corporate presentation pt garuda indonesia (persero) tbk · 0 corporate presentation pt garuda...

TRANSCRIPT

0

Corporate Presentation PT Garuda Indonesia (Persero) Tbk

DAIWA ASEAN Conference – IDX: Best of Indonesia 2013 Tokyo, 21 – 22 October 2013

Delivering Indonesia’s Best to the World

1

Agenda

1. Industry Overview

2. Company Overview

3. Recent Developments

4. 1H-2013 Performance

IMPORTANT DISCLAIMER:

Information contained in this document has been prepared from several sources and the Company does not confirm the accuracy and completeness of such data, particularly where the data is sourced from outside the Company. In addition, any forward looking

statements are subject to change as a result of market conditions and the final result may be different to that indicated. The Company makes no representation or warranty of any type whatsoever on the accuracy or completion of the information contained herein.

2

1. Industry Overview

3

Agenda

1.4 billion

Asia Pacific will have the biggest air passenger traffic volume

2009 2030

Source: Airport Development, IATA

4.9 billion

1.4 billion

2.7 billion

1.5 billion

2.4 billion

1.1 billion

0.4 billion

0.2 billion

0.4 billion

4

(50)

-

50

100

150

200

250

300

-

200

400

600

800

1,000

Indonesia Thailand Malaysia Singapore Philippines Vietnam Brunei Darussalam

Cambodia

GDP Population

-1.8 -0.2 -0.1 0.3 0.9

1.7 1.7 2.0 2.0 2.5 2.5 2.8 2.8 2.9 3.0 3.4

4.4 5.6

6.3

7.8

Ital

y

Fran

ce

Euro

pea

n U

nio

n

Ger

man

y

Un

ited

Kin

gdo

m

Can

ada

Un

ited

Sta

tes

Jap

an

Sou

th A

fric

a

Bra

zil

Ru

ssia

n F

eder

atio

n

Arg

enti

na

Ko

rea

Mex

ico

Au

stra

lia

Turk

ey

Sau

di A

rab

ia

Ind

ia

Ind

on

esia

Ch

ina

‘In terms of its fundamentals, INDONESIA IS IN A STRONG POSITION from which to navigate through current global macroeconomic uncertainties’ (IMF country report, Sep 2012)

Value in %

IMF predicts until 2017 Indonesia will enjoy the highest economic growth as compared to its ASEAN peers

Indonesia is the biggest economy in ASEAN

Source: The World Bank 2012 data, accessed in Oct 2013

Indonesia: 2nd Fastest GDP Growth among G20 countries in 2013

Source: IMF-World Economic Outlook, July 2013

USD billion Million people

5

Outlook of the Indonesia’s economy until 2030 is promising

current 2030

16th-largest economy in the world

7th-largest

45 million

members of the consuming class

135 million

55 million

skilled workers in the Indonesian economy

113 million

$ 0.5 trillion market opportunity

in consumer services, agriculture &

fisheries, resources, & education

$ 1.8 trillion

53% of the population in cities producing

71%

74% of GDP 86%

6

1.2 1.3 1.6

1.9 2.2 2.3

3.0 3.5 3.6

3.8 4.1

4.4 4.8

5.1 5.6

Source: IMF, World Economic Outlook (WEO), Apr 2013; World Bank

Indonesia: GDP per capita

Most populous country in the South East Asia (4th largest in the world) with people distributed across a number of medium - large cities and high density provinces

Largest archipelago in the world lending greater importance to air travel; potential for taking market-share from land / sea travel

Most populated cities in the region

Medan 2.0 million

Kuala Lumpur 1.6 million

Petaling 1.5 million

Jakarta & surrounding area 12.0 million

Singapore 4.6 million

Manila 1.7 million

Surabaya 2.6 million

Ujung Pandang 1.2 million

Indonesia : Unique opportunity within Asia

Sources: Bloomberg, Sep’ 2013

By Air

By Rail

By Sea

37.4

194.1

3.4

2008 71.2

202.2

2.8

2012 +17.5%

+1.0%

-4.7%

CAGR

Monthly traffic statistic 2005-May 2013

Indonesia: Transportation profile (in million)

7

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F 2014F 2015F

Premium Budget Traveler GA Pax

Indonesia is forecast to enjoy a solid air traffic growth for the next three years after a robust economic growth outlook

Domestic and International market size to grow at CAGRs of 15% and 10%, respectively, from 2004 – 2012 GA’s Domestic and international market share expected to reach 34.4% and 25.9% in 2015, respectively, up from 21.5% and 15.1% in 2012

28.8

43.8 51.6

60.0

71.2

94.1

108.3

34.0 39.2 37.4

23.8

81.9

Domestic Market Size (million)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F 2014F 2015F

Business Leisure GA Pax

30.0

11.0 10.7 11.3 13.2

14.8 16.2 18.9

21.7 23.7

25.7 27.9

International Market Size (million)

Note: GA Pax, S-100 seater & Alliance Sources : Dephub, PT. AP I & II, IATA, PATA, Ministry Transportation, Garuda Forecast

8

Indonesia

Malaysia

Australia

In terms of air traffic, Indonesia has much room to grow

5.4

39 (722%)

Population

Air Traffic

Singapore

7.2

42 (583%)

Hong Kong

22.8

81 (355%)

Numbers are in million

63.1

171 (271%)

UK

29.0

48 (166%)

94.9 * (39%)

Sources: IATA, CAPA – Jun 2013 * DepHUb, IATA, PATA

9

Some Major Airport Development Project 2013 - 2018

Morotai Rp 150bn, 2014

Medan Rp 1.6tn, 2013

Majalengka Rp 8.3tn, 2018

Yogyakarta Rp 3.7tn, 2018

Samarinda Rp1.2tn, 2015

Balikpapan Rp 1.6tn, 2014

Denpasar Rp2.1 tn, 2013

Jakarta Rp8.4 tn, 2014 Surabaya

Rp 530bn, 2014

Data source : PT. Angkasa Pura I & II, Ministry of Transportation, Investor Daily

Development project plan for 10 airports reach approximately USD 2,8 billion.

