lbg monday draft last

TRANSCRIPT

Roland George Investments Program Bond Swap Recommendation

Stephan Farias-Bastos 03/31/2015

Buy Candidate Analysis

Lloyds Banking Group plc is a major British financial institution that provides services into retail

banking, commercial, life, pensions & insurance, and Wealth & International in the US, Europe, the

Middle-East and Asia. Their retail division provides current accounts, savings, loans and mortgages to

personal and small business. LBG plc offer on their retail division an extensive multi-brand, multi-

channel offering, where millions of customers are served through Lloyds Bank, Halifax, and Bank of

Scotland and Scottish Widows brands. Their commercial banking provides lending, deposits, and

transaction banking services to corporate clients as well as offering expertise in capital markets, financial

markets, and private equity. The Asset finance provides asset finance and solutions and credit cards to

consumer and commercial customer, Lex Autolease one of LBG’s subsidiaries, is UK’s leading fleet

management and fleet funding specialist with close to 300,000 vehicles under management. As for the

insurance division, long-term savings, investment and protection products are offered under the Scottish

Widows brand. Products are available through intermediaries, direct channels and also through our Retail

division via Lloyds Bank, Halifax and Bank of Scotland. The General Insurance business is a leading

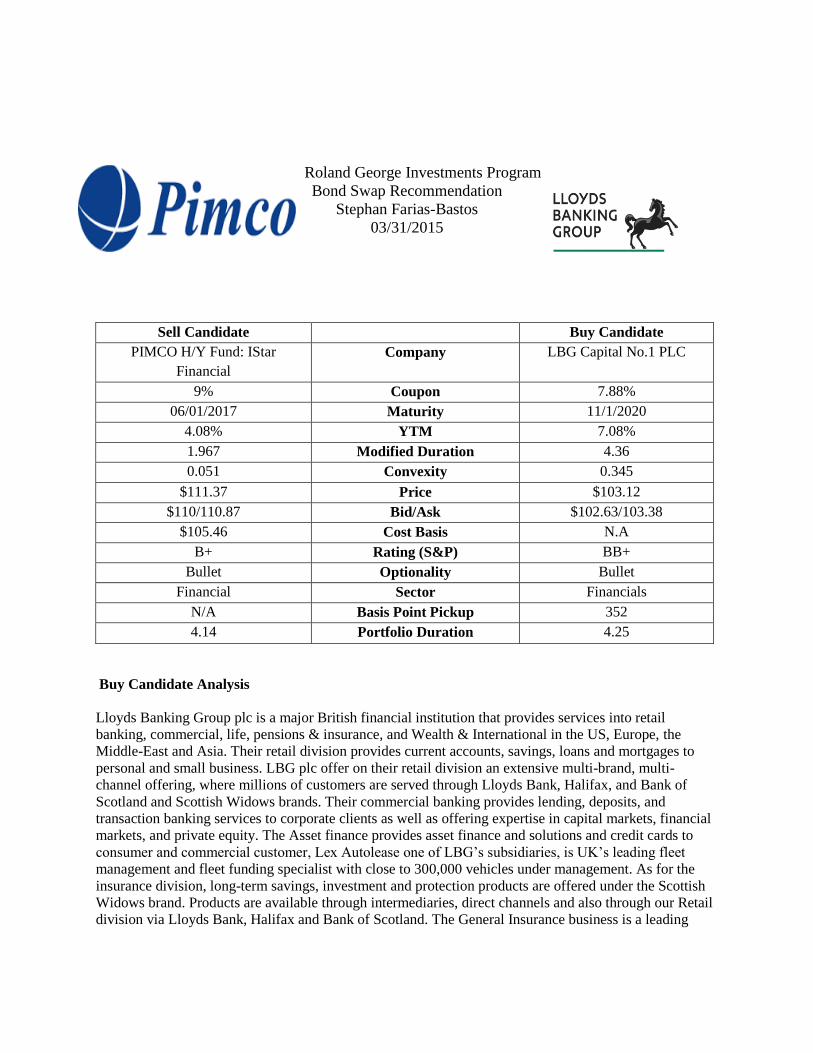

Sell Candidate Buy Candidate

PIMCO H/Y Fund: IStar

Financial

Company LBG Capital No.1 PLC

9% Coupon 7.88%

06/01/2017 Maturity 11/1/2020

4.08% YTM 7.08%

1.967 Modified Duration 4.36

0.051 Convexity 0.345

$111.37 Price $103.12

$110/110.87 Bid/Ask $102.63/103.38

$105.46 Cost Basis N.A

B+ Rating (S&P) BB+

Bullet Optionality Bullet

Financial Sector Financials

N/A Basis Point Pickup 352

4.14 Portfolio Duration 4.25

provider of home insurance in the UK, with products sold through the branch network, direct channels

and strategic corporate partners.

Lloyds Bank Group has been and will be good to their bondholders in the past year. Moody’s has issued

repeatedly issued positive reports on LBG plc upgrading their issuer and deposit ratings to A1 in

May,2014 due to their stabilization of the group’s operating model and the group’s reduced downside

risk. Further, they emphasized their improvements in Lloyd’s liquidity and funding metrics, as well as

achieving a solid capital and leverage metrics due to their improved earnings generation capacity in the

last 4 years. LBG has also very stable financially and has been able to grow their free cash flow in the last

4 years by 15% average in the last 4 years. Another benefit to our portfolio is the increase of our portfolio

duration by swapping into LBG, which will benefit the portfolio return in times of lowering interest rates.

This is beneficial considering my later prediction on interest rates; I state a decrease of interest rates in

between 20 to 35 bps in our workout period (12 to 18 months). LBG’s positive credit outlook, their

improving cash flows, and the higher duration are the primary reasons why swapping into LBG bonds

would be a beneficial decision for the Roland George Investment Program.

Interest Rate Forecast

Towards the beginning of the year the political uncertainty in Greece and low global inflation to low oil

prices brought instability to the region, which had an impact on the 10y Generic UK bond that spiked up

to 1.85% in January. Further, the Sterling rate decline by about 20bps along with a rise of the US dollar vs

the sterling for 5 bps at the beginning of February an approximate 4% depreciation of the dollar. The US

economy saw a growth of 1.2%, a smaller growth than seen in stages before which recommends pictures

a slower growth period in the US economy. Further, as we go into February Greek elections and the

escalation of the Ukraine conflict made the spread in between the Greek sovereign bond vs the German

bond widened. These continuous instability lead to an increase in short-term rates in the UK. However, as

we get close to the end of the 1Q of 2015, the European credit spreads have fallen due to more political

stability in the area. Greece have finally reached an agreement with the European committee in order to

pay their sovereign debt towards the end of March and June along with more strict fiscal policies, the

Ukraine conflict has not materialized, and German metalworkers union have reached a 3.4 % settlement.

As a consequence, this last month saw a mixed growth in the EU, especially in France, Spain and

Portugal with an average GDP Growth of 0.8% in the last month. Credit conditions have stabilized with

an impact on the credit spreads and stronger cash holdings in the British corporations.

