florida keys community college district board of trustees

TRANSCRIPT

FLORIDA KEYS COMMUNITY COLLEGE DISTRICT BOARD OF TRUSTEES

REGULAR MEETING September 26, 2011

2:00 PM Key Colony Beach City Hall

AG E N D A

I. CALL TO ORDER II. PLEDGE TO THE FLAG

III. ADOPTION AND ADDITION TO THE AGENDA IV. APPROVAL OF MINUTES of meeting held July 25, 2011. V. CONSENT AGENDA A. Continuing Workforce Ed. Fees Attachment #1

B. Disposition of Property Attachment #2 C. Library Fees Attachment #3 VI. DISTRICT BOARD OF TRUSTEES

PRESIDENT A. President’s Report B. Focus on Students – None C. Faculty Council Report – Penni Wise D. Distance Learning Presentation – Georgina Skinner E. Re-Certification of FKCC Foundation as a DSO and Audit Attachments #4 F. Presidential Search – Draft Proposal Attachments #5

• Presidential Profile • Composition of Search Committee • Timeline • Budget

ATTORNEY A. Board Rule Changes

1. BR 6.200 Programs Attachments #6 2. BR 1.410 Formulation of Rules and Adm. Procedures Attachment #7 3. BR 5.510 Grievance Resolution Attachment #8

VII. HUMAN RESOURCES A. Personnel Actions Attachments #9

VIII. FINANCIAL SERVICES A. Report by VP Jean Mauk on

Finance and Construction Projects Attachments #10 B. Financial Statements June, July and August 2011 Attachments #11 C. Annual Financial Report Sep. Attachment D. Capital Budget 2011-12 Attachment #12 E. MOU between FKCC and The Florida Keys Attachment #13

College Campus Foundation IX. INSTRUCTIONAL SERVICES

A. Report by Provost Brittany Snyder Attachments #14 B. IAA Agreement Island Christian School 2011-12 Attachments #15 C. Addendum to College Catalog 2011-12 Attachments #16 D. Faculty Credentials – For Information Only Attachment #17

X. STUDENT SERIVCES A. Report by Dean Erika MacWilliams

on Student Affairs and Accreditation Attachment #18 XI. GOOD OF THE ORDER

Public Input The next meeting will be held on October 24, 2011, Key West.

PROPOSED BOARD ACTION

To approve the course fees for upcoming Continuing Education course offerings.

AUTHORITY FOR ACTION

Recommend approval from the Florida Keys Community College Board for the attached course fees for upcoming courses.

BACKGROUND INFORMATION

The office of Continuing Education and Workforce promotes life-long learning by extending the resources of Florida Keys Community College. Self-supporting programs which build on the strengths and expertise of Florida Keys Community College faculty, adjunct staff and community subject matter specialists. The office of Continuing Education and Workforce develops and offer non-credit continuing education offerings that are responsive to the professional/career development and personal enrichment needs of individuals as well as business and industry.

Continuing Education Price Summary

Course Name Course # Tuition Access 2007 Fundamentals MSO0940 $125.00 Access 2007 Intermediate MSO0941 $125.00 Adult Ballet BAL0010 $165.00 Advanced Conversation Part 2 EAS0257 $155.00 Advanced Reading, Writing and Grammar Review Part 1 EAS0276 $155.00 Advanced Reading, Writing and Grammar Review, Part 2 EAS0277 $155.00 Basic Voice BGV0201 $300.00 Beginner's Digital Photography IDP0103 $100.00 Bootcamp with Hally BTC0101 $90.00 Bravo! Italian Conversation and Culture BSI0104 $155.00 Cake Decorating CAK0010 $60.00 Childrens Ballet BAL0013 $79.00 Childrens Ballet BAL0011 $79.00 Conversational Spanish SPK0100 $155.00 Conversational Spanish for Beginners SPB0106 $168.80 Creative Photography ICP0100 $100.00 Creative Still Life/Composition CSL0010 $25.00 Dental Assistant Program DAP0300 $1,199.00 Digital Photography 1 & 2 All Inclusive IDP0102 $120.00 Dreamweaver Basics CS5 DWB0904 $139.50 EKG Technician Certification Program EKG0300 $999.00 Electronic Health Management Program EHM0300 $1,999.00 ESL: Basics Level 1 Part 1 EAS0203 $155.00 ESL: Basics Level 1 Part 2 EAS0204 $155.00 ESL: Eng Ab Beg 1 Part 1 EAS0213 $155.00 Excel 2007 Fundamentals MSO0930 $125.00 Excel 2007 Intermediate MSO0931 $125.00 Finding Your Creative Voice FYC0010 $90.00 Great Decisions LLC0105 $60.00 How to Prepare for the TOEFL Part 1 TPC0200 $155.00 How to Prepare for the TOEFL Part 2 TPC0203 $155.00 Hydroponic Gardening LLC0120 $60.00 Intermediate Conversational Spanish for Beginners SPB0107 $168.80 Intro to Cortical Field Re-education ICF0010 $15.00 Intro to Personal Computers IPC0900 $125.00 Introduction to Ceramics CER0010 $160.00 Keys to Oil Painting OIL0101 $155.00 Life Drawing Workshop for Beginners to Advanced LDW0100 $25.00 Medical Assistant Administration Program MAA0300 $999.00 Medical Coding and Billing MDC0300 $1,799.00 Mixed Community Chorus MCC0201 $105.00 Mystery Monsters of Florida MMF0100 $65.00 OSHA 8-Hour HAZWOPER First Responder Refresher Training OSH0103 $200.00 Outlook 2007 Fundamentals MSO0950 $125.00 Pharmacy Technician Cert Prgm PTC0300 $999.00 Phlebotomy Technician PBT0300 $1,599.00

Continuing Education Price Summary

Course Name Course # Tuition Photoshop for Beginners PSH0901 $130.00 Power Point 2007 Fundamentals MSO0920 $125.00 Pre-Ballet BAL0012 $79.00 Public Safety Diving Stress PSD0701 $200.00 Quickbooks 2010 QKB0903 $150.00 Reading, Writing & Grammer Review Part 1 EAS0254 $155.00 Reading, Writing & Grammer Review Part 2 EAS0255 $155.00 Real Estate Sales Associate Training EST0200 $450.00 Sight-Singing SSI0010 $86.50 Specialized Creative Welding WLD0903 $450.00 Survival Spanish for JIATF SPB0102 $132.50 Survival Spanish SPB0102 $155.00 Survival Spanish II SPB0112 $155.00 The Spirit of Clay CER0016 $400.00 W&L Eng: Basics Level 2 Part 1 EAS0231 $155.00 W&L Eng: English for Absolute Beginners Part 1 EAB0203 $155.00 W&L Eng: English for Absolute Beginners Part 2 EAB0204 $155.00 W&L Eng: Advanced Level 1 Part 1 EAS0221 $155.00 W&L Eng: Advanced Level 1 Part 2 EAS0222 $155.00 W&L Eng: Basics Level 1 Part 1 EAS0201 $155.00 W&L Eng: Basics Level 2 Part 2 EAS0232 $155.00 W&L Eng: Intermediate Level 1 Part 1 EAS0211 $155.00 W&L Eng: Intermediate Level 1 Part 2 EAS0212 $155.00 W&L Eng: Intermediate Level 2 Part 1 EAS0225 $155.00 W&L Eng: Intermediate Level 2 Part 2 EAS0226 $155.00 Wire-Wrap Jewelry Workshop JWL0205 $113.00 Woman and Wealth: Creating a Strategy That Works for You WAW0100 $25.00 Word 2007 Fundamentals MSO0910 $125.00 Word 2007 Intermediate MSO0911 $125.00 Writing Life Stories LLC0126 $60.00 Yoga-Toner YOG0104 $165.00 Zumba ZUM0010 $180.00 Zumba ZUM0010 $90.00 Catherine Torres Submitted by Catherine Torres Director of Continuing Education and Workforce

PROPOSED BOARD ACTION

To approve the disposal of property that is no longer of value to the College.

