aleman-chile_latin_america_us_policy jan 1411

DESCRIPTION

“Monetary Policy, Fiscal Policy, Devaluation & The China/Wal-Mart Effect” Eugenio J. Aleman, Director and Senior Economist January 17, 2011 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 2 Source: BCRA, Wells Fargo Securities, LLC 6 Jan-9 1 Jan-0 2 Jan-0 Economics 4 J an-9 8 J an-0 4 J an-0 8 J an-9 3 J an-0 J an-9 3 -10 10 20 30 40 50 (% change year-over-year) Source: INDEC, Wells Fargo Securities, LLC 0 -0 -1 0TRANSCRIPT

“Monetary Policy, Fiscal Policy, Devaluation & The China/Wal-Mart Effect”Eugenio J. Aleman, Director and Senior EconomistJanuary 17, 2011

Economics 2

Argentina: Large Currency Devaluation

Abandonment of the Convertibility Law:

Devaluation of 70 percent in one year

Source: BCRA, Wells Fargo Securities, LLC

Argentine Peso (pesos per U.S. dollar)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Jan-94

Jan-95

Jan-96

Jan-97

Jan-98

J an-99

Jan-00

Jan-01

J an-02

Jan-03

Jan-04

Jan-05

J an-06

Jan-07

Jan-08

Jan-09

Jan-10

Economics 3

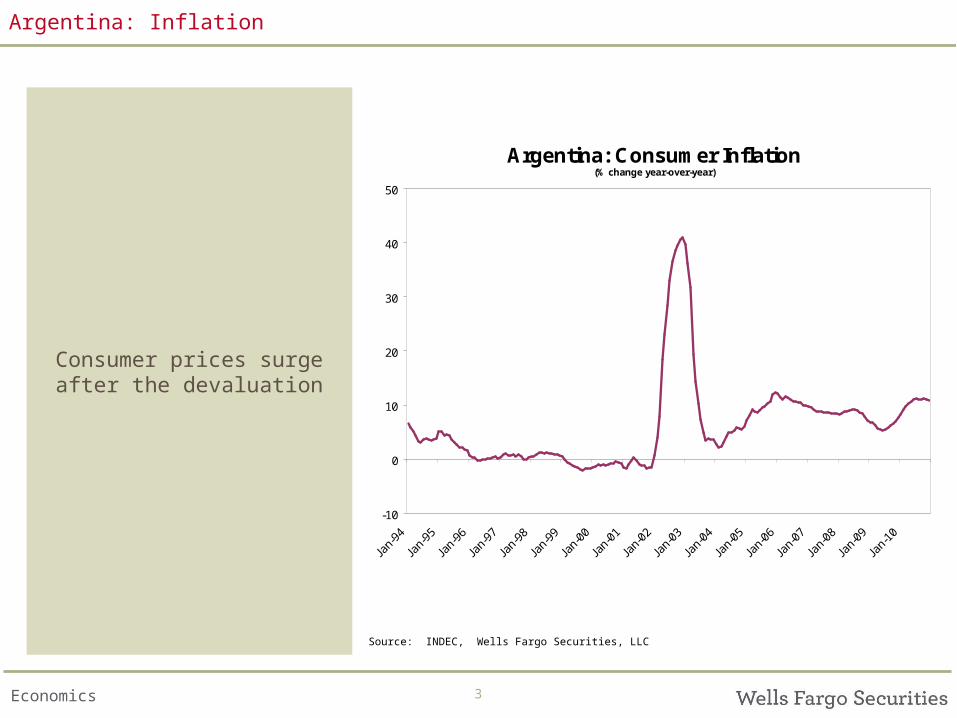

Argentina: Inflation

Consumer prices surge after the devaluation

Argentina: Consumer Inflation(% change year-over-year)

-10

0

10

20

30

40

50

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Source: INDEC, Wells Fargo Securities, LLC

Economics 4

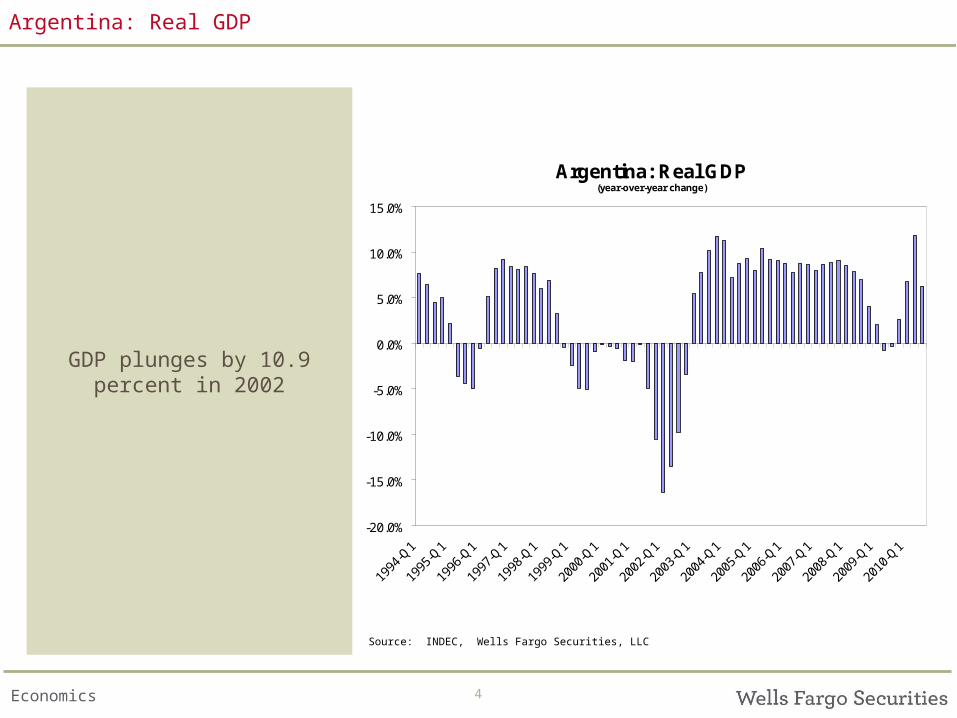

Argentina: Real GDP

GDP plunges by 10.9 percent in 2002

Argentina: Real GDP(year-over-year change)

