rba chart pack (8 may 2013)

TRANSCRIPT

The Australian Economy andFinancial MarketsChart Pack May 2013

Contents

GraphsWorld Economy 1–3Australian GDP Growth and Inflation 4Household Sector 5–6Business Sector 7–8Credit and Money 9Factors of Production and Labour Market 10–11Regions and Industry 12–13Government 14Commodity Prices 15Balance of Payments and External Position 16–17Interest Rates 18–22Share Markets 23–24Bond Issuance 25Equity Raisings and Business Financing 26Exchange Rates 27–28Banking Indicators 29–30

The Australian Economy and Financial Markets

CHARt PACk | MAy 2013 1

-4

-2

0

2

4

6

-4

-2

0

2

4

6

GDP Growth – WorldYear-ended

% %

Major trading partners*

World**

* Weighted using Australian export shares** PPP-weighted; accounts for 87 per cent of world GDPSources: ABS; CEIC; IMF; RBA; Thomson Reuters

2012200620032000 20090

5

10

0

5

10

2013

GDP Growth – China and IndiaYear-ended

India

China

% %

2010200720042001Sources: CEIC; RBA

-12

-8

-4

0

4

-12

-8

-4

0

4

GDP Growth – Advanced EconomiesYear-ended

Source: Thomson Reuters2013

Euro area

% %

US

Japan

200720042001 2010-10

-5

0

5

10

-10

-5

0

5

10

GDP Growth – East AsiaYear-ended

% %

ASEAN-4*

Higher-income Asian economies**

* Indonesia, Malaysia, Philippines and Thailand; PPP-weighted** Hong Kong, Singapore, South Korea and Taiwan; PPP-weightedSources: CEIC; IMF; RBA

2012200620032000 2009

World Economy

CHARt PACk | MAy 2013 2

-4

0

4

8

-4

0

4

8

2013

Inflation – East AsiaYear-ended

% %

201020072004* Indonesia, Malaysia, Philippines and Thailand; PPP-weighted** Hong Kong, Singapore, South Korea and Taiwan; PPP-weightedSources: CEIC; IMF; RBA; Thomson Reuters

ASEAN-4*

Higher-income Asianeconomies**

2001

2

6

10

2

6

10

Unemployment Rate – Advanced Economies

Source: Thomson Reuters

Euro area

%

US

Japan

%

20132010200720042001

-2

-1

0

1

2

-2

-1

0

1

2

Core Inflation* – Advanced EconomiesYear-ended

US**

Euro area

Japan

%%

* Excluding food and energy, and for the euro area also excluding alcoholand tobacco

** Core price index for personal consumption expendituresSource: Thomson Reuters

20132010200720042001-4

0

4

8

-4

0

4

8

Inflation – China and IndiaYear-ended

* Consumer price index** Wholesale price indexSources: CEIC; RBA

2013

India**

%

China*

%

2010200720042001

World Economy

CHARt PACk | MAy 2013 3

China – Monthly Activity Indicators*Nominal growth

2011

0

3

0

3

-3

0

3

-3

0

3

%Retail sales%

20092007

%%

* RBA estimates prior to February 2011Sources: CEIC; RBA

Fixed asset investment

2013

90

100

110

120

130

Index

35

50

65

80

95

Prices2006 average = 100

Floor space sold

China – Residential Property Market*

M(m2)

2013200920132009* RBA estimatesSources: CEIC; RBA

10

20

30

10

20

30

China – Credit and Money Supply GrowthYear-ended

Source: CEIC

Credit

%%

201120092007

M2 money supply

2013

China – Output IndicatorsLog scale; 2005 average = 100

Industrial production

Index

Sources: CEIC; RBA

5050

100100

200200

Index

Crude steel

Rail freight

Electricityconsumption

20132009201320092005 2005

World Economy

CHARt PACk | MAy 2013 4

Australian GDP Growth and Inflation

-2

0

2

4

-2

0

2

4

Year-ended

2012

%%

Quarterly

GDP Growth

2008Source: ABS

1996 20042000-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

Consumer Price Inflation*

2013

%%

Year-ended

* Excluding interest charges prior to the September quarter 1998 andadjusted for the tax changes of 1999–2000

Sources: ABS; RBA

Quarterly (seasonally adjusted)

20092005200119971993

Underlying Inflation*

%

0

1

2

3

4

5

0

1

2

3

4

5

2013

Weighted median

Trimmed mean

* Excluding interest charges prior to the September quarter 1998 andadjusted for the tax changes of 1999–2000

Sources: ABS; RBA

CPI excl volatile items

%

20092005200119971993

Non-tradables and Tradables Inflation

-2

0

2

4

-2

0

2

4

2013

%

Year-ended

Non-tradables* Tradables**%

* Excluding deposit & loan facilities to June 2011** Excluding volatile items (fruit, vegetables & automotive fuel) and tobaccoSources: ABS; RBA