However the outlook seems more positive about the UK economy towards this 2015, towards the end of

2014 the GDP growth reached the 2.6 % the fastest pace since 2007 along with a record unemployment of

5.7% reached in January 2015. Further, the inflation has stayed low to a 0.3% with estimations of

possibly reaching 1.8% towards the beginning of 2016 to finally reach their 2% inflation goal. The short

and midterm growth will still be linked to the international risks, which brings hope to the economy due

to the medium term improvement in the economic environment. This positive trend on the

macroeconomics in the EU along with the improvements in the overall financial sector in England will

cumulative provides a drop of 15 bps in interest rate.

The beginning of 2015 was bittersweet for the US economic outlook; this was mainly affected by the

uncertainty in regards of different variables. One of these variables was the increase in the worth of the

dollar vs the Euro that depreciated for a record low against the dollar to a $1.14. As a consequence a flight

to quality to US corporate bonds is a possibility that would put downward pressure to the corporate yields

making the yield curve to possibly narrow on a midterm scale. 4 years after recession the Fed has finally

stopped the pump of money into the economy by the issuance of debt in order to stimulate the economy.

In 2015, the Fed has taken a new standpoint in regards of the outlook of the economy, which has gone

from recessionary to slow growth. However, this outlook changed when the Fed in the latest minutes

changed their language in regards of an increase in interest rate which was noticed by the absence of the

word ‘patience’. This immediately pushed the interest rates of the 10Y treasury up to one of 2%.

However, the Fed still remains hesitant about an immediate increase in interest rates due to a possible

counter effect on the economic growth that has been paced down in the last 2 years after having record

growth in 2012 and 2013 with a 2.8%, however, last year the GDP growth slowed down to 1.9%. The

slowdown in the beginning of this 2015 will have an impact on of an increase in 15bps on the interest

rates.

Further, the strength of the dollar vs the Euro and the Sterling pound has brought the attention of the

economist due to the possible impact on the trade volume that could bring a trading deficit and

consequently impacted the US corporations in falling in their profits. Another factor to believe in a

possible slowdown of the economy in this beginning of 2015 is the recent layoffs on the materials sectors

as well as the utilities sector in the month of March. Another impactful event to the economy has been

the big decrease in oil prices and its volatility due to the increase in oil production from Saudi Arabia in

the market. This has impacted tremendously one of the fastest growing industries in the US which was

fracking in 2014. A decrease in oil prices was expected to bring more consumers spending to the

beginning of 2015; however, construction spending has seen a decline in 1.1% in January. Further,

consumer spending has risen only a 0.2% increases the lowest increase since 2009. Due to all these

conditions mentioned previously I estimate an increase in the Treasury 10Y bonds interest rates in

between 25 and 35 bps.

As mentioned before we are currently living in times when the economy variables are a clear sign that the

economy has stacked in a slow growth period. The market descriptions for projections are specific. Based

on the previous description of the economy, the market is anticipating a total increase in interest rates of

about 35bps in between our bond holding period of 12 to 18 months to 1.30% along with a decrease in

UK and EU interest rates of their 10Y benchmark in between 25 to 25bps.

Swap Rationale

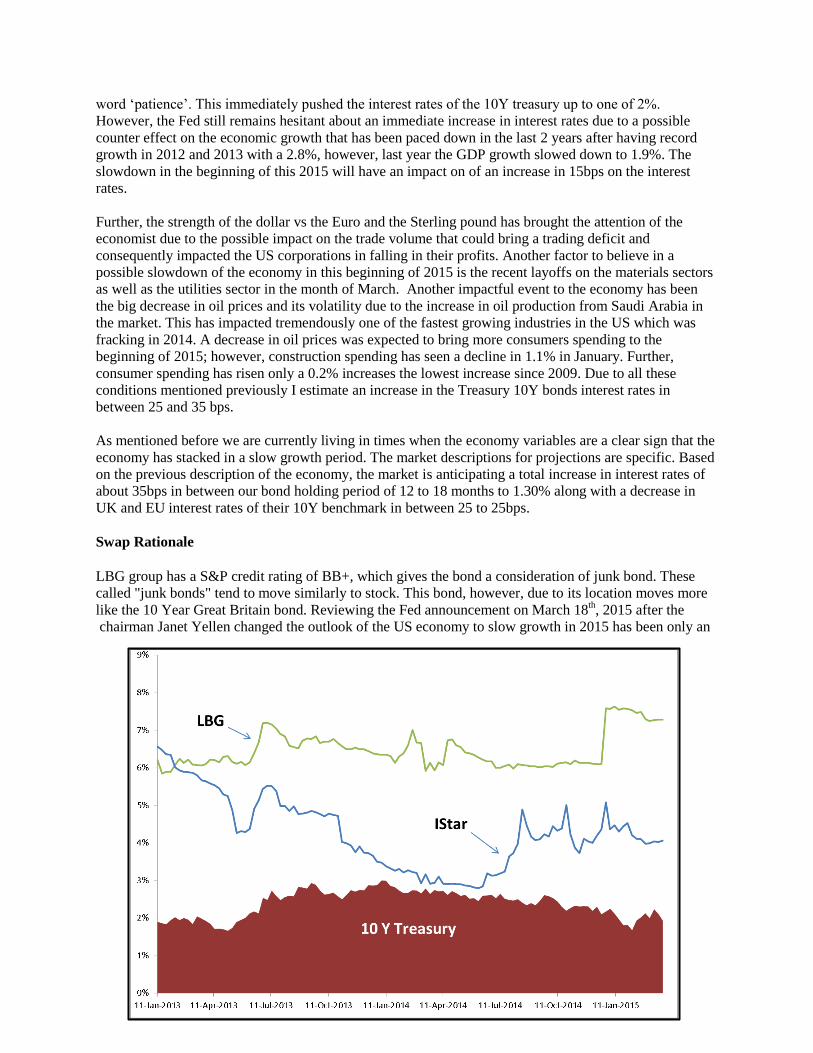

LBG group has a S&P credit rating of BB+, which gives the bond a consideration of junk bond. These

called "junk bonds" tend to move similarly to stock. This bond, however, due to its location moves more

like the 10 Year Great Britain bond. Reviewing the Fed announcement on March 18th, 2015 after the

chairman Janet Yellen changed the outlook of the US economy to slow growth in 2015 has been only an

affirmation of the current economic situation that has brought concern to all sectors of the economy. As

the economy continues to slow down, an increase in rates is less probable with a 10Y Treasury yielding

1.96% it seems more viable to continue the decrease in yields in order to avoid a counter effect to the

economic growth of the economy in 2015. That being said, I estimate a decrease in interest rates in

between 15 bps and 25 bps, a conservative outlook based on the uncertainty of the economy in this 2015.

Swapping LBG Group for the PIMCO H/Y: IStar brings the portfolio a number of positive scenarios.