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: INDEC, Wells Fargo Securities, LLC

Economics 5

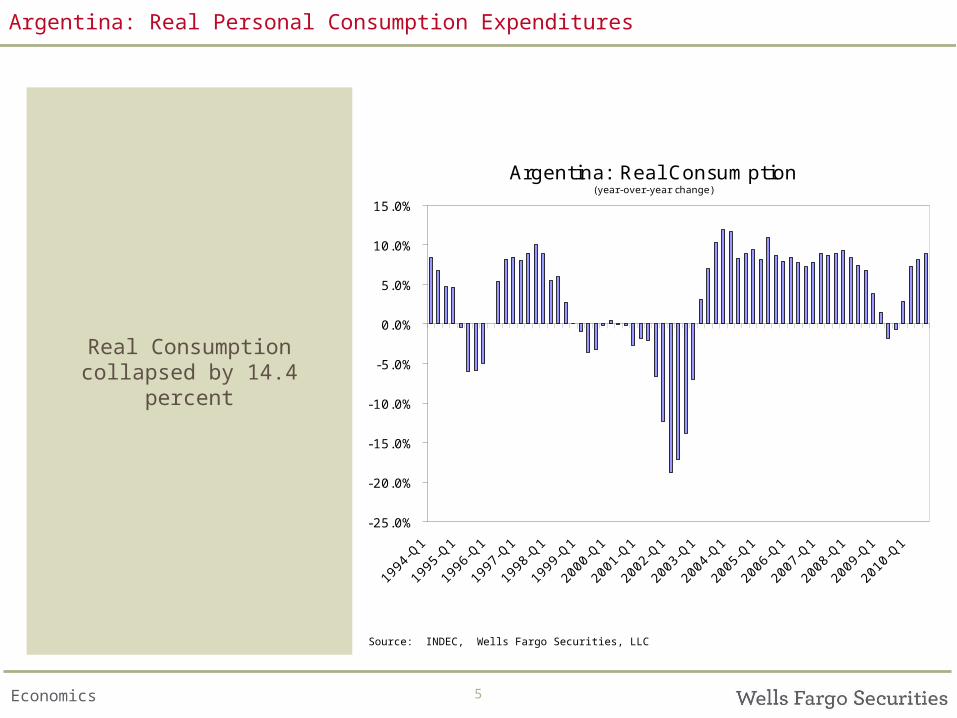

Argentina: Real Personal Consumption Expenditures

Real Consumption collapsed by 14.4 percent

Argentina: Real Consumption(year-over-year change)

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: INDEC, Wells Fargo Securities, LLC

Economics 6

Argentina: Current Account

The Current Account changes from a deficit to a

strong positive

Argentina: Current Account(percentage of GDP)

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: INDEC, Wells Fargo Securities, LLC

Economics 7

Brazil: Devaluation of the Real in two periods

Brazil abandons the “managed peg” in January

of 1999

Brazilian Currency (reais per U.S. dollars, monthly average)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-94

