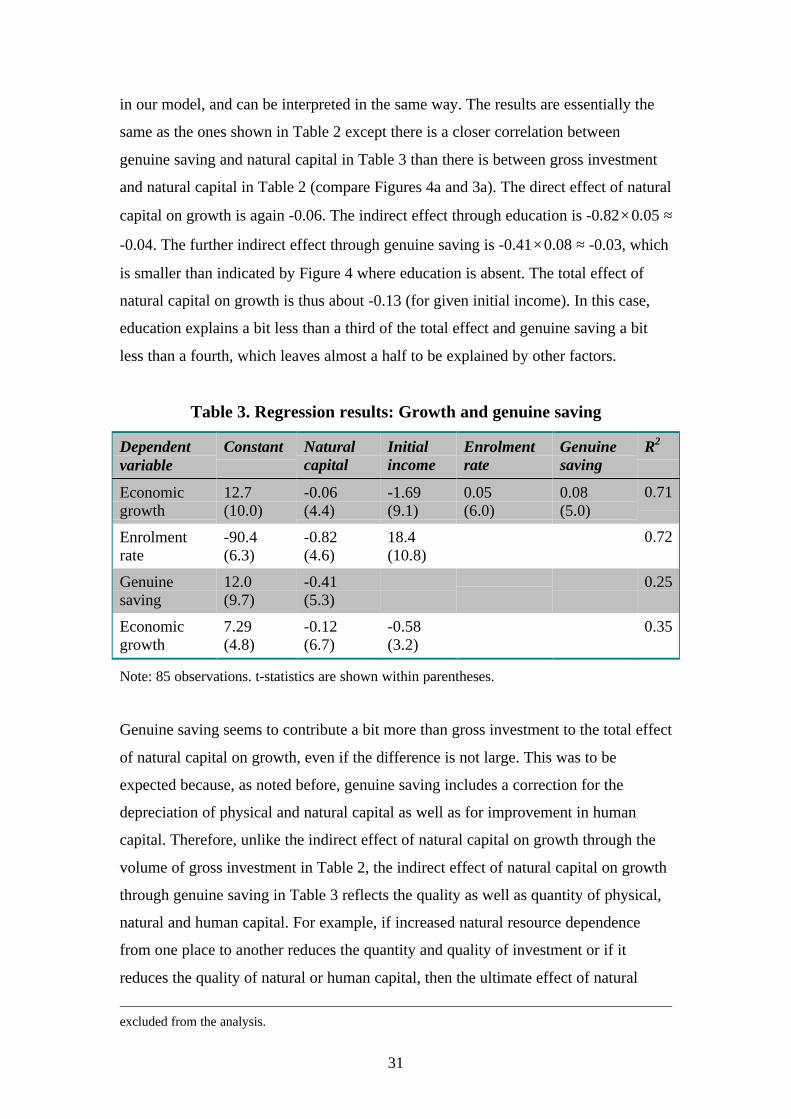

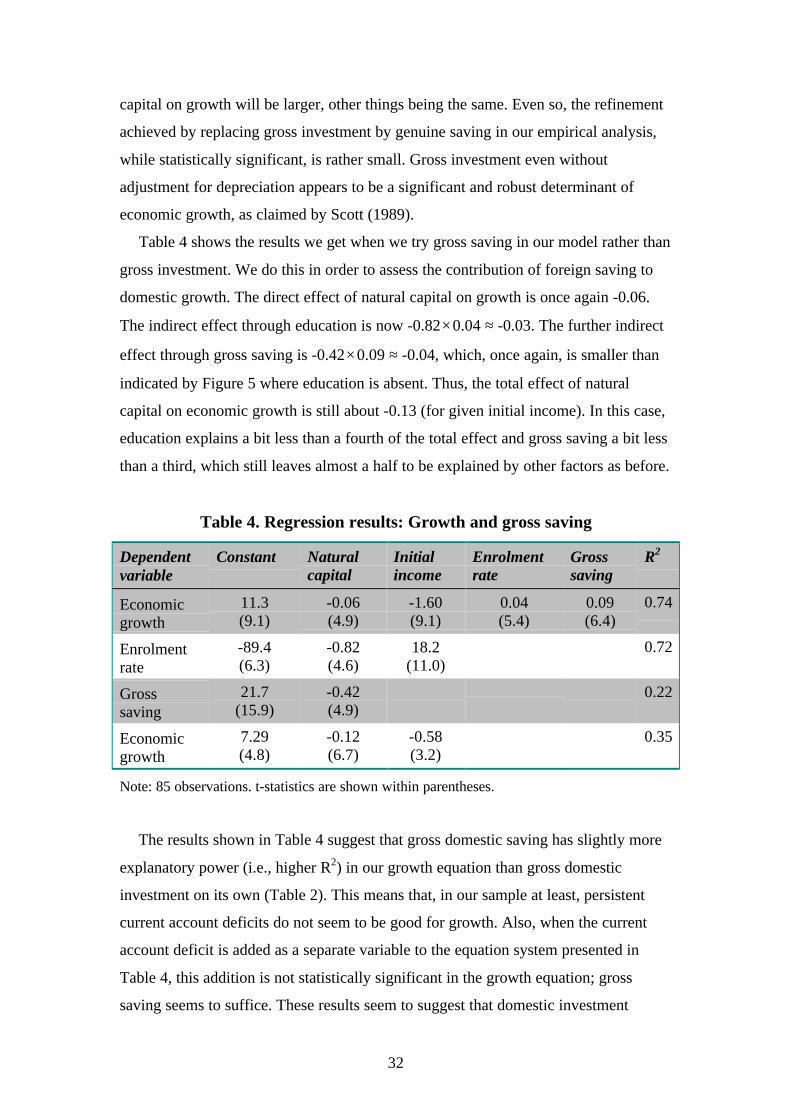

natural resources and economic growth: the role of investment

TRANSCRIPT

Natural Resources and Economic Growth:The Role of Investment

by

Thorvaldur Gylfason and Gylfi Zoega*

Revised June 2001

Abstract

This paper begins by a brief review of empirical evidence that seems to indicate thateconomic growth since 1965 has varied inversely with natural resource abundance orintensity across countries. The paper then proposes a new linkage between naturalresources and economic growth, through saving and investment. When the share ofoutput that accrues to the owners of natural resources rises, the demand for capitalfalls and this leads to lower real interest rates and less rapid growth. Moreover, theanalysis shows that the discrepancy between the privately and socially optimal ratesof growth increases with the natural capital share. Empirical evidence from 85countries from 1965 to 1998 suggests that natural capital may on average crowd outphysical as well as human capital, thereby inhibiting economic growth. The resultsalso suggest that, across countries, heavy dependence on natural resources may hurtsaving and investment indirectly by slowing down the development of the financialsystem.

JEL: O11.

Keywords: Economic growth, natural resources, investment, genuine saving.

* Thorvaldur Gylfason is Research Professor of Economics, University of Iceland; Research Fellow,CEPR; and Research Associate, SNS—Center for Business and Policy Studies, Stockholm. Address:Faculty of Economics and Business Administration, University of Iceland, 101 Reykjavík, Iceland. Tel:354-525-4533 or 4500. Fax: 354-552-6806. E-mail: [email protected]. Gylfi Zoega is Senior Lecturer inEconomics, Birkbeck College, and Research Affiliate, CEPR. Address: Department of Economics,Birkbeck College, University of London, 7-15 Gresse Street, London W1P 2LL, United Kingdom. Theauthors are indebted to Rögnvaldur Hannesson, Ron Smith and two referees for helpful comments and

1

1. Introduction

Natural resources are an important source of national wealth around the world. Yet,

experience shows that natural riches are neither necessary nor sufficient for economic

prosperity and progress. The world’s richest countries include Hong Kong, Japan,

Singapore and Switzerland which do not owe their national wealth to nature and many

others, such as the United States and the United Kingdom, where natural resources

nowadays play only a minor role in the generation of national income.

Among developing countries, natural resources are relatively more prevalent. This

may to some extent reflect their underdevelopment: the modest size of the modern

sector of the economy makes agriculture and other natural-resource-based economic

activity relatively more important. But there are also clear examples of countries that

are genuinely rich in terms of natural resources but still have not been able to sustain

economic growth. It thus appears that the generosity of nature may sometimes –

although by no means always – turn out to be a mixed blessing. Take Botswana and

Sierra Leone, both of which produce diamonds for export. By and large, Botswana

has managed the revenue and rent stream from its main natural resource in ways that

have contributed to impressive economic growth since independence in 1966 – in

fact, the world’s highest recorded rate of growth of gross national product (GNP) per

capita from 1965 to 1998, even if it slowed down after 1990. Meanwhile, Sierra

Leone has remained mired in poverty, ravaged by crippling internal warfare as local

warlords have continued to fight for control over the diamond trade. Sierra Leone was

the world’s poorest country in 1998 according to the World Bank (2000). Apparently,

the rich supply of diamonds has turned out to be a source of domestic strife that has

both diverted precious national resources towards rent seeking of the most destructive

kind and destroyed the infrastructure and social institutions that are so important for

economic life. This example shows that the existence of natural resources can be both

a blessing and a curse to economic growth and development.

In this paper, we consider the interaction between institutions, natural resource

dependence and economic growth. In particular, we are interested in the possible

mechanisms through which natural resources can stifle capital accumulation and

growth and the conditions under which economic growth can take place in the

presence of abundant natural resources. In this context it will be interesting to

suggestions.

2

consider the experience of those countries – if any – which at some point in the past

relied on nature’s bounty but now enjoy the benefits of developed and diversified

manufacturing and service industries.

Recent empirical research suggests that an abundance of natural resources can hurt

economic growth indirectly by unleashing forces that hamper the development of the

national economy, primarily through the Dutch disease, rent seeking and neglect of

education. We will review this literature below, in Section 3. To some, these findings

may seem counterintuitive for it should, in principle, be possible to harness natural

resources without hurting national economic welfare and growth. We concur.

This paper is intended to make two main points. First, natural resource abundance

may under certain conditions – to be specified – blunt incentives to save and invest

and thereby reduce economic growth. We demonstrate this proposition by deriving

the optimal saving rate in an endogenous growth model of an economy with natural

resources and then subject it to empirical tests in a cross-sectional sample of 85

countries from 1965 to 1998. Second, on the premise that mature institutions

contribute to an efficient use of resources, including natural resources, and that poorly

developed institutions do not, we argue that natural resource abundance may also

under certain conditions – to be specified – retard the development of financial

institutions in particular and hence hamper saving, investment and economic growth

through that channel as well.

