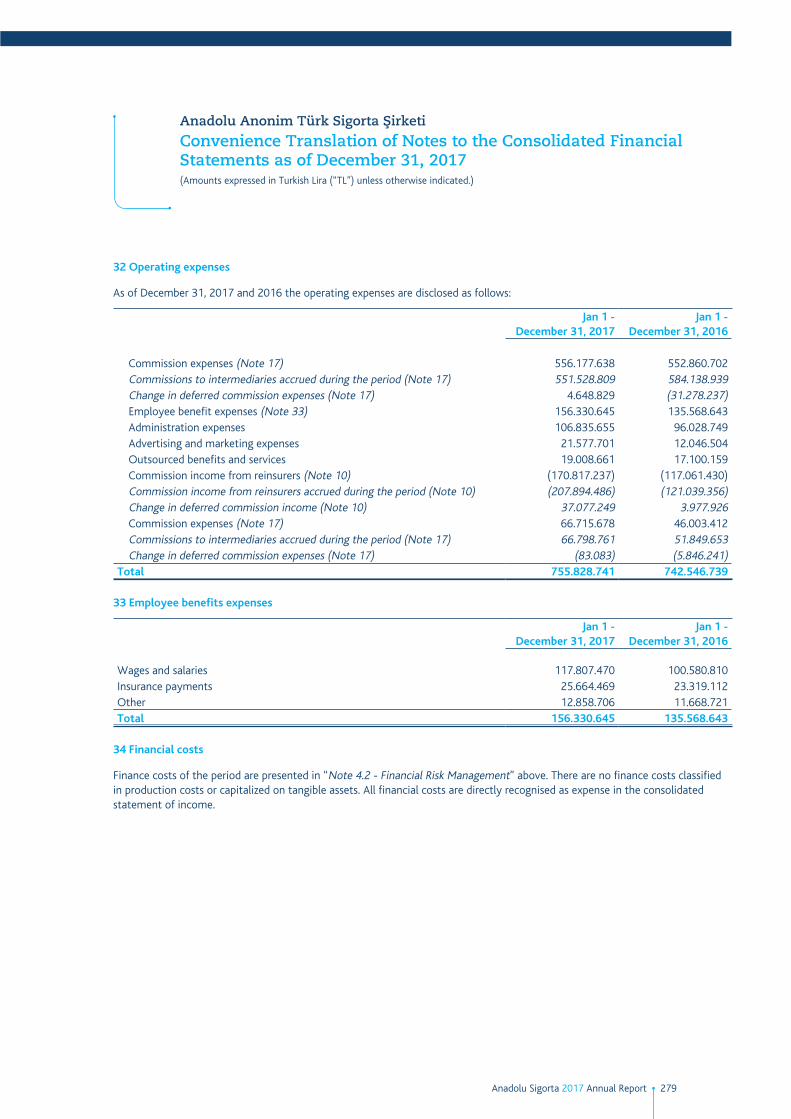

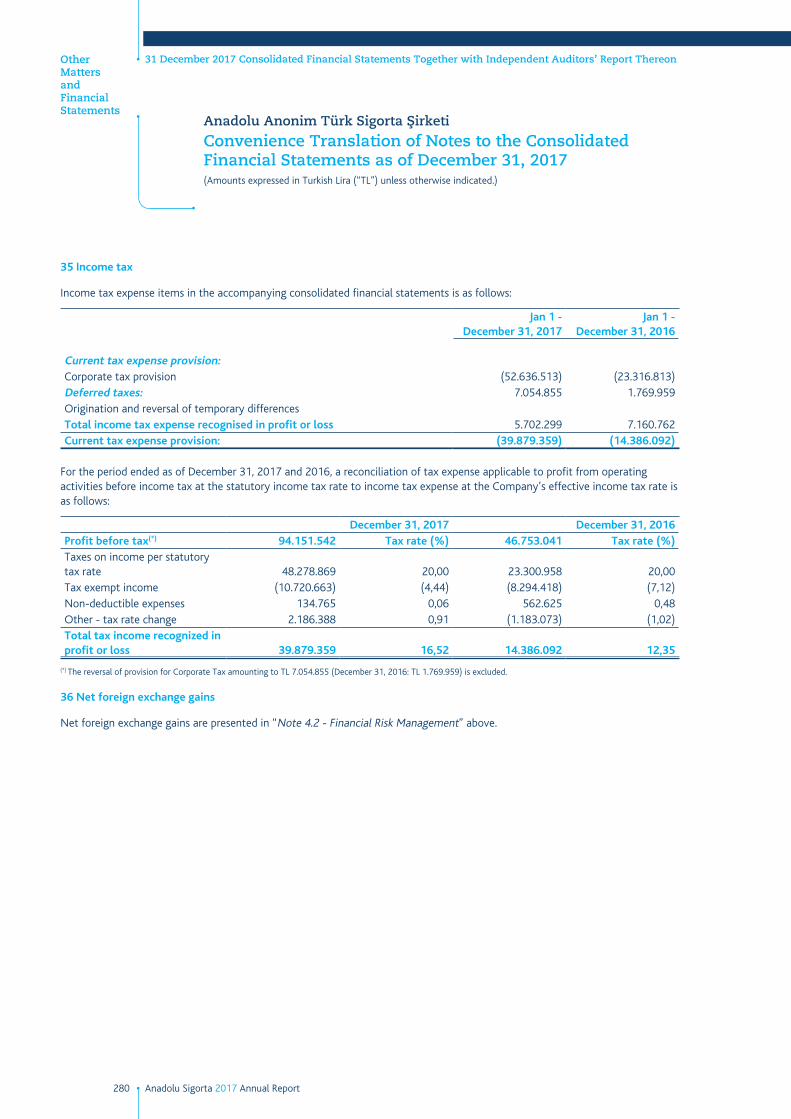

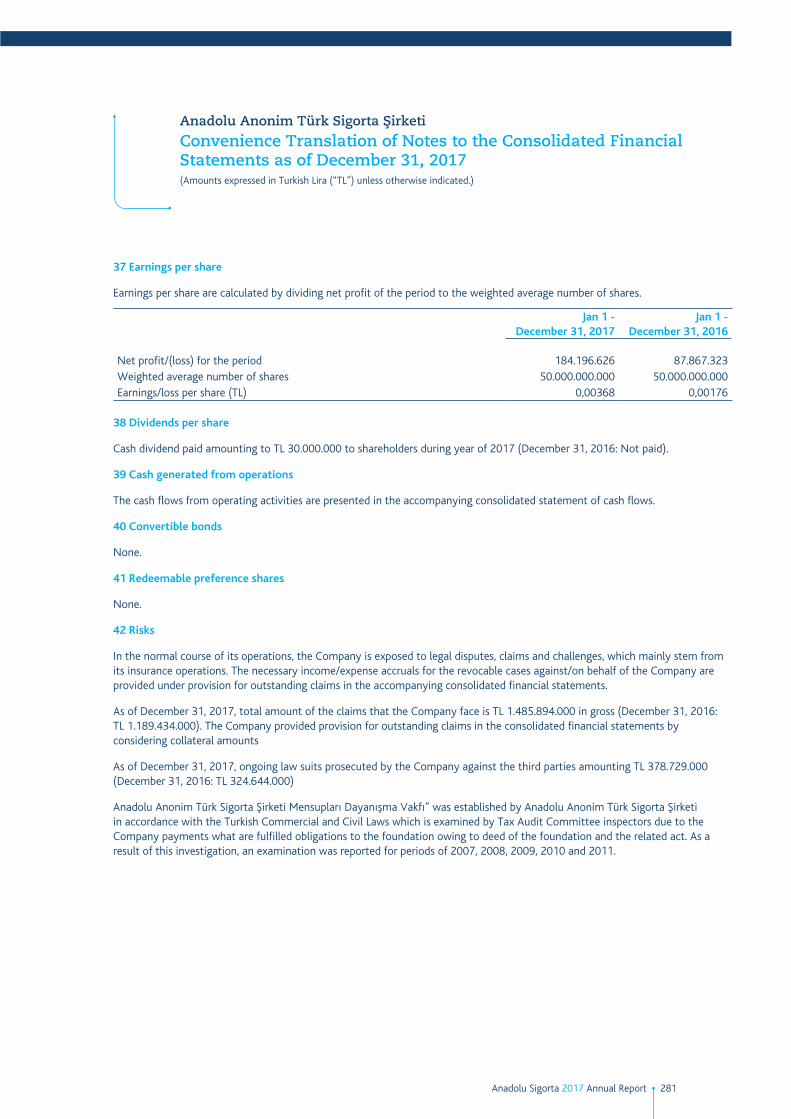

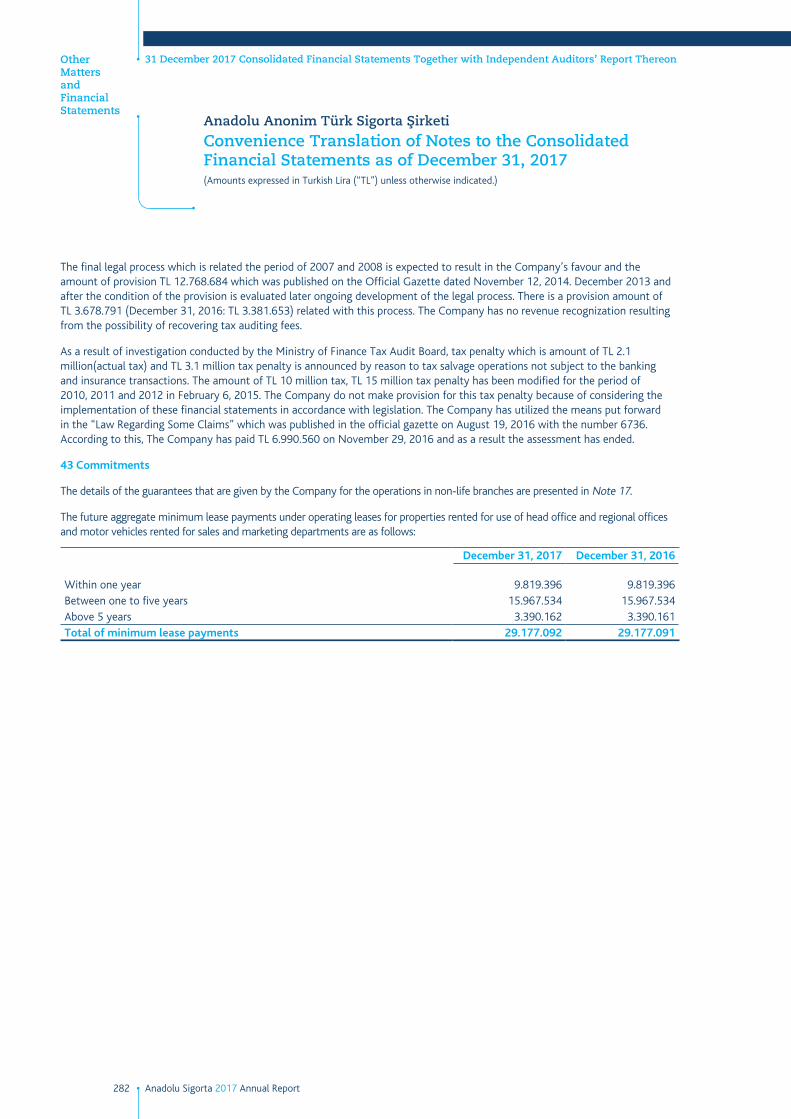

2017 - anadolu sigorta sigorta... · anadolu sigorta founded in 1925 as turkey’s first national...

TRANSCRIPT

1Anadolu Sigorta 2017 Annual Report

2017

Annual Report

Digital everywhere, Anadolu Sigorta for

everyone

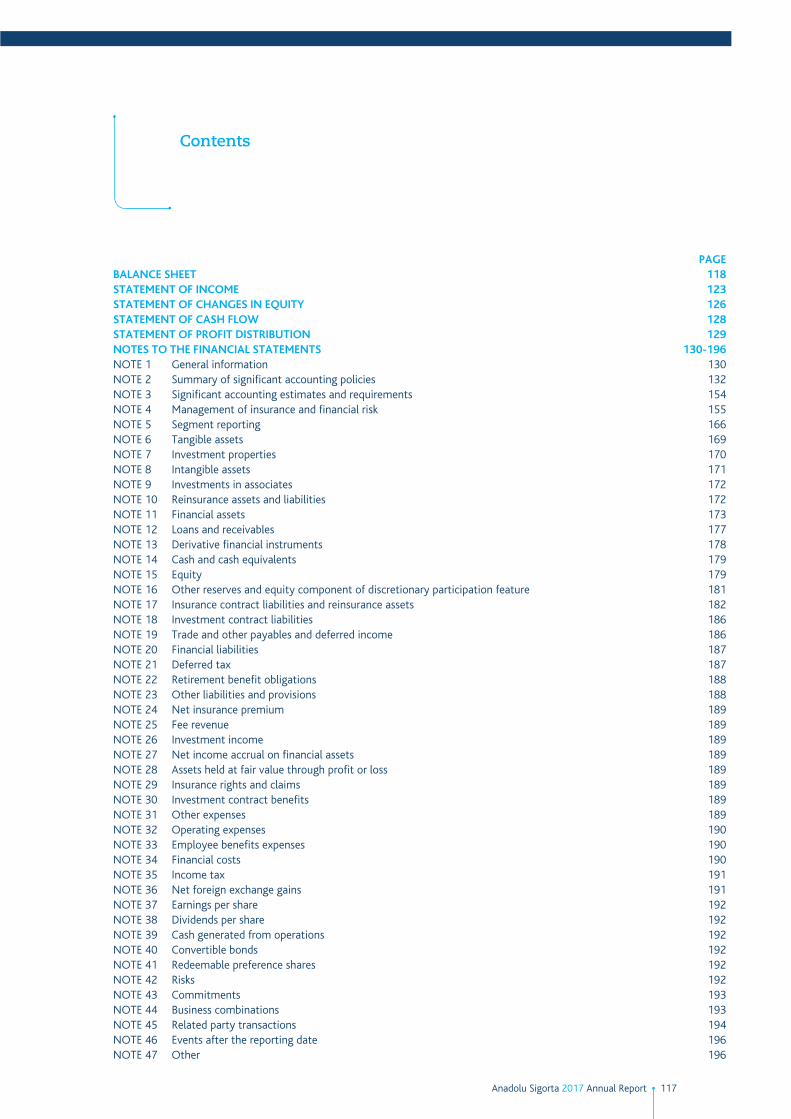

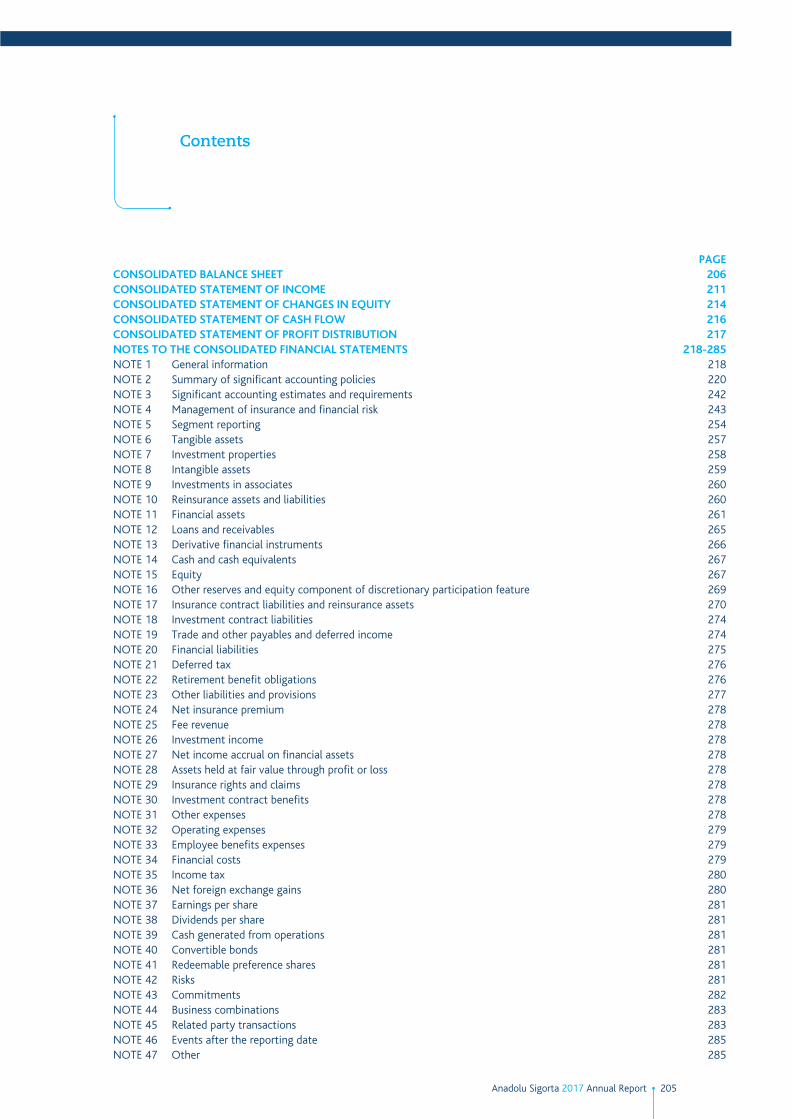

Contents

General Information 1Corporate Profile, Our Vision, Our Mission, Our Corporate Values 4

Milestones from the History of Anadolu Sigorta 6

Message from the Chairman 10

Message from the CEO 14

The Organization, Capital and Shareholder Structure of the Company 18

Organization Chart 18

Capital and Shareholder Structure 19

Disclosures on Preferred Shares 19

Governing Body, Executives and the Number of Employees 20

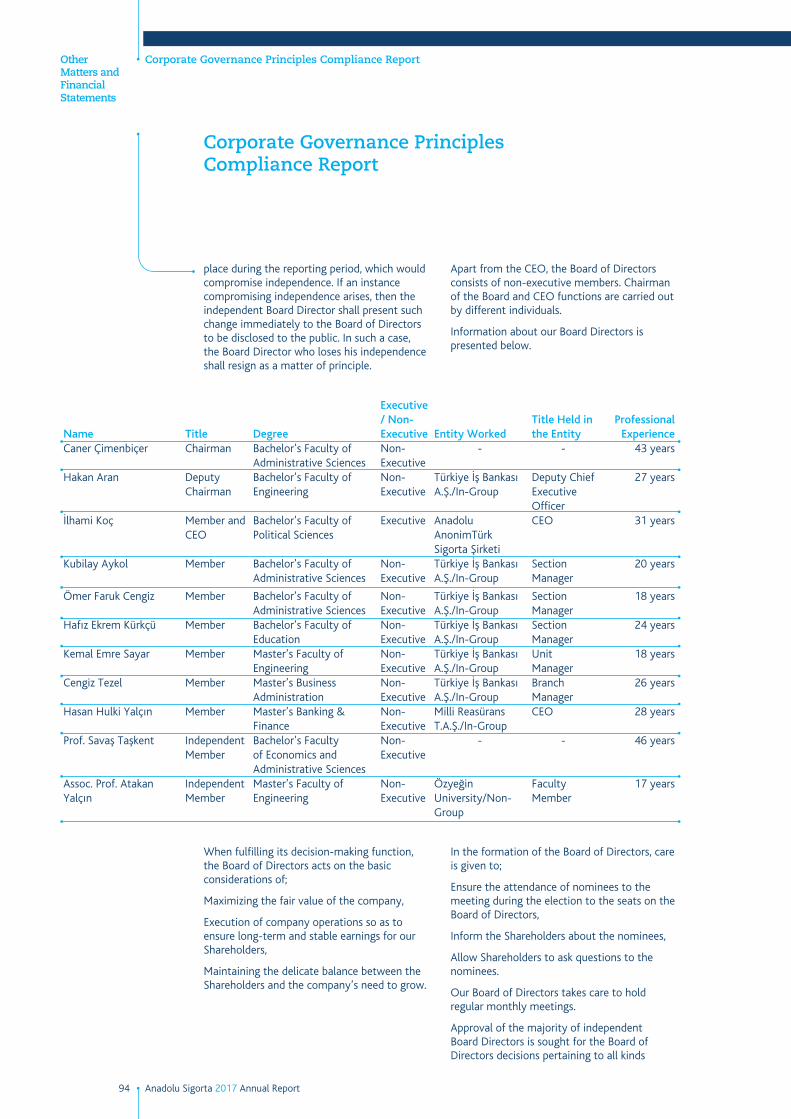

Board of Directors 20

Declarations of Independence by Independent Members of the Board of Directors 23

Executive Committee 24

Heads of Units Under the Internal Systems 26

Average Number of Employees by Categories During the Reporting Period 26

Financial Affairs and Actuarial Unit Managers 27

Financial Rights Provided to the Members of the Governing Body and Executives 27

Research and Development Activities of the Company 30Research and Development Pertaining to New Services and Business Activities 30

Company Activities and Major Developments in Activities 312017-2018 Primary Goals, Policies 31

Information on the Company’s Investments 31

Internal Control System and Internal Audit Activities 32

An Assessment of 2017 by the Board

of Inspectors 32

Internal Control System and an Assessment by the Governing Body 33

Information on Associates 34

Repurchased Own Shares by the Company 34

Disclosures Concerning Special Audit and Public Audit 34

Lawsuits Filed Against the Company and Potential Results 34

Disclosure of Administrative or Judicial Sanctions Against the Company and/or Board of Directors Members 34

Assessment of Prior Period Targets and General Assembly Decisions 34

Expenses Incurred in Relation to Donations and Grants and Social Responsibility Projects 34

