the potential demise of the inter-bank check collection system presentation to the float roundtable...

TRANSCRIPT

The Potential Demise Of The Inter-Bank Check Collection

System Presentation To The Float

Roundtable

Robert Ballen

Schwartz & Ballen LLP

June 15, 2006

2

Executive Summary

• Traditionally the payer selected the payment instrument and the law required the inter-bank collection and payment of that instrument

• Payers overwhelmingly selected checks as their preferred payment methodology and the law required the check to be collected and settled under check law through the inter-bank collection and settlement system

• In 1995, Fed estimated 50 billion checks written and collected under check law in the United States

3

Executive Summary

• Recent legal changes, championed by NACHA and facilitated by the Federal Reserve, no longer require inter-bank collection and payment of payer’s payment instrument

• Net effect of these legal changes is that it is now the payee, not the payer, that determines the method of inter-bank collection and settlement

• Payee has very different considerations• As of December 2005, Fed estimated inter-bank check

collection and settlement handled 36.7 billion check payments (down 33% from 1995), and electronic payments (44.5 billion) for the first time exceeded checks

4

The Tradition: Check Written, Check Collected

• Historically, checks were the king of the payment system

• Payers preferred to pay by check– Traditional form of payment

– Typically no per check cost to payer

– Information rich

– Universal acceptance—no need for payment agreement with payee

– Well established legal framework

5

The Tradition: Check Written, Check Collected

• Let’s look at the statistics• In 1995, Fed estimates 50 billion checks written• As late as 2001 (just before the start of the check

conversion initiatives I will discuss today), Fed estimates 42.5 billion checks were written

• General purpose credit cards: 12.3 billion transactions• Private label credit cards: 2.7 billion transactions• Offline debit (signature based): 5.3 billion transactions• Online debit (PIN based): 3.0 billion transactions• ACH: 5.6 billion transactions• EBT: 0.5 billion transactions

6

The Tradition: Check Written, Check Collected

• Law required checks written by payer to be collected and settled through inter-bank check collection and settlement system, subject to check law, the Uniform Commercial Code

• In 1995, 50 billion checks written• In 1995, 50 billion checks collected through the

inter-bank check collection and settlement system, subject to check law

7

The World Begins To Change

• In 1999, NACHA pioneers concept that payer’s check is collected and settled through ACH– NACHA adopts an interim rule, effective September 17, 1999

through September 19, 2000, permitting PPD entries to be used to pilot converting check purchases made in person at point of sale to ACH transactions

– NACHA adopts a short-term rule, effective December 17, 1999 through December 14, 2000, permitting PPD entries to be used to pilot converting consumer checks received through the U.S. mail for the payment of goods or services to ACH transactions.

• Check used as source document to create ACH transaction

8

The Fed Provides Legal Cover

• Fed amends Regulation E, effective March 15, 2001, authorizing use of check as source document to create a one-time EFT, upon notice to consumer. 52 Fed. Reg. 15187 (March 16, 2001)– Rule applies whether the check is blank, partially

completed, or fully completed and signed– Rule applies whether the check is presented at POS or

mailed to merchant or lockbox– Rule applies whether the check is retained by the

consumer, the merchant or the merchant’s bank

9

The Fed Provides Legal Cover

• On December 31, 2005, Fed confirms notice=authorization approach

• Permits payee to provide notice that payee may either convert to EFT or process as a check transaction, providing even more control by payee over the decision how to collect and settle the payment

• Notice by payee to person holding the account imputed to anyone who writes check as payment on that account

• Model notices are provided to reduce payee uncertainty

10

The World Begins To Change

• First non-pilot application of new theory was NACHA point-of-purchase entry (POP)

• Merchant authorized in 2000 to convert customer’s check at point of purchase for an in-person purchase of goods or services– Effective September 15, 2000, new POP standard entry

class code replaced interim 1999 rule that allowed PPD format to be used for point-of-purchase entries

– Payer’s written authorization required

11

The World Begins To Change

• Subsequent changes in POP rules to address impediments to implementation– New return reason codes adopted (improper source

document, source document presented for payment). Effective March 15, 2002

– Enable more ready identification of business checks ineligible for conversion (Aux On-Us Field in MICR line or greater than $25,000). Effective September 15, 2006

• In 2005, 168 million POP transactions

12

Change Continues…

• The next NACHA non-pilot application of this new theory is Account Receivable Entry (ARC)

• Merchant authorized in 2002 to convert payer’s check received via U.S. mail or at dropbox location for payment of goods or services to ACH

• Notice via customer agreement or statement

13

Change Continues

• Subsequent changes in ARC rules to address impediments to implementation– Revise information field requirements to decrease manual processing

(individual name field optional). Effective March 14, 2003– New return reason code for check stop payment. Effective March 14,

2003– Remove requirement to maintain copy of back of check source document

to eliminate need for two pass processing. Effective December 12, 2003– Require payer opt-out; but notice to payers of opt-out right not required.