Berau Rp 450bn, 2013

10

• Government priority to develop and improved Airport and Aviation Infrastructures in Indonesia

• High competition in LCC domestic segment • High competition in FSC and LCC international

segment

• 2015: ASEAN Open Sky Policy

• Robust demand in domestic traffic • Growing international tourist traffic, by locals

and foreigners

• Strong Economic Growth • Large population • Low air travel penetration

In Summary : Indonesia has Large Market & Big Opportunity for Air Travel

Market

Traffic

Policy

Infrastructure

Competition

11

2. Company Overview

12

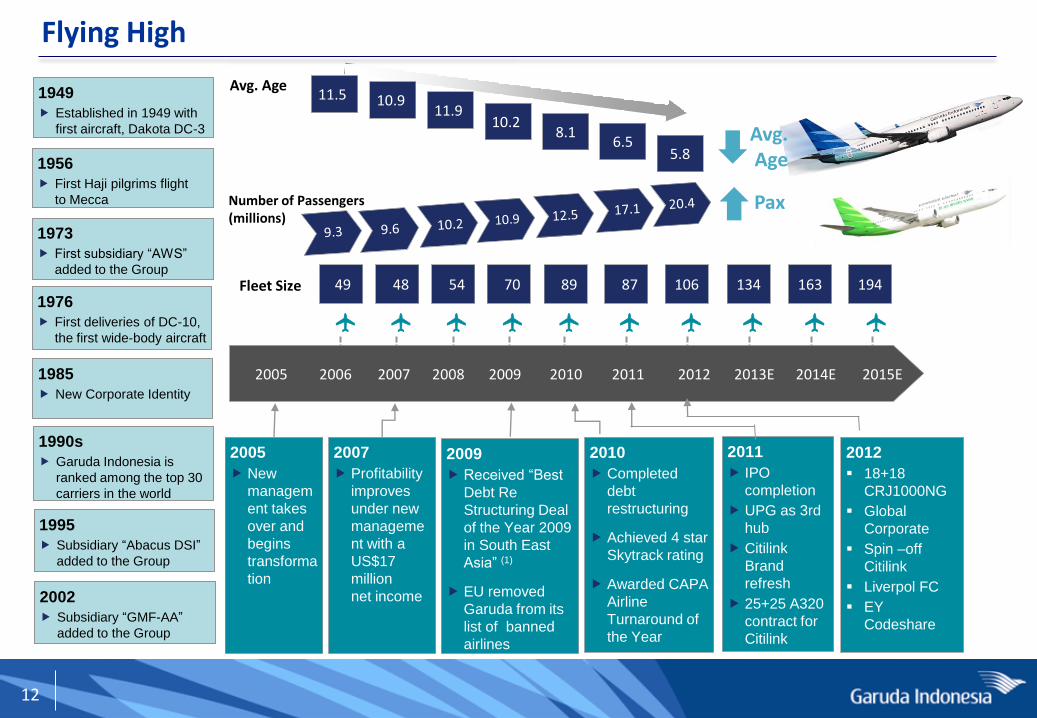

Flying High

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E

1956

First Haji pilgrims flight

to Mecca

1976

First deliveries of DC-10,

the first wide-body aircraft

1973

First subsidiary “AWS”

added to the Group

1949

Established in 1949 with

first aircraft, Dakota DC-3

1990s

Garuda Indonesia is

ranked among the top 30

carriers in the world

2010

Completed

debt

restructuring

Achieved 4 star

Skytrack rating

Awarded CAPA

Airline

Turnaround of

the Year

2005

New

managem

ent takes

over and

begins

transforma

tion

2007

Profitability

improves

under new

manageme

nt with a

US$17

million

net income

2009

Received “Best

Debt Re

Structuring Deal

of the Year 2009

in South East

Asia” (1)

EU removed

Garuda from its

list of banned

airlines

Avg. Age

Fleet Size 49 48 54 70 89 134 163 87 194 106

Number of Passengers (millions)

