nvs wealth managers steel authority of india...

TRANSCRIPT

NVS Wealth Managers

Nifty 8740.95

Sensex 28240.52

Nifty PE 23.29

Sensex PE 21.98

Sector Metals

BSE Code 500113

NSE Code SAIL

FV 10

Market Cap (Rs. Cr) 27073

Market Cap (US$ mn) 402

Equity Share Cap. 4,131

2r

Stock Data

Stock Performance (%)

52-week high/low Rs. 67.15 / 33.50

1M 6M 12M Absolute (%) 29.98 36.21 49.42

Shareholding Pattern (%)

Sensex and stock movement

3rd February, 2017

CMP: 65.55 ‘SAIL’ing with the strongest steel… ACCUMULATE

Company Update | Metals | India Research

Steel Authority of India Ltd.

• Steel Authority of India Ltd. (SAIL), a company promoted by Government of India, was established in the year 1954 and currently is one of the largest steel-making

company in India and one of the seven MAHARATNAS of the country’s central

public sector enterprises with an installed capacity of 14.3 MT.

• SAIL operates and owns five integrated steel plants at Bhilai, Durgapur, Bokaro, Rourkela and Burnpur along with three special steel plants at Salem, Durgapur and Bhadravati. The steel making capacity of SAIL post expansion will reach a whopping

21.4 MT. SAIL has a strong product mix that includes flat products such as HR coils, CR Coils, electric sheets which form around 46% of their total sales and long products like TMT bars and wire rods which form around 43% of the total sales along with long rails, blooms, slabs, billets, channels, angles, forged alloys, special steel products among others.

• SAIL caters to the large and marquee institutional buyers in sectors like Defence,

Railways, Construction, Fabrication, Agricultural Equipments, Auto, Power and host of other infrastructure sector with its world class products.

• In line with the turnaround in Steel Sector, from mid of 2016, SAIL Chairman Mr. P K

Singh pointed to the brighter days for SAIL during his recent interview with CNBC TV18, where he remarked “Our sales used to be around 12-13 Million. This year we will cross

14 Million tonne sales. However, in the subsequent year there will be quantum jump in the production as well as in the sales. Our exports this year, we are doubling our exports and this trend will continue next year also. We would like to see that at least 10 percent of our production, we should be able to export.”

• SAIL is in the final stage of completing its expansion and modernization program involving a mammoth capex of over Rs. 62,000 Cr which will augment its steel making capacity from 14.3 MT to 21.4 MT, ushering exciting times for the company’s stakeholders.

• SAIL had posted its lifetime best performance in FY 2007-08 with top line of over Rs.

45,500 Cr, PBT of over Rs. 11,400 Cr and PAT of over Rs. 7,500 Cr on equity of Rs. 4,130 Cr with market price touching over Rs. 290 per share in December 2007 with a whopping market capitalization of little over Rs. 1,20,000 cr creating huge wealth for its stakeholders. Currently the stock is trading in the range of Rs.64-66.50 with a market cap less than Rs.

27,500 Cr –i.e. USD 4.08 Billion (with expanded steel capacity of 21.4 MT-One of the

largest steel producer in India) is available at a very attractive price, considering that the turnaround is in sight and is on the threshold of exploiting the huge potential emanating from aggressive expansion and modernization. SAIL has a large equity base of Rs. 4,130 Cr but it is well placed in the strong hands, with 75% held by the Government of India, 20.77% by Mutual Funds, Financial

Institutions, Banks, Insurance Companies and FPI, leaving only 4.23% in the hands of

the Retail Public Shareholders spread over little less than four lakhs shareholders.

We believe SAIL is on the move and the best is yet to come. We recommend strong accumulation on SAIL.

Disclosure:

We have bought shares of SAIL for us and our clients at Rs. 49-51 levels before 31st December, 2016

(Conversion of 1 US$= 67.38 INR )

NVS Wealth Managers

I. SAIL- THE COMPANY PROFILE AND PRODUCT PORTFOLIO

� SAIL, one of the largest steel making company in India and 24th

largest steel producer in the world, has a

market share of around 14% in the Indian steel industry.

� SAIL operates and owns five integrated steel plants at Bhilai, Durgapur, Bokaro, Rourkela and Burnpur

along with three special steel plants at Salem, Durgapur and Bhadravati along with R&D centre for Iron

& Steel (RDCIS), Centre for Engineering and Technology (CET), Management Training Institute (MTI) and SAIL Safety Organisation (SSO) located at Ranchi capital of Jharkhand.

� SAIL has the most diverse product range offered by any domestic steel company. SAIL caters to almost the entire gamut of the Hot Rolled Steel, Cold Rolled Steel, Rails, Wire Rods, Structural Steel. In addition,

Electric Resistance Welding Pipes, Spiral Welded Pipes and Silicon Steel Sheets form a part of

company’s rich product mix, offered to large and marquee institutional buyers in sectors like Defence,

Railways, Construction, Fabrication, Agricultural Equipments, Auto, Power and host of other infrastructure sectors with its world class products.

� Post Expansion the Bhilai Steel Plant would include a state of the art Universal Rail Mill, capable of producing the longest single piece rail in the world. Commissioning of this mill would provide SAIL with the

capability of producing high quality rails to meet the requirements of the Indian Railways, Metro

Projects, dedicated freight and passenger corridors as well as the exports market.

� The massive expansion of SAIL is funded by internal accrual and debt (without any increase in equity share

capital), this should hugely benefit the equity shareholders in any positive bullish cycle

in the steel industry.

Exhibit 1: SAIL Durgapur plant

NVS Wealth Managers

II. SAIL- THE MANAGEMENT VISION AND EXUDING CONFIDENCE

We are reproducing below some of the excerpts from the annual report, chairman letter, interview of the

chairman Mr. P. K. Singh with CNBC TV18 which exudes huge confidence about future of SAIL.

