perception of card users towards...

TRANSCRIPT

PERCEPTION OF CARD USERS TOWARDS

PLASTIC MONEY

This chapter analyses the perception of card holders towards plastic money in

India. The emphasis has been laid on the adoption, usage, value attributes, bottlenecks

and factors influencing plastic money adoption. The previous chapter surveyed the

current scenario on legal and regulatory frame work in India and it was found that

though more reforms have to be initiated. The current system is able to support the

smooth adoption and monitoring payments through plastic money. Also, it has been

indicated by the recent research that plastic money adoption is on the rise as there is an

increasing number of merchant establishments in India accepting majority of cards. The

current analysis has been divided into seven sections which include perceptional

analysis age-wise, occupation-wise, gender-wise, education wise, income-wise, analysis

of antecedents and spending pattern, and lastly analysis of perceived risk and utility.

5.1 Usage of Plastic Money

The objective of this question was to observe the type of plastic money used by

various respondents, so that the importance of a particular type of plastic money could

be judged. Whether the plastic money used has any relation with age, gender, income,

occupation, and educational level or not , the following analysis was done:

5.1.1 Usage of Plastic Money (Age –wise)

Age-wise, the card users have been considered vital in evaluating perception of

people at their different ages in relation to adoption of plastic money. Many researches

show that age is significantly related to the adoption of plastic money. This research has

sought to find out whether age-wise analysis brings out different perspectives from

other dimensions like gender wise, income wise, occupation-wise and education-wise.

Card users were asked to indicate the type of card they have used. Since the

other types of cards were not so popular during pilot study, only credit and debit cards

represent plastic money. Table 5.1.1 indicates the result of plastic money usage (Age-

wise) in India.

Perception of Card Holders towards Plastic Money

98

Table 5.1.1: Usage of Plastic Money (Age – wise)

Variable 18-30 years 31-45 years 46 years and above Total

Debit card 37

(50)

72

(33)

4

(5.4)

74

(25.34)

Credit card 72

(33)

108

(49.5)

38

(17.4)

218

(74.65)

Total 109

(37.3)

141

(48.3)

42

(14.4)

292

(100)

χχχχ2=10.09, df= 2 , t- value at 5% = 5.99

Note: Number in parenthesis show percentages

The table above shows that majority of users have credit cards (218 respondents)

while 74 respondents reported that they possess debit cards. The age-wise analysis

indicates that out of the total respondents with credit cards majority (49.5%) were

young middle aged (31-45 years) followed by younger users with less than 30 years.

The aged respondents (17.4%) indicated that they are using credit cards. This may be

perhaps due to lack of proper awareness or customer ignorance about change in

technology or may be they are cash conservatives. Further, the result shows that

majority (50%) of debit cards holders were less than 30 years of age, followed by the

young middle aged (44.6%), only 5% of aged people adopted debit card.

The chi-square value of responses from the age perspective on the usage of

plastic money is significant at 5 % level of significance. Hence, there is a strong

association between the age and utility derived from plastic money usage. Thus, age is

the important variable to enhance the usage of plastic money.

5.1.2 Usage of Plastic Money (Gender-wise)

Gender wise opinions reveal what exactly is existing between male and female

card users and what they perceive about plastic money. This section will try to analyse

the card users’ perception gender wise.

The result indicated that the majority of respondents (77.4%) were male and

female respondents comprised only 22.6 %.

Perception of Card Holders towards Plastic Money

99

Table 5.1.2 Usage of Plastic Money (Gender -wise)

Variable Male Female Total

Debit card 51

(68.9)

14

(31.1) 74

(25.34)

Credit card 175

(80.3)

43

(19.7) 218

(74.65)

Total 226

(77.4)

66

(22.6)

292

(100)

χχχχ2=4.07, df= 2, t-value at 5% = 5.99

Note: Number in parenthesis show percentages

Table 5.1.2 indicates that out of the respondents who indicated to have adopted

credit cards, 80.3% were male and only 19.7% were female. Also, 68.9% of debit card

adopters were male and 31.1% of the debit card adopters were females. This indicates

that male respondents use and adopt more plastic cards than their counterparts.

Chi-square value of responses from the gender perspective on the usage of

plastic money is insignificant at 5% level of significance. Hence, given the weak

association between gender and utility derived from plastic money usage, this variable

is independent in nature.

5.1.3 Usage of Plastic Money (Income wise)

From the income perspective, interesting result was also noticed. Table 5.1.3

revealed that out of all users surveyed, majority (54.5%) belong to the class of people

who earn a monthly income of Rs. 20,001-60,000, followed by the income class of upto

Rs. 20,000. Those who belong to a higher income class were only 2.7%. This can be

interpreted that the higher income class do not use plastic cards or did not reveal their

true range of monthly income. Further, the result shows that out of those who use debit

card, 44.6% belong to income of Rs. 20,001-60,000 while the minority were high class

earners above Rs. 100,000 per month. Also, 43.2% of the respondents who use debit

cards earns upto Rs. 20,000.

Table 5.1.3 Usage of plastic money (Income wise)

Variable Up to

Rs.20000

20001-60000 60001-

100000

Above

Rs.100000

Total

Debit card 32

(43.2)

33

(44.6)

8

(10.8)

1

(1.40) 74

(25.34)

Credit card 43

(19.7)

126

(57.8)

42

(19.3)

7

(3.2) 218

(74.65)

Total 75

(25.70)

159

(54.50)

50

(17.10)

8

(2.70)

292

(100)

χχχχ2=16.67, df= 3, t-value at 5% = 7.81

Note: Number in parenthesis show percentages

Perception of Card Holders towards Plastic Money

100

The respondents who indicated that they are using credit cards, majority of them

earn between Rs. 20,001-60,000 per month, followed by those who earn upto Rs.

20,000 and from Rs. 60,000 to Rs. 100,000 per month. Minority were the higher class

earners (above Rs. 100,000). This might be because norms for providing credit cards are

tough for small income earners. In many institutions, they prefer offering credit cards to

heavy pocketed clients than light pocketed clients. This tradition has hindered many

clients especially those who belong to small and medium income class. The result

indicates that higher class of income gainers prefer credit card to debit card. With the

increase in income level, the ratio of credit card to debit card is increasing. The chi-

square value of responses income-wise for the usage of plastic money is significant at

5% level of significance. Hence, plastic money is affected by the income level of

respondents.

5.1.4 Usage of Plastic money (Education wise)

Education of cards users is vital parameter. This analysis sought to find out if

there exists any disparity of card users’ perception from the perspective of educational

qualification of the users. It was evident from the result that majority (50.7%) of the

respondents were well learned with post graduate qualification, followed by graduates

and others with 3.8% respectively. This indicates that those who have adopted cards are

well qualified and the people without good educational qualification seems to be

reluctant to use plastic money.

Table 5.1.4 Usage of plastic money (Education -wise)

Variable Graduate Post Graduate Any Other Total

Debit card 41

(55.4)

29

(39.2)

4

(5.4) 74

(25.34)

Credit card 92

(42.2)

119

(54.6)

7

(3.2) 218

(74.65)

Total 133

(45.5)

148

(50.7)

11

(3.8)

292

(100)

χχχχ2=5.41, df= 2, t- value at 5% = 5.99

Note: Number in parenthesis show percentages

Table 5.1.4 shows that the majority of respondents surveyed use credit cards.

Among them, 54.6% are post graduates, 42.2% are graduates and 3.2% belong to other

Perception of Card Holders towards Plastic Money

101

class. Also, among those who reported that they have adopted debit cards, 55.4% were

just graduates and 39.2% were post graduates. These results show that only those

people with good educational background sought to adopt more credit cards as

compared to debit cards. This may be easy for the highly qualified people to manage

their funds more wisely as compared to other groups. The chi-square value of

responses from the education perspective is insignificant at 5% level of significance. It

can be concluded that usage of plastic money is not affected by the educational

qualification of the respondents rather it is dependent upon some other variable.

5.1.5 Usage of Plastic money (Occupation- wise)

This section analyses the perceptions of plastic card users on the basis of their

occupation. This perspective reveals that majority of respondents, (61.3%) were

services class people, 23.6% were professionals and 15% were business people. This

indicates that mostly the service class people prefer using cards than business class

people.

Table 5.1.5 Usage of plastic money (occupation -wise)

Variable Business Service class Professional Total

Debit card 3

(4.1)

52

(70.3)

19

(25.7) 74

(25.34)

Credit card 41

(18.8)

127

(58.3)

50

(22.9) 218

(74.65)

Total 44

(15.1)

179

(61.3)

69

(23.6)

292

(100)

χχχχ2=9.46, df= 2, t- value at 5% =5.99

Note: Number in parenthesis show percentages

Table 5.1.5 indicates that majority (74.65%) of the respondents have credit

cards. Out of them, 58.3% were service people, 22.9% were professional and 18.8%

were business people. Among those who were debit card holders, 70.3% were

servicemen, 25.7% professional and 4.1% business people. This shows that service

class people are in majority of card users, followed by professionals. Businessmen don’t

prefer using cards in payments. Chi-square value of responses for the usage of plastic

money from the occupation perspective is significant at 5% level of significance. This

Perception of Card Holders towards Plastic Money

102

shows that the occupation affects the usage pattern of respondent as different

occupational groups use the plastic money in their own way.

