domestic tourism and saa pricing - amazon web...

TRANSCRIPT

Private and Confidential

Domestic Tourism and SAA Pricing

August 2012

YOUR LOGO Page 2

Domestic Market Share

5 years ago… Current…

Source SAA RCT report

SAA market share has reduced due to: • short-haul travel commoditisation; • stronger competition; and • low GDP growth restricting market growth .

YOUR LOGO

Domestic Operating Enviroment

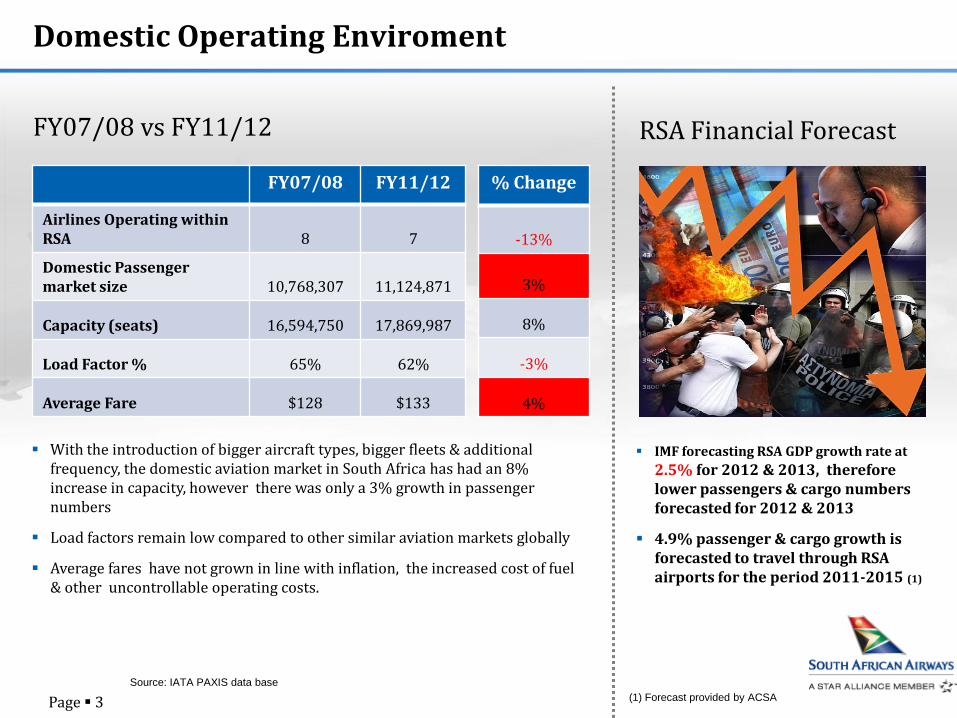

FY07/08 vs FY11/12

FY07/08 FY11/12

Airlines Operating within RSA 8 7

Domestic Passenger market size 10,768,307 11,124,871

Capacity (seats) 16,594,750 17,869,987

Load Factor % 65% 62%

Average Fare $128 $133

% Change

-13%

3%

8%

-3%

4%

Source: IATA PAXIS data base

With the introduction of bigger aircraft types, bigger fleets & additional frequency, the domestic aviation market in South Africa has had an 8% increase in capacity, however there was only a 3% growth in passenger numbers

Load factors remain low compared to other similar aviation markets globally

Average fares have not grown in line with inflation, the increased cost of fuel & other uncontrollable operating costs.

RSA Financial Forecast

IMF forecasting RSA GDP growth rate at 2.5% for 2012 & 2013, therefore lower passengers & cargo numbers forecasted for 2012 & 2013

4.9% passenger & cargo growth is forecasted to travel through RSA airports for the period 2011-2015 (1)

(1) Forecast provided by ACSA Page 3

YOUR LOGO

Private and Confidential

SAA’s Domestic Passenger Profile

SAA’s passengers profile is divided amongst the following:

Corporate

Government

Leisure

VFR

International Connecting Passengers

SAA has the following distribution channels:

Online via flysaa.com

Direct Call Centre Payment through credit card or through Pick ‘n Pay stores (nationally)

City Town Offices in Johannesburg, Durban and Cape Town

Airport Offices: JNB, CPT, DUR, PLZ, ELS, BFN, KIM, PTG, MQP, GRJ, RCB

National Travel Agencies

National Tour operators

Page 4

YOUR LOGO

CLASS BASIC ONE WAY FARE

Y 1240

M 1080

K 920

H 760

Q 600

V 450

L 300

G 220

e.g.

