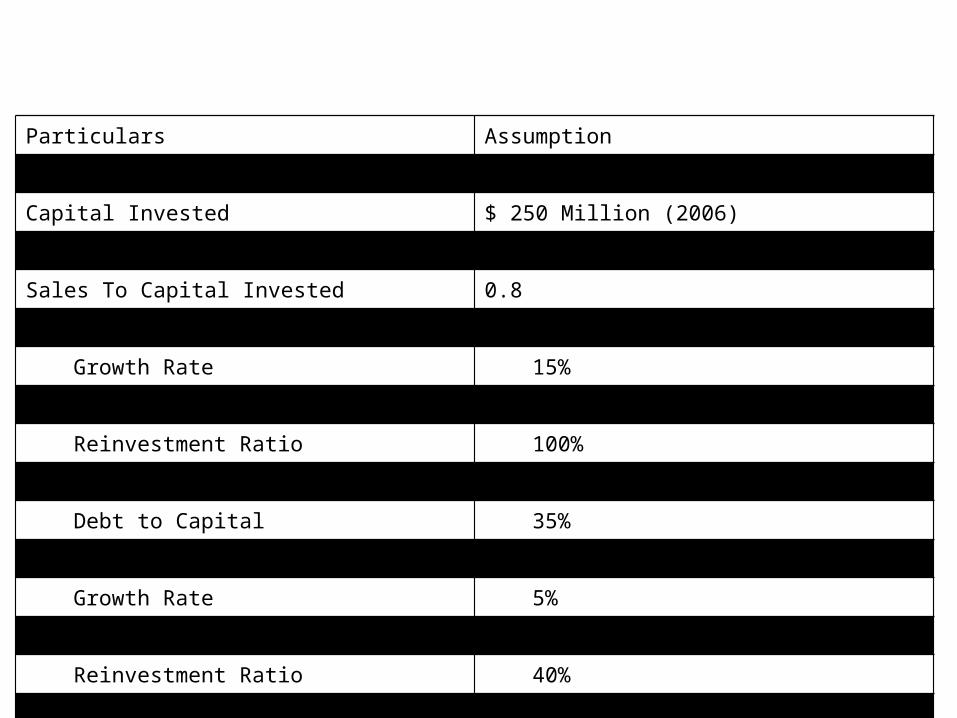

Scenario 1 - OptimisticParticulars Assumption

Revenue $ 200 Million (2006)

Capital Invested $ 250 Million (2006)

German Corporate Tax Rate 30% (Marginal)

Sales To Capital Invested 0.8

High Growth Period 8 years

Growth Rate 20%

EBIT Margin 25%

Reinvestment Ratio 100%

ROIC 20%

Debt to Capital 35%

Stable Period Perpetuity

Growth Rate 6%

EBIT Margin 20%

Reinvestment Ratio 40%

ROIC 15%

Debt to Capital 35%

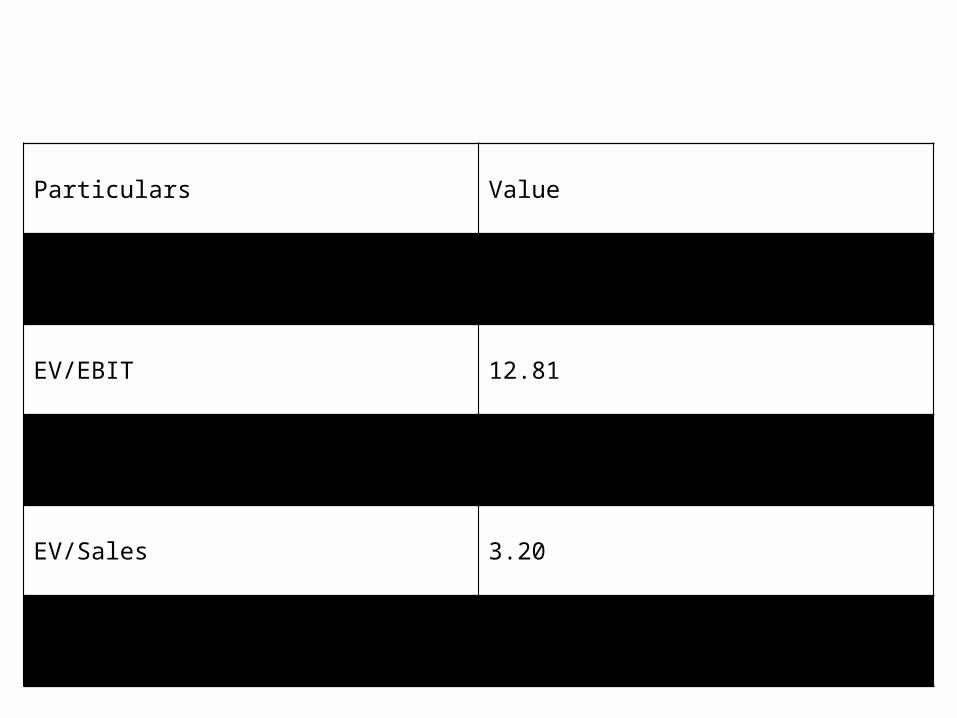

Valuation - Optimistic

Particulars Value

Enterprise Value (EV) $ 640.47 Million

EV/EBIT 12.81

EV/EBIT(1-t) 18.30

EV/Sales 3.20

EV/Capital Invested 3.66

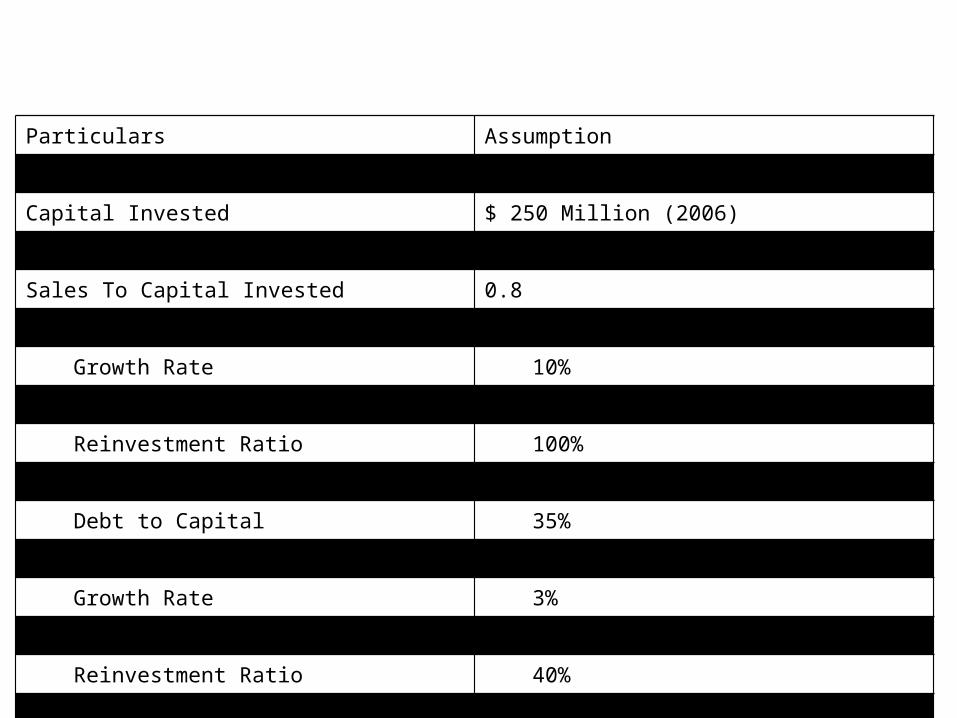

Scenario 2 - PessimisticParticulars Assumption

Revenue $ 200 Million (2006)