Commitment to Social Responsibility 35

The Company’s Transactions with the Risk Group 37

Financial Status 40Summary Report by the Board of Directors 40

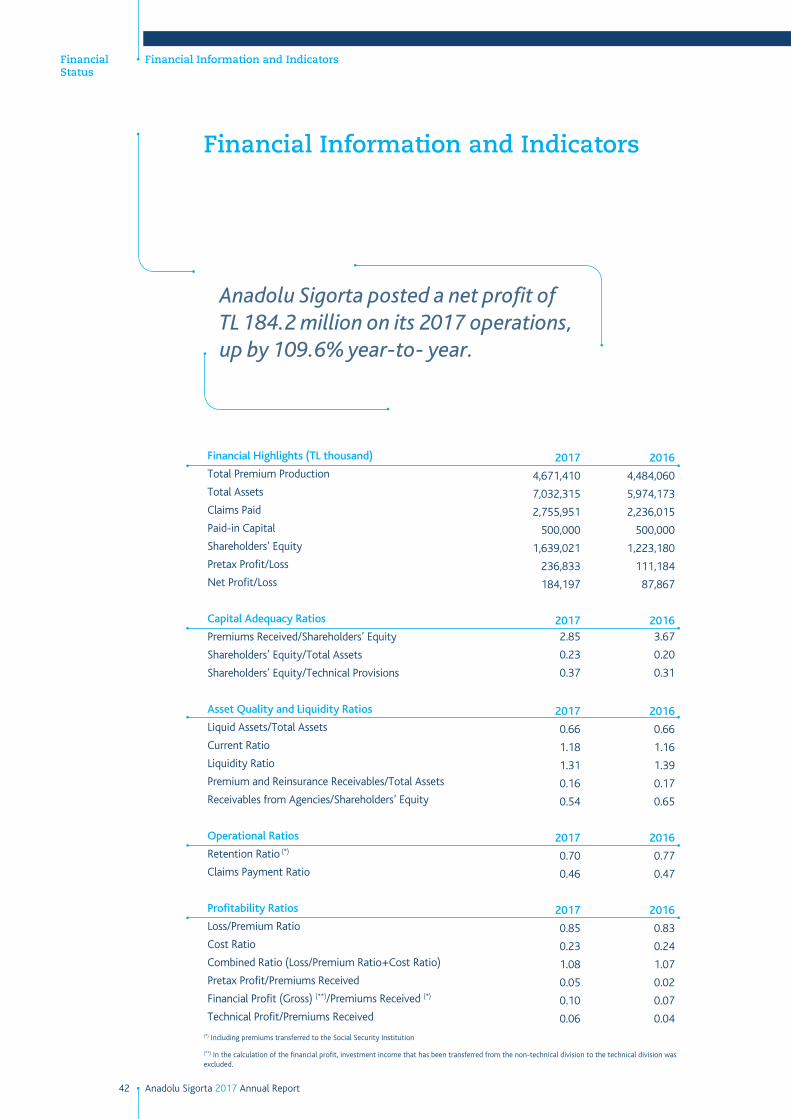

Financial Information and Indicators 42

2017 Economic Overview 46

Overview of the World and Turkish Insurance Industries and Future Outlook 49

Developments and Changes in Legislation 52

An Assessment of Anadolu Sigorta in 2017 56

Assessment of the Company Capital and Comments 75

Profit Distribution Policy 76

Risks and an Assessment by the Governing Body 77Risk Management Policies Adhered to by Types of Risks 77

Activities of the Committee of Early Determination of Risk 80

Other Matters and Financial Statements 82Independent Auditor’s Report Related to Annual Report 82

An Assessment of the Board Directors by the Corporate Governance Committee 83

Disclosure Policy 85

Corporate Governance Principles Compliance Report 88

Committees Operating Within Anadolu Sigorta and an Assessment by the Board of Directors 98

An Assessment of the Operation of the Independent Audit Firm in 2017 Activity Period via the Audit Committee 102

