stephen sexauer jan 1411 (2)

DESCRIPTION

Superhero and Profits Maker Stephen Sexauer GIC Santiago Chile January 2010 The Grand Teton and Mount Rainier A Sudden Stop in Everything Everywhere The Superheroes Arrive Corporate Profits: What Recession? 2 Stephen Sexauer GIC January 2010TRANSCRIPT

Stephen Sexauer

GIC Santiago Chile

January 2010

The US Central Bank:

Superhero and Profits Maker

Stephen Sexauer GIC January 2010

2

2008 to 2010

A Stunningly Large Non-bank Bank Run

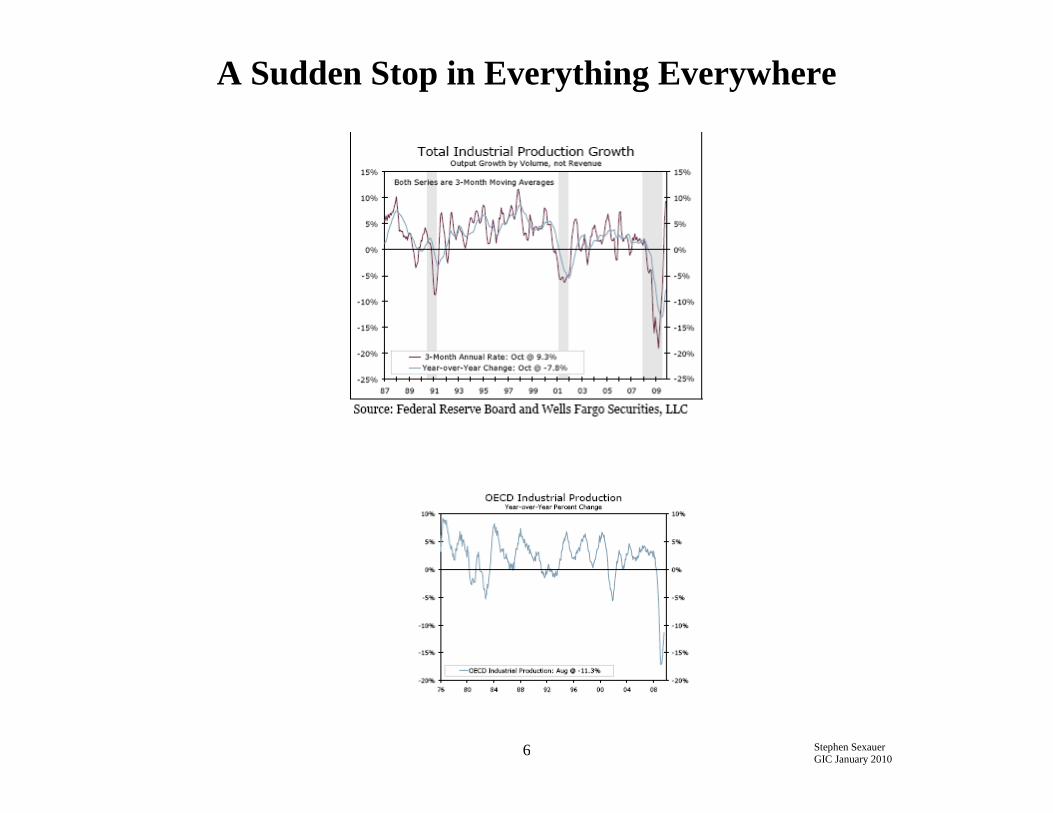

A Sudden Stop in Everything Everywhere

The Superheroes Arrive

Corporate Profits: What Recession?