J an-95

Jan-96

Jan-97

Jan-98

Jan-99

J an-00

J an-01

Jan-02

Jan-03

J an-04

Jan-05

Jan-06

J an-07

J an-08

J an-09

Jan-10

Source: BCB, Wells Fargo Securities, LLC

Economics 8

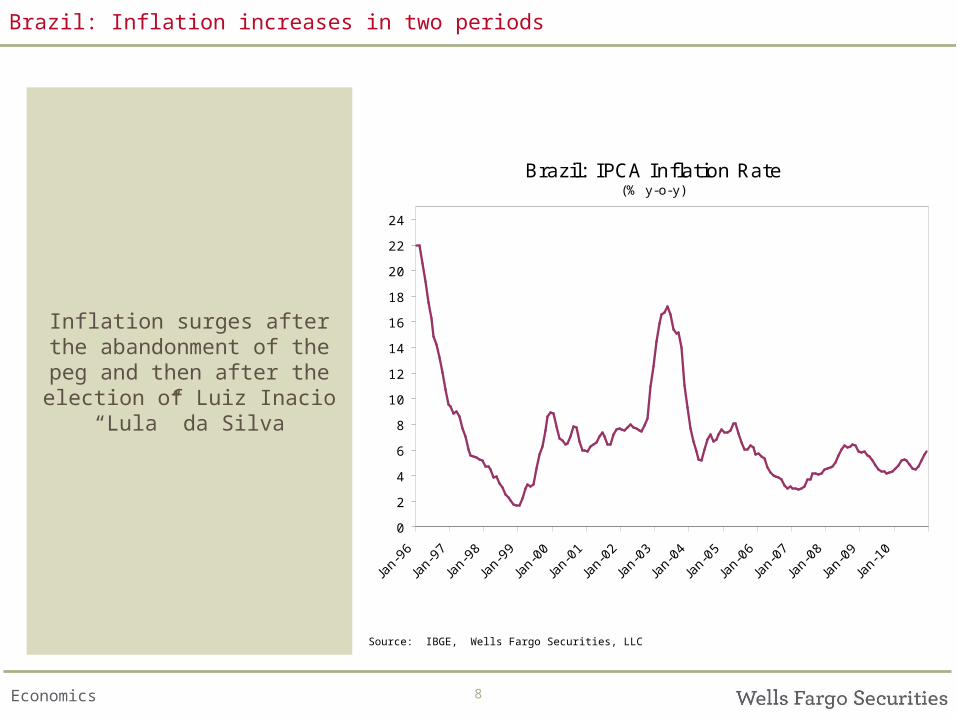

Brazil: Inflation increases in two periods

Inflation surges after the abandonment of the peg

and then after the election of Luiz Inacio “Lula” da

Silva

Brazil: IPCA Inflation Rate(% y-o-y)

02468

1012141618202224

Jan-96

Jan-97

Jan-98

J an-99

Jan-00

Jan-01

J an-02

Jan-03

Jan-04

J an-05

Jan-06

Jan-07

Jan-08

J an-09

Jan-10

Source: IBGE, Wells Fargo Securities, LLC

Economics 9

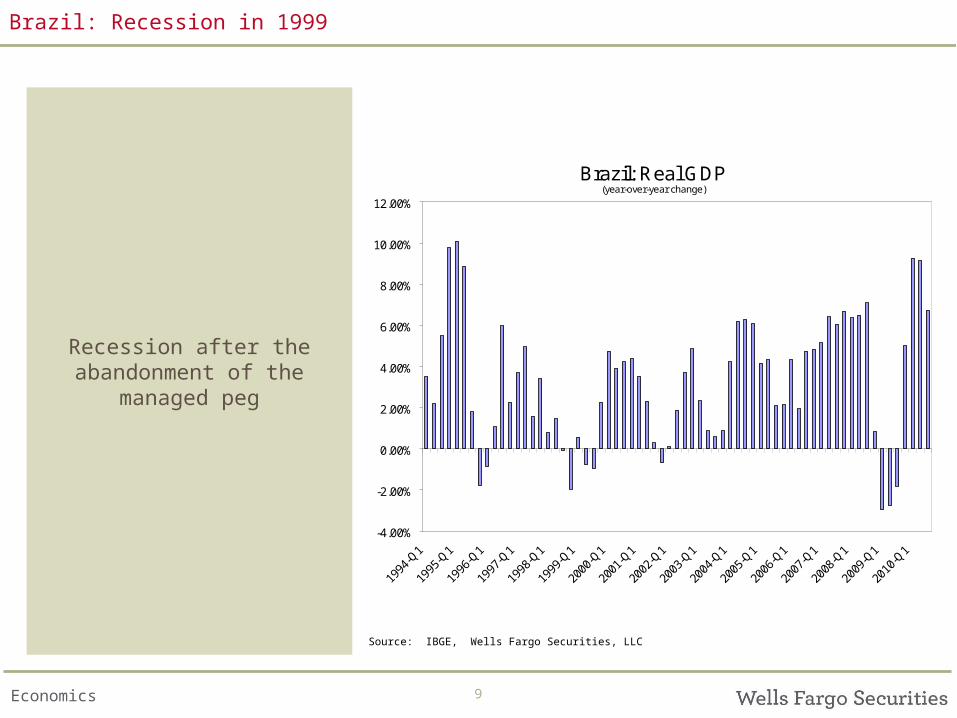

Brazil: Recession in 1999

Recession after the abandonment of the

managed peg

Brazil: Real GDP(year-over-year change)

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: IBGE, Wells Fargo Securities, LLC

Economics 10

Brazil: Real Personal Consumption Expenditures

Real personal consumption expenditures drops after the

abandonment of the managed peg

Brazil: Real Consumption(year-over-year change)

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: IBGE, Wells Fargo Securities, LLC

Economics 11

Brazil: Current Account

Current account is not affected by the

abandonment of the managed peg but it is after

the second round of devaluation after the

election of Lula

Brazil: Current Account (percentage of GDP)

-1.5

-1.0

-0.5

0.0

0.5

1.0

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: IBGE, Wells Fargo Securities, LLC

