prasar bharati broadcasting …prasarbharati.gov.in/information/documents/doordarshan - gst...prasar...

TRANSCRIPT

PRASAR BHARATI BROADCASTING CORPORATION OF INDIA

Training and Overview July 24 and 25, 2017

GOODS & SERVICES TAX (‘GST’)

ByD C G & Co., Chartered Accountants

1

GST effective date – July 01, 2017 (Other than Jammu & Kashmir)/ July 08, 2017 for Jammu & Kashmir

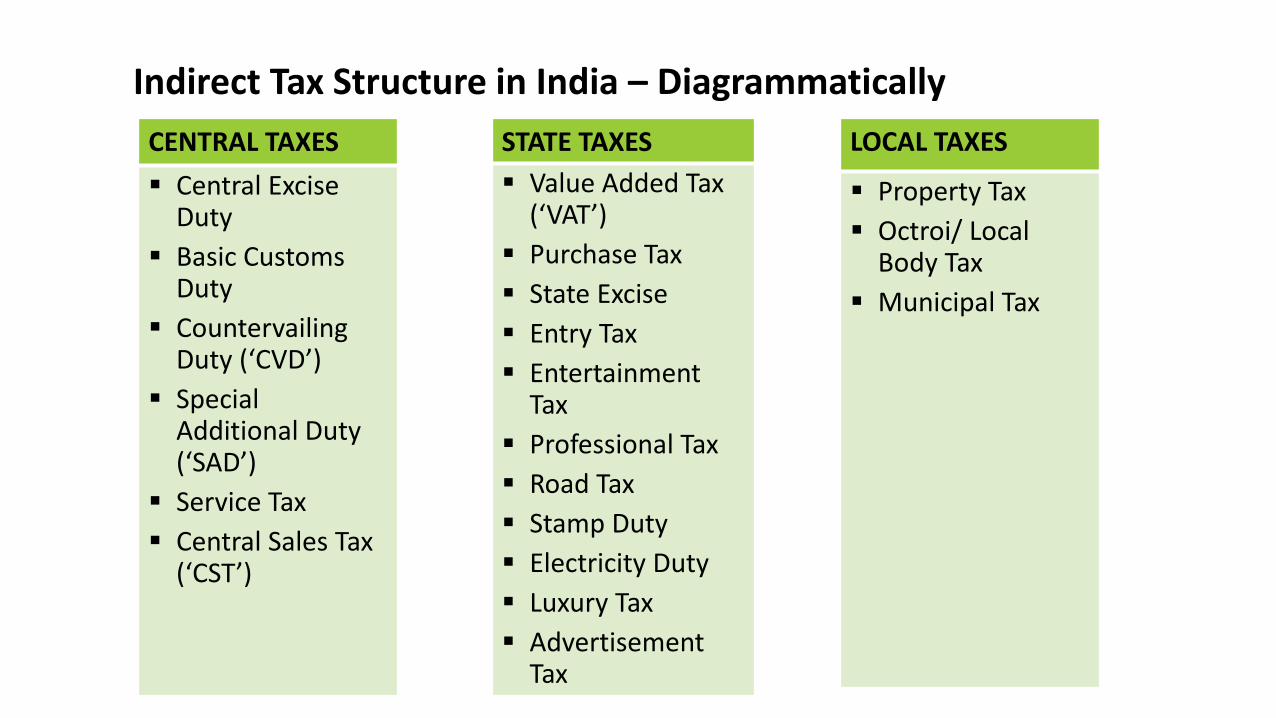

Indirect Tax Structure in India – Diagrammatically

CENTRAL TAXES

▪ Central Excise Duty

▪ Basic Customs Duty

▪ Countervailing Duty (‘CVD’)

▪ Special Additional Duty (‘SAD’)

▪ Service Tax

▪ Central Sales Tax (‘CST’)

LOCAL TAXES

▪ Property Tax

▪ Octroi/ Local Body Tax

▪ Municipal Tax

STATE TAXES

▪ Value Added Tax (‘VAT’)

▪ Purchase Tax

▪ State Excise

▪ Entry Tax

▪ Entertainment Tax

▪ Professional Tax

▪ Road Tax

▪ Stamp Duty

▪ Electricity Duty

▪ Luxury Tax

▪ Advertisement Tax

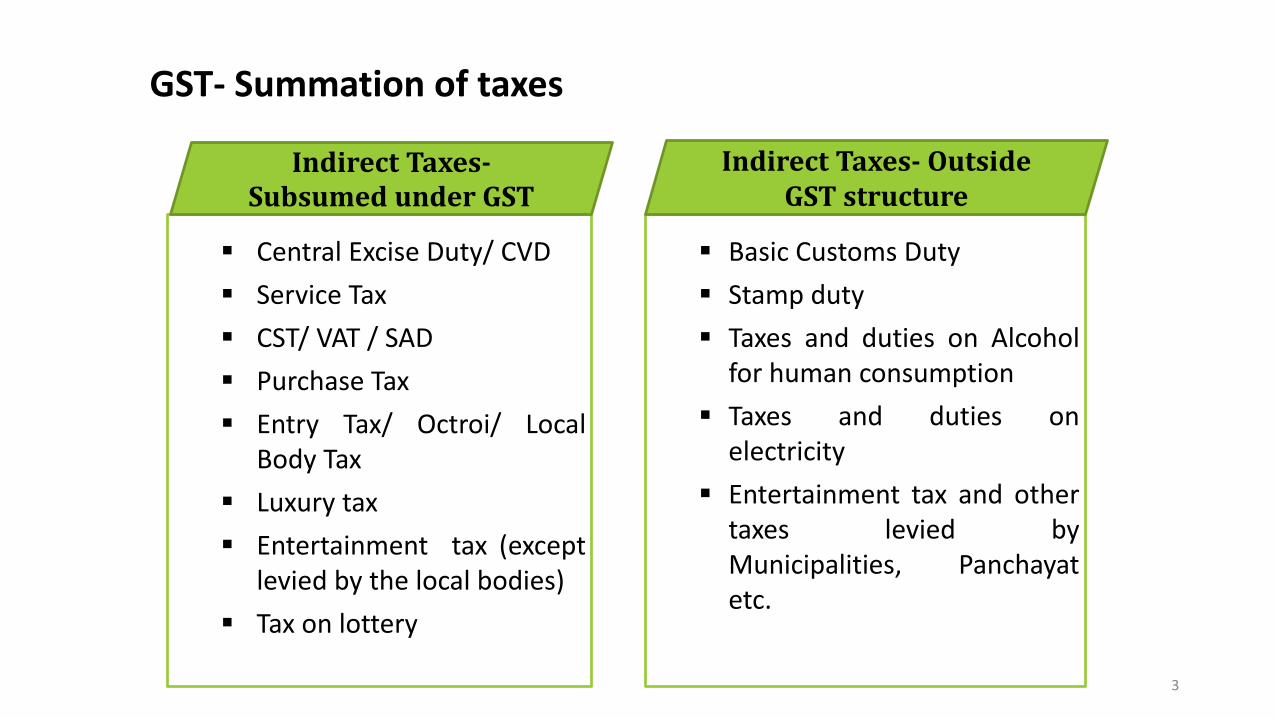

GST- Summation of taxes

3

▪ Central Excise Duty/ CVD

▪ Service Tax

▪ CST/ VAT / SAD

▪ Purchase Tax

▪ Entry Tax/ Octroi/ LocalBody Tax

▪ Luxury tax

▪ Entertainment tax (exceptlevied by the local bodies)

▪ Tax on lottery

▪ Basic Customs Duty

▪ Stamp duty

▪ Taxes and duties on Alcoholfor human consumption

▪ Taxes and duties onelectricity

▪ Entertainment tax and othertaxes levied byMunicipalities, Panchayatetc.

Indirect Taxes-Subsumed under GST

Indirect Taxes- Outside GST structure

More about GST

4

Levy

GST Rate

▪ Dual GST Regime

▪ Central Goods and Services Tax (CGST) and State/UT Goods andServices Tax (SGST)/(UTGST) levied on Intra-State supplies. i.e.within same State or UT

▪ Integrated Goods and Service tax (IGST) to be levied on Inter-State supplies i.e. outside other State or UT

▪ Other cess

▪ To be levied on all transactions of supply of goods and services.

▪ Rates of GST are 5%, 12%, 18% & 28% (plus cess on fewproducts), with lower rates for essential items and the highestfor luxury items and de-merit goods

5

Registration under GST

▪ Single Registration for IGST/ SGST/ UTGST/CGST per State

▪ Separate registration for AIR & DD in each State i.e., business vertical wise

▪ Registration required in each State from where supplies made

6

Intra/Inter-State Supply of Goods/Services

Location of Supplier Place of SupplyNature of

Transaction

1 Delhi Punjab Inter-State

2 Delhi Delhi Intra-State

•Illustration – Whether Inter-State or Intra-State

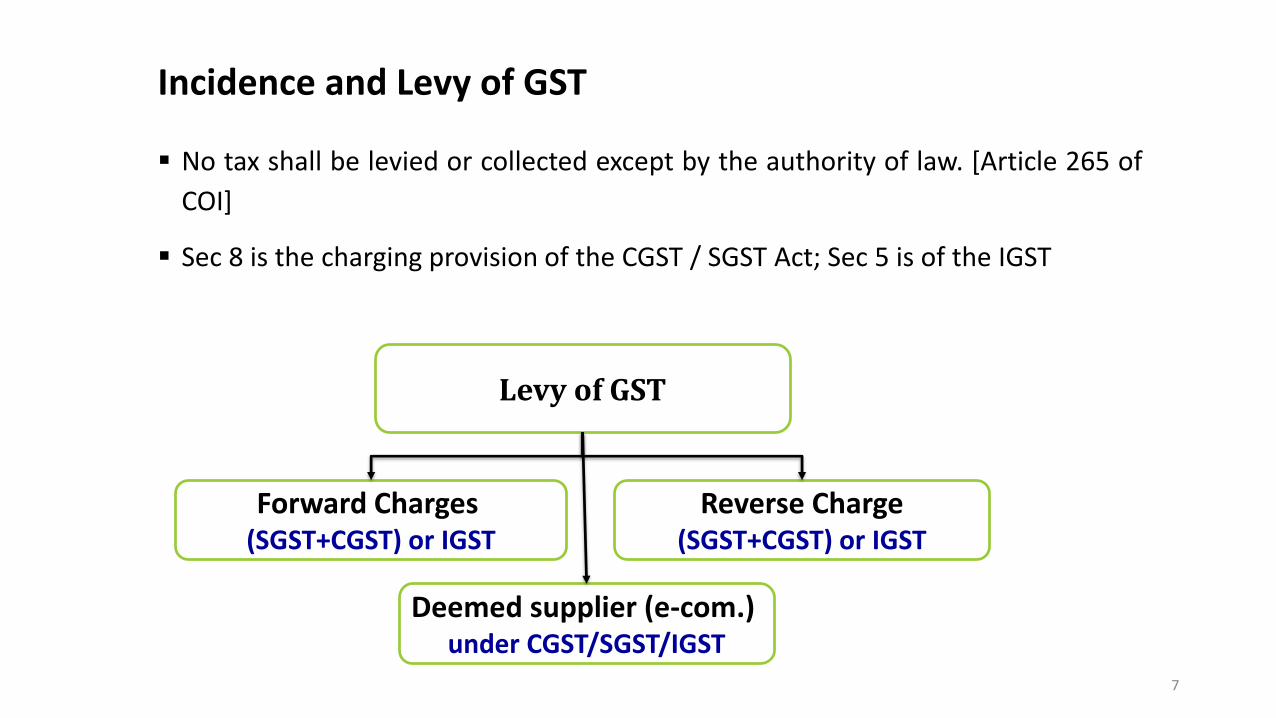

Incidence and Levy of GST

▪ No tax shall be levied or collected except by the authority of law. [Article 265 of

COI]

▪ Sec 8 is the charging provision of the CGST / SGST Act; Sec 5 is of the IGST

7

Levy of GST

Forward Charges (SGST+CGST) or IGST

Reverse Charge(SGST+CGST) or IGST

Deemed supplier (e-com.) under CGST/SGST/IGST

Who is Taxable Person

• Person effecting Inter-State Supply

• Person liable pay tax under reverse charge

• Casual Taxable Person

• Non-Resident Taxable Person

• Person who supplies goods/services on behalf of another registered taxable

person.