Business Travelers Leisure Travelers

Currently 40%

Wants frequency

Books closer to departure time

Inflexible (wants specific time)

Currently 60%

Price sensitive, search all airlines for cheapest price

Books in advance

Flexible (Time)

Pricing Strategy is driven by passenger demand

Designs “fare products”

Sets fare levels

Page 5

YOUR LOGO

Private and Confidential

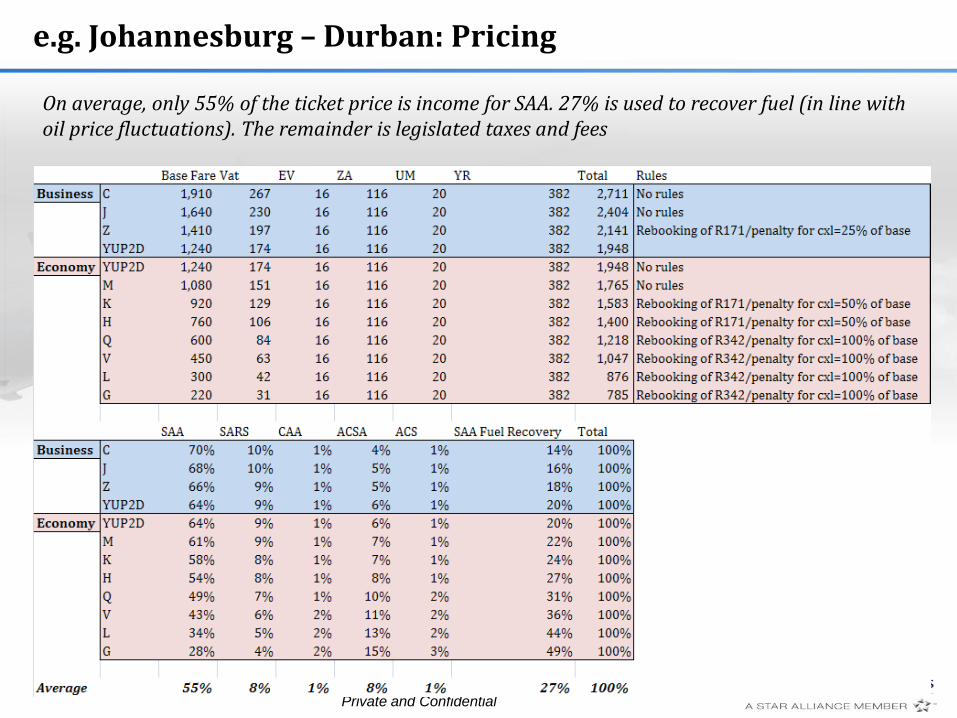

e.g. Johannesburg – Durban: Pricing

Page 6

On average, only 55% of the ticket price is income for SAA. 27% is used to recover fuel (in line with oil price fluctuations). The remainder is legislated taxes and fees

YOUR LOGO

SAA operates two airline brands: SAA; and Mango.

SAA Cargo supports the passenger business to promote trade.

SAA Technical and Air Chefs provide services to a range of international airlines.

SA Travel Centre sells SA destination travel products.

SAA is very clear on its mandate and strategic objectives as a State Owned Company, which include new route development, enabling tourism and creating employment in the economy.

Our Corporate Plan is targeting strong growth.

SAA is seeking to strengthen its tourism sectoral growth role and relationship with SA Tourism.

SAA Group

Premium airline Low cost airline Cargo airline/division

Aircraft engineering In-flight catering Retail travel franchises

SAA Already Plays a Strong Role in South African Tourism

All SAA businesses strongly support the tourism sector

Page 7

YOUR LOGO

SAA Already Plays a Strong Role in South African Tourism

SAA has a major catalytic demand¹ effect on the tourism sector

SAA’s activity has four distinct channels of effect

Direct impacts: activity and scale growth in the aviation sector, e.g. airport infrastructure development, airport retail.