Human Resources Practices at Anadolu Sigorta 103

Agenda of the Annual General Assembly Meeting 104

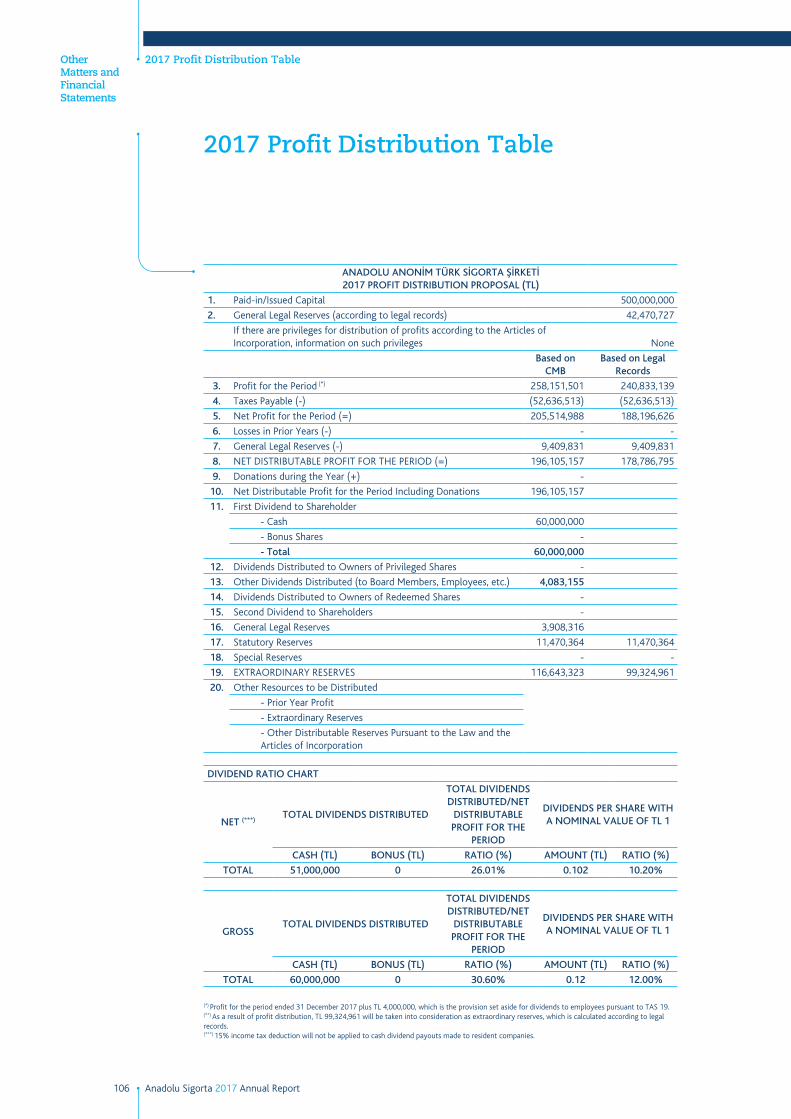

2017 Profit Distribution Proposal 105

2017 Profit Distribution Table 106

2017 Annual Report Compliance Statement 107

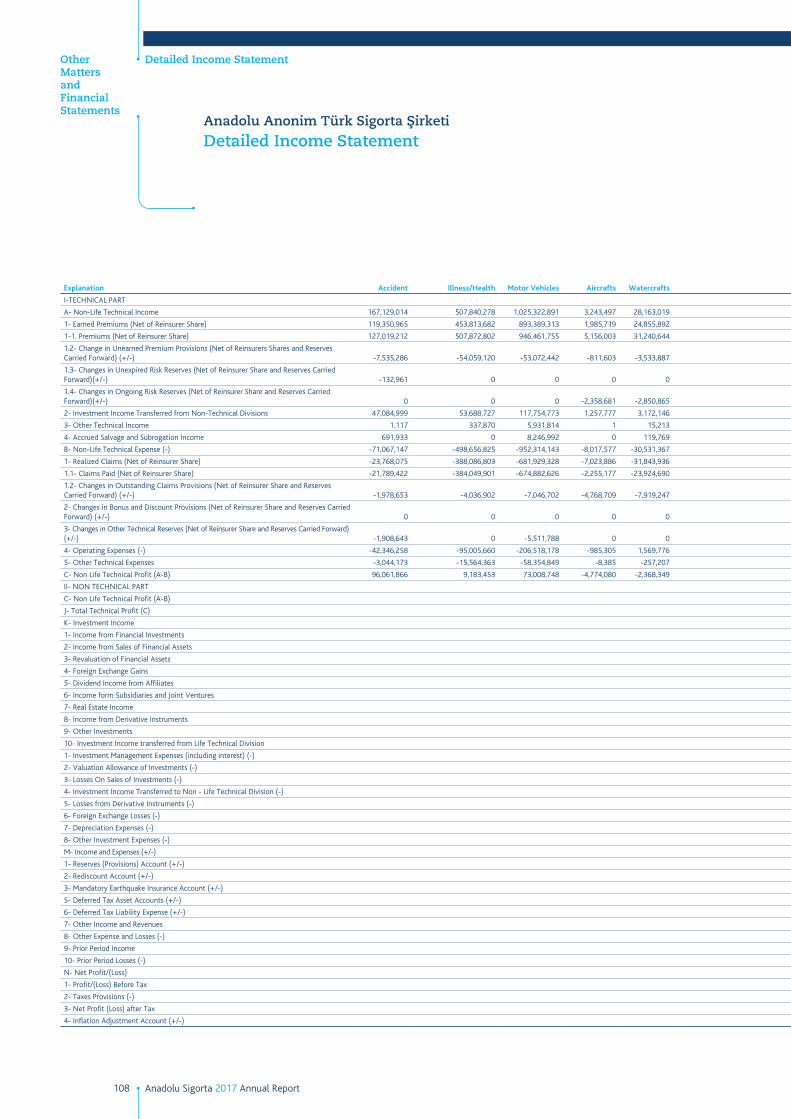

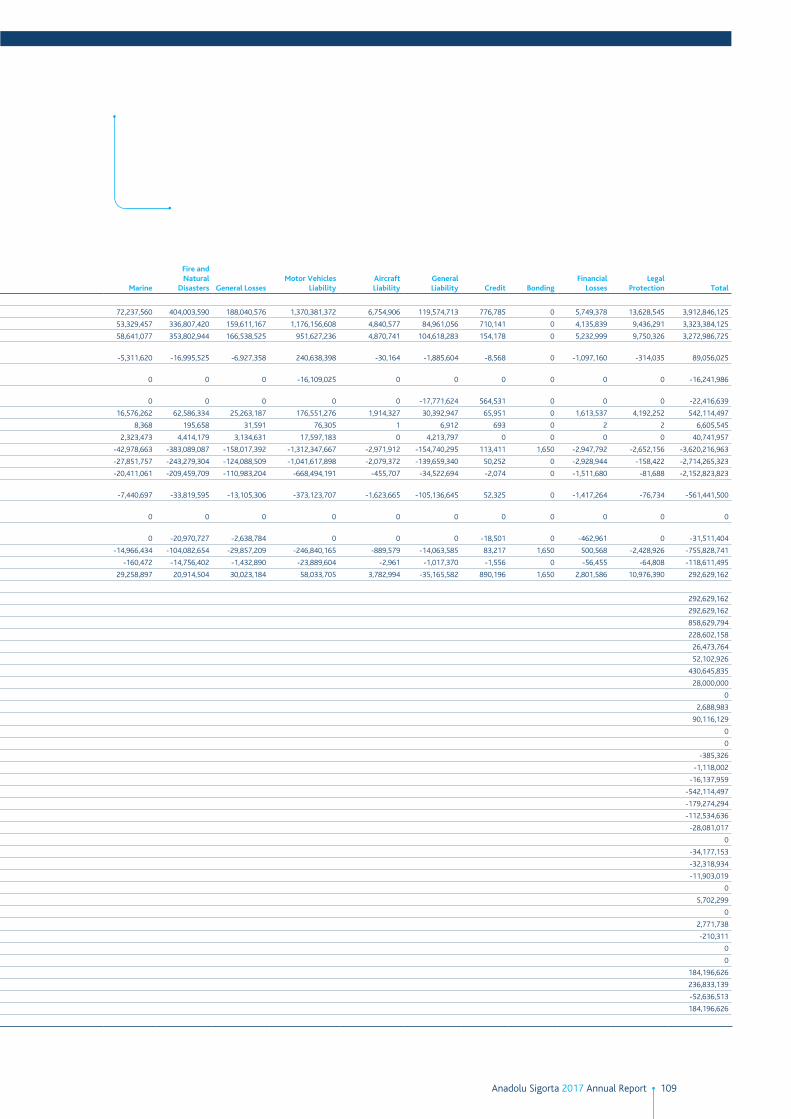

Detailed Income Statement 108

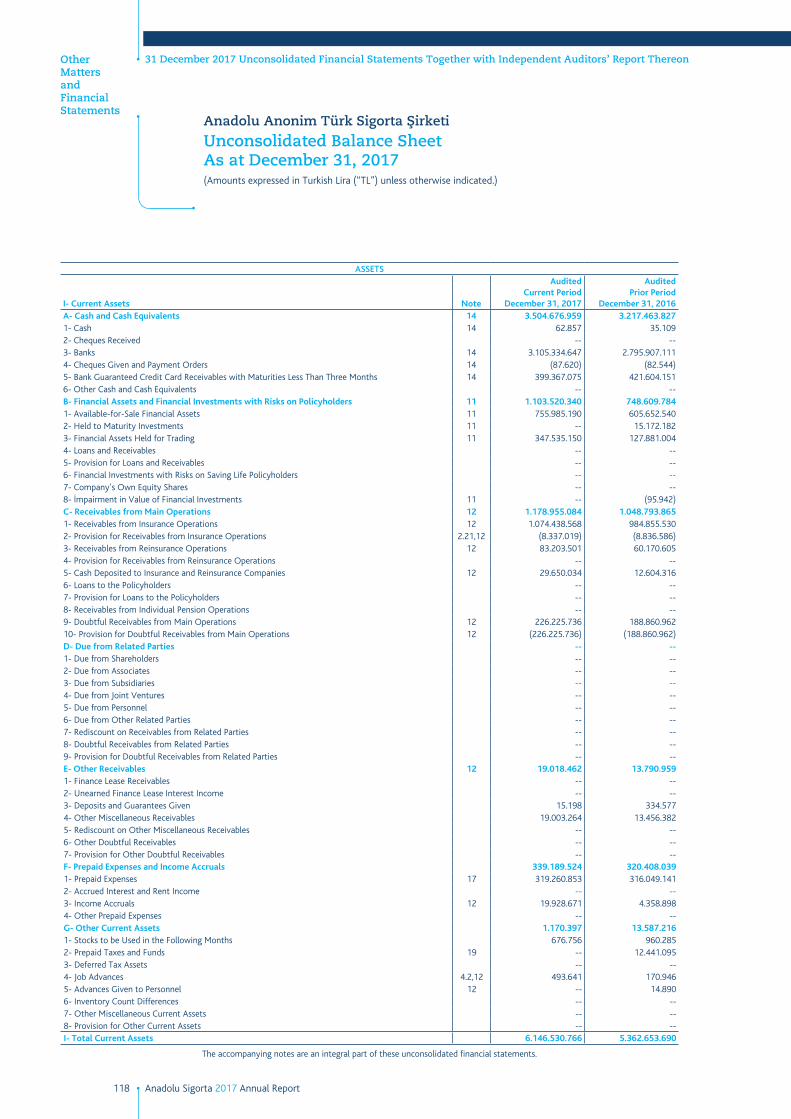

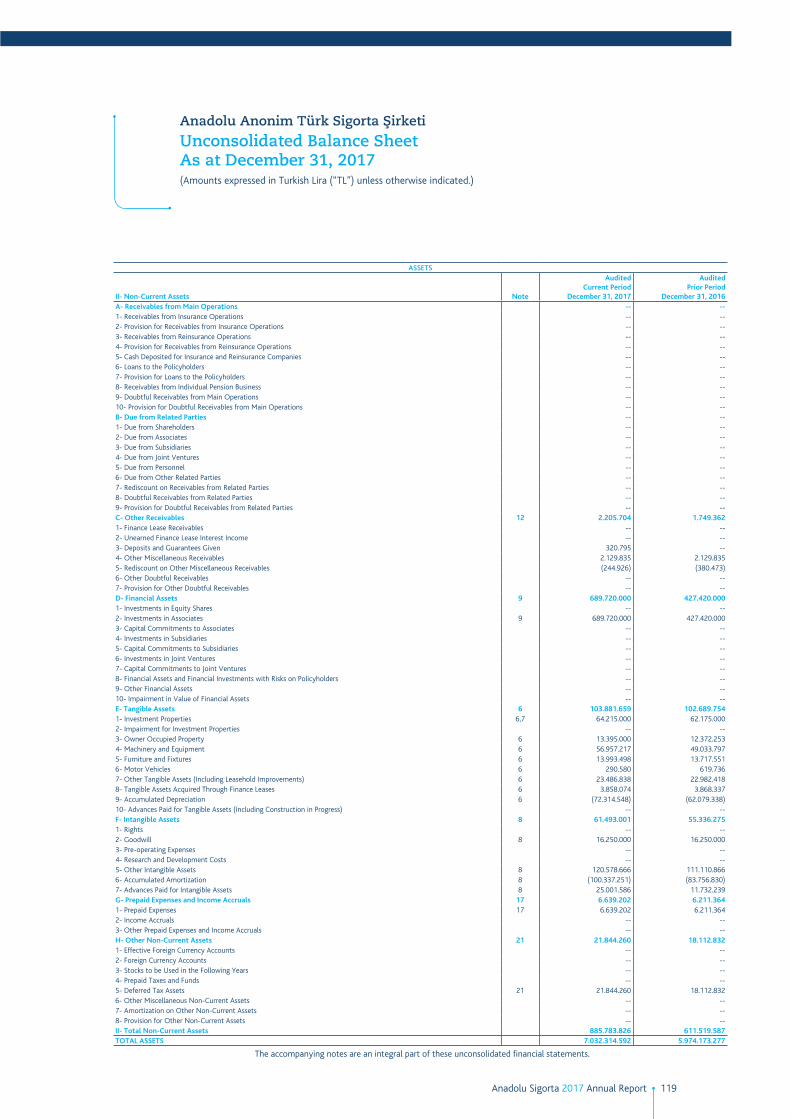

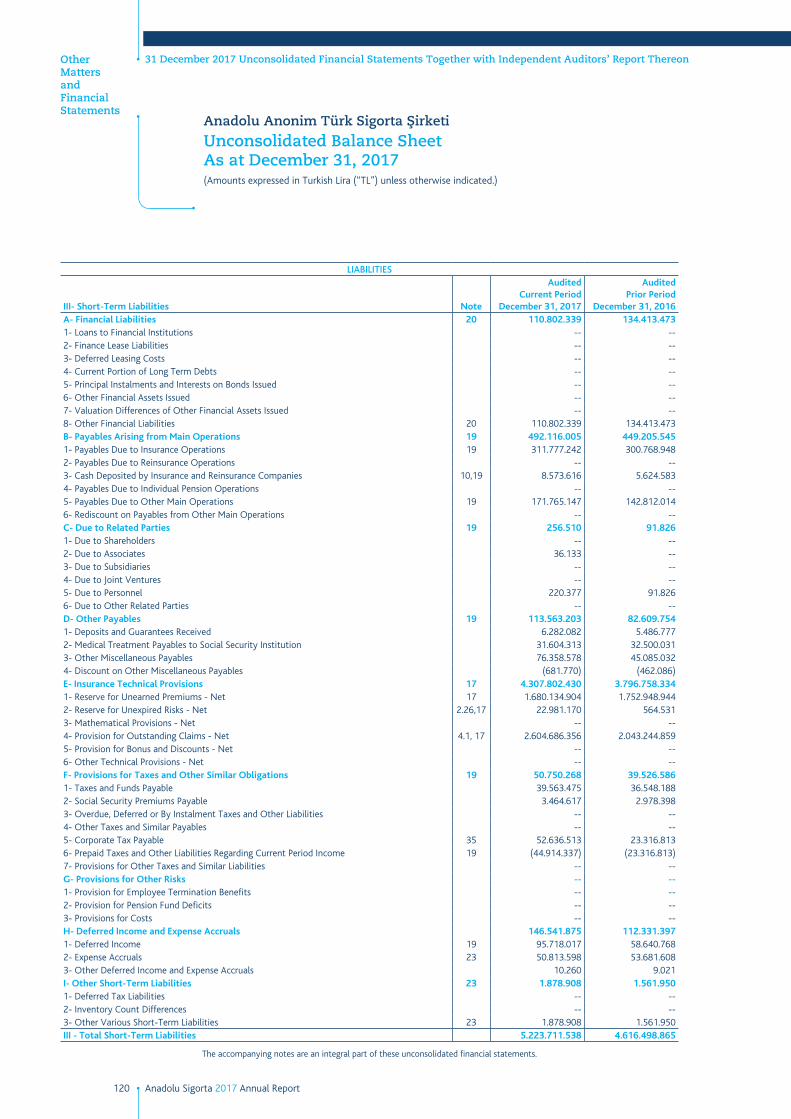

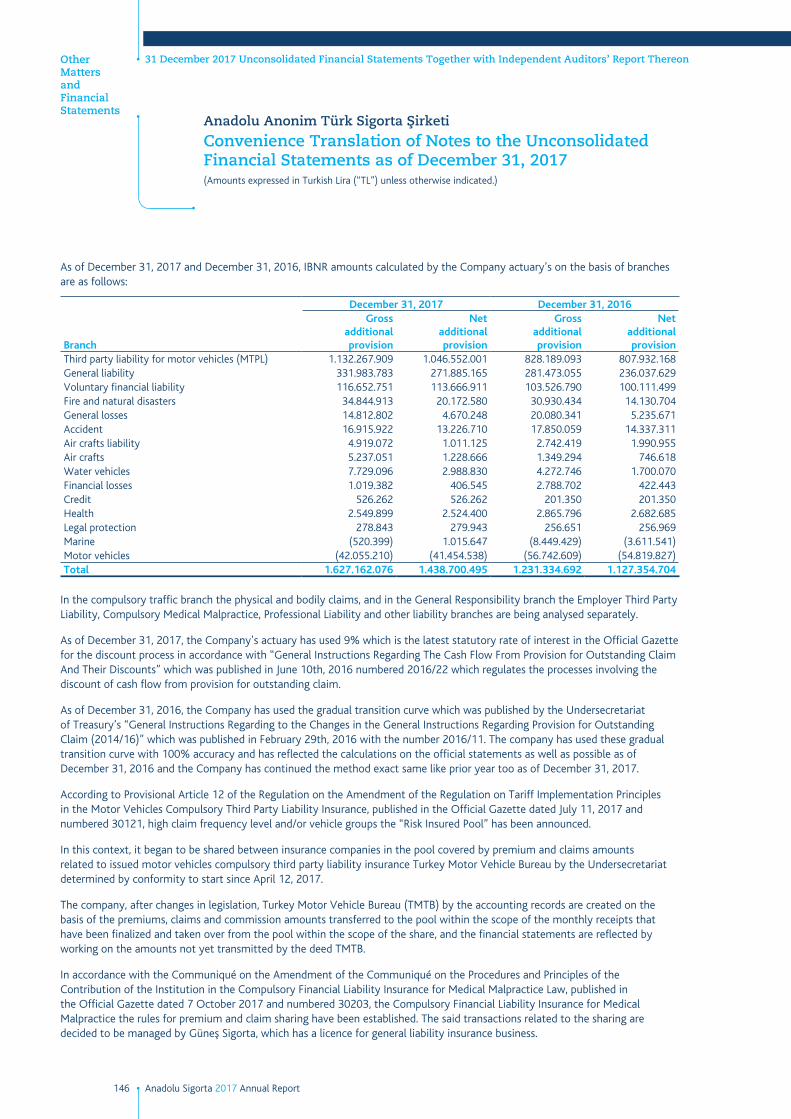

31 December 2017 Unconsolidated Financial Statements Together with Independent Auditors’ Report Thereon 111

Information on Consolidated Subsidiaries 198

31 December 2017 Consolidated Financial Statements Together with Independent Auditors’ Report Thereon 199

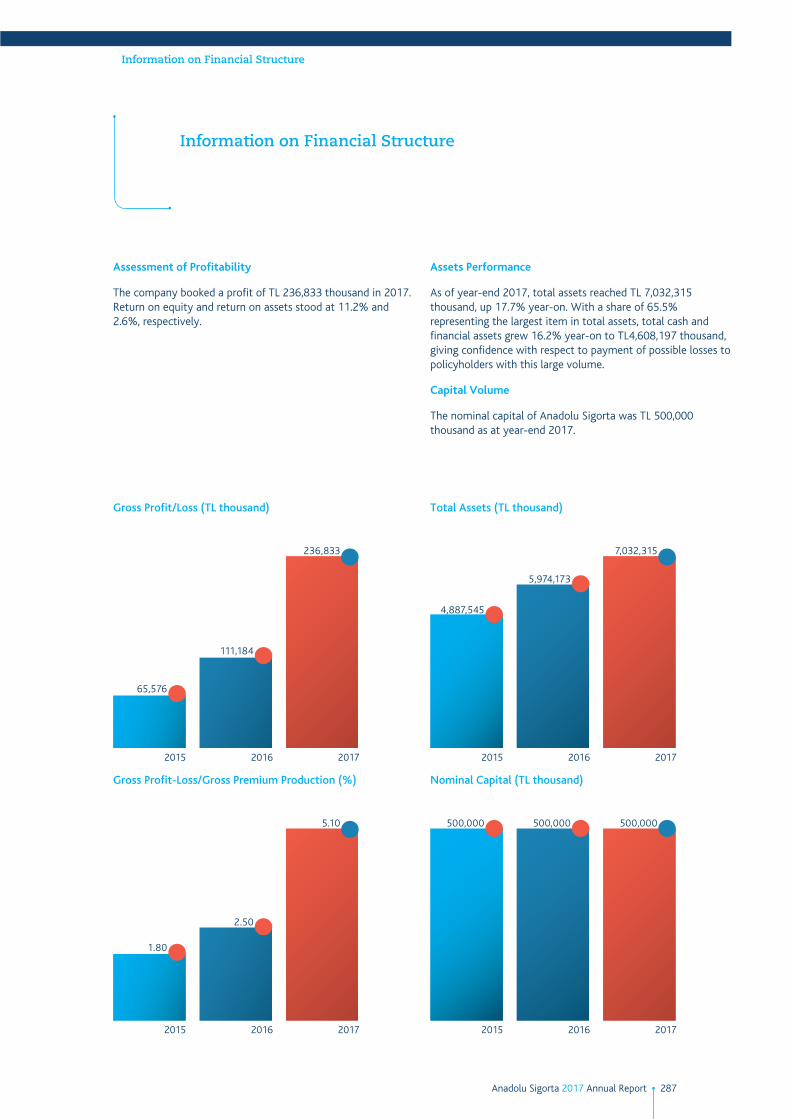

An Assessment of Financial Standing, Profitability and Solvency 286

Information on Financial Structure 287

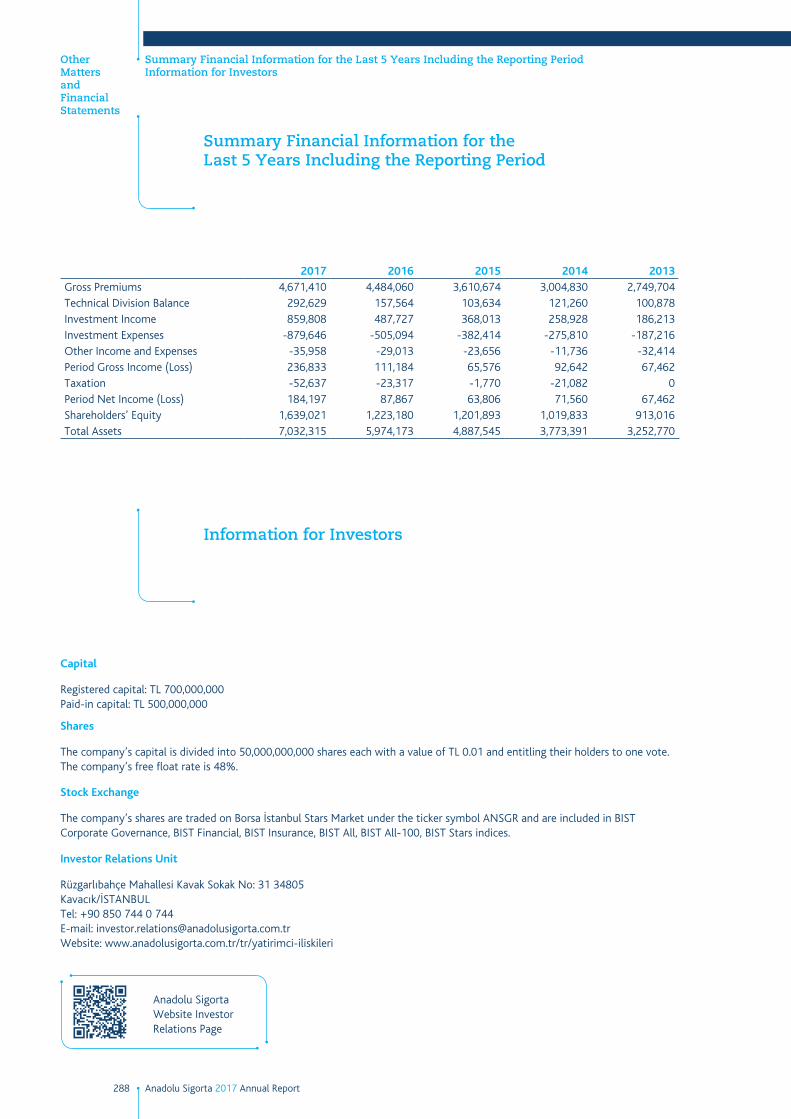

Summary Financial Information for the Last 5 Years Including the Reporting Period 288

Information for Investors 288

General Information

1Anadolu Sigorta 2017 Annual Report

General Information

Anadolu Anonim Türk Sigorta Şirketi2017 Annual Report

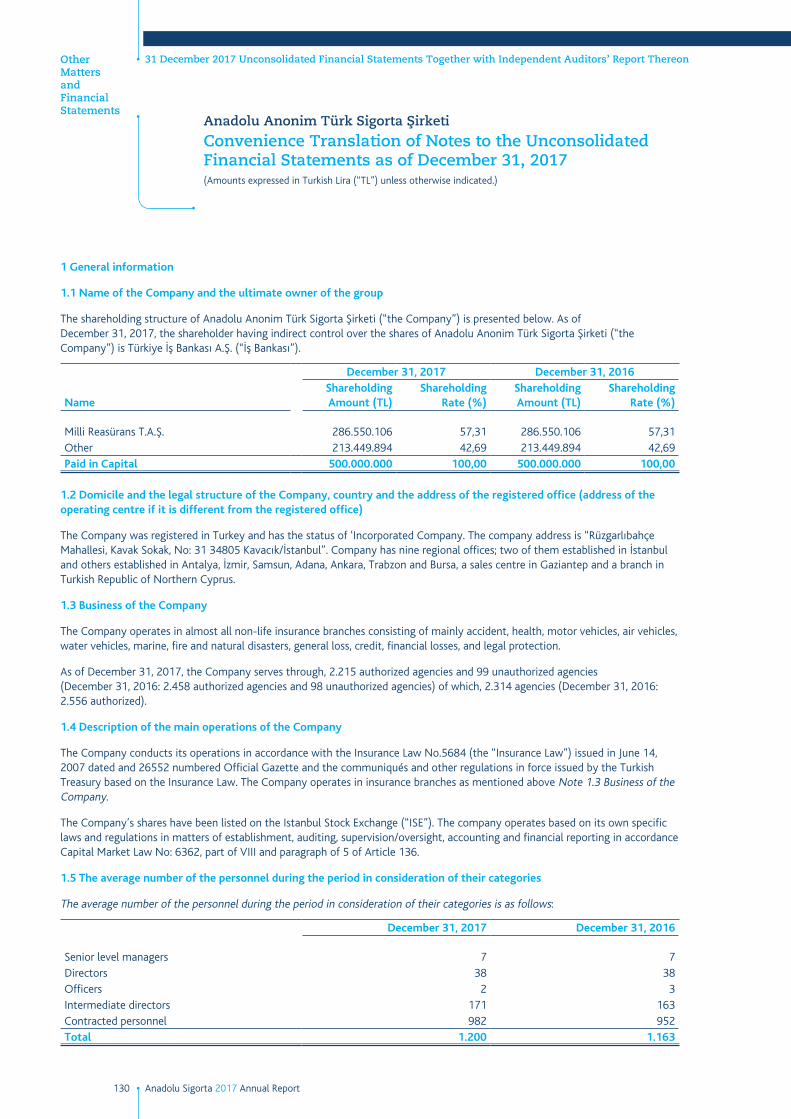

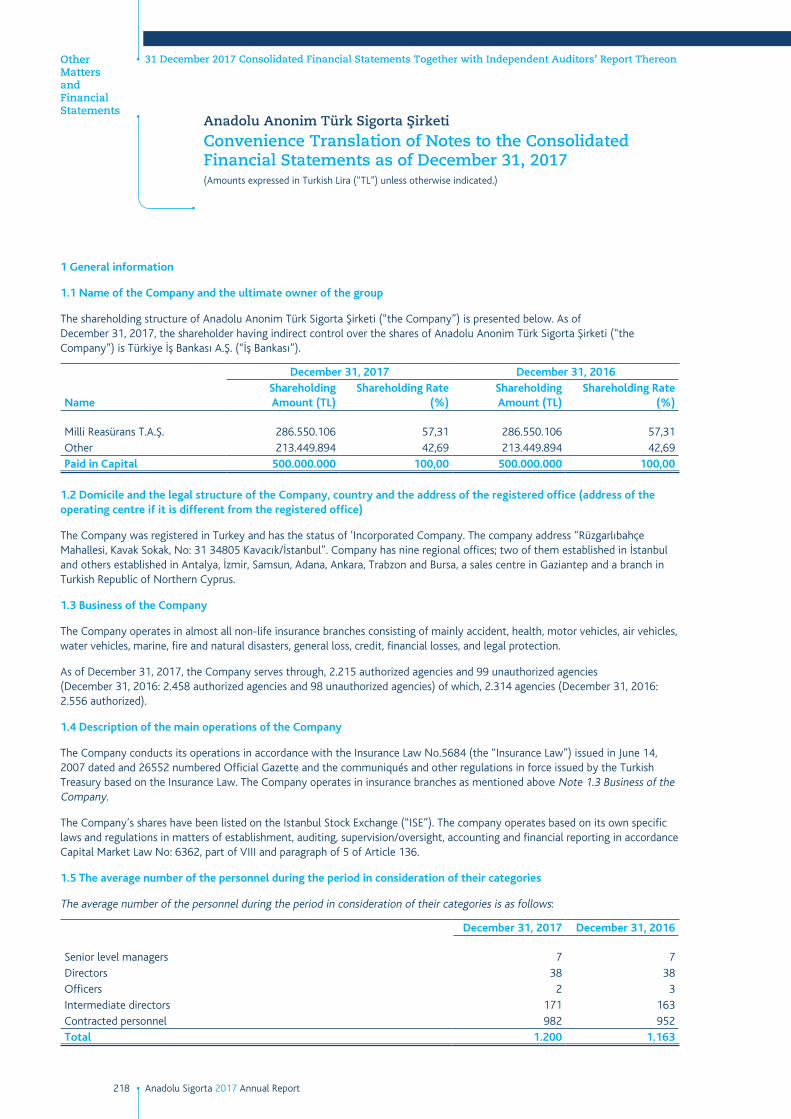

Corporate TitleAnadolu Anonim Türk Sigorta Şirketi

Websitewww.anadolusigorta.com.tr

Anadolu Sigorta Trade Registration No4593/557

DirectoryHead OfficeRüzgarlıbahçe Mah. Kavak Sok. No: 31 Kavacık 34805 İstanbulTel: +90 850 744 0 744Fax: +90 850 744 0 745E-mali: [email protected]

İstanbul Regional BranchLevent Mah. Meltem Sok. No: 10İş Kuleleri Kule: 2 Kat: 8 34330 Beşiktaş İstanbulTel: +90 850 744 0 744Fax: +90 850 744 0 753E-mali: [email protected]

Kadıköy Regional Branch Küçükbakkalköy Mah. Vedat Günyol Cad. 20/11 34750 Ataşehir Tel: +90 850 744 0 744Fax: +90 850 744 0 754E-mali: [email protected]

Mediterranean Regional BranchKonyaaltı Cad. No: 78 Muratpaşa 07050 Antalya Tel: +90 850 744 0 744Fax: +90 850 744 0 752E-mali: [email protected]

Western Anatolia Regional BranchAtatürk Cad. No: 92 Anadolu Sigorta Binası 2 Pasaport Konak 35210 İzmirTel: +90 850 744 0 744Fax: +90 850 744 0 747E-mali: [email protected]

Middle Black Sea Regional BranchKılıçdede Mah. Ülkem Sok. No: 8-A/7 İlkadım 55060 SamsunTel: +90 850 744 0 744Fax: +90 850 744 0 750E-mali: [email protected]

Southern Anatolia Regional BranchReşatbey Mah. 62029. Sok. No: 16/A Seyhan 01120 AdanaTel: +90 850 744 0 744Fax: +90 850 744 0 746E-mali: [email protected]

Central Anatolia Regional BranchCinnah Cad. Farabi Sok. No: 43 Kavaklıdere 06690 AnkaraTel: +90 850 744 0 744Fax: +90 850 744 0 749E-mali: [email protected]

Black Sea Regional BranchKarşıyaka Mah. 4 Nolu Sok. No: 479 Ortahisar 61040 TrabzonTel: +90 850 744 0 744Fax: +90 850 744 0 751E-mali: [email protected]

Marmara Regional Branch Odunluk Mah. Akademi Cad. Zeno İş Merkezi A Blok No: 10/5 Nilüfer 16110 Bursa Tel: +90 850 744 0 744Fax: +90 850 744 0 748E-mali: [email protected]

TRNC Branch Memduh Asaf Sok. 8 Köşklüçiftlik Lefkoşa/TRNCTel: +90 392 227 95 95Fax: +90 392 227 95 96E-mali: [email protected]

Gaziantep Sales Officeİncilipınar Mah. Gazi Muhtar Paşa Bulvarı 36017 Sok. Kepkepzade Park iş Merkezi C Blok No: 6/10 Şehitkamil GaziantepFax: +90 850 744 0 755E-mali: [email protected]

Previous years’ annual reports of Anadolu Sigorta

2 Anadolu Sigorta 2017 Annual Report

3Anadolu Sigorta 2017 Annual Report

150

We carried out our first Hackathon on 18 & 19 November.

Contestants applied to take part in the

Hackathon.

4 Anadolu Sigorta 2017 Annual Report

Corporate Profile, Our Vision, Our Mission, Our Corporate Values

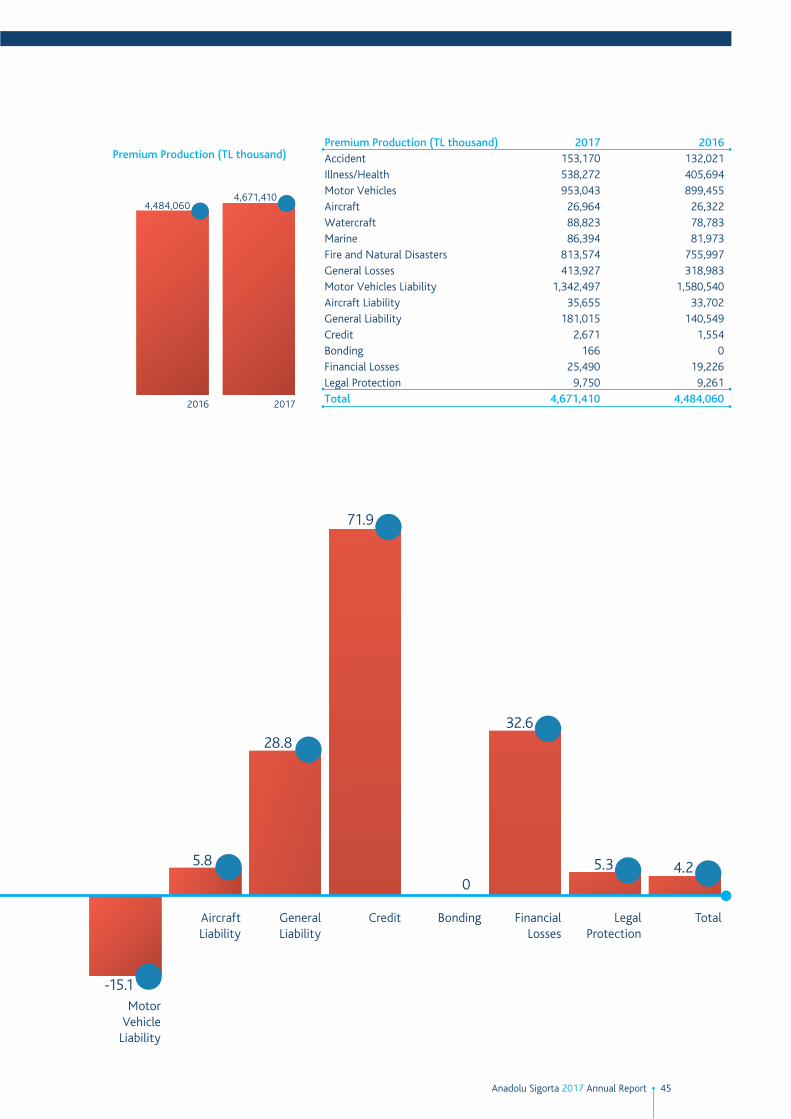

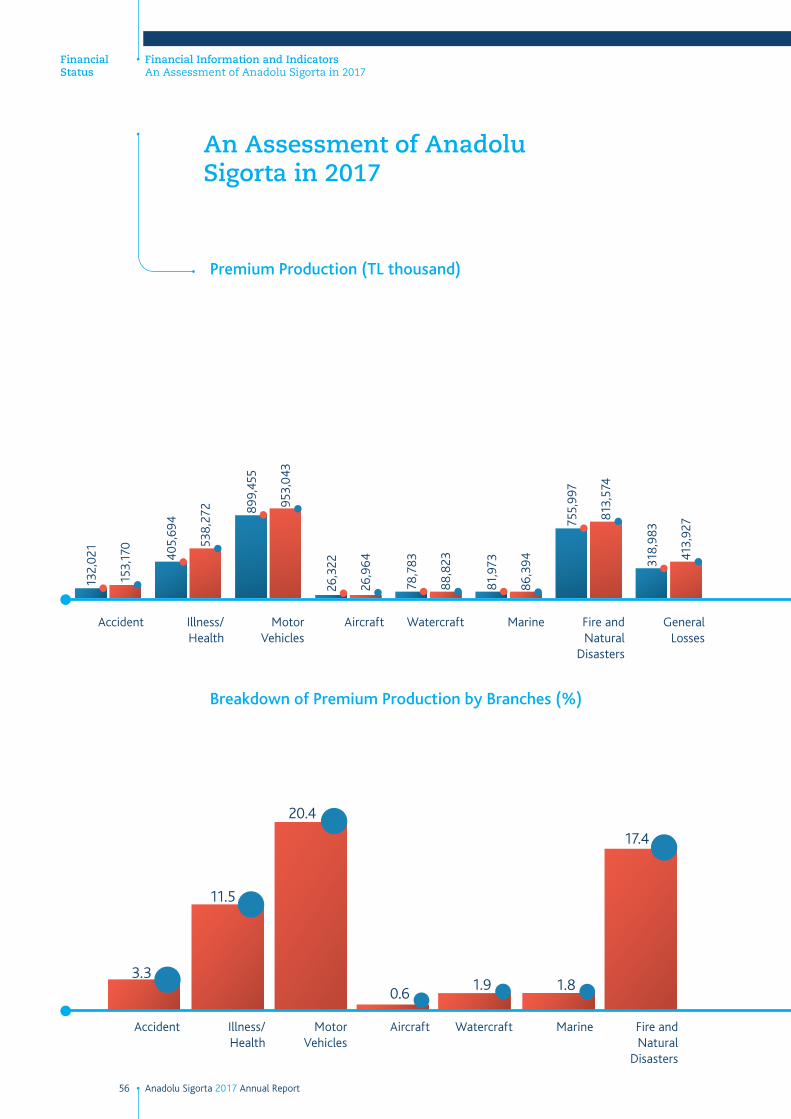

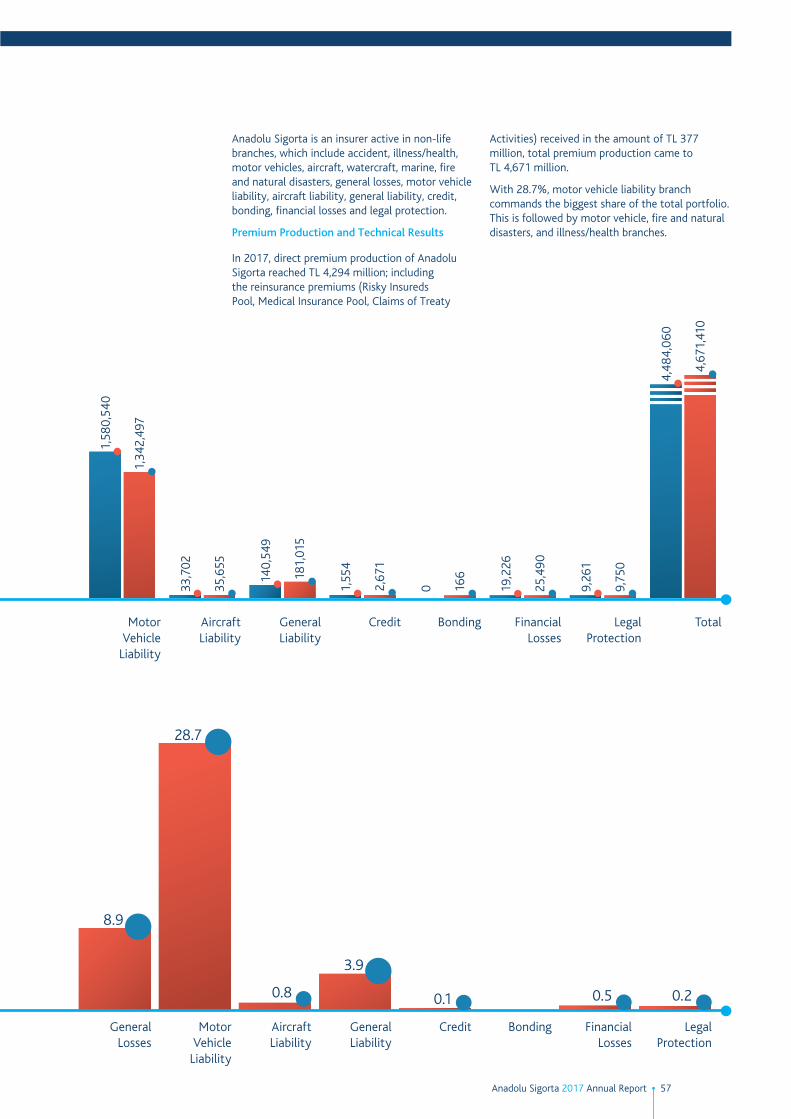

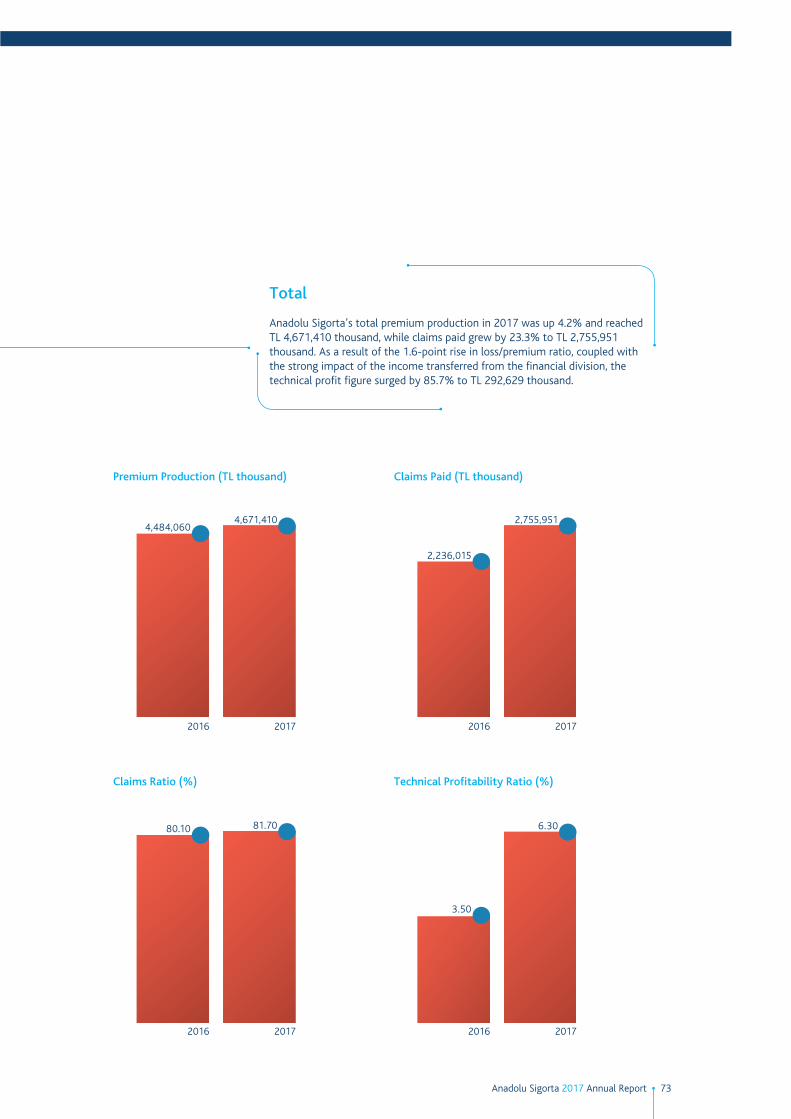

Corporate ProfileIn 2017, Anadolu Sigorta expanded its total premium production by 4.2% year-on-year to TL 4,671 million and controlled an 11.8% share of the overall market among non-life companies.

