indian coking coal requirement sourcing options coking coal requirement... · mozambique...

TRANSCRIPT

Indian Coking Coal Requirement &

Sourcing Options

Arun Kumar Jagatramka Chairman & Managing Director

Gujarat NRE Coke Limited

India Unbound

Recently growth has slowed, but...

Growth story is far from being over….

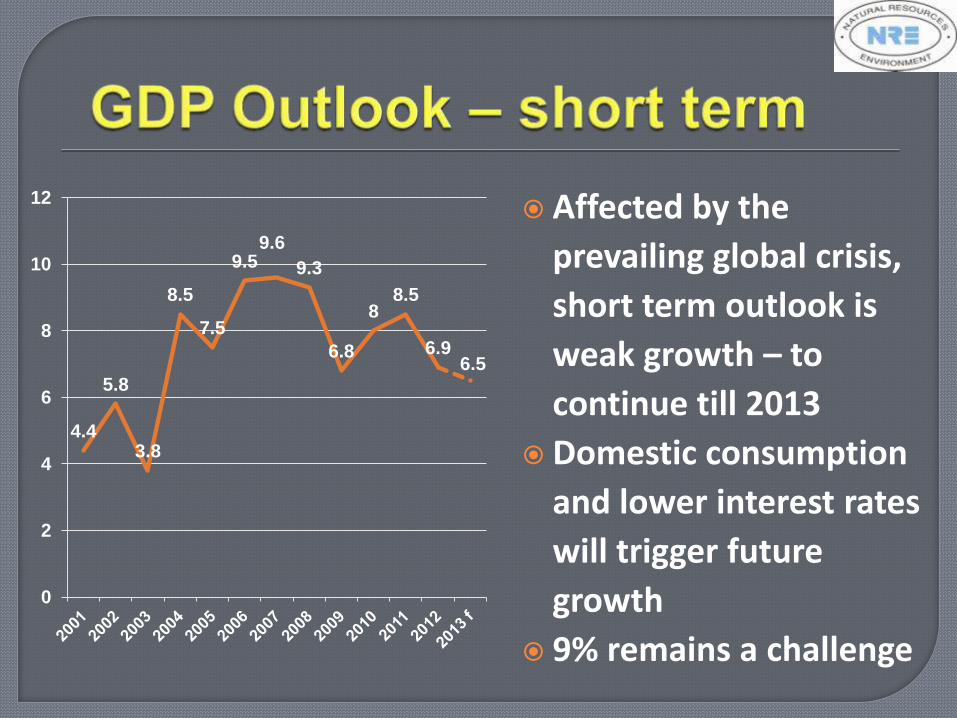

Affected by the

prevailing global crisis,

short term outlook is

weak growth – to

continue till 2013

Domestic consumption

and lower interest rates

will trigger future

growth

9% remains a challenge

4.4

5.8

3.8

8.5

7.5

9.5 9.6

9.3

6.8

8 8.5

6.9 6.5

0

2

4

6

8

10

12

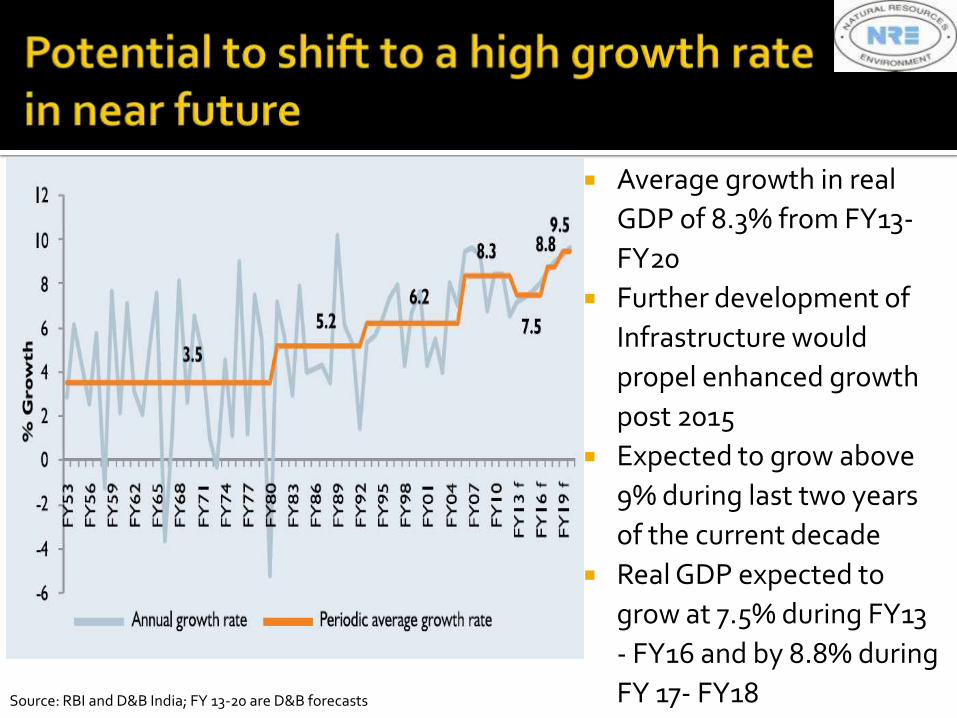

Average growth in real

GDP of 8.3% from FY13-

FY20

Further development of

Infrastructure would

propel enhanced growth

post 2015

Expected to grow above

9% during last two years

of the current decade

Real GDP expected to

grow at 7.5% during FY13

- FY16 and by 8.8% during

FY 17- FY18 Source: RBI and D&B India; FY 13-20 are D&B forecasts

• High savings rates

• Availability of low cost, skilled and semi skilled labour & good knowledge of English

• Growing affluent Middle Class

• Technology – supporting the Service sector

• Favourable demographics

• Benefits from future infrastructure development

• Trade opening and Free markets – opportunities from increased FDI in future

• Manufacturing • Growth in parts manufacturing

• Emerging centre for small car development and manufacturing

• Plans for intelligent engineering products

• Potential for “smart” light engineering

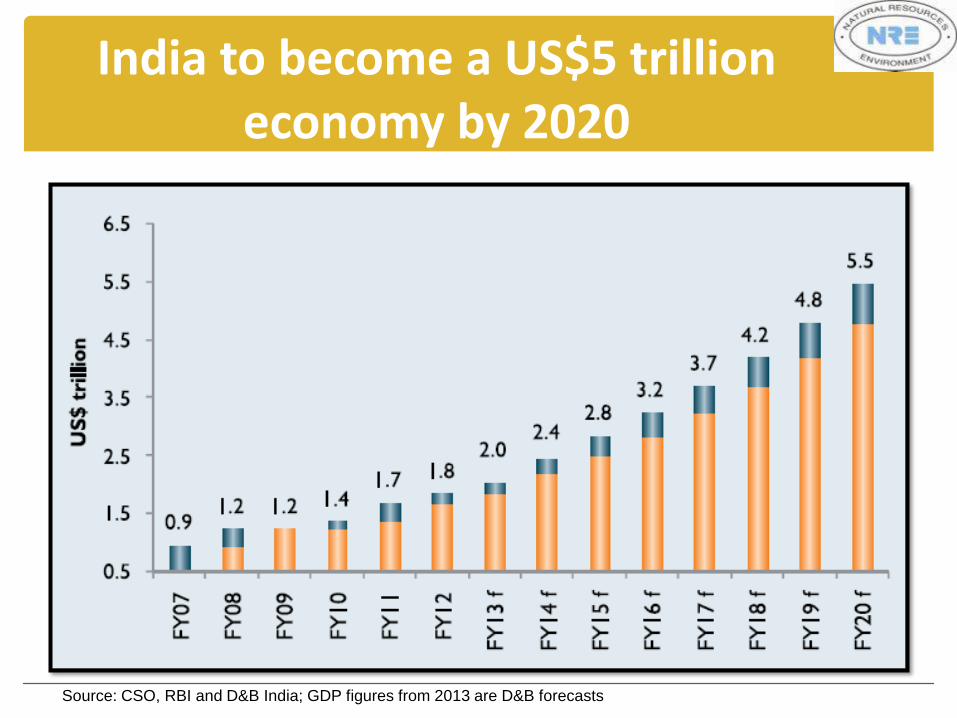

India to become a US$5 trillion economy by 2020

Source: CSO, RBI and D&B India; GDP figures from 2013 are D&B forecasts

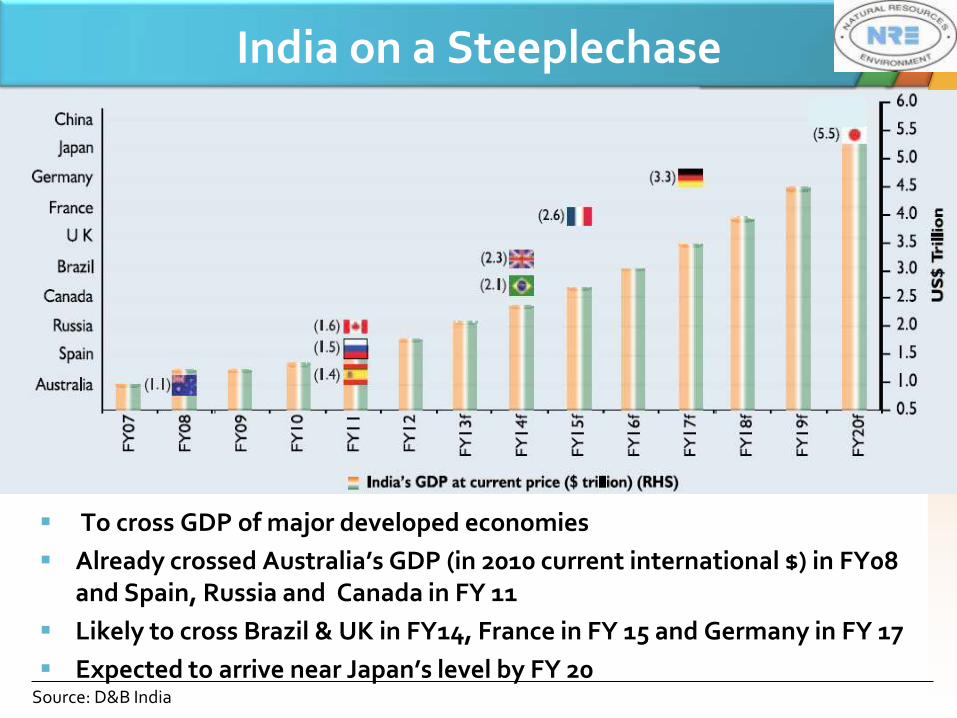

India on a Steeplechase

To cross GDP of major developed economies

Already crossed Australia’s GDP (in 2010 current international $) in FY08 and Spain, Russia and Canada in FY 11