Indirect impacts: acitivity supporting non-aviation tourism infrastructure development, e.g. car rental, hotels, ground transport, tours.

Induced impacts: activity (consumption and investment) generated by those directly/indirectly benefiting from aviation activity.

Consumer welfare impacts: general benefits to South Africans from increased tourism access.

¹ Catalytic demand models (e.g. International Civil Aviation Organisation, US Department of Transport and Oxford Economics) are a key part of any holistic analysis of the benefits of aviation activity. They also form a major element of SAA’s support for New Growth Path, beyond its direct employment and KPI’s agreed with DPE in the Shareholder’s Compact.

Page 8

YOUR LOGO

Current Challenges Facing the Aviation Sector in SA

Higher fuel costs with some volatility increases price of ticket

Fuel is approximately 1/3 of an airline’s operating costs

The Brent price moved above USD 115 per barrel.

Fuel is priced in USD, so airlines must manage commodity price and exchange rate risk.

Fuel price increases can only be partially recovered via passenger and cargo fuel levies.

Brent price Jan 2006 to July 2012. Source: World Bank

Page 9

YOUR LOGO

Current Challenges Facing the Aviation Sector in SA

High airport charges

South Africa’s airports are already high cost by global standards

In competitive developed market airport models, there is an element of negotiation with airlines (prior to construction) and there are alternative airports.

Airport charges increases: 129% from 2010 to 2015.

Airport charges are recovered by airlines through higher fares.

Page 10

YOUR LOGO

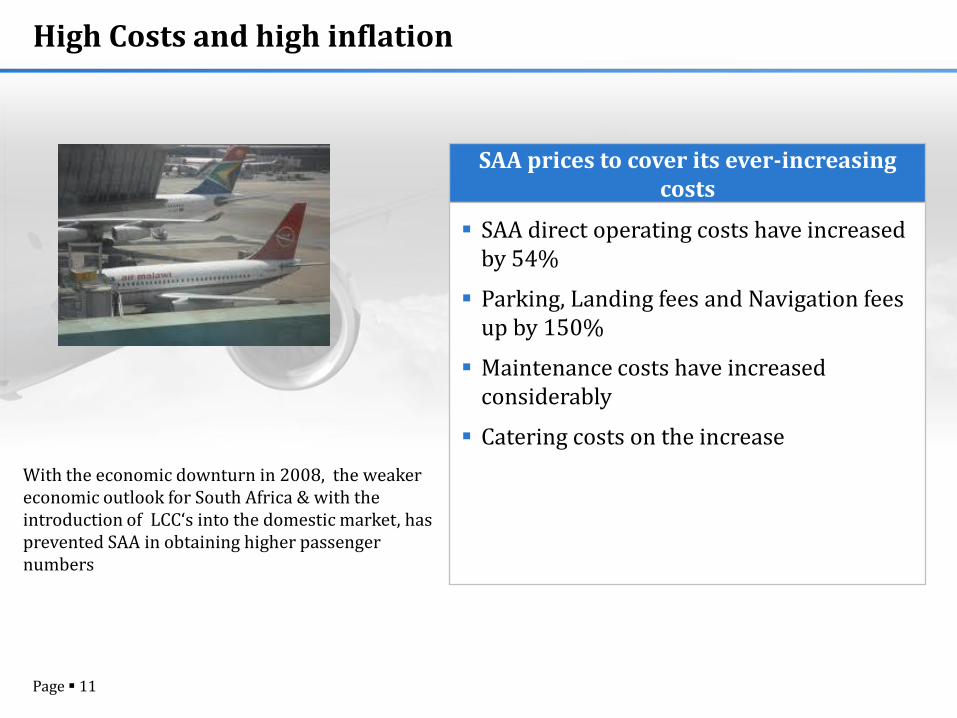

High Costs and high inflation

SAA prices to cover its ever-increasing costs

SAA direct operating costs have increased by 54%

Parking, Landing fees and Navigation fees up by 150%

Maintenance costs have increased considerably

Catering costs on the increase

With the economic downturn in 2008, the weaker economic outlook for South Africa & with the introduction of LCC‘s into the domestic market, has prevented SAA in obtaining higher passenger numbers

