stpi sez echnology excise service tax ifrs … · strategy dtc growth update gst corporate laws...

TRANSCRIPT

EXCISE

• • • ISSUE - VII VOLUME - VI MAY - 2011

CO

MM

ER

CIA

L SER

VIC

ES

STR

ATE

GIC

MA

NA

GEM

EN

T W

ITH

IN L

EG

AL

FR

AM

EW

OR

K

IFRSDIRECT TAXES

EOU

FOREIGN TRADE

INFO

RM

ATI

ON

TEC

HN

OLO

GYSEZ

BUSINESS

EXPORT - IMPORT

ECONOMIC GROWTH

IND

USTR

Y W

ATC

H

STPIBTP

STRATEGY

DTCGROWTH

UPDATE

GST

CORPORATE LAWS

FEMA

COMMERCIAL LAWS

BENEFITS

www.bizsolindia.com

CUSTOMS

SERVICE TAX

We believe in C-2

This Month 4 U C-2

Editorial 1

By Ashok Nawal

By Ashok Nawal

What's New 22

Beyond the obvious 38

Breaking News 42

Did you miss this 43

Lighter Moments 44

Bizsol Services C-3

Greetings for New year C-4

Entitlement of Cenvat Credit of 2

various Input Services

Service Tax – Point of Taxation 15

& Cenvat Entitlement

A DEFINING DECADE IN THE 20

MAKING

Venkat R Venkitachalam

IN THIS ISSUE

• For important due dates please turn over

May - 2011

UPDATE

THISMONTH

4U

Payments Due Dates

Central Sales Tax –April 2011 Return-cum-Challan 21/05/2011

VAT – April 2011 Return 21/05/2011

ESI Contribution 21/05/2011

Profession Tax 31/05/2011

Excise Duties-May 2010 05/06/2011

Excise Duties- May 2010 By E-Payment 06/06/2011

Service Tax – May 2010 05/06/2011

Service Tax -May 2010–By E Payment 06/06/2011

TDS/TCS- May 2010 07/06/2011

Provident Fund- May 2010 15/06/2011

Returns

ER-1 and ER-2 Monthly return for May 2010 10/06/2011

ER-6- May 2010 10/06/2011

W E B E L I E V E I N

E D I T O R I A LBarack Obama must be a happy and relieved man. He has enough reason to be. After having slain the biggest enemy of the US he now has virtually and automatically re-elected himself to the White House for another term. It may be an irony that a man called Obama is the President of the US when another called Osama was the most wanted enemy of that country. With such homonymic names one may be pardoned for any proverbial slip-of-tongue for saying Osama is the President and Obama is the Enemy. The relief for Obama may be real in that introductory speeches and encomiums for him at felicitations can now be expected to go on smoothly with no embarrassment caused by misspelling of names. That is some relief indeed at a personal level for Obama. Remember one's own name is the sweetest word for any one in any language.

With so many conspiracy theories making the rounds, the script writers in Hollywood must be busy penning a new thriller featuring the two O'mas. The operation by the Navy Seal is perhaps the toast of the town except in the town of Islamabad. The Seal may have dethroned the Israeli Mossad for the most daring and adventurous state outfit to counter terror. Whether you agree with the Americans for violating the sovereignty of Pakistan or not, you have got to admire the operation, the way it is reported to have been executed. It may be a matter of debate as to when was Pakistan more embarrassed – when Bangladesh was freed by India or when Osama was killed right in the backyard of the Pakistani establishment. You violate Pakistan's air space and be their uninvited guests for well over forty minutes, conduct a coup of sorts and walk away with the trophy in the form of the dead body of Osama bin Laden. If true, these are stuff you find only in Hollywood movies. As we go to press rumours are afloat that the ISI Chief of Pakistan has fled the country completing the story of a failed state becoming an embarrassment for its own coutrymen.

Back home away from adventures and accolades the scene is pretty depressing. There is hardly any icon untouched by scams and scandals. If a Tata is arraigned for corruption and when the list of who-is-who in the corporate sector applying for anticipatory bail, either it heralds a new era where no one however high or mighty will be spared or is a symptom of a deeper malaise that the fundamental Indian national character has undergone a mutation. Look around. There are hardly any icons in left in the country. The powerful satraps of the land look like sad caricatures of their glorious past. While Sharad Pawar will be spending the rest of his life denying one allegation or other in some part of the country, Karunanidhi will be spending his autumn evenings as a sad man having perhaps to see his daughter go to jail for a crime the booty of which was shared by all in his own family. Yeddiyrappa has no time to govern the state as he is constantly busy dousing fires for clearing files for the benefit of his family. In Maharashtra the competition in the ministry is confined only to the extent of land (or flat) you can grab while you are in power. The signal contribution ironically of Anna Hazare's crusade against corruption has so far been to help expose his own comrades from the civil society in corrupt deals. It looks that the DNA of an Indian has already undergone serious mutation making propensity to corruption an integral personality trait.

With fake pilots on the loose your life is now on the line like unauthorised and unsafe constructions being certified for occupation. Corruption now threatens your life. The employees, particularly the Pilots of Air India go on strike periodically. No one so far appears to have gained anything from these strikes. In every strike situation Air India talks tough to start tough but capitulates before you could say 'oh no'. The employees almost always with growing pressure from the media and the Courts stop short of a long drawn out battle and eventually succumb. For the Government, whose money is it any way? With all lucrative routes having been given away to private players, programmed shoddy service to the passengers, rampant corruption right from the stage of procurement of aircraft and deliberate poor planning of available resources, it will not be too long before the closure of the organisation whose icon was the pride of the nation not too long ago.

There is one reform process which we will see for sure – the prison reforms. With so many high profile politicians, influential sports administrators and corporate honchos in jail and with so many more likely to visit the jails one can reasonably expect the conditions in the jails to improve. And it is high time. The Bureaucrats in Government and the Executives in the corporate sector have one thing in common. They have all the powers in the world on paper but nothing in practice. The corporate executives may have gone to jail for alleged corruption. But this episode is likely to change the way these high-flyers look at their own jobs. It is bound to put the fear of God into the management cadres. A formal certificate in corporate governance from the auditors is no longer sufficient. You will need to practice what you preach – literally.

Mahatma Gandhi never ceases to be a topic of controversy. It is possible that the two most written about people are Gandhi and Hitler. What a twosome! With new authors coming up with new profiles of Gandhi it is but natural that more opinions float around all the time, conjecture or otherwise. The recent controversy about his sex life is a case in point. The Congressmen are over-eager to do anything if the name 'Gandhi' is involved. For them it does not matter whether it is the original Gandhi or duplicate. The biggest disservice we do to Gandhi is to deify him. The moment we do so he ceases to be a man and what is so great about a God being able to do anything including getting independence for a country? Gandhi was a man and he achieved what he did despite being only a man. He may have had his own faults and foibles. So be it. After all he was a man like you and me. Then why this fuss?

The same over-enthusiasm of the Congressmen was in evidence in good measure when the irrepressible Shashi Tharoor came up with a repartee to the Kerala CM's comparison of Rahul Gandhi to an Amul Baby. His tweet did not go down well with the dyed-in-the-wool Congressmen for whom only set eulogies are acceptable. What Tharoor does not understand is that his nuanced humour in English is too much for the foot soldiers of the Congress whose very identity and livelihood depends entirely in pleasing those in the Gandhi household.

The flavour of the season is Cricket. And why not? We have just won the World Cup and the players are busy now making their fortune in the IPL. If Indians are accused of excesses I, for one, will not object. If we lose a Tournament we hunt down the players and haunt them. If we win we go to the other extreme. The BCCI started the ball rolling by announcing a booty of Rupees One Crore for each player (this was later increased to Two Crores when the players almost threatened to go on strike). Every State true to the competitive spirit of the game announced its own contributions. What largesse and at whose expense? But then whose money is it anyway? Every politician wants to have credit for the World Cup victory – if you cannot participate in the game, participate in the celebrations ! What a vicarious pleasure. Anyone daring to object is either unpatriotic or is accused of un-sportsman like behaviour.

Thank you.

Venkat R Venkitachalam

May - 2011

1

Finance Bill has been approved by Parliament and has been given assent by Hon'ble President thereby it has

thbecome enactment w.e.f. 8 April 2011.

During the budget, definition of Input Services is totally changed and therefore, the doubts have been raised across w.r.t entitlement of Cenvat Credit on input services and therefore, attempt has been made to analyse the legal provisions.

Input Service has been defined as-

(l) “input service” means any service, -

(i) used by a provider of taxable service for providing an output service; or

(ii) used by a manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products upto the place of removal, and includes services used in relation to modernization, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion, market research, storage upto the place of removal, procurement of inputs, accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, security, business exhibition, legal services, inward transportation of inputs or capital goods and outward transportation upto the place of removal; but excludes services,-

(A) specified in sub-clauses (p), (zn), (zzl), (zzm), (zzq), (zzzh) and (zzzza) of clause (105) of section 65 of the Finance Act (hereinafter referred as specified services), in so far as they are used for-

(a) construction of a building or a civil structure or a part thereof; or

(b) laying of foundation or making of structures for support of capital goods, except for the provision of one or more of the specified services; or

(B) specified in sub-clauses (d), (o), (zo) and (zzzzj) of clause (105) of section 65 of the Finance Act, in so far as they relate to a motor vehicle except when used for the provision of taxable services for which the credit on motor vehicle is available as capital goods; or

(C) such as those provided in relation to outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, membership of a club, health and fitness centre, life insurance, health insurance and travel benefits extended to employees on vacation such as Leave or Home Travel Concession, when such services are used primarily for personal use or consumption of any employee;

The definition can be divided into 3 categories, mainly,

1. Category A - Services used directly or indirectly in relation to manufacture and clearance of excisable goods up to place of removal.