Anadolu Sigorta pursues its operations via nine regional branches across the nation and one branch in the Turkish Republic of Northern Cyprus. The number of employees on the company’s payroll averaged 1,200 in 2017.

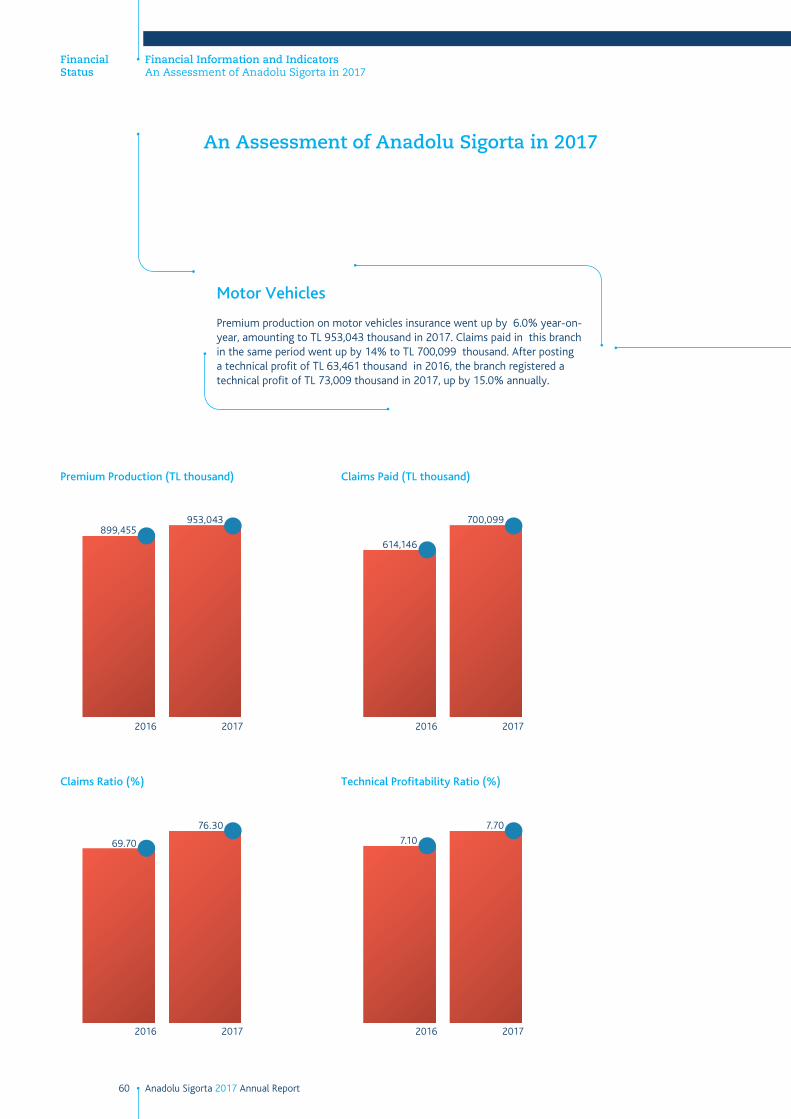

Anadolu Sigorta registered its highest premium production in the motor

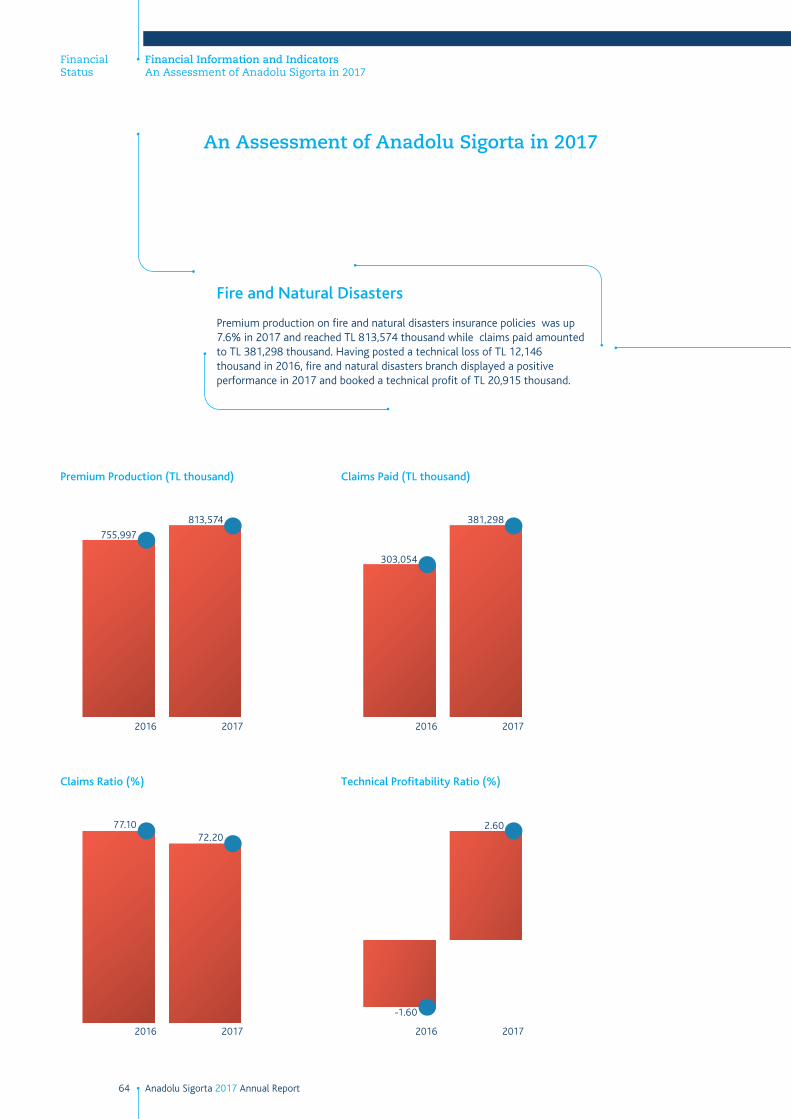

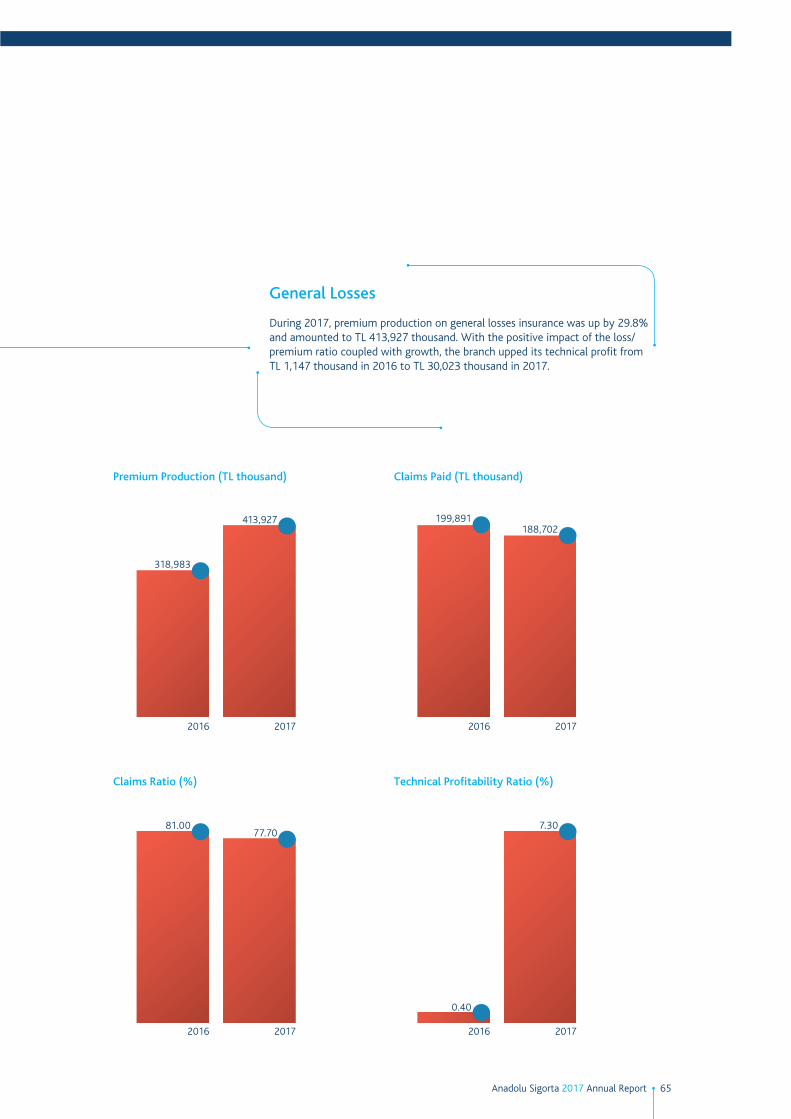

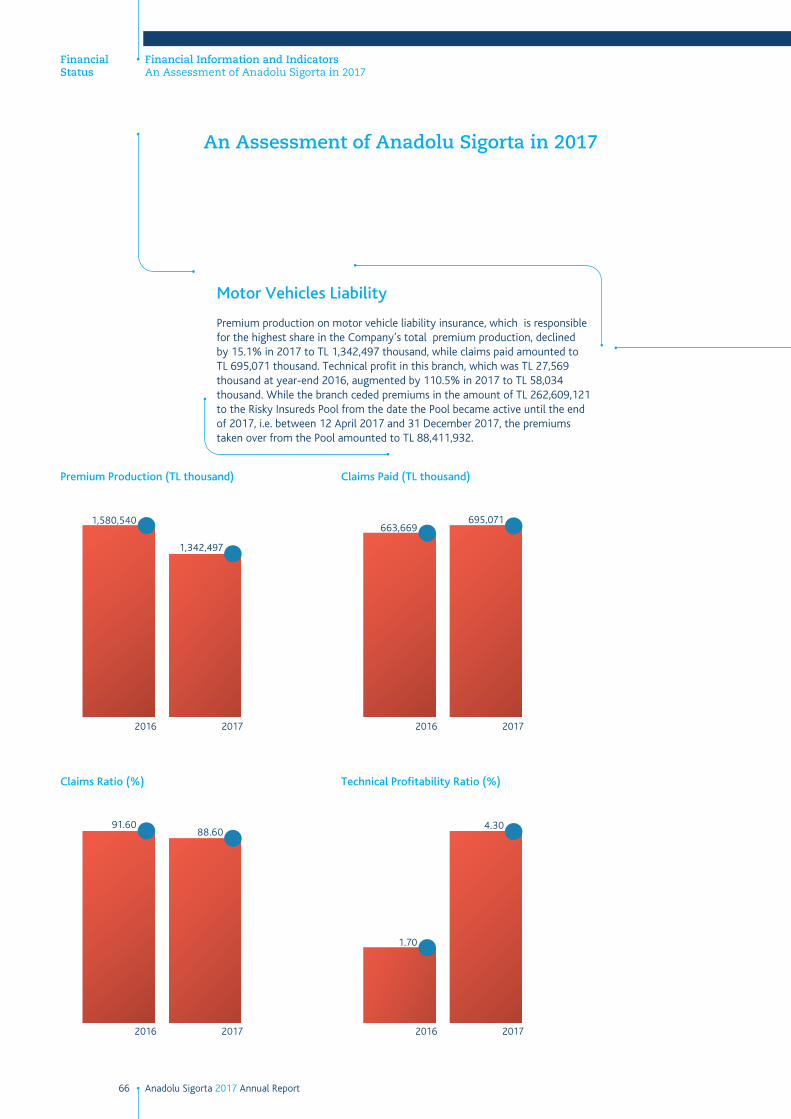

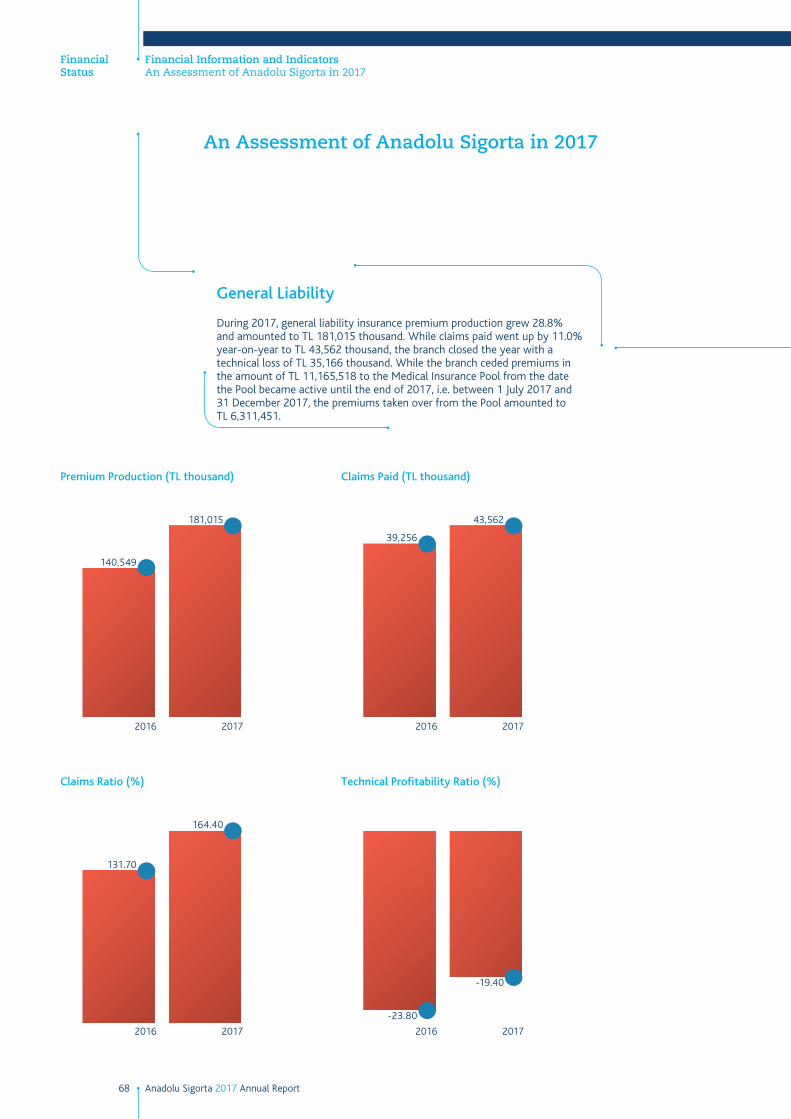

vehicle liability with TL 1,342 million, followed by the motor vehicles branch with TL 953 million in 2017. Trailing these two branches, in order, were fire and natural disasters with TL 814 million, illness/health with TL 538 million, general losses with TL 414 million and general liability with TL 181 million.

Turkey’s first national insurance company and the pioneer in the sector, Anadolu Sigorta will keep contributing to the advancement of the insurance business in Turkey in the light of its mission and vision, and further build on its solid position in the industry on the back of its powerful digital insurance initiative.

Engaged in all non-life branches, i.e. fire, marine, accident, engineering, agriculture, legal protection, personal accident, illness/health and credit and bonding, Anadolu Sigorta will keep contributing to the advancement of the insurance business in Turkey, guided by its mission and vision.

11.8%Anadolu Sigorta controlled an 11.8% share of the overall market among non-life companies.

General Information

Corporate Profile, Our Vision, Our Mission, Our Corporate Values

5Anadolu Sigorta 2017 Annual Report

In keeping with the deeply-rooted, pioneering, honest, and solid corporate values of Anadolu Sigorta to:• Lead the sector,• Help create a broad public awareness of insurance in

Turkey,• Implement a customer-focused approach to service,• Increase our financial strength to international

standards,• Enhance the value of our company.

• To make Anadolu Sigorta the insurance brand preferred by everyone who needs insurance.

• To achieve a strength that makes it a reference point in the worldwide insurance industry as well.

A Company Entrenched In History

• It was founded in accordance with the instructions given by Mustafa Kemal Atatürk.

• It is Turkey’s first national insurance company.

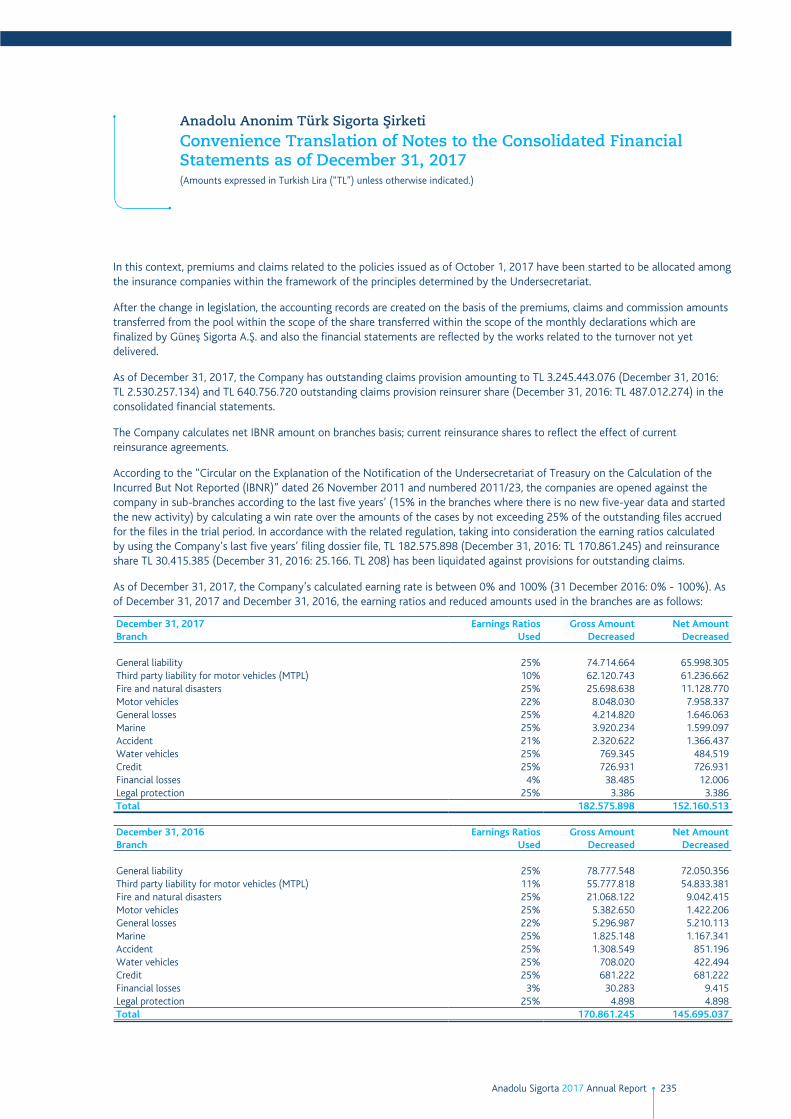

• It has a powerful corporate structure built on its knowledge of insurance accumulated through the years.

Pioneership

• Pioneer in creating product;

• Pioneer in service;• Pioneer in

technology;• With its self-renewing

ability preserves its pioneering position;

• It plays a pioneering role in social responsibility.

Integrity

• It has ethical merits;• It fulfills its promises

definitely;• It inheres in

transparency as principle;

• It never abandons human values.

Powerful Structure It has a stable financial power;

• It has an extended and efficient service network;

• It has a sophisticated and high qualified human source;

• It gains power from the synergy created by İşbank.

Our Corporate Values

Our Mission

Our Vision

6 Anadolu Sigorta 2017 Annual Report

Milestones from the History of Anadolu Sigorta

Founded in 1925 as Turkey’s first national insurance company, Anadolu Sigorta has been pursuing operations, aware of its role as the pioneer of the Turkish insurance industry for 92 years.

