keisuke sadamori director of energy markets and …eneken.ieej.or.jp/data/6326.pdf · keisuke...

TRANSCRIPT

© OECD/IEA 2015 © OECD/IEA 2015

Keisuke Sadamori Director of Energy Markets and Security, IEA

The 88th IEEJ Energy Seminar, 5th October 2015

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

Profound changes underway in energy markets

Signs of decoupling of energy-related CO2 emissions and global economic growth

Oil prices have fallen precipitously, raising questions over the competitiveness of renewables

But policy drivers for renewable electricity – energy diversification, local pollution and decarbonisation – remain robust

Renewables are key to the unprecedented pledges ahead of COP 21

Renewables to become first source for electricity in the longer term, but addressing policy uncertainty in the next five years is crucial

2

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

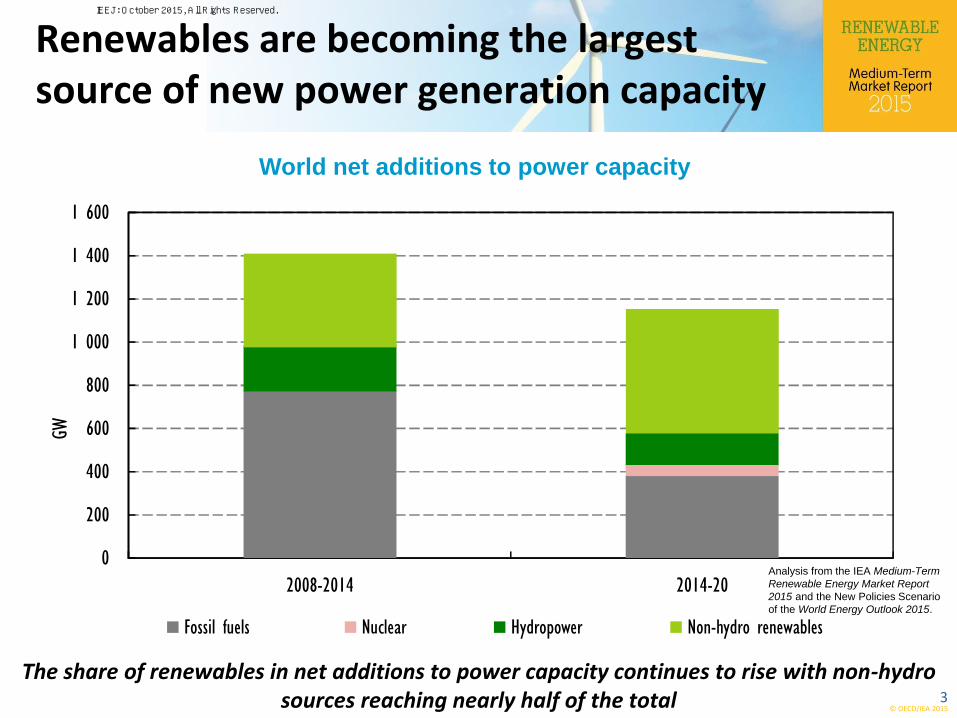

The share of renewables in net additions to power capacity continues to rise with non-hydro sources reaching nearly half of the total

Renewables are becoming the largest source of new power generation capacity

World net additions to power capacity

Analysis from the IEA Medium-Term

Renewable Energy Market Report

2015 and the New Policies Scenario

of the World Energy Outlook 2015.

0

200

400

600

800

1 000

1 200

1 400

1 600

2008-2014 2014-20

GW

Fossil fuels Nuclear Hydropower Non-hydro renewables

3

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

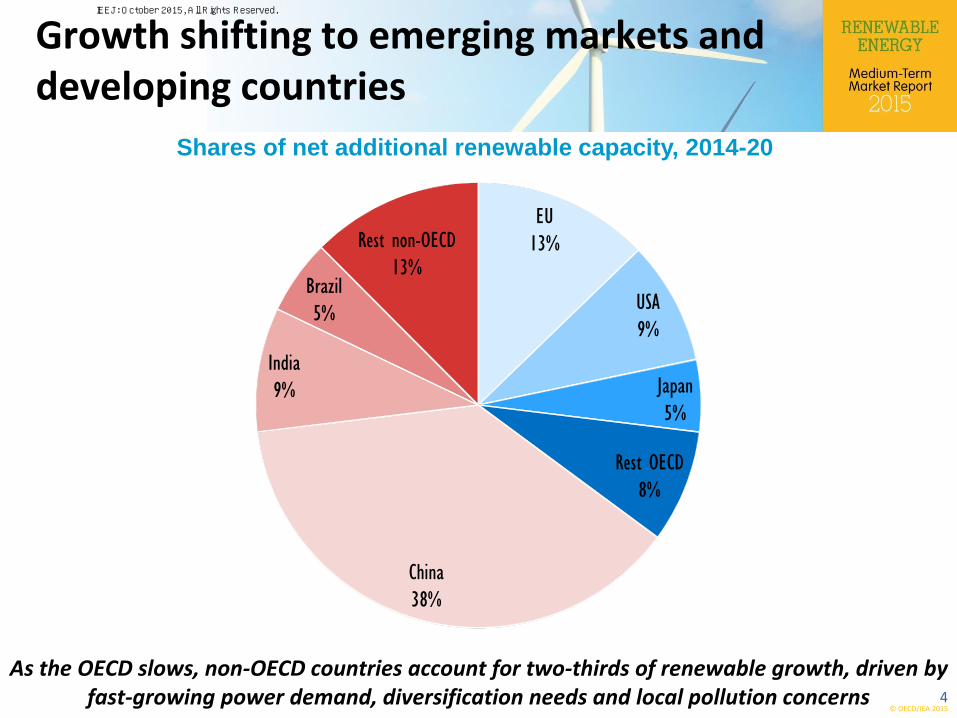

As the OECD slows, non-OECD countries account for two-thirds of renewable growth, driven by fast-growing power demand, diversification needs and local pollution concerns

