tap gps pfr

Post on 11-Sep-2014

2.557 views

DESCRIPTION

TRANSCRIPT

1Disclaimer:The information provided herein does not constitute a formal endorsement of any company, its products, or services by the

Department of Defense. Specifically, the appearance of external hyperlinks does not constitute endorsement by the U.S. Department of Defense of the linked web sites, or the

information, products or services contained therein. The U.S. Department of Defense does not exercise any editorial control

over the information you may find at these locations. This information is being provided as informational resource material to assist military personnel and their families and should be used

to assist in identifying or exploring resources and options.

Competencies:Completion of a working/realistic spending plan for transition that will contain current spending, transitional spending, and

future requirements.

2

Agenda

• How to plan and prepare financially• Develop a solid Individual Transition Plan• Familiarity with the tools to help manage your

finances• Awareness of available benefits• How to use your resources before transition

The DoD has developed six core financial readiness areas that will aid in the successful transition from the military. At the conclusion of today’s briefing you will have a better understanding of the following financial readiness competencies.

3

Core PFRP for Transition

Module 1Credit

Reports

4

Why Is It Important To Look At Your Credit Report?

There are several reasons why it is important to review your credit reports on a regular basis. 1. Check for accuracy-55% of all military members have errors on their reports2. Ensure you are not the victim of identity theft-Identity theft is the fastest growing crime in the world.3. To see how lenders and merchants view you as a liability or risk.4. ETC.

5

Analyzing Your Credit Report & Score

513.3

6

Credit Reports

6

A credit report is a record of an individual’s credit history. It contains: Credit Employment Residences Judgments Tax Liens Bankruptcies Inquiries

7

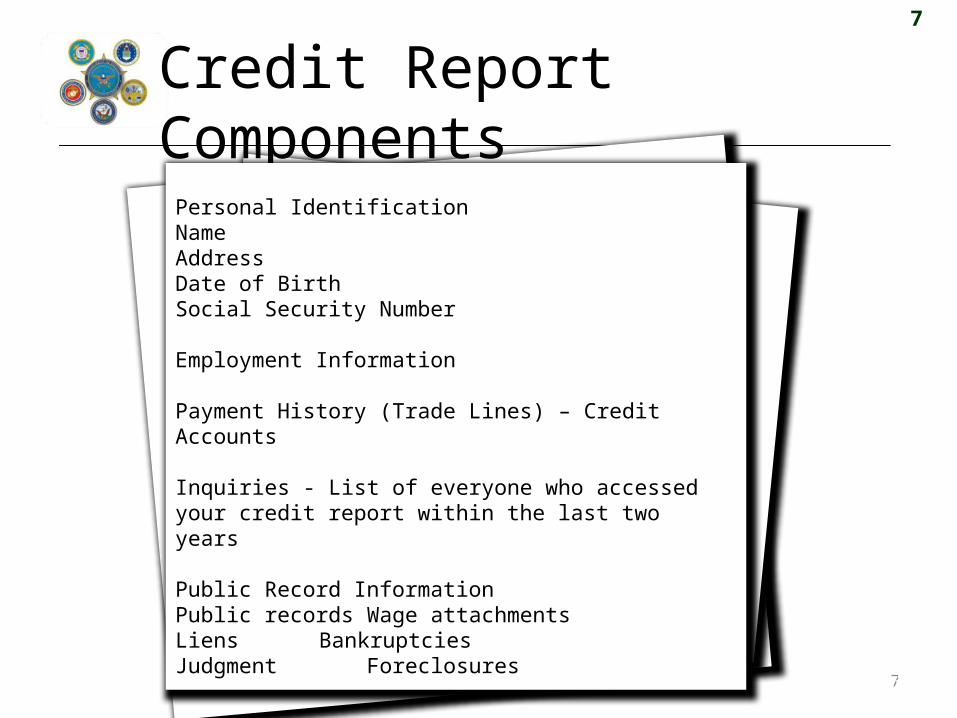

Credit Report Components

7

Personal IdentificationNameAddressDate of BirthSocial Security Number

Employment Information

Payment History (Trade Lines) – Credit Accounts

Inquiries - List of everyone who accessed your credit report within the last two years

Public Record InformationPublic records Wage attachmentsLiens BankruptciesJudgment Foreclosures

13.4

8

Credit Reporting Agencies

8

9

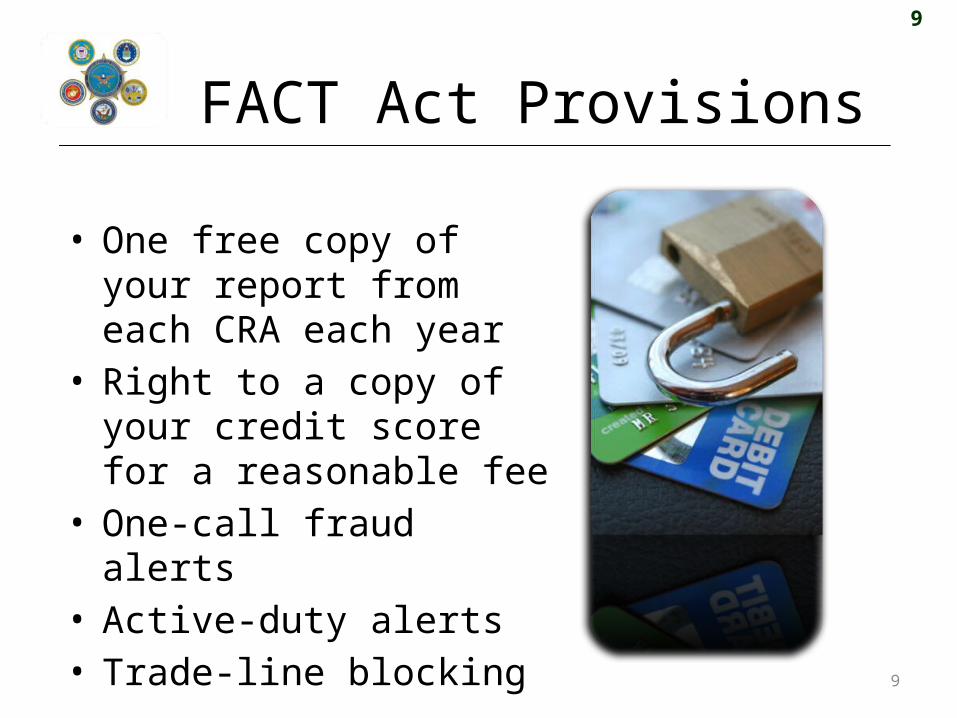

FACT Act Provisions

• One free copy of your report from each CRA each year

• Right to a copy of your credit score for a reasonable fee

• One-call fraud alerts• Active-duty alerts• Trade-line blocking

9

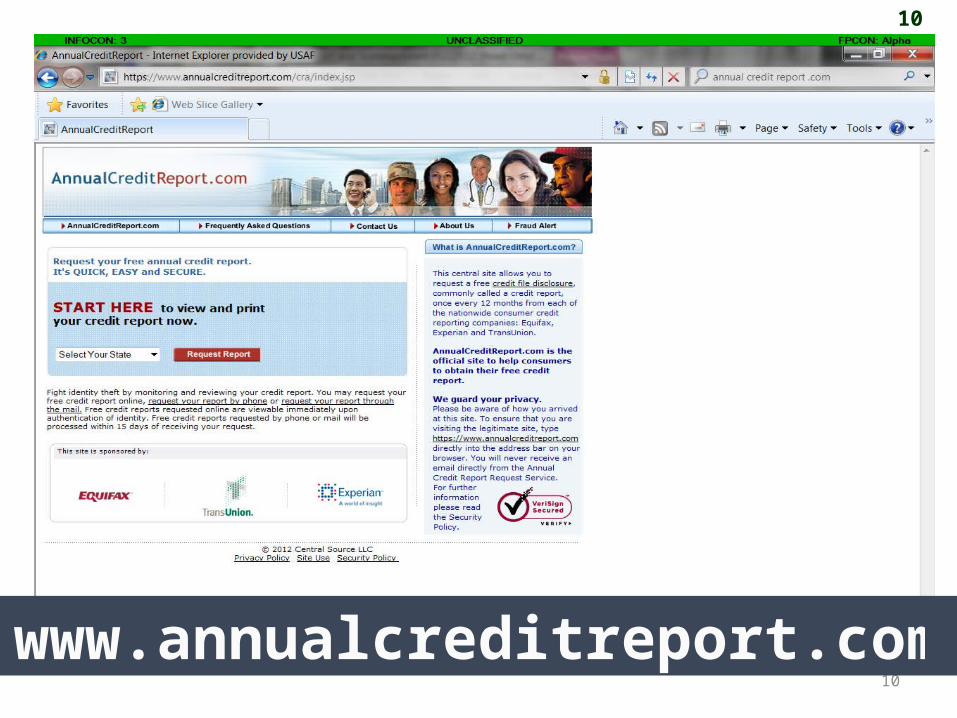

10

10

www.annualcreditreport.com

11

What to Expect

11

• You’ll need to provide and validate:• Name• Address• SSN• Date of birth• Current & previous address (if moved in last 2 years)• Other information listed on your file

• An additional free report can be obtained if:• Denied credit, insurance, employment, rental housing• Adverse action was taken against you based on your

credit file• Unemployed• Receiving public welfare assistance• Your state offers a free or reduced-price credit report• You’ve been a victim of identity theft

12

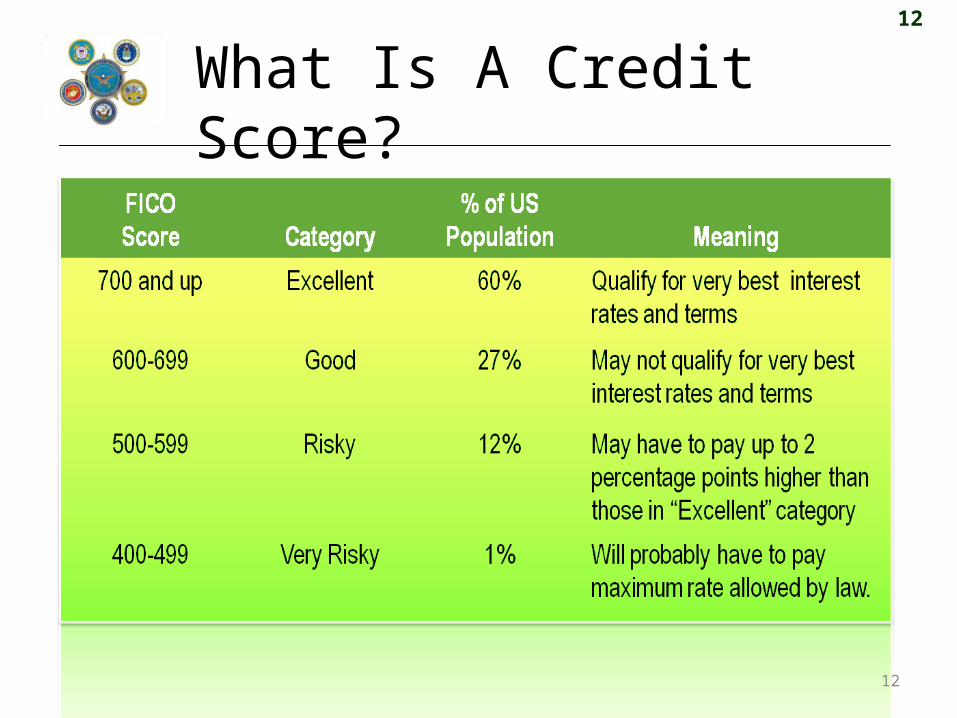

What Is A Credit Score?

12

13

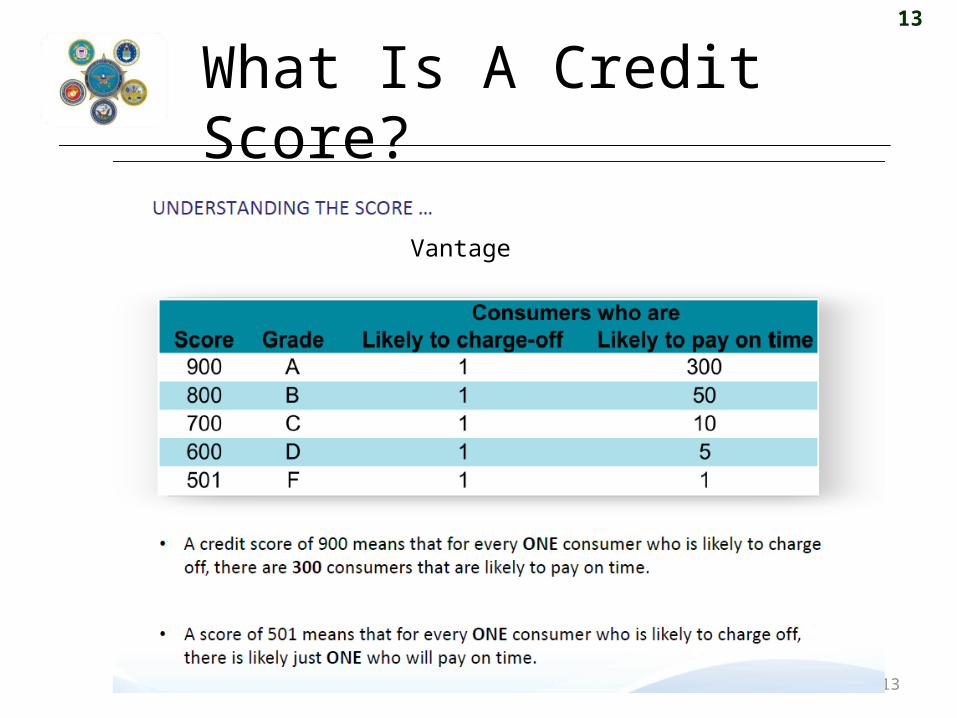

What Is A Credit Score?