2. Category B - Inclusive

3. Category C - Specific exclusions

Therefore, first category is specified as

(i) used by a provider of taxable service for providing an output service; or

(ii) used by a manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products upto the place of removal

Second category is for “inclusive” services used in relation to modernisation, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion, market research, storage up to the place of removal, procurement of inputs, accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, security, business exhibition, legal services, inward transportation of inputs or capital goods and outward transportation upto the place of removal;

Third category of “Specific exclusions” is specified as “but excludes-

)(A) specified in sub-clauses (p), (zn), (zzl), (zzm), (zzq), (zzzh) and (zzzza) of clause (105) of section 65 of the Finance Act (hereinafter referred as specified services), in so far as they are used for-

(i) construction of a building or a civil structure or a part thereof; or

— By CMA A. B. Nawal

May - 2011

2

Entitlement of Cenvat Credit of

various Input Services

functions” for entitlement of Cenvat Credit. However, it is recommended that such expenses should be considered by the service provider and charge the Service Tax considering the value inclusive of such reimbursement /expenditure which is otherwise also to be included in determining taxable value of services in accordance with “Service Tax (Determination of Value) Rules, 2006”. However, department may raise dispute on the expenditure or the reimbursement in connection with / or in relation with services availed for use of the person even though the same may be for business purpose.

As far as exclusion categories are concerned, there is absolute clarity on the following excluded services

A) Architect Services, Architect, Port & other Port Services, Airport Authorities, Commercial & Industrial Construction, Construction of complex, Execution of Works Contract used in relation to construction of a building or a civil structure or a part thereof, laying of foundation or making of structures for support of capital goods.

(B) such as those provided in relation to outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, membership of a club, health and fitness center, life insurance, health insurance and travel benefits extended to employees on vacation such as Leave or Home Travel Concession, when such services are used primarily for personal use or consumption of any employee.

Consumed has been defined in the “Shorter Oxford English Dictionary Volume 1 as “to use up, to eat up, to drink up or to destroy or to accomplish or to complete”. However it has been stated in the Corpus Secundam Vol. 16 Page 1523 that the word “consumed” does not necessarily mean eat up or destruction but may often thus contemplate the ultimate use to which all intermediate ones lead.

Personal use means “private use”. Person includes a corporation, so goods purchased for a corporation could be goods purchased for the personal use of corporation as decided by the Bombay High Court (158-IC-703:1935 & 415:37 LR 703). It has been held by Honourable Tribunal in the case of Anand Jaisal v/s. CCE (1988 (37) ELT 320) that a VCR which has been cleared as baggage, on payment of duty, as it is used by proprietor in his business of running videotorium. It has to be considered as personal use and not as used for commercial purpose. Therefore, in view of the above, there may be some disputes for certain services even though it may relate to inclusive services used for the business.

We give below the categories of services and our opinion w.r.t entitlement of Cenvat Credit considering new definition of input services.

(ii) laying of foundation or making of structures for support of capital goods, except for the provision of one or more of the specified services; or

(B) specified in sub-clauses (d), (o), (zo) and (zzzzj) of clause (105) of section 65 of the Finance Act, in so far as they relate to a motor vehicle except when used for the provision of taxable services for which the credit on motor vehicle is available as capital goods; or

(C) such as those provided in relation to outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, membership of a club, health and fitness centre, life insurance, health insurance and travel benefits extended to employees on vacation such as Leave or Home Travel Concession, when such services are used primarily for personal use or consumption of any employee.

There will be no disputes w.r.t services utilized whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products up to the place of removal or used by a provider of taxable service for providing an output service since it can be related to each other in almost all the cases, except few cases like telephone.

The second category, there may be some disputes in relating the services w.r.t inclusive functions such as

1. advertisement or sales promotion,

2. market research

3. business exhibition

4. procurement of inputs

5. and the services utilized by persons / representatives / employees in relation to the functions as stated in “inclusive” definition e.g. reimbursement of travel of auditors by air - whether can be considered services utilized for performing auditing function or can be treated as services are used primarily for personal use.

Though it can be argued, exclusion is only for services which are used primarily for personal use or consumption for employees or the perquisites or benefits offered to employees for their personal use or compensated by the company which has no relationship with business of the company and normally required to be considered while calculating the TDS for salary and issuing Form 16. Any services for personal use cannot be treated as business expenditure and if it is accepted as business expenditure as per Indian Accounting Standard or under IFRS or any other generally accepted Accounting Standards, then it should be considered as “business purpose” and to be linked with “inclusive

May - 2011

3

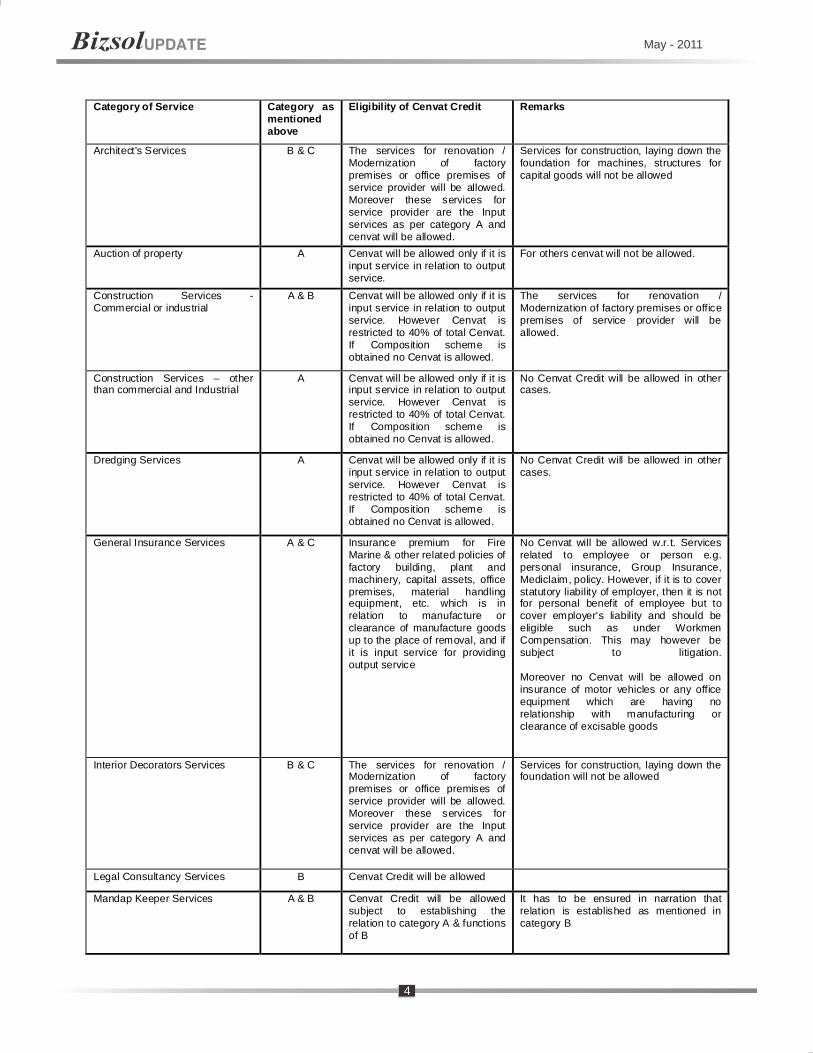

Category of Service Category as mentioned above

Eligibility of Cenvat Credit Remarks

Architect's Services B & C The services for renovation / Modernization of factory premises or office premises of service provider will be allowed. Moreover these services for service provider are the Input services as per category A and cenvat will be allowed.

Services for construction, laying down the foundation for machines, structures for capital goods will not be allowed

Auction of property A Cenvat will be allowed only if it is input service in relation to output service.

For others cenvat will not be allowed.

Construction Services - Commercial or industrial

A & B Cenvat will be allowed only if it is input service in relation to output service. However Cenvat is restricted to 40% of total Cenvat. If Composition scheme is obtained no Cenvat is allowed.

The services for renovation / Modernization of factory premises or office premises of service provider will be allowed.

Construction Services – other than commercial and Industrial

A Cenvat will be allowed only if it is input service in relation to output service. However Cenvat is restricted to 40% of total Cenvat. If Composition scheme is obtained no Cenvat is allowed.

No Cenvat Credit will be allowed in other cases.

Dredging Services A Cenvat will be allowed only if it is input service in relation to output service. However Cenvat is restricted to 40% of total Cenvat. If Composition scheme is obtained no Cenvat is allowed.

No Cenvat Credit will be allowed in other cases.

General Insurance Services A & C Insurance premium for Fire Marine & other related policies of factory building, plant and machinery, capital assets, office premises, material handling equipment, etc. which is in relation to manufacture or clearance of manufacture goods up to the place of removal, and if it is input service for providing output service

No Cenvat will be allowed w.r.t. Services related to employee or person e.g. personal insurance, Group Insurance, Mediclaim, policy. However, if it is to cover statutory liability of employer, then it is not for personal benefit of employee but to cover employer's liability and should be eligible such as under Workmen Compensation. This may however be subject to litigation. Moreover no Cenvat will be allowed on insurance of motor vehicles or any office equipment which are having no relationship with manufacturing or clearance of excisable goods

Interior Decorators Services B & C The services for renovation / Modernization of factory premises or office premises of service provider will be allowed. Moreover these services for service provider are the Input services as per category A and cenvat will be allowed.