• Person supplying goods/services through an Electronic Commerce Operator

• Electronic Commerce Operators

8

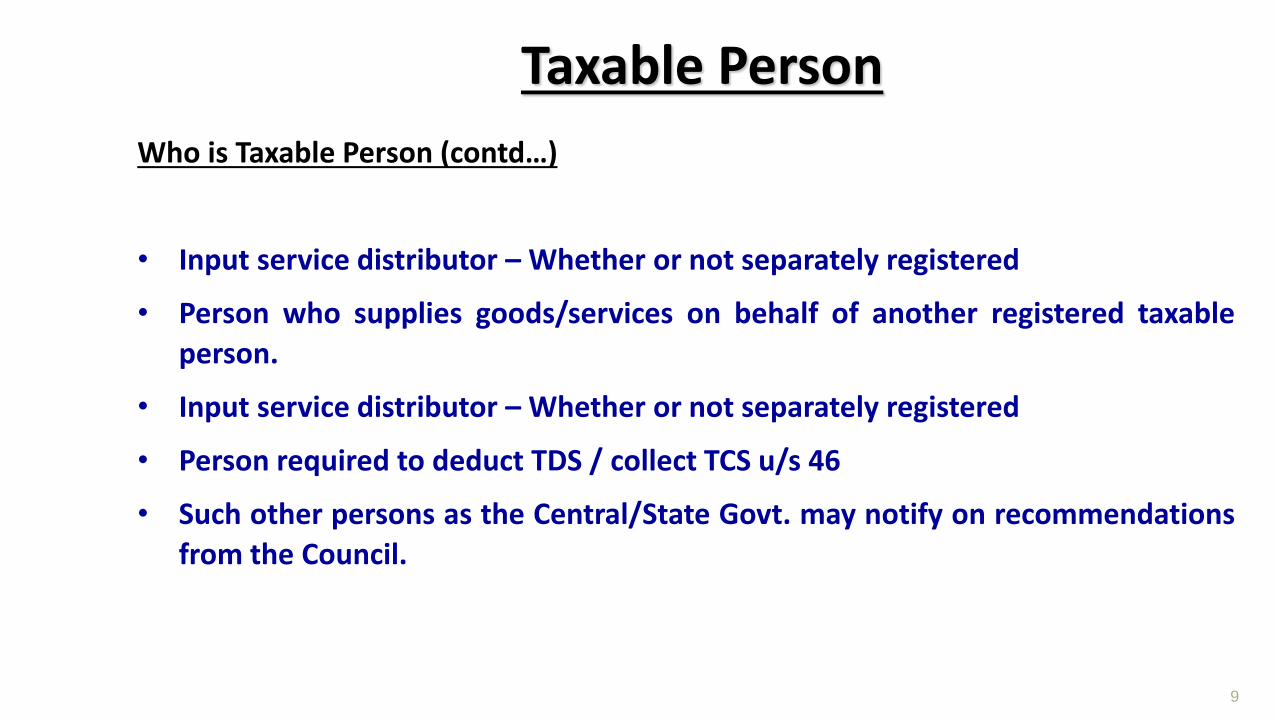

Taxable Person

Who is Taxable Person (contd…)

• Input service distributor – Whether or not separately registered

• Person who supplies goods/services on behalf of another registered taxable

person.

• Input service distributor – Whether or not separately registered

• Person required to deduct TDS / collect TCS u/s 46

• Such other persons as the Central/State Govt. may notify on recommendations

from the Council.

9

Taxable Person

10

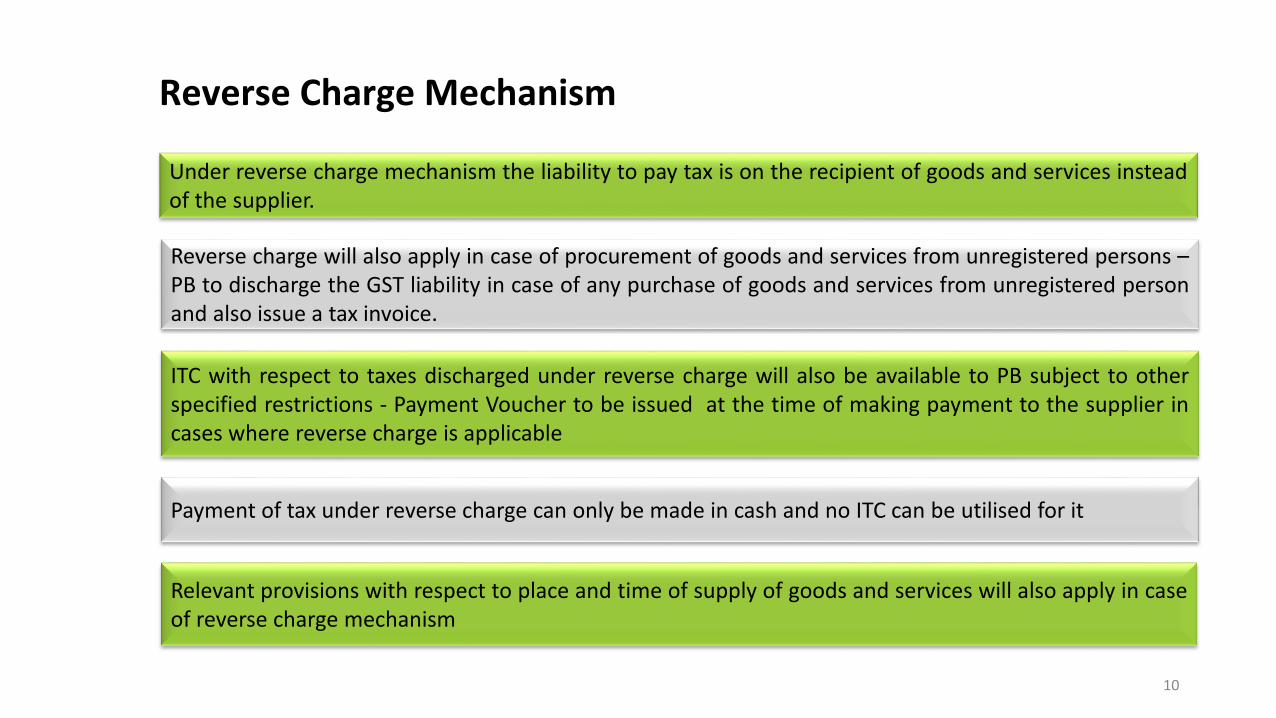

Under reverse charge mechanism the liability to pay tax is on the recipient of goods and services insteadof the supplier.

Reverse charge will also apply in case of procurement of goods and services from unregistered persons –PB to discharge the GST liability in case of any purchase of goods and services from unregistered personand also issue a tax invoice.

ITC with respect to taxes discharged under reverse charge will also be available to PB subject to otherspecified restrictions - Payment Voucher to be issued at the time of making payment to the supplier incases where reverse charge is applicable

Payment of tax under reverse charge can only be made in cash and no ITC can be utilised for it

Relevant provisions with respect to place and time of supply of goods and services will also apply in caseof reverse charge mechanism

Reverse Charge Mechanism

11

Service Categories Provider Of Service % GST Payable Under RCM By PB

Rate of Tax

Import of Services from service providerlocated outside India (non taxable territory)

Any person who islocated in a non-taxable territory

100% 18%

Services by an individual advocate or firm ofadvocates by way of legal services, directly orindirectly

An individualadvocate or firm ofadvocates

100% 18%

Services provided or agreed to be provided bya goods transport agency (GTA) in respect oftransportation of goods by road

Goods TransportAgency (GTA)

100% 5%

Sponsorship services Any person 100% 18%

*Note: There are more services on which Reverse Charge is applicable.List of services under RCM released by GST Council on 19 May 2017 is already published in the GST Guidance Note

Key Services under Reverse Charge Mechanism*

12

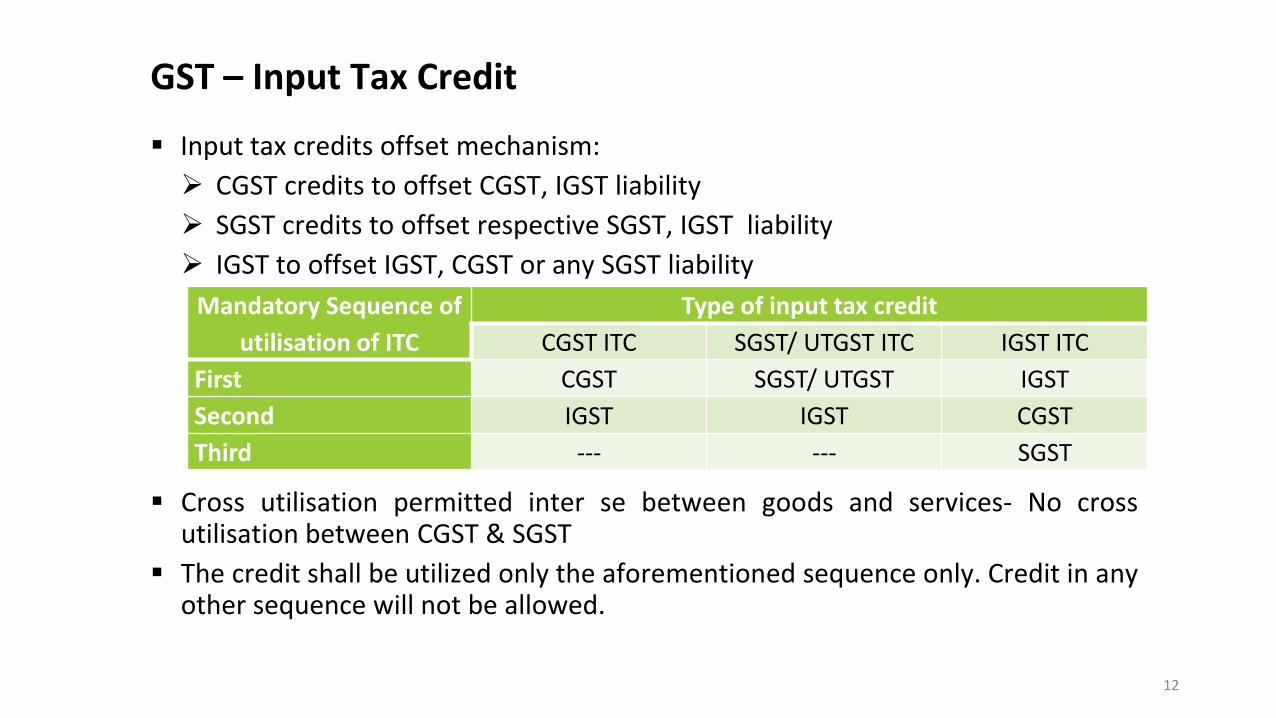

GST – Input Tax Credit

▪ Input tax credits offset mechanism:

➢ CGST credits to offset CGST, IGST liability

➢ SGST credits to offset respective SGST, IGST liability

➢ IGST to offset IGST, CGST or any SGST liability

▪ Cross utilisation permitted inter se between goods and services- No crossutilisation between CGST & SGST

▪ The credit shall be utilized only the aforementioned sequence only. Credit in anyother sequence will not be allowed.

Mandatory Sequence of

utilisation of ITC

Type of input tax credit

CGST ITC SGST/ UTGST ITC IGST ITC

First CGST SGST/ UTGST IGST

Second IGST IGST CGST

Third --- --- SGST

Local Supply - Manner

Tax Paid on Purchases

Input CGST (Say Rs.100)

Input SGST (Say Rs.100)

Tax Charged on Sales

Output CGST (Say Rs.120)

Output SGST (Say Rs.120)

Tax Payable to Govt.

O – I (Rs.20)To Centre

O – I (Rs.20)To State

Inter-State Supply - Manner

Tax Paid on Purchases

Input CGST (say 100)

Input SGST (say 100)

Tax Charged on Central Sales

Output IGST = CGST + SGST

Tax Payable to Central Govt.

O – Input IGST –CGST – SGST

(Say) 220 = 110 + 110

220 – 0 – 100 – 100 = 20

Every Inter-State Supply would have ONE component – IGST

Inter-State Supply - MannerEvery Inter-State Supply would have ONE component – IGST

Tax Paid on Central Purchases

Output CGST [Say Rs. 120]

Output SGST [Say Rs.120]

Tax Charged on Local Sales

Input IGST [Rs. 220]

Tax Payable to Govt.