AUTHORITY FOR ACTION

Recommend approval from the Florida Keys Community College Board for the attached list of disposition of property.

BACKGROUND INFORMATION

The Purchasing Office continually maintains a list of assets of the College and updates the lists when items are no longer of value. Property is disposed of when items are broken, antiquity or obsolete and are taken off the fixed asset listing.

FLORIDA KEYS COMMUNITY COLLEGE 5901 College Road, Key West, FL 33040

(305) 296-9081, fkcc.edu MEMORANDUM

Date: September 12, 2011

To: Jean Mauk

From: Doug Pryor

Subject: Disposition of Property

College property is regularly monitored as to its condition and usefulness. As property is determined to be no longer useful for college purposes, because it is obsolete, broken, lost or stolen, a request is made for a formal disposition approval. I request you recommend that the property listed below be reviewed by the District Board of Trustees in accordance with State requirements, for the reasons stated. The total value of the listed property for FKCC Board of Trustees disposition approval is $29,146.00. Tag No. Acquisition Date Description Cost Condition 1 1652 10/31/1979 Baldwin Piano $1,375.00 Obsolete 2 4491 3/10/1980 Baldwin Piano $1,375.00 Obsolete 3 5114 8/11/2004 Johnson Outboard

SN# 07053489 $1,224.00 Obsolete /

Cannibalized 4 5115 8/11/2004 Johnson Outboard

SN# 07053571 $1,224.00 Obsolete /

Cannibalized 5 5116 8/11/2004 Johnson Outboard

SN# 07053572 $1,224.00 Obsolete /

Cannibalized 6 5117 8/11/2004 Johnson Outboard

SN# 07053573 $1,224.00 Obsolete /

Cannibalized 7 5118 8/11/2004 Johnson Outboard

SN# 07053570 $1,224.00 Obsolete /

Cannibalized 8 5119 8/11/2004 Johnson Outboard

SN# 07053492 $1,224.00 Obsolete /

Cannibalized 9 5120 8/11/2004 Johnson Outboard

SN# 07053491 $1,224.00 Obsolete /

Cannibalized 10 5276 8/14/2006 Johnson Outboard

SN# 22035175 $1,698.00 Obsolete /

Cannibalized 11 5277 8/14/2006 Johnson Outboard

SN# 22035173 $1,698.00 Obsolete /

Cannibalized 12 5284 8/24/2006 Johnson Outboard

SN# 22037462 $1,698.00 Obsolete /

Cannibalized 13 5427 11/5/2007 Pay-Per-Print System $12,734.00 In Working

SN# 460706781 Condition. Changed to new WEPA Wireless System

______________________________ ______________________________ Board Approved Date Disposal Signature and Date ______________________________ Disposal Witness and Date ______________________________ Disposal Method and/or Location

FLORIDA KEYS COMMUNITY COLLEGE

LEARNING RESOURCES CENTER / LIBRARY Memorandum

DATE: September 15, 2011 TO: Board of Trustees FROM: Juana Careaga, Director of Learning Resources Center / Library SUBJECT: Revision of library fees

PROPOSED BOARD ACTION Approval of the revisions of library fees

BACKGROUND INFORMATION New WEPA printing system has been installed and new costs per print page. Black and White prints are 15 cents per page and color prints are 65 cents per page.

FKCC Library Services & Fees

We are asking for board approval of new library fees which are marked with a

Service Fee

Faxing $1.50 per page

WEPA Print Card $5.00

Printing

15¢ per black & white page

65¢ per color page

20¢ transaction fee if a credit card is used at the kiosk

Copier 15¢ per page

Overdue Books 5¢ per day, per item

Lost Books Depends on price of book + $10.00 processing fee

Community Computer User

$25.00 for 1 month

$40.00 for 2 months

$5.00 for 1 day

Library Card Replacement $1.00 per new card

Book Sale

.25 cents for selected paperbacks

$1.00 for unmarked items

$5.00 for stickered items Students with unpaid fees will have a Hold placed on their Library and Banner accounts. This will prevent them from registering for classes. Holds will only be removed when items are returned and/or payment is received for delinquent items.

FKCC Board of Trustees Faculty Council Report: Sept 26, 2011

A new academic year has begun and there are many new faculty faces. The faculty is excited over our new colleagues. We are honored to say FKCC faculty is amazing, seasoned, and well diverse. Even more importantly, a few of our new full‐time faculty are former adjunct faculty. This gives credence to the fine adjunct faculty who teach at FKCC.

On September 8, the Faculty Council met. The Faculty Council elected a new Parliamentarian, John Majewicz. We then proceeded to engage in discussions as to Faculty Scheduling and Faculty Evaluations.

I predict the Faculty Council will be proposing well thought‐out motions with resolutions like we have in the past. We continue to communicate college issues with the Provost and staff. FKCC’s Faculty Council remains active and committed to making FKCC an outstanding college.

We look forward to the SAC’s Reaffirmation visit and to demonstrating how incredible our students, faculty, and staff really are.

Respectfully submitted,

Penni Wise, FKCC Faculty Council President

To review Direct-Support Organization Florida Keys Educational Foundation’s Audit Review Check List and recertify Florida Keys Educational Foundation as a DSO.

PROPOSED BOARD ACTION

Board Rule 2.510, Direct Support Organization (DSO) Accountability and Florida Statute 1004.70, Community College Direct Support Organizations

AUTHORITY FOR ACTION

The Board of Trustees annually reviews approved standards for DSOs and certifies that they meet the operating requirements established by the Board (B.R. 2.510). Part of this process includes review of the annual audit and IRS Tax Form 990.

BACKGROUND INFORMATION

The following information from Florida Keys Educational Foundation, Inc., is provided to the Board for review and approval:

1) Direct-Support Organizations (DSO) Audit Review Check List 2) Financial Statements For the Years Ended March 31, 2011 and 2010 3) Management Letter March 31, 2011 4) Return of Organization Exempt From Income Tax 2010.

Return to: Department of Education Rev. 10/26/06 Community College Budget Office 325 W. Gaines Street, Suite 1224 Tallahassee, FL 32399-0400

DIRECT-SUPPORT ORGANIZATIONS (DSO) AUDIT REVIEW CHECK LIST

DSO NAME _____Florida Keys Educational Foundation

FOR THE YEAR ENDING: ___

_________

March 31, 2011

____

COLLEGE PRESIDENT’S RESPONSE TO DSO AUDIT: 1. In accordance with Section 1004.70(2), Florida Statutes, did the chairperson of the board of trustees

appoint a representative to the board of directors and the executive committee of each direct-support organization established under Section 1004.70, Florida Statutes?

YES __X__ NO____ 2. In accordance with Section 1004.70(2), Florida Statutes, did the president or the president’s

designee serve on the board of directors and the executive committee of the college’s direct-support organization?

