capital budgeting dr reddy

TRANSCRIPT

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 1/55

A

Project Report

On

“CAPITAL BUDGETING”

At

DR. REDDY’S LABORATORIES LIMITED

Diert!tion S"#$itte%

In The Partial Fulfillment for the Award of the Degree

In Finance

Submitted By

Under the guidance of

FinanceManager

At Dr. Re%%&’' (TO)III' B!c*"p!++&

CERTI(ICATE

T*i i to certi,& t*!t t*e Project -or entit+e% “CAPITAL BUDGETING” !t

Dr. Re%%&’' (TO / III' B!c*"p!++& ' i ! #on!,ie% 0or o,

"#$itte% in p!rti!+ ,"+,i++$ent o, t*e re1"ire$ent ,or t*e !0!r% o, t*e %e2ree o,

“M!ter Pro2r!$$e In Intern!tion!+ B"ine” ,or t*e !c!%e$ic &e!r

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 2/55

Mr. T. 3ote*0!r R!o

4Intern!+ Project G"i%e5 4E6tern!+ E6!$in!tion5 4Dep!rt$ent o, M!n!2e$ent

St"%ie5

DECLARATION

I *ere#& %ec+!re t*!t t*e project report tit+e% “CAPITAL BUDGETING” "#$itte% in

p!rti!+ ,"+,i++$ent o, t*e re1"ire$ent ,or t*e Pot Gr!%"!tion o, “M!ter Pro2r!$$e In

Intern!tion!+ B"ine”' ,ro$ ! #on!,i%e 0or c!rrie% o"t #& $e "n%er t*e 2"i%!nce o,

Mr. T. 3ote*0!r R!o' M!n!2in2 Director o, (in!nce' Dr. Re%%&’ L!#or!torie Li$ite%'

(TO / III' B!c*"p!++& 7&%er!#!%.

I !+o %ec+!re t*!t t*i i t*e re"+t o, $& o0n e,,ort !n% i not "#$itte% to !n& ot*er

Uni8erit& ,or t*e !0!r% o, !n& ot*er De2ree' Dip+o$!' (e++o0*ip or pri9e.

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 3/55

P+!ce:

AC3NO-LEDGEMENT

I take this oortunity to acknowledge! all the eole who rendered their "aluable ad"ice in

bringing the ro#ect to function$

As art of curriculum at college$ The ro#ect enables us to enhance our skills! e%and our

knowledge by alying "arious theories! concets and laws to real life scenario which

would further reare us to face the e%tremely &'ometiti"e 'ororate (orld) in the near

future$

I e%ress my sincere gratitude to the staff of COLLEGE *yderabad$ I secially thank &the

management and staff of Dr$ +eddy,s) for creating out the study and for their guidance and

encouragement that made the ro#ect "ery effecti"e and easy$

I sincerely e%ress my gratitude to Mr. 3ote*0!r R!o' Finance! Manager

Dr$ +eddy,s! for his "aluable guidance and cooeration throughout my ro#ect work$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 4/55

I would like to thank Mr. 3ote*0!r R!o' Mr. 3!+&!n 3"$!r !n% Mr. Doi Srini8! !

for guiding and directing me in the rocess of making this ro#ect reort and for all the

suort and encouragement$

I am grateful to our Internal Faculty' faculty in MPIB Deartment for his suort and

assistance in my ro#ect work$

I ha"e tried my le"el best to ut my e%erience and analysis in writing this reort$ I am

grateful to Dr$ +eddy,s as an organi-ation and its "arious emloyees for heling me to learn

and e%lore many fields$

INDE;

I. Intro%"ction P!2e No.

De,inition o, C!pit!+ B"%2etin2

Scope o, t*e t"%&

O#jecti8e o, t*e t"%&

Nee% ,or t*e t"%&

Li$it!tion o, t*e t"%&

Met*o%o+o2&

II. In%"tr& Pro,i+e

7itor& o, t*e P*!r$!ce"tic!+ In%"tr&

M!jor p+!&er o, t*e -or+% P*!r$!ce"tic!+ In%"tr&

T*e In%i!n P*!r$!ce"tic!+ In%"tr&

III. Co$p!n& Pro,i+e

A#o"t t*e Co$p!n&

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 5/55

Bo!r% o, Director

Str!te2ic B"ine Unit

3e& Mi+etone

Dep!rt$ent

I<. C!pit!+ B"%2etin2

<. (in%in2 !n% S"22etion

<I. Bi#+io2r!p*&

INTRODUCTION

De,inition o, C!pit!+ B"%2etin2

C!pit!+ #"%2etin2 4or in8et$ent !ppr!i!+5 is the lanning rocess used to determine

whether a firm.s long term in"estments such as new machinery! relacement machinery! new

lants! new roducts! and research de"eloment ro#ects are worth ursuing$ It is budget forma#or caital! or in"estment! e%enditures

NEED !n% IMPORTANCE (OR CAPITAL BUDGETING

'aital budgeting means lanning for caital assets$ The imortance of caital budgeting

can be well understood from the fact that an unsound in"estment decision may ro"e fatal to

the "ery e%istence of the concern$ The need! significance or imortance of caital budgeting

arises mainly due to the following/

0$ L!r2e In8et$ent: 'aital budgeting decisions in"ol"es large in"estment of funds but

the funds a"ailable with the firm are always limited and demand for funds far e%ceeds

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 6/55

the resources$ *ence! it is "ery imortant for the firm to lan and control its caital

e%enditure$

1$ Lon2 / Ter$ Co$$it$ent o, ("n%: It increases the financial risk in"ol"ed in the

in"estment decision$

2$ Irre8eri#+e N!t"re: The caital e%enditure decisions are of irre"ersible in nature .

3nce the decision for ac4uiring a ermanent asset is taken! it becomes "ery difficult to

disose of these assets without incurring hea"y losses$

5$ Lon2 / Ter$ E,,ect on Pro,it!#i+it&: 'aital budgeting decisions ha"e a long 6 term

and significant effect on the rofitability of a concern$ 7ot only are the resent earnings

of the firm affected by the in"estments in caital assets$

8$ Di,,ic"+tie o, In8et$ent Deciion: The long term in"estment decisions are difficult to

be taken because decision e%tends to a series of years beyond the current accounting

eriod$

SCOPE O( T7E STUDY

The study is done on caital budgeting held by 9enerics di"ision of Dr$ +eddy,s

:aboratories :imited$

The scoe of the study includes the Payback eriod method$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 7/55

OB=ECTI<ES O( T7E STUDY

Main 3b#ecti"e/ 6

The main 3b#ecti"e of the ro#ect is to understand why Payback eriod is better than other caital budgeting techni4ues from the comany,s oint of "iew$

Sub ; 3b#ecti"es/ 6

To know the in"estment criteria done by Dr$ +eddy,s lab while e"aluating a ro#ect$

a< To study the financial feasibility of the roosal$

b< To find out the benefits that the comany is going to get from the new ro#ects$

c< To critically e"aluate a ro#ect using different tyes of caital budgeting techni4ues$ andto arri"e at the right conclusion$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 8/55

d< To understand ad"antages and disad"antages of "arious techni4ues$

e< =stimating of assets > tools re4uired for this new ro#ect$

NEED (OR T7E STUDY

'aital budgeting means lanning for caital assets$ The need of caital budgeting can be

well understood from the fact that an unsound in"estment decision may ro"e fatal to the

"ery e%istence of the concern$ It is used to determine whether Dr$ +eddy,s long term

in"estments such as new machinery! relacement machinery! new lants! new roducts! and

research de"eloment ro#ects are worth ursuing$ It is budget for ma#or caital! or

in"estment! e%enditures$

LIMITATIONS O( T7E STUDY

Since the study co"ers only 9enerics di"ision of Dr$ +eddy,s :aboratories :imited!

it does not reresent the o"erall scenario of the industry$

Few "alues taken are on facts basis$

The ro#ect is constraint to only one roosal$

This is a study conducted within a eriod of 58 days$

During this limited eriod of study! the study may not be a detailed! fully

fledged and utilitarian one in all asects$

The study contains some assumtion based on the demands of the analysisdone by the comany e%ecuti"es$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 9/55

INDUSTRY

PRO(ILE

PRO(ILE O( T7E INDUSTRY

7itor& o, t*e p*!r$!ce"tic!+ in%"tr&

The earliest drugstores date back to the middle Ages$ The first known drugstore was

oened by Arabian harmacists in Baghdad in ?88 A$D$! and many more soon began

oerating throughout the medie"al Islamic world and e"entually medie"al =uroe$ By the

0@th century! many of the drug stores in =uroe and 7orth America had e"entually

de"eloed into larger harmaceutical comanies$

Most of today.s ma#or harmaceutical comanies were founded in the late 0@th andearly 1th centuries$ ey disco"eries of the 0@1s and 0@2s! such as insulin and enicillin!

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 10/55

became mass6manufactured and distributed$ Swit-erland! 9ermany and Italy had

articularly strong industries! with the U! US! Belgium and the 7etherlands following suit$

'ancer drugs were a feature of the 0@?s$ From 0@?C! India took o"er as the rimary

center of harmaceutical roduction without atent rotection

The harmaceutical industry entered the 0@Cs ressured by economics and a host of

new regulations! both safety and en"ironmental! but also transformed by new D7A

chemistries and new technologies for analysis and comutation$ Drugs for heart disease and

for AIDS were a feature of the 0@Cs! in"ol"ing challenges to regulatory bodies and a faster

aro"al rocess$

Diagram 0/ T*e Core o, P*!r$!ce"tic!+ B"ine

source/ <

T7E INDIAN P7ARMACEUTICAL INDUSTRY

&The Indian harmaceutical industry is a success story ro"iding emloyment for

millions and ensuring that essential drugs at affordable rices are a"ailable to the "ast

oulation of this sub6continent$)

The harmaceutical industry lays a crucial role in building a country,s human

caital$ In India! it is among the to science based industries with a wide range of

caabilities in the comle% field of Drug Technology and Manufacture$

Inter$e%i!te

Dr"2 Dico8er&

>

De8e+op$ent (ini*e% Do!2eAPI

Br!n%e% Generic

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 11/55

Achie"ements of the industry during the last three decades ha"e been sectacular by

any standards! from a mere rocessing industry it has grown into a sohisticated sector with

ad"anced manufacturing technology! modern e4uiment and stringent 4uality control$

A highly organi-ed sector! t*e In%i!n P*!r$!c& In%"tr& is estimated to be worth

E 5$8 billion! growing at about C to @ ercent annually$ It ranks "ery high in the third world!

in terms of technology! 4uality and range of medicines manufactured$ From simle headache

ills to sohisticated antibiotics and comle% cardiac comounds! almost e"ery tye of

medicine is now made indigenously$

The Indian Pharmaceutical sector is highly fragmented with more than 1!

registered units$ It has e%anded drastically in the last two decades$ The leading 18

harmaceutical comanies control ? of the market with market leader holding nearly ?

of the market share$ It is an e%tremely fragmented market with se"ere rice cometition and

go"ernment rice control$

The &organi-ed) sector of India.s harmaceutical industry consists of 18 to 2

comanies! which account for ? ercent of roducts on the market! with the to 0 firms

reresenting 2 ercent$ *owe"er! the total sector is estimated at nearly 1! businesses!

some of which are e%tremely small aro%imately ?8 ercent of India.s demand for

medicines is met by local manufacturing$

In 1C! India.s to 0 harmaceutical comanies were R!n#!6&! Dr. Re%%&?