Capital Invested $ 250 Million (2006)

German Corporate Tax Rate 30% (Marginal)

Sales To Capital Invested 0.8

High Growth Period 5 years

Growth Rate 15%

EBIT Margin 15%

Reinvestment Ratio 100%

ROIC 10%

Debt to Capital 35%

Stable Period Perpetuity

Growth Rate 5%

EBIT Margin 15%

Reinvestment Ratio 40%

ROIC 8%

Debt to Capital 35%

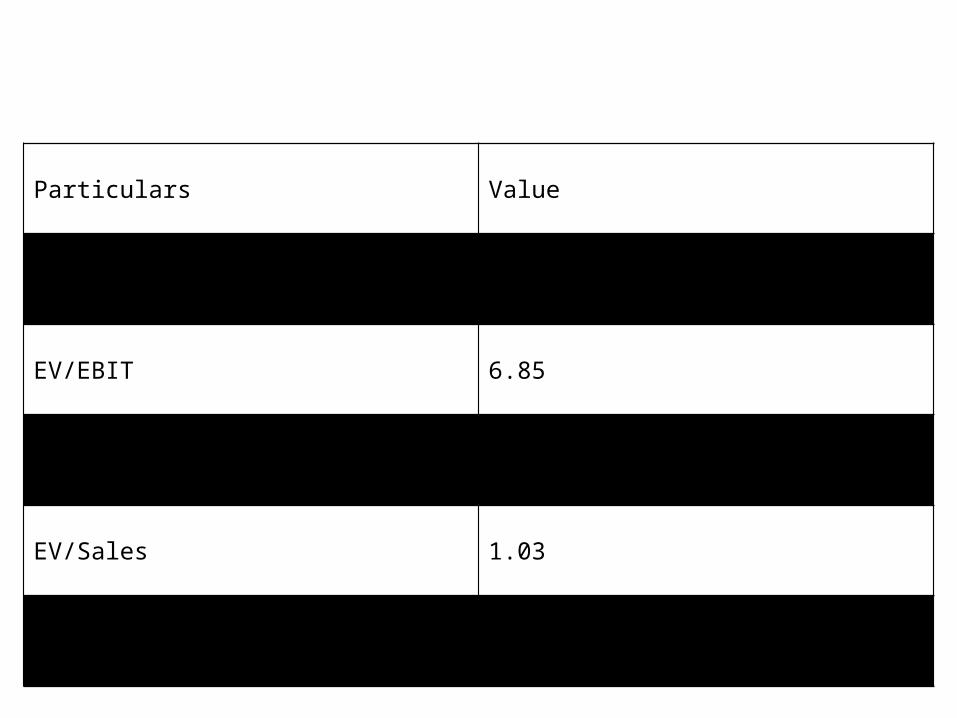

Valuation - Pessimistic

Particulars Value

Enterprise Value (EV) $ 205.52 Million

EV/EBIT 6.85

EV/EBIT(1-t) 9.79

EV/Sales 1.03

EV/Capital Invested 0.82

Scenario 3 - Worst CaseParticulars Assumption

Revenue $ 200 Million (2006)

Capital Invested $ 250 Million (2006)

German Corporate Tax Rate 30% (Marginal)