YES X

NO____

3. In accordance with Section 1004.70(4)(c), Florida Statutes, did the board of trustees approve all transactions or agreements between one direct support organization and another direct support organizations or between a direct-support organization and a center of technology innovation designated under s. 1004.77, Florida Statutes?

YES X

NO N/A____

4. In accordance with Section 1004.70(5), Florida Statutes, did this direct-support organization submit

to the board of trustees a copy of its federal IRS Application for Recognition of Exemption form (Form 1023) and its federal Internal Revenue Service Return of Organization Exempt from Income Tax form (Form 990)?

YES X

NO N/A____

5. Did the board of trustees review the following issues and accept the annual audit? A. College support of direct-support organization’s operating expenses. B. Annual change in the direct -support organization’s net assets. C. Direct-Support Organization’s ability to cover indebtedness (both current and projected). YES X

NO N/A ____

COLLEGE NAME ______Florida Keys Community College

___________________________________

_________________________________________________________ ___________________ PRESIDENT (SIGNATURE) DATE _______ Dr. Lawrence W. Tyree (Printed)

____________________________________________________

____________________________________________________________ _________________ CHAIRMAN, BOARD OF TRUSTEES (SIGNATURE) DATE _______ Spencer Slate________________________________________________________________

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC. D/B/A FKCC FOUNDATION

Financial Statements

For the Years Ended

March 31, 2011 and 2010

(With Independent Auditors’ Report Thereon)

TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS’ REPORT ........................ 1 - 2 FINANCIAL STATEMENTS: Statements of Financial Position ................... 3 Statements of Activities ............................ 4 - 5 Statements of Cash Flows ....... .................... 6 Notes to Financial Statements ....................... 7 - 20 COMPLIANCE AUDIT REPORTS: Independent Auditors’ Report on Compliance and on Internal Control Over Financial Reporting and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ............................................ 21 - 22

SMITH, BUZZI & ASSOCIATES, LLC. CERTIFIED PUBLIC ACCOUNTANTS

2103 CORAL WAY, SUITE 305 MIAMI, FLORIDA 33145

TEL. (305) 285-2300 FAX (305) 285-2309

JULIO M. BUZZI, C.P.A. MEMBERS: JOSE E. SMITH, C.P.A. AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS FLORIDA INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS

INDEPENDENT AUDITORS’ REPORT

To the Board of Directors Florida Keys Educational Foundation, Inc. D/B/A FKCC Foundation: We have audited the accompanying statements of financial position of Florida Keys Educational Foundation, Inc. (D/B/A FKCC Foundation) (a non-profit organization), as of March 31, 2011 and 2010 and the related statements of activities and cash flows for the years then ended. These financial statements are the responsibility of Florida Keys Educational Foundation, Inc.’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America, Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Florida Keys Educational Foundation, Inc’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

-1-

In our opinion, based on our audits, the financial statements referred to above present fairly, in all material respects, the financial position of Florida Keys Educational Foundation, Inc., as of March 31, 2011 and 2010 and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America. In accordance with Government Auditing Standards, we have also issued our report dated May 17, 2011, on our consideration of Florida Keys Educational Foundation, Inc’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audits.

May 17, 2011

-2-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Statements of Financial Position

March 31, 2011 and 2010

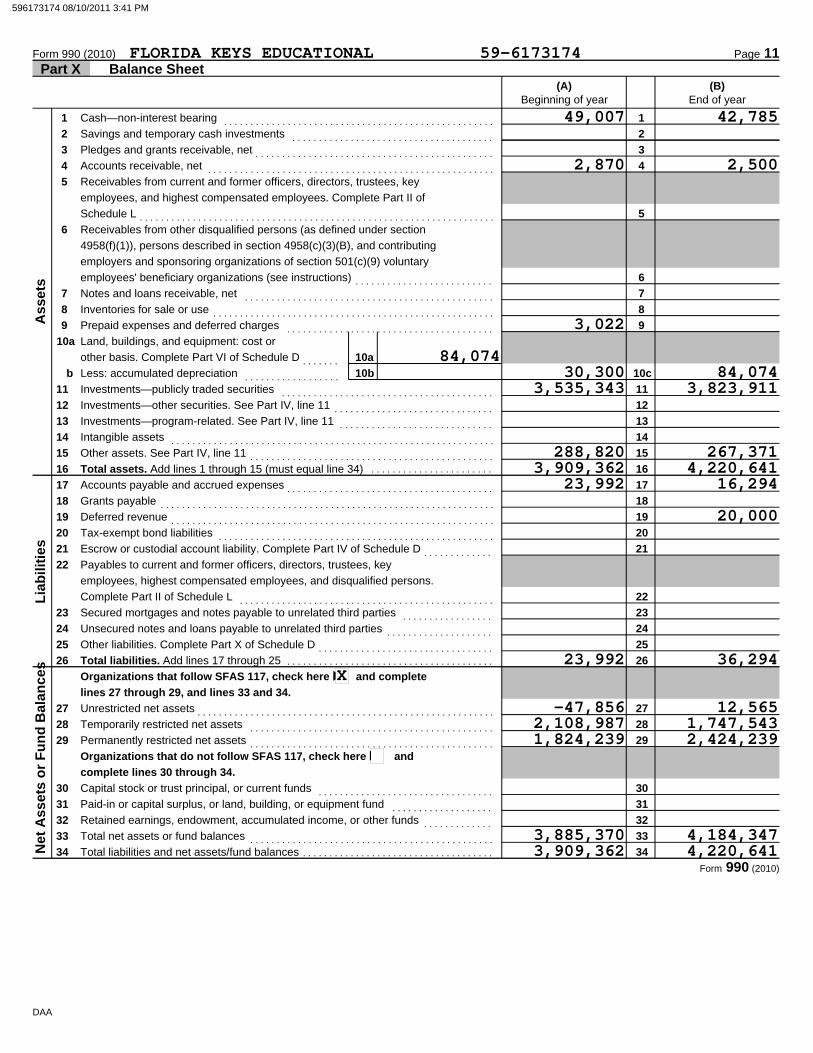

2011 2010 ASSETS CURRENT ASSETS Cash and equivalents $ 42,785 49,007 Investments 3,823,911 3,535,343 Accounts receivable 2,500 2,870 Prepaid expenses - 3,022 Accrued interest and dividends receivable - 1,096 TOTAL CURRENT ASSETS 3,869,196 3,591,338 NON CURRENT ASSETS Prepaid scholarships 267,371 287,724 Land 43,774 - Inventory 40,300 _ 30,300 TOTAL NON CURRENT ASSETS 351,445 318,024 TOTAL ASSETS $4,220,641 3,909,362 LIABILITIES AND NET ASSETS CURRENT LIABILITIES Accounts payable $ 16,294 23,992 Deferred support 20,000 - - TOTAL CURRENT LIABILITIES 36,294 23,992 NET ASSETS Unrestricted 12,565 (47,856) Temporarily Restricted 1,747,543 2,108,987 Permanently Restricted 2,424,239 1,824,239 TOTAL NET ASSETS 4,184,347 3,885,370 TOTAL LIABILITIES AND NET ASSETS $4,220,641 3,909,362