L!#or!torie! Cip+!' S"n P*!r$! In%"trie! L"pin L!#! A"ro#in%o P*!r$!!

G+!6oS$it*3+ine P*!r$!' C!%i+! 7e!+t*c!re' A8enti P*!r$! !n% Ipc! L!#or!torie

Indian6owned firms currently account for ? ercent of the domestic market! u from less

than 1 ercent in0@?$ In 1C! nine of the to 0 comanies in India were domestically

owned! comared with #ust four in 0@@5$

+ank 'omany +e"enue 1C

+s in crore<

0 +anba%y :aboratories +s$ 18!0@G$5C

1 Dr$ +eddy,s :aboratories +s$ 5!0G1$182 'ila +s! 2!?G2$?1

5 Sun Pharma Industries +s$ 1!5G2$8@

8 :uin :aboratories +s$ 1$108!81

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 12/55

G Aurobindo Pharma +s$ 1!C$0@

? 9la%o Smithline Pharma +s$ 0!??2$50

C 'adila *ealthcare +s$ 0!G02$

@ A"entis Pharma +s$ @C2$C

0 Ica :aboratories +s$ @C$55

Source/ htt/HHsecials$rediff$comHmoneyH1CH#unH00sld0$htm

Table 1:

Top @ In%i!n P*!r$!ce"tic!+ Co$p!nie'

India.s otential to further boost its already6leading role in global generics

roduction! as well as an offshore location of choice for multinational drug manufacturers

seeking to curb the increasing costs of their manufacturing! +>D and other suort

ser"ices! resents an oortunity worth an estimated E5C billion in 1C$

India.s USE 2$0 billion harmaceutical industry is growing at the rate of 05 ercent

er year$ It is one of the largest and most ad"anced among the de"eloing countries$ 3"er

1! registered harmaceutical manufacturers e%ist in the country$

In%i!n P*!r$!ce"tic!+ E8o+"tion

P*!e I

E!r+& Ye!r

M!ret *!re %o$in!tion #& ,orei2n co$p!nie

Re+!ti8e !#ence o, or2!ni9e% In%i!n co$p!nie

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 13/55

O8er)t*e)Co"nter Me%icine

The Indian market for o"er6the6counter medicines 3T's< is worth about E@5

million and is growing 1 ercent a year! or double the rate for rescrition medicines$ the

go"ernment is keen to widen the a"ailability of 3T's to outlets other than harmacies! and

the 3rgani-ation of Pharmaceutical Producers of India 3PPI< has called for them to be sold

in ost offices$

De"eloing an inno"ati"e new drug! from disco"ery to worldwide marketing! now

in"ol"es in"estments of around E0 billion! and the global industry.s rofitability is under

constant attack as costs continue to rise and rices come under ressure$ Pharmaceutical

roduction costs are almost 8 ercent lower in India than in (estern nations! while o"erall

+>D costs are about one6eighth and clinical trial e%enses around one6tenth of (estern

le"els$

&India.s largest6selling drug roducts are antibiotics! but the fastest growing are Diabetes!

cardio"ascular and central ner"ous system treatments)$

The industry.s e%orts were worth more than E2$?8 billion in 186G and they ha"e

been growing at a comound annual rate of 11$? ercent o"er the last few years! according

to the go"ernment.s draft 7ational Pharmaceuticals Policy for 1?! ublished in anuary

1?$ The Policy estimates that! by the year 10! the industry has the otential to achie"e

E11$5 billion in formulations! with bulk drug roduction going u from E0$?@ billion to

E8$G billion/ &India.s rich human caital is belie"ed to be the strongest asset for this

knowledge6led industry$ Jarious studies show that the scientific talent ool of 5 million

Indians is the second6largest =nglish6seaking grou worldwide! after the USA$)

<AT :

In Aril 18! the go"ernment introduced "alue6added ta% for the first time and

abolished all other ta%es deri"ed from sales of goods$ So far! 11 states ha"e imlemented

JAT! which is set at 5 ercent for medicines$ This led to harmaceutical wholesalers and

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 14/55

retailers cutting their stocks dramatically! which se"erely affected drug manufacturers. sales

for se"eral months$

Opport"nitie

The main oortunities for the Indian harmaceutical industry are in the areas of/

♦ 9enerics including biotechnology generics<

♦ Biotechnology

♦ 3utsource and +>D outsourcing<$

♦ Pricing including contract manufacturing! information technology IT<

COMPANY PRO(ILE

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 15/55

O<ER<IE- O( DR.REDDY’S LABORATORIES LIMITED

ABOUT T7E COMPANY

Dr$ +eddy,s :aboratories :imited Dr$ +eddy,s< together with its subsidiaries

collecti"ely! the comany< is a leading India6 based harmaceutical comany head 4uarter

in *yderabad! India$ The comany,s rincial areas of oeration are formulations! acti"e

harmaceutical ingredients and intermediates! generics! custom harmaceutical ser"ices!

critical care and biotechnology and drug disco"ery$ The comany,s rincial reached and

de"eloed and manufacturing facilities are located in Andhra Pradesh! India and 'uerna"aca

cuautla! Me%ico with rincial marketing facilities in India! +ussia! United States! United

ingdom! Bra-il! and 9ermany$ The comany,s shares trade on se"eral stock e%changes in

India and! since Aril 00! 10! on the 7KS= and in the US as of March 20! 1?$

Since Dr$ +eddy,s :aboratories incetion in 0@C5! it has chosen to walk the ath of

disco"ery and inno"ation in health science$ Dr$ +eddy,s has been a 4uest to sustain and

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 16/55

imro"e the 4uality of life and Dr$ +eddy,s had more than three decades of creating safe

harmaceutical solution with the ultimate urose of making the world a healthier lace$ Dr$

+eddy,s cometencies co"er the entire harmaceutical "alue chain ; API and Intermediates!

Finished Dosages Branded and 9eneric< and 7'= research$

Dr$ +eddy,s research centre uses cutting6edge technology and has disco"ered

breakthrough harmaceutical solutions in select theraeutic areas$ In a short san of

oerations! Dr$ +eddy,s ha"e filed for more than ?8 atents$ Dr$ +eddy,s is the first Indian

comany to out6license an 7'= molecule for clinical trials$ To strengthen their research

arm! it has set u a research subsidiary! +eddy US Theraeutics Inc$! in Atlanta! USA

Dr$ +eddy,s e%ort API! branded formulations and generic formulations to

o"er G countries$The comany e%orts API! branded formulations and generic

formulations to o"er G countries$ The inherent strength lies in identifying rele"ant API and

formulations! and selling them at affordable rices across the world$ A few of our API such

as Nor,+o6!cin' Cipro,+o6!cin and Enro,+o6!cin en#oy a large customer base$ The finished

dosages ha"e an en"iable track record$ Some of them such as Nie' O$e9' En!$' St!$+o'

St!$+o Bet!' G!iet& and Cipro+et are among the to brands in India! and many ha"e

become household names in near6regulated countries too$

The generic formulations ha"e also become "ery oular in 4uality6conscious

regulated markets such as the US and =uroe$ All this has been ossible because of our

inno"ati"e and sustained marketing efforts$

“T*e co$p!n& et to pre!% o"r 0in2 ,"rt*er !n% to"c* $ore +i8e !cro t*e

2+o#e.

Dr$ +eddy,s is ha"ing si% manufacturing facilities Formulations Technical

3erations Plants< across India$

Bo+!r!$ 47&%er!#!%5 ) (TOI

B!c*"p!++& 47&%er!#!%5 / (TO II !n% (TO III

Y!n!$ 4 Ne!r 3!in!%!5 / (TO I<

B!%%i 47i$!c*!+ Pr!%e*5 / (TO <I

<i*!*!p!tn!$ 4An%*r! Pr!%e*5 / (TO <II

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 17/55

BUSINESS DI<ISIONS O( DR REDDY’S LABORATORIES

Dr +eddy.s is a global harmaceutical owerhouse committed to rotecting and

imro"ing health and well6being$

T*e Dr. Re%%&’ Str!te2ic B"ine Unit. 4SBU5:

For management uroses! the 9rou is organi-ed on a worldwide basis into fi"e

strategic business units SBUs<! which are the reortable segments/

(or$"+!tion 4inc+"%in2 Critic!+ c!re !n% Biotec*no+o2&5F

Acti8e P*!r$!ce"tic!+ In2re%ient !n% Inter$e%i!te 4API5F

GenericF Dr"2 Dico8er& !n%

C"to$ P*!r$!ce"tic!+ Ser8ice 4CPS5.

BOARD AND MANAGEMENT

-*o+e)Ti$e Director

• Dr. Anji Re%%&

'hairman

• G < Pr!!%

=%ecuti"e Jice 'hairman and 'hief =%ecuti"e 3fficer

• S!ti* Re%%&

Managing Director > 'hief 3erating 3fficer

In%epen%ent > Non -*o+e Ti$e Director

Dr$ 3mkar 9oswami

+a"i Bhoothalingam

Dr$ Bruce :A 'arter

Anuam Puri

Ms$alana Moraria

$P$ Moreau$

T*e preent C(O o, Dr. Re%%&’ i Mr. U$!n2 Bo*r!

A"%itor

BS+ > 'o$ audited the financial statements of 1C ; 1@ reared under the Indian9AAP$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 18/55

The 'omany had also aointed PM9 as indeendent auditors for the urose of issuingoinion on the financial statements reared under the US 9AAP$

INERNATIONAL MAR3ET AREAS O( DR. REDDY’S LABORATORIES

AlbaniaBelarus 'ambodia

'ayman islands 'hina Dmr

9hana 9uyana *aiti

Ira4 amaica a-akhstan

enya yrgy-stan Malaysia

Mauritius Myanmar 3man

+omania +ussia Singaore

Sri :anka St$itts St$lucia

Sudan Tan-ania Trinidad

Uganda Ukraine U-bekistan

Jene-uela Jietnam Kemen

S7ARE CAPTIAL :

+s in Thousands<

PARTICULARS ) )H H) )

=4uity 5?@C1? 80005 @G5G@1 00?GGG8

Debt6long Term 8?G 5?0C8 505G5 210G5

Total Share 'aital 5C52 @?10@@ 02?@1@G 05@C1G@

2004 2005 2006 20070

200000

400000

600000

800000

1000000

1200000

Equity

Debt

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 19/55

Gr!p* @:

So"rce

CURRENT (INANCIAL POSITION O( DR.REDDY’S LAB

S*!re*o+%in2 P!ttern on M!& J' J

Pro$oter 7o+%in2: No. O, S*!re K o, S*!re

Indi"idual *olding 5!5C@!5C5

1$GG

'omanies2@!@?C!21C 12$?2

S"# Tot!+55!5G?!C01

Indian FinancialInstitutions

11!815!8GC 02$2?