2011

IPO

completion

UPG as 3rd

hub

Citilink

Brand

refresh

25+25 A320

contract for

Citilink

1985

New Corporate Identity

1995

Subsidiary “Abacus DSI”

added to the Group

2002

Subsidiary “GMF-AA”

added to the Group

11.5 10.9 11.9

10.2 8.1

6.5 5.8

2012

18+18

CRJ1000NG

Global

Corporate

Spin –off

Citilink

Liverpol FC

EY

Codeshare

Avg. Age

Pax

13

World Airline Awards – Global Airline Rankings

2013 Rank

Airline 2012 Rank

2011 Rank

1 Emirates 8 10

2 Qatar Airways* 1 1

3 Singapore Airlines* 3 2

4 ANA All Nippon Airways * 5 11

5 Asiana Airlines* 2 3

6 Cathay Pacific Airways* 4 4

7 Etihad Airways 6 6

8 Garuda Indonesia 11 19

9 Turkish Airlines 7 9

10 Qantas Airways 15 8

11 Lufthansa 14 15

12 EVA Air 13 16

13 Virgin Australia 12 32

14 Malaysia Airlines* 10 12

15 Thai Airways International 9 5

16 Swiss Int’l Air Lines 18 13

17 Korean Air 16 24

18 Air New Zealand 17 7

19 Hainan Airlines* 20 23

20 Air Canada 19 21

Since embarking on a transformation plan in 2005, GIAA has greatly improved its global and regional rankings and won several international accolades in recognition of its quality performance

* Airlines with 5-star skytrax rating

World’s Best Economy Class 2013

Best Economy Class Airline Seat 2013

GA quality has been perceived better from year to year

World Best Economy Class

2013 Rank

Airline 2012 Rank

1 Garuda Indonesia 4

2 Asiana Airlines* 3

3 Singapore Airlines* 1

4 Qatar Airways* 2

5 ANA All Nippon Airways * 5

6 Cathay Pacific Airways* 9

7 Turkish Airlines 7

8 Emirates n/a

9 Oman Air n/a

10 Qantas Airways n/a

34 Awards in 1H13: - DOM: 23 awards - INT’L: 11 awards

14

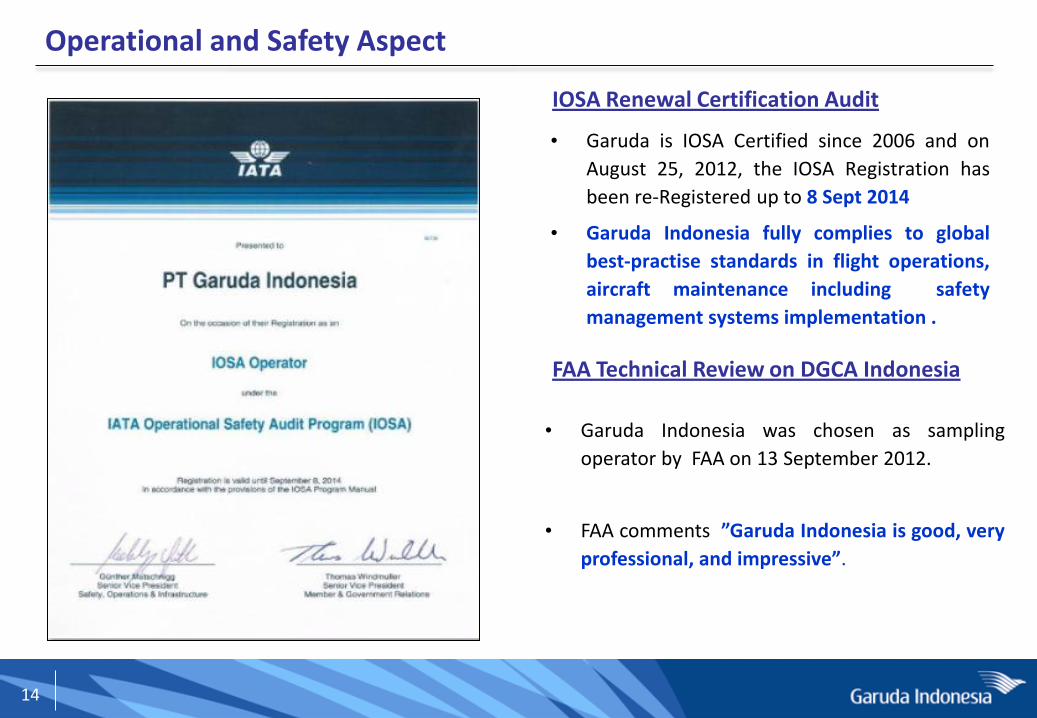

IOSA Renewal Certification Audit

• Garuda is IOSA Certified since 2006 and on

August 25, 2012, the IOSA Registration has

been re-Registered up to 8 Sept 2014

• Garuda Indonesia fully complies to global

best-practise standards in flight operations,

aircraft maintenance including safety

management systems implementation .

• Garuda Indonesia was chosen as sampling

operator by FAA on 13 September 2012.

• FAA comments ”Garuda Indonesia is good, very

professional, and impressive”.

FAA Technical Review on DGCA Indonesia

Operational and Safety Aspect

15

Domestic

Grow and dominate

full-service

International

Enormous upside

potential

2

Fleet

Expand, simplify and

rejuvenate Fleet

4

Brand

Stronger brand, better

product and services

5

LCC

Citilink to address the

LCC Opportunity

3 Human Capital

Right quality and

right quantity

7

Cost Discipline

Efficient in cost structure compared to

peers

6

Quantum Leap – 7 Strategies to Drive Growth

Management focuses on implementing the “Quantum Leap” with 7 main strategies to expand and dominate the Indonesian aviation market.