Page 11

YOUR LOGO

Private and Confidential

Domestic Statistics

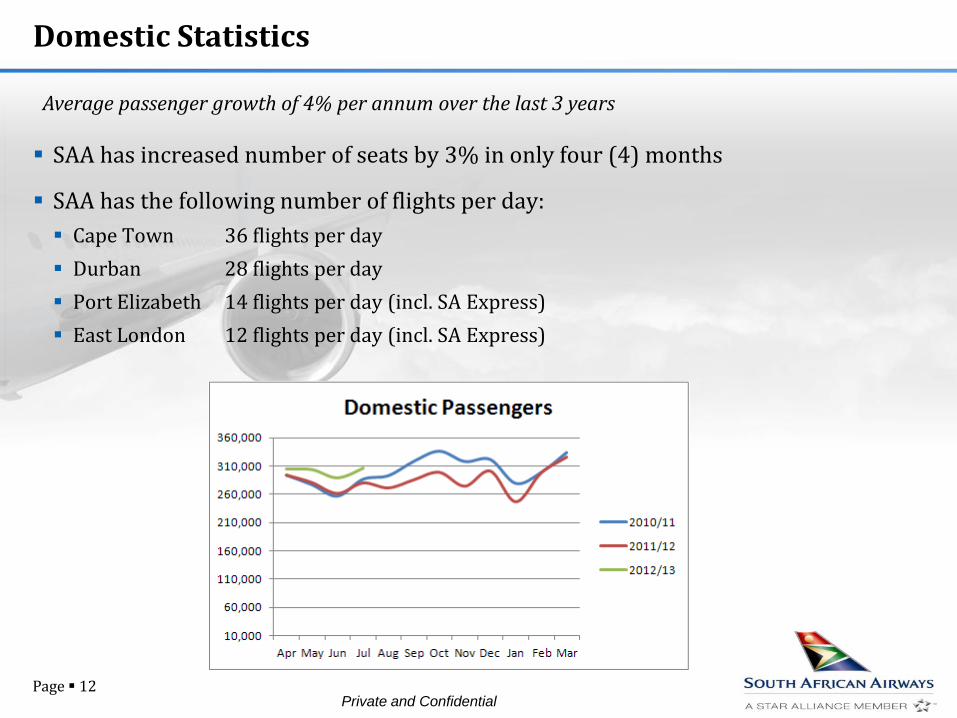

SAA has increased number of seats by 3% in only four (4) months

SAA has the following number of flights per day:

Cape Town 36 flights per day

Durban 28 flights per day

Port Elizabeth 14 flights per day (incl. SA Express)

East London 12 flights per day (incl. SA Express)

Average passenger growth of 4% per annum over the last 3 years

Page 12

YOUR LOGO

Private and Confidential

Domestic Tactical Promotions

Page 13

However, SAA is competitive in the domestic market. Examples of marketing campaigns using the SAA newsletter

YOUR LOGO

Private and Confidential

Domestic Tactical Promotions

Page 14

Examples of marketing campaigns using the SAA newsletter

Fly from Johannesburg to Beijing from R7004* book now London from R7350* book now Mumbai from R4522* book now Hong Kong from R8458* book now Durban from R685** book now Dubai from R6734* book now (operated by our codeshare partner Emirates)

31649 seats available

Quote booking code: ws19jan12

Book now on www.flysaa.com or through the SAA Call Centre on 0861 606 606

YOUR LOGO

Private and Confidential

Domestic Tactical Promotions

Page 15

National newspaper marketing

YOUR LOGO

Private and Confidential

Domestic Tactical Promotions

Page 16

Selling Cape Town through our package division – SAA Holidays

YOUR LOGO

Private and Confidential

Domestic Tactical Promotions

Page 17

Selling Durban through our package division – SAA Holidays

YOUR LOGO

Private and Confidential

Domestic Tactical Promotions

Page 18

Selling Johannesburg & Limpopo through our package division – SAA Holidays

YOUR LOGO

Private and Confidential

Questions?

Page 19