Economics 12

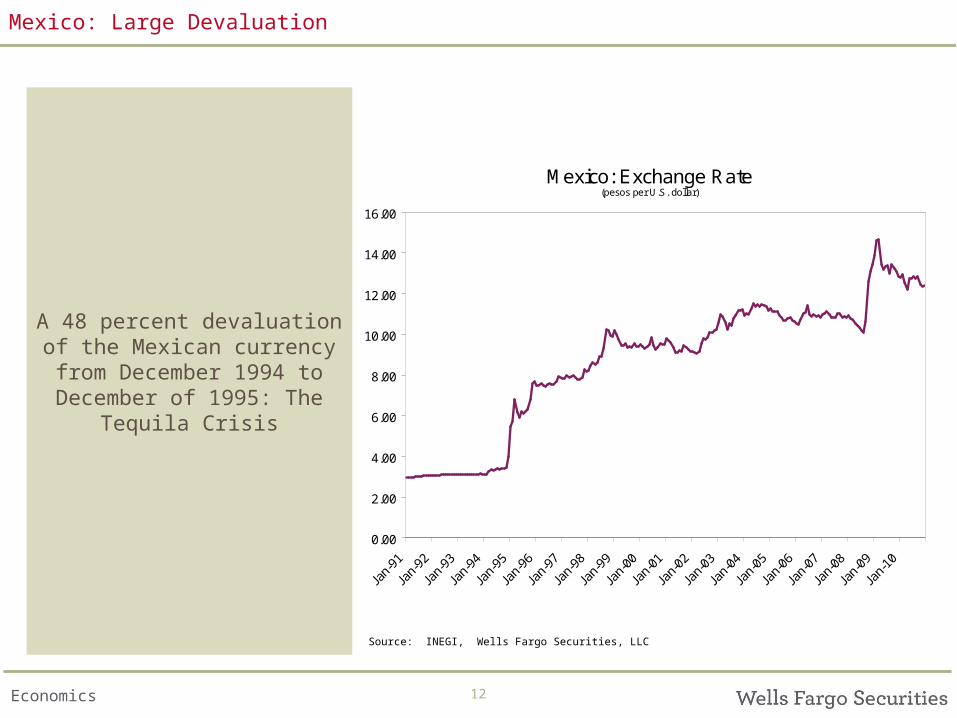

Mexico: Large Devaluation

A 48 percent devaluation of the Mexican currency from

December 1994 to December of 1995: The

Tequila Crisis

Mexico: Exchange Rate(pesos per U.S. dollar)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Jan-9

1

Jan-9

2

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Source: INEGI, Wells Fargo Securities, LLC

Economics 13

Mexico: High Inflation

Inflation surges after the devaluation in 1994

Mexico:Consumer Inflation (% change year-over-year)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Jan-91

Jan-92

Jan-93

J an-94

J an-95

Jan-96

J an-97

Jan-98

Jan-99

Jan-00

J an-01

Jan-02

J an-03

Jan-04

J an-05

J an-06

Jan-07

J an-08

Jan-09

Jan-10

Source: INEGI, Wells Fargo Securities, LLC

Economics

Mexico: Real GDP plunges

Real GDP plunges by 6.2 percent after the

devaluation

Mexico: Real GDP(year-over-year change)

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: INEGI, Wells Fargo Securities, LLC

Economics 15

Mexico: Real Personal Consumption Expenditures

Real personal consumption expenditures collapses by

9.5 percent

Mexico: Real Consumption(year-over-year change)

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: INEGI, Wells Fargo Securities, LLC

Economics 16

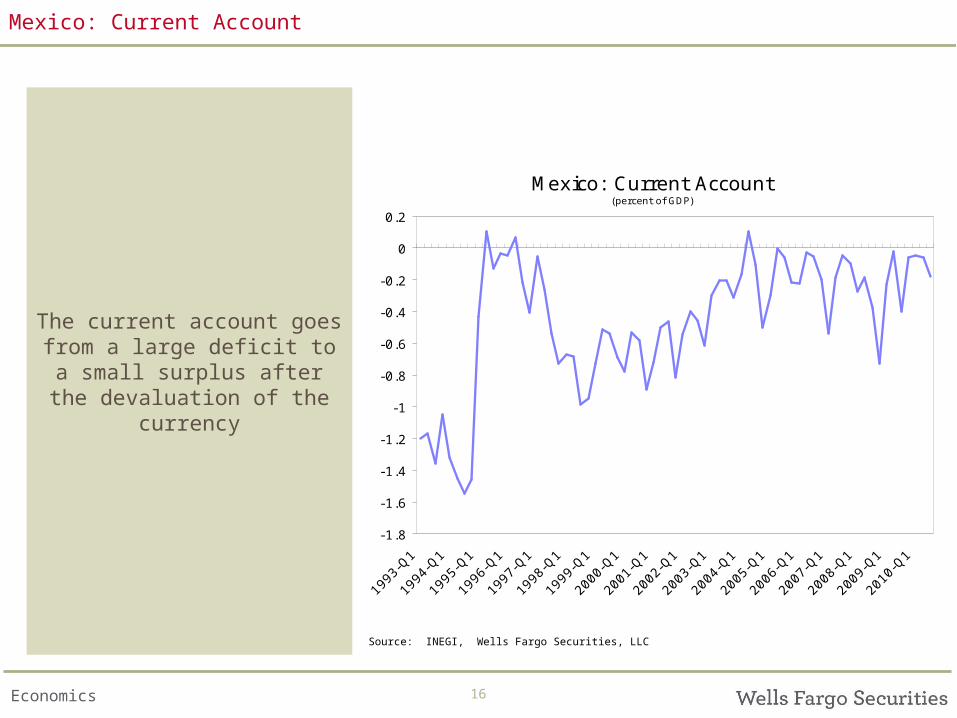

Mexico: Current Account

The current account goes from a large deficit to a small surplus after the

devaluation of the currency

Mexico: Current Account(percent of GDP)