Growth shifting to emerging markets and developing countries

Shares of net additional renewable capacity, 2014-20

EU

13%

USA

9%

Japan

5%

Rest OECD

8%

China

38%

India

9%

Brazil

5%

Rest non - OECD

13%

4

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

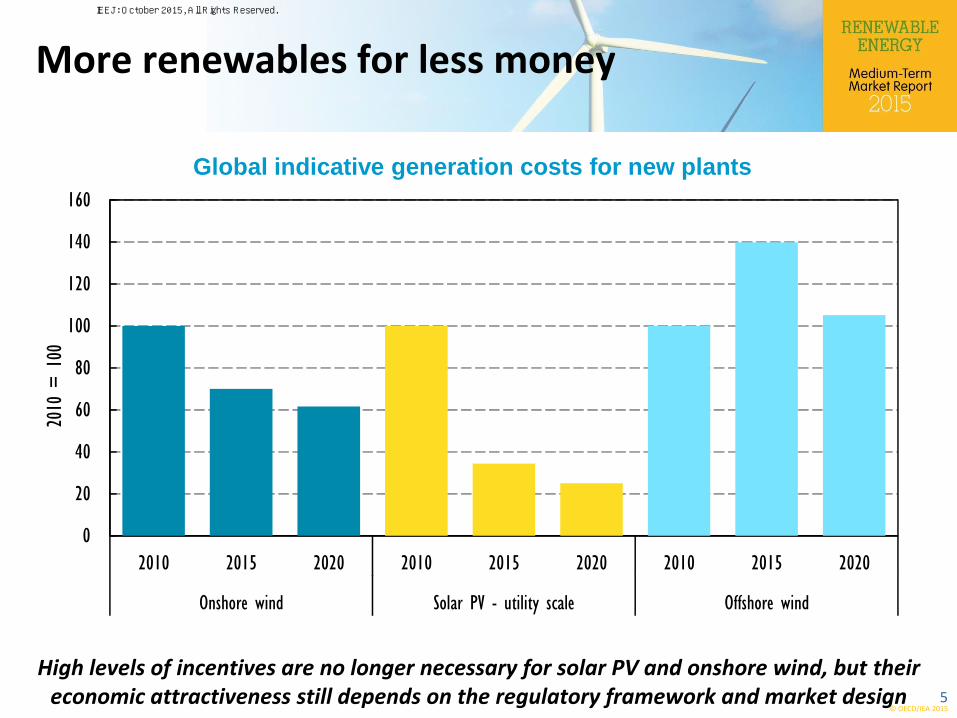

More renewables for less money

High levels of incentives are no longer necessary for solar PV and onshore wind, but their economic attractiveness still depends on the regulatory framework and market design

Global indicative generation costs for new plants

0

20

40

60

80

100

120

140

160

2010 2015 2020 2010 2015 2020 2010 2015 2020

Onshore wind Solar PV - utility scale Offshore wind

2010

= 1

00

5

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

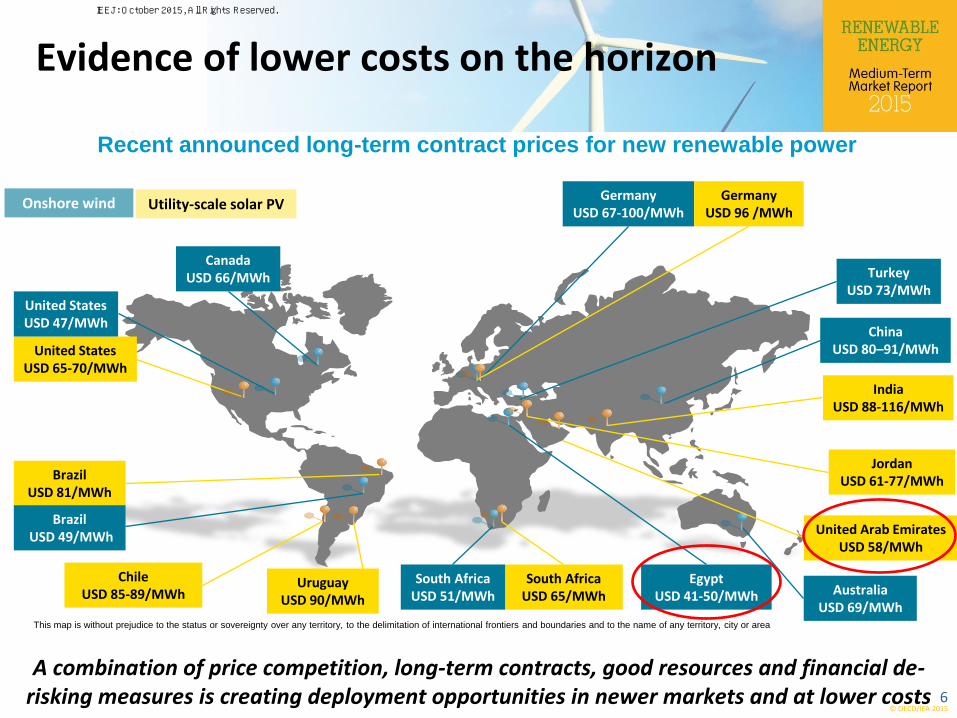

Evidence of lower costs on the horizon

A combination of price competition, long-term contracts, good resources and financial de-risking measures is creating deployment opportunities in newer markets and at lower costs

Recent announced long-term contract prices for new renewable power

Utility-scale solar PV Onshore wind

Chile USD 85-89/MWh

Brazil USD 81/MWh

United States USD 65-70/MWh

India USD 88-116/MWh

United Arab Emirates USD 58/MWh

South Africa USD 65/MWh

United States USD 47/MWh

Brazil USD 49/MWh

South Africa USD 51/MWh Australia

USD 69/MWh

Turkey USD 73/MWh

China USD 80–91/MWh

Germany USD 67-100/MWh

Egypt USD 41-50/MWh

Jordan USD 61-77/MWh

Uruguay USD 90/MWh

Germany USD 96 /MWh

Canada USD 66/MWh

This map is without prejudice to the status or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area

6

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

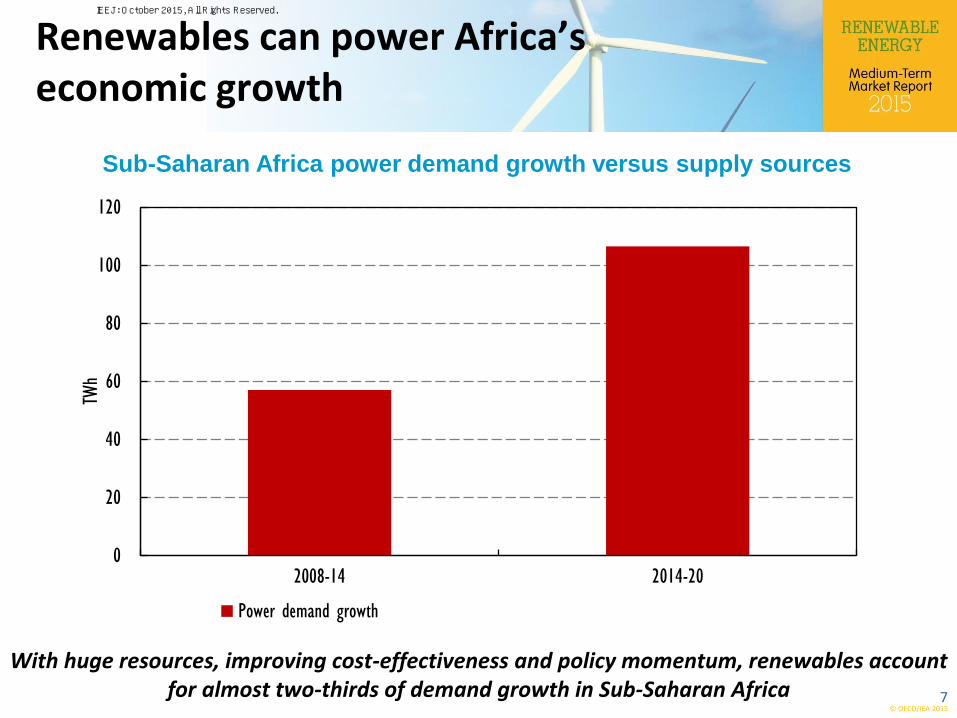

Renewables can power Africa’s economic growth

With huge resources, improving cost-effectiveness and policy momentum, renewables account for almost two-thirds of demand growth in Sub-Saharan Africa