General Information

Milestones from the History of Anadolu Sigorta

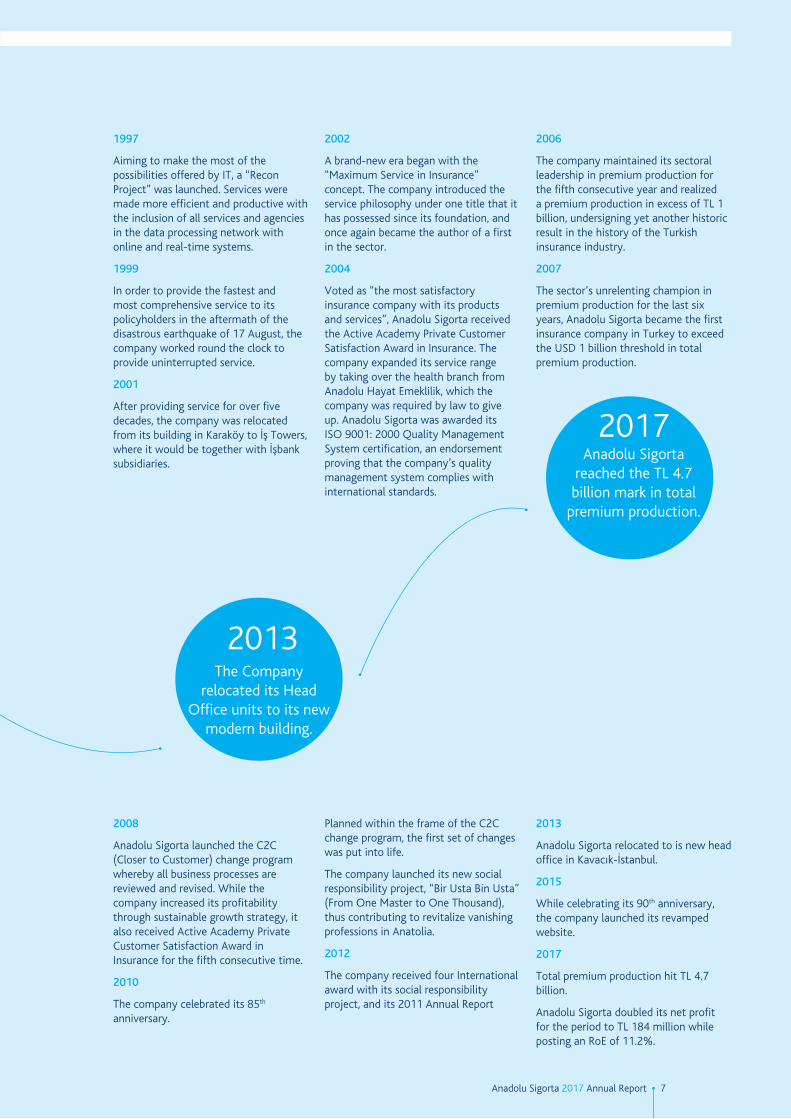

1925

Anadolu Sigorta was founded on April 1st at the initiative of Atatürk and under the leadership of İşbank, Turkey’s first national bank.

1961

The first data processing system was set up.

1975

Being the leader of national insurance since the onset of the Turkish Republic, Anadolu Sigorta celebrated its 50th anniversary.

1983

“Blue Insurance” policies marking the introduction of comprehensive insurance system in Turkey and offering 17 types of cover were put on sale for the first time.

1984

Highly acclaimed by the public and the sector, “Insurance of the Future”, the most comprehensive life policy ever offered in Turkey until then, was introduced.

1986

Representing a new branch in the Turkish insurance business, “Electronic Equipment Insurance” was first started by Anadolu Sigorta.

1987

Activities commenced in the agricultural insurance branch.

1991

The life branch was transferred to Anadolu Hayat Sigorta, a newly-formed life insurer as required by law.

1993

Extending administrative and technical assistance to Günay Anadolu Sigorta, founded and started to operate in Azerbaijan, Anadolu Sigorta became the first Turkish insurance company to set up an international operation.

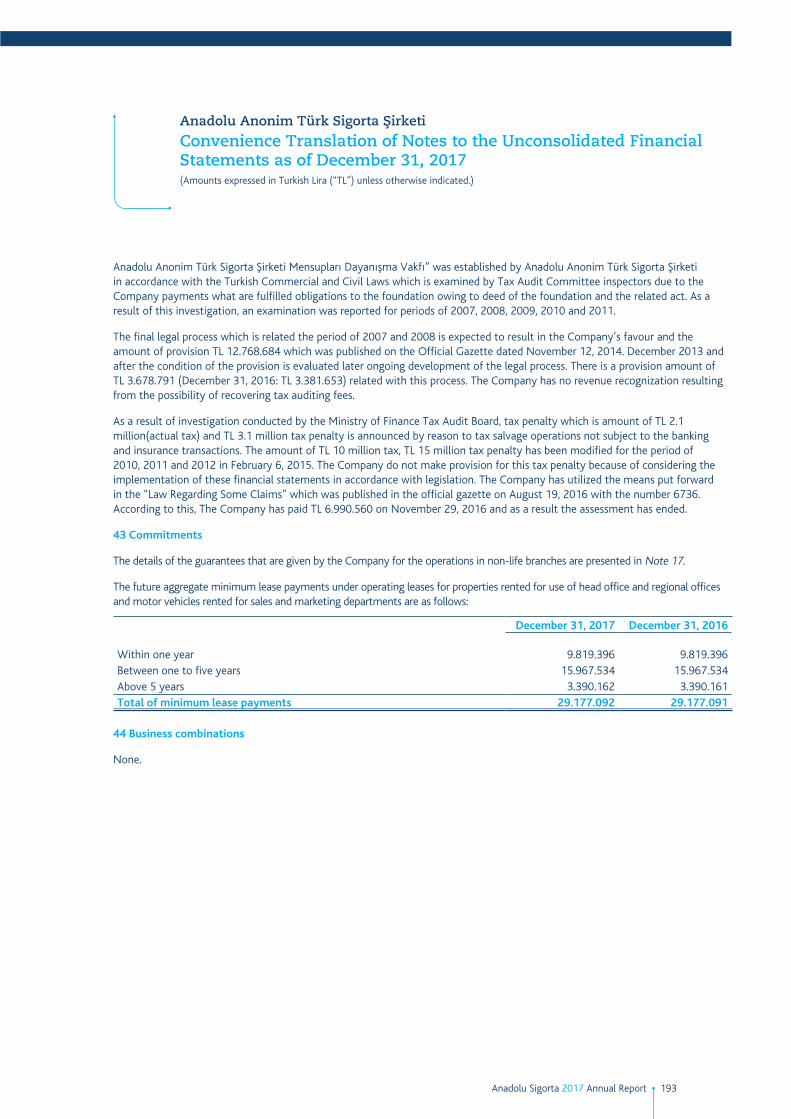

1996

Policies in legal protection insurance branch, another first in our country, were written.

1925Anadolu Sigorta was founded at the initiative of

Atatürk.

2007Anadolu Sigorta became

the first company in the Turkish insurance

business to exceed USD 1 billion in premium

production.

7Anadolu Sigorta 2017 Annual Report

2008

Anadolu Sigorta launched the C2C (Closer to Customer) change program whereby all business processes are reviewed and revised. While the company increased its profitability through sustainable growth strategy, it also received Active Academy Private Customer Satisfaction Award in Insurance for the fifth consecutive time.

2010

The company celebrated its 85th anniversary.

Planned within the frame of the C2C change program, the first set of changes was put into life.

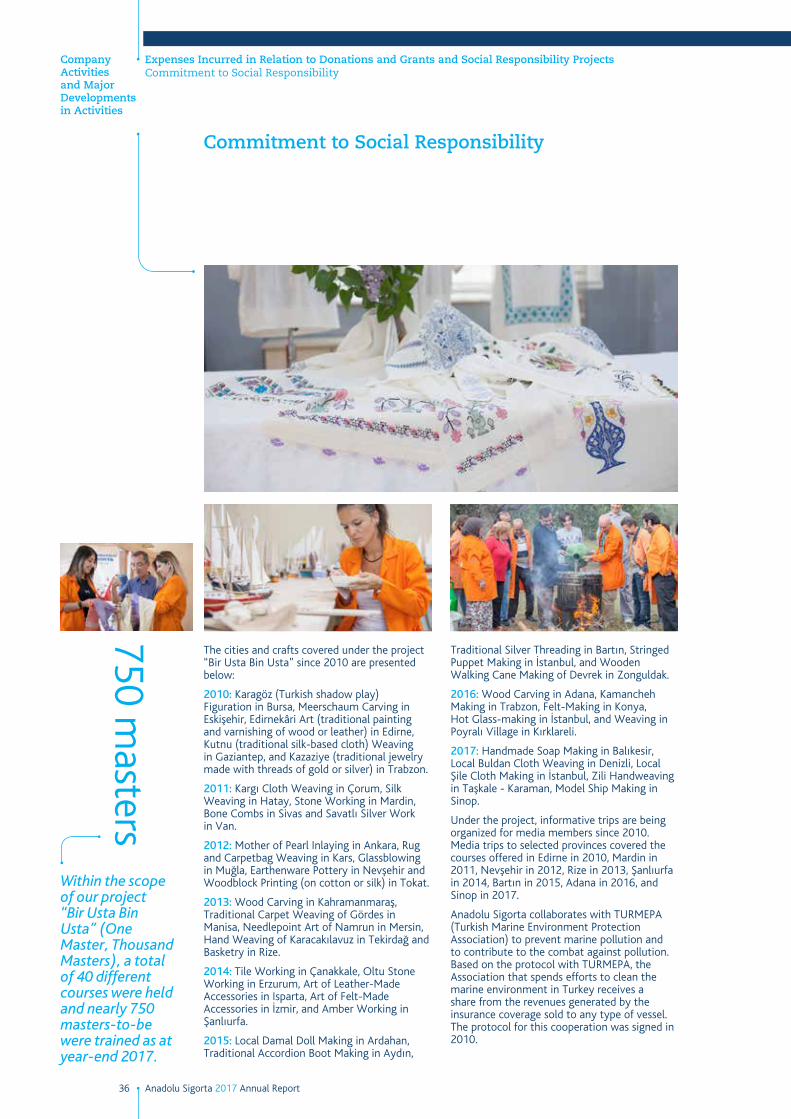

The company launched its new social responsibility project, “Bir Usta Bin Usta” (From One Master to One Thousand), thus contributing to revitalize vanishing professions in Anatolia.

2012

The company received four International award with its social responsibility project, and its 2011 Annual Report

2013

Anadolu Sigorta relocated to is new head office in Kavacık-İstanbul.

2015

While celebrating its 90th anniversary, the company launched its revamped website.

2017

Total premium production hit TL 4.7 billion.

Anadolu Sigorta doubled its net profit for the period to TL 184 million while posting an RoE of 11.2%.

1997

Aiming to make the most of the possibilities offered by IT, a “Recon Project” was launched. Services were made more efficient and productive with the inclusion of all services and agencies in the data processing network with online and real-time systems.

1999

In order to provide the fastest and most comprehensive service to its policyholders in the aftermath of the disastrous earthquake of 17 August, the company worked round the clock to provide uninterrupted service.

2001

After providing service for over five decades, the company was relocated from its building in Karaköy to İş Towers, where it would be together with İşbank subsidiaries.

2002

A brand-new era began with the “Maximum Service in Insurance” concept. The company introduced the service philosophy under one title that it has possessed since its foundation, and once again became the author of a first in the sector.

2004

Voted as “the most satisfactory insurance company with its products and services”, Anadolu Sigorta received the Active Academy Private Customer Satisfaction Award in Insurance. The company expanded its service range by taking over the health branch from Anadolu Hayat Emeklilik, which the company was required by law to give up. Anadolu Sigorta was awarded its ISO 9001: 2000 Quality Management System certification, an endorsement proving that the company’s quality management system complies with international standards.

2006

The company maintained its sectoral leadership in premium production for the fifth consecutive year and realized a premium production in excess of TL 1 billion, undersigning yet another historic result in the history of the Turkish insurance industry.

2007

The sector’s unrelenting champion in premium production for the last six years, Anadolu Sigorta became the first insurance company in Turkey to exceed the USD 1 billion threshold in total premium production.

2013

2017

The Company relocated its Head

Office units to its new modern building.

Anadolu Sigorta reached the TL 4.7 billion mark in total

premium production.

8 Anadolu Sigorta 2017 Annual Report

9Anadolu Sigorta 2017 Annual Report

Quick payment via Sigortam Cepte for

claims up to TL

Quick claim payment in 5

seconds

1,000

10 Anadolu Sigorta 2017 Annual Report

Message from the Chairman

We regard every one of our policyholders, who have been a part of our success story of 92 years and who inspired us, a member of Anadolu Sigorta family, and we carefully plan our efforts along this line.

General Information

Message from the Chairman

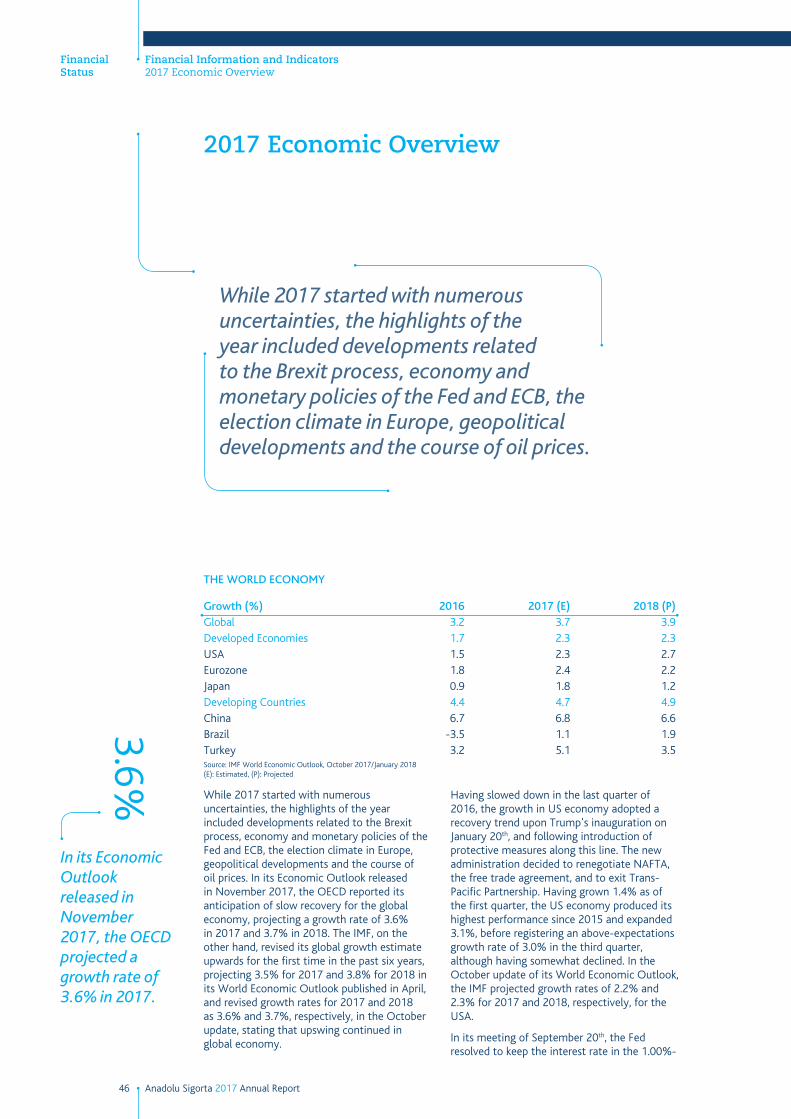

2017 has been the scene to macroeconomic improvement across the world.

During 2017, monetary policies pursued by the central banks of developed countries continued to set the course of financial markets. The US Federal Reserve (the Fed) carried on with rate hikes initiated by late 2016, and increased the rates three times during 2017, each time by 25 bps, in line with the projections; the interest rate was raised to 1.25-1.50% band at the end of the year. The Fed also started balance sheet reduction as of October 2017. Having launched extraordinarily loose monetary policy implementations relatively later than the central banks of other developed countries,

the European Central Bank (ECB) passed a decision to reduce its asset-buying program and took its first step towards monetary policy normalization. Bank of Japan (BoJ), on the other hand, kept its loose monetary policy implementation unchanged, and continued to extend support to the economy.

In 2017, acceleration in economic growth in developed countries has been noteworthy. While the US economy kept growing despite the uncertainties stemming from the policies of the new US administration justifying a new global environment prediction, the labor market approached full employment level. Inflation, on the other hand, still floats below the 2% target.

11Anadolu Sigorta 2017 Annual Report

The Turkish economy grew by 11.1% on an annual basis in the third quarter of 2017, and ranked at the top among OECD and G20 countries.

In spite of the cracks in the EU formation that became evident with the so-called Brexit, i.e. UK’s exit from the European Union (EU), coupled with the heavy election program, countries in the European region showed relative recuperation. While the rate of unemployment registered a marked decline in the last quarter of the year,

economic activity has also been a factor in increased prices. However, below-projected performance of economic activity in China put a downward push on oil prices. Other commodity prices also display an upturn.

inflation rate accelerated. Defying the political events that negatively affected the risk appetite for the Eurozone, the EUR/USD parity adopted an uptrend stimulated by the weakened US dollar combined with the positive outlook of the economic activity in the Eurozone.

During 2017 when growth performance of developing countries also backed global economic activity, continued high level of global risk appetite that picked up after the first quarter added momentum to capital inflows to developing countries.

On the other hand, the effects of China’s economic rebalancing and the course of oil and commodity prices have also been visible on the global outlook. While concerns of supply surplus persisted, extended duration of oil producing countries’ decision to cut output propped the upward move of oil prices; the positive development of global

The Turkish economy draws attention with its growth that transcended the projections.

The Turkish economy grew by 11.1% on an annual basis in the third quarter of 2017; while this growth performance that outdid the projections went down in the records as the highest growth data for the past 6 years, Turkey ranked at the top among OECD (Organization for Economic Cooperation and Development) and G20 countries.

The main contributors to this result included the revived domestic demand by virtue of tax reductions granted on furniture and white goods in a bid to enliven the economy, KKDF-backed loans practically serving as lifeline to SMEs, and increased employment owing to the employment mobilization. Growth received significant support from private consumption outlays and machinery & equipment investments. In the first nine months of the year,

12 Anadolu Sigorta 2017 Annual Report

Message from the Chairman

In the coming years, we are anticipating that the sector’s potential will turn into growth at a faster pace and the insurance business will enter a rapid, stable growth path.

General Information

Message from the Chairman

cumulative growth rate was registered as 7.4%. Accordingly, it is estimated that the Turkish economy will end 2017 with a growth rate of above 6%.

In terms of macroeconomic variables, inflation remains our soft belly. The CPI, after floating high since the start of the year, was 11.92% on an annual basis, completing the year in double digits for the first time since 2011. While this led to high interest rates, on one hand, it reminds the fact that focus must be placed particularly on structural issues in order to take inflation under control, on the other.

Despite increased export performance, higher energy prices, course of gold trade, and strong domestic demand resulted in faster growth of imports in 2017. As current deficit sustained its negative course, the rise in foreign trade deficit has been telling on the expansion of the current deficit. The ratio of current deficit to GDP is estimated to have gone up to the order of 4.5% in 2017.

Settling down of the chaos in Syria and the Middle East and mitigation of geopolitical and political risks pose priority for Turkey in the period ahead. The steps that gain the foreground in the restrengthening of economy include sustained momentum in the increase in private investments and industrial production in order for growth composition to shift in favor of investments and exports, acceleration of exports in parallel with the recovery in EU economies, and on another front, winning the struggle against inflation to return to single-digit figures, and balancing exchange rates. We believe from the bottom of our hearts that our country’s efforts to reach a more affluent future will not remain unreciprocated by virtue of the reflex our country acquired against crises and shocks, and her internal dynamics.

Altered risk outlook in the world adds to the importance of insurance.

2017 saw three of the most powerful hurricanes in the US, the first time in history to feature multiple Category 5 hurricanes in the same year, and hail and flood disasters that hit our country at short intervals. The increased intensity and frequency of meteorological phenomena are scientifically explained as a consequence of global climate change.

2017 has been an active year not only in terms of natural disasters but also of manmade damages. Manmade damages to date, such as terrorist acts, chemical explosions and severe fires, could be usually classified under such branches as liability, fire and engineering. However, the fact that the cyber attacks in 2017 are not covered under any classic reinsurance branch despite the major economic loss they caused revealed a striking fact. As a result of these events, there has been an unprecedented rise in demand for insurance providing cover against cyber risks. In this respect, 2017 also stands out as the birth year of an evolution bearing a very significant potential for the insurance business.

The development of the sector will continue at an increased speed in our country.

In the coming years, we are anticipating that the sector’s potential will turn into growth at a faster pace and the insurance business will enter a rapid, stable growth path. The prerequisites for this development include increased disposable income per capita, an economically stronger population that is demographically young, and enhanced awareness of insurance ownership.

13Anadolu Sigorta 2017 Annual Report

Our approach to be able to respond to growing needs and produce innovative solutions therefor in line with the advances in technology put us one step ahead of our peers.

Projects for raising awareness of insurance to be co-executed by the government and insurance companies contribute to creating societal awareness and the sector’s development. Anadolu Sigorta carries on with its customer-oriented proactive initiatives that will support enhanced awareness of insurance and flourished insured base through printed and social media.

the main pillars of being accessible, our perspective targeting constant change, our strict adherence to principles such as transparency, respect, discipline and integrity, and our reliability.

As we underline once again that we will always stand by our policyholders with our service and business model designed to realize our promise “never lose” drawing on our strong financial

We believe that, beyond our commercial achievements, owning our people and values played a very big part in reaching our current position.

We regard every one of our policyholders, who have been a part of our success story of 92 years and who inspired us, a member of Anadolu Sigorta family, and we carefully plan our efforts along this line. Gaining an insight into our customers’ needs, ensuring satisfaction of our policyholders at every phase of product and service delivery, and seeking and valuing their opinions make up our working principles. Our approach to be able to respond to growing needs and produce innovative solutions therefor in line with the advances in technology put us one step ahead of our peers.

In addition, the long-lived relationship we have built with our customers rise on

structure, competent human resource, and effective delivery channels being one of the sector’s leading companies, we would like to extend our thanks to our colleagues, business partners, delivery channels with whom we have been striving to achieve this goal, and to our policyholders and all our shareholders who have been giving us strength with their constantly growing trust.

Sincerely,

Caner ÇimenbiçerChairman of the Board of Directors

14 Anadolu Sigorta 2017 Annual Report

Message from the CEO

In 2017, we secured an above-the-market growth alongside high increase in profitability.

General Information

Message from the CEO

The insurance industry maintains its stable growth.