13

Vantage

14

The Score Matters

Higher scores =

lower interest rates

& more credit

14

15

Where To Get A Score

1513.5

16

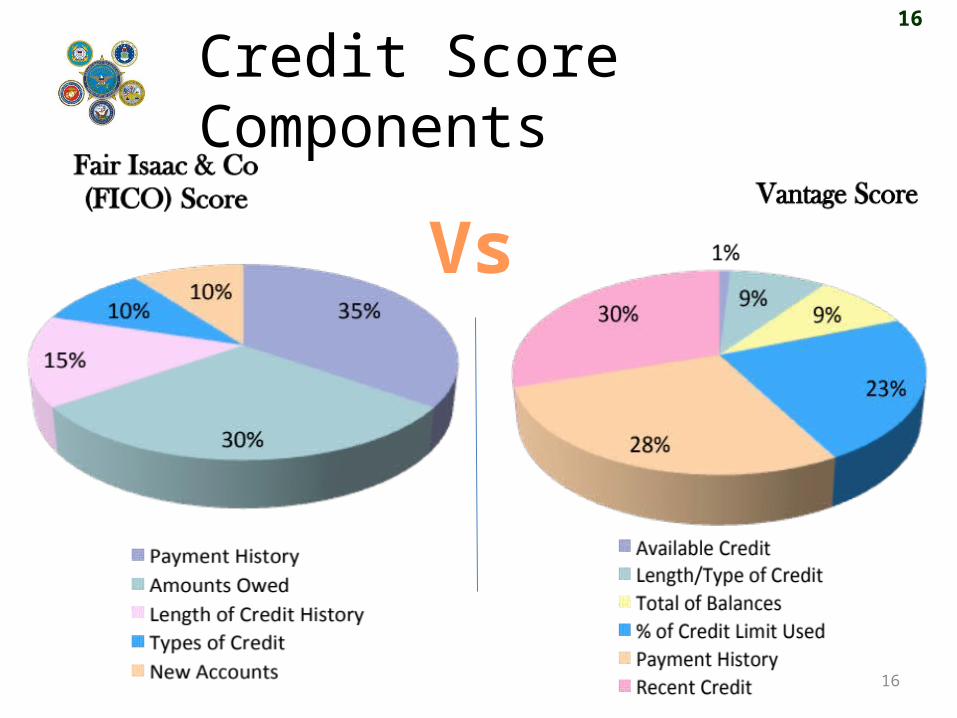

Credit Score Components

16

Vs

17

Improving A Score

17

Ensure credit report is accurate

Make all payments promptly

Stay within credit limits

Take advantage of auto payment plans/options

Set up a bill-payment calendar

Match credit to appropriate purchase

Don’t exceed 10% of the limit on a credit card

Pay down installment loans

Don’t add new accounts to lower balances on older ones

Establish new credit only if you have little existing history

Keep your older accounts in good standing

Limit inquiries

18

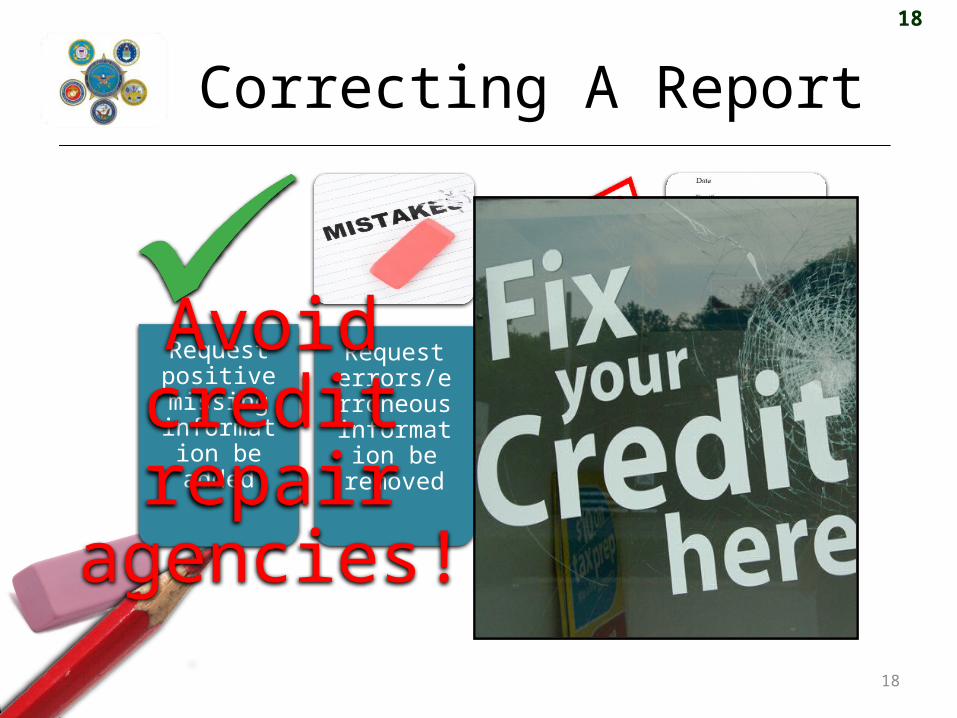

Correcting A Report

18

Request positive missing

information be added

Request errors/errone

ous information be removed

Request outdated

information be removed

Place a consumer

statement on the report

Avoid credit repair

agencies!

19

Fixing A Report

19

20

Fair Credit Report Act• Consumers have the right

to:– know the contents of their

report– an accurate and complete file– have mistakes fixed– tell their side of the story– a fresh start– understand their report– know who has seen their

report– confidentiality– know if their report has been

used against them– sue the CRA

20

21

Who Can See Your Credit Report?

21

CreditorsEmployers

Gov’t Agencies

Insurance Companies

Landlords

22

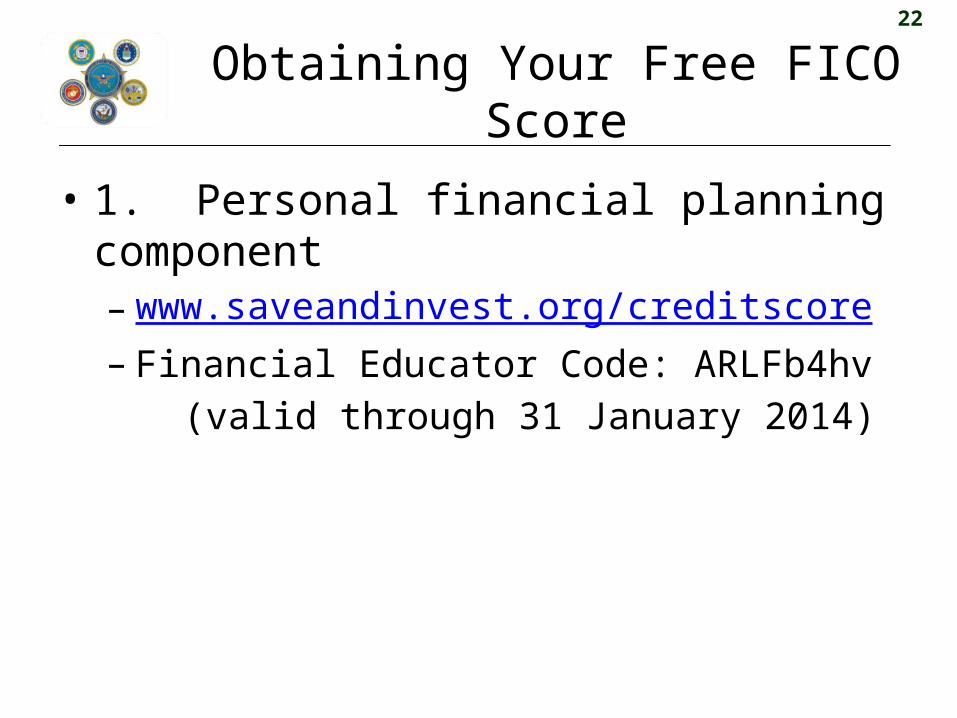

Obtaining Your Free FICO Score

• 1. Personal financial planning component– www.saveandinvest.org/creditscore– Financial Educator Code: ARLFb4hv

(valid through 31 January 2014)

23

What’s Worth Knowing? Wrap-Up

23

24

CORE PFRP FOR TRANSITION

Module 2Cost of Living

Analysis

Core PFRP for Transition

25

Cost of Living Analysis

When relocating, consider what could impact your financial plan

– Salary– Housing– Utilities– Taxes (including tax benefits for veterans)– Food– Child care– Commuting costs, clothing, entertainment,

school costs, climate, health insurance

26

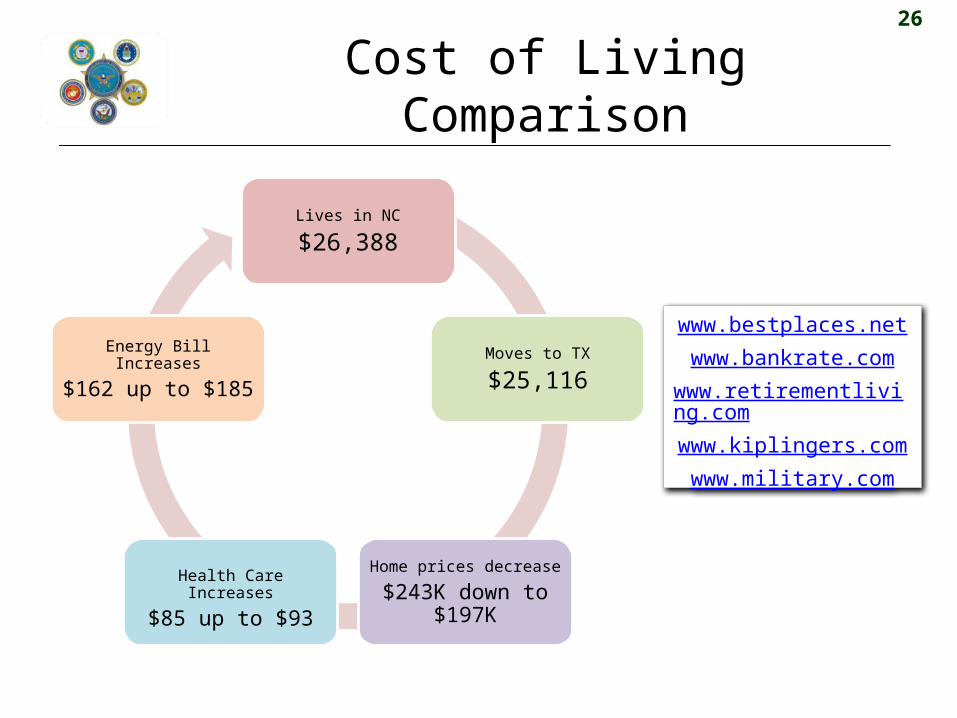

Cost of Living Comparison

www.bestplaces.netwww.bankrate.com

www.retirementliving.comwww.kiplingers.comwww.military.com

Lives in NC

$26,388

Moves to TX

$25,116

Home prices decrease

$243K down to $197KHealth Care Increases

$85 up to $93

Energy Bill Increases

$162 up to $185

27

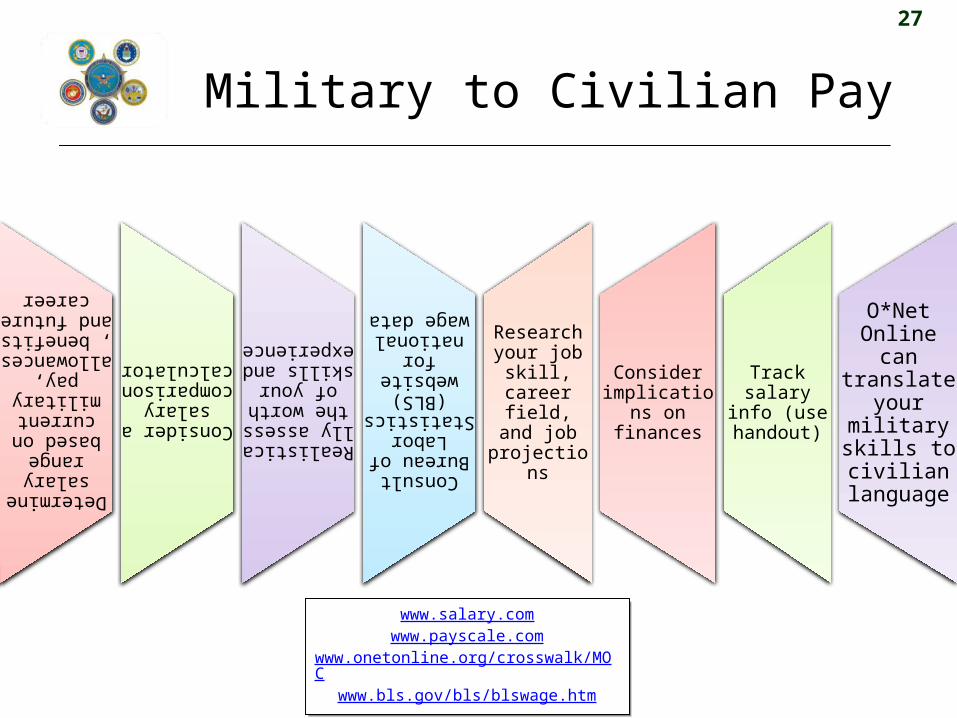

Military to Civilian Pay

Determine salary range based on current military pay, allowances, benefits and future

careerConsider a salary comparison calculator Realistically assess the worth of your skills

and experienceConsult Bureau of Labor Statistics (BLS)

website for national wage data

Research your job skill, career field, and job projectionsConsider implications on financesTrack salary info (use handout)O*Net Online can translate your

military skills to civilian language

www.salary.comwww.payscale.com

www.onetonline.org/crosswalk/MOCwww.bls.gov/bls/blswage.htm

www.salary.comwww.payscale.com

www.onetonline.org/crosswalk/MOCwww.bls.gov/bls/blswage.htm

28

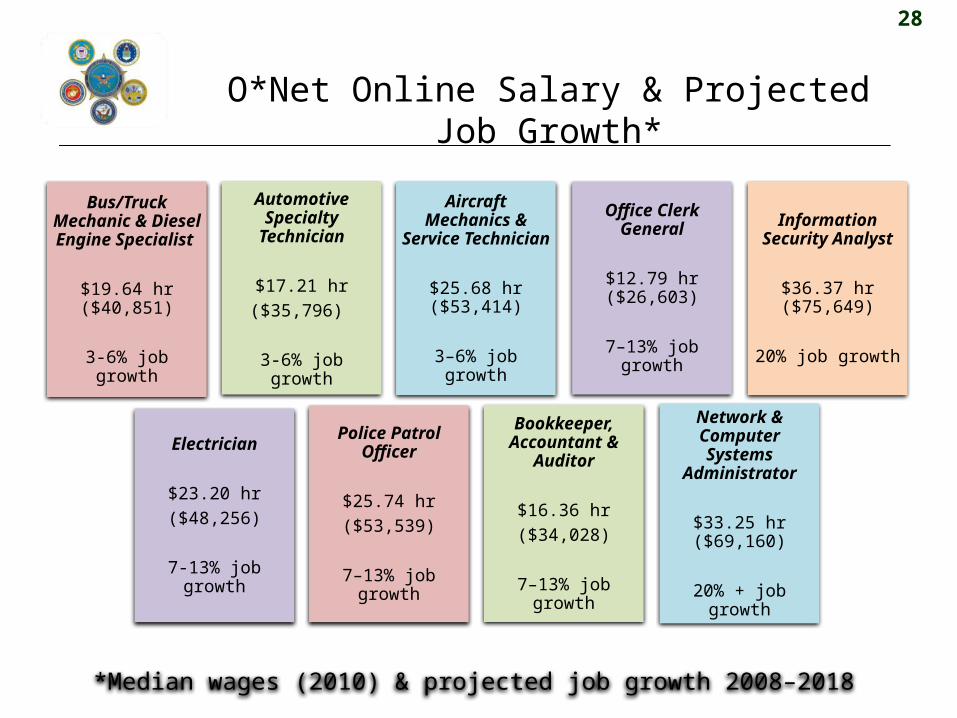

O*Net Online Salary & Projected Job Growth*

Bus/Truck Mechanic &

Diesel Engine Specialist

$19.64 hr ($40,851)