The paper proceeds as follows. Section 2 looks briefly at the empirical evidence on

natural resource dependence and economic growth. Section 3 provides a brief

overview of recent literature on the subject. In Section 4, we compare the experience

of Norway, the world’s most successful oil exporter, with that of other oil-producing

countries. In Section 5, we derive our main proposition that natural resource

dependence tends to blunt incentives to save and invest. We also distinguish between

the quantity and quality of investment. In Section 6, we summarize the data through

simple bivariate correlations between natural resource dependence, different measures

of saving and investment and economic growth. In Section 7, we then proceed to

more elaborate tests of our hypothesis by multiple regression analysis in the spirit of

the recent empirical growth literature. Section 8 summarizes our main results and

offers a few concluding comments.

3

2. Preview

A rapidly expanding body of research has attempted to discern empirical growth

relationships across countries. While aggregative and simple, such cross-sectional and

panel data sets – often covering large numbers of countries – do provide an interesting

starting point.

Figure 1 is representative of one of the empirical findings that have emerged from

some recent studies, beginning with Sachs and Warner (1995). The figure covers 85

countries, and shows a scatterplot of economic growth per capita from 1965 to 1998

and natural resource dependence as measured by the share of natural capital in

national wealth in 1994 – i.e., the share of natural capital in total capital, which

comprises physical, human and natural capital (but not social capital; see World Bank,

1997). The natural capital variable used here is close to the source: it is intended to

come closer to a direct measurement of the intensity of natural resources across

countries than the various proxies that have been used in earlier studies, mainly the

share of primary (i.e., nonmanufacturing) exports in total exports or in gross domestic

product (GDP) and the share of the primary sector in employment or the labor force.1

The latter proxies may be prone to bias due to product and labor market distortions.

The growth rate has been adjusted for initial income: the variable on the vertical axis

is that part of economic growth that is not explained by the country’s initial stage of

development, obtained from a regression of growth during 1965-1998 on initial GNP

per capita (i.e., in 1965) as well as natural capital. When we also purge the natural

capital share of that part which is explained by the country’s initial stage of

development, we get very similar results as in Figure 1. The 85 countries in the

sample are represented by one observation each for each variable under study, an

average for the entire sample period, 1965-1998 (see Table 1 and Appendix).2

1 Alas, 1994 is the only year for which the World Bank has as yet produced data on natural capital, for92 countries. In most cases, however, natural capital in 1994 is probably a pretty good proxy for naturalresource abundance in the period under review, 1965-1998. There are exceptions, true, such asMalaysia, Mauritius and Mexico, where the share of primary exports in merchandise exports decreaseddramatically from 1965 to 1998 as a result of economic diversification away from primary production.Even so, all the empirical results reported in this paper can be reproduced without significant deviationsby using the average primary export share during 1965-1998 rather than natural capital in 1994 as aproxy for natural resource abundance, and also by measuring growth in terms of GNP per worker ratherthan GNP per capita.2 The reason why there are 85 countries in the sample and not 92 is that (a) for five countries for whichestimates of natural capital exist, there are missing data on economic growth since 1965 (Bolivia,Germany, Tanzania, Uganda and Vietnam) and (b) for two countries, the available data are problematic

4

The regression line through the scatterplot in Figure 1 suggests that an increase of

about eight or nine percentage points in the natural capital share from one country to

another is associated with a decrease in per capita growth by one percentage point per

year on average.3 The relationship is also significant in a statistical sense (Spearman’s

r = -0.64), and conforms to the partial correlations that have been reported in multiple

regression analyses where other relevant determinants of growth (investment,

education, etc., as well as initial income) are taken into account.4 A similar

relationship has been reported in a number of recent studies, including Sachs and

Warner (1995, 1999), Gylfason and Herbertsson (2001), and Gylfason, Herbertsson

and Zoega (1999).

We are aware that the study of bivariate cross-sectional relationships has many

shortcomings. For one thing, such studies bypass the diversity of individual country

experiences as well as intranational developments over time. For another, they do not

distinguish cause from effect. We intend the correlations presented in this paper

merely to describe the data in ways that are consistent with the results of multiple

regression analysis that can help account for more potential sources of growth.

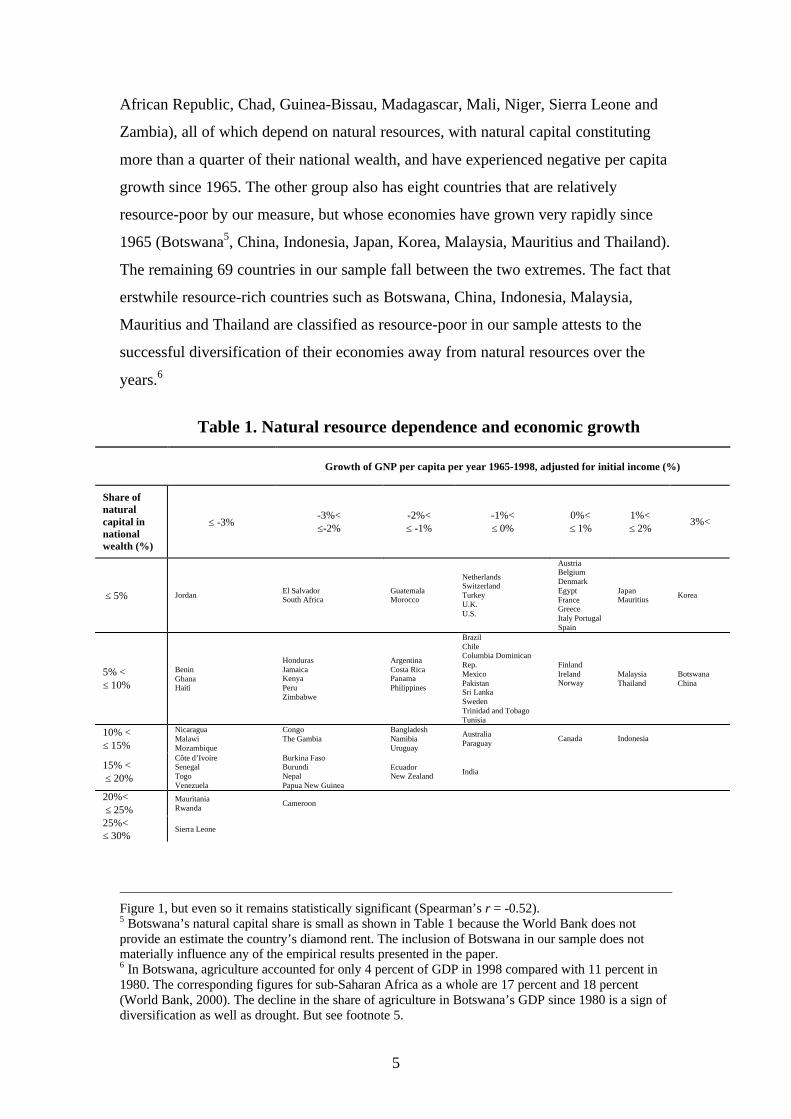

The classification of all 85 countries is presented in Table 1. The table indicates

that good growth performance appears incompatible with a share of natural resources

in excess of 15 percent of national wealth. More generally, in line with Figure 1, the

countries in our sample appear to be concentrated on the diagonal linking the south-

west and the north-east corners of the table. There are also quite a few countries above

the diagonal, with slow economic growth and a small endowment of natural

resources, including several countries in Central and South America and the

Caribbean. Perhaps more interestingly, we detect two distinct groups of countries in

Figure 1 and Table 1. The first group consists of eight African countries (Central

(Lesotho and Saudi-Arabia). Specifically, Lesotho is omitted because of its extremely low recordedgenuine saving rate (-55 percent of GDP), and Saudi-Arabia is omitted because of extreme fluctuationsin its recorded average rate of economic growth over long periods. With the exception of the latter twocountries, no outliers are excluded from the analysis, so that the sample size remains the same, 85,throughout the paper.3 There is admittedly an element of statistical bias in Figure 1 in that increased investment increasesphysical capital, thereby reducing the share of natural capital in national wealth and increasingeconomic growth. (The same point can be made about education and human capital.) This bias,however, is probably not serious because Figure 1 can be reproduced by using different measures ofnatural resource abundance, such as the share of the primary sector in the labor force (as in Gylfason,Herbertsson and Zoega, 1999) and the share of primary exports in total exports or GDP (as in Sachsand Warner, 1999).4 The correlation weakens a bit if we confine the regression to the 77 countries where the natural capitalshare is below 0.25, thus leaving out the cluster of eight observations in the southeastern corner of

5

African Republic, Chad, Guinea-Bissau, Madagascar, Mali, Niger, Sierra Leone and

Zambia), all of which depend on natural resources, with natural capital constituting

more than a quarter of their national wealth, and have experienced negative per capita

growth since 1965. The other group also has eight countries that are relatively

resource-poor by our measure, but whose economies have grown very rapidly since

1965 (Botswana5, China, Indonesia, Japan, Korea, Malaysia, Mauritius and Thailand).