Effective June 11, 2004– Provide more flexibility on information to be included in Company Name

Field. Effective December 16, 2005– Enable more ready identification of business checks ineligible for

conversion (Aux On-Us Field in MICR line or greater than $25,000). Effective September 15, 2006

• In 2005, 2.15 billion ARC transactions (60% growth from 2004)

14

And Continues…

• Use of POP lags (168 million transactions in 2005) due to inherent limitations of conversion at the point of purchase (slows check out, signed consumer authorization, cashier training challenges)

• To address limitations of POP, NACHA authorizes merchants, effective March 16, 2007, to convert at the back office checks received at point of purchase or manned bill payment location to ACH (BOC)

• Same type of de minimis notice requirements as ARC (post sign and receipt notation)

• Business checks (Aux On-Us Field and $25,000 or greater) not eligible

• Archive digital image of check for at least 60 days

15

And Continues

• We believe that billions of checks will be converted using the back-off process in the not-too-distant future. Elliott McEntee, NACHA President & CEO

• BOC will be more cost-effective to the merchant than converting checks at the register, because they can be scanned in batches. In addition, many consumers ask questions about the POP process when clerks hand them back their checks – extending a process that was designed to make transactions faster. George Thomas, EVP, The Clearing House Payments Co. LLC

• BOC will be very popular because it allows merchants to store their checks and send them to the back office to process in a batch, the same way that banks do. Richard Crone, Founder, Crone Consulting

Source: American Banker, May 10, 2006.

16

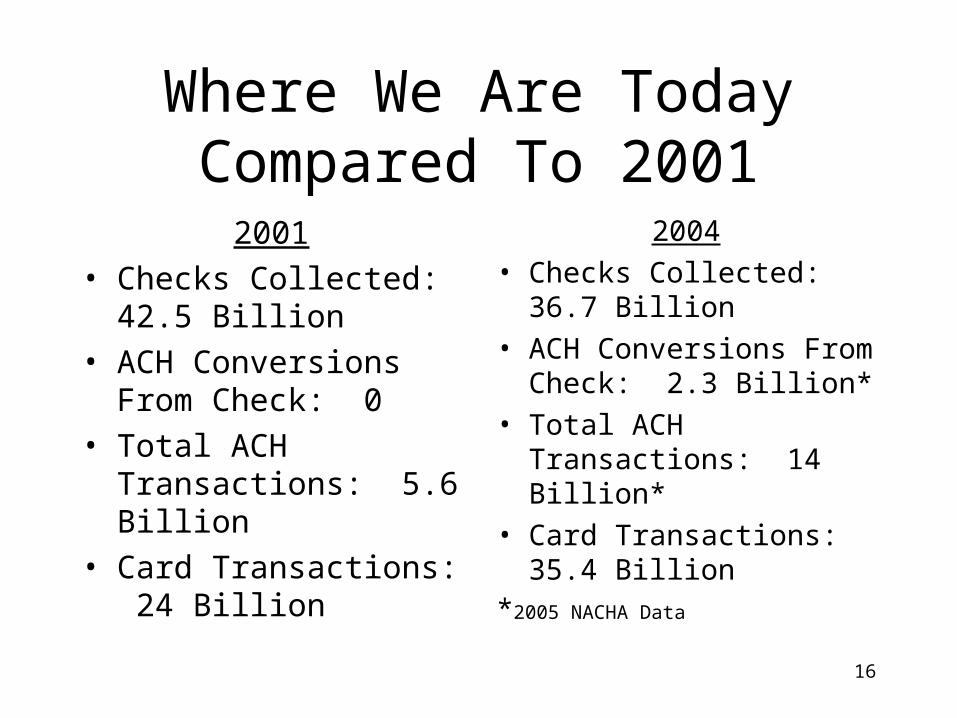

Where We Are Today Compared To 2001

2001

• Checks Collected: 42.5 Billion

• ACH Conversions From Check: 0

• Total ACH Transactions: 5.6 Billion

• Card Transactions: 24 Billion

2004

• Checks Collected: 36.7 Billion

• ACH Conversions From Check: 2.3 Billion*

• Total ACH Transactions: 14 Billion*

• Card Transactions: 35.4 Billion

*2005 NACHA Data

17

Don’t Stop Now

• NACHA working on new application to permit depositary bank to convert deposited check to ACH (Point of Deposit or POD)

• NACHA initiated a one year test pilot on November 1, 2002; pilot extended until October 31, 2005.