3-6% job growth

Automotive Specialty

Technician

$17.21 hr($35,796)

3-6% job growth

Office Clerk General

$12.79 hr ($26,603)

7–13% job growth

Aircraft Mechanics &

Service Technician

$25.68 hr ($53,414)

3–6% job growth

Information Security Analyst

$36.37 hr ($75,649)

20% job growth

Police Patrol Officer

$25.74 hr($53,539)

7–13% job growth

Bookkeeper, Accountant &

Auditor

$16.36 hr($34,028)

7–13% job growth

Electrician

$23.20 hr($48,256)

7-13% job growth

Network & Computer Systems

Administrator

$33.25 hr ($69,160)

20% + job growth

*Median wages (2010) & projected job growth 2008–2018

29

A Pay Comparison

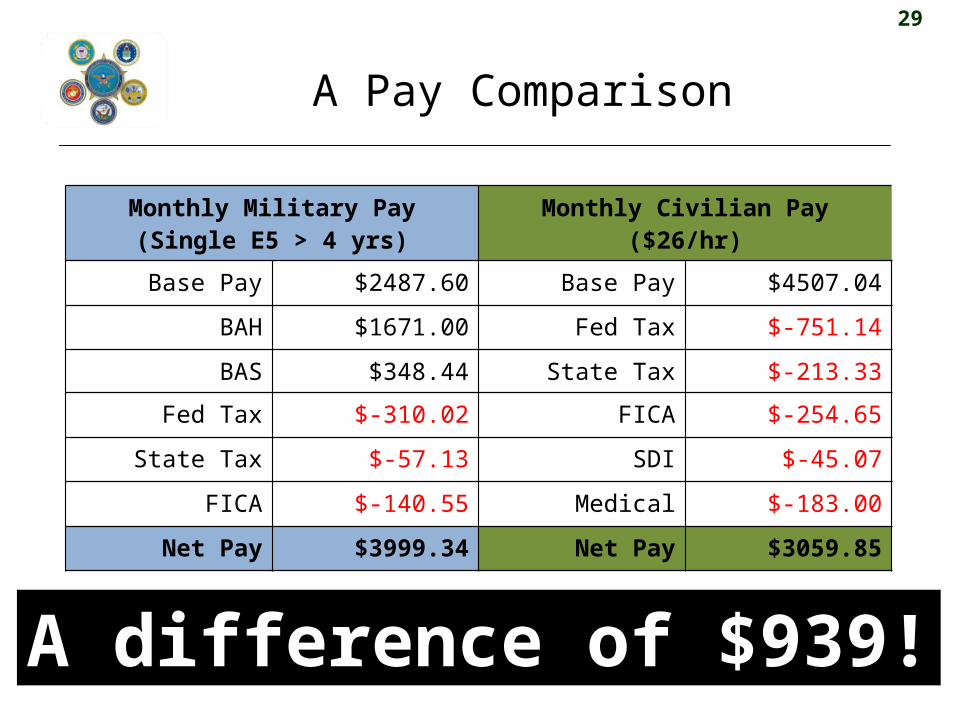

Monthly Military Pay (Single E5 > 4 yrs)

Monthly Civilian Pay ($26/hr)

Base Pay $2487.60 Base Pay $4507.04

BAH $1671.00 Fed Tax $-751.14

BAS $348.44 State Tax $-213.33

Fed Tax $-310.02 FICA $-254.65

State Tax $-57.13 SDI $-45.07

FICA $-140.55 Medical $-183.00

Net Pay $3999.34 Net Pay $3059.85

A difference of $939!

30

Military to Civilian Pay Calculator

http://calculator.gijobs.com/paycalculator.aspx

30

31

Compensation Comparison

• Use “Compensation Comparison” handout to compare compensation packages and track future job offers

• Include retirement plans, healthcare, insurance, and other benefits

• Consider what you will need for both replacement income and benefits

32

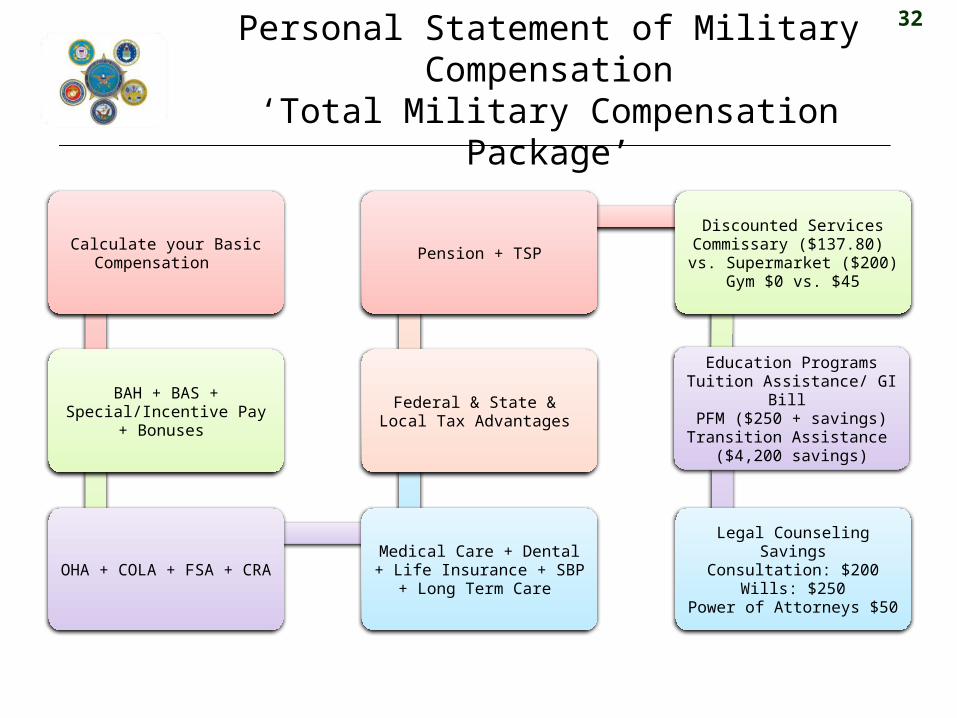

Personal Statement of Military Compensation

‘Total Military Compensation Package’

Calculate your Basic Compensation

BAH + BAS + Special/Incentive Pay +

Bonuses

OHA + COLA + FSA + CRA Medical Care + Dental + Life Insurance + SBP +

Long Term Care

Federal & State & Local Tax Advantages

Pension + TSP

Discounted ServicesCommissary ($137.80) vs. Supermarket ($200)

Gym $0 vs. $45

Education ProgramsTuition Assistance/ GI Bill

PFM ($250 + savings)Transition Assistance

($4,200 savings)

Legal Counseling SavingsConsultation: $200

Wills: $250Power of Attorneys $50

33

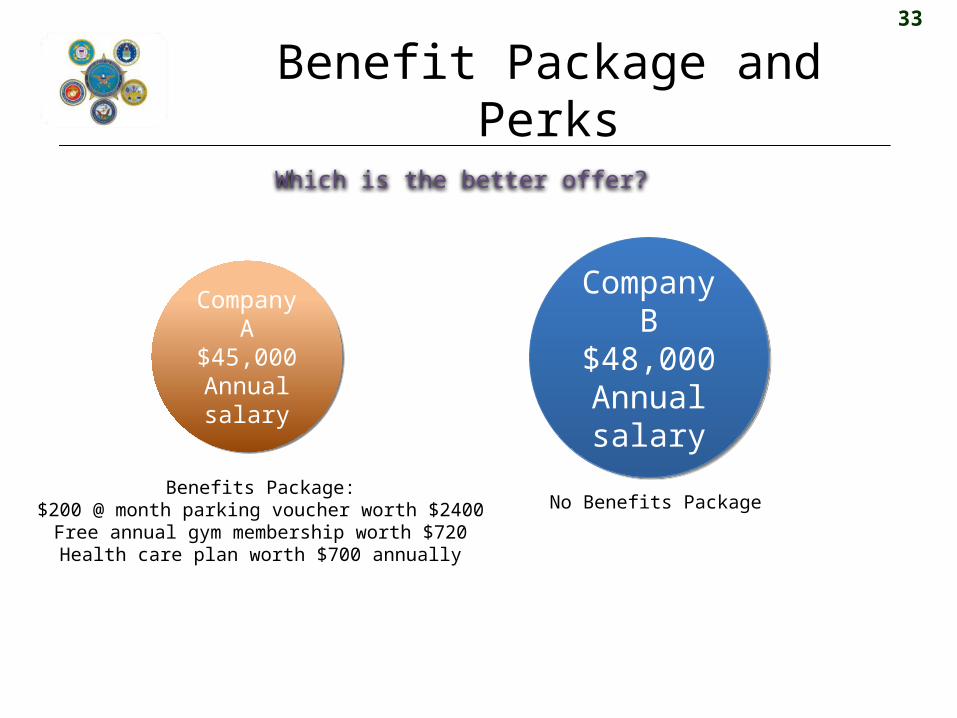

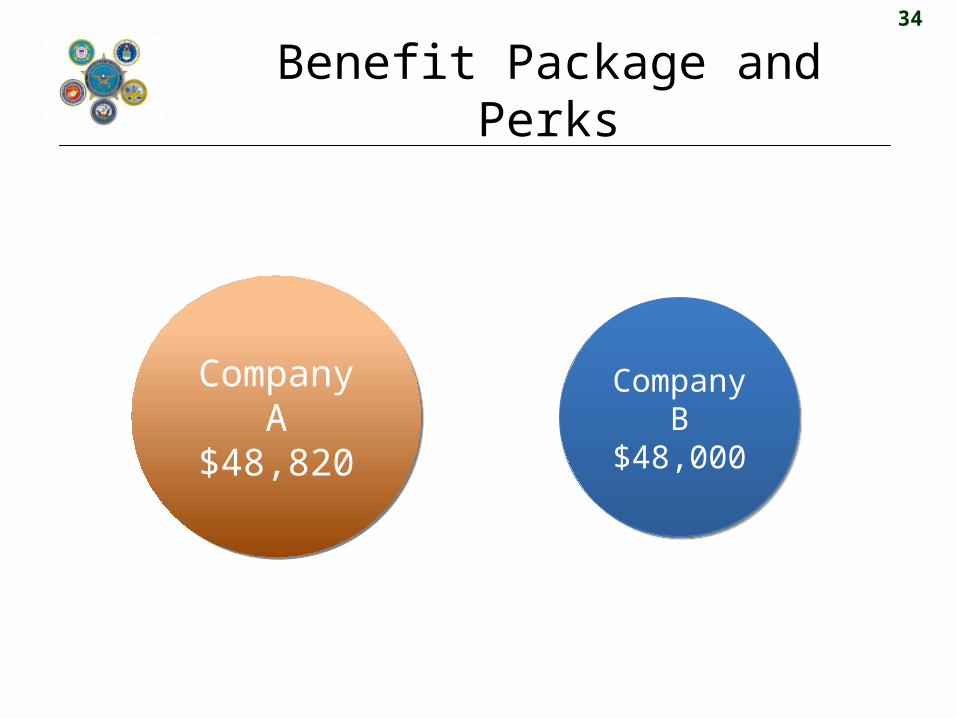

Benefit Package and Perks

Which is the better offer?