Services for construction, laying down the foundation will not be allowed

Legal Consultancy Services B Cenvat Credit will be allowed

Mandap Keeper Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

May - 2011

4

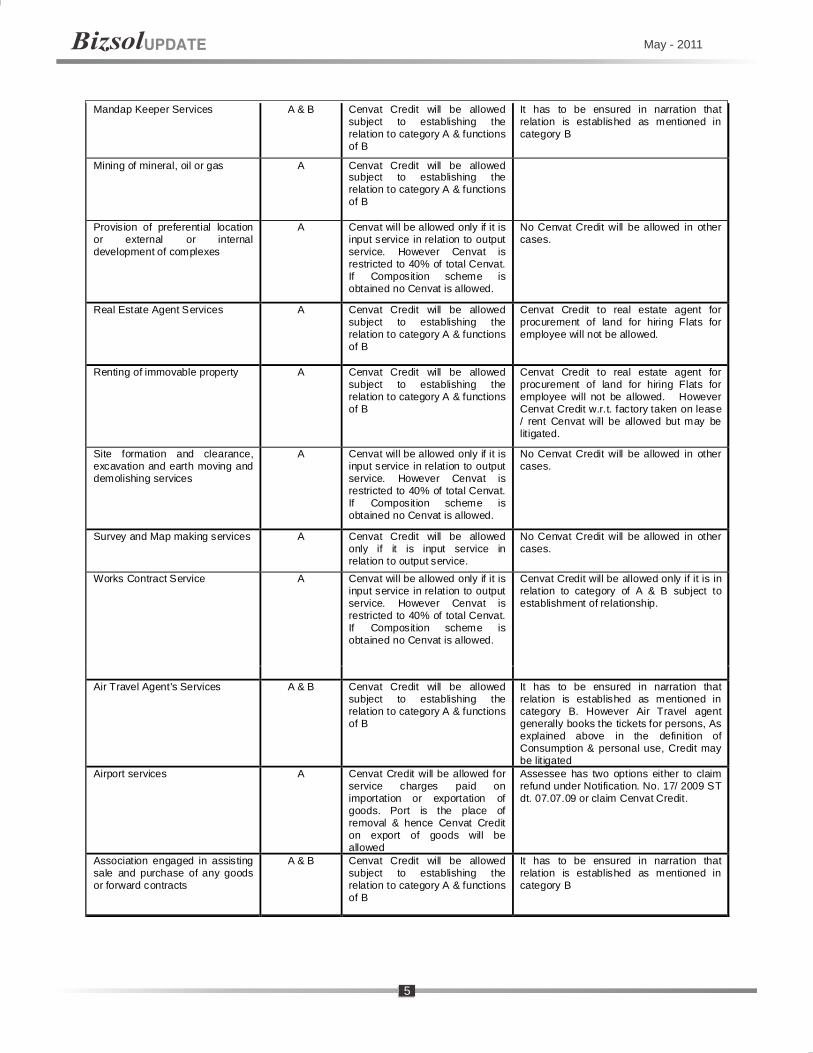

Mandap Keeper Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

Mining of mineral, oil or gas A Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Provision of preferential location or external or internal development of complexes

A Cenvat will be allowed only if it is input service in relation to output service. However Cenvat is restricted to 40% of total Cenvat. If Composition scheme is obtained no Cenvat is allowed.

No Cenvat Credit will be allowed in other cases.

Real Estate Agent Services A Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Cenvat Credit to real estate agent for procurement of land for hiring Flats for employee will not be allowed.

Renting of immovable property A Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Cenvat Credit to real estate agent for procurement of land for hiring Flats for employee will not be allowed. However Cenvat Credit w.r.t. factory taken on lease / rent Cenvat will be allowed but may be litigated.

Site formation and clearance, excavation and earth moving and demolishing services

A Cenvat will be allowed only if it is input service in relation to output service. However Cenvat is restricted to 40% of total Cenvat. If Composition scheme is obtained no Cenvat is allowed.

No Cenvat Credit will be allowed in other cases.

Survey and Map making services A Cenvat Credit will be allowed only if it is input service in relation to output service.

No Cenvat Credit will be allowed in other cases.

Works Contract Service A Cenvat will be allowed only if it is input service in relation to output service. However Cenvat is restricted to 40% of total Cenvat. If Composition scheme is obtained no Cenvat is allowed.

Cenvat Credit will be allowed only if it is in relation to category of A & B subject to establishment of relationship.

Air Travel Agent's Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B. However Air Travel agent generally books the tickets for persons, As explained above in the definition of Consumption & personal use, Credit may be litigated

Airport services A Cenvat Credit will be allowed for service charges paid on importation or exportation of goods. Port is the place of removal & hence Cenvat Credit on export of goods will be allowed

Assessee has two options either to claim refund under Notification. No. 17/ 2009 ST dt. 07.07.09 or claim Cenvat Credit.

Association engaged in assisting sale and purchase of any goods or forward contracts

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

May - 2011

5

Authorized Service Station Services

C No Cenvat Credit will be allowed since there is specific exclusions

Beauty Treatment services C No Cenvat Credit will be allowed since there is specific exclusions

Business Exhibition Services B It is in relation to sales promotion hence Cenvat Credit is allowed subject to establishing the relationship with the functions mentioned in category B

Cargo Handling services A Cenvat Credit will be allowed for service charges paid on importation or exportation of goods. Port is the place of removal & hence Cenvat Credit on export of goods will be allowed

Assessee has two options either to claim refund under Notf. No. 17/ 2009 ST dt. 07.07.09 or claim Cenvat Credit.

Cleaning Activity Services A Cleaning with respect to category A will be allowed. Cenvat Credit will be allowed even if it is cleaning of container for import or export of goods

In any other case credit will not be allowed

Clearing and forwarding agents services

A Cenvat Credit will be allowed for services paid CFI agents or CHA since warehouse is also the place of removal.

Commercial Coaching & Training Services

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Services in relation to personnel development which have no relationship with manufacturing will not be eligible for cenvat credit

Convention Services A & B The Convention w.r.t. training & development will be allowed subject to establishing the relationship with category A & functions of category B

It has to be ensured in narration that relation is established as mentioned in category B. However conventions are attended by the persons. As explained above in the definition of Consumption & personal use, Credit may be litigated

Cosmetic and Plastic Surgery Services

C No Cenvat Credit will be allowed since there is specific exclusions

Courier Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

Custom House Agency Services A Cenvat Credit will be allowed for service charges paid on importation or exportation of goods. Port is the place of removal & hence Cenvat Credit on export of goods will be allowed

Assessee has two options either to claim refund under Notf. No. 17/ 2009 ST dt. 07.07.09 or claim Cenvat Credit.

Dry Cleaning Services C There is no specific mention of said service in category C the service for persons / employee hence Cenvat Credit will not be allowed

However if relationship is established with the functions in category A or B Cenvat Credit may be allowed subject to litigation.

May - 2011

6

Erection, Commissioning & Installation Services

A Cenvat will be allowed only if it is input service in relation to output service and if it is related to manufacturing like installation of plant and machinery. However Cenvat is restricted to 40% of total Cenvat. If Composition scheme is obtained no Cenvat is allowed.

Cenvat Credit will be allowed only if it is in relation to category of A & B subject to establishment of relationship.

Event Management Services A & B The Event Management managing the specific event w.r.t. training & development will be allowed subject to establishing relationship with category of A & functions of category B

It has to be ensured in narration that relation is established as mentioned in category B. However conventions are attended by the persons. As explained above in the definition of Consumption & personal use, Credit may be litigated

Fashion Designing Services C There is no specific mention of said service in category C the service for persons / employee hence Cenvat Credit will not be allowed

However if relationship is established with the functions in category A or B Cenvat Credit may be allowed subject to litigation.

Forward Contract Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Health and Fitness Services C No Cenvat Credit will be allowed since there is specific exclusions

Health Checkup and Treatment Services

C No Cenvat Credit will be allowed since there is specific exclusions

Internet Cafe Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Management, Maintenance & Repairs Services

A, B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Management, Maintenance & Repairs Services with respect to motor vehicle will not be allowed

Membership of Club or Association Services

C No Cenvat Credit will be allowed since there is specific exclusions

Other Port Services A Cenvat Credit will be allowed for service charges paid on importation or exportation of goods. Port is the place of removal & hence Cenvat Credit on export of goods will be allowed

Assessee has two options either to claim refund under Notification No. 17/ 2009 ST dt. 07.07.09 or claim Cenvat Credit.

Outdoor Catering Services C No Cenvat Credit will be allowed since there is specific exclusions

Outdoor catering service would be eligible if it is in connection with sales or finance (e.g. sales conference or shareholder's meeting) and have absolute relation with functions of category B. However it may be subject to litigation

Packaging Activity Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B.

May - 2011

7

Pandal or Shamiana Contractor Services

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

Photography Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

Port Services A Cenvat Credit will be allowed for service charges paid on importation or exportation of goods. Port is the place of removal & hence Cenvat Credit on export of goods will be allowed

Assessee has two options either to claim refund under Notf. No. 17/ 2009 ST dt. 07.07.09 or claim Cenvat Credit.

Processing or Clearing House Services

B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Rail Travel Agent's Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B. However Rail Travel agent generally books the tickets for persons, As explained above in the definition of Consumption & personal use, Credit may be litigated

Renting of Cab Scheme operators Services

B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

However Cenvat Credit may litigated considering definition of Consumption & personal use.

Security / Detective Agency Services

B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Sound Recording Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Steamer Agent's Services B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Stock Broker's Services B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Stock Exchange Services B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Storage & Warehousing Services A Cenvat Credit will be allowed subject to relationship with import or export of goods up to warehouse / depot of the Assessee, i.e. Place of removal.