Likely to cross Brazil & UK in FY14, France in FY 15 and Germany in FY 17

Expected to arrive near Japan’s level by FY 20 Source: D&B India

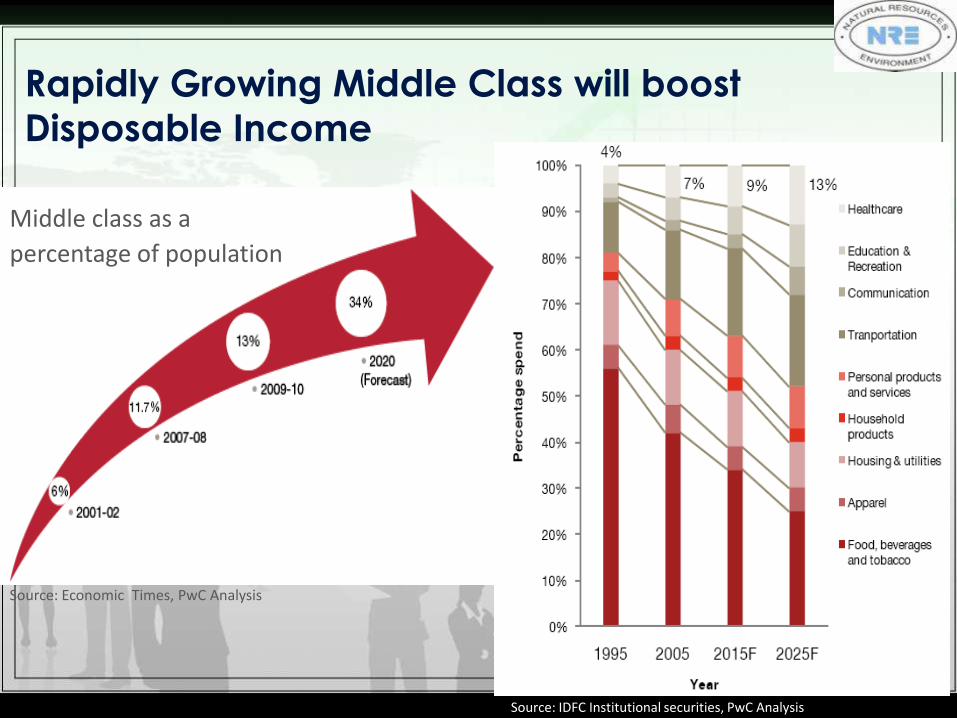

Rapidly Growing Middle Class will boost

Disposable Income

Ascent of Indian Middle

Class – Percentage of

population

Middle class as a

percentage of population

Source: Economic Times, PwC Analysis

Source: IDFC Institutional securities, PwC Analysis

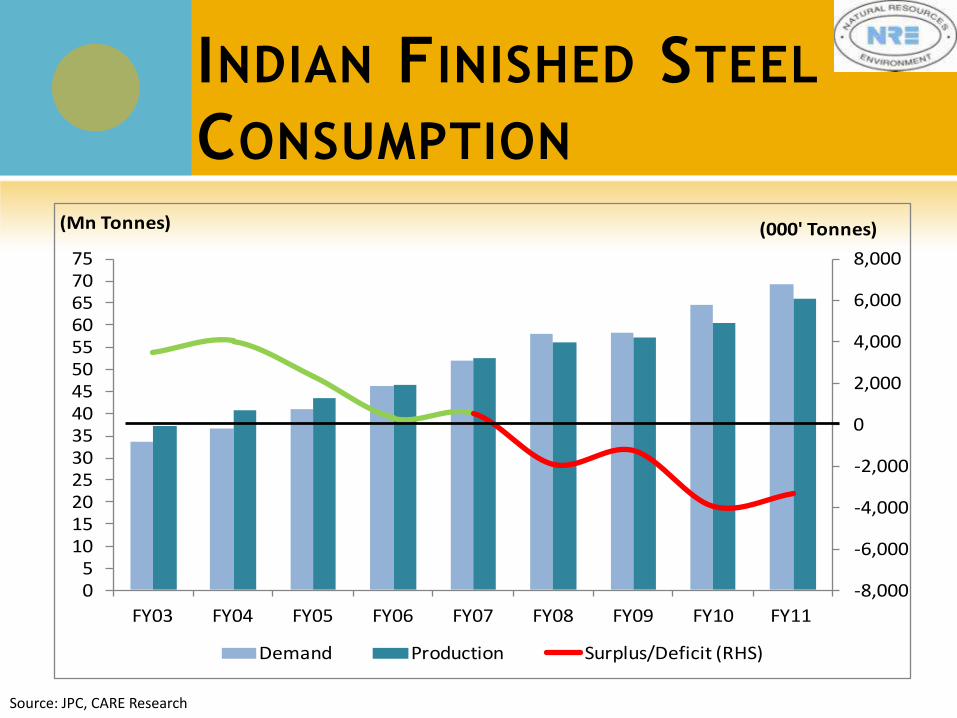

INDIAN FINISHED STEEL

CONSUMPTION

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

05

1015202530354045505560657075

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

(000' Tonnes)(Mn Tonnes)

Demand Production Surplus/Deficit (RHS)

Source: JPC, CARE Research

IMMENSE GROWTH POTENTIAL IN

INDIAN STEEL SECTOR Domestic crude steel production grew at a

compound annual growth rate of 8.4% in the last few years and is projected to be around 110 million tonne by 2012-13.

222 MoUs signed for planned capacity of around 276 MT by 2020 (challenge remains of how many translates into actual commissioning).

Investments at stake are to the tune of $187 billion

Increase in the demand of steel in India is expected to be 14% against the global average of 5-6%

THE STEEL GROWTH DRIVERS

Target for $ 1 trillion of investments in infrastructure during the 12th Five Year Plan (2012-17).

Infrastructure projects (like Golden Quadrilateral and Dedicated Freight Corridor) will give boost to the demand in the steel sector in near future.

Projected New Greenfield & up-grading of existing Airports will keep the momentum up.

Government has identified ports, airports, railways, power, coal and road sectors for special monitoring of investment totalling around USD 40 billion in 2012-13.

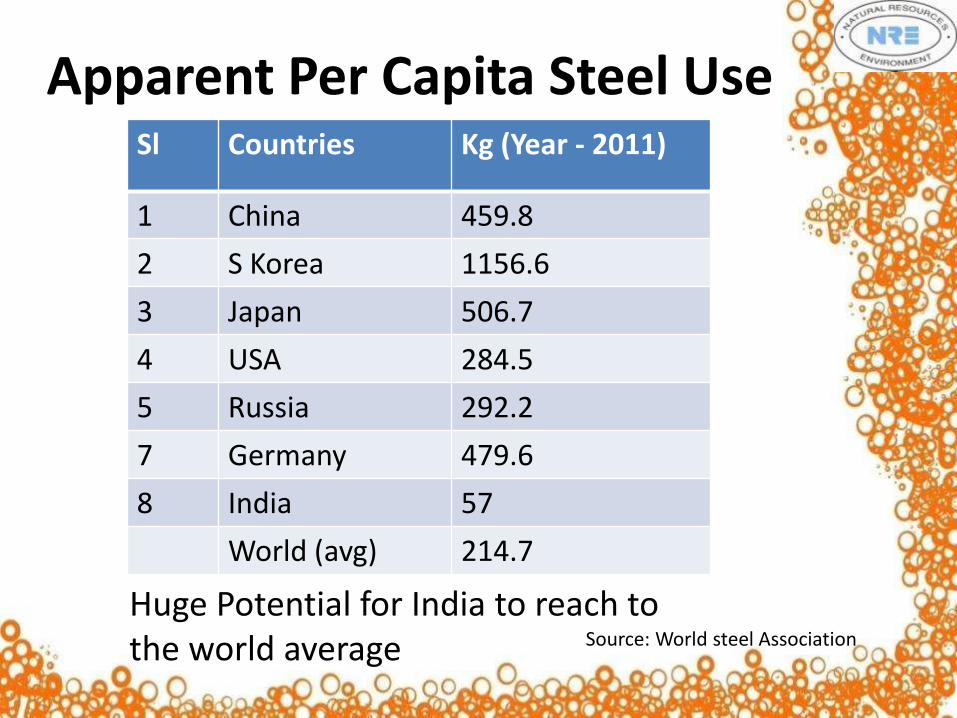

Apparent Per Capita Steel Use Sl Countries Kg (Year - 2011)

1 China 459.8

2 S Korea 1156.6

3 Japan 506.7

4 USA 284.5

5 Russia 292.2

7 Germany 479.6

8 India 57

World (avg) 214.7

Huge Potential for India to reach to the world average Source: World steel Association

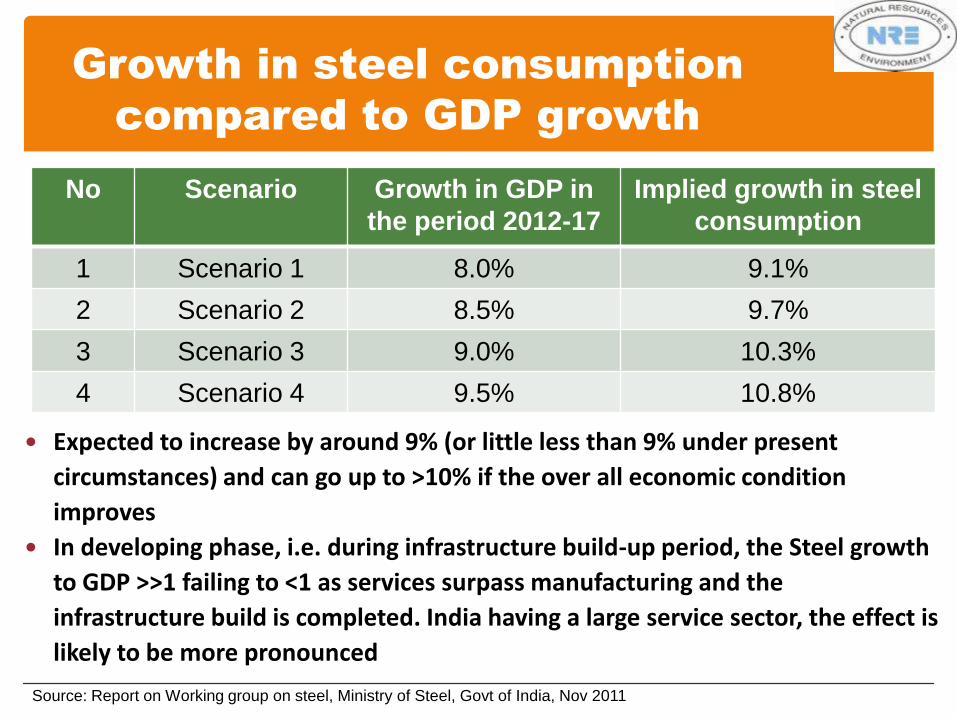

Growth in steel consumption

compared to GDP growth

No Scenario Growth in GDP in

the period 2012-17

Implied growth in steel

consumption

1 Scenario 1 8.0% 9.1%

2 Scenario 2 8.5% 9.7%

3 Scenario 3 9.0% 10.3%

4 Scenario 4 9.5% 10.8%

Expected to increase by around 9% (or little less than 9% under present

circumstances) and can go up to >10% if the over all economic condition

improves

In developing phase, i.e. during infrastructure build-up period, the Steel growth

to GDP >>1 failing to <1 as services surpass manufacturing and the

infrastructure build is completed. India having a large service sector, the effect is

likely to be more pronounced

Source: Report on Working group on steel, Ministry of Steel, Govt of India, Nov 2011