Output CGST –IGST (O-I)

= 0 [120 – 120]

Output SGST –IGST [O-I]

= 20 [120-100]

16

Availability of ITC under GSTPB should be eligible to take input tax credit on any procurement of goods (including capital goods)and services, subject to the specified conditions:

▪ Conditions of availing ITC:➢ Goods/Services should be used or intended to be used in the course or furtherance of business➢ Possession of tax invoice/ debit note issued by person registered under GST➢ Receipt of goods/ services➢ Payment to supplier should be made within 180 days from the date of invoice. In case payment is

not made within stipulated time period, input tax credit would need to be reversed (along withinterest) and re-claimed, once paid – In respect of inter-office transactions (withoutconsideration) where actual payments would not be made, it would be deemed to have beenpaid)

➢ In case of capital goods, depreciation under Income tax should not be claimed on the taxcomponent

➢ Tax paid by supplier.➢ Supplier has filed GSTR-1 and 3.

17

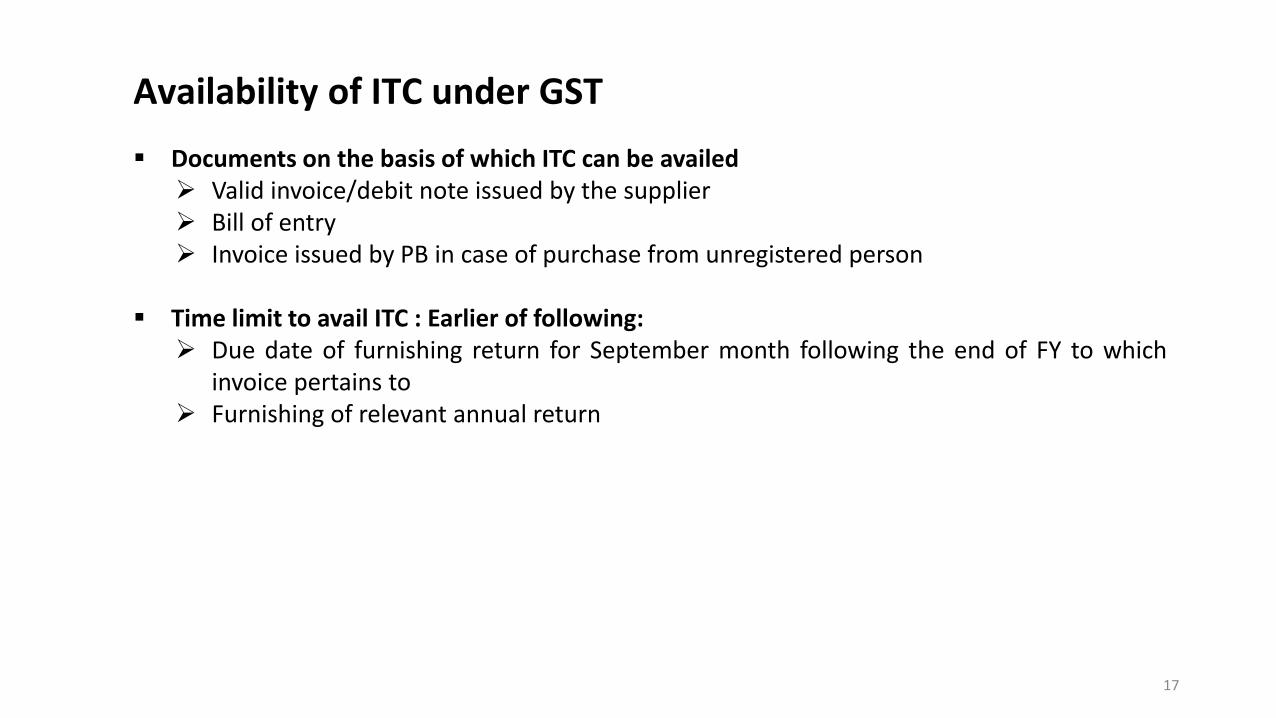

Availability of ITC under GST

▪ Documents on the basis of which ITC can be availed➢ Valid invoice/debit note issued by the supplier➢ Bill of entry➢ Invoice issued by PB in case of purchase from unregistered person

▪ Time limit to avail ITC : Earlier of following:➢ Due date of furnishing return for September month following the end of FY to which

invoice pertains to➢ Furnishing of relevant annual return

18

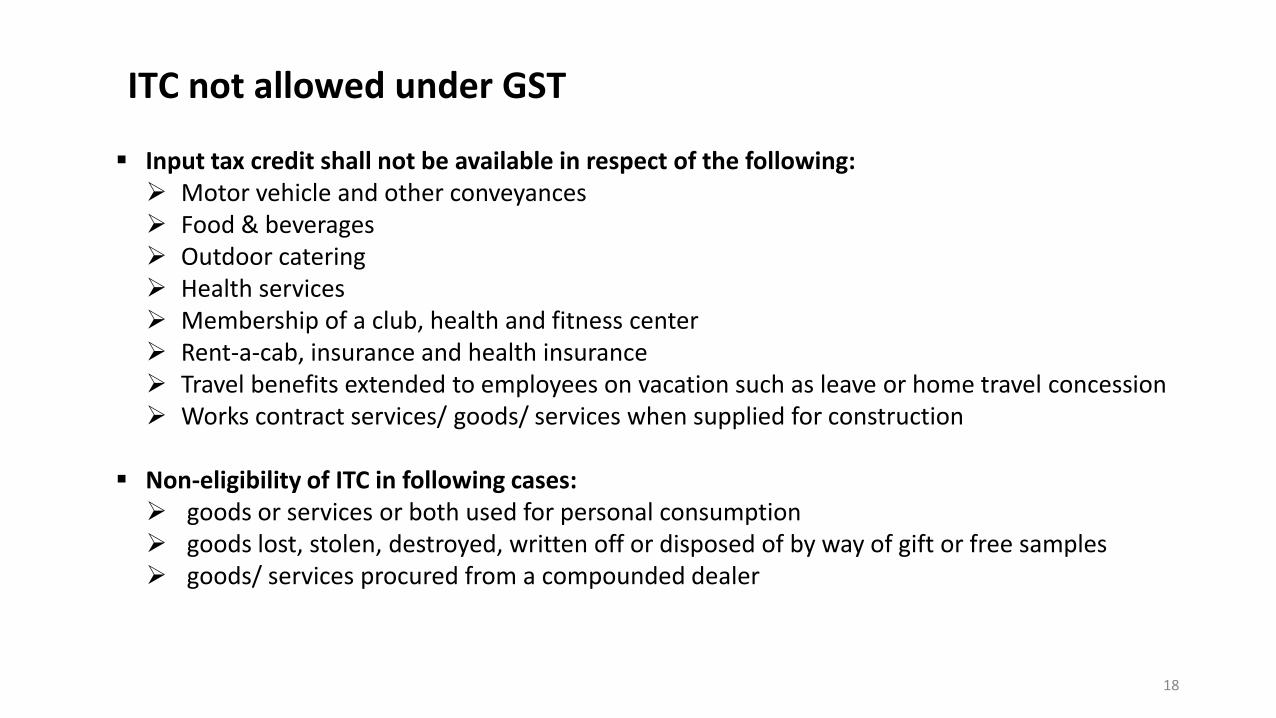

ITC not allowed under GST

▪ Input tax credit shall not be available in respect of the following:➢ Motor vehicle and other conveyances➢ Food & beverages➢ Outdoor catering➢ Health services➢ Membership of a club, health and fitness center➢ Rent-a-cab, insurance and health insurance➢ Travel benefits extended to employees on vacation such as leave or home travel concession➢ Works contract services/ goods/ services when supplied for construction

▪ Non-eligibility of ITC in following cases:➢ goods or services or both used for personal consumption➢ goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples➢ goods/ services procured from a compounded dealer

19

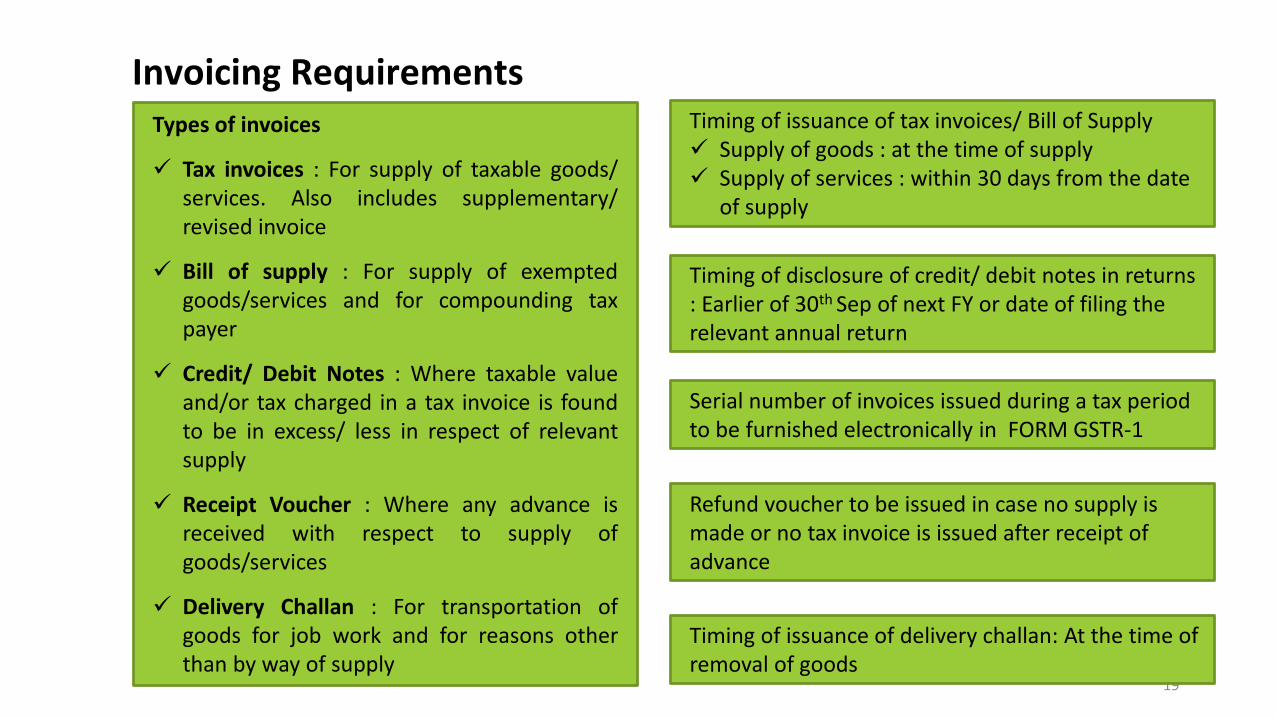

Types of invoices

✓ Tax invoices : For supply of taxable goods/services. Also includes supplementary/revised invoice

✓ Bill of supply : For supply of exemptedgoods/services and for compounding taxpayer

✓ Credit/ Debit Notes : Where taxable valueand/or tax charged in a tax invoice is foundto be in excess/ less in respect of relevantsupply

✓ Receipt Voucher : Where any advance isreceived with respect to supply ofgoods/services

✓ Delivery Challan : For transportation ofgoods for job work and for reasons otherthan by way of supply

Timing of issuance of tax invoices/ Bill of Supply✓ Supply of goods : at the time of supply✓ Supply of services : within 30 days from the date

of supply

Timing of disclosure of credit/ debit notes in returns : Earlier of 30th Sep of next FY or date of filing the relevant annual return

Serial number of invoices issued during a tax period to be furnished electronically in FORM GSTR-1

Refund voucher to be issued in case no supply is made or no tax invoice is issued after receipt of advance

