©tns 2013 3.14 x axis 6.65 base margin 5.95 top margin 4.52 chart top 11.90 left margin 11.90 right...

TRANSCRIPT

©TNS 2013

TNS

(Hidden) fees for card payments:

Would transparency change consumer behaviour?

Elke HimmelsbachNico A. Siegel

30 September 2013 – Applying Behavioural Insights to Policy-Making – EC Conference, Brussels

©TNS 2013

TNS

2

Contents

1 Rationale

2 Methodology

3 Findings

4 Policy Implications

©TNS 2013

TNS

3

The issue: Hidden payment charges

©TNS 2013

TNS

4

The issue: Hidden payment charges

©TNS 2013

TNS

5

Policy Objectives of the European Commission

More transparency

of payment charges

Changing behaviour of consumers

More price competition

Lower charges for consumers

©TNS 2013

TNS

6

Research Objectives

Explore consumers´ decision process:

A. Identify the main individual biases and external barriers

B. Identify the most effective policy options

… that prevent/drive cost-conscious payment choices from a

consumer perspective

©TNS 2013

TNS

Mapping the Payers´ Decision Process

ACCESS ASSESSING & ANALYSING ACTING (or not)

Awareness Intention Behaviour Beliefs & Attitudes

7

Cultural norms & national legislation

Individual resources available Overconfidence bias Indiv. habits/status quo bias Context/Choice architecture

Low relevance of cost savings High preferences for

convenience, security Information overload Loss aversion bias

Push/Provision:No (easy) access

Pull/Attention: Low issue salience

BEHAVIORAL THEORY: Potential biases and barriers

©TNS 2013

TNS

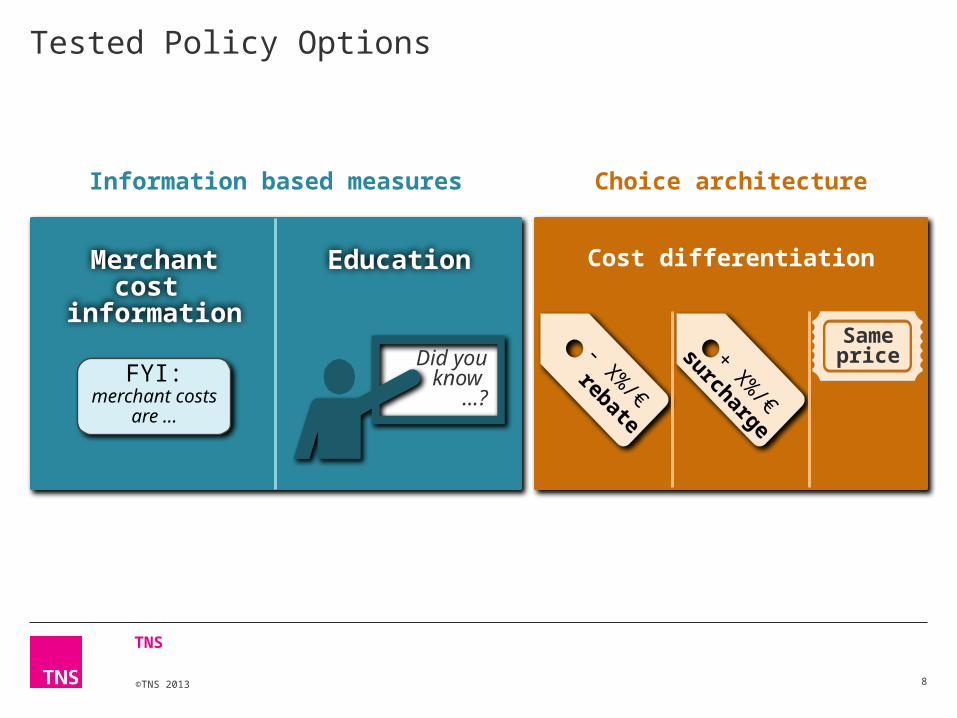

Choice architectureInformation based measures

Tested Policy Options

8

Education

Did you know

…?