1

16

2005 Growth 2012 Growth 2015

Number of Aircraft 57 86% 106 83% 194

Average age (yr) 11.2 -48% 5.8 -14% 5

ASK/employee (000) 3,761 40% 5,250 56% 8,210

Passenger Carried 9.3 mio 119% 20.4 mio 123% 45.4 mio

Frequency/week 765 213% 2,400 242% 8,198

Skytrax Rating 3 star + 4 star + 5 star

Aiming to complete the 2nd journey in 2015

5 star skytrax airlines : 1. Asiana Airlines 2. Cathay Pacific Airways 3. Hainan Airlines 4. Qatar Airways 5. Singapore Airlines 6. Malaysia Airlines 7. All Nippon Airways

"The key factor behind 5-Star status is an airline's ability to deliver a truly consistent and high quality of Product and Service. A great product standard is not by itself the key to a 5-Star Airline ranking, and Skytrax focus deeply on the Quality of front-line service an airline provides. A 5-Star Airline ranking is centred on identifying airlines whose front-line staff (across the airport and onboard experience) deliver a true and consistent 5-Star standard of service delivery." Sources: skytrax website http://www.airlinequality.com/StarRanking/5star.htm

17

3. Recent Development

18

Garuda Indonesia Group 2012

IT Services

Aero

Systems

Hospitality

and Tourism

Aerowisata

Global

Distribution

Systems

Abacus

Ground

Handling

Gapura

Angkasa

MRO

Services

GMF

AeroAsia

Key Subsidiaries & Associated Companies

Cargo

Domestic Feeder

Hajj / Charter

International

Low Cost

Carries

Citilink

Indonesia

83%

8%

9%

Ops Revenue Contribution 2012

Scheduled Airlines Non-scheduled Airlines Others

19

5.31 5.34

1.7 1.9

Jan-Jun 2012 Jan-Jun 2013 Others GA Int'l

16.1 16.5

0.7 1.9 6.4

7.2

Jan-Jun 2012 Jan-Jun 2013 Others Citilink GA Dom

1.8 2.1

2.4 2.4 2.5 3.0 3.2 3.3 3.1 3.3 3.5 3.5 3.4 3.8 22%

24%

26% 25%

26%

29% 29% 29%

28% 28% 28% 29% 28.6% 27%

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Total GA Passengers (in million) Market Share

0.5

0.6 0.7 0.6 0.7 0.8 0.8 0.8 0.8 0.9 0.9 0.9 0.9 0.95 18%

20% 20% 21%

22% 23% 23% 24% 24%

25% 24% 24%

26% 25.5%

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Total GA Passengers (in million) Market Share

Competition on routes which GA flies – per Jun 2013

Source: Airport Authority & GA (traffic in/out CGK, DPS, SUB, UPG airports)

Garuda Domestic Passengers in/out Selected Airports Garuda International Passengers in/out Selected Airports

GA International Market Share 1H13: 25.7% incr. 1.6 ppts GA Domestic Market Share 1H13: 28.0% incr. 0.3 ppts

Traffic in million passenger Traffic in million passenger 7.2 7.0

0.5%

8.1%

2.3% 25.5 23.2

2.7%

11.1%

9.9%

162.3%

20

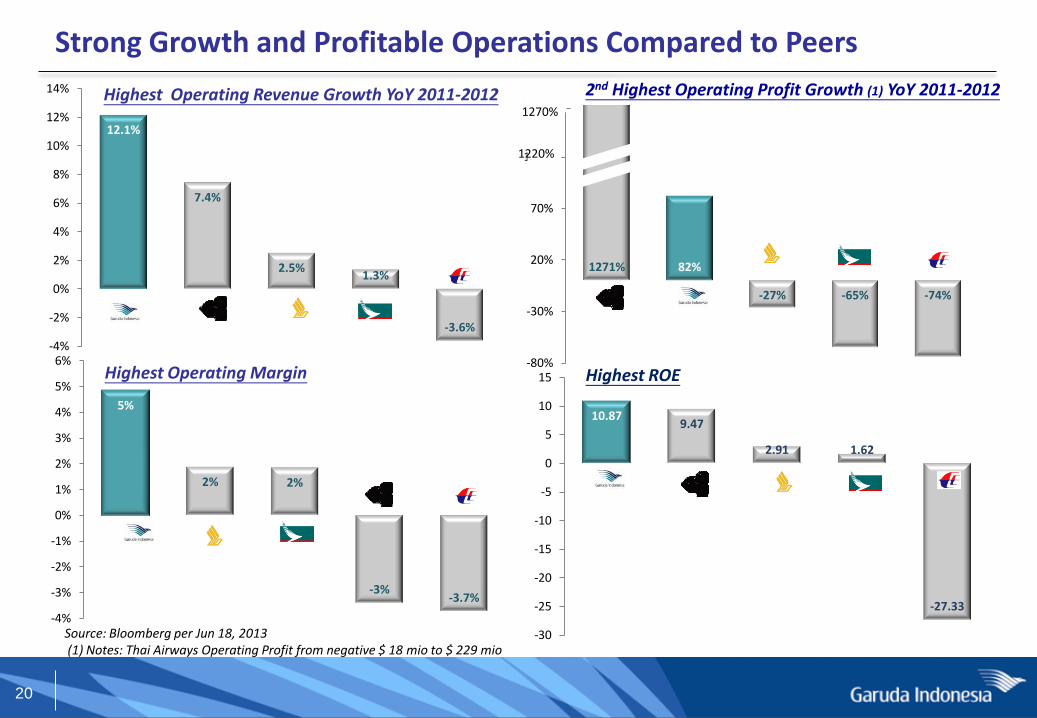

1271% 82%

-27% -65% -74%

-80%

-30%

20%

70%

120%

170%

10.87 9.47

2.91 1.62

-27.33

-30

-25

-20

-15

-10

-5

0

5

10

15

5%

2% 2%

-3% -3.7%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

12.1%

7.4%

2.5% 1.3%

-3.6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Strong Growth and Profitable Operations Compared to Peers