From the above analysis, it can be concluded that plastic money usage is

affected by age, occupation and income level which indicates that these variables are

not independent but dependent whereas gender and educational qualification has no

relation with the usage of plastic money as these variables are independent.

5.2 Number of Cards Held by Users

Plastic card users have the tendency of using more than one card. This behaviour

comes about due to the demand for service satisfaction from card providers, and the

dissimilar services provided. The card users were asked to indicate the number of cards

held by them. This section will analyses the number of cards held with customers on

different parameters.

5.2.1 Numbers of cards held by users ( Age - wise)

The opinion from age wise may reveal what actually utility perceived by

different age group from the number of cards they hold

Table 5.2.1 Number of Card held (Age- Wise)

Variable 18-30 years 31-45 years 46 years and above Total

1 Card 32

(60.40)

17

(32.1)

4

(7.5) 53

(18.15)

2-3 Cards 61

(36.10

85

(50.3)

23

(13.6) 169

(57.87)

4-5 Card 14

(25)

23

(13.6)

10

(17.9) 56

(19.17)

>5 Card 2

(14.30)

169

(57.87)

5

(35.7) 14

(4.79)

Total 109

(37.30)

141

(48.3)

42

(14.4)

292

(100)

χχχχ2=22.52, df= 6, t-value at 5% = 12.6

Note: Number in parenthesis show percentages

Table 5.2.1 shows that majority of the respondents (57.87%) have 2-3 cards,

followed by the second lot (19.17%) with 4-5 cards. It was indicated that only 4.79%

possess more than five cards which belong to different institutions. For those who

reported to have 2-3 cards, majority (50.3%) were of the age between 31-45, followed

by younger (less than 30 years) lot with 36.10%. The respondents who reported that

Perception of Card Holders towards Plastic Money

103

they had only one card, majority of them belonged to young category (less than 30 years

of age). Also, minority was the older people with the age of over 45 years. The table

further shows that the respondents who indicated that they possess 4-5 cards and above

5 cards majority were of the age 31-45 years (57.1% and 50% respectively). 25% of the

respondents from the age of less than 30 years and 17.9% more than 46 years said that

they possess 4-5 cards whereas 14.30% and 35.7% of the respondents said that they

possess more than five cards out the total 14 respondents from this category. The chi-

square value of responses from age-wise for the holding of number of card is significant

at 5% level of significance. It can be concluded from the above analysis that there is a

strong association between age and number of cards held by respondents. The co-

relation value is positively correlated with the given attributes shows, with the age the

possession of cards has been increased as majority of the respondents are the young

middle aged people.

5.2.2 Numbers of cards held by users (Gender- wise)

This section will try to analyse the number of cards held by users gender wise.

The opinion from gender wise reveals from what number of cards they receive the

utility.

Table 5.2.2 Numbers of Cards held (Gender- Wise)

Variable Male Female Total

1 card 34

(64.2)

19

(35.8) 53

(18.15)

2-3 cards 127

(75.1)

42

(24.9) 169

(57.87)

4-5 cards 51

(91.1)

5

(8.9) 56

(19.17)

75 cards 14

(100)

-

- 14

(4.79)

Total 226

(77.4)

66

(22.6)

292

(100)

χχχχ2=15.88, df= 3, t-value at 5% = 7.81

Note: Number in parenthesis show percentages

Table 5.2.2 shows the result regarding the number of cards held by users on

gender basis. It was clear that out of the majority of males and females respondents

(57.87%) who reported that have 2-3 cards, 75.1% were male respondents and 24.9%

were female. Among those who said that they prefer using only one card, 64.2% were

Perception of Card Holders towards Plastic Money

104

male and only 35.8% were female. It was interesting that only male respondents were

having more than 5 cards in possession. However, it was not clear whether they use all

of them or not.

19.17% of the male and female respondents reported to have 4-5 cards. Among

those who possess 4-5 cards, 91.1% were males and 8.9% were females. This can be

interpreted that female rarely possess or use plastic money as the possession of plastic

cards is dominated by males. The chi-square value of responses from gender-wise for

the holding of cards is significant at 5% level of significance. Hence, there is an

association between gender and number of cards held with users. Therefore, it is

concluded from the analysis that the possession of plastic money is dominated by males

as compared to females.

5.2.3 Numbers of cards held by users (Income-Wise)

The opinion from income-wise may reveal what actually utility perceived by

different income group from the number of cards they hold. Table 5.2.3 indicates that

out of the total respondents who reported to be possess 2-3 cards, majority (59.2%)

belonged to the class of users who receive a monthly income between Rs. 20,001-

60,000, 23.1% belonged to upto Rs. 20,000 per month. Also, 2.4% of those who possess

2-3 cards were high income gainers (above Rs. 100,000). Among the respondents who

posses only one card, the income of majority of them was less than Rs. 20,000 followed

by income between Rs. 20,001-60,000. This indicates that the users of cards are mostly

low income class.

Table 5.2.3 Number of cards held (Income- Wise)

Variable Up to

Rs.20000

20001-60000 60001-

100000

Above

Rs.100000

Total

1 Card 28

(52.8)

21

(39.6)

1

(1.9)

3

(5.70) 53

(18.15)

2-3 Cards 39

(23.1)

100

(59.2)

26

(15.4)

4

(2.4) 169

(57.87)

4-5 Cards 7

(12.5)

32

(57.10)

16

(28.6)

1

(1.8) 56

(19.17)

More than 5

Cards

1

(7.1)

6

(42.9)

7

(50)

- 14

(4.79)

Total 75

(25.70)

159

(54.50)

50

(17.10)

8

(2.70)

292

(100)

χχχχ2=47.48, df= 9, t-value at 5% = 16.9

Note: Number in parenthesis show percentages

Perception of Card Holders towards Plastic Money

105

The table further shows that the users who possess more than 5 cards belonged

to high income (Rs. 60,001-100,000). This indicates that the plastic card is a symbol

status to the higher class people. The result also shows that among those who indicated

that they possess 4-5 cards, majority of them (85.7%) earn Rs. 20,001-60,000. The chi-

square value of responses from the income-perspective of users for the number of cards

they hold is positively and significantly associated with it. This shows that with the

increase in income of respondents, there is a tendency to hold more number of cards.

5.2.4 Number of cards held by users (Education- Wise)

This section analyses the perception of cardholders from education perspective

for the number of cards they hold. In this section users were asked to report the number

of cards held by them. Table 5.2.4 shows that majority (57.87%) of the respondents said

that they possess 2-3 plastic cards and among them 49.7% were post graduates, 45.6%

were graduates and only 4.7% did not specify their qualification. Among those who

reported that they possess only one card, 58.5% were graduates and 41.5% were post

graduates. 19.17% of those who said they possess 4-5 cards 55.4% were post graduates

and 39.3% were graduates.

Table 5.2.4 Number of cards held (Education-Wise)

Variable Graduate Post Graduate Any Other Total

1 card 31

(58.5)

2

(41.5)

- 53

(18.15)

2-3 cards 77

(45.6)

84

(49.7)

8

(4.7) 169

(57.87)

4-5 cards 22

(39.3)

31

(55.4)

3

(5.4) 56

(19.17)

>5 cards 3

(21.4)

11

(78.6)

- 14

(4.79)

Total 133

(45.5)

148

(50.7)

11

(3.8)

292

(100)

χχχχ2=10.84, df= 6, t- value at 5% = 12.6

Note: Number in parenthesis show percentages

The table further shows that there were respondents who said that they have

more than 5 cards and among them 78.6% were post graduates and 21.4% were

graduates.. The value of chi-square of responses from the education perspective for the

holding of cards is insignificant at 5% level of significance. This shows that holding of

Perception of Card Holders towards Plastic Money

106

more number of cards is not dependent upon the education of the users. Hence, we can

say good qualification does not leads to holding of more cards.

5.2.5 Number of Cards Held by users (occupation- wise)

The occupation wise category of card holders indicated that that some possess

more than one card.

Table 5.2.5 Number of cards held (occupation- Wise)

Variable Business Service class Professional Total

1 Card 5

(9.4)

32

(60.4)

16

(30.2) 53

(18.15)

2-3 Cards 25

(14.8)

107

(63.3)

37

(21.9) 169

(57.87)

4-5 Cards 13

(23.2)

31

(55.4)

12

(21.4) 56

(19.17)

More than 5

Cards

1

(7.1)

9

(64.3)

4

(28.6) 14

(4.79)

Total 44

(15.1)

179

(61.3)

69

(23.6)

292

(100)

χχχχ2=6.07, df= 6,t-value at 5% = 12.6

Note: Number in parenthesis show percentages

Table 5.2.5 indicates that out of total number of respondents, majority possess 2-

3 cards and from them 63.3% were service class and 21.9% were professionals. Further,

the table shows that out of those who reported to possess only one card, majority were

service class, followed by (30.2%) professionals and (9.4%) business people. Some

respondents also said that they possess more than 5 cards of which majority were from

service class. The chi-square value is insignificant at 5% level of significance which

means there is no association between occupation and the possession of cards by

respondents as these variables are independent.

The above analysis shows that age, gender and income level affect the number

of cards held by users whereas occupational level and educational level does not seem

to affect the number of cards in the possession of users.

