murphy's law in action

TRANSCRIPT

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 1/13

Kuwait Financial Centre “Markaz” R E S E A R C H

Murphy’s Law at PlayMarkets tumble post downgrade

August 2011 Returns (%)

S&P 500 MSCI World MSCI EM S&P GCC

-5.68 -7.26 -9.47 -5.12

World markets tumbled under pressure from continued economic issues inthe US in addition to the impact of the 5 th August S&P downgrade of UScredit. Mid-month saw Fitch affirm the US rating while awarding it a „Stable‟ outlook versus „Negative‟ calls from S&P and Moody‟s. Also during themonth, Moody‟s downgraded Japan‟s government debt by one -notch to

Aa3, with a „Stable‟ outlook, due to a build-up of debt since the 2009recession.

Signs of flagging US demand and progress in Libya brought crude oil pricesdown 2% in August with a YTD gain of 24%. Conversely, the uncertaintyhas been a boon for Gold; the precious metal saw its highest monthly gainin 21-months, up 13% in August to close at $1,826/oz.

The broad World index tumbled by 7.3% in August bringing the YTD loss to4%.

GCC markets were down significantly on global cues during the month; S&PGCC lost 5.12% as Saudi fell 6.5%. Kuwait‟s weighted index followed with aloss of 3.4%.

Liquidity was down again in August as the month of Ramadan sawlackluster trading; GCC value traded declined 15% to USD 17.76 bn whilevolume was down 6% to just 6.65 bn. Saudi and Kuwait saw value tradeddecline by 21% and 14%, respectively. GCC Value Traded in the YTD periodis at USD 232 bn.

Risk in the GCC (as measured by the Markaz Volatility Index – MVX) was up just 28% in August after expanding 1% in July. The highest jump was inMVX Qatar, which doubled, while MVX Kuwait was down 16%.

Valuations are down across most markets, between 10x-15x, as marketperformance has declined while earnings growth remains relatively healthy.

September 2011

Research Highlights:Review of global and regionalstock markets for the month of

August 2011

Markaz Research isavailable on BloombergType “MRKZ” <Go>

M.R. Raghu CFA, FRMHead of Research+965 2224 [email protected]

Layla Al-Ammar Assistant Manager+965 2224 8000 ext. [email protected]

Kuwait Financial CentreS.A.K. “Markaz”

P.O. Box 23444, Safat 13095,KuwaitTel: +965 2224 8000Fax: +965 2242 5828markaz.com

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 2/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 2

Global Markets Review – August 2011

World markets tumbled under pressure from continued economic issues inthe US in addition to the impact of the 5 th August S&P downgrade of UScredit. Signs of flagging US demand and progress in Libya brought crude oil

prices down 2% for the month, closing at $115.09 per bbl (Brent), with a YTD gain of 24%. Conversely, the uncertainty has been a boon for Gold;the precious metal saw its highest monthly gain in 21-months, up 13% in

August to close at $1,826/oz.

The broad index tumbled by 7.3% in August bringing the YTD loss to 4%(Figure 1). The largest contribution was the US with a market cap weightedloss of 2.4%.Figure 1: MTD Market Cap Weighted returns of MSCI World

Monthly returns were highly negative across the board; the worstperformance came from MSCI Europe, tumbling 10.4% for the month.Shanghai and Frontier Markets saw the least losses, shedding 5% and5.2%, respectively, during August.

Figure: 2 –Returns – August 2011 (%)

The broad index tumbled by

7.3% in August bringing the YTD loss to 4%

Monthly returns were negativeacross the board

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 3/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 3

World

Investor‟s remained focused on the US for the month, reacting to the S&Pcredit downgrade in addition to subsequent downgrade of Fannie Mae andFreddie Mac to AA+ from triple A. Mid-month saw Fitch affirm the US rating

while awarding it a „Stable‟ outlook versus „Negative‟ calls from S&P andMoody‟s.