� “I am confident that the worst is behind us and your Company would turnaround in this financial year as most of the enablers are in place. Ramp-up of production from our new Units under modernization and expansion plan is not just increasing production and leading to better quality, but has also helped us in

reducing cost of production. Higher production from the new efficient Units and rationalizing production from cost intensive routes have manifested in the form of a reduction in variable cost of production by 10% in Q4

compared to Q1 of 2015-16 and the same trend continues. This financial year we have targeted to increase our

production and sales by more than 20% over last year.”

� “In this year we shall be completing the balance modernization and expansion projects in our Bhilai Steel Plant. The facilities include a state of the art Universal Rail Mill capable of producing the longest single piece rail

in the world. Commissioning of this mill would provide SAIL with the capability of producing high quality

rails to meet the requirements of the Indian Railways, Metro projects, dedicated freight & passenger

corridors as well as the exports market.”

� “Despite the present challenges, India's long-term outlook for the steel sector continues to be bright. The Government of India is taking appropriate steps to bolster the growth of the sector. In the Union Budget 2016-

17, a sum of Rs. 2,18,000 crore has been earmarked for infrastructure like roads and railways. Such a scenario augers well for the domestic steel sector. Other initiatives of the Government such as Housing for All

by 2022, Power for All by 2019, 100 Smart Cities by 2022 and Atal Mission for Rejuvenation & Urban Transformation (AMRUT) are likely to drive steel demand in the Country significantly.”

� “Besides the ongoing Modernization and Expansion Program, which is on the verge of completion, we have taken up new projects to improve our product mix and profitability. The significant one being installation

of a 3.0 MT per annum capacity 2250 mm wide Hot Strip Mill in our Rourkela Steel Plant. This mill scheduled to be commissioned in 2018 will enable us to produce very high quality hot rolled coils including

advanced high strength grades for the growing automotive industry in the Country.”

� “Our Sales used to be around 12 -13 million. This year we will cross 14 million tone sales. However, in the subsequent year there will be quantum jump in the production as well as in the sales. Our exports this year, we are doubling our exports and this trend will continue next year also. We would like to see that at least 10

percent of our production, we should be able to export.”

� “You will find that our production rise is almost phenomenal. It is more than almost 15 percent rise

production in this financial year compared to last year. So this as per the targets we have taken. Largely, whatever targets we have taken, we are on track. In the next year also we are again going to take challenging target and I am very confident, my entire team is very confident seeing the last one year performance that

we are going to achieve that”

� “We are under going through process of ramping up and this is a challenging time for SAIL. Nevertheless, we

are quite confident and quickly you will find that lot of the improvement in the production volumes will

come from the newer units.”

� “Our plan is today we will be achieving after the recent wave of modernisation is complete and ramping process

is complete, we will reach around 21 million tonne of finished steel capacity. Our plan is to achieve 50

million tonne.”

NVS Wealth Managers

� “I would like to thank the Government of India for stepping in at this critical juncture and undertaking

necessary corrective trade measures. The Government introduced the Minimum Import Price (MIP)

mechanism in February 2016, to curb dumping of steel in the country.”

� “The products being manufactured by our new rolling mills have been received well by the customers and it is

our constant endeavor to add more and more value added grades from these mills. In conjunction with

increased production, focus is being given to efficient and strategic marketing for improving sales and

realizations.”

� “With regard to the raw materials security of your Company, the entire requirement of iron ore is being met

from the captive mines. The capacities of existing iron ore mines are being expanded and new iron ore mines are being developed to meet the increasing requirement of iron ore. We have been allotted the Parbatpur

Coking Coal block in Jharkhand which will add to our coking coal security. We intend to commence production from this block at the earliest after the approval of the revised mine plan based on simultaneous extraction of coking coal by SAIL and Coal Bed Methane (CBM) by ONGC.”

All these indications point to a bright and an exciting future for SAIL.

III. GLOBAL STEEL SCENARIO

� In 2015, world steel production stood at 1,623 MT, a decline of 2.8% from the year 2014. From January - November 2016, the world steel production stood at 1,468 MT and is estimated to finish the year end at 1,600

MT which shows a degrowth of 1.2%. India is the third largest producer of steel in the world next to

China and Japan, which registered a growth of 2.6% overtaking United States of America which saw a

decline of 10.5% to become the third largest producer of steel with the total production standing at

around 90 MT for the Period of January 2016 – November 2016. China continues to dominate the global crude steel production accounting for almost 50% of total production. In 2015, China produced 804 MT of crude steel, down by 2.3% as compared to 2014.

� The global steel demand decreased by 0.8% to 1,488 MT in 2016, followed a contraction of 3.0% in 2015. In 2017, World Steel Association (WSA) has forecast that global steel demand will grow by 0.4%. The steel industry environment remains challenging, with escalated uncertainties driven by geopolitical situations in various parts of the world. Recently the UK referendum outcome has further raised uncertainty on the long-awaited recovery of investment in the EU.

� A better than expected forecast for China, along with continued growth in emerging economies, will help the

global steel industry to move back to a positive growth path for 2017. We expect this growth path to be slightly weak due to the continued rebalancing in China and also weak recovery in the developed economies. Also, on a positive note, as per the WSA, steel demand in emerging and developing economies excluding

China is expected to grow at 4% in 2017 thanks to the resilent emerging Asian countries and stabilization

of commodity prices.

� The per capita steel consumption in India is currently pegged at 61 Kgs as compared to to 515 Kgs in China,

516 Kgs in Japan, 1057 Kgs in South Korea and to world average level of 208 Kgs per annum.

NVS Wealth Managers

IV. SAIL AND INDIAN STEEL SCENARIO

� In FY 2016, crude steel production in India was around 90 MT, with the total crude steel production growing

at a CAGR of 12.61% over the last five years overtaking United States of America to become the third

largest producer of steel.