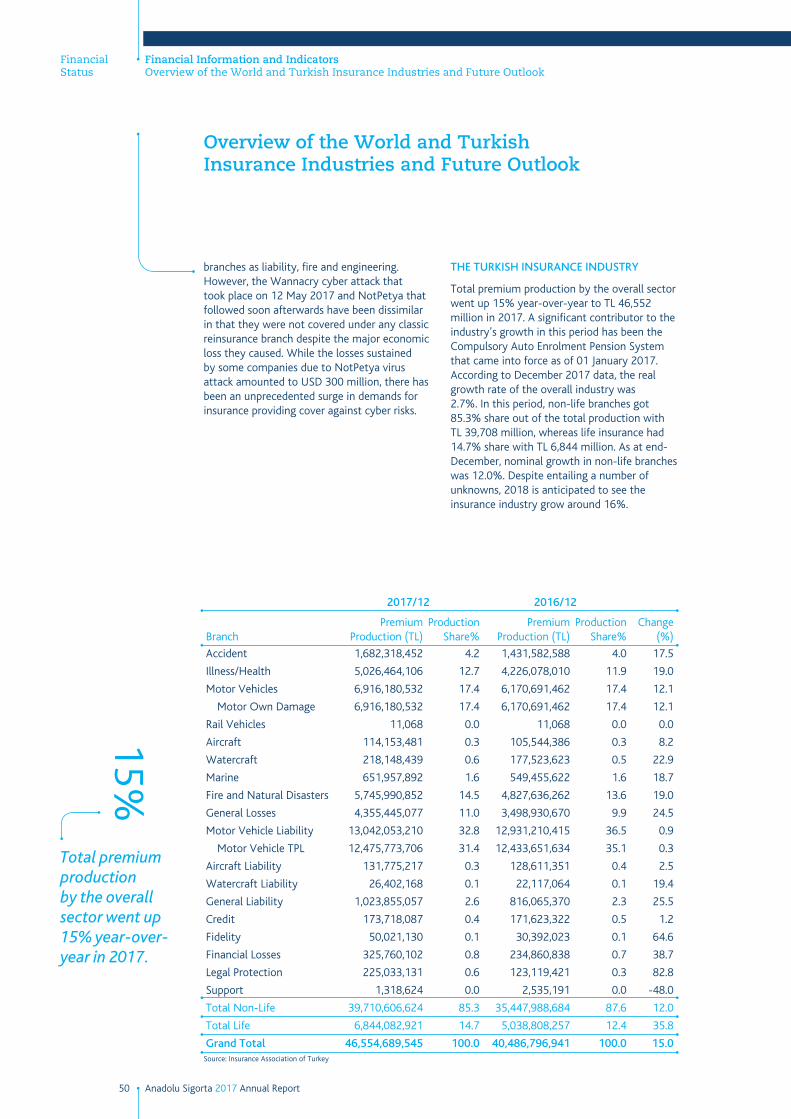

Our industry ended 2017 posting a premium production of TL 39 billion 711 million, up 12% year-on-year. From this perspective, we can suggest that it has been an exceptional year for our sector, which had registered an average annual growth rate of 15.3% over the last decade.

This modest increase in premiums was mainly the result of the price cap implementation in traffic insurance. In fact, traffic insurance premiums had already adopted a downtrend and the price cap implementation served to shorten this process.

Although premium production shows steady expansion, the production figure of USD 10 billion and its ratio to GDP that stands at 1.3% are still very low compared to other emerging countries. This, however, also represents an opportunity. Our country presents significant opportunities with her high economic growth, demographic characteristics and changing sociocultural structure.

We secured an above-the-market growth alongside high increase in profitability.

Our Company increased its premium production by 4.2% year-on-year to TL 4 billion 671 million. While the highest premium generator was the Motor Vehicles Liability branch with TL 1 billion 342 million, it was followed by Motor Vehicles with TL 953 million,

15Anadolu Sigorta 2017 Annual Report

At Anadolu Sigorta, we consider digitalization as a multi-faceted holistic strategy in terms of products, services, channels and business models.

Fire and Natural Disasters with TL 814 million, and Illness/Health with TL 538 million.

While Anadolu Sigorta ranked second among non-life companies with a market share of 11.8%, it was the sector’s leader in Motor Own Damage, Watercraft, Motor Vehicles, Fire and Natural Disasters, and General Liability branches.

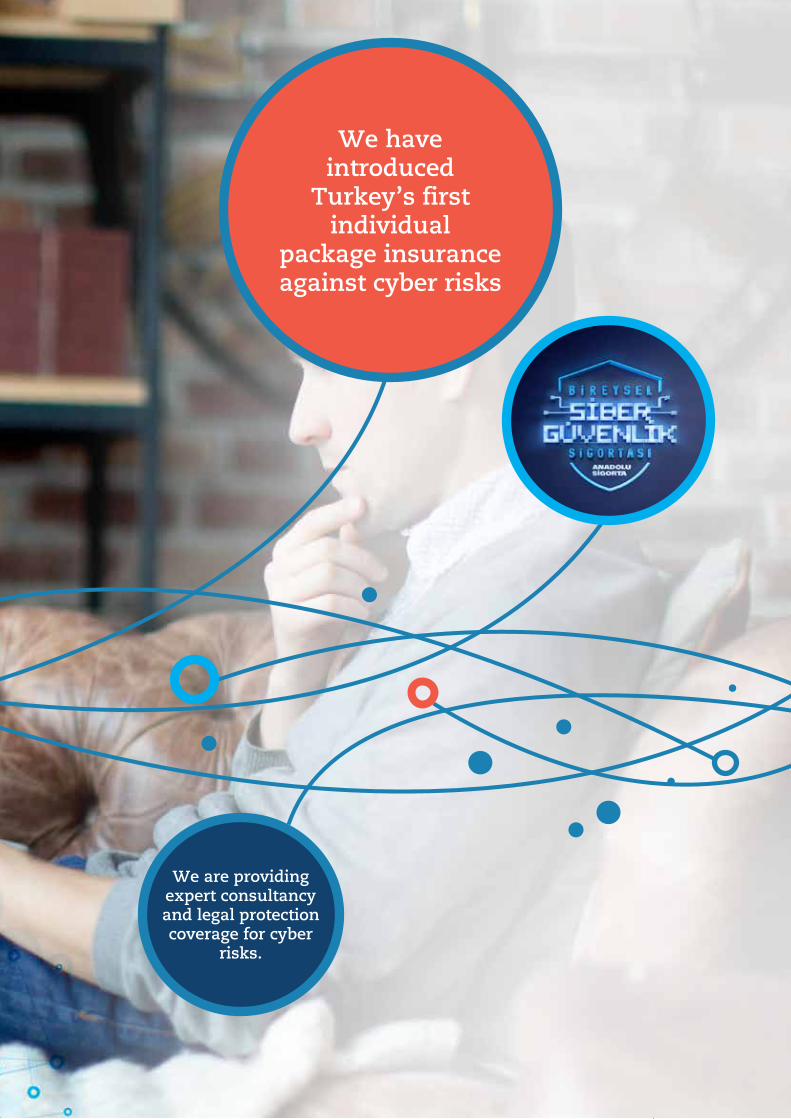

During 2017, we introduced six new products for our policyholders. We have drawn intense interest from our customers with “Full Maintenance Traffic Insurance” in traffic insurance, “Economical Motor Own Damage Insurance” and “Volkswagen Motor Own Damage Insurance” in motor own damage, “Mehmetçik Complementary Health Insurance for the Turkish Army” in illness/health, “Common Area Package Insurance” for shared living spaces like housing compounds and apartment buildings and managers’ responsibilities, and “Individual Cyber Security Insurance”, a first in our country against cyber threats.

We outgrew the market average, while securing high increase in profitability

alongside. With a 109.6% rise, we have more than doubled our net profit from TL 88 million in 2016 to TL 184.2 million in 2017. Our financial performance reflected also upon the prices of our shares traded on the exchange. While BIST-100 index increased by 47% during 2017, Anadolu Sigorta stock went up by 61% and reached a market capitalization of TL 1,550,000,000.

We have accelerated the steps we take in digital insurance.

At Anadolu Sigorta, we consider digitalization as a multi-faceted holistic strategy in terms of products, services, channels and business models.

Our digitization efforts progress on two main axes: digitalization of the Company’s own business processes and digitalization of relations with the policyholders. The steps Anadolu Sigorta takes towards digitalization are intended to maximize the productivity of all our existing channels and to enable our policyholders to access our products and services in the fastest and the most efficient way. Anadolu Sigorta digital platforms are designed to deliver the best customer experience, irrespective

16 Anadolu Sigorta 2017 Annual Report

Message from the CEO

Anadolu Sigorta digital platforms are designed to deliver the best customer experience.

General Information

Message from the CEO

of the channel through which the product is sold. For this purpose, we are integrating our digital platforms with the innovations and improvements we make in our call center implementations.

More importantly, we regard digitalization as a journey to be made together with our agents. With the Digital Agency Platform (DAP) Project, we have enabled 24/7 online sales of retail insurance products by Anadolu Sigorta agencies via their respective web pages that will run over the cloud technology.

Furthermore, we began incorporating artificial intelligence and robot technology in our processes at a greater extent. ASLI has been our first application in this area. ASLI is an RPA (Robotic Process Automation) robot and began taking over the operational workload of our agencies. Presently identifying the motor own damage policies of our agencies with imminent renewal dates and creating proposals in advance for them, ASLI’s job description will expand and evolve from standard tasks to smart ones in the future, relying on its underlying analytical structure.

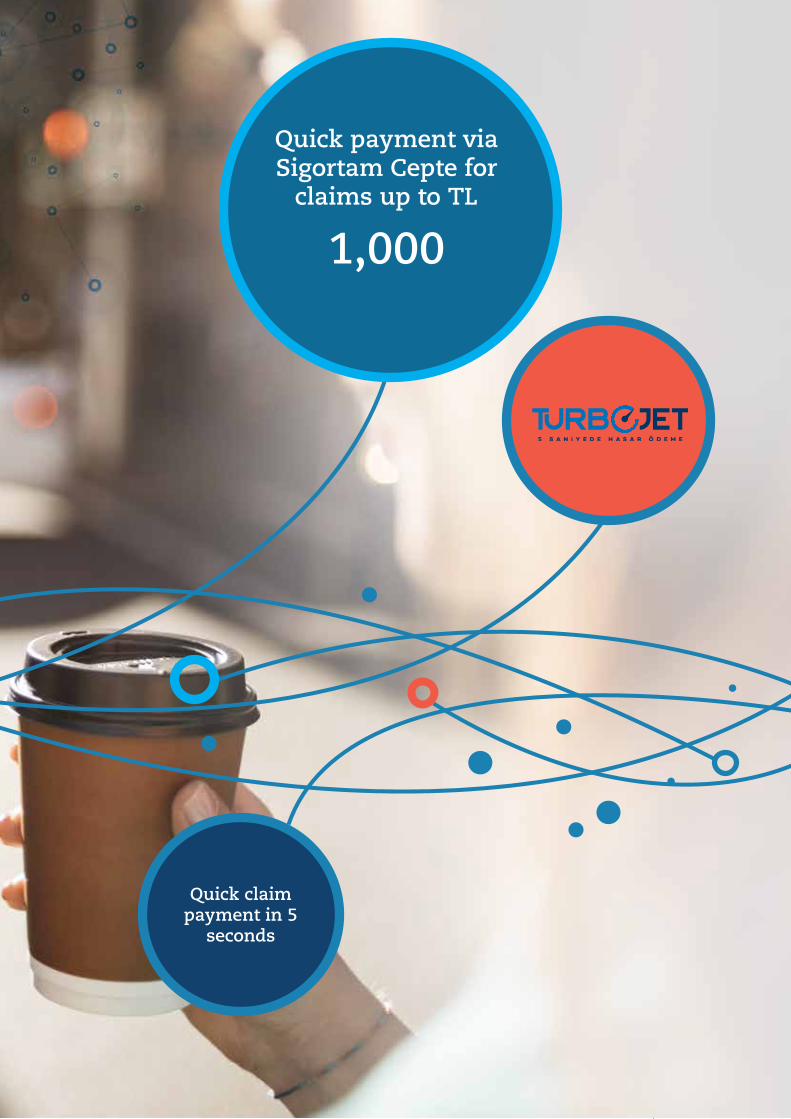

On the customer side, we have updated Sigortam Cepte, our basic mobile application, with the addition of features aimed at user-friendliness. Turbo Jet, the claims application we developed within this frame, represents a first in our country. With this application, our policyholders, who report their glass, machinery breakdown and electronic appliance damages covered in their policies via “Sigortam Cepte”, are provided with the opportunity to receive their claims payments up to TL 1,000 within 5 seconds following their claims notification. We are targeting to further expand the scope of this practice in 2018.

2017 also saw Anadolu Sigorta Hackathon take place, which we regard as a significant event that will contribute to our digital transformation journey.

Organized on 18-19 November at our Head Office with the aim of making life easier in the insurance business, Anadolu Sigorta Hackathon received nearly 150 individual applications for participation. Based on the presentations made to the jury following the competition that has welcome new digital technology projects, the projects were scored according to “innovation”, “creativity” and “feasibility” criteria. From among 14 teams formed by participants to compete in the Hackathon, the ones that ranked in the top three also received prize money.

We are providing Anadolu Sigorta assurance against cyber risks, as well.

Insurance policies to be developed against cyber risks are a hot topic both nationally and internationally. Appearing as one of the negative outcomes of technology and digitalization, cyber risks threat individuals, as well as organizations, and the dimensions of losses resulting from cyber attacks grow by the day. During 2017, we have developed the first cyber security package for individuals based on the increased importance of this matter. The “Individual Cyber Security Policy” enables taking proactive measure against potential losses stemming from cyber crimes and provides legal protection in a number of aspects.

Standing out with its comprehensive coverage, our Individual Cyber Security Insurance policy entails expert advisory for curing the possible damages suffered by reason of cyber risks and legal protection coverage, along with dark web scan that helps our policyholders protect

17Anadolu Sigorta 2017 Annual Report

themselves against personal data theft and cyber attacks.

We have left behind eight years in our project “Bir Usta Bin Usta” (One Master, Thousand Masters).

In its eighth year, the project “Bir Usta Bin Usta” (One Master, Thousand Masters) continued to revive vanishing crafts and to train the skilled masters of the future. A total of 90 masters-to-be from five cities and five crafts covered in the 2017 program of the project successfully completed the training that lasted 3 to 6 months and qualified to get their certificates.

Within the scope of the project that is honored with numerous awards in the national and international arena, 40 vocational training courses were held over eight years and 750 masters-to-be were given training; at graduation, course participants received their course completion certificates approved by the Ministry of National Education and endorsing their status as master students.

We extend our thanks to all our stakeholders who contributed to our achievements.

Also in the period ahead, we will keep pushing the limits of our own achievements and contributing to building a better future for us all in the light of our deep-rooted corporate principles and values. I would like to thank our employees who join us in our commitment to sign our name under new achievements, İşbank, bank branches that make up our bank insurance network, our agents, our policyholders and all our other stakeholders.

İlhami KoçCEO

We will keep contributing to building a better future for us all.

18 Anadolu Sigorta 2017 Annual Report

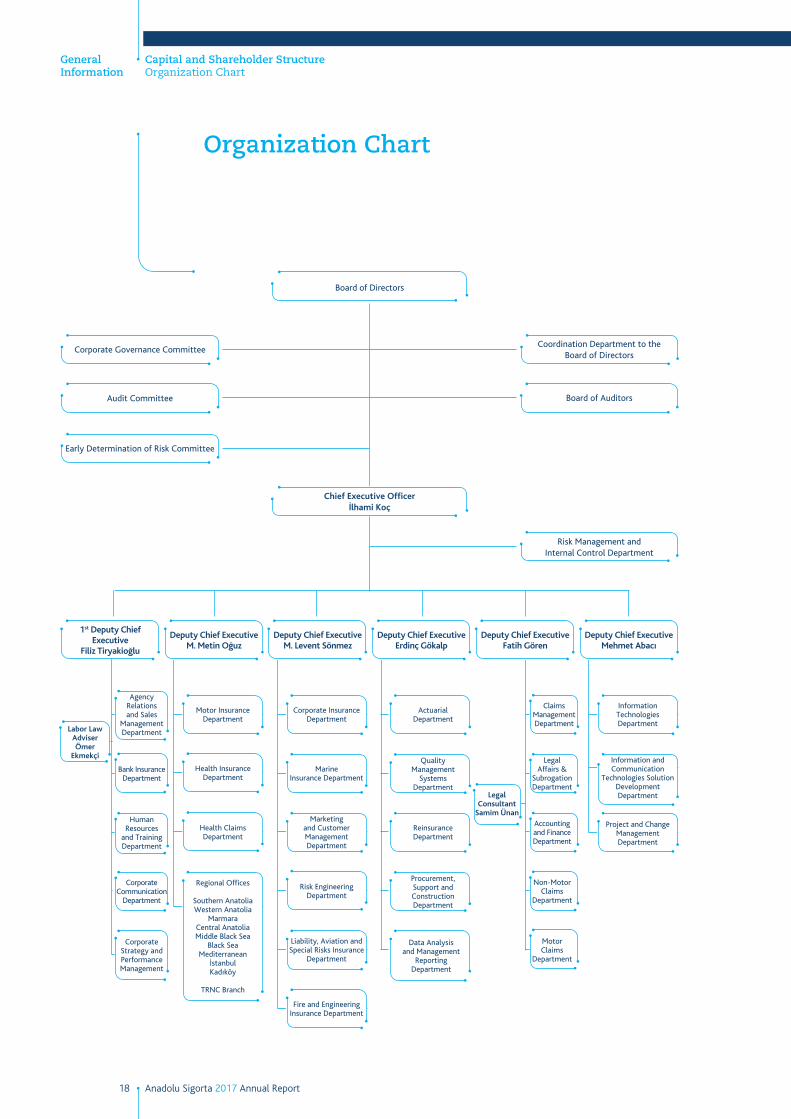

Organization Chart

General Information

Capital and Shareholder StructureOrganization Chart

Board of Directors

Chief Executive Officerİlhami Koç

Coordination Department to the Board of Directors

Board of Auditors

Risk Management and Internal Control Department

Early Determination of Risk Committee

Audit Committee

Corporate Governance Committee

1st Deputy Chief Executive

Filiz Tiryakioğlu

Motor Insurance Department

Agency Relations and Sales

Management DepartmentLabor Law

AdviserÖmer

Ekmekçi

Legal Consultant

Samim Ünan

Corporate InsuranceDepartment

Actuarial Department

Information Technologies Department

Liability, Aviation and Special Risks Insurance

Department

Fire and Engineering Insurance Department

Health Insurance Department

Health Claims Department

Marine Insurance Department

Risk Engineering Department

Marketing and Customer Management Department

Regional Offices

Southern AnatoliaWestern Anatolia

MarmaraCentral AnatoliaMiddle Black Sea

Black SeaMediterranean

İstanbulKadıköy

TRNC Branch

Deputy Chief ExecutiveM. Levent Sönmez

Deputy Chief ExecutiveFatih Gören

Deputy Chief ExecutiveM. Metin Oğuz

Deputy Chief ExecutiveErdinç Gökalp

Deputy Chief ExecutiveMehmet Abacı

Legal Affairs &

Subrogation Department

Claims Management Department

Accounting and Finance Department

Non-Motor Claims

Department

Motor Claims

Department

Bank InsuranceDepartment

Corporate Communication

Department

Corporate Strategy and Performance Management

Human Resources

and Training Department

Information and Communication

Technologies Solution Development Department

Project and Change Management Department

Quality Management

Systems Department

Reinsurance Department

Procurement, Support and Construction Department

Data Analysis and Management

Reporting Department

19Anadolu Sigorta 2017 Annual Report

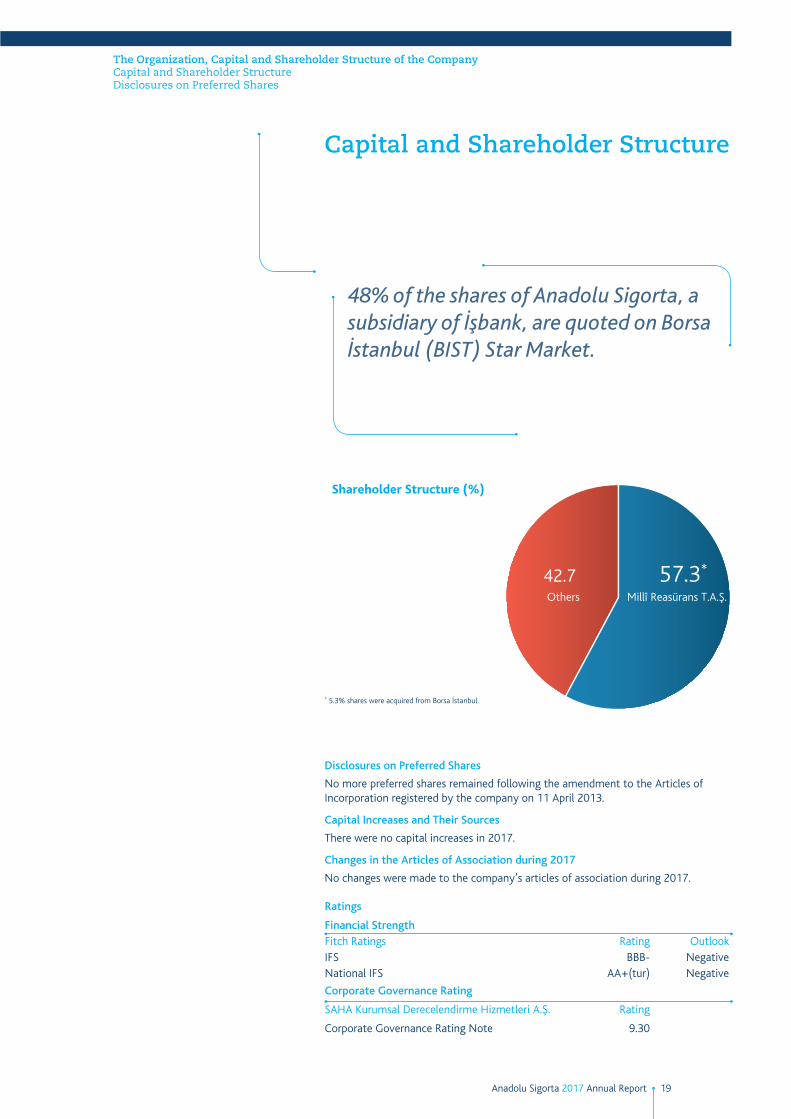

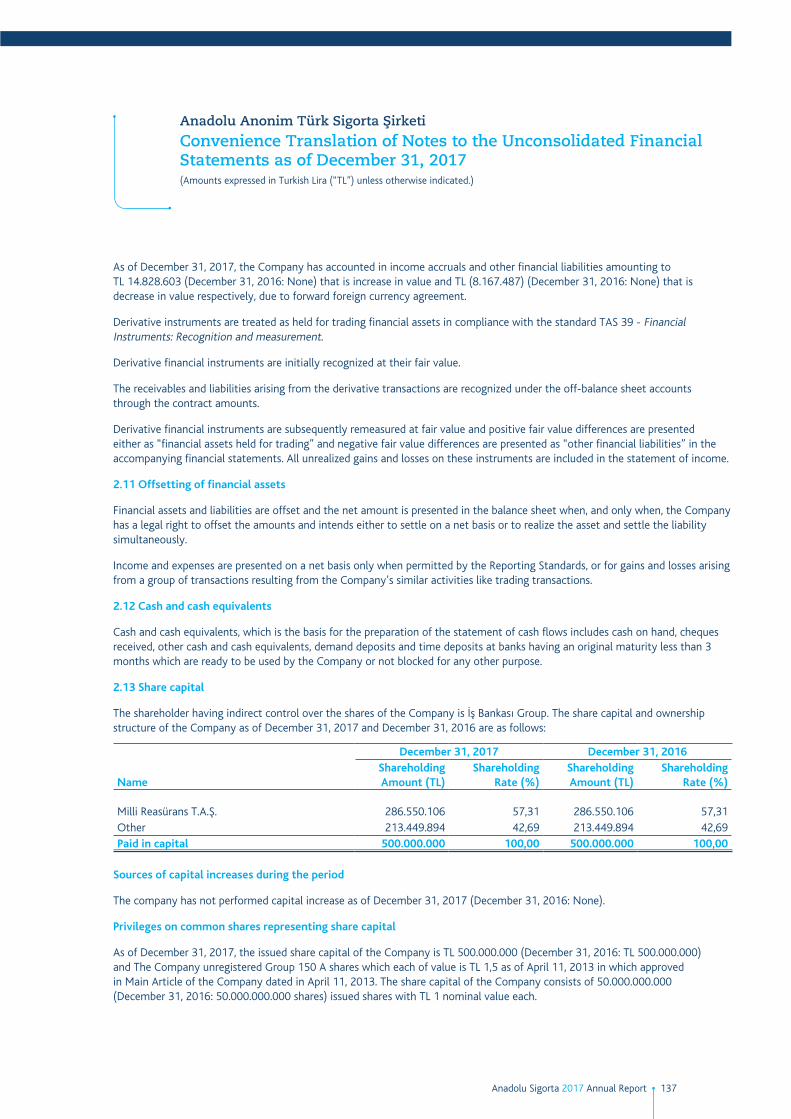

Capital and Shareholder Structure

The Organization, Capital and Shareholder Structure of the CompanyCapital and Shareholder StructureDisclosures on Preferred Shares

Disclosures on Preferred Shares

No more preferred shares remained following the amendment to the Articles of Incorporation registered by the company on 11 April 2013.