Investors were also rankled by problems at Bank of America (BoA) whoseshares tumbled 20% in the first week of August after AmericanInternational Group (AIG) filed a USD 10 bn lawsuit against the Bank alleging misrepresentation on the quality of mortgages that went intoMortgage-backed Securities (MBS) that ultimately led to AIG‟s massivelosses.

Also during the month, Moody‟s downgraded Japan‟s government debt byone-notch to Aa3, with a „Stable‟ outlook, citing a build -up of debt since the

global recession of 2009 in addition to unstable political conditions whichare hampering the implementation of effective economic policies. Accordingto Moody‟s, Japan‟s public debt is almost 5x the size of its economy1.

Bond yields have been dropping as well, pushing prices up; the JPMorganEmerging Market Bond Index jumped 25% for the month after gaining 10%in July (Figure 12).

Predictably, risk spiked in August as markets fluctuated vastly; MVX S&Pand MVX EM doubled during the month while MVX India and MVX Chinaexpanded by 1.7x and 1.2x, respectively. The CBOE VIX Index jumped 25%for the month and is up 78% for the year.

Chart Pack – Global Markets

Figure: 3 – Capital Flows to Emerging Economies Figure: 4 - Feds Fund Target Rate

Figure: 5 - Trade Weighted Dollar Figure: 6 -Homebuilders housing market index

1 Reuters

Predictably, risk spiked in August as markets fluctuatedvastly

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 4/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 4

Figure: 7 - US Unemployment rate (Seasonally Adj) Figure: 8 - Crude Brent Oil Prices

Figure: 9 - Ted Spread Figure: 10 - CBOE VIX

Figure: 11 - CRB Commodity Index Figure 12: JPM EMBI Global Spread

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 5/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 5

GCC Markets Review – August 2011

GCC markets tumbled on global cues during the month; S&P GCC lost5.12% as Saudi tumbled 6.46% for the month. Kuwait‟s weighted indexfollowed with a loss of 3.4%. All markets were in the red; the least decline

was a 0.67% loss on the Abu Dhabi exchange which is the best performingGCC index for the year thus far.

Table: 1 - Market Indicators

M. Cap (USDBn)

Last August 2011 YTD 2010 P/E

Indicators Close % % TTM

Saudi (TASI) 317 5,979 -6.46 -9.69 8.15 12

Kuwait SE WT.INDEX 108 402 -3.39 -17.07 25.00 14

Qatar(Doha SM) 92 8,290 -1.34 -4.51 24.50 11

Abu Dhabi (ADI)^ 76 2,602 -0.67 -4.33 -1.51 8

Dubai (DFMGI) 50 1,475 -2.84 -9.57 -10.08 8

Bahrain (BAX) 18 1,261 -2.37 -11.96 -2.11 9Oman(Muscat SM) 13 5,703 -1.82 -15.58 5.92 11

S&P GCC CompositeIndex

221 89 -5.12 -11.54 12.70 12

Source: Excerpt from Markaz „Daily Morning Brief‟ Aug 29th , 2011

Inflation was a concern briefly for GCC states during 2010 and early 2011as governments enacted large-scale spending and welfare programs.However, Inflation has started to ease and should decline further in 2012.Worries about food inflation should abate given the global economicslowdown, bringing down commodity prices2.

According to Booz & Co., GCC countries should push for morecomprehensive economic integration to boost competitive advantages on aglobal scale. The consultancy group stated that "The region has shownadmirable growth in the past decade, yet that growth represents the effortsof six individual states, rather than a coherent and aligned group operatingas an integrated economic entity." Such economic cohesion would bringsizeable benefits to the bloc, through the exploiting of comparativeeconomic advantages, creating a more attractive environment for foreigninvestors in addition to strengthening the bloc‟s bargaining power withother economic blocs such as the EU.

Saudi Arabia

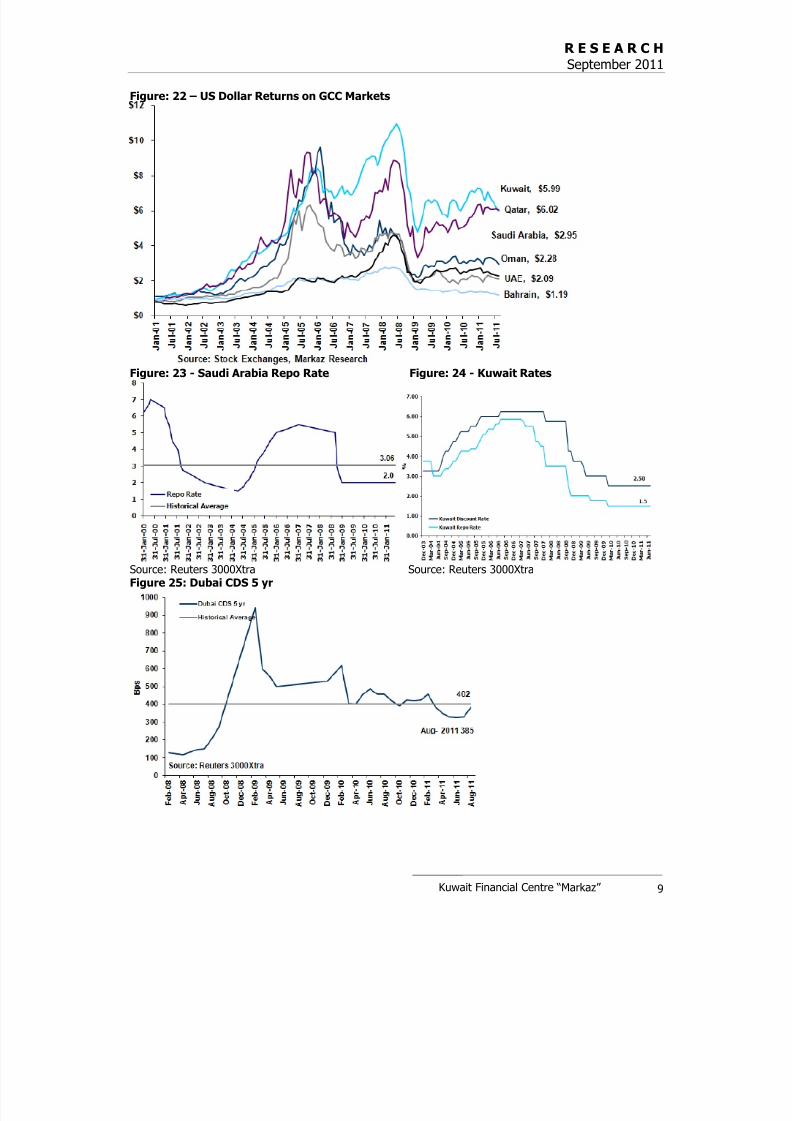

SAMA held its key interest rates unchanged; overnight reverse repo at0.25% and benchmark repurchase at 2%, citing modest growth in lendingactivity among the Kingdom‟s banks. Money supply in the Kingdom (M3)was up 13% YoY in July while net foreign assets expanded by 20%.Inflation was up to 4.9% in July (the largest monthly jump since 2008),although a moderate increase from the 4.7% registered in the previousmonth; inflation is being closely monitored given large scale funding andsocial welfare programs enacted during the year.

Saudi Electricity (SEC) will start an electricity-transmission unit early nextyear as part of a restructuring plan which was announced in mid-2009. Thepower producer is also aiming to start a distribution unit and four separate

power-generating units by early 2013. The stock was down 2.63% forthe month.

2 Capital Economics

GCC markets tumbled in August

Inflation has started to easeand should decline furtherin 2012

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 6/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 6

Savola Group was up 3.86% for the month as 2Q11 net income wasup 11% YoY on sales growth and expansion. However, bottom line for 1H11was down 34% YoY.

United Arab Emirates

According to official figures, UAE non-oil import growth more than doubledto 22% in May (YOY), however, exports and re-exports slowed sharply dueto a continued global economic slowdown. UAE Non-oil foreign trade pickedup early in the year, boosted by growth in Asia.

Nakheel completed its restructuring of USD16 bn in debt and is workingtowards delivering pending projects and the repayment of investors. Thedeveloper has begun issuing the first tranche of its $1 bn Sukuk.

Dubai CDS jumped 17% for the month, but is still down 8% for the year.

Kuwait

According to a statement by the State‟s ruler, m isuse of Kuwait's statebudget surplus, including unproductive spending, has led to structuralimbalances in the economy. The state posted a budget surplus of USD 19.4bn in the 2010/11 fiscal year, a decline of 38%.

Global Investment House, which undertook a restructuring of nearly USD 2bn in debt back in 2009, has begun initial talks with creditors on thepossibility of extending debt repayments3. The investment company made anet loss of USD 142 mn in 1H11, compared with a net loss of USD 126mn inthe same period of the previous year. Global stock was down 9.68%for the month and has shed 41% for the year.

Qatar

Qatar National Bank (QNB) is planning to set up a USD7.5 bn medium-termnote bond program to fund its banking activities. The bank registered a30% increase in net profits in 1H11 while the stock was flat for themonth.

The central bank cut interest rates to 4.5% to further boost loans growth;total lending was up 14% YoY in July boosted by the trade and real estatesectors.

Qatar is planning to invest between USD 20-25 bn in tourism infrastructuredevelopment over the next decade in preparation for the 2022 World Cup,the majority of which will be in hotels. The country, which currently has10,000 hotel rooms, will add an additional 5,500 in 2011 with a goal toreach 30,000 by 2013 with 5,000 new rooms coming on stream each yearthrough 20224.

Qatar is also one of the bidding nations to host the Summer Olympics in2020.

3 Al Qabas4 Qatar Tourism Authority

Dubai CDS jumped 17% forthe month, but is still down8% for the year

Liquidity was down again in August; GCC value tradeddeclined 15% to USD 17.76bn

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 7/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 7

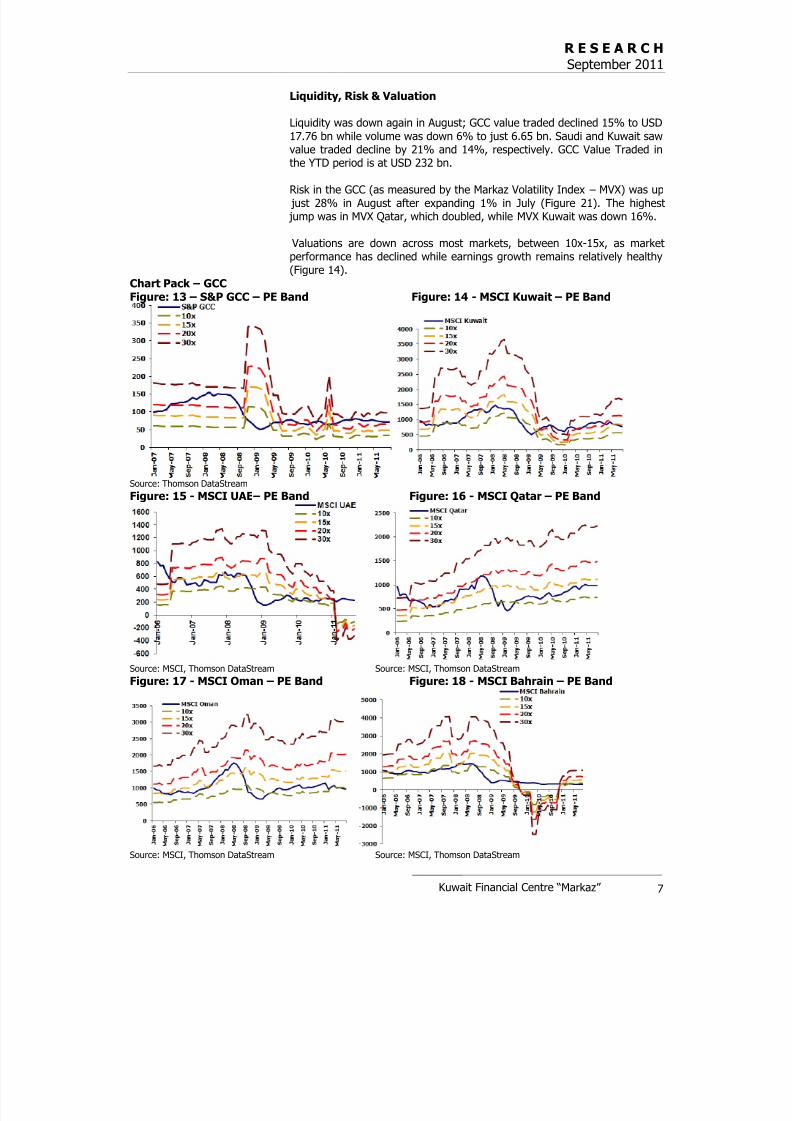

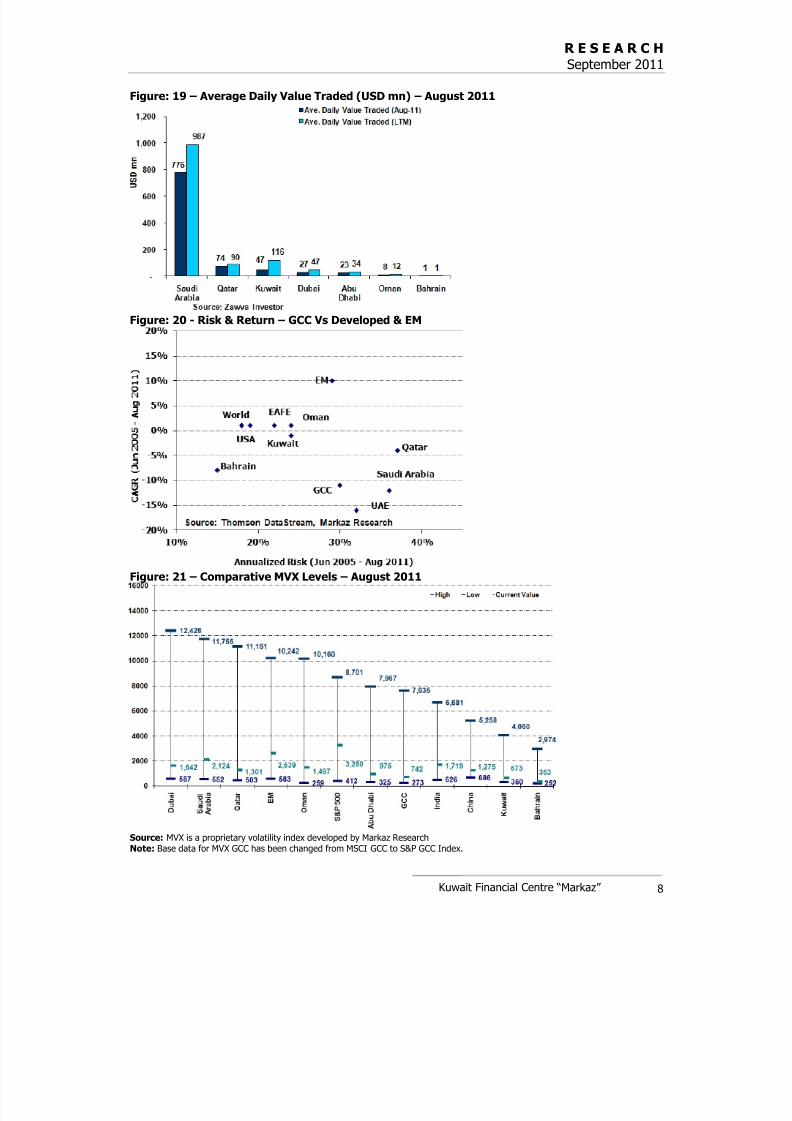

Liquidity, Risk & Valuation

Liquidity was down again in August; GCC value traded declined 15% to USD17.76 bn while volume was down 6% to just 6.65 bn. Saudi and Kuwait sawvalue traded decline by 21% and 14%, respectively. GCC Value Traded in

the YTD period is at USD 232 bn.

Risk in the GCC (as measured by the Markaz Volatility Index – MVX) was up just 28% in August after expanding 1% in July (Figure 21). The highest jump was in MVX Qatar, which doubled, while MVX Kuwait was down 16%.

Valuations are down across most markets, between 10x-15x, as marketperformance has declined while earnings growth remains relatively healthy(Figure 14).

Chart Pack – GCCFigure: 13 – S&P GCC – PE Band Figure: 14 - MSCI Kuwait – PE Band

Source: Thomson DataStream

Figure: 15 - MSCI UAE – PE Band Figure: 16 - MSCI Qatar – PE Band

Source: MSCI, Thomson DataStream Source: MSCI, Thomson DataStream Figure: 17 - MSCI Oman – PE Band Figure: 18 - MSCI Bahrain – PE Band

Source: MSCI, Thomson DataStream Source: MSCI, Thomson DataStream

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 8/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 8

Figure: 19 – Average Daily Value Traded (USD mn) – August 2011

Figure: 20 - Risk & Return – GCC Vs Developed & EM

Figure: 21 – Comparative MVX Levels – August 2011

Source: MVX is a proprietary volatility index developed by Markaz ResearchNote: Base data for MVX GCC has been changed from MSCI GCC to S&P GCC Index.

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 9/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 9

Figure: 22 – US Dollar Returns on GCC Markets

Figure: 23 - Saudi Arabia Repo Rate Figure: 24 - Kuwait Rates

Source: Reuters 3000Xtra Source: Reuters 3000XtraFigure 25: Dubai CDS 5 yr

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 10/13

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz” 10

Data Tables – GCC

Data Table: 1 - Value & Volume Traded Indicators

Volume Parameters Value Parameters

% of

VolumeTraded

% of

ValueTraded

Volume

Traded(Mn)

LTM Avg Volume

Traded(Mn)

MoMTop 5 Volume

Traded

Concentrationin Market Cap

ValueTraded

(USDMn)

LTM Avg ValueTraded

(USDMn)

MoMTop 5 Value

Traded

Concentrationin Market Cap

Deviation(%)

Deviation(%)

34% 79%Saudi

Arabia2,234 3,384 -14% 28% 13,976 20,068 -21% 30%

23% 6% Kuwait 1,542 3,744 -14% 1% 991 2,384 -14% 37%

38% 6% UAE 2,529 4,088 3% 8% 1,064 1,687 16% 25%

2% 9% Qatar 133 188 71% 25% 1,552 1,885 76% 47%

2% 1% Oman 165 215 75% 25% 166 252 81% 42%

1% 0% Bahrain 46 42 41% 30% 14 20 19% 37%

TotalGCC

6,648 11,661 -6% 17,762 26,296 -15%

Source: Markaz Research

Data Table: 2 - Value traded (USD Bn)

2004 2005 2006 2007 2008 2009 2010 2011Saudi (TASI) 473 1103 1403 682 522 338 202 187

Kuwait (KSE) 51 97 60 131 134 75 44 16

Abu Dhabi (ADX) 4 29 19 48 83 19 9 5.2

Dubai (DFM) 14 110 95 103 63 48 19 7.1

Qatar (DSM) 6 28 21 30 47 26 19 15.4

Oman (MSM) 2 3 2 5 9 6 3 1.9

Bahrain (BAX) 0.4 0.6 1.4 0.9 2.2 0.48 0.29 0.2

Total 550 1371 1601 1000 860 512 296 232

Note: 2011 Value Traded is up to July 2011Source: Zawya

Data Table: 3 - Blue Chips Performance

Companies

M.Cap(USDBn)

LastClose(Lc)

MonthlyChange

2010Change P/E TTM

2Q 2011Earnings

YTD PAGrowth)

Saudi Arabia (SAR)

SABIC 74 92 -10.5 -12 31 10 8,101 62

Al-Rajhi Bank 28 69.8 -3.1 -1621 15 1,700 1

Saudi Telecom 18 34.3 -2.6 -19 4 7 2,256 9

Saudi Electricity Co. 14 13 -2.6 -7 32 21 1,335 25

Samba Fin. Group 11 43.9 -9.7 -28 25 9 1,102 -10

United Arab Emirates (AED)ETISALAT 22 10.3 0 -5 14 11 1,594 -15

NBAD 9 11.3 0.4 15 5 9 1,026 2

First Gulf Bank 7 15.9 -3.6 -9 17 7 890 13

Emirates NBD 6 4.1 -3.7 50 0 8 744 87Emaar Properties 5 2.8 -2.4 -21 -8 11 250 -69

Kuwait (KWD)

ZAIN 15 0.9 -5.1 -38 71 13 70* 36

NBK 15 1.1 -1.9 -19 55 14 66 -5

KFH 9 0.9 1.1 -17 16 29 23 -27

Gulf Bank 4 0.5 -3 -15 90 34 9 485

Comm. Bk. Kuwait4 0.9 1.2 -8 -1 26 1 NM

Qatar (QAR)

Industries Qatar19 123.1 -10.5 -11 21 10 2,076 46

QNB24 139.1 -0.3 5 61 12 1,809 26

Ezdan Real Est. Co.16 22 -0.6 -28 46 NM 37 -49

Q-TEL 7 143.5 -4.3 -4 23 10 762 -37

Comr‟cial Bk of Qatar 5 78.1 5.4 -15 49 11 509 25

Source: Excerpt from Markaz Daily Morning Brief

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 11/13

R E S E A R C H September 2011

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 12/13

R E S E A R C H September 2011

8/4/2019 Murphy's Law in Action

http://slidepdf.com/reader/full/murphys-law-in-action 13/13

R E S E A R C H September 2011

Disclaimer

This report has been prepared and issued by Kuwait Financial Centre S.A.K (Markaz), which is regulated bythe Central Bank of Kuwait. The report is owned by Markaz and is privileged and proprietary and is subjectto copyrights. Sale of any copies of this report is strictly prohibited. This report cannot be quoted without theprior written consent of Markaz. Any user after obtaining Markaz permission to use this report must clearlymention the source as “Markaz “.This Report is intended to be circulated for general information only andshould not to be construed as an offer to buy or sell or a solicitation of an offer to buy or sell any financialinstruments or to participate in any particular trading strategy in any jurisdiction. The information andstatistical data herein have been obtained from sources we believe to be reliable but in no way arewarranted by us as to its accuracy or completeness. Markaz has no obligation to update, modify or amendthis report.

This report does not have regard to the specific investment objectives, financial situation and the particular

needs of any specific person who may receive this report. Investors are urged to seek financial adviceregarding the appropriateness of investing in any securities or investment strategies discussed orrecommended in this report and to understand that statements regarding future prospects may not berealized. Investors should note that income from such securities, if any, may fluctuate and that eachsecurity‟s price or value may rise or fall. Investors should be able and willing to accept a total or partial lossof their investment. Accordingly, investors may receive back less than originally invested. Past performanceis historical and is not necessarily indicative of future performance.

Kuwait Financial Centre S.A.K (Markaz) does and seeks to do business, including investment banking deals,with companies covered in its research reports. As a result, investors should be aware that the firm mayhave a conflict of interest that could affect the objectivity of this report.

For further information, please contact „Markaz‟ at P.O. Box 23444, Safat 13095, Kuwait. Tel: 00965 1804800 Fax: 00965

22450647. Email: [email protected]