The Grand Teton and Mount Rainier

Stephen Sexauer GIC January 2010

3

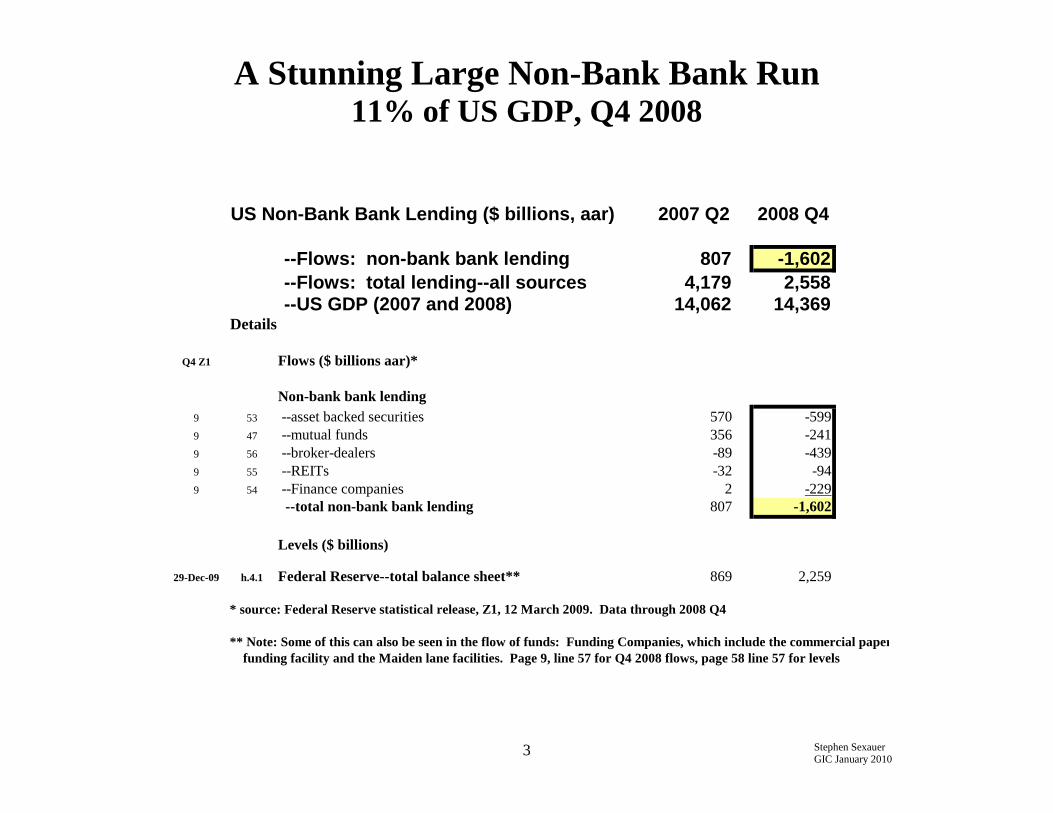

A Stunning Large Non-Bank Bank Run 11% of US GDP, Q4 2008

US Non-Bank Bank Lending ($ billions, aar) 2007 Q2 2008 Q4

--Flows: non-bank bank lending 807 -1,602

--Flows: total lending--all sources 4,179 2,558

--US GDP (2007 and 2008) 14,062 14,369

Details

Q4 Z1 Flows ($ billions aar)*

Non-bank bank lending

9 53 --asset backed securities 570 -599

9 47 --mutual funds 356 -241

9 56 --broker-dealers -89 -439

9 55 --REITs -32 -94

9 54 --Finance companies 2 -229

--total non-bank bank lending 807 -1,602

Levels ($ billions)

29-Dec-09 h.4.1 Federal Reserve--total balance sheet** 869 2,259

* source: Federal Reserve statistical release, Z1, 12 March 2009. Data through 2008 Q4

** Note: Some of this can also be seen in the flow of funds: Funding Companies, which include the commercial paper

funding facility and the Maiden lane facilities. Page 9, line 57 for Q4 2008 flows, page 58 line 57 for levels

Stephen Sexauer GIC January 2010

4

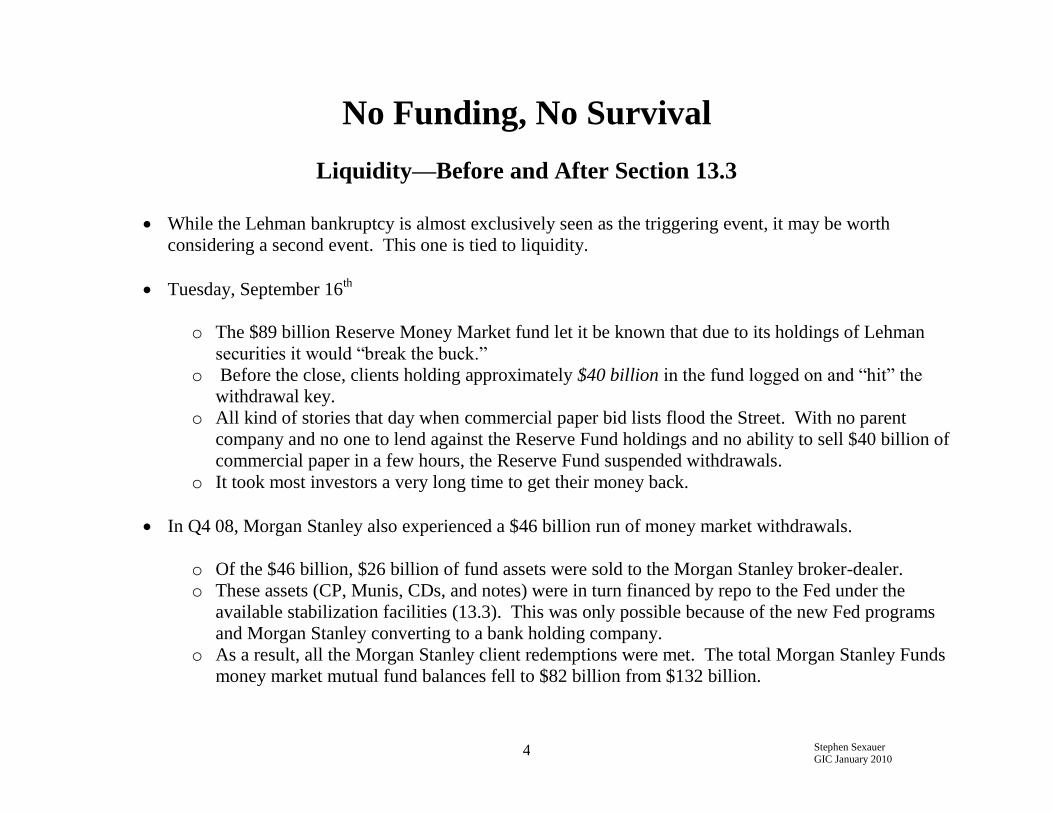

No Funding, No Survival

Liquidity—Before and After Section 13.3

While the Lehman bankruptcy is almost exclusively seen as the triggering event, it may be worth

considering a second event. This one is tied to liquidity.

Tuesday, September 16th

o The $89 billion Reserve Money Market fund let it be known that due to its holdings of Lehman

securities it would “break the buck.”

o Before the close, clients holding approximately $40 billion in the fund logged on and “hit” the

withdrawal key.

o All kind of stories that day when commercial paper bid lists flood the Street. With no parent

company and no one to lend against the Reserve Fund holdings and no ability to sell $40 billion of

commercial paper in a few hours, the Reserve Fund suspended withdrawals.

o It took most investors a very long time to get their money back.

