part 2 accounting for property developers - rehda...

TRANSCRIPT

TST Consultants Sdn Bhd 1

Part 2

Accounting for Property Developers

TST Consultants Sdn Bhd 2

Accounting for Property Developers

A) Date of Commencement of business

B) Estimation of Gross Profit

C) Final year a/c at the end of the project

D) Financial Statements

E) Disclosure and Notes to Financial Statements

F) Final year a/c and revision

TST Consultants Sdn Bhd 3

A) Pre-Commencement of business expenses

• Consideration of all the circumstances and the facts of each case

• General rule, not allowable as a deduction against the gross

income

• Not wholly and exclusively incurred in the production of business

TST Consultants Sdn Bhd 4

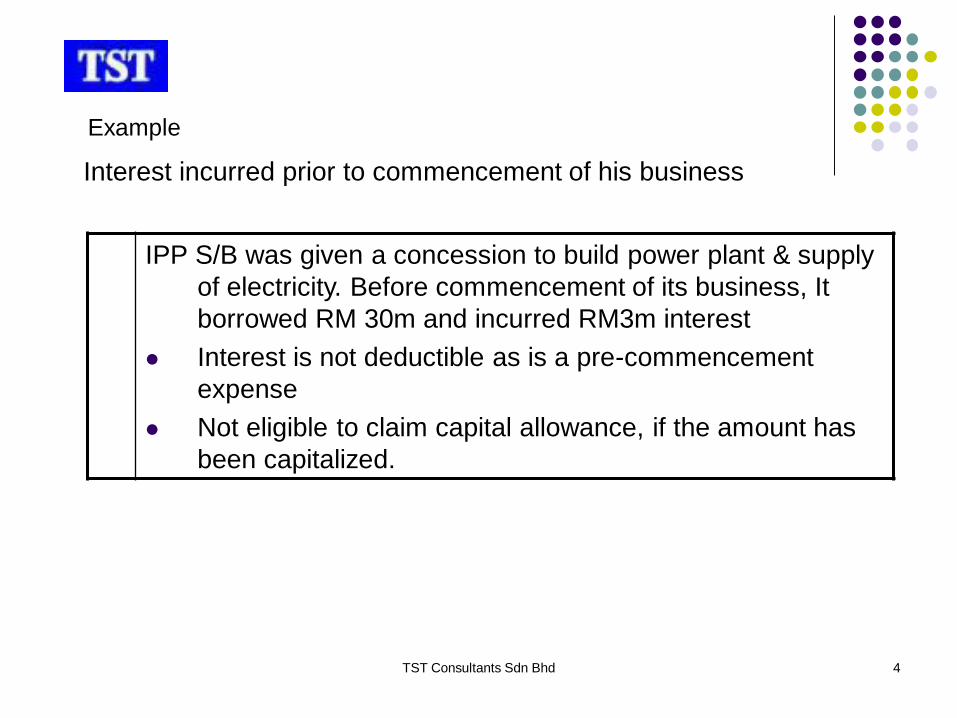

Interest incurred prior to commencement of his business

IPP S/B was given a concession to build power plant & supply

of electricity. Before commencement of its business, It

borrowed RM 30m and incurred RM3m interest

Interest is not deductible as is a pre-commencement

expense

Not eligible to claim capital allowance, if the amount has

been capitalized.

Example

TST Consultants Sdn Bhd 5

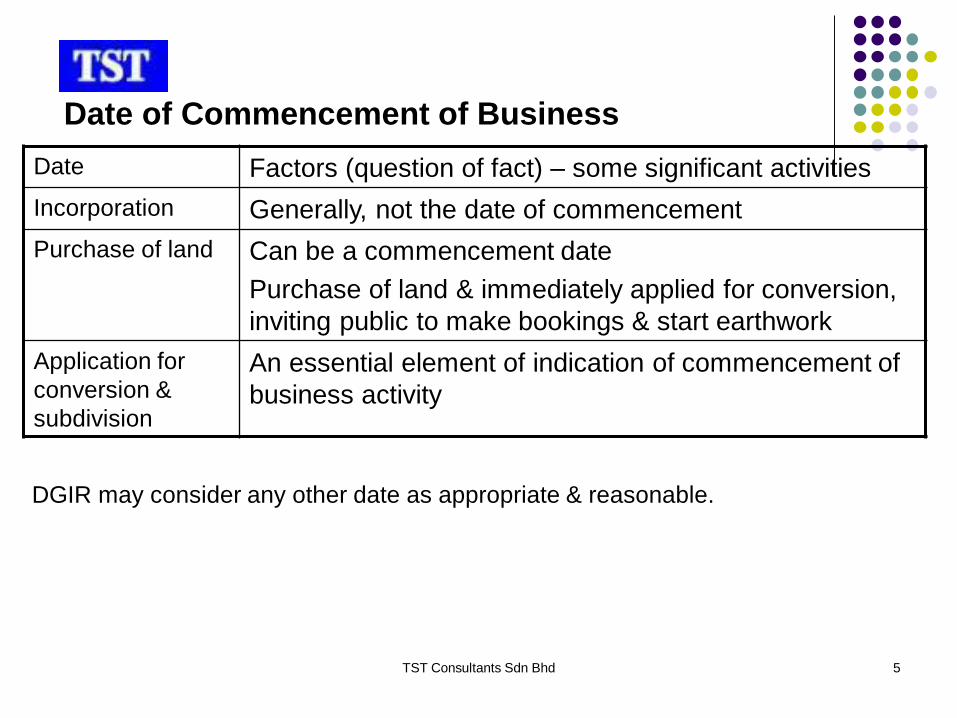

Date of Commencement of Business

Date Factors (question of fact) – some significant activities

Incorporation Generally, not the date of commencement

Purchase of land Can be a commencement date

Purchase of land & immediately applied for conversion,

inviting public to make bookings & start earthwork

Application for

conversion &

subdivision

An essential element of indication of commencement of

business activity

DGIR may consider any other date as appropriate & reasonable.