5.3 Utility of Plastic Money

The demand for plastic money is accelerated by the utility perceived by the

users. This study attempted to get the perceived utility of plastic money which leads to

Perception of Card Holders towards Plastic Money

107

the need of cards adoption. The aim of this section was to observe to what extent, users

perceived the utility from plastic money. The analysis was done keeping in mind

different parameters, which are as follow:

5.3.1 Utility of Plastic Money (Age – wise)

This section will analyse the perceived utility of plastic money from different

categories. From the age perspective, out of the total sample surveyed, 51.7 % of the

respondents indicated that plastic money is essential, 30.13% reportedly indicated that

plastic money is vital as shown in Table 5.3.1. Also 1.36% and 68% respectively said

that it is a waste of resources or they cannot say exactly.

Table 5.3.1 Utility of Plastic Money (Age –wise)

Variable 18-30 years 31-45 years 46 years and above Total

Vital 29

(33)

47

(13.6)

12

(13.6) 88

(30.13)

Essential 60

(39.7)

68

(45)

23

(15.2) 151

(51.7)

Desirable 16

(34)

24

(51.1)

7

(14.9) 47

(16.09)

A Waste of

resource

2

(50)

2

(50)

- 4

(1.36)

Can’t say

exactly

2

(100) - - 2

(.68)

Total 109

(37.3)

141

(48.3)

42.

(14.4)

292

(100)

χχχχ2=5.93, df= 8, t-value at 5% = 15.5

Note: Number in parenthesis show percentages

Out of the 151 respondents (51.7%) who said plastic money is essential,

majority of them (45%) were between 31-45 years of age, 39.7% were less than 30

years of age and 15.2% were over 46 years. Further, it was indicated that among those

who said plastic money is vital, majority 53.4% were of the age between 31-45 years,

followed by 33% at the age of less than 30 years. For the respondents who said that

plastic money is desirable, majority (51.1%) were between the age of 31-45, followed

by those who were at the age of less than 30 years and lastly, 14.9% indicated that they

were at the age of above 46 years. 2 respondents were unable to say exactly about the

utility of plastic money. Inferential statistics shows that age has insignificant

relationship with the perception of users at 5% level of significance. It can be concluded

Perception of Card Holders towards Plastic Money

108

from above analysis that young users derived more utility from plastic money as

compared to aged people.

5.3.2 Utility of Plastic Money (Gender – wise)

From gender perspective, the respondents were asked to indicate as to what

extent they perceived the utility from plastic money. The result is presented in table no

5.3.2.the result indicates that among the majority (51.7%) of respondents who reported

that plastic money is essential, 78.1% were males and 21.9% were females. 30.13%

who reported that plastic money is vital, 73.9% were males and 26.1% were females.

Table 5.3.2 Utility of plastic money (Gender – wise)

Variable Male Female Total

Vital 65

(73.9)

23

(26.1) 88

(30.13)

Essential 118

(78.1)

33

(21.9) 151

(51.7)

Desirable 39

(83)

8

(17) 47

(16.09)

A waste of resources 3

(75)

1

(25) 4

(1.36)

Can’t say exactly 1

(50)

1

(50) 2

(.68)

Total (226)

(77.4)

(66)

(22.6)

292

(100)

χχχχ2=2.39, df= 4, t-value at 5% = 9.49

Note: Number in parenthesis show percentages

This shows also that male respondents consider plastic money to be vital. This

may be because of the reason that they are involved in many situations where payments

are needed.

Further, it clear that 16.09% who said that plastic money is desirable, 83% were

males and 17% females. Among those who reportedly said that it is a waste of money,

75.0% were male and 25% were female. However, 2 respondents were unable to

express their value attitude towards plastic money. The chi-square value of responses on

the utility of plastic money for the gender wise is insignificant at 5% level of

significance. It shows both males and females do not differentiate between the utility

derived from plastic money although the possession is dominated by the males as

compared to females.

Perception of Card Holders towards Plastic Money

109

5.3.3 Utility of Plastic Money (Income-wise)

Respondents were asked to indicate whether plastic money is vital, essential,

and desirable or a waste of resources. From income perspective, table 5.3.3 shows the

result.

Table 5.3.3 Utility of plastic money (Income-wise)

Variable Upto

Rs.20000

20001-

60000

60001-

100000

Above

Rs.100000

Total

Vital 15

(17)

53

(60.2)

20

(22.7)

- 88

(30.13)

Essential 41

(27.2)

84

(55.6)

21

(13.9)

5

(3.3) 151

(51.7)

Desirable 15

(31.9)

20

(42.6)

9

(19.1)

3

(6.4) 47

(16.09)

A Waste of

resources

3

(75)

1

(25)

- - 4

(1.36)

Can’t say

exactly

1

(50)

1

(50)

- - 2

(.68)

Total 75

(25.70)

159

(54.50)

50

(17.10)

8

(2.70)

292

(100)

χχχχ2=18.78, df= 12, t-value at 5% = 21.0

Note: Number in parenthesis show percentages

Those respondents who reported that plastic money is essential, 55.6% earns

between Rs. 20,001-60,000, 27.2% earn less than Rs. 20,000 and 13.9% earn Rs.

60,001-100,000. Further, the result indicated that among those who said that plastic

money is vital, 60% earn Rs. 20,001-60,000, 22.7% earn Rs. 60,001-1,00,000 and 17%

earn less then Rs. 20,000. 16.09% of those who said that it is desirable, 42.6% belonged

to the class of people who earn Rs. 20,001-60,000, 19.1% earn Rs. 60,001-100,000 and

31.9% earn less than Rs. 20,000. Only four respondents said that it is a waste of

resources and majority were those who earn less than Rs. 20,000. The chi-square value

of responses on the utility derived from plastic money is insignificant at 5% level of

significance from the income perspective. It can be concluded that higher income group

does not receive more utility as compared to other lower income group, rather income

was observed and does not seem to affect the utility value of plastic money.

Perception of Card Holders towards Plastic Money

110

5.3.4 Utility of Plastic Money (Education-wise)

The responses from the users on the basis of their educational level reported

whether plastic money adoption is vital, essential, desirable, or a waste of resources.

Table 5.3.4 Utility of plastic money (Education-wise)

Variable Graduate Post Graduate Any Other Total

Vital 39

(44.3)

46

(52.3)

3

(3.40)

88

(30.13)

Essential 66

(43.7)

79

(52.3)

6

(4)

151

(51.7)

Desirable 24

(51.1)

21

(44.7)

2

(4.3)

47

(16.09)

A waste of

resources

3

(75)

1

(25)

- 4

(1.36)

Can’t say

exactly

1

(50)

1

(50)

- 2

(.68)

Total 133

(45.5)

148

(50.7)

11

(3.8)

292

(100)

χχχχ2=2.51, df= 8, t- value at 5% = 15.5

Note: Number in parenthesis show percentages

Table 5.3.4 shows that majority of the respondents reported that plastic money

adoption was essential. Among those who said so, 52.3% were post graduates and

43.7% were graduates. Out of those who said that plastic money adoption is vital,

44.3% were graduates and 52.3% were post graduates. Only 3.40% belong to other

class which did not specify their educational qualification. For those who said that

plastic money is desirable, 51.1% were graduates, 44.7% were post graduates and only

4.3% did not specify their qualification. Some respondents also said that it is a waste of

resources, of which 3 respondents were graduates and 1 respondent was post graduate.

This result shows that plastic money is perceived to be essential and should be adopted

as it provides useful services which replaces the conventional way of making purchases

and payment. Inferential statistics shows there is no association between educational

qualification and customers perceptions at 5 percent level of significance. It shows that

Perception of Card Holders towards Plastic Money

111

utility derived from plastic money is not dependent upon the educational qualification

rather it is influenced by some other variable.

5.3.5 Utility of Plastic Money (Occupation-wise)

Utility of plastic money is different for various occupational group. In this

section, the extent of utility is derived from plastic money is analyzed from different

occupational groups. The result are shown on table no.5.3.5

Table 5.3.5 Utility of plastic money (Occupation-wise)

Variable Business Service class Professional Total

Vital 19

(21.6)

47

(53.4)

22

(25) 88

(30.13)

Essential 19

(12.6)

92

(60.9)

40

(26.5) 151

(51.7)

Desirable 6

(12.8)

35

(74.5)

6

(12.8) 47

(16.09)

A Waste of

resources

- 3

(75)

1

(25) 4

(1.36)

Can’t say

exactly

- 2

(100)

- 2

(.68)

Total 44

(15.1)

179

(61.3)

69

(23.6)

292

(100)

χχχχ2=10.43, df= 8, t-value at 5% = 15.5

Note: Number in parenthesis show percentages

Table 5.3.5 shows that majority (51.7%) of the respondents said that plastic

money is essential. Among those who supported this intensity, 60.9% were service

people, 26.5% were professionals and 12.6% were business people. Among those who

said that plastic money is vital, 53.4% were service people, 21.6% of each were

businessmen and 25% professional. Only six respondents said they either can’t say or it

is a waste of resources.

The chi-square value of responses for the utility of plastic money on

occupational basis is insignificant at 5% level of significance. It can be concluded from

the above analysis that occupation does not seem to affect the utility derived from the

usage of plastic money

From the study, it is revealed that none of variables (age, gender, occupation,

income and educational) has utility perceived from plastic money as all the variables are

independent in mature.