Source: Bloomberg per Jun 18, 2013 (1) Notes: Thai Airways Operating Profit from negative $ 18 mio to $ 229 mio

Highest Operating Revenue Growth YoY 2011-2012 2nd Highest Operating Profit Growth (1) YoY 2011-2012

Highest Operating Margin Highest ROE

12 1270%

12 1220%

21

Milestones 1H - 2013

• New Boards Members were appointed by the AGM

• Signing Agreement ALAFCO & Garuda Indonesia for Financing of 2 aircraft B777-300ER with Sharia principles

APR

• Garuda Indonesia named “The World’s Best Economy Class” by Skytrax at Paris Airshow

• Fully repaid the US$ 55 million syndicated – commercial loan from Citi Club Deal

• Welcome the 1st Delivery of Boeing 777-300ER aircraft

JUN

• New Destinations: Tanjung Pandan (Belitung) & Bengkulu

• Introduced Immigration On Board on the Shanghai – Jakarta service MAY

• Broaden flight network to 6 New destinations in Europe & Middle East (Frankfurt, Brussel, Milan, Dusseldorf, Munich, Bahrain) that served by Etihad Airways

• Extended “Immigration on Board” Agreement JAN

• “2012 Domestic Airlines of The Year” from Ray Morgan Research, Australia

• “ASEAN Premium Airline of The Year” from Frost & Sullilvan, USA MAR

•Garuda Indonesia and General Electric (NYSE:GE) launched the CFM56-7B engine shop capability for the Garuda Maintenance Facility (GMF AeroAsia) FEB

22

Introduced New Service Concepts 2 July 2013

Fly Liverpool FC for the LFC Tour 2013 17 July 2013

Moved from Polonia Airport to Kuala Namu International Airport - Medan

25 July 2013

Welcome the 2nd delivery of B777-300ER 31 July 2013

Recent Developments

Operation

Funding

IDR Bond: Listing in Indonesia Stock Exchange 8 July 2013

Garuda’s New Destinations: • Cengkareng – Bengkulu • Cengkareng – Tanjung Pandan • Medan – Penang • Cengkareng – Tanjung Pinang • Balikpapan – Berau

15 May 2013 15 May 2013 1 June 2013 3 Aug 2013 1 Aug 2013

88 Extra Flights during Eid-ul Fitr 5-16 Aug 2013

Network

23

4. 1H-2013 Performance

24

Indicator 1H13 Achievement D% YoY

11.9 million 23.4

172,262 tons 30.4

75.3 % 0.5 *

US$c 9.1 (3.5)

USD 1,725.4 million 14.1

USD 1,448.2 million 13.7

USD 14.3 million (0.6)

-USD 10.7 million n/a

1H-2013 Highlights

• Operating Indicator figures are for Garuda Indonesia and Citilink • Financial Indicator figures are for Garuda Indonesia Group • * in percentage points

Passenger Carried

Cargo Uplifted

Passenger Yield

Operating Revenue

Passenger Revenue

Operating Income

Income for the Period

Seat Load Factor

DOMESTIC

• Continued growth in traffic & capacity • Impacted by weakening IDR/USD

INTERNATIONAL

• Improved operational performance • Welcoming First B777-300ER

CITILINK

• Improved operational performance • Improved domestic market share • At an early stage of Investment