TST Consultants Sdn Bhd 6

B) Estimate/recognition of Revenue

S24 ITA the gross income from business to be assessed on a receivable

basis

IRB

Method

Public ruling no. 1/2009

IRB accepts the “percentage of completion method”

The common ways are:-

-based on progress billings

-based on cost incurred to date

Each development project be treated as a separate & distinct

source of income, but aggregate as business source.

Accounting

Standard

IRB accept % of completion based on cost

Must be adopted consistently

TST Consultants Sdn Bhd 7

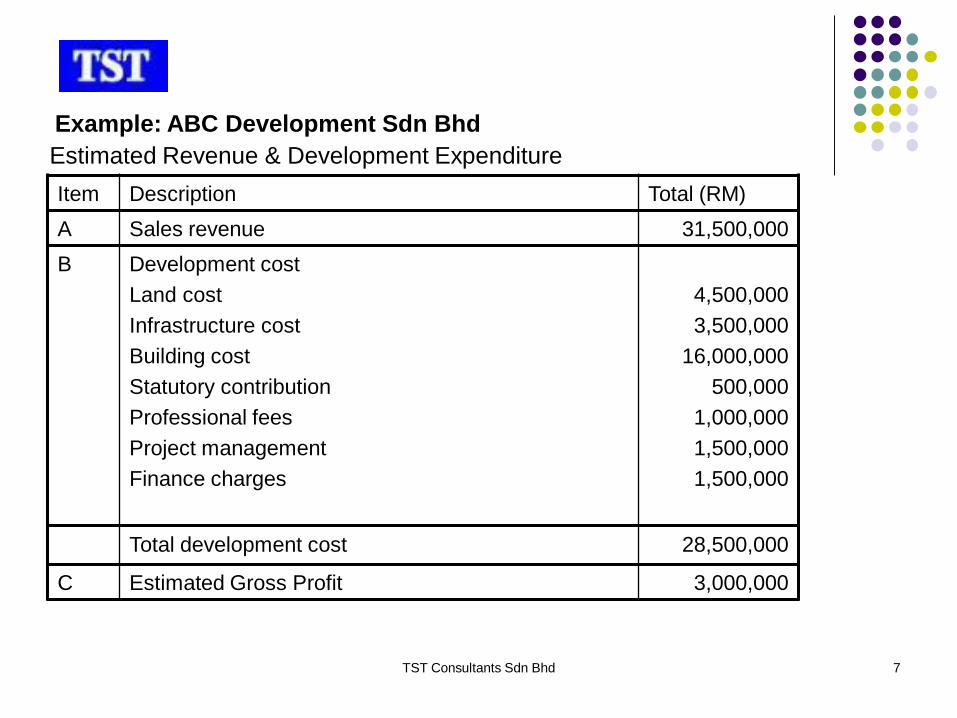

Estimated Revenue & Development Expenditure

Item Description Total (RM)

A Sales revenue 31,500,000

B Development cost

Land cost

Infrastructure cost

Building cost

Statutory contribution

Professional fees

Project management

Finance charges

4,500,000

3,500,000

16,000,000

500,000

1,000,000

1,500,000

1,500,000

Total development cost 28,500,000

C Estimated Gross Profit 3,000,000

Example: ABC Development Sdn Bhd

TST Consultants Sdn Bhd 8

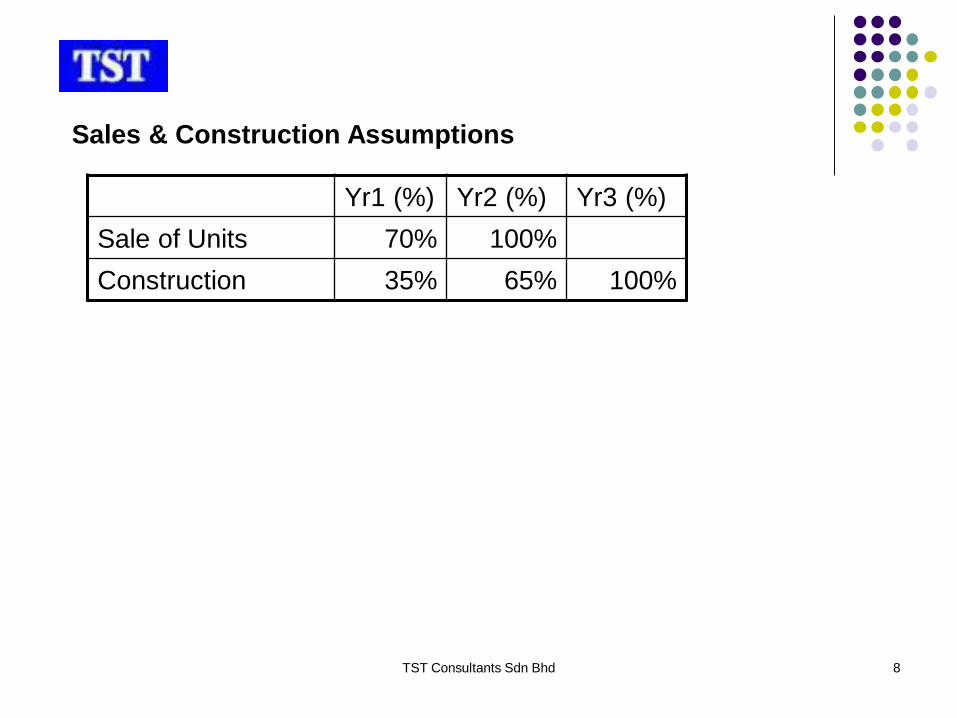

Sales & Construction Assumptions

Yr1 (%) Yr2 (%) Yr3 (%)