First of all, it extends our portfolio duration by 4.25 this will bring the capacity to our portfolio to take

advantage of the narrowing tendency of the credit spread in between the Treasury bonds with gives us the

possibility of taking more risk and having a longer duration to our portfolio, which will increase our

capital return. Since the LBG Group is related to neither the S&P 500 nor the 10Y treasury, we can rely

on the strong financials of Lloyds Bank group. Their competitive advantage on the British market along

with their diversification on the US markets provides LBG the capacity of providing high cash flow in

order to repay their debt. The uniqueness of LBG is their relation to company specifics, which has been

almost unreactive to the oil prices or even low prices of commodities. Further, the British economy is

located in point of inflexion coming back from an almost recessionary period back in 2010 right after the

London Olympics to expectations of a 2.5% growth in 2015. This will be a huge boost for the banking

sector, which will be benefited from the growth of other emerging markets. This growth will give the

economy an interesting look for investors, who will not find large profit margins in the U.S bond market

and will encounter higher returns in an economy that with a faster pace growth than the U.S economy.

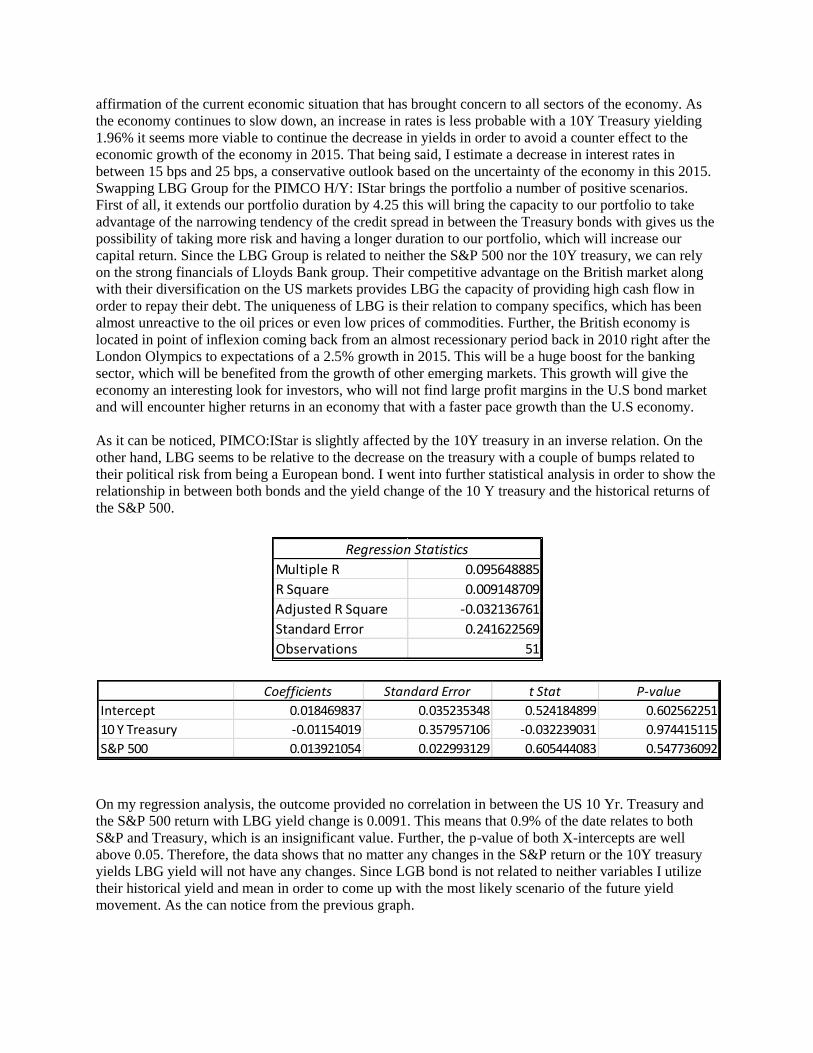

As it can be noticed, PIMCO:IStar is slightly affected by the 10Y treasury in an inverse relation. On the

other hand, LBG seems to be relative to the decrease on the treasury with a couple of bumps related to

their political risk from being a European bond. I went into further statistical analysis in order to show the

relationship in between both bonds and the yield change of the 10 Y treasury and the historical returns of

the S&P 500.

On my regression analysis, the outcome provided no correlation in between the US 10 Yr. Treasury and

the S&P 500 return with LBG yield change is 0.0091. This means that 0.9% of the date relates to both

S&P and Treasury, which is an insignificant value. Further, the p-value of both X-intercepts are well

above 0.05. Therefore, the data shows that no matter any changes in the S&P return or the 10Y treasury

yields LBG yield will not have any changes. Since LGB bond is not related to neither variables I utilize

their historical yield and mean in order to come up with the most likely scenario of the future yield

movement. As the can notice from the previous graph.

Regression Statistics

Multiple R 0.095648885

R Square 0.009148709

Adjusted R Square -0.032136761

Standard Error 0.241622569

Observations 51

Coefficients Standard Error t Stat P-value

Intercept 0.018469837 0.035235348 0.524184899 0.602562251

10 Y Treasury -0.01154019 0.357957106 -0.032239031 0.974415115

S&P 500 0.013921054 0.022993129 0.605444083 0.547736092

The outlook for the S&P 500 during this 2015 is less certain that it was at the beginning of 2015. After a 4

consecutive day loss on the S&P losing 0.2%, the Dow Jones has also been affected by the market

towards the end of March 2015. On the other hand the oil prices have surged up to 4% in the same time

span, which has been attributed to the Geopolitical pressure by Saudi Arabia on military installations and

the latest Middle East instability mainly with the uncertainty in the Iran Nuclear talks with the US

representatives. The estimates for a record setting rally from the S&P may not be the outcome for the

2015, considering the Fed for the sake of the economy growth has to reduce their open market policies to

a more conservative position. Along with the fly to quality from investors after a turbulent 2014 year for

European corporate bonds and a stop to the Chinese downshift economy growth by 0.3% has set the US

bond’s market as an attractive possibility, which would definitely have a negative impact on S&P and the

Dow that as mentioned before have seen 4 day loss currently. All this factors along with a more

conservative economic policy by the fed seem that will impact the stock market, which is why I suggest

decreased on the returns in the 2015:

∆𝐿𝐵𝐺 𝑦𝑖𝑒𝑙𝑑 =6.102+6.47

2

2− 6.94 = −0.38%

In order to find the bps increase or decrease of LBG yield, I utilize the lowest yield and added up with

their average yield which I subsequently divided by two to obtain a ‘low average’. Further, I added this

‘low average’ with their highest yield and divided by two in orders to obtain an average high yield. This

was 6.938, which I subsequently subtracted to their current yield and gave out a bps difference of 38bps.

∆𝐼𝑆𝑇𝐴𝑅 𝑦𝑖𝑒𝑙𝑑 = .031 − (.04 ∗ 9%)

∆𝐼𝑆𝑇𝐴𝑅 𝑦𝑖𝑒𝑙𝑑 = −0.33%

On the formula above I utilize my S&P500 estimations of 10% return for 2015 and multiplied it by the

it’s coefficient. Later I subtracted the intercept coefficient to finally obtaining an increase/decrease of a 36

bps for ISTAR yield.