� In February 2016, the Government has imposed the Minimum Import Price (MIP) mechanism on imports of 173 steel items, to curb dumping of steel in the country. The MIP conditions laid down in the Notification are valid for six months from the date of notification or until further orders, whichever is earlier. The notification covers all major flat and long steel products. Further, in March 2016, the Government has extended the Safeguard Duty on HRC imports that was placed in September 2015, till March 2018. However, the Duty would be reduced to 10% in stages over the next two years. Further, during April, 2016, the Government of India

has initiated Countervailing Duty/Anti-subsidy investigation on imports of certain "Hot Rolled and Cold

Rolled Stainless Steel Flat Products" from China. It is largely believed that the cumulative impact of these recent and other existing policy measures would lead to further reduction in imports into the Country and thus boost the local Steel Sector. In fact this is largely helped the domestic steel industry in securing the remunerative prices and capture the gradual growth in demand in the country.

� During FY2016, the crude steel production saw a growth of around 0.4% to 89.3 MT. However the finished steel production registered a decline of 1.1% leading to import of around 11.2 MT due to an ever growing demand and supply gap. The imports saw a growth of 20.2%. With the growth of steel production in India in times to come, we expect this gap to reduce thus giving a much needed thrust to the domestic steel producers especially the big players like SAIL.

� Easy availability of low cost manpower and presence of abundant iron ore reserves (SAIL has 100% access to their own captive mine for Iron ore) make India competitive in global set up.

� As per IBEF Market size of Indian steel sector is bound to grow at a CAGR of 14% from 92.5 MT in 2015 to

300 MT in 2025.

V. SAIL- DEMAND DRIVERS

� Urbanisation directly influences steel consumption. India is presently only about 31% urban and with

higher migration, newer centres of development and Government programmes such as the 100 Smart

Cities by 2022 and Housing for All (as per union budget 2017-18, 1 Cr affordable houses for All by 2019), the rate of urbanisation and urban renewal is expected to rise significantly in the near-future thus fostering growth of steel in country. Such a scenario benefits the domestic steel sector. Other initiatives of the Government such as Make in India, Power for All by 2019 and Atal Mission for Rejuvenation & Urban

Transformation (AMRUT) are likely to drive steel demand in the Country significantly.

� Demographic trends further support the case for increasing steel demand in India. Each year approximately 12 mn people join the workforce in India. There is a corresponding increase in demand for housing, transportation, consumer goods and public infrastructure, all of which are major drivers for steel demand.

� Union Budget 2017-18 has allocated a sum of Rs. 3,96,135 cr for infrastructure like roads, railways, ports,

airports etc. This will aid the demand for steel going forward and SAIL being one of the largest steel

producer is ought to be the beneficiary in coming years.

� The big steel producers tend to be a big automobile producing countries. As is well known, India is becoming

auto hub in the world where many global auto companies have set up/ will be setting up plants such as

VW, Suzuki, Toyota, Honda, etc. With India automobile industry witnessing a rebound in demand and growing at the rate of 9.4% CAGR, such a scenario augurs well for the domestic steel sector and the demand for steel is going to increase in coming years. India is expected to reach world average per capita

consumption of steel in coming 10 years and this should hugely benefit SAIL in coming years.

NVS Wealth Managers

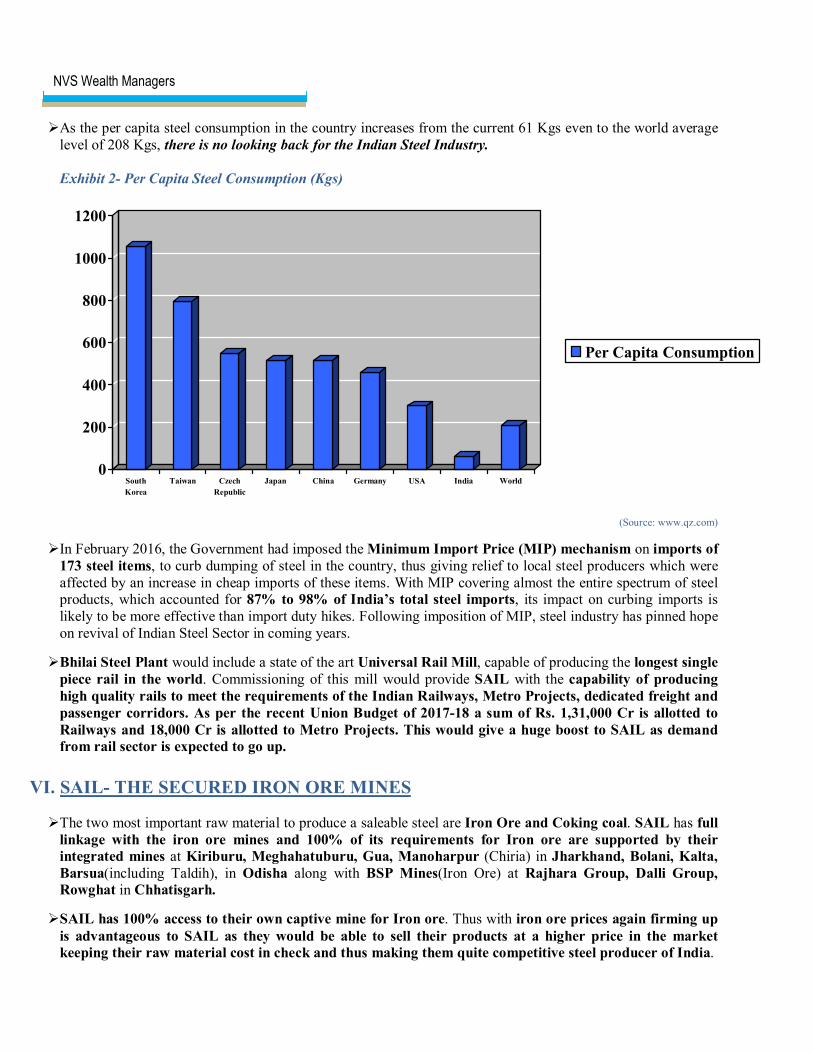

� As the per capita steel consumption in the country increases from the current 61 Kgs even to the world average level of 208 Kgs, there is no looking back for the Indian Steel Industry.

