mns viewpoint ott disruption in the telecom market...

TRANSCRIPT

Viewpoint

1 OTT disruption in the telecom market: opportunity or threat ?

MNS Viewpoint

OTT disruption in the telecom market: opportunity or threat ?

1. Introduction

OTT (Over the Top) refers to any application that provides a product or service over the internet and

bypasses traditional distributors such as internet service providers and telecom operators.

Since 2009, key OTT players rapidly disrupted the telecom market, and incurred to traditional

operators loss of revenues and declining profitability by introducing new delivery models and

business models.

We will focus in this whitepaper on the analysis of the strategy of the key players of the 2 main

segments: OTT communication and OTT media as described in the figure 1 below, and their related

impact on the telecom market.

Viewpoint

2 OTT disruption in the telecom market: opportunity or threat ?

Fig.1: the 2 main OTT segments

.The market is dominated by the « Fab Five », composed by: Google, Apple, Microsoft, Facebook,

Amazon, which usually operate on both segments.

2. Communication segment

The communication segment is splitted in

two:

Messaging applications such as WhatsApp

Voice and Video applications such as

Skype.

But more and more OTT applications provide

both services on the same platform.

OTT communications providers basically

deliver “free” services: they enable to send

text, media messages, or to make voice and

video phone calls via a dedicated “VoIP”

application free of charge.

They create minimum constraints and

requirements for consumers who only need

to get compatible devices with internet

access. (Potentially both end-users need to

install the same application, the same mobile

OS or a termination enabled service).

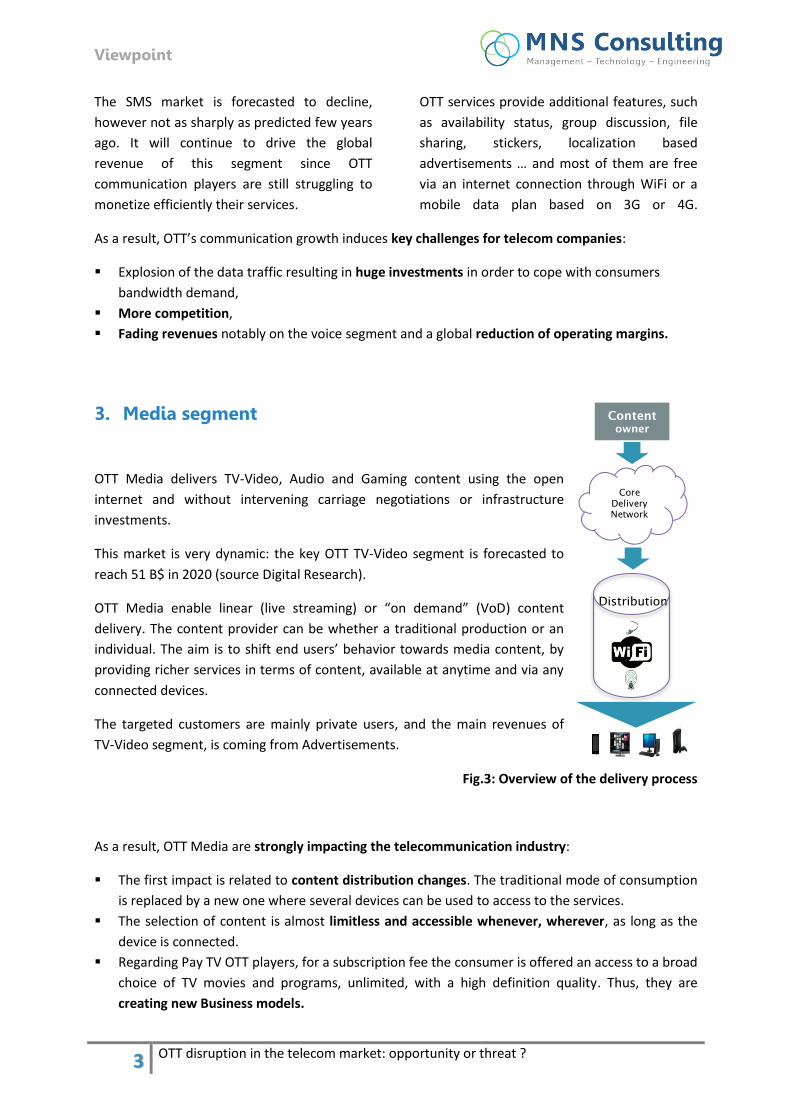

This strategy has leaded to quick successes and opened new perspectives: OTT applications are

today overtaking traditional SMS and voice services. According to Analysys Mason (see Figure 2), SMS

is taken over by OTT messaging (including text and media messages) since 2013.

Fig.2: Messages forecasts (trillion)

0

5

10

15

20

25

30

35

40

45

50

OTT IP Messaging

Operator IP Messaging

SMS

Viewpoint

3 OTT disruption in the telecom market: opportunity or threat ?

The SMS market is forecasted to decline,

however not as sharply as predicted few years

ago. It will continue to drive the global

revenue of this segment since OTT

communication players are still struggling to

monetize efficiently their services.

OTT services provide additional features, such

as availability status, group discussion, file

sharing, stickers, localization based

advertisements … and most of them are free

via an internet connection through WiFi or a

mobile data plan based on 3G or 4G.

As a result, OTT’s communication growth induces key challenges for telecom companies:

Explosion of the data traffic resulting in huge investments in order to cope with consumers

bandwidth demand,

More competition,

Fading revenues notably on the voice segment and a global reduction of operating margins.

3. Media segment

OTT Media delivers TV-Video, Audio and Gaming content using the open

internet and without intervening carriage negotiations or infrastructure

investments.

This market is very dynamic: the key OTT TV-Video segment is forecasted to

reach 51 B$ in 2020 (source Digital Research).

OTT Media enable linear (live streaming) or “on demand” (VoD) content

delivery. The content provider can be whether a traditional production or an

individual. The aim is to shift end users’ behavior towards media content, by

providing richer services in terms of content, available at anytime and via any

connected devices.

The targeted customers are mainly private users, and the main revenues of

TV-Video segment, is coming from Advertisements.

Fig.3: Overview of the delivery process

As a result, OTT Media are strongly impacting the telecommunication industry:

The first impact is related to content distribution changes. The traditional mode of consumption

is replaced by a new one where several devices can be used to access to the services.

The selection of content is almost limitless and accessible whenever, wherever, as long as the

device is connected.

Regarding Pay TV OTT players, for a subscription fee the consumer is offered an access to a broad

choice of TV movies and programs, unlimited, with a high definition quality. Thus, they are

creating new Business models.

Content owner

Core

Delivery

Network

Distribution

Viewpoint

4 OTT disruption in the telecom market: opportunity or threat ?

Network Operators used to provide control and distribute the media content. When OTTs have

emerged, their only value and task became the delivery of content packets.

The explosion of data traffics: OTT media is the major contributor to the boming mobile data

traffic with VoD and Live Streaming (Youtube is at the forefront of this revolution)

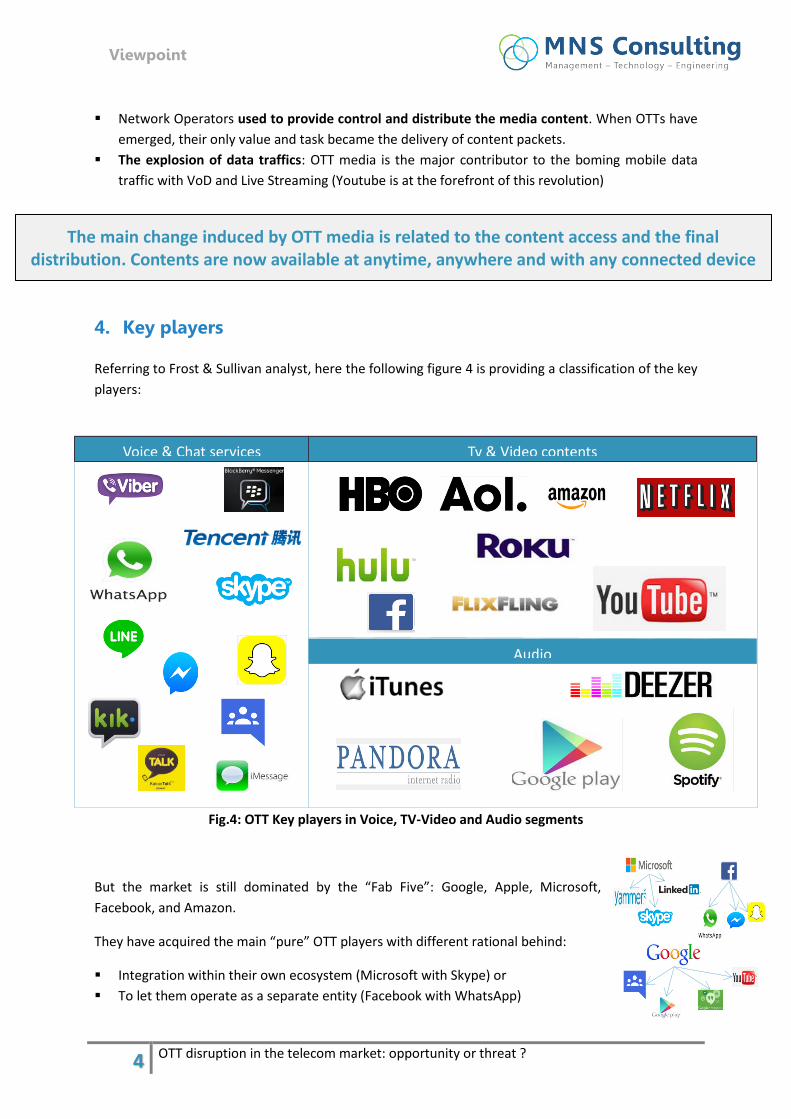

4. Key players Referring to Frost & Sullivan analyst, here the following figure 4 is providing a classification of the key

players:

Fig.4: OTT Key players in Voice, TV-Video and Audio segments

But the market is still dominated by the “Fab Five”: Google, Apple, Microsoft,

Facebook, and Amazon.

They have acquired the main “pure” OTT players with different rational behind:

Integration within their own ecosystem (Microsoft with Skype) or

To let them operate as a separate entity (Facebook with WhatsApp)

The main change induced by OTT media is related to the content access and the final distribution. Contents are now available at anytime, anywhere and with any connected device

Voice & Chat services Tv & Video contents

Audio

Viewpoint

5 OTT disruption in the telecom market: opportunity or threat ?

5. The disruption induced by the launch of OTTs

During the last 7 years, the rapid growth of OTT players

quickly leaded to huge loss of revenues for traditional Telecom

providers, especially regarding voice and messaging market

segments. The impact has been most evident in Europe where

notably WhatsApp gained a particular traction.

Today, the loss of revenue to OTT messaging services is worth

7% in the voice segment, and up to 28% of mobile network

operator’s messaging revenue (Source OVUM), and the

forecasts clearly underline the growing market share of OTT

messaging players. Fig.5: Operators’ EBITDA Margin

However, there are signs of stabilization in the margin trends since 2014, mainly due to market

consolidation, moves and rationalization of operators.

Several strategies have been adopted by mobile network operators (MNOs), in order to compete

with OTT players:

A defensive strategy: consisting to block OTT services in particular VoIP. For example, last year

UAE operators blocked the VoIP call functionality rolled out by WhatsApp messenger.

An offensive strategy: where MNOs develop and promote their own OTT messaging service. For

example, in France, Bouygues Telecom has launched « World& YOU », an OTT messaging app

like, enabling to send messages and make calls for the company’s customer who are staying

abroad. The pre-requisite is to have a WiFi access.

A collaborative strategy: working closely with OTT messaging players in order to monetize

effectively the services. For example, Vodafone UK has launched a data plan, available with a 4G

subscription that gives a free subscription to Netflix or Spotify for example.

And finally the neutral strategy: adopted by a large majority of network operators few years ago.

The combination of offensive and collaborative strategies seems to be the most relevant to be adopted by telecom operators

36,90% 36,40%

34,90%

33,50% 33,30% 33,50%

Viewpoint

6 OTT disruption in the telecom market: opportunity or threat ?

6. The key issues for OTT development

Even if OTTs were successful in the last decade, they are still facing major challenges to continue

their development:

The need for global reach: infrastructure is a key challenge for OTT players. Even though

reachability is not an issue within big connected cities and more generally in developed

countries, according to the latest figures from Internet World Stats, 57% of the world

population don’t have access to internet

High and dynamic consumer demand: end users are having more and more requirements

regarding the quality of experience as well as the richness of the contents. OTT services are

unmanaged and the quality of delivery depends on the quality of the end user’s network.

However, major improvements have been made in the end delivery chain including for

example ABR streaming which enables the switch between different versions of a given video

when a low bandwidth is detected.

Regulatory challenges: regarding Pay TV operators and audio content distributors. Rights

management have been an increasing issue with the proliferation of Peer to Peer sharing

Monetization of OTT services: deals with the ability of OTT players to find the right business

model that gives incentives to pay for their services. That statement is particularly true for

OTT communication players.

The ability to add more adjacent services thanks to localization, target advertising and a

more sophisticated use of end users pieces of information.

A better collaboration between OTT players and connected devices manufacturer, in order

to expand their device penetration and notably within emerging markets. According to GSMA

study, the adoption rate within developed markets has almost reached 60% in 2014, ranging

from 51% in Europe to 70% in North America

Reachability, less dependence to traditional players’ infrastructure and a good monetization model is key to the growth of OTT players

Viewpoint

7 OTT disruption in the telecom market: opportunity or threat ?

7. About MNS

MNS Consulting is an international strategy and engineering consulting firm specialized in the

telecommunications industry. We have developed a unique expertise in Telecoms network domains.

We distinguish ourselves with a strong combination of deep technological expertise and strategic

vision that allows us to address the challenges of our customers. We are committed to delivering

outstanding consulting services and highest value to our clients by helping them to drive growth,

manage complexity, and improve operations and performance in a complex and fast changing

market. Our strategy consulting capabilities are structured around 5 practices as described below.

MNS is headquartered in Paris and has also operations in Africa and the Middle East.

For further information please visit: www.mns-consulting.com

5 MAIN CAPABILITIES

Business Strategy

Operational Excellence

Technology Advisory

Private Equity Telecoms

Regulatory & Policy Mngt