Sales To Capital Invested 0.8

High Growth Period 5 years

Growth Rate 10%

EBIT Margin 15%

Reinvestment Ratio 100%

ROIC 8%

Debt to Capital 35%

Stable Period Perpetuity

Growth Rate 3%

EBIT Margin 15%

Reinvestment Ratio 40%

ROIC 6.5%

Debt to Capital 35%

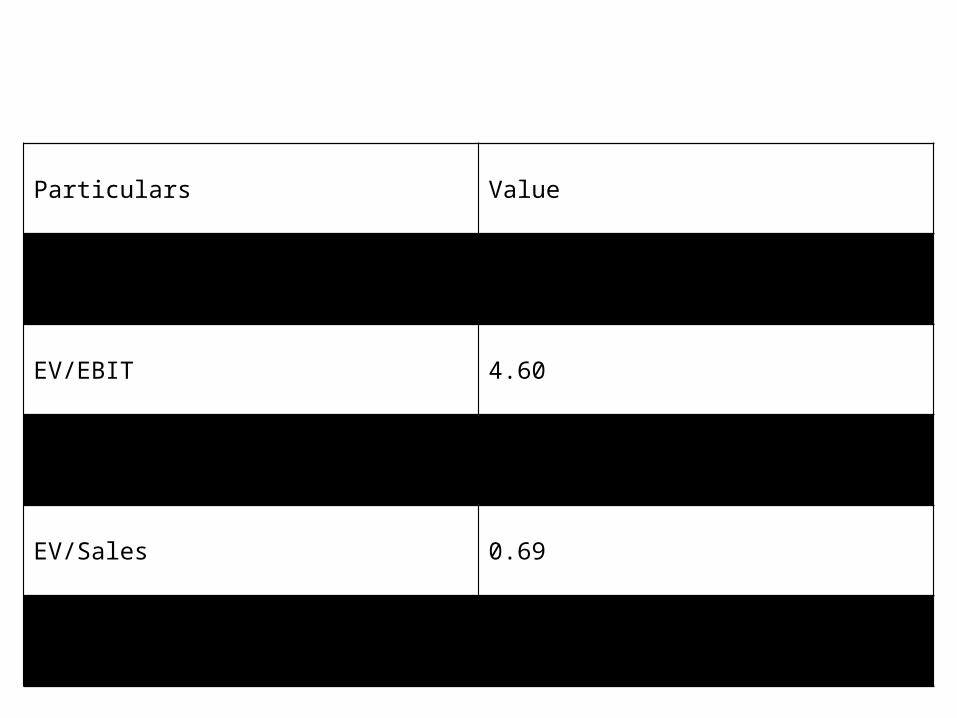

Valuation - Worst Case

Particulars Value

Enterprise Value (EV) $ 138.53 Million

EV/EBIT 4.60

EV/EBIT(1-t) 6.61

EV/Sales 0.69

EV/Capital Invested 0.55

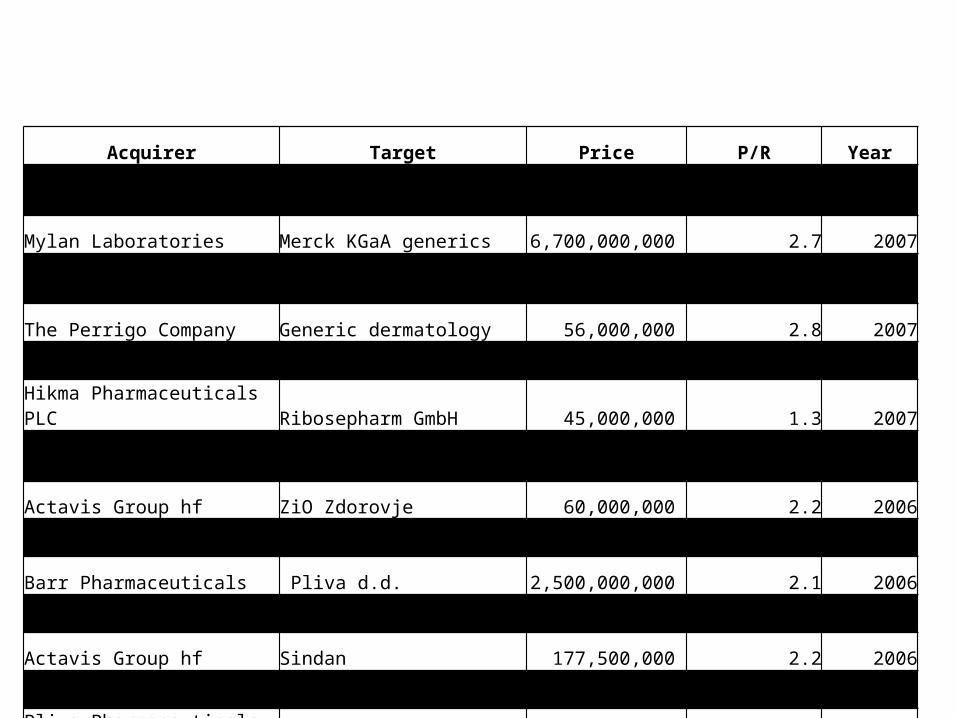

Comparable TransactionsAcquirer Target Price P/R Year

Sun Pharmaceutical Industries Taro 454,000,000 1.5 2007

Mylan Laboratories Merck KGaA generics 6,700,000,000 2.7 2007

Ranbaxy Laboratories. Be-Tabs Pharmaceuticals 70,000,000 2.2 2007

The Perrigo Company Generic dermatology 56,000,000 2.8 2007

Zentiva NV Eczacibisi Generic 606,200,000 2.4 2007Hikma Pharmaceuticals PLC Ribosepharm GmbH 45,000,000 1.3 2007

Actavis Group hfAbrika Pharmaceuticals, Inc. 225,000,000 8.7 2006

Actavis Group hf ZiO Zdorovje 60,000,000 2.2 2006

Dava Pharmaceuticals Stada, Inc. 40,000,000 0.8 2006

Barr Pharmaceuticals Pliva d.d. 2,500,000,000 2.1 2006

Ranbaxy Laboratories. Terapia S.A. 324,000,000 4.1 2006

Actavis Group hf Sindan 177,500,000 2.2 2006

Watson Pharmaceuticals Andrx Corporation 1,900,000,000 1.7 2006

Pliva Pharmaceuticals d.d Uso Racional 25,640,000 1.8 2006

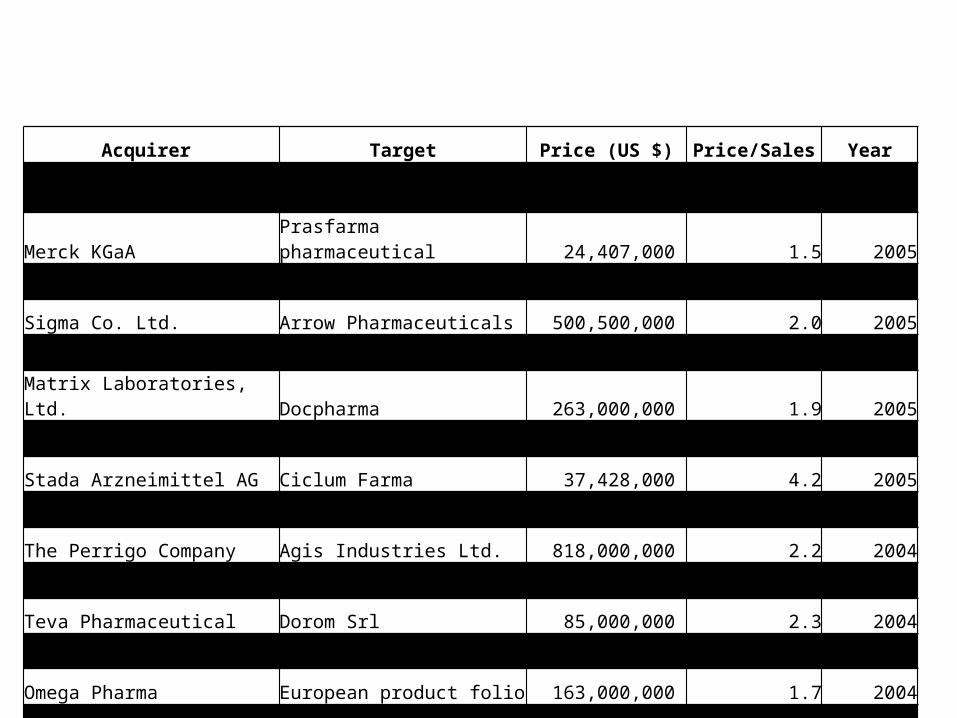

Comparable TransactionsAcquirer Target Price (US $) Price/Sales Year

Actavis Group hf Global generics business 810,000,000 1.1 2005

Merck KGaA Prasfarma pharmaceutical 24,407,000 1.5 2005

Zentiva NV SC Sicomed SA 102,000,000 1.4 2005

Sigma Co. Ltd. Arrow Pharmaceuticals 500,500,000 2.0 2005

Teva Pharmaceutical Ivax Corporation 7,960,000,000 4.2 2005

Matrix Laboratories, Ltd. Docpharma 263,000,000 1.9 2005

Actavis Group hf Amide Pharmaceutical, 600,000,000 5.6 2005

Stada Arzneimittel AG Ciclum Farma 37,428,000 4.2 2005

Novartis AG Two generic companies 8,400,000,000 3.9 2005

The Perrigo Company Agis Industries Ltd. 818,000,000 2.2 2004

Merck KGaA NM Pharma 65,000,000 1.4 2004

Teva Pharmaceutical Dorom Srl 85,000,000 2.3 2004

Novartis AG Sabex Holding, Inc. 565,000,000 6.3 2004

Omega Pharma European product folio 163,000,000 1.7 2004

3i Group Plc betapharm Arzneimittel 366,000,000 2.8 2004

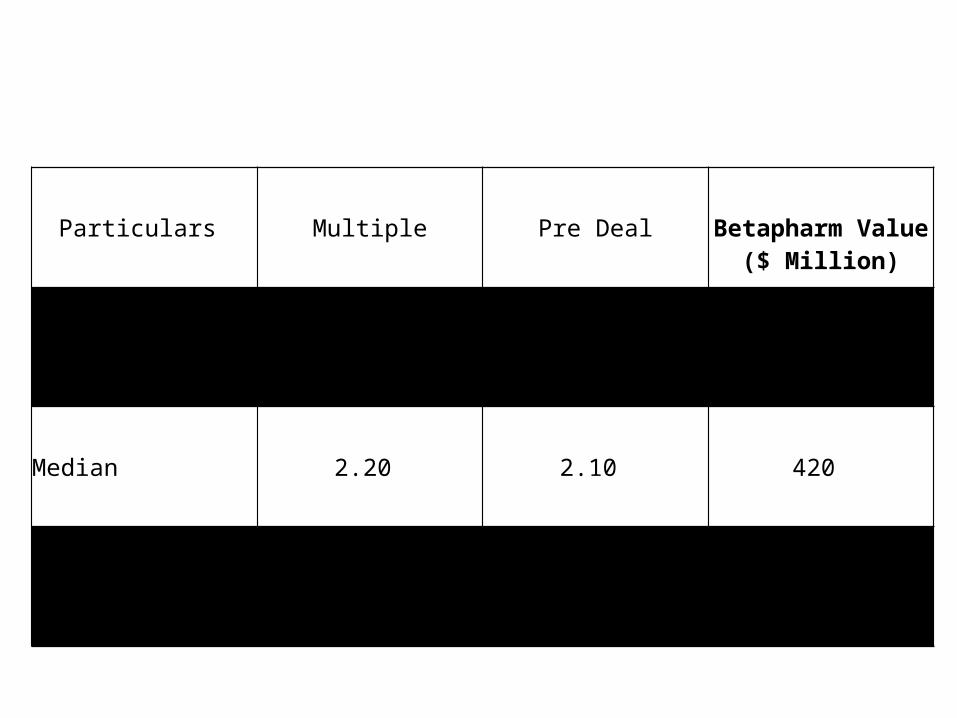

Valuation - Comparable Deals

Particulars Multiple Pre Deal Betapharm Value

($ Million)