FINANCIAL

• Fully Repaid USD 55 million Citi Club Deal-1

25

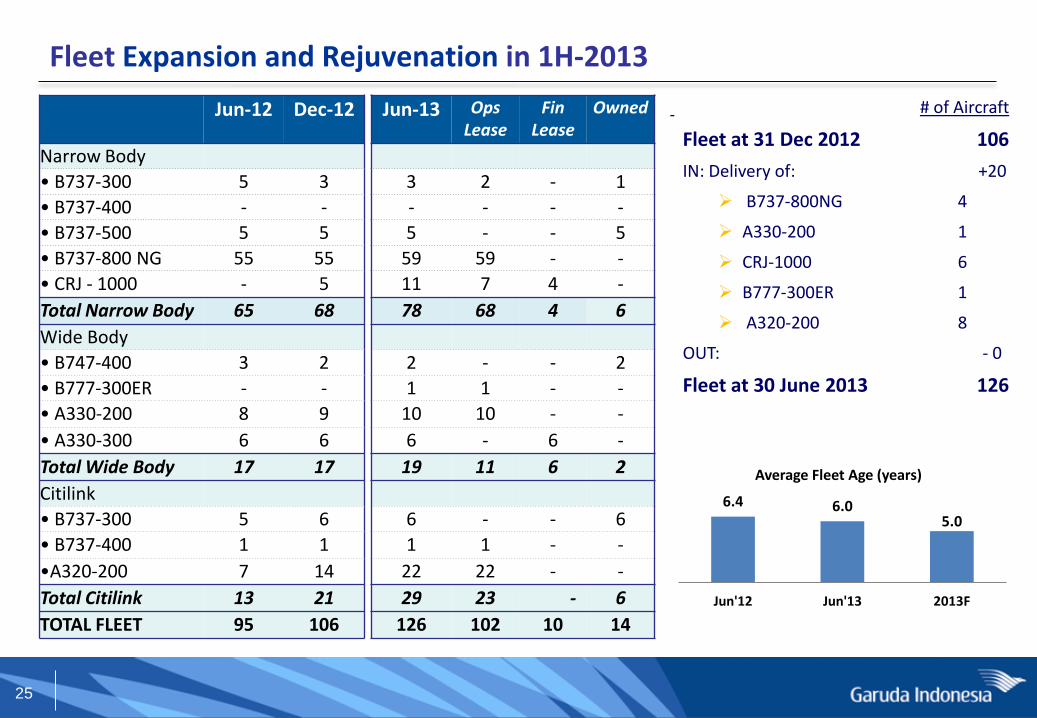

Fleet Expansion and Rejuvenation in 1H-2013

# of Aircraft

Fleet at 31 Dec 2012 106

IN: Delivery of: +20

B737-800NG 4

A330-200 1

CRJ-1000 6

B777-300ER 1

A320-200 8

OUT: - 0

Fleet at 30 June 2013 126

6.4 6.0 5.0

Jun'12 Jun'13 2013F

Average Fleet Age (years)

Jun-12 Dec-12 Jun-13 Ops Lease

Fin Lease

Owned

Narrow Body

• B737-300 5 3 3 2 - 1

• B737-400 - - - - - -

• B737-500 5 5 5 - - 5

• B737-800 NG 55 55 59 59 - -

• CRJ - 1000 - 5 11 7 4 -

Total Narrow Body 65 68 78 68 4 6

Wide Body

• B747-400 3 2 2 - - 2

• B777-300ER - - 1 1 - -

• A330-200 8 9 10 10 - -

• A330-300 6 6 6 - 6 -

Total Wide Body 17 17 19 11 6 2

Citilink

• B737-300 5 6 6 - - 6

• B737-400 1 1 1 1 - -

•A320-200 7 14 22 22 - -

Total Citilink 13 21 29 23 - 6

TOTAL FLEET 95 106 126 102 10 14

26

1H12 1H13 ∆ % YoY

Aircraft Utilization (Hours) 10:47 11:00 0:13

Frequencies 72,693 93,198 28.2

On Time Performance (%) 85.3 86.9 1.6 *

ASK (’000) 17,775,764 20,881,690 17.5

Average Fuel Price (USD/L) 0.92 0.88 (4.3)

Fuel Burn / ATK 0.251 0.250 (0.2)

Fuel Burn / Blockhours 4,053 3,481 (14.1)

Passenger Carried 9,617,568 11,869,439 23.4

RPK (‘000) 13,291,314 15,721,097 18.3

Seat Load Factor (%) 74.8 75.3 0.5 *

Passenger Yield (US¢) 9.4 9.1 (3.5)

Cargo/Mail Uplifted (Ton) 132,062 172,262 30.4

CASK (US¢) 7.9 7.5 (4.4)

CASK-excl Fuel (US¢) 4.6 4.4 (4.2)

Operating Indicators - Group

Notes: All figures include GA & Citilink, except aircraft Utilization and OTP are for GA Main Brand only * in percentage points

Operational

Passenger & Cargo

Financial

Efficiency

27

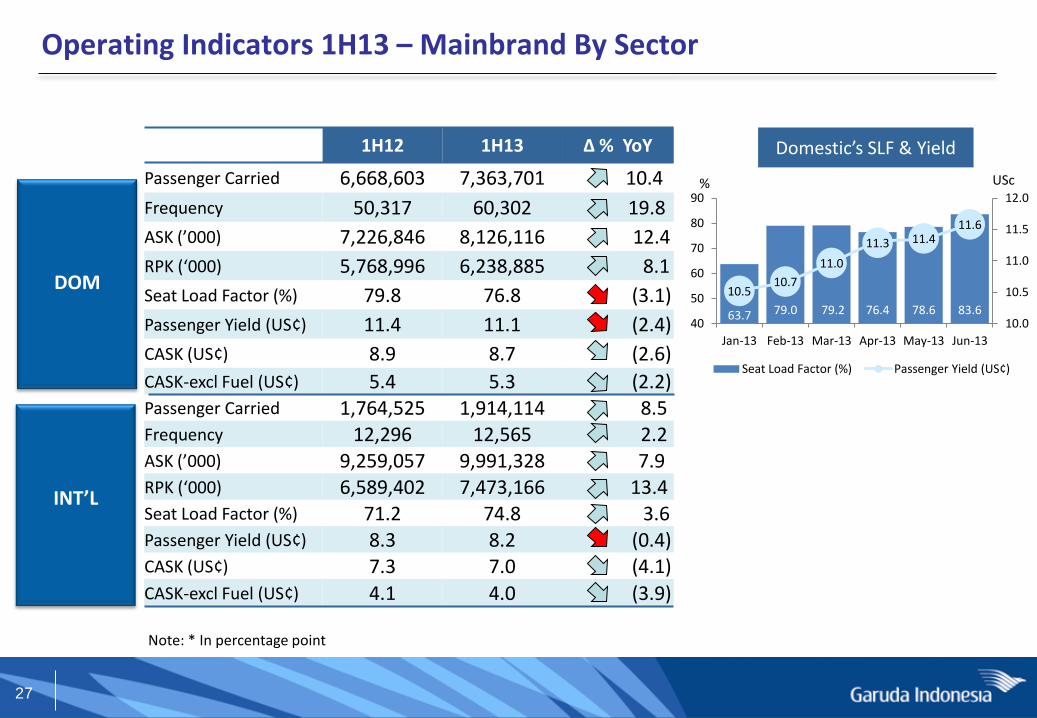

1H12 1H13 ∆ % YoY

Passenger Carried 6,668,603 7,363,701 10.4

Frequency 50,317 60,302 19.8

ASK (’000) 7,226,846 8,126,116 12.4

RPK (‘000) 5,768,996 6,238,885 8.1

Seat Load Factor (%) 79.8 76.8 (3.1)