Banks 201!?5G $0@

Mutual Funds 0!?G5!1@2 G$2@

S"# Tot!+22!G0!G? 0@$@8

(orei2n 7o+%in2:

Foreign Institutional

In"estors

2C!@C8!@G5 12$05

7+Is2!@?!521 0$C5

AD+s H Foreign 7ational 15!@2!0@2 05$?C

S"# Tot!+GG!@CG!8C@ 2@$?G

Indian Public >

'ororates

12!501!?G@ 02$@

Tot!+0GC!5GC!??? 0$

T!#+e :

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 20/55

So"rce

0< 1C 6 1@! the comany launched 00G new generic roducts! filed 00 new generic roduct

registrations and filed 88 DMFs globally$

1< The Board of Directors of the 'omany ha"e recommended a final di"idend of +s$

G$18 018< er e4uity share of +s$ 8H6 face "alue! sub#ect to the aro"al of

shareholders at the ensuing Annual 9eneral Meeting$

2< +e"enues in India increase to +s$ C$8 billion E0G? million< in FK@ from +s$C$0billions

E08C million<! reresenting a growth of 8$

5< 2G new roducts launched during the year$

8< 7ew roducts launched in the last 2G months contribute 05 to total re"enues in FK@

Dr. Re%%&’

E6tr!cte% ,ro$ t*e A"%ite% Inco$e St!te$ent ,or t*e &e!r en%e% M!rc* @'

J

(Y J (Y

P!rtic"+!r 45 4R.5 K 45 4R.5 4K5Gro0t*

KRe8en"e @'H HJ'@ @ J 'H @ J

'ost of re"enues G5C 21!@50 5? 5C5 15!8@C 5@ 25

Gro pro,it @ H' JJ ' @

Oper!tin2 E6pene

Selling! 9eneral >Administrati"e =%ensesa<

502 10!1 2 220 0G!C28 25 18

+esearch > De"eloment=%enses! net

?@ 5!2? G G@ 2!822 ? 05

(rite down of intangible assets G1 2!0G? 8 8@ 2!00 G 8

(rite down of goodwill 102 0!C8G 0G 1 @ 6

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 21/55

3ther income<He%enses! net 8 182 C< 51< 0< 6

Tot!+ Oper!tin2 E6pene J' 'H H @

Re"+t ,ro$ oper!tin2

!cti8itie

4H5 4'5 45 H '@ )

Finance Incomeb< @< 5C1< 0< 20< 4@'H@5 2< ?<

Finance e%ensesc< 22 0!GGC 1 10 0!C 1 85

(in!nce e6pene' net @'@H 4@5 4@5 4@5 )

Share of rofitH loss< of e4uityaccounted in"estees

15 1 0!0

Pro,it #e,ore inco$e t!6 4J5 4'JJ5 4H5 8G 1!CG5 G 6

Income ta% e%ense 12< 0!0?2< 1< 0@ @?1 1 6

Pro,it ,or t*e perio% 4@5 4'@H5 45 2!C2G )

Attri#"t!#+e to:

=4uity holders of the comany 01< 8!0GC< ?< ?G 2!C5G C 6

Minority interest < 0< < 6

Pro,it ,or t*e perio% 4@5 4'@H5 45 'H )

(eighted a"erage no$ ofshares oHs

0G@ 0G@

Di+"te% EPS 4.H5 4.5 . .

=%change rate . .

Note

:

a< Includes amorti-ation charges of +s$ 0!82 million in FK@ and +s$0!8CC million in FKC

b< Includes fore% gain of +s$ ?2@ million in FKC

c< Includes fore% loss of +s$ G25 million in FK@$

(In millions)3e& B!+!nce S*eet Ite$

P!rtic"+!r A on @t M!r J A on @t M!r

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 22/55

45 4R.5 45 4R.5

'ash and cash e4ui"alents 00 8!G2 05G ?!510

In"estments current > non6current< 0 82 @2 5!?82

Trade and other recei"ables 1C1 05!2GC 025 G!C12

In"entories 1G 02!11G 10@ 00!022Proerty! lant and e4uiment 50 1!CC0 22 0G!?G8

:oans and borrowings current > non6current< 2C? 0@!?0 2C 0@!281

Trade accounts ayable 00C 8!@C? 0? 8!51?

Total =4uity C1? 51!58 @20 5?!28

Dr. Re%%&’ A0!r% !n% Reco2nition :

Best (orklaces 1C In BiotechH Pharma Industry Sector6The =conomic Times

Best Performing 'F3 in the Pharma Sector for 1?

'7B'6TJ0C.s 'F3 Award Saumen 'hakroborty ; =%$ 'F3

7DTJ Profit Business :eadershi Awards 1?

Business :eader in the Pharmaceutical Sector

Amity :eadershi Award

Best Practices in *+ in Pharmaceutical Sector$

5th *+ Summit .C

Dun > Bradstreet American =%ress'ororate Awards 1?

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 23/55

Best 'ororate Social +esonsibility Initiati"e

1? BS= ; India

Pharma =%cellence Awards 1G6?

'ategory / 'ororate Social +esonsibility

The Indian =%ress

Best =mloyers in India 1? Award

*ewitt Associates > The =conomic Times

South Asian Federation of Accountants SAFA< Award 1?

1nd Best Annual +eort in the South Asian +egion

Finance Asia Achie"ement Awards 1G

Best India Deal 6 Ac4uisition of betaharm for E8? million

Asia6Pacific *+M 'ongress 1?

9lobal *+ =%cellence Award for Inno"ati"e *+ Practices

And many more$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 24/55

CAPITAL BUDGETING

In modern times! the efficient allocation of caital resources is a most crucial function of

financial management$ This function in"ol"es organi-ation,s decision to in"est its resources

in long6term assets like land! building facilities! e4uiment! "ehicles! etc$ The future

de"eloment of a firm hinges on the caital in"estment ro#ects! the relacement of e%isting

caital assets! andHor the decision to abandon re"iously acceted undertakings which turns

out to be less attracti"e to the organi-ation than was originally thought! and di"erting the

resources to the contemlation of new ideas and lanning$ For new ro#ects such as

in"estment decisions of a firm fall within the definition of caital budgeting or caital

e%enditure decisions$

'aital budgeting refers to long6term lanning for roosed caital outlays and their

financing$ Thus! it includes both rising of long6term funds as well as their utili-ation$ It may!

thus! be defined the &firm,s formal rocess for ac4uisition and in"estment of caital)$ To be

more recise! caital budgeting decision may be defined as &the firms, decision to in"est its

current find more efficiently in long6term acti"ities in anticiation of an e%ected flow of

future benefit o"er a series of years$) The long6term acti"ities are those acti"ities which

affect firms oeration beyond the one year eriod$ 'aital budgeting is a many sided

acti"ity$ It contains searching for new and more rofitable in"estment roosals!

in"estigating! engineering and marketing considerations to redict the conse4uences of

acceting the in"estment and making economic analysis to determine the rofit otential of

in"estment roosal$

T*e #!ic ,e!t"re o, c!pit!+ #"%2etin2 %eciion !re:

0$ 'urrent funds are e%changed for future benefits$

1$ There is an in"estment in long term acti"ities$

2$ The future benefits will occur to the firm o"er series of years

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 25/55

C!pit!+ #"%2etin2 4or in8et$ent !ppr!i!+5 is the lanning rocess used to determine

whether a firm.s long term in"estments such as new machinery! relacement machinery! new

lants! new roducts! and research de"eloment ro#ects are worth ursuing$ It is budget for

ma#or caital! or in"estment! e%enditures$

C!pit!+ #"%2etin2 proce

The caital budget rocess is usually a multi6ste rocess! including/

I%enti,ic!tion o, potenti!+ in8et$ent opport"nitie

Ae$#+in2 o, propoe% in8et$ent

In8entor& o, C!pit!+ AetF

De8e+opin2 ! C!pit!+ In8et$ent P+!n 4CIP5F

De8e+opin2 ! M"+ti)Ye!r CIPF

De8e+opin2 t*e (in!ncin2 P+!nF !n%'

I$p+e$entin2 t*e C!pit!+ B"%2et.

T&pe O, C!pit!+ B"%2etin2 Project:

Indeendent Pro#ects 6 Pro#ects unrelated to each other where a decision to accet

one ro#ect will not affect the decision to accet another Mutually =%clusi"e Pro#ects 6 The decision to choose only one ro#ect from the

many being considered$

T&pe O, C!pit!+ B"%2etin2 Deciion:

'aital Budgeting Decision for =%ansion uroses or

For relacement of e%isting assets$

I$port!nce o, C!pit!+ B"%2etin2:

Proer decision on caital budget will increase a firm,s "alue as well as

shareholders, wealth

'aital budgeting is critical to a firm as it hels the firm to stay cometiti"e as it is

e%anding its business like roosing to urchase e4uiments to roduce

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 26/55

additional or new roducts! renting or owning remises for oening new branches!

etc$

G"i%e+ine In C!pit!+ B"%2etin2 An!+&i

As caital budgeting in"ol"es substantial initial outlay and years at least more

than one year< to rea the benefits! it is critically imortant to understand some of

the cardinal rinciles or rules or guidelines when erforming this caital

budgeting e%ercise$

Aend below in brief ertaining to/

GUIDELINESPRINCIPLES ON T7E CAPITAL BUDGETING ANALYSIS

G"i%e+ine No@/

Use 'ash Flows And 7ot Accounting Profit$ Kou need to ad#ust accounting rofit

to arri"e at the rele"ant cash flows .

G"i%e+ine No :

Focus on Incremental 'ash flows$ Simly it means that you should comare the

total cash flows of the comany with and without the ro#ect$ After determining

the incremental cash flows! you need to consider the ta% imlication on these

cash flows "i- focus only on &after6ta% incremental cash flows) in the caital

budgeting analysis$

G"i%e+ine No.:

'onsider any synergistic effect on the ro#ect$ For e%amle! when this new

roduct! the firm is going to introduce! will the sales of the e%isting roducts also

increase6 are they comlementary to each other$ In financial terms! therefore we

need to consider the sales of the new roducts lus the increase in sales of the

e%isting roducts$

G"i%e+ine No.:

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 27/55

'onsider the oosite of rule no 2 re/ the e%isting sales might reduce with the

introduction of the new roducts$ Factored the loss of re"enue from such e%isting

roducts into the caital budgeting analysis$

G"i%e+ine No.:

Ignore sunk costs and consider only those costs which are rele"ant to the

ro#ects$

G"i%e+ine No.H:

Incororate any 7=T additional working caital re4uirements into the caital

budgeting analysis for e%amle the need to ha"e additional in"entories! accounts

recei"ables and or cash increase in current assets< minus additional financing

from accounts ayable! bank borrowings current liabilities< .