Timing of issuance of delivery challan: At the time of removal of goods

Invoicing Requirements

20

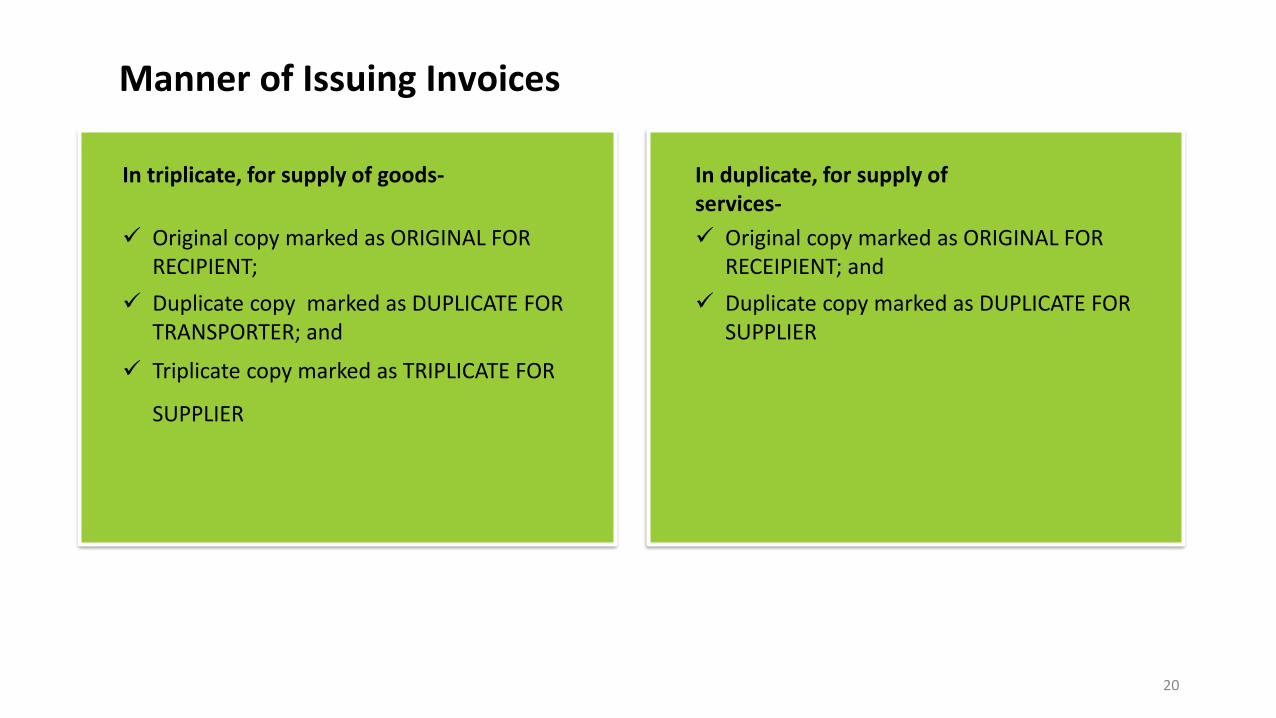

In triplicate, for supply of goods-

✓ Original copy marked as ORIGINAL FOR RECIPIENT;

✓ Duplicate copy marked as DUPLICATE FOR TRANSPORTER; and

✓ Triplicate copy marked as TRIPLICATE FOR

SUPPLIER

In duplicate, for supply of services-

✓ Original copy marked as ORIGINAL FOR RECEIPIENT; and

✓ Duplicate copy marked as DUPLICATE FOR SUPPLIER

Manner of Issuing Invoices

21

Invoice Contents

▪ Name, address and GSTIN of the supplier▪ Consecutive serial number containing only alphabets and/or numerals, unique for

a FY▪ Date of issue▪ Name, address and GSTIN/ Unique ID Number, if registered, of the recipient▪ Name & address of recipient and delivery address, along with State code & name,

in case of unregistered recipient and taxable supply >= INR 50,000 (Not applicable in case of exports)

▪ HSN code of goods or Accounting Code of services▪ Description of goods or services▪ Quantity in case of goods and unit▪ Total value of goods or services▪ Taxable value of goods or services taking into account discount or abatement

22

Invoice Contents

▪ Rate of tax (CGST, SGST or IGST)▪ Amount of tax charged in respect of taxable goods or services (CGST, SGST or

IGST)▪ Place of supply along with name of State, in case of an inter-state supply▪ Place of delivery where same is different from place of supply▪ Whether tax is payable on reverse charge▪ Word “Revised Invoice” or “Supplementary Invoice”, where applicable along with

the date and invoice number of the original invoice▪ Signature issuer

23

▪ GST on advance received by PB for goods/service – GST to bepaid based on the rate of service/good as applicable

▪ If details of service to be supplied are not known at the time ofreceipt of advance, IGST @ 18%

▪ In case of advance paid by PB for purchase of goods/ servicesvendor deposit GST. PB can claim credit only when the actualinvoice is received from vendor

▪ Advance receipt voucher to be reported only for such advanceswhich are unadjusted at the end of the month

RECEIPT VOUCHER

Documentation – Advance Received

24

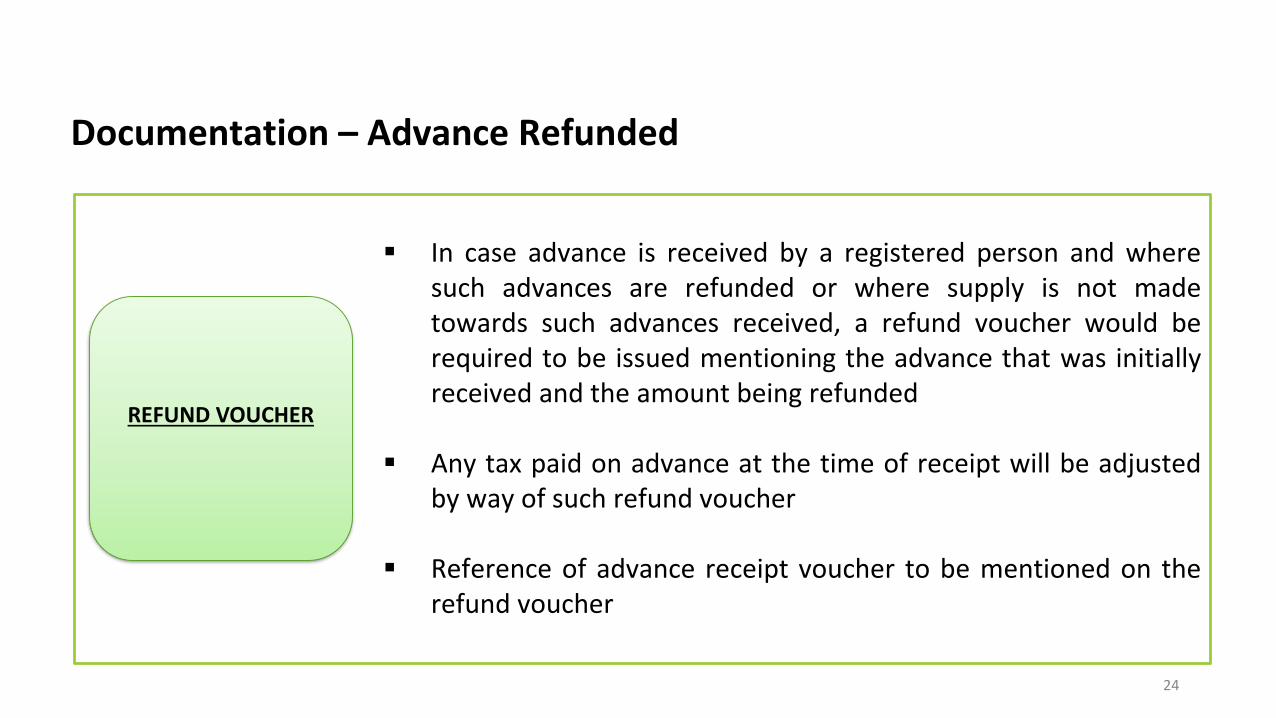

▪ In case advance is received by a registered person and wheresuch advances are refunded or where supply is not madetowards such advances received, a refund voucher would berequired to be issued mentioning the advance that was initiallyreceived and the amount being refunded

▪ Any tax paid on advance at the time of receipt will be adjustedby way of such refund voucher

▪ Reference of advance receipt voucher to be mentioned on therefund voucher

REFUND VOUCHER

Documentation – Advance Refunded

25

▪ Supplies received from unregistered persons, a registered personto raise an invoice for such receipt of supplies

▪ GST to be paid

▪ Input Credit of such GST available as credit to the recipient PB

▪ Payment made to unregistered persons towards suppliesreceived and for which tax is required to be paid, a paymentvoucher would be required to be issued by the recipient PB

▪ Credit of such supplies received from unregistered person wouldbe available only on payment of the same to the vendor

SELF-INVOICE TO BE ISSUED

PAYMENT VOUCHER TO BE ISSUED

Documentation - Supplies Received From Unregistered Persons

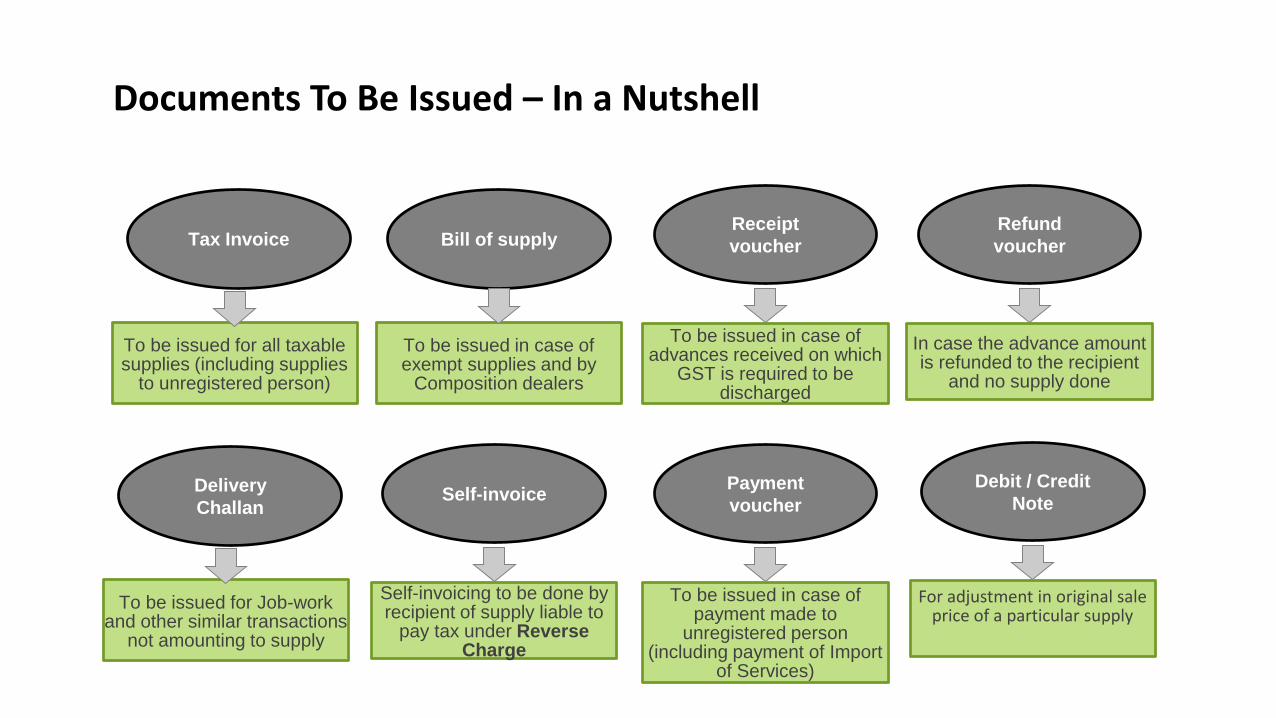

Bill of supplyReceipt

voucher

To be issued in case of exempt supplies and by

Composition dealers

To be issued in case of advances received on which

GST is required to be discharged

Tax Invoice

To be issued for all taxable supplies (including supplies

to unregistered person)

Delivery

Challan

To be issued for Job-work and other similar transactions

not amounting to supply

Refund

voucher

In case the advance amount is refunded to the recipient

and no supply done

Self-invoice

Self-invoicing to be done by recipient of supply liable to

pay tax under Reverse Charge

Payment

voucher

To be issued in case of payment made to

unregistered person (including payment of Import

of Services)