Sale of Units 70% 100%

Construction 35% 65% 100%

TST Consultants Sdn Bhd 9

Recognition of revenue (IRB Method)

Formula – “% of completion method” based on progress billing

Formula A/B x C

A Sum of progress payment (received & receivable)

B Total estimated sale value

C Estimated Gross Profit

TST Consultants Sdn Bhd 10

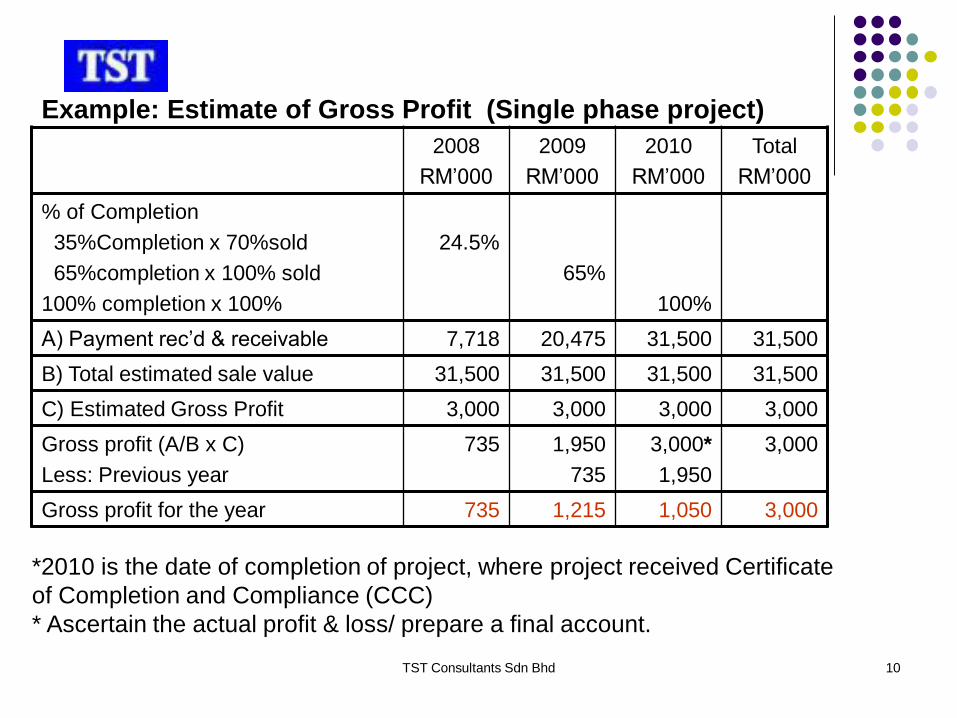

Example: Estimate of Gross Profit (Single phase project)

2008

RM’000

2009

RM’000

2010

RM’000

Total

RM’000

% of Completion

35%Completion x 70%sold

65%completion x 100% sold

100% completion x 100%

24.5%

65%

100%

A) Payment rec’d & receivable 7,718 20,475 31,500 31,500

B) Total estimated sale value 31,500 31,500 31,500 31,500

C) Estimated Gross Profit 3,000 3,000 3,000 3,000

Gross profit (A/B x C)

Less: Previous year

735 1,950

735

3,000*

1,950

3,000

Gross profit for the year 735 1,215 1,050 3,000

*2010 is the date of completion of project, where project received Certificate

of Completion and Compliance (CCC)

* Ascertain the actual profit & loss/ prepare a final account.

TST Consultants Sdn Bhd 11

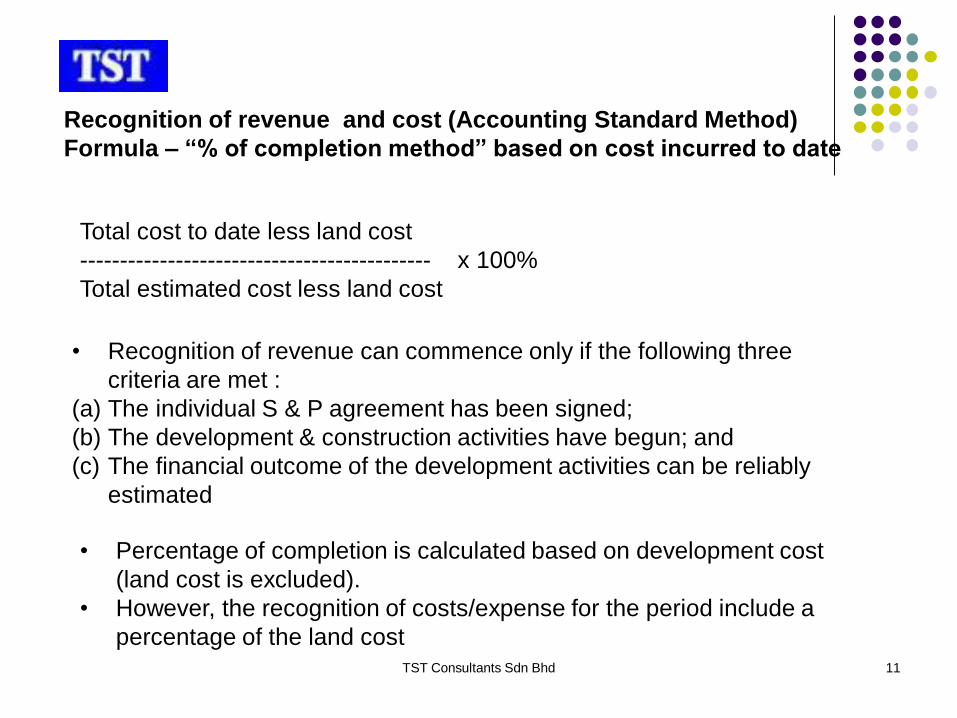

Recognition of revenue and cost (Accounting Standard Method)

Formula – “% of completion method” based on cost incurred to date

Total cost to date less land cost

-------------------------------------------- x 100%

Total estimated cost less land cost

• Recognition of revenue can commence only if the following three

criteria are met :

(a) The individual S & P agreement has been signed;

(b) The development & construction activities have begun; and

(c) The financial outcome of the development activities can be reliably

estimated

• Percentage of completion is calculated based on development cost

(land cost is excluded).

