welcome to oerlikon solar eu pvsec hamburg 2009 · dr. paolo campinoti, ceo of pramac group...

TRANSCRIPT

Welcome to Oerlikon SolarEU PVSEC Hamburg 2009

Hamburg, September 2009

This presentation is based on information currently available tomanagement. The forward-looking statements contained herein could be substantially impacted by risks and influences that arenot foreseeable at present, so that actual results may vary materially from those anticipated, expected or projected.

Disclaimer

Business Overview

Page 4 22/09/2009 EU PVSEC 2009 Presentation

Oerlikon is a provider of clean-technology solutions100 year history, 2008 sales of CHF 4.8 billion

Oerlikon Vacuum

Oerlikon Coating

Oerlikon Fairfield

Oerlikon Systems

Leading coatings in the automotive sector:- 10x durability- 4% less energy consumption

Vacuum solutions for the solar industry

Loose gears for wind turbines

Advanced Nanotechnology for solar cells, thermo-electric generators and batteries

Oerlikon Graziano

Transmissions for hybrid cars

Oerlikon SolarOerlikon Solar

Leading provider of silicon based thin film solar technology

Page 5 22/09/2009 EU PVSEC 2009 Presentation

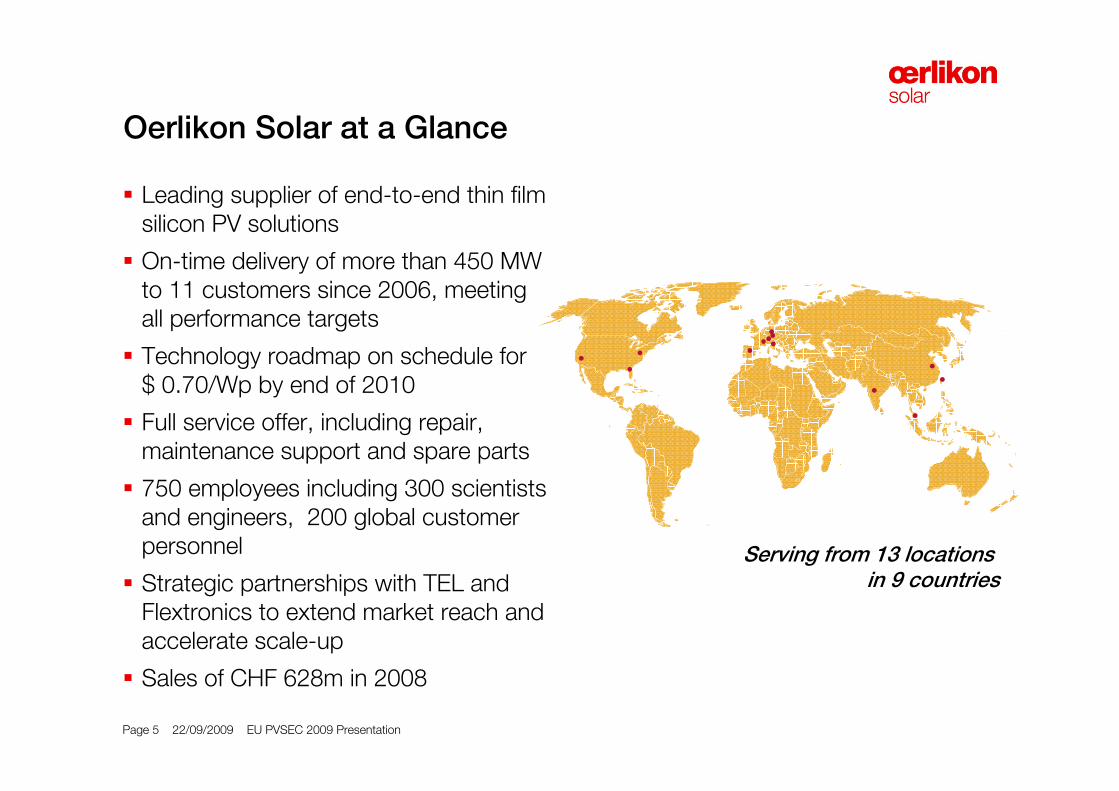

Oerlikon Solar at a Glance

Leading supplier of end-to-end thin film silicon PV solutions

On-time delivery of more than 450 MW to 11 customers since 2006, meeting all performance targets

Technology roadmap on schedule for $ 0.70/Wp by end of 2010

Full service offer, including repair, maintenance support and spare parts

750 employees including 300 scientists and engineers, 200 global customer personnel

Strategic partnerships with TEL and Flextronics to extend market reach and accelerate scale-up