In Q4 08, Morgan Stanley also experienced a $46 billion run of money market withdrawals.

o Of the $46 billion, $26 billion of fund assets were sold to the Morgan Stanley broker-dealer.

o These assets (CP, Munis, CDs, and notes) were in turn financed by repo to the Fed under the

available stabilization facilities (13.3). This was only possible because of the new Fed programs

and Morgan Stanley converting to a bank holding company.

o As a result, all the Morgan Stanley client redemptions were met. The total Morgan Stanley Funds

money market mutual fund balances fell to $82 billion from $132 billion.

Stephen Sexauer GIC January 2010

5

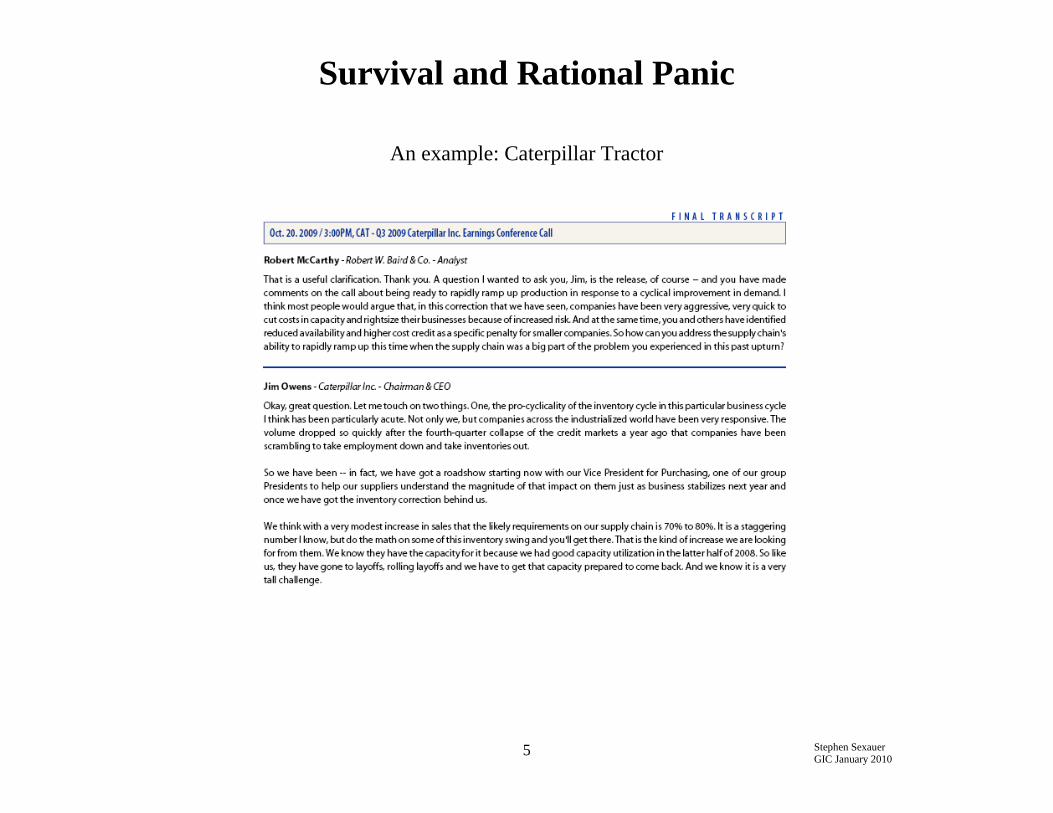

Survival and Rational Panic

An example: Caterpillar Tractor

Stephen Sexauer GIC January 2010

6

A Sudden Stop in Everything Everywhere

Stephen Sexauer GIC January 2010

7

Saved

The Superheroes:

The Fed and rule 13.3

The FDIC guarantees bank debt

The Non-bank Bank Run and the Bank Run end

Stephen Sexauer GIC January 2010

8

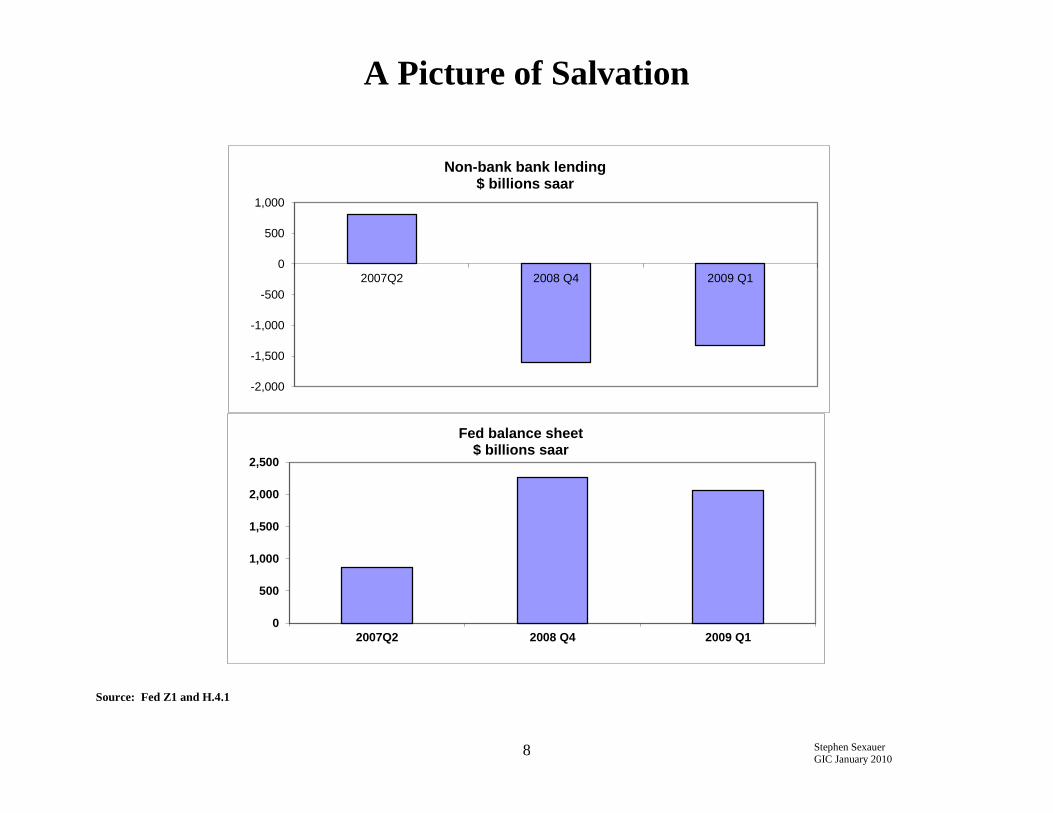

A Picture of Salvation

-2,000

-1,500

-1,000

-500

0

500

1,000

2007Q2 2008 Q4 2009 Q1

Non-bank bank lending$ billions saar

0

500

1,000

1,500

2,000

2,500

2007Q2 2008 Q4 2009 Q1

Fed balance sheet$ billions saar

Source: Fed Z1 and H.4.1

Stephen Sexauer GIC January 2010

9

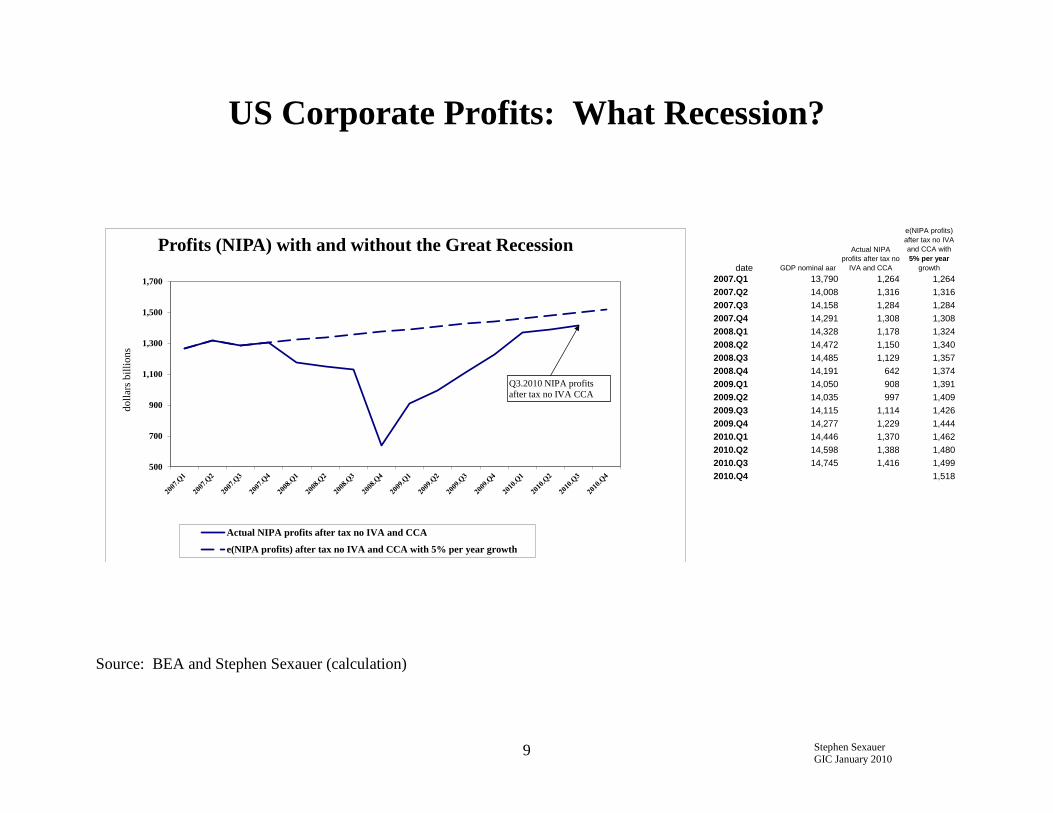

US Corporate Profits: What Recession?

date GDP nominal aar

Actual NIPA

profits after tax no

IVA and CCA

e(NIPA profits)

after tax no IVA

and CCA with

5% per year

growth

2007.Q1 13,790 1,264 1,264

2007.Q2 14,008 1,316 1,316

2007.Q3 14,158 1,284 1,284

2007.Q4 14,291 1,308 1,308

2008.Q1 14,328 1,178 1,324

2008.Q2 14,472 1,150 1,340

2008.Q3 14,485 1,129 1,357

2008.Q4 14,191 642 1,374

2009.Q1 14,050 908 1,391

2009.Q2 14,035 997 1,409

2009.Q3 14,115 1,114 1,426

2009.Q4 14,277 1,229 1,444

2010.Q1 14,446 1,370 1,462

2010.Q2 14,598 1,388 1,480

2010.Q3 14,745 1,416 1,499

2010.Q4 1,518500

700

900

1,100

1,300

1,500

1,700

do

llar

s b

illi

on

s

Profits (NIPA) with and without the Great Recession

Actual NIPA profits after tax no IVA and CCA

e(NIPA profits) after tax no IVA and CCA with 5% per year growth

Q3.2010 NIPA profits

after tax no IVA CCA

Source: BEA and Stephen Sexauer (calculation)