Same price- X%

/€

rebate

+ X%

/€

surcharge

Merchant cost

information

FYI: merchant

costs are …

Cost differentiation

©TNS 2013

TNS

Methodology

9

©TNS 2013

TNS

10

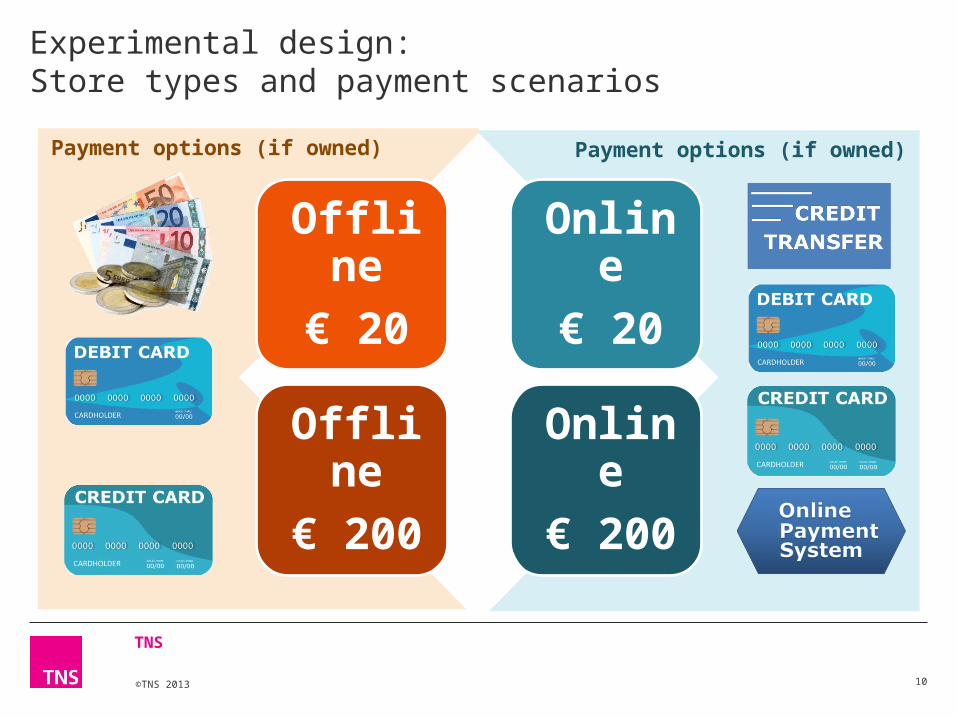

Experimental design:Store types and payment scenarios

Offline

€ 20

Online

€ 20

Offline

€ 200

Online

€ 200

Payment options (if owned)Payment options (if owned)

©TNS 2013

TNS

11

30 Treatment splits + 1 control group Covering all relevant stimuli combinations

Education Merchant cost

information

Payment costs

not included

Payment costs

included

Yes or no Yes or no Surcharge Rebate No rebate

The overall sample of 10 041 respondents across 10 EU countries allowed for robust sample base per split (n=324).

Did you know

…?

Same price

- X%/€

rebate

+ X%

/€

surcharge

FYI: merchant

costs are …

Timings of information given:

Before first entrance

At entrance and at the till

Only at the till

At the till and on the receipt

©TNS 2013

TNS

12

Example/Extract of experimental design

© TNS Infratest 2013

This store will accept several payment methods:

All the prices displayed include VAT and payment charges.

If you pay cash, a 2% rebate will be applied to your bill. If you pay by debit card, a 1% rebate will be applied.

©TNS 2013

TNS

13

Example/Extract of experimental design

That will be 200 €.How would you like to pay?

>>

Payment conditions: 2% rebate 1% rebate no rebateTotal amount to be paid: 196.00 € 198.00 € 200.00 €

I would walk to nearest ATM and

then pay with cash.

I am collecting reward points.

© TNS Infratest 2013

©TNS 2013

TNS

14

Example/Extract of experimental design

© TNS Infratest 2013

Here is your receipt.

>>

Thank you for your purchase!

Total incl. VAT (in €): 200.00Payment charge:Rebate for Debit Card - 2.00Final total incl. VAT (in €): 198.00

©TNS 2013

TNS

3Findings

15

©TNS 2013

TNS

Which policy options were most effective in driving cost-conscious consumer choices?

0.074 0.143

0.632

1.255

0.012 0.206

1.203

1.739

Education

Did you know

…?

Extract of results based on logistic regression analysis to identify statistically significant drivers of cost-conscious choices. Values display strength of regression coefficients. Base: EU10 (without missing variables) – offline scenario (n = 8018) – online scenario (n = 7490)

Not significant

--

On-line

Off-line

Strongly significant *** (p < 0.001)

16

Rebates

- X%/€

rebate

Surcharges+ X%

/€

surchargeMerchant cost

information

FYI: merchant

costs are …

©TNS 2013

TNS

17

Which behavioural biases were identified?Loss aversion & Overconfidence

A. STATED PREFERENCES: Should you face surcharges (…), do you intend to - Refuse to shop in this store 25%

B. OBSERVED BEHAVIOUR:Always made cost-efficient choices …- In the offline shopping scenarios 30%

Base: EU10 – all respondents (n = 10 041)

+ X%

/€

surcharge

Overconfidence bias (A-B): 24%-points

- Generally use a cheaper payment method and avoid surcharges 54%

- Generally pay the surcharge 6%- Only avoid the surcharge when spending a higher amount 10%- Don´t know 6%