Sales of CHF 628m in 2008

Serving from 13 locations in 9 countries

Page 6 22/09/2009 EU PVSEC 2009 Presentation

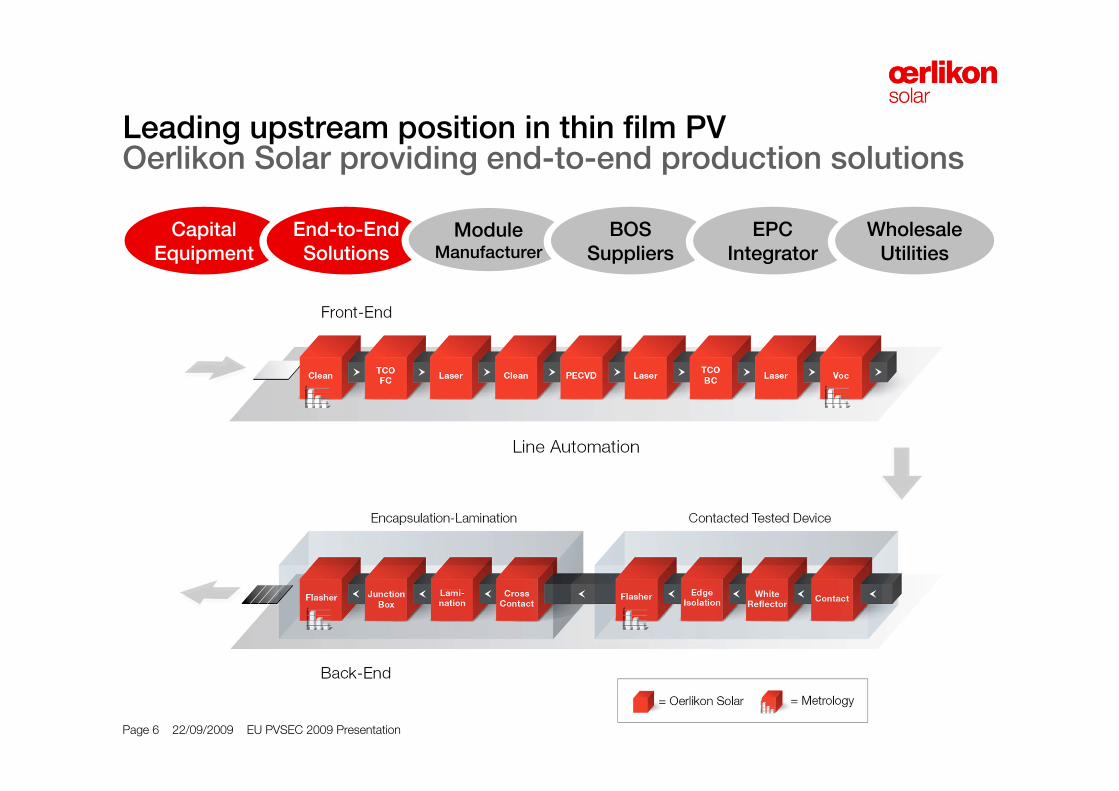

Leading upstream position in thin film PVOerlikon Solar providing end-to-end production solutions

Capital Equipment

Capital Equipment

Capital EquipmentEnd-to-EndSolutions

Capital Equipment

Module Manufacturer

Capital Equipment

BOS Suppliers

Capital Equipment

EPC Integrator

Capital Equipment

Wholesale Utilities

Page 7 22/09/2009 EU PVSEC 2009 Presentation

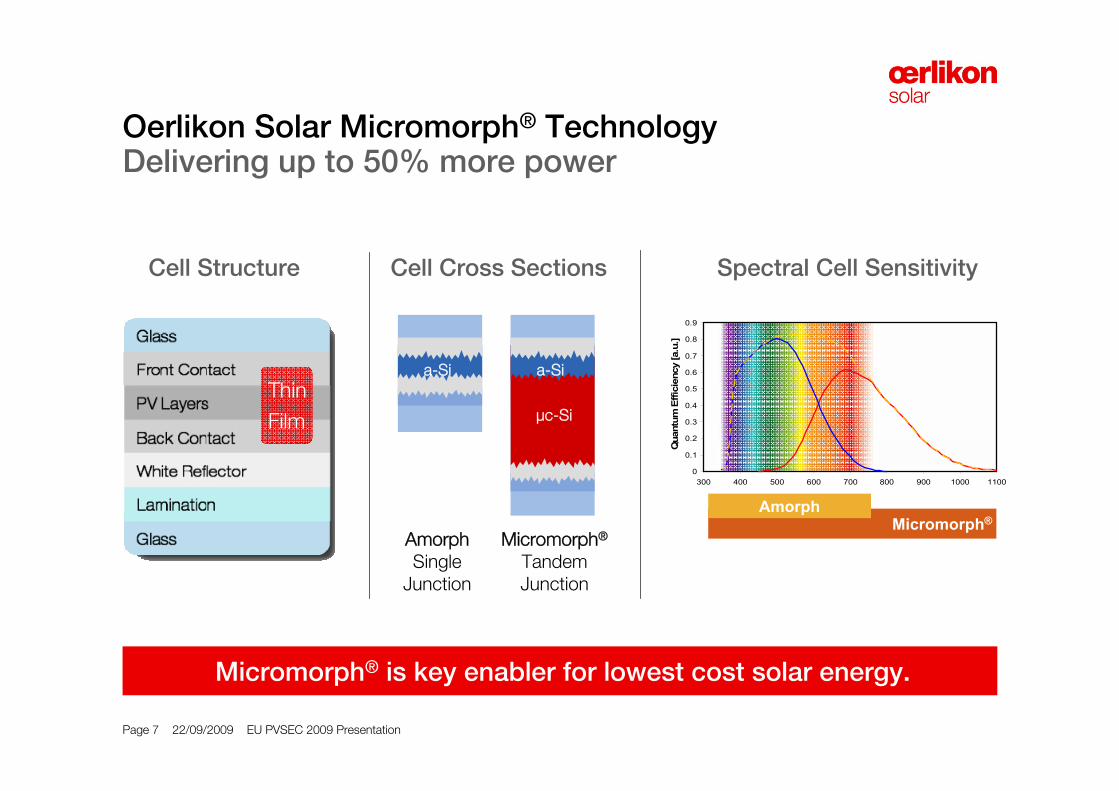

Oerlikon Solar Micromorph® TechnologyDelivering up to 50% more power

Cell Structure

Thin

Film

Cell Cross Sections

a-Si

AmorphSingle

Junction

a-Si

μc-Si

Micromorph®

Tandem Junction

Spectral Cell Sensitivity

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

300 400 500 600 700 800 900 1000 1100

Qua

ntum

Effi

cien

cy [a

.u.]

Micromorph®Amorph

Micromorph® is key enabler for lowest cost solar energy.