Quarterly(seasonally adjusted)

200920092005 2013 2005

CHARt PACk | MAy 2013 5

Household Sector

4

8

4

8

% %Retail Sales Growth

* Percentage change over year to latest three monthsSource: ABS

-5

0

-5

0

Volumes (quarterly)% %

20132010200720042001

Volumes(year-ended)

Values(year-ended*)

-5

0

5

10

15

-5

0

5

10

15

Household Saving Ratio*Per cent of household disposable income

* Net of depreciationSource: ABS

2012

%

2007200219921987

%

1997

0

5

10

15

0

5

10

15

Private Residential Building Approvals

Source: ABS2013

’000Total

’000

Higher-density housing

Detachedhouses

2008200319981993

Monthly

60

80

100

120

60

80

100

120

Consumer SentimentAverage since 1980 = 100

201320092005

Index Index

Source: Melbourne Institute and Westpac200119971993

CHARt PACk | MAy 2013 6

Household Sector

25

50

75

100

125

150

4

6

8

10

12

14

* Household sector excludes unincorporated enterprises; disposableincome is after tax and before the deduction of interest payments

Sources: ABS; RBA

201220021992

% %Debt Interest paid

20122002

Household Finances*Per cent of household disposable income

19920

150

300

450

600

0

150

300

450

600

%%

* Household liabilities exclude the liabilities of unincorporated enterprises;disposable income is after tax and before the deduction of interest payments

Sources: ABS; RBA; RP Data-Rismark

20122008200420001996

Liabilities

Net worth

Dwellings

Financial assets

Household Wealth and Liabilities*Per cent of annual household disposable income

Dwelling Prices

200

300

400

500

600

200

300

400

500

600

Brisbane

Sydney

Perth

MelbourneAdelaide

Canberra

Regional*

2013

Australia

2009 20132009* Excluding apartments; measured as areas outside of capital cities in

mainland statesSources: RBA; RP Data-Rismark

$’000$’000

0

5

10

15

20

0

5

10

15

20

$b$b

Sources: ABS; RBA20132011200920072003

Total

Non-first home buyerowner-occupiers

First home buyers

Investors

Housing Loan Approvals

2005

CHARt PACk | MAy 2013 7

Business Sector

0

4

8

12

0

4

8

12

2012

%

Private Non-financial Corporation Profits*Share of nominal GDP

%

Mining

2008* Gross operating profits; inventory valuation adjustedSources: ABS; RBA

Non-mining

20042000

-30

-15

0

15

-30

-15

0

15

72

75

78

81

84

72

75

78

81

84

-30

-15

0

15

-30

-15

0

15

NAB Business Survey

* Net balance; deviation from average since 1989Sources: NAB; RBA

pptBusiness conditions*

Business confidence*

Capacity utilisation

20132008200319981993

ppt

%

ppt

ppt

%

30

40

50

60

9

12

15

18

% %Business Finances

Business creditPer cent of nominal GDP

Interest paid*Per cent of profits**

* Interest on intermediated debt from Australian-domiciled financialinstitutions

** Profits are private non-financial gross operating surplus (adjusted forprivatisations) and gross mixed income

Sources: ABS; RBA

2012200720022012200720021997

CHARt PACk | MAy 2013 8

Business Sector

Business Investment*

10

12

14

16

18

10

12

14

16

18

Share of nominal GDP

2002

%%

2012* Excludes second-hand asset transfers between the private and other

sectors; no adjustments have been made for privatisationsSource: ABS

20071992 1997

Capital Expenditure – Mining and Non-mining*Nominal, financial year, log scale

* Sample of firms’ spending plans; dots represent the survey’s most recentestimates for 2012/13 adjusted for historical realised spending

Sources: ABS; RBA

2013

$b Mining $bNon-mining

20031993

4

8

16

32

64

2

4

8

16

32

64

2201320031993

128 128

0

2

4

6

8

0

2

4

6

8

Business Investment Components*Share of nominal GDP

Buildings

%%

Machinery and equipment

20122007200219971992* Excludes second-hand asset transfers between the private and other