Stephen Sexauer GIC January 2010

10

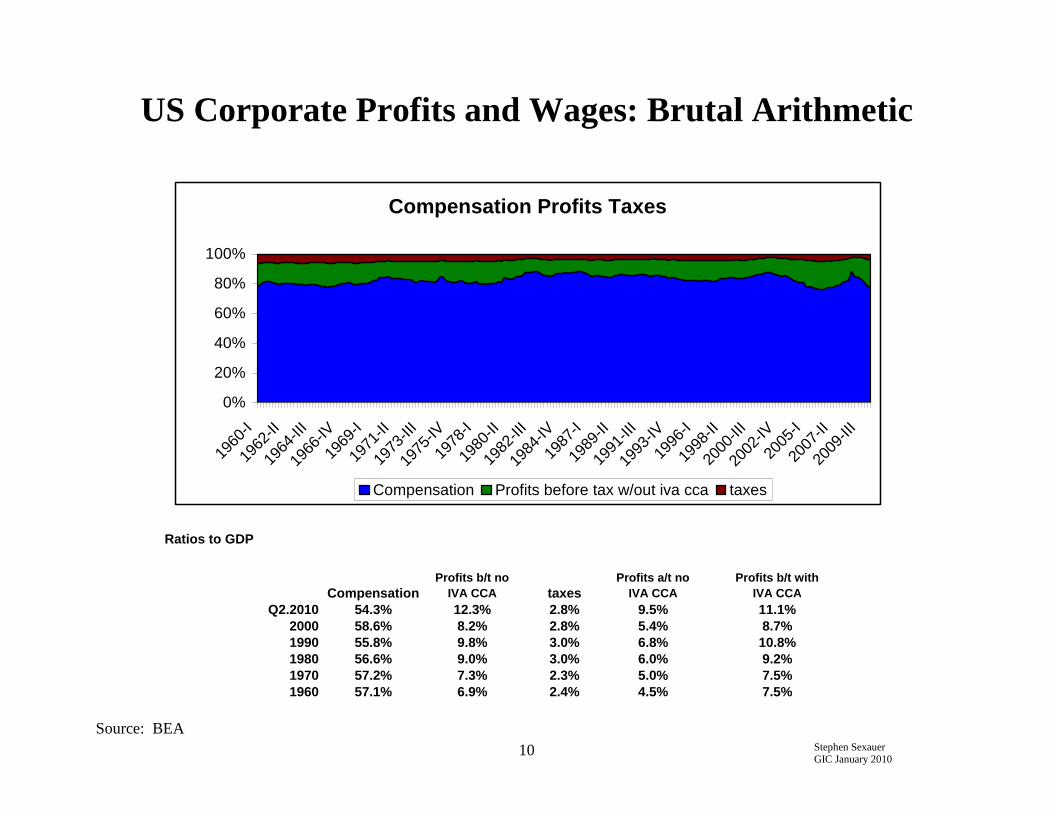

US Corporate Profits and Wages: Brutal Arithmetic

Ratios to GDP

Compensation

Profits b/t no

IVA CCA taxes

Profits a/t no

IVA CCA

Profits b/t with

IVA CCA

Q2.2010 54.3% 12.3% 2.8% 9.5% 11.1%

2000 58.6% 8.2% 2.8% 5.4% 8.7%

1990 55.8% 9.8% 3.0% 6.8% 10.8%

1980 56.6% 9.0% 3.0% 6.0% 9.2%

1970 57.2% 7.3% 2.3% 5.0% 7.5%

1960 57.1% 6.9% 2.4% 4.5% 7.5%

Compensation Profits Taxes

0%

20%

40%

60%

80%

100%

196

0-I

196

2-II

196

4-III

196

6-IV

196

9-I

197

1-II

197

3-III

197

5-IV

197

8-I

198

0-II

198

2-III

198

4-IV

198

7-I

198

9-II

199

1-III

199

3-IV

199

6-I

199

8-II

200

0-III

200

2-IV

200

5-I

200

7-II

200

9-III

Compensation Profits before tax w/out iva cca taxes

Source: BEA