Sub-Saharan Africa power demand growth versus supply sources

0

20

40

60

80

100

120

2008-14 2014-20

TWh

Power demand growth

7

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

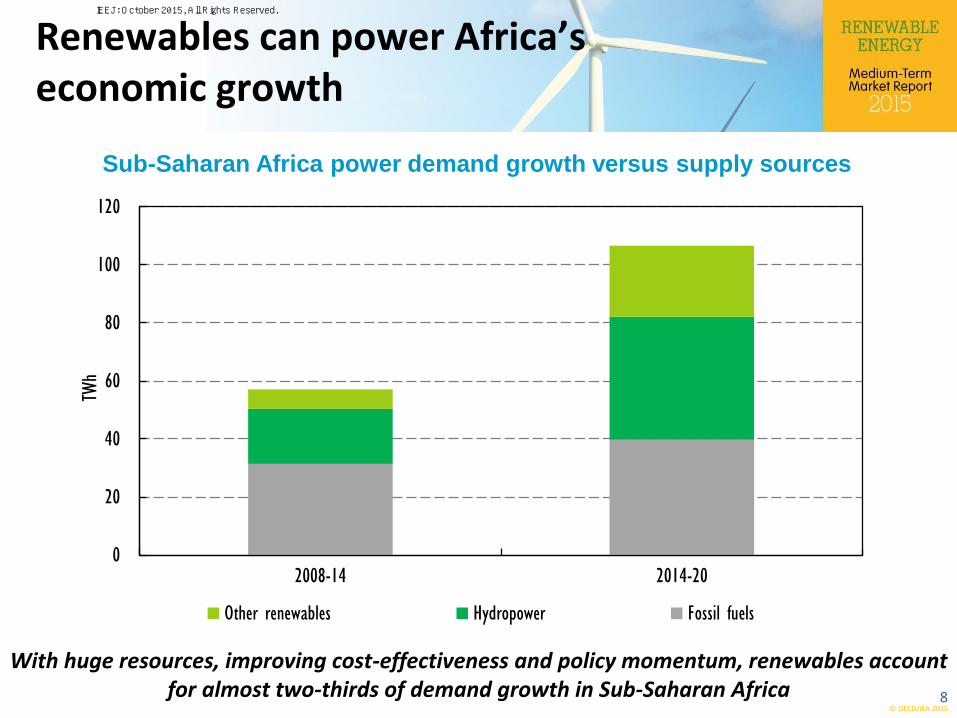

Renewables can power Africa’s economic growth

With huge resources, improving cost-effectiveness and policy momentum, renewables account for almost two-thirds of demand growth in Sub-Saharan Africa

Sub-Saharan Africa power demand growth versus supply sources

0

20

40

60

80

100

120

2008-14 2014-20

TWh

Other renewables Hydropower Fossil fuels

8

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

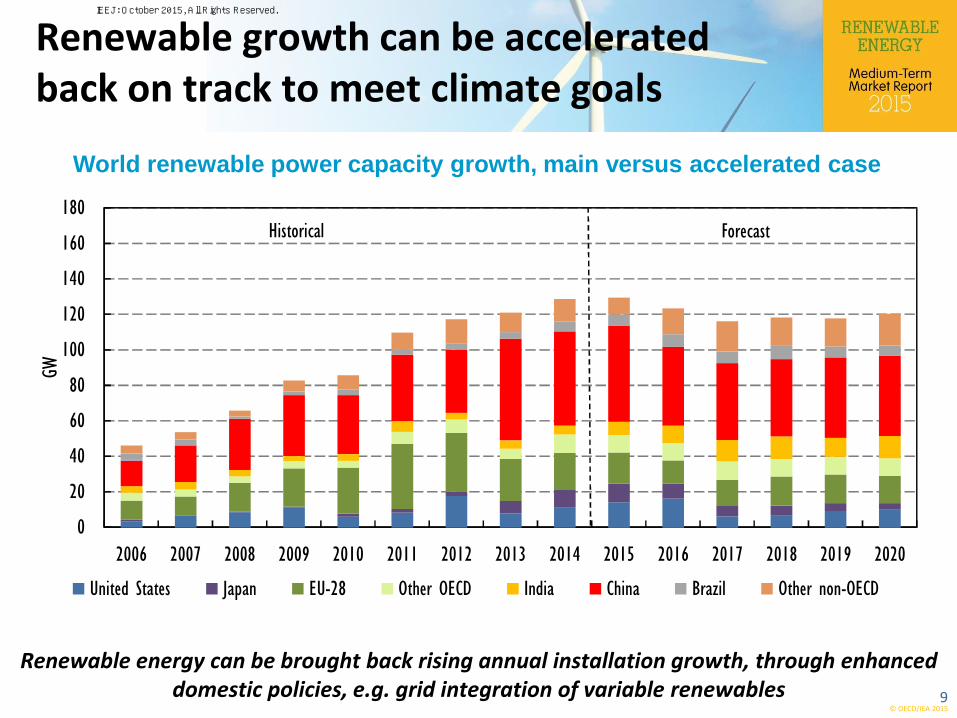

Renewable growth can be accelerated back on track to meet climate goals

Renewable energy can be brought back rising annual installation growth, through enhanced domestic policies, e.g. grid integration of variable renewables