Storage of inputs outside factory premises in a warehouse will also be allowed for cenvat credit

May - 2011

8

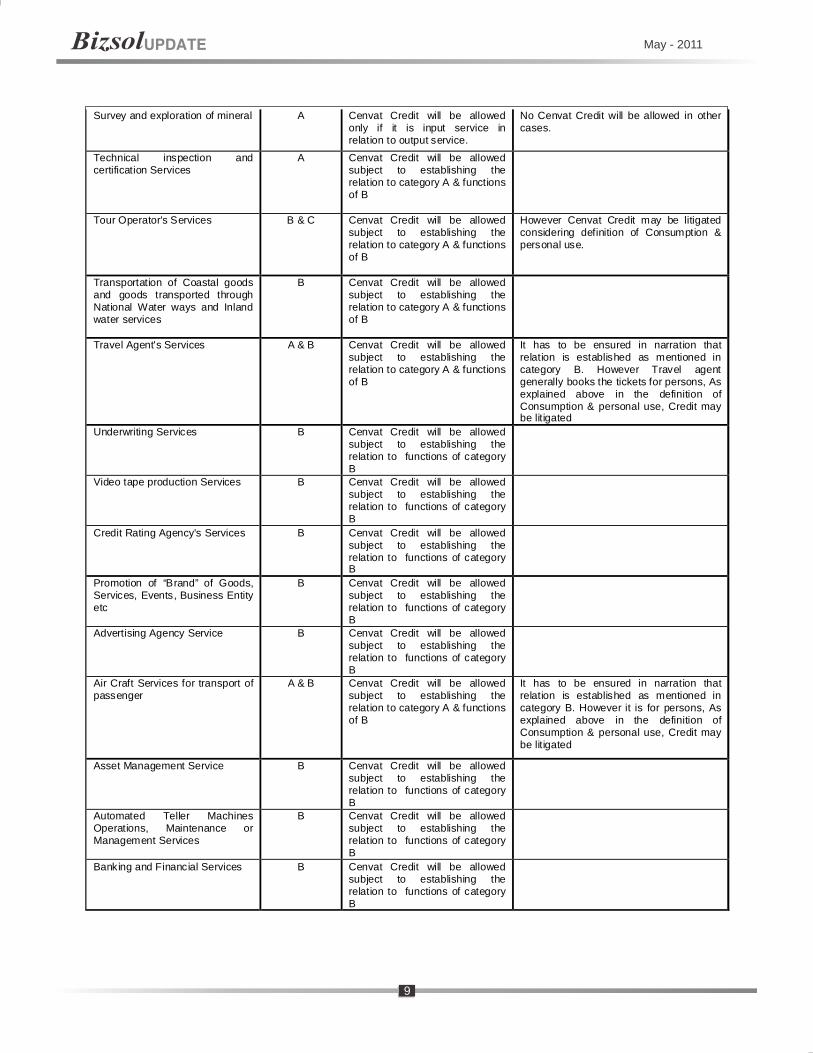

Survey and exploration of mineral A Cenvat Credit will be allowed only if it is input service in relation to output service.

No Cenvat Credit will be allowed in other cases.

Technical inspection and certification Services

A Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Tour Operator's Services B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

However Cenvat Credit may be litigated considering definition of Consumption & personal use.

Transportation of Coastal goods and goods transported through National Water ways and Inland water services

B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Travel Agent's Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B. However Travel agent generally books the tickets for persons, As explained above in the definition of Consumption & personal use, Credit may be litigated

Underwriting Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Video tape production Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Credit Rating Agency's Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Promotion of “Brand” of Goods, Services, Events, Business Entity etc

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Advertising Agency Service B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Air Craft Services for transport of passenger

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B. However it is for persons, As explained above in the definition of Consumption & personal use, Credit may be litigated

Asset Management Service B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Automated Teller Machines Operations, Maintenance or Management Services

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Banking and Financial Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

May - 2011

9

Broadcasting Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Business Auxiliary Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Business Support Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Cable Operator Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Commercial use or exploitation of any event

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Consulting Engineer's Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Copyright Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Credit Card, Debit Card, Charge Card or Other payment card related services

B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

However Cenvat may litigate considering definition of Consumption & personal use.

Design Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Development and supply of contents in Telecom Services etc.

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Electricity Exchanges Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Facsimile Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

Foreigner Exchange Broker B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Franchise Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

May - 2011

10

Hotel, guest house, inn, club or campsite services having tariff Rs 1000/- or more

B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

However Cenvat Credit may be litigated considering definition of Consumption & personal use.

Information Technology Software services

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Input credit on softwares for email communication, anti-virus, business reporting, etc. will be subject to litigation

Insurance Auxiliary Services A & C Insurance premium for Fire Marine & other related policies which is in relation to manufacture or clearance of manufacture goods up to the place of removal, and if it is input service for providing output service

No Cenvat will be allowed w.r.t. Services related to employee or person e.g. personal insurance, Group Insurance, Mediclaim, policy under Workmen Compensation.

Insurance Auxilliary Services concerning Life Insurance Business

A & C Insurance premium for Fire Marine & other related policies which is in relation to manufacture or clearance of manufacture goods upto the place of removal, and if it is input service for providing output service

No Cenvat will be allowed w.r.t. Services related to employee or person e.g. personal insurance, Group Insurance, Mediclaim, policy. However, if it is to cover statutory liability of employer, then it is not for personal benefit of employee but to cover employer's liability and should be eligible such as under Workmen Compensation. This may however be subject to litigation

Intellectual Property Services C Cenvat Credit will not be allowed though there is no specific exclusion in category C, generally royalty will be paid on sale hence may be considered as post removal activity.

Royalty may not be on sale of goods, but is computed on the value of the goods sold. Royalty is for transferring the rights to manufacture and sale of goods. It may include use of brand name, trade name etc. In some cases it is part of the payment for transferring the know-how. The manufactured products are marketed under the brand name. Cenvat is entitled but will be subject to definite litigation

Internet TelecommunicationServices

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Leased Circuit Services A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Life Insurance Services C No Cenvat Credit will be allowed since there is specific exclusions

Mailing List Compilation & Mailing Services

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

It has to be ensured in narration that relation is established as mentioned in category B

Management Consultant'sServices

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

May - 2011

11

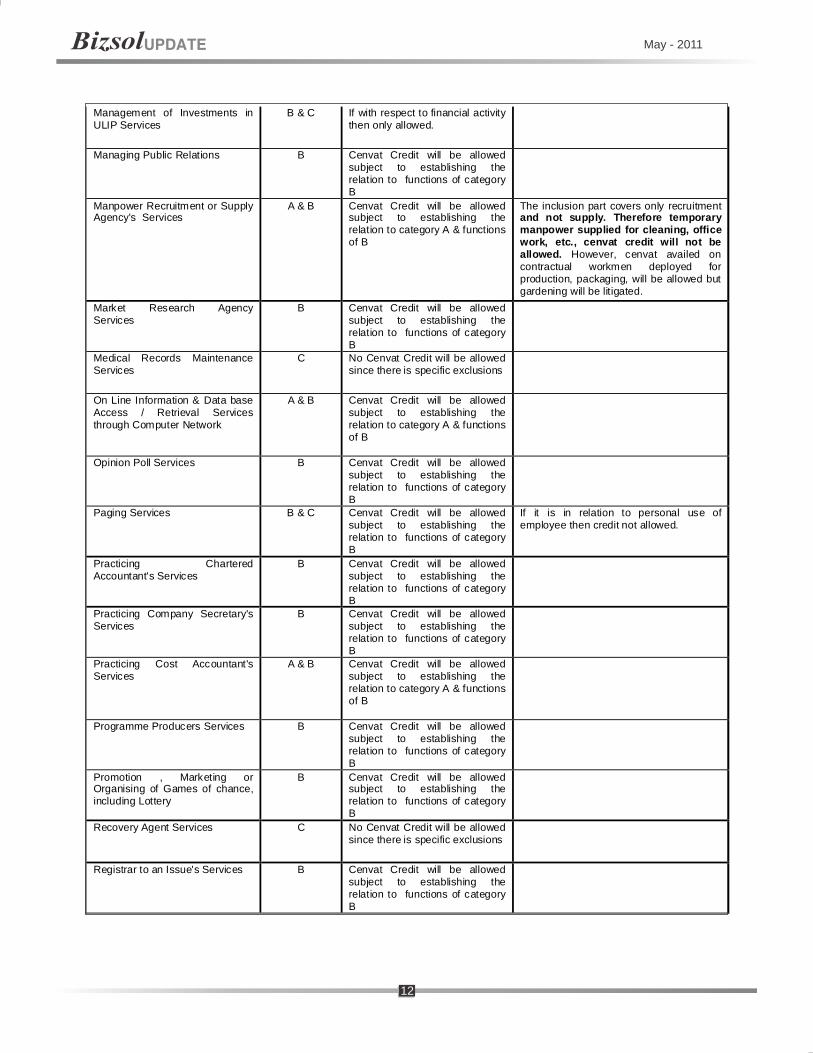

Management of Investments in ULIP Services

B & C If with respect to financial activity then only allowed.

Managing Public Relations B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Manpower Recruitment or Supply Agency's Services

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

The inclusion part covers only recruitment and not supply. Therefore temporary manpower supplied for cleaning, office work, etc., cenvat credit will not be allowed. However, cenvat availed on contractual workmen deployed for production, packaging, will be allowed but gardening will be litigated.

Market Research Agency Services

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Medical Records Maintenance Services

C No Cenvat Credit will be allowed since there is specific exclusions

On Line Information & Data base Access / Retrieval Services through Computer Network

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Opinion Poll Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Paging Services B & C Cenvat Credit will be allowed subject to establishing the relation to functions of category B

If it is in relation to personal use of employee then credit not allowed.