sectors; no adjustments have been made for privatisationsSource: ABS

Engineering

0

1

2

3

0

1

2

3

Private Non-residential Building ApprovalsPer cent of nominal GDP

Source: ABS2013

%%

20082003199819931988

CHARt PACk | MAy 2013 9

Credit and Money

0

5

10

15

0

5

10

15

% %

Credit

Broad money

Source: RBA

Credit and Broad Money GrowthYear-ended

20132005 2009200119970.5

0.8

1.1

1.4

0.5

0.8

1.1

1.4

Credit*Ratio to nominal GDP

Ratio Ratio

* Not adjusted for breaksSources: ABS; RBA

20132003 200819981993

Monetary Aggregates GrowthYear-ended

% %

M3

0

6

12

18

0

6

12

18

Currency

Source: RBA20132005 200920011997

-10

0

10

20

-10

0

10

20

Credit Growth by SectorYear-ended

Business

Housing

Personal

% %

Source: RBA20132005 200920011997

CHARt PACk | MAy 2013 10

Factors of Production and Labour Market

Year-ended changeLabour Productivity

Source: ABS

2012

Output

%

-4

0

4

8

-4

0

4

8

-8

-4

0

4

-8

-4

0

4

Total hours worked

Output per hour worked

200720021997199219871982

%

%%

Annual growthFactors of Production

* Excluding livestock & orchards, dwellings and ownership transfer costsSources: ABS; RBA

11/12

%Capital stock*

3

5

3

5

1.0

1.5

2.0

1.0

1.5

2.0

05/0699/00

Working-age population

%

%%

93/9487/8881/82

-4

-2

0

2

4

-4

-2

0

2

4

Growth in Labour Input

Year-ended, trend

Source: ABS2013

Employment

%%Total hours worked

2009200520011997199380

100

120

140

160

180

80

100

120

140

160

180

Capital Ratios*

1979/80 = 100

* Capital stock excludes livestock & orchards, dwellings and ownershiptransfer costs

Sources: ABS; RBA

11/12

Capital-labour ratio

IndexIndex

Capital-output ratio

06/0701/0296/9791/9286/8781/82

CHARt PACk | MAy 2013 11

Factors of Production and Labour Market

Unemployment and Participation Rates

62

63

64

65

66

3

5

7

9

11

% %

2013200920052001Source: ABS

Participation rate(RHS)

Unemployment rate(LHS)

19971993

Full-time and Part-time Employment

5.5

6.0

6.5

7.0

7.5

8.0

1.5

2.0

2.5

3.0

3.5

4.0

5.5

6.0

6.5

7.0

7.5

8.0

1.5

2.0

2.5

3.0

3.5

4.0

M M

2013Source: ABS

Full-time(LHS)

Part-time(RHS)

20092005200119971993

0

1

2

3

4

5

0

1

2

3

4

5

Source: ABS

2012

%%

201220072002

Wage Price Index Growth

Private sector

Year-ended

Quarterly

Public sector

20072002 0.5

1.0

1.5

2.0

0.5

1.0

1.5

2.0

Job Vacancies and AdvertisementsPer cent of labour force

* This survey was suspended between May 2008 and November 2009Sources: ABS; ANZ

2013

Vacancies*(ABS survey)

% %Advertisements

(ANZ survey)

2010200720042001

CHARt PACk | MAy 2013 12

Regions and Industry

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

State Share of Output*

* NominalSource: ABS

11/12

New South Wales%

Victoria

Queensland

Western Australia

South Australia

Tasmania

03/04 07/0899/0095/9691/92

%

-5

0

5

10

-5

0

5

10

-10

-5

0

5

10

15

-10

-5

0

5

10

15

-5

0

5

10

15

-5

0

5

10

15

New South Wales

Victoria

State Final Demand Growth

Year-ended

Western Australia

Queensland

Tasmania*South Australia

% %

201220082004200019961992* Adjusted for the purchase and sale of ferries in 2002Sources: ABS; RBA

% %

% %

State Unemployment Rates

Trend

2

3

4

5

6

7

2

3

4

5

6

7

Source: ABS2013

New South Wales

% %

2009 20132009

Queensland

Victoria

Tasmania

Western Australia

South Australia

2005

CHARt PACk | MAy 2013 13

Regions and Industry

2

4

6

8

10

12

14

2

4

6

8

10

12

14

11/12

%Industry Share of Output*

Manufacturing

Retail and wholesale trade

Construction

Mining

Other business services**

07/0803/0499/0095/96* Nominal gross value added** Includes: information media and telecommunications; rental, hiring and real

estate services; professional scientific and technical services;administrative and support services

Source: ABS

%

91/92

Agriculture

Financial and insuranceservices

0

10

20

30

40

0

10

20

30

40

Industry Share of Business Investment*

Manufacturing

%

Other businessservices**

Agriculture

Mining

Retail andwholesale trade

Construction

11/1207/0803/0499/0095/9691/92* Nominal** Includes: information media and telecommunications; rental, hiring and real

estate services; professional scientific and technical services;administrative and support services

Source: ABS

%

Financial andinsurance services

50

100

150

200

250

300

350

50

100

150

200

250

300

350

2008 201320032008 20132003

Other businessservices** (14.9%)

Retail and wholesale trade (14.5%)

Mining (2.3%)

Manufacturing (8.1%)

Construction (8.8%)

Financial andinsurance services

(3.5%)

* Figures in parentheses represent share of total employment based onlatest quarterly data