See accompanying notes to financial statements

-3-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Statements of Activities

For the Year Ended March 31, 2011

Temporarily Permanently Unrestricted Restricted Restricted Total REVENUES: State matching revenue $ - 8,700 - 8,700 Contributions 8,145 108,449 - 116,594 In-kind donations - 53,500 - 53,500 Investment income 401 143,785 287,666 431,852 Net assets released from restrictions: Satisfaction of requirements 363,544 (675,878) 312,334 - __ TOTAL REVENUES 372,090 (361,444) 600,000 610,646

EXPENSES: Program Services: Scholarship programs $ 128,531 - - 128,531 College/program support 170,472 - - 170,472 Administrative and general 12,666 - - 12,666 TOTAL EXPENSES 311,669 - - 311,669

CHANGE IN NET ASSETS 60,421 (361,444) 600,000 298,977 NET ASSETS AT BEGINNING OF YEAR (47,856) 2,108,987 1,824,239 3,885,370 NET ASSETS AT YEAR END $ 12,565 1,747,543 2,424,239 4,184,347

See accompanying notes to financial statements

-4-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Statements of Activities

For the Year Ended March 31, 2010

Temporarily Permanently Unrestricted Restricted Restricted Total REVENUES: State matching revenue $ - 8,719 - 8,719 Contributions 16,484 178,884 - 195,368 In-kind donations 1,575 20,300 - 21,875 Investment income (loss) - 344,256 318,510 662,766 Net assets released from restrictions: Satisfaction of requirements 606,004 (287,494) (318,510) - __ TOTAL REVENUES 624,063 264,665 - 888,728

EXPENSES: Program Services: Scholarship program $ 182,089 - - 182,089 College/program support 404,756 - - 404,756 Administrative and general 40,109 - - 40,109 TOTAL EXPENSES 626,954 - - 626,954

CHANGE IN NET ASSETS (2,891) 264,665 - 261,774 NET ASSETS AT BEGINNING OF YEAR (44,965) 1,844,322 1,824,239 3,623,596 NET ASSETS AT YEAR END $ (47,856) 2,108,987 1,824,239 3,885,370

See accompanying notes to financial statements

-5-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Statements of Cash Flows

For the Years Ended March 31, 2011 and 2010

2011 2010 CASH FLOWS FROM OPERATING ACTIVITIES: Cash received from State matching $ 8,700 6,417 Cash received from contributions 116,964 192,498 Cash paid to suppliers and beneficiaries (339,350) (613,253) Investment income ___129,541 266,313 Net cash flows used in operating activities (84,145) (148,025) CASH FLOWS FROM INVESTING ACTIVITIES Net purchases/disposition of securities 57,570 188,587 (Acquisition) Disposition of prepaid scholarships 20,353 (287,724) Net cash flows provided by investing activities 77,923 (99,137) NET DECREASE IN CASH AND EQUIVALENTS (6,222) (247,162) CASH AND EQUIVALENTS, BEGINNING OF YEAR 49,007 _ 296,169 CASH AND EQUIVALENTS, END OF YEAR $ 42,785 49,007 Adjustments to reconcile changes in net assets to net cash flows from operating activities: Increase in net assets $ 298,977 261,774 Increase in market value of investments (346,138) (431,216) Change in assets and liabilities: Increase in other assets (53,774) - Decrease in accounts and other receivables 1,466 2,136 Decrease in prepaid expenses 3,022 5,580 Increase in accounts payable ___12,302 _ 13,701 Net cash flows used in operating activities $ (84,145) (148,025) Non Cash Transactions: In-Kind donation activities $ 53,500 21,875

See accompanying notes to financial statements

-6-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(1) Summary of Significant Accounting Policies

(a) Organization

Florida Keys Educational Foundation, Inc. (the “Foundation”) was incorporated as a non-profit organization on March 8, 1966, in the State of Florida and is a direct-support organization to Florida Keys Community College. On January 20, 2010, the Board approved the fictitious name of FKCC Foundation and such name was registered on February 17, 2010. The objectives of the Foundation are to encourage, solicit, receive and administer gifts, bequests of property and funds for scholarships and programs for the advancement of Florida Keys Community College and its objectives. The Foundation’s support comes primarily from donor contributions and governmental grants. Since the Foundation and College are physically located in the Florida Keys, donor support is primarily generated from sources connected in some manner with Monroe County, Florida. The accounting policies of the Foundation conform to accounting principles generally accepted in the United States of America. The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. The following is a summary of the more significant policies:

(b) Basis of Presentation The accompanying financial statements have been prepared on the

accrual basis of accounting. Net assets and revenues, expenses, gains, and losses are classified based on the existence or absence of donor-imposed restrictions. Accordingly, net assets of the Foundation and changes therein are classified and reported as follows:

• Unrestricted Net Assets – Net assets that are not

subject to donor-imposed stipulations.

• Temporarily Restricted Net Assets – Net assets subject to donor-imposed stipulations that may or will be met either by actions of the Foundation and/or the passage of time. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statements of activities as net assets released from restrictions.

-7-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(1) Summary of Significant Accounting Policies – (Cont.) (b) Basis of Presentation – (Cont.)

Permanently Restricted Net Assets – Net assets that are subject to donor-imposed stipulations that require they be maintained permanently by the Foundation and not used for operating purposes. Generally, the donors of these assets permit the Foundation to use all or part of the income earned on any related investments for specific purposes.

(c) Public Support and Revenue Contributions, including unconditional promises to give, are

recorded as made. All contributions are available for unrestricted use unless specifically restricted by the donor. Conditional promises to give are recognized when the conditions on which they depend are substantially met. Unconditional promises to give due in the next year are recorded at their net realizable value. Unconditional promises to give due in subsequent years are reported at the present value of their net realizable value, using risk-free interest rates applicable to the years in which the promises were received.

Grants and other contributions of cash and other assets are

reported as temporarily restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restrictions.

Endowment contributions and investments are permanently

restricted by the donor. Investment earnings available for distribution are recorded in temporarily restricted net assets.

Contributions of donated non-cash assets are recorded at their

fair values in the period received. Contributions of donated services that create or enhance non-financial assets or that require specialized skills, are provided by individuals possessing those skills, and would typically need to be purchased if not provided by donation, are recorded at their fair values in the period received.

-8-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(1) Summary of Significant Accounting Policies – (Cont.)

(d) Cash and Cash Equivalents

The Foundation considers all highly liquid investments with a

maturity of three (3) months or less when purchased to be cash equivalents.

(e) Income Tax Status

The Foundation is a non-profit organization that is exempt from income taxes under Section 501(c)(3) of the Internal Revenue Code. The Foundation has also been classified as an entity that is not a private foundation within the meaning of Section 509 (a) and qualifies for deductible contributions as provided in Section 170 (b)(1)(A)(vi). The Foundation has no excise or unrelated business income taxes for the years ended March 31, 2011 and 2010.

(f) Investments Investments are composed of direct investments in equity and

fixed income securities and are carried at fair value. Realized gains and losses are computed on the average cost method. Unrealized gains and losses are charged or credited to the statement of activities.

(g) Receivables Receivables are presented on the statement of financial position

net of an allowance for doubtful accounts based on the Foundation’s assessment of collectability. As of March 31, 2011 and 2010, the Foundation considered all receivables to be collectible and no allowances have been recorded.

-9-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(1) Summary of Significant Accounting Policies – (Cont.)

(h) Fair Values of Financial Instruments

The following method and assumptions were used by the Foundation in estimating the fair value disclosures for financial instruments:

Cash and cash equivalents, certificates of deposit, accounts

receivable, contributions receivables, interest receivable and payables - The carrying amounts reported in the statement of financial position approximate fair values due to relatively short maturities of these instruments.