Regression Statistics

Multiple R 0.234379289

R Square 0.054933651

Adjusted R Square 0.036032324

Standard Error 0.281979694

Observations 52

Coefficients Standard Error t Stat P-value

Intercept 0.031703327 0.039545371 0.801695013 0.426523159

S&P 500 -0.040555966 0.0237893 -1.704798619 0.094438935

After running a similar regression in between PIMPCO: IStar there was no relationship with the 10Y

Treasury as can be noticed from the historical 10Y treasury yield graph. Never the less, the regression

shown above proofs no significance of the date with the S&P 500 either as it can be seen from the P-value

being larger than the 0.05. Further, the data shows a small negative correlation in between IStar and

S&P500 of 5% of the data as shown on the R Square value.

If one refer to the yield curve from PIMPCO H/Y: IStar, the bond has shown a down trend in the last 3

years of an average of 100bps per year. However, in June the yield increased 100 bps. Due to the

proximity to the maturity date of the bond, the risk of holding the bond decreases meaning in a decrease

in their yield. On the other hand, by looking at the historical yield of LBG it can be assumed that there are

volatile changes in their yield. However, LBG highest yield was 7.59% in December 19th, 2014 and their

lowest yield has been 5.85%, which indicates a yield span of only 179bps. The average yield of this bond

since it’s released has been 6.47% this indicates a up max yield change of 112bps and a down max yield

change of only 62 bps.

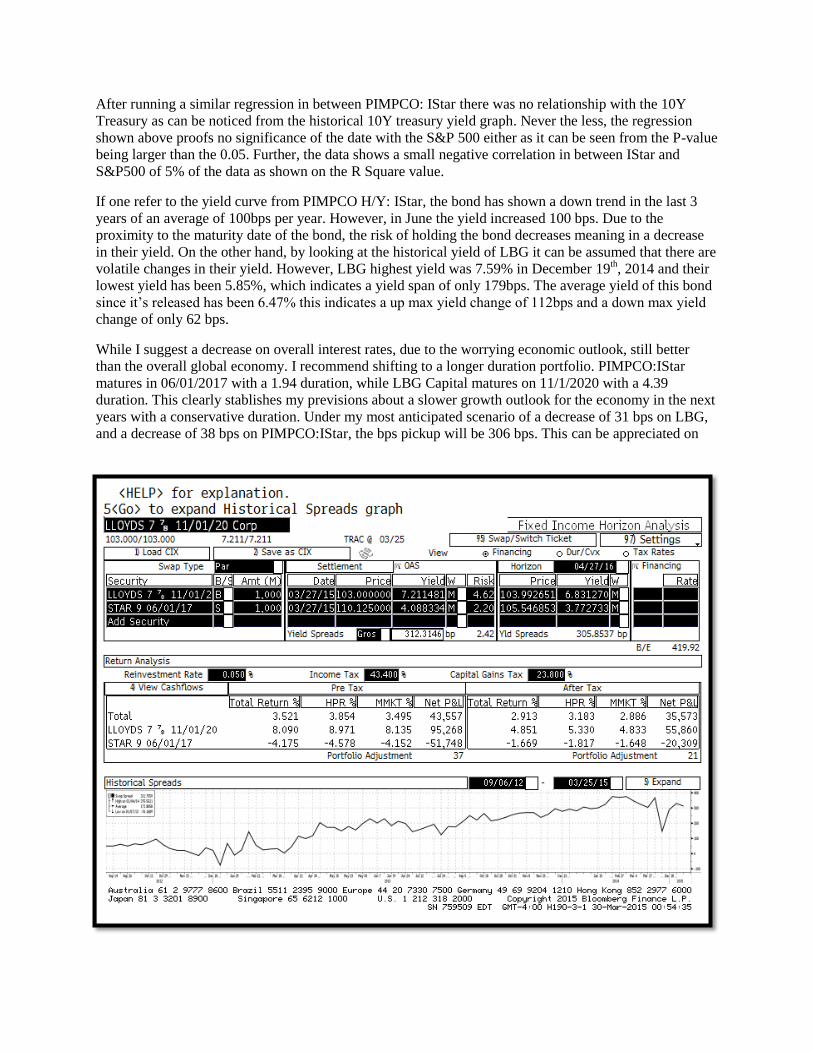

While I suggest a decrease on overall interest rates, due to the worrying economic outlook, still better

than the overall global economy. I recommend shifting to a longer duration portfolio. PIMPCO:IStar

matures in 06/01/2017 with a 1.94 duration, while LBG Capital matures on 11/1/2020 with a 4.39

duration. This clearly stablishes my previsions about a slower growth outlook for the economy in the next

years with a conservative duration. Under my most anticipated scenario of a decrease of 31 bps on LBG,

and a decrease of 38 bps on PIMPCO:IStar, the bps pickup will be 306 bps. This can be appreciated on

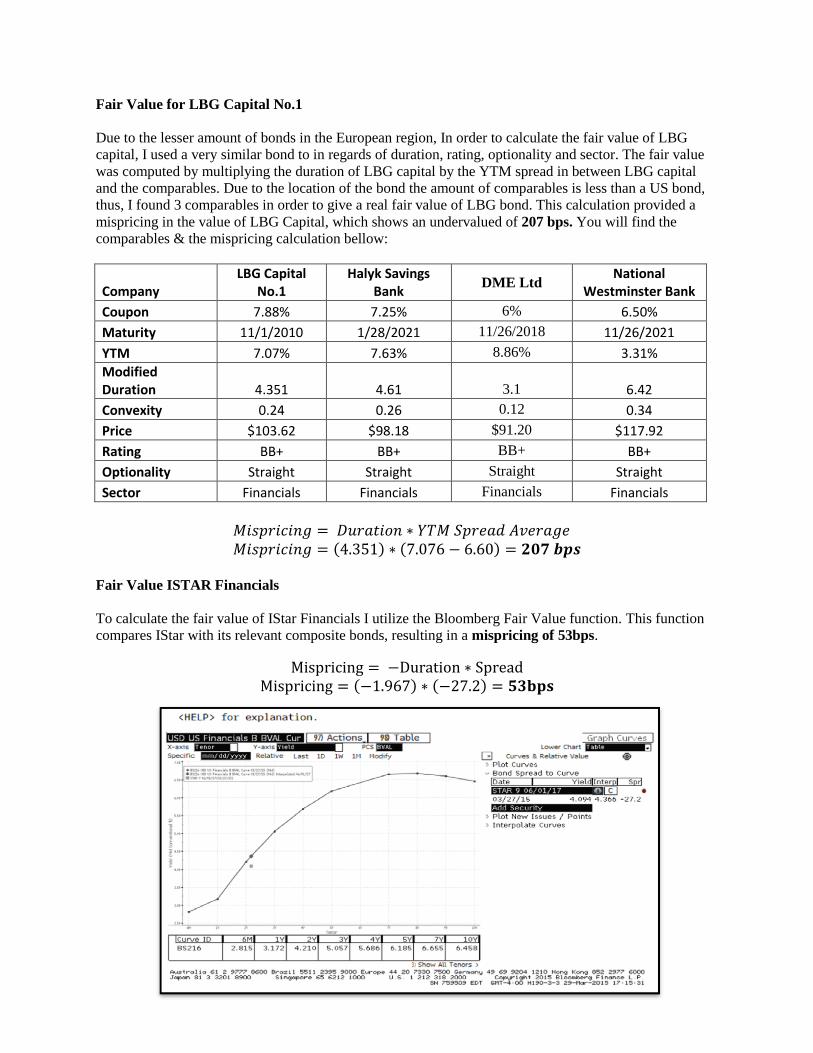

Fair Value for LBG Capital No.1

Due to the lesser amount of bonds in the European region, In order to calculate the fair value of LBG