Capital Increases and Their Sources

There were no capital increases in 2017.

Changes in the Articles of Association during 2017

No changes were made to the company’s articles of association during 2017.

48% of the shares of Anadolu Sigorta, a subsidiary of İşbank, are quoted on Borsa İstanbul (BIST) Star Market.

Shareholder Structure (%)

57.3*

Millî Reasürans T.A.Ş. Others

42.7

Ratings

Financial StrengthFitch Ratings Rating OutlookIFS BBB- NegativeNational IFS AA+(tur) Negative

Corporate Governance Rating

SAHA Kurumsal Derecelendirme Hizmetleri A.Ş. Rating

Corporate Governance Rating Note 9.30

* 5.3% shares were acquired from Borsa İstanbul.

20 Anadolu Sigorta 2017 Annual Report

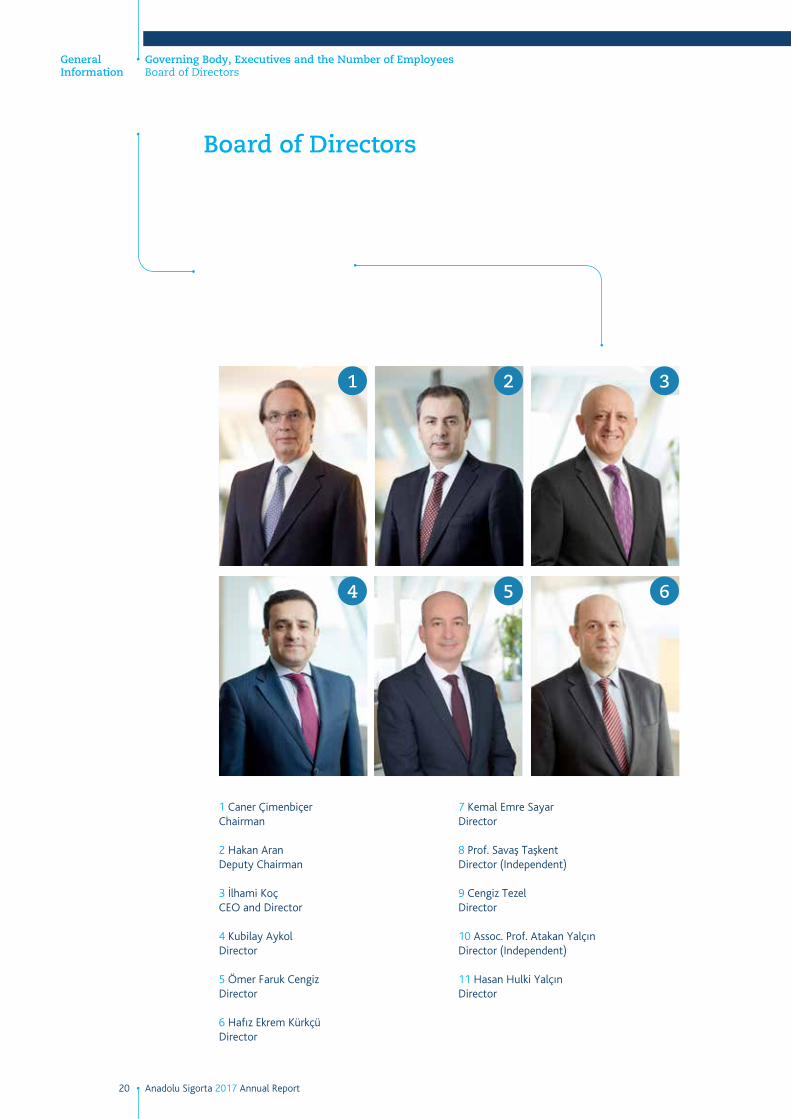

Board of Directors

General Information

Governing Body, Executives and the Number of Employees Board of Directors

1

4

2

5

3

6

1 Caner ÇimenbiçerChairman

2 Hakan AranDeputy Chairman

3 İlhami KoçCEO and Director

4 Kubilay AykolDirector

5 Ömer Faruk CengizDirector

6 Hafız Ekrem KürkçüDirector

7 Kemal Emre SayarDirector

8 Prof. Savaş TaşkentDirector (Independent)

9 Cengiz TezelDirector

10 Assoc. Prof. Atakan YalçınDirector (Independent)

11 Hasan Hulki YalçınDirector

21Anadolu Sigorta 2017 Annual Report

7

10

8

11

9

Information on Board Meetings Held in 2017 Fiscal Year

During 2017, Board of Directors of Anadolu Sigorta met 12 times and held its 1225nd meeting at the end of the year.

Topics discussed in the meetings generally consist of the reports by the Board of Directors Committees and by the Board of Inspectors, executive reports, proposals laid down by the Head Office for approval, informative memos, and working study reports that deal with the bank insurance activities. In addition, other topics raised by the members and not covered in the agenda are also discussed.

Nine meetings were held where full participation could not be achieved due to members’ justified excuses. In three of these meetings, a total of 9 members were absent, whereas six meetings were held with the absence of one member in each.

The Chairman’s invitation letter and files related to the agenda items are distributed to the members five days in advance of the meeting date.

Ayşen AygülBoard of Directors Reporter

22 Anadolu Sigorta 2017 Annual Report

Board of Directors

General Information

Governing Body, Executives and the Number of Employees Board of Directors

Caner ÇimenbiçerChairman

Born in 1952, Bursa, Caner Çimenbiçer graduated from the Business Administration department of the Faculty of Administrative Sciences at Middle East Technical University in 1973. He started his professional career at Koç-Burroughs the same year. He joined İşbank in 1974 as an assistant inspector trainee on the Board of Inspectors. After holding various positions in the Bank, he was appointed as Senior Executive Vice President in 1998, and elected as Board of Directors member from 2005 to 2008 and the Chairman of the Board from 2008 to 2011. Appointed as the Chairman and Managing Director of Anadolu Sigorta on 1 April 2011, Çimenbiçer was afterwards elected as the Chairman, on 25 March 2014. Caner Çimenbiçer served in various companies in the past ten years. Mr. Çimenbiçer was the Chairman of the Board at İzmir Demir Çelik Sanayi A.Ş. (1999-2005), Petrol Ofisi A.Ş. (2000-2005) and Petrol Ofisi Alternatif Yakıtlar Toptan Satış A.Ş. (2005). He was Deputy Chairman at Erk Petrol Yatırımları A.Ş. (2003-2005), and Petrol Ofisi Gaz İletim A.Ş. (2005), Board member at Avea İletişim Hizmetleri A.Ş. (2003-2005) and Chairman of the Board at Milli Reasürans T.A.Ş. (2008-2009). Mr. Çimenbiçer was elected the Chairman and Executive Board Director at Anadolu Sigorta on 1 April 2014, and then the Chairman on 25 March 2014.

Hakan AranDeputy Chairman

Born in 1968, Antakya, Hakan Aran graduated from the Middle East Technical University, Department of Computer Engineering in 1990. He started his career at İşbank as a Software Specialist the same year, and completed his MBA dissertation on Process Management and a Model on Information Technologies Supporting Customer-Centric Approach to Banking at Başkent University, Institute of Social Sciences, Business Administration Department between 2002 and 2003. After working as a Software Development Manager from 2005 until 2008, he was appointed Deputy CEO on 17 July 2008 at İşbank, a position he still holds. Representing Turkey on MasterCard Technology Advisory Board, Mr. Aran currently serves as the chairman of the boards of directors of İşbank Russia, SoftTech A.Ş., İşNet A.Ş., Erişim A.Ş. and LiveWell A.Ş. companies, and as Deputy Chairman of İşBank AG.

İlhami KoçCEO and Director

Born in 1963, Mr. İlhami Koç graduated from Ankara University, Department of International Relations in 1986 and started his career at İşbank as Assistant Auditor. In 1994, he was appointed as the Vice President in the Securities Department of İşbank. Following the foundation of Is Investment, he was appointed as the Head of Capital Markets and Portfolio Management in 1997. In 2001, İlhami Koç moved to Is Private Equity as the CEO. In 2002, he became the CEO of Is Investment. Mr. Koç was promoted as the Deputy Chief Executive of İşbank in 2013. In 2014, he was elected as the Chairman of the TCMA and became a Board Member at Borsa Istanbul. As of 14 November 2016, he was appointed to Anadolu Sigorta as CEO.

Kubilay AykolDirector

Born in 1974, Bolu. Kubilay Aykol graduated from Middle East Technical University (Faculty of Economics and Administrative Sciences) department of Business Administration. He began his career in 1997 at Türkiye İş Bankası, as assistant inspector at Bank’s Board Member of Inspectors. He was appointed Merter branch as branch manager position. He become an assistant manager in Retail Banking Marketing Department

in 2007. He promoted to group manager position in the Retail Banking Marketing, unit of Micro Individual Segment. Mr. Aykol was elected an Auditor at Anadolu Sigorta on 29 March 2010, and then a Board Director on 27 March 2013.

Ömer Faruk CengizDirector

Born in 1974, Ankara, Ömer Faruk Cengiz graduated from the Public Administration Department of Faculty of Political Science at Ankara University in 1998. He started his career as an assistant credit specialist at Konya Branch of İşbank in 1999, where he later functioned as credit specialist at Büşan/Konya Branch, assistant regional director at Commercial Banking Sales Division of Kayseri Regional Directorate, manager of Kahramanmaraş Branch, Gaziantep District Sales Director, and manager of Konya Commercial Branch. On 27 April 2017, he was appointed as the head of SME Banking Division. Mr. Cengiz was named a Board Director of Anadolu Sigorta on 12 June 2017.

Hafız Ekrem KürkçüDirector

1966, İstanbul. Ekrem Kürkçü graduated from Uludağ University/Education Faculty. He started his career as officer at Is Bank Harbiye Branch. He was promoted to Section Head and Sub Manager between 1995-2005 at Beyoğlu Branch, Assistant Manager between 2005-2008 at Central Operations Division. He was promoted to Unit Manager the same year. Effective from September 2008 he became Division Manager at Foreign Trade and Commercial Loans Operations Division. Mr. Kürkçü was elected a Board Director at Anadolu Sigorta on 24 March 2015.

Kemal Emre SayarDirector

1976, Ankara. A graduate of Industrial Engineering Department of the Middle East Technical University, Kemal Emre Sayar completed the graduate programs on Information Technologies in Management(MS) at Sabancı University, and on Economics and Finance(MA) at Boğaziçi University. He started his career in 1999 as an assistant internal auditor for Türkiye İş Bankası A.Ş. Following his service at Change Management and Strategy & Corporate Performance Management departments, he was appointed to Subsidiaries Department, where he still works as Unit Manager. Mr. Sayar was elected a Board Director at Anadolu Sigorta on 26 November 2015. He is also a Board Director at Milli Re and Anadolu Hayat Emeklilik.

Prof. Savaş TaşkentDirector (Independent)

Born in İstanbul, 1943, Prof. Savaş Taşkent graduated from Faculty of Law at İstanbul University. He started his academic career in 1971 as an assistant in the Department of Law of the Faculty of Basic Sciences at İstanbul Technical University. He received his Ph.D. degree from the Faculty of Law of İstanbul University and became assistant professor at İstanbul Technical University, Faculty of Management and associate professor in the Department of Labour and Social Security Law and professor in 1990 in the same faculty. He also served as Deputy Dean and Vice Rector in the same university. In 1982 and in 1987, he undertook research studies abroad (at the Universities of Erlangen and Heidelberg). Writing many articles and books on the subject of labor law, he made translations from German law into Turkish. Prof. Taşkent served also as the Head of Major Discipline of Law at the Faculty of Business Administration of İstanbul Technical University. He superannuated on 12 January 2010 and then continued to lecture “Labor Law” and “Enterprise Law”. He was appointed to Counselor position to Rector, regarding

23Anadolu Sigorta 2017 Annual Report

Governing Body, Executives and the Number of Employees Board of DirectorsDeclarations of Independence by Independent Members of the Board of Directors

law affairs as of November 2013. Between 1 April - 19 September he served as the Dean of the Gedik University Economic, Administrative and Social Sciences Faculty. Prof. Taşkent currently works freelance at the Taşkent Law and Consultancy company. Apart from these, Prof. Taşkent served as a Counselor to the Minister at the Ministry of Labor and Social Security between the years 1991-2000 and he attended the ILO Conference held in Geneva as the Counselor to the Government during the years 1991-2003. He was elected to İşbank’s Board in 2005, 2008 and 2011 respectively. He was also appointed as a member of the Audit Committee in March, 2008, the TRNC Internal Systems Committee in June, 2009, and the Corporate Governance Committee in February, 2013 at İşbank. Taşkent left his position at İşbank as of March 2014. Prof. Taşkent was elected a Board Director at Anadolu Sigorta on 16 April 2014.

Cengiz TezelDirector

1962, Antalya. Cengiz Tezel has graduated from Freie Universität of Berlin, Germany and has a diploma in Business Administration. His professional career has started at İşbank in 1986, as a team member at Berlin Branch. He has become Money Market Dealer and International Bond dealer at Head Office Ankara in 1991, Assistant Manager responsible for Treasury at Isbank GmbH Head Office Frankfurt/Main in 1995, Assistant Manager at Isbank GmbH Frankfurt/Main Branch in 1998, Assistant Manager, responsible for Investment Banking, Investment Funds & Public Relations at Isbank GmbH Head Office Frankfurt/Main in 2006, Assistant Manager responsible for Retail Banking at Balmumcu Branch in 2007, Assistant Manager responsible for Retail Banking at Galata Branch in 2008, Branch Manager at Arapcamii Branch in 2008 and Branch Manager at İşbank Multinationals Branch (Corporate Branch) in 2012. He currently holds this position. Mr. Tezel was elected a Board Director at Anadolu Sigorta on 24 March 2015.

Assoc. Prof. Atakan YalçınDirector (Independent)

Born in 1971, İstanbul, Associate Professor Atakan Yalçın is on the faculty of School of Economics and Administrative Sciences at Özyeğin University. He previously was on the faculty of Koç University and has held visiting positions at Brandeis University and Boston College. Assoc. Prof. Yalçın received an MBA degree from Cox School of Business at Southern Methodist University in 1996, and a Ph.D. degree in finance from Carroll School of Management at Boston College in 2002. Assoc. Prof. Yalçın has taught courses in Investment Management, Derivatives Securities and Financial Management. His research interest is in empirical asset pricing and empirical aspects of financial economics. His work has been published in such journals as the Journal of Empirical Finance, Journal of Banking and Finance, Journal of Financial Research, Quarterly Review of Economics and Finance, and the Journal of Marketing. Assoc. Prof. Yalçın is a member of the American Finance Association, Western Finance Association, Financial Management Association and the CFA Institute. Assoc. Prof. Yalçın was elected a Board Director at Anadolu Sigorta on 27 March 2013.

Hasan Hulki YalçınDirector

Born in 1964, Ankara, Hasan Hulki Yalçın holds a degree in Economics from the Middle East Technical University and a Master’s Degree in International Banking and Finance from the University of Birmingham (UK). After serving in various positions and capacities with İşbank for fourteen years, he joined Milli Re in 2003 and subsequently took part in a number of professional training programs abroad. He has been appointed to Milli Re as a member of Board of Directors and General Manager on 16 January 2009. Hasan Hulki Yalçın is also serving as a member of Board of Directors in the Association of the Insurance Association of Turkey. Mr. Yalçın was elected a Board Director at Anadolu Sigorta on 24 March 2011.

2 March 2017

To: Anadolu Anonim Türk Sigorta Şirketi Corporate Governance Committee

I hereby declare that I satisfy the criteria of independence pursuant to applicable legislation within the framework of the criteria covered in the Communiqué on the Determination and Implementation of Corporate Governance Principles, and submit my candidacy as an independent member of the Board of Directors of Anadolu Anonim Türk Sigorta Şirketi.

Yours sincerely,

Prof. Savaş Taşkent

2 March 2017

To: Anadolu Anonim Türk Sigorta Şirketi Corporate Governance Committee

I hereby declare that I satisfy the criteria of independence pursuant to applicable legislation within the framework of the criteria covered in the Communiqué on the Determination and Implementation of Corporate Governance Principles, and submit my candidacy as an independent member of the Board of Directors of Anadolu Anonim Türk Sigorta Şirketi.

Yours sincerely,

Assoc. Prof. Atakan Yalçın

Declarations of Independence by Independent Members of the Board of Directors

24 Anadolu Sigorta 2017 Annual Report

Executive Committee

General Information

Governing Body, Executives and the Number of Employees Executive Committee

1

4

2

5

3

6

7

1 İlhami KoçCEO

2 Filiz Tiryakioğlu1st Deputy Chief Executive

3 Mehmet Metin OğuzDeputy Chief Executive

4 M. Levent SönmezDeputy Chief Executive

5 Erdinç GökalpDeputy Chief Executive

6 Fatih GörenDeputy Chief Executive

7 Mehmet AbacıDeputy Chief Executive

25Anadolu Sigorta 2017 Annual Report

İlhami KoçCEOBorn in 1963, Mr. İlhami Koç graduated from Ankara University, Department of International Relations in 1986 and started his career at İşbank as Assistant Auditor. In 1994, he was appointed as the Vice President in the Securities Department of İşbank. Following the foundation of Is Investment, he was appointed as the Head of Capital Markets and Portfolio Management in 1997. In 2001, İlhami Koç moved to Is Private Equity as the CEO. In 2002, he became the CEO of Is Investment. Mr. Koç was promoted as the Deputy Chief Executive of İşbank in 2013. In 2014, he was elected as the Chairman of the TCMA and became a Board Member at Borsa İstanbul. As of 14 November 2016, he was appointed to Anadolu Sigorta as CEO.

Filiz Tiryakioğlu1st Deputy Chief ExecutiveAgency Relations and Sales Management DepartmentBank Insurance Department Human Resources and Training Department Corporate Communication DepartmentCorporate Strategy and Performance ManagementBorn on 26 June 1967 in İstanbul, Filiz Tiryakioğlu graduated from Anadolu University, Faculty of Business Administration, Department of Business Administration. She started her career at Anadolu Sigorta as a Clerk at the Fire Department on 16 September 1985. She rose to Assistant Superintendent at the same department on 1 January 1990. She was appointed to the Claims Department on 1 February 1993 as Superintendent, then rose to Chief Superintendent on 1 May 1996, and Assistant Manager on 1 March 1998 at the same department. She became a Manager at the Training Department on 1 June 2000 and was then appointed as the Human Resources and Training Manager on 1 August 2004. She was appointed as Deputy Chief Executive Officer on 1 February 2008 and 1st Deputy Chief Executive on 25 December 2013.

Mehmet Metin OğuzDeputy Chief Executive Regional OfficesTRNC BranchMotor Insurance DepartmentHealth Insurance DepartmentHealth Claims DepartmentBorn on 4 April 1959 in Çanakkale, M. Metin Oğuz graduated from Middle East Technical University, Faculty of Arts and Sciences, Department of Physics and Mathematics, and holds a master’s degree from Marmara University Institute of Banking and Insurance, Department of Insurance. M. Metin Oğuz began his career at Anadolu Sigorta as a Clerk in the Accident Department on 16 October 1985 and subsequently rose to Assistant Superintendent on 1 February 1989, Superintendent on 1 February 1992, Chief Superintendent on 1 February 1995, Assistant Manager on 1 May 1997, Manager on 1 March 1998, and Motor Insurance Manager on 1 June 2002. Having served in the last position until 31 July 2004, M. Metin Oğuz became a Deputy Chief Executive Officer on 1 August 2004.

M. Levent SönmezDeputy Chief ExecutiveMarketing and Customer Management DepartmentCorporate Insurance DepartmentMarine Insurance DepartmentRisk Engineering DepartmentLiability Aviation and Special Risks Insurance DepartmentFire and Engineering Insurance Department Born on 22 June 1962 in Ankara, M. Levent Sönmez graduated from İstanbul Technical University, Faculty of Maritime Studies, Department of Marine Engineering in 1985, got his master’s degree in “Contemporary Management Techniques” from Marmara University & Maine University and completed the “SITC (Swiss Re) Marine Insurance” program. Having participated in various training programs in Turkey and abroad, M. Levent Sönmez also holds “Chartered Insurance Institute/London Dip. CII” degree. He started his career at Anadolu Sigorta as a Specialist at the Marine Department on 1 May 1991 and continued working with same title

till 30 April 1996. He subsequently rose to Specialist position on 1 March 1994, Chief Superintendent position on 1 May 1996, Assistant Manager on 1 October 1997, and Manager on 1 May 1999. M. Levent Sönmez has become Bakırköy Regional Manager on 1 June 2002 and Kadıköy Regional Manager on 1 August 2004. He has been appointed as Deputy Chief Executive Officer on 1 February 2008.