Debit / Credit

Note

For adjustment in original sale price of a particular supply

Documents To Be Issued – In a Nutshell

27

Goods/ Services of Prasar Bharati

Sl. No. Description of Goods / Service Type of

Code

Code* Rate of GST

1 Turntables (Record-Decks), Record-Players, Cassette-

players and other Sound Reproducing Apparatus, not

incorporating a sound recording device coin or Disc-

operated Record-players

HSN 85191000 18% with ITC

2 Cinematographic film, Exposed and Developed, whether

or not incorporating sound track or consisting only of

sound track of a width of 35mm or more: Feature Films:

made wholly in black and white and a length exceeding

4,000 M

HSN 37061012 18% with ITC

3 Broadcasting Service SAC 00440165 18% with ITC

4 Commercial Training and Coaching SAC 00440229 18% with ITC

5 Other Taxable Services-Other than ones mentioned SAC 00441480 18% with ITC

6 Advertising Agency SAC 00440013 18% with ITC

7 Rent a Cab Operators SAC 00440048 5% with-out

ITC

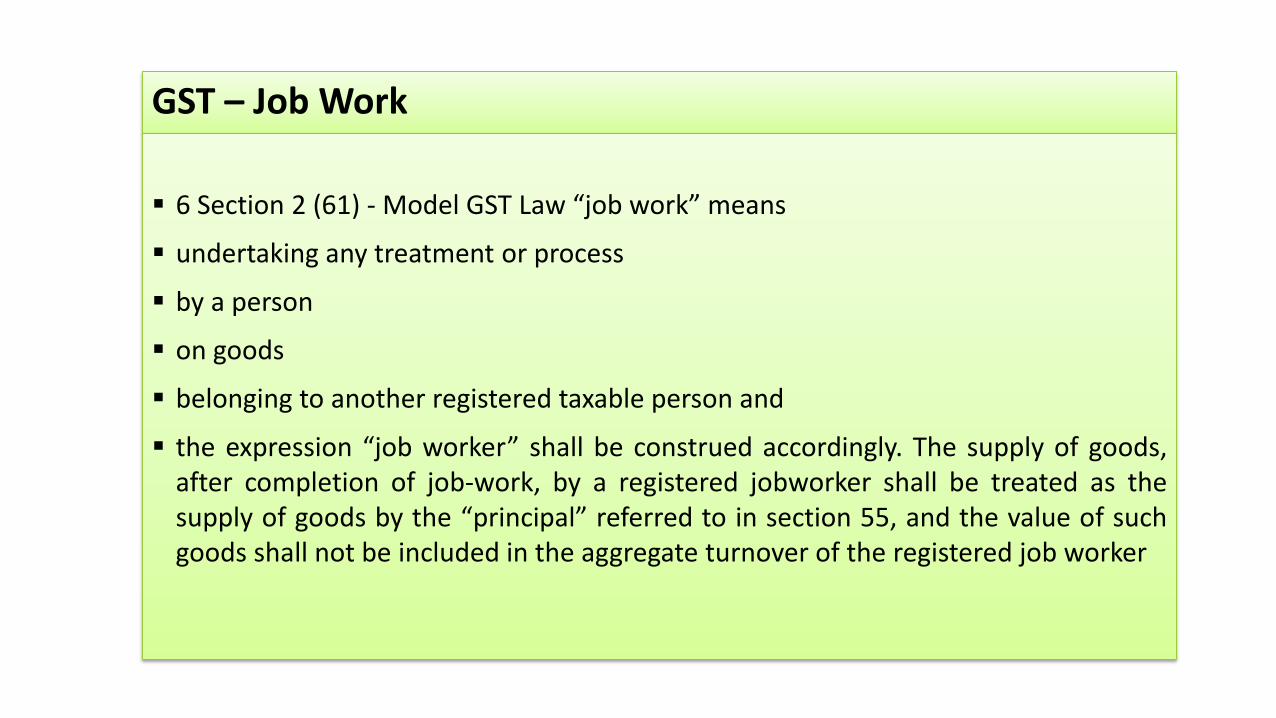

GST – Job Work

▪ 6 Section 2 (61) - Model GST Law “job work” means

▪ undertaking any treatment or process

▪ by a person

▪ on goods

▪ belonging to another registered taxable person and

▪ the expression “job worker” shall be construed accordingly. The supply of goods,after completion of job-work, by a registered jobworker shall be treated as thesupply of goods by the “principal” referred to in section 55, and the value of suchgoods shall not be included in the aggregate turnover of the registered job worker

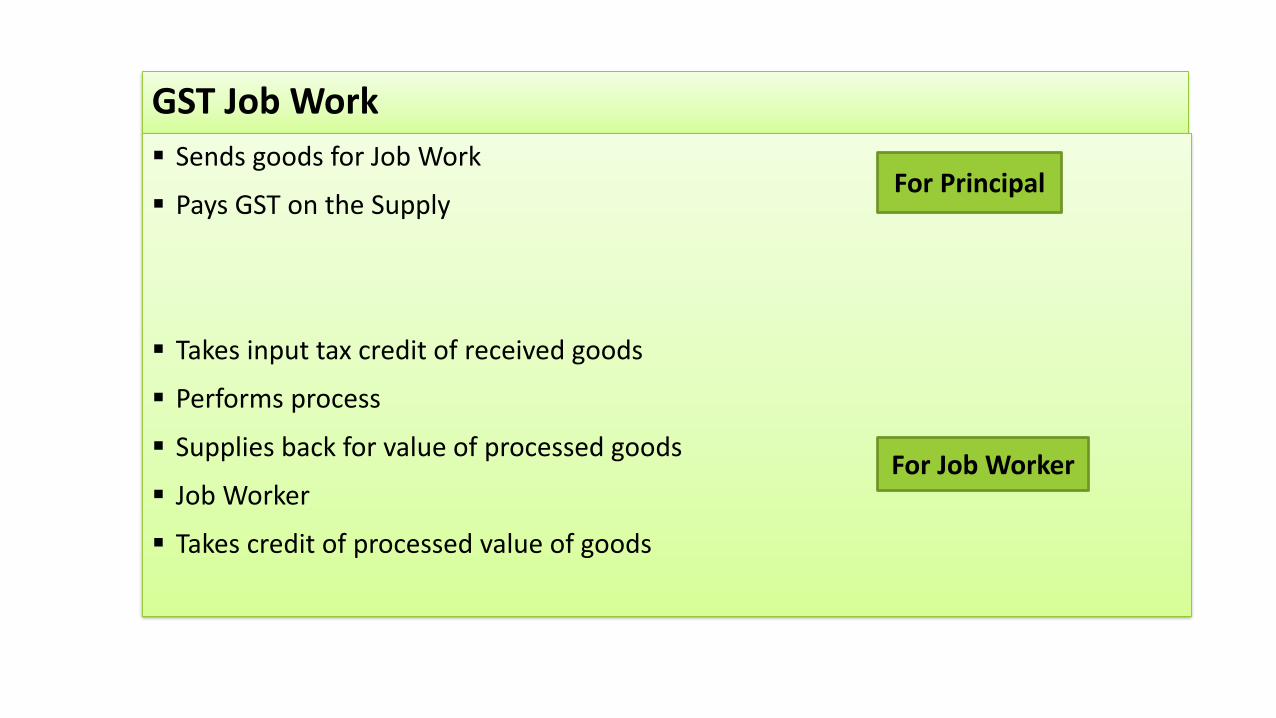

GST Job Work

▪ Sends goods for Job Work

▪ Pays GST on the Supply

▪ Takes input tax credit of received goods

▪ Performs process

▪ Supplies back for value of processed goods

▪ Job Worker

▪ Takes credit of processed value of goods

For Job Worker

For Principal

GST Returns and TimelineReturn Form

What to file? By Whom? By When?

GSTR-1Details of outward supplies of taxable goods and/ or services effected

Registered Taxable Supplier

10th of the next month

GSTR-2Details of inward supplies of taxable go and/or services effected claiming input tax credit.

Registered Taxable Recipient

15th of the next month

GSTR-3

Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the payment of amount of tax.

Registered Taxable Person

20th of the next month

GSTR-9 Annual ReturnRegistered Taxable Person

31st December of next financial year

GSTR-10 Final Return

Taxable person whose registration has been surrendered or cancelled.

Within three months of the date of cancellation or date of cancellation order, whichever is later.

31

▪ Defers Returns filing due date for July & August, 2017 extended to August 20, 2017 & September 20,2017 respectively;

▪ Alternative Form is introduced i.e. GSTR-3B to be furnished for July & August, 2017 - reflectingsummary of outward & inward supplies

▪ GSTR-1 reflecting invoice wise outward supply details for July , 2017 can be filed by September 05,2017 and for August, 2017 can be filed by September 20, 2017

▪ Facility for uploading of outward supplies for July, 2017 will be available from July 15, 2017▪ No late fees and penalty would be levied for the interim period

* Vide Press Release dated June 18, 2017

Month GSTR-3B GSTR-1 GSTR-2 (auto populated from GSTR-1)

July, 2017 20th August, 2017 1st-5th September, 2017 6st-10th September, 2017

August, 2017 20th September, 2017

16th-20th September, 2017 21st-25th September, 2017

Due Date For Return Filing For July & August, 2017 Extended*

32

In cash*by debit in the electronic Cash Ledger (TDS/TCS, Composition levy to be paid only through cash ledger)

✓ Internet banking through authorized banks✓ Credit/ Debit card after registering the same with

GSTN✓ Over the Counter (‘OTC’) through authorized banks

for deposits up to Rs. 10,000 per challan per tax period

By debit of electronic Credit Ledger-Only tax payment is allowed

*Challan to be generated in Form GST PMT-4 (valid for 15 days).The date of credit to the Government account shall be considered as date of deposit of the tax dues

₹ %

GST Payments

33

Relevant Provision Applicability on PB

Services by an employee to employer in course of employment –do not qualify as ‘supply’.

Any supply by employer to employee may qualify as ‘supply’liable to GST. However, gifts not exceeding INR 50,000 in afinancial year shall not be treated as ‘supply’

No implications onservices by employeeto PB

Supply from PB to itsemployees should beexamined for GSTimplicationsSince ‘employer’ and ‘employee’ qualify as ‘related’ persons, any

supply of goods/services from employer to employee liable toGST, even if made without consideration

Key GST Provisions & Brief Applicability on PB

34

Relevant Provision Applicability on PB

Zero-rated Supply:1) Export of Goods : Taking goods out of India to a place outside

India2) Export of Services : Supply of service wherein:

➢ The supplier of service is located in India;➢ The recipient of service is located outside India;➢ The place of supply of service is outside India➢ The payment for such service is received in convertible

foreign exchange3) Supply of goods/services to Special Economic Zone

Credit of input tax for making zero rated supply is eligible.

Specifically withrespect to export ofservices, even if anyone of the givenconditions is notfulfilled, the same willbe treated as supplyand IGST shall beapplicable on thesame

Key GST Provisions & Brief Applicability on PB

35

Taxability of Inter-Office Transactions▪ Under GST, supply of goods/ services between distinct persons, when made in the

course or furtherance of business would qualify as ‘supply’ even if made withoutconsideration

▪ All offices of PB (separately registered under GST) would qualify as ‘distinct’ persons▪ Accordingly, any inter-office transactions between two PB offices should qualify as

‘supply’ liable to GST▪ Value on which GST has to be paid shall be determined in reference to the Valuation

Rules▪ We understand that following types of inter-office transactions may qualify ‘supply’

under GST regime➢ Marketing and support services (including common costs incurred by HO) provided

by HO to respective BO

➢ Inter-state stock transfer of goods (including movement of goods under warrantytransactions)

36

Inter-state Stock Transfer of Goods

▪ Supply of goods between distinct persons would qualify as ‘supply’ even if madewithout consideration

▪ All offices of PB (separately registered under GST) would qualify as ‘distinct’ persons▪ Accordingly, inter-state stock transfer/ other movement of goods between two PB’s

offices would qualify as ‘supply’ liable to GST▪ Office dispatching goods would be required to raise a tax invoice with applicable GST

and the recipient office to avail input tax credit of such GST charged▪ Value on which GST has to be paid shall be determined in reference to the Valuation

Rules (discussed separately)▪ Supply of goods to an unrelated person without consideration doesn’t fall under the

purview of ‘supply’. Therefore, movement of goods from an PB location directly to acustomer (like in case of return of products post repairing under in-warranty, etc.)