Stephen Sexauer GIC January 2010

11

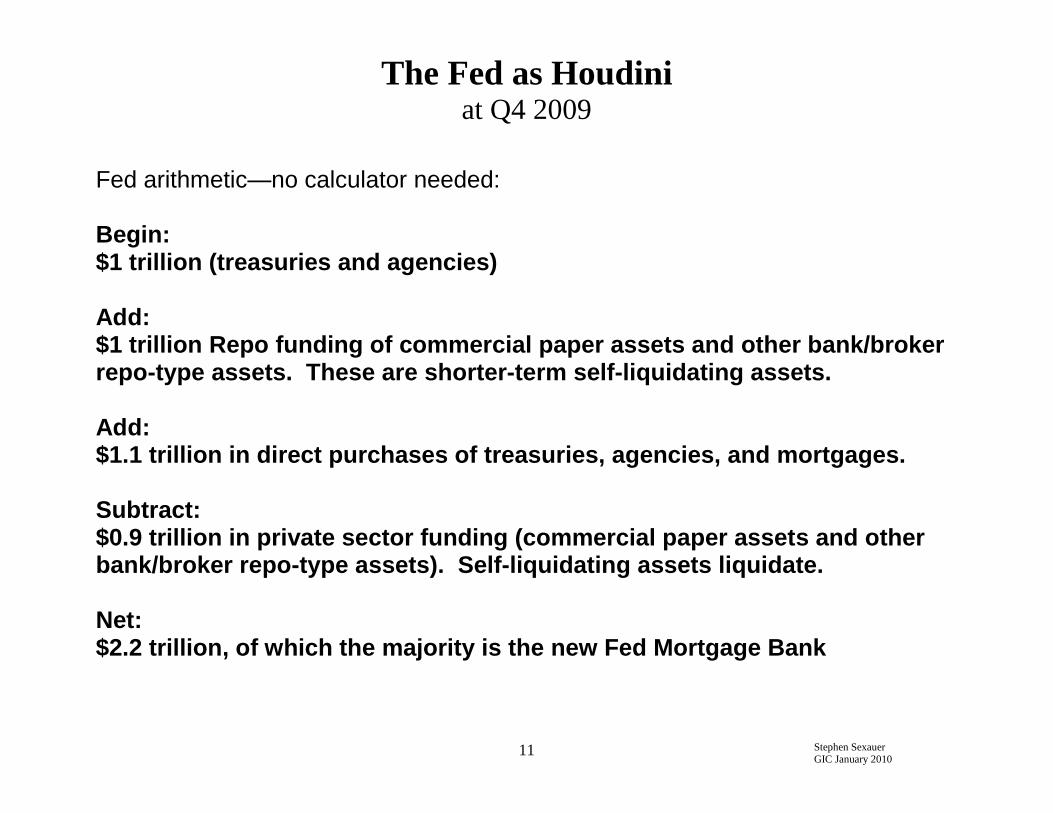

The Fed as Houdini at Q4 2009

Fed arithmetic—no calculator needed: Begin: $1 trillion (treasuries and agencies) Add: $1 trillion Repo funding of commercial paper assets and other bank/broker repo-type assets. These are shorter-term self-liquidating assets. Add: $1.1 trillion in direct purchases of treasuries, agencies, and mortgages. Subtract: $0.9 trillion in private sector funding (commercial paper assets and other bank/broker repo-type assets). Self-liquidating assets liquidate. Net: $2.2 trillion, of which the majority is the new Fed Mortgage Bank

Stephen Sexauer GIC January 2010

12

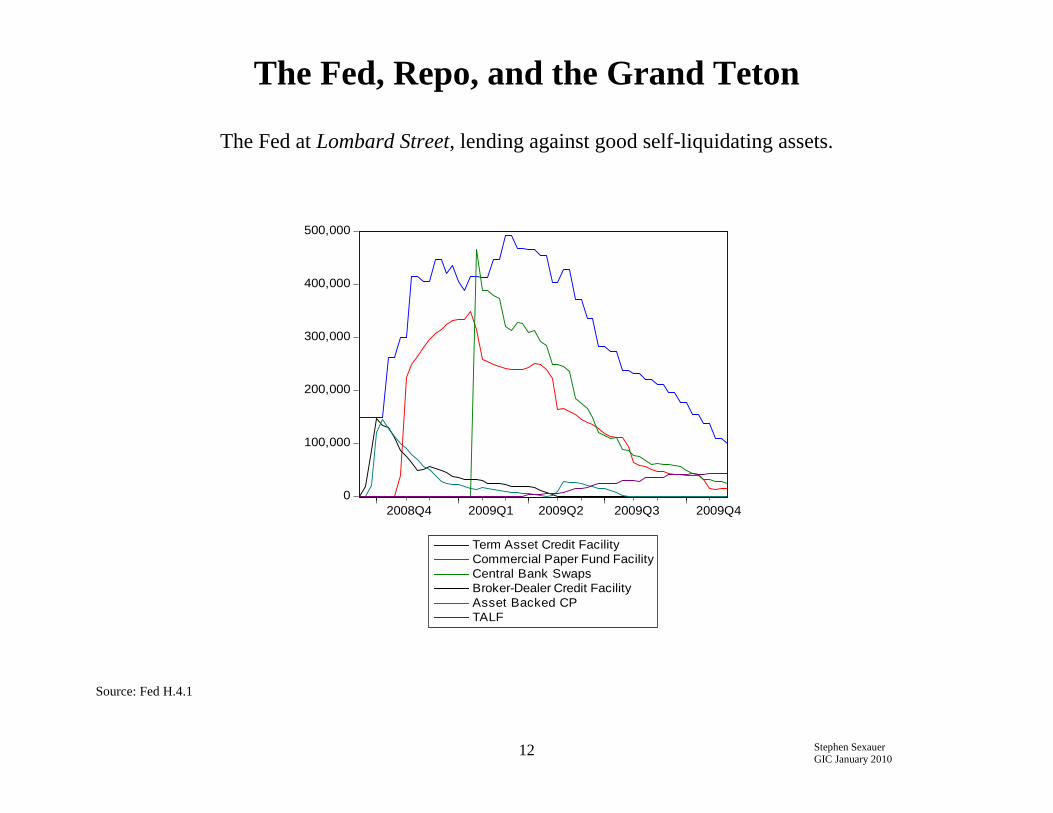

The Fed, Repo, and the Grand Teton

The Fed at Lombard Street, lending against good self-liquidating assets.