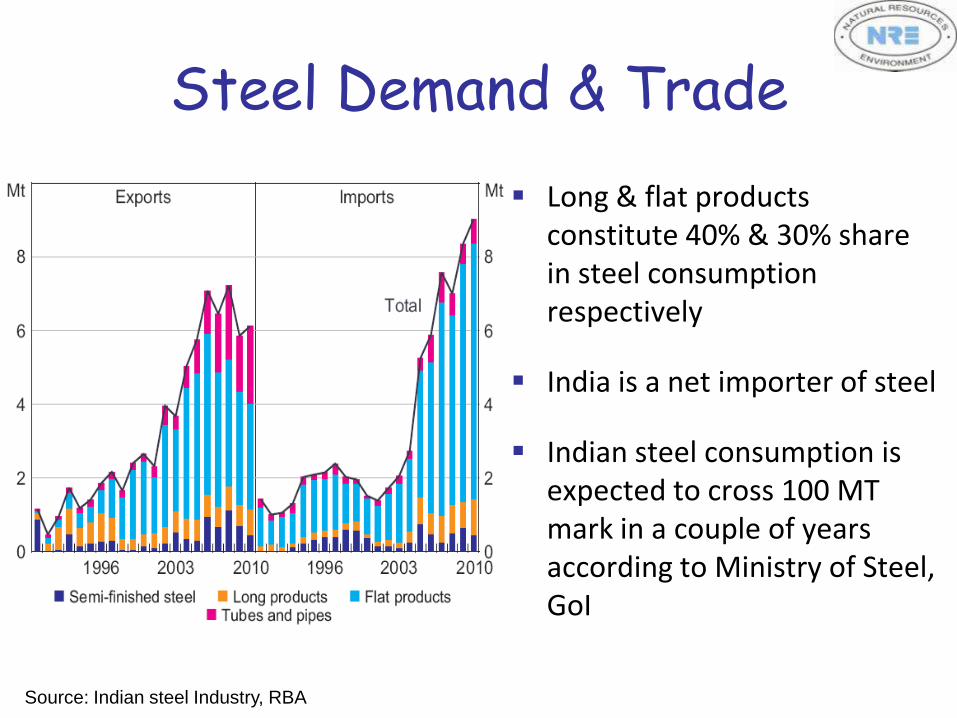

Steel Demand & Trade

Long & flat products constitute 40% & 30% share in steel consumption respectively

India is a net importer of steel

Indian steel consumption is expected to cross 100 MT mark in a couple of years according to Ministry of Steel, GoI

Source: Indian steel Industry, RBA

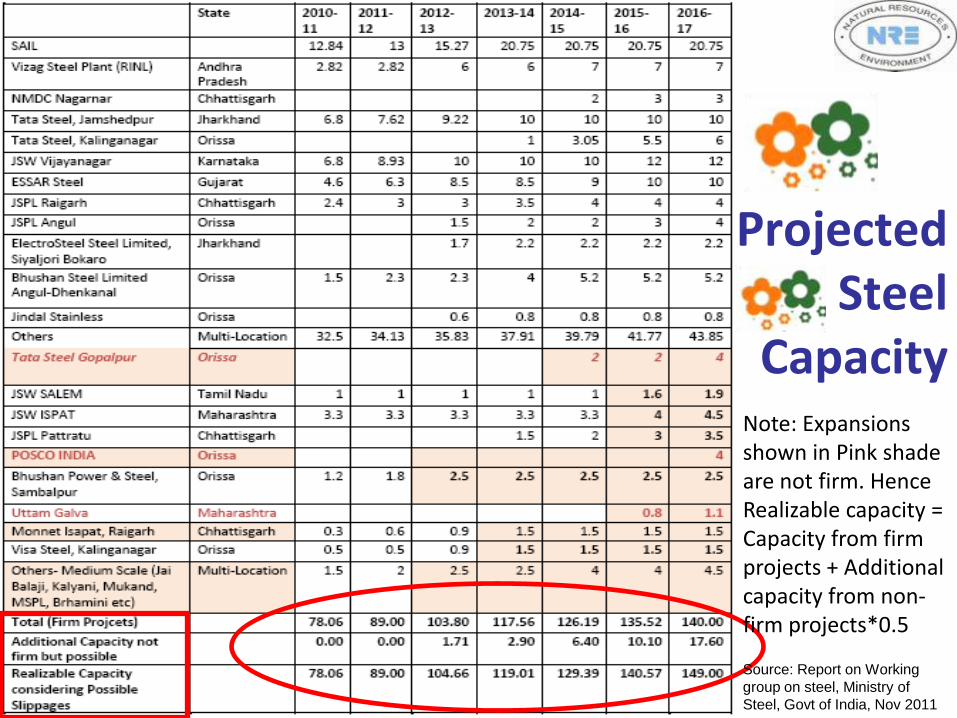

Projected Steel

Capacity

Source: Report on Working

group on steel, Ministry of

Steel, Govt of India, Nov 2011

Note: Expansions shown in Pink shade are not firm. Hence Realizable capacity = Capacity from firm projects + Additional capacity from non-firm projects*0.5

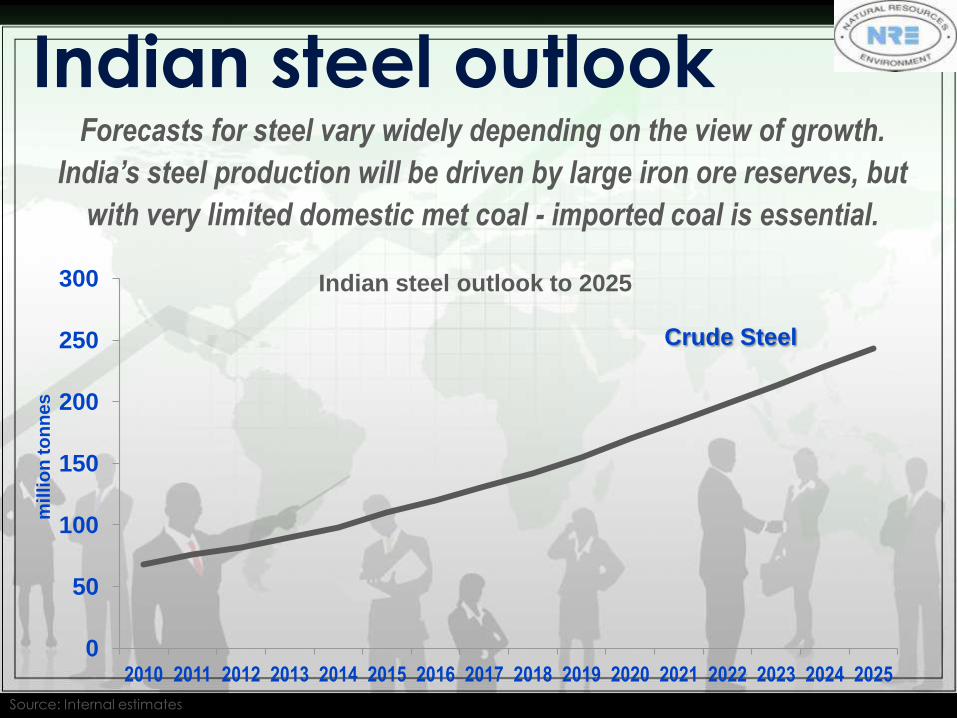

Indian steel outlook Forecasts for steel vary widely depending on the view of growth.

India’s steel production will be driven by large iron ore reserves, but

with very limited domestic met coal - imported coal is essential.

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

mil

lio

n t

on

ne

s

Indian steel outlook to 2025

Crude Steel

Source: Internal estimates

Although India has large coal reserves it is very short of prime HCC

Domestic Coking coal is characteristic of :-

o High ash

o Tends to have poor coke strength

o Requires imported high quality HCC

o Not really suitable for PCI

Domestic coking coal production has remained essentially flat for the past 10 years

Production has infact declined since 2004

Coke production has risen by almost 30% since 2004 and is poised to grow further

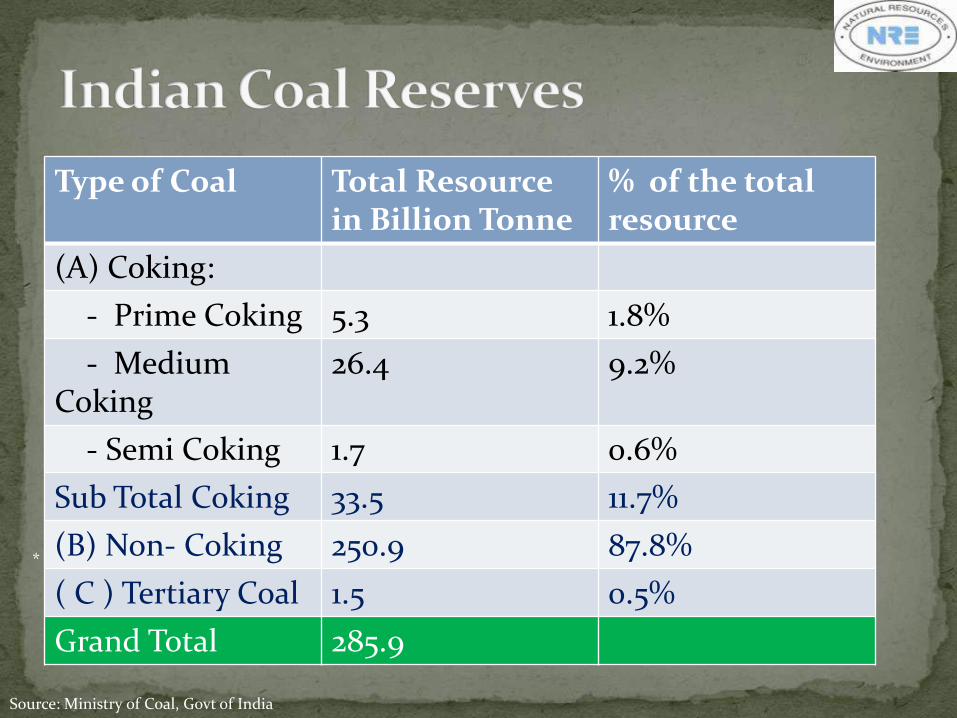

* Includes 749.92 M.T. of Inferred resources established through mapping in North-Eastern region.