▪ Caution point➢ Minimize the movement of goods between PB offices➢ In case of return of repaired goods (if any), preferably goods to be sent directly to

customers (instead of routing though branch)

37

Goods Written off, Scrap Sales, Disposal▪ Scrap Sales – Sale Proceeds involved➢ Shall qualify as a ‘taxable supply’ liable to GST➢ Tax invoice would required to be raised with appropriate GST

▪ Scrap Sales/ Disposal – NIL Sale Proceeds➢ Disposal of business assets where input tax credit has been availed to be treated as

‘supply’ of goods even if made without consideration➢ Valuation of goods in such cases will be determined in terms of Valuation Rules➢ It is suggested to assign a value to such sales and raise a tax invoice with appropriate GST

▪ Goods Written off/ lost/ stolen/ destroyed➢ ITC (if claimed earlier) with respect to such goods would need to be reversed➢ Quantum of ITC to be reversed in case of capital goods shall be determined as Total ITC

claimed less higher of following:▪ ITC computed at the rate of 5% points for every quarter or part thereof from the date of

invoice▪ Tax on the transaction value of such capital goods

38

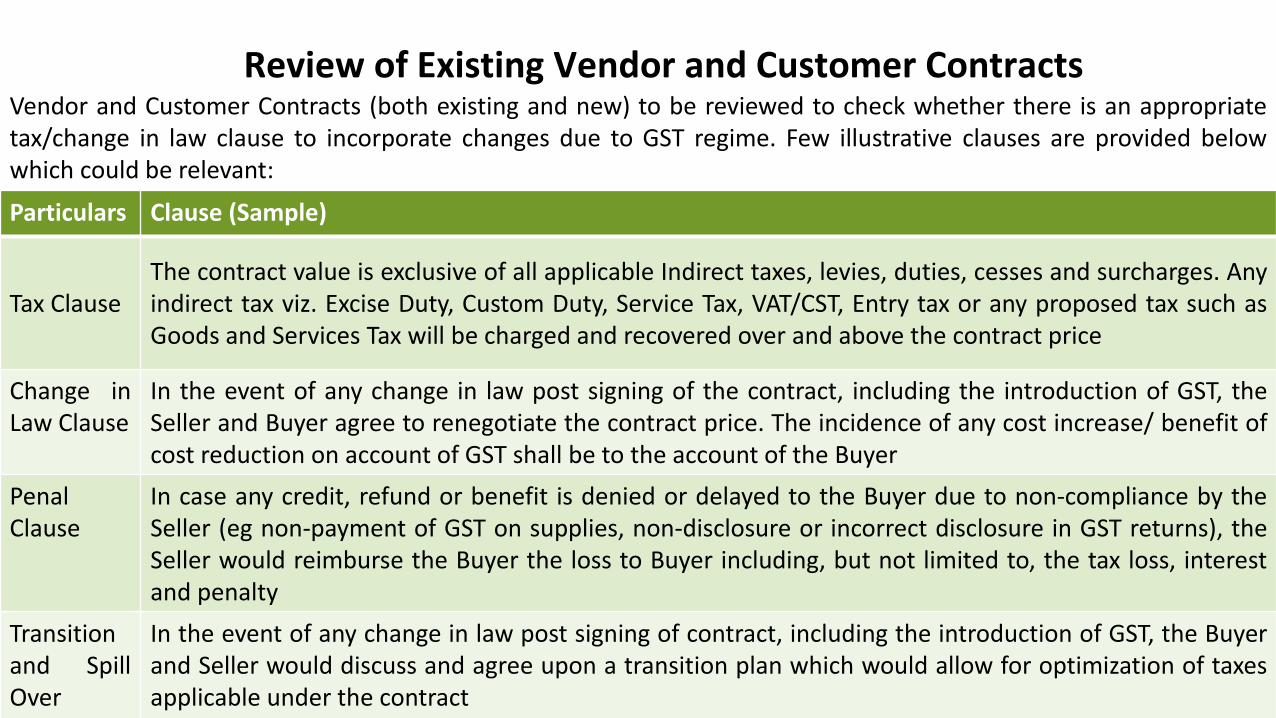

Particulars Clause (Sample)

Tax ClauseThe contract value is exclusive of all applicable Indirect taxes, levies, duties, cesses and surcharges. Anyindirect tax viz. Excise Duty, Custom Duty, Service Tax, VAT/CST, Entry tax or any proposed tax such asGoods and Services Tax will be charged and recovered over and above the contract price

Change inLaw Clause

In the event of any change in law post signing of the contract, including the introduction of GST, theSeller and Buyer agree to renegotiate the contract price. The incidence of any cost increase/ benefit ofcost reduction on account of GST shall be to the account of the Buyer

PenalClause

In case any credit, refund or benefit is denied or delayed to the Buyer due to non-compliance by theSeller (eg non-payment of GST on supplies, non-disclosure or incorrect disclosure in GST returns), theSeller would reimburse the Buyer the loss to Buyer including, but not limited to, the tax loss, interestand penalty

Transitionand SpillOver

In the event of any change in law post signing of contract, including the introduction of GST, the Buyerand Seller would discuss and agree upon a transition plan which would allow for optimization of taxesapplicable under the contract

Review of Existing Vendor and Customer ContractsVendor and Customer Contracts (both existing and new) to be reviewed to check whether there is an appropriatetax/change in law clause to incorporate changes due to GST regime. Few illustrative clauses are provided belowwhich could be relevant:

39

Responsibilities of Nodal Officer

▪ The officer to provide GSTIN number to all vendors (from whom the goods/ services havebeen procured) i.e. Telephone agency, Internet Agency, Manpower Agency etc. for takingeligible credit under GST law.

▪ The State Nodal Officer will ensure that the data provided to them by station inchargepersons is proper and contains all details for taking credit.

▪ The State Nodal Officer will ensure that all the station incharge persons have shared thedetails relevant for filing of GSTR 2 with them and will file the GSTR 2 post review of dataprovided by 15th of the next month.

▪ The State Nodal Officer should guide Station Incharge persons to check that all requisites ofan essential invoice are mentioned on the invoice.

▪ Proper records must be maintained evidencing the extent of work completed beforeintroduction of GST regime i.e., before 01-07-2017.

40

Responsibilities of Nodal Officer…Conti▪ The State Nodal Officer should ensure that the GST registration certificate shall be

displayed at the principal place of business and additional place of business.

▪ The State Nodal Officer should ensure that GSTIN number is mentioned on the nameboard of the Prasar Bharati at the entry gate.

▪ The details with respect to invoices, the payment of which is pending for more than 180days (under forward charge) is to be maintained separately.

▪ All the contracts to be entered with the vendors and clients must have the updated clausesin the agreement. Please refer the file shared separately for suggested changes.

▪ All nodal officer shall keep books of account such as invoices, bills of supply, credit anddebit notes, and delivery challans relating to stocks, deliveries, inward supply and outwardsupply etc. of the office at principal place of business.

41

Responsibilities of Nodal Officer…Conti

▪ The State Nodal officer should collect the GSTN number of all agencies/ otherservice recipients through Vendor registration form (format shared).

▪ The State Nodal Officer should ensure that the credit details showing separatelyCGST, SGST/UTGST and IGST is maintained and verified.

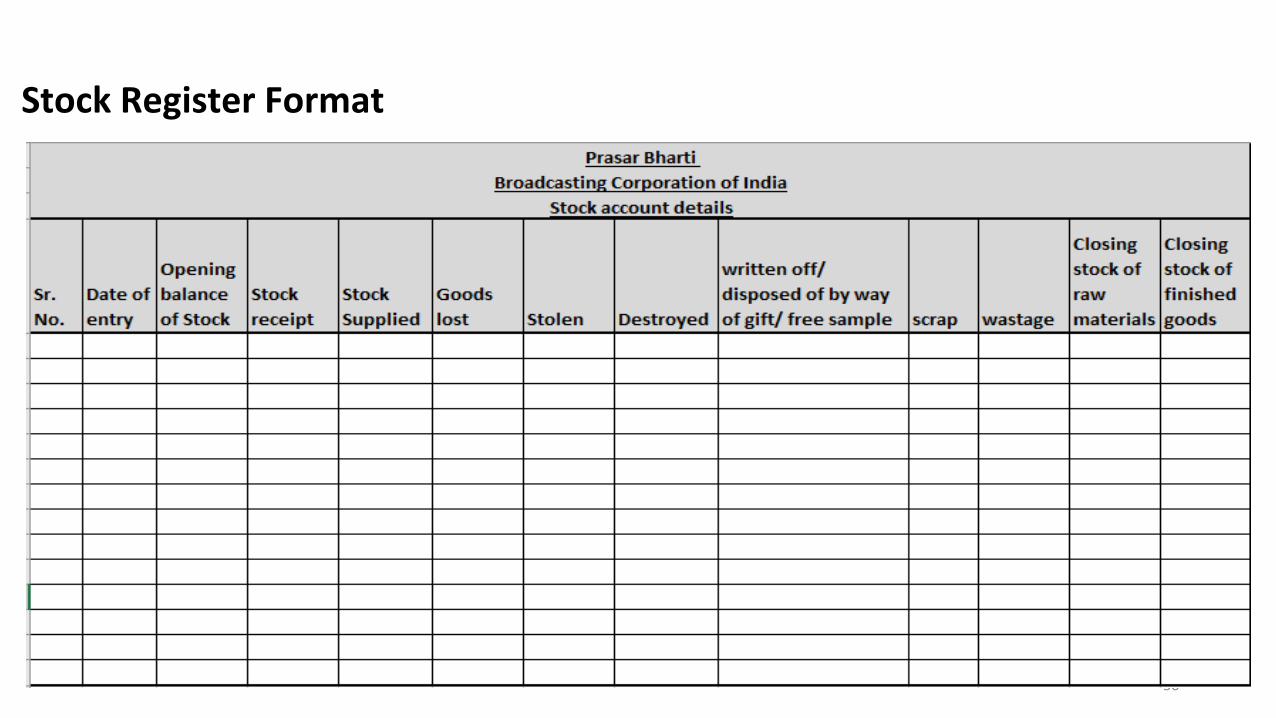

▪ The State Nodal Officer should also ensure that proper Stock register has beenmaintained.

▪ The State Nodal Officer should also ensure that the proper accounts of stock inrespect of goods received & supplied and such accounts shall contain particulars ofthe opening balance, receipt, supply, goods lost, stolen, destroyed, written off ordisposed of by way of gift or free sample and the balance of stock including rawmaterials, finished goods, scrap and wastage thereof is maintained. The format oflist for this will be provided within this week.

42

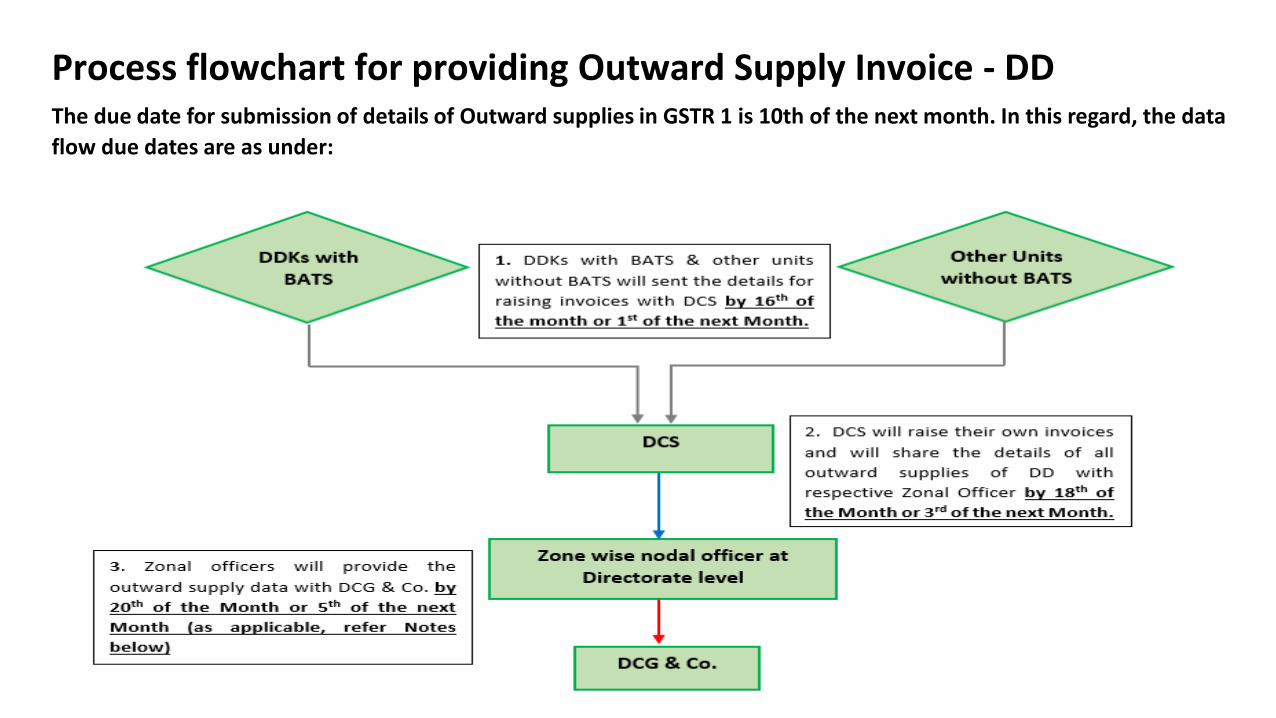

Process flowchart for providing Outward Supply Invoice - DDThe due date for submission of details of Outward supplies in GSTR 1 is 10th of the next month. In this regard, the data

flow due dates are as under:

43

Process flowchart for providing Outward Supply Invoice - DD

Note:

▪ The specified timelines are must to be followed unless otherwise changed.

▪ The outward supply data to be provided in all cases (i.e., the confirmation for NIL data is also to be

given on aforesaid time).

▪ The Outward supply data are to be provided on fortnightly basis i.e., in the below manner:

▪ For 1st to 15th of the Month by 20 of the Month to DCG & Co.

▪ For 16th to last date of the Month by 5th of the next Month to DCG & Co.

▪ The arrows in Black (Stage 1) are to be done till 16th of the month or 1st of the next Month.

