real estate assignment 1 final copy

TRANSCRIPT

1

Hospitality Real Estate

Faculty: Adams

February

Hospitality Real Estate

Assignment #1- Trends in US

Hotel Real Estate Market

Andrew Axelrad

304628

2

2014

Statement of authorship

I certify that this assignment is my own work and contains no material which has been accepted for the

award of any degree or diploma in any institute, college or university. Moreover, to the best of my

knowledge and belief, it contains no material previously published or written by another person, except

where due reference is made in the text of the dissertation.

Signed ____________Andrew Axelrad_________________________

Date _________________15/02/2014__________________________

3

Table of Contents Executive Summary ............................................................................................................................ 4

I. Literary Review ........................................................................................................................... 5

A. Investor Profiles ....................................................................................................................... 5

1. Research .............................................................................................................................. 5

2. Analysis............................................................................................................................... 5

B. Investor Trends for Purchasing and Financing ............................................................................ 5

1. Purchasing Trends: Quality Properties and Secondary Markets ............................................... 5

2. Asset-Light Trends with Management and Franchising Contracts ............................................ 6

3. Investor Purchasing Analysis ................................................................................................ 6

C. Financing Trends: REITs and CMBS........................................................................................ 7

1. Real Estate Investment Trusts ............................................................................................... 7

2. Commercial Mortgage-backed Securities ............................................................................... 7

3. Investor Financing Analysis .................................................................................................. 8

D. Investor Expectations in Regards to Risk and Return .................................................................. 8

1. Theory on Return ................................................................................................................. 8

2. Theory on Risk..................................................................................................................... 9

3. Risk and Return of US Hotel Market ..................................................................................... 9

4. Risk and Return Analysis .................................................................................................... 10

II. Conclusions and Recommendations ............................................................................................ 11

III. Appendices A through I .......................................................................................................... 12

Appendix A: Other US Hospitality Trends ..................................................................................... 12

Appendix B: Sales Comparison by Price/Room with Assets > $10 Million ....................................... 12

Appendix C: Hotel Management 2013 Franchise Percentages.......................................................... 13

Appendix D: HVS Recommended Valuation Approaches ............................................................... 13

Appendix E: Specific HVS Risk Factor with Andrew’s Examples ................................................... 14

Appendix F: Aon Risk Solutions’ Investor Survey Rankings ........................................................... 14

Appendix G: Average Cap Rates for US Hotel Properties................................................................ 14

Appendix H: Reported Internal Rates of Return (by market)............................................................ 15

Appendix I: PESTEL Analysis and Food for Thought ......................................................................... 15

Works Cited ..................................................................................................................................... 16

4

Executive Summary This report was commissioned to examine the US hotel real estate market through the likes of investor

profiles, purchasing and financing trends of investors, and investor expectations in terms of risk and

return. The key findings in the literary review stipulate an influx of foreign investors in the US hotel

market as well as the transitioning of financing from REITs to private equity. Furthermore, investors are

trending to purchase quality hotel properties in larger markets and select service, franchised properties in

secondary markets. With increases in investor confidence from historically low interest and capitalization

rates, perceptions of risk are inherently low with high expectations of profit. Thus, the US hotel real estate

market is expected to continue growth through 2016 and beat transaction numbers in 2014. However,

what are the inconsistencies between real estate reports, academic articles and reports, and my personal

contributions on the market? We find that some reports and academic articles focus on different kinds of

numbers and intangible factors influencing different perspectives and advocacies. Hence, investors should

be weary of bidding wars for high quality properties and over supply with lower RevPARs for select

service branded properties in secondary markets. Also, with cheap financing and low capitalization rates,

investors should mind the inevitable future of increased interest rates and over-valuation of properties

when looking to purchase. Nevertheless, the US hotel market looks generally optimistic and a good place

to invest for the foreseeable future with RevPARs expected in the high single digits.

5

I. Literary Review

A. Investor Profiles

1. Research

Investors in the US hotel market stem mostly from private equity firms, wealthy family conglomerates,

sovereign wealth funds, and real estate investment trusts (REITs). Majority of the private equity investors

come from the US, Europe, and Southeast Asia who compete for properties from two kinds of sellers:

owners from quality, well performing assets and owners with debt repayment issues. The US market has a

lot of demand coming from Middle Eastern and Chinese investors who look to diversify their portfolios

with stable political, economic, and currency macro factors (Jones Lang LaSalle, 2013, p.5). In regards to

the American investor, Colliers reported 50% of investors willing to take on more risk and 50% not as

willing within the next year. US investors were most interested in yield, economic growth, barriers to

entry, and the property itself. However, even with a relatively flexible approach towards taking on more

risk with favorable parameters, for US investors, hotels were one of the “lease desired” property types

(Colliers International, 2014). Moreover, Jason Freed from HotelNewsNow.com, quotes Lauro Ferroni,

VP of research and strategic advisory for the American branch of Jones Lang LaSalle to identify a shift

from REITs to private equity investment (Freed, 2014).

Figure 1: Hotel Buyer Types

Year/Buyer

Type

Private Public Equity Fund Inst’l Cross-Border

2013 (Q3) 41% 21% 20% 5% 12%

2012 33% 19% 26% 8% 12% 2011 26% 34% 19% 8% 10%

(Mellen, The Hotel Industry Outlook − U.S. Hotel Transactions, 2014) (Source: Real Capitalist Analytics

(RCA))

2. Analysis

All-in-all, most reports concur on popularity shifts to private equity and increased volumes of foreign

investors. However, seller profiles have some disparity since hotel valuations are on the rise, especially

for quality properties. In fact, I believe most quality properties are not for sale since reports expect growth

in the market through 2016 (Rushmore Jr., Kuehnle, & Buckhout, 2013). I would suspect quality property

owners to ride the high times driving up prices with intense bidding wars (PKF Consulting USA, LLC,

2013). On the other hand, with impending slowdown of BRIC and other emerging economies, I think

investment from those countries could decline. However, even with potential currency risks imposed on

foreign investors, there is still more likely to be an influx of investors looking to diversify into a more

stabilized economy like the US. Why not invest in a growing hospitality market?

B. Investor Trends for Purchasing and Financing

1. Purchasing Trends: Quality Properties and Secondary Markets

Two major trends in the US market are investments in high quality properties and investment in secondary

or tertiary markets (Freed, 2014; PKF Consulting USA, LLC, 2013; Smith Mai & Morton, 2013). HVS is

in agreement to the two aforementioned trends considering they have data showing trends in the upscale

market, with the high-end upscale increasing room numbers by 10.4% and upscale increasing by 25%.

6

Even though this data is from April 2013, the RevPAR growth is not expected for 3-5 years (Rushmore

Jr., Kuehnle, & Buckhout, 2013). Despite increases in upscale room production and acquisitions, Zachs

Equity Research finds investment opportunities from demand exceeding supply and quotes PwC as

forecasting 0.8% supply growth compared to a 1.8% demand growth (Zacks Equity Research, 2013).

Although PwC indicates positive occupancy rates in the high-priced market segment, HVS notes increases

in supply from the extended-stay and select service segment. Investors seem to be optimistic regarding

high demands, but are concerned with operating performance and consequently overpaying in a risky

market (Rushmore Jr., Kuehnle, & Buckhout, 2013, p. 16). Contrary to potential increased supply from

HVS, PwC contends select service hotels as being a very popular trend in secondary and tertiary markets

where RevPAR growth is less consistent (PwC and the Urban Land Institute , 2012, p. 58). On the other

hand, the secondary and tertiary market could face limited amounts of buyers due to pricing conflicts

inflicted by brand and management impediments (Jones Lang LaSalle, 2013, p. 12). Hence, more

formidable options for the hotel market is to redevelop, upgrade, and renovate existing properties to

attempt to reestablish RevPAR growth expectations which were dilapidated from a contracted world

economy (PwC and the Urban Land Institute , 2012, p. 58; Zacks Equity Research, 2013). (See Appendix

A: Other US Hospitality Trends for more information on less popular trends and see Appendix B: Sales

Comparison by Price/Room with Assets > $10 Million)

2. Asset-Light Trends with Management and Franchising Contracts

A major trend in the US hotel market is heading towards an “asset light” model. Asset light construes

popularity in management contracts as opposed to ownership which in turn can increase growth and

stability. Hoteliers focus on the operations side while owners concentrate on the real estate, providing

capital efficiencies (Zacks Equity Research, 2013). Ernst & Young more specifically adds to the “asset

light” approach through specific terminology, Opco-Propco structures. Not only does Opco-Propco

consider global tax, it also separates real estate assets to one company and operating assets to another

while providing structure to focus on one business entity, and providing potential to maximize brand value

amongst other intangibles. For example, REITs serve as the Propco and hotel operator represents the

Opco. However, public hospitality companies are popularizing a new approach by taking a minority

position on the Propco end through Opco common stock. Shareholders for the public hotel operator then

get a diversified portfolio from the Opco-Propco as a whole (Roth & Fishbin, 2013).

Trends in the US highlight midscale and economy properties with 32.9% and 23.5% of rooms respectively

representing franchise contracts in 2013. Additionally, franchising amongst midscale properties has been

the trend for the last several years (Ricca, 2013) (see Appendix C: Hotel Management 2013 Franchise

Percentages for more information).

3. Investor Purchasing Analysis

Analysis is difficult when numerous reports indicate differing trends within the US market. However, the

overall trends in common from most reports seem to be quality properties in large markets, and limited

service properties in secondary and tertiary markets. Most reports indicate an increased supply, especially

from the select service segment. Even though competition should increase from supply, revenue and

occupancy shouldn’t decrease too much. Both domestic and international tourism have regained

momentum which will have positive effects on occupancy and revenues (UBS, 2014). I disagree with

UBS because most foreign tourists will prefer large market cities like New York. The increase of supply

with the select service segment in secondary markets will not be as positively affected. With increased

7

franchising with midscale and economy properties, there could be increased brand impediments and

contract disputes. I think many investors in secondary markets may soon see cannibalization due to

excess supply and lower RevPAR growths.

C. Financing Trends: REITs and CMBS

1. Real Estate Investment Trusts

The SEC defines REITs as a company that owns and sometimes operates income yielding real estate

(SEC, 2012). REITs act as a kind of security and sell similar as a stock, but invest in real estate directly.

REITs usually receive tax benefits, are highly liquid, and offer high yields (Investopedia US, 2014). To

be considered a REIT in the US, a company must primarily have a bulk of their assets in real estate

investment, and must give 90% of its taxable income in the form of dividends. The SEC also requires

several other factors for companies to qualify as a REIT. Finally, there are typically three different kinds

of REITs including: equity REITs which are most common in owning and operating real estate, mortgage

REITs, and hybrid REITs (SEC, 2012).

In debate to the “asset light” and REIT trends in the US market, HVS cites a drop in REIT acquisitions in

the second half of 2011. HVS finds the Euro crisis, the US debt ceiling breakdown, share price cascades,

and other economic hindrances as causes to the decrease in REITs. Though REIT’s recovered in 2012,

they were very prudent in their acquisitions and signified an overall slowdown in transactions (Rushmore

Jr., Kuehnle, & Buckhout, 2013, p. 8).

2. Commercial Mortgage-backed Securities

Mortgage-backed securities are debt obligations tenable by mortgage loans to access cash flow (SEC,

2010; Investopedia US, 2014). Generally, investors can purchase loans from banks and mortgage brokers

who then either utilize the government or private companies to accumulate pools. Securities are then

issued to represent claims on the original amount in the pool borrowed plus interest payments made, or

securitization (SEC, 2010). Commercialized mortgage-backed securities are a type of mortgage-backed

security that are not standardized, are difficult to value, and are usually fixed terms initiating lesser

amounts of prepayment risk (Investopedia US, 2014).

Another funding trend in the US market is that debt liquidity is limited, but was expected to be at its

highest in 2013. Jones Lang LaSalle identifies large banks as the main player in debt financing in

hospitality real-estate, but do not have the ability to lend large amounts of money to most investors.

Hence, the main trend is commercial mortgage-backed securities (CMBS) which dictate favorable pricing

and terms within the market. Balance sheet lenders, although more stringent on their lending, offer

floating rate loan structures favorable to hotel owners. Since the US market has taken more of a one-

dimensional approach with CMBS, other forms of financing will provide senior debt including insurance

companies, mutual funds, and sovereign wealth funds. Later down the line, Jones Lang LaSalle expects

pension fund investors to enter the property and hotel markets (Jones Lang LaSalle, 2013, p. 5).