Source: Ministry of Coal, Govt of India

Type of Coal Total Resource in Billion Tonne

% of the total resource

(A) Coking:

- Prime Coking 5.3 1.8%

- Medium Coking

26.4 9.2%

- Semi Coking 1.7 0.6%

Sub Total Coking 33.5 11.7%

(B) Non- Coking 250.9 87.8%

( C ) Tertiary Coal 1.5 0.5%

Grand Total 285.9

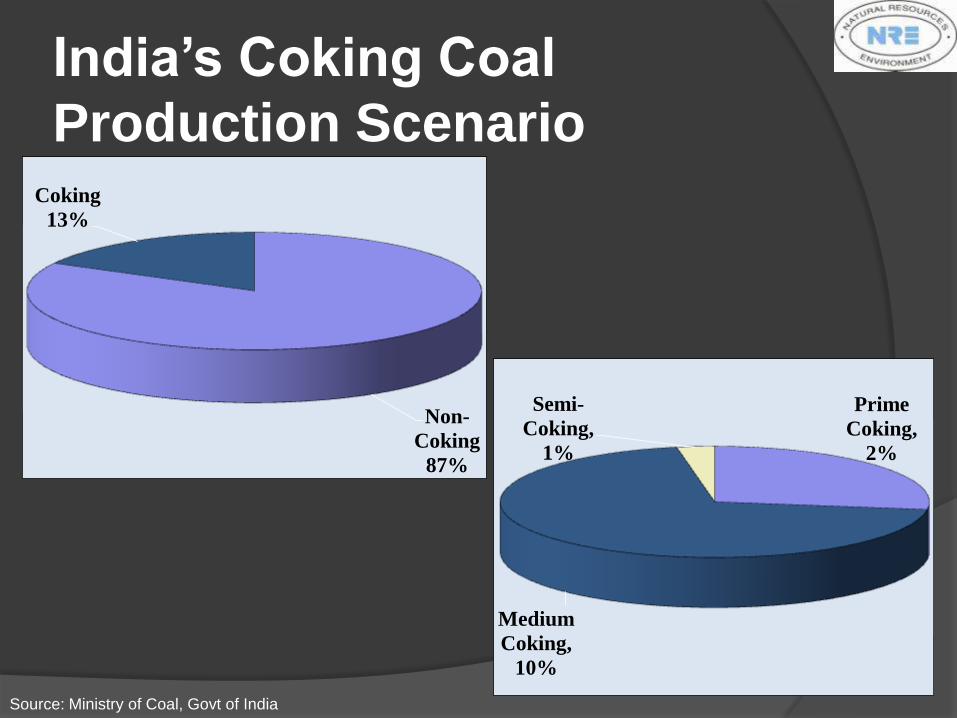

India’s Coking Coal

Production Scenario

Non-

Coking

87%

Coking

13%

Prime

Coking,

2%

Medium

Coking,

10%

Semi-

Coking,

1%

Source: Ministry of Coal, Govt of India

Increasing Coking Coal Demand in Line with Crude Steel Production

125.9

90.2

4.5

0

1

2

3

4

5

0

40

80

120

160

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

Mil

lio

n T

on

nes

Steel Production

Coking Coal Demand

PCI

Source: Report on Working group on steel, Ministry of Steel, Govt of India, Nov 2011

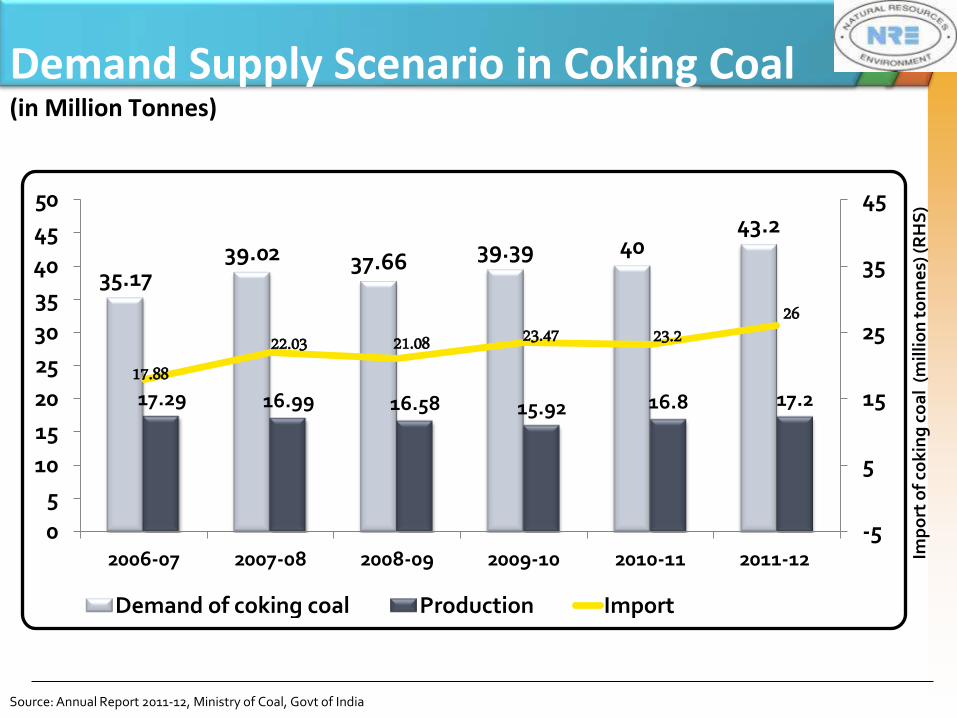

Demand Supply Scenario in Coking Coal (in Million Tonnes)

Imp

ort

of

cok

ing

co

al

(mil

lio

n t

on

ne

s) (R

HS

)

Source: Annual Report 2011-12, Ministry of Coal, Govt of India

35.17 39.02 37.66 39.39 40

43.2

17.29 16.99 16.58 15.92 16.8 17.2

17.88 22.03 21.08 23.47 23.2

26

-5

5

15

25

35

45

0

5

10

15

20

25

30

35

40

45

50

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Demand of coking coal Production Import

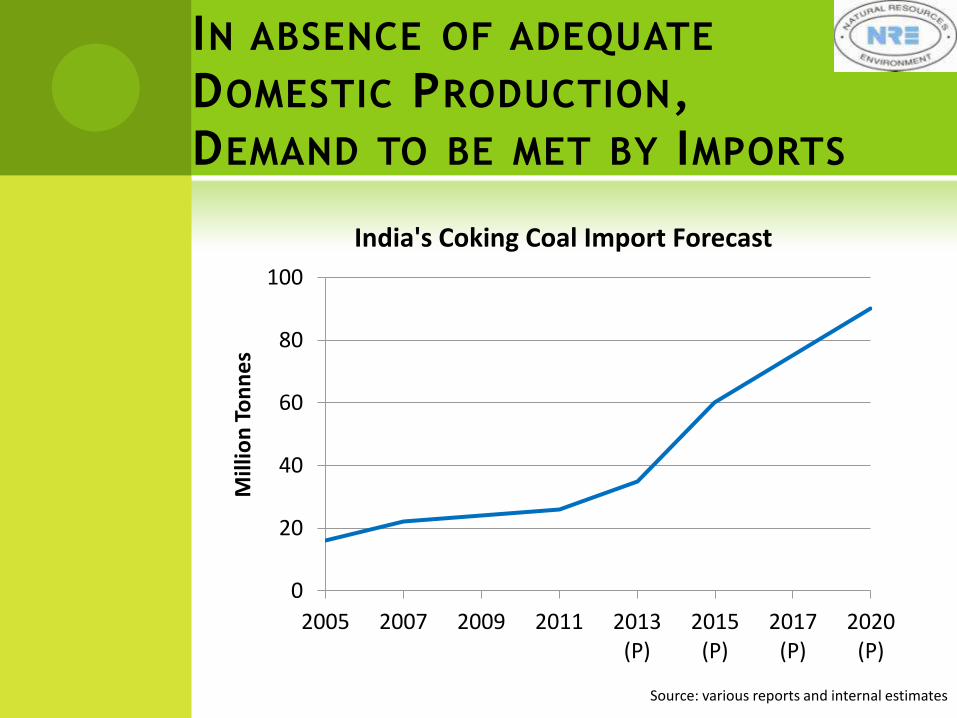

IN ABSENCE OF ADEQUATE

DOMESTIC PRODUCTION,

DEMAND TO BE MET BY IMPORTS

0

20

40

60

80

100

2005 2007 2009 2011 2013 (P)

2015 (P)

2017 (P)

2020 (P)