Company A$45,000Annual salary

Company A$45,000Annual salary

Company B$48,000Annual salary

Company B$48,000Annual salary

Benefits Package:$200 @ month parking voucher worth $2400

Free annual gym membership worth $720Health care plan worth $700 annually

No Benefits Package

34

Benefit Package and Perks

Company B$48,000

Company B$48,000

Company A$48,820

Company A$48,820

35

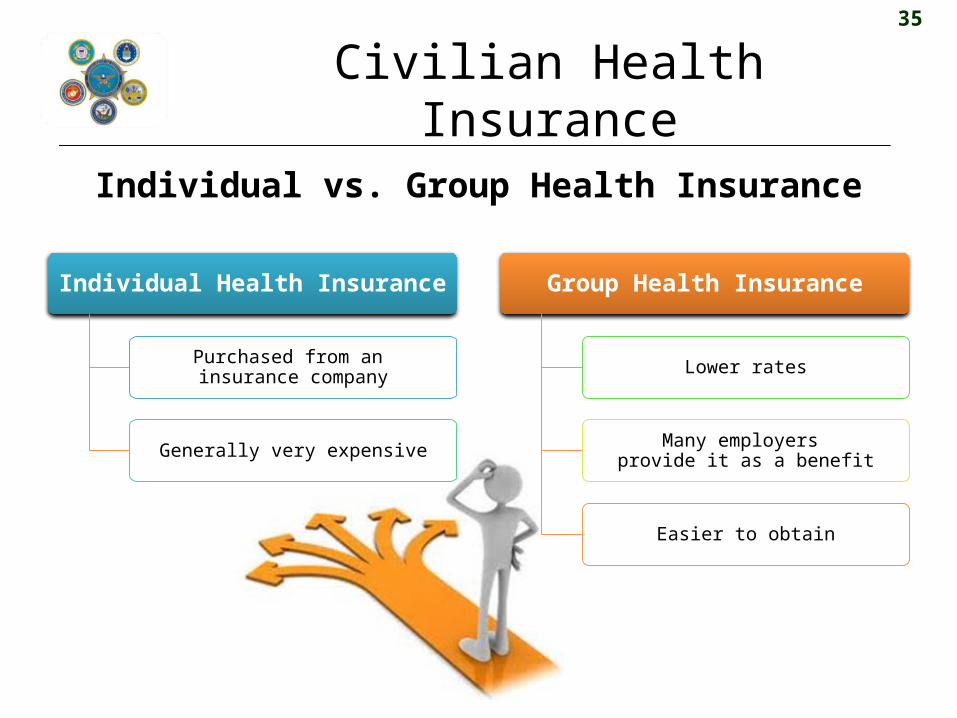

Civilian Health Insurance

Individual vs. Group Health Insurance

Individual Health Insurance

Purchased from an insurance company

Generally very expensive

Group Health Insurance

Lower rates

Many employers provide it as a benefit

Easier to obtain

36

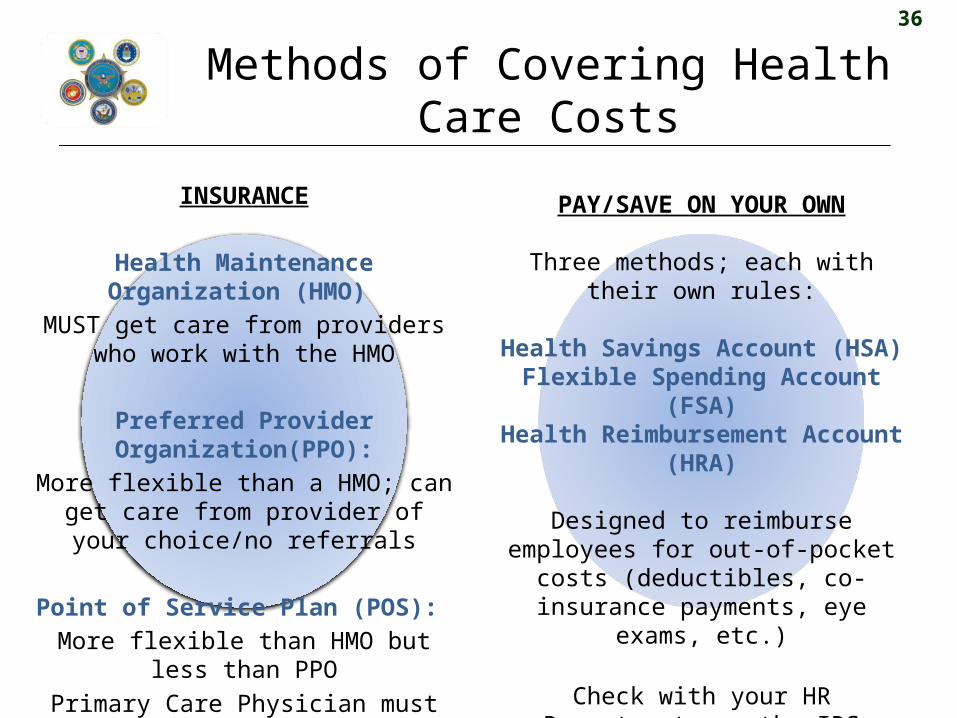

Methods of Covering Health Care Costs

INSURANCE

Health Maintenance Organization (HMO)

MUST get care from providers who work with the HMO

Preferred Provider Organization(PPO):

More flexible than a HMO; can get care from provider of your

choice/no referrals

Point of Service Plan (POS): More flexible than HMO but less

than PPOPrimary Care Physician must be within the participating provider

list

PAY/SAVE ON YOUR OWN

Three methods; each with their own rules:

Health Savings Account (HSA)Flexible Spending Account

(FSA)Health Reimbursement

Account (HRA)

Designed to reimburse employees for out-of-pocket costs

(deductibles, co-insurance payments, eye exams, etc.)

Check with your HR Department, or the IRS website (www.irs.gov)

for the more information

37

Continued Health Care Benefit Program (CHCBP)

• For Service-members separating from active duty (& families) – Must be under other than adverse conditions – Eligibility is for up to 18 months of CHCBP health

benefits after enrollment• Enrollment & Fees

– Must enroll w/in 60 days of loss of military health care benefits

– Coverage must be effective as of the date eligibility for military health care is terminated

– Quarterly premiums • $1,138 (FY13) member only / $1,193 (FY14) member

only • $2,555 (FY13) mbr and fmly / $2,682 (FY14) mbr and

fmly – Enrollees responsible for paying cost shares and

deductibles

38

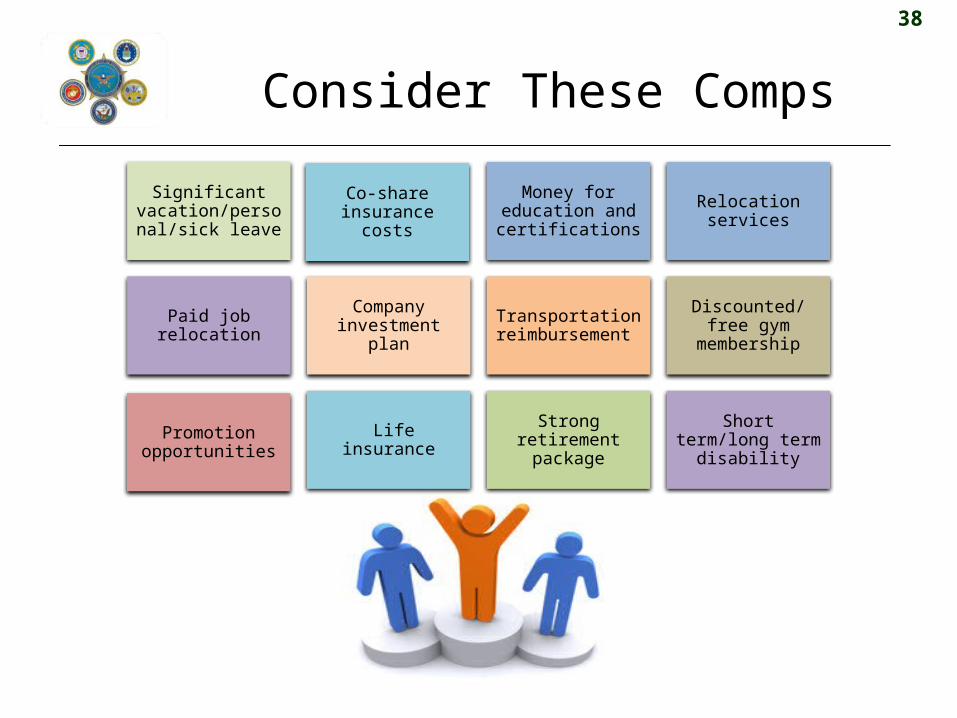

Consider These Comps

Significant vacation/persona

l/sick leave

Promotion opportunities

Money for education and certifications

Relocation services

Paid job relocation

Company investment plan

Transportation reimbursement

Discounted/free gym membership

Co-share insurance costs

Life insurance Strong retirement package

Short term/long term disability

39

Module 3Retirement Pensions

40

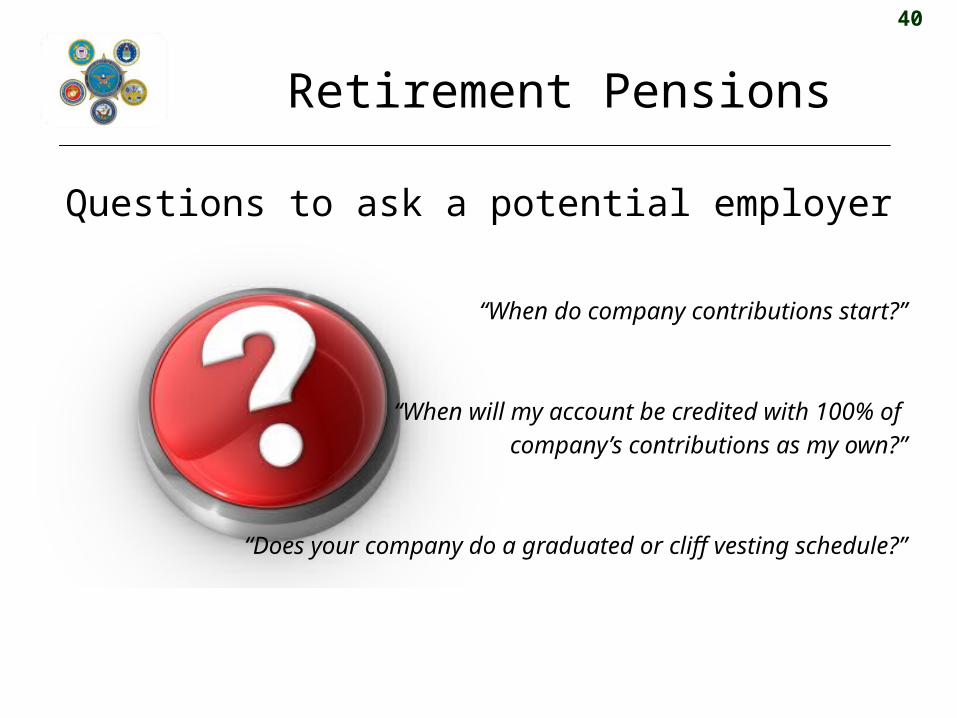

Retirement Pensions

Questions to ask a potential employer

“When do company contributions start?”

“When will my account be credited with 100% of company’s contributions as my own?”

“Does your company do a graduated or cliff vesting schedule?”

41

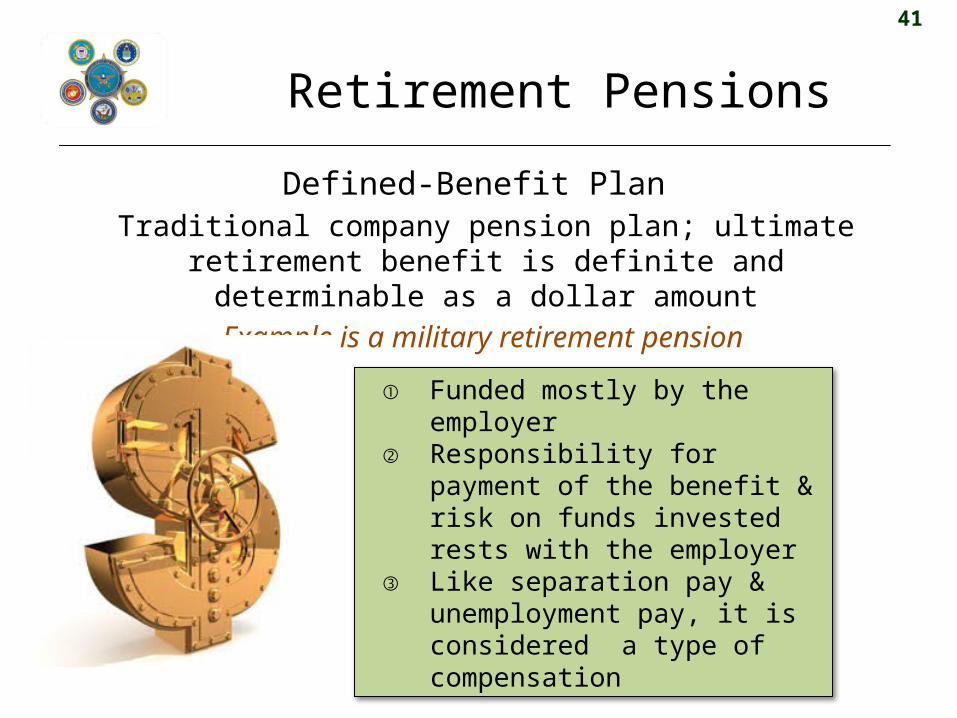

Retirement Pensions

Defined-Benefit PlanTraditional company pension plan; ultimate retirement

benefit is definite and determinable as a dollar amount

Example is a military retirement pension

① Funded mostly by the employer

② Responsibility for payment of the benefit & risk on funds invested rests with the employer

③ Like separation pay & unemployment pay, it is considered a type of compensation

42

Retirement Pensions

Defined-Contribution PlanA qualified retirement plan in which the contribution is defined

yet the ultimate benefit to be paid is not

① Contributions are from the employee② A portion may/may not be matched by

employer③ Each participant has an individual

account④ The benefit at retirement depends on

amounts contributed + investment performance of account

⑤ Investment risk may rest solely with the employee due to opportunity to choose from a number of investment options

Examples are 401(k) and 403(b) plans, Roth 401(k), Thrift Savings Plan (TSP), SIMPLE IRA, SEP, Employee Stock

Ownership (ESOP), and profit sharing

43

Thrift Savings Plan (TSP) Options

• Leave funds in TSP account (if balance is more than $200)

• Roll your TSP into another eligible account i.e., IRA, annuity, civilian 401(k)

• Withdraw your TSP funds completely

Some funds may include tax-exempt

contributions!Contact ThriftLine(1-TSP-YOU-FRST)

www.tsp.gov

44

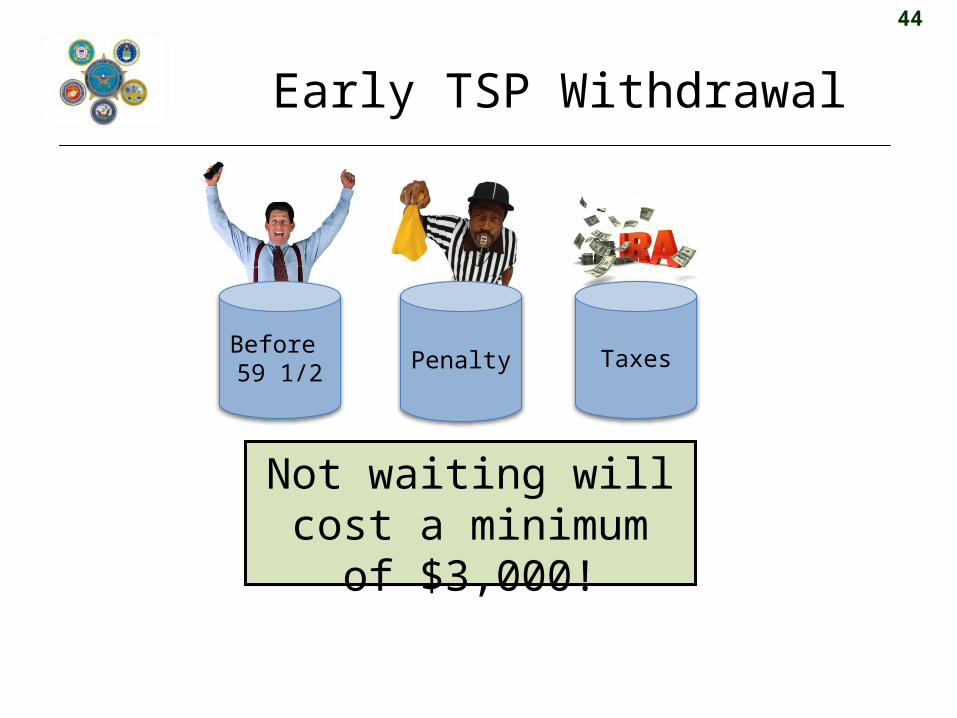

Early TSP Withdrawal

ExampleMember @ 42 withdrawals $10,000 balance from TSP

A premature withdrawal penalty costs $1,000

Penalty

Factor in a minimum 20% tax rate

that will cost $2,000

Not waiting will cost a minimum of

$3,000!

Before 59 1/2 Taxes

45

Cutting Taxes While Investing

• Tax-deferred accounts allow the investor to delay paying taxes on earnings.

• Immediate benefit is that the contribution is deducted from paychecks before income taxes are calculated, so taxable pay is reduced today.

46

Module 4 Housing:

To Rent Or Buy

47

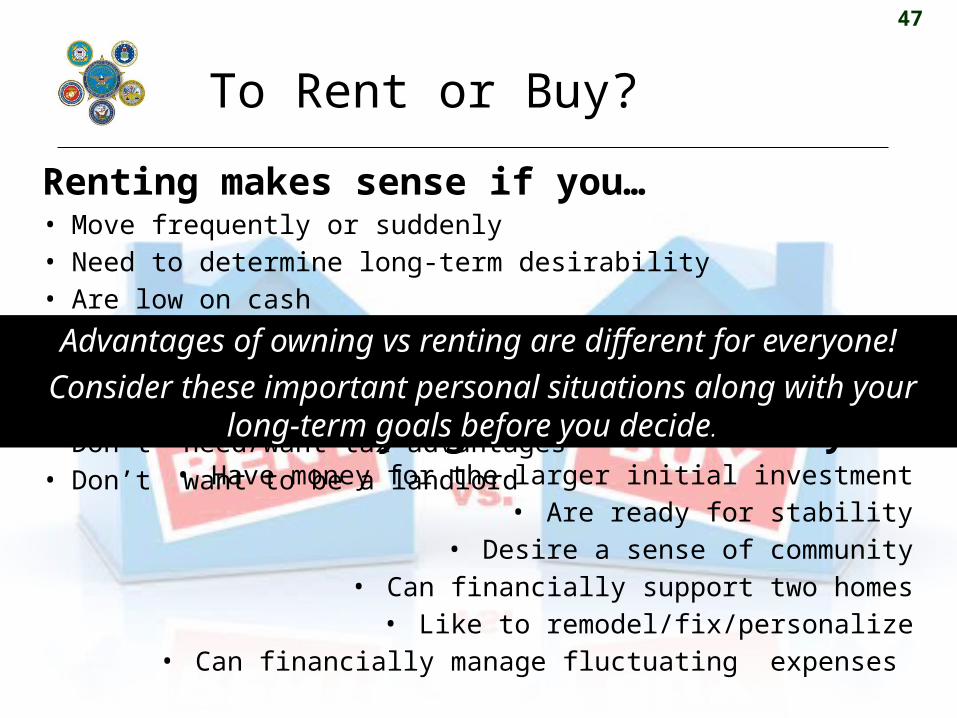

To Rent or Buy?

Buying makes sense if you…• Have money for the larger initial investment

• Are ready for stability• Desire a sense of community

• Can financially support two homes• Like to remodel/fix/personalize

• Can financially manage fluctuating expenses

Renting makes sense if you…• Move frequently or suddenly• Need to determine long-term desirability• Are low on cash• Don’t have time/desire/funds for maintenance/improvements• Don’t want to risk loss of equity• Don’t need/want tax advantages• Don’t want to be a landlord

Advantages of owning vs renting are different for everyone!

Consider these important personal situations along with your long-term goals before you decide..

48

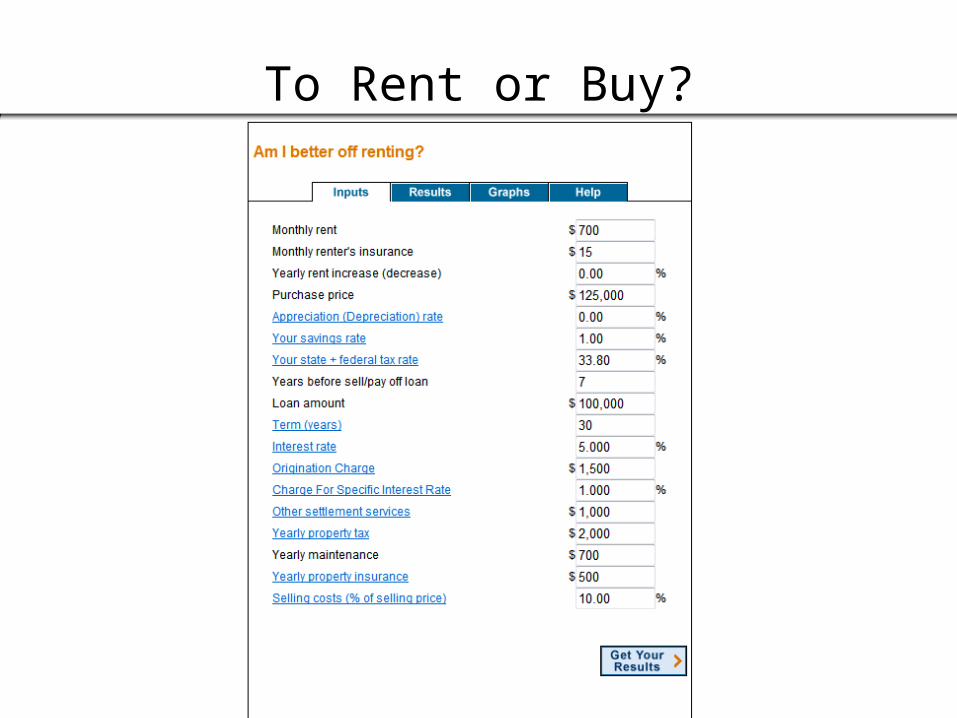

To Rent or Buy?

49

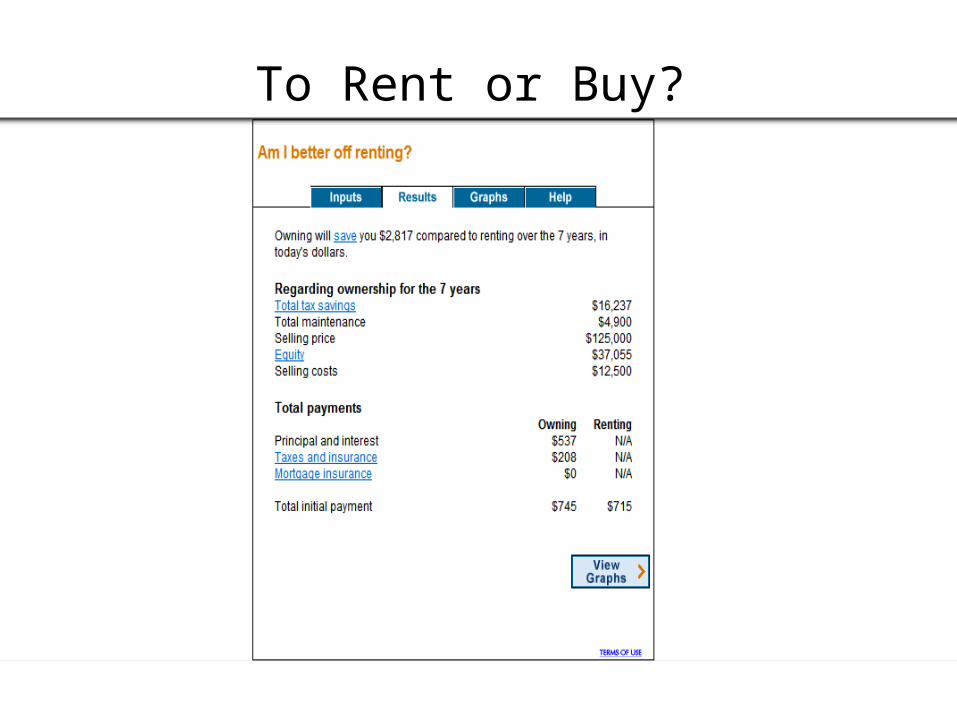

To Rent or Buy?

50

50

Relocation Assistance

The Relocation Assistance Program (RAP), Transportation Management

Office (TMO) and Personal Financial Management Specialist (PFMs) can

assist with information regarding:• Entitlements• Allowances• Needs• Costs

51

51

Beyond Renting vs Buying

A Personal Financial Management Specialist (PFMs) can assist with:

• Selling Your Home• Buying a Home• Short Sales• Foreclosure• Negative Equity

Additional resource: http://www.freddiemac.com/homeownership/educational/?intcmp=AHTRER

52

Module 5Taxes

Core PFRP For Transition

53

Military Tax Issues

• Tax Advantages• FICA (Social

Security)• Federal taxes• State taxes

• Withholding• Marital status• Exemptions

535.7

Use VITA, www.irs.gov, state calculators

54

Tax Considerations

• No more auto extension• May need assistance for

TSP tax issues• Important to factor state

tax laws into salary considerations & budget

• Separating veterans only have one year from separation to view/print

myPay W-2 • Advantages of educational

expenses

55

Contact Installation Legal Office

• Include several items:– Will– Trusts (as needed)– Power of Attorney (POA)– Medical directive or

medical POA– Financial plan to care for

survivors• Ensure information on

designated beneficiaries is current and correct

• Update every couple of years or when major life changes occur

Determine distribution of assets during lifetime and at death

56

Core PFRP for Transition

Module 6Spending

Plan

57

Learning Objectives• Define long-term/short term

transition goals• Determine cost of each goal• Determine current financial

situation using the Financial Planning Worksheet for Transition

• Compare current financial spending plan to goals

• Analyze current/desired financial state

• Anticipate future requirements

• Complete the following sections in their financial spending plan– Net Worth Statement

– Income Statement– Savings & Expenses– Indebtedness Summary– Action plan / Goals– Daily Expense / Spend

Plan• Develop a post-service, 12-

month transition spending plan

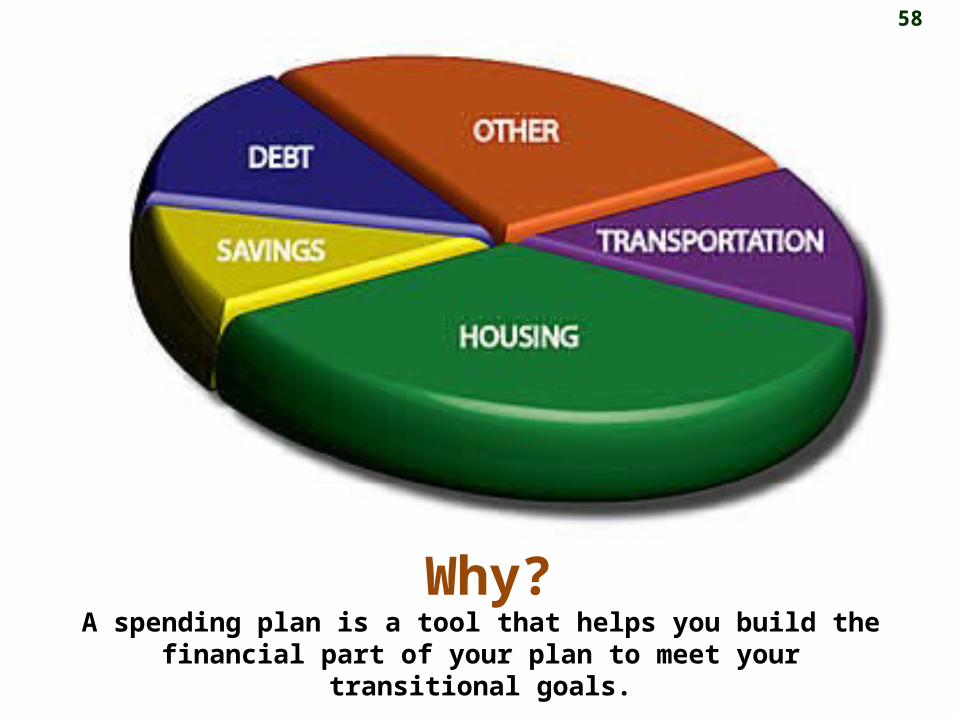

58

A spending plan is a tool that helps you build the financial part of your plan to meet your transitional

goals.

Why?