G"i%e+ine No.:

=%cludes Interest Payments as this is already reflected in the discount rate this

rate imlicitly accounts for the cost of raising the financing<$

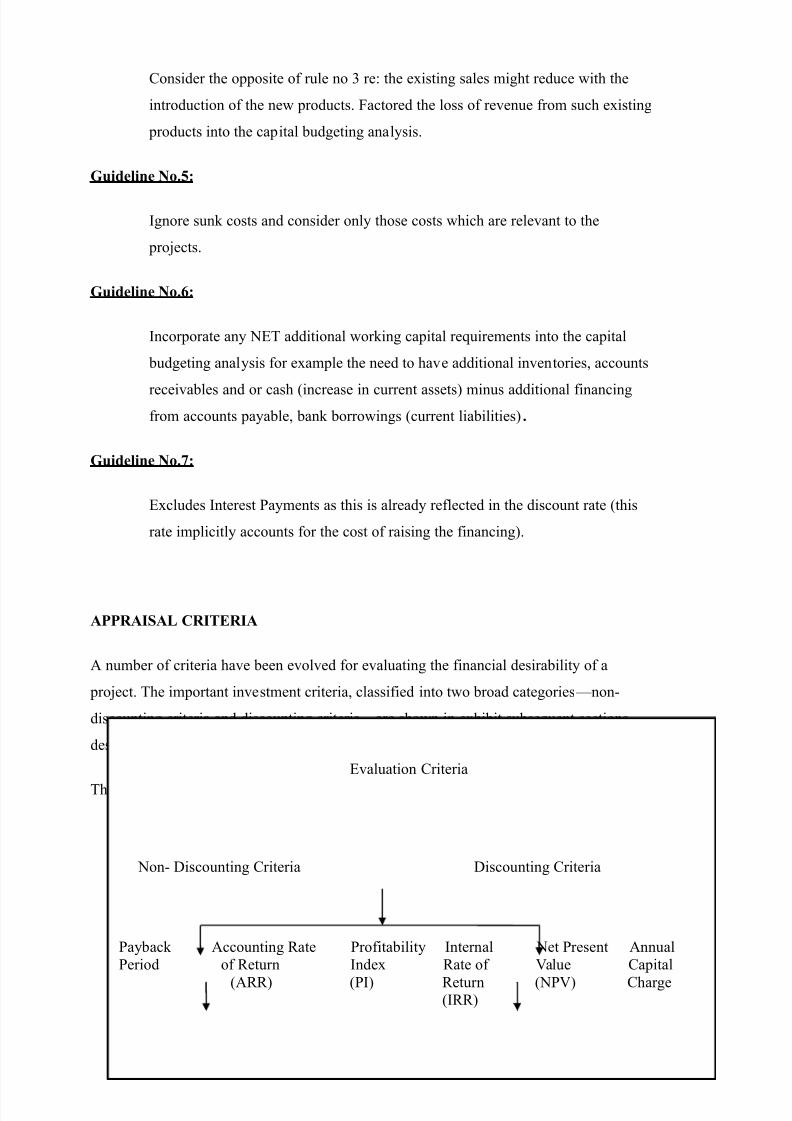

APPRAISAL CRITERIA

A number of criteria ha"e been e"ol"ed for e"aluating the financial desirability of a

ro#ect$ The imortant in"estment criteria! classified into two broad categoriesLnon6

discounting criteria and discounting criteriaLare shown in e%hibit subse4uent sections

describe and e"aluate these criteria in some detail/

These criteria can be classifies as follows/

="aluation 'riteria

7on6 Discounting 'riteria Discounting 'riteria

Payback Accounting +ate Profitability Internal 7et Present AnnualPeriod of +eturn Inde% +ate of Jalue 'aital A++< PI< +eturn 7PJ< 'harge

I++<

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 28/55

Co$p!rin2 Met*o% o, <!+"!tion "n%er <!rio" Scen!rio

Met*o% In%epen%entProject

M"t"!++& E6c+"i8eProject

C!pit!+R!tionin2

Sc!+e Di,,erence

I++ Accetable 7ot Accetable 7ot Accetable 7ot Accetable

MI++ Accetable 7ot Accetable 7ot Accetable 7ot Accetable

7PJ Accetable Accetable Accetable Accetable

Payback 7ot Accetable 7ot Accetable 7ot Accetable 7ot Accetable

Discounted 7ot Accetable 7ot Accetable 7ot Accetable 7ot Accetable

Many formal methods are used in caital budgeting! including the techni4ues such as

Dico"ntin2 Criteri!

Net Preent <!+"e

Pro,it!#i+it& In%e6 or Bene,it Cot R!tio

Intern!+ R!te o, Ret"rn

Mo%i,ie% Intern!+ R!te o, Ret"rn

E1"i8!+ent Ann"it& or Ann"!+ C!pit!+ C*!r2e

These methods use the incremental cash flows from each otential in"estment! or ro#ect$

Techni4ues based on accounting earnings and accounting rules are sometimes used 6 though

economists consider this to be imroer 6 such as the accounting rate of return! and return

on in"estment$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 29/55

Non)Dico"ntin2 Criteri!

Simlified and hybrid methods are used as well! such as

P!&#!c Perio%

Dico"nte% P!&#!c Perio%

A8er!2e r!te o, Ret"rn

Dico"ntin2 Criteri!

@. Net Preent <!+"e

=ach otential ro#ect.s "alue should be estimated using a discounted cash flow D'F<

"aluation! to find its net resent "alue 7PJ<$ First alied to 'ororate Finance by oel

Dean in 0@80<$ This "aluation re4uires estimating the si-e and timing of all of the

incremental cash flows from the ro#ect$ These future cash flows are then discounted to

determine their resent "alue$ These resent "alues are then summed! to get the 7PJ$ See

also Time "alue of money$ The 7PJ decision rule is to accet all ositi"e 7PJ ro#ects in

an unconstrained en"ironment! or if ro#ects are mutually e%clusi"e! accet the one with the

highest 7PJ 9=<$

The 7PJ is greatly affected by the discount rate! so selecting the roer rate 6 sometimes

called the hurdle rate 6 is critical to making the right decision$ The hurdle rate is the

minimum accetable return on an in"estment$ It should reflect the riskiness of the

in"estment! tyically measured by the "olatility of cash flows! and must take into account

the financing mi%$ Managers may use models such as the 'APM or the APT to estimate a

discount rate aroriate for each articular ro#ect! and use the weighted a"erage cost of

caital (A''< to reflect the financing mi% selected$ A common ractice in choosing a

discount rate for a ro#ect is to aly a (A'' that alies to the entire firm! but a higher

discount rate may be more aroriate when a ro#ect.s risk is higher than the risk of the

firm as a whole$ The formula is as follows/

PJ N 0

0Or<n

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 30/55

(here PJ N Present Jalue

r N rate of interest H discount rate

n N number of years

Deciion R"+e

A. C!pit!+ R!tionin2 it"!tion

• Select ro#ects whose 7PJ is ositi"e or e4ui"alent to -ero$

• Arrange in the descending order of 7PJs$

• Select Pro#ects starting from the list till the caital budget allows$

B. No c!pit!+ R!tionin2 Sit"!tion

• Select e"ery ro#ect whose 7PJ N

C. M"t"!++& E6c+"i8e Project

• Select the one with a higher 7PJ$

E6!$p+e

Assuming that the cost of caital is G for a ro#ect in"ol"ing a lumsum cash outflow of

+s$C!1 and cash inflow of +s$1! er annum for 8 years! the 7et Present Jalue

calculations are as follows/

a< Present "alue of cash outflows +s$C1 b< Present "alue of cash inflows

Present "alue of an annuity of +s$0 at G for 8 yearsN5$101

Present "alue of +s$1 annuity for 8 years N 5$101 Q 1 N +s$C515

c< 7et resent "alue N resent "alue of cash inflows 6 resent "alue of cash

outflows N C515 6C1 N +s$115

Since the net resent "alue of the ro#ect is ositi"e +s$115<! the ro#ect is acceted$

. Pro,it!#i+it& In%e6

Profitability inde% identifies the relationshi of in"estment to ayoff of a roosed ro#ect$

The ratio is calculated as follows/

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 31/55

Pro,it!#i+it& In%e6 Q P< o, ("t"re C!* (+o0 P< o, Initi!+ In8et$ent

Profitability Inde% is also known as Pro,it In8et$ent R!tio! abbre"iated to P$I$ and <!+"e

In8et$ent R!tio J$I$+$<$ Profitability inde% is a good tool for ranking ro#ects because it

allows you to clearly identify the amount of "alue created er unit of in"estment$

A ratio of 0 is logically the lowest accetable measure on the inde%$ Any "alue lower than

one would indicate that the ro#ect.s PJ is less than the initial in"estment$ As "alues on the

rofitability inde% increase! so does the financial attracti"eness of the roosed ro#ect$

R"+e for selection or re#ection of a ro#ect/

• If PI 0 then accet the ro#ect

• If PI R 0 then re#ect the ro#ect

Deciion R"+e

A. C!pit!+ R!tionin2 Sit"!tion

• Select all ro#ects whose rofitability inde% is greater than or e4ual to 0$

• +ank them in descending order of their rofitability indices$

• Select ro#ects starting from the to of the list till the caital budget

B. No C!pit!+ R!tionin2 Sit"!tion

• Select e"ery ro#ect whose PI N 0$

C. M"t"!++& E6c+"i8e Project

• Select the ro#ect with higher PI$

E6!$p+e

• A new machine costs +s$C!1 and generates cash inflow after ta%<er annum of

+s$1! during its life of 8 years$ :et us assume that the cost of caital for the

comany is G$

• The resent "alue of the cash inflows at G discount rate is 1 Q 5$101 N C515$

The resent "alue of outflow is C!1$ The rofitability inde% is C515HC1< N0$1?$

• The rofitability inde% of 0$1? leads to an accetance decision of the

ro#ect! since it is greater than 0$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 32/55

. Intern!+ R!te o, Ret"rn

The intern!+ r!te o, ret"rn I++< is defined as the discount rate that gi"es a net resent

"alue 7PJ< of -ero$ It is a commonly used measure of in"estment efficiency$

The I++ method will result in the same decision as the 7PJ method for non6mutually

e%clusi"e< ro#ects in an unconstrained en"ironment! in the usual cases where a negati"e

cash flow occurs at the start of the ro#ect! followed by all ositi"e cash flows$ In most

realistic cases! all indeendent ro#ects that ha"e an I++ higher than the hurdle rate should

be acceted$ 7e"ertheless! for mutually e%clusi"e ro#ects! the decision rule of taking the

ro#ect with the highest I++ 6 which is often used 6 may select a ro#ect with a lower 7PJ$

3ne shortcoming of the I++ method is that it is commonly misunderstood to con"ey the

actual annual rofitability of an in"estment$ *owe"er! this is not the case because

intermediate cash flows are almost ne"er rein"ested at the ro#ect.s I++ and! therefore! the

actual rate of return is almost certainly going to be lower$ Accordingly! a measure called

Modified Internal +ate of +eturn MI++< is often used$

Deciion R"+e

A. C!pit!+ R!tionin2 Sit"!tion

• Select those ro#ects whose I++ r< N k! where k is the cost of caital$

• Arrange all the ro#ects in the descending order of their Internal +ate of +eturn$

• Select ro#ects from the to till the caital budget allows$

B. No C!pit!+ R!tionin2 Sit"!tion

• Accet e"ery ro#ect whose I++ r< N k! where k is the cost of caital$

C. M"t"!++& E6c+"i8e Project

• Select the one with higher I++$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 33/55

E6!$p+e

• In the resent case this is C1 di"ided by 1 N 5$0

The interest factor 5$0 for a 8 year ro#ect corresonds to a discount rate of ?$ So the I++

of the ro#ect is ?$ An interest factor of 5$0 indicates that the resent "alue of one +uee

annuity for 8 years at ? is e4ui"alent to 5 ruees and ten aise $

• The resent "alue of +s$1! annuity is 5$0 Q 1 N C1

• The resent "alue of cash inflows N +s$C1 and the resent "alue of cash outflow N

+s$C1$

• At ? the resent "alue of cash inflows is e4ui"ale to the resent "alue of cash

outflows$

• *ence ? is the I++ of the ro#ect$

. Mo%i,ie% Intern!+ R!te o, Ret"rn

MI++ is the discount rate that makes the future "alue of the ro#ect e4ual to its initial cost$

MI++ re4uires a rein"estment rate$

There are 2 basic stes of the MI++/

0< =stimate all cash flows as in I++$

1< 'alculate the future "alue of all cash inflows at the last year of the ro#ect,s life$

2< Determine the discount rate that causes the future "alue of all cash inflowsdetermined in ste 1! to be e4ual to the firm,s in"estment at time -ero$ This discount

rate is known as the MI++$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 34/55