Perception of Card Holders towards Plastic Money

112

5.4 Frequency of Card Usage

Even though card users possess multiple cards, the way they use them is also

vital to the cards industry. Some respondents possess more than 2 cards but they don’t

use them frequently. Users were asked to indicate their frequency in using their cards to

know whether they are active cardholders or inactive one. This will help the card

providing firm to know if the increase in the number of cards actually do the work they

are adopted for. In the study since the number of inactive cardholders as per data

collection is 9 out of 292, which is very negligible, it is not found worth while to

differentiate between active and in active users for the present study. So, all the

respondents under study are active cardholders. Perhaps persons who rarely use the

card, may be only for withdrawals from ATM, comes in the category of inactive card

user. Secondly, because ATM withdrawals have become compulsion for salaried

peoples, who only use the card to withdraw their salaries. The active cardholders are

those who use card for purchasing of goods or services but not only withdrawal of

money through ATM.

5.4.1 Frequency of Card Usage (Age-wise)

Different age-group may have the different frequency for using their cards.

From the age perspective, the frequency of card usage is shown on table No. 5.4.1

Table 5.4.1 Frequency of Card usage (Age-wise)

Variable 18-30 years 31-45 years 46 years and above Total

Almost daily 15

(57.7)

9

(34.6)

2

(7.7) 26

(8.90)

6-10 times in month 30

(39.5)

36

(47.4)

10

(13.2) 76

(26.02)

3-5 times in month 36

(28.3)

69

(54.3)

22

(17.3) 127

(43.49)

1-2 time in month 21

(45.7)

21

(45.7)

4

(8.7) 46

(15.75)

Not more than once a

month

2

(25)

3

(37.5)

3

(37.5) 8

(2.74)

Rarely used 5

(55.6)

3

(33.3)

1

(11.1) 9

(3.08`)

Total 109

(37.3)

141

(48.3)

42

(14.4)

292

(100)

χχχχ2=16.19, df= 10 , t-value at 5% = 18.3

Note: Number in parenthesis show percentages

Perception of Card Holders towards Plastic Money

113

From table 5.4.1, it was indicated that majority (43.49%) of respondents use

their cards 3-5 times in a month, 26.02% use their cards at point of sale terminals 6-10

times in a month and 15.75% of respondents reported that they use their cards 1-2 times

a month. The high frequency of use will indicate that card user have placed their faith

and confidence in using plastic money. From age wise perspective, majority of the users

who said that they use their cards 3-5 times a month were 54.3% with the age of 31-45

years. Also 28.3% with the age of less than 30 years said that they use their cards 3-5

times a month. Further, from the table, it is indicated that among those who report that

they use their cards 6-10 times in a month, again majority were in age between 31-45

years, followed by 39.5% who were less than 30 years. The overall outlook suggests,

that more than 75% respondents reportedly indicated that they use their cards at least

five times a month. This shows that the trend is picking up. However, there is a need for

more to be done, for instance, taking the customers to confidence. The chi-square value

of responses for the frequency of card usage from the age perspective is insignificant at

5% level of significance. This shows that frequency of card usage is not affected by the

age factor but it is dependent upon some other policy variable which is needed to be

explored for the policy variable. .

5.4.2 Frequency of Card Usage (Gender-wise)

Gender wise analysis for the frequency of card usage depicts whether there

exists any disparity among the males and females for using the plastic money. The

result are presented in table no.5.4.2

Table 5.4.2 Frequency of card usage (Gender-wise)

Variable Male Female Total

Almost Daily 22

(84.6)

4

(15.4) 26

(8.9)

6-10 times in a month 61

(80.3)

15

(19.7) 76

(26.02)

3-5 times in a month 101

(79.5)

26

(20.5) 127

(43.49)

1-2 times in a month 33

(71.7)

13

(28.3) 46

(15.75)

Not more than once a month 7

(87.5)

1

(12.5) 8

(2.74)

Rarely used 2

(22.2)

7

(77.8) 9

(3.08)

Total 226

(77.4)

66

(22.6)

292

(100)

χχχχ2=18.43, df= 5, t- value at 5% = 11.1

Note: Number in parenthesis show percentages

Perception of Card Holders towards Plastic Money

114

From table 5.4.2, it was indicated that 8.9% respondents who reportedly said

that they use their cards daily, majority (84.6%) were male and 15.4% were females.

80.3% of the respondents who were male indicated that they use 6-10 times in a month

and the rest were female who said that they use their cards 6-10 times in a month.

15.75% of respondents who use 1-2 times a month, 71.7% were males and 28.3%

females. 43.49% of male and female both use plastic money 3-5 times in a month, but

again it is dominated by male as compared to their counter parts. Among those who said

that they rarely use their cards, 77.8% were females and 22.2% were males. From this

result, it is clearly indicated that female respondents don’t use their cards in spending

which may be because either they are not involved in spending procedures or they don’t

like spending by using plastic money. The chi-square value of responses for the

frequency of card usage on the gender basis is significant at 5% level of significance.

Hence, gender has the association with the frequency usage of plastic money. It is clear

from the analysis that male respondents are more involved in spending with card as

compared to their counterparts.

5.4.3 Frequency of Card Usage (Income-wise)

The researcher sought to know from different income groups their frequency for

using the plastic money. From income perspective, the result for frequency of card

usage is shown on table 5.4.3

Table 5.4.3 Frequency of card usage (Income-wise)

Variable Up to

Rs.20000

20001-60000 60001-100000 Above

Rs.100000

Total

Almost Daily 10

(38.5)

12

(46.2)

3

(11.5)

1

(3.8) 26

(8.9)

6-10 times a

month

16

(21.1)

41

(53.9)

17

(22.4)

2

(2.6) 76

(26.02)

3-5 times month 27

(21.3)

75

(59.1)

23

(18.1)

2

(1.6) 127

(43.49)

1-2 times a

month

16

(34.8)

26

(56.5)

2

(4.3)

2

(4.3) 46

(15.75)

Not more that a

month

2

(25)

1

(12.5)

5

(62.5)

- 8

(2.74)

Rarely used 4

(44.4)

4

(44.4)

- 1

(11.1) 9

(3.08)

Total 75

(25.70)

159

(54.50)

50

(17.10)

8

(2.70)

292

(100)

χχχχ2=30.60, df= 15, t- value at 5% = 25.0

Note: Number in parenthesis show percentages

Perception of Card Holders towards Plastic Money

115

The table shows that majority of the respondents using plastic money 3-5 times

in a month earn between Rs. 20,001-60,000. Also 18.1% of them earn Rs. 60,001-

100,000 and 21.3% earn less than Rs. 20,000. Further, 15.75% who use their cards one

to twice, among 56.5% earn between Rs. 20,001 to 60,000, 34.8% earn less than Rs.

20,000 and 4.3% earns above Rs. 100,000. 8.9% respondents reported that they use

their card almost daily. Among them, 38.5% earn less then Rs. 20,000, 46.2% earn

between Rs. 20,001-60,000 and 3.8% earn above Rs. 100,000. Those who said that they

use their cards once a month were only 8 respondents and among them majority earn

between Rs. 60,001-100,000.

The chi-square value of responses for the frequency of card usage on the income

basis is significant at 5% level of significance. So, there is a strong association between

income and frequency of card usage but they are negatively co-related to each other.

Hence, with the increase in income level does not mean usage frequency will also

increase. Rather it will decrease.

5.4.4 Frequency of card usage (Education-wise)

Education being the vital parameter. From this perspective, researcher sought to

know whether there is any disparity among the more educated then the less qualified

user. The result is shown in table 5.4.4

Table 5.4.4 Frequency of card usage (Education-wise)

Variable Graduate Post Graduate Any Other Total

Almost daily 12

(46.2)

13

(50)

1

(3.8)

26

(8.9)

6-10 times in a

month

30

(39.5)

41

(53.9)

5

(6.6)

76

(26.02)

3-5 times in a

month

52

(40.9)

71

(55.9)

4

(3.1)

127

(43.49)

1-2 times in a

month

28

(60.9)

18

(39.1)

- 46

(15.75)

Not more than

once a month

6

(75)

2

(25)

- 8

(2.74)

Rarely used 5

(55.6)

3

(33.3)

1

(11.1)

9

(3.08)

Total 133

(45.5)

148

(50.7)

11

(3.8)

292

(100)

χχχχ2=13.98, df= 10 , t- value at 5% = 18.3

Note: Number in parenthesis show percentages

Perception of Card Holders towards Plastic Money

116

Table 5.4.4 shows that majority of card users use them 3-5 times a month,

followed by those who use 6-10 times a month and then those who use their cards 1-2

times a month. Among 43.49% of who use 3-5 times a month, 55.9% were post

graduates and 40.9% of were graduates. Also, 26.02% of those who use their cards 6-10

times in a month, 53.9% were post graduates, 39.5% were graduates and 6.6% did not

specify their qualification. Further, the result revealed that 15.75% of those who said

that they use plastic money once to twice a month, 60.9% were graduates and 39.1%

were post graduates. Only 8 respondents said that they use it once a month and 9

respondents reported that they rarely use their cards. This indicates that still all card

users have not full trusted the use of plastic money. The chi-square value of responses

for the usage frequency on the educational basis is insignificant at 5% level of

significance. Hence, higher education has no relation with the usage frequency of cards

but it is dependent upon some other variable.