capital, I used a very similar bond to in regards of duration, rating, optionality and sector. The fair value

was computed by multiplying the duration of LBG capital by the YTM spread in between LBG capital

and the comparables. Due to the location of the bond the amount of comparables is less than a US bond,

thus, I found 3 comparables in order to give a real fair value of LBG bond. This calculation provided a

mispricing in the value of LBG Capital, which shows an undervalued of 207 bps. You will find the

comparables & the mispricing calculation bellow:

Company LBG Capital

No.1 Halyk Savings

Bank DME Ltd

National Westminster Bank

Coupon 7.88% 7.25% 6% 6.50%

Maturity 11/1/2010 1/28/2021 11/26/2018 11/26/2021

YTM 7.07% 7.63% 8.86% 3.31%

Modified Duration 4.351 4.61

3.1 6.42

Convexity 0.24 0.26 0.12 0.34

Price $103.62 $98.18 $91.20 $117.92

Rating BB+ BB+ BB+ BB+

Optionality Straight Straight Straight Straight

Sector Financials Financials Financials Financials

𝑀𝑖𝑠𝑝𝑟𝑖𝑐𝑖𝑛𝑔 = 𝐷𝑢𝑟𝑎𝑡𝑖𝑜𝑛 ∗ 𝑌𝑇𝑀 𝑆𝑝𝑟𝑒𝑎𝑑 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑀𝑖𝑠𝑝𝑟𝑖𝑐𝑖𝑛𝑔 = (4.351) ∗ (7.076 − 6.60) = 𝟐𝟎𝟕 𝒃𝒑𝒔

Fair Value ISTAR Financials

To calculate the fair value of IStar Financials I utilize the Bloomberg Fair Value function. This function

compares IStar with its relevant composite bonds, resulting in a mispricing of 53bps.

Mispricing = −Duration ∗ Spread Mispricing = (−1.967) ∗ (−27.2) = 𝟓𝟑𝐛𝐩𝐬

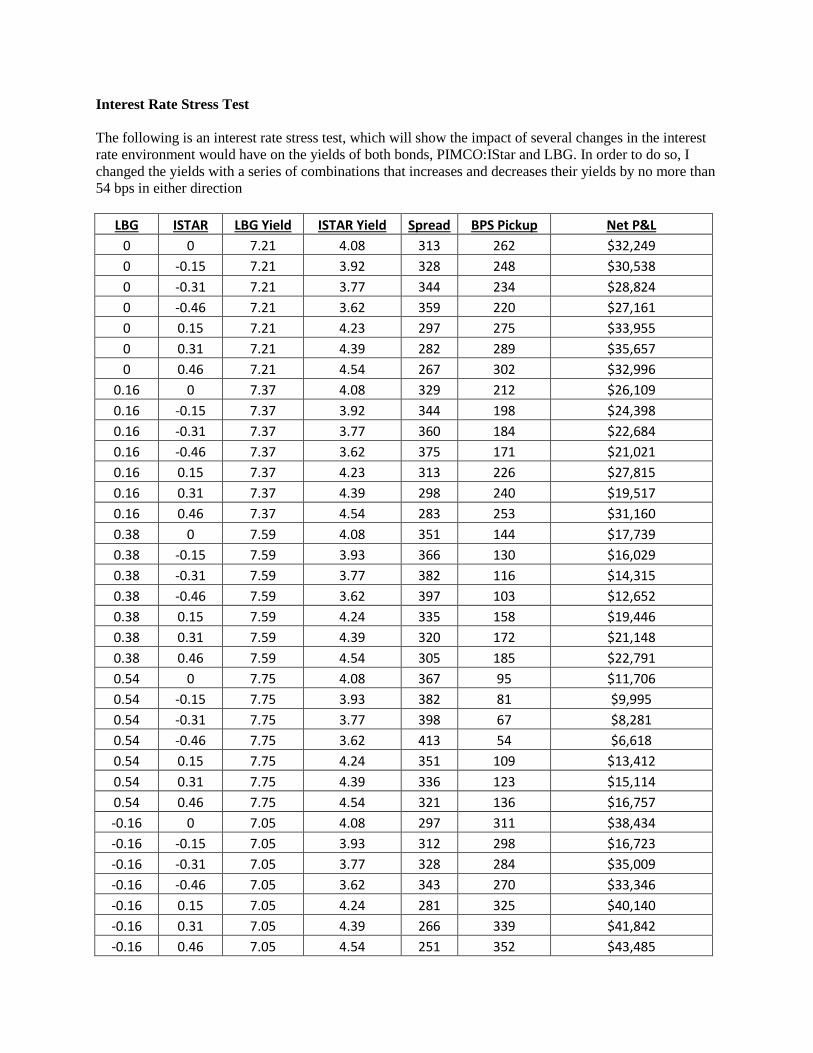

Interest Rate Stress Test

The following is an interest rate stress test, which will show the impact of several changes in the interest

rate environment would have on the yields of both bonds, PIMCO:IStar and LBG. In order to do so, I

changed the yields with a series of combinations that increases and decreases their yields by no more than