Investments - The fair values of investments are based on

quoted market prices for those instruments. Pledged contribution receivable - The fair value of these

unconditional promises to give is estimated by discounting the future cash flows using a current risk-free rate of return, based on the yield of a U.S. Treasury security with a maturity date similar to expected collection period. Typically, this is the five (5) year treasury date.

Inventory - Inventories are stated at the fair value at the

date of donation. (2) Cash and Cash Equivalents and Investments

Cash and cash equivalents are composed of the following at March 31, 2011 and 2010:

2011 2010

Cash, Checking Account $ 42,785 49,007 $ 42,785 49,007

-10-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(2) Cash and Cash Equivalents and Investments - (Cont.) Deposits

Custodial Credit Risk - Custodial credit risk is the risk that in the event of a bank failure, the Foundation’s deposits may not be returned to it.

The Foundation maintains cash at financial institutions located in

Key West, Florida. The bank balances for the checking at March 31, 2011 are $42,090 and at March 31, 2010 of $68,600. Balances at the institution are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 for 2011 and 2010. Although the Foundation does not have a formal policy requiring collateralization, the financial institution has all depository accounts fully collateralized with a mortgage backed security pledged by the institution and held in safekeeping in their account at another financial institution.

Investments:

Credit Risk - The Foundation invests or previously invested in common stock, mutual funds, and other securities including those guaranteed by the United States of America. The investments are recorded at cost and adjusted to fair market value, i.e. quoted market price, as provided by the Foundation’s agent.

At year-end the Foundation’s investments are categorized to give an indication of the level of risk assumed by the entity. Level One investments are purchased at cost and adjusted to fair value. Level One consists of investments that have quoted prices in active markets for identical assets that the Foundation has the ability to access at March 31, 2011 and 2010. Level One investments are held by an institution on behalf of the Foundation and are insured under the Security Investors Protective Corporation (SPIC) up to $500,000, including up to $100,000 in cash. In addition, the institution together with certain affiliates, has purchased supplemental coverage. The insured amounts are limited to the total amounts held in the accounts to the lesser of cost or market.

-11-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(2) Cash and Cash Equivalents and Investments - (Cont.) Investments: - (Cont.)

Level One investments consisted of the following as of March 31,

2011 and 2010: March 31, 2011 ____________________________________ Unrealized Cost Fair Value Appreciation Cash and equivalents $ 19,844 19,844

Appreciation - Mutual Funds - Equities 1,909,421 2,195,186 285,765 Mutual Funds – Fixed Income 1,576,972 1,608,881 31,909 Total long-term investments $ 3,506,237 3,823,911 317,674 March 31, 2010 ____________________________________ Unrealized Cost Fair Value Appreciation Cash and equivalents $ 370 370 - Mutual Funds – Equities 1,765,201 1,811,743 46,542 Mutual Funds – Fixed Income 1,710,658 1,723,230 12,572 Total long-term investments $ 3,476,229 3,535,343 59,114

-12-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(2) Cash and Cash Equivalents and Investments - (Cont.)

The following schedule summarizes the investment return and its

classification in the statement of activities for the years ended March 31, 2011 and 2010:

March 31, 2011 ____________________________________ Temporarily Permanently Unrestricted Restricted Restricted __Total_ Dividends and interest $ 1,258 42,485 60,052 103,795 Advisor fees (242) (8,280) (11,461) (19,983) Realized gain(loss) on sale of Investments, net - 37,058 52,380 89,438 Unrealized gain on investments (615) 72,522 186,695 258,602 Net investment income $ 401 143,785 287,666 431,852 March 31, 2010 ____________________________________ Temporarily Permanently Unrestricted Restricted Restricted __Total_ Dividends and interest $ - 69,842 64,619 134,461 Advisor fees - (13,523) (12,512) (26,035) Realized gain(loss) on sale of Investments, net - 243,686 225,462 469,148 Unrealized gain on investments - 44,251 40,941 85,192 Net investment income $ - 344,256 318,510 662,766

-13-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(3) Fair Values of Financial Instruments

Financial Accounting Standards Board Statement No. 157, Fair Value Measurements (FASB) Statement No. 157), establishes a framework for measuring fair value. That framework provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy under FASB Statement No. 157 are described below:

• Level 1 -- Inputs to the valuation methodology are unadjusted quoted market prices for identical assets or liabilities in active markets that the Foundation has the ability to access.

• Level 2 -- Inputs to the valuation methodology includes quoted

prices for similar assets or liabilities in active markets; quoted prices for identical or similar assets or liabilities in inactive markets; inputs other than quoted prices that are observable for the asset or liability; inputs that are derived principally from or corroborated by observable market data by correlation to other means.

If the asset or liability has a specified (contractual) term, the Level 2 input must be observable for substantially the full term of the asset or liability.

• Level 3 -- Inputs to the valuation methodology are

unobservable and significant to the fair value measurement. The asset’s or liability’s fair value measurement within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. Valuation techniques used need to maximize the use of observable inputs and minimize the use of unobservable inputs. The following description of the valuation used for assets measured at fair value are as follows:

• Common Stocks, corporate bonds, mutual funds and U.S. government securities: -- value at closing market price reported on the active market which the individual securities are traded.

-14-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(3) Fair Values of Financial Instruments – (Cont.)

The methods described above may produce a fair value calculation that may not be indicative of net realizable value or reflective of future fair values. Furthermore, while the Foundation believes its valuation methods are appropriate and consistent with other market participants, the use of different methodologies or assumptions to determine fair value of certain financial instruments could result in a different fair value measurement at the reporting date. The Foundation investments meet Level 1 measurements as of March 31, 2011 and 2010.

(4) In-Kind Donations:

Donated Inventory The Foundation receives donations of land, boats, engines, marine equipment, supplies and materials for use in its educational programs or resale. These donations are recorded at their fair market value on the date given. During the two years ended March 31, 2011 and 2010, the Foundation received $43,000 and $30,300 in land and marine equipment, respectively. Total inventory at March 31, 2011 and 2010 amount to $84,074 and $30,300, respectively. Donated Services The Foundation receives donated services from employees of Florida Keys Community College who assist in the Foundation’s operations. No amounts have been recognized in the statement of activities as the criteria for recognition under SFAS No. 116 have not been satisfied. This income, if any, is reported on the statement of activities.

(5) Accounts Payable

Accounts payable as of March 31, 2011 and 2010, consisted of amounts due to various vendors of $16,294 and $23,992, respectively.

-15-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(6) Temporarily Restricted Net Assets

For investment purposes, the Foundation pools all of their assets. Each net asset class participates in the investment earnings or loss based on their proportionate share of the assets invested, except for those donors who specifically request not to participate. Due to a market decline, certain temporarily restricted balances became negative. The total amount of negative temporarily restricted accounts at March 31, 2011 and 2010, were $0 and $47,882, respectively.