Page 8 22/09/2009 EU PVSEC 2009 Presentation

Recent technical highlights

Oerlikon Solar Receives Micromorph®

Master Certificate

TÜV IEC master certification for Amorph and Micromorph®

Announced record cell efficiency with over 10 % stabilized on amorphous silicon

New record Micromorph® module with 151 Watt performance and over 11% efficiency (initial)

VLSI Research Inc announced the ranking of the top 5 turnkey line suppliers to the PV manufacturing industry for 2008

Oerlikon Solar KAI 1200 PECVD system wins the Cell Award 2009

Oerlikon Solar TCO 1200 systems wins the Solar Award 2009

Page 9 22/09/2009 EU PVSEC 2009 Presentation

Start of production reached

- Tianwei a-Si; 46 MW

- Pramac Micromorph; 30 MW

- Auria Solar Micromorph; 60 MW

New order

- NST Micromorph; 120 MW

Repeat order

- HelioSphera Micromorph; 30 MW

U.S. project MOU

- Clairvoyant/Ford Micromorph, 90+ MW

Recent Customer NewsPositive growth even in challenging market conditions

Page 10 22/09/2009 EU PVSEC 2009 Presentation

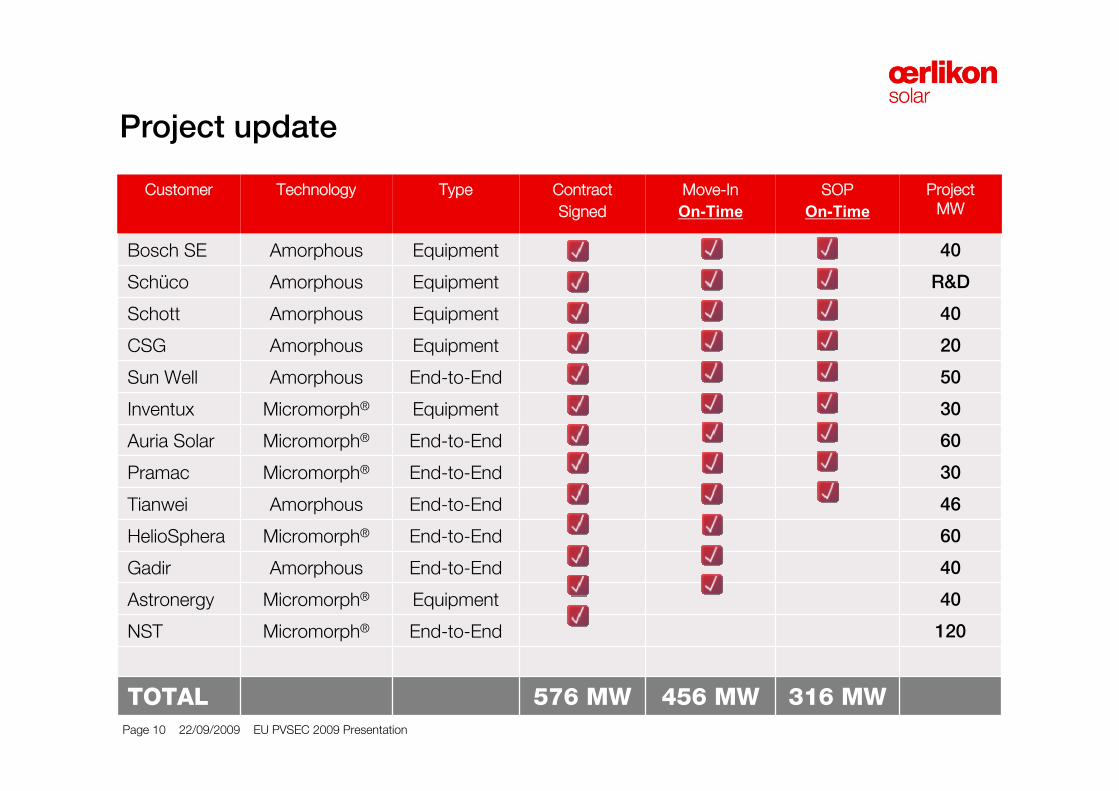

Project update

Customer Technology Type Contract

Signed

Move-In

On-TimeSOP

On-TimeProject

MW

Bosch SE Amorphous Equipment 40

Schüco Amorphous Equipment R&D

Schott Amorphous Equipment 40

CSG Amorphous Equipment 20

Sun Well Amorphous End-to-End 50

Inventux Micromorph® Equipment 30

Auria Solar Micromorph® End-to-End 60

Pramac Micromorph® End-to-End 30

Tianwei Amorphous End-to-End 46

HelioSphera Micromorph® End-to-End 60

Gadir Amorphous End-to-End 40

Astronergy Micromorph® Equipment 40

NST Micromorph® End-to-End 120

TOTAL 576 MW 456 MW 316 MW

Page 11 22/09/2009 EU PVSEC 2009 Presentation

Oerlikon Micromorph is now entering the marketMore than 960,000 panels produced with Oerlikon equipment