Practicing CharteredAccountant's Services

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Practicing Company Secretary's Services

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Practicing Cost Accountant's Services

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Programme Producers Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Promotion , Marketing or Organising of Games of chance, including Lottery

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Recovery Agent Services C No Cenvat Credit will be allowed since there is specific exclusions

Registrar to an Issue's Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

May - 2011

12

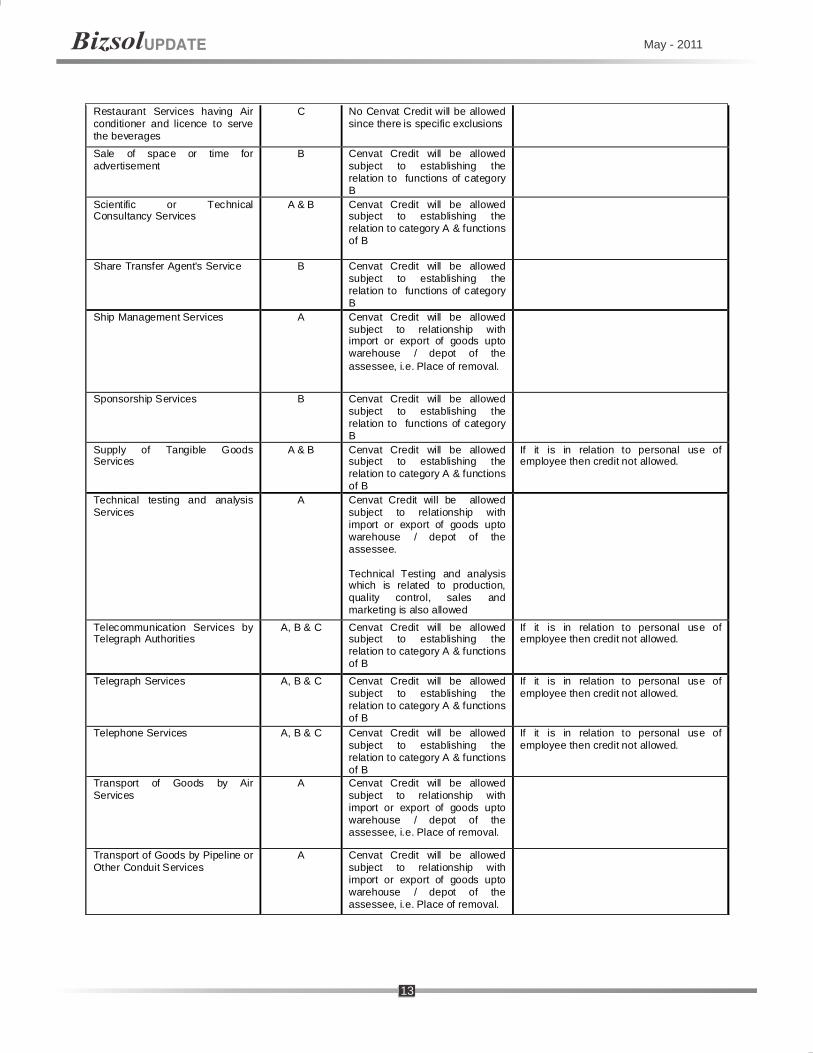

Restaurant Services having Air conditioner and licence to serve the beverages

C No Cenvat Credit will be allowed since there is specific exclusions

Sale of space or time for advertisement

B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Scientific or TechnicalConsultancy Services

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

Share Transfer Agent's Service B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Ship Management Services A Cenvat Credit will be allowed subject to relationship with import or export of goods upto warehouse / depot of the assessee, i.e. Place of removal.

Sponsorship Services B Cenvat Credit will be allowed subject to establishing the relation to functions of category B

Supply of Tangible Goods Services

A & B Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

If it is in relation to personal use of employee then credit not allowed.

Technical testing and analysis Services

A Cenvat Credit will be allowed subject to relationship with import or export of goods upto warehouse / depot of the assessee. Technical Testing and analysis which is related to production, quality control, sales and marketing is also allowed

Telecommunication Services by Telegraph Authorities

A, B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

If it is in relation to personal use of employee then credit not allowed.

Telegraph Services A, B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

If it is in relation to personal use of employee then credit not allowed.

Telephone Services A, B & C Cenvat Credit will be allowed subject to establishing the relation to category A & functions of B

If it is in relation to personal use of employee then credit not allowed.

Transport of Goods by Air Services

A Cenvat Credit will be allowed subject to relationship with import or export of goods upto warehouse / depot of the assessee, i.e. Place of removal.

Transport of Goods by Pipeline or Other Conduit Services

A Cenvat Credit will be allowed subject to relationship with import or export of goods upto warehouse / depot of the assessee, i.e. Place of removal.

May - 2011

13

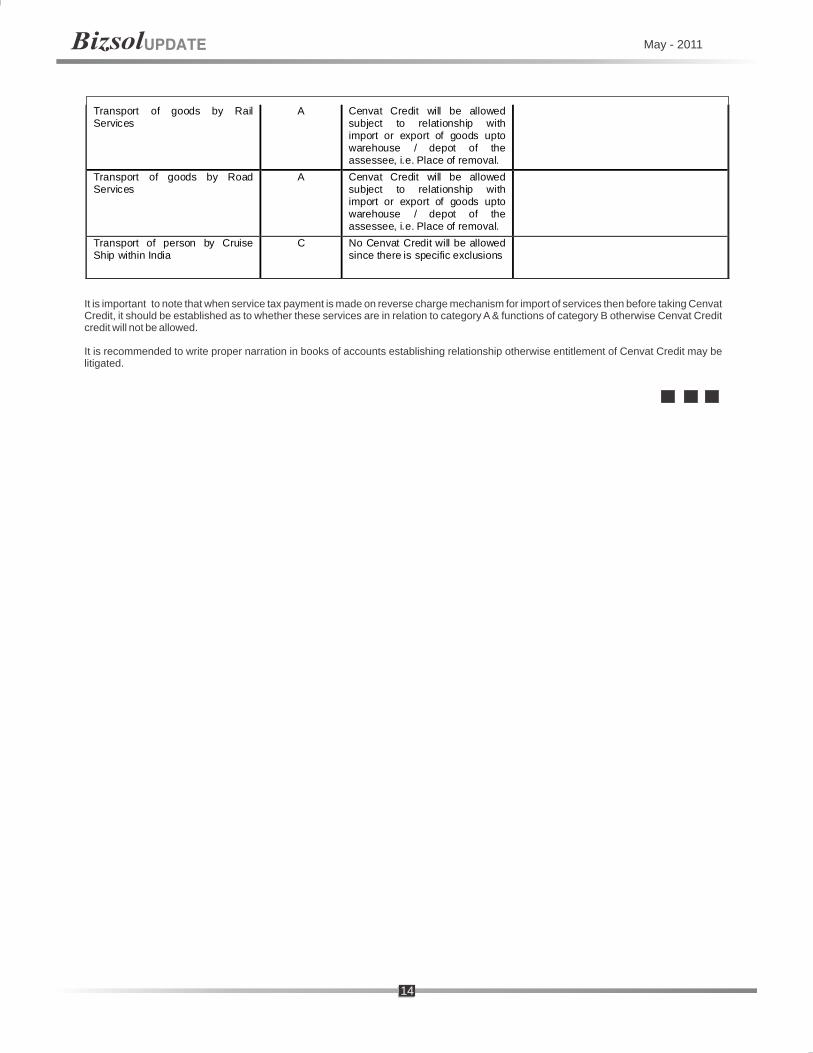

Transport of goods by Rail Services

A Cenvat Credit will be allowed subject to relationship with import or export of goods upto warehouse / depot of the assessee, i.e. Place of removal.

Transport of goods by Road Services

A Cenvat Credit will be allowed subject to relationship with import or export of goods upto warehouse / depot of the assessee, i.e. Place of removal.

Transport of person by Cruise Ship within India

C No Cenvat Credit will be allowed since there is specific exclusions

It is important to note that when service tax payment is made on reverse charge mechanism for import of services then before taking Cenvat Credit, it should be established as to whether these services are in relation to category A & functions of category B otherwise Cenvat Credit credit will not be allowed.

It is recommended to write proper narration in books of accounts establishing relationship otherwise entitlement of Cenvat Credit may be litigated.

May - 2011

14

— By CMA A. B. Nawal

During the Budget discussion, Honorable Finance Minister, Shri Pranab Mukherjee hinted that he had appreciated the concerns w.r.t Point of Taxation Rules, st st2011 and promised that implementation thereof can be postponed to 1 July 2011. However, on 31 March 2011, number of notifications have been issued

changing the provision of Point of Taxation Rules, 2011 as well as amending the provisions of Cenvat Credit Rules, 2004 and thereby in the attempt of simplification, number of options have been provided and therefore, the attempt has been made in this article to provide comparative provisions prior to

stBudget and present provisions w.e.f 1 April 2011 on the issues of Cenvat Credit & Service Tax.

Service Tax – Point of Taxation & Cenvat Entitlement

FREQUENTLY ASKED QUESTIONS Sr. No.