5.4.5 Frequency of Card usage (Occupation-wise)

Frequency of card usage is dependent upon the need of the user. Different

occupational group may have different frequency for using their card according to their

needs. Frequency for card usage on occupational wise is shown on table no.5.4.5. Study

reveals that the majority (43.49%) of the respondents use their cards 3-5 times a month.

Out of them, 62.2% were service people, 23.6% professionals and 14.2% were business

people. Among those who said that they use their cards almost daily, 65.4% were from

service class, 15.4% were professionals and 19.2% were business people.

Table 5.4.5 Frequency of card usage (Occupation-wise)

Variable Business Service class Professional Total

Almost Daily 5

(19.2)

17

(65.4)

7

(15.4) 26

(8.90)

6-10 time in a

month

8

(10.5)

47

(61.8)

21

(27.6) 76

(26.02)

3-5 time in a

month

18

(14.2)

79

(62.2)

30

(23.6) 127

(43.49)

1-2 time in a

month

13

(28.3)

27

(58.7)

6

(13) 46

(15.75)

Not more than

once month

- 7

(87.5)

1

(12.5) 8

(2.74)

Rarely used - 2

(22.2)

7

(77.8) 9

(3.08)

Total 44

(15.1)

179

(61.3)

69

(23.6)

292

(100)

χχχχ2=27.59, df= 10, t-value at 5% = 18.3

Note: Number in parenthesis show percentages

Perception of Card Holders towards Plastic Money

117

Further, the table reveals that 26.02% of the respondents who said that they use

their cards 6-10 times in a month, 61.8% were service people, 27.6% were professionals

and 10.5% were business class people. The result also shows that some respondents

(17) use once or rarely use their cards, among them were only servicemen and

professionals. Business class people who possess plastic money reported use of their

cards atleast once to twice a month. This is evident that service people are regular users

of plastic money, followed by professionals and then businessmen who prefer using

mostly other means of payment apart from plastic money. The chi-square value of

responses on the occupational basis for the frequency of card usage is significant at 5%

level of significance. Hence, it is also clear from the analysis usage frequency of service

class is more as compared to professional or business class people.

It is inferred from above analysis that frequency of card usage is being affected

by gender, income and occupational level. As the males counterparts are having more

cards than the female ones and they spend more by cards than the females whereas the

persons having fixed and regular income are likely to spend more on purchasing the

goods. The age and educational qualification does not seem to affect the frequency for

using the cards.

5.5 Monthly Spending on Cards

From this perspective, the actual amount spent will be important apart from the

frequency. The users may use the cards in purchasing small quantity of goods which

may become significant in spending. Customer trust on the card providers and brand

will determine the amount spent on the cards. This section will try to analyse the

monthly spending on cards from different perspective.

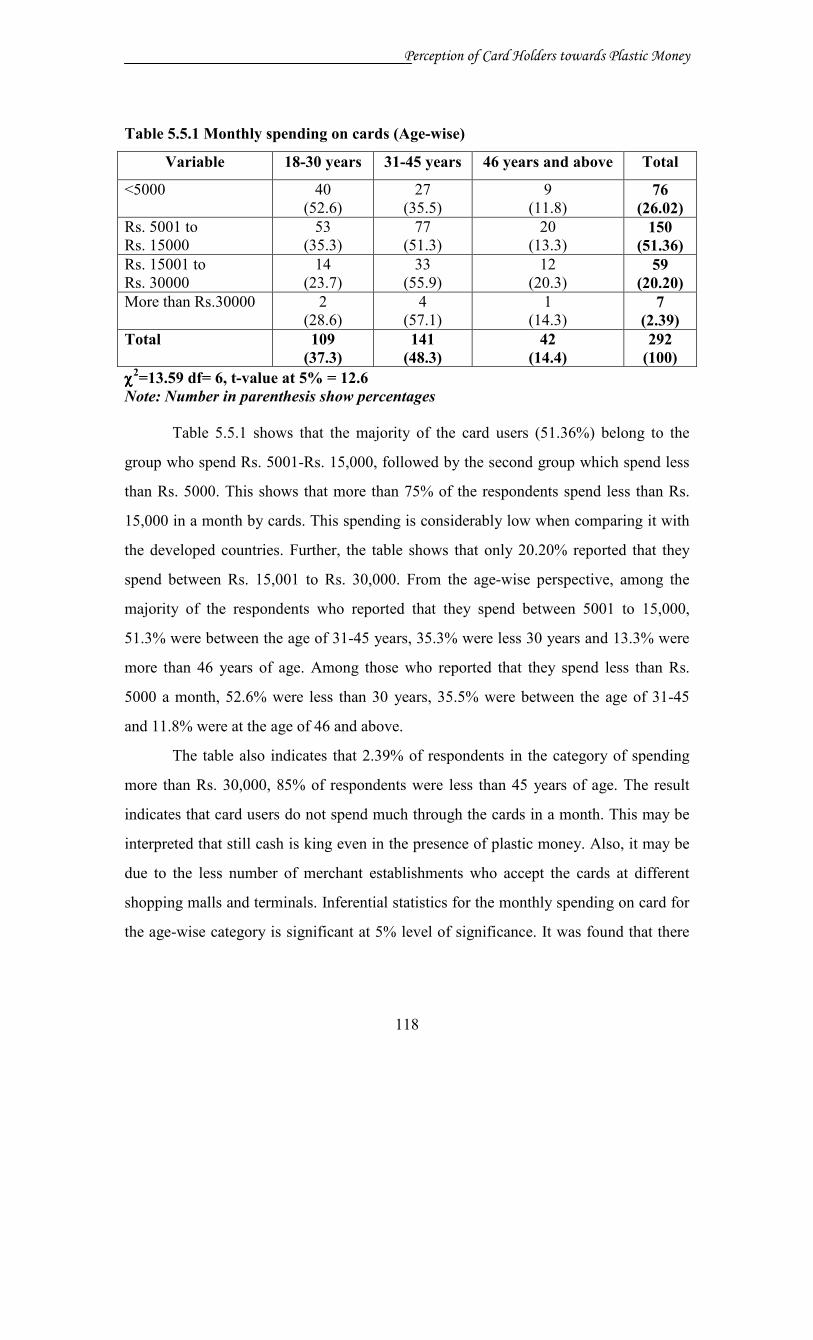

5.5.1 Monthly Spending on Cards (Age-wise)

This section analyses the monthly spending on card from the age perspective,

the result for monthly spending on card is shown Table No. 5.5.1

Perception of Card Holders towards Plastic Money

118

Table 5.5.1 Monthly spending on cards (Age-wise)

Variable 18-30 years 31-45 years 46 years and above Total

<5000 40

(52.6)

27

(35.5)

9

(11.8) 76

(26.02)

Rs. 5001 to

Rs. 15000

53

(35.3)

77

(51.3)

20

(13.3) 150

(51.36)

Rs. 15001 to

Rs. 30000

14

(23.7)

33

(55.9)

12

(20.3) 59

(20.20)

More than Rs.30000 2

(28.6)

4

(57.1)

1

(14.3) 7

(2.39)

Total 109

(37.3)

141

(48.3)

42

(14.4)

292

(100)

χχχχ2=13.59 df= 6, t-value at 5% = 12.6

Note: Number in parenthesis show percentages

Table 5.5.1 shows that the majority of the card users (51.36%) belong to the

group who spend Rs. 5001-Rs. 15,000, followed by the second group which spend less

than Rs. 5000. This shows that more than 75% of the respondents spend less than Rs.

15,000 in a month by cards. This spending is considerably low when comparing it with

the developed countries. Further, the table shows that only 20.20% reported that they

spend between Rs. 15,001 to Rs. 30,000. From the age-wise perspective, among the

majority of the respondents who reported that they spend between 5001 to 15,000,

51.3% were between the age of 31-45 years, 35.3% were less 30 years and 13.3% were

more than 46 years of age. Among those who reported that they spend less than Rs.

5000 a month, 52.6% were less than 30 years, 35.5% were between the age of 31-45

and 11.8% were at the age of 46 and above.

The table also indicates that 2.39% of respondents in the category of spending

more than Rs. 30,000, 85% of respondents were less than 45 years of age. The result

indicates that card users do not spend much through the cards in a month. This may be

interpreted that still cash is king even in the presence of plastic money. Also, it may be

due to the less number of merchant establishments who accept the cards at different

shopping malls and terminals. Inferential statistics for the monthly spending on card for

the age-wise category is significant at 5% level of significance. It was found that there

Perception of Card Holders towards Plastic Money

119

was an association between the age and monthly spending on card. Hence, majority of

young middle aged people spend more as compared to other groups.

5.5.2 Monthly Spending on Cards (Gender-wise)

When respondents were asked to indicate the amount spent in using cards,

majority (51.36%) indicated that they spend Rs. 5000 to 15,000 in a month. Among the

respondents who said this, 79.3% were males and 20.7% were females.

Table 5.5.2 Monthly spending on cards (Gender-wise)

Variable Male Female Total

<5000 55

(72.4)

21

(27.6) 76

(26.02)

Rs. 5000 to 15000 119

(79.3)

31

(20.7) 150

(51.36)

Rs. 15001 to 39000 47

(79.7)

12

(20.3) 59

(20.20)

More than Rs.