Erdinç GökalpDeputy Chief ExecutiveActuarial DepartmentQuality Management Systems DepartmentReinsurance DepartmentProcurement and Construction DepartmentData Analysis and Management Reporting Department Born on 26 July 1967 in Ankara, Erdinç Gökalp graduated from Kuleli Military High School and Turkish Military Academy, Department of Business Administration. He then got his master’s degree in insurance from Marmara University, Institute of Banking and Insurance. During his employment with Anadolu Sigorta, he earned the Atatürk scholarship granted by TSB (Insurance Association of Turkey) and pursued his studies abroad. Having started his career at Anadolu Sigorta as Specialist at the Marketing Department on 1 May 1991, Erdinç Gökalp was appointed to the Reinsurance Department on 23 September 1991, rose to senior specialist position and continued working till 30 April 1996 with the same title. He promoted to Chief Superintendent position on 1 May 1996 and to Assistant Manager position on 1 October 1997, he was appointed to the Marketing Department. Erdinç Gökalp was appointed to the Accident Department on 26 December 1997 with the same title. He rose to the position of Manager and was assigned to the Reinsurance Department on 1 July 2001. Erdinç Gökalp has been appointed as Deputy Chief Executive Officer on 1 February 2008.

Fatih GörenDeputy Chief ExecutiveClaims Management Department Legal Affairs & Subrogation DepartmentAccounting and Finance DepartmentMotor Claims DepartmentNon-Motor Claims DepartmentBorn on 11 November 1969 in Ankara, Fatih Gören graduated from Ankara University, Faculty of Political Sciences, Department of International Relations. He worked as a Specialist at Retail Banking and Agricultural Loans Departments at Ziraat Bank between 1991 and 1994. Having joined Anadolu Sigorta as an Assistant Inspector on the Board of Inspectors on 1 November 1994, Fatih Gören rose to Senior Assistant Inspector on 1 November 1997 and grade 3 Inspector on 1 November 1998. He was appointed as Assistant Manager to the Accounting and Finance Department on 1 June 2000, where he was promoted to Manager position on 1 August 2004. Fatih Gören has been appointed as Deputy Chief Executive Officer on 1 February 2008.

Mehmet AbacıDeputy Chief ExecutiveInformation Technologies Department Information and Communication Technologies Software Development DepartmentProject and Change Management DepartmentBorn in 1967 in Ankara. Mehmet Abacı, graduated from the Department of Metallurgical and Materials Engineering, Faculty of Engineering at Middle East Technical University in 1991. Starting his professional career at İşbank IT Department, as a Software Specialist the same year, Mehmet Abacı, was appointed as Assistant Manager in 1999, and Unit Manager in 2004. He was promoted as Deputy Chief Executive Officer at SoftTech in 2008, and became Solution Development Manager and Project & Change Manager at İşbank in 2010 and in 2011 respectively. Mehmet Abacı was appointed as Deputy Chief Executive Officer of SoftTech for a second term, on 1 January 2011. As of June 2012, he took office at Anadolu Sigorta as Deputy Chief Executive Officer.

26 Anadolu Sigorta 2017 Annual Report

Heads of Units Under the Internal Systems

General Information

Governing Body, Executives and the Number of Employees Heads of Units Under the Internal SystemsAverage Number of Employees by Categories During the Reporting Period

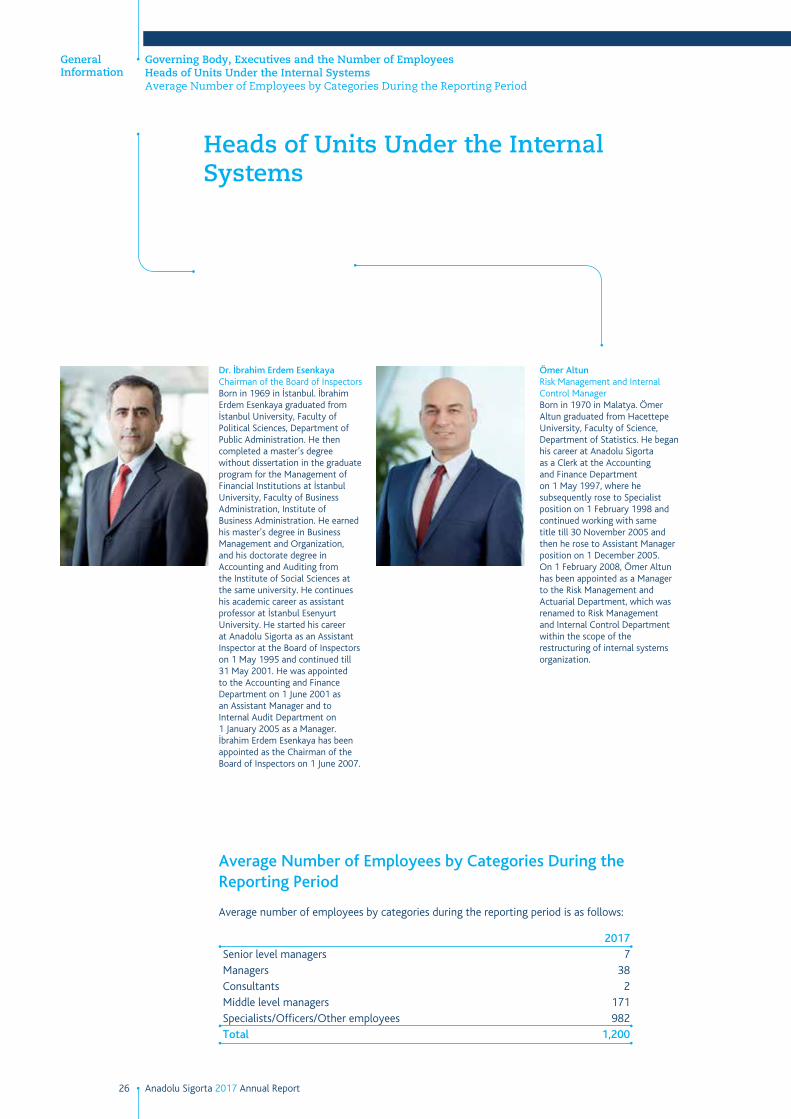

Ömer AltunRisk Management and Internal Control Manager Born in 1970 in Malatya. Ömer Altun graduated from Hacettepe University, Faculty of Science, Department of Statistics. He began his career at Anadolu Sigorta as a Clerk at the Accounting and Finance Department on 1 May 1997, where he subsequently rose to Specialist position on 1 February 1998 and continued working with same title till 30 November 2005 and then he rose to Assistant Manager position on 1 December 2005. On 1 February 2008, Ömer Altun has been appointed as a Manager to the Risk Management and Actuarial Department, which was renamed to Risk Management and Internal Control Department within the scope of the restructuring of internal systems organization.

Dr. İbrahim Erdem EsenkayaChairman of the Board of Inspectors Born in 1969 in İstanbul. İbrahim Erdem Esenkaya graduated from İstanbul University, Faculty of Political Sciences, Department of Public Administration. He then completed a master’s degree without dissertation in the graduate program for the Management of Financial Institutions at İstanbul University, Faculty of Business Administration, Institute of Business Administration. He earned his master’s degree in Business Management and Organization, and his doctorate degree in Accounting and Auditing from the Institute of Social Sciences at the same university. He continues his academic career as assistant professor at İstanbul Esenyurt University. He started his career at Anadolu Sigorta as an Assistant Inspector at the Board of Inspectors on 1 May 1995 and continued till 31 May 2001. He was appointed to the Accounting and Finance Department on 1 June 2001 as an Assistant Manager and to Internal Audit Department on 1 January 2005 as a Manager. İbrahim Erdem Esenkaya has been appointed as the Chairman of the Board of Inspectors on 1 June 2007.

Average Number of Employees by Categories During the Reporting Period

Average number of employees by categories during the reporting period is as follows:

2017Senior level managers 7Managers 38Consultants 2Middle level managers 171Specialists/Officers/Other employees 982Total 1,200

27Anadolu Sigorta 2017 Annual Report

Financial Affairs and Actuarial Unit ManagersFinancial Rights Provided to the Members of the Governing Body and Executives

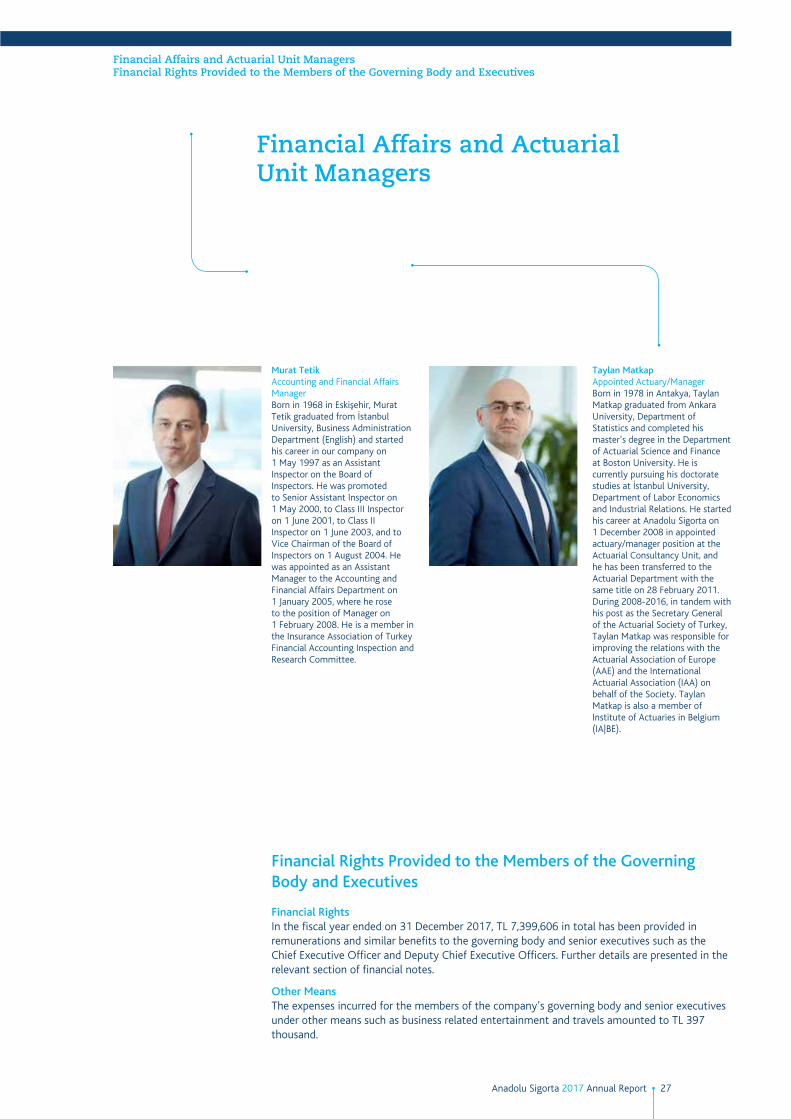

Taylan MatkapAppointed Actuary/ManagerBorn in 1978 in Antakya, Taylan Matkap graduated from Ankara University, Department of Statistics and completed his master’s degree in the Department of Actuarial Science and Finance at Boston University. He is currently pursuing his doctorate studies at İstanbul University, Department of Labor Economics and Industrial Relations. He started his career at Anadolu Sigorta on 1 December 2008 in appointed actuary/manager position at the Actuarial Consultancy Unit, and he has been transferred to the Actuarial Department with the same title on 28 February 2011. During 2008-2016, in tandem with his post as the Secretary General of the Actuarial Society of Turkey, Taylan Matkap was responsible for improving the relations with the Actuarial Association of Europe (AAE) and the International Actuarial Association (IAA) on behalf of the Society. Taylan Matkap is also a member of Institute of Actuaries in Belgium (IA|BE).

Murat TetikAccounting and Financial Affairs ManagerBorn in 1968 in Eskişehir, Murat Tetik graduated from İstanbul University, Business Administration Department (English) and started his career in our company on 1 May 1997 as an Assistant Inspector on the Board of Inspectors. He was promoted to Senior Assistant Inspector on 1 May 2000, to Class III Inspector on 1 June 2001, to Class II Inspector on 1 June 2003, and to Vice Chairman of the Board of Inspectors on 1 August 2004. He was appointed as an Assistant Manager to the Accounting and Financial Affairs Department on 1 January 2005, where he rose to the position of Manager on 1 February 2008. He is a member in the Insurance Association of Turkey Financial Accounting Inspection and Research Committee.

Financial Rights Provided to the Members of the Governing Body and Executives

Financial RightsIn the fiscal year ended on 31 December 2017, TL 7,399,606 in total has been provided in remunerations and similar benefits to the governing body and senior executives such as the Chief Executive Officer and Deputy Chief Executive Officers. Further details are presented in the relevant section of financial notes.

Other MeansThe expenses incurred for the members of the company’s governing body and senior executives under other means such as business related entertainment and travels amounted to TL 397 thousand.

Financial Affairs and Actuarial Unit Managers

28 Anadolu Sigorta 2017 Annual Report

29Anadolu Sigorta 2017 Annual Report

We have introduced

Turkey’s first individual

package insurance against cyber risks

We are providing expert consultancy and legal protection coverage for cyber

risks.

30 Anadolu Sigorta 2017 Annual Report

Research and Development Pertaining to New Services and Business Activities

Research and Development Activities of the Company

Research and Development Pertaining to New Services and Business Activities

In a bid to increase product diversity and respond to demands for different assurance needs, “Common Area Package Insurance”, “Volkswagen Motor Own Damage Insurance”, “Economical Motor Own Damage Insurance”, “Full Maintenance Traffic Insurance”, “Mehmetçik Complementary Health Insurance for the Turkish Army” and “Individual Cyber Security Insurance”, a first in the sector, have been launched. Home Package and Compulsory Earthquake Insurance products started to be issued from the new policy management platform, ASOS.

To mitigate operational workload and offer uninterrupted service to policyholders of commodity marine insurance, the most comprehensive certificate program available in the industry has been introduced.

A brand new visual design was prepared and related system changes were performed in order to standardize secure saving from the number of pages and simplification of the policy printouts.

Digital Agency Platform (DAP), which is designed to allow agencies to carry out policy sales via their own web pages, went live and was put to use for our agencies.

Introduced for allowing agencies to easily perform a number of day-to-day transactions from a single screen, Asenta platform was enriched with new products, cross-selling, premium calculation and comparison capabilities.

An incentive and compensation management system was put into use for managing and more effective monitoring of campaigns directed towards our delivery channels, their integration with other systems and automation of processes that were previously handled manually.

Work was carried out to improve user experience on digital channels; within this frame, frontends of our applications were upgraded in view of current design principles.

Personal health insurance policies can now be issued using our digital channels with the “My Policy is Ready” application. “Bireysel Şube”, “Ofisim Cepte” and “Sigortam Cepte” applications give access to coverage limits, used and remaining limits and similar information related to health insurance policies. In addition,

appointment creation within the scope of VIP assistance service and viewing the hospitals and pharmacies nearest the users’ locations are added as new functions to Sigortam Cepte application.

In line with the objective of speeding up claims processes and enhance customer satisfaction, “No Touch” application went live, which allows settlement of fire and engineering claims within set amounts in 24 hours the latest, subject to surveyor’s ascertainment and approval. In addition, via the so-called “Turbo Jet” application, which is a first in Turkey, once the notification information and photo of the invoice are uploaded to Sigortam Cepte application for policyholders and damages that conform to certain criteria, the claim is instantly handled by artificial intelligence and the payment can be made to the policyholder’s bank account within approximately 5 seconds.

In order to better manage the intensity caused by hail/flood damages that occurred during the reporting period, agreements were made with new suppliers in addition to existing repair centers, and Anadolu Sigorta Hail Repair Centers started operations in İstanbul and Mersin.

A project was initiated aimed at more effective management of our claims and legal processes.

Operational processes, which were handled via email between regional branches and agencies and which could not be measured and monitored, were redesigned, and a workflow application called PAS was developed and rolled over across all regional branches.

Analysis, feasibility and coordination work were carried out to determine the processes that can run within the scope of Robotic Process Automation (RPA). Analysis, design and launch phases were completed for Motor Own Damage renewal process.

The new reinsurance application (ART) went live following development and testing.

Risk engineering application, which is developed for effective monitoring of risk analysis processes, started to be used across the Company, including all sales departments.

“No Touch” application went live for settlement of claims within 24 hours maximum.

“No Touch”

31Anadolu Sigorta 2017 Annual Report

2017-2018 Primary Goals, PoliciesInformation on the Company’s Investments

2017-2018 Primary Goals, Policies

Being Turkey’s deepest-rooted and most experienced insurance company, our vision is defined as being the brand preferred by everyone who needs insurance, and our mission is spelled out as helping create a broad awareness of insurance in our country, leading the sector, and enhancing the value of our company.

In keeping with this vision and mission, securing a successful performance that is also reflected on the financial results amid the fiercely competitive environment of the insurance sector is an inevitable necessity in order to maintain our solid financial strength. To achieve this goal, sustainable technical profitability and increased market share are targeted to be attained in 2018 on the back of a delicate balance between growth and profitability.

In view of the existing risks and forecasts in relation to the national economy, priority will be given to efficiency while adhering to growth targets, utmost sensitivity will be exercised in risk selection and correct pricing will not be compromised. Furthermore, processes will be simplified in order to increase the speed and productivity of operations, and technology automation that will secure higher productivity will be introduced on one hand, while targets will be tracked carefully, employing performance and budget management methods, on the other.

In the period ahead, compulsory insurance introduced by the government and insurance receiving government support are anticipated to keep driving the industry. Although the arrangements introduced by the regulatory authority in compulsory traffic insurance, the most commonly known product in the industry which is also responsible for a substantial portion of premium production, have somewhat cutback the premiums that have adopted an uptrend in the previous years, it is an absolute necessity for the industry to generate sustainable and reasonable technical profit in order for it to maintain solid reserves in this branch that has been basically set up for the public interest.

One of our strategic goals is to develop new products and services directed at fulfilling the changing needs of the insurable audience. Within this scope, we will continue in 2018, as we did in 2017, to introduce new and innovative products, and highlight differentiated price and service levels for customers paying regard to current economic conditions and risks.

Digital insurance will remain as another topic of focus for us. Use of digital tools and digital business models are anticipated to persist in the insurance industry. Hence, we will keep developing functions that will increase the

usage ratios of our mobile applications by our customers and our business partners, and we will continue to upgrade existing services. Addition of new products to digital channels and investing in technology and business models that will facilitate transacting and interacting of all our business partners and especially our agencies via digital channels are inevitable requirements of our day.

Non-life insurance sector places much emphasis on the language to be used with the insurable audience and customers. The tone of the messages conveyed is also crucial with respect to correct perception of insurance and leveraging the credibility of the sector. A powerful brand reputation is directly linked to positive perception of our brand by our target audiences. For this purpose, we will uninterruptedly carry on with product and service communication initiatives. The communication maintained on all media where our policyholders and target audiences have a presence positions Anadolu Sigorta as an accessible, consumer-friendly company that is a benchmark in its own field. In addition to these efforts, our brand reputation is further strengthened through media relations, risk communication, reputation management and social responsibility initiatives contributing value to the community.

Possessing a talented, highly motivated workforce that efficiently uses technology will be one of the most critical success factors in the medium term. To further leverage the Company’s overall business performance and to be able to proactively follow up the trends particularly in the digitalizing world, it is crucial to attract highly qualified employees to our Company. We will be attaching even more importance to this topic in the future, while employer brand initiatives will be carried out and weight will be given to efforts to be a company that is preferred at a much higher extent by the candidates.

Information on the Company’s InvestmentsThe company’s outlays in 2017 amounted to USD 10.2 million for projects carried out for revising basic insurance implementations, enhancing operational efficiency within the scope of the company’s information and communication technology investments. These projects are detailed under the heading “Research and Development Activities of the Company”.

We will keep concentrating on digital insurance.

digital

Company Activities and Major Developments in Activities

32 Anadolu Sigorta 2017 Annual Report

An Assessment of 2017 by the Board of Inspectors

Company Activities and Major Developments in Activities

Internal Control System and Internal Audit Activities An Assessment of 2017 by the Board of Inspectors

Pursuant to the Regulation on the Internal Systems of Insurance and Reinsurance and Pension Companies, the internal audit activity at our company is carried out by the Board of Inspectors reporting to our company’s Board of Directors. The Board of Directors reviewed and acquainted itself with the 2017 Activity Report of the Board of Inspectors.

In 2017, 28 headquarters units, 9 regional branches and 1 branch adding up to 38 units in total were audited and the resulting determinations and assessments were reported.

Initiated in order to monitor the extent at which the audited units fulfill the requirements of the reports resulting from the audits conducted, follow-up audits continued to be carried out in 2017. A total of 24 follow-up audits were conducted during 2017, 10 of which resulted from 2016 audits.

Auditing of agencies persisted pursuant to the Regulation on the Internal Systems of Insurance and Reinsurance and Pension Companies during 2017, and 971 agencies were audited, and the results were reported.

On the other hand, based on Articles 16/1 and 17/2 of the Regulation on the Internal Systems of Insurance and Reinsurance and Pension Companies, audits were conducted at all of the agencies that remain after eliminating those that were dissolved during the reporting period from the 2,410 agencies that were listed in the audit programs approved by the Board of Directors and planned to be audited in the 2015-2017 period.

In line with the experiences derived from agency audits, agencies were continued to be assessed through scoring based on the financial data for the past three years, within the frame

of efforts to further expand and strengthen the central auditing of agencies and to create early warning systems that correctly identify and reveal the risk elements in advance.

In 2017, 33 studies were completed: 12 investigations, 12 examinations and 9 other studies.

As of year-end 2017, the Board of Inspectors was staffed by 15 board members consisting of inspectors and assistant inspectors. With the aim to support professional development of the Board members and to expand their professional knowledge, their participation in various seminars, meetings and training programs in Turkey and abroad have been facilitated. In this frame, efforts were carried on also in 2017 so that the members of the Board of Inspectors obtain nationally and internationally recognized professional certificates.

Developments are carefully monitored to ensure that the audits conducted and the reports subsequently issued take account of the “International Standards for Internal Audit”, are risk-focused, provide assurance for risk management and contribute added value to our company and necessary revisions and changes are made accordingly.

The Board of Inspectors will keep carrying out the activities within the context of the internal audit program prepared, as well as other activities outside of this scope, based on the fundamental approach for maximizing the benefits expected from internal auditing.

33Anadolu Sigorta 2017 Annual Report

Internal Control System and Internal Audit Activities Internal Control System and an Assessment by the Governing Body

Internal Control System and an Assessment by the Governing Body

Pursuant to the provisions of the “Regulation on the Internal Systems of Insurance, Reinsurance and Pension Companies” enforced upon its publication in the Official Gazette issue 26913 dated 21 June 2008, the Risk Management and Internal Control Department was set up in a structure so as to be conducted and administered directly by the CEO, and vested in the powers and responsibilities that will allow the Department to assess the risk exposure and internal control environment in an independent/impartial and effective fashion. The Board Director responsible for Internal Systems is also responsible toward the Board of Directors for the formation of the Department and ensuring, monitoring and coordinating its operability, adequacy and effectiveness.

The duties, powers and responsibilities of the individuals charged with the operation and activities of the Internal Control system, and for conducting the activities are defined in the relevant Operating Guidelines released. The internal control system is set up as a separate mechanism independent from the internal audit system, based on applicable legislation and numerous references available in national and international literature.