The remaining 69 countries in our sample fall between the two extremes. The fact that

erstwhile resource-rich countries such as Botswana, China, Indonesia, Malaysia,

Mauritius and Thailand are classified as resource-poor in our sample attests to the

successful diversification of their economies away from natural resources over the

years.6

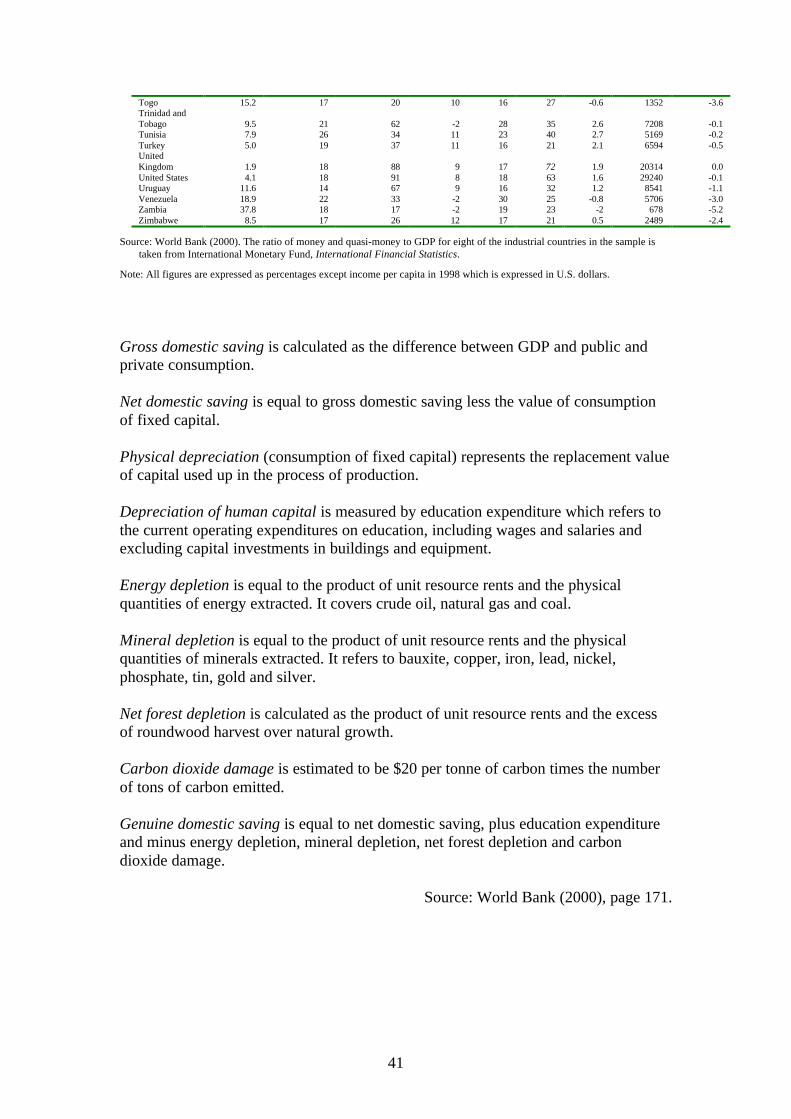

Table 1. Natural resource dependence and economic growth

Growth of GNP per capita per year 1965-1998, adjusted for initial income (%)

Share ofnaturalcapital innationalwealth (%)

≤ -3%-3%<≤-2%

-2%<≤ -1%

-1%<≤ 0%

0%<≤ 1%

1%<≤ 2%

3%<

≤ 5% JordanEl SalvadorSouth Africa

GuatemalaMorocco

NetherlandsSwitzerlandTurkeyU.K.U.S.

AustriaBelgiumDenmarkEgyptFranceGreeceItaly PortugalSpain

JapanMauritius

Korea

5% <≤ 10%

BeninGhanaHaiti

HondurasJamaicaKenyaPeruZimbabwe

ArgentinaCosta RicaPanamaPhilippines

BrazilChileColumbia DominicanRep.MexicoPakistanSri LankaSwedenTrinidad and TobagoTunisia

FinlandIrelandNorway

MalaysiaThailand

BotswanaChina

10% <≤ 15%

NicaraguaMalawiMozambique

CongoThe Gambia

BangladeshNamibiaUruguay

AustraliaParaguay

Canada Indonesia

15% < ≤ 20%

Côte d’IvoireSenegalTogoVenezuela

Burkina FasoBurundiNepalPapua New Guinea

EcuadorNew Zealand

India

20%< ≤ 25%

MauritaniaRwanda

Cameroon

25%<≤ 30%

Sierra Leone

Figure 1, but even so it remains statistically significant (Spearman’s r = -0.52).5 Botswana’s natural capital share is small as shown in Table 1 because the World Bank does notprovide an estimate the country’s diamond rent. The inclusion of Botswana in our sample does notmaterially influence any of the empirical results presented in the paper.6 In Botswana, agriculture accounted for only 4 percent of GDP in 1998 compared with 11 percent in1980. The corresponding figures for sub-Saharan Africa as a whole are 17 percent and 18 percent(World Bank, 2000). The decline in the share of agriculture in Botswana’s GDP since 1980 is a sign ofdiversification as well as drought. But see footnote 5.

6

30%<

Central African Rep.ChadGuinea BissauMadagascarMaliNigerZambia

The question is bound to arise what makes the eight high-performance economies in

the second group different from the eight African laggards in the first. A key factor

that distinguishes the two groups is saving and investment. Specifically, the group of

natural-resource-rich, slow-growth countries shown in the south-west corner of Table

1 has an average gross saving rate of only 5 percent, ranging from -2 percent in

Guinea-Bissau to 19 percent in Zambia, whereas the natural-resource-poor, high-

growth group shown in the north-east corner has an average gross saving rate of 32

percent, with individual observations clustered in the range between 28 and 35

percent. A similar pattern emerges when we replace gross domestic saving with gross

domestic investment. In this case, the group of natural-resource-rich, slow-growth

countries has an average gross investment rate of 14 percent, ranging from 7 percent

in Chad to 29 percent in Guinea-Bissau, whereas the natural-resource-poor, high-

growth group has an average gross investment rate of 28 percent, with individual

observations clustered in the range between 26 and 31 percent. Hence our focus on

saving and investment in this paper.

An important limitation of our data is a lack of observations on the share of natural

resources in national wealth at the beginning of the sample period. While economic

growth is measured as an average from 1965 to 1998, our measure of the importance

of natural resources – their share of total wealth – applies to the year 1994. This may

explain, in part, why some formerly resource-dependent countries such as Botswana,

China, Malaysia, Mauritius and Thailand are counted as relatively resource-poor. The

pattern in the table can thus conceivably arise through self selection as the good

performers move towards the upper right-hand corner – having high growth and a low

share of natural resources in national wealth – while the poor performers move into

the bottom left-hand corner – with low or negative growth and heavily dependent on

natural resources. However, when alternative measures of natural-resource

dependence – their share of exports, national output, or the labor force – are used at

the beginning of the period or as period averages, we also find an inverse relationship

between natural resource intensity and economic growth (see Gylfason, Herbertsson

and Zoega, 1999, and Gylfason and Herbertsson, 2001).

7

3. Literature

Four key linkages between abundant natural resources and economic growth have

been described in recent literature.

First, natural resource abundance can lead to the Dutch disease, which can appear

in several guises. A natural resource boom and the associated surge in raw-material

exports can drive up the real exchange rate of the currency, thus possibly reducing

manufacturing and service exports (Corden, 1984). Recurrent booms and busts tend to

increase exchange rate volatility (Gylfason, Herbertsson and Zoega, 1999;

Herbertsson, Skuladottir and Zoega, 1999), thus reducing investment in the tradable

sector as well as exports and imports of goods and services (see Dixit and Pindyck,

1994). The Dutch disease can also strike in countries that do not have their own

currency (e.g., Greenland, which uses the Danish krone; see Paldam, 1997). A boom

in the primary sector then increases wages in that sector, thereby attracting labor from

other industries or imposing higher wage costs on them, especially in countries with

centralized wage bargaining.7 Through some or all of these channels the Dutch

disease can reduce total exports relative to GNP (Gylfason, 1999) or at least skew the

composition of exports away from manufacturing and service exports that may

contribute more to economic growth.

This idea accords with the view that technological discoveries and innovation take

place in manufacturing rather than agriculture (see Kaldor, 1966). To the extent that

the great productivity improvements that have taken place in agriculture in recent

decades reflect technological spillovers from other sectors, the Dutch disease may

slow down economic growth by impeding manufacturing and service exports, which

are probably good for growth (Frankel and Romer, 1999)8 – not only their quantity

but their kind and quality as well.9

In second place, huge natural resource rents, especially in conjunction with ill-

defined property rights, imperfect or missing markets and lax legal structures in many

developing countries and emerging market economies, may create opportunities for

7 Herbertsson, Skuladottir and Zoega (1999) provide empirical support for this thesis by showing howdomestic supply shocks in Iceland – which take the form of changes in the fish catch – affect realwages, not only in the fisheries but in all other sectors as well.8 A dissenting view is expressed in Rodriguez and Rodrik (2000).9 In our sample of 85 countries, there is a significant negative correlation between the ratio of exportsto GDP, adjusted for country size based on population, and the share of natural capital in nationalwealth (not shown). There is also a significant positive correlation between the export ratio adjusted forcountry size and per capita growth adjusted for initial income (not shown).

8

rent-seeking behavior on a large scale on the part of producers, thus diverting

resources away from more socially fruitful economic activity (Auty, 2001a, 2001b;

Gelb, 1988). For example, Tornell and Lane (1998) show that terms of trade windfalls

and natural resource booms may trigger political interaction, or games, among

powerful interest groups that result in current account deficits, disproportionate fiscal

redistribution and reduced growth. The combination of abundant natural resources,

missing markets and lax legal structures may have quite destructive consequences. In

extreme cases, civil wars break out – such as Africa’s diamond wars – which not only

divert factors of production from socially productive uses but also destroy societal

institutions and the rule of law. Collier and Hoeffler (1998) show empirically how

natural resources increase the probability of civil war. Moreover, an abundance of

natural resources may tempt foreign governments to invade with destructive

consequences and the possibility of such an event may prompt the domestic

authorities to spend vast resources on national defense. Military expenditures tend to

inhibit growth through their adverse effects on capital formation and resource

allocation (Knight, Loayza and Villaneuva, 1996).

Rent seeking can also take more subtle forms. For example, governments may be

tempted to thwart markets by granting favored enterprises or individuals privileged

access to common-property natural resources, as, for example, in Russia, or they may

offer tariff protection or other favors to producers at public expense, creating

competition for such favors among the rent seekers (Krueger, 1974). Extensive rent

seeking – i.e., seeking to make money from market distortions – can breed corruption

in business and government, thus distorting the allocation of resources and reducing

both economic efficiency and social equity (Shleifer and Vishny, 1993). Empirical

evidence and economic theory suggest that import protection, cronyism and

corruption all tend to impede economic efficiency and growth (Bardhan, 1997;

Mauro, 1995; Murphy, Shleifer, and Vishny, 1993).

The question of causality remains. Clearly, the presence of natural resources is a

necessary condition for such rent seeking to take place. However, it is by no means

enough. In principle, natural resources can, of course, coexist with well-defined

property rights, well-functioning markets and the rule of law in an efficient and

dynamic market economy. The interesting question from our point of view is whether,

in practice, natural resource abundance tends to thwart attempts towards establishing

such a growth-friendly institutional framework.