Mean 2.73 2.77 554

Median 2.20 2.10 420

Harmonic Mean 2.08 2.14 427

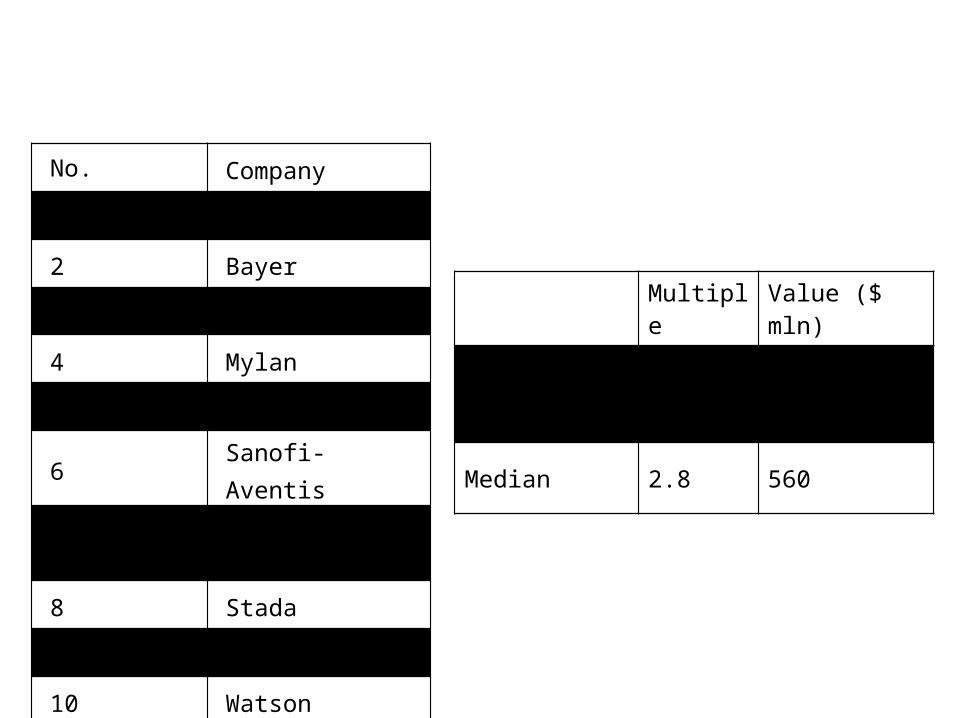

Comparable Multiples

No. Company

1 Barr

2 Bayer

3 Merck

4 Mylan

5 Novartis

6 Sanofi-Aventis

7Schering Plough

8 Stada

9 Teva

10 Watson

Multiple Value ($ mln)

Harmonic Mean 2.9 581

Median 2.8 560

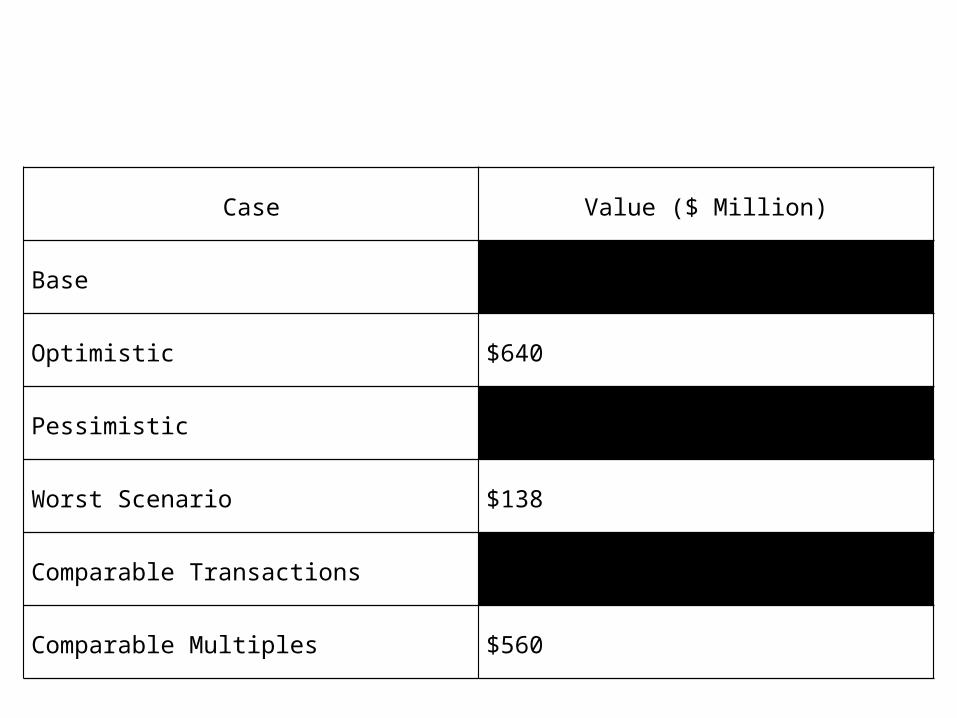

Valuation - Summary

Case Value ($ Million)