Frequently Asked Questions

Practice /Provisions prior to Budget

Present Provision w.e.f 1st April 2011

For Non-Continuous Service

1 What is Point of Taxation?

Though there was no Point of Taxation Rules, there was a provision to raise the invoice within 14 days from the provision of services or payment received, whichever is earlier

Completion of service

Raising of invoice

Payment Point of taxation

For Individual Partnership / Proprietorship providing services with related to Architect, Interior Decorators, Practicing Chartered Accountants, Practicing Cost Accountants, Practicing Company Secretaries, Legal Consultancy Services, Scientific or Technical Services

Export of Services

Services under Reverse Charge Mechanism like GTA, Import of Services, Sponsorships, Mutual Fund & Insurances

Associated Enterprises

For Other Categories

May

- 2

011

15

May

- 2

011

16

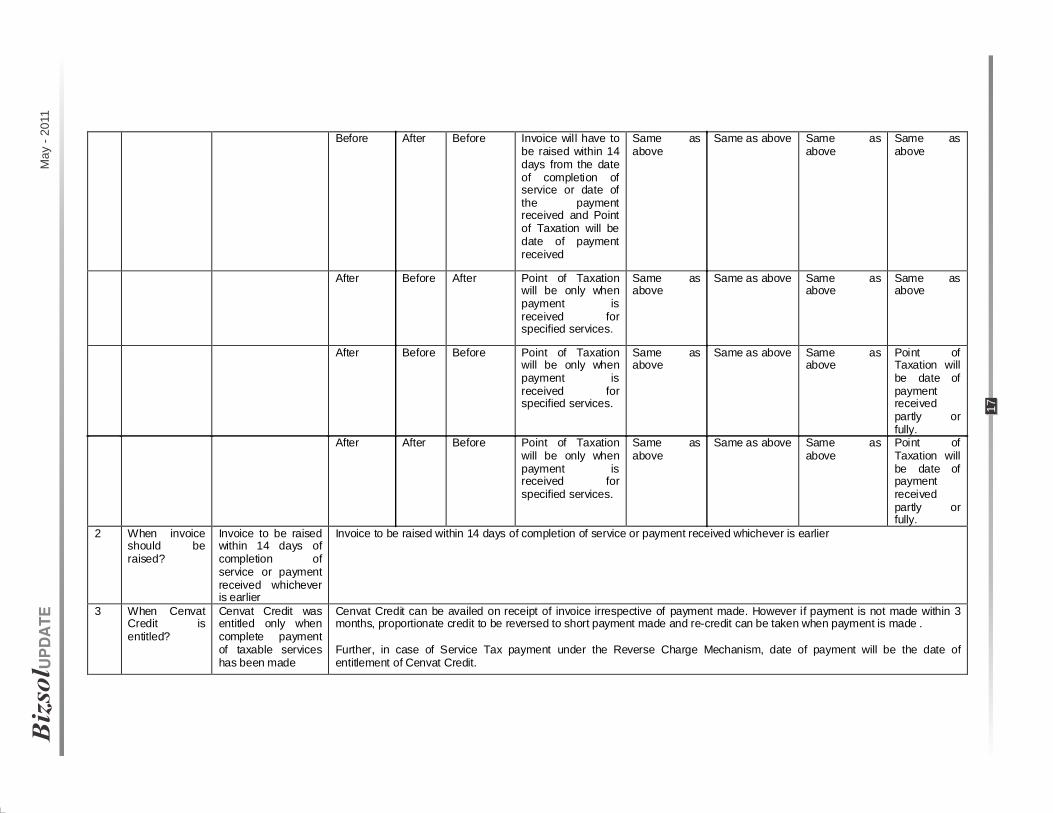

Before After After Point of Taxation will be only when payment isreceived forspecified services.

Point ofTaxation will be when payment is received. Therefore, when rebate claim is being filed, Point of Taxation will be when payment is received. However, if payment is not received within specified time limit of RBI then the Point ofTaxation will be raising of invoice and Service Tax will have to be paid with interest

Point ofTaxation is the date ofpayment. However if payment is not made within six months then Point of Taxation will be from the date ofreceiving the invoice and Service Tax will have to be paid along with interest.

If services are provided to Associate Enterprises within India then Point of Taxation will be completion of services / invoice. However, it is option either to make iteffective from 1st April 2011 or 1st July 2011. However, if services are provided to Associated Enterprises which arelocated outside of India, then Point ofTaxation will be date of credit in the books ofservice availers or the date of making payment, whichever is earlier.

Point ofTaxation will be completion of services / invoice. If invoice is not raised with 14 days, Point ofTaxation will be invoice or payment whichever is earlier. However, it is option either to make it effective from 1st April 2011 or 1st July 2011.

Before Before After Same as above Same as above

Same as above Same asabove

Same as above

Before After Before Invoice will have to be raised within 14 days from the date of completion of service or date of the paymentreceived and Point of Taxation will be date of payment received

Same as above

Same as above Same asabove

Same as above

After Before After Point of Taxation will be only when payment isreceived forspecified services.

Same as above

Same as above Same asabove

Same as above

After Before Before Point of Taxation will be only when payment isreceived forspecified services.

Same as above

Same as above Same asabove

Point ofTaxation will be date of payment received partly or fully.

After After Before Point of Taxation will be only when payment isreceived forspecified services.

Same as above

Same as above Same asabove

Point ofTaxation will be date of payment received partly or fully.

2 When invoice should beraised?

Invoice to be raised within 14 days of completion ofservice or payment received whichever is earlier

Invoice to be raised within 14 days of completion of service or payment received whichever is earlier

3 When Cenvat Credit isentitled?

Cenvat Credit was entitled only when complete payment of taxable services has been made

Cenvat Credit can be availed on receipt of invoice irrespective of payment made. However if payment is not made within 3 months, proportionate credit to be reversed to short payment made and re-credit can be taken when payment is made . Further, in case of Service Tax payment under the Reverse Charge Mechanism, date of payment will be the date of entitlement of Cenvat Credit.

May

- 2

011

17

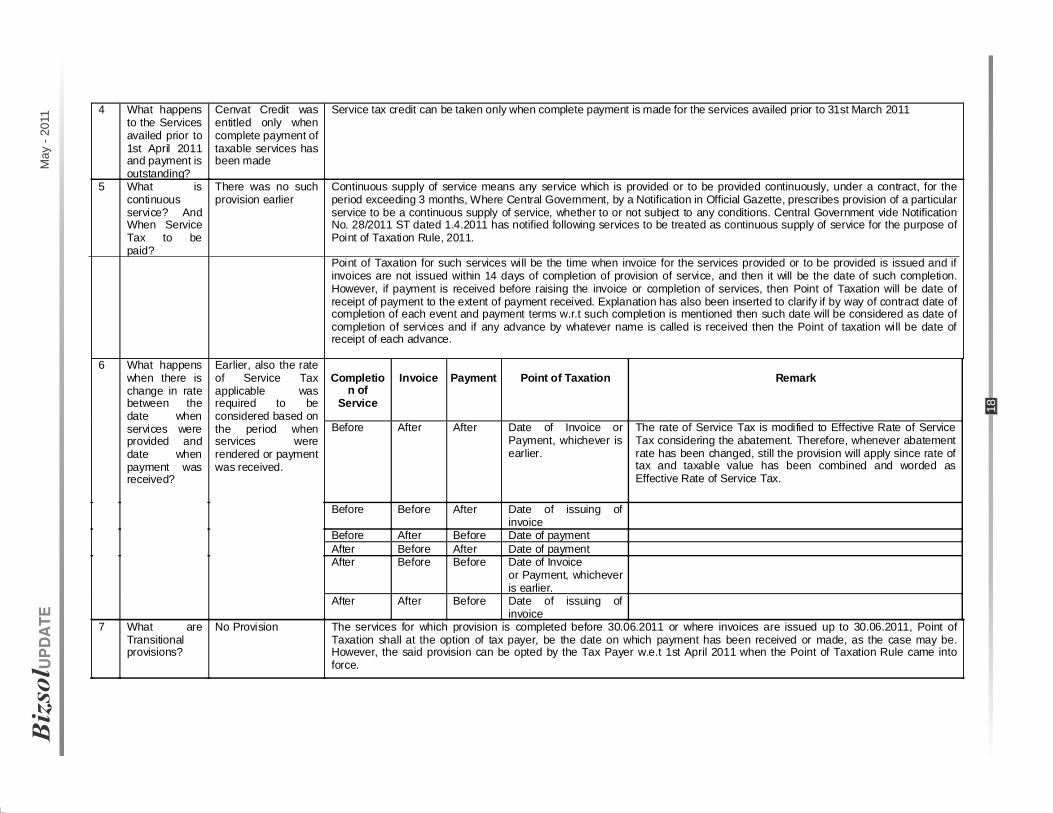

4 What happens to the Services availed prior to 1st April 2011 and payment is outstanding?

Cenvat Credit was entitled only when complete payment of taxable services has been made

Service tax credit can be taken only when complete payment is made for the services availed prior to 31st March 2011

5 What iscontinuous service? And When Service Tax to be paid?

There was no such provision earlier

Continuous supply of service means any service which is provided or to be provided continuously, under a contract, for the period exceeding 3 months, Where Central Government, by a Notification in Official Gazette, prescribes provision of a particular service to be a continuous supply of service, whether to or not subject to any conditions. Central Government vide Notification No. 28/2011 ST dated 1.4.2011 has notified following services to be treated as continuous supply of service for the purpose of Point of Taxation Rule, 2011. Point of Taxation for such services will be the time when invoice for the services provided or to be provided is issued and if invoices are not issued within 14 days of completion of provision of service, and then it will be the date of such completion. However, if payment is received before raising the invoice or completion of services, then Point of Taxation will be date of receipt of payment to the extent of payment received. Explanation has also been inserted to clarify if by way of contract date of completion of each event and payment terms w.r.t such completion is mentioned then such date will be considered as date of completion of services and if any advance by whatever name is called is received then the Point of taxation will be date of receipt of each advance.

6 What happens when there is change in rate between the date when services were provided and date when payment was received?

Earlier, also the rate of Service Tax applicable wasrequired to be considered based on the period when services wererendered or payment was received.

Completio

n of Service

Invoice

Payment

Point of Taxation

Remark

Before After After Date of Invoice or Payment, whichever is earlier.

The rate of Service Tax is modified to Effective Rate of Service Tax considering the abatement. Therefore, whenever abatement rate has been changed, still the provision will apply since rate of tax and taxable value has been combined and worded as Effective Rate of Service Tax.

Before Before After Date of issuing of invoice

Before After Before Date of payment After Before After Date of payment After Before Before Date of Invoice

or Payment, whichever is earlier.