30000

5

(71.4)

2

(28.6) 7

(2.39)

Total 226

(77.4)

66

(22.6)

292

(100)

χχχχ2=1.74, df= 3, t- value at 5% = 7.81

Note: Number in parenthesis show percentages

Among 26.02% of the respondents who spend less than Rs. 5000 per month,

72.4% were males and 27.6% were females. The result also shows that 20.20% of the

respondents who spend between Rs. 15,000 to Rs. 30,000 ,79.7% were males and

20.3% were females. Few respondents said that they spend more than Rs. 30,000 a

month through plastic money and the majority who do this spending 71.4% were males.

The chi-square value of responses on the monthly spending on card from the gender

perspective is insignificant at 5% level of significance. It was found that there was a

weak association between the gender and monthly spending on card. It can be

concluded that there was no difference between the monthly spending on card by males

and females.

5.5.3 Monthly Spending on Cards (Income-wise)

Different income groups may have the different spending pattern. From income

perspective, monthly spending on card by different income group, the result is as

follow:

Perception of Card Holders towards Plastic Money

120

Table 5.5.3 Monthly spending on cards (Income-wise)

Variable Up to

Rs.20000

20001-60000 60001-

100000

Above

Rs.100000

Total

Rs. <5000 36

(47.4)

30

(39.5)

9

(11.8)

1

(1.3)

76

(26.02)

Rs. 5001-15000 34

(22.7)

96

(64)

15

(10)

5

(3.3)

150

(51.36)

15001-30000 5

(8.5)

29

(49.2)

24

(40.7)

1

(1.7)

59

(20.20)

> Rs. 30000 - 4

(57.1)

2

(28.6)

1

(14.3)

7

(2.39)

Total 75

(25.70)

159

(54.50)

50

(17.10)

8

(2.70)

292

(100)

χχχχ2=58.73, df= 9, t-value at 5% = 16.9

Note: Number in parenthesis show percentages

Table 5.5.3 shows how respondents spend using their cards. It was clear that out

of the total respondents, 51.36% spend between Rs. 5001-15,000, followed by those

who spend less than Rs. 5000 and then those who spend between Rs. 15001 to 30,000.

26.02% of those who spend less than Rs. 5000, majority of them earn less than Rs.

20,000, followed by those who earn between Rs. 20,001-60,000, Rs. 60,001 to 100,000

and lastly those who earn Rs. 100,000 and above. Also among those who spend

between Rs. 5000-15,000 majority (64.0%) were users who earn between Rs. 20,001-

60,000, followed by those who earn upto Rs. 20,000. 20.20% of those who spend

between Rs. 15,000 to Rs. 30,000, majority belong to the class of users who earn Rs.

20,001-60,000, followed by 40.7% who earn between Rs. 60,000-100,000 and 8.5%

were those who earn less then Rs. 20,000. Among the class of people who spend above

Rs. 30,000, majority were those who earn between Rs. 20,001 to less than Rs. 100,000.

The result shows that medium income earners spend between Rs. 5000-30,000 as low

income class don’t spend much using cards. The chi-square value of responses on the

monthly spending on card from income perspective is positively co-related and

significant at 5% level of significance which shows that with the increase in the income

level of users there is tendency to spend more from the card because of the strong

association between the given attributes.

Perception of Card Holders towards Plastic Money

121

5.5.4 Monthly Spending on Cards (Education- wise)

From education perspective, monthly spending on card usage is shown in table 5.5.4

Table 5.5.4 Monthly spending on cards (Education– wise)

Variable Graduate Post Graduate Any Other Total

Rs. <5000 50

(65.8)

24

(31.6)

2

(2.6) 76

(26.02)

Rs.5000 to

Rs. 15000

59

(39.3)

87

(58)

4

(2.7) 150

(51.36)

Rs. 15000 to

Rs. 30000

20

(33.9)

35

(59.3)

4

(6.8) 59

(20.20)

More than

Rs. 30000

4

(57.1)

2

(28.6)

1

(14.3) 7

(2.39)

Total 133

(45.5)

148

(50.7)

11

(3.8)

292

(100)

χχχχ2=22.89, df= 6, t- value at 5% =12.6

Note: Number in parenthesis show percentages

Table 5.5.4 indicates the spending pattern of different classes of card users who

possess different qualifications. The table reveals that majority (51.36%) of the

respondents spend between Rs. 5000 to Rs. 15000 and among them, 58% were post

graduates and 39.3% were graduates. Also, out of those who spend less than Rs. 5000,

65.8% were graduates, 31.6% were post graduates and 2.6% did not specify their

qualifications. Further, it is revealed that 59.3% of those who said that they spend

between Rs. 15000 to 30,000 were post graduates, 33.9% were graduates and 6.8% did

not specify their qualifications. This result confirms that majority of card users spend

less than Rs. 15000 a month and many of do not have confidence of spending much on

the cards. This perhaps might be due to the less number of traders accepting cards or

technical problems related to cards and branch restrictions on card usage. The chi-

square value of responses on monthly spending on card from education-wise variable is

positively co-related and significant at 5% level of significance. Hence it is proved that

people with good educational background are sought to use more from the plastic

money. This may be easy for the highly qualified people to manage their funds more

wisely as compared to other groups.

Perception of Card Holders towards Plastic Money

122

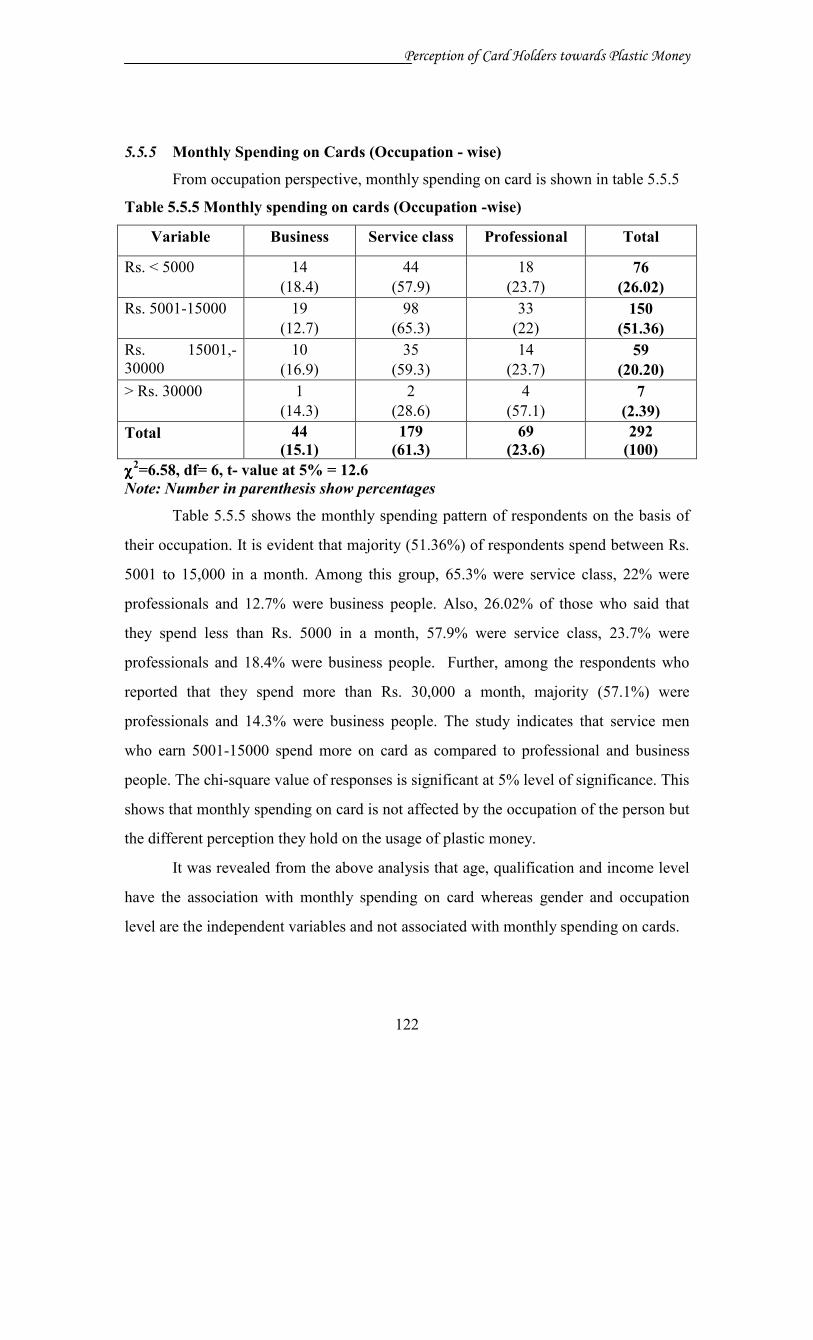

5.5.5 Monthly Spending on Cards (Occupation - wise)

From occupation perspective, monthly spending on card is shown in table 5.5.5

Table 5.5.5 Monthly spending on cards (Occupation -wise)

Variable Business Service class Professional Total

Rs. < 5000 14

(18.4)

44

(57.9)

18

(23.7)

76

(26.02)

Rs. 5001-15000 19

(12.7)

98

(65.3)

33

(22)

150

(51.36)

Rs. 15001,-

30000

10

(16.9)

35

(59.3)

14

(23.7)

59

(20.20)

> Rs. 30000 1

(14.3)

2

(28.6)

4

(57.1)

7

(2.39)

Total 44

(15.1)

179

(61.3)

69

(23.6)

292

(100)

χχχχ2=6.58, df= 6, t- value at 5% = 12.6

Note: Number in parenthesis show percentages

Table 5.5.5 shows the monthly spending pattern of respondents on the basis of

their occupation. It is evident that majority (51.36%) of respondents spend between Rs.