Exhibit 2- Per Capita Steel Consumption (Kgs)

0

200

400

600

800

1000

1200

South

Korea

Taiwan Czech

Republic

Japan China Germany USA India World

Per Capita Consumption

(Source: www.qz.com)

� In February 2016, the Government had imposed the Minimum Import Price (MIP) mechanism on imports of

173 steel items, to curb dumping of steel in the country, thus giving relief to local steel producers which were affected by an increase in cheap imports of these items. With MIP covering almost the entire spectrum of steel products, which accounted for 87% to 98% of India’s total steel imports, its impact on curbing imports is likely to be more effective than import duty hikes. Following imposition of MIP, steel industry has pinned hope on revival of Indian Steel Sector in coming years.

� Bhilai Steel Plant would include a state of the art Universal Rail Mill, capable of producing the longest single

piece rail in the world. Commissioning of this mill would provide SAIL with the capability of producing

high quality rails to meet the requirements of the Indian Railways, Metro Projects, dedicated freight and

passenger corridors. As per the recent Union Budget of 2017-18 a sum of Rs. 1,31,000 Cr is allotted to

Railways and 18,000 Cr is allotted to Metro Projects. This would give a huge boost to SAIL as demand

from rail sector is expected to go up.

VI. SAIL- THE SECURED IRON ORE MINES

� The two most important raw material to produce a saleable steel are Iron Ore and Coking coal. SAIL has full

linkage with the iron ore mines and 100% of its requirements for Iron ore are supported by their

integrated mines at Kiriburu, Meghahatuburu, Gua, Manoharpur (Chiria) in Jharkhand, Bolani, Kalta,

Barsua(including Taldih), in Odisha along with BSP Mines(Iron Ore) at Rajhara Group, Dalli Group,

Rowghat in Chhatisgarh.

� SAIL has 100% access to their own captive mine for Iron ore. Thus with iron ore prices again firming up

is advantageous to SAIL as they would be able to sell their products at a higher price in the market

keeping their raw material cost in check and thus making them quite competitive steel producer of India.

NVS Wealth Managers

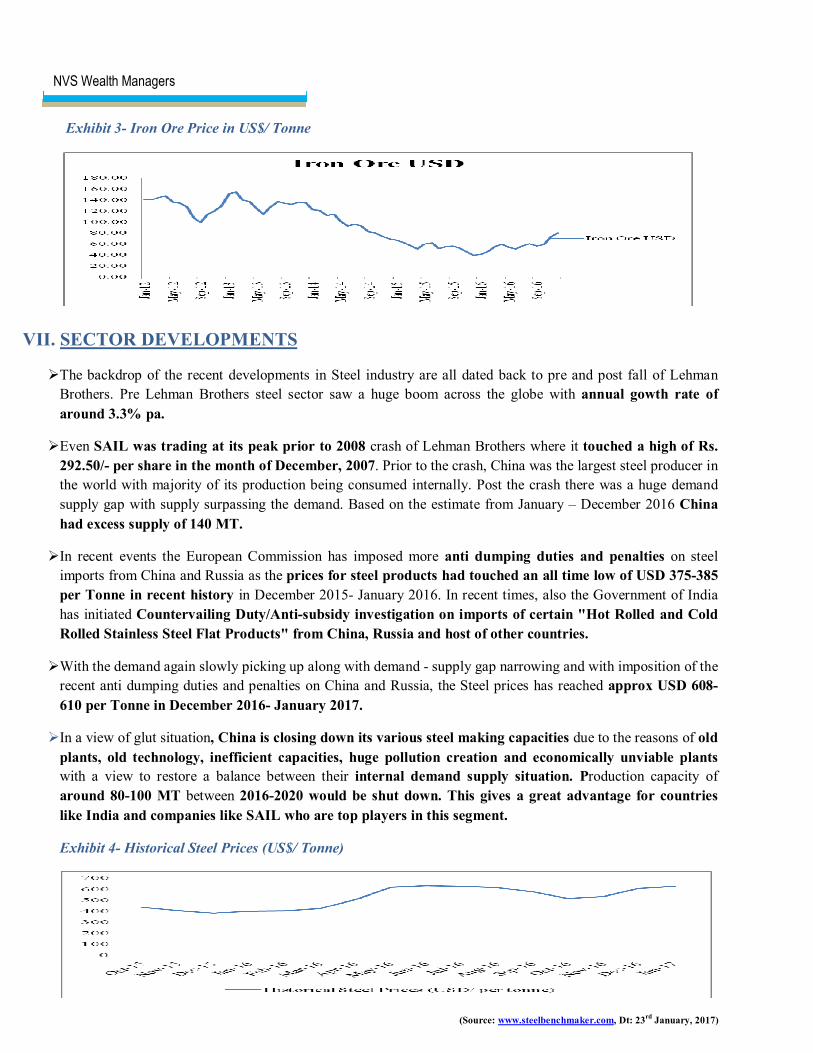

Exhibit 3- Iron Ore Price in US$/ Tonne

VII. SECTOR DEVELOPMENTS

� The backdrop of the recent developments in Steel industry are all dated back to pre and post fall of Lehman

Brothers. Pre Lehman Brothers steel sector saw a huge boom across the globe with annual gowth rate of

around 3.3% pa.

� Even SAIL was trading at its peak prior to 2008 crash of Lehman Brothers where it touched a high of Rs.

292.50/- per share in the month of December, 2007. Prior to the crash, China was the largest steel producer in

the world with majority of its production being consumed internally. Post the crash there was a huge demand

supply gap with supply surpassing the demand. Based on the estimate from January – December 2016 China

had excess supply of 140 MT.

� In recent events the European Commission has imposed more anti dumping duties and penalties on steel

imports from China and Russia as the prices for steel products had touched an all time low of USD 375-385

per Tonne in recent history in December 2015- January 2016. In recent times, also the Government of India

has initiated Countervailing Duty/Anti-subsidy investigation on imports of certain "Hot Rolled and Cold

Rolled Stainless Steel Flat Products" from China, Russia and host of other countries.

� With the demand again slowly picking up along with demand - supply gap narrowing and with imposition of the

recent anti dumping duties and penalties on China and Russia, the Steel prices has reached approx USD 608-

610 per Tonne in December 2016- January 2017.