Passenger Yield (US¢) 11.4 11.1 (2.4)

CASK (US¢) 8.9 8.7 (2.6)

CASK-excl Fuel (US¢) 5.4 5.3 (2.2) Passenger Carried 1,764,525 1,914,114 8.5 Frequency 12,296 12,565 2.2 ASK (’000) 9,259,057 9,991,328 7.9 RPK (‘000) 6,589,402 7,473,166 13.4 Seat Load Factor (%) 71.2 74.8 3.6 Passenger Yield (US¢) 8.3 8.2 (0.4) CASK (US¢) 7.3 7.0 (4.1) CASK-excl Fuel (US¢) 4.1 4.0 (3.9)

Operating Indicators 1H13 – Mainbrand By Sector

DOM

INT’L

Note: * In percentage point

Domestic’s SLF & Yield

63.7 79.0 79.2 76.4 78.6 83.6

10.5 10.7

11.0

11.3 11.4 11.6

10.0

10.5

11.0

11.5

12.0

40

50

60

70

80

90

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13

Seat Load Factor (%) Passenger Yield (US¢)

% USc

28

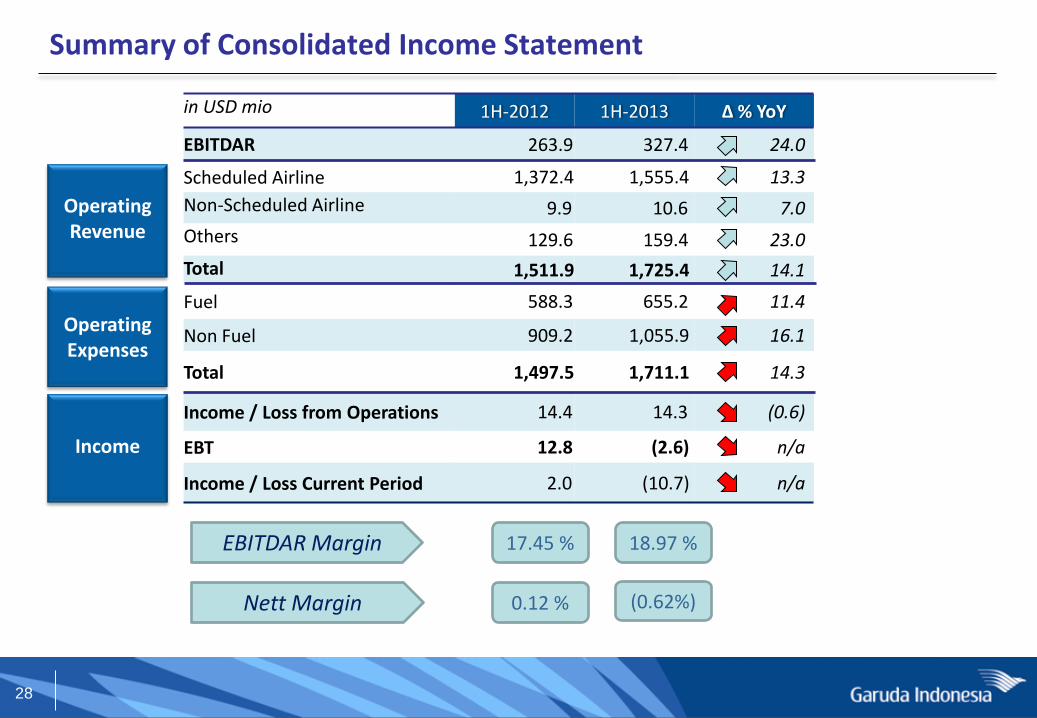

in USD mio 1H-2012 1H-2013 ∆ % YoY

EBITDAR 263.9 327.4 24.0

Scheduled Airline 1,372.4 1,555.4 13.3

Non-Scheduled Airline 9.9 10.6 7.0

Others 129.6 159.4 23.0

Total 1,511.9 1,725.4 14.1

Fuel 588.3 655.2 11.4

Non Fuel 909.2 1,055.9 16.1

Total 1,497.5 1,711.1 14.3

Income / Loss from Operations 14.4 14.3 (0.6)

EBT 12.8 (2.6) n/a

Income / Loss Current Period 2.0 (10.7) n/a

Summary of Consolidated Income Statement

Operating Revenue

Operating Expenses

Income

EBITDAR Margin

Nett Margin

17.45 % 18.97 %

0.12 % (0.62%)

29

in USD mio 1H-2012 1H-2013 ∆ % YoY

Scheduled Airline 1,372.7 1,430.3 4.2

Non-Scheduled Airline 9.9 10.6 7.0

Others 40.3 34.3 (14.8)

Total 1,423.0 1,475.2 3.7

Fuel 545.4 576.4 5.7

Non Fuel 872.3 855.2 (2.0)

Total 1,417.7 1,431.6 1.0

Income / Loss from Operations 5.2 43.6 736.0

EBT 3.2 28.4 778.4

Income / Loss Current Period (4.9) 20.9 525.2

Summary of Income Statement – Parent Company only

Operating Revenue

Operating Expenses

Income

30

in USD mio 31 Dec 2012 30 Jun 2013 ∆ %

Current Assets 636.6 655.4 3.0

Non-Current Assets 1,881.4 2,139.4 13.7

Total Assets 2,518.0 2,794.8 11.0

Current Liabilities 754.2 916.4 21.5

Non-Current Liabilities 648.8 774.1 19.3

Total Liabilities 1,403.0 1,690.5 20.5

Total Equities 1,115.0 1,104.3 (1.0)

Total Liabilities & Equities 2,518.0 2,794.8 11.0

Summary of Consolidated Balance Sheet

Asset

Liabilities

Equities

Lease Adjusted Net Debt/EBITDAR

Debt/Equity

4.7 x

0.7 x

4.4 x

0.6 x

31

in USD mio 30 Jun 2012 30 Jun 2013 ∆ % YoY

Beginning Cash/Cash Equivalents 417.3 325.8 (21.9)

•Operating Activities 122.6 111.6 (9.0)

•Investing Activities (242.2) (314.2) 29.7

•Financing Activities (36.9) 166.5 551.6

Net Increase (Decrease) in Cash/Cash Equivalents (156.4) (36.0) 77.0

Effect of Foreign Exchange Rate Changes (9.7) (5.9) 39.5

Ending Cash/Cash Equivalents 251.1 283.9 13.0

Summary of Consolidated Cash Flow

Operating Activities

Increased on interest & financial charges paid and income taxes paid

Investing Activities

USD 349.7 million was the payment for PDP & Maintenance Reserve Fund

USD 27.4 million was the payment for Security Deposit

USD 118.2 million was the refund of PDP and Maintenance Reserve Fund

Financing Activities

New Loan: $ 321.8 million Payment of long-term Loan & Bank

Loan: $ 153.3 million

32

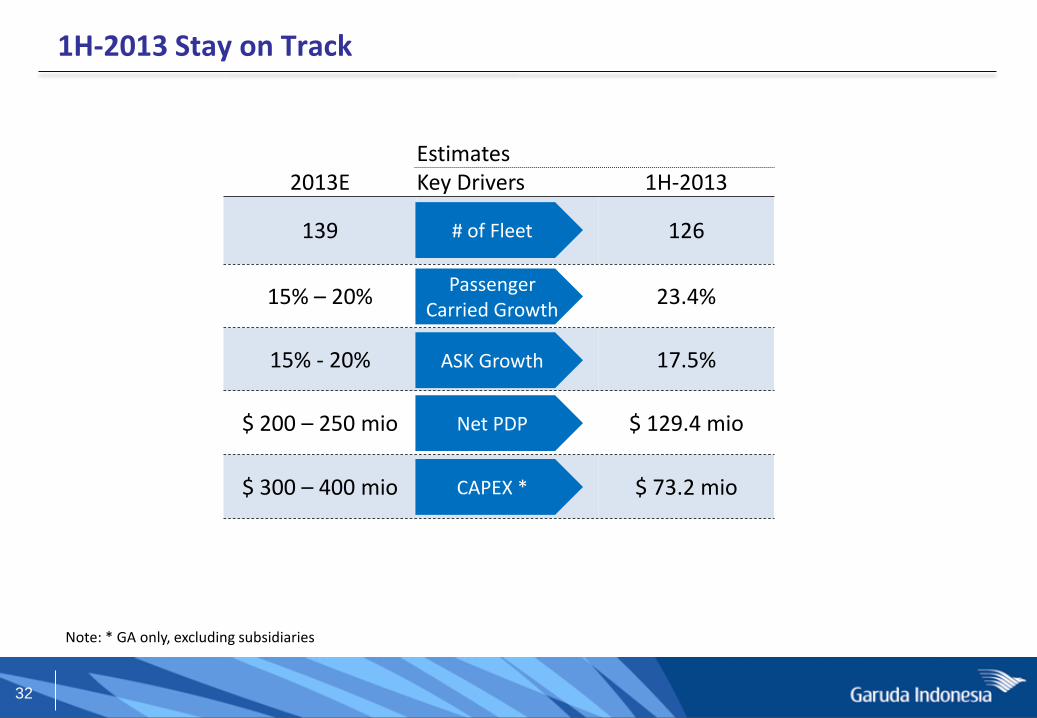

1H-2013 Stay on Track

Estimates 2013E Key Drivers 1H-2013

139 126

15% – 20% 23.4%

15% - 20% 17.5%

$ 200 – 250 mio $ 129.4 mio

$ 300 – 400 mio $ 73.2 mio

# of Fleet

Passenger Carried Growth

ASK Growth

CAPEX *

Net PDP

Note: * GA only, excluding subsidiaries

33

PT Garuda Indonesia (Persero) Tbk. Investor Relations Department 2nd Floor Management Building Garuda City Soekarno Hatta International Airport Phone : 62-21-2560 1201 Email : [email protected]

THANK YOU