5001 to 15,000 in a month. Among this group, 65.3% were service class, 22% were

professionals and 12.7% were business people. Also, 26.02% of those who said that

they spend less than Rs. 5000 in a month, 57.9% were service class, 23.7% were

professionals and 18.4% were business people. Further, among the respondents who

reported that they spend more than Rs. 30,000 a month, majority (57.1%) were

professionals and 14.3% were business people. The study indicates that service men

who earn 5001-15000 spend more on card as compared to professional and business

people. The chi-square value of responses is significant at 5% level of significance. This

shows that monthly spending on card is not affected by the occupation of the person but

the different perception they hold on the usage of plastic money.

It was revealed from the above analysis that age, qualification and income level

have the association with monthly spending on card whereas gender and occupation

level are the independent variables and not associated with monthly spending on cards.

Perception of Card Holders towards Plastic Money

123

5.6 Making Payment of Credit Card Bills

Cards users decide to make payments in different patterns. Some make

payments up to the minimum required, some pay full payment within grace period and

some beyond grace period. This section try to analyses from different parameters the

behaviour of the respondents for making the payment. The results are presented here

below:

5.6.1 Making Payment of Credit Card Bills (Age–wise)

Different age group users make payment on credit card in diverse way. The

result from age perspective for the payment of credit card bill is shown in table 5.6.1.

Table 5.6.1 shows that 63.35% of the respondents prefer making full payment

within the grace period, 10.96% make payment on fixed amount each month, greater

than the minimum required. Only 13.01% and 4.79% indicated that they make payment

more than minimum required and full payment beyond grace period respectively.

Table 5.6.1 Payment of credit card bills (Age – wise)

Variable <30 years 31-45 years 746 years Total

Minimum balance required 14

(60.9)

8

(34.8)

1

(4.3) 23

(7.87)

More than minimum required 20

(52.6)

16

(42.1)

2

(5.3) 38

(13.01)

Fixed amount each month, greater

than minimum required

12

(37.5)

14

(43.8)

6

(18.8) 32

(10.96)

Full payment within grace period 58

(31.4)

95

(51.4)

32

(17.3) 185

(63.35)

Full payment beyond grace period 5

(35.7)

8

(57.1)

1

(7.1) 14

(4.79)

Total 109

(37.3)

141

(48.3)

42

(14.4)

292

(100)

χχχχ2=15.31, df= 8, t-value at 5% = 15.5

Note: Number in parenthesis show percentages

Similarly, out the total respondents who reported that they make full payment

within the grace period, majority (51.4%) were between the age of 31-45 years and

31.4% were less than 30 years. Also, those who indicated that they make fixed amount

each month, greater than minimum required, majority (52.6%) belong to the age group

less then 30 years and 42.1% aged between 31-45 years. Inferential statistics shows that

Perception of Card Holders towards Plastic Money

124

there is no association between age and payment of credit card bills at 5 percent level of

significance. It can be concluded that pattern of bill payment is not affected by age, but

with some other attribute.

5.6.2 Making Payments on Credit Card Bills (Gender – wise)

Different card users have various ways of making payment on credit card bills.

From the gender prospective, it was indicated in Table 5.6.2 that, among those who

make payment up to the minimum balance required, majority (60.9%) were male and

the rest female.

Table 5.6.2 Payments of credit card bills (Gender – wise)

Variable Male Female Total

Minimum balance required 14

(60.9)

9

(39.1)

23

(7.87)

More than minimum required 25

(65.8)

13

(34.2)

38

(13.01)

Fixed amount each month, Greater

than minimum required

25

(78.1)

7

(21.9)

32

(10.96)

Full payment within Grace period 150

(81.1)

35

(18.9)

185

(63.35)

Full Payment beyond grace period 12

(85.7)

2

(14.3)

14

(4.79)

Total 226

(77.4)

66

(22.6)

292

(100)

χχχχ2=8.52, df= 4, t- value at 5% =9.49

Note: Number in parenthesis show percentages

The overall result indicated that 63.35% people make full payment within the

grace period required and among them, only 81.1% where males and 18.9% were

female. Further, it was indicated that those who make payment more than minimum

required majority (65.8%) were males and 34.2% were females. The chi-square value of

responses for the payment of credit card bills is insignificant at 5% level of significance.

Hence, it is proved that both males and females pay their dues within time, there is no

difference in making the bill payment on gender basis.

Perception of Card Holders towards Plastic Money

125

5.6.3 Making Payment on Credit Card Bills (Income – wise)

Different card users make payments on credit card in diverse ways. Table 5.6.3

shows the result indicating how different income classes make payments on credit card.

Table 5.6.3 Payment on credit card bills (Income – wise)

Variable Upto

Rs.20000

20001-60000 60001-

100000

Above

Rs.10000

Total

Minimum Balance

required

10

(43.5)

13

(56.5)

- - 23

(7.87)

More than minimum

Balance

15

(39.5)

19

(50)

4

(10.5)

- 38

(13.01)

Fixed amount greater

than minimum required

9

(28.1)

19

(59.4)

4

(12.5)

- 32

(10.96)

Full payment within

grace period

38

(20.5)

100

(54.1)

39

(21.1)

8

(4.3) 185

(63.35)

Full payment beyond the

grace period

3

(21.4)

8

(57.1)

3

(21.4)

- 14

(4.79)

Total 75

(25.70)

159

(54.50)

50

(17.10)

8

(2.70)

292

(100)

χχχχ2=19.82, df= 12, t-value at 5% = 19.7

Note: Number in parenthesis show percentages

It is clear from the table that the majority of the respondents make full payment

within the grace period. Out of them 54.1% earn Rs. 20,001-60,000, 21.1% earn Rs.

60,001-100,000 and 4.3% earn above Rs. 100,000. Among those who reported that they

make payment upto the minimum required majority (65.5%) earn Rs. 20,000-60,000

and 43.5% earn less than Rs. 20,000.

Also, the result indicated that among those who make payment more than the

minimum balance required, majority (50%) earn between Rs. 20,001-60,000, followed

by those who earn upto Rs. 20,000. The result confirms that many users like making

payments within period required which means that the users always do not like to

increase liabilities on using their cards. The chi-square value of responses on the

income-wise variable for the payment of bills is insignificant at 5% level of

significance. This shows that person with the fixed and regular income has no hesitation

to pay their dues within time, because they does not like to increase their liabilities.

Perception of Card Holders towards Plastic Money

126

5.6.4 Making Payment on Credit Card Bills (Education – wise)

From education perspective, the results are shown in table no. 5.6.4.

Respondents were asked to indicate on how they make their payments on credit card

bills. Study shows that majority (63.35%) of the respondents make full amount of

payment within the grace period. Among them, 51.9% were post graduates, 45.9% were

graduates and 2.2% did not specify their qualifications.

Table 5.6.4 Payment on credit card bills (Education – wise)

Variable Graduate Post Graduate Any Other Total

Minimum balance

required

11

(47.8)

10

(43.5)

2

(8.7)

23

(7.87)

More than minimum

required

17

(44.7)

18

(47.4)

3

(7.9)

38

(13.01)

Fixed amount each

month, Greater than

minimum required

17

(53.1)

14

(43.8)

1

(3.1)

32

(10.96)

Full amount within

grace period.

85

(45.9)

96

(51.9)

4

(2.2)

185

(63.35)

Full payment beyond

grace period

3

(21.4)

10

(71.4)

1

(7.1)

14

(4.79)

Total 133

(45.5)

148

(50.7)

11

(3.8)

292

(100)

χχχχ2=9.02, df= 8, t- value at 5% = 15.5

Note: Number in parenthesis show percentages

Also 10.96% of those who said that they make fixed amount of payment each

month, more than the minimum required, 53.1% were graduates, 43.87% were post

graduates and 3.1% did not specify their qualification. Further, it is revealed that among

those who said that they make payment upto minimum payment required, 43.5% were

post graduates, 47.8% wee graduates and 8.7% did not specify. This result shows that

qualification also matters when it comes to matters related to payment pattern of card

users. The chi-square value of responses on education –wise for making the payment of

dues is insignificant at 5% level of significance. Hence, people with or without good

education do not make a difference in making the dues clear within time.

Perception of Card Holders towards Plastic Money

127

5.6.5 Making Payment of Credit Card Bills (Occupation – wise)

Different card users make payments in numerous ways. Table 5.6.5 indicates

that majority (63.35%) of the respondents make full payment within grace period. This

means that they do not like liabilities to stand as unnecessary tension.