8

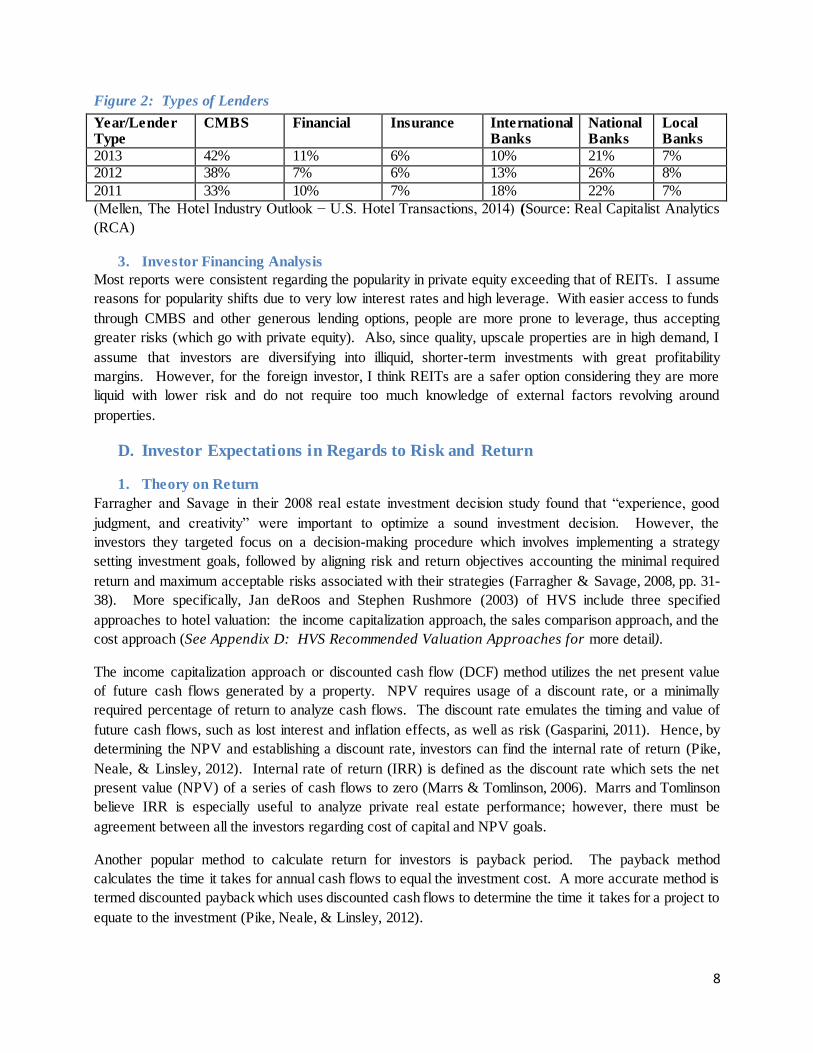

Figure 2: Types of Lenders

Year/Lender Type

CMBS Financial Insurance International Banks

National Banks

Local Banks

2013 42% 11% 6% 10% 21% 7% 2012 38% 7% 6% 13% 26% 8%

2011 33% 10% 7% 18% 22% 7%

(Mellen, The Hotel Industry Outlook − U.S. Hotel Transactions, 2014) (Source: Real Capitalist Analytics

(RCA)

3. Investor Financing Analysis

Most reports were consistent regarding the popularity in private equity exceeding that of REITs. I assume

reasons for popularity shifts due to very low interest rates and high leverage. With easier access to funds

through CMBS and other generous lending options, people are more prone to leverage, thus accepting

greater risks (which go with private equity). Also, since quality, upscale properties are in high demand, I

assume that investors are diversifying into illiquid, shorter-term investments with great profitability

margins. However, for the foreign investor, I think REITs are a safer option considering they are more

liquid with lower risk and do not require too much knowledge of external factors revolving around

properties.

D. Investor Expectations in Regards to Risk and Return

1. Theory on Return

Farragher and Savage in their 2008 real estate investment decision study found that “experience, good

judgment, and creativity” were important to optimize a sound investment decision. However, the

investors they targeted focus on a decision-making procedure which involves implementing a strategy

setting investment goals, followed by aligning risk and return objectives accounting the minimal required

return and maximum acceptable risks associated with their strategies (Farragher & Savage, 2008, pp. 31-

38). More specifically, Jan deRoos and Stephen Rushmore (2003) of HVS include three specified

approaches to hotel valuation: the income capitalization approach, the sales comparison approach, and the

cost approach (See Appendix D: HVS Recommended Valuation Approaches for more detail).

The income capitalization approach or discounted cash flow (DCF) method utilizes the net present value

of future cash flows generated by a property. NPV requires usage of a discount rate, or a minimally

required percentage of return to analyze cash flows. The discount rate emulates the timing and value of

future cash flows, such as lost interest and inflation effects, as well as risk (Gasparini, 2011). Hence, by

determining the NPV and establishing a discount rate, investors can find the internal rate of return (Pike,

Neale, & Linsley, 2012). Internal rate of return (IRR) is defined as the discount rate which sets the net

present value (NPV) of a series of cash flows to zero (Marrs & Tomlinson, 2006). Marrs and Tomlinson

believe IRR is especially useful to analyze private real estate performance; however, there must be

agreement between all the investors regarding cost of capital and NPV goals.

Another popular method to calculate return for investors is payback period. The payback method

calculates the time it takes for annual cash flows to equal the investment cost. A more accurate method is

termed discounted payback which uses discounted cash flows to determine the time it takes for a project to

equate to the investment (Pike, Neale, & Linsley, 2012).

9

Finally capitalization rates are another key aspect in in analyzing accounting rates of return. Although

accounting rates of return are not a popular or accurate way for analysis, capitalization rates depict the

relationship between a property’s net income and its value. However, cap rates taken from sales

transaction do not accurately define the effects of capital improvements upon the purchase price or

expectations of returns (Mellen, Hotel Capitlaization Rates And The Impact Of CAP EX, 2014).

Despite the previous procedures and methods to assess value and returns for hotels and real estate, there is

no “single perfect” way. There are a plethora of assessment methods utilizing many ratios and they are

only useful if applied properly. Consequentially, these analytical techniques are only valuable when

benchmarked appropriately with other ratios, methods, competition, and industry factors (Thompson,

2005).

2. Theory on Risk

HVS divides investment risk into 3 periods: development, operation, and exit. Development risks

comprise all the risks of starting a new project from locating the best piece of land to building the

property. Operating risks entail the holding period, depreciation, and cash flow generated to yield

expected returns to rationalize keeping or selling the investment. Exit risk affects the owner’s capability

to leave the investment or attempt to prolong the economic life. Internal obsolescence is a kind of exit

risk which has to deal with the deterioration of the building and whether it makes sense to push capital in

repairs. External obsolescence is an exit risk dealing with negative PESTEL factors making a project less

viable (Younes & Kett, 2006). Certain markets are more volatile to the aforementioned factors than

others; and usually incur RevPAR declines in recessionary years, but take on larger revenue yields in

subsequent cycles (Rushmore Jr., Kuehnle, & Buckhout, 2013, pp. 37-39). From a differing angle, Lee

(2001) includes review on the Modern Portfolio Theory which says investors should look at risk and

return of their overall portfolio as opposed to a single specific asset because individual risks are

diversified in the overall scheme. (See Appendix E: Specific HVS Risk Factors with Andrew’s Examples

and Appendix F: Aon Risk Solutions’ Investor Survey Rankings for more information)

3. Risk and Return of US Hotel Market

One major consensus within the US market is that it is relatively a good time be an investor in the hotel

sector. Hence, most hotel surveyors and hospitality forecasters describe similar outlooks in the US sector

being fuelled by positive investor sentiments. Historically lower interest rates paired with higher dividend

yields and investment confidence is causing capitalization rates to decline (Freed, 2014; PKF Consulting

USA, LLC, 2013; Smith Mai & Morton, 2013). However, with the increase of supply, competition will

arise providing greater options for consumers. Technologically advanced, newer properties will encumber

popularity amongst major market segments. Hence, technologically deficient properties will be forced to

invest in upgrades which can highlight issues for existing owners. Other risks to consider are the need for

contracting more employees for hotel operators - that may prefer unionized labor, complying properties

with American Disabilities Act standards, and decisiveness on whether to brand or not (Butler, 2014).

On the other hand, Jim Butler (2014), a renowned hotel lawyer internationally, believes peaking interest

from international investors utilizing many sources of capital, combined with competitive CMBS

financing will push the 2014 transaction figures beyond the $18 billion recorded in 2013. Furthermore,

HVS predicts overall growth in the US market to occur through 2016 and should have already exceeded

2006 values by the end of 2013. However, they are not sure just how fast revenue will continue to rise

(Rushmore Jr., Kuehnle, & Buckhout, 2013). With favorable returns in the upcoming future, banks are

10

mending troubled lodging assets which enable fewer loan sales and adjustments. Likewise, quality hotel

properties are not being put on the market for sale which is driving prices higher with intense bidding wars

(PKF Consulting USA, LLC, 2013). On a final positive note, numerous consulting firms expect hotel

RevPARs to be in the upper single digits with rising occupancies, along with newer markets to develop in

2014 (Jones Lang LaSalle, 2013; PKF Consulting USA, LLC, 2013; Roth & Fishbin, 2013; Rushmore Jr.,

Kuehnle, & Buckhout, 2013; Smith Mai & Morton, 2013).

Finally, the US market and economic outlook appear favorable for the hotel industry due to the overall

ease of financing, but as the economy further recovers, the Federal Reserve may decide to normalize

interest rates and reduce heavy bond purchases (OECD, 2013). How will the aforementioned affect the

US hotel market? (See Appendix G: Average Cap Rates for US Hotel Properties and Appendix H:

Reported Internal Rates of Return (by market) for specific numerical information))

4. Risk and Return Analysis

Most reports on real estate associate returns with meaningless numbers to an uneducated investor while

the academics use complex equations and theory to justify the application to different investing scenarios.

Reports are generally looking at trends in the market while academics are using history. There is no

correct analysis for real estate investment, although popular and accurate methods revolve around DCF

and payback period methods. Risk on the other hand is something that needs to be looked at since each

investment will incur a variety of external factors that need to be considered in conjunction with DCF

analysis. In regards to the US market, low interest rates, cap rates, and increasing IRRs are behind the

likes of a favorable market. There is intense competition to buy quality properties due to high leverage

and cheap debt. However, despite the outlook looking favorable in the short while, supply and other

economic factors may start to impact certain markets (Mellen, Hotel Capitlaization Rates And The Impact

Of CAP EX, 2014; Mellen, The Hotel Industry Outlook − U.S. Hotel Transactions, 2014). With increased

risk from external weather factors, construction can take longer than expected and potentially cause delays

in expected future cash flows. Since most investor reports usually do not take into account external risk

factors, investors are limited to their own common sense in evaluating these effects.

11

II. Conclusions and Recommendations The US hospitality market is on the up and up with popularity stemming from quality properties and

select service/extended stay in secondary markets. Key markets to focus on according to HVS are

convention center cities like San Francisco, New Orleans, Miami, Las Vegas, and New York. Also,

smaller emerging markets like West Palm Beach/Boca Raton, Jacksonville, Tampa, Tucson, Phoenix, and

Richmond are increasing in valuation and popularity for hotel investors (Rushmore Jr., Kuehnle, &

Buckhout, 2013). Debt is currently cheap, capitalization rates are low, and IRR has gone up. Private

equity seems to be popular raising capital through highly leveraged CMBS. In other words, the returns,

especially for quality properties are high relative to the risk. Although, I believe certain smaller markets

utilizing franchise agreements and select service properties, should be cautious. As hotels look to cater to

Gen X and Gen Y, branded hotels hurt by the recession may get left behind when it comes to upgrading

customized amenities and technological services. Smaller markets as mentioned should be weary of

excess supply and low RevPARs.

Hence, I recommend for investors to continue investing optimistically. However, I would start to diverge

from franchised/branded, select service/extended stay markets into quality properties in convention cities

and markets increasing in valuation. On a side note, investors should be mindful of the size of the pie and

should evaluate projects beyond the financial analysis for calculating returns. Investors should utilize

external analysis such as SWOT, PESTEL, and Industry Analysis in conjunction with DCF, IRR, and cap

rates to evaluate the opportunities for slices of the pie (in which may not be reported in real estate

sentiments). Finally, as interest rates possibly rise, although not anytime soon, investors should consider

utilizing REITs as a primary source for investing in hotel projects. REITs can offer higher liquidity and

comparatively less risk amongst other positive factors during times of expensive debt. (see Appendix I:

PESTEL Analysis and Food for Thought to have an overall picture of the current hotel market as well as

consideration that should be made for the future.)

12

III. Appendices A through I

Appendix A: Other US Hospitality Trends

Other Trends Positives Negatives

AIR (All-inclusive resorts) 1. New “hybrid” resorts can cater to multiple market segments due to new technologies

2. Have better overall stigma (Roth & Fishbin, 2013).

3. Potential future demand and positive oper. performance (Jones Lang LaSalle, 2013, p. 12).

1. Inabilities to upsell guests and generate alt. revenues (Roth & Fishbin, 2013).

2. Investments on decline (Jones Lang LaSalle, 2013, p. 12)

Serviced Apartments, Hostels, Portable and Transit Hotels

Offer guests cheaper lodging with more social and communal philosophies (Roth & Fishbin, 2013).

Have only taken in off in larger markets, have high barriers to entry, may only be a fad, difficult to brand (Roth & Fishbin, 2013).

Appendix B: Sales Comparison by Price/Room with Assets > $10 Million

(Mellen, The Hotel Industry Outlook − U.S. Hotel Transactions, 2014)(Source Taken Directly from HVS

and Real Capital Analytics (RCA))

13

Appendix C: Hotel Management 2013 Franchise Percentages

Property Type Percentage* Midscale 32.9 %

Economy 23.5 % Upscale 14.1 %

Upper Midscale 11.8 % Upper Upscale 11.8 %

Luxury 4.7 % Source: Hotel Management 2013 Franchise Fees survey

(Ricca, 2013)

*Percentage based on rooms franchised in respective property type

Appendix D: HVS Recommended Valuation Approaches

(deRoos & Rushmore, 2003)

•Determined by the net return or the “present worth of future benefits.”

• Future benefits are forecasted revenues and expenses along with a proposed resale value.

• Market value is calculated by converting benefits via capitalization and discounted cash flows.

Income Valuation

• Not as reliable as income valuation.

• Create indication of pricing momentum through comparing values of previous sales.

Sale Comparison

•Solid valuation procedure on whether to buy or build new properties

•Does not accurately calculate lost value in older buildings

•Does account income and ROI - hence, not primary valuation method

Cost

14

Appendix E: Specific HVS Risk Factor with Andrew’s Examples

HVS Risk Factors Examples

Property Management Under staffing, management neglect, poor budgeting and cost controls

Excess Supply Too many properties in region, too many competitors

Low Demand Bad property reputation, low occupancy, too many choices, high buyer power

Brand Recognition Boutique properties vs. brands, recognizing brands from competitor brands

Risk Leveraging Operations Property bubble burst, Issuing too much debt, Increased interest rates

Natural Disasters Hurricane Katrina on New Orleans, Hurricane Sandy on Atlantic City and New York, No snowfall for ski resorts

Economics Affects from natural disaster, rising interest rates, high capitalization rates, economic contractions, bubble bursts

(Rushmore Jr., Kuehnle, & Buckhout, 2013, pp. 37-39)

Appendix F: Aon Risk Solutions’ Investor Survey Rankings

Ranking Risk Factor

First Economic Slowdown Second Legislation Change

Third Increasing Competition Fourth Damage to Reputation/Brand

Fifth Failure to Attract/Retain Top Talent Sixth Failure to Innovate/Meet Customer Needs

Seventh Business Interruption Eighth Commodity Price Risk

Ninth Liquidity/Cash Flow Risk Tenth Political Uncertainty/Risk

(Aon Risk Solutions, 2013)

Appendix G: Average Cap Rates for US Hotel Properties

Year/Property Type Full Service & Luxury Select Service &

Extended Stay

Limited Service

2013 6.2% 7.4% 9.2%

2012 5.8% 7.4% 9.3%

2011 6.1% 7.7% 9.5% (Mellen, Hotel Capitlaization Rates And The Impact Of CAP EX, 2014)

15

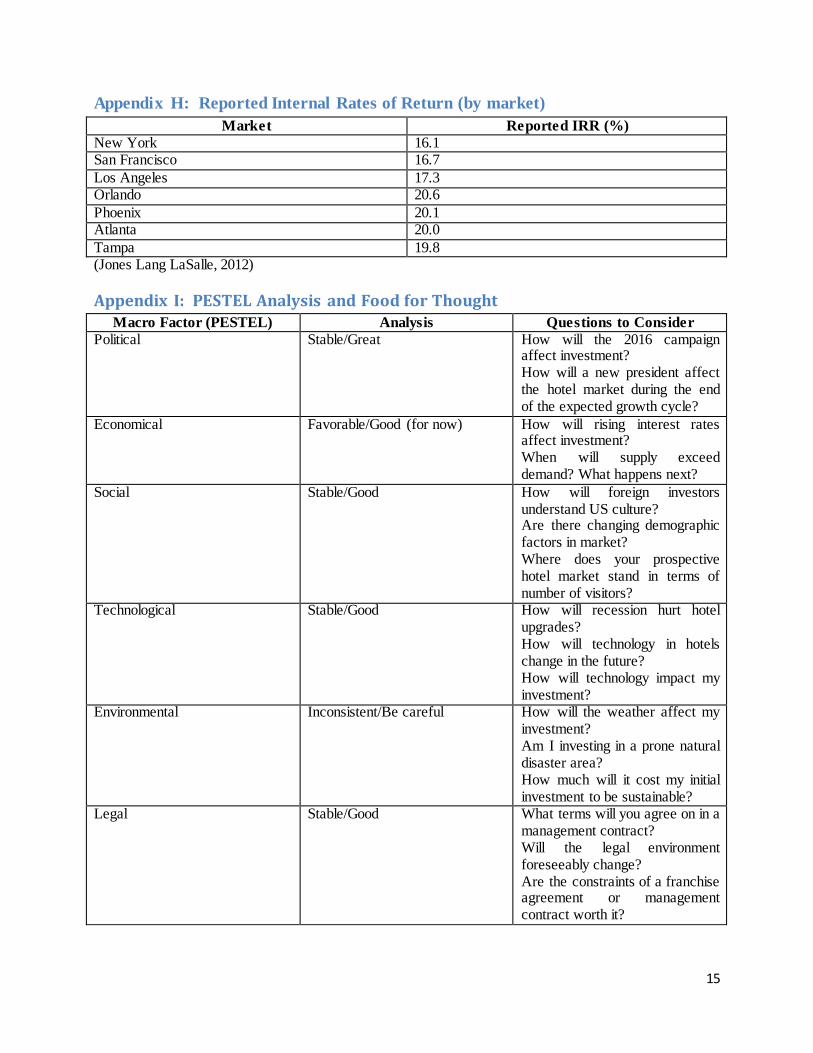

Appendix H: Reported Internal Rates of Return (by market)

Market Reported IRR (%)

New York 16.1 San Francisco 16.7

Los Angeles 17.3 Orlando 20.6

Phoenix 20.1 Atlanta 20.0

Tampa 19.8 (Jones Lang LaSalle, 2012)

Appendix I: PESTEL Analysis and Food for Thought Macro Factor (PESTEL) Analysis Questions to Consider

Political Stable/Great How will the 2016 campaign affect investment? How will a new president affect the hotel market during the end of the expected growth cycle?

Economical Favorable/Good (for now) How will rising interest rates affect investment? When will supply exceed demand? What happens next?

Social Stable/Good How will foreign investors understand US culture? Are there changing demographic factors in market? Where does your prospective hotel market stand in terms of number of visitors?

Technological Stable/Good How will recession hurt hotel upgrades? How will technology in hotels change in the future? How will technology impact my investment?

Environmental Inconsistent/Be careful How will the weather affect my investment? Am I investing in a prone natural disaster area? How much will it cost my initial investment to be sustainable?

Legal Stable/Good What terms will you agree on in a management contract? Will the legal environment foreseeably change? Are the constraints of a franchise agreement or management contract worth it?

16

Works Cited Aon Risk Solutions. (2013). Global Risk Management Survey. Retrieved from aon.com:

http://www.aon.com/2013GlobalRisk/2013-Global-Risk-Management-Survey-updated-05-01-

2013.pdf

Butler, J. (2014, January 20). Hotel Industry Outlook: Jim Butler's Top 10 for 2014. Retrieved from

hotelnewsresource.com: http://www.hotelnewsresource.com/article75938.html

Colliers International. (2014). 2014 Global Investment Sentiment. Colliers International. Retrieved from

http://viewer.zmags.com/publication/70cb18a6#/70cb18a6/38

deRoos, J., & Rushmore, S. (2003). Hotel Valulation Techniques. HVS International Journal. Retrieved

from http://www.hvs.com/Bookstore/HotelValuationTechniques.pdf

Farragher, E. J., & Savage, A. (2008). An Investigation of Real Estate Investment Decision-Making

Practices . Journal of Real Estate Practice and Education, 29-39.

Freed, J. Q. (2014, January 8). Investors shift focus to secondary markets. Retrieved from Hotel News

Now: http://www.hotelnewsnow.com/Article/12914/Investors-shift-focus-to-secondary-markets

Gasparini, G. (2011, October). Understanding Hotel Valuation Techniques. Retrieved from

tourism.blogs.ie.edu :

http://tourism.blogs.ie.edu/files/2011/10/IE_Hotel_Valuation_Techniques_October_2011.pdf

Investopedia US. (2014). Commercial Mortgage-Backed Securities (CMBS). Retrieved from

investopedia.com: http://www.investopedia.com/terms/c/cmbs.asp

Investopedia US. (2014). Real Estate Investment Trust - REIT. Retrieved from investopedia.com:

http://www.investopedia.com/terms/r/reit.asp

Jones Lang LaSalle. (2012). Hotel Investor Sentiment Survey. Jones Lang LaSalle IP.

Jones Lang LaSalle. (2013). Hotel Invesment Outlook. Jones Lang LaSalle IP, INC. Retrieved from

http://www.joneslanglasalle.com/ResearchLevel1/JLL_Hotel_Investment_Outlook_2013_1.pdf

Lee, S. L. (2001). The Risks of Investing in the Real Estate Markets of the Asian Region. The University of

Reading, Department of Land Management. Reading: Whiteknights.

Marrs, N. M., & Tomlinson, S. G. (2006). Deficiencies of IRRs and TWRs as Measures of Real Estate

Investment and Manager Performance. Real Estate Finance Journal.

Mellen, S. (2014). Hotel Capitlaization Rates And The Impact Of CAP EX. HVS.

Mellen, S. (2014). The Hotel Industry Outlook − U.S. Hotel Transactions. HVS.

OECD. (2013, November ). United States - Economic forecast summary (November 2013). Retrieved from

oecd.org: http://www.oecd.org/eco/outlook/unitedstateseconomicforecastsummary.htm

17

Pike, R., Neale, B., & Linsley, P. (2012). Corporate Finance and Investment Decisions and Strategy (7th

ed.). London: Pearson.

PKF Consulting USA, LLC. (2013, June 20). PKF Survey Finds Optimism In U.S. Hotel Investments. Retrieved

from hospitalitynet.org: http://www.hospitalitynet.org/news/4061199.html

PwC and the Urban Land Institute . (2012). Emerging Trends in Real Estate 2013. Washington D.C.: PwC

and the Urban Land Institute .

Ricca, S. (2013, June 3). Fee survey reflects growth in midscale franchising. Retrieved from

hotelmanagement.net: http://www.hotelmanagement.net/legal-matters/fee-survey-reflects-

growth-in-midscale-franchising-20743

Roth, H., & Fishbin, M. (2013). Global Hospitlaity Insight: Top thought for 2014. EYGM Limited.

Rushmore Jr., S., Kuehnle, K., & Buckhout, C. (2013). 2013 HVS-STR U.S. Hotel Valuation Index. Mineola :

HVS Global Hospitality Services.

SEC. (2010, July 23). Mortgage-Backed Securities. Retrieved from sec.gov:

https://www.sec.gov/answers/mortgagesecurities.htm

SEC. (2012, January 17). Real Estate Investment Trusts (REITs). Retrieved from sec.gov:

http://www.sec.gov/answers/reits.htm

Smith Mai, S., & Morton, B. (2013, September 19). 2013 Hospitality Investment Survey - Are We There

Yet? Retrieved from hospitalitynet.org: http://www.hospitalitynet.org/news/4062227.html

Thompson, P. (2005). AN INTRODUCTION TO REAL ESTATE INVESTMENT ANALYSIS: A TOOL KIT

REFERENCE FOR PRIVATE INVESTORS. Retrieved from thompsonlaw.ca:

http://www.thompsonlaw.ca/pdf_folder/RE_Inv_intro.pdf

UBS. (2014). US Real Estate Market Outlook 2014. Hartford: UBS Realty Investors LLC. Retrieved from

http://www.ubs.com/global/en/asset_management/gre/_jcr_content/rightpar/teaser/linklist/lin

k.783114550.file/bGluay9wYXRoPS9jb250ZW50L2RhbS91YnMvZ2xvYmFsL2Fzc2V0X21hbmFnZW

1lbnQvZ3JlL3VzL2dyZXItdXMtMjAxNC1vdXRsb29rLnBkZg==/grer-us-2014-outlook.pdf

Younes, E., & Kett, R. (2006). Hotel Investment Risk: What are the Chances? London: HVS.

Zacks Equity Research. (2013, April 9). Hotels & Lodging Stock Outlook - April 2013. Retrieved from

zacks.com: http://www.zacks.com/commentary/26697/hotels-lodging-stock-outlook---april-

2013