introduction to the farm credit system

TRANSCRIPT

INTRODUCTION TO THEFARM CREDIT SYSTEM

CHARLES DANA, GENERAL COUNSEL, THE FARM CREDIT COUNCIL, WASHINGTON, DC

RICHARD MANNER, SENIOR CORPORATE ATTORNEY, COBANK,ACB, DENVER, CO

The Farm Credit System is a Creation of Congress

STATUTORY AND REGULATORY FOUNDATION

• ESTABLISHED BY CONGRESS IN 1916 AS FIRSTGOVERNMENT SPONSORED ENTERPRISE (GSE)

– Following the model of the Federal Reserve System

• SIGNIFICANTLY UPDATED IN 1933

– One of the “New Deal” Reforms adopted as part of FDR’s “100Days of Action”

• All Government capitalization repaid by the mid-1960s

FARM CREDIT ACT OF 1971

• IN 1969 THE COMMISSION ON AGRICULTURALCREDIT WAS ESTABLISHED BY THE FARM CREDITADMINISTRATION

• System had about $14 Billion in loan volume and about$1Billion in capital stock and another $1 Billion in “networth reserves”.

• System had a market share of about 23% of mortgagecredit and 17% of operating credit used by farmers andabout 60% of credit used by farmer cooperatives.

Mission of the System Today

“...the farmer-owned cooperative Farm Credit System be designed toaccomplish the objective of improving the income and well-being ofAmerican farmers and ranchers by furnishing sound, adequate, andconstructive credit and closely related services to them, theircooperatives, and to selected farm-related businesses necessary forefficient farm operations.”

“...farmer- and rancher-borrowers participation in the management,control, and ownership of a permanent system of credit foragriculture which will be responsive to the credit needs of all types ofagricultural producers having a basis for credit…”

The Farm Credit Act of 1971, as amended

The Farm Credit Act sets out in general terms

-- the System’s structure

-- ownership

-- governance

-- lending authority

-- tax treatment

-- regulatory oversight

-- borrower rights

-- access to debt markets

-- insurance fund

The Farm Credit System

Discussion Points:• No “parent” or

“headquarters”• Ownership

National Farm Credit Council

(Trade Association)

FCCServices, Inc.

Ownership Flow of Funds Regulatory Oversight

Farm CreditAdministration

(RegulatoryOversight)

Farm CreditSystem

InsuranceCorporation

4 Farm Credit Banks (FCBs)

1 Agricultural Credit Bank (ACB)

90 Associations

System-ownedService

Companies

Farmer Mac

Flow of FundsRegulationLinked by legislation, regulation,funding and public perception

PresidentsPlanning

Committee(PPC)

Approximately 500,000 borrowers

Farmers / Ranchers / Cooperatives / Agribusiness / Rural Homes

Federal Farm CreditBanks Funding

Corporation

It is the Farm Credit Administration that interprets the Act

As an independent entity, the Farm Credit System Insurance Corporation shall:

Protect investors in insured Farm Credit System obligationsand taxpayers through sound administration of the Insurance Fund;

Exercise its authorities to minimize loss to the Insurance Fund;

Help ensure the future of a permanent system for deliveryof credit to agricultural borrowers.

Farm Credit System Insurance Corporation

AGENCY STATUS

• INTEREST ON SYSTEM BONDS EXEMPT FROM STATE AND LOCALTAX

• FAVORABLE CAPITAL TREATMENT AS INVESTMENTS BYDEPOSITORY INSTITUTIONS

• ELIGIBLE AS COLLATERAL FOR PUBLIC DEPOSITS, INCLUDINGTREASURY TAX AND LOAN ACCOUNTS

• ELIGIBLE FOR PURCHASE BY FEDERAL RESERVE IN CONNECTIONWITH ITS OPEN MARKET OPERATIONS

• ELIGIBLE COLLATERAL FOR COMMERCIAL BANK BORROWING FROMTHE FEDERAL RESERVE DISCOUNT WINDOW

• ABILITY TO USE BOOK ENTRY FACILITIES OF THE FED

• EXEMPT FROM REGISTRATION AND PROSPECTUS REQUIREMENTSOF THE SECURITIES ACT AND THE EXCHANGE ACT

Key Differences Between FarmCredit System and other

Commercial LendersStatus as a Government Sponsored Enterprise (GSE)– Congressional charter