World renewable power capacity growth, main versus accelerated case

0

20

40

60

80

100

120

140

160

180

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

GW

United States Japan EU-28 Other OECD India China Brazil Other non-OECD

Historical Forecast

9

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

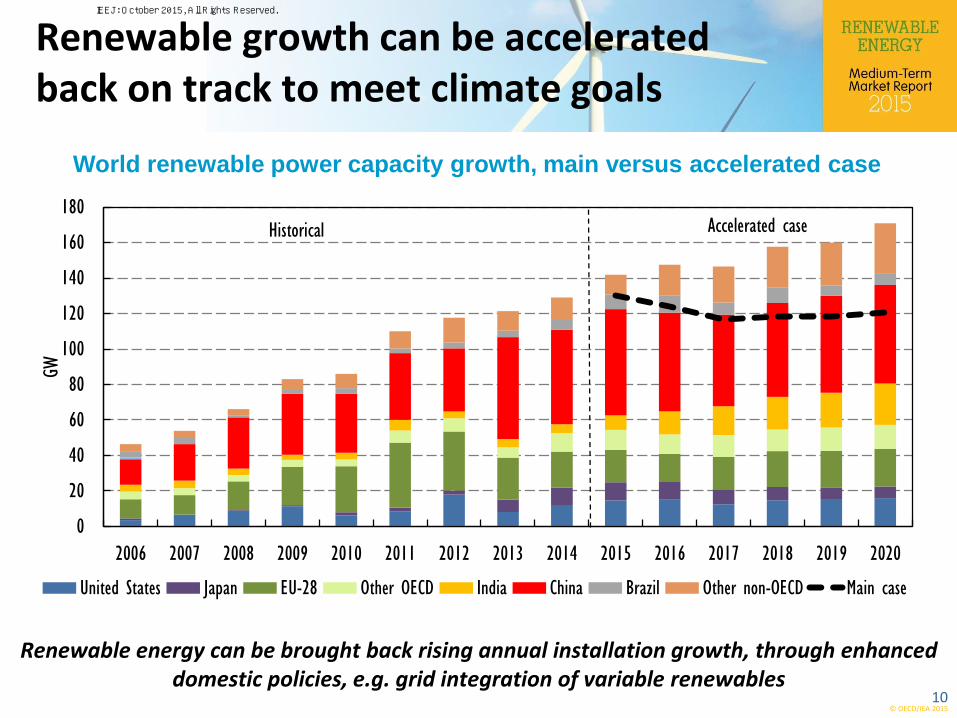

Renewable growth can be accelerated back on track to meet climate goals

Renewable energy can be brought back rising annual installation growth, through enhanced domestic policies, e.g. grid integration of variable renewables

World renewable power capacity growth, main versus accelerated case

0

20

40

60

80

100

120

140

160

180

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

GW

United States Japan EU-28 Other OECD India China Brazil Other non-OECD Main case

Historical Accelerated case

10

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

A decisive moment for the future of renewables

11

Increasingly affordable renewables are set to dominate the growing power systems of the world

The effect of the lower oil price environment on global renewable growth is more perception than reality, though biofuels are an exception

Further policy action is needed for heat and biofuel sectors, in the face of structural challenges.

Yet, wavering policy commitments risk undermining investor confidence and are dampening growth

While variability of renewables is a challenge energy systems can learn to adapt to, variability of policies poses a far greater risk

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

Global Renewable Technologies

12

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

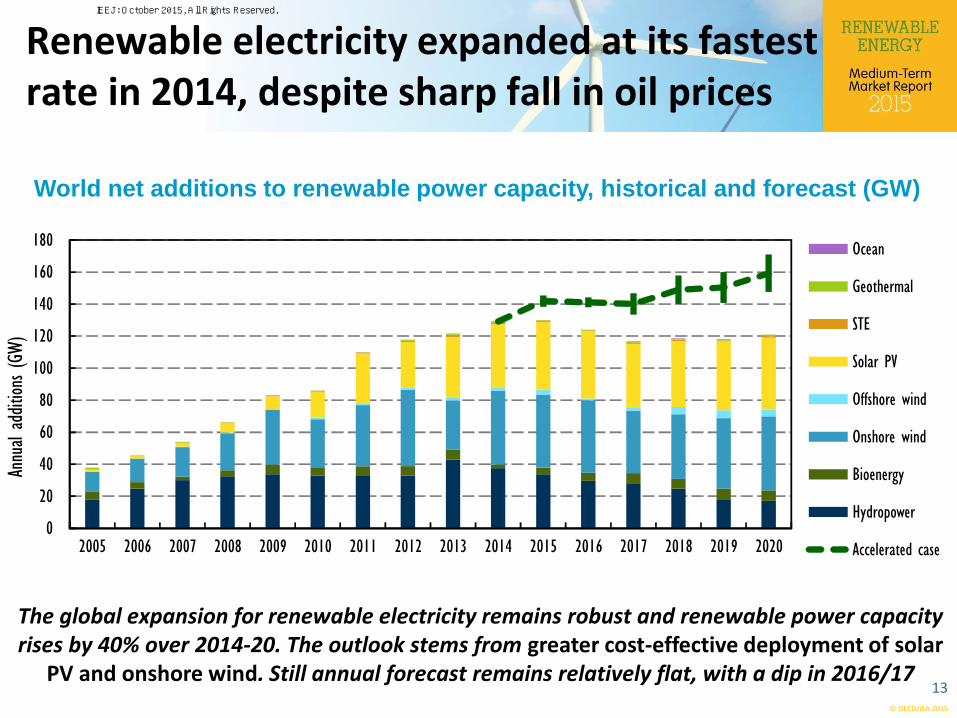

Renewable electricity expanded at its fastest rate in 2014, despite sharp fall in oil prices

World net additions to renewable power capacity, historical and forecast (GW)

The global expansion for renewable electricity remains robust and renewable power capacity rises by 40% over 2014-20. The outlook stems from greater cost-effective deployment of solar

PV and onshore wind. Still annual forecast remains relatively flat, with a dip in 2016/17 13

0

20

40

60

80

100

120

140

160

180

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Annu

al a

ddition

s (GW)

Ocean

Geothermal

STE

Solar PV

Offshore wind

Onshore wind

Bioenergy

Hydropower

Accelerated case

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

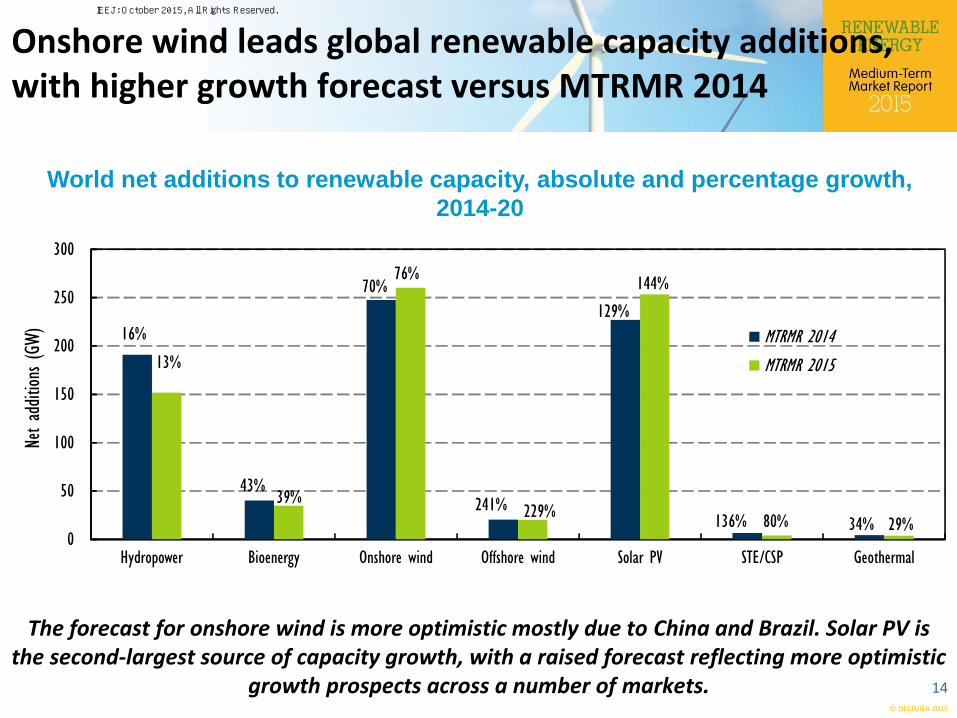

Onshore wind leads global renewable capacity additions, with higher growth forecast versus MTRMR 2014

