smud’s pv program: - donald aitken associates€¦ · web viewit is also important to realize...

TRANSCRIPT

SMUD PV PROGRAM REVIEW

SMUD’S PV PROGRAM:Past, Present, and Future

FINAL REPORTDecember 30, 2000

A Report to the Sacramento Municipal Utility District

Prepared by:

Donald W. Aitken, Ph.D.Donald Aitken Associates

Warren SchirtzingerHigh Tech Strategies, Inc.

Steven StrongSolar Design Associates

Sponsored by theSacramento Municipal Utility District

SMUD Consulting Services Contract No. I-143

SMUD Project ManagerDonald E. Osborn

1

EXECUTIVE SUMMARY

This SMUD PV Program Review looks at elements of SMUD’s PV Program success to date, assesses what elements may continue to work in the future, and suggests ways in which SMUD’s program might be progressively reoriented to place it in a position of long term sustainability while also becoming internally self-supporting. This study was initiated by the Solar Program within SMUD, under the direction of Donald Osborn.

Section 1: Overview of SMUD’s PV Program Technology Decisions and Experience

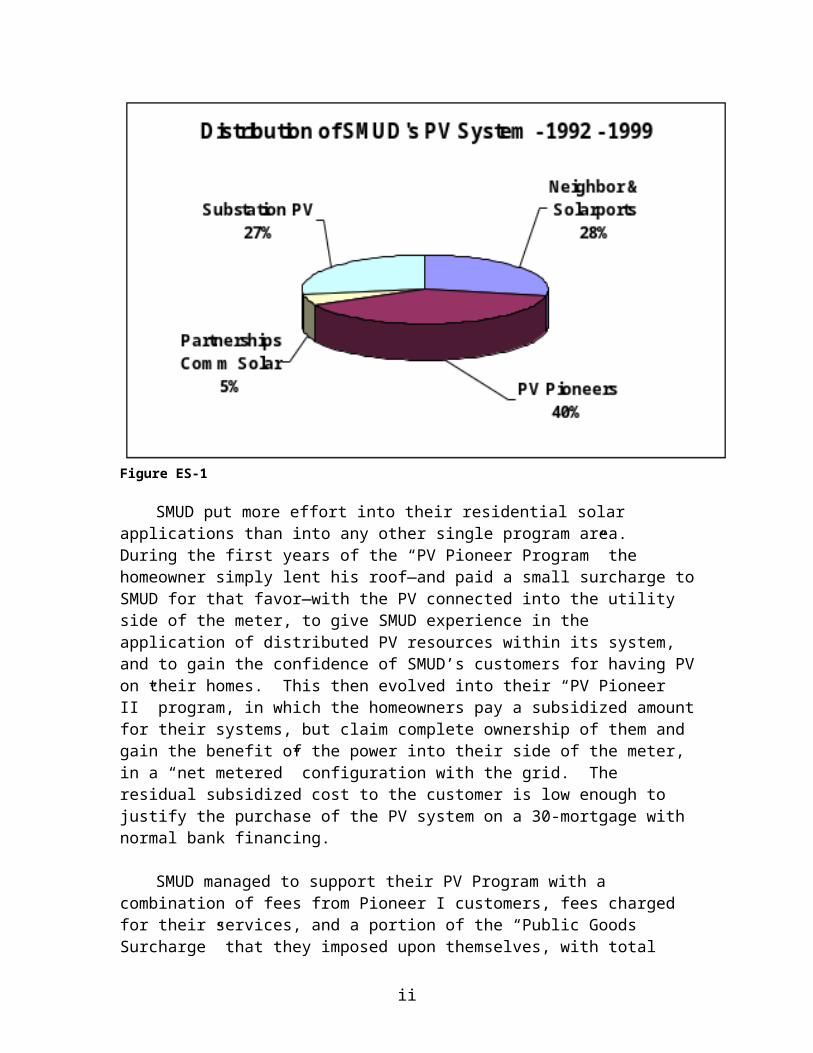

From the beginning SMUD elected not to choose a single type of PV application, but rather to gain both technical and economic experience from multiple applications. Early on, however, they made a decision to go for applications that would allow them to purchase PV modules by bid in substantial quantities, to progressively reduce the cost of their PV along a “Sustained Orderly Development and Commercialization” (SODC) path. In this regard, SMUD did not place much emphasis on the “high value”, but small and labor-intensive, “niche” markets, preferring to reduce market costs for the majority of its customers, rather than simply to exploit applications that are already cost-effective within present market costs.

Figure ES-1

i

SMUD put more effort into their residential solar applications than into any other single program area. During the first years of the “PV Pioneer Program” the homeowner simply lent his roof—and paid a small surcharge to SMUD for that favor—with the PV connected into the utility side of the meter, to give SMUD experience in the application of distributed PV resources within its system, and to gain the confidence of SMUD’s customers for having PV on their homes. This then evolved into their “PV Pioneer II” program, in which the homeowners pay a subsidized amount for their systems, but claim complete ownership of them and gain the benefit of the power into their side of the meter, in a “net metered” configuration with the grid. The residual subsidized cost to the customer is low enough to justify the purchase of the PV system on a 30-mortgage with normal bank financing.

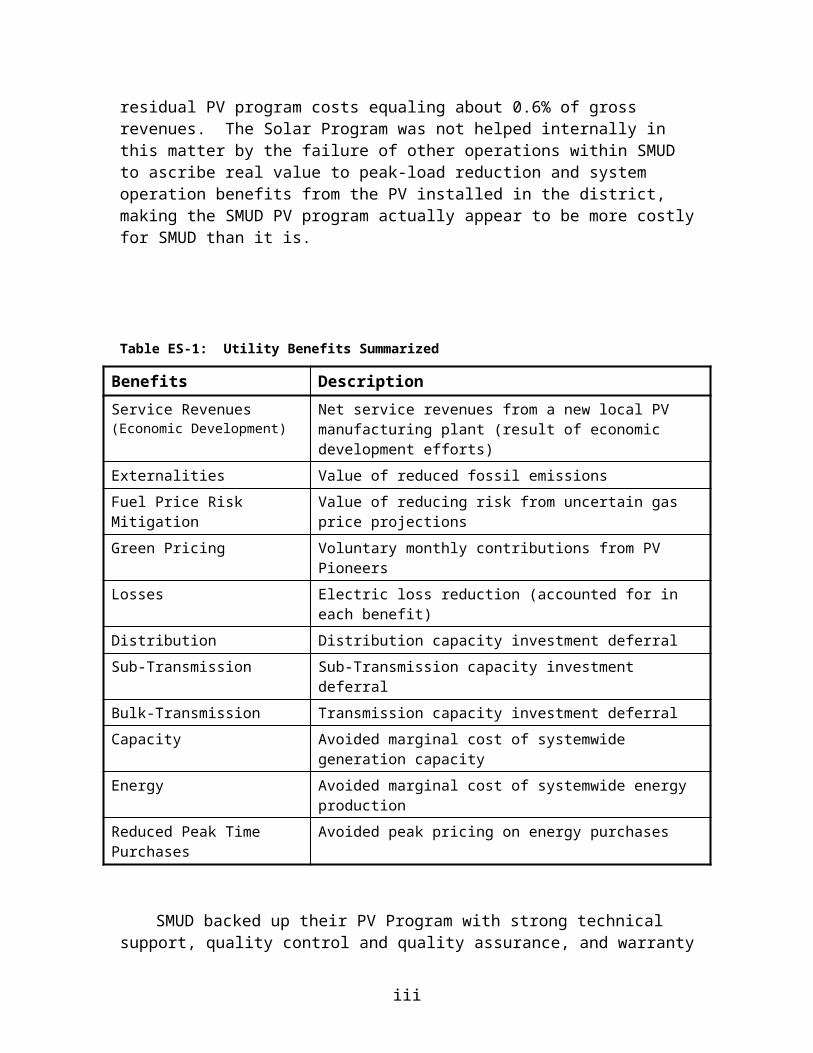

SMUD managed to support their PV Program with a combination of fees from Pioneer I customers, fees charged for their services, and a portion of the “Public Goods Surcharge” that they imposed upon themselves, with total residual PV program costs equaling about 0.6% of gross revenues. The Solar Program was not helped internally in this matter by the failure of other operations within SMUD to ascribe real value to peak-load reduction and system operation benefits from the PV installed in the district, making the SMUD PV program actually appear to be more costly for SMUD than it is.

Table ES-1: Utility Benefits Summarized

Benefits DescriptionService Revenues (Economic Development)

Net service revenues from a new local PV manufacturing plant (result of economic development efforts)

Externalities Value of reduced fossil emissionsFuel Price Risk Mitigation Value of reducing risk from uncertain gas price projectionsGreen Pricing Voluntary monthly contributions from PV PioneersLosses Electric loss reduction (accounted for in each benefit)Distribution Distribution capacity investment deferralSub-Transmission Sub-Transmission capacity investment deferralBulk-Transmission Transmission capacity investment deferralCapacity Avoided marginal cost of systemwide generation capacityEnergy Avoided marginal cost of systemwide energy productionReduced Peak Time Purchases Avoided peak pricing on energy purchases

SMUD backed up their PV Program with strong technical support, quality control and quality assurance, and warranty backing, resulting in excellent system performance with high availability and reliability.

ii

Section 1 Recommendations

The authors of this Review believe that SMUD’s emphasis on residential rooftop applications of PV should be continued, as this will be the largest, most stable market within its District, and allows for cost-reducing standardization.

It is important, as future phases of the program take form, that SMUD continues to maintain contractual flexibility in terms of options, so that the program’s success is not dependent on any single supplier.

SMUD should work with their chosen suppliers to identify ways to mitigate the area-related penalty from low-efficiency PV at both the module and system level.

SMUD should work with their chosen contractors and suppliers to identify and/or develop cost-effective methods to retrofit residential rooftop systems on non-composition roofs.

SMUD should work with their chosen suppliers to identify ways to expand the options for PV roof-integration in new residential and light commercial constructions, as well as for roof replacements.

SMUD should work with their chosen suppliers to develop PV-friendly design and construction approaches that make future retrofits easier.

SMUD should work with their chosen suppliers to expand the range of cost-competitive hardware options for BIPV to commercial buildings.

SMUD should investigate the prospect of offering residential PV Pioneer II customers a battery bank option capable of carrying some portion of the house loads through a “typical” power outage, to tap into the market segment where reliability of electrical service is an important feature.

SMUD needs to develop a closer integration of their energy efficiency and solar programs to realize the benefits of both as part of an overall approach.

As solar domestic water heating (SDWH) can return three to four times the energy savings per unit roof area as PV, the SDWH program should be vigorously pursued and integrated with the efficiency and solar programs.

As the popularity of the PV Pioneer II systems continues to grow, SMUD should begin to develop PV Pioneer II systems for commercial buildings.

SMUD should concentrate on their own service territory first and foremost, as this provides the greatest opportunity for achieving their program goals.

SMUD absolutely must give internal recognition for actual value added to SMUD operations and cost reductions for operations and infrastructure by the PV systems installed in its District.

In the promotion of the PV Pioneer II options, SMUD should emphasize the highly valued but intangible benefits of owning a PV system, and capitalize on the security of having it backed by SMUD—a known and trusted partner in the community which will be there for the long term.

Section 2: SMUD’s PV Market Development and its Relationship to Other Utility Programs

iii

The involvement of SMUD in photovoltaic applications began seriously with their installation in 1984 of their first 1MW PV powerplant, and they have not looked back. SMUD’s goal is to obtain half of its energy from energy efficiency, existing hydroelectric plants, and renewable energy resources, but SMUD has also determined that the SMUD Solar Program is a business development and commercialization activity.