Mill

ion

To

nn

es India's Coking Coal Import Forecast

Source: various reports and internal estimates

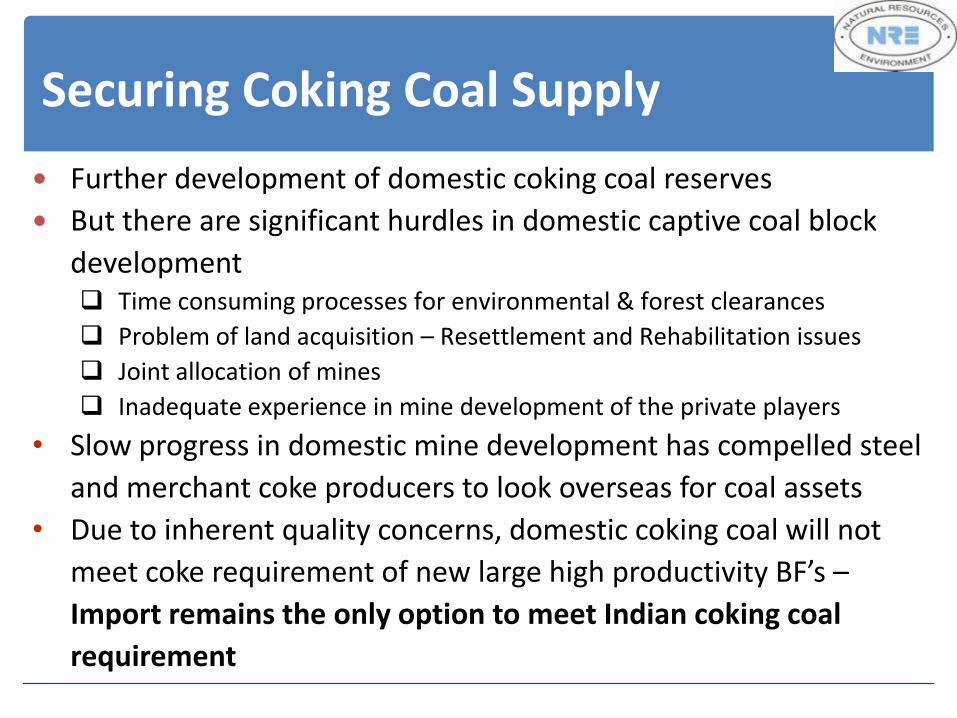

Securing Coking Coal Supply

Further development of domestic coking coal reserves

But there are significant hurdles in domestic captive coal block

development Time consuming processes for environmental & forest clearances

Problem of land acquisition – Resettlement and Rehabilitation issues

Joint allocation of mines

Inadequate experience in mine development of the private players

• Slow progress in domestic mine development has compelled steel

and merchant coke producers to look overseas for coal assets

• Due to inherent quality concerns, domestic coking coal will not

meet coke requirement of new large high productivity BF’s –

Import remains the only option to meet Indian coking coal

requirement

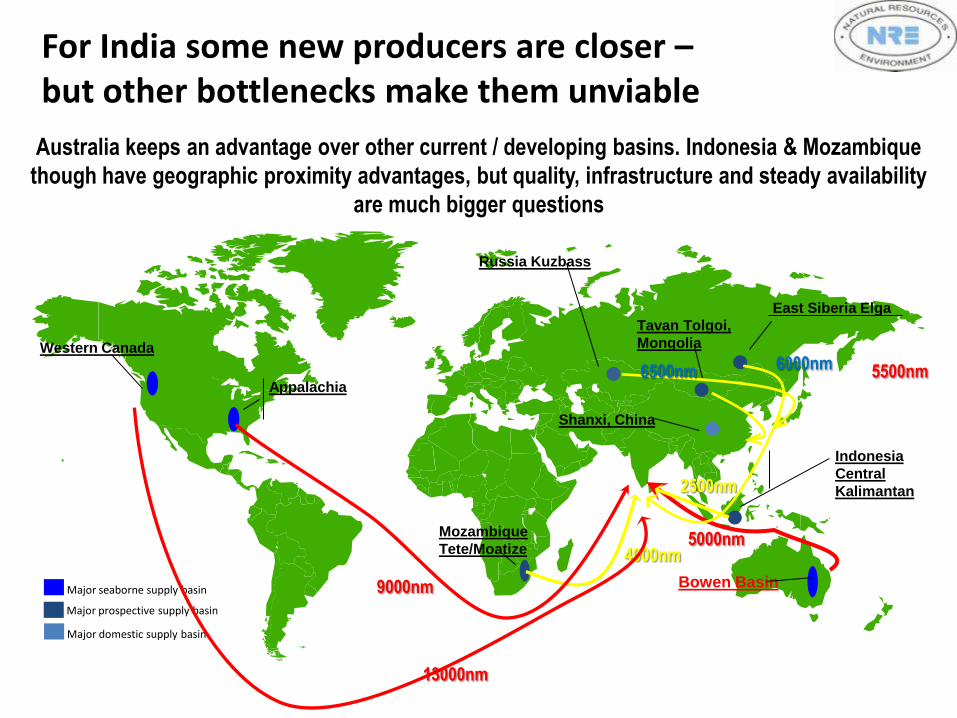

For India some new producers are closer – but other bottlenecks make them unviable

Major seaborne supply basin

Major prospective supply basin

Major domestic supply basin

Tavan Tolgoi,

Mongolia

Shanxi, China

Indonesia

Central

Kalimantan

Bowen Basin

Mozambique

Tete/Moatize

Appalachia

Western Canada

East Siberia Elga

Russia Kuzbass

Australia keeps an advantage over other current / developing basins. Indonesia & Mozambique

though have geographic proximity advantages, but quality, infrastructure and steady availability

are much bigger questions

9000nm

5500nm

5000nm 4000nm

6500nm 6000nm

2500nm

13000nm

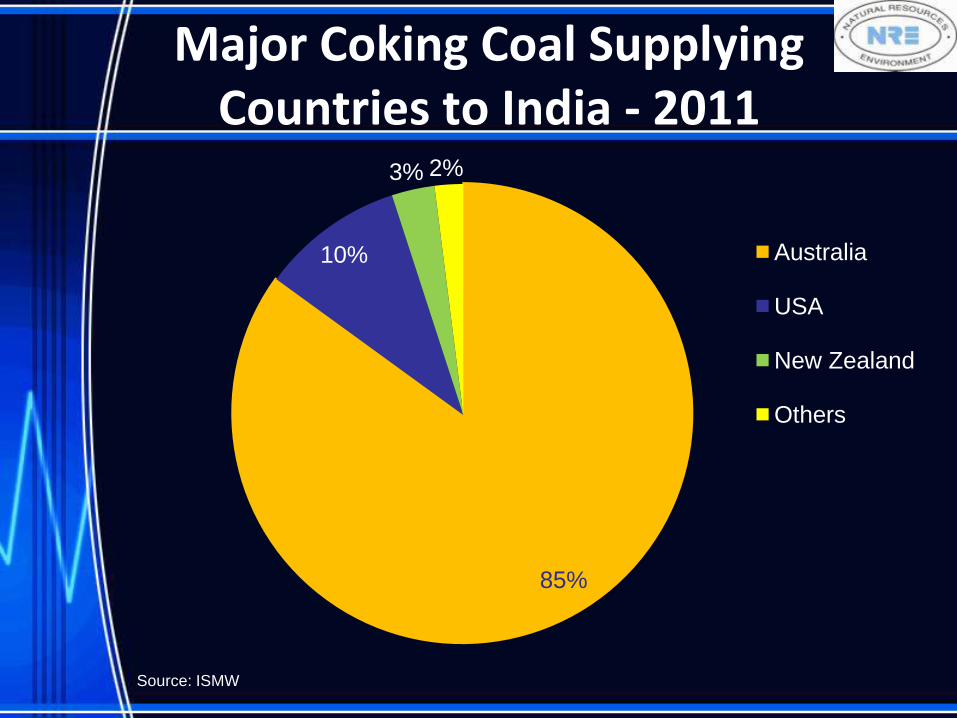

Major Coking Coal Supplying Countries to India - 2011

85%

10%

3% 2%

Australia

USA

New Zealand

Others

Source: ISMW

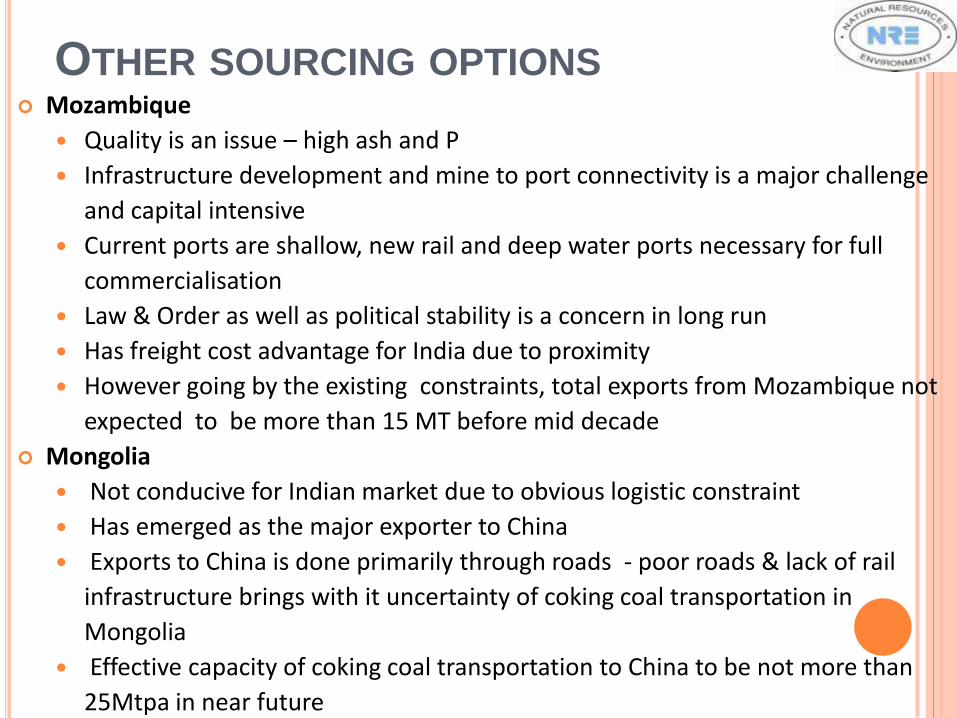

OTHER SOURCING OPTIONS Mozambique

Quality is an issue – high ash and P

Infrastructure development and mine to port connectivity is a major challenge

and capital intensive

Current ports are shallow, new rail and deep water ports necessary for full

commercialisation

Law & Order as well as political stability is a concern in long run

Has freight cost advantage for India due to proximity

However going by the existing constraints, total exports from Mozambique not

expected to be more than 15 MT before mid decade

Mongolia

Not conducive for Indian market due to obvious logistic constraint

Has emerged as the major exporter to China

Exports to China is done primarily through roads - poor roads & lack of rail

infrastructure brings with it uncertainty of coking coal transportation in

Mongolia

Effective capacity of coking coal transportation to China to be not more than

25Mtpa in near future

Other sourcing options

Russia

New capacity is dependant on expansion of ports

Logistics becomes a major constrain for exports to India

USA

Was recently offering coking coal to India in spot market at much cheaper

rates of around $170 per tonne

However recent rise in Atlantic freight has put the US miners in a

disadvantage - now need to achieve USD 150 per tonne to USD 160 per

tonne FOB to remain competitive…. which is difficult

This makes US coal a not so viable alternative for Indian market - makes just

guest appearances

Indian mills have standardized their technical parameters to Australian

specifications - moreover, Indian PSUs are inflexible on quality parameters

Most US coal is HV, and India needs LV and MV HCC coals for blending

(leads onto benefits for GCC)

Advantage Australia

Democratic traditions

Shared commonwealth traditions

English speaking population

Strong, stable Government where Rule of Law

prevails

Industry friendly, proactive bureaucracy

India has Law

China has Order

While

Australia has both Law & Order

Australia Has all the coking coal that INDIA Needs

• However bottlenecks exist

• Infrastructure & port development

• New Taxes (Carbon Tax + MRRT)

• Mining Industry made the whipping boy

In pursuance of

Environmental

Activism……

We tend to forget….