Pramac

Florence/ItalyMicromorph®

Bosch

Stockstadt/GermanyAmorphous

Page 12 22/09/2009 EU PVSEC 2009 Presentation

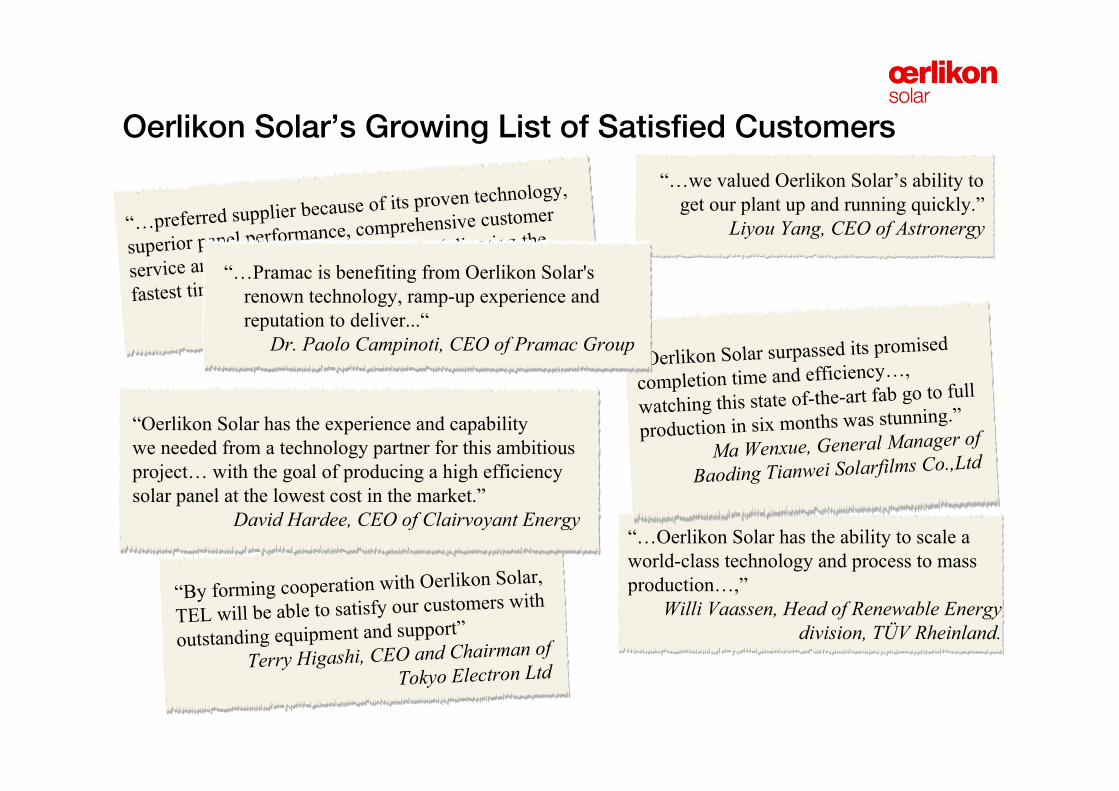

“By forming cooperation with Oerlikon Solar,

TEL will be able to satisfy our customers with

outstanding equipment and support”

Terry Higashi, CEO and Chairman of Tokyo Electron Ltd

“…Oerlikon Solar has the ability to scale a world-class technology and process to mass production…,”

Willi Vaassen, Head of Renewable Energy division, TÜV Rheinland.

“Oerlikon Solar surpassed its promised

completion time and efficiency…,

watching this state of-the-art fab go to full

production in six months was stunning.”

Ma Wenxue, General Manager of

Baoding Tianwei Solarfilms Co.,Ltd

“…we valued Oerlikon Solar’s ability to get our plant up and running quickly.”

Liyou Yang, CEO of Astronergy“…preferred supplier because of its proven technology,

superior panel performance, comprehensive customer

service and unmatched track record in delivering the

fastest time-to-market….”Dr. Chi-Yao Tsai, CEO of Auria Solar“…Pramac is benefiting from Oerlikon Solar's

renown technology, ramp-up experience and reputation to deliver...“

Dr. Paolo Campinoti, CEO of Pramac Group

“Oerlikon Solar has the experience and capability we needed from a technology partner for this ambitious project… with the goal of producing a high efficiency solar panel at the lowest cost in the market.”

David Hardee, CEO of Clairvoyant Energy

Oerlikon Solar’s Growing List of Satisfied Customers

Solar Market and Thin Film Competitiveness

Page 14 22/09/2009 EU PVSEC 2009 Presentation

Drivers for new energy sourcesFundamentals don’t change

Energy Demand

Rising Costs

Diminishing Fossil Fuel Resources

Environmental Concerns and Regulations

National Security

Page 15 22/09/2009 EU PVSEC 2009 PresentationPage 15 22/09/2009 EU PVSEC 2009 Presentation

Vast addressable market for low-cost solar PVElectricity world market size

Source: EIA

Oil

Nuclear

2%

4000 GW

16%

Gas

15%

6%

20%

41%

Renewables

Hydro

Coal

2006

1%

29%Wind

2006

15%Solar

Waste

80 GW

Geothermal

Biomass

Others

13%

39%

3%

Solar power still holds less than 0.02% share of total world electricity production worldwide and bears strong growth potential