59

Spending Plan Characteristics

Guide & servant

No need to account for

each penny

Easy to understand

Reflects wants & needs

Based on current

income/expenses

Practical & realistic

Flexible

Provides for necessities

and fun

60

Why a Spending Plan is Important

• Live within your income

• Realize personal goals

• Maintain good credit history

• Get more for your money

• Reduce financial stress

• Enjoy financial freedom

61

The Financial Planning Worksheet

Six components of the worksheet

1. Net Worth Statement

2. Income Statements

3. Savings & Expenses

4. Indebtedness Summary

5. Action Plan / Goals

6. Daily Expense / Spending Plan

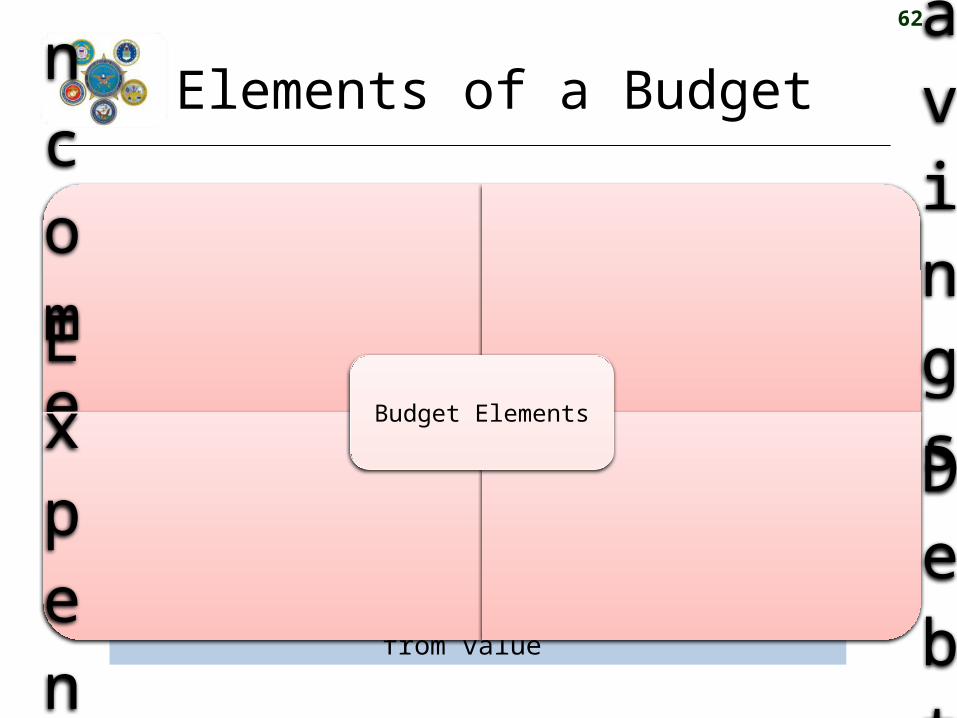

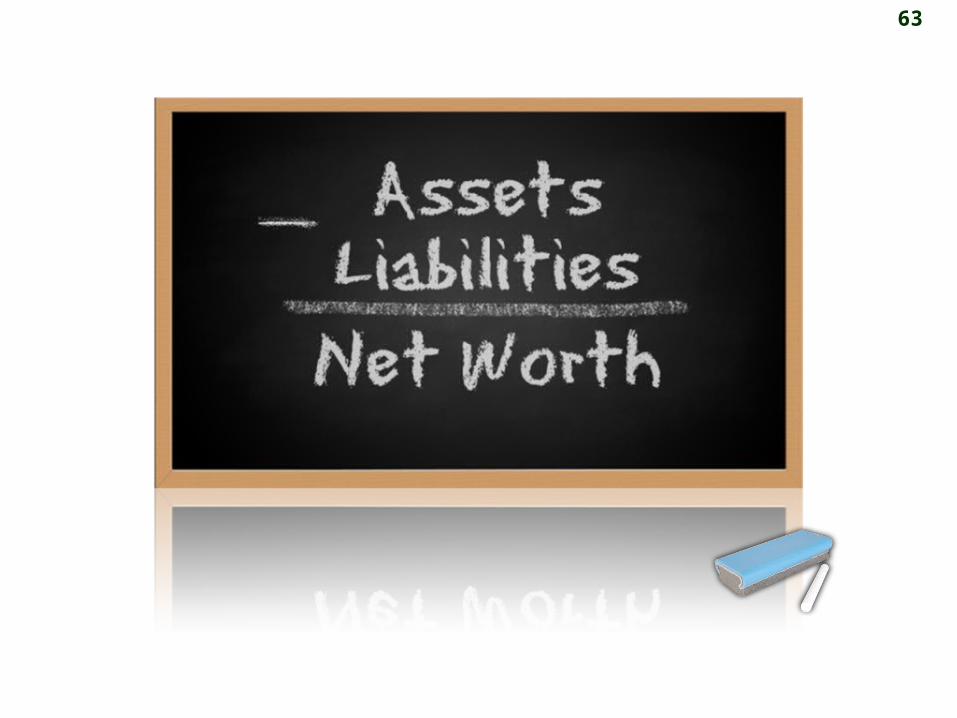

62

To calculate net worth, subtract balance from value

Elements of a Budget

Income

SavingsE

xpenses

Debts

Budget Elements

63

4.12

64

Estimating Net Worth

www.savingsbond.govwww.homegain.com

www.nada.com

65

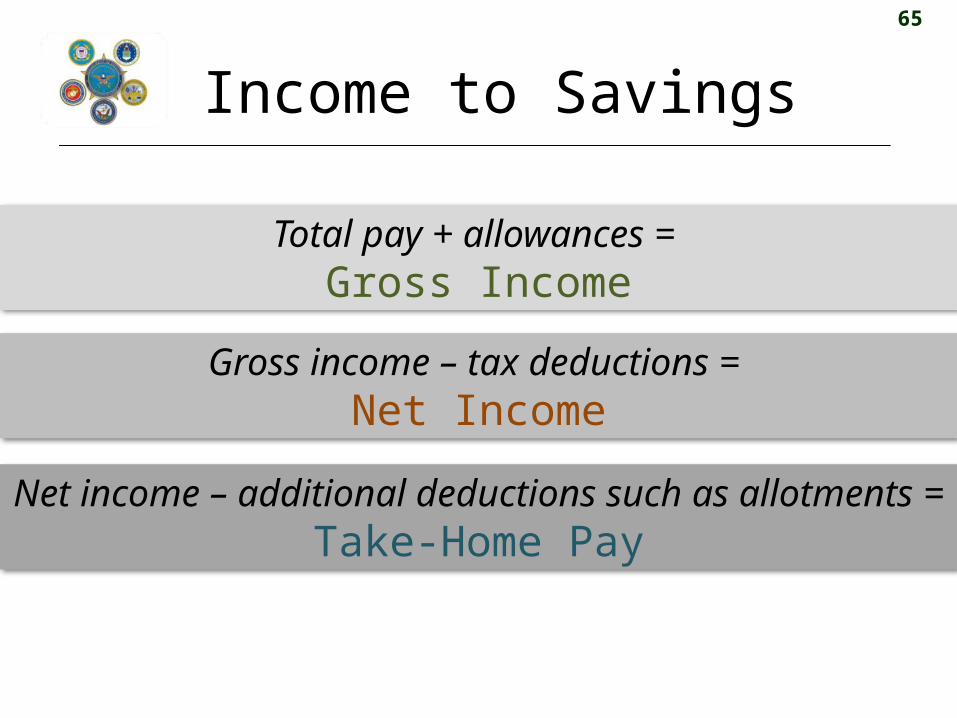

Income to Savings

4.13

Total pay + allowances = Gross Income

Gross income – tax deductions = Net Income

Net income – additional deductions such as allotments =

Take-Home Pay

66

4.13

Complete the Income and Savings portion of the worksheet

67

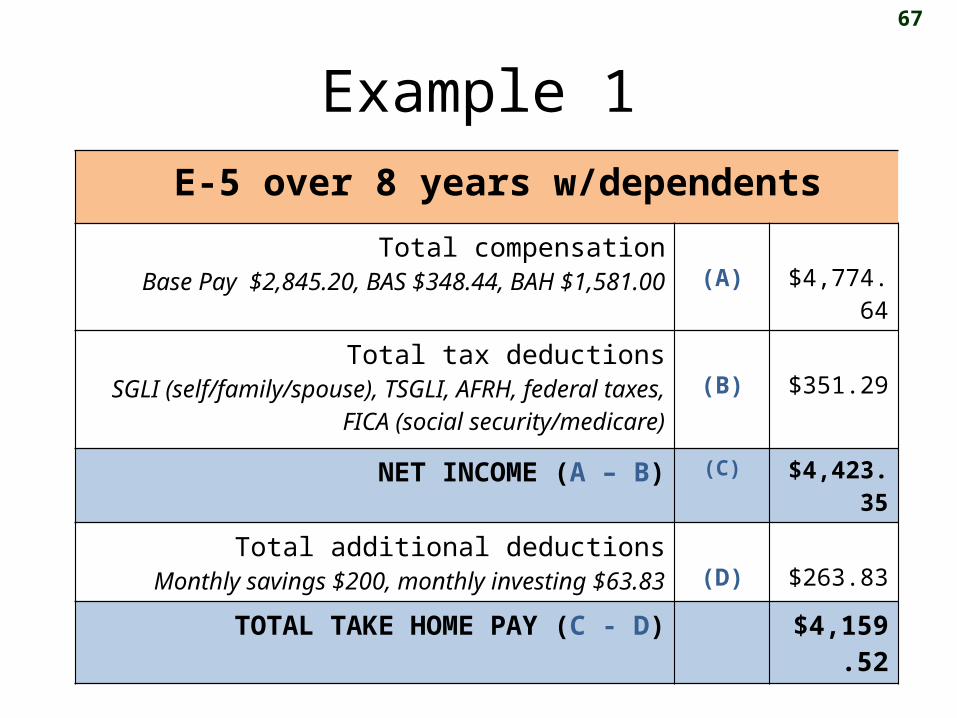

Example 1 E-5 over 8 years w/dependents

Total compensation Base Pay $2,845.20, BAS $348.44, BAH $1,581.00 (A) $4,774.64

Total tax deductionsSGLI (self/family/spouse), TSGLI, AFRH, federal taxes,

FICA (social security/medicare)(B) $351.29

NET INCOME (A – B) (C) $4,423.35

Total additional deductionsMonthly savings $200, monthly investing $63.83 (D) $263.83

TOTAL TAKE HOME PAY (C - D) $4,159.52

68

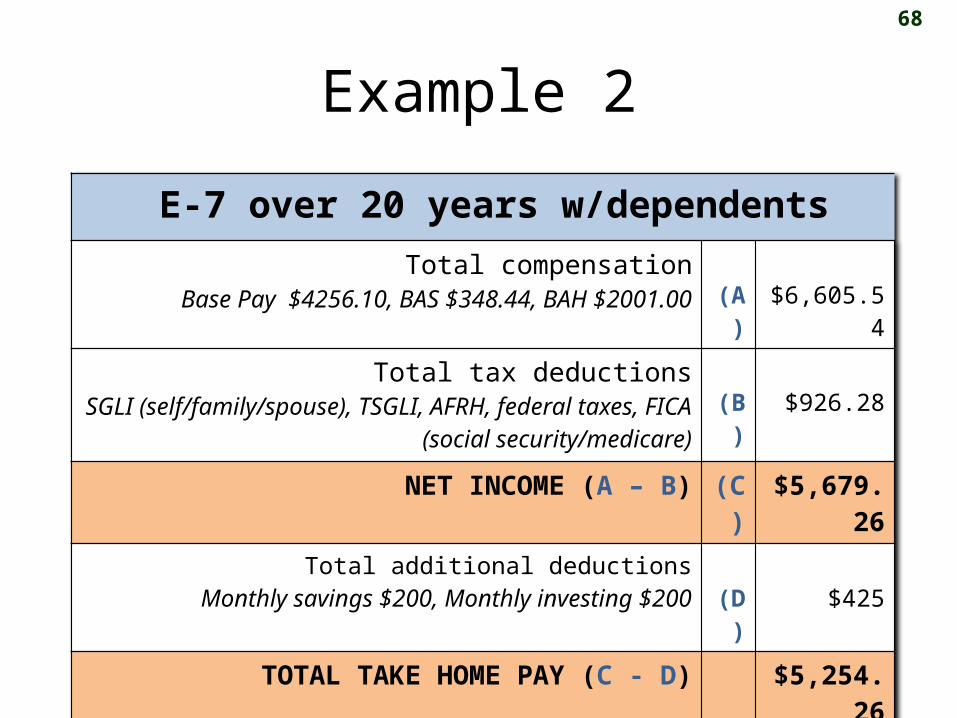

Example 2

E-7 over 20 years w/dependents

Total compensation Base Pay $4256.10, BAS $348.44, BAH $2001.00 (A) $6,605.54

Total tax deductionsSGLI (self/family/spouse), TSGLI, AFRH, federal taxes, FICA

(social security/medicare)(B) $926.28

NET INCOME (A – B) (C) $5,679.26

Total additional deductionsMonthly savings $200, Monthly investing $200 (D) $425

TOTAL TAKE HOME PAY (C - D) $5,254.26

69

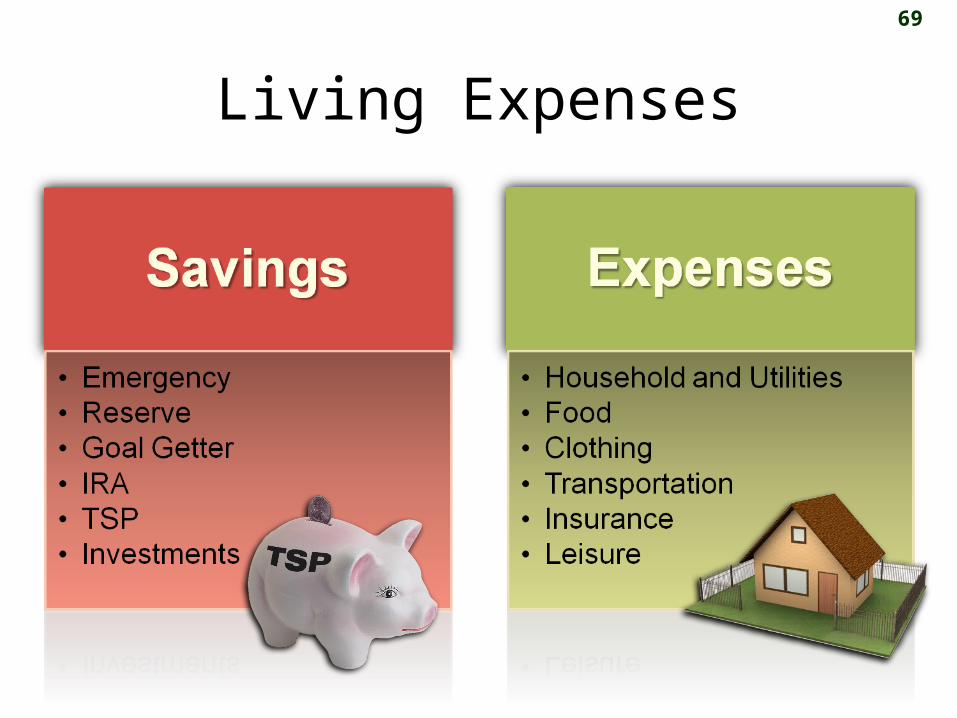

Living Expenses

70

Tracking Expenses

• Track spending for 2-4 weeks• Record all expenses daily• Group expenditures by

category

71

4.13

Calculate the living expenses on the Financial Planning Worksheet

72

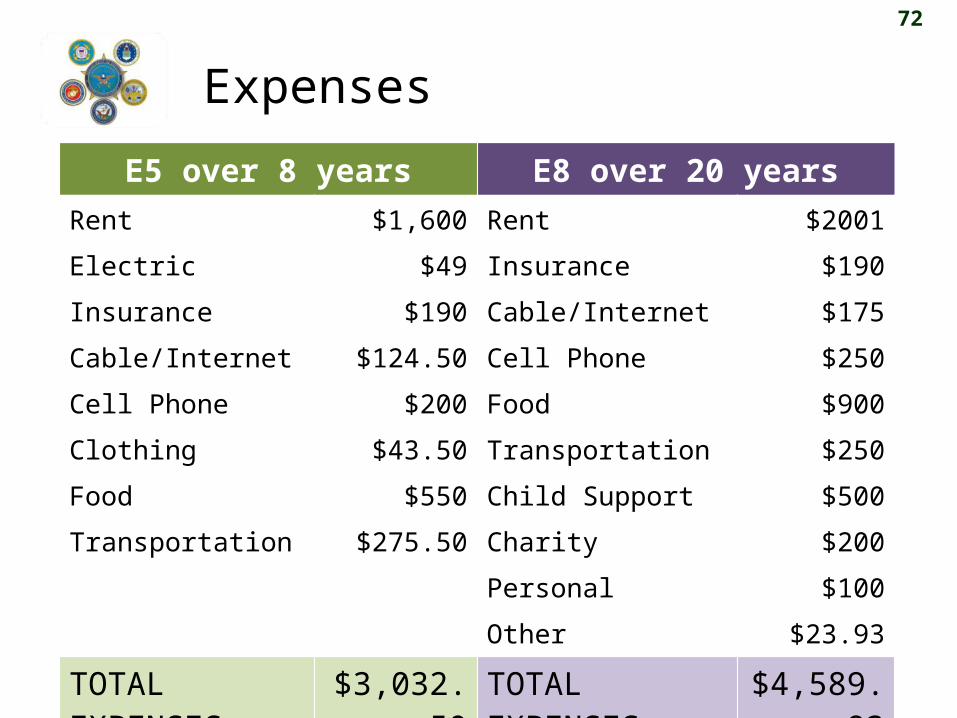

ExpensesE5 over 8 years E8 over 20 years

Rent $1,600 Rent $2001Electric $49 Insurance $190Insurance $190 Cable/Internet $175Cable/Internet $124.50 Cell Phone $250Cell Phone $200 Food $900Clothing $43.50 Transportation $250Food $550 Child Support $500Transportation $275.50 Charity $200