Temporarily restricted net assets are available for the following purposes at March 31, 2011 and 2010:

2011 2010 Scholarship programs $ 973,698 860,003 College/program support 773,845 1,248,984

Total temporarily restrict net assets $1,747,543 2,108,987 Net assets were released from donor restrictions by incurring expenses satisfying the purpose specified by donors as follows:

2011 2010 Scholarship programs $ 128,531 182,089 College/program support 235,013 423,915

Total restrictions released $ 363,544 606,004

-16-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(7) Permanently Restricted Net Assets

Net assets were permanently restricted for the following purposes at March 31, 2011 and 2010:

2011 2010 Scholarship programs $1,118,354 1,118,354 College/program support 1,205,885 605,885 Operating endowment 100,000 100,000

Total permanently restricted net assets $ 2,424,239 1,824,239 Investment earnings from the endowments are reclassified as temporarily restricted to the respective programs as follows:

2011 2010 Scholarship programs $ 134,428 195,264 College/program support 141,217 105,787 Administration and general 12,021 17,459

Total investment earnings (loss) reclassified $ 287,666 318,510

(8) Endowment Fund Disclosures

In 2008, the Financial Accounting Standards Board (FASB) issued Staff Position No. FAS 117-1, Endowment of Not-for-Profit Organizations; Net Asset Classification of Funds Subject to an Enacted Version of the Uniform Prudent Management of Institutional Funds Act, and Enhanced Disclosures for All Endowment Funds. This FASB Staff Position (FSP) provides guidance on the net asset

-17-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(8) Endowment Fund Disclosures – (Cont.)

classification of donor restricted endowment funds for a not-for-profit organization that is subject to an enacted version of the Uniform Prudent Management of Institutional Funds Act of 2006 (UPMIFA) and is effective for fiscal years ending after December 15, 2008. UPMIFA is a model act approved by the Uniform Law Commission (ULC: formerly known as the National Conference of Commissioners on Uniform State Laws) that serves as a guideline for states to use in enacting legislation. This FSP also improves disclosures about the Foundation’s endowment funds (both donor restricted endowment funds and board designated endowment funds), whether or not the Foundation is subject to UPMIFA.

As of March 31, 2011 and 2010, the Foundation’s endowment included

15 and 14, respectively, individual funds established for the purposes of scholarships and college support. These funds include donor restricted endowment funds. As required by GAAP, net assets associated with endowment funds are classified and reported based on the existence or absence of donor imposed restrictions.

Interpretations of Relevant Law The Foundation’s Board has interpreted that the Foundation is not

subject to the Uniform Prudent Management of Institutional Funds Act under State law. However, the Foundation does follow guidelines of preservation of the fair value of the original gift as of the gift date of the donor restricted endowment funds absent explicit donor stipulations to the contrary. As a result, the Foundation classifies as permanently restricted net assets (a) the original value of gifts donated to the permanent endowment, (b) the original value of subsequent gifts to the permanent endowment, and (c) accumulations to the permanent endowment made in accordance with the direction of the applicable donor gift instrument at the time the accumulation is added to the fund. The remaining portion of the donor restricted endowment fund that is not classified in permanently restricted net assets is classified as temporarily restricted net assets until those amounts are appropriated for expenditure by the Foundation in a manner consistent with the standard or prudence described in the Act.

-18-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(8) Endowment Fund Disclosures – (Cont.)

In accordance with the Act, the Foundation considers the following

factors in making investment decisions for donor restricted endowment funds:

(1) The duration and preservation of the fund. (2) The purposes of the Foundation and the donor restricted

endowment. (3) General economic conditions. (4) The possible effect of inflation and deflation. (5) The expected total return from income and the appreciation of

investments. (6) Other resources of the Foundation. (7) The investment policies of the Foundation.

Spending Policy and How the Investment Objectives Rate to Spending Policy The Foundation’s policy is to not provide any distribution of its

endowment fund’s assets (corpus). In establishing this policy, the Foundation considered the long term expected return on its endowment. Accordingly, over the long term, the Foundation expects the current spending policy to allow its endowment to stay constant. This is consistent with the Foundation’s objective to maintain the purchasing power of the endowment assets held in perpetuity or for a specified term as well as to provide additional real growth through new gifts and investment return.

Risk Objectives and Risk Parameters The Foundation has adopted investment and spending policies for

endowment assets that attempt to provide a predictable stream of funding to programs supported by its endowment while seeking to maintain the purchasing power of the endowment assets. Endowment assets include those assets of donor restricted funds that the Foundation must hold in perpetuity for donor specified period(s). Under this policy, as approved by the Board of Directors, the endowment assets are invested in a manner that exceeds inflation while assuming a low level of investment risk. The Foundation expects its endowment funds, over time, to provide an average rate of return of approximately five percent (5%) annually. Actual returns in any given year may vary from this amount.

-19-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC.

Notes to Financial Statements

March 31, 2011 and 2010

(8) Endowment Fund Disclosures – (Cont.)

Strategies Employed for Achieving Objectives To satisfy its long term rate of return objectives, the Foundation

relies on a total return strategy in which investment returns are achieved through both capital appreciation (realized and unrealized) and current yield (interest and dividends). The Foundation targets a diversified asset allocation that places a greater emphasis on equity based investments to achieve its long term return objectives within prudent risk constraints.

Funds with Deficiencies From time to time, the fair value of assets associated with

individual donor restricted endowment funds may fall below the level that the donor requires the Foundation to retain as a fund of perpetual duration or the Uniform Prudent Management of Institutional Funds Act requires the Foundation to retain as a fund of perpetual duration. In accordance with GAAP, deficiencies of this nature are reported in temporarily restricted net assets. These deficiencies are the result of unfavorable market fluctuations that occurred after the investment of permanently restricted contributions.

-20-

SMITH, BUZZI & ASSOCIATES, LLC. CERTIFIED PUBLIC ACCOUNTANTS

2103 CORAL WAY, SUITE 305 MIAMI, FLORIDA 33145

TEL. (305) 285-2300 FAX (305) 285-2309

JULIO M. BUZZI, C.P.A. MEMBERS: JOSE E. SMITH, C.P.A. AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS FLORIDA INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE AND ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Board of Directors of Florida Keys Educational Foundation, Inc. D/B/A FKCC Foundation: We have audited the financial statements of Florida Keys Educational Foundation, Inc. (D/B/A FKCC Foundation) (a non-profit organization) as of and for the years ended March 31, 2011 and 2010 and have issued our report thereon dated May 17, 2011. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Internal Control Over Financial Reporting In planning and performing our audits, we considered Florida Keys Educational Foundation, Inc’s internal control over financial reporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Florida Keys Educational Foundation, Inc’s internal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of Florida Keys Educational Foundation Inc’s internal control over financial reporting.

-21-

A control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects Florida Keys Educational Foundation, Inc’s ability to initiate, authorize, record, process, or report financial data reliably in accordance with generally accepted accounting principles such that there is more than a remote likelihood that a misstatement of Florida Keys Educational Foundation, Inc’s financial statements that is more than inconsequential will not be prevented or detected by Florida Keys Educational Foundation, Inc’s internal control. A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement of the financial statements will not be prevented or detected by Florida Keys Educational Foundation Inc’s internal control. Our consideration of internal control over financial reporting was for the limited purpose described in the first paragraph of this section and would not necessarily identify all deficiencies in internal control that might be significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over financial reporting that we consider to be material weaknesses or significant deficiencies, as defined above.

Compliance As part of obtaining reasonable assurance about whether the Foundation’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts and grants, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit and, accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance that are required to be reported under Government Auditing Standards. This report is intended for the information and use of the Board of Directors, management and others deemed appropriate and is not intended to be and should not be used by anyone other than these specified parties.