▪ The arrows in Blue (Stage 2) are to be done till 18th of the Month or 3rd of the next Month.

▪ The arrows in Red (Stage 3) are to be done till 20th of the Month or 5th of the next Month

▪ DCG & Co. will co-ordinate for any queries related to outward supply data with State Nodal Officer

unless otherwise required.

44

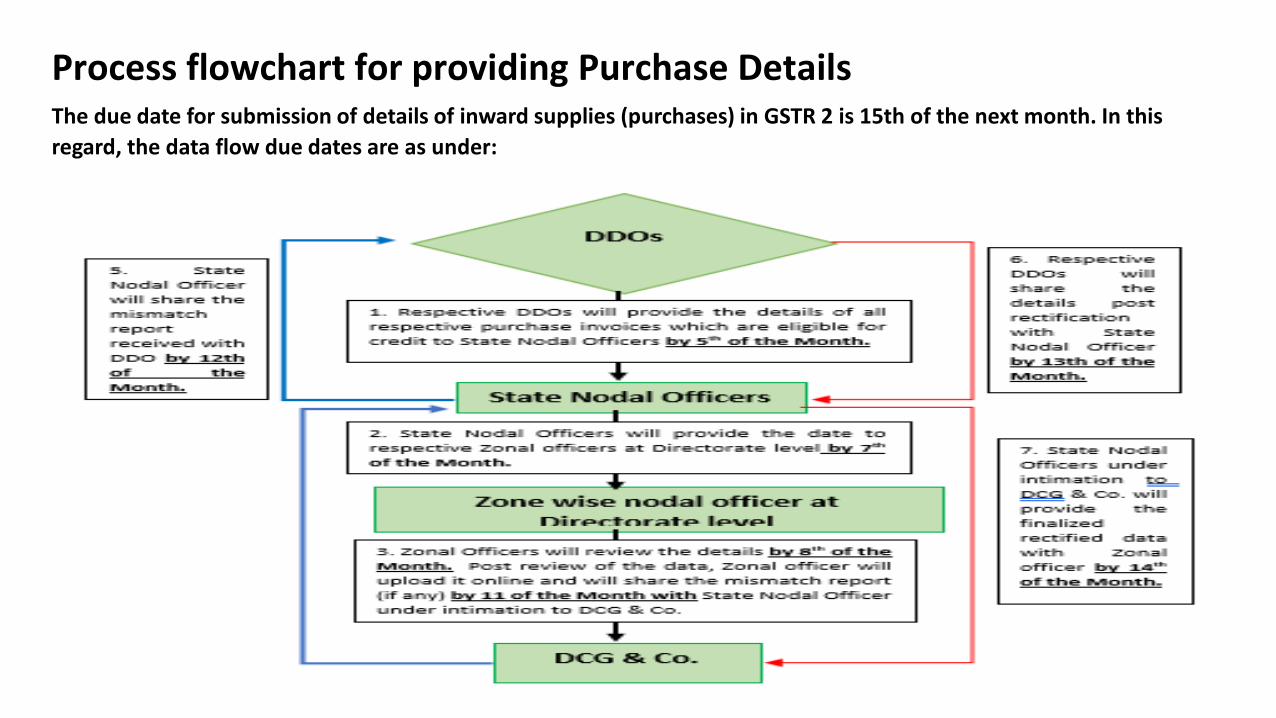

Process flowchart for providing Purchase DetailsThe due date for submission of details of inward supplies (purchases) in GSTR 2 is 15th of the next month. In this

regard, the data flow due dates are as under:

45

Process flowchart for providing Purchase Details

Note:

▪ The specified timelines are must to be followed unless otherwise changed.

▪ The purchases data to be provided in all cases (i.e., the confirmation for NIL data is also to be given on

aforesaid time).

▪ The arrows in Black (Stage 1) are to be done till 8th of the month

▪ The arrows in Blue (Stage 2) are to be done till 12th of the month

▪ The arrows in Red (Stage 3) are to be done till 14th of the month

46

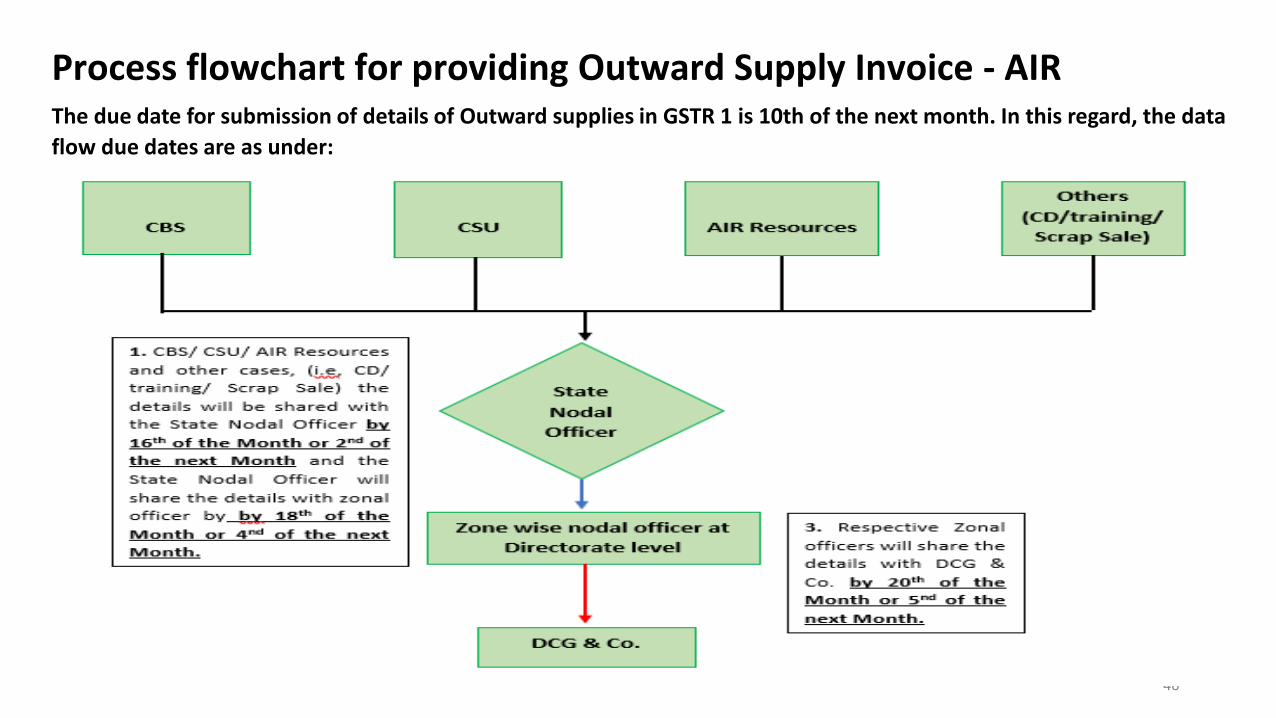

Process flowchart for providing Outward Supply Invoice - AIRThe due date for submission of details of Outward supplies in GSTR 1 is 10th of the next month. In this regard, the data

flow due dates are as under:

47

Process flowchart for providing Outward Supply Invoice - AIR

Note:

▪ The specified timelines are must to be followed unless otherwise changed.

▪ The outward supply data to be provided in all cases (i.e., the confirmation for NIL data is also to be

given on aforesaid time).

▪ The Outward supply data are to be provided on monthly basis i.e., in the below manner:

▪ For 1st to 15th of the Month by 20th of the Month to Zonal Nodal Officer(ZNO) and ZNO to DCG & Co.

▪ For 16th to last date of the Month by 5th of the next Month ZNO to DCG & Co.

▪ The arrows in Black (Stage 1) are to be done till 16th of the month or 2nd of the next Month.

▪ The arrows in Blue (Stage 2) are to be done till 18th of the month or 4th of the next Month.

▪ The arrows in Red (Stage 3) are to be done till 20th of the Month or 5th of the next Month

▪ DCG & Co. will co-ordinate for any queries related to outward supply data with State Nodal Officer

unless otherwise required.

48

Goods Procurement Sheet

49

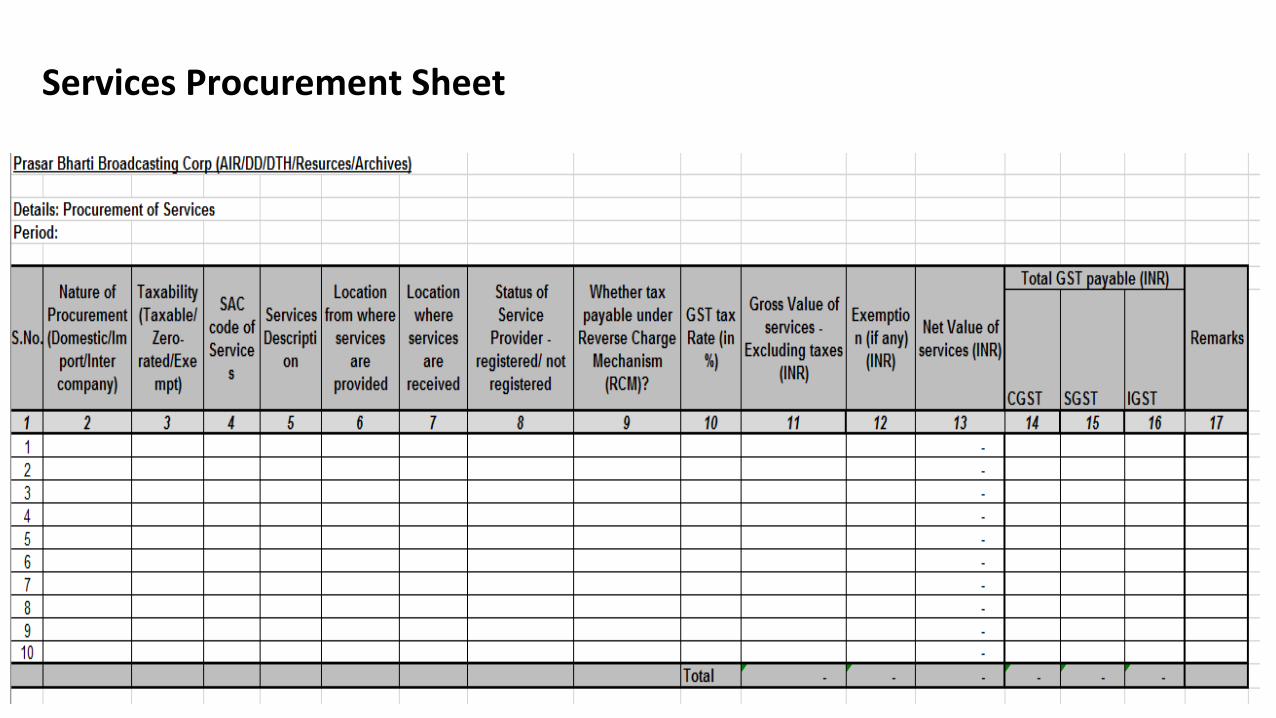

Services Procurement Sheet

50

Stock Register Format

51

ITC electronic

matching by GSTN

✓ GSTIN of

supplier &

recipient

✓ Invoice date &

number

✓ Taxable value &

tax amount

Matched File GSTR-2

Return

Un-

matched

GSTN to inform both supplier

& recipient to correct error within 2

days

Rectification by

Recipient/Supplier

File GSTR-2

ReturnReconciled

Un-

reconciled

Reverse Credit and

Pay taxes

ITCMatching by GSTN

52

Responsibilities of DDOs▪ The Credit with respect to personal use of immovable property should not be taken.

▪ The tax payments with respect to Goods and/ or Services received in the period prior toimplementation of GST regime i.e., before July 01, 2017 shall be made in terms with the lawapplicable at that point in time [which is hereinafter referred to as Old Indirect Tax Regime].In this regard, it is important to note here that, if an invoice is received on or after July 01,2017 but the goods or services has been received before July 01, 2017, the tax with respectto same has to be paid under Old Indirect Tax Regime.

▪ Further, the taxes with respect to the Goods and/ or Services received on or after the date,the same shall be taxed under the New Indirect Tax Regime which is by charging CentralGoods and Service Tax (CGST) and State Goods and Service Tax (SGST) or Integrated Goodsand Service Tax (IGST) as applicable on the transaction. The levy under GST is in the followingmanner:➢ Dual GST Regime - CGST and SGST to be levied on Intra-State supplies (supplies within

the same state)➢ IGST to be levied on Inter-State supplies (supplies in different state)

53

Responsibilities of DDOs▪ The DDO’s should also ensure that the Station Incharge persons has duly checked that all

requisites of an essential invoice are mentioned on the invoice.