54 bps in either direction

LBG ISTAR LBG Yield ISTAR Yield Spread BPS Pickup Net P&L

0 0 7.21 4.08 313 262 $32,249

0 -0.15 7.21 3.92 328 248 $30,538

0 -0.31 7.21 3.77 344 234 $28,824

0 -0.46 7.21 3.62 359 220 $27,161

0 0.15 7.21 4.23 297 275 $33,955

0 0.31 7.21 4.39 282 289 $35,657

0 0.46 7.21 4.54 267 302 $32,996

0.16 0 7.37 4.08 329 212 $26,109

0.16 -0.15 7.37 3.92 344 198 $24,398

0.16 -0.31 7.37 3.77 360 184 $22,684

0.16 -0.46 7.37 3.62 375 171 $21,021

0.16 0.15 7.37 4.23 313 226 $27,815

0.16 0.31 7.37 4.39 298 240 $19,517

0.16 0.46 7.37 4.54 283 253 $31,160

0.38 0 7.59 4.08 351 144 $17,739

0.38 -0.15 7.59 3.93 366 130 $16,029

0.38 -0.31 7.59 3.77 382 116 $14,315

0.38 -0.46 7.59 3.62 397 103 $12,652

0.38 0.15 7.59 4.24 335 158 $19,446

0.38 0.31 7.59 4.39 320 172 $21,148

0.38 0.46 7.59 4.54 305 185 $22,791

0.54 0 7.75 4.08 367 95 $11,706

0.54 -0.15 7.75 3.93 382 81 $9,995

0.54 -0.31 7.75 3.77 398 67 $8,281

0.54 -0.46 7.75 3.62 413 54 $6,618

0.54 0.15 7.75 4.24 351 109 $13,412

0.54 0.31 7.75 4.39 336 123 $15,114

0.54 0.46 7.75 4.54 321 136 $16,757

-0.16 0 7.05 4.08 297 311 $38,434

-0.16 -0.15 7.05 3.93 312 298 $16,723

-0.16 -0.31 7.05 3.77 328 284 $35,009

-0.16 -0.46 7.05 3.62 343 270 $33,346

-0.16 0.15 7.05 4.24 281 325 $40,140

-0.16 0.31 7.05 4.39 266 339 $41,842

-0.16 0.46 7.05 4.54 251 352 $43,485

-0.38 0 6.83 4.08 275 380 $47,013

-0.38 -0.15 6.83 3.93 290 366 $45,303

-0.38 -0.31 6.83 3.77 306 352 $43,491

-0.38 -0.46 6.83 3.62 321 339 $41,925

-0.38 0.15 6.83 4.24 259 394 $48,718

-0.38 0.31 6.83 4.39 244 407 $50,421

-0.38 0.41 6.83 4.50 233 417 $51,583

-0.54 0 6.67 4.08 259 431 $53,307

-0.54 -0.15 6.67 3.93 274 417 $51,597

-0.54 -0.31 6.67 3.77 290 403 $49,882

-0.54 -0.46 6.67 3.62 305 390 $48,219

-0.54 0 6.67 4.08 259 431 $53,307

-0.54 0.15 6.67 4.20 247 441 $54,573

-0.54 0.31 6.67 4.39 228 458 $56,715

After receiving the results of the interest rate stress test, out of all the scenarios tested there is a 100%

positive basis point pickup. The overall average dollar profit is $31,535.04 or 261.1 bps. Through running

my regression analysis and making estimations based on the historical movement of the yields of both

LBG and IStar, I calculated my most probable scenario, which is bolded with no background, would be

for both bonds to decrease for 31bps on IStar yield and 38bps decrease on LBG yield. I felt that the

reduction of PIMCO H/Y:IStar by 31bps would be conservative based on the fact that the bond is getting

closer to maturity, and it has moved averagely decreased 31bps. One the other hand, LBG yield decrease

was also conservative considering the spread from its highest yield to the lowest is almost 200bps. The

other two most likely scenarios are with decrease in yields, and the other one by a potential increase in the

yield of LBG due to their political risk and a decrease of PIMPCO:H/Y due to its closeness to the

maturity date.

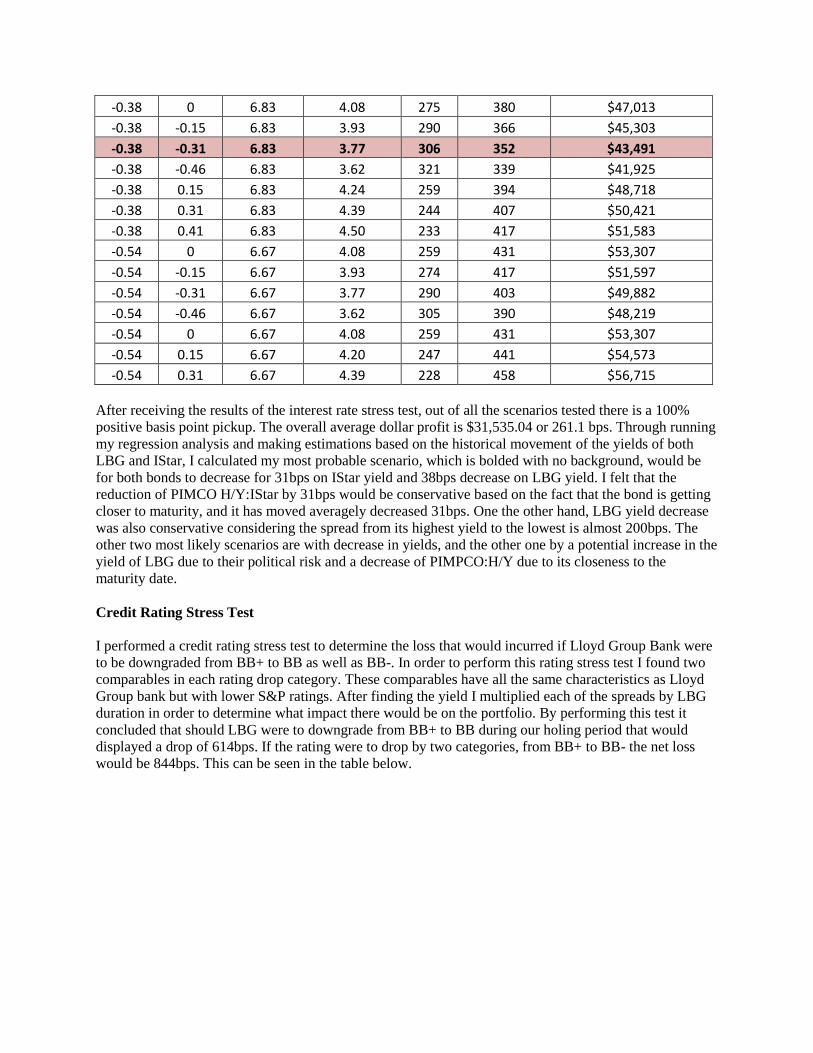

Credit Rating Stress Test

I performed a credit rating stress test to determine the loss that would incurred if Lloyd Group Bank were

to be downgraded from BB+ to BB as well as BB-. In order to perform this rating stress test I found two

comparables in each rating drop category. These comparables have all the same characteristics as Lloyd

Group bank but with lower S&P ratings. After finding the yield I multiplied each of the spreads by LBG

duration in order to determine what impact there would be on the portfolio. By performing this test it

concluded that should LBG were to downgrade from BB+ to BB during our holing period that would

displayed a drop of 614bps. If the rating were to drop by two categories, from BB+ to BB- the net loss

would be 844bps. This can be seen in the table below.