** Includes: information media and telecommunications; rental, hiring andreal estate services; professional, scientific and technical services;administrative and support services

Source: ABS

Employment by Industry*2000 average = 100

IndexIndex

1998-60 -40 -20 0 20 40 60

Contributions to Employment GrowthYear to February 2013, trend

Source: ABS’000

Health care & social assistance

Mining

Public administration & safety

Professional, scientific & technical

Financial & insuranceOther services

Wholesale trade

Rental, hiring & real estateUtilities

Information & telecommunications

Arts & recreation

Administrative & support

Education & training

Agriculture, forestry & fishing

Construction

Transport, postal & warehousing

Manufacturing

Retail trade

Accommodation & food services

CHARt PACk | MAy 2013 14

Government

-5

-4

-3

-2

-1

0

1

2

-5

-4

-3

-2

-1

0

1

2

%%

Australian Government Budget Balance*

Per cent of nominal GDP

* Underlying cash balanceSource: Australian Treasury

15/1609/1003/0497/9891/9285/86-1.2

-0.8

-0.4

0.0

0.4

0.8

-1.2

-0.8

-0.4

0.0

0.4

0.8

State Budget Balances*Per cent of nominal GDP

%%

* Underlying cash balanceSource: ABS

11/1206/0701/0291/9286/87 96/9781/82

0

1

2

3

0

1

2

3

Public Construction Work DonePer cent of nominal GDP

Source: ABS

2012

Total

%

Engineering

Building

%

20082004200019961992 -10

0

10

20

30

-10

0

10

20

30

11/1207/0803/04

Non-financial Public Sector Net Debt*Per cent of nominal GDP

% %Non-financial public sector

Australian Government

State and local general governments

* Estimates as at the 2012/13 MYEFOSource: Australian Treasury

99/0095/9691/92

CHARt PACk | MAy 2013 15

Commodity Prices

20

40

60

80

100

20

40

60

80

100

20

40

60

80

100

20

40

60

80

100

RBA Index of Commodity Prices

SDR, 2011/12 average = 100Index Index

20132008200319981993Source: RBA

1988

Base Metals, Rural and Oil PricesWeekly

l l l l l l l I70

100

130

160

190

220

l l l l l l l I 25

50

75

100

125

150

* RBA Index of Commodity Prices sub-indices; SDR terms;2005 average = 100

Sources: Bloomberg; RBA

Index US$/b

Base metals*

Brent oil

2009

Rural*

2013 2009 20132005

l l I 50

150

250

350

l l I50

90

130

170

Bulk Commodity PricesFree on board basis

* Iron ore fines, Newcastle thermal coal and premium hard coking coalSources: ABS; Bloomberg; Citigroup; Energy Publishing; globalCOAL;

Macquarie Bank; RBA

2013

Spot price*

Iron ore(LHS)

Thermal coal(LHS)

Coking coal(RHS)