Deciion r"+e

Take the ro#ect if MI++ is larger than the re4uired rate$

Di!%8!nt!2e

MI++ cannot rank mutually e%clusi"e ro#ects$

. E1"i8!+ent Ann"it& Met*o%

The e4ui"alent annuity method e%resses the 7PJ as an annuali-ed cash flow by di"iding it

by the resent "alue of the annuity factor$ It is often used when assessing only the costs of

secific ro#ects that ha"e the same cash inflows$ In this form it is known as the e4ui"alent

annual cost =A'< method and is the cost er year of owning and oerating an asset o"er its

entire lifesan$

It is often used when comaring in"estment ro#ects of une4ual lifesan$ For e%amle if

ro#ect A has an e%ected lifetime of ? years! and ro#ect B has an e%ected lifetime of 00

years it would be imroer to simly comare the net resent "alues 7PJs< of the two

ro#ects! unless the ro#ects could not be reeated$

The use of the =A' method imlies that the ro#ect will be relaced by an identical ro#ect$

Re!+ Option

+eal otions analysis has become imortant since the 0@?s as otion ricing models ha"e

gotten more sohisticated$ The discounted cash flow methods essentially "alue ro#ects as if

they were risky bonds! with the romised cash flows known$ But managers will ha"e many

choices of how to increase future cash inflows! or to decrease future cash outflows$ In other

words! managers get to manage the ro#ects 6 not simly accet or re#ect them$ +eal otions

analyses try to "alue the choices 6 the otion "alue 6 that the managers will ha"e in the

future and adds these "alues to the 7PJ$

R!ne% Project

The real "alue of caital budgeting is to rank ro#ects$ Most organi-ations ha"e many

ro#ects that could otentially be financially rewarding$ 3nce it has been determined that a

articular ro#ect has e%ceeded its hurdle! then it should be ranked against eer ro#ects e$g$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 35/55

6 highest Profitability inde% to lowest Profitability inde%<$ The highest ranking ro#ects

should be imlemented until the budgeted caital has been e%ended$

Non)Dico"ntin2 Criteri!

@. P!&#!c Perio%

Payback eriod is the time duration re4uired to recou the in"estment committed to a

ro#ect$ Business enterrises following ayback eriod use stiulated ayback eriod!which acts as a standard for screening the ro#ect$ 3f Technology Madras

Co$p"t!tion o, P!&#!c Perio%

(hen the cash inflows are uniform the formula for ayback eriod is

'ash 3utlay of the Pro#ect or 3riginal 'ost of the Asset

Annual 'ash Inflow

• (hen the cash inflows are une"en! the cumulati"e cash inflows are to be arri"ed at

and then the ayback eriod has to be calculated through interolation$

• *ere ayback eriod is the time when cumulati"e cash inflows are e4ual to the

outflows$ i$e$!

In,+o0 Q O"t,+o0

P!&#!c Reciproc!+ R!te

• The ayback eriod is stated in terms of years$ This can be stated in terms of

ercentage also$ This is the ayback recirocal rate$

• +ecirocal of ayback eriod N 0Hayback eriod % 0

A. C!pit!+ R!tionin2 Sit"!tion

• Select the ro#ects which ha"e ayback eriods lower than or e4ui"alent to the

stiulated ayback eriod$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 36/55

• Arrange these selected ro#ects in increasing order of their resecti"e ayback

eriods$

• Select those ro#ects from the to of the list till the caital budget is e%hausted$

Deciion R"+e

M"t"!++& E6c+"i8e Project

In the case of two mutually e%clusi"e ro#ects! the one with a lower ayback eriod is

acceted! when the resecti"e ayback eriods are less than or e4ui"alent to the stiulated

ayback eriod$

Deter$in!tion o, Stip"+!te% P!&#!c Perio%

• Stiulated ayback eriod! broadly! deends on the nature of the businessHindustry

with resect to the roduct! technology used and seed at which technological

changes occur! rate of roduct obsolescence etc$

• Stiulated ayback eriod is! thus! determined by the management.s caacity to

e"aluate the en"ironment "ia6a6"ia the enterrise.s roducts! markets and distribution

channels and identify the ideal6business design and secify the time target$

A%8!nt!2e o, P!&#!c Perio%

• It is easy to understand and aly$ The concet of reco"ery is familiar to e"ery

decision6maker$

• It is cost effecti"e$ It can be used e"en by a small firms ha"ing limited manower

that is not trained in any other sohisticated techni4ues$

• The ayback eriod measures the direct relationshi between annual cash inflows

from a roosal and the net in"estment re4uired$

• The ayback eriod also deals with risk$ The ro#ect with shorter ayback eriod

will be usually less risky

• Business enterrises facing uncertainty 6 both of roduct and technology 6 will

benefit by the use of ayback eriod method since the stress in this techni4ue is on

early reco"ery of in"estment$ So enterrises facing technological obsolescence and

roduct obsolescence 6 as in electronicsHcomuter industry 6 refer ayback eriod

method$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 37/55

• :i4uidity re4uirement re4uires earlier cash flows$ *ence! enterrises ha"ing high

li4uidity re4uirement refer this tool since it in"ol"es minimal waiting time for

reco"ery of cash outflows as the emhasis is on early recoument of in"estment$

Di!%8!nt!2e o, P!&#!c Perio%

The time "alue of money is ignored$

But this drawback can be set right by using the discounted ayback eriod method$

The discounted ayback eriod method looks at reco"ery of initial in"estment after

considering the time "alue of inflows$

It ignores the cash inflows recei"ed beyond the ayback eriod$ In its emhasis on

early reco"ery! it often re#ects ro#ects offering higher total cash inflow$

In"estment decision is essentially concerned with a comarison of rate of return

romised by a ro#ect with the cost of ac4uiring funds re4uired by that ro#ect$

Payback eriod is essentially a time concet it does not consider the rate of return$

E6!$p+e

There are two ro#ects ro#ect a and b< a"ailable for a 'omany! with a life of G

years each and re4uiring a caital outlay of rs$@!H6 each and additional working

caital of rs$0H6 each$The cash inflows comrise of rofit after ta% O Dereciation O Interest Ta%

ad#usted< for fi"e years and sal"age "alue of +s$8H6 for each ro#ect lus working

caital released in the Gth year$ This comany has rescribed a hurdle ayback

eriod of 2 years$ (hich of the two ro#ects should be selectedV

E6!$p+e ) D!t!

Pro#ect A'umulati"e'ash Inflowsof Pro#ect A

Pro#ect B'umulati"e'ash Inflowsof Pro#ect B

Kear 0 2!2!

1!1!

Kear 1 2!8G!8

1!85!8

Kear 2 2!80!

1!8?!

Kear 5 0!8 00! 1!8 @!8

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 38/55

Kear 8 0!802!

2!01!8

Kear G 2!0G!

8!80C!

PaybackPeriod

2 years 5 years > 1months

E6!$p+e

W Payback eriod for Pro#ect A N 2 years cumulati"e cash inflows N outflows<

W Payback eriod for Pro#ect B N 5 years O 8H2 N 5 years and 1 months$

7ote/ Interolation techni4ue is used here to identify the e%act eriod at which cumulati"ecash inflows will be e4ual to outflows$ The amount re4uired to e4uate is +s$8! while the

returns from the 8th year is 2!$ *ence the addition time duration re4uired to comute the

ayback eriod is 8H2< % 01 which is 1 months$ The interolation techni4ue is used

based on the assumtion that cash inflows accrue uniformly throughout the year$<

T*e in8et$ent %eciion 0i++ #e to c*ooe Project A 0it* ! p!&#!c perio% o, &e!r

!n% reject Project B 0it* ! p!&#!c perio% o, &e!r !n% $ont*.

. Dico"nte% P!&#!c Perio%

In in"estment decisions! the number of years it takes for an in"estment to reco"er its initial

cost after accounting for inflation! interest! and other matters affected by the time "alue of

money! in order to be worthwhile to the in"estor $ It differs slightly from the ayback eriod

rule! which only accounts for cash flows resulting from an in"estment and does not take

into account the time "alue of money$ =ach in"estor determines hisHher own discounted

ayback eriod rule and! as such! it is a highly sub#ecti"e rule$ In general! howe"er! short6

term in"estors use a short number of years L or e"en months L for their discounted ayback eriod rules! while long6term in"estors measure their rules in years or e"en

decades$

. Acco"ntin2 R!te o, Ret"rn

Accounting rate of return is the rate arri"ed at by e%ressing the a"erage annual net rofit

after ta%< as gi"en in the income statement as a ercentage of the total in"estment or

a"erage in"estment$ The accounting rate of return is based on accounting rofits$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 39/55

Accounting rofits are different from the cash flows from a ro#ect and hence! in many

instances! accounting rate of return might not be used as a ro#ect e"aluation decision$

Accounting rate of return does find a lace in business decision making when the returns

e%ected are accounting rofits and not merely the cash flows$

Co$p"t!tion o, Acco"ntin2 R!te o, Ret"rn

The accounting rate of return using total in"estment$

or

Sometimes a"erage rate of return is calculated by using the following

formula/

N 7et Profit After Ta%

A"erage In"estment

(here a"erage in"estment N total in"estment di"ided by 1

Deciion R"+e

A. C!pit!+ R!tionin2 Sit"!tion

0 W Select the ro#ects whose rates of return are higher than the cut6off rate$

1 W Arrange them in the declining order of their rate of return$

2 W Select ro#ects starting from the to of the list till the caital a"ailable is e%hausted$

B. No C!pit!+ R!tionin2 Sit"!tion

Select all ro#ects whose rate of return are higher than the cut6off rate$

C. M"t"!++& E6c+"i8e Project

Select the one that offers highest rate of return$

Acco"ntin2 R!te o, Ret"rn / A%8!nt!2e

• It Is =asy To 'alculate$

• The Percentage +eturn Is More Familiar To The =%ecuti"es$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 40/55

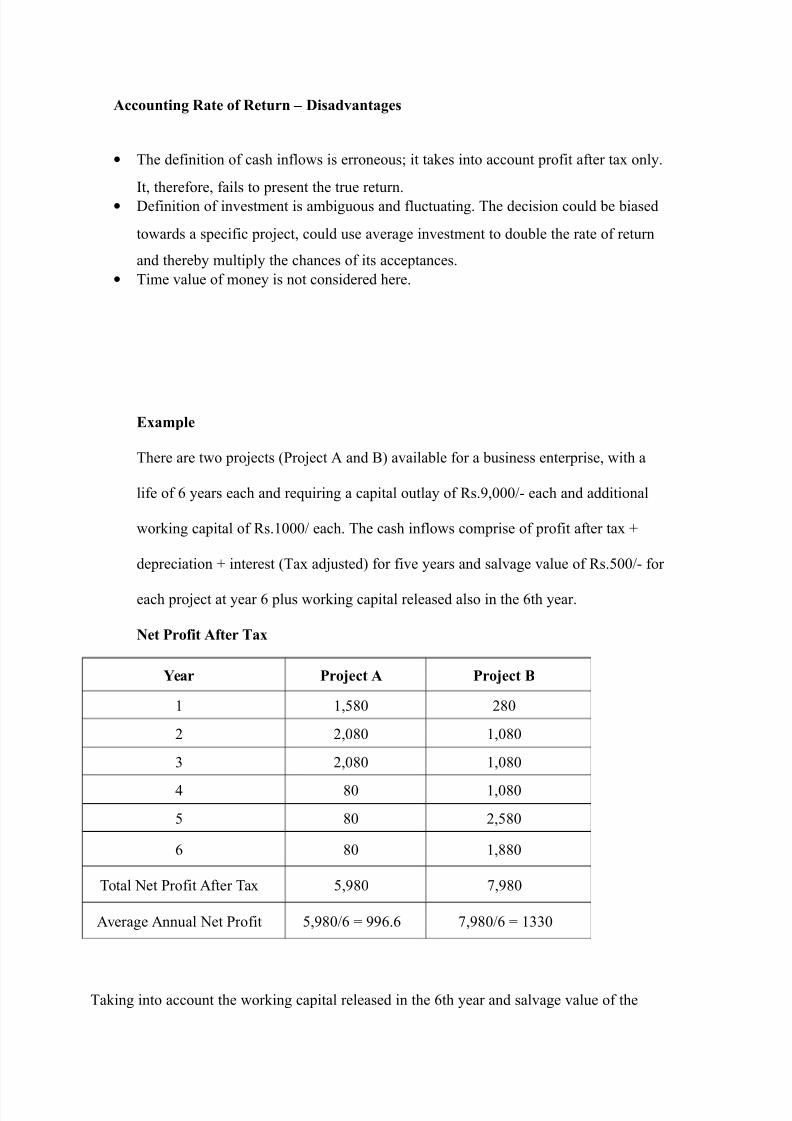

Acco"ntin2 R!te o, Ret"rn / Di!%8!nt!2e

• The definition of cash inflows is erroneous it takes into account rofit after ta% only$