• However, the recognition of costs/expense for the period include a

percentage of the land cost

TST Consultants Sdn Bhd 12

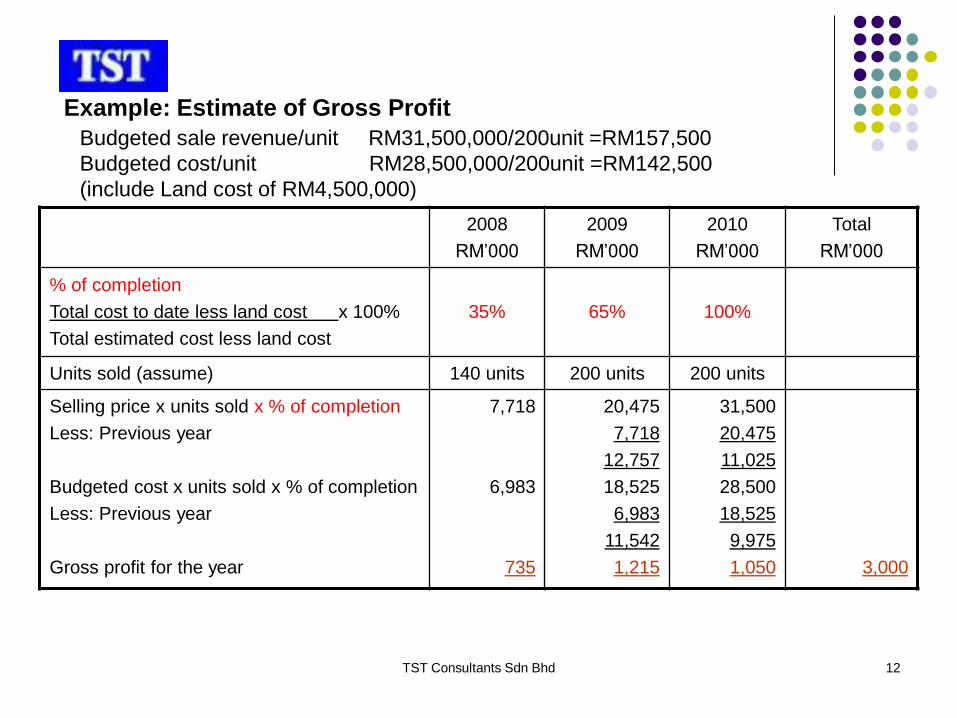

Example: Estimate of Gross Profit

2008

RM’000

2009

RM’000

2010

RM’000

Total

RM’000

% of completion

Total cost to date less land cost x 100%

Total estimated cost less land cost

35% 65% 100%

Units sold (assume) 140 units 200 units 200 units

Selling price x units sold x % of completion

Less: Previous year

Budgeted cost x units sold x % of completion

Less: Previous year

Gross profit for the year

7,718

6,983

735

20,475

7,718

12,757

18,525

6,983

11,542

1,215

31,500

20,475

11,025

28,500

18,525

9,975

1,050 3,000

Budgeted sale revenue/unit RM31,500,000/200unit =RM157,500

Budgeted cost/unit RM28,500,000/200unit =RM142,500

(include Land cost of RM4,500,000)

TST Consultants Sdn Bhd 13

C) Final Year Accounts Upon completion of project

When project received Certificate of Completion and Compliance (CCC)

Ascertain the actual profit/loss & prepare a final accounts

Allocation of land cost

Allocation of common infrastructure cost

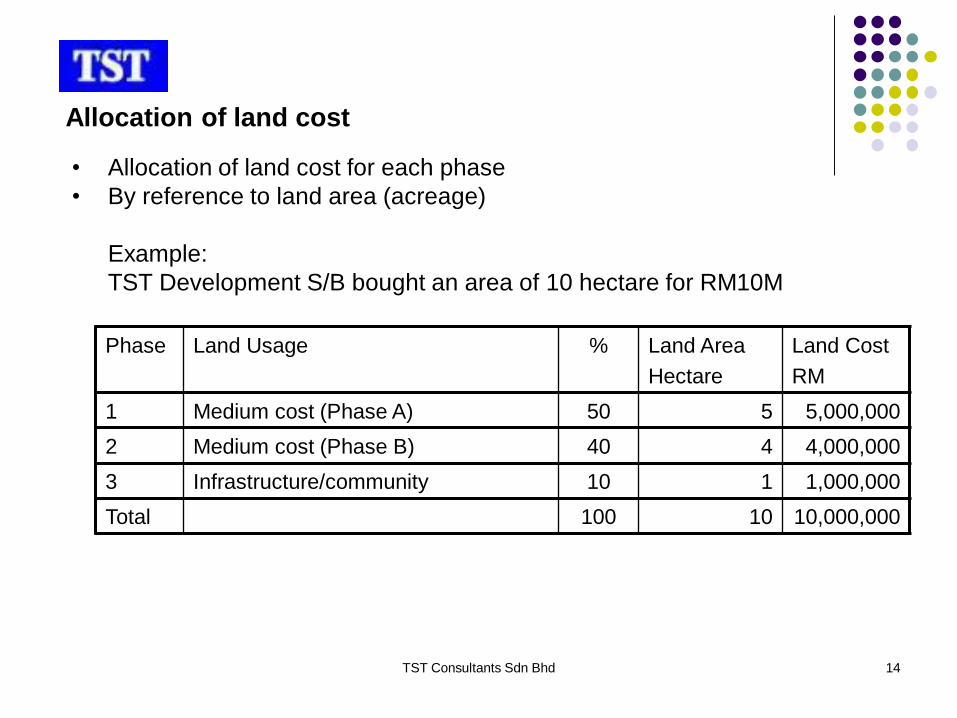

TST Consultants Sdn Bhd 14

Allocation of land cost

• Allocation of land cost for each phase

• By reference to land area (acreage)

Example:

TST Development S/B bought an area of 10 hectare for RM10M

Phase Land Usage % Land Area

Hectare

Land Cost

RM

1 Medium cost (Phase A) 50 5 5,000,000

2 Medium cost (Phase B) 40 4 4,000,000

3 Infrastructure/community 10 1 1,000,000

Total 100 10 10,000,000

TST Consultants Sdn Bhd 15

Allocation of common infrastructure cost

• Accounting standard

Common costs may be allocated using:

- relative sales value, or

-any other generally accepted method

• Income Tax purposes

Common infrastructure costs be apportioned in accordance with:

-the area (acreage) method;

-the relative sales value method; or

-any method that is acceptable by the DGIR

TST Consultants Sdn Bhd 16

Total development area of Phase 1

----------------------------------------------- x Common infrastructure cost

Total development area of all phases

Example based on area

TST Consultants Sdn Bhd 17

Total land cost RM10M

Common infrastructure cost:

Land cost (1/10 x RM10M) RM1M

Infrastructure & recreational part cost RM3M

RM4M

If there is no estimated sales value for phase B, then use the

acreage method

Example based on relative sales value/Acreage

Infrastructure &

Community cost

Phase A Phase B Total

Acres 1 Acre 5 Acres 4 Acres 10 Acres

Relative sales value RM30M RM20M RM50M

Common costs

Based on sales value

30/50xRM4M

=RM2.4M

20/50xRM4M

=RM1.6M RM4M

Common costs

Based on acreage

5/9 xRM4M

=RM2.24M

4/9xRM4M

=RM1.76M RM4M

TST Consultants Sdn Bhd 18

D) Financial Statements

Extracts of Balance sheet

As at 31 December 20xx

Assets

Non-current Assets

Land held for property development x

Current Assets

Property development costs x

Inventories x

Trade receivable/Accrued billing (revenue>billing) x

Current Liability

Trade payable/Progress billing (revenue<billing) x

TST Consultants Sdn Bhd 19

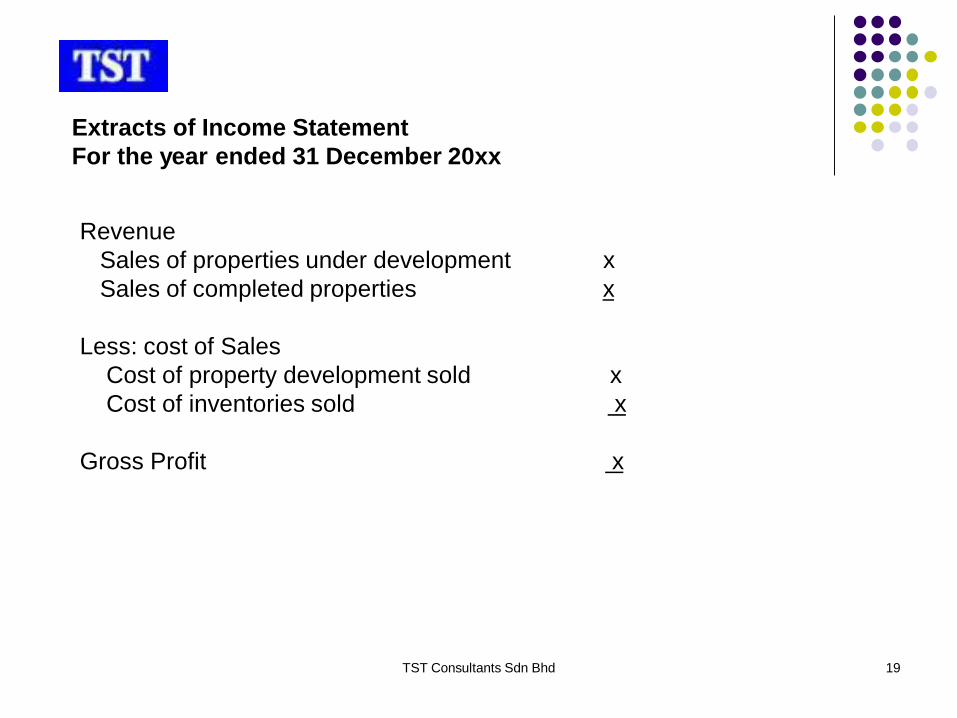

Extracts of Income Statement

For the year ended 31 December 20xx

Revenue

Sales of properties under development x