Average Australianexport price

20132013 201120112011

US$/tUS$/t

l l I 20

40

60

80

100

20

40

60

80

100

Terms of Trade*

2010/11 average = 100Index Index

2012* Annual data are used prior to 1960Sources: ABS; RBA

1997198219671952

CHARt PACk | MAy 2013 16

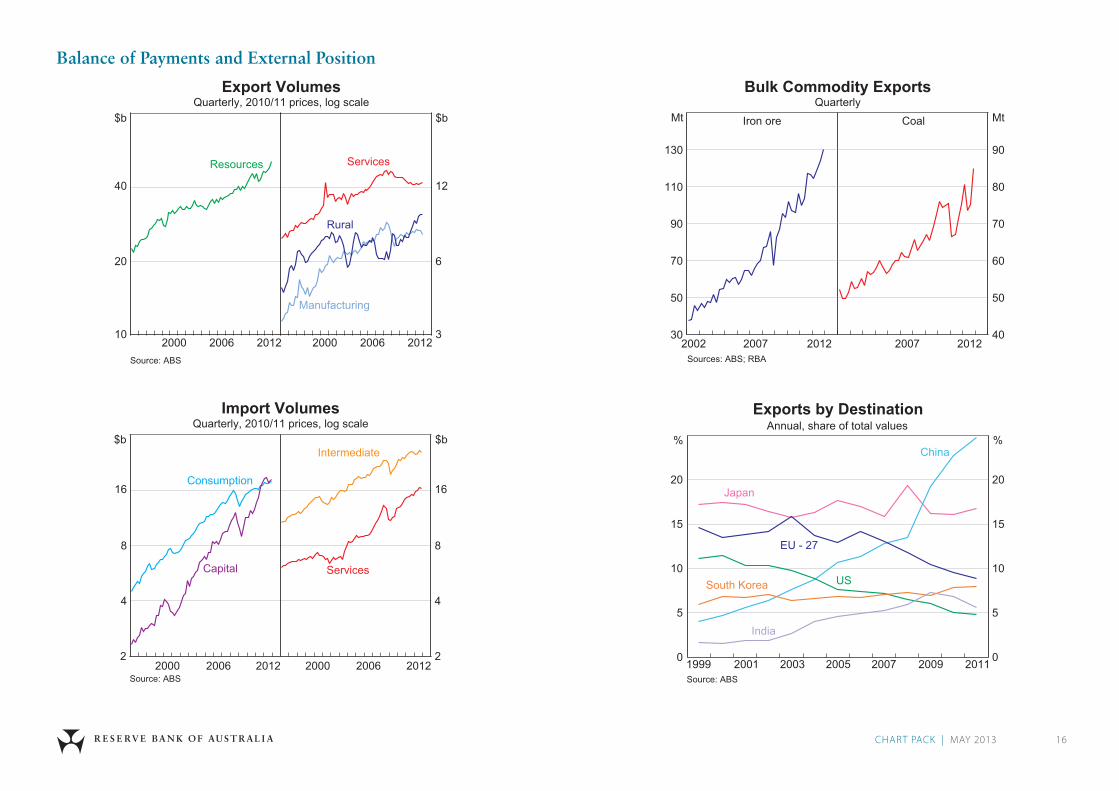

Balance of Payments and External Position

Export VolumesQuarterly, 2010/11 prices, log scale

Source: ABS

$b $b

20122006

20

Resources

Rural

Services

Manufacturing

200020122006200010

40

6

3

12

30

50

70

90

110

130

Bulk Commodity ExportsQuarterly

40

50

60

70

80

90

Sources: ABS; RBA2012

Mt Iron ore MtCoal

20072002 20122007

Import VolumesQuarterly, 2010/11 prices, log scale

Source: ABS

$b $b

20122006

4

8

16

2 2

4

8

16Consumption

Capital Services

Intermediate

20002012200620000

5

10

15

20

0

5

10

15

20

Exports by Destination

Annual, share of total values

Source: ABS2011

% %

200920072003

Japan

EU - 27

US

China

South Korea

India

2001 20051999

CHARt PACk | MAy 2013 17

Balance of Payments and External Position

-9

-6

-3

0

-9

-6

-3

0

Current Account BalancePer cent of nominal GDP

Net incomebalance

Current account balance

Trade balance

% %

Source: ABS20132008200319981993

-4

-2

0

2

4

6

8

-4

-2

0

2

4

6

8

% %

Debt

Equity

20122009Source: ABS

2006

Net Capital InflowPer cent of nominal GDP

20032000

* 2012 values for GDP and net capital flows are year to SeptemberquarterSource: ABS

Net Foreign LiabilitiesPer cent of nominal GDP

0

15

30

45

60

0

15

30

45

60

% %

Total

Debt

Equity

Source: ABS20132008200319981993

l l l l l l l l l l 0

500

External PositionComposition after hedging, quarterly*

Gross foreign assets

n Foreign currencyn Australian dollar

$bGross foreign liabilities$b

1 000

1 500

1 000

1 500

* Hedge ratios inferred from the Foreign Currency Exposure surveySources: ABS; RBA

2 0002 000

l l l l l l l l l l0

500

2012 20082004 201220082004

CHARt PACk | MAy 2013 18

Policy Interest Rates – Selected

Advanced Economies

SwitzerlandSweden

Canada

UK

% %

0

2

4

6

8

0

2

4

6

8NZ

Source: central banks2007 2009 2011 20132005

-3

0

3

6

9

-3

0

3

6

9

Australian Cash Rate

Real cash rate*

2003

Cash rate

% %

201320081998

Sources: ABS; RBA* Calculated using average of weighted median and trimmed mean inflation1993

Policy Interest Rates – G3

US

Euro area

% %

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

Japan*

2005 2007 2009 20132011* Since April 2013, the Bank of Japan's main operating target has been

the money baseSource: central banks

l l l l l l l l l2

3

4

5

6

7

8

2

3

4

5

6

7

8

Australian Cash Rate and 90-day Bill Yield%

Cash rate

90-day bill yield

Sources: AFMAData; RBA

2005

%

2007 2009 20132011

Interest Rates

CHARt PACk | MAy 2013 19

%

0

1

2

3

4

5

6

0

1

2

3

4

5

6US

%

Germany

Japan

2013

10-year Government Bond Yields

Source: Thomson Reuters2010200720042001

0

5

10

15

20

0

5

10

15

20

% %

South Africa

Mexico

Brazil

Russia

Policy Interest Rates – Emerging Markets

Source: central banks2013

Poland

2009 201120072005

%

Indonesia

Policy Interest Rates – Asia

Malaysia

China*

0

1

2

3

4

5

%South Korea

Taiwan

Thailand

* 1-year lending rateSource: central banks

201320090

3

6

9

12

15

India

2005201320092005Source: RBA

2

3

4

5

6

7

2

3

4

5

6

7

% %

20102001

10-year Australian Government Bond Yield

20072004 2013

Interest Rates

CHARt PACk | MAy 2013 20

0

3

6

9

0

3

6

9

%

AAA corporates*

US government

%

BBB corporates*

* Includes financials and non-financialsSources: Bank of America Merrill Lynch; Bloomberg