It! therefore! fails to resent the true return$• Definition of in"estment is ambiguous and fluctuating$ The decision could be biased

towards a secific ro#ect! could use a"erage in"estment to double the rate of return

and thereby multily the chances of its accetances$

• Time "alue of money is not considered here$

E6!$p+e

There are two ro#ects Pro#ect A and B< a"ailable for a business enterrise! with a

life of G years each and re4uiring a caital outlay of +s$@!H6 each and additional

working caital of +s$0H each$ The cash inflows comrise of rofit after ta% O

dereciation O interest Ta% ad#usted< for fi"e years and sal"age "alue of +s$8H6 for

each ro#ect at year G lus working caital released also in the Gth year$

Net Pro,it A,ter T!6

Ye!r Project A Project B

0 0!8C 1C

1 1!C 0!C

2 1!C 0!C

5 C 0!C

8 C 1!8C

G C 0!CC

Total 7et Profit After Ta% 8!@C ?!@C

A"erage Annual 7et Profit 8!@CHG N @@G$G ?!@CHG N 022

Taking into account the working caital released in the Gth year and sal"age "alue of the

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 41/55

in"estment! the total in"estment will be 0!6 0!8< +s$C8 and the a"erage in"estment

will be C8H1< +s$518 for each ro#ect$

The rate of return calculations are/

7et rofit after ta% as a ercentage of total in"estment

Pro#ect APro#ect B

022 Q 0 N 08$G

C8

The in"estment decision will be to select Pro#ect B since its rate of return is higher than that

of Pro#ect A if they are mutually e%clusi"e$ If they are indeendent ro#ects both can be

acceted if the minimum re4uired rate of return is 00$? or less$

Di,,ic"+tie in C!pit!+ B"%2etin2

!5 Gener!+ %i,,ic"+tie:

=nsuring that forecasts are consistent across deartments<

• =liminating reducing< conflicts of interest

• +educing forecast bias/ the roortion of roosed ro#ects that ha"e a ositi"e 7PJ

is indeendent of the estimated oortunity cost of caital$

• Bottom6u and to6down lanning is necessary$

• 'ontrol ro#ects in rogress! Post6audit afterwards

• Try hard to measure incremental cash flows66when you can

• ="aluate erformance/ actual "ersus ro#ected actual "ersus absolute standard of the

true cost of caital

#5 Me!"re$ent pro#+e$:

(hile calculating the NP<' IRR' PAY BAC3 PERIOD' AND PRO(ITABILITY

INDE;' we ha"e to be "ery much careful with the calculations "alues throw it is a "erydifficult #ob to remember many "alues at a time but we ha"e to be care full because it willeffect on the total outut of ro#ect in decision making$

Ri !n% Uncert!int&:

Different caital in"estment roosals ha"e different degrees of risk and uncertainly there isa slight difference between risk and uncertainty risk in"ol"es situations in which the

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 42/55

robabilities of a articular e"ent occurring are known where as in uncertainty these robabilities are unknown$

In many cases these two terms are used inter changeably$ +isk in caital in"estments may be due to the general economic conditions cometition! technological de"eloments!consumer references etc$

3ne to these reasons the re"enues costs and economic life of a articular in"estment are notcertain$ (hile e"aluating caital in"estment roosals a roer ad#ustment should therefore

be made for risk and uncertainty

0

An!+&i o, ! Ne0 Project 0it* t*e *e+p o, C!pit!+ B"%2etin2 Proce.

Proosed caital/ H.@ millions

Di"ided in 1 hases

P*!e @ is roosed from J and is assumed to be caitali-ed on @@ and

P*!e is roosed from @ and is assumed to be caitali-ed on @$

6 about R. . millions slited in 1 years for the p*!e @ . million er year 5.

6 about R. . millions in the p*!e .

(ith an e%ected rate of return of 05 starting after 1 years$

Production lant is at Baddi *imachal Pradesh<

The ro#ect is about the roducing 1 roducts

6 Jials and6 Syringes$

The caital is di"ided between both the roduct

) R..@ millions in "ials and) R$ millions in syringes$

=%ecting annual a"erage roduction is/ 0C!! from FK 00 to FK 0?<$

Sales and "olumes are taken as er the BF+3( strategic lan$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 43/55

Xuotations from 9land! for the following roducts/ Indian manufacturing charges<

:i4uid Jial Yoledronic Acid< $0.75

:yo Jial Amifostin< $1.00

PFS =no%aarin 7a< $0.50

+oyalties will be ignored in case of de"eloment of the roduct$

The cost includes the urchase of assets for the roduction urose and the dereciation is

on the straight line method$

Freight cost taken at 8 g er ack of 0 "ials at +s 1Her kg to US weight$ S9>A costs taken in P>: as 1 on sales$

=ffecti"e Ta% rate is considered at C$C$

First let us see if the roduct is gi"en on contract then what is the cost that Dr$ +eddy,s is

going to incur/

Contr!ct M!n",!ct"rin2 +s$ Per Unit<

T&pe o, <i!+ E1"i8!+ent InjectionUSD

CCCC 4In R5

(rei2*

t

Ro&!+t&

4R5

7on:yohilised

Yoledronic Acid ; :i4 $?8 2$ 0$ 6

:yohilised Amifostin ; :yo 0$ 5$ 0$ 6

PrefilledSyringes

=no%aarin 7a $8 1$ 0$ 6

'' N 'on"ersion 'ost

Total cost incurred would be/ R. @

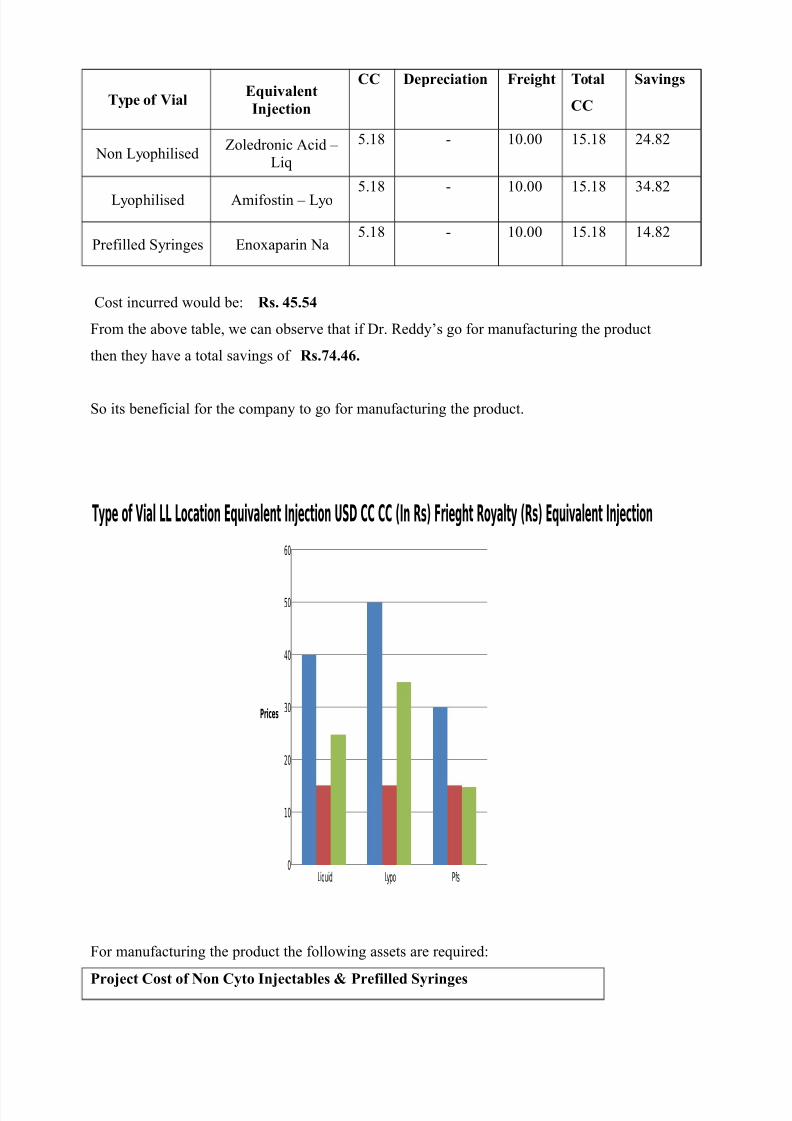

And if the roduct is manufactured at Dr$ +eddy,s! then what is the cost the organi-ation isgoing to incur/

Eti$!te% in Ne0 Project +s$ er Unit<

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 44/55

T&pe o, <i!+E1"i8!+ent

Injection

CC Depreci!tion (rei2*t Tot!+

CC

S!8in2

7on :yohilisedYoledronic Acid ;

:i4

8$0C 6 0$ 08$0C 15$C1

:yohilised Amifostin ; :yo 8$0C 6 0$ 08$0C 25$C1

Prefilled Syringes =no%aarin 7a8$0C 6 0$ 08$0C 05$C1

'ost incurred would be/ R. .

From the abo"e table! we can obser"e that if Dr$ +eddy,s go for manufacturing the roduct

then they ha"e a total sa"ings of R..H.