9

Third, natural resource abundance may reduce private and public incentives to

accumulate human capital due to a high level of non-wage income – e.g., dividends,

social spending, low taxes.10 Empirical evidence shows that, across countries, school

enrolment at all levels is inversely related to natural resource abundance, as measured

by the share of the labor force engaged in primary production (Gylfason, Herbertsson

and Zoega, 1999). There is also evidence that, across countries, public expenditures

on education relative to national income, expected years of schooling and secondary-

school enrolment are all inversely related to natural capital as measured here

(Gylfason, 2001).11 This matters because more and better education stimulates

growth. For example, Temple (1999) shows that economic growth varies directly with

educational attainment across countries once a few outliers have been removed from

the sample of Benhabib and Spiegel (1994), who had found limited support in their

data for the hypothesis that education is good for growth.

Again, the question of causality remains. It is likely that economic

underdevelopment – poverty – causes natural resources to be relatively important and

makes it difficult to fund and operate educational establishments. On the other hand,

and more interestingly from our point of view, it is also possible that abundant natural

resources reduce the demand for training and education.

Fourth, and this point is closely related to the preceding one, abundant natural

resources may imbue people with a false sense of security and lead governments to

lose sight of the need for good and growth-friendly economic management, including

free trade, bureaucratic efficiency, institutional quality and sustainable development

(Sachs and Warner, 1999; Rodriguez and Sachs, 1999). Put differently, abundant

natural capital may crowd out social capital in a similar manner as human capital

(Woolcock, 1998; Paldam and Svendsen, 2000). From this perspective, one reason

why high inflation tends to hurt economic growth (Bruno and Easterly, 1998;

Gylfason and Herbertsson, 2001) may be that high inflation reflects flawed policies or

weak institutions which impede growth. Incentives to create wealth through good

10 However, the rent stream from abundant natural resources may enable nations to give a high priorityto education – as in Botswana, for instance.11 As far as economic growth is concerned, however, the supply of education may matter less thandemand (see Birdsall, 1996). This is relevant here because public expenditure on education tends to besupply-determined and of mediocre quality, and may thus fail to foster efficiency, equality and growth,in contrast to private expenditure on education, which is generally demand-led and thus, perhaps, likelyto be of a higher quality and more conducive to growth. For this reason, we prefer to use secondary-school enrolment rates rather than public expenditures on education as our measure of education in theempirical analysis presented in Sections 6 and 7.

10

policies and institutions may wane because of the relatively effortless ability to extract

wealth from the soil or the sea. Manna from heaven can be a mixed blessing.

Unconditional foreign aid may be a case in point (see Burnside and Dollar, 2000).

4. Norway

It is by no means inevitable that existing natural resources prevent the emergence of a

dynamic economy or that the discovery of such resources acts to dampen an already

developed economy. Natural resources can be a blessing as well as a curse.

Norway is a case in point. The world’s second largest oil exporter (after Saudi-

Arabia), Norway shows as yet no clear symptoms of the Dutch disease – other,

perhaps, than a stagnant ratio of exports to GDP, albeit at a rather high level, or about

40 percent of GDP, since before the oil discoveries, indicating that Norway’s oil

exports have crowded out non-oil exports krone for krone relative to income;

moreover, Norway has attracted a relatively limited, yet gradually increasing inflow

of gross foreign direct investment, equivalent to 8 percent of GDP in 1998 (adjusted

for purchasing power parity; see World Bank, 2000), far below the figures for Sweden

and Finland next door (23 percent and 36 percent). Nor does Norway show any signs

yet of socially damaging rent-seeking behavior even if increasingly loud calls are

being voiced – and heard! – for using more of the oil revenue to address domestic

social needs rather than continue to build up the government-owned oil fund, which is

invested in foreign securities. There are as yet no clear signs either of a false sense of

security or of an inadequate commitment to education, on the contrary: for example,

college enrolment rose from 26 percent of each cohort to 62 percent between 1980

and 1997. Growth has thus far remained stubbornly high. Even so, some observers of

the Norwegian scene have recently expressed concerns that some deep-seated

structural problems in the country’s education and health care sectors (government

monopoly, insufficient competition, low efficiency, etc.) may be misdiagnosed as

financial problems because the money available from the oil fund may blunt the

willingness of politicians to undertake difficult structural reforms.

Most other oil-producing countries, including virtually the entire membership of

OPEC, carry these symptoms to varying degrees. From 1965 to 1998, GNP per capita

in the OPEC countries decreased on average by 1.3 percent per year. Negative

economic growth over this 33-year period was accompanied by an average ratio of

11

gross domestic fixed investment to GDP of 23 percent for the 11 OPEC countries on

average, a respectable ratio by world standards (compared with 27 percent in

Norway). Why did all this investment in the OPEC countries go hand in hand with

negative growth for so long? – a phenomenon familiar also from the former Soviet

block which, under socialism, saved and invested more of its national economic

output year after year than most OECD countries and yet failed to grow (Easterly and

Fischer, 1995). The answer must involve the efficiency of investment. For it is not

enough to invest; to sustain economic growth, the investments must be of high

quality. A false sense of security may lull countries with oil in abundance or other

natural resources into reducing, if not the quantity of investment, then its quality, or

both. The same argument applies to human capital and perhaps to social capital as

well.

One of the factors that separates the different experiences of Norway and the

OPEC countries, we suggest, is timing. Norway was already a developed country at

the time of the oil discoveries in the 1970s. Most importantly, Norway’s political and

social institutions were mature and the economic and financial system was relatively

developed, although by no means fully liberalized. All of this facilitated judicious and

far-sighted management of Norway’s oil wealth, at least compared with most other oil

producers (Hannesson, 2001). In contrast, full-fledged capitalist development did not

take place in most OPEC countries prior to the discovery of their oil resources, or

since for that matter (Karl, 1997). While Norway has built up substantial assets

abroad, Saudi-Arabia has accumulated debts.

It appears from our informal discussion that saving and the quantity and quality of

investment may be among the key factors that separate those resource-rich countries,

like Norway, that have grown rapidly from those that have had less success. We now

turn to the interplay between natural capital and the quantity and quality of investment

in a theoretical context.

5. Theory

Our aim in this section is to show how optimal saving, and hence also the rate of

growth of output and capital, depends on the abundance of natural resources and the

quality of the capital stock.

We take output to be produced by labor L, natural resources N and capital K and

the production function to be of the Cobb-Douglas variety:

12

(1) baba KNALY −−= 1

where A represents overall efficiency, including technology and quality (more on this

in Section 5.3). We can rewrite equation (1) in per capita terms: babkAny −−= 1 where

y = Y/L, n = N/L and k = K/L.

We distinguish between the structure of the economy and its abundance of natural

resources. By structure we mean the importance of natural resources to the national

economy while abundance refers to the supply (per capita) of the natural resources.

Within the Cobb-Douglas framework, the exponents in the aggregate production

function (1) denote factor shares – hence the structure of the economy – while the

factor inputs are absolute quantities. An increase in the parameter b thus means that

the economy now relies more heavily on natural resources in producing output –

independently of its supply – while an increase in N implies that the supply has

increased. The distinction between structure and abundance allows us to distinguish

between the effect of a change in the factor share b on growth, on one hand, and a

change in the abundance of the natural resource N, on the other. In Figure 2, we

describe changes in abundance by horizontal movements, holding the structure of the

economy unchanged, and structural changes by vertical movements, holding resource

abundance unchanged.

5.1 Optimal saving in the Solow model

To set the stage, we start with the Solow model and derive the optimal saving rate in

an economy with natural resources. Consumption per capita, c = C/Y, is proportional

to output:

(2) ( )ysc −= 1

where s = S/Y is the saving rate. In the transition towards a Solovian steady state the

capital/labor ratio evolves according to

(3) γδγδ

γ −−=−−

=−=k

ys

K

KsY

K

K

k

k &&

where γ is the growth of the labor force and δ is the depreciation rate. We abstract

from technological progress. In the steady state where 0/ =kk& , the capital-output

13

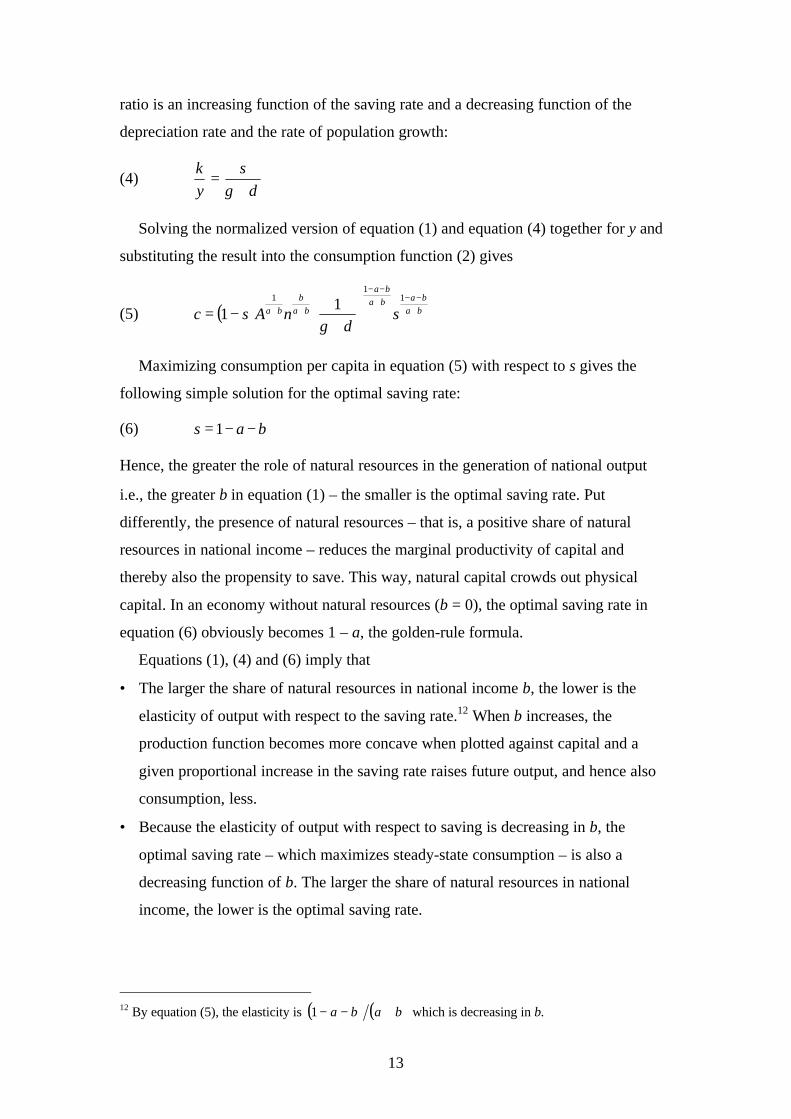

ratio is an increasing function of the saving rate and a decreasing function of the

depreciation rate and the rate of population growth:

(4)δγ +

=s

y

k

Solving the normalized version of equation (1) and equation (4) together for y and

substituting the result into the consumption function (2) gives

(5) ( ) ba

baba

ba

ba

b

ba snAsc +−−+

−−

++

+

−=1

11 1

1δγ

Maximizing consumption per capita in equation (5) with respect to s gives the

following simple solution for the optimal saving rate:

(6) bas −−= 1

Hence, the greater the role of natural resources in the generation of national output –

i.e., the greater b in equation (1) – the smaller is the optimal saving rate. Put

differently, the presence of natural resources – that is, a positive share of natural

resources in national income – reduces the marginal productivity of capital and

thereby also the propensity to save. This way, natural capital crowds out physical

capital. In an economy without natural resources (b = 0), the optimal saving rate in

equation (6) obviously becomes 1 – a, the golden-rule formula.

Equations (1), (4) and (6) imply that

• The larger the share of natural resources in national income b, the lower is the

elasticity of output with respect to the saving rate.12 When b increases, the

production function becomes more concave when plotted against capital and a

given proportional increase in the saving rate raises future output, and hence also

consumption, less.

• Because the elasticity of output with respect to saving is decreasing in b, the

optimal saving rate – which maximizes steady-state consumption – is also a

decreasing function of b. The larger the share of natural resources in national

income, the lower is the optimal saving rate.

12 By equation (5), the elasticity is ( ) ( )baba +−−1 which is decreasing in b.

14

• Heavy dependence on natural resources as measured by their share in national

income b causes the capital-output ratio to be lower due to a lower optimal saving

rate. In effect, natural capital crowds out physical capital to a degree.

• In the long run, the level of output per capita is inversely related to the share of

natural resources in national output, given the level of natural resources N, due to

less saving. However, notice that an increase in their level – holding their share of

national income constant – makes output as well as the stock of capital rise.

• In contrast, the speed of adjustment towards steady state is an increasing function

of the share of natural capital in national income b. The larger the natural capital

share, the smaller is the share of physical capital in national income and hence the

more rapid is the adjustment to steady state.13

In sum, an economy where the owners of natural resources receive a high fraction of

national income converges quickly to a steady state with a low saving rate and a

correspondingly low capital-output ratio and where, most importantly, output per

capita is also low.

5.2 Optimal saving in the Ramsey model

Because our derivation of the optimal saving rate in the Solow model does not

constitute microeconomic optimization from first principles, we now proceed to

derive the optimal saving rate in the Ramsey model which is more firmly grounded in

the optimization behavior of firms and consumers.

Assume the same production function as in the Solow model above. As before,

output can be either saved – that is, added to the capital stock – or consumed. Now

enters the central planner who maximizes the welfare of the representative consumer

by solving the following optimization problem:

(7) dtecu tt

c

ρ−∞

∫ )(max0

where c is consumption per capita as before and ρ is the pure rate of time preference,

subject to the constraints

13 The speed of adjustment is given by ( )( )δγ +−−− )1(1 ba which is increasing in b. This is the rateof decrease of the difference between the current and the steady-state level of capital and isindependent of the saving rate. See Romer (1996), page 22.

15

(8) 0 0k k=

(9) ( )1b a bk An k c kδ γ− −= − − +&

where 0k is a constant. The necessary conditions that have to be satisfied along an

optimal path are

(10) ( )c

cbab

u

ukAnba

&−=−−− −− ρδ1

(11) ( )1b a bk An k c kδ γ− −= − − +&

Equation (10) is the well-known Keynes-Ramsey rule. The left-hand side shows the

marginal benefit of saving – that is, postponing consumption – which is the net

marginal product of capital and the right-hand side shows the marginal cost which is

the sum of the pure rate of time preference and the (absolute) rate of growth of

marginal utility. The higher the net marginal product of capital, the greater is the

benefit from saving more and the more impatient the representative consumer, the

greater is the cost. Finally, if consumption is expected to grow in the future ( cu& < 0),

this constitutes an extra cost of increasing saving: it is costly to postpone consumption

to a later time when it will be valued less.

The Keynes-Ramsey rule tells us that changes in factor intensity that increase the

share of national income going to the owners of natural resources reduce the marginal

benefit of saving and hence also capital accumulation for all plausible parameter

values.14 It follows that an economy whose industries rely heavily on the use of

natural resources tends to have a relatively low steady-state stock of capital, other

things being equal. A structural change that makes oil more important relative to

capital will reduce the optimal saving rate. In contrast, an increase in the natural

resource base (an oil discovery, for instance) – holding the share of the resource in

national income constant – causes the marginal benefit of saving to go up and hence

also its optimal level.

14 An increase in b reduces the marginal product of capital as long as ( ) ( )log / 1 1n k a b< − − .

Assuming that a + b = 0.5 as a minimum makes the critical value of the natural capital/physical capital

ratio equal to 39.72 ≈e which ensures that the above inequality is satisfied for all countries in our dataset where Niger has the highest value of n/k, 5.66.

16

In steady state we have 0c cu u k= =&& which implies, after some manipulation of

equations (10) and (11), that

(12) ( )

++

−−=−

=ρδγδ

bay

cys 1

This result simplifies to bas −−= 1 as in equation (6) in the Solow model if γ = ρ .

In any case, the optimal rate of saving varies inversely with the share of natural

resources in national income, b.

We also find that the speed at which the economy travels along a saddle path

towards steady state is increasing in the share of the natural resource in national

income. An increase in the parameter b makes the production function be more

concave in capital. As a result, a fall in the stock of capital below its steady-state

value has a greater effect on its marginal product and hence also on the incentive to

save and invest. Therefore, saving will increase more and we will move faster back to

steady state.

To see how expectations about how permanent a natural resource boom is enter the

calculations we need to solve the model with the use of a phase diagram (not shown)

and pay close attention to whether it is the structure of the economy – represented by

the parameter b in the production function – that is changing or the supply of the

resource N, holding the factor share constant. To make a long story short, the Keynes-

Ramsey rule (10) can be rewritten as the following Euler equation:

(13) ( ) ( ) ( )[ ]γδθ

+−−−= +− babknbac

c1

1&

where θ is the coefficient of relative risk aversion – assuming that the utility function

in equation (7) is of the CRRA form, θ

θ−

−= 1

1

1)( ccu t . Equations (11) and (13) can

now be used to solve the model and derive the following results:

• A permanent increase in b – the share of natural capital in national income – makes

consumption jump immediately and then gradually decline to a lower level than

before as the capital stock is gradually depleted. While both investment and output

are lower in the new steady state, the saving rate – which is the ratio of the two – is

lower because of the diminishing marginal product of capital.

17

• A transitory increase in b makes consumption jump initially – albeit not by as

much as in the case of a permanent change – and subsequently both consumption

and capital decline until b comes down again. At exactly that moment we hit the

old saddle path. Thereafter, consumption and capital gradually increase along the

old saddle path until we hit the original steady state.

• A permanent increase in N (holding b constant) – i.e., holding technology constant

– makes consumption jump immediately so that we hit the new saddle path after

which we move upwards along the new saddle path towards a new steady state

where both the level of consumption and the stock of capital are higher than

before. Note the interesting twist to this saga: A permanent resource boom –

holding the share of natural resources in national income constant – raises

consumption by more than the increased supply of the natural resource would

imply. There is a secondary effect through capital accumulation. When N goes up,

output increases and so do permanent income and consumption, but because the

marginal product of capital goes up, the incentive to save is enhanced and the

capital stock is gradually increased. As a result, steady-state consumption rises by

more than the rise in income caused by more abundant natural resources.

• A temporary increase in N also causes consumption to jump and then to grow

gradually alongside the capital stock. However, when the natural resource boom

comes to an end we hit the old saddle path and both consumption and capital fall as

we move down the old saddle path (as in Rodriguez and Sachs, 1999). There

occurs a transitory consumption boom. Importantly, consumption is maintained at

a higher level than its original steady state for a period which is longer than the

duration of the natural resource boom.

5.3 Endogenous growth

Rather than focus on medium-term growth, we would now like to write down a model

that shows how economic growth depends on the abundance of natural resources and

the quality of the capital stock, even in the long run. In particular, we will show how

natural resources can affect the rate of growth of output and capital both directly

through the quantity of investment as well as indirectly through the quality of

investment. Our model of choice is only one of several possible ones; accordingly, its

implications need scrutiny and testing.

18

We adopt the pioneer endogenous growth model of Romer (1986) where

sustainable growth arises from constant returns to capital at the social level. At the

firm level, however, we have constant returns to all factors of production and

diminishing returns to capital. The root of constant social returns to capital lies in

learning-by-investing and instantaneous knowledge spillovers across firms.

We expand the model to include natural resources. We assume that both the

productivity of labor as well as that of the natural resource is augmented through

learning and that the level of labor- and natural-resources-augmenting technology can

be proxied by the aggregate stock of capital, which is a function of past investment;

hence the generation of knowledge. We assume that the number of workers is fixed.

This gives us the following production function for the representative firm:

(14) ( ) ( ) ( )ai

bi

baii KLKNqKY −−= 1

where Yi denotes the output of the representative firm i and q is the exogenous

productivity of capital, and takes a value between zero and one. Equation (14) gives

equation (1) when baba KqA +−−= 1 , ∑=i

iKK , ∑=i

iLL , ∑=i

iNN and all firms

are of equal size.

Like Scott (1989), we distinguish between quantity and quality (see also Lal and

Myint, 1996, Ch. 2). If some investment projects miss the mark and fail to add

commensurately to the capital stock, we have q < 1. One way to interpret q is to view

it as an indicator of distortions in the allocation of installed capital due, perhaps, to a

poorly developed financial system, but perhaps also due to trade restrictions or

government subsidies that attract capital to unproductive uses in protected industries

or in state-owned enterprises where capital may be less productive than in the private

sector (Gylfason, Herbertsson and Zoega, 2001). Another way is to view the quality

index q as the ratio of the economic cost (i.e., minimum achievable cost) of creating

new capital to the actual cost of investment (Pritchett, 2000) – that is, K is then

measured on the basis of actual costs which may overstate its productivity. Yet

another way is to view q below 1 as a consequence of aging: the larger the share of

old capital in the capital stock currently in operation, that is, the higher the average

age of capital in use, the lower is its overall quality (Gylfason and Zoega, 2001). For

our purposes, the three interpretations are analytically equivalent. However, we

assume that the quality of capital has remained constant in the past which means that

19

all units of capital are of the same quality. In other words, we are not interested here

in the implications of having different vintages of capital.

The other important new element here is the presence of natural resources.

Whereas capital is owned by a class of capitalists, the natural resources are owned by

individuals – the naturalists. The total stock of natural resources is given and hence

also the supply of their services. We take these services to be fixed and exogenous so

that no opportunities for intertemporal allocation of these resources arise.

We assume a perfectly competitive market for the services of natural resources. In

equilibrium, supply of and demand for natural resources are equalized and the

marginal product is equal to their real price. Similarly, there is perfect competition in

the market for labor and the marginal product of labor is equal to the real wage.

Finally, we have a market for capital where the owners of the capital sell their

services to firms. As in the other two factor markets, we have an equilibrium under

perfect competition where marginal product equals the sum of the real interest rate r

and the rate of depreciation δ:

(15) ( ) ( ) ( ) δ+=−−= −−−− rKLKNKqbadK

dY ai

bi

bai

ba

i

i 11

The depreciation rate δ is the rate at which installed capital loses its usefulness

over time, as a result of economic obsolescence as well as physical wear and tear

(Scott, 1989). The parameters q and δ could both be modeled as endogenous choice

parameters (as in Gylfason and Zoega, 2001), but here we treat them as exogenous

magnitudes for simplicity, even if we acknowledge that depreciation may depend on

quality, through obsolescence.

We thus view quality and durability as two different things. The pyramids of Egypt

were high-quality investments in their day – good at preserving mummies! – and they

have lasted a long time (high q, low δ); they remain among Egypt’s major sources of

foreign exchange. High-quality computers, by contrast, do not last long because they

are quickly rendered obsolete by better machines (high q, high δ). Soviet housing,

which sometimes began to crumble even before construction was completed, is an

example of low-quality, low-durability investment (low q, high δ). But some low-

quality investments last a long time, like Mr. Hoxha’s concrete bunkers, hundreds of

thousands of them, scattered all across Albania: they were built to last as long as the

pyramids, but they remain utterly useless, or worse because it would be so costly to

20

demolish them (low q, low δ).

Households with an infinite planning horizon maximize discounted future utility

with respect to consumption per capita and subject to an asset-accumulation

constraint. This gives the standard Euler equation for the growth of consumption per

worker:

(16) ( )ρσ −= rg

where σ is the elasticity of intertemporal substitution (assuming constant relative risk

aversion) and ρ is the rate of time preference. Using equation (16) and assuming

symmetric equilibrium, we get the following expression for the optimal rate of growth

of consumption and output:

(17) ( )( )ρδσ −−−−= −− abba LNqbag 11

Thus, economic growth depends on several factors:

• The rate of growth varies directly with the quality of the capital stock q. The higher

quality, the higher is the price of capital – for a given level of capital – and hence

the real rate of interest. A higher interest rate induces consumers to postpone

consumption – i.e., to save and accumulate capital.

• The rate of growth depends on the size of the labor force L. This is the scale effect

that is familiar in the growth literature. A larger aggregate labor force raises the

private marginal product of capital and hence also the price of capital – the real

rate of interest. This leads to increased saving and a more rapid rise of

consumption.

• The rate of growth is inversely related to the pure rate of time preference ρ. The

higher the rate of time preference – i.e., the more impatient are workers – the

greater is current consumption and the slower is the growth of consumption in the

future due to less saving.

• The rate of growth is inversely related to the rate of depreciation δ. A “good”

investment combines high quality and low depreciation. Equation (17) shows that

“bad” investments retard the build-up of useful capital over time in two ways: (a)

by adding capital of low quality, with q below 1, hence lowering the price of

capital and blunting the incentive to save and invest, and (b) by increasing the

depreciation rate δ, thus decelerating output from the supply side.

21

Most importantly from our perspective, the abundance of natural resources affects the

rate of growth. Given our assumptions of constant returns to scale and competitive

markets, the exponents a and b in the production function show the share of output

going to labor and the naturalists, respectively, so the remainder goes to the

capitalists. Equation (17) shows that both the share of the naturalists in output b as

well as the term Nb in the production function affect the growth rate.

A rise in the supply of natural resources N causes their price to fall while keeping

the factor share constant at b. However, an increase in the share of output going to the

owners of the natural resource, b, causes the price to rise while leaving N unchanged

due to its fixed supply. These changes affect the rate of growth of consumption and

output:

• A rise in the supply of the natural resource N – with an unchanged state of

technology and hence unchanged factor shares – leads to a fall in its price and an

increase in the quantity used in production. The increased use of the natural

resources raises the marginal product of capital, hence also the demand for capital

and its price – the real rate of interest. A higher real interest rate lowers the price of

future consumption and makes workers substitute future for current consumption.

Saving and investment increase and hence also the pace of learning and knowledge

spillovers. The rate of economic growth has increased. But notice that this is a

scale effect similar to the one involving the size of the labor force.

• A rise in the share of output going to the owners of the natural resource, b, reduces

the marginal productivity of capital. This lowers the real rate of interest and raises

the price of future consumption. Facing a higher price of future consumption,

workers increase current consumption at the expense of future consumption.

Saving is reduced and so are investment, learning and growth in this closed

economy. Given competitive markets, the share going to the naturalists can only

increase due to changes in the production function.15

The socially optimal rate of growth of consumption – which comes from the

solution to the central planner’s problem – depends on the social marginal product of

capital, not the private marginal product. The rate of growth of consumption and

output is now given by

15 Alternatively, we could have derived the same result assuming imperfect competition and monopolyrents in the market for the services of natural resources. Changes in these rents would then affectgrowth.

22

(18) ( )ρδσ −−= −− abba LNqg 1

The difference between equations (17) and (18) lies in the term 1 - a - b in the

marginal product expression in the former equation. As a result, the discrepancy

between the actual and the optimal rate of growth is increasing in the share of output

going to the naturalists b. In other words, the extent of the market failure inherent in

the Romer model varies directly with the share of output going to the owners of the

natural resources.

5.4 Natural capital, financial intermediation and growth

We have identified a direct link between natural resources and economic growth,

through saving and investment. There may also be an indirect effect through the

productivity of capital q. An abundance of natural resources may hamper the

emergence of a well-developed financial system. If so, this outcome is likely to result

in an inefficient allocation of savings across sectors and firms – that is, reduce the

value of q in the equations above – and to reduce the average productivity of capital

and so to further blunt incentives to save and invest by reducing the marginal

productivity of capital at a given level of the capital stock.

When a large part of national wealth is stored in a natural resource, renewable or

not, there is less need for financial intermediation to conduct day-to-day transactions.

Dissaving can take the form of more rapid depletion of the resource and saving can

take the form of less rapid depletion or of more rapid renewal in the case of renewable

natural resources. In some countries, such as the oil-rich OPEC states, saving also

takes the form of deposits in foreign banks. In this case, domestic financial

intermediation becomes even less important. In contrast, when saving is piled up at

home in the form of physical capital, domestic banks and stock markets assume

paramount importance. By linking up domestic savers and investors, the domestic

financial system contributes to a more efficient allocation of capital across sectors and

firms.

Further, a well-developed financial system helps drive a wedge between the effect

of foreign and domestic saving on economic growth. In other words, as the financial

system matures and becomes more efficient at allocating capital at home, foreign

savings – i.e., deficits on the current account of the balance of payments – become

relatively less useful when not channeled through the domestic banking system. In a

23

mature financial system, investment financed through domestic saving can be more

effective at stimulating economic growth than investment financed by foreign saving.

Not only is it thus possible for an abundance of natural resources to hamper the

development of the financial system and hence to distort the allocation of capital but

economic growth may slow down due to a detrimental effect of financial

backwardness on the quantity and quality of saving and investment. King and Levine

(1993) find that indicators of financial development and their predetermined

components predict subsequent growth, physical capital accumulation and

improvements in the efficiency of capital allocation.16 Hence, our hypothesis that

natural resource dependence tends to go along with an underdeveloped financial

system means, if King and Levine are right, that resource dependence also tends to

hinder future gains in efficient capital deepening and economic growth.

6. Correlations

We posit that heavy dependence on natural resources may reduce saving and

investment and hence inhibit economic growth directly. Resource dependence may

also slow down the development of the financial system, thereby reducing the quality

of investment decisions and hence also the productivity of capital and also, perhaps,

raising the ensuing rate of depreciation. If so, a given investment rate is likely to

generate a lower rate of growth of output, other things being equal.

In empirical research on economic growth thus far, however, the volume of gross

investment has been used as the sole measure of investment, with mixed results

(Levine and Renelt, 1992; Barro and Sala-i-Martin, 1995). This practice means that

net investment and replacement investment have been assumed to have identical

effects on growth. We have pointed out that the higher the fraction of gross

investment needed to replace old capital, the lower will be the rate of growth of

output. We now want to take a further step and study the cross-country relationships

among natural resource intensity, gross investment and genuine (i.e., quality-adjusted)

saving which takes into account the depreciation of physical, human and natural

capital as well as the stock of foreign assets.

6.1 Gross investment and growth

16 Benhabib and Spiegel (2000) report similar findings.

24

Before embarking on the regression analysis in Section 7, let us inspect the data. The

upper panel of Figure 3 shows a scatterplot of the average ratio of gross domestic

investment to GDP in 1965-1998 and natural resource intensity measured as before.