-1.8

-1.6

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

1993

-Q1

1994

-Q1

1995

-Q1

1996

-Q1

1997

-Q1

1998

-Q1

1999

-Q1

2000

-Q1

2001

-Q1

2002

-Q1

2003

-Q1

2004

-Q1

2005

-Q1

2006

-Q1

2007

-Q1

2008

-Q1

2009

-Q1

2010

-Q1

Source: INEGI, Wells Fargo Securities, LLC

Economics 17

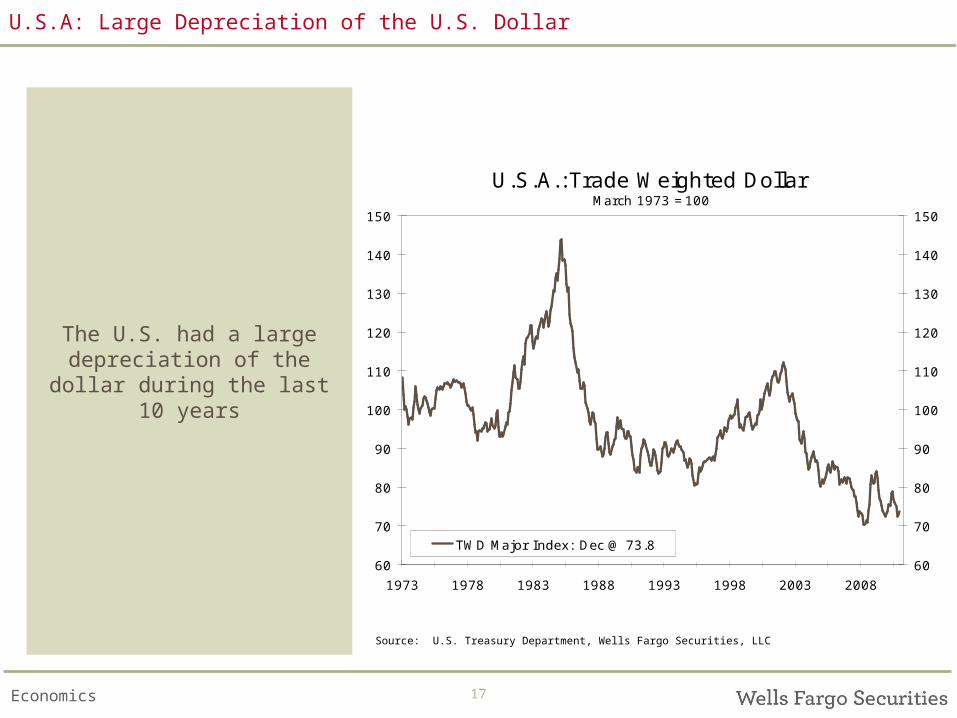

U.S.A: Large Depreciation of the U.S. Dollar

The U.S. had a large depreciation of the dollar during the last 10 years

U.S.A.:Trade Weighted Dollar March 1973 =100

60

70

80

90

100

110

120

130

140

150

1973 1978 1983 1988 1993 1998 2003 200860

70

80

90

100

110

120

130

140

150

TWD Major Index: Dec @ 73.8

Source: U.S. Treasury Department, Wells Fargo Securities, LLC

Economics 18

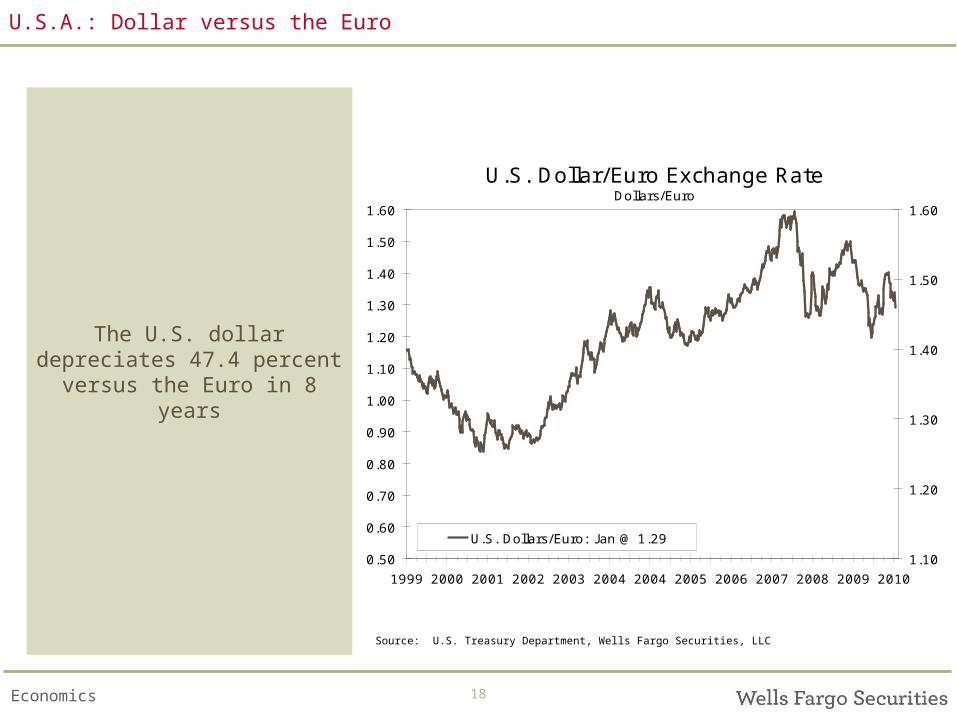

U.S.A.: Dollar versus the Euro

The U.S. dollar depreciates 47.4 percent versus the

Euro in 8 years

U.S. Dollar/Euro Exchange RateDollars/Euro

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1999 2000 2001 2002 2003 2004 2004 2005 2006 2007 2008 2009 20101.10

1.20

1.30

1.40

1.50

1.60

U.S. Dollars/Euro: J an @ 1.29

Source: U.S. Treasury Department, Wells Fargo Securities, LLC

Economics 19

U.S.A.: Consumer Prices

U.S. Consumer Prices are not affected significantly by the depreciation of the U.S.

dollar

U.S. Consumer Price IndexYear-over-Year Percent Change

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

92 94 96 98 00 02 04 06 08 10-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