0

100,000

200,000

300,000

400,000

500,000

2008Q4 2009Q1 2009Q2 2009Q3 2009Q4

Term Asset Credit Facility

Commercial Paper Fund Facility

Central Bank Swaps

Broker-Dealer Credit Facility

Asset Backed CP

TALF

Source: Fed H.4.1

Stephen Sexauer GIC January 2010

13

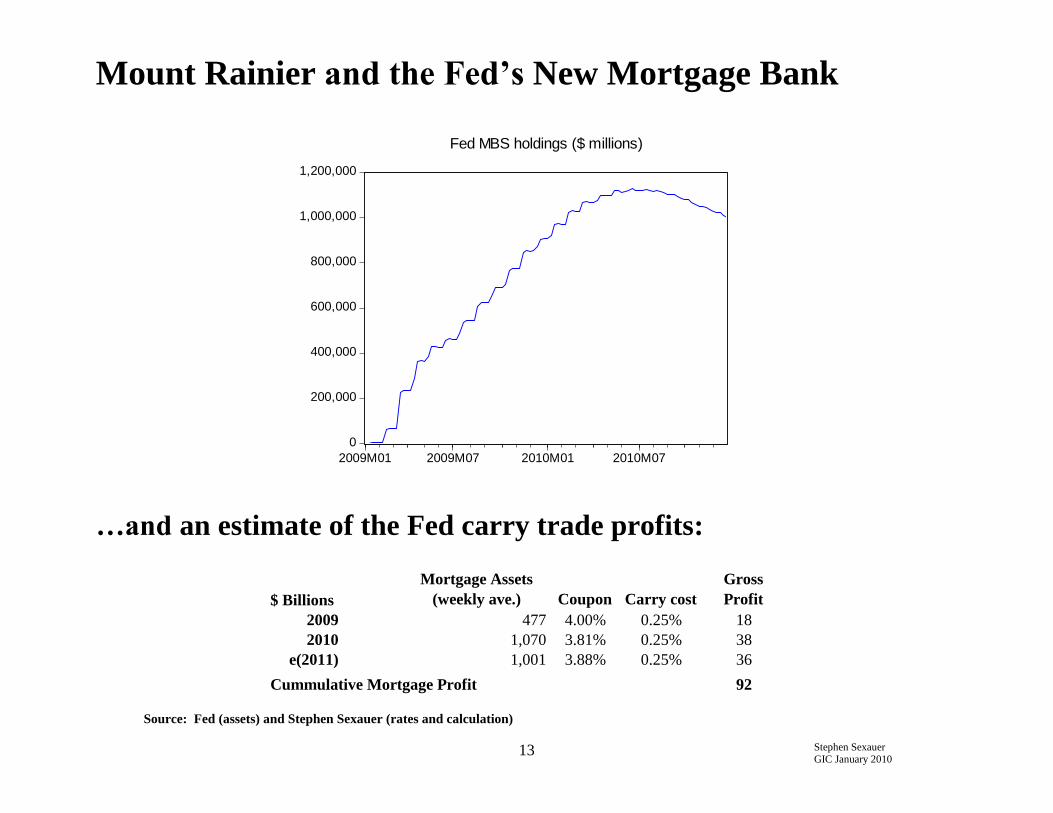

Mount Rainier and the Fed’s New Mortgage Bank

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2009M01 2009M07 2010M01 2010M07

Fed MBS holdings ($ millions)

…and an estimate of the Fed carry trade profits:

$ Billions

Mortgage Assets

(weekly ave.) Coupon Carry cost

Gross

Profit

2009 477 4.00% 0.25% 18

2010 1,070 3.81% 0.25% 38

e(2011) 1,001 3.88% 0.25% 36

Cummulative Mortgage Profit 92

Source: Fed (assets) and Stephen Sexauer (rates and calculation)

Stephen Sexauer GIC January 2010

14

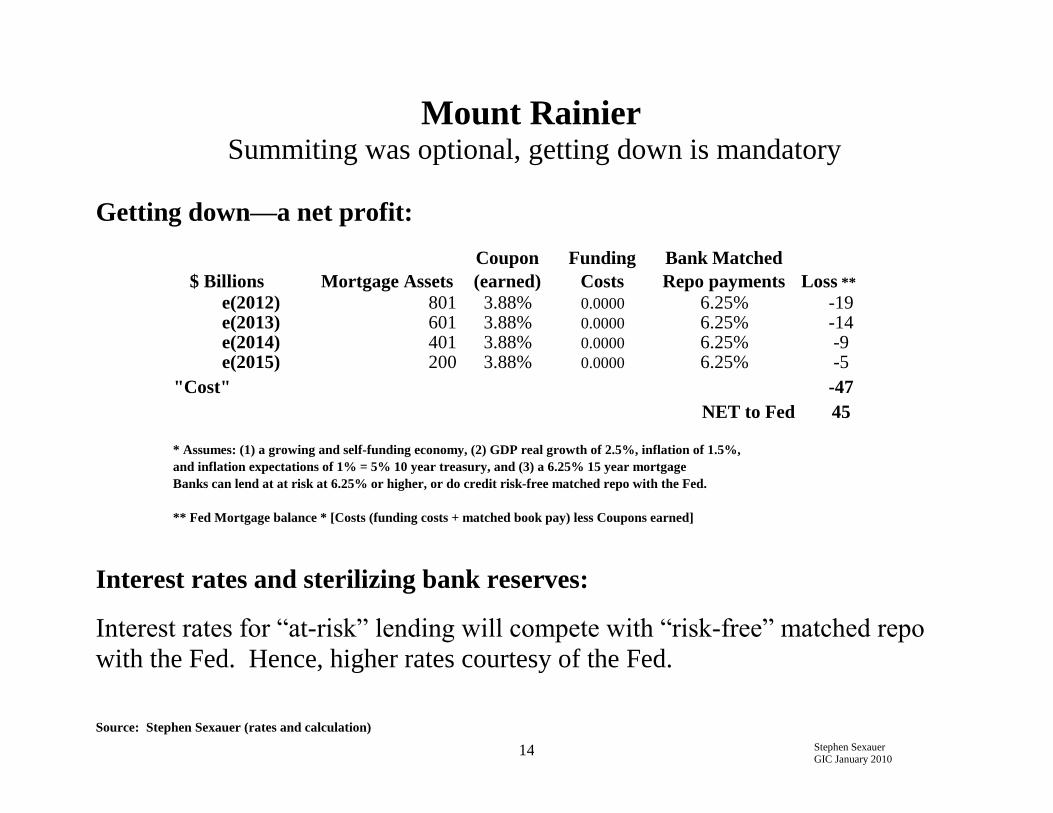

Mount Rainier Summiting was optional, getting down is mandatory

Getting down—a net profit:

$ Billions Mortgage Assets

Coupon

(earned)

Funding

Costs

Bank Matched

Repo payments Loss **

e(2012) 801 3.88% 0.0000 6.25% -19e(2013) 601 3.88% 0.0000 6.25% -14e(2014) 401 3.88% 0.0000 6.25% -9e(2015) 200 3.88% 0.0000 6.25% -5

"Cost" -47

NET to Fed 45

* Assumes: (1) a growing and self-funding economy, (2) GDP real growth of 2.5%, inflation of 1.5%,

and inflation expectations of 1% = 5% 10 year treasury, and (3) a 6.25% 15 year mortgage

Banks can lend at at risk at 6.25% or higher, or do credit risk-free matched repo with the Fed.

** Fed Mortgage balance * [Costs (funding costs + matched book pay) less Coupons earned]

Interest rates and sterilizing bank reserves:

Interest rates for “at-risk” lending will compete with “risk-free” matched repo

with the Fed. Hence, higher rates courtesy of the Fed.

Source: Stephen Sexauer (rates and calculation)

Stephen Sexauer GIC January 2010

15

How Long Does a Growing Global Economy Stay on the Fed’s “Rope Team”?

Stephen Sexauer GIC January 2010

16

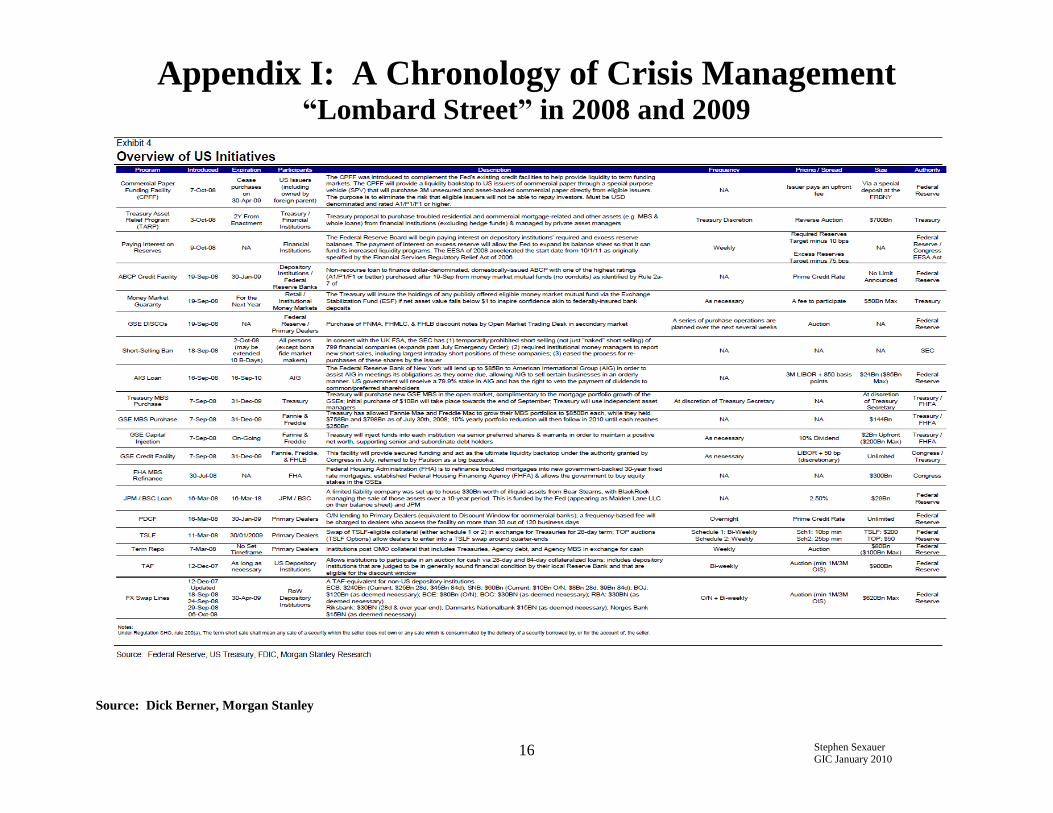

Appendix I: A Chronology of Crisis Management “Lombard Street” in 2008 and 2009

Source: Dick Berner, Morgan Stanley

Stephen Sexauer GIC January 2010

17

Stephen Sexauer

Allianz Global Investors Solutions: Chief Investment Officer

Allianz Global Investors: Performance and Risk: Performance Portal and Risk-Return analysis for AGI WW equity portfolios

(2007-2008)

Allianz Global Investors-Nicholas Applegate Capital Management: Portfolio manager Large-cap Core and Large-cap Value

(2003-2004)

Morgan Stanley Asset Management (1989 – 2002)

Portfolio manager Large-cap value; application of optimization techniques

Risk structures for US Value and Growth portfolios

Salomon Brothers: (1988-1989)

Mr. Sexauer holds an MBA from the University of Chicago (economics and statistics) and a BS (economics) from the

University of Illinois.

Economic data in this presentation are derived from internal research publicly available statistics published by the U.S.

Federal Reserve, the Government of Canada, the U.S. Department of Commerce and the International Monetary Fund.

The information herein is provided for informational purposes only and should not be construed as a recommendation of any

security, strategy or investment product, nor an offer or solicitation for the purchase or sale of any financial instrument. This

material contains the current opinions of the author, which are subject to change without notice.