Personal $100Other $23.93

TOTAL EXPENSES $3,032.50 TOTAL EXPENSES $4,589.9373% OF INCOME 87% OF INCOME

73

Debt Management

Creditor

Balance Due

Minimum

PaymentInterest

Rate Tot

al

74

Summary

• Total pay equals all compensation

• Total compensation minus all deductions equals take home pay

• Take home pay is what you live on for the month

75

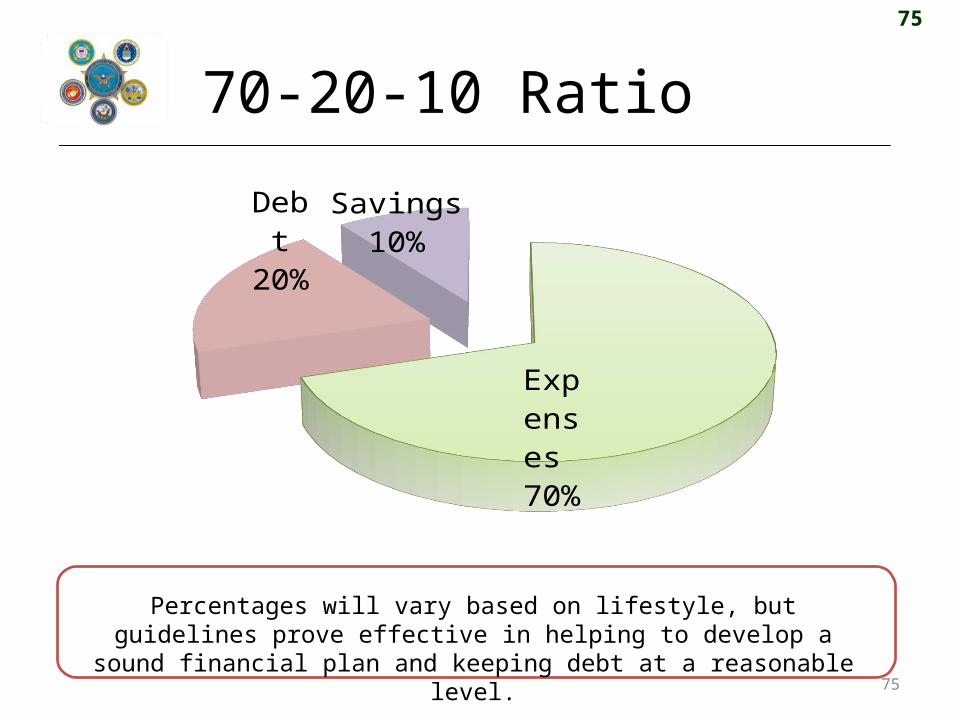

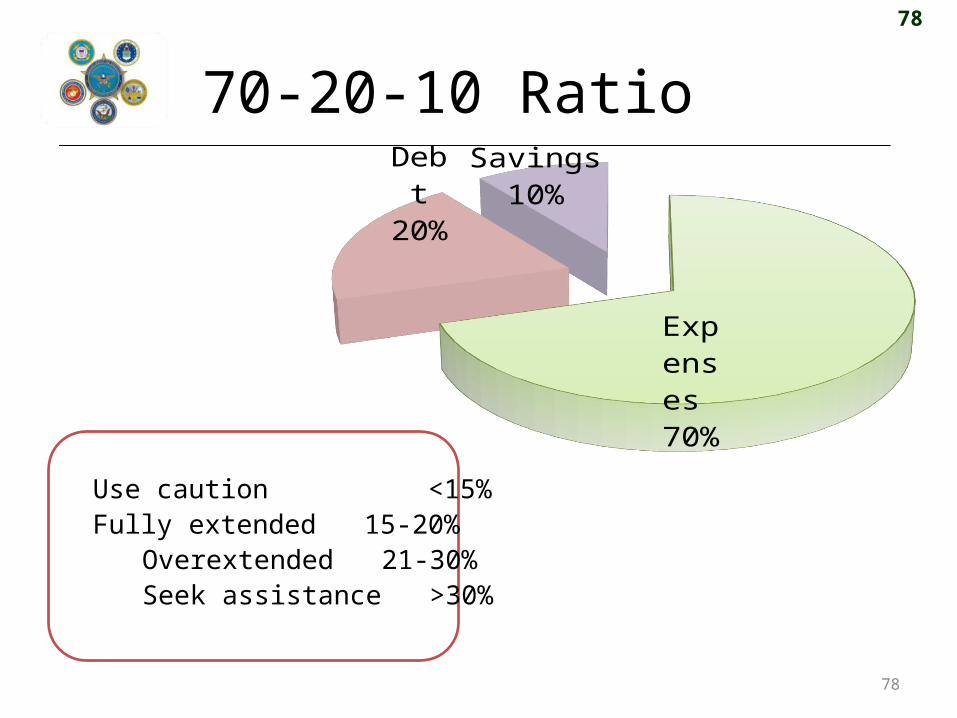

70-20-10 Ratio

75

Ex-penses 70%

Debt

20%

Savings10%

4.18

Percentages will vary based on lifestyle, but guidelines prove effective in helping to develop a sound financial plan and keeping

debt at a reasonable level.

76

4.13

Calculate the indebtedness & summary section of the Financial

Planning Worksheet

77

77

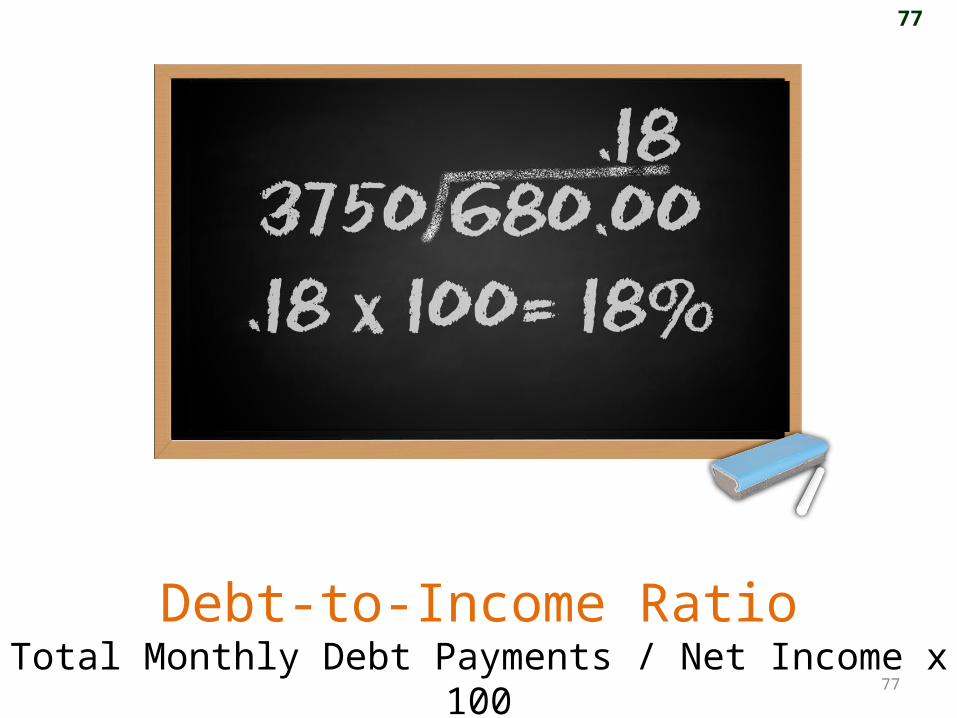

Debt-to-Income RatioTotal Monthly Debt Payments / Net Income x 100

78

70-20-10 Ratio

784.18

Use caution <15%Fully extended 15-20%

Overextended 21-30% Seek assistance >30%

Ex-penses 70%

Debt

20%

Savings10%

79

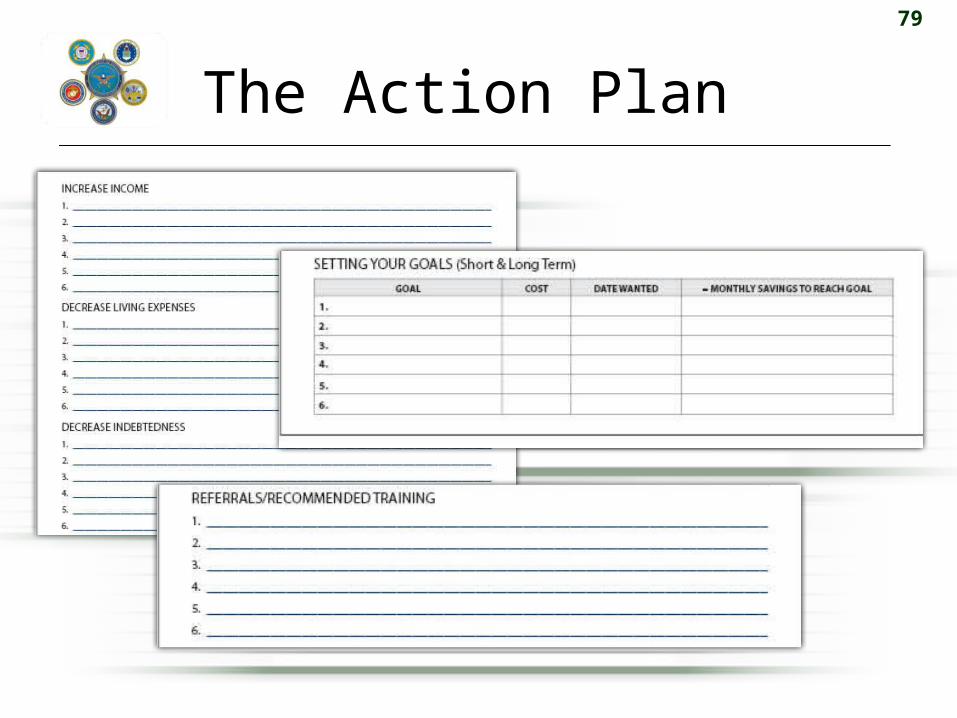

The Action Plan

80

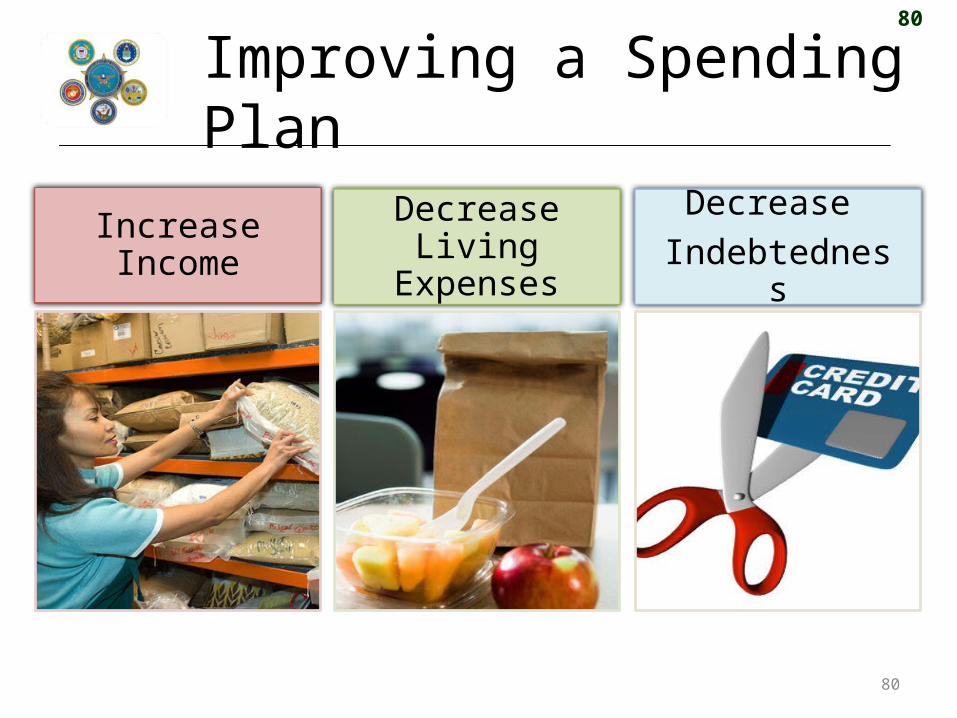

Improving a Spending Plan

80

Increase Income

Decrease

Indebtedness

Decrease Living

Expenses

81

Sources of Help

82

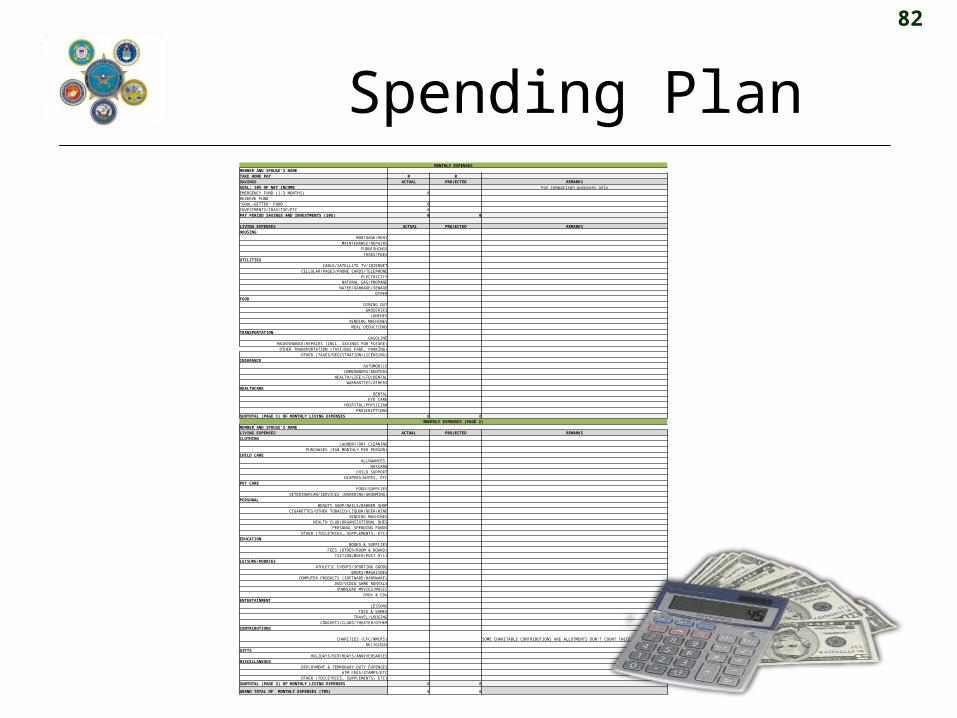

Spending Plan

4.17

MONTHLY EXPENSESMEMBER AND SPOUSE'S NAME TAKE HOME PAY 0 0 SAVINGS ACTUAL PROJECTED REMARKSGOAL: 10% OF NET INCOME For comparison purposes onlyEMERGENCY FUND (1-3 MONTHS) 0 RESERVE FUND "GOAL-GETTER" FUND 0 INVESTMENTS/IRAS/TSP/ETC 0 PAY PERIOD SAVINGS AND INVESTMENTS (10%) 0 0 LIVING EXPENSES ACTUAL PROJECTED REMARKSHOUSING