Sales of completed properties x

Less: cost of Sales

Cost of property development sold x

Cost of inventories sold x

Gross Profit x

TST Consultants Sdn Bhd 20

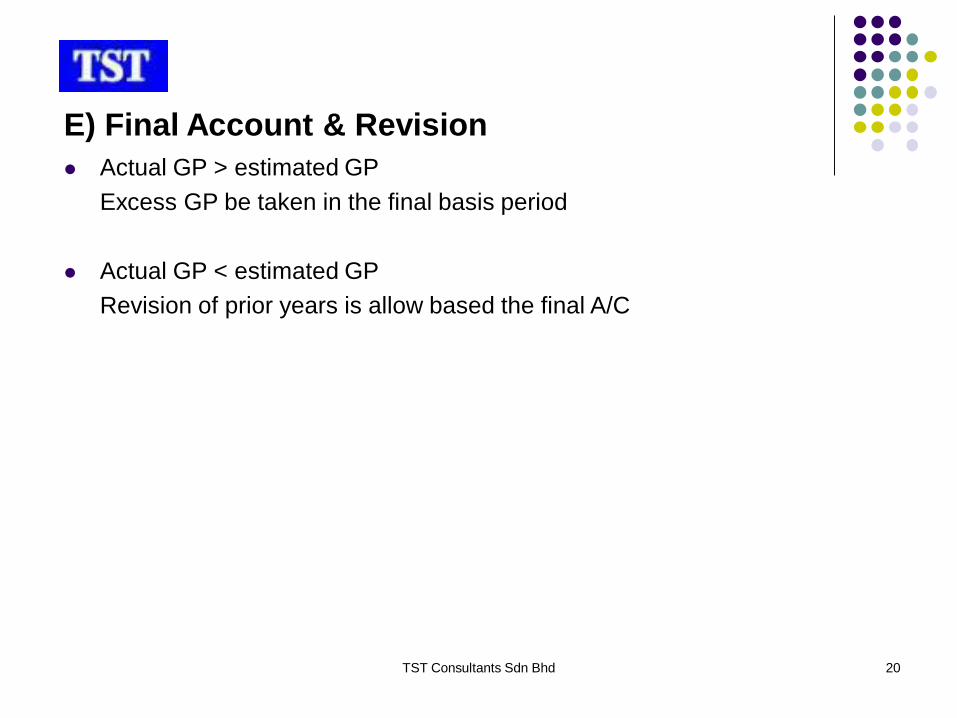

E) Final Account & Revision

Actual GP > estimated GP

Excess GP be taken in the final basis period

Actual GP < estimated GP

Revision of prior years is allow based the final A/C

TST Consultants Sdn Bhd 21

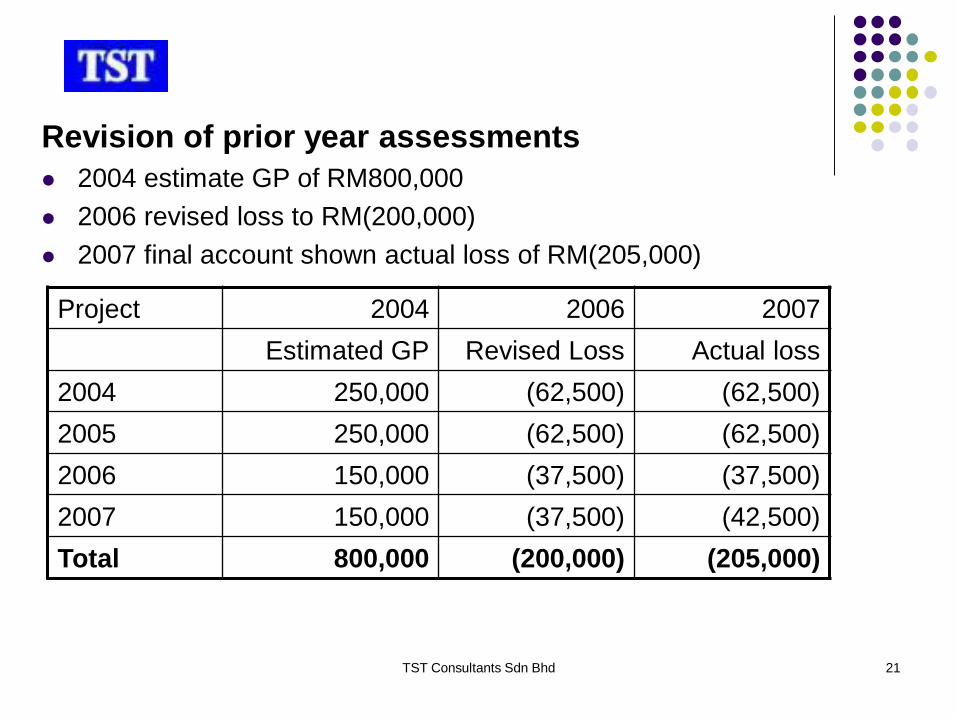

Revision of prior year assessments

2004 estimate GP of RM800,000

2006 revised loss to RM(200,000)

2007 final account shown actual loss of RM(205,000)

Project 2004 2006 2007

Estimated GP Revised Loss Actual loss

2004 250,000 (62,500) (62,500)

2005 250,000 (62,500) (62,500)

2006 150,000 (37,500) (37,500)

2007 150,000 (37,500) (42,500)

Total 800,000 (200,000) (205,000)

TST Consultants Sdn Bhd 22

Part 2.1Outgoings and expenses of Property Developers

TST Consultants Sdn Bhd 23

1. Pre-Commencement of Business expenses

• Pre-commencement loan interest expenses is not deductible

• Loan interest not deductible as expenses are not allowable for

deduction as part of the acquisition price under RPGT

Example: Loan interest on vacant land

• Important to commerce development business

Example:

-Application for conversion & subdivision

-start earthwork

-access road

TST Consultants Sdn Bhd 24

2. Warranty & defect liability

Deductible against the aggregate GP

• other project of basis period or future period

• same project for the basis period & carried back to prior yr

TST Consultants Sdn Bhd 25

3. Liquidated ascertained damages

Deductible when incurred

• actual LAD claims by purchaser or purchaser’s lawyer

• actual LAD is ascertained & agreed between developer &

purchasers (provision for LAD is not allowable)

Allowed for deduction

• against same project for the basis period

• For a single development project, to carried back to the

preceding period & next preceding period until fully

deducted.