There is hardly

any alternative

to Coal

It is Coal which steers our Economy

Mining has helped us to tide over the recent global economic crisis – & may do the same for the impending one...

If We Do Not Want to Kill the Goose that Lays the Golden Eggs

• Development must continue while we meet the challenges of

climate change

• Global Climate Change is a truth but we need to ensure that

facts & figures are not used to forcefully slaughter the human

civilization that we have built over ages

A Sustainable and qualified response to Global Climate

Change is required without stopping development

The Coal industry is sensitive to the carbon emissions and

is taking all the right steps

A matured workable strategy needs to be designed so

that we do not jeopardize development and at the

same time address the challenge of climate change

AT GUJARAT NRE

We Produce Premium Hard Coking Coal

Which is considered the Greenest variety of coal

Coking Coal….Its Different • Coking coal has special coking properties……Is used

primarily in steel production - - coking coal is converted to

met coke, which is then used in blast furnaces as a

reducing agent to make steel

• Every tonne of steel around us contains 1 ton of coking

coal and is the basic building block of society

• Coking Coal needs to be treated differently & coking coal

producers seek preferential treatment and not bundled in

a single category of coal – based on the value and severe

scarcity of the commodity mined

At Gujarat NRE we mine this essential & valuable commodity

Prime Hard Coking Coal

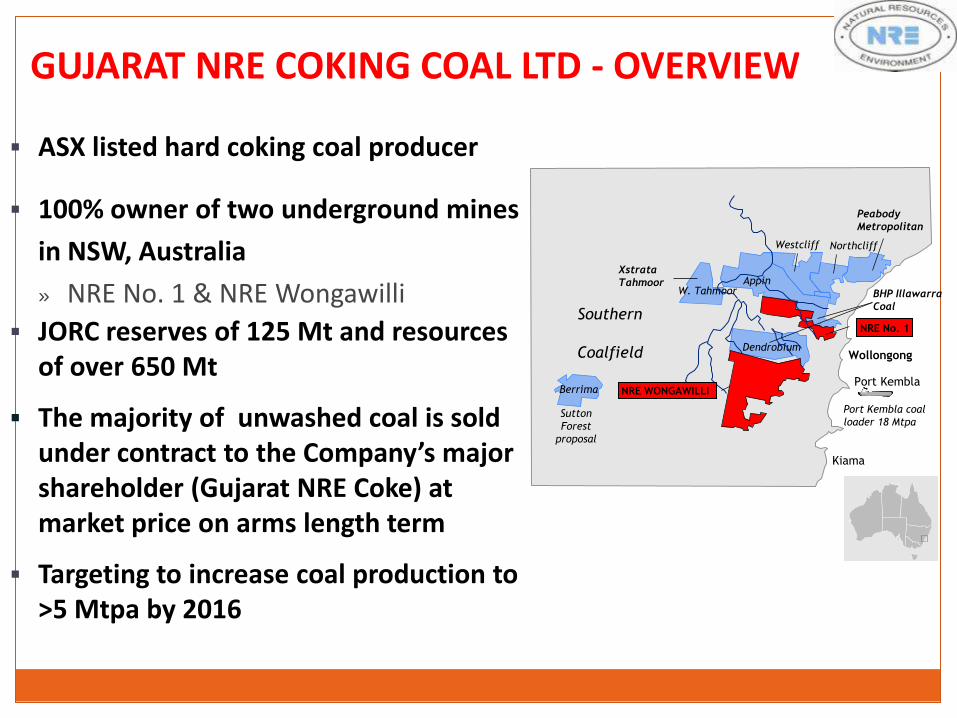

GUJARAT NRE COKING COAL LTD - OVERVIEW

ASX listed hard coking coal producer

100% owner of two underground mines

in NSW, Australia

» NRE No. 1 & NRE Wongawilli

JORC reserves of 125 Mt and resources of over 650 Mt

The majority of unwashed coal is sold under contract to the Company’s major shareholder (Gujarat NRE Coke) at market price on arms length term

Targeting to increase coal production to >5 Mtpa by 2016

Wollongong

Kiama

Port Kembla

Port Kembla coal

loader 18 Mtpa Sutton

Forest

proposal

Berrima

Dendrobium

W. Tahmoor Appin

Westcliff Northcliff

Southern

Coalfield

NRE No. 1

NRE WONGAWILLI

BHP Illawarra

Coal

Peabody

Metropolitan

Xstrata

Tahmoor

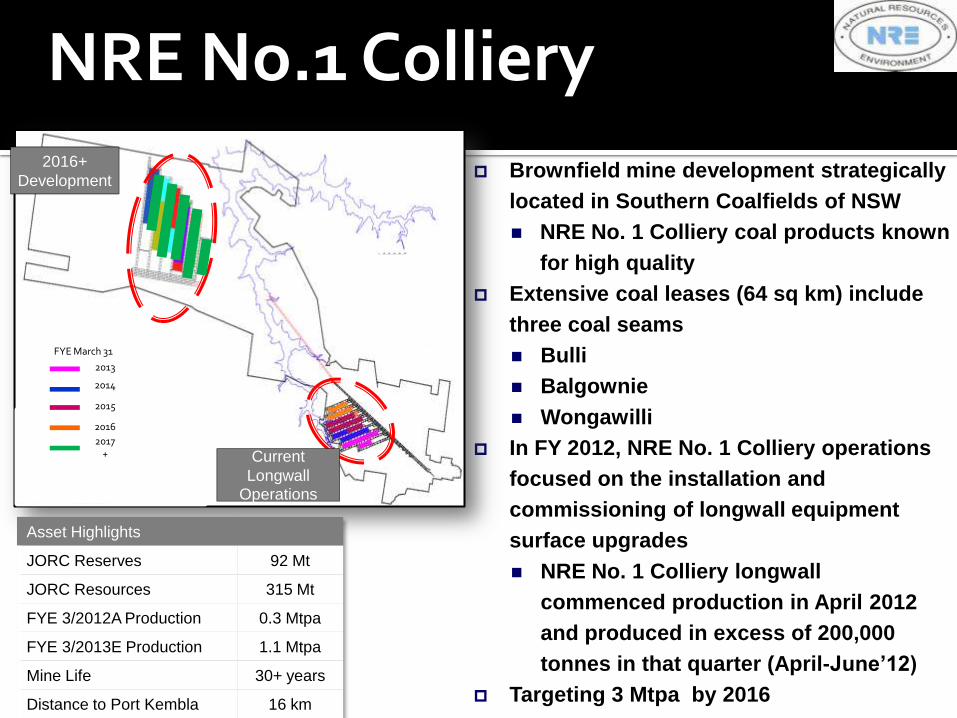

NRE No.1 Colliery

Brownfield mine development strategically

located in Southern Coalfields of NSW

NRE No. 1 Colliery coal products known

for high quality

Extensive coal leases (64 sq km) include

three coal seams

Bulli

Balgownie

Wongawilli

In FY 2012, NRE No. 1 Colliery operations

focused on the installation and

commissioning of longwall equipment

surface upgrades

NRE No. 1 Colliery longwall

commenced production in April 2012

and produced in excess of 200,000

tonnes in that quarter (April-June’12)

Targeting 3 Mtpa by 2016

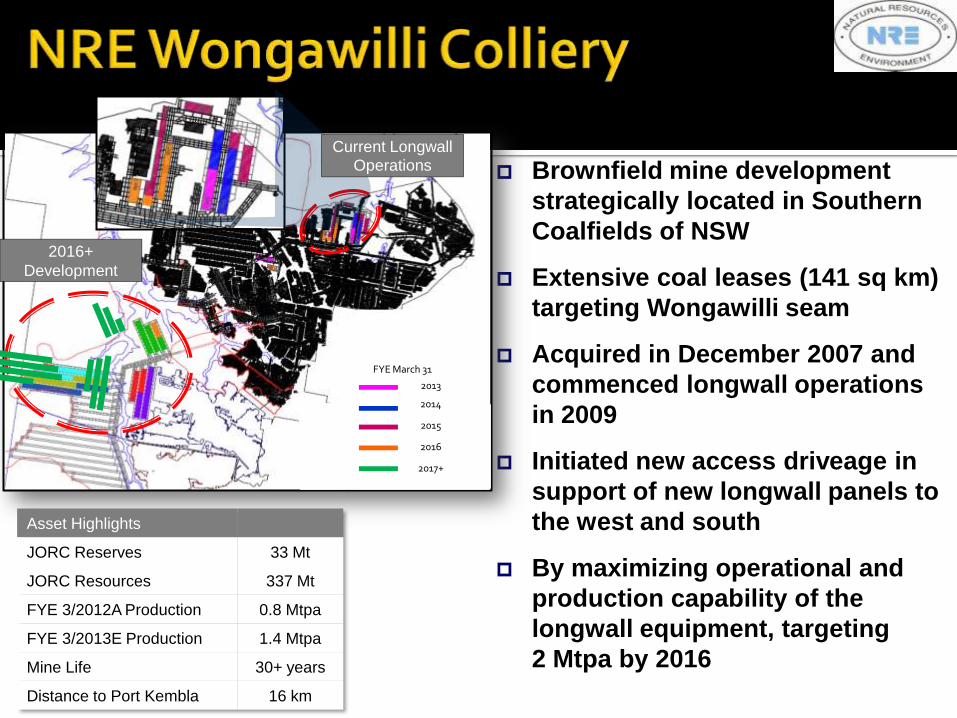

2016+

Development

Current

Longwall Operations

2013

2014

2015

2016

2017+

FYE March 31

Asset Highlights

JORC Reserves 92 Mt

JORC Resources 315 Mt

FYE 3/2012A Production 0.3 Mtpa

FYE 3/2013E Production 1.1 Mtpa

Mine Life 30+ years

Distance to Port Kembla 16 km

Brownfield mine development

strategically located in Southern

Coalfields of NSW

Extensive coal leases (141 sq km)