Page 16 22/09/2009 EU PVSEC 2009 Presentation

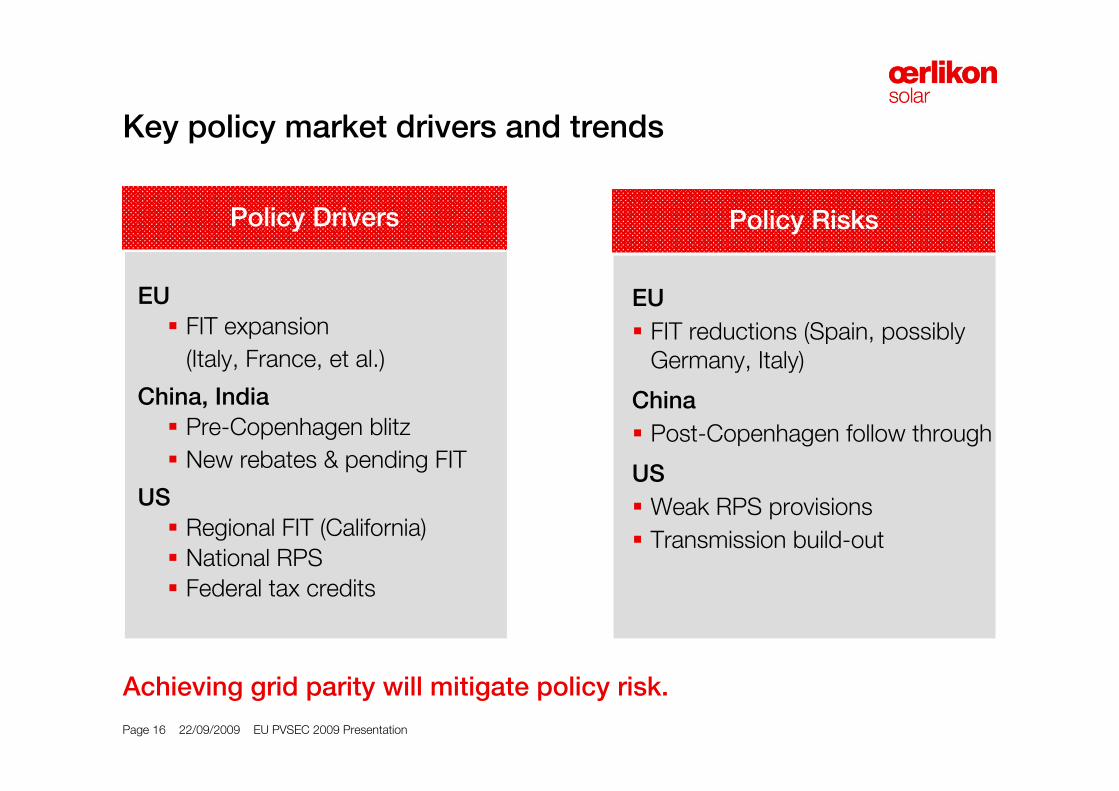

Key policy market drivers and trends

EU

FIT expansion

(Italy, France, et al.)

China, India

Pre-Copenhagen blitz

New rebates & pending FIT

US

Regional FIT (California)

National RPS

Federal tax credits

EU

FIT reductions (Spain, possibly Germany, Italy)

China

Post-Copenhagen follow through

US

Weak RPS provisions

Transmission build-out

Achieving grid parity will mitigate policy risk.

Policy Drivers Policy Risks

Page 17 22/09/2009 EU PVSEC 2009 Presentation

Annual PV module shipments

Source: Oerlikon Solar

0

5

10

15

20

2008 2009 2010 2011 2012 2013

C-Si Thin Film

GWp

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013OC base case, 09/2009 OC upside case, 09/2009NEF upside, 06/2009 McKinsey uside, 06/2009Navigant accel, 07/2009 Yole, 07/2009iSuppli, 09/2009 Gartner, 08/2009UBS, 06/2009 Merril Lynch, 07/2009

PV Market forecastThin Film share will increase in the next 5 years

Growing share for TF

(annual module shipments)GWp

Source: Oerlikon Solar (upside case)

Growth will return in 2010.

CAGR 2009-13

Thin-Film 53%

c-Si 29%

Total Market 36%

Page 18 22/09/2009 EU PVSEC 2009 Presentation

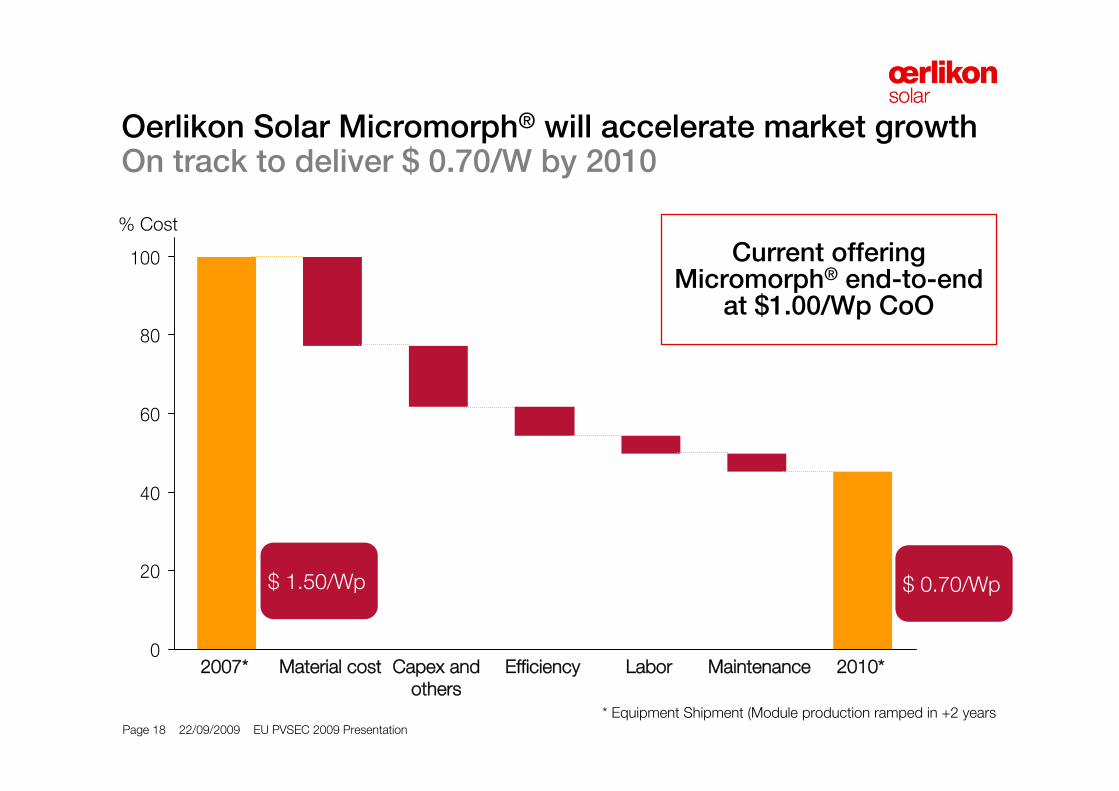

0

20

40

60

80

100

Maintenance2007* Material cost Capex and others

Efficiency Labor 2010*

% Cost

$ 1.50/Wp $ 0.70/Wp

Oerlikon Solar Micromorph® will accelerate market growthOn track to deliver $ 0.70/W by 2010