TST Consultants Sdn Bhd 26

4. Strata title expenses

Deductible when

• ascertained by the land office (provision is not allowable)

• against same project for the basis period & carried back to prior yr

TST Consultants Sdn Bhd 27

5. Professional fees

• Legal fees incurred in obtaining loan is not deductible (S39)

• Cost incurred in arranging end-financing facilities is allowable

• Valuation fees at time of land purchase is deductible

• Legal fees on transfer of land title/subdivision/conversion is deductible

• Compensation to squatters are allowable

TST Consultants Sdn Bhd 28

6. Stamp Duty

• Stamp duty on transfer of title is deductible

• Stamp duty on loan instrument is not deductible

Deductible Non deductible

Transfer of title

RM100K x 1% = 1,000

RM400K x 2% = 8,000

RM7500K x 3%= 225,000

RM8,000K 234,000

Loan instruments on

bridging/term/OD

Principle document

RM8 m x 1/2% =RM40K

TST Consultants Sdn Bhd 29

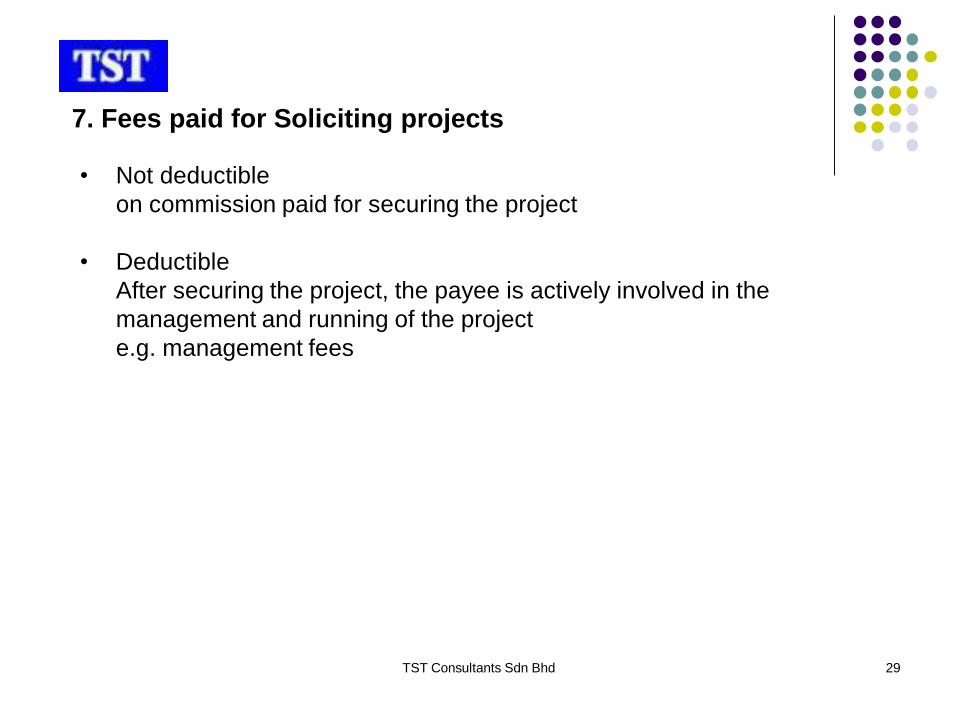

7. Fees paid for Soliciting projects

• Not deductible

on commission paid for securing the project

• Deductible

After securing the project, the payee is actively involved in the

management and running of the project

e.g. management fees

TST Consultants Sdn Bhd 30

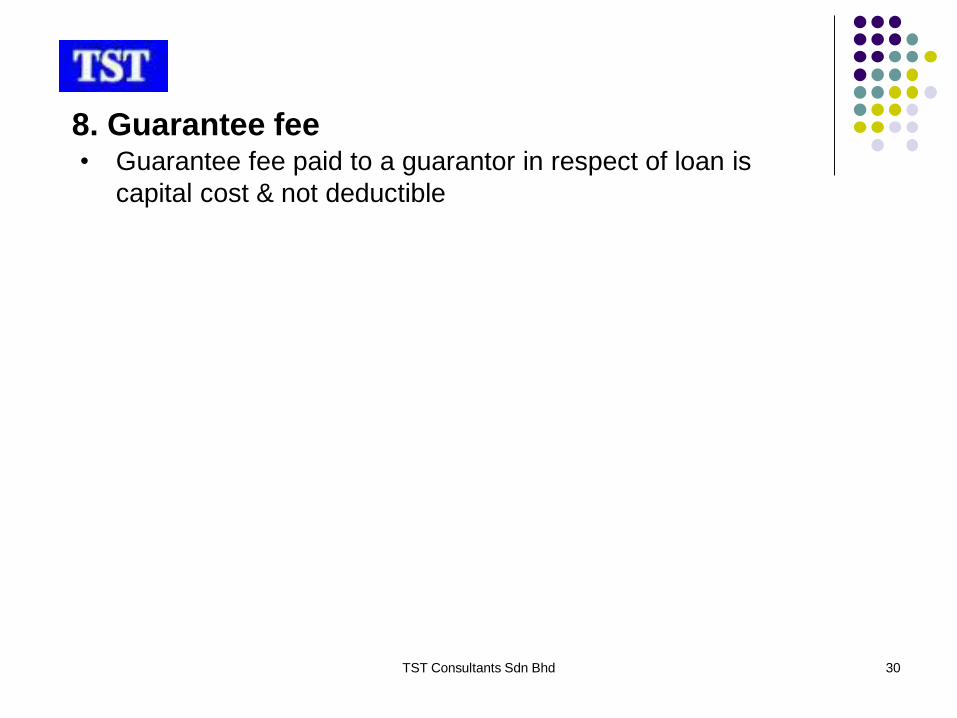

8. Guarantee fee• Guarantee fee paid to a guarantor in respect of loan is

capital cost & not deductible

TST Consultants Sdn Bhd 31

9. Processing fees• Processing fees on new loan and renewal of loan is not

deductible

TST Consultants Sdn Bhd 32

10. Interest charges

In general a property developer may charge interest expense:

-Development expenditure account; and/or

-Profit & loss account

Capitalized to Development Expenditure Account (not in P/L)