CPI : Dec @ 1.5%

Source: U.S. Department of Labor, Wells Fargo Securities, LLC

Economics 20

U.S.A.: Real GDP

While Real GDP weakens during the short recession

in 2001 it continues to grow until the Great Recession in

2008

U.S.A.: Real GDPBars = Compound Annual Rate Line = Yr/Yr % Change

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Real GDP: Q3 @ 2.6%Real GDP: Q3 @ 3.2%

Source: U.S. Department of Commerce, Wells Fargo Securities, LLC

Economics 21

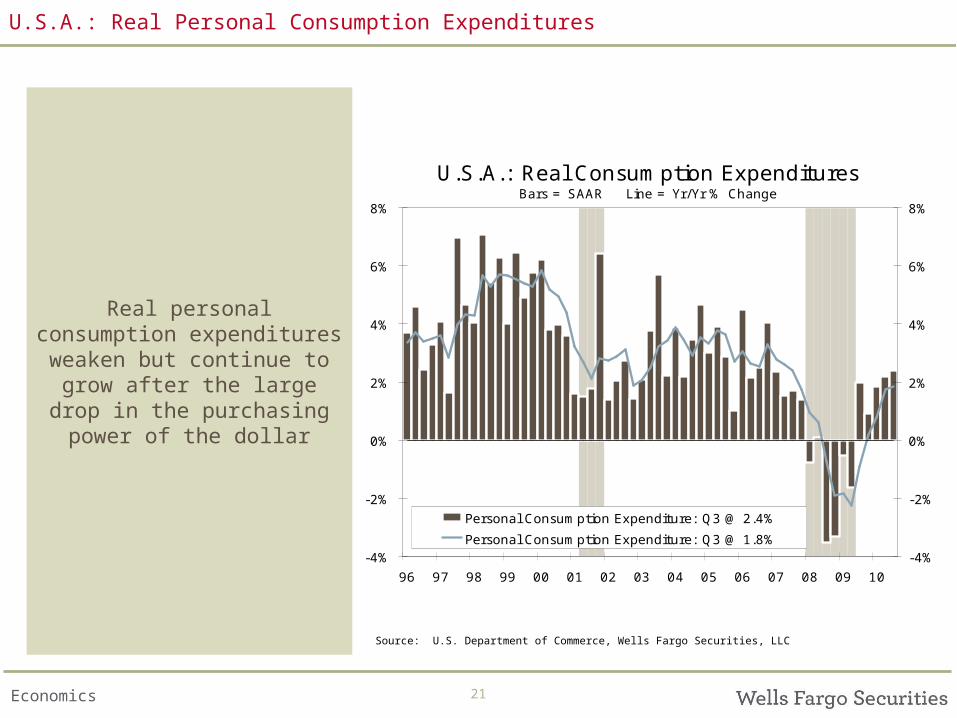

U.S.A.: Real Personal Consumption Expenditures

Real personal consumption expenditures weaken but continue to grow after the

large drop in the purchasing power of the

dollar

U.S.A.: Real Consumption ExpendituresBars = SAAR Line = Yr/Yr % Change

-4%

-2%

0%

2%

4%

6%

8%

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10-4%

-2%

0%

2%

4%

6%

8%

Personal Consumption Expenditure: Q3 @ 2.4%Personal Consumption Expenditure: Q3 @ 1.8%

Source: U.S. Department of Commerce, Wells Fargo Securities, LLC

Economics 22

U.S.A.: Monetary Policy Helps

The U.S. Federal Reserve conducts a very expansive

monetary policy

Source: U.S. Department of Commerce, Wells Fargo Securities, LLC

U.S. Federal Reserve Target Rate

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

2000 2002 2004 2006 2008 20100.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%US Federal Reserve: J an @ 0.25%

Economics 23

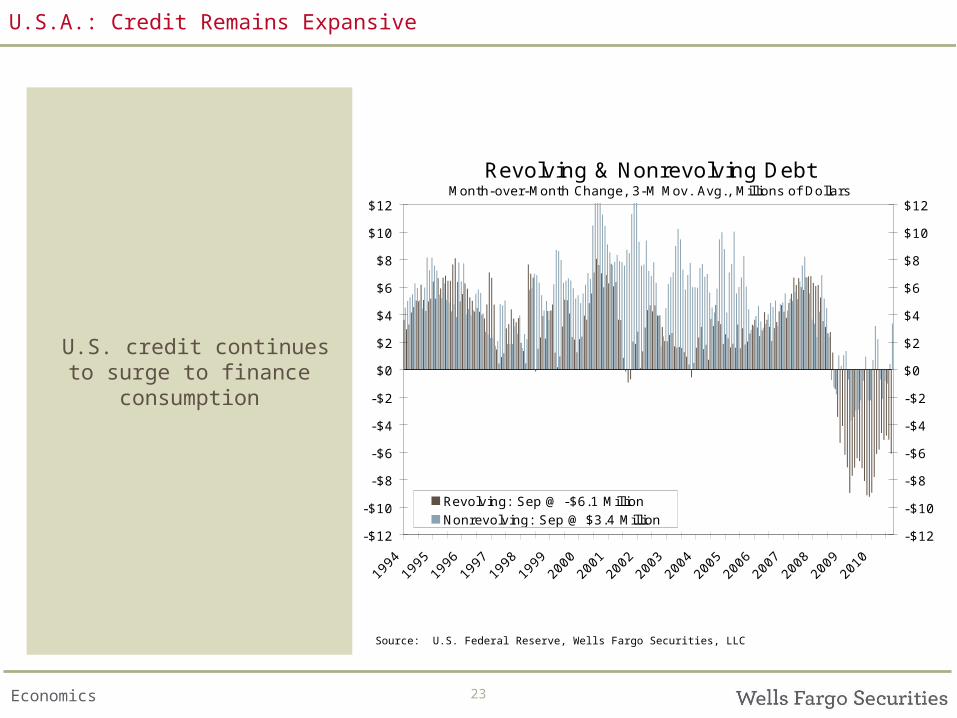

U.S.A.: Credit Remains Expansive

U.S. credit continues to surge to finance

consumption

Revolving & Nonrevolving DebtMonth-over-Month Change, 3-M Mov. Avg., Millions of Dollars