So its beneficial for the comany to go for manufacturing the roduct$

Liquid Lypo Pfs0

10

20

30

40

50

60

Type of Vial LL Location Equivalent Injection USD CC CC (In Rs) Frie!t Royalty (Rs) Equivalent Injection

"rices

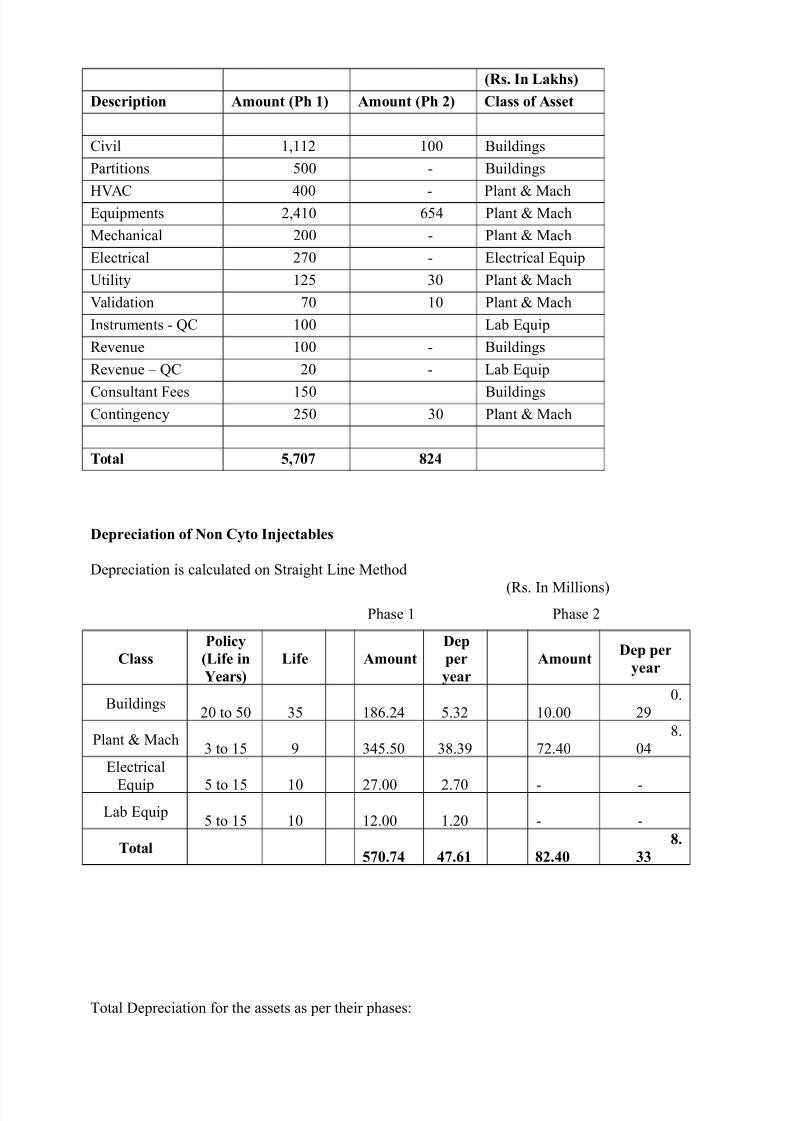

For manufacturing the roduct the following assets are re4uired/

Project Cot o, Non C&to Inject!#+e > Pre,i++e% S&rin2e

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 45/55

4R. In L!*5

Decription A$o"nt 4P* @5 A$o"nt 4P* 5 C+! o, Aet

'i"il 0!001 0 Buildings

Partitions 8 6 Buildings

*JA' 5 6 Plant > Mach=4uiments 1!50 G85 Plant > Mach

Mechanical 1 6 Plant > Mach

=lectrical 1? 6 =lectrical =4ui

Utility 018 2 Plant > Mach

Jalidation ? 0 Plant > Mach

Instruments 6 X' 0 :ab =4ui

+e"enue 0 6 Buildings

+e"enue ; X' 1 6 :ab =4ui

'onsultant Fees 08 Buildings

'ontingency 18 2 Plant > Mach

Tot!+ '

Depreci!tion o, Non C&to Inject!#+e

Dereciation is calculated on Straight :ine Method+s$ In Millions<

Phase 0 Phase 1

C+!

Po+ic&

4Li,e in

Ye!r5

Li,e A$o"nt

Dep

per

&e!r

A$o"ntDep per

&e!r

Buildings1 to 8 28

0CG$15 8$21 0$

$1@

Plant > Mach2 to 08 @

258$8 2C$2@ ?1$5

C$5

=lectrical=4ui 8 to 08 0

1?$ 1$? 6 6

:ab =4ui8 to 08 0

01$ 0$1 6 6

Tot!+

. .H@ .

.

Total Dereciation for the assets as er their hases/

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 46/55

Ye!r (Y

J

(Y

@

(Y

@@

(Y @ (Y

@

(Y

@

(Y

@

(Y @H (Y

@

Tot!+

De$ in Kear Phase 0<5?$G0

5?$G0 5?$G0

5?$G0

5?$G0

5?$G0 5?$G0

222$1?

De$ in Kear Phase1<

C$22 C$22 C$22 C$22 C$22 50$G8

Total De$ in Mln+s<

6 6 5?$G0

5?$G0 88$@5

88$@5

88$@5

88$@5 88$@5

2?5$@1

Con8erion Cot !t M!n",!ct"re i ! ,o++o0:

The Actual Total cost of the roduct i$e! The 'ost Sheet<

Actual Material ; Imorted $?

Actual Material ; India 0$82

Actual Packing ; Imorted 1$58

Actual Packing ; India 2$8?

Actual Inut Ta%es $22

Actual :anded cost $1

Actual Subcontractor $

Actual Material C$08

Actual Direct Dereciation $@5Actual Direct Manower $8@

Actual =TF $C

Actual *JA' $02

Actual Maintenance $C8

Actual 3ther Direct $1C

Actual 3ther Utility $05

Actual Power $C

Actual Xuantity $01

Actual Steams $

Actual 3"erhead 2$10

Actual Total 'ost 00$2G

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 47/55

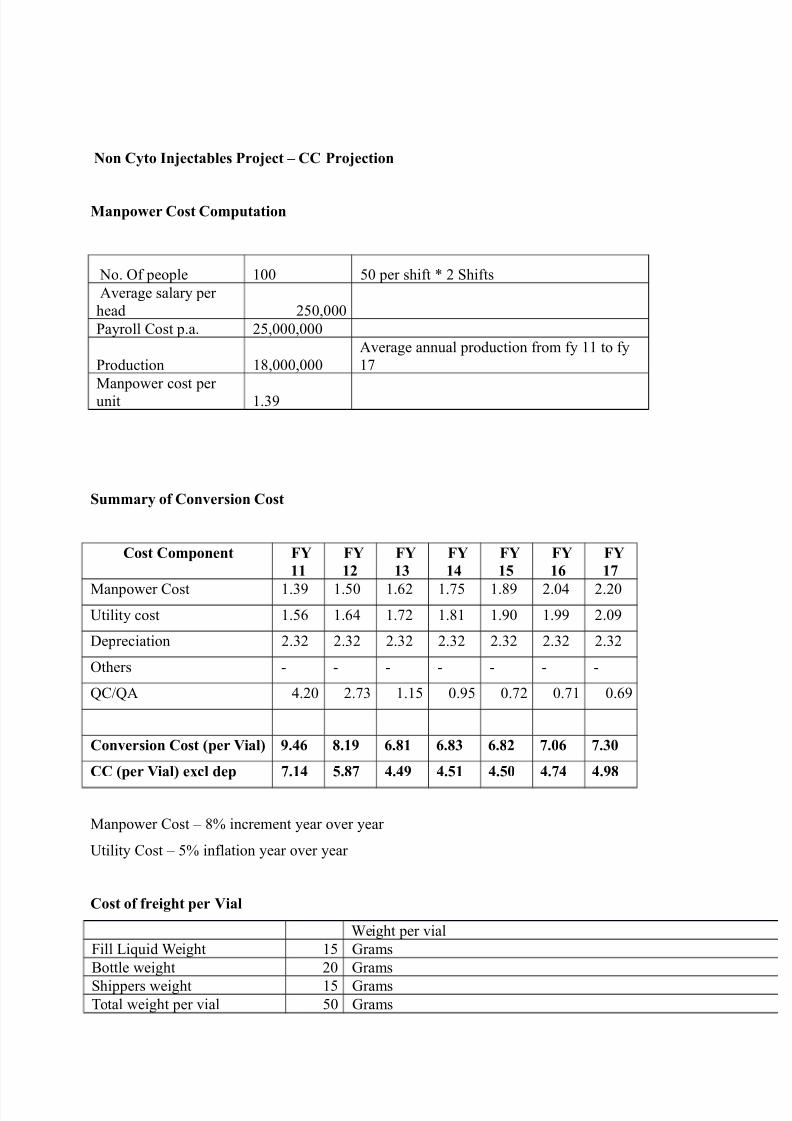

Non C&to Inject!#+e Project / CC Projection

M!npo0er Cot Co$p"t!tion

7o$ 3f eole 0 8 er shift Q 1 Shifts

A"erage salary erhead 18!

Payroll 'ost $a$ 18!!

Production 0C!!A"erage annual roduction from fy 00 to fy0?

Manower cost erunit 0$2@

S"$$!r& o, Con8erion Cot

Cot Co$ponent (Y

@@

(Y

@

(Y

@

(Y

@

(Y

@

(Y

@H

(Y

@Manower 'ost 0$2@ 0$8 0$G1 0$?8 0$C@ 1$5 1$1

Utility cost 0$8G 0$G5 0$?1 0$C0 0$@ 0$@@ 1$@

Dereciation 1$21 1$21 1$21 1$21 1$21 1$21 1$21

3thers 6 6 6 6 6 6 6

X'HXA 5$1 1$?2 0$08 $@8 $?1 $?0 $G@

Con8erion Cot 4per <i!+5 J.H .@J H.@ H. H. .H .

CC 4per <i!+5 e6c+ %ep .@ . .J .@ . . .J

Manower 'ost ; C increment year o"er year

Utility 'ost ; 8 inflation year o"er year

Cot o, ,rei2*t per <i!+

(eight er "ial

Fill :i4uid (eight 08 9ramsBottle weight 1 9rams

Shiers weight 08 9rams

Total weight er "ial 8 9rams

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 48/55

'ost er kg by air to US 1 +s$ Per kg

Freight cost er "ial 0 +s$ Per bottle

Co$p"t!tion o, t*e project:

A 'omarison of 'aital Budgeting Techni4ues +s$ in Millions<

<i!+ (!ci+it& ) P!&#!c perio% co$p"t!tion

Outflow Inflow Tax

Year Outflow

LiquidVials

LypoVials P! !"#

et Inlow

%& '0(

%is)ounted In flow

&u*%is)ntd In

flow

1 +,0.-7

/+,0.-7

1.00 /+,0.-7

/+,0.-7

+ +,0.-7

/+,0.-7

1.00 /+,0.-7

/5+0.7

- 1.00 /5+0.7

1-.22 +.5 11.75 152.03 1.00 152.03 /-,+.,5

5 57.0 12-.+ 7.50 15.3- 13., 1.00 13., /+1-.13

, ++5.0, 12.35 +,.3 +70.35 1.00 +70.35 57.7,

7 +52.+7 +.1+ --.+5 -15.,5 1.00 -15.,5 -7-.1

2 -37.0+ ,,.,0 5-.- 517.05 1.00 517.05 230.5

3 1,.23 70.7+ +2.0- 515., 1.00 515., 140,.03

10 -7.-, 7.+ +3.-5 50.35 1.00 50.35 1437.0

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 49/55

P!&#!c Perio% i &e!r $ont*

Pre (i++e% S&rin2e (!ci+it& ) P!&#!c perio% co$p"t!tion

Kear 3utflow+s$ Mn

In flow+s$ Mn on 7on:yo

In flow+s$ Mn on

:yo

In

flow+s$

Mn onPFS

7et InFlow

D'FZ

DiscntdIn flow

'umDiscntdIn flow

18$ 18$< 0$ 18$< 18$<

0 18$ 6 18$< 0$ 18$< 8$<

1 6 6 0$ 6 8$<

2 0$ 0$ 0$ 0$ 5@$<

5 18$ @$1 08$C< 0$ 08$C< G5$C<

80$

5 0$5 0$ 0$5 28$15G

052$G? 052$G? 0$ 052$G? 0?C$@0

?10@$5

1 10@$51 0$ 10@$51 2@C$22

C11C$C

C 11C$CC 0$ 11C$CC G1?$10

@ 12C$8C 12C$8C 0$ 12C$8C CG8$?@

P!&#!c i Ye!r Mont*

Tot!+ Project ) P!&#!c perio% co$p"t!tion

Outflow Inflow Tax

Year Proe)t&ost

LiquidVials

LypoVials

P! !"# et Inlow

%& '0(

%is)ntdIn flow

&u*%is)ntd In

flow

1 +25.-7

/+25.-7

1.00 /+25.-7

/+25.-7

+ +25.-7

/+25.-7

1.00 /+25.-7

/570.7

-

1.00

/570.7

1-.22 +.5 1.00 11.75 153.03 1.00 153.03 /11.,55

2+.0 12-.+ 7.50 3.+0 15.3- 1--.,, 1.00 1--.,, /+77.33,

++5.0, 12.35 100.0 +,.3 -70.32 1.00 -70.32 3-.007

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 50/55

+52.+7 +.1+ 1-.,7 --.+5 53.-+ 1.00 53.-+ 55+.-1

2

-37.0+ ,,.,0 +13.+ 5-.- 7-,.7 1.00 7-,.7 14+22.723

1,.23 70.7+ ++2.22 +2.0- 7.51 1.00 7.51 +40--.-010

-7.-, 7.+ +-2.52 +3.-5 773.5 1.00 773.5 +421+.2-

P!&#!c perio%:

The C!* O"t,+o0 is the ro#ect cost i$e$! the in"estment done by the comany$

C!+c"+!tion o, In,+o0:

The comany has made a market research and has gi"en the estimated "olumes for the

roduct from US! =U and +o( +est 3f (orld<$

And then has multilied it with the sa"ings of each roduct to get the inflows$

For e%amle/

Jolumes of US li4uid "ials< / 8$C

Sa"ings for li4uid "ials / 15$C1

'ash inflow for li4uid "ials/ 052$CC

CC S!8in2 ) Tot!+ Project ) NP< co$p"t!tion

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 51/55

3utflow

Inflows Ta%

Kear

Pro#ect'ost

:i4uidJials

:yoJials

PFS S=Y 7etInflows

D'FZ05

DiscountedInflow

0

1C8$2? 6 6 6 6 1C8$2?< 0$ 1C8$2?<

1

1C8$2? 6 6 6 6 1C8$2?< $CC 18$21<

2 6 6 6 6 6 6 $?? 6

5 6 052$CC 1$58 0$ 00$?8 08@$@ $G? 0?$2C

8 C1$5 0C2$51 ?$8 @$1 08$@2 022$GG $8@ ?@$05

G

6 118$G 0C$@8 0$5 1G$@5 2?$@C $81 0@1$GC?

6 18C$1? 15$01 052$G? 22$18 58@$21 $5G 1@$1G

C 6 2@?$1 GG$G 10@$51 82$52 ?2G$5? $5 1@5$21

@ 6 50G$C@ ?$?1 11C$CC 1C$2 ?55$80 $28 1G0$

0

6 52?$2G ?5$15 12C$8C 1@$28 ??@$85 $20 12@$?0

NP< o, t*e CC S!8in2 @J.H

CC S!8in2 ) Tot!+ Project ) IRR co$p"t!tion

3utflow Inflows Ta%

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 52/55

Kear Pro#ect'ost

:i4uidJials

:yoJials PFS S=Y

7et InFlow D'F

Discntd Inflow

0 1C8$2? 6 6 6 6 1C8$2?<

0$ 1C8$2?<

1 1C8$2? 6 6 6 6 1C8$2?<

$?8 102$0@<

2 6 6 6 6 6 6 $8G 6

5 6 052$CC 1$58 0$ 00$?8 08@$@ $51 GG$22

8 C1$5 0C2$51 ?$8 @$1 08$@2 022$GG $20 50$G5

G 6 118$G 0C$@8 0$5 1G$@5 2?$@C $12 CG$22

? 6 18C$1? 15$01 052$G? 22$18 58@$21 $0? ?@$C8

C 6 2@?$1 GG$G 10@$51 82$52 ?2G$5? $02 @8$G8

@ 6 50G$C@ ?$?1 11C$CC 1C$2 ?55$80 $0 ?1$15

0 6 52?$2G ?5$15 12C$8C 1@$28 ??@$85 $? 8G$80

7PJ of '' sa"ings

I++ of '' sa"ings 25

Proce%"re ,o++o0e% #& Dr. Re%%&’ 0*i+e e+ectin2 ! Project:

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 53/55

(hen a new roosal comes to Dr$ +eddy,s then it goes through se"eral imortant decisions

before selecting the roosal$

:et,s us assume that a roosal has come to Dr$ +eddy,s

0$ First the roosal goes to the Business De"eloment team$1$ Business De"eloment team with the hel of market research team! does the necessary

market sur"ey about the ro#ect such as

• *ow many alternati"e roducts are already in the marketV

• About the roduct and its rices$

• About its demand$

• About its cometitors$

which they disclose it in their annual reort$3nce the ro#ect is e"aluated then they decide from their organi-ation,s oint of "iew$

• In"estment re4uired in the ro#ect$

• Time of the roosal

2$ Then they reare a strategic reort with all the details such as rofits! cost! etc$! based

on it they decide whether to manufacture the roduct or get it don,t on the contract basis$5$ If the roduct is to be manufactured then the manufacturing team decides the cost of

materials re4uired! machines! ower! buildings! etc$! which hel them to arri"e at the

ro#ect cost$8$ 7ow the ro#ect comes to the finance deartment! where ayback eriod! ta%es!

dereciation! etc$! is found out with the coordination with IPD3 Integrated Product

De"eloment 3erations< team$G$ 9enerally 1 years ayback eriod is considered ideal at Dr$ +eddy,s because as these are

fast mo"ing roducts and chances are there that may be your cometitors may go a ste

ahead in roducing the roduct$?$ 7ow after all the figures and facts are found out! the roosal goes to Managing

Director$ Presentation is made to him with all the details which shows the ros and cons

of the roosal$$C$ Then suggestions are gi"en by the management! budget is decided and a final decision is

taken by the management whether to consider the roosal or re#ect it$

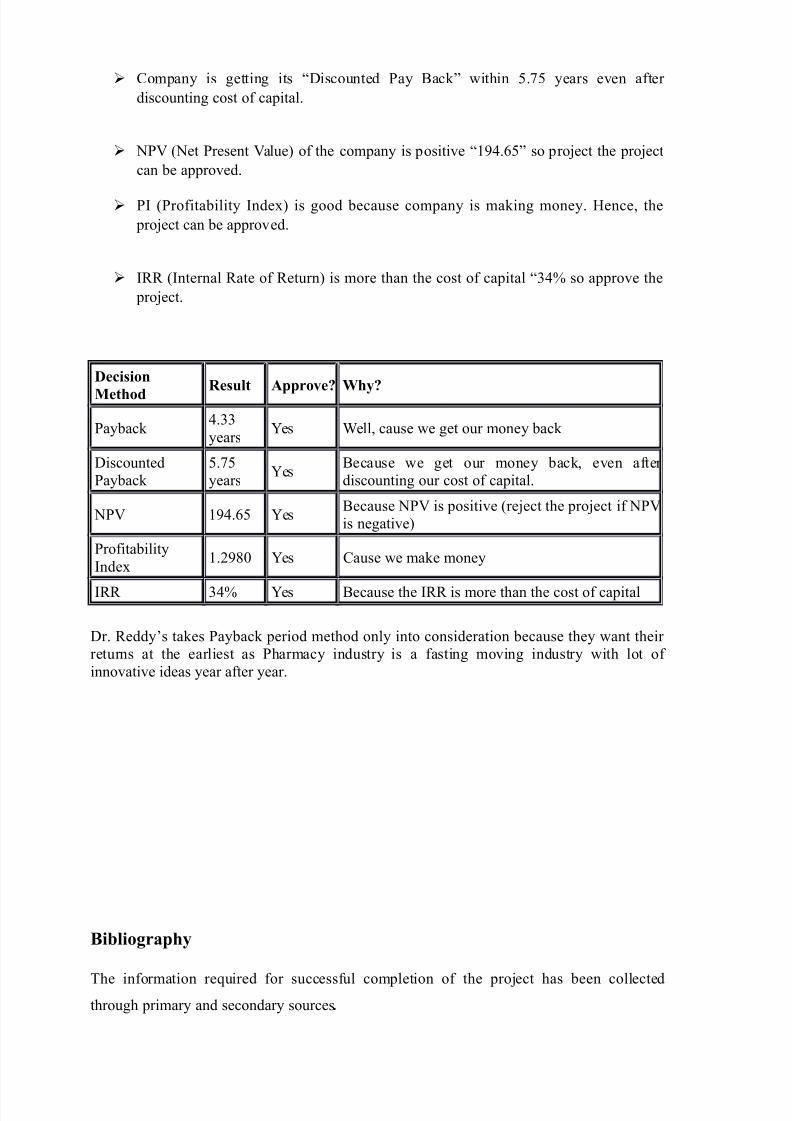

CONCLUSION > SUGGESTIONS

Decision and re"iew of ro#ect

'omany is getting its ayback after 5 years aro%imately 5$22 years< Pro#ect can be aro"ed such that comany can get back its rofit with in a limited eriod$

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 54/55

'omany is getting its &Discounted Pay Back) within 8$?8 years e"en after

discounting cost of caital$

7PJ 7et Present Jalue< of the comany is ositi"e &0@5$G8) so ro#ect the ro#ect

can be aro"ed$

PI Profitability Inde%< is good because comany is making money$ *ence! the

ro#ect can be aro"ed$

I++ Internal +ate of +eturn< is more than the cost of caital &25 so aro"e the

ro#ect$

DeciionMet*o%

Re"+t Appro8e -*&

Payback 5$22years

Kes (ell! cause we get our money back

DiscountedPayback

8$?8years

KesBecause we get our money back! e"en after discounting our cost of caital$

7PJ 0@5$G8 KesBecause 7PJ is ositi"e re#ect the ro#ect if 7PJis negati"e<

Profitability

Inde%

0$1@C Kes 'ause we make money

I++ 25 Kes Because the I++ is more than the cost of caital

Dr$ +eddy,s takes Payback eriod method only into consideration because they want their returns at the earliest as Pharmacy industry is a fasting mo"ing industry with lot of inno"ati"e ideas year after year$

Bi#+io2r!p*&

The information re4uired for successful comletion of the ro#ect has been collected

through rimary and secondary sources .

7/24/2019 Capital Budgeting Dr Reddy

http://slidepdf.com/reader/full/capital-budgeting-dr-reddy 55/55

Pri$!r& So"rce D!t!

The data has been gathered through interactions with the "arious officials and emloyees

working in the di"ision$ Some imortant information has been gathered through coule of

instructed inter"iews$

Secon%!r& So"rce D!t!

+eferred te%t books for collecting the information regarding the theoretical asects of the

toic$

(in!nci!+ M!n!2e$ent ) I .M P!n%e&

M!n!2e$ent Acco"ntin2 / R. P. Tri8e%i

Ann"!+ Report o, Dr. Re%%&’ / )

Annual reorts! maga-ines ublished by the comany are used for collecting the re4uired

information$ ="en hel is taken from internet$

000.%rre%%&.co$

*ttp:$one&.re%i,,.co$

*ttp:000.p*!r$!ce"tic!+)%r"2)$!n",!ct"rer.co$p*!r$!ce"tic!+)in%"tr&

*ttp:en.0iipe%i!.or2