targeting Wongawilli seam

Acquired in December 2007 and

commenced longwall operations

in 2009

Initiated new access driveage in

support of new longwall panels to

the west and south

By maximizing operational and

production capability of the

longwall equipment, targeting

2 Mtpa by 2016

2013

2014

2015

2016

2017+

FYE March 31

Current Longwall Operations

2016+

Development

Asset Highlights

JORC Reserves 33 Mt

JORC Resources 337 Mt

FYE 3/2012A Production 0.8 Mtpa

FYE 3/2013E Production 1.4 Mtpa

Mine Life 30+ years

Distance to Port Kembla 16 km

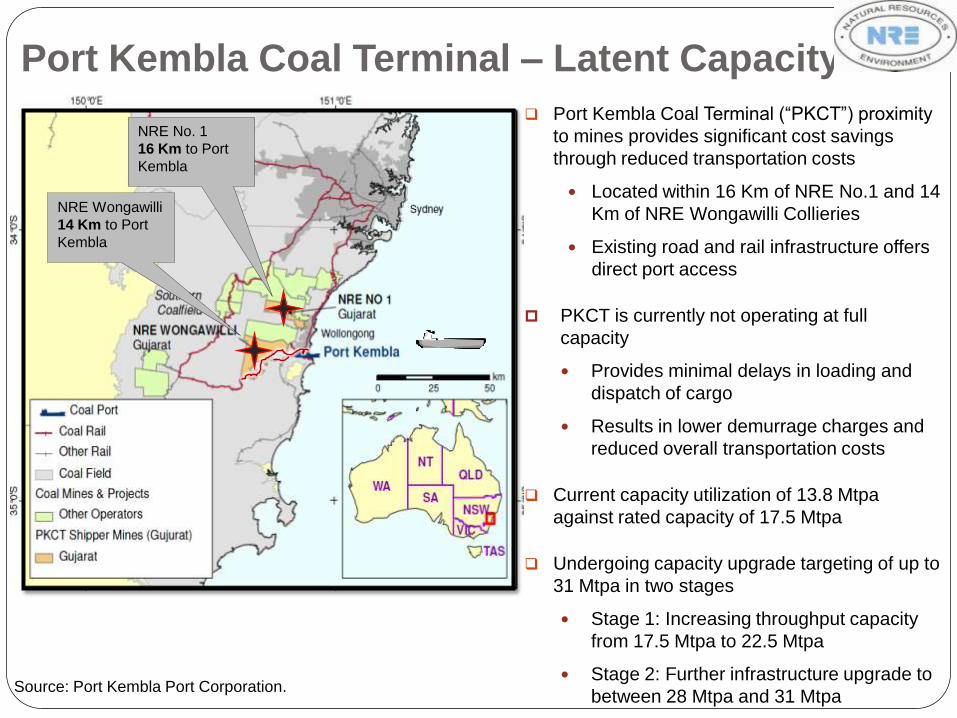

NRE Wongawilli

14 Km to Port

Kembla

NRE No. 1

16 Km to Port

Kembla

Source: Port Kembla Port Corporation.

Port Kembla Coal Terminal (“PKCT”) proximity

to mines provides significant cost savings

through reduced transportation costs

Located within 16 Km of NRE No.1 and 14

Km of NRE Wongawilli Collieries

Existing road and rail infrastructure offers

direct port access

PKCT is currently not operating at full

capacity

Provides minimal delays in loading and

dispatch of cargo

Results in lower demurrage charges and

reduced overall transportation costs

Current capacity utilization of 13.8 Mtpa

against rated capacity of 17.5 Mtpa

Undergoing capacity upgrade targeting of up to

31 Mtpa in two stages

Stage 1: Increasing throughput capacity

from 17.5 Mtpa to 22.5 Mtpa

Stage 2: Further infrastructure upgrade to

between 28 Mtpa and 31 Mtpa

Port Kembla Coal Terminal – Latent Capacity

We are in Australia

The only ASX-listed pure-play metallurgical coal

developer/producer

Positioned for significant production growth to >5 Mtpa

by 2016

Attractive valuation metrics relative to other ASX coal

explorers, developers and producers

GUJARAT NRE COKE LIMITED (GNCL)

GNCL - A SNAPSHOT Largest independent producer of Metallurgical Coke in India

Profit earning and dividend paying with strong financials and

credit rating

Present Met Coke capacity of over 1.43 MT, being increased to

4 MT by 2015

Strong focus on the Environment with ISO 14001:2004 & OHSAS

18001:1999 certification

Rated one of the top 10 company by 10-years profit

performance issued by Business Today on India’s Most Valuable

Companies (Nov 2009 edition)

43

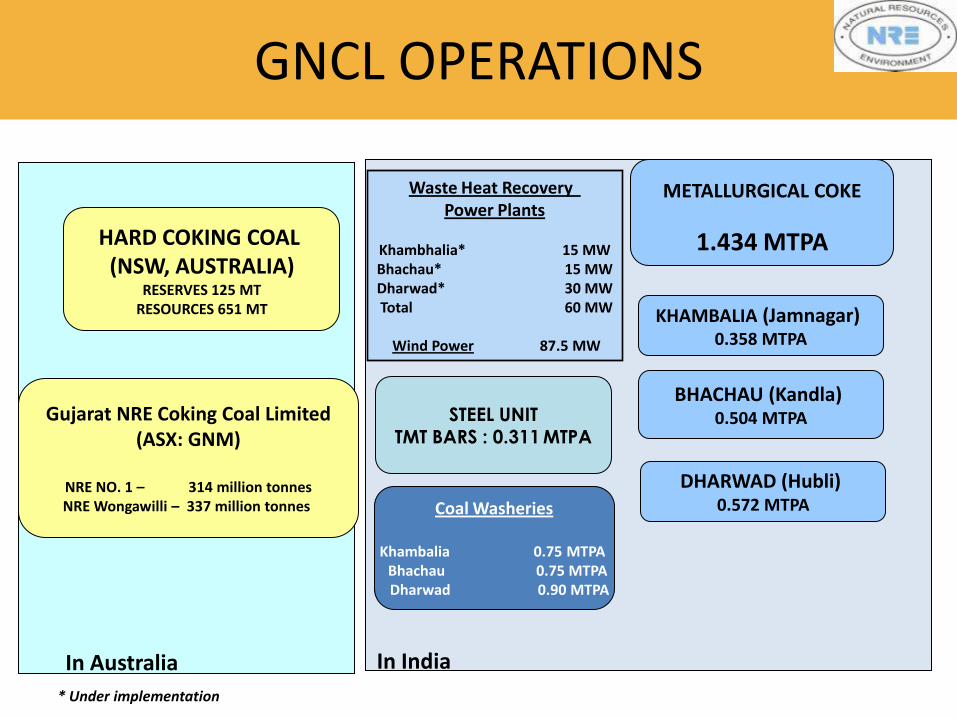

GNCL OPERATIONS

HARD COKING COAL

(NSW, AUSTRALIA) RESERVES 125 MT

RESOURCES 651 MT

METALLURGICAL COKE

1.434 MTPA

Gujarat NRE Coking Coal Limited (ASX: GNM)

NRE NO. 1 – 314 million tonnes NRE Wongawilli – 337 million tonnes

STEEL UNIT TMT BARS : 0.311 MTPA

BHACHAU (Kandla) 0.504 MTPA

KHAMBALIA (Jamnagar) 0.358 MTPA

Waste Heat Recovery Power Plants

Khambhalia* 15 MW Bhachau* 15 MW Dharwad* 30 MW Total 60 MW

Wind Power 87.5 MW

In Australia In India

Coal Washeries

Khambalia 0.75 MTPA Bhachau 0.75 MTPA Dharwad 0.90 MTPA

* Under implementation

DHARWAD (Hubli) 0.572 MTPA

Evolving Global Met Coke Scenario

Existing export tax levied by China and as such China does not plan to resume high levels of coke exports

Coke supply from other sources - e.g. Poland, Russia, Ukraine, Colombia, Japan - has limited potential for increase in future.

Major steelmakers, while currently operating at low rates are structurally coke short when demand and steel production recovers.

Once coke trade returns to levels of around 30 MTPA (with global industrial activity picking up), it would be a challenge to meet the shortfall of China’s 14-15 MTPA peak export capacity

Can India become a leading coke exporter?

INDIA AS A COKE EXPORTER

• Why India? At first glance not a natural coke exporter due to:

– Poorer quality coking coals

– Strong domestic demand growth

– Traditional significant coke importer

– Limited deep water ports

• However, some advantages

– Rapidly growing merchant coke producer

– Adoption of quick to build non recovery, heat recovery ovens

– In between Atlantic and Pacific markets

– Has already sold coke to Brazil, Japan, SE Asian and European countries

• Emerging Huge Void - In 2007 Chinese export was 15 Mt which got reduced to 12 Mt in 2008 and in 2009 it stood at just over an ½ Mt, recovering to ~3Mt currenlty

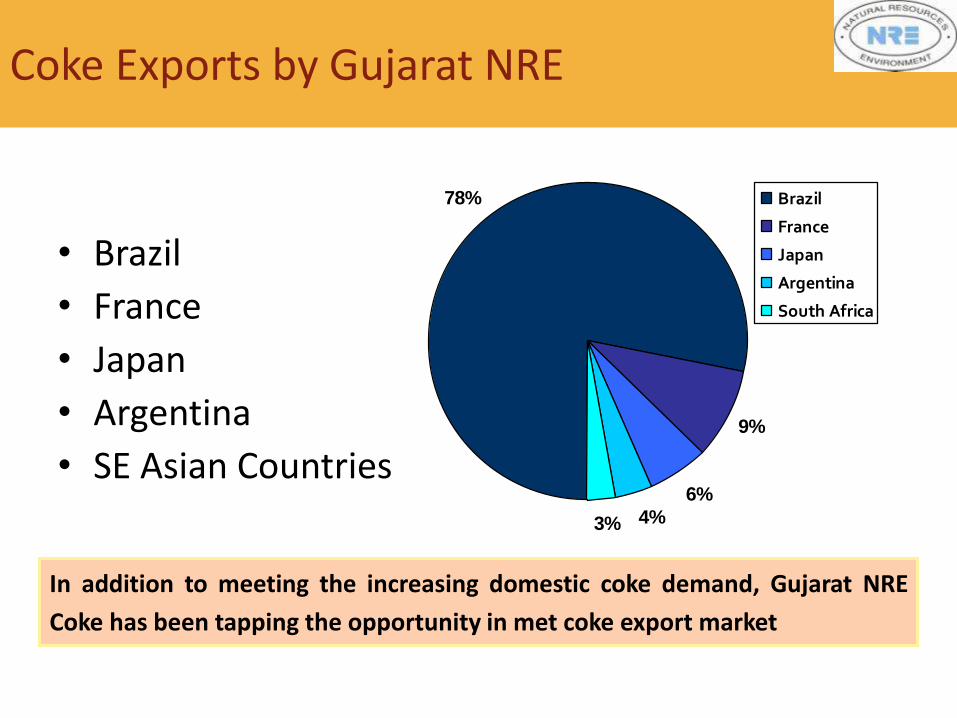

Coke Exports by Gujarat NRE

• Brazil

• France

• Japan

• Argentina

• SE Asian Countries

In addition to meeting the increasing domestic coke demand, Gujarat NRE

Coke has been tapping the opportunity in met coke export market

78%

9%

6%

4%3%

Brazil

France

Japan

Argentina

South Africa

DISCLAIMER & IMPORTANT NOTICE

FORWARD LOOKING STATEMENTS AND OTHER MATTERS

UNLESS OTHERWISE NOTED, THE FORECASTED INDUSTRY AND MARKET DATA CONTAINED IN THE ASSUMPTIONS FOR THE PROJECTIONS ARE BASED UPON

MANAGEMENT ESTIMATES AND INDUSTRY AND MARKET PUBLICATIONS AND SURVEYS. THE INFORMATION FROM INDUSTRY AND MARKET PUBLICATIONS HAS BEEN

OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT THERE CAN BE NO ASSURANCE AS TO THE ACCURACY OR COMPLETENESS OF THE INCLUDED

INFORMATION. GUJARAT NRE COKING COAL LTD (“GNM”) HAS NOT INDEPENDENTLY VERIFIED ANY OF THE DATA FROM THIRD-PARTY SOURCES, NOR HAS GNM

ASCERTAINED THE UNDERLYING ECONOMIC ASSUMPTIONS RELIED UPON THEREIN.

THE INFORMATION AND OPINIONS SUPPLIED BY WOOD MACKENZIE (AUSTRALIA) PTY LIMITED, DOES NOT INCLUDE, NOR SHALL BE CONSTRUED AS INCLUDING,

ADVICE, GUIDANCE OR RECOMMENDATIONS FROM WOOD MACKENZIE TO TAKE, OR NOT TO TAKE, ANY ACTIONS OR DECISIONS IN RELATION TO ANY MATTER,

INCLUDING WITHOUT LIMITATION RELATING TO INVESTMENTS OR THE PURCHASE OR SALE OF ANY SECURITIES, SHARES OR OTHER ASSETS OF ANY KIND. SHOULD

YOU TAKE SUCH ACTION OR DECISION BASED ON SUCH INFORMATION OR OPINION, YOU DO SO ENTIRELY AT YOUR OWN RISK AND WOOD MACKENZIE SHALL HAVE

NO LIABILITY WHATSOEVER FOR ANY LOSS, DAMAGE, COSTS OR EXPENSES INCURRED OR SUFFERED BY YOU AS A RESULT. FURTHER, WOOD MACKENZIE

REPRESENTS THAT ALTHOUGH IT HAS USED REASONABLE ENDEAVOURS TO OBTAIN RELEVANT FACTUAL INFORMATION WHOLLY FROM PUBLIC SOURCES DEEMED

BY IT, IN ITS DISCRETION, TO BE RELIABLE AT THE TIME THE INFORMATION WAS OBTAINED, IT MAKES NO WARRANTIES OR REPRESENTATIONS ABOUT THE

ACCURACY OR COMPLETENESS OF SUCH INFORMATION. ALSO, ALTHOUGH WOOD MACKENZIE REPRESENTS THAT IT HAS USED REASONABLE SKILL AND CARE IN

INTERPRETING SUCH FACTUAL INFORMATION, IT MAKES NO WARRANTIES OR REPRESENTATIONS ABOUT THE ACCURACY OR COMPLETENESS OF SUCH

INTERPRETATION.

THESE MATERIALS ARE BEING SUPPLIED TO YOU SOLELY FOR YOUR INFORMATION AND FOR USE AT THE PRESENTATION. THIS PRESENTATION AND THESE

MATERIALS MAY NOT BE REPRODUCED, REDISTRIBUTED OR PASSED ON, DIRECTLY OR INDIRECTLY, TO ANY OTHER PERSON OR PUBLISHED, IN WHOLE OR IN PART,

BY ANY MEDIUM OR FOR ANY PURPOSE.

THIS PRESENTATION IS NOT INTENDED TO CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN ANY JURISDICTION. NO

REPRESENTATION, WARRANTY OR UNDERTAKING (EXPRESSED OR IMPLIED) IS MADE IN RELATION TO THIS PRESENTATION. THE PRESENTATION CONTAINS

FORWARD LOOKING STATEMENTS WHICH INVOLVE RISKS AND UNCERTAINTIES AND ACTUAL RESULTS AND DEVELOPMENTS MAY DIFFER MATERIALLY FROM THOSE

EXPRESSED OR IMPLIED HEREIN DEPENDING ON A VARIETY OF FACTORS. NO RESPONSIBILITY IS TAKEN OR ACCEPTED BY GNM AND/OR ANY OF ITS PARENTS,

SUBSIDIARIES, AFFILIATES AND THEIR RESPECTIVE OFFICERS, DIRECTORS, EMPLOYEES, AGENTS AND ASSIGNS FOR THE ADEQUACY, COMPLETENESS OR

ACCURACY OF THE PRESENTATION OR THE ASSUMPTIONS ON WHICH IT IS BASED AND ALL LIABILITY IS HEREBY EXPRESSLY EXCLUDED AND DENIED. ANYONE

USING THE PRESENTATION DOES SO AT THEIR OWN RISK AND NO RESPONSIBILITY IS ACCEPTED FOR ANY LOSSES WHICH MAY RESULT FROM SUCH USE DIRECTLY

OR INDIRECTLY. RECIPIENTS SHOULD CARRY OUT THEIR OWN DUE DILIGENCE IN CONNECTION WITH THE ASSUMPTIONS CONTAINED HEREIN.

WE HAVE MADE CERTAIN ASSUMPTIONS WITH RESPECT TO ECONOMIC CONDITIONS, THE LEVEL OF MARKET DEMAND FOR OUR PRODUCT AND SEVERAL OTHER

MATERIAL CONTINGENCIES AND MATTERS WHICH ARE NOT WITHIN OUR CONTROL AND THE OUTCOME OF WHICH CANNOT BE PREDICTED BY US WITH ANY

EXPECTATION OF ACCURACY. OUR ASSUMPTIONS ARE INHERENTLY IMPRECISE, SPECULATIVE , IN SOME CASES, AND SUBJECT TO UNCERTAINITIES AND ACTUAL

RESULTS WILL DEFER, PERHAPS MATERIALLY,FROM THOSE PROJECTED. THE FORGOING PROJECTIONS ARE BASED IN LARGE PARTS UPON US RECEIVING AND

MAINTAINING A CERTAIN LEVEL OF COAL PURCHASE FROM OUR PARENT-GUJARAT NRE COKE LIMITED. THERE CAN BE NO ASSURANCES THAT OUR PARENT WILL

PURCHASE COAL FROM US AT PROJECTED VOLUMES THROUGH FISCAL YEARS 2013 & 2014. THE FORGOING PROJECTIONS ARE BASED UPON OUR ABILITY TO

MAINTAIN CONSISTENT MINING OPERATIONS AT BOTH OF OUR MINES THROUGHOUT FISCAL YEARS 2013 & 2014. THERE CAN BE NO ASSURANCE THAT WE WILL NOT

ENCOUNTER ADVERSE GEOLOGICAL CONDITIONS OR OTHER OPERATING CONDITIONS WHICH IMPAIR OUR ABILITY TO OBTAIN THE PROJECTED PRODUCTION

LEVELS.

IT IS POSSIBLE THAT ASSUMED EVENTS, PERFORMANCE OR CIRCUMSATNCES WILL NOT MATERIALIZE, THAT ANTICIPATED EVENTS MAY NOT OCCUR OR MAY HAVE

DIFFERENT RESULTS THAN PROJECTED OR THAT AN ANTICIPATED EVENTS MAY OCCUR TO CAUSE FUTURE REVENUE, OPERATING EXPENSES AND NET CASH FLOW

TO VARY MATERIALLY FROM THE PROJECTIONS.

COMPETENT PERSON STATEMENT

The information in this Presentation that relates to Exploration Results, Mineral Resources or

Ore Reserves is based on information compiled by, in relation to the Coal Resources for both

NRE Wongawilli Colliery and NRE No.1 Mine, by Mr. Barry Clark an employee of Gujarat NRE

Coking Coal Ltd, and in relation to the Coal Reserves for both NRE Wongawilli Colliery and NRE

No.1 Mine, by Mr. Kris Markowski, also an employee of Gujarat NRE Coking Coal Ltd.

Mr. Clark is a Member of The Australasian Institute of Mining and Metallurgy or the Australian

Institute of Geoscientists. Mr. Clark has sufficient experience which is relevant to the style of

mineralization and type of deposit under consideration and to the activity which he is undertaking

to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for

Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr. Clark consents to

the inclusion in the Presentation of the matters based on his information in the form and context

in which it appears.

Mr. Markowski is a Member of The Australasian Institute of Mining and Metallurgy or the

Australian Institute of Geoscientists. Mr. Markowski has sufficient experience which is relevant to

the style of mineralization and type of deposit under consideration and to the activity which he is

undertaking to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian

Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr.

Markowski consents to the inclusion in the Presentation of the matters based on his information

in the form and context in which it appears.

THANK YOU 50