� In a view of glut situation, China is closing down its various steel making capacities due to the reasons of old

plants, old technology, inefficient capacities, huge pollution creation and economically unviable plants

with a view to restore a balance between their internal demand supply situation. Production capacity of

around 80-100 MT between 2016-2020 would be shut down. This gives a great advantage for countries

like India and companies like SAIL who are top players in this segment.

Exhibit 4- Historical Steel Prices (US$/ Tonne)

(Source: www.steelbenchmaker.com, Dt: 23rd

January, 2017)

NVS Wealth Managers

VIII. SAIL- MAPPING OUT ITS PATH TO SUCCESS

� At present, the installed capacity of the company is 14.3 MT and post modernization the envisaged capacity is bound to increase to 21.4 MT. As per SAIL Chairman Mr. P.K.Singh, SAIL to maintain its current

dominance in the domestic market and to meet the future challenges, is working towards its long term strategic plan ‘Vision 2025’, which will steer the company towards the target of 50 MT of Hot Metal

capacity.

� The company is aiming for a increased market share (current around 14%), improved product mix/ higher

proportion of value added products, need for eliminating technological obsolescence, achieving energy savings, enriching product mix, reducing pollution, developing mines and collieries, introducing customer centric processes and developing matching infrastructure facilities and also enhanced pollution control measures. These measures besides achieving higher production targets also will address cost saving, hence

improving company’s margins.

� A total capital expenditure of over Rs.62,000 Cr has been made for expansion of current facilities, to

increase value added products, technological upgradation & modernization, de-bottlenecking of existing

plants and also a capex plan of Rs.10,624 Cr has been made for augmentation of raw material facilities. For FY17, a total capex plan of Rs.4,000 Cr is planned, out of which Rs.2,374 Cr is made in H1FY17.

� On the Raw material front also, the company is ramping up its existing facilities of iron ore to meet the

requirement of iron ore post ongoing phase of expansion. The capacity of exisiting mines at Kiriburu, Meghahutuburu, Gua and Bolani are being ramped up. Also three new pellet plants of 7 MT per annum

capacity have been planned for better utilization of Iron ore fines. The current Iron ore consumption is

around 24 MT per annum, and post expansion the captive Iron ore consumption is going to be 39 MT per annum. The entire requirement of the increased capacity shall be met through captive mines and the timeline for mines expansion is expected to be in line with steel plants expansion.

� The company’s 86% of coal requirement is imported and 14% is indigenous, where in, 90% of imported coal is from Australia and domestic coal is largely sourced from Coal India Ltd. SAIL has an existing captive coking coal production of nearly 0.5 MT per annum. The company is currently exploring new linkages/

acquisitions.

IX. SAIL- STRATEGIC INITIATIVES

SAIL has adopted multi pronged approach that includes organic growth, brown field projects, technology

leadership through strategic alliances, ensuring raw material security through acquisition and

development of new mines, diversifying in allied areas, R&D Master Plan and a technology plan. Such a strategy of investing in different areas will mitigate risk and help SAIL in maximising returns. Over a span of last few years, SAIL has formed joint venture companies in different areas viz. power generation, rail

transportation, slag cement production, securing supplies of key input raw materials (like cooking coal from indigenous as well as imported sources), etc. New joint venture in the area of production of specialised

products to cater to automotive sector, etc. is being envisaged.

The strategic initiatives taken by SAIL are as follows:

� With an aim to develop large capacity mega steel projects in the country to the tune of 300 MT of crude steel

by 2025-26, Ministry of Steel has evolved a concept of developing Ultra Mega Steel Plants. SAIL is participating along with NMDC and Government of Chhattisgarh for setting up of an Ultra Mega Steel

Plant having capacity 6 MT per annum in Bastar, Chhattisgarh. To shore up the same, SAIL along with NMDC, IRCON and Government of Chhattisgarh is developing a Rail Corridor from Rowghat to

Jagdalpur in the state of Chhattisgarh to facilitate faster supply of iron ore from their Rowghat Mines and finished products to and fro from their Bastar Project. Also the Rail Corridor will connect the Tribal area of

Bastar directly to the National Railways. The Rail Corridor would result in ROI of 7% per annum.

NVS Wealth Managers

� An MOU was singed forming a JV between SAIL and ArcelorMittal for exploring the possibility for setting

up an automotive steel manufacturing facility in India. The JV will construct a state of the art COLD

ROLLING MILL (CRM) and the downstream finishing facility in India which will offer technologically

advanced steel products to India’s rapidly growing automotive sector. The input material for the CRM would come from SAIL’s new Hot Strip Mill being set up at Rourkela Steel Plant in the state of Odisha,

with an approx. capacity of 3 MT per annum. The annual target of CRM is expected to be at 1.5 MT per

annum.