When we purge the natural capital share of that part which is explained by the

country’s initial income per head, we get very similar results as in Figure 3a.17 The

group of eight low-growth, natural-resource-rich African countries identified in

Figure 1 is visible in the lower right-hand corner of Figure 3a. The high-growth,

natural-resource-poor countries are also easy to spot in the upper left-hand corner of

the figure. Apart from these two groups, the relationship between the two variables is

not very clear, even if it remains statistically significant. A clearer relationship

emerges when we plot economic growth against the investment ratio over the same

period, 1965-1998. The figure in the lower panel of Figure 3 shows the cross-country

relationship between the rate of growth, on the one hand, and the sum of domestic and

foreign saving (the latter measured by the current account deficit) without any attempt

to adjust investment for quality, q. The regression line through the 85 observations

suggests that an increase in the investment ratio by about four percentage points is

associated with an increase in annual economic growth by 1 percentage point. The

relationship is significant (Spearman’s r = 0.65).18

6.2 Genuine saving and growth

As we saw in Section 5, however, high saving and investment rates do not necessarily

stimulate growth if they are accompanied by rapid depreciation of physical capital.19

Depreciation calls for investment to replace the depleted capital, thus rendering a

smaller share of domestic (and foreign) saving available for fresh capital formation. A

similar argument applies to natural capital. This is where the World Bank’s new

estimates of genuine saving rates enter the picture (see Appendix for a description of

the data). Countries that run down their stocks of physical and natural capital will

17 The same applies to Figures 4a, 5a and 6a.18 The slope of the regression line through the scatterplot is consistent with the coefficients oninvestment in cross-country growth regressions reported in recent literature (Levine and Renelt, 1992;Doppelhofer, Miller and Sala-i-Martin, 2000).19 Scott (1989) is of a different opinion. He claims that depreciation reflects mainly the economicobsolescence of capital, and does not necessarily reduce its usefulness. To him, therefore, grossinvestment is the correct measure of capital accumulation in growth research. In his own words,“workers … benefit from rising wages which result in appreciation which is omitted from theconventional accounts. Were it included, it would offset depreciation on capital assets. It would then beclear that net investment for society as a whole is (approximately) equal to gross investment as

25

have low, perhaps even negative, genuine saving rates which, therefore, may be taken

as a rough indication of the physical and economic durability of their capital and the

sustainability of their natural resource management, at least in a physical sense. For

example, the average genuine domestic saving rate of the 11 OPEC countries in 1970-

1998 was -7 percent, ranging from -25 percent in Kuwait to 10 percent in Indonesia,

compared with 17 percent for Norway.

Genuine domestic saving differs from net domestic saving (i.e., gross domestic

saving minus depreciation) by the rundown and depreciation of natural capital,

adjusted by current expenditure on education, which increases or improves human

capital20 even if it is classified as current expenditure in national income accounts.

Genuine saving is intended to indicate the difference between sustainable net national

product and consumption, where sustainable net national product means the

maximum amount that could be consumed without reducing the present value of

national welfare along the optimum path (Hamilton, 2001).21 Genuine saving rates are

higher than net saving rates in those countries where improvements in human capital

outweigh the deterioration of natural capital, and conversely. In view of these

adjustments, one might expect genuine saving rates to be more closely correlated with

natural capital and economic growth than gross investment rates.

The data seem to confirm this conjecture. The upper panel of Figure 4 shows a

scatterplot of genuine domestic saving in 1970-1998 (the World Bank figures do not

reach further back) and natural capital as measured before. The regression line

through the 85 observations suggests that an increase of about two and a half

percentage points in the natural capital share from one country to the next is

associated with a decrease in genuine saving by one percent of GDP. The relationship

is statistically significant (Spearman’s r = -0.53).22 The correlation between genuine

conventionally measured, and not to gross investment minus depreciation.” (p. 92).20 But recall the reservations expressed in footnote 11.21 More specifically, genuine domestic saving is defined as net domestic saving plus educationexpenditure minus energy depletion, mineral depletion, net forest depletion and carbon dioxide damage(World Bank, 2000, p. 171). Estimates that are missing include the depletion and degradation of soilsand net depletion of fish stocks. The most important pollutants affecting human health and economicassets are also excluded (particulate emissions, ground-level ozone, acid rain). In some cases, theresource depletion estimates of the World Bank are quite high because the entire mineral-resource rentis counted as depletion whereas the alternative user cost approach allocates only a fraction of the rent todepletion. The median genuine saving rate in our sample is 9 percent, and ranges from -21 percent to23 percent. The corresponding figures for the gross investment rate are 20 percent, 7 percent and 32percent.22 The correlation weakens a bit if we limit the regression to the 77 countries where the natural capitalshare is below 0.25, but it remains statistically significant (Spearman’s r = -0.43).

26

saving and natural capital in Figure 4a is closer than that between gross investment

and natural capital in Figure 3a. On the other hand, the inverse relationship between

net investment and natural capital (not shown) is weaker than the ones shown in

Figures 3a and 4a, but still significant. This seems to suggest that it is not enough to

adjust gross investment for depreciation of physical capital; we need to adjust it for

depreciation of other types of capital as well.

The lower panel of Figure 4 shows a scatterplot of economic growth and genuine

domestic saving in 1970-1998 in the same 85 countries. The regression line suggests

that an increase in the genuine saving rate by about seven percentage points is

associated with an increase in annual economic growth by 1 percentage point. The

relationship is highly significant (Spearman’s r = 0.72). Again, the correlation

between genuine saving and growth in Figure 4b is closer than that between gross

investment and growth in Figure 3b. Further, the direct relationship between

economic growth and net investment (not shown) is weaker than the ones shown in

Figures 3b and 4b, but still highly significant. This suggests once more that it is not

enough to adjust gross investment for physical depreciation. It seems that, in a broad

sense, quality counts.

6.3 Gross saving and growth

The difference between gross investment and genuine saving comprises four terms:

(a) depreciation of physical capital, (b) depreciation of natural capital, (c) depreciation

of human capital and (d) rundown of foreign capital – the current account deficit.

How much of the difference between the results reported in Figures 3 and 4 can be

traced to the current account? To find out, we subtract the current account

deficit/GDP ratio from the gross investment rate in order to obtain the gross domestic

saving rate and then redraw the scatterplots.

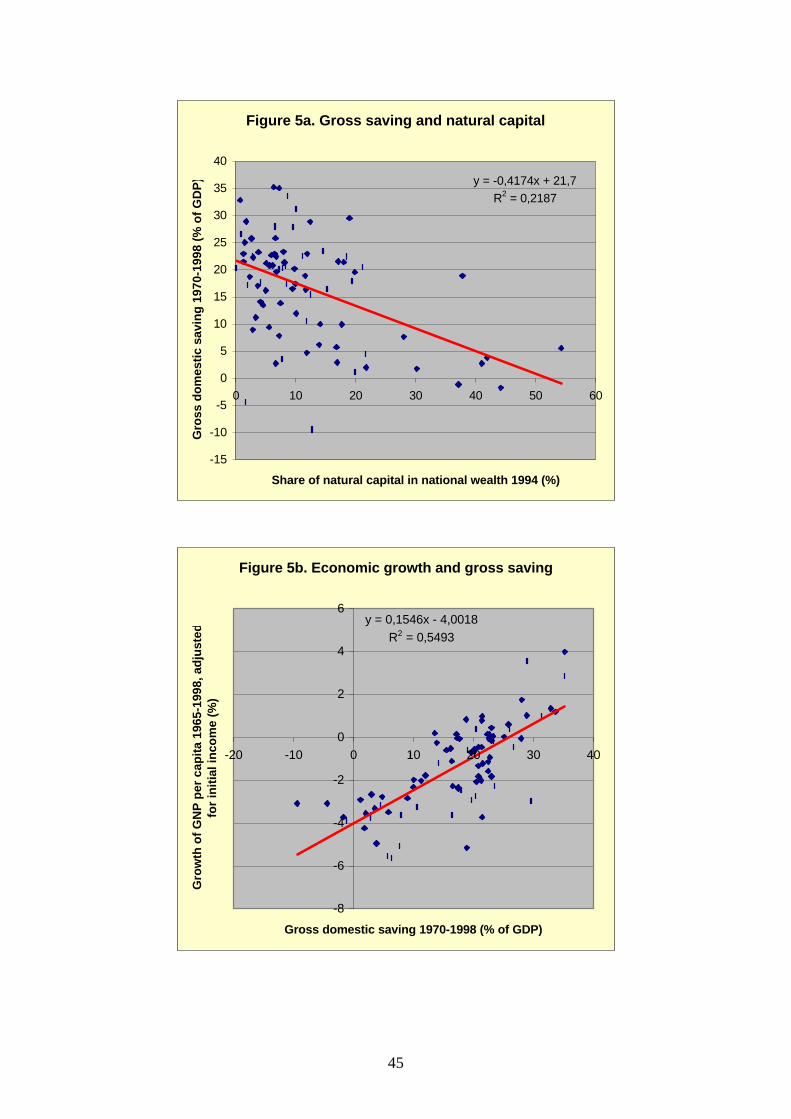

The upper panel of Figure 5 shows the scatterplot of gross domestic saving in

1970-1998 and natural capital. The results are essentially the same as in Figure 4a,

even if the correlation now is a bit weaker (Spearman’s r = -0.40). The lower panel of

Figure 5 shows the scatterplot of economic growth and gross domestic saving in the

same 85 countries. Again, the results are essentially the same as in Figure 4b

(Spearman’s r = 0.73). The correlations between natural capital, gross saving and

growth in Figure 5 are a bit stronger than the ones between natural capital, gross

investment and growth in Figure 3, but the differences are small.

27

To summarize, the data show that, across countries,

(a) economic growth varies directly with gross investment, genuine saving and

gross saving (Figures 3b, 4b, and 5b),

(b) gross investment, genuine saving and gross saving are all inversely related to

resource dependence (Figures 3a, 4a, and 5a), and

(c) growth varies inversely with natural resource dependence (Figure 1).

Through any one of the three possible channels under review here (gross investment,

genuine saving or gross saving), an increase in the share of natural capital in national

wealth by 10 percentage points from one country to another is associated with a

decrease in per capita economic growth by 0.5-0.6 percentage points. Natural resource

dependence thus appears to inhibit economic growth significantly by weakening

public and private incentives to save and invest as well as to build up human capital

(Barro, 1997; Temple, 1999; Gylfason, 2001), in addition to the linkages through the

Dutch disease, rent seeking, policy failures and institutional weaknesses stemming

from a false sense of security, reviewed in Section 3. If so, the adverse effects of

natural resource dependence on economic growth since the 1960s that have been

reported in the literature may, in part, reflect the effect of investment and genuine

saving on growth.