Base $333

Optimistic $640

Pessimistic $205

Worst Scenario $138

Comparable Transactions $420

Comparable Multiples $560

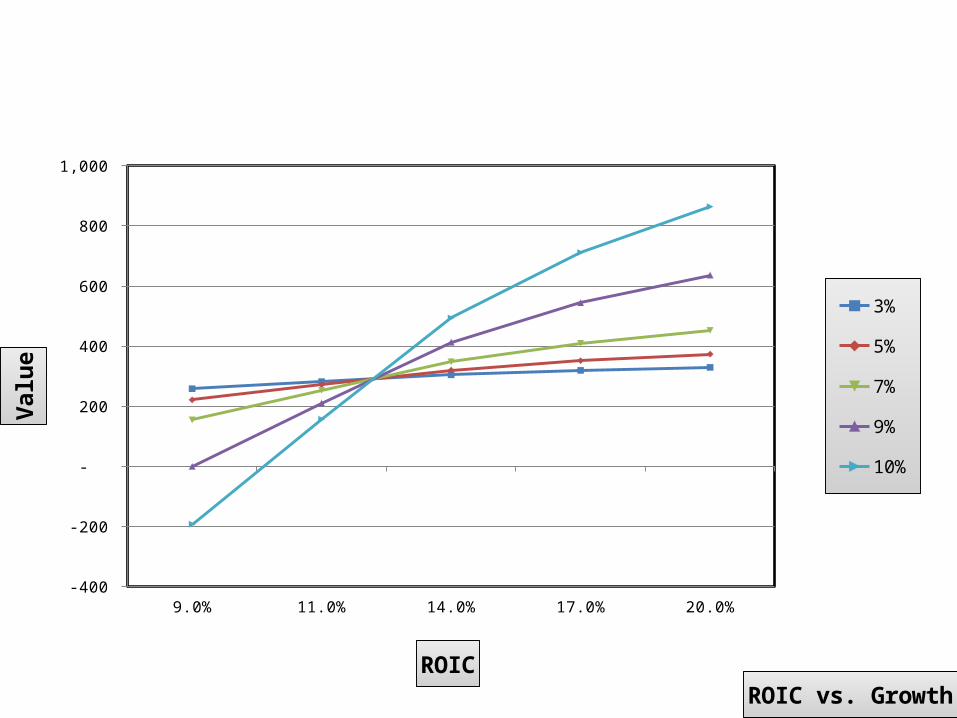

Sensitivity Analysis

9.0% 11.0% 14.0% 17.0% 20.0%-400

-200

-

200

400

600

800

1,000

ROIC vs. Growth

3%

5%

7%

9%

10%

ROIC

Valu

e

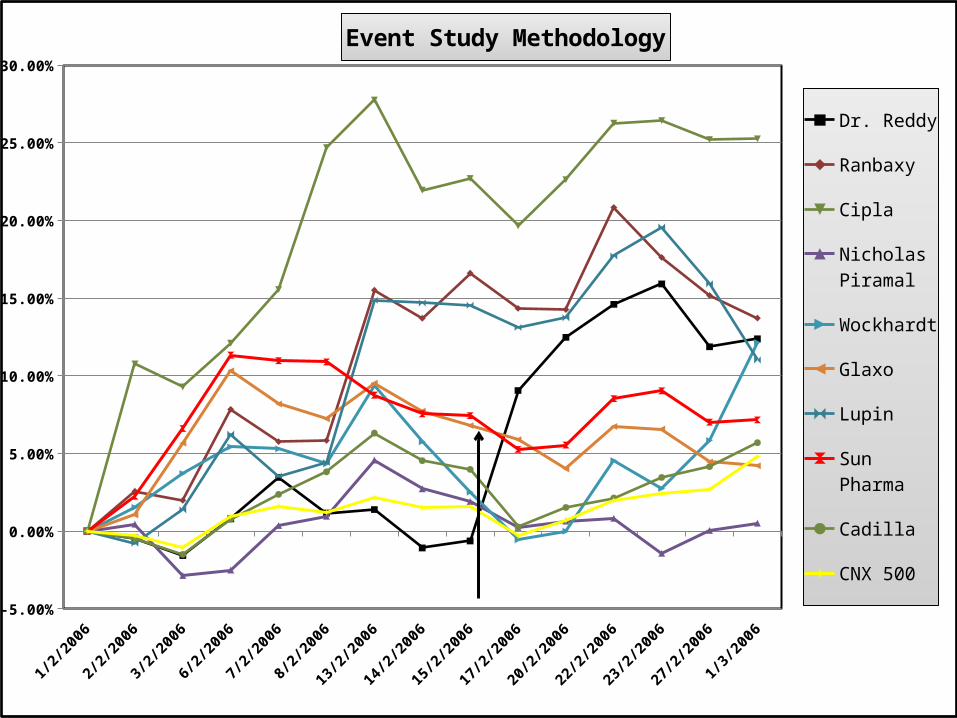

Market Perception - Event Study

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Event Study Methodology

Dr. Reddy

Ranbaxy

Cipla

Nicholas Piramal

Wockhardt

Glaxo

Lupin

Sun Pharma

Cadilla

CNX 500

Post Deal

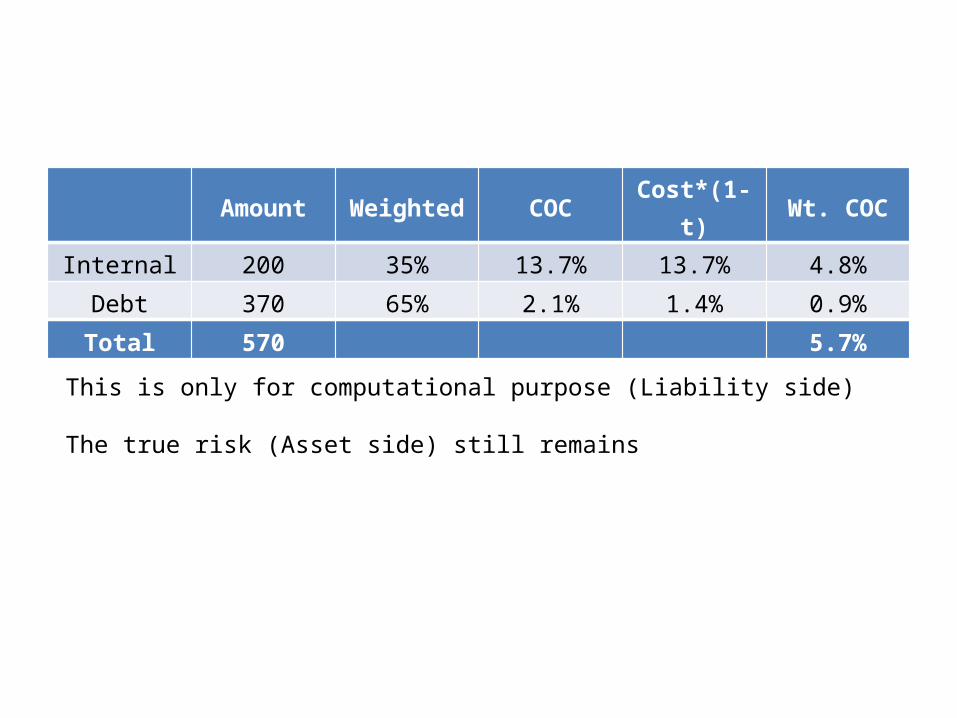

Financing

Amount Weighted COCCost*(1-

t)Wt. COC

Internal 200 35% 13.7% 13.7% 4.8%

Debt 370 65% 2.1% 1.4% 0.9%

Total 570 5.7%

This is only for computational purpose (Liability side)

The true risk (Asset side) still remains

Synergy

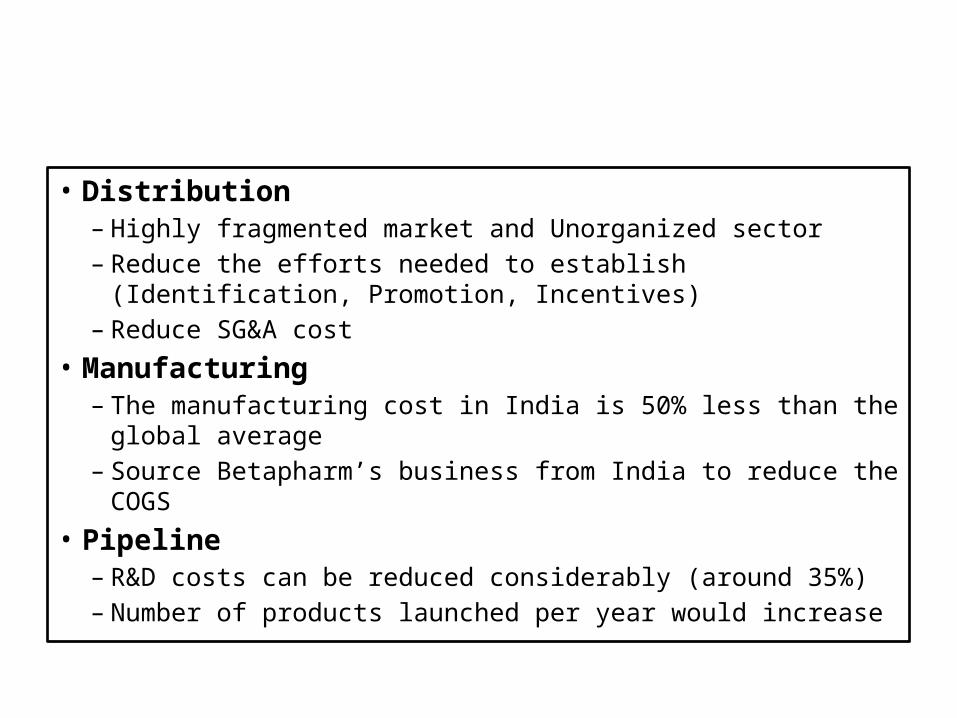

• Distribution– Highly fragmented market and Unorganized sector– Reduce the efforts needed to establish (Identification,