World net additions to renewable capacity, absolute and percentage growth,

2014-20

The forecast for onshore wind is more optimistic mostly due to China and Brazil. Solar PV is the second-largest source of capacity growth, with a raised forecast reflecting more optimistic

growth prospects across a number of markets. 14

0

50

100

150

200

250

300

Hydropower Bioenergy Onshore wind Offshore wind Solar PV STE/CSP Geothermal

Net ad

ditio

ns (GW

) 16%

43%

70%

241%

129%

136% 34%

MTRMR 2014

13%

39%

76%

229%

144%

80% 29%

MTRMR 2015

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

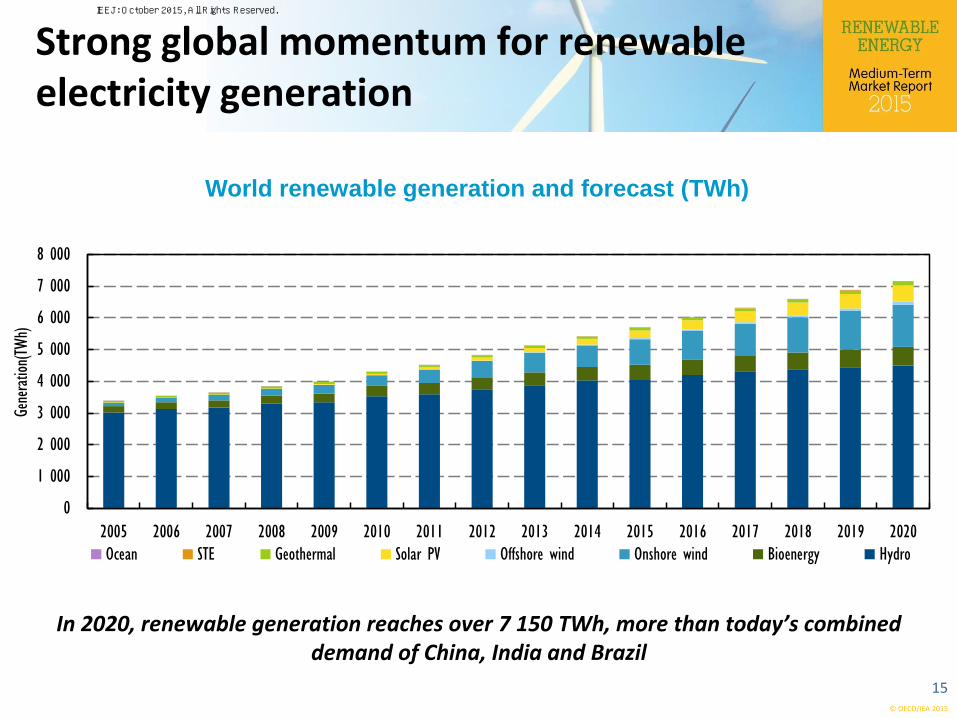

Strong global momentum for renewable electricity generation

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Generatio

n(TW

h)

Ocean STE Geothermal Solar PV Offshore wind Onshore wind Bioenergy Hydro

World renewable generation and forecast (TWh)

In 2020, renewable generation reaches over 7 150 TWh, more than today’s combined demand of China, India and Brazil

15

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

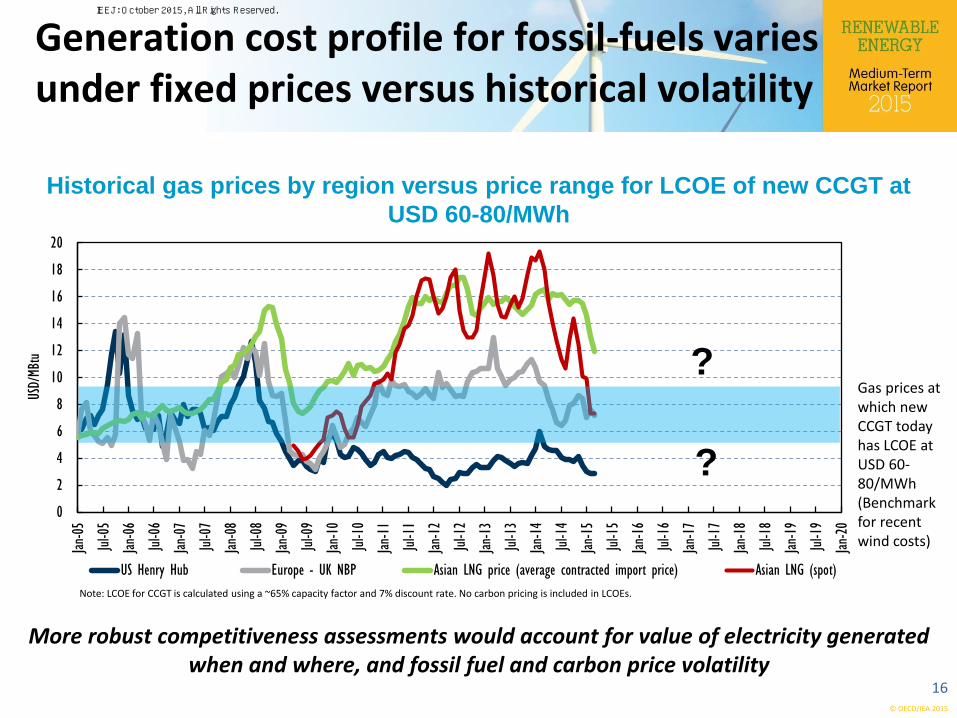

Note: LCOE for CCGT is calculated using a ~65% capacity factor and 7% discount rate. No carbon pricing is included in LCOEs.

0

2

4

6

8

10

12

14

16

18

20

Jan-05

Jul-0

5

Jan-06

Jul-0

6

Jan-07

Jul-0

7

Jan-08

Jul-0

8

Jan-09

Jul-0

9

Jan-10

Jul-1

0

Jan-11

Jul-1

1

Jan-12

Jul-1

2

Jan-13

Jul-1

3

Jan-14

Jul-1

4

Jan-15

Jul-1

5

Jan-16

Jul-1

6

Jan-17

Jul-1

7

Jan-18

Jul-1

8

Jan-19

Jul-1

9

Jan-20

USD/

MBtu

US Henry Hub Europe - UK NBP Asian LNG price (average contracted import price) Asian LNG (spot)

?

?