-$12

-$10

-$8

-$6

-$4

-$2

$0

$2

$4

$6

$8

$10

$12

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

-$12

-$10

-$8

-$6

-$4

-$2

$0

$2

$4

$6

$8

$10

$12

Revolving: Sep @ -$6.1 MillionNonrevolving: Sep @ $3.4 Million

Source: U.S. Federal Reserve, Wells Fargo Securities, LLC

Economics 24

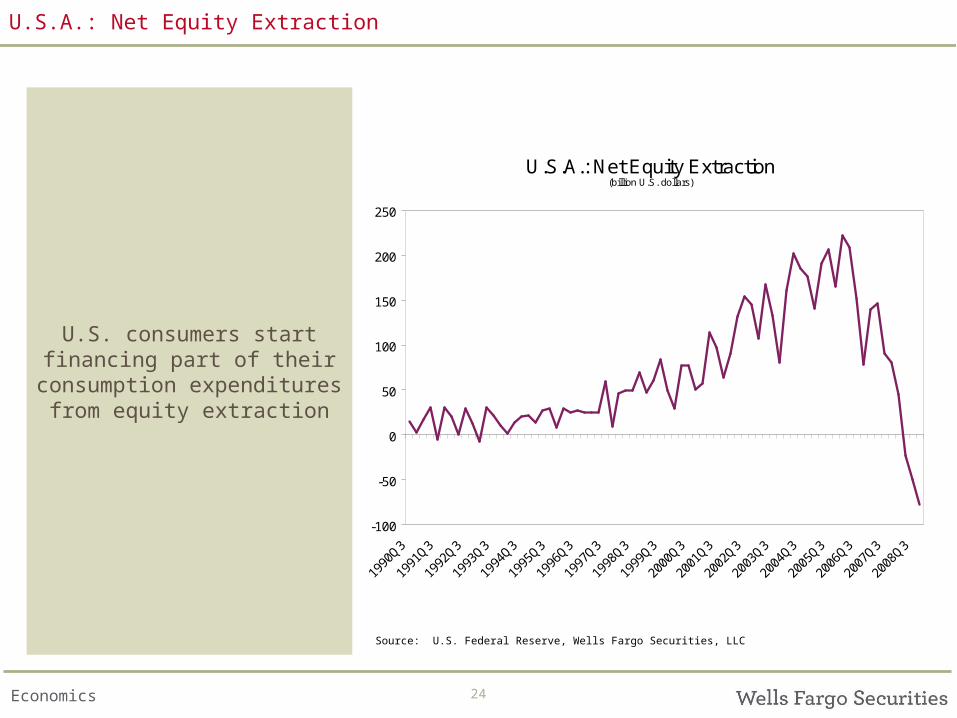

U.S.A.: Net Equity Extraction

U.S. consumers start financing part of their

consumption expenditures from equity extraction

U.S.A.: Net Equity Extraction(billion U.S. dollars)