X. SWOT ANALYSIS

NVS Wealth Managers

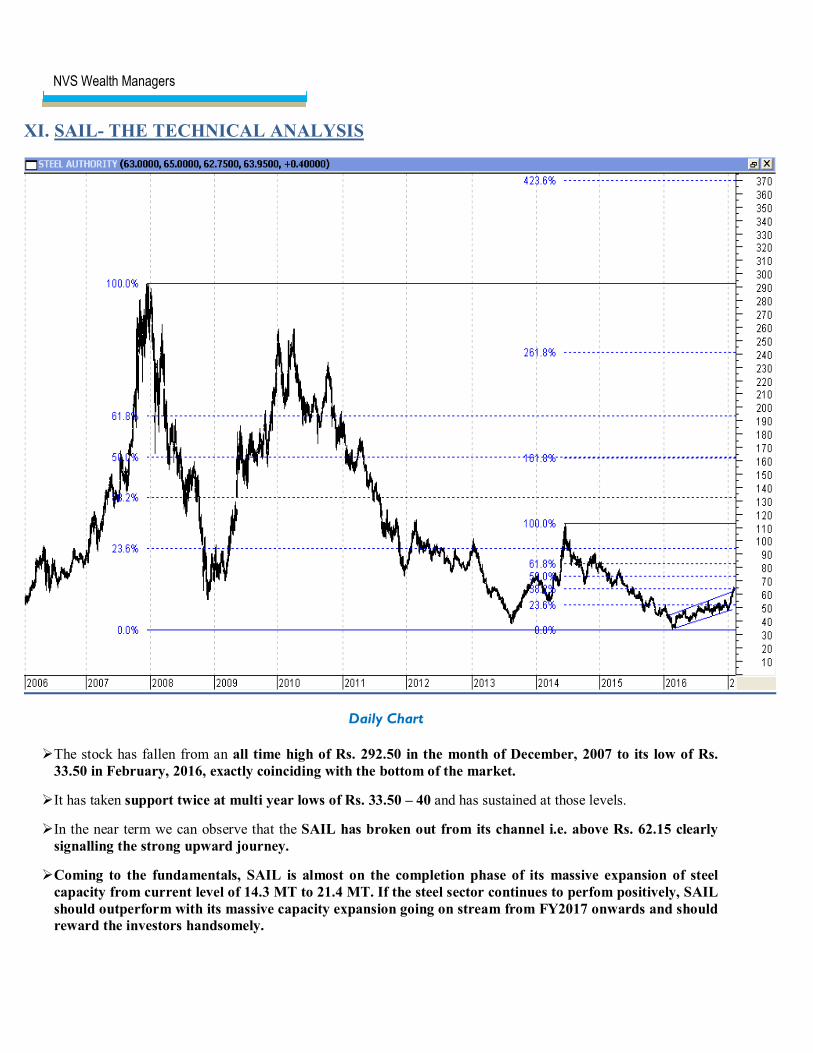

XI. SAIL- THE TECHNICAL ANALYSIS

Daily Chart

� The stock has fallen from an all time high of Rs. 292.50 in the month of December, 2007 to its low of Rs.

33.50 in February, 2016, exactly coinciding with the bottom of the market.

� It has taken support twice at multi year lows of Rs. 33.50 – 40 and has sustained at those levels.

� In the near term we can observe that the SAIL has broken out from its channel i.e. above Rs. 62.15 clearly

signalling the strong upward journey.

� Coming to the fundamentals, SAIL is almost on the completion phase of its massive expansion of steel

capacity from current level of 14.3 MT to 21.4 MT. If the steel sector continues to perfom positively, SAIL

should outperform with its massive capacity expansion going on stream from FY2017 onwards and should

reward the investors handsomely.

NVS Wealth Managers

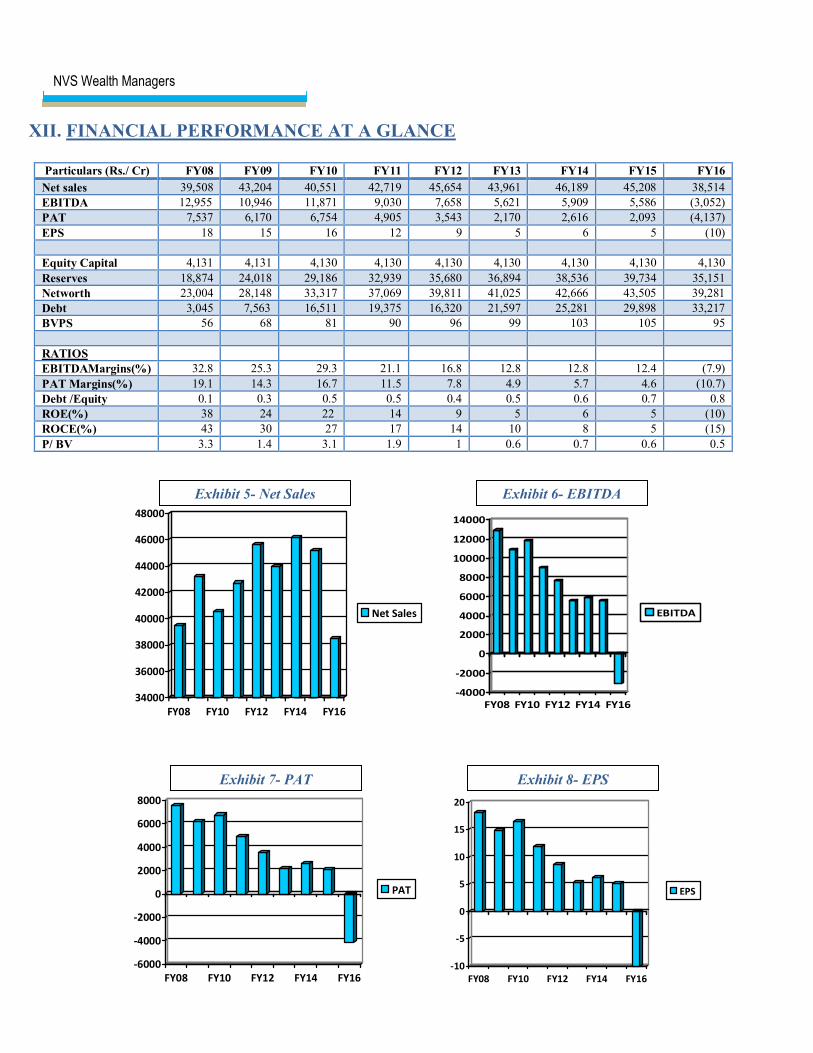

XII. FINANCIAL PERFORMANCE AT A GLANCE

Particulars (Rs./ Cr) FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Net sales 39,508 43,204 40,551 42,719 45,654 43,961 46,189 45,208 38,514

EBITDA 12,955 10,946 11,871 9,030 7,658 5,621 5,909 5,586 (3,052)

PAT 7,537 6,170 6,754 4,905 3,543 2,170 2,616 2,093 (4,137)

EPS 18 15 16 12 9 5 6 5 (10)

Equity Capital 4,131 4,131 4,130 4,130 4,130 4,130 4,130 4,130 4,130

Reserves 18,874 24,018 29,186 32,939 35,680 36,894 38,536 39,734 35,151

Networth 23,004 28,148 33,317 37,069 39,811 41,025 42,666 43,505 39,281

Debt 3,045 7,563 16,511 19,375 16,320 21,597 25,281 29,898 33,217

BVPS 56 68 81 90 96 99 103 105 95

RATIOS

EBITDAMargins(%) 32.8 25.3 29.3 21.1 16.8 12.8 12.8 12.4 (7.9)