Generation cost profile for fossil-fuels varies under fixed prices versus historical volatility

Historical gas prices by region versus price range for LCOE of new CCGT at

USD 60-80/MWh

More robust competitiveness assessments would account for value of electricity generated when and where, and fossil fuel and carbon price volatility

16

Gas prices at which new CCGT today has LCOE at USD 60-80/MWh (Benchmark for recent wind costs)

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

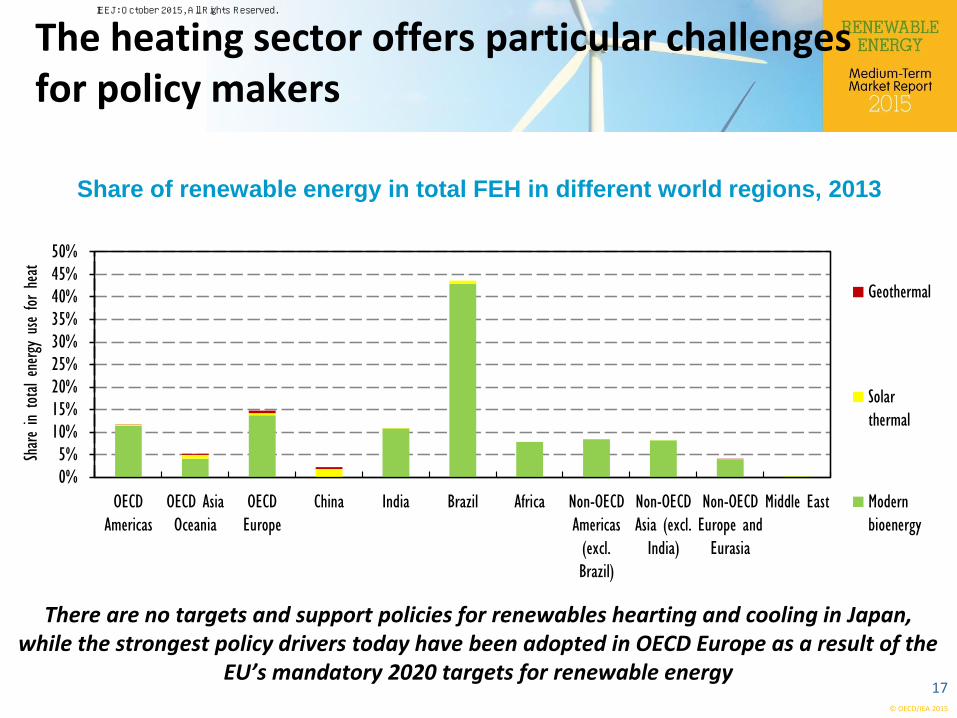

The heating sector offers particular challenges for policy makers

Share of renewable energy in total FEH in different world regions, 2013

There are no targets and support policies for renewables hearting and cooling in Japan, while the strongest policy drivers today have been adopted in OECD Europe as a result of the

EU’s mandatory 2020 targets for renewable energy 17

0%5%

10%15%20%25%30%35%40%45%50%

OECD

Americas

OECD Asia

Oceania

OECD

Europe

China India Brazil Africa Non-OECD

Americas

(excl.

Brazil)

Non-OECD

Asia (excl.

India)

Non-OECD

Europe and

Eurasia

Middle East

Share in total energy use for heat

Geothermal

Solar

thermal

Modern

bioenergy

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

Focus on Japan

18

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

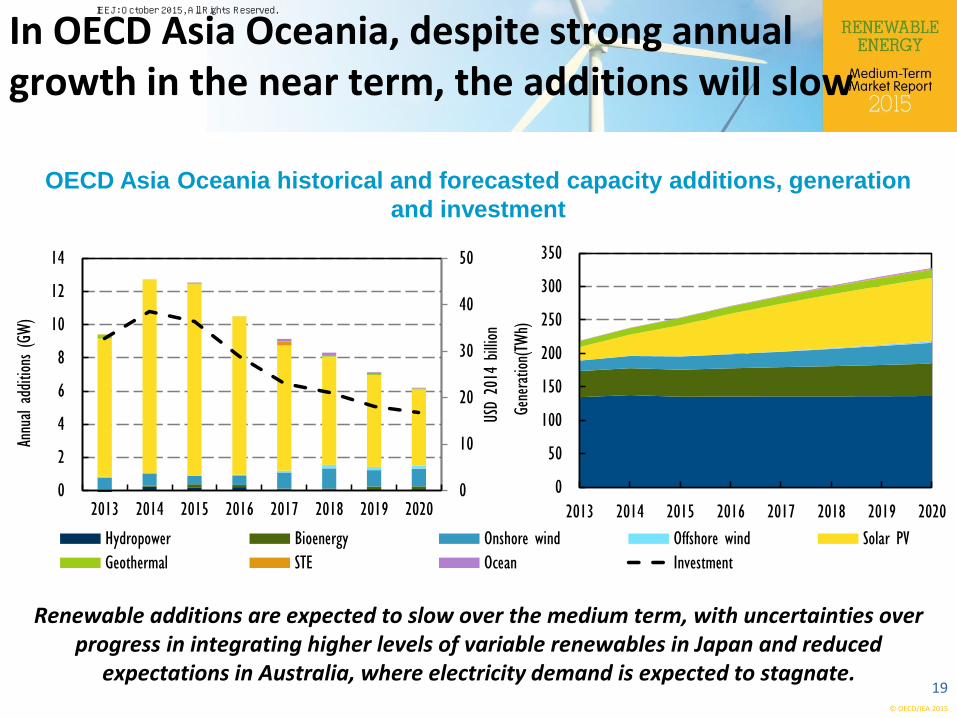

In OECD Asia Oceania, despite strong annual growth in the near term, the additions will slow

Renewable additions are expected to slow over the medium term, with uncertainties over progress in integrating higher levels of variable renewables in Japan and reduced

expectations in Australia, where electricity demand is expected to stagnate.

OECD Asia Oceania historical and forecasted capacity additions, generation

and investment

19

0

50

100

150

200

250

300

350

2013 2014 2015 2016 2017 2018 2019 2020Ge

neratio

n(TW

h)

0

10

20

30

40

50

0

2

4

6

8

10

12

14

2013 2014 2015 2016 2017 2018 2019 2020US

D 20

14 billion

Annu

al a

ddition

s (GW)