After After Before Date of issuing of invoice

7 What areTransitional provisions?

No Provision The services for which provision is completed before 30.06.2011 or where invoices are issued up to 30.06.2011, Point of Taxation shall at the option of tax payer, be the date on which payment has been received or made, as the case may be. However, the said provision can be opted by the Tax Payer w.e.t 1st April 2011 when the Point of Taxation Rule came into force.

May

- 2

011

18

May

- 2

011

19

8 How the value of the services to bedetermined by Banking & financial Institution and Foreign Exchange Broker inrelation tomoney changing and what will be rate of tax?

Gross amount of currency exchange was the taxable value and rate of tax was 0.25%

Difference between buying rate and selling rate with reference to RBI Reference Rate at particular time of money exchange will be the taxable value and rate of tax will be 0.01% of gross amount of currency exchange up to Rs. 1 lac subject to minimum amount of Rs. 25,000/- or Rs. 100/- and 0.5% if the amount of gross amount exchange is between Rs. 1lac to Rs. 10 lacs or Rs. 550/- & 0.01% if amount of gross amount exchange exceeding Rs. 10lacs and amount of Service Tax will be maximum Rs. 5,000/-

9 How valuation of exempted services i.e. trading to be considered while reversal of Cenvat credit under Rule 6 (3) when exempted service ortaxable service or exempted goods and excisable goods are produced?

No such provision Value of exempted service w.r.t traded goods will be difference between sale price (-) cost of goods based on generally accepted Accounting Principles without including the expenses incurred towards their purchase or 10% of the cost of goods sold , whichever is more.

10 Whether Cenvat Credit can be availed on supplementary invoice, bill or challan for differential Service Tax?

Though there was no specificprovision, it was entitled.

Now, it has been restricted only in case when differential Service Tax is not paid by reason of fraud, collusion or willful misstatement or contravention of any of the provision of Finance Act or the rules made thereunder with intend to evade Service Tax.

It can be observed from the above that one have to be more vigilant for discharging the Service Tax liability and also availment of Cenvat credit on invoices received

from Service Provider or under Reverse Charge Mechanism. There has to be mechanism of internal control so as to be 100% statutory compliant.

The title to this piece may look presumptuous and opinionated – presumptuous because it is futuristic in nature and opinionated because it is not supported by any empirical data to warrant some far-reaching predictions. Be that as it may, let us look at what is in store in the decade that has just now started unravelling itself. However, before doing the crystal- gazing it may be in order to place on record some caveats. Every decade, year or for that matter any period in time looks a defining one with or without compelling reasons. However, for the sheer pace and nature of change the immediate future looks much more impactful than any before. Looking back, there was an element of certainty about even the uncertainties. But no more. The shape and size of events taking place these days leave one breathless and amazed.

Gone are the days of a bipolar world in which the US and the USSR laid down the rules of the geo-political games. Just as everyone was settling down to a world ruled by a single super power, fault lines have started emerging in its ability to lord over the world. The very phrase world view had become a euphemism for American opinion. Over the years America had become a land of opportunists just because it indeed was a land of opportunities. The recent economic meltdown there has hurt its ability to sustain the self-acquired burden of the world. The Jasmine Revolution in the Middle East would turn out to be watershed event in the process of unravelling of the American role on the world stage. One by one the kingdoms, sheikhdoms and the fiefdoms of the Middle East are crumbling. All these autocrats or despots owed their allegiance to American support for their very survival. The US has been put in a piquant situation when it is being called upon to support either the ruler or the ruled. Political convenience favoured the former but allegiance to democracy demanded that it supported the latter. Come to think of it, here is an event not planned or prepared for by the US. Imagine a major revolution taking place without a CIA hand! In all these the ability of America to dictate terms in the new world order is bound to diminish. That is bound to be a major earth-shaking event in the new decade.

In the past whenever anyone in India spoke of globalisation it was always from an 'inside-out' perspective - more in the nature of we taking the option of integrating ourselves with the world. Even if we had not taken that option this integration would any case have taken place. It would have been impossible for us to be insulated by the volatile world events like what is happening in the Middle East.

Volatile oil prices and fast changing technologies would have made us look to the outside world and change ourselves. As if that is not enough the climate-change phenomena and the resultant adjustments that we are called upon to make would have exerted enormous pressure on us to be part of the world stage. The recent global economic slowdown serves as a grave reminder to us about the need and necessity of getting integrated with the rest of the world. The one prediction on which few people differ is the inevitability of China becoming the numero uno economy of the world. The moot question here is whether the country would continue to be an oxymoron with 'controlled capitalism'.

It is not only in the global macro terrain that we will see changes in this decade. Closer home the changes which will come to visit us in the current decade will be much more far reaching than any in the past. Let us look at some of the important ones.

The decade beginning with 1991 came to be known as the shining example of what economic reforms can do for a country like India. The reforms may have started out of compulsion and today it is a testimony to the world as to what free economy and unbridled entrepreneurial spirit can do to a country. However, after the initial success of the economic reforms there has been quite a lull when politics hijacked economics. However, a wave of second generation reforms are about to be ushered in with the introduction Goods and Services Tax, the new Tax Code and the mandating of IFRS for large organisations. Current political opposition notwithstanding, these are bound to be implemented whoever will be in the Government. The process may be slow but the outcome is a certainty.

Though people may shy away from articulating the consequences of terrorism in the sub continent, one cannot wish away the impact it will have on the politics and economy of this country. For the coming decade this may be the single most important factor which will affect the country's future. The success and failure of any Government in the country will depend on how it handles this one factor. With the ever changing geo-politics and the growth in ideological fanaticism, the chances of fringe elements taking centre stage in India is far more real today. By definition democracy is a breeding ground for fanatical ideologies in the name of nationalism or religion.

It may look natural that a country's standard of corruption is measured by the number of scandals

May - 2011

20

A DEFINING DECADE IN THE MAKING

While it is an opportunity, it will also prove to be a challenge to those in power. Before leaving the topic of Politics one cannot but be aware of one universal truth. Capitalism and more so crony capitalism bring in a big chasm between the 'haves' and the 'have-nots'. If recent indications are anything to go by there is enough evidence in the country where obscene display of wealth does not meet with enough criticism. The romance with Communism begins here. Despite the experience to the contrary, it would be easy for those who have been deprived to fall prey to some form of socialistic posturing. The Communists, even if they lose the coming state elections, can take heart in the fact that things could change in their favour and much of it will be in evidence by the time this decade runs out.

Expectations of a better standard of living with decent civic amenities, robust infrastructure, caring healthcare, etc. may be too obvious to state. Moreover it will also be recurring themes for any Government for any period in time. Even those who do not subscribe to the view that the Naxal movement is essentially a manifestation of lopsided development of better part of India would readily agree that these would definitely alleviate the suffering of the masses in the undeveloped regions and also at the same time alienate them from the Naxals. Incidentally containment of the Naxal movement would be top of the Agenda for both Central and State Governments and would indeed be a major challenge in the decade ahead.

The list of Challenges and Opportunities in the coming decade could be endless. Many of them could be common to any developing economy and it could even look daunting. However, in the case of India hope stems from the fact that few people had expected an invitation to India to the high table with the comity of nations as a shining example of development even a decade earlier. The unthinkable has happened and we are proud of it. That should give us the hope and confidence in the coming decade to do even better. While signing off one cannot but rue the fact that at the beginning of this decade there are very few idols still left standing. All those who stood tall at the beginning the previous decade are now mired in corruption and corporate governance issues. The list includes politicians, industrialists, bureaucrats, artistes, et al. Let us hope that this does not happen when we take a review at the end of this decade.

Thank you.

Venkat R Venkitachalam

Courtesy “Footprints”

and scams which come out of the cupboards kept in the corridors of power. Strangely however, it may not be true. Everyone in India knew and at the same time did nothing about it when it came to corruption. With more and more skeletons tumbling out and more and more names dragged into the mud, it is quite natural to assume that ours is a corrupt society. We already know about it. But what is new is that here there is chance to do something about it by bringing the culprits to book. All those who are getting booked for corrupt on are those who have done the crime in the past. What is now important is that at least the names are coming out, albeit not fast enough. There are systemic deficiencies which need to be addressed. If one were to go by the signals emanating all round the chances are that this decade will see something tangible done on this score.

Unlike any time in the past the demographic profile of the country is set to change totally during the coming years. The population of the young and the impatient are about to take charge and take change they will. Age may no longer be mistaken for wisdom any more nor will the youth be patient to pardon the aged for that reason. The demand pull from the youth will create its own pressure points in all spheres of activities – be it politics or the so called morality. Youth power will decide whether Baisakhi is more important to celebrate or Valentine's Day! In fact India is in a crucial phase. There will more people in the earning group than in the non-earning group. History shows that a country grows more in the demographic dividend phase. This will call for imaginative state planning for providing employment opportunities and the ability of the Government to channelise the productive energies of the youth of the country. This by far will be the most formidable challenge to the Government of the day in the coming decade.

A discussion on Politics in India could be a vulnerable issue especially if it is to be interspersed with predictions. Ideologies had never been the weakness of any party in India. An expressed hope that there would be change in this direction any time soon could be termed as utopian. But one cannot run away from reality. Inclusive growth today may be a slogan than a conviction. In an era when 'vote-bank' politics and 'vote-for-freebies' rule the roost, it may even look unattainable. Economic reforms undeniably did achieve growth, though modest. That is not enough anymore. More people will need to be taken above the poverty line and more will need to be empowered. Again it should not be confined to a slogan. The empowerment of the youth and the deprived sections through affirmative action will decide the future of the nation. Much of which will be in evidence in the coming decade.