* Equipment Shipment (Module production ramped in +2 years

Current offeringMicromorph® end-to-end

at $1.00/Wp CoO

Page 19 22/09/2009 EU PVSEC 2009 Presentation

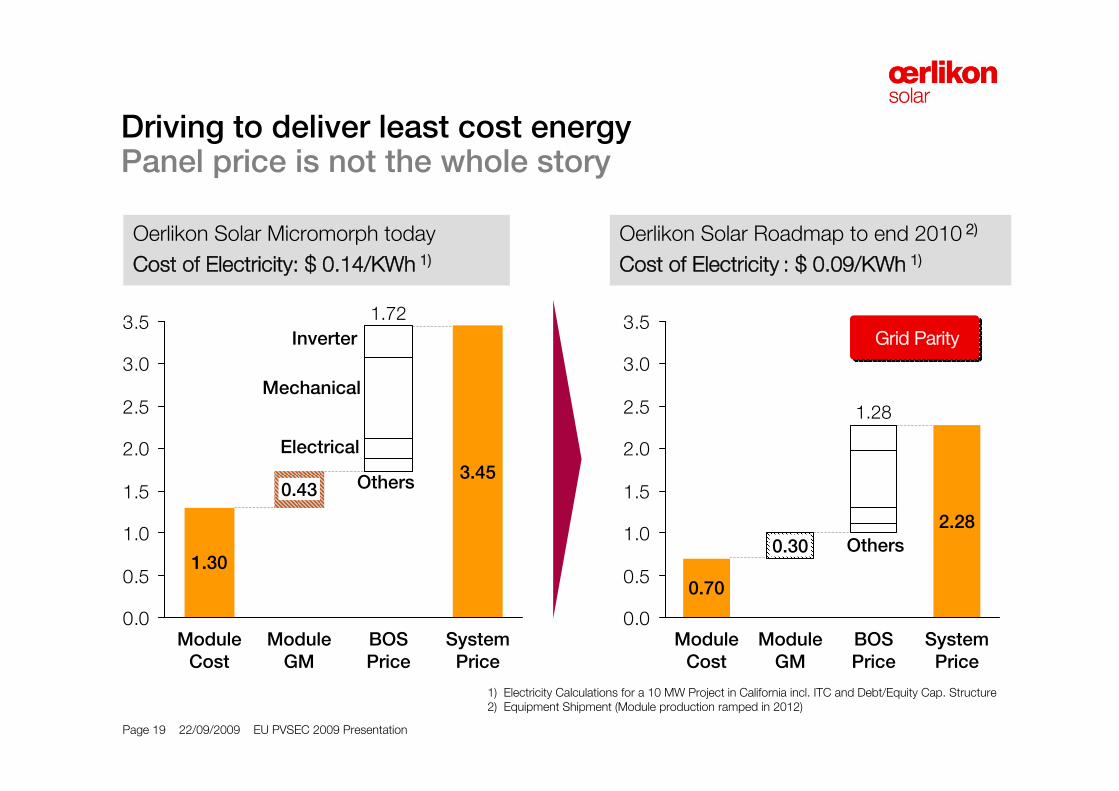

1.30

Grid ParityGrid Parity

Driving to deliver least cost energyPanel price is not the whole story

Oerlikon Solar Micromorph today

Cost of Electricity: $ 0.14/KWh 1)

1) Electricity Calculations for a 10 MW Project in California incl. ITC and Debt/Equity Cap. Structure2) Equipment Shipment (Module production ramped in 2012)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Module GM

0.43

Module Cost

1.30

System Price

3.45

BOS Price

1.72

Mechanical

Inverter

Others

Electrical

1.30

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Module GM

0.30

BOS Price

1.28

0.70

Module Cost

System Price

2.28

Others

Oerlikon Solar Roadmap to end 2010 2)

Cost of Electricity : $ 0.09/KWh 1)

Page 20 22/09/2009 EU PVSEC 2009 PresentationPage 20 22/09/2009 EU PVSEC 2009 PresentationPage 20 22/09/2009 EU PVSEC 2009 PresentationPage 20 22/09/2009 EU PVSEC 2009 Presentation