PAT Margins(%) 19.1 14.3 16.7 11.5 7.8 4.9 5.7 4.6 (10.7)

Debt /Equity 0.1 0.3 0.5 0.5 0.4 0.5 0.6 0.7 0.8

ROE(%) 38 24 22 14 9 5 6 5 (10)

ROCE(%) 43 30 27 17 14 10 8 5 (15)

P/ BV 3.3 1.4 3.1 1.9 1 0.6 0.7 0.6 0.5

34000

36000

38000

40000

42000

44000

46000

48000

FY08 FY10 FY12 FY14 FY16

Net Sales

-4000

-2000

0

2000

4000

6000

8000

10000

12000

14000

FY08 FY10 FY12 FY14 FY16

EBITDA

-6000

-4000

-2000

0

2000

4000

6000

8000

FY08 FY10 FY12 FY14 FY16

PAT

-10

-5

0

5

10

15

20

FY08 FY10 FY12 FY14 FY16

EPS

Exhibit 5- Net Sales Exhibit 6- EBITDA

Exhibit 7- PAT Exhibit 8- EPS

NVS Wealth Managers

Critical Analysis

� FY 2008 was a milestone year for SAIL with overall improvement in operational areas and financial performance. This was the first time SAIL produced more than 14 MT of crude steel and 13 MT of saleable

steel. SAIL achieved a mammoth PBT of Rs. 11,469 cr and PAT of Rs. 7,537 cr, accomplishing an all time

high market capitalization of little over Rs. 1,20,000 cr . While an improved demand for iron & steel helped in recording better financial performance, significant improvements also came by way of several internal initiatives viz. higher capacity utilization at 118%, record production through continuous cast route, best

ever performance in key techno-economic parameters like overall energy consumption and coke rate,

highest production and sales of value added products, continuous emphasis on cost reduction and prudent

fund management. The PBT rose from Rs. 9,423 cr in FY 2007 to a high of Rs. 11,469 cr in FY 2008.

� Till FY 2010 SAIL saw a strong and consistent financial performance, where in PBT was in the range of Rs.

9,400-11,500 cr. Post FY 2010 the performance of SAIL decreased in a gradual manner. The profitability was affected mainly due to adverse impact of input prices, royalty on minerals, salaries and wages, higher

interest cost and depreciation. FY 2016 was the worst year in recent history for SAIL. The price of SAIL plunged to a low of Rs. 33.50 in February, 2016, market capitalization plunging to an all time low of Rs. 13,850 cr.

� Revenue grew at a CAGR of 1.5% over the last 10 years (FY08-Rs.39,508cr). There was a major de-growth in FY16 primarily because of decrease in Net Sales Realisaton of Saleable Steel of 5 integrated Steel Plants by about 20%. The prices of steel products kept falling throughout the year and touched an all time low in recent years around USD 375-385 PMT due to fall in global steel prices leading to predatory imports from China,

Japan, Korea, etc. The steel sector was facing headwinds in the form of an overall muted steel demand scenario both domestically and globally. However there was an increase in the price realization after

imposition of MIP w.e.f 5th

February, 2016.

� SAIL has continued its thrust for optimum utilization of funds by better fund management. This included replacement of high cost short term loans with low cost debts, timely repayment of loans including interest, strategic parking of surplus funds with scheduled banks, advance actions for future fund raising, etc. to meet growth objectives

� After the imposition of MIP mechanism and curbing the dumping of steel from China, Russia and other

countries, the prices has bottomed out in January 2016 and has gradually increased to a high of USD 608-610 PMT in the month of December 2016 - January 2017. In fact this has largely helped the domestic steel industry in securing the remunerative prices and capture the gradual growth in demand in the country.

XIII. Valuation & Recommendation � SAIL is in the final stage of completing its expansion and modernization program involving a mammoth capex

of over Rs. 62,000 Cr which will augment its steel making capacity from 14.3 MT to 21.4 MT. The expanded capacity should come on stream from FY 2017-18 onwards in phased manner, ushering the exciting times

for the company stakeholders.

� SAIL crashed from high of Rs. 292.5 per share in December, 2007 (little over Rs. 1,20,000 cr in market

capitalization) to a low of Rs. 33.5 per share in February, 2016 (Rs. 13,850 cr in market capitalization)

and is currently around Rs.65-66 per share (around Rs. 26,850 in market capitalization). SAIL has

currently the BV per share of Rs. 95 per share as against the CMP of Rs. 65, making it available at an

attractive valuation of only 0.68x the BV- A MUST ACCUMULATE FOR ALL INVESTOR.

It will be interesting to note that JSW steel, one of the peer, has a BV of Rs. 69 per share and is currently

trading at Rs. 190-200 per share, with a P/ Bv at a 2.8x, indicating that SAIL has strong potential for

appreciation from the present level.

NVS Wealth Managers

� Realisations have also increased from Rs.29,500 per tonne for HRC in January 2016 to Rs.42,500 per

tonne in December 2016 and from Rs.34,500 per tonne in January 2016 to Rs.48,000 per tonne in

December 2016 for CRC it is therefore obvious that realisations have substantialy improved and same should get positively refelected gradually in the performance of company from H2FY2017 onwards.

� When we compare the financial performance and stock market performance with its peers like Tata Steel

and JSW Steel, we believe SAIL has huge potential to reward its investors with strong performance and

the journey has just begun.

“SAIL - BEST IS YET TO COME”

Source:

� SAIL Annual Report FY2016

� SAIL Investor Presentation

� World Steel Association- World Steel Output 2016-17

� IBEF Steel Report November 2016

� SAIL Chairman Mr. P. K. Singh Interview with CNBC TV-18.

Glossary:

� HRC/ HR: Hot Rolled Coil

� CRC/ CR: Cold Rolled Coil

� IBEF: India Brand Equity Foundation

� MT: Million Tonne

NVS Wealth Managers

Disclosures and Disclaimers:

This report has been prepared and issued by NVS Wealth Managers Pvt. Ltd. "SEBI registered Investment Advisers".