• Notice to payer trickier here because depositor may not be payer, but this could potentially be solved by:– NACHA requirement that all banks subject to NACHA rules

provide notice to their depositors that their checks may be converted to ACH when deposited by payee

– NACHA marketing/notice campaign– Bank lobby/ATM signs

18

The New Paradigm

• Tradition: payer writes check, inter-bank check collection and settlement under check law

• New Paradigm: payer writes check, payee (or payee’s bank) determines whether to collect check as check under check law (UCC/EFAA) or ACH under ACH law (NACHA rules/EFTA)

19

The New Paradigm

• Payee considerations:– ***Cost: ACH a clear winner for the payee

• Scanning technology advances permit creation of ACH entry and electronic transmission to payee bank with no manual involvement, except for exceptions items

• Payee bank fees substantially less for ACH origination (big loss for payee banks)

– Availability: Perception that ACH is a winner; reality is probably a toss up

– Return Risk: • ACH posted before check at most paying bank resulting in fewer returns• Perception that payee representment easier and more effective (better

control timing of representment) with ACH • ACH extended 60 day return process more automated than check

warranty/adjustments

20

The New Paradigm

• Depositary Bank considerations:– ***Cost: ACH a clear winner

• Fed costs to collect check from depositary bank over $0.05 per item compared with Fed costs to collect ACH of $0.01 per entry

– Availability: Perception that ACH is a winner; reality is depends on mix of local and non-local checks, mix of paper checks, substitute checks and check images collected

– Return Risk: • ACH posted before check at most paying bank resulting in fewer returns• Paying bank responsibility for unauthorized drawer signature, but see Price v.

Neal overrides (remotely-created checks, clearinghouse rules)• Perception that depositary bank representment easier and cheaper with ACH • ACH extended 60 day return process more automated than check

warranty/adjustments

21

The New Paradigm

• Where are the consumers on all of this?

• Consumer groups are cheering conversion to ACH. EFTA/Regulation E coverage for check transactions is their holy grail

• No hue and cry from consumers– For ARC, consumer opt-out rate is 0.1-0.25%

22

The Future

• Now that the link between the payer’s decision on which payment system to use to pay and the system that is used for the inter-bank collection and settlement of that payment has been broken, payees (and depositary banks for POD) will push to take advantage of the cost savings to them of ACH for as many payments as possible

• NACHA will respond to this payee (and depositary bank for POD) pressure by removing practical impediments to existing conversion applications (as NACHA has done for POP and ARC) and developing new conversion applications (as NACHA has done for BOC and is doing for POD)

23

The Future

• More and more checks will be converted to ACH for inter-bank collection and settlement

• Credit cards, debit cards, prepaid cards, ACH non-check conversion transactions (WEB, TEL) will continue to make inroads

• According to Fed studies, compound annual growth rate from 2001-2003:

• Credit Card +15.4% (19 billion transactions)• Debit Card +23.5% (15.6 billion transactions)

• According to NACHA statistics, annual growth rate from 2004-2005:• WEB +40.69% (1 billion transactions)• TEL +27.40% (0.239 billion transactions)

• According to Fed studies, compound annual growth rate from 2001-2003 for check transactions: -4.3%

24

The Future

• Fewer and fewer checks will be collected and settled through inter-bank check collection system

• Of the 36.7 billion checks estimated by the Fed in the 2005 study, approximately ½ are drawn by consumer payees (19 billion) potentially subject to ACH conversion or non-check replacement

• As more and more of these approximately 19 billion checks are no longer collected through the inter-bank check collection system, the per item cost of the remaining checks collected through the inter-bank check collection system will rise, even with the efficiencies of Check 21/check imaging

25

The Future

• Checks drawn by businesses (estimated by the Fed to be about 1/3 of checks or about 12 billion checks in 2004) will be the last to go from the inter-bank check collection system

• Businesses likely will be the last to give up on the inter-bank check collection system– Float– Legacy systems– Costs of conversion– Risks of electronic debiting to potentially larger dollar business

accounts– No EFTA/Regulation E protections for them

26

The Future

• But as the per item cost differential between inter-bank check collection and ACH collection increases, businesses will more and more throw in the towel

• And you can bet that NACHA will do all it can to encourage businesses to make the switch to ACH collection

• No payee will want to pay for the last check to be collected through the inter-bank check collection system

27

The Federal Reserve Has Seen The Future And…

• The Fed has recognized all of the trends I have discussed today and…

• Since 2003, the Fed has reduced its locations where paper checks are processed from 45 to 29 and will close another 6 locations in 2006.

• The Fed credits the inroads made by electronic payments, including ACH, debit and credit cards, as responsible for these changes. Fed Press Release, May 31, 2006

28

And Your Bank…

• Questions?

• Comments?

• Will I be invited back to speak before another Float Roundtable?