Hydropower Bioenergy Onshore wind Offshore wind Solar PV

Geothermal STE Ocean Investment

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

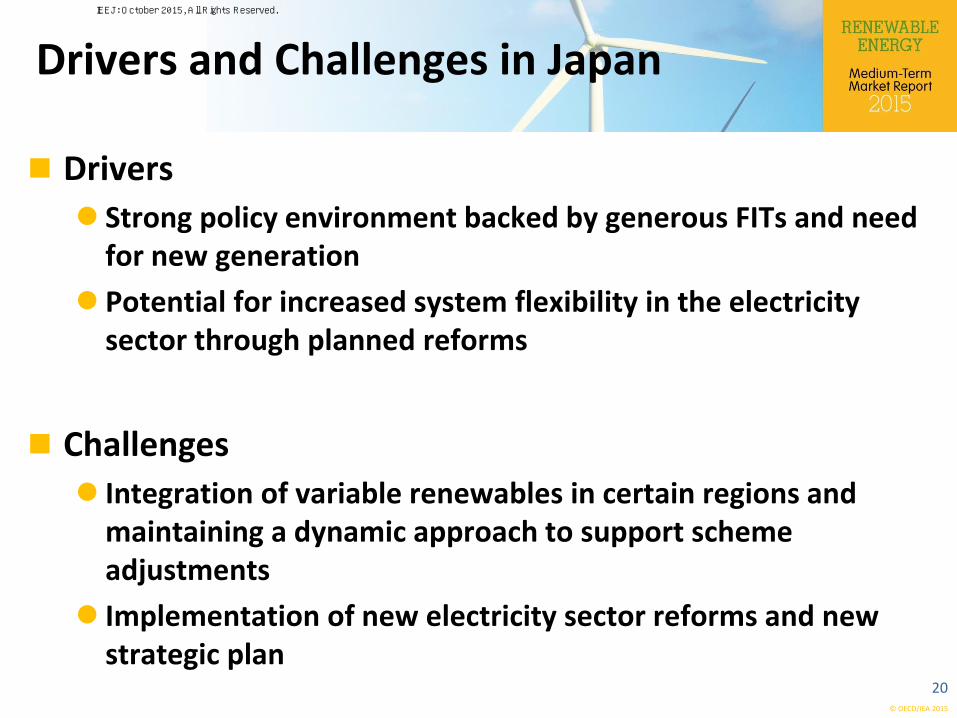

Drivers and Challenges in Japan

Drivers

Strong policy environment backed by generous FITs and need for new generation

Potential for increased system flexibility in the electricity sector through planned reforms

Challenges

Integration of variable renewables in certain regions and maintaining a dynamic approach to support scheme adjustments

Implementation of new electricity sector reforms and new strategic plan

20

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

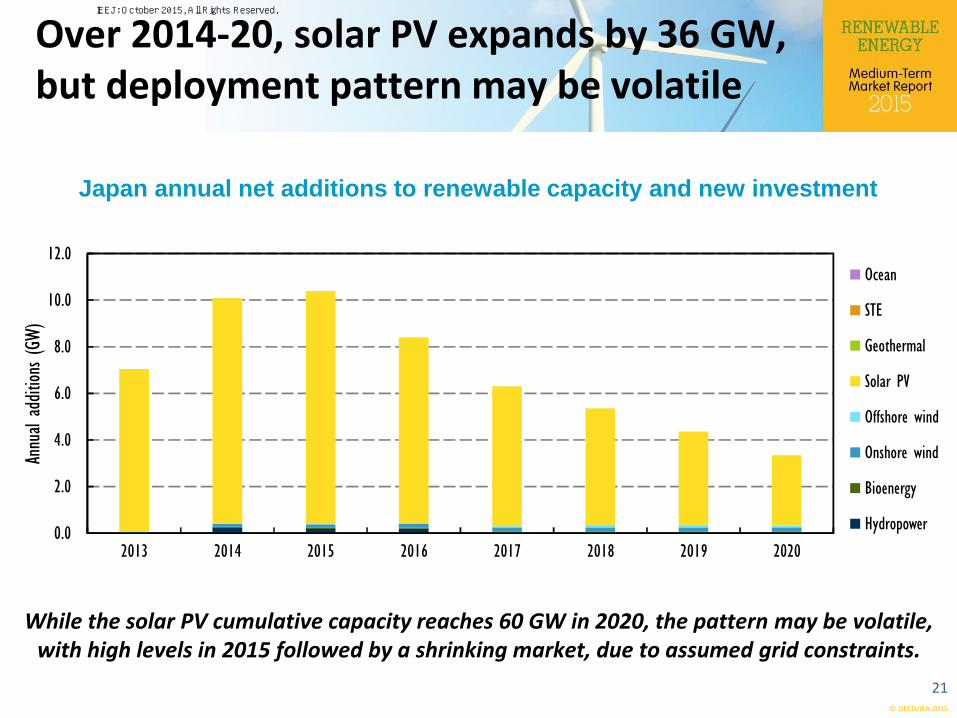

Over 2014-20, solar PV expands by 36 GW, but deployment pattern may be volatile

While the solar PV cumulative capacity reaches 60 GW in 2020, the pattern may be volatile, with high levels in 2015 followed by a shrinking market, due to assumed grid constraints.

Japan annual net additions to renewable capacity and new investment

21

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2013 2014 2015 2016 2017 2018 2019 2020

Annu

al a

ddition

s (GW)

Ocean

STE

Geothermal

Solar PV

Offshore wind

Onshore wind

Bioenergy

Hydropower

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

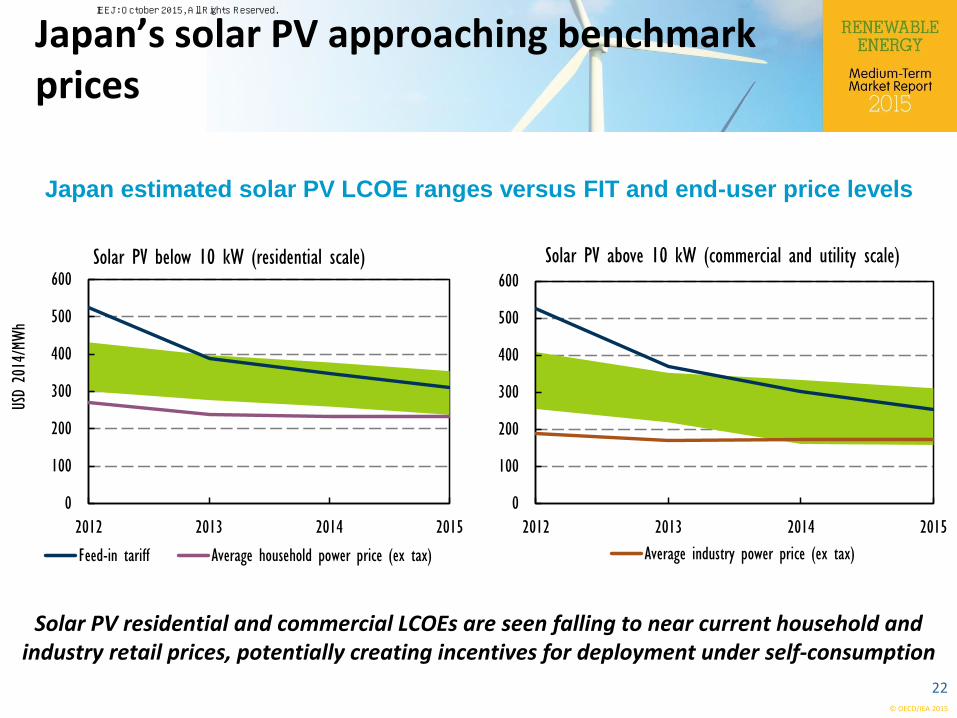

Japan estimated solar PV LCOE ranges versus FIT and end-user price levels

Solar PV residential and commercial LCOEs are seen falling to near current household and industry retail prices, potentially creating incentives for deployment under self-consumption