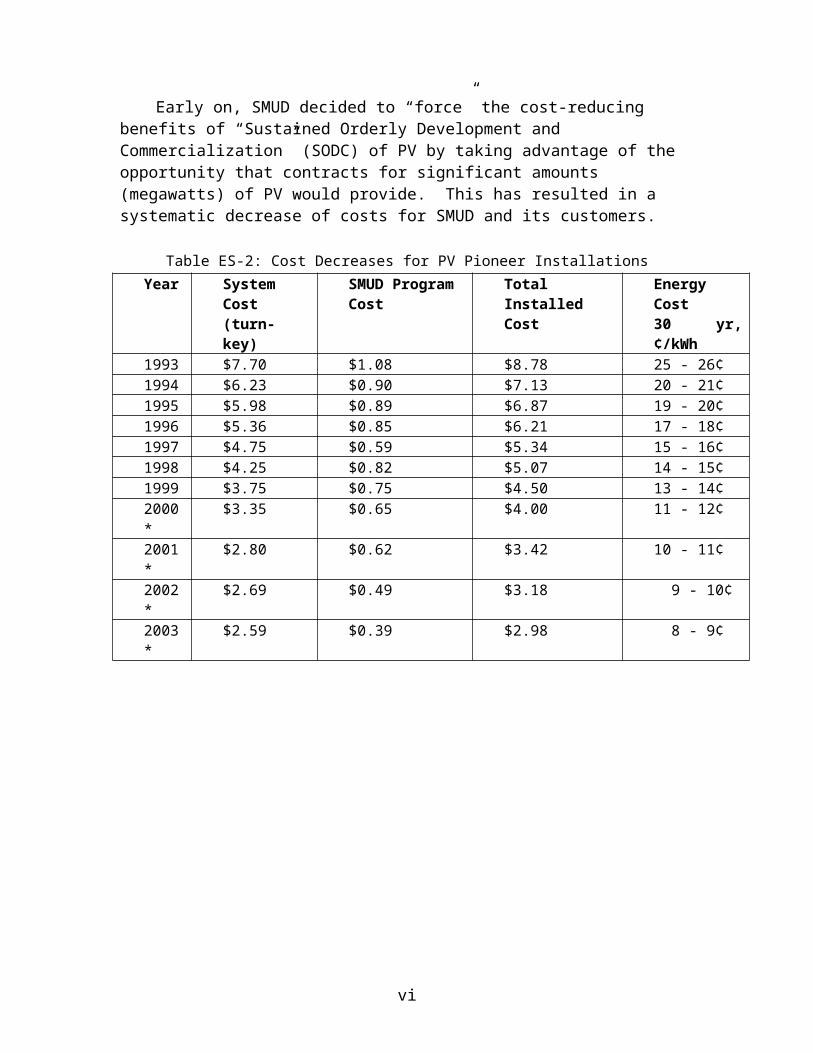

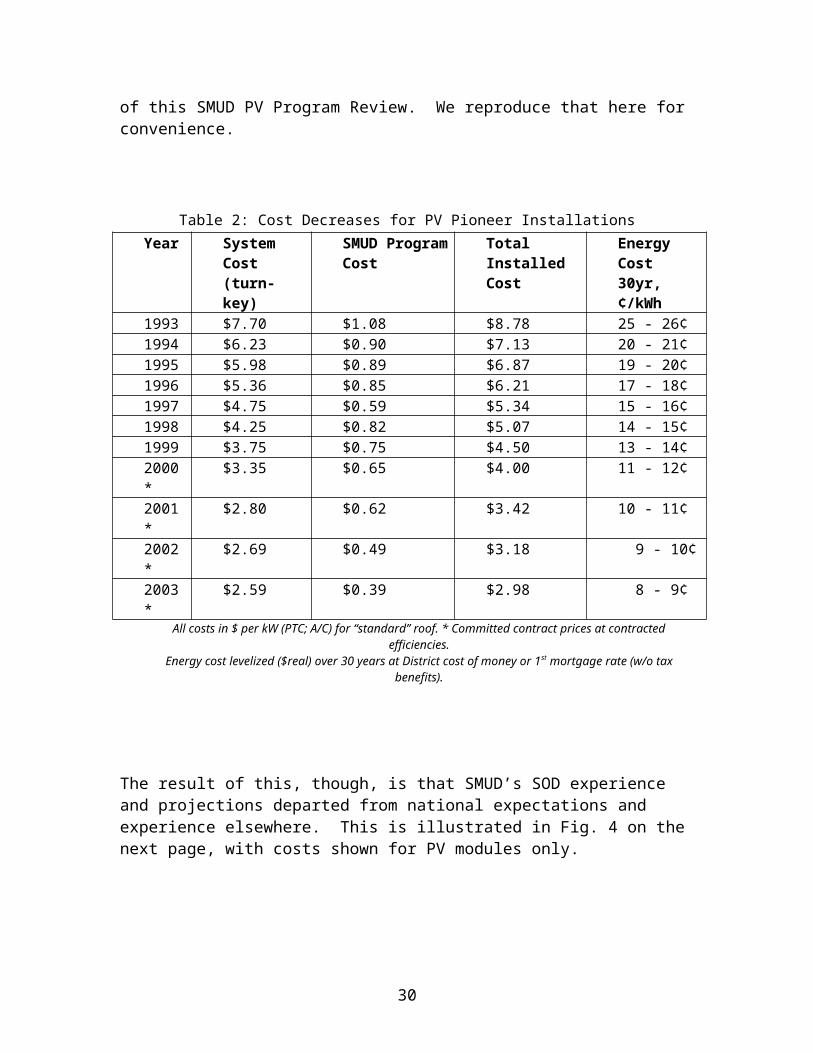

Early on, SMUD decided to “force” the cost-reducing benefits of “Sustained Orderly Development and Commercialization” (SODC) of PV by taking advantage of the opportunity that contracts for significant amounts (megawatts) of PV would provide. This has resulted in a systematic decrease of costs for SMUD and its customers.

Table ES-2: Cost Decreases for PV Pioneer InstallationsYear System Cost

(turn-key)SMUD ProgramCost

Total InstalledCost

Energy Cost30 yr, ¢/kWh

1993 $7.70 $1.08 $8.78 25 - 26¢1994 $6.23 $0.90 $7.13 20 - 21¢1995 $5.98 $0.89 $6.87 19 - 20¢1996 $5.36 $0.85 $6.21 17 - 18¢1997 $4.75 $0.59 $5.34 15 - 16¢1998 $4.25 $0.82 $5.07 14 - 15¢1999 $3.75 $0.75 $4.50 13 - 14¢2000* $3.35 $0.65 $4.00 11 - 12¢2001* $2.80 $0.62 $3.42 10 - 11¢2002* $2.69 $0.49 $3.18 9 - 10¢2003* $2.59 $0.39 $2.98 8 - 9¢

iv

It was also important for SMUD to contribute to the larger economic development goals of the City of Sacramento. A long-term contract with EPV for the manufacture of PV within the Sacramento City limits, as well as for Trace inverters to be assembled within Sacramento, bring significant additional economic benefits to the City.

SMUD participates in the “Utility Photovoltaic Group” (UPVG), an organization of over 100 utilities with some interest in the development and application of PV. While it might then be expected that the success of SMUD’s large effort in PV applications would lead to a number of replications, this has not turned out to be the case. Only two municipal utilities have renewable programs with elements and goals that reflect portions of SMUD’s, the Los Angeles Department of Water and Power (LADWP) and Austin Energy. The LADWP program stands alone in its goals for the application of PV, but has slipped in the last couple of years in getting its ambitious program launched full-scale. Investor-owned utilities are still driven by short-term price motives, and are only engaged in PV applications either as part of their “green” programs, financed by surcharges, or in response to governmental mandates, such as renewable portfolio standards (required percentage increases over time for renewable energy applications). SMUD, therefore, continues to pioneer its integrated, large-scale PV program and thereby to provide valuable potential experience for other, later followers.

SMUD has the opportunity within its own District, provided it carefully targets its evolving customer segments (see Section 3), to maintain a stable PV program for many years to come. The ability of SMUD to remain organized as a “vertically integrated” company, whereas the investor-owned utilities are being disaggregated into multiple entities, gives SMUD a uniquely valuable framework for realizing the benefits of PV within its various operations, all under one financial accounting system. As noted earlier in this Executive Summary, however, SMUD fails to capitalize on quantifying and ascribing these benefits at present.

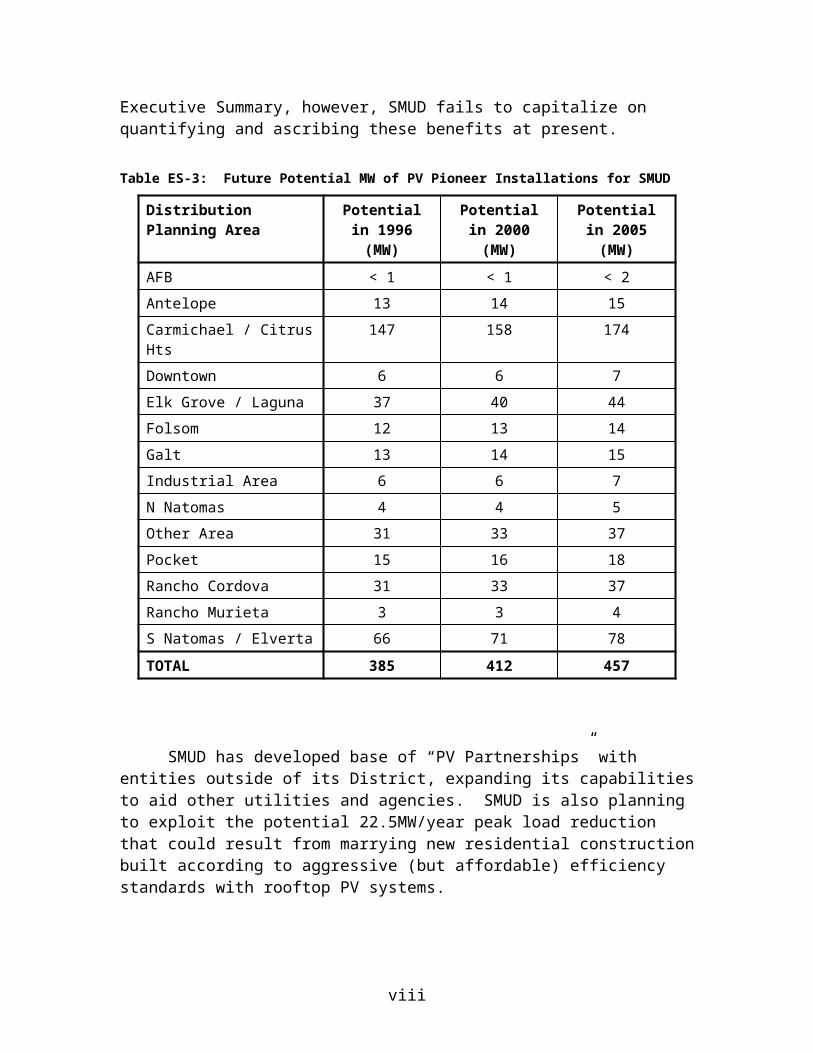

Table ES-3: Future Potential MW of PV Pioneer Installations for SMUD

Distribution Planning Area

Potential in 1996 (MW)

Potential in 2000 (MW)

Potential in 2005 (MW)

AFB < 1 < 1 < 2Antelope 13 14 15Carmichael / Citrus Hts 147 158 174Downtown 6 6 7Elk Grove / Laguna 37 40 44Folsom 12 13 14Galt 13 14 15Industrial Area 6 6 7N Natomas 4 4 5Other Area 31 33 37Pocket 15 16 18

v

Rancho Cordova 31 33 37Rancho Murieta 3 3 4S Natomas / Elverta 66 71 78

TOTAL 385 412 457

SMUD has developed base of “PV Partnerships” with entities outside of its District, expanding its capabilities to aid other utilities and agencies. SMUD is also planning to exploit the potential 22.5MW/year peak load reduction that could result from marrying new residential construction built according to aggressive (but affordable) efficiency standards with rooftop PV systems.

Section 2 Recommendations

SMUD should continue to seek to make the PV program self-supporting within SMUD—indeed, possibly an internal “profit” center—so that SMUD’s public goods funds can be allocated to other socially important needs (e.g. low-income, efficiency, or RD&D).

SMUD should nevertheless continue subsidies at a modest level for the PV program, even as it becomes essentially self-supporting, to continue to accelerate the accrual of benefits.

SMUD needs to continue to obtain PV systems at bulk, multi-year prices, and to pass the savings on to their customers, to provide incentives to a long-term market in their District.

SMUD should more vigorously identify and exploit other “niche” markets for PV in its District, but not let this drain attention or resources from the primary large-volume installation programs, e.g. BIPV.

SMUD should continue and expand their “PV Partnership Program”, with “profits” going to defray some PV program and personnel costs, but not let this drain attention or resources from the primary large-volume installation programs within their District.

SMUD should continue to develop their PV-in-new-construction program, in conjunction with their own architectural department, and to strive for the goal of “zero net peak demand” new houses, as their District customer-base expands.

SMUD should continue to collaborate actively with other utilities; local, state and federal agencies; and other stakeholders, to continue to facilitate the application of PV and the reduction of costs.

vi

Section 3: A Blueprint for Commercialization

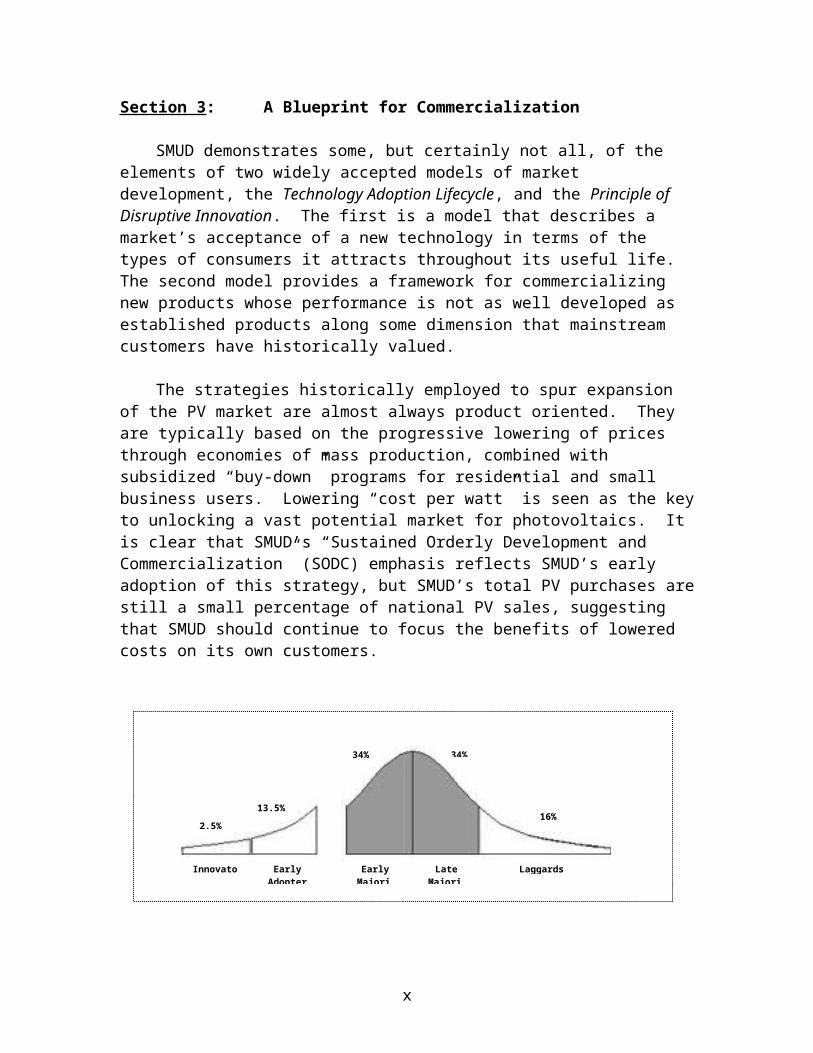

SMUD demonstrates some, but certainly not all, of the elements of two widely accepted models of market development, the Technology Adoption Lifecycle, and the Principle of Disruptive Innovation. The first is a model that describes a market’s acceptance of a new technology in terms of the types of consumers it attracts throughout its useful life. The second model provides a framework for commercializing new products whose performance is not as well developed as established products along some dimension that mainstream customers have historically valued.

The strategies historically employed to spur expansion of the PV market are almost always product oriented. They are typically based on the progressive lowering of prices through economies of mass production, combined with subsidized “buy-down” programs for residential and small business users. Lowering “cost per watt” is seen as the key to unlocking a vast potential market for photovoltaics. It is clear that SMUD’s “Sustained Orderly Development and Commercialization” (SODC) emphasis reflects SMUD’s early adoption of this strategy, but SMUD’s total PV purchases are still a small percentage of national PV sales, suggesting that SMUD should continue to focus the benefits of lowered costs on its own customers.

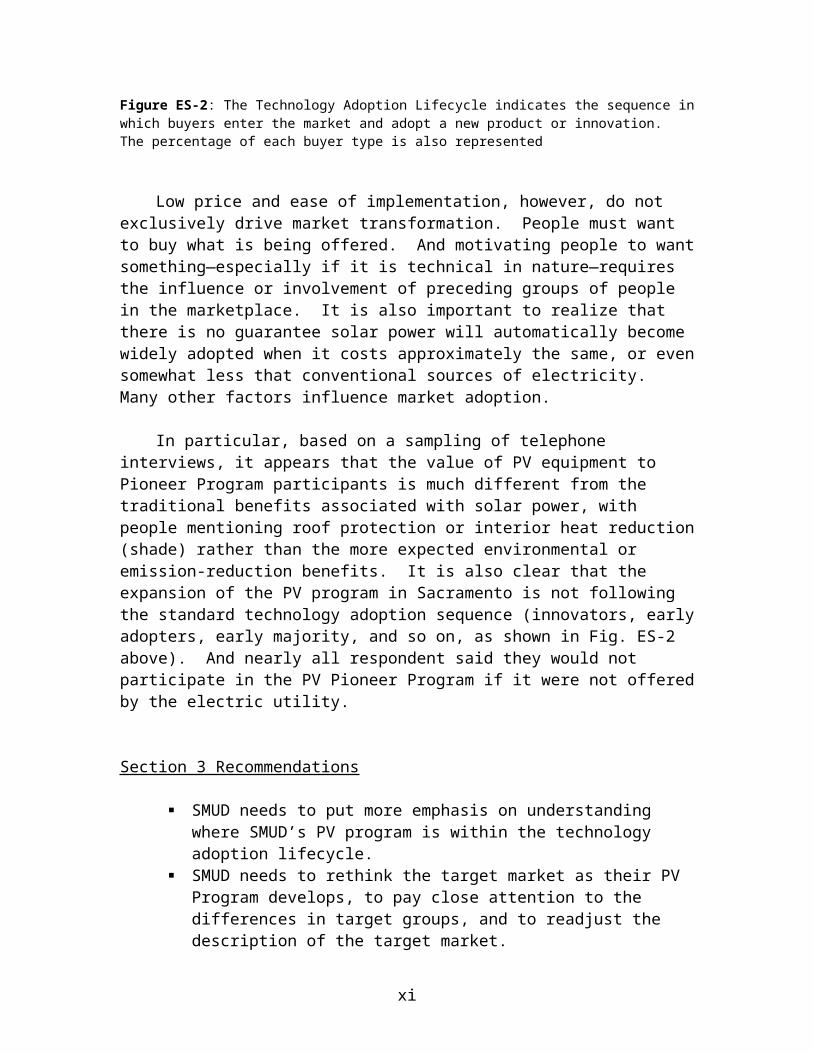

Figure ES-2: The Technology Adoption Lifecycle indicates the sequence in which buyers enter the market and adopt a new product or innovation. The percentage of each buyer type is also represented

Low price and ease of implementation, however, do not exclusively drive market transformation. People must want to buy what is being offered. And motivating people to want something—especially if it is technical in nature—requires the influence or involvement of preceding groups of people in the marketplace. It is also important to realize that there is no guarantee solar power will automatically become widely adopted when it costs approximately the same, or even somewhat less that conventional sources of electricity. Many other factors influence market adoption.

In particular, based on a sampling of telephone interviews, it appears that the value of PV equipment to Pioneer Program participants is much different from the traditional benefits associated with solar power, with people mentioning roof protection or interior

2.5%

34% 34%

16%13.5%

Innovators EarlyAdopters

EarlyMajority

LaggardsLateMajority

vii

heat reduction (shade) rather than the more expected environmental or emission-reduction benefits. It is also clear that the expansion of the PV program in Sacramento is not following the standard technology adoption sequence (innovators, early adopters, early majority, and so on, as shown in Fig. ES-2 above). And nearly all respondent said they would not participate in the PV Pioneer Program if it were not offered by the electric utility.

Section 3 Recommendations

SMUD needs to put more emphasis on understanding where SMUD’s PV program is within the technology adoption lifecycle.

SMUD needs to rethink the target market as their PV Program develops, to pay close attention to the differences in target groups, and to readjust the description of the target market.

Each target market needs to be clearly identified and profiled, as well as tracked as that profile changes over time.

SMUD needs to develop a testimonial program where early users discuss and promote their experience with PV to the appropriate audience.

SMUD needs to promote more of the intangible benefits of PV using communications techniques that are acceptable to the type of customer being targeted.

SMUD needs to keep an eye out for unconventional applications that exploit PV’s limitations.

SMUD needs to determine and clarify what makes the product “complete” in the eyes of the target customer.

SMUD needs to continue to build a customer-oriented channel of distribution so that customers are comfortable making the PV purchase.

If SMUD were to follow the relevant guidelines offered by the Technology Adoption Lifecycle and the Principle of Disruptive Innovation, several fundamental practices would emerge:

1. SMUD would focus on serving specific groups of customers in sequence, one group at a time. This is often called target marketing.

2. A new emphasis would be placed on discovering the psychographic and value profiles of potential customers.

3. SMUD would continue to build the organization needed to install and service PV systems for customers. As a utility SMUD lowers risk for conservative customers and therefore accelerates market transformation.

4. SMUD would tailor their promotional activities to fit the preferences of their target market.

viii

CONTENTS

INTRODUCTION………………………………………………………………..1

1. OVERVIEW OF SMUD’S PV PROGRAM TECHNOLOGY DECISIONSAND EXPERIENCE…………………………………………………………31.1 Introduction………………………………………………………………..31.2 PV Application Assessment……………………………………………….3

1.2.1 Applications Selected……………………………………………...31.2.2 Niche Markets……………………………………………………..81.2.3 Process and Suitability of Selection……………………………….8

1.3 Ascribing an Appropriate Market Value to PV Generation……………...101.4 Assessment of Program Implementation………………………………... 13

1.4.1 Contractor Selection and Management…………………………..131.4.2 Technical Support and Warranties……………………………….141.4.3 System Performance/Availability……………………………….. 151.4.4 Potential Technical Application Evolution of the

SMUD PV Program…………………………………………. 151.5 Summary of Technical Approach……………………………………….. 17

1.5.1 How is the program doing relative to its goals?………………… 171.5.2 Recommendations for the Future……………………………….. 17

2. SMUD’S PV MARKET DEVELOPMENT AND ITS RELATIONSHIPTO OTHER UTILITY PROGRAMS…………………………………….. 192.1 Introduction………………………………………………………………192.2 Overview of SMUD’s Market Development Philosophy………………..192.3 Evidence for the Emulation of the SMUD Model by Other Utilities…… 23

2.3.1 Lessons Learned from Comparing the LADWP ProgramTo SMUD’s…………………………………………………..24

2.3.2 Some Observations on Other Utility PV Programs……………... 262.3.2.1 Commonwealth Edison, the City of Chicago, and

the SPIRE Corporation……………………………… 262.3.2.2 Idaho Power………………………………………………272.3.2.3 Tucson Electric and Global Solar………………………...272.3.2.4 Austin Energy…………………………………………… 28

2.3.3 Conclusion from These Other Utility Experiences………………282.4 Marketing Challenges Facing SMUD……………………………………292.5 Trends in Emerging Utility Market Structures…………………………...312.6 Additional Market Potential for SMUD’s PV Program………………….332.7 Conclusions………………………………………………………………36

ix

3. A BLUEPRINT FOR COMMERCIALIZATION………………………. 383.1 Introduction………………………………………………………………38

3.2 Definitions and Assumptions…………………………………………….383.3 New Business Fundamentals……………………………………………. 383.4 Overview of Commercial/Market Adoption Models…………………….393.5 Historical Perspective: Sustained Orderly Development and

Commercialization (SODC)………………………………………….413.6 Comparing SMUD With Commercial Market Development…………… 423.7 The Delivered Value of PV………………………………………………433.8 Migrating Toward a Commercial Enterprise……………………………. 443.9 Summary…………………………………………………………………46Appendix: Psychographic Profiles of Each Buyer Type in the

Adoption process………………………………………... 48

FIGURES

Figure 1: The Distribution of SMUD’ PV System Applications……………….. 4Figure 2: Utility Benefits of Tracking & Fixed PV in the SMUD System

At Distribution Voltages…………………………………………10Figure 3: System Load and PV Output Profiles on Peak Day, July 14, 1994…. 12Figure 4: Cost of PV vs. Year, “Business as Usual” Compared to

“SMUD With SODC”………………………………………………..21Figure 5: Direct and Indirect Effects of SMUD’s PV Purchase Commitment…22Figure 6: Surveyed Market Potential for PV Pioneer II PV Installations……... 30Figure 7: The Technology Adoption Lifecycle………………………………...40Figure 8: The Shift From Customer Tangibles to Intangibles………………….44

TABLES

Table 1: Summary of SMUD PV Installations through 1999………………….. 5Table 2: Cost Decreases for PV Pioneer Installations……………… 13, and 21Table 3: Future Potential MW of PV Pioneer Installations for SMUD………. 31Table 4: PV Pioneer II: Estimated Unit Prices………………………………..32Table 5: SMUD PV Partnerships 1997 Through 1999………………………...34

x

xi

INTRODUCTION

The testimonials that have come and continue to come to the Sacramento Municipal Utility District (SMUD) regarding their program in the application of photovoltaic power and their contribution to the national effort in promoting and accelerating PV markets are now legion. We share just three of those here, to set the stage for our own work in this Report.

First, from the Natural Resources Defense Council, in their “Review for NRDC of Sacramento Municipal Utility District Public Benefits Programs”1:

Overall, SMUD is one of the most innovative, aggressive, and successful utilities anywhere in promoting energy efficiency and renewable energy. SMUD has developed an organizational culture that has integrated energy efficiency and renewables as core values and keys to its future role, and has cultivated a customer base that understands, supports, and responds to these values.”

Second, a testimonial from one of the authors of this report (DA) that is often quoted in SMUD public presentations2:

It is critically important to note that SMUD’s rapidly reducing costs are the result of the utility’s decision to be a substantial and consistent player in the PV market, year after year. This has been shown to be the key to accomplishing the economic benefits of “Sustained Orderly Development” of the solar electric utilities.

And third, a quote from a private memorandum to the authors of this report from a very well known management consultant with special expertise in solar energy3:

SMUD was a true pioneer in proving that people will choose renewables if given he opportunity, and that they will pay more for environmentally-superior power generation…there is no doubt that SMUD’s program is one of the major programs in the world, and it is worth caring about.

In those three testimonials lie our reasons for preparing this SMUD PV Program Review, and selecting the topical areas included in it. SMUD is “worth caring about”, not only because it has made pioneering contributions to utility applications of photovoltaics to date, but also because it has the potential to continue to play a critically important and, indeed, a leadership role for utilities in the future.

1 Gordon, F., Hewitt, D., and Pratt, J., Review for NRDC of Sacramento Municipal Utility District Public Benefits Programs, Final Report, Prepared for Natural Resources Defense Council, Pacific Energy Associates, Inc., Aug. 12, 1999.

2 Aitken, Donald W., then Senior Staff Scientist for the Union of Concerned Scientists, and developer of the conceptual framework of “Sustained Orderly Development and Commercialization”, the market dynamic selected early on by SMUD as the framework for their PV market-development efforts.3

? The author of this comment, and the memorandum, prefers to remain anonymous.

1

To realize this potential, however, requires looking at the elements of SMUD’s success to date, assessing what elements may continue to work in the future, and suggesting ways in which SMUD’s program might be progressively reoriented to place it in a position of long term sustainability while also becoming internally self-supporting. This is the task we have set before us.

The authors of this SMUD PV Program Review do not proclaim to be the last word on these subjects, nor the ultimate experts in gazing into the crystal PV ball of the future. But each of us has experience relevant to SMUD, and two of us (DA and SS) have long contributed directly and indirectly to SMUD’s PV programs, giving us perspectives that have developed over time, while the 3rd author (WS) has unique experience in understanding the transition steps from the early stages of the introduction of a new technology (PV) to full public and market acceptance.

Each of us has principally authored one of the three main sections of this Review: Section 1, “Overview of SMUD’s PV Program Technology Decisions and Experience” (SS); Section 2, “SMUD’s PV Market Development and its Relationship to Other Utility Programs” (DA); and Section 3, “A Blueprint for Commercialization” (WS). We have fully collaborated on the mutual editing of all three sections, and the agreement upon the recommendations set forth.

It is in the spirit of our admiration for SMUD’s leadership to date, our faith in SMUD’s commitment to its customers to continue to protect their interests in the progressive energy resource transition that must and will take place this century, and our acknowledgement that SMUD recognizes that adaptability and change are necessary for continued success, that we offer the following review and recommendations.

2

1. OVERVIEW OF SMUD’S PV PROGRAM TECHNOLOGY DECISIONS AND EXPERIENCE

1.1 Introduction

In 1984 the Sacramento Municipal Utility District embarked on a program with no precedent—an ambitious effort to bring PV power first to their system and later, more directly, to hundreds of their customers while also using PV power for other useful purposes within SMUD’s system. Without humility, their first step was simply to build the world’s largest PV plant on the grounds of the decommissioned Rancho Seco Nuclear Plant. Phase 1, consisting of 1MW of modules (which, because of tracking, operate as effectively 1.23 MW), was constructed in 1984, and phase 2, also for 1 MW (or 1.23 MW with tracking benefits) was constructed in 1986. That system has been working ever since, day after day delivering power reliably to the SMUD grid, the value of which has never depended on the availability or cost of fuel, and never will. Expansions since then and planned for this coming year will bring the size of that system to over 3.5MW, making it once again the world’s largest central station PV plant.

In 1993 SMUD continued to move forward, launching a program that would see a total of over 8 Megawatts (MW) in place in over 650 different PV applications in Sacramento within the next 7 years, and 8MW more planned by 2003. As with any new venture, there was an element of risk, greater than the traditionally conservative utility company criteria would normally accept. But with an unwavering consistency of vision, SMUD soon became a model for other utilities to follow, also becoming known worldwide for their courage and their mounting grid-connected PV experience, and receiving national and international recognition and honors for the utility and for its employees.

It is our task to look at the ingredients of this (obviously successful to date) experience, and to extrapolate to conditions and circumstances that we see in our energy crystal ball.

In this section of this SMUD PV Program Review, we look at the technical aspects of SMUD’s PV Program choices, and draw conclusions and recommendations.

1.2 PV Application Assessment

1.2.1 Applications Selected

Right from the beginning, SMUD clearly elected not to choose a single type of PV application, but rather to gain both technical and economic experience from multiple applications. Early on, however, they made a decision to go for applications that would allow them to purchase PV modules by bid in substantial quantities, to progressively reduce the cost of their installed PV systems along a “Sustained Orderly Development

3

and Commercialization” (SODC) path. (The marketing philosophy of this is described and evaluated in Section 2 of this Report.) The relevance here is that this approach led SMUD to favor applications that required modest amounts of PV (from 1 to 400 KW), and with the smaller units (1-4 kW) installed on residences in great numbers. On the basis of their years of PV applications, SMUD has the benefit of actual real-world performance and cost data to assess the pros and cons of all PV system options. SMUD is well positioned to prioritize their program emphasis as their scale-up continues.

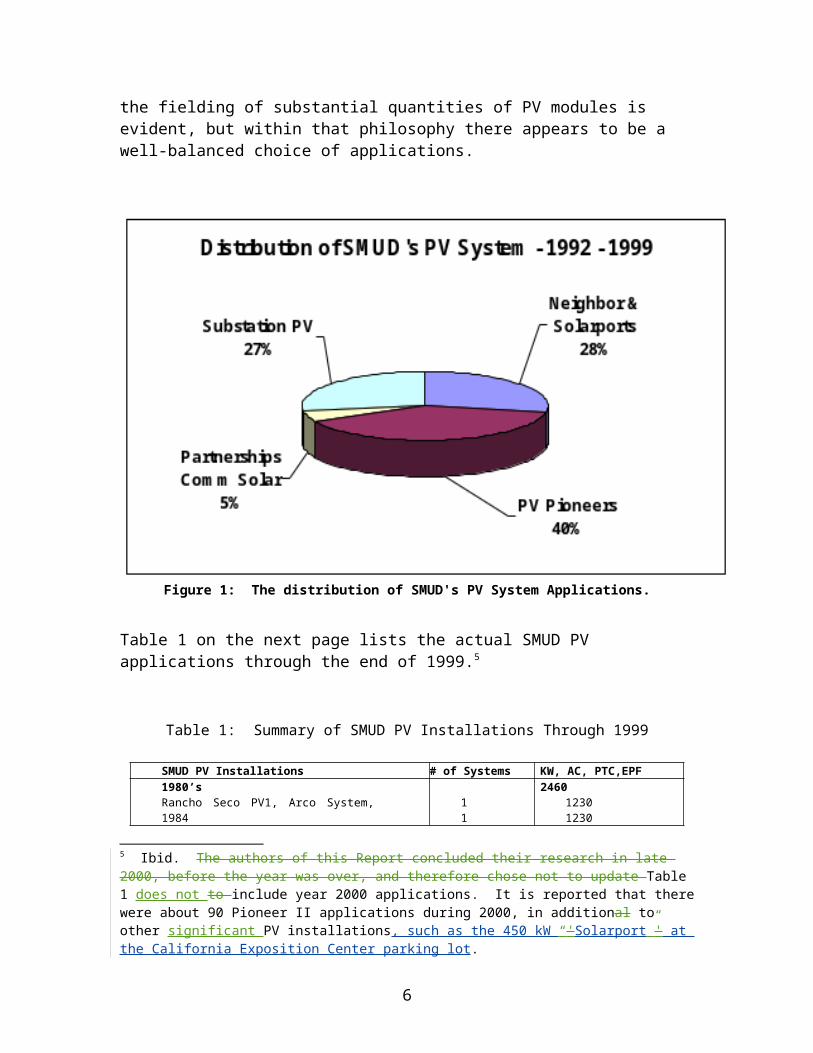

The distribution of SMUD’s PV system applications (for all but the Rancho Seco central PV stations) is shown below in Figure 1.4 The reliance on systems that would result in the fielding of substantial quantities of PV modules is evident, but within that philosophy there appears to be a well-balanced choice of applications.

Figure 1: The distribution of SMUD's PV System Applications.

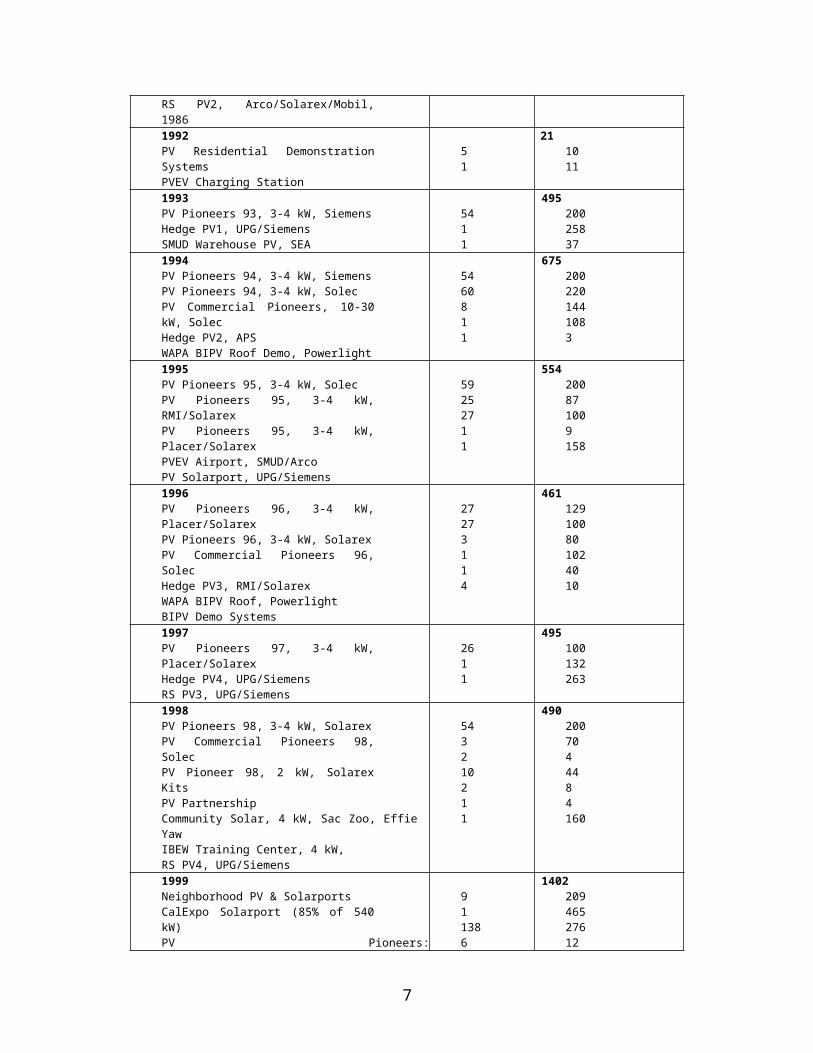

Table 1 on the next page lists the actual SMUD PV applications through the end of 1999.5

Table 1: Summary of SMUD PV Installations Through 1999

4 Osborn, D., Sustained Orderly Development and Commercialization of Grid-Connected Photovoltaics: SMUD as a Case Example, Advances in Solar Energy, Vol. .., No. .. (2001)5 Ibid. The authors of this Report concluded their research in late 2000, before the year was over, and therefore chose not to update Table 1 does not to include year 2000 applications. It is reported that there were about 90 Pioneer II applications during 2000, in additional to other significant PV installations, such as the 450 kW “'Solarport”' at the California Exposition Center parking lot.

4

SMUD PV Installations # of Systems KW, AC, PTC,EPF1980’sRancho Seco PV1, Arco System, 1984RS PV2, Arco/Solarex/Mobil, 1986

11

246012301230

1992PV Residential Demonstration SystemsPVEV Charging Station

51

211011

1993PV Pioneers 93, 3-4 kW, SiemensHedge PV1, UPG/SiemensSMUD Warehouse PV, SEA

5411

49520025837

1994PV Pioneers 94, 3-4 kW, SiemensPV Pioneers 94, 3-4 kW, SolecPV Commercial Pioneers, 10-30 kW, SolecHedge PV2, APSWAPA BIPV Roof Demo, Powerlight

5460811

6752002201441083

1995PV Pioneers 95, 3-4 kW, SolecPV Pioneers 95, 3-4 kW, RMI/SolarexPV Pioneers 95, 3-4 kW, Placer/SolarexPVEV Airport, SMUD/ArcoPV Solarport, UPG/Siemens

59252711

554200871009158

1996PV Pioneers 96, 3-4 kW, Placer/SolarexPV Pioneers 96, 3-4 kW, SolarexPV Commercial Pioneers 96, SolecHedge PV3, RMI/SolarexWAPA BIPV Roof, PowerlightBIPV Demo Systems

27273114

461129100801024010

1997PV Pioneers 97, 3-4 kW, Placer/SolarexHedge PV4, UPG/SiemensRS PV3, UPG/Siemens

2611

495100132263

1998PV Pioneers 98, 3-4 kW, SolarexPV Commercial Pioneers 98, SolecPV Pioneer 98, 2 kW, Solarex KitsPV PartnershipCommunity Solar, 4 kW, Sac Zoo, Effie YawIBEW Training Center, 4 kW, RS PV4, UPG/Siemens

543210211

4902007044484160

1999 Neighborhood PV & SolarportsCalExpo Solarport (85% of 540 kW) PV Pioneers: UPG/Shawnee/Siemens/Solarex/EPVCommunity SolarPV PartnershipsRS PV5a (35% of 750 kW) UPG/EPV

91138681

140220946527612180260

TOTAL TODATE PV PioneersNeighborhood PV & SolarportsPV PartnershipsCommunity SolarSubstation PV (Hedge PV 1-4, RS PV 3-5a)Substation PV (RS PV 1&2)

5583518872

7053182612752242012482460

It is evident from Table 1 and Figure 1 that SMUD put more effort into their residential solar applications than into any other single program area. The authors believe this emphasis was and is correctly placed as the potential for the residential

5

rooftop market is very large indeed. Further, these systems tend to be the most amenable to standardization, which further reduces costs. While this emphasis continues today, the nature of the residential PV program has evolved.

During the first years of the PV Pioneer program (1993-99), the PV was connected into the utility side of the meter, giving the homeowner no direct value for lending his rooftop to SMUD, and even asking him to pay $4 each month for the privilege! This approach allowed SMUD to “test the market” for acceptance of residential roof-top PV while also assessing the geographically disbursed benefits of “distributed PV”, a PV version of a larger structural direction—distributed generation--that is today becoming increasingly important for all utilities.

In particular, all distributed PV systems:

Provide grid support Eliminate costs and losses in transmission and distribution Create a diverse and resilient energy system Typically require no special “impact assessment”, approvals or permits Can be fielded very rapidly, in response to need

Mounting distributed PV on buildings such as on residential rooftops also provides SMUD with these additional benefits:

The real estate comes “free” with the building There are no site development costs—the PV is simply placed on the building

roof Customer acceptance (e.g. willingness to make their roofs available to SMUD

and even to pay a little each month to subsidize it) arises in part as the rooftop PV systems are a highly visible expression of the homeowner’s environmental commitment.

The utility interconnection already exists to serve the building There is no (additional) real estate tax on land to support the PV system or on

the PV itself

SMUD’s “Neighbors and Solarports”, the second largest slice of the Figure 1 pie, represents larger distributed PV systems, but with much the same benefits for SMUD as the residential applications. The third largest slice of that pie was for “Substation PV”using even larger arrays integrated into their distribution facility support systems.

In 1999 SMUD began offering the PV Pioneer II Program as an alternative to its customers. In this case, the residential customer purchases and owns the PV system, enabled both by SMUD’s low costs and by SMUD’s attractive “buy down” incentives and financing. (This is presented in more detail in Section 2 of this Report.) The PV system output is therefore connected on the customer’s side of the meter. The meters run in a “net metering” configuration, recording power flow both ways between the building and the grid, thereby automatically providing a credit at full retail value for the customer

6

which can be used in evening hours to offset the evening purchases of electricity. (In simple language, the meter runs both forwards and backwards.)

With the PV Pioneer II program, the customer gains considerable benefits from the systems on their roofs. Most important, they receive the full use of the solar-generated electricity either directly in their home or, via the ‘net metering’ policy that SMUD has implemented system-wide, they realize measurable financial return from their investment. SMUD also gains many of the benefits of distributed PV on their system from these applications, while having the benefit that the customers now share a major portion of the costs

Another innovation that SMUD now provides as part of their PV Pioneer II program, as well as their PV programs for commercial establishments, is offering distributed PV generation as “Building integrated PV” (BIPV). While this does not gain SMUD further benefits from the installations, it brings further benefits and incentives to building owners and occupants. Among these are:

BIPV can displace conventional building material and labor, reducing the net installed cost of the PV system on both residential and commercial applications

The architecturally clean, well-integrated systems increase market acceptance for PV

For commercial buildings, BIPV can provide significant demand charge reductions

With building-integrated PV systems, building owners are already paying for facade and/or roofing materials and the labor to install them. The land is already paid for, the support structure is already in place, the building is already wired, the utility is already connected, and developers can finance the PV as part of their overall project. Another benefit comes from distributing the BIPV installations over a very broad geographic area and a large number of buildings, mitigating the effects of local weather conditions on the aggregate, and producing a very resilient source of supply.

With reduced installation costs, improved aesthetics and all the benefits of distributed generation, building-integrated PV systems are a prime candidate for early widespread market adoption. These systems should be encouraged especially within the architectural community, as the architects are the ones who make the decisions to incorporate BIPV.

In closing this brief discussion about SMUD’s choice of applications, it is interesting to note that, in 1992, while they were gaining the experience that enabled them to launch the PV Pioneer I program, SMUD also built the first PV electric vehicle charging station in California (and only the second one in the U.S.), to service their own Evs at their headquarters building, showing their interest in having their solar program support other important energy conserving programs within SMUD.

1.2.2 Niche Markets

7

SMUD elected not to invest much of their emphasis into “niche” or “high value” applications early in their PV program. While the economics of these applications are easier to justify on a case-by-case basis, they also tend to be applications for very small quantities of PV, thereby not contributing to a sufficient market impact to reduce the costs of the PV systems. Niche markets also often require custom configuration of PV modules and balance-of-system (BOS) equipment, which requires design-intensive support. If this support is provided directly by the SMUD program it could adversely dilute SMUD’s technical resources that might be better used to pursue the greater overall program goals. This is further discussed in Section 2 of this Report.

1.2.3 Process and Suitability of Selection

SMUD began their PV program with a broad cross section of applications from individual residential and commercial rooftop systems to medium-scale PV at the ‘neighborhood’ and substation level to central-station PV. This was a wise starting point, as it would provide SMUD program personnel with a broad base of both technical operating experience and economic performance on all of the PV system applications.

The authors believe that all of the key PV systems applications that SMUD has selected will achieve widespread commercial acceptance. We believe that the sequence of commercialization will start with residential roof-top systems, followed by roof-top and BIPV systems for commercial buildings with substation and ‘neighborhood’ systems coming next and central station systems following last.

Our reasons for these conclusions are that residential and commercial PV systems can and do displace utility power on the customers’ side of the meter at the retail rate, while the substation and central station systems compete with the cost of avoided fuel or bulk kilowatt-hours – both at the wholesale level.

The reason that residential systems are favored as the first application to reach widespread commercial acceptance is that residential customers have access to home mortgage financing for home improvements (such as PV systems). This provides 15 – 30-year financing terms at reasonable rates with tax deductible interest. Further, residential electric rates have traditionally been the highest rate class so the PV power is worth more to the residential customer who is also more likely to accept a longer-term ‘payback’ than a commercial customer.

We believe the commercial building market will follow because there are generous federal incentives for commercial customers with a federal tax liability to field PV on their facilities. Further, commercial electric rates are on the rise as are (or will be) the demand charges associated with on-peak consumption.

The substation systems can and will be fielded to provide grid support and, when the value of this grid support is recognized, this will put the substation systems ahead of the central station deployment.

8

The retail value of the electricity is well known and the payment method (displaced utility bills via net metering) is already defined and in place, while the value of the PV-generated electricity to the utility is still, in our opinion, way undervalued – even at SMUD. Until the real value of PV-generated electricity is recognized, the larger systems at the substation and, especially at the central station scale, will lag behind the smaller distributed systems for individual buildings when market forces, rather than government policies, are the drivers for the applications.

It is important to note here that in other utility circumstances very different decisions from SMUD's may also emerge. For example, Tucson Electric Power (TEP), an investor-owned utility (and hence unlike SMUD) is now required to commit to significant PV applications by the state government-mandated "Environmental Portfolio Standard". (This is presented in more detail in Section 2 of this SMUD PV Program Review.)

TEP is therefore seeking ways to install the maximum amount of PV at the minimum cost to the utility, leading them to conclude from their analyses that central station PV will be the least expensive starting point for them. They will just put up big systems, rather than many smaller ones. (The legislated requirement does not permit the utility to recoup costs from individual customers. Those are done in separate "green power" programs, which do not qualify towards meeting the mandated installation percentages.)

The conclusion of this is that PV program development priorities for utilities are highly situational. Conclusions appropriate to one utility (e.g. in this case TEP) do not extrapolate to other utilities (e.g. SMUD), nor are our recommendations to SMUD necessarily appropriate to other utilities. We have seen criticisms of the SMUD program, which have confused this point.

It is important that SMUD focus their PV Program’s near-term resources on those applications that show the highest near-term promise for meeting the overall goals established for the program and SODC. Although the application mix will vary and special opportunities will come up (perhaps stimulated by compelling political motivation), we recommend that SMUD prioritize the allocation of financial and technical resources to distributed PV systems for individual buildings. If the number of opportunities are limited by these applications, SMUD should take pro-active steps to increase them.

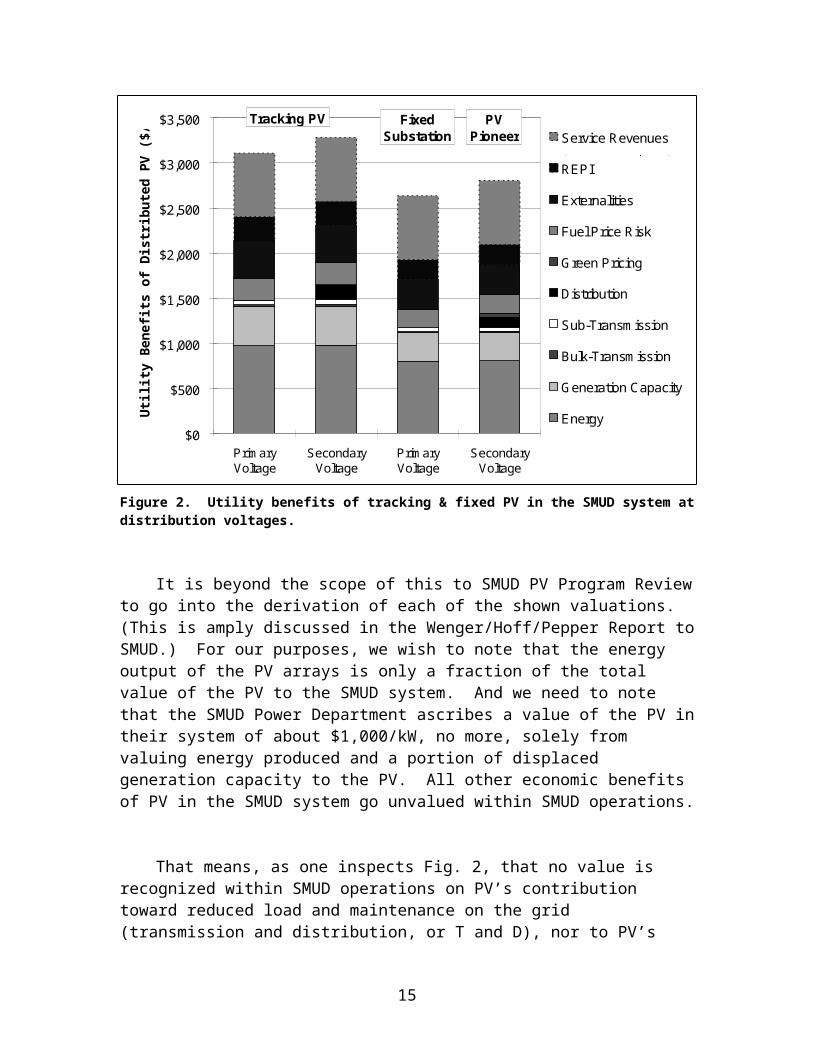

1.3 Ascribing an Appropriate Market Value to PV Generation

9

A detailed analysis of “Photovoltaic Economics and Markets” that focused on SMUD was prepared in 1996.6 Figure 2 below summarizes the benefits that the authors of that report determined could be ascribed to the value of PV in SMUD grid-connected applications.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

PrimaryVoltage

SecondaryVoltage

PrimaryVoltage

SecondaryVoltage

Utili

ty B

enef

its o

f Dis

tribu

ted

PV ($

/kW

, 199

6) Service Revenues

REPI

Externalities

Fuel Price Risk

Green Pricing

Distribution

Sub-Transmission

Bulk-Transmission

Generation Capacity

Energy

Tracking PV PVPioneer

FixedSubstation

(economic development)

Figure 2. Utility benefits of tracking & fixed PV in the SMUD system at distribution voltages.

It is beyond the scope of this to SMUD PV Program Review to go into the derivation of each of the shown valuations. (This is amply discussed in the Wenger/Hoff/Pepper Report to SMUD.) For our purposes, we wish to note that the energy output of the PV arrays is only a fraction of the total value of the PV to the SMUD system. And we need to note that the SMUD Power Department ascribes a value of the PV in their system of about $1,000/kW, no more, solely from valuing energy produced and a portion of displaced generation capacity to the PV. All other economic benefits of PV in the SMUD system go unvalued within SMUD operations.

That means, as one inspects Fig. 2, that no value is recognized within SMUD operations on PV’s contribution toward reduced load and maintenance on the grid (transmission and distribution, or T and D), nor to PV’s value in reducing fuel price risk, 6 Wenger, H., Hoff, H., and Pepper, J., Photovoltaic Economics and Markets: The Sacramento Municipal Utility District as a Case Study, SMUD Contract G253

10

nor to the contribution of PV toward clean air (“externalities”). SMUD sets aside $20 million per year as a “hedge” against purchased energy costs in low hydropower years, and yet gives no value to its renewable energy programs as a means to reduce dependence on varying hydro capacity. And power providers certainly don’t care for the economic benefits resulting from locating manufacturing plants in the District (shown in Fig. 2 as the resultant “Service Revenues”). These value omissions all add up to an unwarranted barrier within SMUD’s own accounting and operations systems.

We wish to examine just one of the omissions in valuing SMUD’s investment in grid-connected PV, the time-of-day economic benefits of PV output, which has emerged during the summer of 2000 as especially significant.

Renewable resources are often devalued because of their intermittency (depending on variable sun or wind resources), with “capacity factors” around 20% to 25%, and compared unfavorably to “baseload” resources which can run all night with consequent high capacity factors (but why do the need to?). And renewable energy resources are also frequently devalued by the inability to “dispatch” them on demand. But since the greatest time of need for power is during the daytime, and especially during sunny days when it is also hot, generating a considerable peak in demand for cooling in the Sacramento climate, it is the “effective” capacity factor of the PV that is important—its availability when the power it produces is actually needed. It has been shown by Professor Richard Perez of the State University of New York in Albany that PV can in favorable circumstances have an “effective capacity factor” for delivering valuable energy to the grid exceeding 90%.

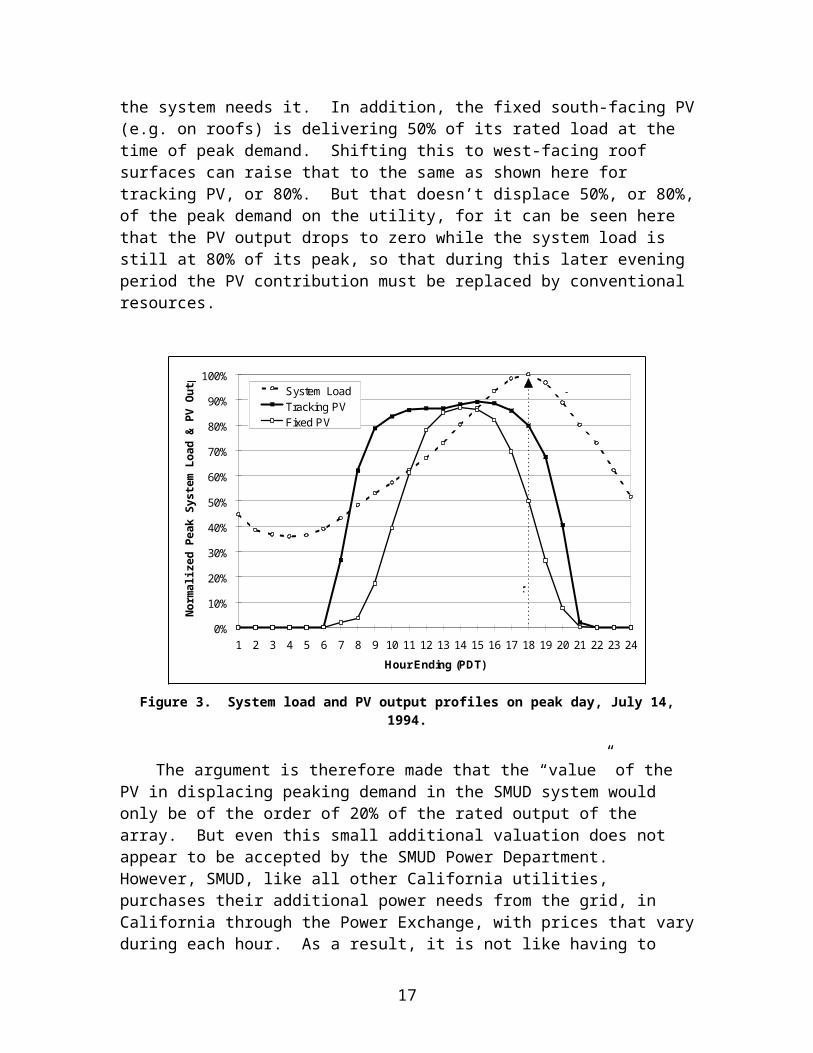

Fig. 3 on the next page shows the coincidence of the output of grid-connected PV in the SMUD District in proportion to overall system load on the peak demand day in 1994. The PV delivers energy during most of the time that the system needs it. In addition, the fixed south-facing PV (e.g. on roofs) is delivering 50% of its rated load at the time of peak demand. Shifting this to west-facing roof surfaces can raise that to the same as shown here for tracking PV, or 80%. But that doesn’t displace 50%, or 80%, of the peak demand on the utility, for it can be seen here that the PV output drops to zero while the system load is still at 80% of its peak, so that during this later evening period the PV contribution must be replaced by conventional resources.

11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Hour Ending (PDT)

Norm

aliz

ed P

eak

Syst

em L

oad

& PV

Out

put System Load

Tracking PVFixed PV

System Load

Peak Hour

Figure 3. System load and PV output profiles on peak day, July 14, 1994.

The argument is therefore made that the “value” of the PV in displacing peaking demand in the SMUD system would only be of the order of 20% of the rated output of the array. But even this small additional valuation does not appear to be accepted by the SMUD Power Department. However, SMUD, like all other California utilities, purchases their additional power needs from the grid, in California through the Power Exchange, with prices that vary during each hour. As a result, it is not like having to suddenly bring a peaker on line and quickly up to 80% of its capacity in the late evening hours. Instead, the PV has actually displaced the value of its output directly out of the power purchase costs of the utility, truly saving SMUD that money.

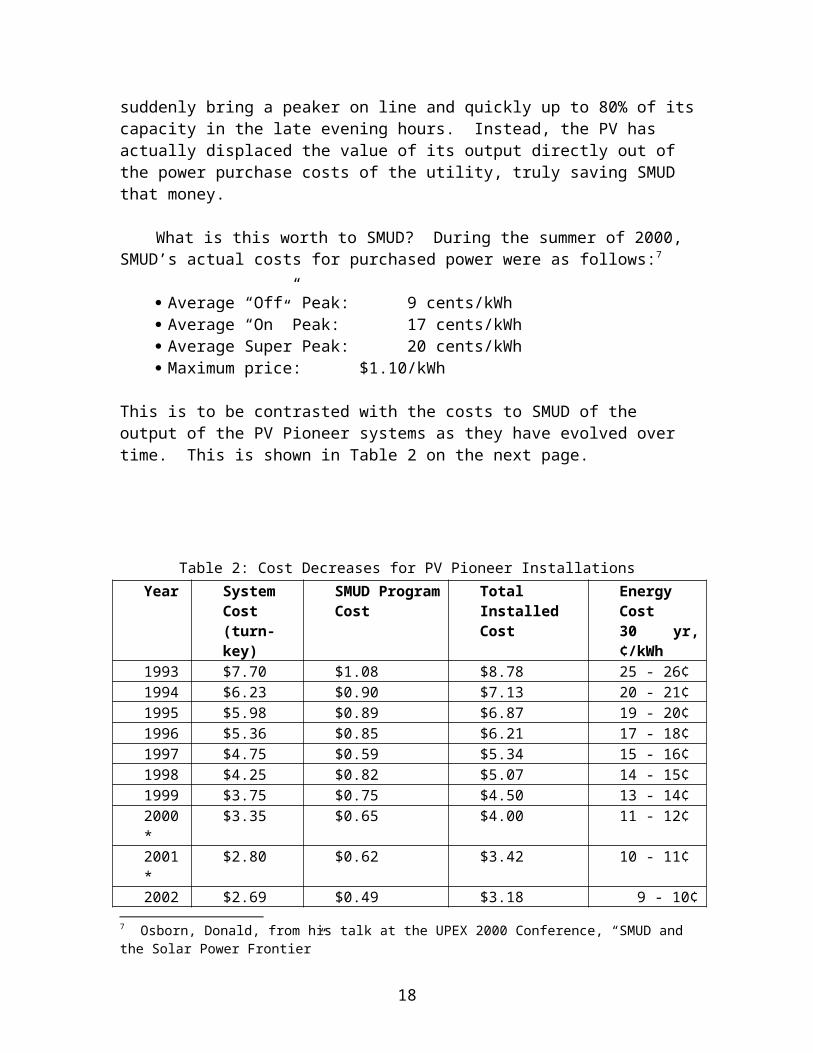

What is this worth to SMUD? During the summer of 2000, SMUD’s actual costs for purchased power were as follows:7

Average “Off” Peak: 9 cents/kWh Average “On” Peak: 17 cents/kWh Average Super Peak: 20 cents/kWh Maximum price: $1.10/kWh

This is to be contrasted with the costs to SMUD of the output of the PV Pioneer systems as they have evolved over time. This is shown in Table 2 on the next page.

7 Osborn, Donald, from his talk at the UPEX 2000 Conference, “SMUD and the Solar Power Frontier”

12

Table 2: Cost Decreases for PV Pioneer InstallationsYear System

Cost(turn-key)

SMUD ProgramCost

Total InstalledCost

Energy Cost30 yr, ¢/kWh

1993 $7.70 $1.08 $8.78 25 - 26¢1994 $6.23 $0.90 $7.13 20 - 21¢1995 $5.98 $0.89 $6.87 19 - 20¢1996 $5.36 $0.85 $6.21 17 - 18¢1997 $4.75 $0.59 $5.34 15 - 16¢1998 $4.25 $0.82 $5.07 14 - 15¢1999 $3.75 $0.75 $4.50 13 - 14¢2000* $3.35 $0.65 $4.00 11 - 12¢2001* $2.80 $0.62 $3.42 10 - 11¢2002* $2.69 $0.49 $3.18 9 - 10¢2003* $2.59 $0.39 $2.98 8 - 9¢

All costs in $ per kW (PTC; A/C) for “standard” roof. * Committed contract prices at contracted efficiencies.Energy cost levelized ($real) over 30 years at District cost of money or 1st mortgage rate (w/o tax benefits).

Clearly the SMUD PV program has already reached a point where purchasing energy from the SMUD PV arrays is competitive at all times with SMUD’s costs for purchased power, and a bargain during all peak times.8 And this still doesn’t take into account the several other benefits quantified by Wenger, Hoff and Pepper but not accepted by the SMUD Power Department. We certainly recommend that this and other actual economic benefits of PV to the SMUD system be valued by SMUD, to offset some more of the apparent costs to SMUD, or, better, to internalize some of the costs against real benefits, so

1.4 Assessment of Program Implementation

1.4.1 Contractor Selection and management

From the very beginning of their Program, SMUD has used competitive procurements to select the contractors for installation of their PV systems. Requests for proposals (RFPs) were issued and multiple awards were made for multiple systems based on qualifications and cost. Awarding volume contracts to multiple vendors helped to build a foundation for a healthy market while also keeping unit costs down through competition and volume purchases. (The first column in Table 1 reveals the multiplicity of participating vendors.)

In 1997, SMUD changed their approach and, in an effort to gain maximum purchasing leverage issued single five-year contracts for module and inverter supply. Since these two contracts were issued under a competitive solicitation, the lowest cost

8 The authors of this report sought to make an actual valuation of this for the summer of 2000, but were not given the requested cost information to enable the calculations. This is also a SMUD problem.

13

was assured. However, the five-year contracts meant that SMUD would be dependent on this single supplier for the success of the program for the period of the contract.

To reduce this exposure, SMUD did structure these contracts so that if the given supplier did not perform, SMUD was free to look elsewhere for sources of supply. The result was that SMUD limited the downside exposure to the loss of time, which would result from sub-par performance or total non-performance.

In retrospect, this strategy appears to be paying off. Although both the inverter and module supplier were late in meeting their delivery schedules, there has been little negative impact on the program. SMUD simply supplemented module delivery from its contracted supplier with modules purchased ‘on the market’ to meet its program plan and accepted substitute product and/or rescheduled installation sequences to accommodate the lateness of the inverter delivery.

In general, management of the contractors has been quite good under the program. The SMUD purchasing group issued contracts with performance terms favorable to SMUD, and SMUD’s technical group kept a watchful eye on field installations. While there was some schedule slippage, overall performance of the suppliers and installation contractors has been very positive, especially when one considers that the entire PV program was breaking new ground.

It is important, as future phases of the program take form, that SMUD continue to maintain maximum contractual flexibility in terms of options so that the program’s success is not dependent on the performance of any single supplier.

1.4.2 Technical Support and Warranties

One of the great strengths of the SMUD Solar program is the quality of their technical support. This does not just mean service in the field, or replacement of faulty product. SMUD has developed a careful quality assurance/quality control (QA/QC) program to which all suppliers of PV and components must adhere. They actually sign QA/QC assurance documents.

Furthermore, SMUD’s own constant testing has turned up potential problems that they have then gone back to the manufacturer to solve—often using the suggestions of SMUD’s technicians—as a means of avoiding problems before they can occur in the field. This is a significant factor in the overall excellent and long-term performance that SMUD is realizing in the field.

Warranty provisions were clearly established for key components during the RFP process and reinforced as the contracts were put into place. SMUD has had little in the way of field failures and has gotten the manufacturers to make good on their equipment under the terms of the warranties.

14

1.4.3 System performance/availability

In the Introduction to this section we noted that SMUD’s 1984 and 1986 PV installations at the Rancho Seco site have been working reliably ever since. The only difficulties have been with the inverter for the Phase II array. Replacing that cleared up those problems, but that was an indicator of the fact that, while the hundreds of PV arrays that SMUD has installed show no signs of lifetime degradation or lack of reliability, the weak point has been in the power conditioning electronics.

SMUD is in the unique utility position of having 16 years of experience with a multi-megawatt grid-connected application, thus lending confidence to SMUD’s expectations of future reliability. Quoting from Osborn (see footnote #1):

After 16 years, 7MW [now, in 2000, 8MW] and nearly 600 PV systems of PV operational experience, SMUD has determined that PV can be simply installed and operated with high reliability. Indeed, the performance and reliability improves with volume. Installation of large numbers of like systems results in better performance than that of demonstration projects of a few systems…

Scientists from the Sandia National Laboratory studied 100 of the first Pioneer I PV systems, installed in 1993 and 1994. This analysis produced “availability factors” (PV systems working) of 92% or higher for 88% of the systems, with the one lowest still at 44%. A second way of rating PV system performance is the “Performance Index”9, which rates the actual performance of PV systems against their simulated performance, taking into account realistic variables and losses. A PI of better than 90% is considered excellent. Measurements on SMUD’s installed systems consistently show this kind of performance.

1.4.4 Potential Technical Application Evolution of the SMUD PV Program

The leading candidate technologies to meet the goals for low-cost PV are thin-film products. While they currently promise lower cost per watt, all the available thin-film technologies are lower in efficiency than their crystalline counterparts – some dramatically so. A thin-film array needs to be larger in size to deliver a given amount of power when compared to an array of crystalline modules. Thus, the number of individual modules that need to be mounted, fastened and wired is greater. This is an important criterion as it can reduce or eliminate the cost advantage of the thin-film products.

SMUD should work with their chosen suppliers to identify ways to mitigate this area-related cost penalty at both the module and system level. In this regard it is noteworthy that the new Sacramento-based EPV plant is beginning to produce Copper Indium diselenide (CIS) modules, a technology which has achieved the highest efficiency

9 Wenger, Hoff and Pepper, see footnote 6.

15

of all thin film products, potentially competitive with crystalline efficiencies. That should be a good technical choice for SMUD.

As the number of residential rooftop retrofit systems increases within the SMUD service territory, the availability of candidate sites with ‘ideal roofs’ will eventually become a constraining factor to limit further program opportunity. One of the factors, which currently make a residential roof attractive, is if it has composition (asphalt) shingles. There are many homes within the District with tile or shake roofing, which, save for the difference in roof materials, would be good candidates. SMUD should work with their chosen contractors and suppliers to identify and/or develop cost effective methods to retrofit residential roof-top systems on non-composition roofs. This will expand the pool of desirable candidate roofs, allowing the program more room for growth while satisfying a larger cross-section of customers.

New residential construction represents a major opportunity for the SMUD PV program. SMUD’s present method of installing a PV array on a new residence during the initial construction makes use of solar tiles called ‘Sunslates’ which displace conventional roofing materials to become the finished roof. While this concept is very appealing, the present product is too expensive to achieve the longer-term cost goals set out for the rooftop program. SMUD should work with their chosen suppliers to identify ways to expand the options for PV roof integration in new residential and light commercial construction as well as roof replacements. One option might be to explore the development of larger-area modules using lower-cost thin-film PV configured for direct roof-integration.

Another aspect of new residential construction is the provision of the basic infrastructure to make the future installation of a rooftop PV system easier in homes where the systems cannot be installed during construction. SMUD should work with their chosen suppliers to develop PV-friendly design and construction approaches, which make future PV retrofits easier.

There is considerable potential promise for the SMUD program in the use of building-integrated PV in new commercial construction. The architects are the gatekeepers to this market and must be inspired to incorporate BIPV at the very beginning of the design process. SMUD has begun to successfully engage the architectural community and interest in building. One way to help to increase the incorporation of BIPV systems is to expand the range of options for available PV modules. Currently the thin-film PV modules are only available in a two by four foot format. Architects constantly ask for other sizes and options. SMUD should work with their chosen suppliers to identify ways to expand the range of cost-competitive hardware options for BIPV in commercial buildings.

16

1.5 Summary of Technical Approach

1.5.1 How is the program doing relative to its goals?

Any program working with the initial introduction of a wholly new technology on such a scale represents considerable risk. The authors believe that SMUD has understood and managed this risk well. In most respects, the SMUD PV program seems ‘on track’ with their overall goals and in some respects is actually ahead. Some could argue that the cost reductions in the coming phase of the program may be more of a challenge to achieve than those of prior phases. While this may be true, the PV industry has changed dramatically during the first decade of the SMUD PV program and is now far more able to reach the goals set out for the program than it has been previously. With continued consistent support from upper management, the SMUD program appears well positioned to achieve its overall goals for Sustained Orderly Development and Commercialization during the next phase of the effort.

1.5.2 Recommendations for the future.

During the author of this Section’s (SS) work with PV for residences, the one thing homeowners have most often inquired about is the availability of their utility-interactive PV system in the event of a utility outage. It is suggested that SMUD investigate the prospect of offering residential PV Pioneer II customers a battery bank option capable of carrying some portion of the house loads (such as the critical ‘core’ loads) through a ‘typical’ power outage. While this would add cost and complexity to the residential program offering, it is the function most often requested and could be offered only when the customer wanted it.

One of the most important opportunities available to SMUD is to leverage the PV program effort with the Energy-efficiency program. It is well known that it is easier to save energy than it is to produce it. Further, if the energy needs of, for example, a new house are reduced during the planning and construction, the contribution from a roof-top PV system would contribute a far more meaningful percentage of the home’s power.

Energy-efficient demonstration homes have been designed and constructed in hot climates where cooling requirements dominate, that combine advanced conservation techniques with solar water heating and rooftop PV. The results are impressive, with no net addition to the utility peak demand from the residence even during heavy cooling periods.10

These results emphasize the benefits of an integrated approach where the energy efficiency and the solar systems are incorporated together as part of an overall approach. The results further would suggest that SMUD revisit the emphasis of their solar water-heating program. While solar water heating systems do compete for available roof area

10 “Field Evaluation of Efficient Building Technology With Photovoltaic Power Production in New Florida Residential Housing”, FSEC-CR 1044-98, November, 1998. See also Parker, D., and Sheinkopf, K., “Cool Home Features Bring Peak Energy Savings”, Home Energy, July/August 1999 (pp. 22-27).

17

with PV systems, the properly designed and installed solar water heating system will displace 3 to 4 times the kWh per dollar when compared to the same investment in a PV system. Just as PV hardware and systems have evolved in recent years, so have SDHW systems. The authors believe these systems can and should play a more important role in SMUD’s overall strategy.

As the popularity of the PV Pioneer II systems continues to grow, SMUD should begin to develop PV Pioneer 2 systems for commercial buildings. While the authors believe that the residential market will be the first to reach full commercial status, the commercial buildings market will not be far behind. The SMUD program has fielded many PV systems on commercial buildings. It will be a relatively simple task of defining the optimum system package, with perhaps a few variations in size and configuration, to offer to the commercial customer.

Other recommendations for SMUD’s PV Future:

SMUD should concentrate on their own service territory first and foremost as this is the area that provides the greatest opportunity for achieving their program goals. If organizations outside of SMUD request collaboration, SMUD should help them as it can. But SMUD should not spend a significant amount of resources cultivating such opportunities until later in the program

In the promotion of the PV Pioneer 2 options, SMUD should emphasize the highly valued but intangible benefits of owning your own PV system, such as:• It is environmentally responsible• It has a clear and very visible ‘green appeal’• It is backed by SMUD – a known and trusted partner in the community who will be there in the long term.

SMUD should seek to understand in more detail the market development cycle as described in Section 3 of this report and market first to the innovators and early adopters as they are indeed the first customers. The use of detailed web site will help to reach and convince these prospects.

18

2. SMUD’s PV MARKET DEVELOPMENT AND ITS RELATIONSHIP TO OTHER UTILITY PROGRAMS

2.1 Introduction

The involvement of SMUD in photovoltaic applications arises from the utility’s goal of obtaining at least half of its energy from energy efficiency, existing hydroelectric plants, and renewable energy resources, beginning in the year 2000 and extending beyond. But the involvement of SMUD in the market development of PV goes beyond these aims, for SMUD has also been convinced that their large and visible role in the PV market should contribute in a significant way toward the lowering of costs for installed PV systems in general, which would benefit all PV purchasers, and lower the costs for SMUD’s own PV applications even further. And SMUD has clearly seen a business opportunity growing out of this that transcends their own applications.

This latter aim is confirmed in written descriptions of SMUD’s commercialization philosophy, such as “The SMUD Solar Program is a business development and commercialization effort for the sustained orderly development and commercialization (SODC) of grid-connected PV.”11 And “SMUD would rather…provide photovoltaics as a business opportunity than concede that to someone else.”12

This being the case, it is important to look at the ingredients of SMUD’s “business plan for photovoltaics” as shown by the history of their Solar Program since 1993, to look for evidence that their business plan has also stimulated other utilities to follow their lead, and to appraise elements of a future business plan for photovoltaics that might help SMUD to achieve their long-range PV business goals. This and the next major Section of this report seeks to present our views on this.

2.2 Overview of SMUD’s Market Development Philosophy

The underlying philosophy adopted for the SMUD Solar Program had first been enunciated by one of the authors of this report (DA) in a report to the State of California in 1991, and further refined in later publications13:

Simply stated, it [SODC] represents a condition in which the costs of a new technology progressively decline through the action of a growing and stable market that is stimulated by orders placed on a reliable and predictable schedule. The orders increase in magnitude as previous deliveries and engineering and field experience lead to further reductions in costs. And, with respect to the renewable electric power resource, the reliability of these orders can be projected many years

11 Osborn, Donald E., Sustained Orderly Development and Commercialization of Grid-Connected Photovoltaics: SMUD as a Case Example, Advances in Solar Energy, Vol. , No. , pp. 12 Ibid.13 See, for example, Aitken, D.W., Sustained Orderly Development of the Solar Electric Technologies, SOLAR TODAY, Vol. 6, No. 3, p. 20 (May/June, 1992).

19

into the future, on the basis of long term contracts, to minimize market risks and investor exposure.14

Early on, SMUD decided to “force” the cost-reducing benefits of SODC by taking advantage of the opportunity those contracts for significant amounts (megawatts) of PV would provide. These were initially awarded on a year-by-year basis to the winning bidders. But then SMUD added the advantage of a five-year guaranteed contract, again for MWs of PV. PV manufacturers and installers willingly responded with bids guaranteeing continuing year-by-year cost reductions, on the assumption that they could reduce their own costs at a sufficiently rapid pace to provide at least minimal profit over the term of the contract. The results, from the inception of the Solar Program to the end of the present 5-year cycle, for systems applied to the PV “Pioneer” programs, were first shown in Table 2, Section 1 of this SMUD PV Program Review. We reproduce that here for convenience.

Table 2: Cost Decreases for PV Pioneer InstallationsYear System Cost

(turn-key)SMUD ProgramCost

Total InstalledCost

Energy Cost30yr, ¢/kWh

1993 $7.70 $1.08 $8.78 25 - 26¢1994 $6.23 $0.90 $7.13 20 - 21¢1995 $5.98 $0.89 $6.87 19 - 20¢1996 $5.36 $0.85 $6.21 17 - 18¢1997 $4.75 $0.59 $5.34 15 - 16¢1998 $4.25 $0.82 $5.07 14 - 15¢1999 $3.75 $0.75 $4.50 13 - 14¢2000* $3.35 $0.65 $4.00 11 - 12¢2001* $2.80 $0.62 $3.42 10 - 11¢2002* $2.69 $0.49 $3.18 9 - 10¢2003* $2.59 $0.39 $2.98 8 - 9¢

All costs in $ per kW (PTC; A/C) for “standard” roof. * Committed contract prices at contracted efficiencies.Energy cost levelized ($real) over 30 years at District cost of money or 1st mortgage rate (w/o tax benefits).

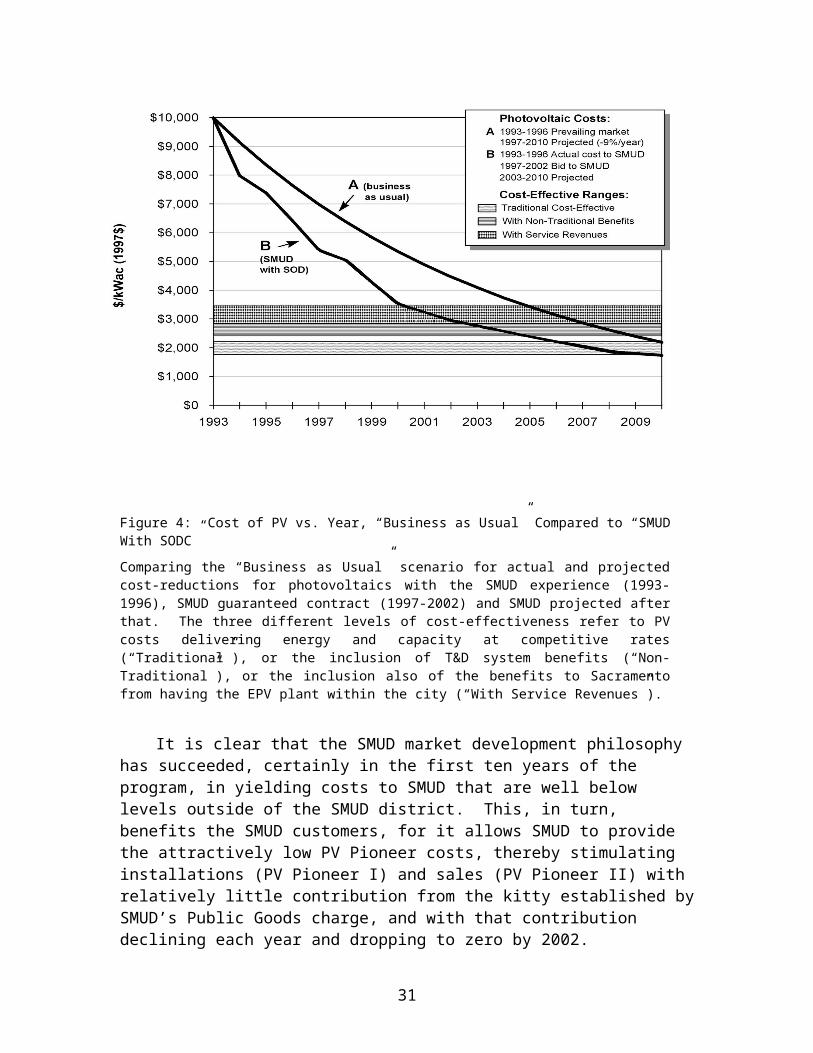

The result of this, though, is that SMUD’s SOD experience and projections departed from national expectations and experience elsewhere. This is illustrated in Fig. 4 on the next page, with costs shown for PV modules only.

14 Aitken, Donald W., New Economic Thinking and Approaches to Utility Scale Application of Solar Energy in the 90s, Advances in Solar Energy, Vol. 11 (1997). The “SOD” market dynamic was only recently slightly retitled by SMUD to “SODC”, to take into explicit account the commercialization aim of the philosophy.

20

Figure 4: Cost of PV vs. Year, “Business as Usual” Compared to “SMUD With SODC”

Comparing the “Business as Usual” scenario for actual and projected cost-reductions for photovoltaics with the SMUD experience (1993-1996), SMUD guaranteed contract (1997-2002) and SMUD projected after that. The three different levels of cost-effectiveness refer to PV costs delivering energy and capacity at competitive rates (“Traditional”), or the inclusion of T&D system benefits (“Non-Traditional”), or the inclusion also of the benefits to Sacramento from having the EPV plant within the city (“With Service Revenues”).

It is clear that the SMUD market development philosophy has succeeded, certainly in the first ten years of the program, in yielding costs to SMUD that are well below levels outside of the SMUD district. This, in turn, benefits the SMUD customers, for it allows SMUD to provide the attractively low PV Pioneer costs, thereby stimulating installations (PV Pioneer I) and sales (PV Pioneer II) with relatively little contribution from the kitty established by SMUD’s Public Goods charge, and with that contribution declining each year and dropping to zero by 2002.

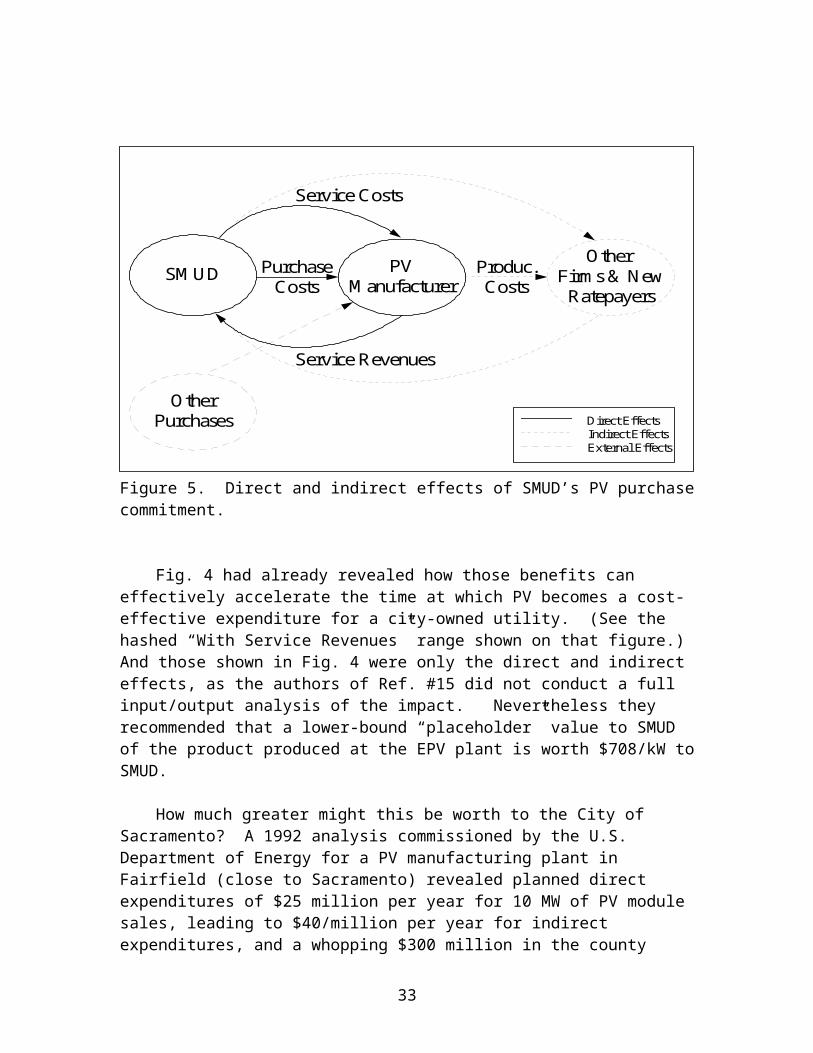

A second important part of SMUD’s market development philosophy is to leverage the societal benefit of the funds that they spend for PV by developing PV and balance-of-system production and assembly within the SMUD District. In this way jobs and tax revenues are produced locally, with consequent “multiplier” benefits of those expenditures. The winning bidder in SMUD’s present five-year contractual period, Energy Photovoltaics, Inc. (EPV) has indeed located a plant within Sacramento, and will soon deliver Copper Indium diselenide modules (CIS) manufactured in that facility to SMUD. Fig. 5 schematically illustrates two of the three multiple economic benefits resulting from PV-related expenditures when such a PV manufacturing facility is located in the District. [The three levels of benefits are 1) direct (sales of manufactured product),

21

2) indirect (acquisition of materials and supplies from within the District for the manufacture of finished product), and 3) induced (tax revenues, job-production and expenditure of PV plant employee income in the District)].15

Produc.Costs

PurchaseCosts

SMUD PVManufacturer

Other Firms & New

Ratepayers

Service Costs

OtherPurchases

Service Revenues

Direct Effects Indirect Effects

External Effects

Figure 5. Direct and indirect effects of SMUD’s PV purchase commitment.

Fig. 4 had already revealed how those benefits can effectively accelerate the time at which PV becomes a cost-effective expenditure for a city-owned utility. (See the hashed “With Service Revenues” range shown on that figure.) And those shown in Fig. 4 were only the direct and indirect effects, as the authors of Ref. #15 did not conduct a full input/output analysis of the impact. Nevertheless they recommended that a lower-bound “placeholder” value to SMUD of the product produced at the EPV plant is worth $708/kW to SMUD.

How much greater might this be worth to the City of Sacramento? A 1992 analysis commissioned by the U.S. Department of Energy for a PV manufacturing plant in Fairfield (close to Sacramento) revealed planned direct expenditures of $25 million per year for 10 MW of PV module sales, leading to $40/million per year for indirect expenditures, and a whopping $300 million in the county resulting from the sum total of “induced” expenditures16. One might conclude, therefore, that the benefits to Sacramento 15 Wenger, H., Hoff, T., and Pepper, J.: Photovoltaic Economics and Markets: A Case Study of the Sacramento Municipal Utility District, report sponsored by the California Energy Commission, Sacramento Municipal Utility District and the U.S. Department of Energy (1996).16 Demeter, Christian, Economic Impacts of a Photovoltaic Module Manufacturing Facility, United States Department of Energy, Office of Conservation and Renewable Energy, Office of Solar Energy Conversion, Photovoltaic Program, Washington, D.C. May 7, 1992.

22

from locating the EPV plant within City limits could be from 8 to 12 times the direct value, greatly enhancing the economic benefits of SMUD’s PV program for the City. And it should also be pointed out that SMUD has succeed in attracting a major components manufacturer, Trace Engineering, to locate the assembly of the inverters within the SMUD District, further enhancing the economic benefits to Sacramento.

The questions to be posed now are whether this marketing philosophy is

sustainable, or in what ways might SMUD begin to position their evolving Solar Program to keep it as a sustainable business element within SMUD that at least earns back its own costs, while continuing to benefit their customers and their District in important and practical ways.

2.3 Evidence for the Emulation of the SMUD Model by Other Utilities

One way to approach the question posed just above is to examine the extent to which other utilities may have emulated SMUD’s program, or at least some elements of it, perhaps revealing that they also believe that it is or will be good utility business to get into the PV business early, and in a significant way. In his fine contribution to the publication “Advances in Solar Energy”17, author Donald Osborn presented several case examples, specifically for LADWP, the Spire/ComEd/City of Chicago SODC Solar Program, GPU Solar, Idaho Power’s Applied Power Corporation, Tucson Electric Company and Global Solar, Duke Solar, and the Arizona Environmental Portfolio Standard. The author of this section of the present report (DA) visited the LADWP offices to interview the founder of both that program and SMUD’s (David Freeman), along with representatives from the LADWP PV program. He also conducted telephone interviews with the solar program managers for all of the other programs, save for Duke Solar, which is a solar thermal-electric program. In the interest of brevity of the present report, we shall not repeat the descriptions of those other programs, preferring to refer the reader to Osborn’s publication. Nevertheless, some comments on the results of these interviews are presented in the following as they affect an interpretation of SMUD’s marketing philosophy.

The overall conclusions from the telephoned interviews is that there is really only one other utility program that is of a scope in both size and multi-year focus similar to that of SMUD, and which also shares the same sort of utility-benefit-centered PV marketing goals as SMUD, and that is the LADWP solar program. As noted above, both programs were founded by the same person, David Freeman, who was SMUD’s Administrator during the conception of SMUD’s Solar Program, and who hired Donald Osborn to direct it. So the LADWP program is not exactly an “emulation” so much as an “evolution of concept”. It nevertheless demonstrates that elements of the SMUD model work in other and even larger municipal utility frameworks, and therefore that the

17 See Footnote 11. Donald Osborn is SMUD’s Superintendent for Renewable Generation including Photovoltaic and Distributed Technologies (PV/DT) group in the Power Generation Department.

23

extrapolation of the SMUD model rests more on utility leadership than on the particulars of the model.