Promotion, Incentives) – Reduce SG&A cost

• Manufacturing– The manufacturing cost in India is 50% less than the

global average– Source Betapharm’s business from India to reduce the

COGS

• Pipeline– R&D costs can be reduced considerably (around 35%)– Number of products launched per year would increase

Synergy

• Branding– Brand Beta– Global Presence

• Presence– Entry into Germany – Central & Eastern Europe

• Size– DRL was able to reach the $1Billion size due to

this acquisition– Leverage its generic business to grow in Drug

discovery

Integration

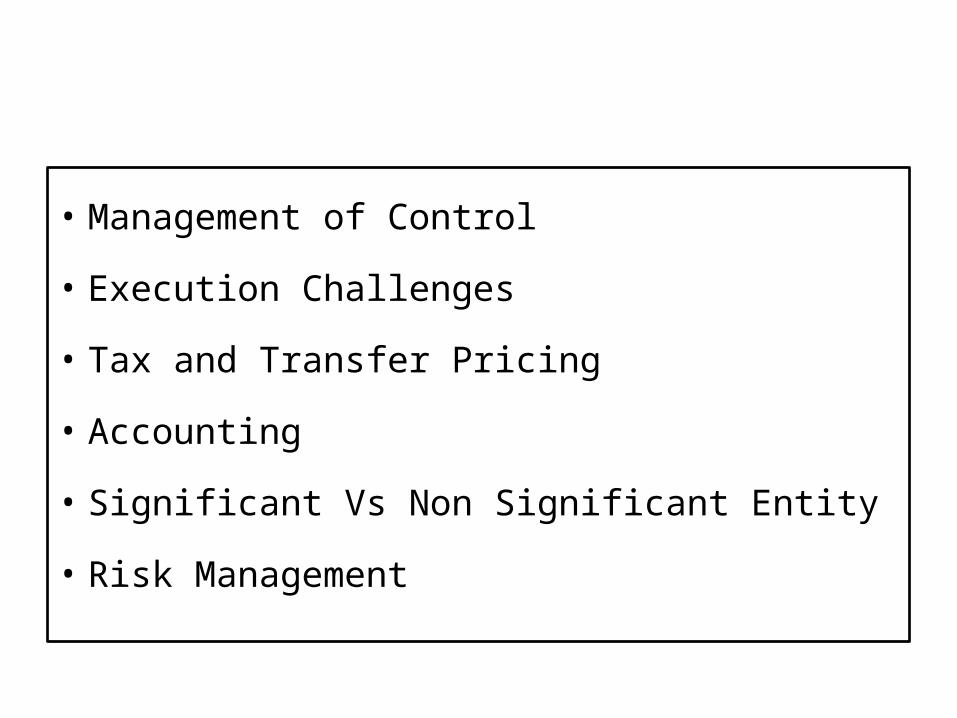

Post Merger Integration

• Management of Control

• Execution Challenges

• Tax and Transfer Pricing

• Accounting

• Significant Vs Non Significant Entity

• Risk Management

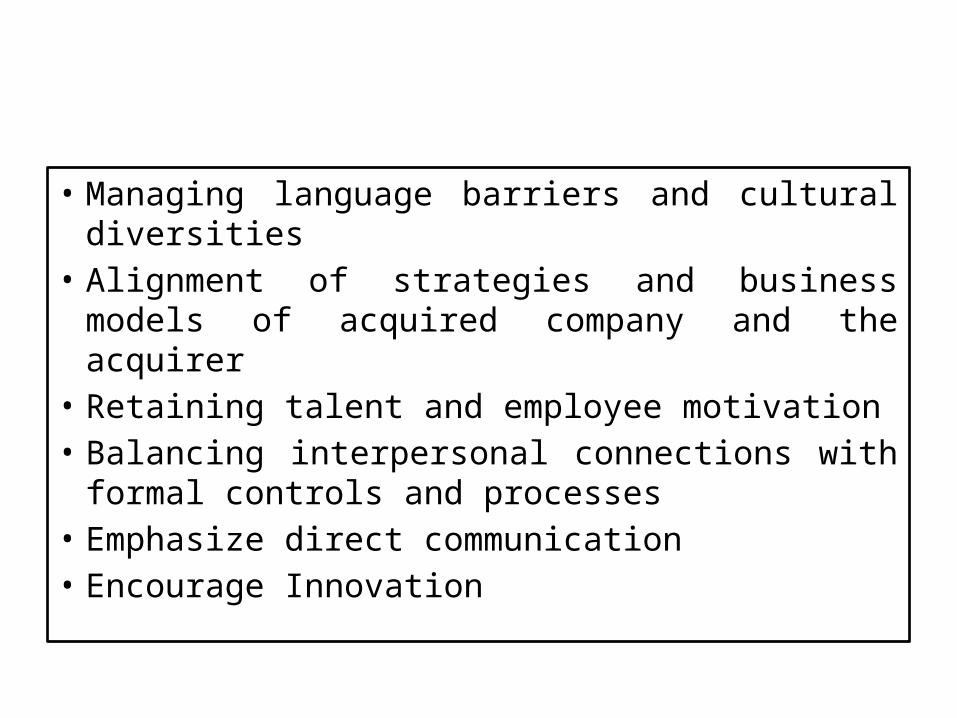

Cultural Integration

• Managing language barriers and cultural diversities

• Alignment of strategies and business models of acquired company and the acquirer

• Retaining talent and employee motivation• Balancing interpersonal connections with

formal controls and processes• Emphasize direct communication• Encourage Innovation

What Went Wrong

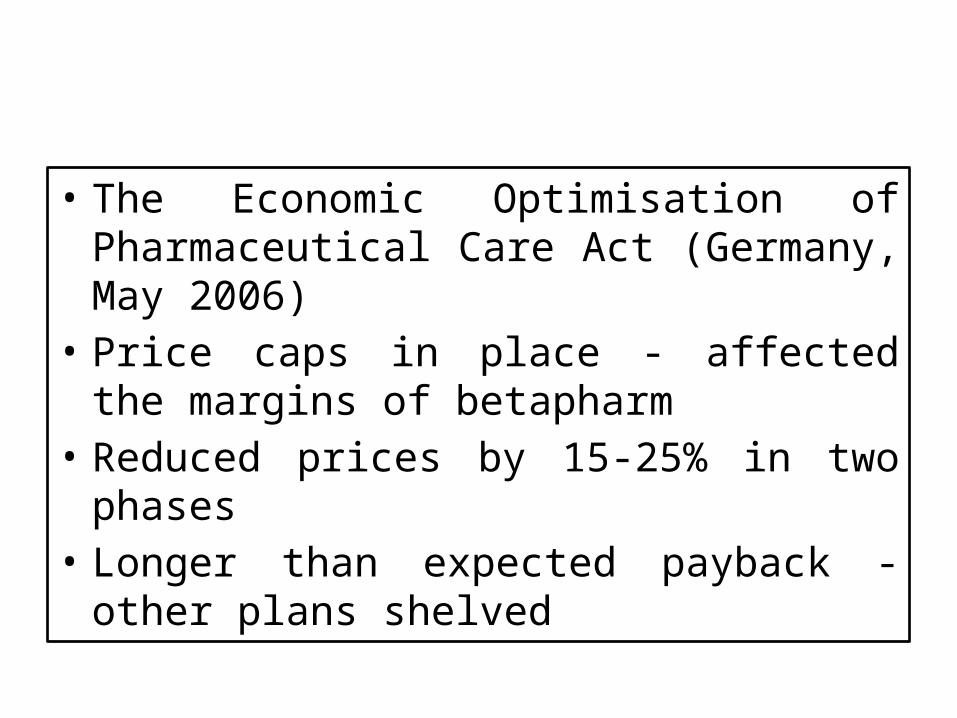

• The Economic Optimisation of Pharmaceutical Care Act (Germany, May 2006)