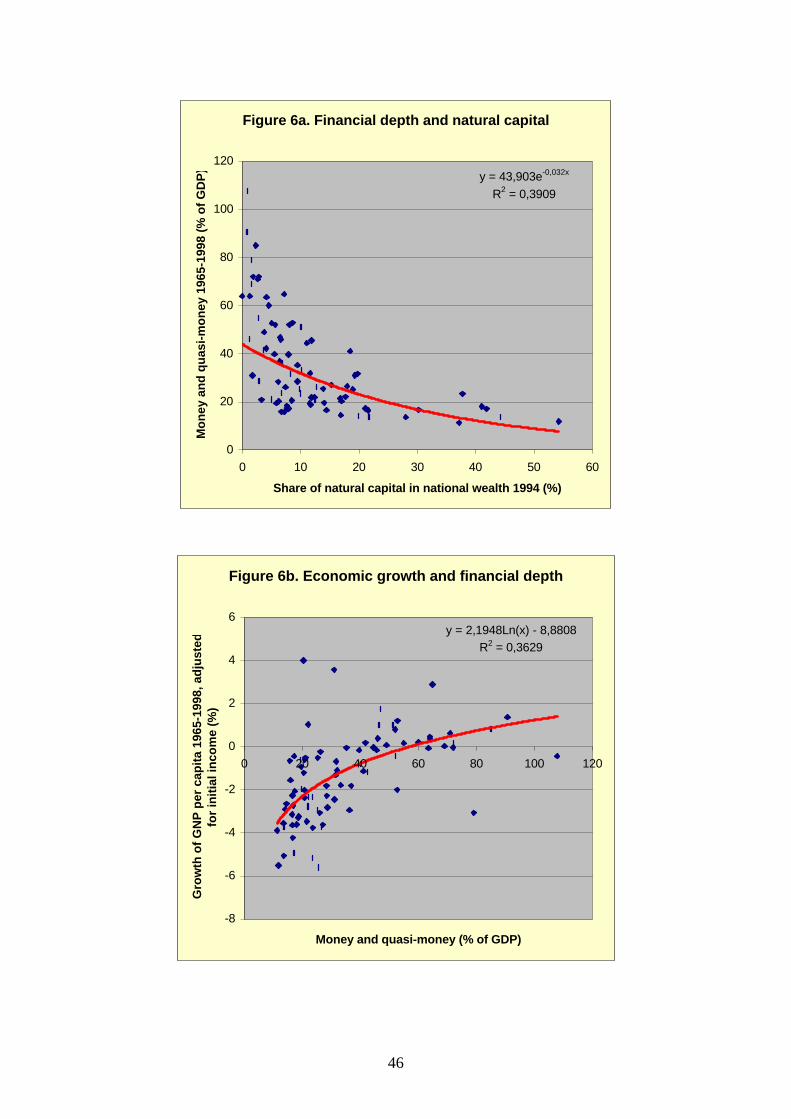

At last, we look at the data on financial development. The upper panel of Figure 6

below shows a cross-sectional scatterplot of financial development, for which we use

the average ratio of M2 and GDP in 1965-1998 as a proxy, like King and Levine

(1993), and natural resource dependence as measured before. The figure covers the

same 85 countries as before. The lower panel of the figure relates our measure of

financial development to average economic growth per capita over the same period.

Figure 6a shows a clear negative correlation between natural resource dependence and

financial depth (Spearman’s r = -0.68).23 Similarly, Figure 6b shows a positive

relationship between our measure of financial depth and average economic growth

(Spearman’s r = 0.66). However, the question of causality remains. It is possible that

heavy dependence on natural resources actually hinders the development of the

financial sector and hence also growth, as we are inclined to think, but other

possibilities also exist; in particular, some unspecified third factor may inhibit both

23 The exponential regression curve becomes steeper if we limit the regression to the 77 countrieswhere the natural capital share is below 0.25, but even so the correlation remains highly significant(Spearman’s r = -0.61).

28

financial development and economic growth.

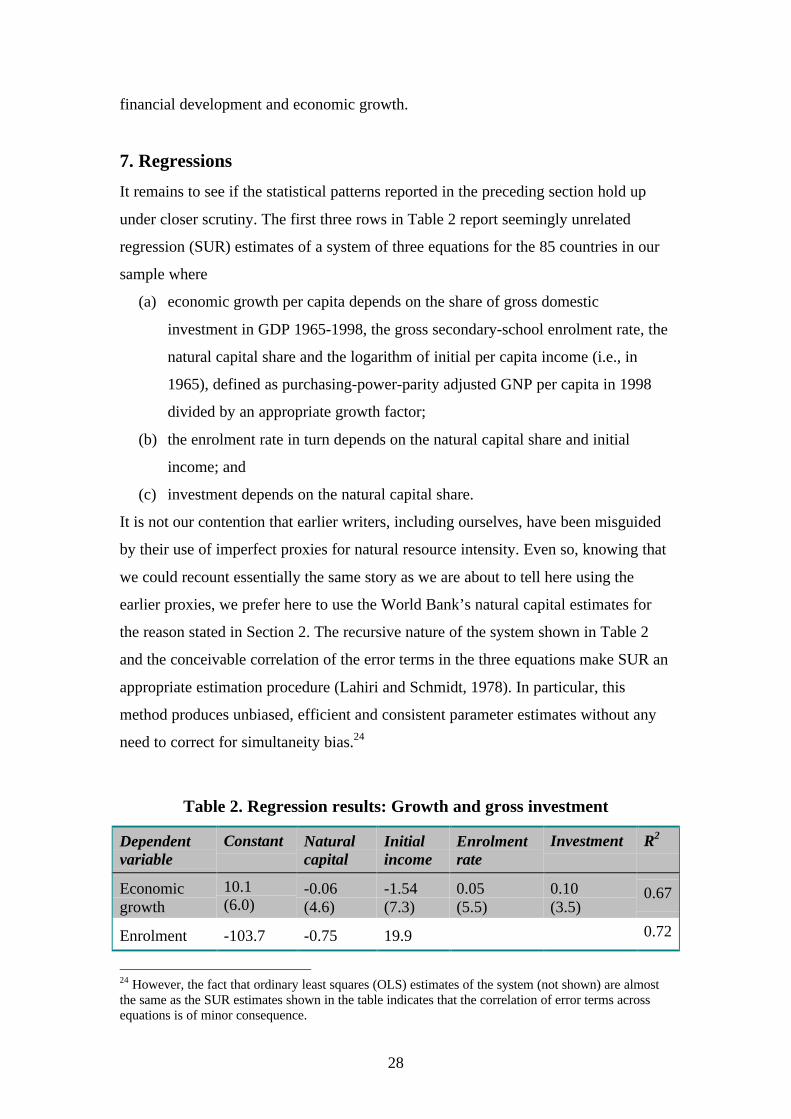

7. Regressions

It remains to see if the statistical patterns reported in the preceding section hold up

under closer scrutiny. The first three rows in Table 2 report seemingly unrelated

regression (SUR) estimates of a system of three equations for the 85 countries in our

sample where

(a) economic growth per capita depends on the share of gross domestic

investment in GDP 1965-1998, the gross secondary-school enrolment rate, the

natural capital share and the logarithm of initial per capita income (i.e., in

1965), defined as purchasing-power-parity adjusted GNP per capita in 1998

divided by an appropriate growth factor;

(b) the enrolment rate in turn depends on the natural capital share and initial

income; and

(c) investment depends on the natural capital share.

It is not our contention that earlier writers, including ourselves, have been misguided

by their use of imperfect proxies for natural resource intensity. Even so, knowing that

we could recount essentially the same story as we are about to tell here using the

earlier proxies, we prefer here to use the World Bank’s natural capital estimates for

the reason stated in Section 2. The recursive nature of the system shown in Table 2

and the conceivable correlation of the error terms in the three equations make SUR an

appropriate estimation procedure (Lahiri and Schmidt, 1978). In particular, this

method produces unbiased, efficient and consistent parameter estimates without any

need to correct for simultaneity bias.24

Table 2. Regression results: Growth and gross investment

Dependentvariable

Constant Naturalcapital

Initialincome

Enrolmentrate

Investment R2

Economicgrowth

10.1(6.0)

-0.06(4.6)

-1.54(7.3)

0.05(5.5)

0.10(3.5)

0.67

Enrolment -103.7 -0.75 19.9 0.72

24 However, the fact that ordinary least squares (OLS) estimates of the system (not shown) are almostthe same as the SUR estimates shown in the table indicates that the correlation of error terms acrossequations is of minor consequence.

29

rate (7.5) (4.2) (12.4)

Investment22.5(29.3)

-0.20(4.1)

0.16

Economicgrowth

7.29(4.8)

-0.12(6.7)

-0.58(3.2)

0.35

Note: 85 observations. t-statistics are shown within parentheses.

All the parameter estimates in Table 2 are economically and statistically significant.

The coefficient on initial income in the growth equation indicates a convergence

speed of 1.5 percent per year, which is not far below the 2-3 percent range typically

reported in statistical growth research. The direct effect of natural capital on growth is

-0.06. The indirect effect of natural capital on growth through education is -0.75× 0.05

≈ -0.04 and the additional indirect effect through investment is -0.20× 0.10 = -0.02.

The novelty here is the part of the story involving investment; as far as we know, this

linkage – from heavy dependence on natural resources to slow growth via investment

– has not been documented in econometric work before. Sachs and Warner (1997,

2001) report that they have found little evidence of a link between natural resource

abundance and investment. The total effect of natural capital on growth is thus about -

0.12 (for given initial income), which is very close to the value of the slope of the

regression line in Figure 1. This means that the implicit constraint on the coefficient

of initial income as well as the omission of education and investment in Figure 1 do

not bias the quasi-reduced-form estimate of the slope of the regression line in the

figure. The bottom row in Table 2 shows the OLS estimate of the reduced-from

equation for growth implied by the equation system above. Like Figure 1, Table 2

indicates that an increase in the natural capital share by eight or nine percentage

points is associated with a decrease in growth by about one percentage point. Of the

total effect of natural capital on growth, about a third can thus be attributed to

education according to this interpretation, and about one-sixth to investment. This still