Table 5.6.5 Payment on credit card bills (Occupation – wise)

Variable Business Service class Professional Total

Minimum balance

required

2

(8.7)

11

(47.8)

10

(43.5)

23

(7.87)

More than minimum

required

4

(10.5)

26

(68.4)

8

(21.1)

38

(13.01)

Fixed amount each

month greater the

minimum required

6

(18.8)

18

(56.3)

8

(25)

32

(10.96)

Full payment within

grace period

29

(15.7)

114

(61.6)

42

(22.7)

185

(63.35)

Full payment

beyond the grace

period

3

(21.4)

10

(71.4)

1

(7.10)

14

(4.79)

Total 44

(15.1)

179

(61.3)

69

(23.6)

292

(100)

χχχχ2=8.86, df= 8, t- value at 5% = 15.5

Note: Number in parenthesis show percentages

Among those who reported so, 61.6% were service class, 22.7% were

professionals and 15.7% were business class. Among those who make fixed amount

each month greater than minimum included 56.3% service people, 25% professionals

and 18.8% business people. Also 4.79% of those who make full payment beyond the

grace period, 71.4% were service class, 21.4% were business people and 7.10% were

professionals. This result shows that perhaps service class make payment with great

caution as they need not to be liable to balances later. The chi-square value of responses

for making the payment on occupational basis is insignificant at 5% level of

significance. This shows occupation does not affect the behaviour of the person to make

the bill payments.

Perception of Card Holders towards Plastic Money

128

It can be concluded that all the variables (age, gender, income, qualification and

occupation)do not affect the making payment of credit card bills. Perhaps, this was

affected by behavior of the person to make the payments.

5.7 Carrying of Revolving Balance

In this section, respondents were asked to indicate if they carry revolving

balance while using their credit cards. The card users carry revolving balance in

different patterns which is as follow.

5.7.1 Carrying of Revolving Balance (Age – wise)

The researcher sought to know from different age group whether they carry the

revolving balance or not. The result presented on table no. 5.7.1.From Table, it is

clearly indicated that majority (44.17%) of the respondents indicated that they never

carry revolving balance, 18.49% reported that they seldom carry revolving balance,

Further, 25.68% of the total respondents indicated that they frequently carry revolving

balance and only 11.64% of the total respondents indicated that they always carry such

balance.

Table 5.7.1 Carrying of Revolving Balance (Age – wise)

Variable 18-30 years 31-45 years 46 years and above Total

Never 41

(31.8)

61

(47.3)

27

(20.9) 129

(44.17)

Seldom 26

(48.1)

23

(42.6)

5

(9.30) 54

(18.49)

Frequently 30

(40)

40

(53.3)

5

(6.7) 75

(25.68)

Always 12

(35.3)

17

(50)

5

(14.7) 34

(11.64)

Total 109

(37.3)

141

(48.3)

42

(14.4)

292

(100)

χχχχ2=11.68, df= 6 , t- value at 5% = 12.6

Note: Number in parenthesis show percentages

From the age perspective, majority of those who reported that they never carry

such balance were between the age of 31-45 years (47.3%). Also, 31.2% were less than

30 years of age. Among those who seldom carry their balances majority (48.1%) were

less than 30 years of age and 42.6% were between 31-45 years. This indicates that

Perception of Card Holders towards Plastic Money

129

younger card users seldom carry the balances while middle aged never carry revolving

balances when using their plastic money. Among those respondents who said that they

carry their revolving balance always, majority (50%) were of the age between 31-45

years and 35.37% were less than 30 years. Inferential statistics shows that the age has

the insignificant relationship with carrying of revolving balance at 5% level of

significance. It is clear from the analysis all the age groups respondents do not like to

carry their revolving balance as it is likely to increase their liabilities in future.

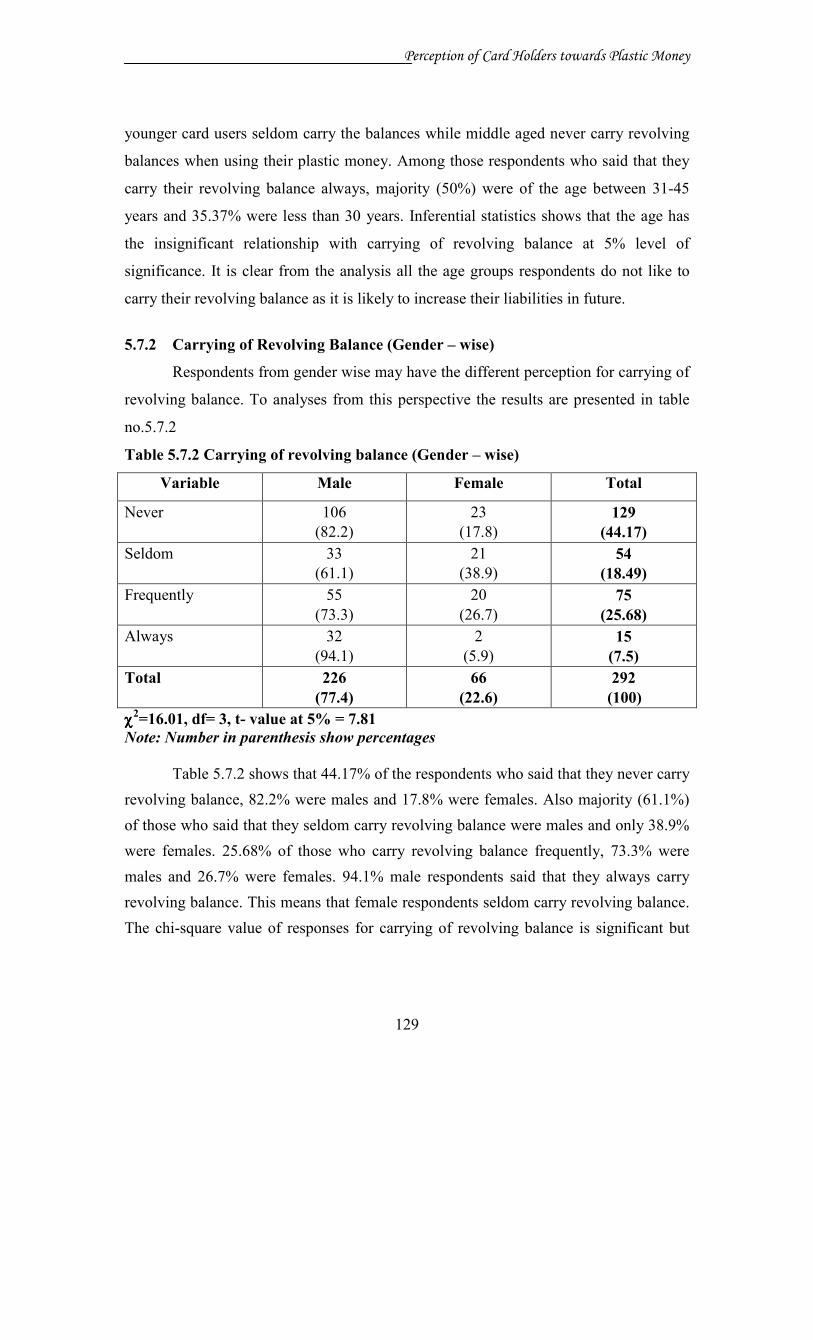

5.7.2 Carrying of Revolving Balance (Gender – wise)

Respondents from gender wise may have the different perception for carrying of

revolving balance. To analyses from this perspective the results are presented in table

no.5.7.2

Table 5.7.2 Carrying of revolving balance (Gender – wise)

Variable Male Female Total

Never 106

(82.2)

23

(17.8)

129

(44.17)

Seldom 33

(61.1)

21

(38.9)

54

(18.49)

Frequently 55

(73.3)

20

(26.7)

75

(25.68)

Always 32

(94.1)

2

(5.9)

15

(7.5)

Total 226

(77.4)

66

(22.6)

292

(100)

χχχχ2=16.01, df= 3, t- value at 5% = 7.81

Note: Number in parenthesis show percentages

Table 5.7.2 shows that 44.17% of the respondents who said that they never carry

revolving balance, 82.2% were males and 17.8% were females. Also majority (61.1%)

of those who said that they seldom carry revolving balance were males and only 38.9%

were females. 25.68% of those who carry revolving balance frequently, 73.3% were

males and 26.7% were females. 94.1% male respondents said that they always carry

revolving balance. This means that female respondents seldom carry revolving balance.

The chi-square value of responses for carrying of revolving balance is significant but

Perception of Card Holders towards Plastic Money

130

negatively co-related at 5% level of significance. This shows both the males and

females never or seldom carry the revolving balance as both do not like liabilities.

5.7.3 Carrying of revolving balance (Income – wise)

To carry the revolving balance in the account may be on the income of the

respondents. Here, in this section researcher want to observe from different income

group their behaviour for carrying the revolving balance. The result are presented here

below:

Table 5.7.3 Carrying of revolving balance (Income – wise)

Variable Up to

Rs.20000

20001-

60000

60001-

100000

Above

Rs.100000

Total

Never 26

(20.2)

67

(51.9)

29

(22.5)

7

(5.4) 129

(44.17)

Seldom 19

(35.2)

25

(46.3)

10

(18.5)

- 54

(18.49)

Frequently 19

(25.3)

48

(64)

8

(10.7)

- 75

(25.68)

Always 11

(32.4)

19

(55.9)

3

(8.8)

1

(2.9) 34

(11.64)

Total 75

(25.70)

159

(54.50)

50

(17.10)

8

(2.70)

292

(100)

χχχχ2=18.46, df= 9, t-value at 5% and 1% level = 16.9 and 21.7

Note: Number in parenthesis show percentages

Table 5.7.3 shows that card users carry revolving balance in different patterns

from income-wise perspective. It is indicated that 44.17% of the respondents never

carry revolving balance when using plastic cards. Among those who said that they never

carry revolving balance, 51.9% earn between Rs. 20,001 to 60,000, 22.5% earn Rs.