• Price caps in place - affected the margins of betapharm

• Reduced prices by 15-25% in two phases

• Longer than expected payback - other plans shelved

What Went Wrong

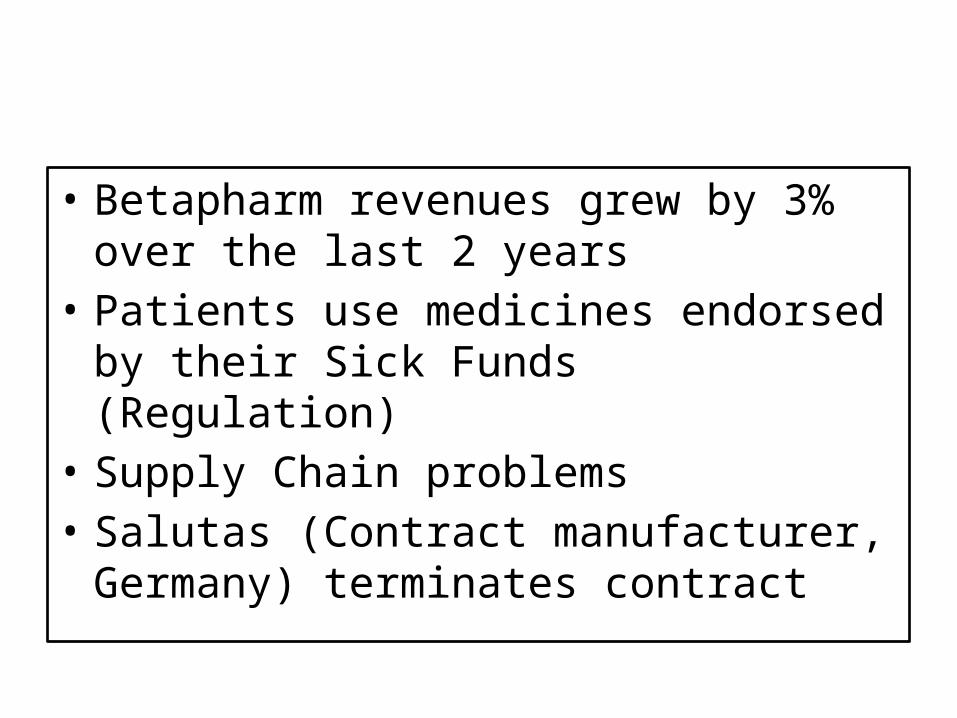

• Betapharm revenues grew by 3% over the last 2 years

• Patients use medicines endorsed by their Sick Funds (Regulation)

• Supply Chain problems• Salutas (Contract manufacturer,

Germany) terminates contract

What Went Wrong

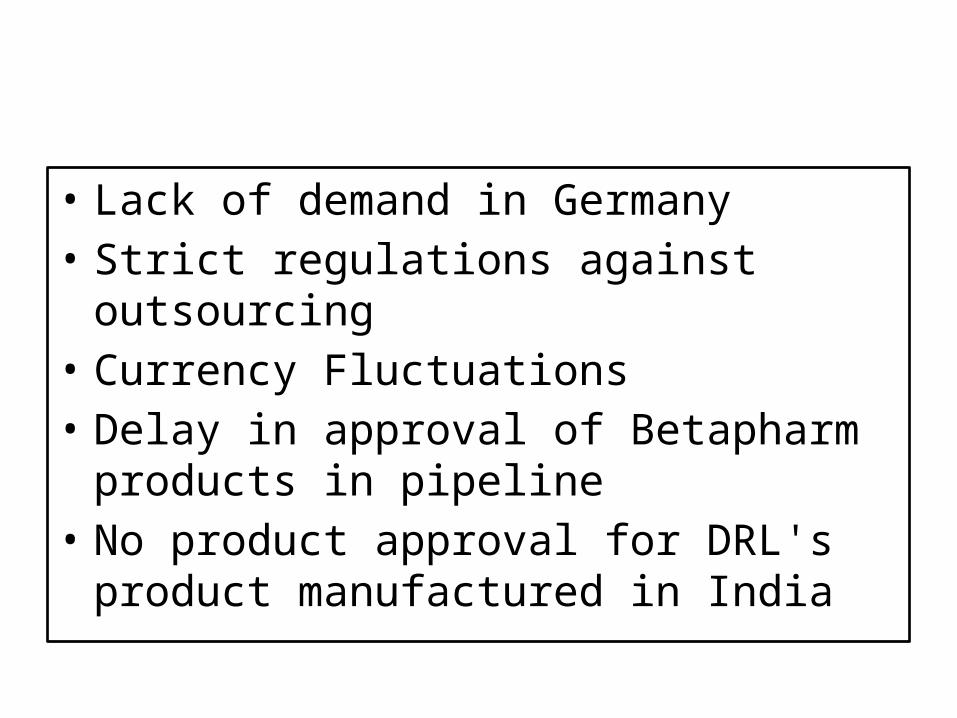

• Lack of demand in Germany• Strict regulations against outsourcing• Currency Fluctuations• Delay in approval of Betapharm

products in pipeline• No product approval for DRL's

product manufactured in India

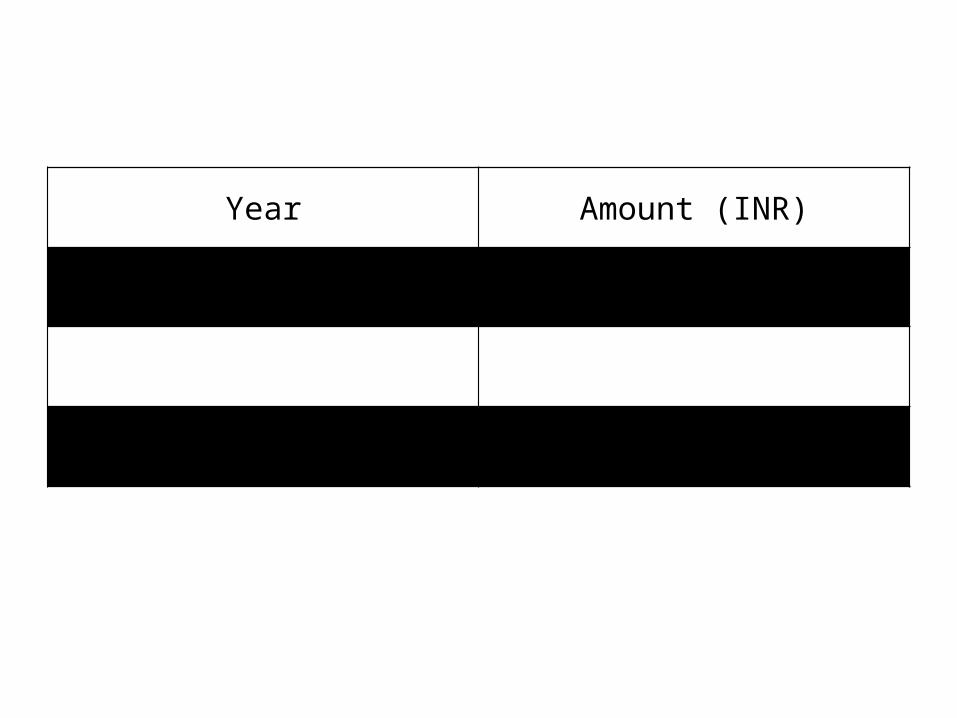

Write - Down

Year Amount (INR)