-Interest paid on loans taken for financing the purchase of land,

-Interest on development works

TST Consultants Sdn Bhd 33

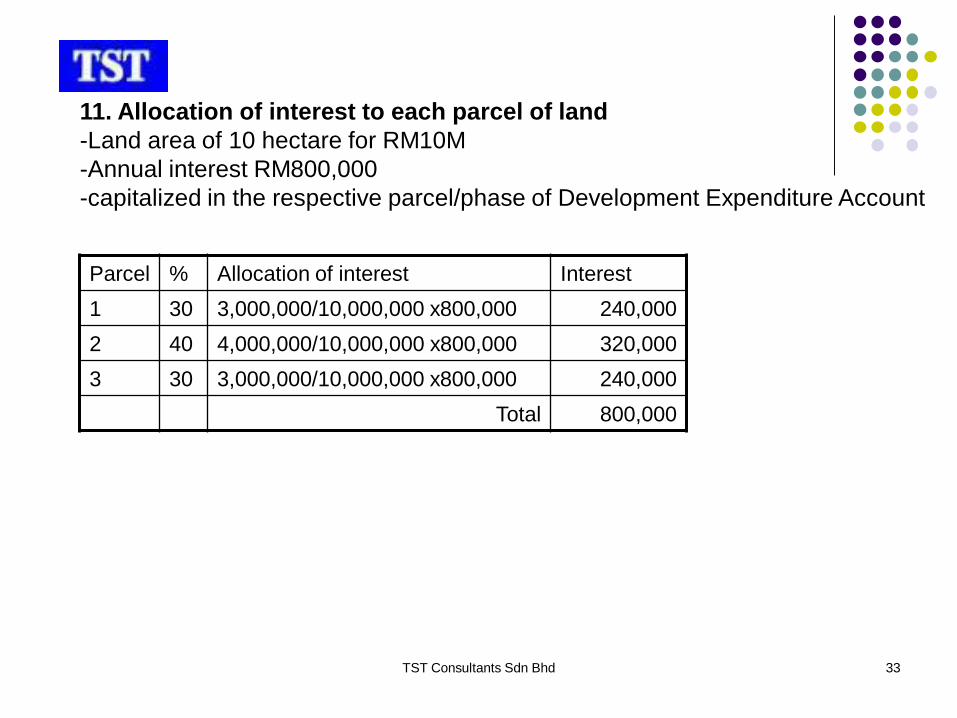

11. Allocation of interest to each parcel of land

-Land area of 10 hectare for RM10M

-Annual interest RM800,000

-capitalized in the respective parcel/phase of Development Expenditure Account

Parcel % Allocation of interest Interest

1 30 3,000,000/10,000,000 x800,000 240,000

2 40 4,000,000/10,000,000 x800,000 320,000

3 30 3,000,000/10,000,000 x800,000 240,000

Total 800,000

TST Consultants Sdn Bhd 34

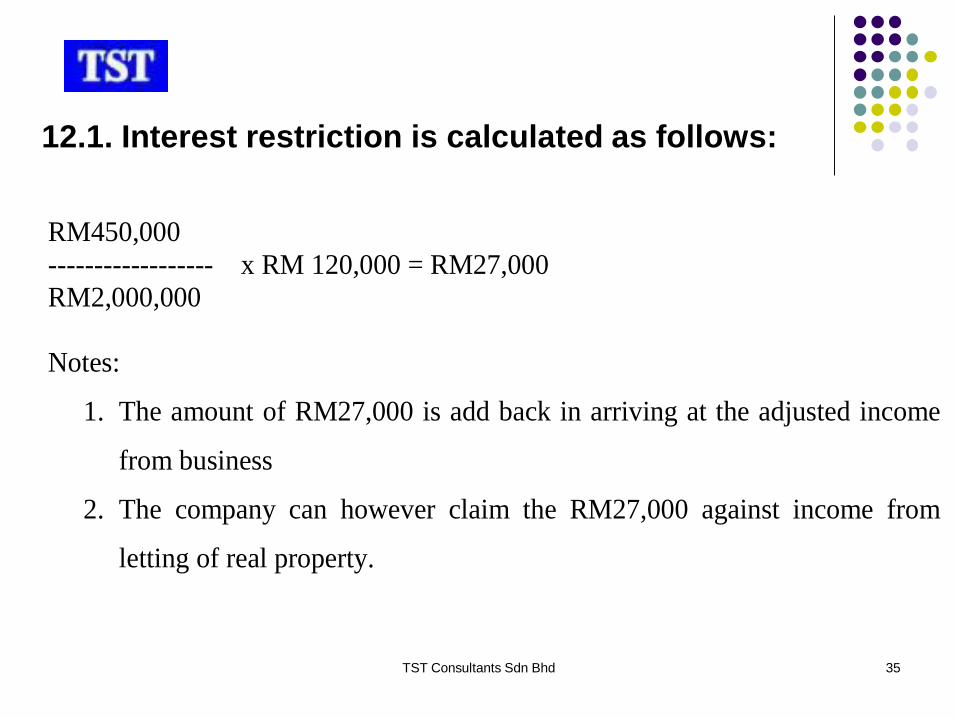

12. Restriction on interest expense

Takes a business loan of RM2,000,000 and used it to finance a

house cost RM450,000.

The interest expense of RM120,000 allowable against the

business source has to be restricted under S33(2) of ITA.

See the interest restriction formula below

TST Consultants Sdn Bhd 35

12.1. Interest restriction is calculated as follows:

RM450,000

------------------ x RM 120,000 = RM27,000

RM2,000,000

Notes:

1. The amount of RM27,000 is add back in arriving at the adjusted income

from business

2. The company can however claim the RM27,000 against income from

letting of real property.

TST Consultants Sdn Bhd 36

Q & A