-100

-50

0

50

100

150

200

250

1990

Q3

1991

Q3

1992

Q3

1993

Q3

1994

Q3

1995

Q3

1996

Q3

1997

Q3

1998

Q3

1999

Q3

2000

Q3

2001

Q3

2002

Q3

2003

Q3

2004

Q3

2005

Q3

2006

Q3

2007

Q3

2008

Q3

Source: U.S. Federal Reserve, Wells Fargo Securities, LLC

Economics 25

U.S.A.: Fiscal Policy Helps

The U.S. government contributes its share with

tax rebates during the Bush administration

Real Disposable IncomeMonth-over-Month Percent Change

-4%

-2%

0%

2%

4%

6%

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10-4%

-2%

0%

2%

4%

6%Real Disposable Income: Nov @ 0.2%

Source: U.S. Department of Commerce, Wells Fargo Securities, LLC

Economics 26

U.S.A.: Household Debt

U.S. household mortgage debt surges to keep up with

expenditures

Household Debt - Consumer & MortgageAs a Percent of Disposable Personal Income

0%

20%

40%

60%

80%

100%

120%

60 65 70 75 80 85 90 95 00 05 100%

20%

40%

60%

80%

100%

120%Consumer Credit: Q3 @ 21.1%Home Mortgages: Q3 @ 88.6%

Source: U.S. Federal Reserve, Wells Fargo Securities, LLC

Economics 27

U.S.A.: Debt Service Ratio

U.S. household debt to service ratio increases

considerably during the period and up until the

Great Recession

Household Debt Service RatioAs a Percent of Disposable Personal Income

10.0%

10.5%

11.0%

11.5%

12.0%

12.5%

13.0%

13.5%

14.0%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 1011.5%

12.0%

12.5%

13.0%

13.5%

14.0%DSR: Q3 @ 11.9%

Source: U.S. Federal Reserve, Wells Fargo Securities, LLC

Economics 28

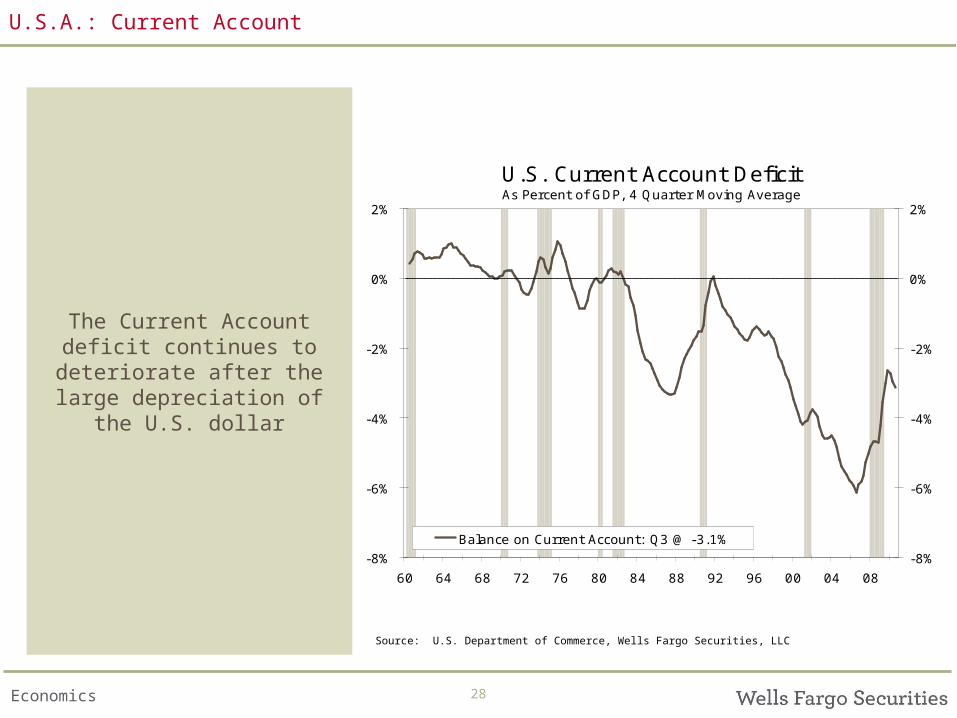

U.S.A.: Current Account

The Current Account deficit continues to deteriorate

after the large depreciation of the U.S. dollar

U.S. Current Account Deficit As Percent of GDP, 4 Quarter Moving Average

-8%

-6%

-4%

-2%

0%

2%

60 64 68 72 76 80 84 88 92 96 00 04 08-8%

-6%

-4%

-2%

0%

2%

Balance on Current Account: Q3 @ -3.1%

Source: U.S. Department of Commerce, Wells Fargo Securities, LLC

Economics 29

U.S.A.: The China/Wal-Mart Effect

Another reason why there was little inflation and little

change in personal consumption expenditures:

The Chinese keep their currency undervalued

Chinese Exchange RateCNY per USD

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

1990 1994 1998 2002 2006 20104.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

CNY per USD: J an @ 6.60

Source: U.S. Department of Commerce, Wells Fargo Securities, LLC

Economics 30

Conclusion

The Day of Reckoning for the U.S. economy is here!

• The Great Recession is just the delayed response to the almost 50 percent devaluation of the U.S. dollar• Monetary policy and fiscal policy, together with lax regulation, contributed to delay the day of reckoning for the U.S. consumer and the U.S. economy• The U.S. current account deficit is deteriorating again which means that U.S. consumers are still consuming too much compared to U.S. production • U.S. savings are increasing, which is good for the medium to long run, even though this is actually hoarding rather than saving• But policies, both fiscal and monetary, remain extremely expansive and could make the U.S. recovery very volatile, especially if consumers start to reduce savings again

Economics 31

Wells Fargo Securities, LLC Economics Group

John Silvia, Chief Economist [email protected] Mark Vitner, Senior Economist [email protected] Jay Bryson, Global Economist [email protected] Scott Anderson, Senior Economist [email protected] Eugenio Aleman, Senior Economist [email protected] Sam Bullard, Senior Economist [email protected]

Anika Khan, Economist [email protected] Azhar Iqbal, Econometrician [email protected] Ed Kashmarek, Economist [email protected] Tim Quinlan, Economist [email protected] Michael Brown, Economist [email protected]

Tyler Kruse, Economic Analyst [email protected] Joe Seydl, Economic Analyst [email protected] Sarah Watt, Economic Analyst [email protected]

Peg Gavin [email protected] Carol Nighengale [email protected]

Economists

Senior Economists

Executive Assistant

Global Head of Research and Economics: Diane Schumaker-Krieg

Chief Economist: John Silvia

301 S. College StreetMAC D1053-077

Charlotte, NC28288

a

Wells Fargo Securities Economics Group publications are produced by Wells Fargo Securities, LLC, a U.S broker-dealer registered with the U.S. Securities and Exchange Commission, the Financial Industry Regulatory Authority, and the Securities Investor Protection Corp. Wells Fargo Securities, LLC, distributes these publications directly and through subsidiaries including, but not limited to, Wells Fargo & Company, Wells Fargo Bank N.A, Wells Fargo Advisors, LLC, and Wells Fargo Securities International Limited. The information and opinions herein are for general information use only. Wells Fargo Securities, LLC does not guarantee their accuracy or completeness, nor does Wells Fargo Securities, LLC assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice, are for general information only and are not intended as an offer or solicitation with respect to the purchase or sales of any security or as personalized investment advice. Wells Fargo Securities, LLC is a separate legal entity and distinct from affiliated banks and is a wholly owned subsidiary of Wells Fargo & Company © 2010 Wells Fargo Securities, LLC.

SECURITIES: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE

Economic Analysts