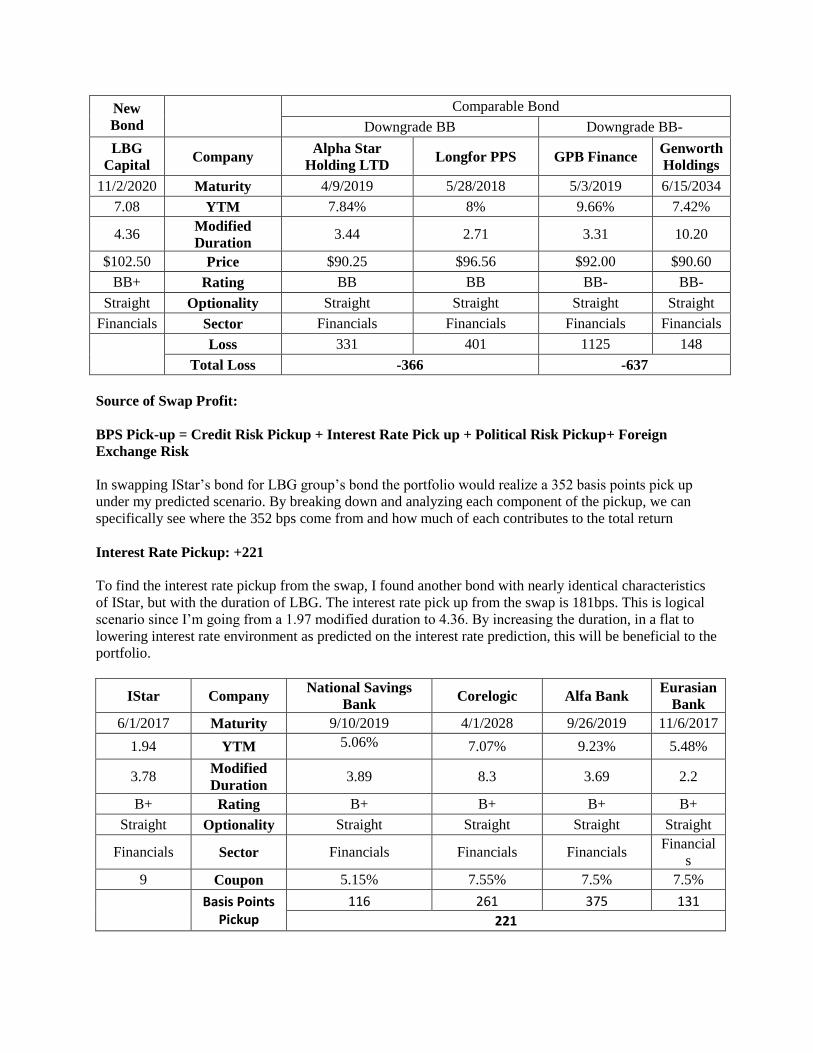

New

Bond

Comparable Bond

Downgrade BB Downgrade BB-

LBG

Capital Company

Alpha Star

Holding LTD Longfor PPS GPB Finance

Genworth

Holdings

11/2/2020 Maturity 4/9/2019 5/28/2018 5/3/2019 6/15/2034

7.08 YTM 7.84% 8% 9.66% 7.42%

4.36 Modified

Duration 3.44 2.71 3.31 10.20

$102.50 Price $90.25 $96.56 $92.00 $90.60

BB+ Rating BB BB BB- BB-

Straight Optionality Straight Straight Straight Straight

Financials Sector Financials Financials Financials Financials

Loss 331 401 1125 148

Total Loss -366 -637

Source of Swap Profit:

BPS Pick-up = Credit Risk Pickup + Interest Rate Pick up + Political Risk Pickup+ Foreign

Exchange Risk

In swapping IStar’s bond for LBG group’s bond the portfolio would realize a 352 basis points pick up

under my predicted scenario. By breaking down and analyzing each component of the pickup, we can

specifically see where the 352 bps come from and how much of each contributes to the total return

Interest Rate Pickup: +221

To find the interest rate pickup from the swap, I found another bond with nearly identical characteristics

of IStar, but with the duration of LBG. The interest rate pick up from the swap is 181bps. This is logical

scenario since I’m going from a 1.97 modified duration to 4.36. By increasing the duration, in a flat to

lowering interest rate environment as predicted on the interest rate prediction, this will be beneficial to the

portfolio.

IStar Company National Savings

Bank Corelogic Alfa Bank

Eurasian

Bank

6/1/2017 Maturity 9/10/2019 4/1/2028 9/26/2019 11/6/2017

1.94 YTM 5.06% 7.07% 9.23% 5.48%

3.78 Modified

Duration 3.89 8.3 3.69 2.2

B+ Rating B+ B+ B+ B+

Straight Optionality Straight Straight Straight Straight

Financials Sector Financials Financials Financials Financial

s

9 Coupon 5.15% 7.55% 7.5% 7.5%

Basis Points Pickup

116 261 375 131

221

Credit Risk Pickup: -103

By swapping of PIMPCO:IStar bond for LBG bond there is a change of credit. In order to calculate the

credit risk implied in the swap I chose two bonds that had similar characteristics to LBG, and had in

average the same modified duration as LBG. This is important to determine the effect that swapping from

a B+ to a BB+ rated bond will have on the return. By going up the ladder two credit rating spots the swap

profit decreases by -116 bps as shown on the table below.