May 17, 2011

-22-

FLORIDA KEYS EDUCATIONAL FOUNDATION, INC. (D/B/A FKCC FOUNDATION)

MANAGEMENT LETTER

MARCH 31, 2011

SMITH, BUZZI & ASSOCIATES, LLC.

CERTIFIED PUBLIC ACCOUNTANTS 2103 CORAL WAY, SUITE 305

MIAMI, FLORIDA 33145 TEL. (305) 285-2300 FAX (305) 285-2309

JULIO M. BUZZI, C.P.A. MEMBERS: JOSE E. SMITH, C.P.A. AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS FLORIDA INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS

May 17, 2011 Board of Directors Florida Keys Educational Foundation, Inc.: We have audited the financial statements of Florida Keys Educational Foundation, Inc., for the year ended March 31, 2011, and have issued our reports thereon dated May 17, 2011. We conducted our audit in accordance with United States generally accepted auditing standards and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. We have issued our Independent Auditors Report; Independent Auditors’ Report on Internal Control Over Financial Reporting and Other Matters based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards. Disclosures in those reports, which are dated May 17, 2011, should be considered in conjunction with this management letter. However, this letter does not affect the reports listed above. In planning and performing our audit of the financial statements of Florida Keys Educational Foundation, Inc. as of and for the year ended March 31, 2011, in accordance with auditing standards generally accepted in the United States of America, we considered its internal control over financial reporting as a basis for designing our audit procedures for the purpose of expressing our opinion on the financial statements but not for the purpose of expressing an opinion on the effectiveness of the internal control structure. A control deficiency exists when the design or operation of a control does not allow management or employees in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis. A significant deficiency is a control deficiency or a combination of control deficiencies, that adversely affects the ability to initiate, authorize, record, process or report financial data reliably in accordance with generally accepted accounting principles such that there is more than a remote likelihood that a misstatement of the financial statements that is more than inconsequential will not be prevented or detected by Florida Keys Educational Foundation, Inc.’s internal control.

Board of Directors Florida Keys Educational Foundation, Inc. May 17, 2011 Page 2 A material weakness is a significant deficiency that results in more than the remote likelihood that a material misstatement of the financial statements will not be prevented or detected by the Florida Keys Educational Foundation, Inc.’s internal control. Our consideration of the internal control structure was limited for the purpose described in the third paragraph and would not necessarily indentify all matters in the internal control structure that might be significant deficiencies or material weaknesses. However, we noted no matters involving internal control structure and its operation that we consider to be material weaknesses or significant deficiencies as defined above. During our audit, we noted certain matters involving the internal control structure and other operational matters that are presented for your consideration. These comments and recommendations, all of which have been discussed with the appropriate members of management, are intended to improve the internal control structure or result in other operating efficiencies and are summarized in Exhibit I. This letter is intended solely for the information and use of the Board of Directors, management, and others within Florida Keys Educational Foundation, Inc. We would like to take this opportunity to express our appreciation for the courtesy and cooperation extended to us by the employees of Florida Keys Educational Foundation, Inc. during the course of our audit. We shall be pleased to discuss, at your convenience, the comments presented in this letter and provide any assistance that you may require for the implementation of our recommendations.

Very truly yours,

SMITH, BUZZI & ASSOCIATES, LLC.

EXHIBIT I 1. FINDING

During the audit and the review of operating internal controls, it was noted that Florida Keys Educational Foundation, Inc., operates in an environment, where the separation of incompatible duties over cash management and financial reporting is not fully possible due to limited staffing. However, we noted that satisfactory policies exist to create oversight to mitigate potential weaknesses resulting from this observation.

RECOMMENDATION

We recommend that constant attention be paid to internal controls and methods of creating oversight where possible because of the limited staffing of the Florida Keys Education Foundation, Inc.

MANAGEMENT RESPONSE

We concur with the finding and recommendation. Because of limited staffing, the Board has directed the Investment Committee to take a proactive role in monitoring financial statements, bank reconciliations and payables.

2. FINDING

During the audit and in conjunction with management, it was noted that a formal disaster recovery plan has not been adopted. We did note that information was backed up in a reasonable manner, including the back up of information onto the servers of the Florida Keys Community College. However, offsite storage of back ups was not current. The organization does have a copy of the college’s disaster recovery plan (Information Technology Emergency Plan). The organization has located similar software and hardware to recover accounting information in the event of a disaster. However, the back up software/ hardware are the personal computers of the Executive Director. Although the accounting software used is readily available, the version they are using is older and the chart of accounts is very specific in nature. Accordingly, significant effort would be required if the operating software were destroyed and only data backups existed.

RECOMMENDATION

We recommend that information be backed up in a more timely manner, using a hierarchy of backup methods including on-line offsite storage that will also have software backup in case of a catastrophic event at the College.

-1-

MANAGEMENT RESPONSE

We concur with the finding and recommendation. The Foundation will insure that Foundation files are adequately backed up.

3. FINDING

During the audit and in conjunction with management, it was noted that the organization has not adopted a formal records retention policy. A significant amount of paper and records are processed maintained and stored.

RECOMMENDATION

We recommend that a careful review be made of record retention requirements and that a policy be adopted that maintains records for specified periods of time and provides for their adequate and safeguarded destruction after that specified period. Retention periods should be appropriate for the various types of records. Some records may be permanent, while others have statutory retention requirements (such as taxes). A reasonable retention policy provides for legal and tax protection; affords convenience and aids in records retrieval and maximizes use of limited storage space.

MANAGEMENT RESPONSE

We concur with the finding and recommendation. The Foundation will develop a records retention policy.

4. FINDING

The Foundation has policies and procedures and they are documented. However, the manual has not been updated in over a year. The manual discusses the accounting policies but does not detail each step. In addition, the manual does not contain an update timeline page that would reflect last update and nature of such.

RECOMMENDATION

We recommend that the manual in place be expanded to include detailed and enumerated accounting steps to ensure that in the absence of the executive director, the procedures followed are exact. This will ensure the recording of activity on a consistent basis which enhances the data’s reliability. We further recommend that the organization adopt a policy of reviewing the manual on a semi-annual basis and that updates be logged onto a timeline sheet maintained with the manual to provide evidence of changes and last review date(s)

MANAGEMENT RESPONSE

We concur with the finding and recommendation.

-2-

Smith, Buzzi & Associates, LLC2103 Coral Way Suite 305 Miami, FL 33145

FLORIDA KEYS EDUCATIONALFOUNDATION, INC.5901 COLLEGE ROAD KEY WEST, FL 33040

August 10, 2011

CONFIDENTIAL

FLORIDA KEYS EDUCATIONALFOUNDATION, INC.5901 COLLEGE ROAD KEY WEST, FL 33040

Dear :

We have prepared the following returns from information provided by you without verification or audit.

We suggest that you examine these returns carefully to fully acquaint yourself with all items contained therein to ensure that there are no omissions or misstatements.

Federal Filing Instructions

Your Form 990 for the year ended 3/31/11 shows no balance due. The return should be signed and dated on Page 1 by an officer representing the organization. Mail the return by November 15, 2011 to:

Department of the TreasuryInternal Revenue Service CenterOgden, UT 84201-0027

If a private delivery service is used, mail to:OSPC1973 N. Rulon White Blvd.Ogden, UT 84404

Also enclosed is any material you furnished for use in preparing the returns. If the returns are examined, requests may be made for supporting documentation. Therefore, we recommend that you retain all pertinent records for at least seven years.