– Public purpose

Cooperative Organization– Borrower owned

– Borrower controlled boards

– Patronage

Specialized lending and services– Agriculture and rural America focus

No authority to accept deposits– No checking or savings accounts

THE OTHER GSEs

• FANNIE MAE

• FREDDIE MAC

• FEDERAL HOME LOAN BANKS

• FARMER MAC

• SALLIE MAE

• ALL OF THE ABOVE HAVE PUBLICLY-TRADED EQUITES

The Farm Credit Council

The Troubled Years of 1985 - 1987

Stronger and Restructured FCA

Restructured System

Borrower Rights

Farm Credit System Insurance Corporation (FCSIC)

Farmer Mac

The Farm Credit Council

16

51.044.4

36.0 33.839.4

69.3

60.366.3

85.3

57.963.9

7.512.4

21.522.9

20.7

12.4

16.5

13.0

15.8

11.9

12.2

12.9

12.4

53.7

38.3

53.0

24.4

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009** 2010**

Net cash income, excluding direct government payments Direct government payments

**Forecasted as of February 2010 Average of 2000 – 2009 is $72.9 billion

Source: USDA

$58.5 $56.8

$50.7

$57.5 $56.7

$82.3

$60.1

$70.2

$84.7

$68.8

$78.2

$97.5

($ Billions)

FARMERS' NET CASH INCOME

$70.8$76.3

17

163.5160.5

142.1

122.7105.5

28.4

33.1

36.5

43.8 42.2

6.0

7.1

7.9

10.1 9.8

12/31/05 12/31/06 12/31/07 12/31/08 12/31/09

NET LOANS CASH AND INVESTMENTS OTHER ASSETS

Total Assets

$139.9

($ Billions)

$162.9

$186.5

$214.4 $215.5

18

47.7

22.8

12.1

7.24.02.6

51.7

24.9

14.7

8.14.6

2.3

56.5

28.7

21.1

9.65.3

2.2

63.5

32.3

28.1

10.86.1

2.1

71.9

37.5

26.9

13.9

7.1

4.1

75.4

39.6

23.6

14.6

7.6

4.0

12/31/04 12/31/05 12/31/06 12/31/07 12/31/08 12/31/09

Real estate mortgage loans Production & intermediate-term loans

Agribusiness loans Communication, energy & water/waste disposal loans

Rural residential real estate and other loans International Loans

($ billions)

$96.4$106.3

$142.9

$123.4

Gross Loans

$161.4 $164.8

19

$2,096$2,379

$2,703$2,916 $2,850

2005 2006 2007 2008 2009

Net Income

($ millions)

20

$3,246

$3,584

$4,060

$4,702

$5,392

2005 2006 2007 2008 2009

Net Interest Income

($ millions)

21

39.2%37.6%

35.3%

33.0%31.3%

2005 2006 2007 2008 2009

Operating Expenses as a Percentage of NetInterest Income and Noninterest Income

22

0.44% 0.47%0.59%

1.41%

1.70%

1.89%

2.55%

2.04%

3/31/08 6/30/08 9/30/08 12/31/08 3/31/09 6/30/09 9/30/09 12/31/09

NONACCRUAL LOANS AS A PERCENTAGE OFTOTAL LOANS OUTSTANDING

23

0.2

3.33.22.92.32.3

24.923.2

21.420.018.5

2.1

2.3

2.6

2.9

3.30.9

0.8

0.7

0.8

1.4

(0.2) (0.2) (0.5)(2.1) (1.6)

Total Risk Funds as a Percentage of Loans

$23.5

22.1%

Allowance for Loan Losses

Surplus Restricted Capital – Insurance Fund

Capital Stock and Participation Certificates (including preferred stock)

$25.1

20.4%

$27.2

19.0%

$28.1

17.4%

Accumulated Other Comprehensive Loss

12/31/05 12/31/06 12/31/07 12/31/08 12/31/09

Additional Paid-In-Capital

$31.3

19.0%

Total Risk Funds

24

CAPITAL AS A PERCENTAGE OF TOTAL ASSETS(ADJUSTED FOR OCI)

16.45%

15.10%14.46%

13.65% 13.87% 14.04%14.41% 14.63%

12/31/05 12/31/06 12/31/07 12/31/08 3/31/09 6/30/09 9/30/09 12/31/09

13%

25

STATEMENT OF OPERATIONS DATA($ MILLIONS)

RESULTS OF OPERATIONS

YEAR ENDED DECEMBER 31, QUARTER ENDED

2007 2008 2009 12/31/08 12/31/09

Net Interest Income $4,060 $4,702 $5,392 $1,197 $1,450

Noninterest Income 462 502 447 130 148

Noninterest Expenses (1,597) (1,727) (1,869) (485) (519)

Provision For Loan Losses (81) (408) (925) (284) (192)

Income Before Income Taxes 2,844 3,069 3,045 558 887

Provision for Income Taxes (141) (153) (195) (12) (55)

Net Income $2,703 $2,916 $2,850 $ 546 $ 832

26

$2,272$2,022

$3,249

$2,875$2,559

$40

$40

$40

$40

$40

12/31/05 12/31/06 12/31/07 12/31/08 12/31/09

The Insurance Fund and Allocated Insurance Reserve Accounts as aPercentage of the Insured Obligations

ALLOCATED INSURANCE RESERVE ACCOUNTS

DESIGNATED TO REPAY FLB OF JACKSON LIABILITY

ASSETS FOR WHICH NO SPECIFIC USE HAS BEENIDENTIFIED

$2,062

1.86%

$2,312

1.75%

ASSETS IN THE INSURANCE FUND($ Millions)

$2,599

1.71%

$2,915

1.80%

$3,289

2.14%

Trend of the Allocated and Unallocated Insurance Fund toAdjusted Insured Debt Outstanding

December 31, 2009

A Brief History of the System

• Historically, the System was organizedinto 12 geographical Districts

• Each District had at its center 3 Banks(often jointly managed).

• In addition, scattered throughout theDistrict was a network of locally-ownedFarm Credit Associations.

Traditional District Structure

Banks within each District:

• Federal Land Bank – Made long-term real estate loans to farmers within the Districtthrough a network of locally-owned Federal Land Bank Associations (FLBAs).

• Federal Intermediate Credit Bank – Financed locally-owned Production CreditAssociations (PCAs) within the District, which in turn made short- and intermediate-term operating loans for production needs (feed, fertilizer, equipment, etc.).

• Bank for Cooperatives – The lender to agricultural cooperatives and rural utilitieswithin the District. The Bank for Cooperatives was a direct retail lender and did notwork through local Associations.

Note: There was also a 13th Bank for Cooperatives located in Denver called theCentral Bank for Cooperatives. Its primary function was to participate in large loansmade by the 12 District Banks for Cooperatives.

Present Structure

• Five Farm Credit Districts, each consisting of a FarmCredit Bank for the District and any number of locally-owned Associations. This component of the Systemcontinues to carry out the lending to farmers, ranchers,and producers and harvesters of aquatic products.

• A single, nationwide Bank for Cooperatives that carriesout the direct retail lending to coops and rural utilities.

Present Structure

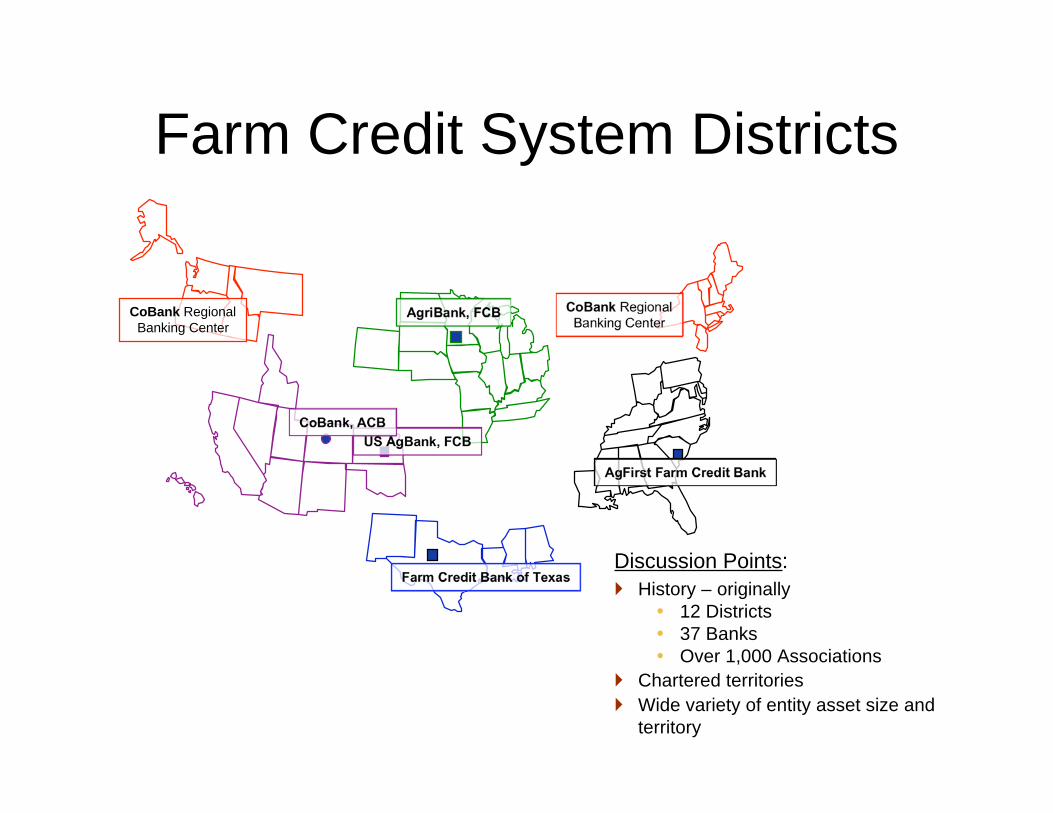

The five District Farm Credit Banks are:

• AgFirst Farm Credit Bank, Columbia, SC

• AgriBank, FCB, St. Paul, MN

• U.S. AgBank, FCB, Wichita, KS

• Farm Credit Bank of Texas, Austin, TX

• CoBank, ACB, Denver, CO

The nationwide Bank for Cooperatives is: CoBank, ACB,Denver, CO

Present Structure

• CoBank is really a hybrid . It is unique inthe System in that it is both a District FarmCredit Bank and the nationwide Bank forCooperatives, all rolled into one. It is theresult of the merger of all 13 Banks forCooperatives and one District Farm CreditBank.

Discussion Points:

History – originally12 Districts37 BanksOver 1,000 Associations

Chartered territories

Wide variety of entity asset size andterritory

AgFirst Farm Credit Bank

AgriBank, FCB CoBank RegionalBanking Center

US AgBank, FCB

CoBank, ACB

Farm Credit Bank of Texas

CoBank RegionalBanking Center

Farm Credit System Districts

Ownership

Farm Credit Banks are cooperatively owned by theAssociations within their respective Districts.

Associations are cooperatively owned by their farmerborrowers.

CoBank, as a hybrid, is owned both by the Associationsin its District and by its direct coop and rural utilityborrowers.

The Farm Credit Council

Formed in November 1982501 (c)(6) tax exempt organization

Farm Credit Council Mission

The Farm Credit Council enhances thecompetitive environment for the Farm

Credit System by promoting andprotecting the legislative and regulatory

interests of System institutions, andhelps them achieve additional benefits

associated with being a System.

• CREATED BY CONGRESS IN 1987

• SERVES AS SECONDARY MARKET FORAGRICULTURAL LOANS

• HAS PROGRAMS FOR FCS, ABA, ICBA ANDOTHERS

• SEE WWW.FARMERMAC.COM

Eligibility and Authorities

Today, the Farm Credit Banks are primarily financialintermediaries, providing funding to their affiliatedAssociations.

The actual farm lending is done primarily by:

• Federal Land Credit Associations (FLCAs) - Long-termreal estate loans

• Production Credit Associations (PCAs) - Short- andintermediate-term loans

Eligibility and Authorities

Most Associations have gone to a holdingcompany structure, where the FLCA andthe PCA are owned by an AgriculturalCredit Association (ACA) -- Borrowersbecome cooperative members of the ACA,but the loans are made by the FLCA andPCA.

(As always, there are exceptions)

Eligibility and Authorities

Eligibility to Borrow from an Association: The Big Three

1. Agricultural producers (farmers, ranchers, and producers and harvesters ofaquatic products)

2. Agricultural marketing and processing operations (lots of technical rules)

3. Providers of farm-related services -- services directly related to on-farmoperating needs

Generally, Association loans are for agricultural purposes, but in the case ofa full-time farmers, the Association can finance any credit needs.

Eligibility and Authorities

Additional Authority - Rural Housing

Associations may finance moderately-priced, single-family homes in rural areas,not to include towns or cities of more than2500 inhabitants. Limited to15% ofoutstanding loans.

Eligibility and Authorities

Eligibility to Borrow from CoBank as a Bank for Cooperatives

1. Farmer-Owned Cooperatives – eligibility parameters rooted in theCapper-Volstead Act. "Grandfather" rule helps keep evolving coopseligible as long as they remain majority controlled by farmers.

2. Cooperative Joint Ventures - Entities at least partially owned byeligible cooperatives.

3. Rural Electric and Telecommunications - Cooperatives and otherentities eligible for financing from the Rural Utilities Service of the

USDA, and subsidiaries of those entities.

Eligibility and Authorities

(CoBank, continued)

4. Cooperatives and certain public and quasi-publicentities for the installation, maintenance, etc., of ruralwater and sewer facilities.

5. Certain domestic and foreign entities in connectionwith import and export of agricultural commodities.

Other Authorities - Participations

A. Intra-System Participations - Any System lender mayparticipate in any loan originated by any other Systemlender.

B. Non-System Originators – A System lender mayparticipate in a loan originated by a non-System lender ifthe borrower is directly eligible for the System lender.

Other Authorities - Participations

C. “Similar Entity” Participations – A System lender mayparticipate, up to 49%, in a loan originated by a non-System lender to a borrower that, while not otherwiseeligible, is “functionally-similar” to a directly eligibleborrower (majority of income from, or a majority ofassets invested in, operations functionally similar tooperations of eligible borrowers). This includestraditional participations as well as syndicated loans.

Other Authorities - Leasing

Systems lender may lease equipment and facilities to

eligible customers.

Some Associations have active leasing programs.

In addition, Farm Credit Leasing Services Corporation(FCL), which is now a wholly-owned subsidiary ofCoBank, has authority to lease to anyone eligible toborrow under the Farm Credit Act.

The Farm Credit Council

Mandate for Programs to Serve Young, Beginning and

Small Farmers

Young farmers -- Individuals 35 years old or

younger

Beginning farmers -- Ten years or fewer of

farming experience

Small farmers -- Ones that typically generate

less than $250,000 in annual sales

Range of YBS Programs

Credit EnhancementsCredit Enhancements

•• Adjusted underwriting standardsAdjusted underwriting standards

•• Interest rate concessionsInterest rate concessions

•• Fee waivers/paymentsFee waivers/payments

Educational AssistanceEducational Assistance

•• Financial skillsFinancial skills

•• Leadership trainingLeadership training

•• Business plan developmentBusiness plan development

Capital PoolsCapital Pools

YBS Mission and Scope• Congress: sound and constructive credit

• Regulator: wide latitude, but set goals

• 88 Associations: all independently run

New loans made in 2009 to:

Young: $6.6 billion

Beginning: $9.4 billion

Small: $11.9 billion

The “Who” of Congress is Important

Congressional CompositionHouse

Dem: 258

Rep: 177

Senate

Dem: 57

Rep: 41

Ind: 2 (Dem. Caucus)

– Of the 435 Congressional Districts - 61 meet thedefinition of being rural -Most of its population liveoutside metro area and also outside any metro areawith 25,000 or more people.

– Trends working against rural influence in Congress -Rural population peaked in 1920 - Share ofpopulation living outside metro areas fell from 66% in1920 to 20% in 2000.

– There are only 4 Congressional districts that havenothing to do with a metro area - one each in KS, KY,NE and MO.

– There are 220 districts in which majority of people aresuburban

Source: Congressional Quarterly

• Almost half of House members nowrepresent districts in which minoritiesconstitute 30% or more of the population.

• From 2000 to 2008, the minority share ofthe population increased in 410 of the 435congressional districts.

• Only New England, the Upper Midwestand Appalachia have largely been exemptfrom the trend.

Source: National Journal 12/19/08

Farm Credit Issues

LOOKING TO THE FUTURE

• WHAT’S NEXT FOR FARM CREDIT

• ISSUES FOR AGRICULTURE

1. Financial Institutions Reform• The Wall Street Reform and Consumer

Protection Act (H.R. 4173)

2. GSE Reform• Fannie Mae

• Freddie Mac

3. Farm Bill• USDA Budget Pressure

• Rural Development / Farm Credit LendingAuthorities

4. Uncertainty

GSE ReformFannie MaeFreddie Mac

Risks to Farm CreditThreat to Agency Status TraitsAdverse Impact on Market AccessCommittee JurisdictionRegulatory Oversight

Federal Government’s Assistance to AIG

$183 Billion

Total FCS Loan Volume as of12/31/2010

$165 Billion

Farm Bill• USDA Budget Pressure• Rural Development / Farm

Credit Lending Authorities

Risks / Opportunities for Farm CreditLending AuthoritiesReform Efforts -- FCA & FCSIC AgendaFSA Lending ProgramsRural Development ProgramsGSM ProgramCrop Insurance

Ag Credit Environment

• Banks and Farm Credit 40% share each

• Interest rates are rising

• Lenders must have risk capacity (liquidity)

• Lenders must manage interest rate risk

• Financial crisis moving out from cities

The Landscape and the Lending

• The Demand for Locally Grown

• Factors Limiting the Supply

• Lending on the Urban Edge

• Paradigm Shifts: Urban Edge Lending

OTHER ISSUES

• ANTI-TRUST

– CAPPER VOLSTEAD

– DOJ/DEPT OF AG FIELD HEARINGS

ANIMAL RIGHTS

HSUS INIATIVES AT STATE LEVEL

ADDITIONAL INFO

• WWW.FARMCREDIT.COM

• WWW.FCCOUNCIL.COM

• WWW.FARMCREDITARCHIVE.ORG

• WWW.FCA.GOV

• WWW.FCSIC.GOV

• WWW.FARMCREDIT-FFCB.COM

• WWW.COBANK.COM

Thank You