Swap

US Bond Yields

2005 2009 20132001

3–5 years

1997

0

200

400

600

800

0

200

400

600

800

US Bond Spreads

Bps

AAA corporates*

A corporates*

BBB corporates*

* Includes financials and non-financialsSources: Bank of America Merrill Lynch; Bloomberg

Swap

Bps

2005 2009 20132001

To US government bonds, 3–5 years

1997l l l l l l l l l l l l l l l l l l l l l l l-100

0

100

200

300

400

500

-100

0

100

200

300

400

500

Differential between Australian and US10-year Government Bond Yields

Bps

Sources: Bloomberg; RBA

Bps

1993 1997 2009 201320052001

Source: RBA

-6

-4

-2

0

2

4

-6

-4

-2

0

2

4

% %

Spread between Australian 10-year

Bond Yield and the Cash Rate

1993 1997 2009 201320052001

Interest Rates

CHARt PACk | MAy 2013 21

l l l l l l l l l l l l l l l2

4

6

8

2

4

6

8

Australian Bond Yields*%%

BBB corporates

* Australian Government yields and swap rates are for 3-year maturity.Corporate bond yields are a weighted average of senior bonds withremaining maturities of 1 to 5 years; they include financial and non-financial corporates.

Sources: Bloomberg; RBA; UBS AG, Australia Branch

AustralianGovernment

Swap

AA corporates

2001 2005 2009 2013

* Swap spreads are for 3-year maturity. Corporate bond spreads are aweighted average of senior bonds with remaining maturities of 1 to 5years; they include financial and non-financial corporates.

l l l l l l l l l l l l l l l0

100

200

300

400

500

0

100

200

300

400

500

Australian Bond Spreads*Spread over government yields

Bps

A corporates

Bps

BBB corporates

Swap

Sources: Bloomberg; RBA; UBS AG, Australia Branch

AA corporates

2001 2005 2009 20130

300

600

900

0

300

600

900

Bps

Emerging Market Bond Spreads

Latin America

Asia

Bps

Sources: Bloomberg; RBA; Thomson Reuters

1 500

1 200

1 500

1 200

2001 201320092005

Europe

1997

To US government bonds, duration matched

0

4

8

12

16

20

0

4

8

12

16

20

%Emerging Market Bond Yields

2001

Latin America

Asia

%

Sources: Bloomberg; RBA; Thomson Reuters201320092005

Europe

1997

Interest Rates

CHARt PACk | MAy 2013 22

1993 1998 2003 2008 20132

4

6

8

10

2

4

6

8

10

Australian Housing Lending Rates

Sources: ABS; APRA; Perpetual; RBA

Cash rate

%%

Banks’ indicator rate on new loans

Actual rate on outstanding loans

Average interest rate on variable-rate loans

1993 1998 2003 2008 20132

4

6

8

10

12

2

4

6

8

10

12

Australian Fixed Interest Rates

Sources: Bloomberg; RBA

Small business

%3-year maturity

%

Swap rate

Housing

2

4

6

8

10

12

2

4

6

8

10

12

Australian Small Business Interest Rates

* Indicator rates** Including risk marginsSources: APRA; RBA

Cash rate

%%Weighted-average outstanding

variable rate**

Term loanresidential security*

Overdraftother security*

1997 2001 2005 2009 20131993

Sources: APRA; RBA

6

8

10

6

8

10

2

4

6

8

2

4

6

8

% %

% %

Small business

Large business

Australian Business Lending Rates

20092005 20132001

Average interest rate on outstanding lending

1997

Interest Rates

CHARt PACk | MAy 2013 23

40

100

40

100

Major Economies’ Share Price Indices

Japan

US

UK

IndexIndexLog scale, end December 1994 = 100

Euro area300

200

300

200

Source: Bloomberg1997 20132005 20092001

80

100

80

100

Australian and World Share Price Indices

Log scale, end December 1994 = 100

Sources: Bloomberg; RBA; Thomson Reuters

S&P 500

Index Index

ASX 200

MSCI World

300

200

300

200

350

250

150

350

250

150

2005 2009 201320011997

60

100

60

100

Australian Share Price IndicesLog scale, end December 1994 = 100

Sources: Bloomberg; RBA; Thomson Reuters

Financials

Index Index

Resources

All other sectors

600500

400

300

200

600500

400

300

200

2005 2009 20132001199740

100

40

100

Emerging Asia

Index

Share Price Indices

Latin America

IndexLog scale, end December 1994 = 100

Sources: Bloomberg; MSCI20052001 2009 2013

1 000

1 500Emerging Europe

500500

1 500

1 000

China

World

1997

200 200

Share Markets

CHARt PACk | MAy 2013 24

0

2

4

6

0

2

4

6

%

Source: Thomson Reuters

%

MSCI Worldexcluding Australia

MSCI Australia

Dividend Yields

2001 2007 201319951989

50

70

90

50

70

90

Forecast Earnings per Share

Index

Source: Thomson Reuters

MSCI AustraliaIndex

06/07

07/08

09/10

11/12

08/09

10/11

05/06

12/13

13/14

20132011200920072005

0

10

20

0

10

20

Ratio

Source: Thomson Reuters

Ratio

MSCI World

MSCI Australia

Forward P/E Ratios

2001 2007 201319951989

0

10

20

30

0

10

20

30

Ratio

Source: Thomson Reuters

Ratio

MSCI Worldexcluding Australia

MSCI Australia

Trailing P/E Ratios

2001 2007 201319951989

Share Markets

CHARt PACk | MAy 2013 25

0

100

200

300

0

100

200

300

Non-government Bonds on Issue OffshoreAll currency denominations

* Australian dollar-denominated bonds onlySources: ABS; RBA

Financials

$b

Non-financialcorporates

Non-residents*

$b

201320092001 20051997

Asset-backed securities

1993

Gross issuanceNon-government Bond Issuance

* Excludes ADIs’ self-securitisations** Offshore non-resident issuance includes Australian dollar-denominated

bonds onlySource: RBA

$b Australia

20

40

20

40

$b

$b $bOffshore

2001 2004 2007 2010 20130

20

40

60

0

20

40

60

n Domestic issuers*n Non-resident issuers**

1993 1997 2001 2005 2009 20130

50

100

150

0

50

100

150

Non-government Bonds on Issue in Australia

* Excludes ADIs’ self-securitisationsSources: ABS; RBA

Financials

Asset-backed securities*

Non-residents

$b$b

Non-financial corporates

1993 1997 2001 2005 2009 20130

100

200

300

400

0

100

200

300

400

Bonds on Issue in Australia

$b

Australian Government*

Non-government**$b

State governments

* Excludes bonds purchased by the Australian Government** Excludes ADIs’ self-securitisations, includes government-guaranteed

bondsSources: ABS; RBA

Bond Issuance

CHARt PACk | MAy 2013 26

Net Non-intermediated Capital Raisings*

-25

0

25

50

$b$b Non-financial corporates

-25

0

25

50

Financials and asset-backed securities**

* Includes equity, hybrids, bonds, and short term-debt** Excludes ADIs’ self-securitisations; financials include banks and non-

bank financialsSources: APRA; ASX; Austraclear; RBA

20082003 2013 20082003 2013

$b

4

8

4

8

7

14

21

28

7

14

21

28

-5

0

-10

-5

0

$b

$b$b

$b$b

IPOs

Other raisings

Buybacks

-10

Australian Equity Raisings*

* All listed companiesSources: ASX; RBA

2010 20132004 20072001

-10

-5

0

5

10

15

-10

-5

0

5

10

15

Business External FundingNet change as a share of GDP

%%n Business creditn Non-intermediated debt

n Equity

Sources: ABS; APRA; ASX; RBA

2003 2008 20131993 1998

Total

-5

0

5

10

15

20

25

-5

0

5

10

15

20

25

$b$bn Financials**n Non-financial corporates

Australian Net Equity Raisings*

* All listed companies** Includes banks and non-bank financialsSources: ASX; RBA

2010 20132004 20072001

Equity Raisings and Business Financing

CHARt PACk | MAy 2013 27

20

40

60

80

20

40

60

80

-4

-2

0

2

4

-4

-2

0

2

4

-2

0

2

4

-2

0

2

4

Official Reserve Assets

* Excludes foreign exchange swaps** Includes market, government and other outright transactions, excludes

swap deliveries*** Data up to 29 June 2012; a positive value indicates a purchase of foreign

exchange, while a negative value indicates a sale of foreign exchangeSource: RBA

2013

Gross

A$b

RBA foreign exchange market intervention transactions***

A$b

A$bA$b

Net*

2009200520011997

RBA net purchases of foreign exchange**

A$bA$b

50

100

150

200

0.40

0.60

0.80

1.00

Yen per A$(LHS)

Euro per A$*(RHS)

Yen US$,Euro

* ECU per A$ until 31 December 1998Sources: Thomson Reuters; WM/Reuters

Australian Dollar against US Dollar,

Euro and Yen

20131998 2003 200819931988

US$ per A$(RHS)

40

50

60

70

80

40

50

60

70

80

Real

Nominal

IndexAustralian Dollar TWI*

Index

20131998 2003 200819931988* May 1970 = 100 for nominal; real indexed to equate post-float averagesSources: ABS; RBA; Thomson Reuters; WM/Reuters

Exchange Rates

CHARt PACk | MAy 2013 28

40

60

80

100

120

140

40

60

80

100

120

140

40

60

80

100

120

140

40

60

80

100

120

140

Selected Asian Currencies against the US Dollar

Indonesia

Index1 January 2000 = 100

Index

South Korea

MalaysiaThailand

Source: Bloomberg2004 2007

India

2010 2013

Singapore

2001

50

90

130

170

210

250

2.90

2.50

2.10

1.70

1.30

0.90

Yen US$

Yen per US$(LHS)

US$ per euro*(RHS, inverted scale)

1993 19981988 2013

US Dollar against Euro and Yen

2003 2008* US$ per ECU until 31 December 1998Sources: Bloomberg; Eurostat

60

70

80

90

100

110

9.0

8.5

8.0

7.5

7.0

6.5

Chinese Renminbi

Sources: BIS; Bloomberg; RBA2013

Nominal effective exchange rate(LHS, 2010 average = 100)

Index Yuan

Yuan per US$(RHS, inverted scale)

201020072004200160

80

100

120

60

80

100

120

Nominal TWIMarch quarter 1999 = 100

Sources: Bank of Japan; Board of Governors of the Federal Reserve System; European Central Bank

2013

YenIndex Index

Euro

US dollar

201020072001 2004

Exchange Rates

CHARt PACk | MAy 2013 29

6

12

Bank Profits

$b

0.0

0.4

6

12

0.0

0.4

$b

$b$b

2013-1.6

0.0

1.6

-1.6

0.0

1.6

$b$b

2010201320102007n Actualn Analysts’ forecasts

n Actualn Analysts’ forecasts

Major banks* Major banks*

Regional banks** Regional banks**

Foreign-owned banks*** Foreign-owned banks***

Profits after tax Bad and doubtful debt charge

Sources: APRA; Credit Suisse; Deutsche Bank; Nomura Equity Research;RBA; UBS Securities Australia; banks’ annual and interim reports

* ANZ, NAB and Westpac report half yearly to March and September, whileCBA reports to June and December

** Suncorp Bank, and Bendigo and Adelaide Bank report half yearly to Juneand December, while Bank of Queensland reports to February and August

*** All results are half year to June and December

2007

na na

0

10

20

0

10

20

Bank Profitability*

% %Post-tax and minority interests

0.0

0.5

1.0

1.5

0.0

0.5

1.0

1.5

Charge for bad and doubtful debtsPer cent of average assets

%%

Return on shareholders’ equity

* From 2006 data are on an IFRS basis; prior years are on an AGAAP basis;includes St. George and, from 2009, Bankwest

Sources: RBA; banks’ annual and interim reports

Regional banks

Major banks

Major banks

Institutions operating in Australia

Regional banks

201220072002199719921987

1.5

2.0

2.5

3.0

1.5

2.0

2.5

3.0

Major Banks’ Net Interest Margin*

* From 2006 data are on an IFRS basis; prior years are on AGAAP basis;excludes St George Bank and Bankwest prior to the first half of 2009

%Domestic, half-yearly

%

2009 20132001 2005

Sources: RBA; banks’ financial reports

Banking Indicators

CHARt PACk | MAy 2013 30

0

1

2

3

4

5

0

1

2

3

4

5

Banks’ Non-performing Assets

Domestic books, share of loans by type

* Includes lending to financial businesses, bills and debt securitiesSource: APRA

Housing

% %

Personal

2012

Business and other*

Total*

2010200820062004

Banks’ Non-performing Assets

0

2

4

6

0

2

4

6

Consolidated global operations, share of on-balance sheet assets

Impaired

Total*

* Includes assets 90+ days past due that are well securedSource: APRA

2004 2008 2012200019961992

% %

%

Bank Funding*

%

0

10

20

30

40

50

0

10

20

30

40

50

2011

Short-term debt**

Equity

Securitisation

20092005* Adjusted for movements in foreign exchange rates** Includes deposits and intragroup funding from non-residentsSources: APRA; RBA; Standard & Poor’s

Long-term debt

Share of total, all banks

Domestic deposits

20132007

Capital Ratios*

0

5

10

15

0

5

10

15

Building societies

Other ADIsLocally incorporated banks

Tier 1

Tier 2

Total

Credit unions

1991* Per cent of risk-weighted assets; break in March 2008 due to the

introduction of Basel II for most ADIsSource: APRA

201220051998

% %Consolidated global operations

201220051998

Banking Indicators