2006-2007 177 crore

2007-2008 236.1 crore

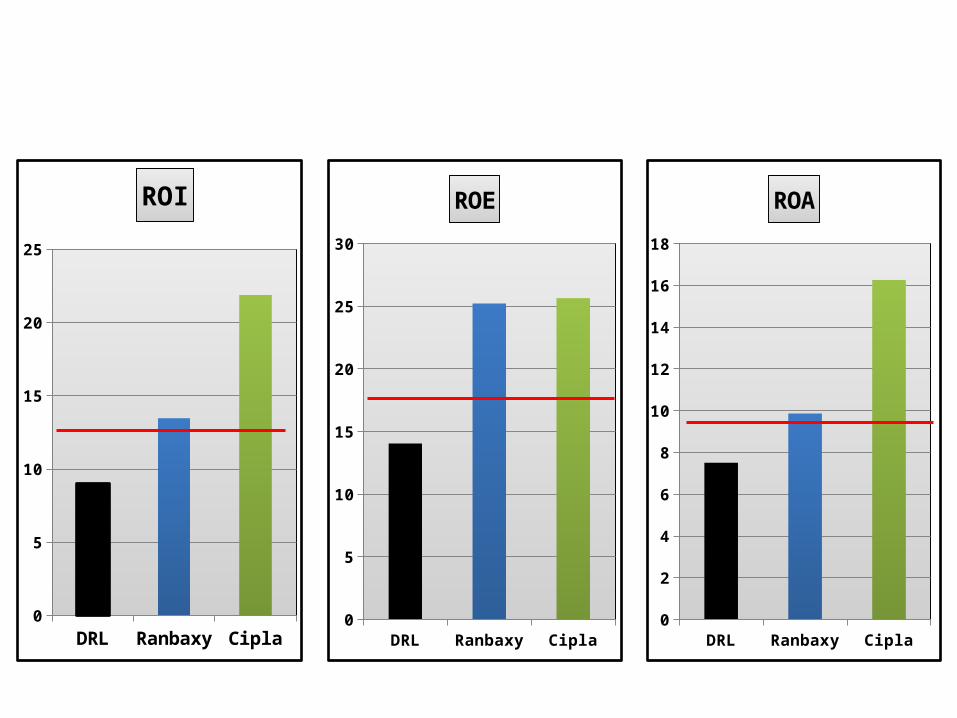

Relative Performance

DRL Ranbaxy Cipla0

5

10

15

20

25

ROI

DRL Ranbaxy Cipla0

5

10

15

20

25

30

ROE

DRL Ranbaxy Cipla0

2

4

6

8

10

12

14

16

18

ROA

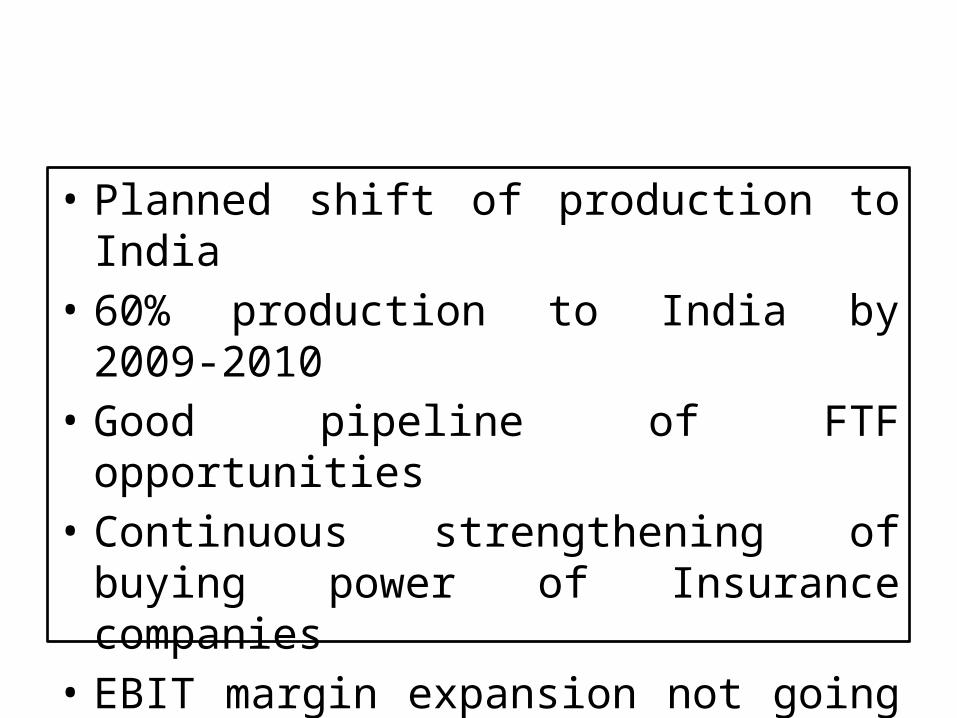

The Road Ahead

• Planned shift of production to India• 60% production to India by 2009-

2010• Good pipeline of FTF opportunities• Continuous strengthening of buying

power of Insurance companies• EBIT margin expansion not going to

be visible over short to medium term

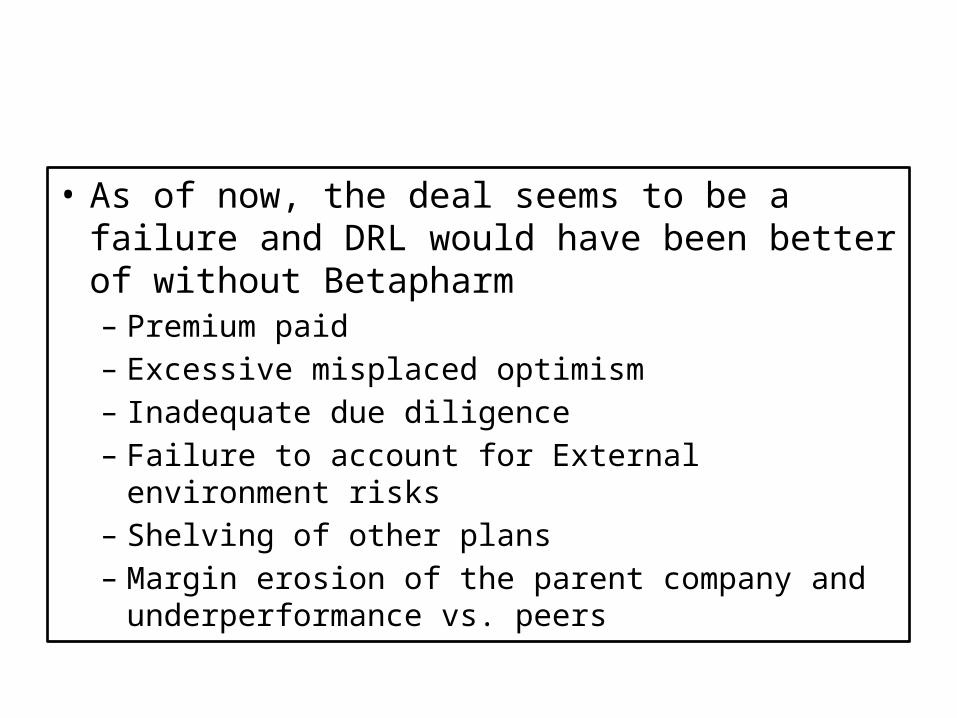

Conclusion

• As of now, the deal seems to be a failure and DRL would have been better of without Betapharm– Premium paid– Excessive misplaced optimism– Inadequate due diligence– Failure to account for External environment

risks– Shelving of other plans– Margin erosion of the parent company and

underperformance vs. peers

Thank You