©TNS 2013

TNS

18

Which behavioural biases were identified?Status quo bias

Extract of results based on logistic regression analysis to identify statistically significant habitual drivers (Q12/13) of cash choices in the offline shopping scenarios. Values display strength of regression coefficients. Base: EU10 (without missing variables) n = 8 018

More frequent cash

payments

B: .274 ***

Habits driving cash choices

Less frequent offline

shopping

B: .190 **

Less frequentcredit card usage

B: .177 ***

High amount of cash in wallet

B: .250 ***

Less frequent

debit card

usage

B: .203 ***

Less frequentmobile

payments

B: .088 **

©TNS 2013

TNS

19

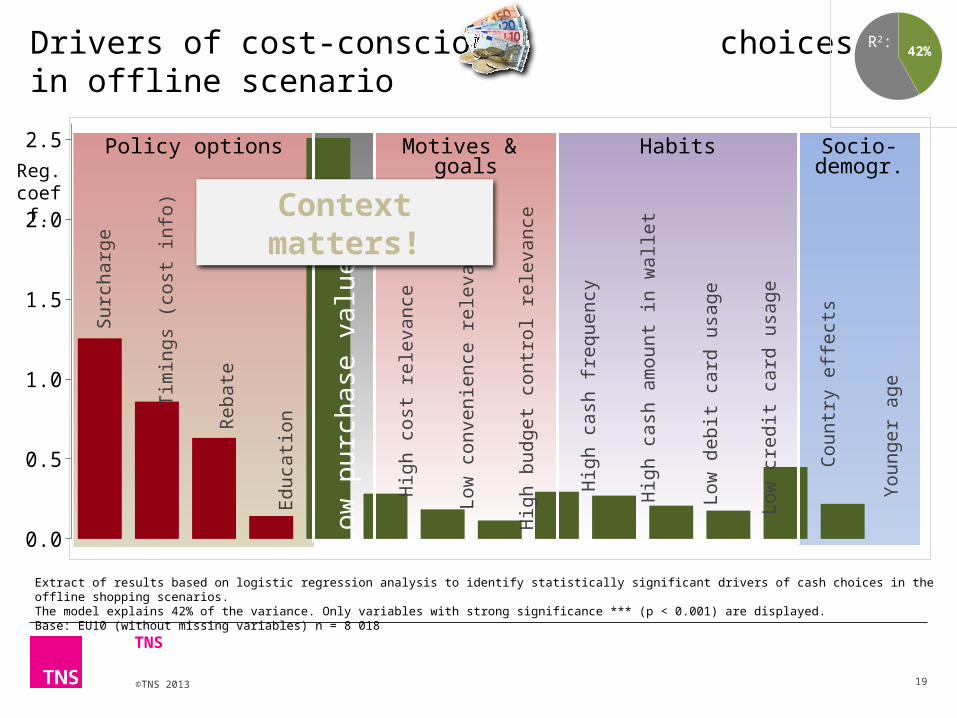

Drivers of cost-conscious choices in offline scenario

42%R2:

0.0

0.5

1.0

1.5

2.0

2.5 Policy options Motives & goals Habits Socio-demogr.

Extract of results based on logistic regression analysis to identify statistically significant drivers of cash choices in the offline shopping scenarios. The model explains 42% of the variance. Only variables with strong significance *** (p < 0.001) are displayed. Base: EU10 (without missing variables) n = 8 018

Low

pu

rch

ase

valu

e

Countr

y e

ffect

s

Young

er

age

Hig

h c

ost

rele

vance

Low

con

ven

ience

rele

vance

Hig

h b

udget

con

trol re

levance

Hig

h c

ash

fre

quency

Low

debit

card

usa

ge

Low

cre

dit

card

usa

ge

Hig

h c

ash

am

ou

nt

in w

alle

t

Su

rcharg

e

Rebate

Tim

ings

(cost

info

)

Ed

uca

tion

Context matters!Reg. coeff.

©TNS 2013

TNS

4Policy Implications

20

©TNS 2013

TNS

21

Summary of Policy Implications IInformation based measures

Did you know

…? Payment choice is highly habitualised with low consumer attention.

Simple notifications do not change consumer behaviour.

Education treatment has strong impact within lab testing. Further evidence required whether impact visible in real life.

Consumers change behaviour only if cost differences are made relevant to them directly in form of rebates or surcharges.

FYI: merchant

costs are …

©TNS 2013

TNS

22

Summary of Policy Implications IIDirect regulatory measures

- X%/€

rebate

Rebate

+ X%

/€

surcharge

Surcharge

Does not drive issue salience.

Provides a positive framing and is more accepted.

Is less effective than surcharges in driving cost-conscious choices.

Is most effective in driving cost-conscious choices.

Drives issue salience.

Provides a negative framing and is less accepted.