IStar Company Ally Financial

6/1/2017 Maturity 3/17/2017

3.78% YTM 2.99%

1.94 Modified Duration 1.89

B+ Rating BB+

Straight Optionality Straight

Financials Sector Financials

9% Coupon 2.25%

Basis Point Pickup -103

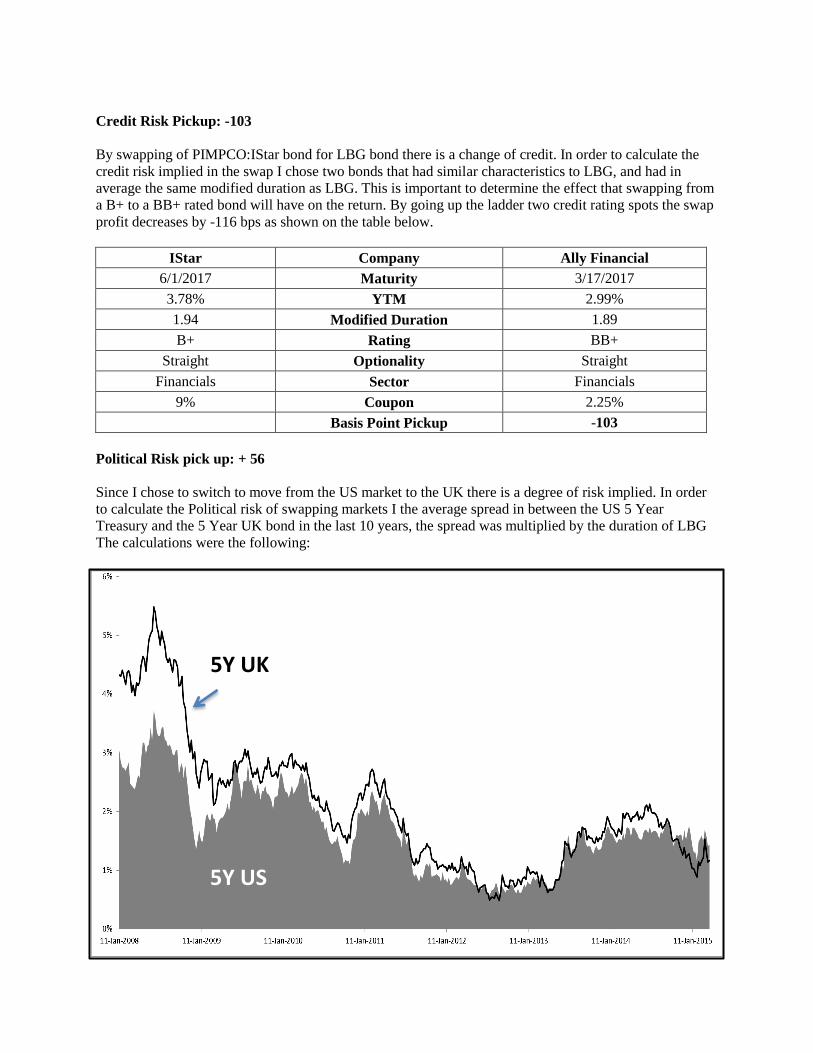

Political Risk pick up: + 56

Since I chose to switch to move from the US market to the UK there is a degree of risk implied. In order

to calculate the Political risk of swapping markets I the average spread in between the US 5 Year

Treasury and the 5 Year UK bond in the last 10 years, the spread was multiplied by the duration of LBG

The calculations were the following:

5Y UK

5Y US

By taking into account the historical spread in between both treasury bonds, we can notice a recent low

yields in the UK treasury as a consequence of the yield ceiling imposed by the government. This has

created a negative spread in between both bonds of -26.6 bps. Taking into account the analysis previously

done, the US interest rates will go up considering the Fed’s policy for a better growth of the economy, as

well as reaching their 2% inflation target. Further, the improvements in the UK economy, shown by the

decrease in unemployment in early 2015 along with the political stability of the region, along with the

quantitative easing one can assume that this spread will just get wider. I estimate an increase of spread for

at least -10bps.

𝑷𝒐𝒍𝒊𝒕𝒊𝒄𝒂𝒍 𝑹𝒊𝒔𝒌 = (𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑆𝑝𝑟𝑒𝑎𝑑 − 𝐶𝑢𝑟𝑟𝑒𝑛𝑡 𝑆𝑝𝑟𝑒𝑎𝑑) ∗ 𝐿𝐵𝐺 𝐷𝑢𝑟𝑎𝑡𝑖𝑜𝑛 =

(39 − 26) ∗ 4.36 = 𝟓𝟔𝒃𝒑𝒔

The graph above shows the relationship in between the US5Y treasury bond vs the UK5Y bond,

as it can be noticed historically the US5Y treasury spread average is 39bps against the UK bond.

The current spread,however, shows that the UK5Y is below the US treasury by -26.6bps. In

order to find the real political risk of LBG, I computed the average spread minus the current

spread by the duration of LBG bond. This resulted in a positive pickup of 56bps from the

political risk.

Foreign Exchange Risk: +252

Since the bond chosen has 49% of their revenue in UK, in order to stimate the impact of foreign

exchange in the risk of the bond, I found a comparable similar to LBG but issued in British

pounds and computed the yield difference multiplied by the duration of LBG and by their

percentage of revenues in UK. The calculation in order to find the risk was the following:

𝑭𝒐𝒓𝒆𝒊𝒈𝒏 𝑬𝒙𝒄𝒉𝒂𝒏𝒈𝒆 𝑹𝒊𝒔𝒌 = 𝑌𝑖𝑒𝑙𝑑 𝐷𝑖𝑓𝑓𝑒𝑟𝑒𝑛𝑐𝑒 ∗ 𝐷𝑢𝑟𝑎𝑡𝑖𝑜𝑛 𝐿𝐵𝐺 ∗ 𝑅𝑒𝑣𝑒𝑛𝑢𝑒 𝑖𝑛 𝑈. 𝐾

(7.08% − 5.9%) ∗ 4.36 ∗ 49% = 𝟐𝟓𝟐𝒃𝒑𝒔

Median 25.60

Average 39.92

Standard Deviation 51.70

Current Spread -26.6

Company LBG Capital No.1 Invester Bank

Maturity 11/1/2020 2/17/2020

YTM 7.08% 5.9

Modified Duration 4.36 5.2

Rating BB+ BB+

Optionality Straight Straight

Price $103.62 $98.50

Copon 7.88% 9.75%

Sector Financials Financials

Optionality: 0

Both bonds are both Bullet style bonds, meaning that they are not callable, so we would not pick up any

basis points in this area from the swap

Mispricing:-60

As it can be noticed the mispricing provides a big part of the basis point pickup, this happens as a

consequence of conservative standpoint taken in regards of the Political Risk, which is being evaluated

forward looking and not current. Otherwise, the political risk would be higher and the mispricing lower.

Credit Analysis

Lloyds Bank Group is currently generating about 37 billion pounds in revenue, with an operating margin

of 9.22% and net income margin of 5.93% beating their industry 2.60% by a comfortable margin. Even

though Lloyd’s cash flow has been negative 4 out of the last 5 years but have substantially improved it by

an average of 25% in the last 4 years, with aims to positive cash flow in 2015. It’s important to consider

that half of their $140billion in debt was issued during the Euro crisis and it was schedule for short-term

payments, which are schedule for the end of the year 2015. Lloyds is moving fast towards the eradication

of debt by the selloff of 200 branches as a plan for 2015, this initiative has started after the sellout of TSB

to Spanish Bank Sabadell for $2.4 billion dollars in 2014, which will bring a much more positive outlook

for LBG financials towards the end of 2015, this makes the bondholder position a more stable one, as the

company demonstrates its ability to repay debt.

Lloyds Bank

Group

Financial

Industry

PIMCO

Total Debt $140 billion N.A 5.9 billion

Debt/ Equity 16.55 3.5 6.57

Coverage Ratio 2.24 4.5 1.52

Current Ratio 0.62 1.68 0.68

ROA 0.17% 0.80% 1 %

Profit Margin 4.7% 10.46% 4.4%

Conclusion

Swapping IStar’s bond for LBG’s bond would bring a number of benefits for the Roland George

Investment bonds portfolio. We have seen that our lack of diversification of our bond has impacted our

return due to the volatility of the oil price, and slow growing sectors. To swap an expensive bond from

Financials to a British Financial bond will provide us security against oil volatility as well as the slow

growth of the US economy. To take extra risk on the yield based on a mispricing and interest rate risk,

will provide the portfolio with a more aggressive bond from a sector with growing possibilities.

Furthermore, even though we are losing points from swapping to a safer rating the interest rate will

compensate the risk. All these factors combined, I believe that Lloyd Group Bank’s bond is an excellent

bond for RGIP purchase.

BPS Pickup Credit Risk Interest Rate Political Risk Foreign Exchange Risk Optionality Mispricing

352 -116 220 56 252 0 -60