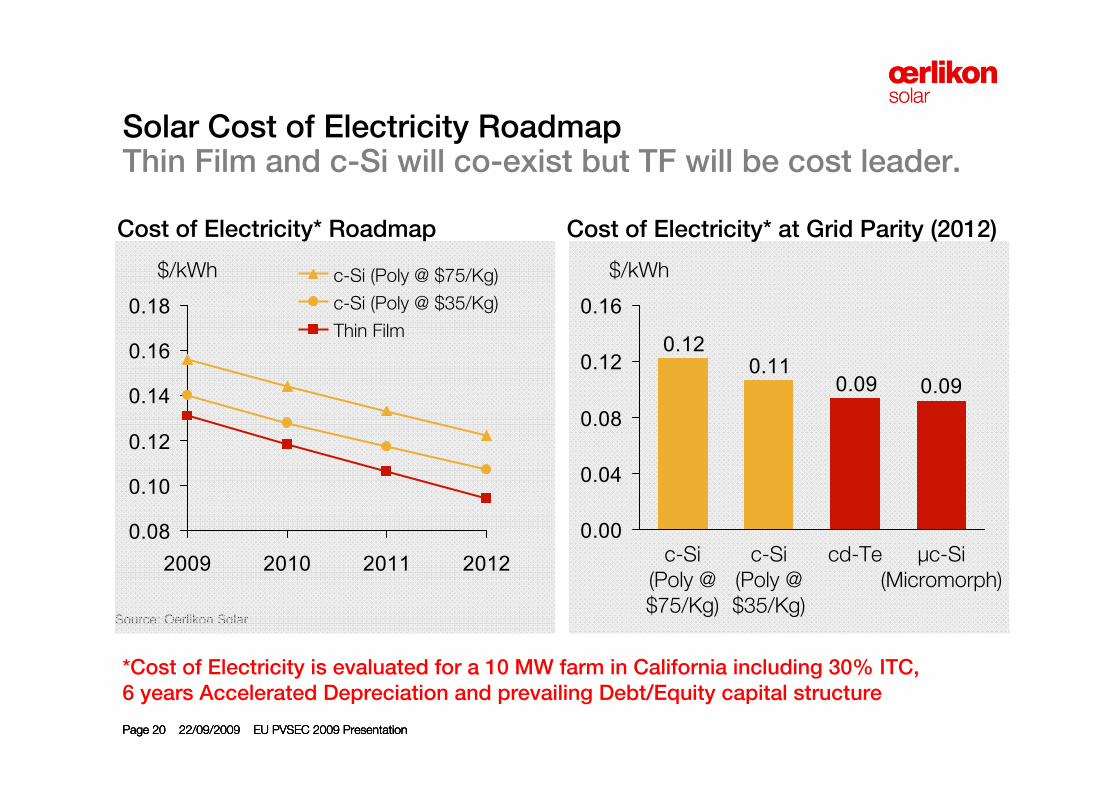

Solar Cost of Electricity RoadmapThin Film and c-Si will co-exist but TF will be cost leader.

Cost of Electricity* Roadmap Cost of Electricity* at Grid Parity (2012)

Source: Oerlikon Solar

0.090.090.11

0.12

0.00

0.04

0.08

0.12

0.16

$/kWh

μc-Si (Micromorph)

cd-Tec-Si (Poly @ $35/Kg)

c-Si (Poly @ $75/Kg)

0.08

0.10

0.12

0.14

0.16

0.18

2009 2010 2011 2012

$/kWh

Thin Film

c-Si (Poly @ $35/Kg)

c-Si (Poly @ $75/Kg)

*Cost of Electricity is evaluated for a 10 MW farm in California including 30% ITC, 6 years Accelerated Depreciation and prevailing Debt/Equity capital structure

Page 21 22/09/2009 EU PVSEC 2009 Presentation

Thin film provides long term competitive advantagesOerlikon Micromorph® technology is smart choice

Lower manufacturing cost than c-Si

Overall lowest cost of electricity

Better performance at higher operating temperatures

Better performance in diffused light

Higher margins in manufacturing

Higher rates of return on investment for solar projects

Page 22 22/09/2009 EU PVSEC 2009 PresentationPage 22 22/09/2009 EU PVSEC 2009 Presentation

Thin film silicon equipment market investing today for 2012 Oerlikon Solar has the largest base, and growing

Source: Oerlikon Solar

0

5

10

15

2008 2009 2010 2011 2012 2013

GW

Base Scenario

Upside Scenario

Thin Film Silicon Installed Base (Equipment)

Major Growth Drivers

Proven mass production solutions

Improved efficiencies

Grid Parity cost roadmap

Recovery of project finance markets

Transition from capacity basedpricing ($/W) to energy based pricing ($/kWh)

Attractive geopolitical initiatives and incentive policies

Page 23 22/09/2009 EU PVSEC 2009 Presentation

On track to achieve grid parity by 2010.

Thin-film is the fastest growing segment within PV market. Total PV end market demand will be $45 billion by 2012

SummarySolutions for a solar powered world

Oerlikon Solar on track to offer grid parity solutions by the end of 2010

Proven manufacturing solutions

More than 960,000 panels already produced

Thank you for your attention.

Page 25 22/09/2009 EU PVSEC 2009 Presentation

Appendix

Page 26 22/09/2009 EU PVSEC 2009 Presentation

Cooperation with Schott Solar on thin film silicon development 40 MWp equipment contract with

Schott Solar

Start of first micromorph®

production at Inventux

Champion cell with ~ 13% efficiency for micromorph®

First micromorph® end-to-end production line contract

SunWell ramps and celebrates SOP for first Asian end-to-end line

VHF PECVD deposition technology Oerlikon

displays first functional 1.4 m2 a-Simodule

Light trapping by TCO & intermediate reflector

PV lab at IMT by Prof Arvind Shah

Inventux achieves record efficiency with micromorph®

120W (>9% efficiency)

Recorded full size module performance of 151W (>11% efficiency)

Tianwei SOP for 46 MW

NST contracts for end-to-end solutions for 120 MW

Micromorph® solar cell (tandem amorphous, microcrystalline)