NVS Wealth Managers (NVS) is a subsidiary of NVS Brokerage Pvt. Ltd. (Stock Broking member of BSE & NSE,

registered with SEBI). This report is prepared and distributed by NVS for information purposes only and neither the

information contained herein nor any opinion expressed should be construed or deemed to be construed as solicitation

or as offering advice for the purposes of the purchase or sale of any security, investment or derivatives. The information

and opinions contained in the Report were considered by NVS to be valid when published. The report also contains

information provided to NVS by third parties. The source of such information will usually be disclosed in the report.

Whilst NVS has taken all reasonable steps to ensure that this information is correct, NVS does not offer any warranty as

to the accuracy or completeness of such information. The ownership of any investment decision(s) shall exclusively vest

with the investor after analyzing all possible risk factors and by exercise of his/her its independent discretion & NVS

shall not be liable or held liable for any consequences thereof. . Prices are subject to market risks which may result in

appreciation or depreciation of investments. Past performance is not necessarily indicative of future results.

This report does not have regard to the specific investment objectives, financial situation and the particular needs of any

specific person who may receive this report. Investors must undertake independent analysis with their own legal, tax

and financial advisors and reach their own conclusion regarding the appropriateness of investing in any securities or

investment strategies discussed or recommended in this report and should understand that statements regarding future

prospects may not be realized. The reports issued from NVS are non-discretionary and non-participation basis. In no

circumstances it is to be used or considered as an offer to sell or a solicitation of any offer to buy or sell the Securities

mentioned in it. The information contained in the reports may have been taken from trade and statistical services and

other sources, which we believe are reliable. NVS or any of its group/associate/affiliate companies do not guarantee that

such information is accurate or complete and it should not be relied upon as such. Any opinions expressed reflect

judgments at this date and are subject to change without notice.

Important: These disclosures and disclaimers must be read in conjunction with the report of which it forms part. Receipt

and use of the report is subject to all aspects of these disclosures and disclaimers. Additional information about the

issuers and securities discussed in this report is available on request.

Certifications: The analyst(s) who prepared this report hereby certifies that the views expressed in this report accurately

reflect the analyst’s personal views about all of the subject issuers and/or securities, that the analyst/entity/associate

have no known material conflict of interest, no financial interest and no part of the analyst’s compensation was, is or

will be, directly or indirectly, related to the specific views or recommendations contained in this report. The analyst has

not served as an officer, director or employee of the subject company. The analyst and related parties have not dealt in

shares of the subject company before 30 days of the report being made public and will not deal for the next 5 days, as

per SEBI (Research Analyst) Regulations, 2014.

Independence: NVS has established information barriers between Research & other business groups. As a result NVS

does not disclose certain client relationships with or compensation received from, subject issuers in these reports. NVS

has not had an investment banking relationship with, and has not received any compensation for investment banking

services from, the subject issuers in the past twelve (12) months, and NVS does not anticipate receiving or intend to

seek compensation for investment banking services from the subject issuers in the next three (3) months. The analyst/

entity or its associates have not received any compensation for products or services other than investment banking or

merchant banking or brokerage services from the subject company in the past twelve months. The analyst/ entity has not

managed or co-managed public offering of securities for the subject company in the past twelve months.

NVS Wealth Managers

The analyst or its associates have not received any compensation or other benefits from the Subject Company or third

party in connection with the report. The subject company is not and was not a client during twelve months preceding the

date of distribution of the report.

The analyst or NVS is not a market maker in the securities mentioned in this report, although it or its affiliates may hold

either long or short positions in such securities. NVS or the analysts do not hold more than 1% of the shares of the

company (ies) covered in this report at any time immediately preceding the date of publication of the report. However,

NVS, associate companies and their clients might be holding this stock in their personal capacities.

Suitability and Risks: This report is for informational purposes only and is not tailored to the specific investment

objectives, financial situation or particular requirements of any individual recipient hereof. Certain securities may give

rise to substantial risks and may not be suitable for certain investors. . It is therefore important carefully/personally

review your entire investment portfolio to ensure that it meets your investment goals and is well within your risk

tolerance, including your objectives for asset and issuer diversification.

The value of any security may be positively or adversely affected by changes in foreign exchange or interest rates, as

well as by other financial, economic or political factors. Past performance is not necessarily indicative of future

performance or results.

Sources, Completeness and Accuracy: The material herein is based upon information obtained from sources that NVS

and the analyst believe to be reliable, but neither NVS nor the analyst represents or guarantees that the information

contained herein is accurate or complete and it should not be relied upon as such. Opinions expressed herein are current

opinions as of the date appearing on this material and are subject to change without notice. Furthermore, NVS is under

no obligation to update or keep the information current.

Copyright: The copyright in this report belongs exclusively to NVS. All rights are reserved. Any unauthorized use or

disclosure is prohibited. No reprinting or reproduction, in whole or in part, is permitted without NVS’s prior consent,

except that a recipient may reprint it for internal circulation only and only if it is reprinted in its entirety.

Caution: Risk of loss in trading can be substantial. You should carefully consider whether trading is appropriate for you

in light of your experience, objectives, financial resources and other relevant circumstances.

Method: We have not rated the stock.

Rating Scale: This is a guide to the rating system used by our team. Our rating system comprises six rating categories,

with a corresponding risk rating.

* WE HAVE BOUGHT SHARES OF SAIL FOR US AND OUR CLIENTS AT RS. 49-51 LEVELS BEFORE 31ST DECEMBER, 2016 AND AS

PER THE REGULATORY REQUIREMENTS WE ARE PUBLISHING THIS REPORT AFTER A GAP OF 30 DAYS.

Contact Details:

Corporate Office Address: 702, Embassy Centre, Nariman Point, Mumbai – 400 021 • Tel.:+91 22 6631 5511/12,

Fax: +91 22 61539134 • Email: [email protected] • Website: www.nvswealthmanagers.com