▪ It is recommended to all Prasar Bharati/ AIR/ DD Offices to prepare details in the Excelformat (attached) for all goods/ service received from the Unregistered and Registered GSTdealers and send the same to State Nodal Officer.

▪ DDO’s should ensure to share the details of creditable purchases available with State NodalOfficer within time.

▪ The DDO should also ensure that the no CGST on the supplies received from anyunregistered supplier not exceeding INR 5,000 per day is paid under RCM. Further, onlySGST portion is to be paid. In this regard, we will keep you updated for any furtherdevelopments for removal of SGST portion.

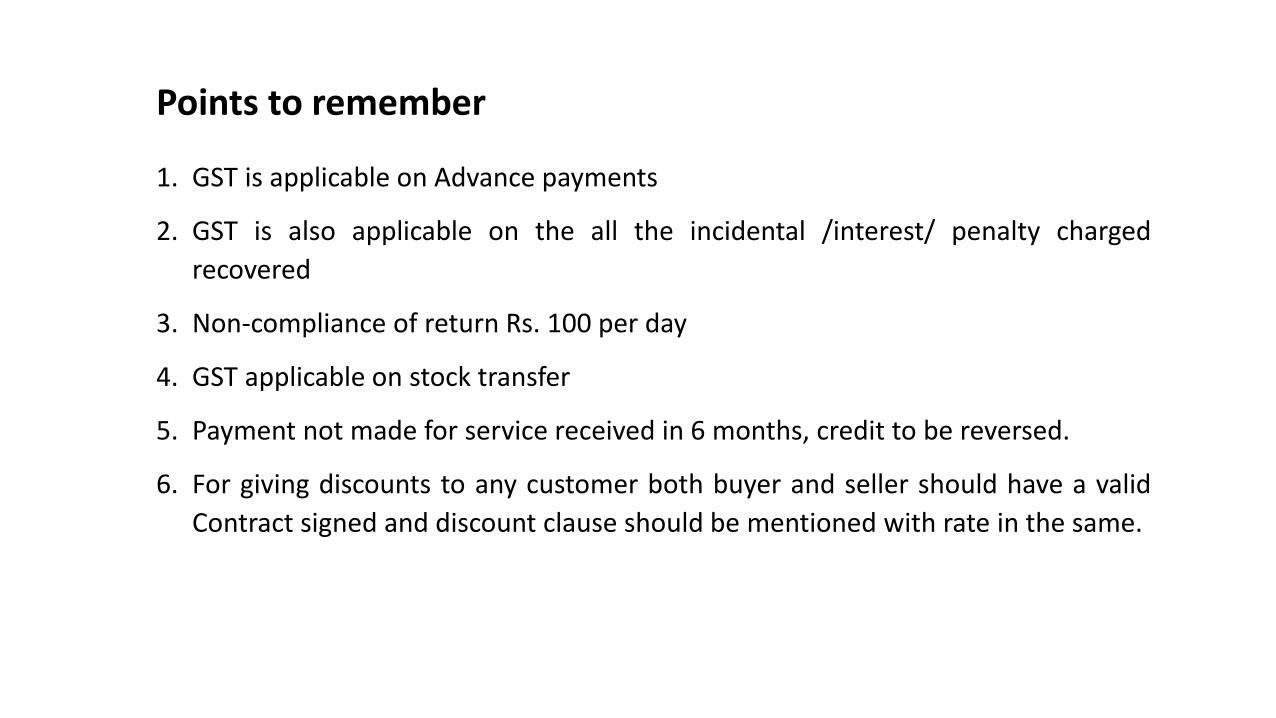

Points to remember

1. GST is applicable on Advance payments

2. GST is also applicable on the all the incidental /interest/ penalty charged

recovered

3. Non-compliance of return Rs. 100 per day

4. GST applicable on stock transfer

5. Payment not made for service received in 6 months, credit to be reversed.

6. For giving discounts to any customer both buyer and seller should have a valid

Contract signed and discount clause should be mentioned with rate in the same.

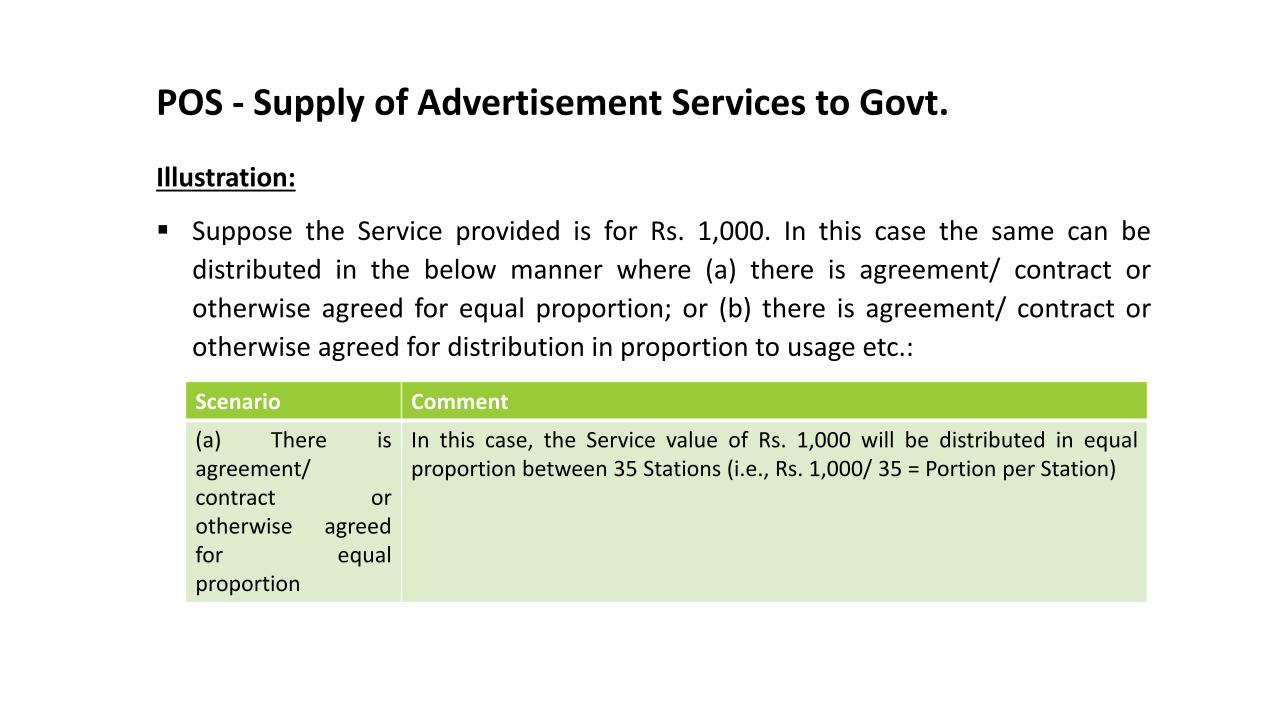

POS - Supply of Advertisement Services to Govt.

The Place of Supply for:

▪ The advertisement services provided to the Central Government, a State

Government, a statutory body or a local authority

▪ Identified in the contract or agreement

▪ Shall be distributed in proportion to the amount attributable to services

provided in the respective States or Union territories in the below manner:

➢ As determined in terms of the contract or agreement entered into in this

regard; or

➢ On such other basis as may be prescribed/ agreed (where no such contract

or agreement is available).

POS - Supply of Advertisement Services to Govt.

Illustration:

▪ Suppose the Service provided is for Rs. 1,000. In this case the same can be

distributed in the below manner where (a) there is agreement/ contract or

otherwise agreed for equal proportion; or (b) there is agreement/ contract or

otherwise agreed for distribution in proportion to usage etc.:

Scenario Comment

(a) There isagreement/contract orotherwise agreedfor equalproportion

In this case, the Service value of Rs. 1,000 will be distributed in equalproportion between 35 Stations (i.e., Rs. 1,000/ 35 = Portion per Station)

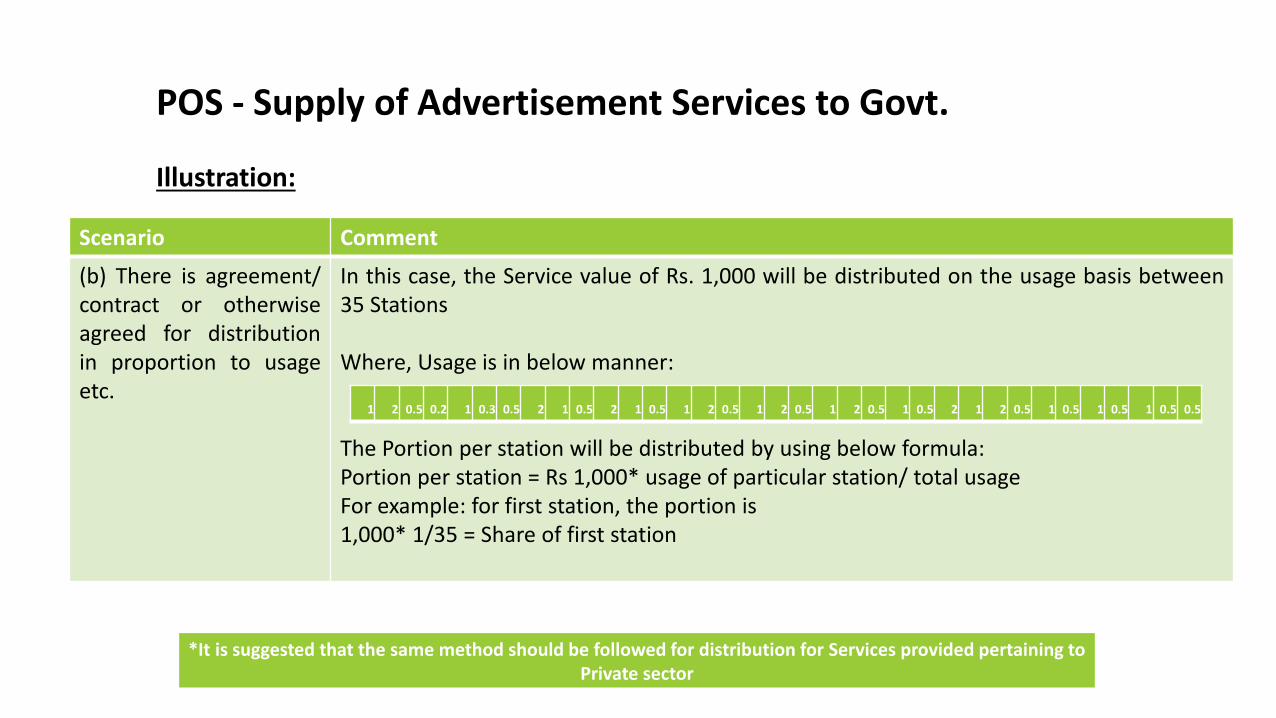

POS - Supply of Advertisement Services to Govt.

Illustration:

Scenario Comment

(b) There is agreement/contract or otherwiseagreed for distributionin proportion to usageetc.

In this case, the Service value of Rs. 1,000 will be distributed on the usage basis between35 Stations

Where, Usage is in below manner:

The Portion per station will be distributed by using below formula:Portion per station = Rs 1,000* usage of particular station/ total usageFor example: for first station, the portion is1,000* 1/35 = Share of first station

1 2 0.5 0.2 1 0.3 0.5 2 1 0.5 2 1 0.5 1 2 0.5 1 2 0.5 1 2 0.5 1 0.5 2 1 2 0.5 1 0.5 1 0.5 1 0.5 0.5

*It is suggested that the same method should be followed for distribution for Services provided pertaining to Private sector

PB – Site Link for all GST related important documents

http://prasarbharati.gov.in/Information/Pages/FINANCEWING.aspx

PB – Site Link for all GST related important documents

▪ Service Contract Value = Rs. 100

▪ Advance received = Rs. 50 (suppose on August 2017)

Here, on advance received, the PB has to raise the receipt voucher for the Rs. 50 mentioningthe taxes as applicable and have to pay and disclose the same in the return for the saidperiod.

▪ Further, the Service provided in September 2017, then the Tax invoice has to be raised for Rs.100 and the tax on the remaining amount i.e., Rs. 50 has to be paid and Rs. 100 has to bedisclosed in the return (adjusting the above mentioned Rs. 50).

Thank You!!!For any queries please contact

D C G & Co, Chartered Accountants

CA Mohit Goyal and CA Deepak Arora

Email: [email protected], [email protected]

Ph-011-45874445, 9810093722, 9971436858, 8586986166