MORTGAGE/RENT MAINTENANCE/REPAIRS

FURNISHINGS TAXES/FEES

UTILITIES CABLE/SATELLITE TV/INTERNET

CELLULAR/PAGES/PHONE CARDS/TELEPHONE ELECTRICITY

NATURAL GAS/PROPANE WATER/GARBAGE/SEWAGE

OTHER FOOD

DINING OUT GROCERIES

LUNCHES VENDING MACHINES

MEAL DEDUCTIONS TRANSPORTATION

GASOLINE MAINTENANCE/REPAIRS (INCL. SAVINGS FOR FUTURE) OTHER TRANSPORTATION (TAXI/BUS FARE, PARKING)

OTHER (TAXES/REGISTRATION/LICENSING) INSURANCE

AUTOMOBILE HOMEOWNERS/RENTERS

HEALTH/LIFE/LTD/DENTAL WARRANTIES/OTHERS

HEALTHCARE DENTAL

EYE CARE HOSPITAL/PHYSICIAN

PRESCRIPTIONS SUBTOTAL (PAGE 1) OF MONTHLY LIVING EXPENSES 0 0

MONTHLY EXPENSES (PAGE 2)MEMBER AND SPOUSE'S NAME LIVING EXPENSES ACTUAL PROJECTED REMARKSCLOTHING

LAUNDRY/DRY CLEANING PURCHASES ($50 MONTHLY PER PERSON)

CHILD CARE ALLOWANCES

DAYCARE CHILD SUPPORT

DIAPERS/WIPES, ETC PET CARE

FOOD/SUPPLIES VETERINARIAN/SERVICES (BOARDING/GROOMING)

PERSONAL BEAUTY SHOP/NAILS/BARBER SHOP

CIGARETTES/OTHER TOBACCO/LIQUOR/BEER/WINE VENDING MACHINES

HEALTH CLUB/ORGANIZATIONAL DUES PERSONAL SPENDING FUNDS

OTHER (TOILETRIES, SUPPLEMENTS, ETC) EDUCATION

BOOKS & SUPPLIES FEES (OTHER/ROOM & BOARD)

TUITION/MGIB/POST 9/11 LEISURE/HOBBIES

ATHLETIC EVENTS/SPORTING GOODS BOOKS/MAGAZINES

COMPUTER PRODUCTS (SOFTWARE/HARDWARE) DVD/VIDEO GAME RENTALS

DOWNLOAD MOVIES/MUSIC DVDs & CDs

ENTERTAINMENT LESSONS

TOYS & GAMES TRAVEL/LODGING

CONCERTS/CLUBS/THEATER/OTHER CONTRIBUTIONS

CHARITIES (CFC/NMCRS) SOME CHARITABLE CONTRIBUTIONS ARE ALLOTMENTS DON’T COUNT TWICERELIGIOUS

GIFTS HOLIDAYS/BIRTHDAYS/ANNIVERSARIES

MISCELLANEOUS DEPLOYMENT & TEMPORARY DUTY EXPENSES

ATM FEES/STAMPS/ETC OTHER (TOILETRIES, SUPPLEMENTS, ETC)

SUBTOTAL (PAGE 2) OF MONTHLY LIVING EXPENSES 0 0 GRAND TOTAL OF MONTHLY EXPENSES (70%) 0 0

83

Summary

• Preparation is key• Develop a solid Individual Transition Plan• Use tools to manage your finances• Take advantage of available benefits• Use your resources before transition

84

Preparation for Wednesday

• Review slides and print handouts on CD if you do not have a computer– Day 3, 4 & 5

• You will be using all the handouts each day

84

85

TAP GPS Program Assessment

• We apologize for requesting you to take two assessments….however we do not receive the results of the OSD Assessment

• Please complete Financial Portion of OSD Assessment – https://www.dmdc.osd.mil/tgpsp

85

86

Post Assessment

• Please complete the Post Assessment and pass to facilitator

86

87

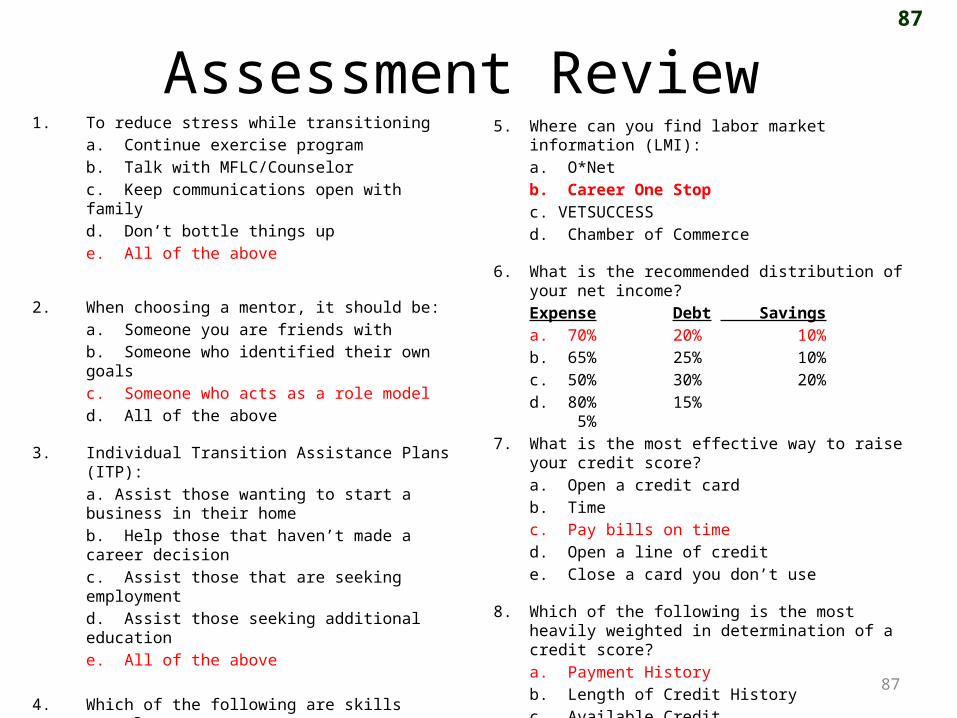

Assessment Review 1. To reduce stress while transitioning

a. Continue exercise programb. Talk with MFLC/Counselorc. Keep communications open with family d. Don’t bottle things upe. All of the above

2. When choosing a mentor, it should be:a. Someone you are friends withb. Someone who identified their own goalsc. Someone who acts as a role modeld. All of the above

3. Individual Transition Assistance Plans (ITP):a. Assist those wanting to start a business in their homeb. Help those that haven’t made a career decisionc. Assist those that are seeking employmentd. Assist those seeking additional educatione. All of the above

4. Which of the following are skills translators:a. Hero2Hired, Career One Stop, VA for Vets, USA Jobsb. VETSUCCESS, Hero2Hired, Career One Stop, O*NETc. USAJOBS, VETSUCCESS, Hero2Hired, Career One Stop, O*NETd. VETSUCCESS, Hero2Hired, Career One Stop, O*NET, VA For Vets

5. Where can you find labor market information (LMI):a. O*Netb. Career One Stopc. VETSUCCESSd. Chamber of Commerce

6. What is the recommended distribution of your net income?Expense Debt Savingsa. 70% 20% 10%b. 65% 25% 10%c. 50% 30% 20%d. 80% 15% 5%

7. What is the most effective way to raise your credit score?a. Open a credit cardb. Timec. Pay bills on timed. Open a line of credite. Close a card you don’t use

8. Which of the following is the most heavily weighted in determination of a credit score? a. Payment Historyb. Length of Credit Historyc. Available Creditd. Types of credit

87

88

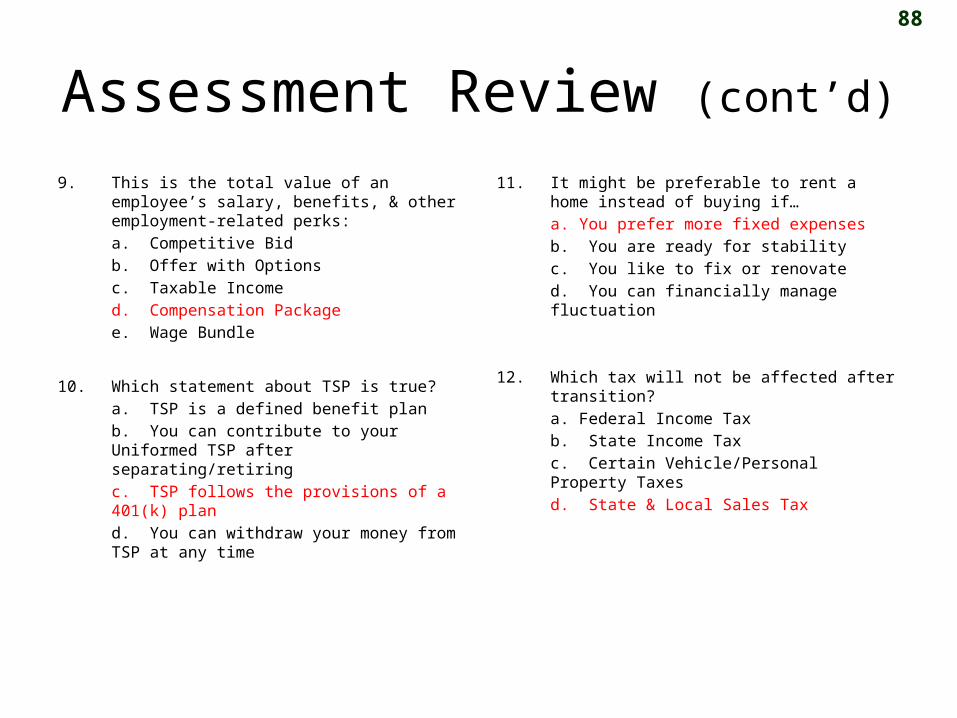

Assessment Review (cont’d)

9. This is the total value of an employee’s salary, benefits, & other employment-related perks:a. Competitive Bidb. Offer with Optionsc. Taxable Incomed. Compensation Packagee. Wage Bundle

10. Which statement about TSP is true?a. TSP is a defined benefit planb. You can contribute to your Uniformed TSP after separating/retiringc. TSP follows the provisions of a 401(k) pland. You can withdraw your money from TSP at any time

11. It might be preferable to rent a home instead of buying if…a. You prefer more fixed expensesb. You are ready for stabilityc. You like to fix or renovated. You can financially manage fluctuation

12. Which tax will not be affected after transition?a. Federal Income Taxb. State Income Taxc. Certain Vehicle/Personal Property Taxesd. State & Local Sales Tax

89

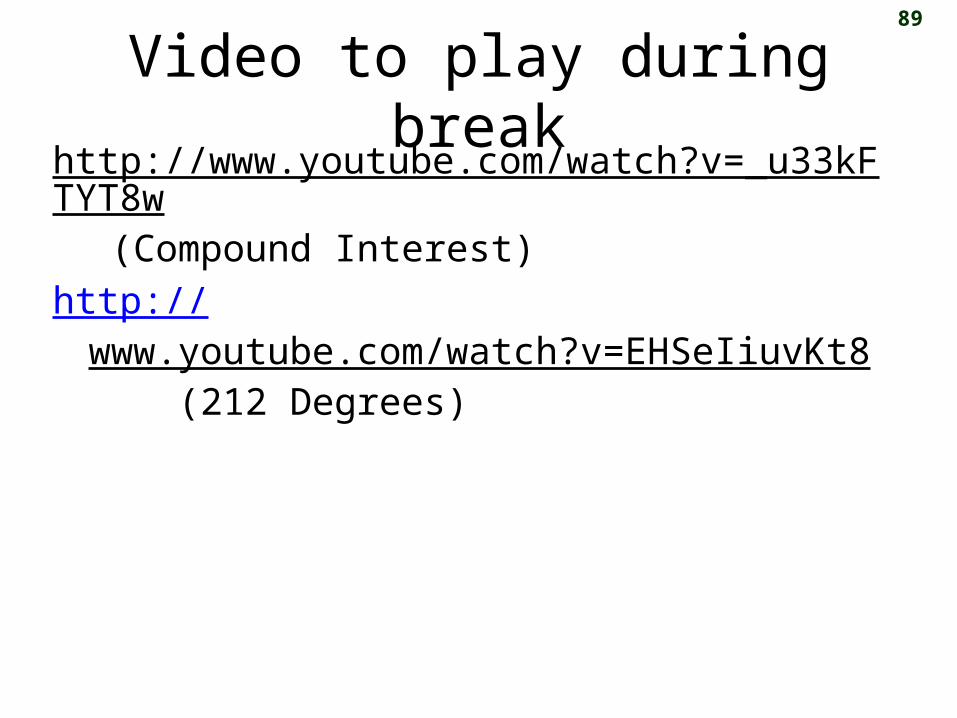

Video to play during breakhttp://www.youtube.com/watch?v=_u33kFTYT8w

(Compound Interest)http://www.youtube.com/watch?v=EHSeIiuvKt8 (212

Degrees)