Japan’s solar PV approaching benchmark prices

0

100

200

300

400

500

600

2012 2013 2014 2015

USD

2014

/MWh

Solar PV below 10 kW (residential scale)

Feed-in tariff Average household power price (ex tax)

0

100

200

300

400

500

600

2012 2013 2014 2015

Solar PV above 10 kW (commercial and utility scale)

Average industry power price (ex tax)

22

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

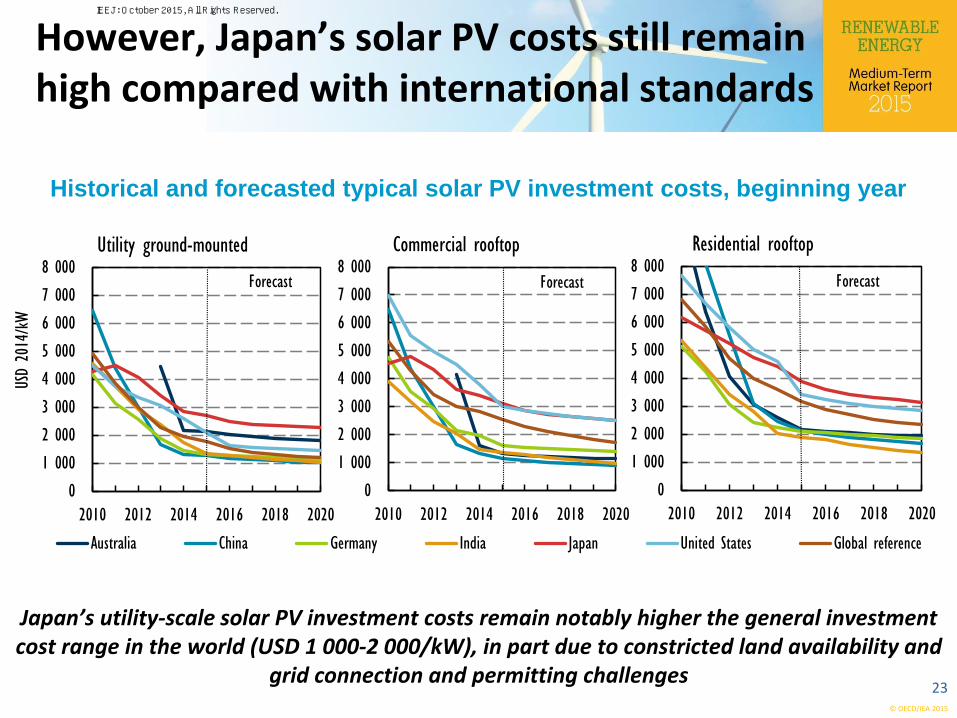

However, Japan’s solar PV costs still remain high compared with international standards

Japan’s utility-scale solar PV investment costs remain notably higher the general investment cost range in the world (USD 1 000-2 000/kW), in part due to constricted land availability and

grid connection and permitting challenges

Historical and forecasted typical solar PV investment costs, beginning year

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2010 2012 2014 2016 2018 2020

USD

2014

/kW

Utility ground-mounted

Australia China Germany India Japan United States Global reference

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2010 2012 2014 2016 2018 2020

Commercial rooftop

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2010 2012 2014 2016 2018 2020

Residential rooftop

Forecast Forecast Forecast

23

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

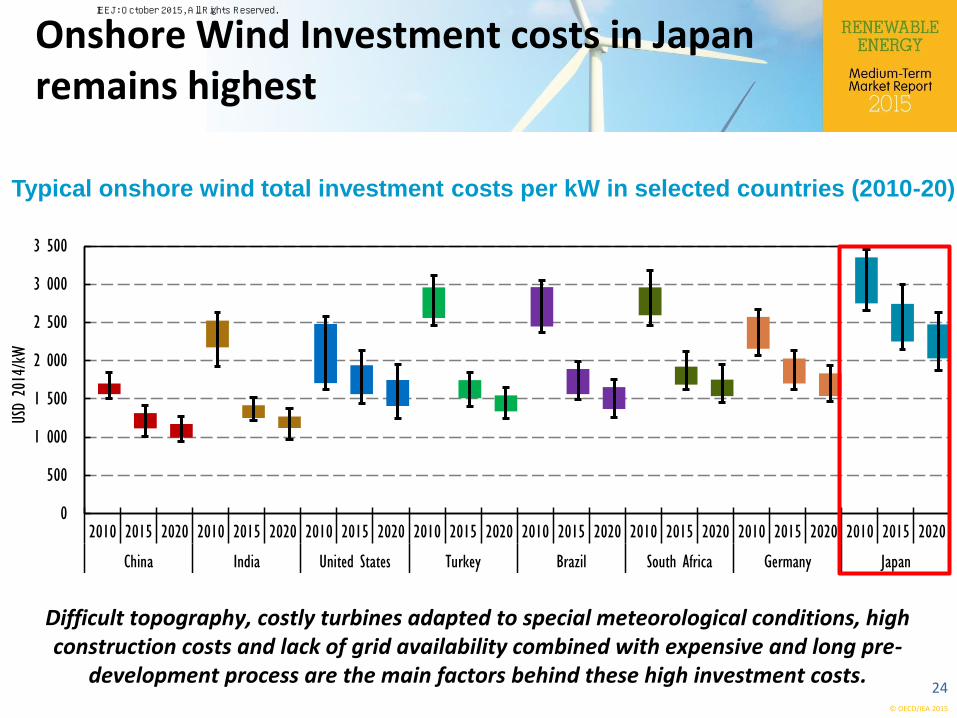

Onshore Wind Investment costs in Japan remains highest

Typical onshore wind total investment costs per kW in selected countries (2010-20)

Difficult topography, costly turbines adapted to special meteorological conditions, high construction costs and lack of grid availability combined with expensive and long pre-

development process are the main factors behind these high investment costs.

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2010 2015 2020 2010 2015 2020 2010 2015 2020 2010 2015 2020 2010 2015 2020 2010 2015 2020 2010 2015 2020 2010 2015 2020

China India United States Turkey Brazil South Africa Germany Japan

USD

2014

/kW

24

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

Priorities for Renewables in Japan

Objective should remain to foster a well-balanced portfolio of renewable energy technologies

Proceed in the power system reforms

Strengthen interconnections and enlarge balancing areas

Allow for fair and equal grid access conditions

Policies on Solar PV should be adapted to reduce unit costs as much as possible and rapidly align with international benchmarks prices

For development of renewable heating and cooling policy, need to obtain reliable data on production, utilisation and costs 25

IEEJ: October 2015, All Rights Reserved.

© OECD/IEA 2015

For further insights and analysis…

The Medium-Term Renewable Energy Market Report 2015 was launched on 2nd October and can be purchased online at:

http://www.iea.org/

Thank you for your attention!

26

IEEJ: October 2015, All Rights Reserved.

Contact:[email protected]