First R&D equipment delivered to Schott Solar

15 years of R&D experience and industrial mass production since 2005

Oerlikon founds own R&D lab and enters thin film silicon PV

Oerlikon presents first micromorph®

tandem module ~125W

First 40MWp front end line contract with Ersol

1986 1989 1995 2003 2004 2005 2007 2008 2009

Opportunity identification

Concept and product

Commercialization Globalization

Page 27 22/09/2009 EU PVSEC 2009 Presentation

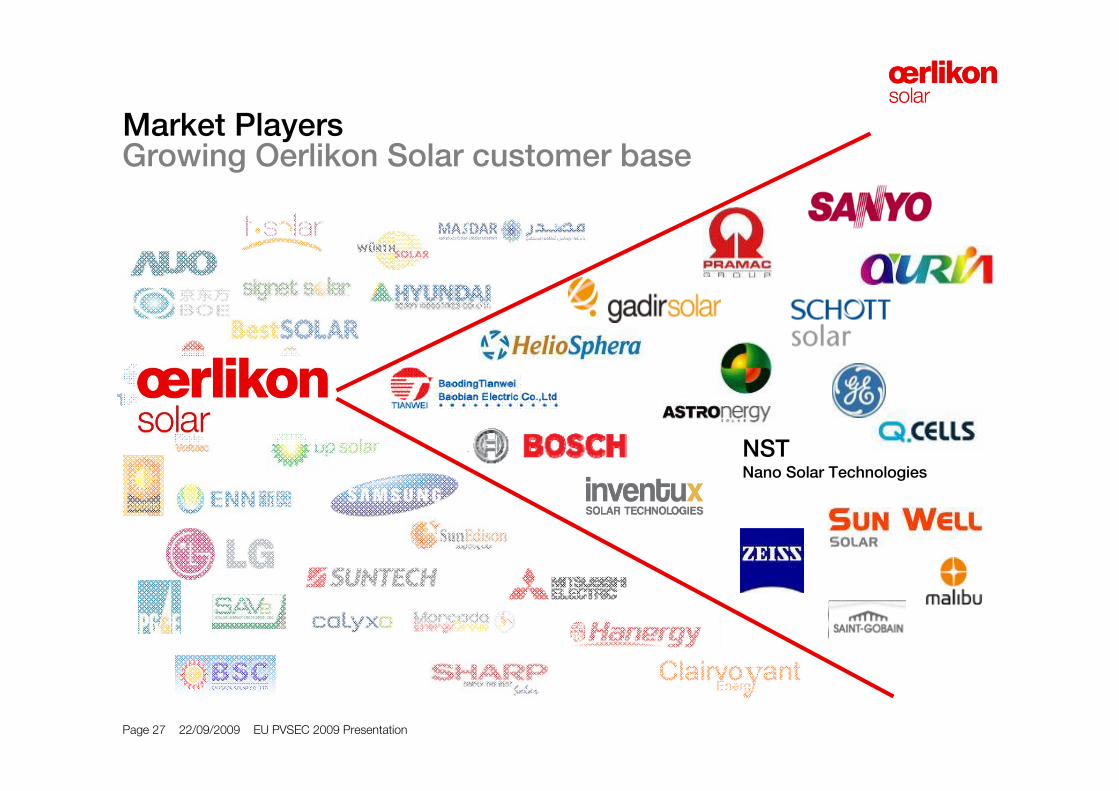

Market Players

NSTNano Solar Technologies

Growing Oerlikon Solar customer base

Page 28 22/09/2009 EU PVSEC 2009 Presentation

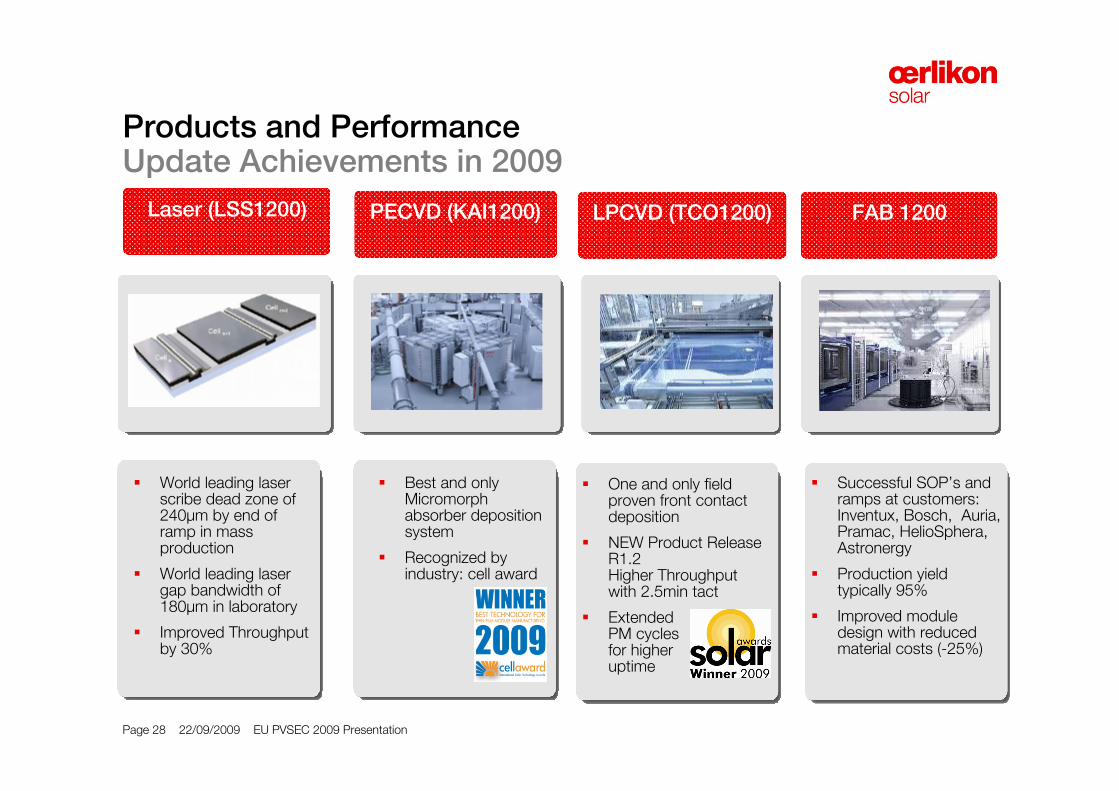

Products and Performance Update Achievements in 2009

Laser (LSS1200)

Best and only Micromorph absorber deposition system

Recognized by industry: cell award

PECVD (KAI1200)

One and only field proven front contact deposition

NEW Product Release R1.2Higher Throughputwith 2.5min tact

Extended PM cycles for higher uptime

LPCVD (TCO1200) FAB 1200

World leading laser scribe dead zone of 240μm by end of ramp in mass production

World leading laser gap bandwidth of 180μm in laboratory

Improved Throughput by 30%

Successful SOP’s and ramps at customers: Inventux, Bosch, Auria, Pramac, HelioSphera, Astronergy

Production yield typically 95%

Improved module design with reduced material costs (-25%)

Page 29 22/09/2009 EU PVSEC 2009 Presentation

Module cost of ownership calculation

Material CostGas, glass, lamination, foil, consumables, etc.

Investment CostEquipment, line automation, back-end, etc.

Labor CostOperators, technicians, management, etc.

ThroughputGlasses per hour

Yield% sellable modules

Uptime% of production availability

Power EfficiencyModule driven by conversion

+

+

x

xMoney

Material Cost

Investment Cost Labor Cost

ThroughputYield UptimePowerWp

Calculation

1

x

=