May - 2011

21

What's New…!!Custom

Tariff :

Ø Basic Custom Duty rate on following goods has been reduced,

ITCHS Description of Goods Duty Rate

2701 Coal having Swelling Index or Crucible NilSwelling Number of 1 and above and mean reflectance of above 0.60, for use in the manufacture of iron or steel using Corex, Finex or PCI technology

8703 Motor cars and other motor vehicles principally designed for the transport of persons (other than those of heading 87.02), including station wagons and racing cars , new, which have not been registered anywhere prior to importation, if imported,-

(1) as a Completely Knocked Down (CKD) kit containing all the necessary components, parts or sub-assemblies, for assembling a complete vehicle,with-

(a) engine, gearbox and transmission 10% mechanism not in a pre-assembled

condition;

(b) engine or gearbox or transmission 30% mechanism in pre-assembled form

but not mounted on a chassis or a body assembly. (2) in any other form. 60%

8711 Motor cycles (including mopeds) and cycles fitted with an auxiliary motor, with or without side cars ,and side cars, new, which have not been registered anywhere prior to importation,-(1) as a Completely Knocked Down (CKD) kit containing all the necessary components, parts or sub-assemblies, for assembling a complete vehicle,with-

(a) engine, gearbox and transmission 10% mechanism not in a pre-assembled condition;

(b) engine or gearbox or transmission 30% mechanism in pre-assembled form, not mounted on a body assembly.

(2) in any other form. 60%

844399 Parts for manufacture of printers falling NILunder heading 8443 32

[CUS NTF NO. 31/2011 DATE 24/03/2011]

Ø Following goods has been exempted from payment of SAD i.e. Custom Duty under Sec 3(5),

Description of Goods ITCHS

Parts for manufacture of printers falling 844399 under heading 8443 32

The following goods, namely:- 847170 or(a) microprocessor for computer, other 847330 or than motherboards; 8523(b) floppy disc drive;(c) hard disc drive(d) CD-ROM Drive;(e) DVD Drive or DVD Writer;(f) Flash memory;(g) Combo drive. Cruise Ships, Boats, Cargo Ships, Barges, 8901ferry-boats etc

Helicopters, aeroplanes etc 8802 (except 8802 60 00)

[CUS NTF NO. 32/2011 DATE 24/03/2011]

Ø Basic Custom Duty will be exempted on following raw Sugar subject to conditions mentioned in the notification,

ITCHS Description of Goods BCD

1701 Raw Sugar Nil

1701 91 00 or Refined or white sugar Nil1701 99 90

1701 Raw sugar if imported by Nila bulk consumer

[CUS NTF NO. 34/2011 DATE 15/04/2011]

May - 2011

22

Ø Drawback amount will not be recovered in case of non realisation of export proceeds subject to following,

a) sale proceeds is compensated by the Export Credit Guarantee Corporation of India Ltd. under an insurance cover and

b) the Reserve Bank of India writes off the requirement of realization of sale proceeds on merits and

c) the exporter produces a certificate from the concerned Foreign Mission of India about the fact of non-recovery of sale proceeds from the buyer. [CUS NTF NO. 30/2011(NT) DATE 11/04/2011]

Ø The tariff rate for brass scrap (all grades) has been revised to Rs. 4272/- Per Metric Ton and for Poppy seeds to Rs. 2745/- Per Metric Ton. [CUS NTF NO. 33/2011(NT) DATE 29/04/2011]

Circulars:

Ø It has been clarified that the exporter is required to declare on the body of the shipping bill under claim of drawback that the goods being exported to Nepal have not been imported into India from third countries and the field formations shall conduct random checking to ensure the genuineness of the exporter’s declaration. [CUS CIR NO. 14/2011 DATE 15/03/2011]

Ø It has been clarified that all packaged/ canned software imported in shrink wrapped packages, will attract Excise duty/CVD on such retail sale price declared being the combined value of the software and the licenses (right to use). Such software will, however, be exempt from payment of service tax under the category ITSS (as provided in Notification

stNo. 53/2010-ST dated 21 December 2010).

On the other hand, such packaged/ canned software, on which affixation of retail sale price is not required under the relevant provisions for the packaged commodities, and the assessment is based therefore, on the value determined under section 4 of the central excise act, 1944, the excise duty/ CVD will be charged only on the value, excluding the value representing consideration for transfer of right to use such packaged/ canned software. However, service tax under the category ITSS would be levied on such portion subsequently. [CUS CIR NO. 15/2011 DATE 18/03/2011]

Ø It has been clarified that some declarations are required to be made by the passengers at the time of arrival at the international airport in Para 7 of the Customs part of Arrival Card for Passengers. [CUS CIR NO. 16/2011 DATE 31/03/2011]

Ø The Finance Bill, 2011 stipulates ‘Self-Assessment’ of Customs duty in respect of imported and export goods by the importer or exporter. This means that while the responsibility for assessment would be shifted to the importer / exporter, the Customs officers would have the power to verify such assessments and make re-assessment, where warranted. The proposed changes shall become effective immediately from the date of enactment of the

Ø Exemption from the payment of additional duty (CVD) in excess of 1% ad valorem has been provided on the fertilisers classified under chapter. [CUS NTF NO. 35/2011 DATE 15/04/2011]

Antidumping Duty Notifications :

Ø Anti-dumping duty on Certain Rubber Chemicals (MBTS) falling under tariff item 2925 20 or 2934 20 or 3812 originating in, or exported from People’s Republic of China has been continued till 25/07/2011. [CUS NTF NO. 28/2011 DATE 04/03/2011]

Ø Anti-dumping duty on Polytetrafluoroethylene (PTFE) falling under heading 39046100 originating in, or exported from People’s Republic of China has been continued till 25/07/2011. [CUS NTF NO. 29/2011 DATE 04/03/2011]

Ø Anti-dumping duty has been imposed on imports of Glass Fibre and articles falling under heading 7019 originating in, or exported from, People’s Republic of China. [CUS NTF NO. 30/2011 DATE 04/03/2011]

Ø Anti-dumping duty imposed on imports of acrylonitrile butadiene rubber (NBR) originating in, or exported from, the Chinese Taipei has been removed. [CUS NTF NO. 33/2011 DATE 30/03/2011]

Ø Definitive Anti-dumping duty has been imposed on Acetone (29141100) originating in, or exported from, Thailand and Japan. [CUS NTF NO. 36/2011 DATE 18/04/2011]

Ø Anti-dumping duty imposed on imports of Silk fabric of weight 20 to 100 gms per metre falling under tariff item 5007 originating in, or exported from People’s

thRepublic of China has been extended upto 5 December 2011. [CUS NTF NO. 37/2011 DATE 21/04/2011]

Non Tariff :

Ø Gandhinagar, Gujarat, has been added as inland container depots for the Unloading of imported goods and the loading of export goods[CUS NTF NO. 22/2011(NT) DATE 08/03/2011]

Ø The Courier Imports and Exports (Electronic Declaration and Processing) Regulations, 2010 is amended. [CUS NTF NO. 26/2011(NT) DATE 01/04/2011]

Ø Hazira, Surat, Gujarat has been declared as inland container depots for the unloading of imported goods and the loading of export goods or any class of such goods. [CUS NTF NO. 28/2011(NT) DATE 06/04/2011]

Ø Ahmedbad, Jamnagar in Gujarat and Rajasansi (Amritsar), Chandigarh in Punjab are notified as customs ports or customs airports for the unloading of imported goods and the loading of export goods. [CUS NTF NO. 29/2011(NT) DATE 06/04/2011]

May - 2011

23

3. Time limit for finalization of Project Imports under PIR, 1986 is adhered to in all cases, so that such finalization is completed within the validity period of the bank guarantee in order to ensure that the government revenue is safeguarded.

4. However, in cases where the importers have not submitted the requisite documents in time, it may be ensured that the bank guarantees are kept alive until finalization of project imports so that resultant delay does not adversely affect the interests of revenue.

5. It has also been clarified that to deter the importers from non-submission or delayed submission of relevant documents, the Commissioners should ensure that in cases where the requisite Statement / documents under Regulation 7 of PIR, 1986 is not submitted in time or submitted incomplete, then necessary action for enforcing bond / undertaking, cash security/ bank guarantees executed in this regard, issue of notice for demand of duty, penalty for non-compliance with the provisions of the Regulations may be initiated against the importer

6. Importer and his Custom House Agent should ensure that the provisionally assessed Bills of Entry for the imported goods at the ports other than the port of registration of project imports are finally assessed and audited at the respective ports, and should be submitted along with the documents submitted for finalization of Project Imports. In these cases the concerned Commissioner should ensure that such Bills of Entry are finalized without undue delay.

7. It has been decided by Board that jurisdictional Central Excise Commissionerate should ensure that Plant Site Verification, where ever applicable, is completed within 15 days of submission of relevant documents by the importers

8. The Board further has directed that the concerned Commissioner of Customs should monitor the pendency of project imports cases and submit a monthly report to the Chief Commissioner of Customs in charge of the Zone, in the prescribed format enclosed along with this circular as in Annexure-I. The Chief Commissioner of Customs will monitor the pendency and send a quarterly consolidated report of

ththe Zone by 15 of next month to the Directorate General of Inspection (Customs & Central Excise), New Delhi in prescribed format as in Annexure-II. The DGIC&CE will in turn monitor the pendency at All India level, in centralized manner and will report to the Board on a quarterly basis about the progress made in finalization of project imports, trend of compliance etc. and suggest corrective measures to be taken, if any. [CUS CIR NO. 22/2011 DATE 04/05/2011]

Instructions:

Ø Food Safety and Standards Authority of India (FSSAI) is required to test samples of food articles, particularly fresh produce exported from Japan after March 11, 2011, such as sea food, fruits, vegetables and meat

Finance Bill, 2011. It is, therefore, some clarifications issued i.r.t. new legislative provisions. [CUS CIR NO. 17/2011 DATE 08/04/2011]