In order that we may properly advise you of tax considerations, please keep us informed of any significant changes in your financial affairs or of any correspondence received from taxing authorities.

If you have any questions, or if we can be of assistance in any way, please call.

Sincerely,

Smith, Buzzi & Associates, LLC

Return of Organization Exempt From Income Tax (Form 990)

Smith, Buzzi & Associates, LLC2103 Coral Way Suite 305

Miami, FL 33145305-285-2300

August 10, 2011

CONFIDENTIAL

FLORIDA KEYS EDUCATIONALFOUNDATION, INC.5901 COLLEGE ROAD KEY WEST, FL 33040

For professional services rendered in connection with the preparation of the following tax forms for year ending 3/31/11.

$ 0.00Amount due

Smith, Buzzi & Associates, LLC2103 Coral Way Suite 305

Miami, FL 33145305-285-2300

FLORIDA KEYS EDUCATIONALFOUNDATION, INC.5901 COLLEGE ROAD KEY WEST, FL 33040

Department of the TreasuryInternal Revenue Service CenterOgden, UT 84201-0027

Other expenses (Part IX, column (A), lines 11a–11d, 11f–24f) . . . . . . . . . . . . . . . . . . . . . . . . .Total expenses. Add lines 13–17 (must equal Part IX, column (A), line 25) . . . . . . . . . . . . .

Gross receipts

Check if applicable:For the 2010 calendar year, or tax year beginning

Application pending

City or town, state or country, and ZIP + 4

Amended return

Terminated

Room/suiteNumber and street (or P.O. box if mail is not delivered to street address)Initial return

Name change

Address changeName of organization

The organization may have to use a copy of this return to satisfy state reporting requirements.Internal Revenue ServiceDepartment of the Treasury

OMB No. 1545-0047Form

Telephone numberE

Employer identification numberDCB, and endingA

benefit trust or private foundation) Open to PublicUnder section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung

Return of Organization Exempt From Income Tax 2010990Inspection

Doing Business As

G $F Name and address of principal officer:

H(a)

H(b)

H(c)

Is this a group return for affiliates?

Are all affiliates included?If "No," attach a list. (see instructions)

Group exemption number

Yes No

NoYes

IJK

Tax-exempt status:

Website: Form of organization:

501(c) 4947(a)(1) or 527( ) (insert no.)

Corporation Trust Association Other L Year of formation: M State of legal domicile:SummaryPart I

1

234567ab

Briefly describe the organization's mission or most significant activities:

Check this box Number of voting members of the governing body (Part VI, line 1a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Number of independent voting members of the governing body (Part VI, line 1b) . . . . . . . . . . . . . . . . . . . . . . . . . .Total number of individuals employed in calendar year 2010 (Part V, line 2a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total number of volunteers (estimate if necessary) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total unrelated business revenue from Part VIII, column (C), line 12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Net unrelated business taxable income from Form 990-T, line 34 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7b

7a6543

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .if the organization discontinued its operations or disposed of more than 25% of its net assets.

89

101112

Contributions and grants (Part VIII, line 1h) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Program service revenue (Part VIII, line 2g) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Investment income (Part VIII, column (A), lines 3, 4, and 7d) . . . . . . . . . . . . . . . . . . . . . . . . . .Other revenue (Part VIII, column (A), lines 5, 6d, 8c, 9c, 10c, and 11e) . . . . . . . . . . . . . . . .Total revenue – add lines 8 through 11 (must equal Part VIII, column (A), line 12) . . . . . .

Prior Year Current Year

13141516a

b171819

Grants and similar amounts paid (Part IX, column (A), lines 1–3) . . . . . . . . . . . . . . . . . . . . .Benefits paid to or for members (Part IX, column (A), line 4) . . . . . . . . . . . . . . . . . . . . . . . . . .Salaries, other compensation, employee benefits (Part IX, column (A), lines 5–10) . . . . . .Professional fundraising fees (Part IX, column (A), line 11e) . . . . . . . . . . . . . . . . . . . . . . . . . .Total fundraising expenses (Part IX, column (D), line 25) . . . . . . . . . . . . . . . . . . . . . . . . . . .

Revenue less expenses. Subtract line 18 from line 12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

202122

Beginning of Current Year End of YearTotal assets (Part X, line 16) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total liabilities (Part X, line 26) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Net assets or fund balances. Subtract line 21 from line 20 . . . . . . . . . . . . . . . . . . . . . . . . . . . .

DAAForm 990 (2010)

SignHere

PaidPreparerUse Only

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it istrue, correct, and complete. Declaration of preparer (other than officer) is based on all information of which preparer has any knowledge.

Signature of officer Date

Type or print name and title

CheckPreparer's signature Date PTINself-employed

Firm's name Firm's EIN

Firm's address Phone no.

For Paperwork Reduction Act Notice, see the separate instructions.

Part II Signature Block

May the IRS discuss this return with the preparer shown above? (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . NoYes

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Act

iviti

es &

Gov

erna

nce

Rev

enue

Expe

nses

Net A

sset

s or

Fund

Bala

nces

501(c)(3)

ifPrint/Type preparer's name

04/01/10 03/31/11FLORIDA KEYS EDUCATIONALFOUNDATION, INC.FKCC FOUNDATION

5901 COLLEGE ROAD

KEY WEST FL 33040

59-6173174

305-809-3299

SAME AS ABOVE

610,646

X

Xhttp://www.fkcc.edu

X FL

TO PROVIDE FINANCIAL AND OTHER ESSENTIAL SUPPORT TO FURTHER THE MISSION ANDGOALS OF FLORIDA KEYS COMMUNUITY COLLEGE.

141200

0

225,962 178,794

662,766 431,852

888,728 610,646182,089 128,531

444,865 183,138626,954 311,669261,774 298,977

3,909,362 4,220,64123,992 36,294

3,885,370 4,184,347

ROGER MCVEIGH TREASURER BOARD OF DIRECTORS

JULIO BUZZI 08/10/11 P00853282

Smith, Buzzi & Associates, LLC 80-06319352103 Coral Way Suite 305Miami, FL 33145 305-285-2300

X

596173174 08/10/2011 3:41 PM

Form 990 (2010) Page 2Part III Statement of Program Service Accomplishments

1 Briefly describe the organization's mission:. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Did the organization undertake any significant program services during the year which were not listed on the2prior Form 990 or 990-EZ? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .If "Yes," describe these new services on Schedule O.

3

4

Did the organization cease conducting, or make significant changes in how it conducts, any programservices? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .If "Yes," describe these changes on Schedule O.Describe the exempt purpose achievements for each of the organization's three largest program services by expenses. Section501(c)(3) and 501(c)(4) organizations and section 4947(a)(1) trusts are required to report the amount of grants and allocations toothers, the total expenses, and revenue, if any, for each program service reported.

4a (Code: . . . . . . . ) (Expenses $ . . . . . . . . . . . . . . . . . . . . . . . including grants of$ . . . . . . . . . . . . . . . . . . . . . . . ) (Revenue $ . . . . . . . . . . . . . . . . . . . . . . . ). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

)$ . . . . . . . . . . . . . . . . . . . . . . .(Revenue)$ . . . . . . . . . . . . . . . . . . . . . . .including grants of$ . . . . . . . . . . . . . . . . . . . . . . .) (Expenses(Code: . . . . . . .4b

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .