analyst meeting pt garuda indonesia (persero) tbk · 1 analyst meeting pt garuda indonesia...

TRANSCRIPT

1

ANALYST MEETING PT GARUDA INDONESIA (PERSERO) Tbk.

9M2015 Result AnnouncementJakarta, 23 October 2015

2

1. Company Profile 3 – 8

2. Operational Performance 9 – 13

3. Financial Performance 14 – 20

4. Subsidiaries 21 – 23

Agenda Hal

Picture’s source: www.google.com

List of Shareholders as of 30 Sept 2015GIAA & JCI

Notes

Av. liquidity (IDR/day)

9M-2014

1.8 bio

9M-2015

4.2 bio

Av. close price (IDR) 453 482

Av. volume (shares/day) 3.9 mio 8.6 mio

Market cap (IDR) 10.7 trillion 7.9 trillionReal free float 15% - excluding Government of Indonesia and Trans Airways ownerships.

Share Performance

GIAA (RHS) JCI (LHS)

3

Number of Shares %

Domestic

Government of Indonesia 15,653,128,000 60.5

Retail 857,530,739 3.3

Employee 78,724,370 0.3

Institutional (Trans Airways) 6,370,697,372 24.6

Other institutional (less than 5%) 1,686,581,134 6.5

Total domestic 24,646,661,615 95.3

International

Retail 3,856,770 0.0

Institutional (less than 5%) 1,218,408,248 4.7

Total international 1,222,265,018 4.7

TOTAL 25,868,926,633 100.0

Percentage of Shares based on Real Free Float

Domestic 68.2%

International 31.8%

4

Picture’s source: www.google.com

Garuda Indonesia Continues its Bright Performance in Challenging Conditions

• Sustainable passenger growth: 17.5% YoY• Sustainable market share

(Dom: 44% & Inter: 28%) • Sustainable high SLF 77.3%

• Manage RPK growth is higher compare to ASK growth

• The non fuel efficiency, exercised ± 70% of target FY 2015

• Top line increase 0.5% YoY• Reduce cost 11.8% YoY• Bottom line improves

(9M2015 – net profit USD 51.4Mio)

5

Awards

• Service: 17 awards• Commercial: 9 awards• Business: 7 awards• Corporate Transformation: 5 awards• Human Capital: 4 awards• People Management: 2 awards• GCG: 2 Awards

46 awards 2015:Domestic: 34 awards

International: 12 awards

• SKYTRAX Awards 2015 “The World’s Best Cabin Crew”• SKYTRAX Awards 2015 “World’s Best Airline” 8th Rank• FinanceAsia Awards 2015 “Asia’s Best Companies 2015”• Schipol Aviation Awards “Passenger Airline of the Year Award 2014-Intercontinental”• Indonesia Human Capital Award 2015 “1st in Human Resources Technology”• Indonesia Good Corporate Governance Award 2015 “Score A (Excellent)”• Pacific Asia Travel Association (PATA) “Gold Awards 2015 for Inflight Magazine”

Picture’s source: www.google.com

Milestones

6

First Quarter 2015• Garuda Indonesia implemented hedging cooperation through Cross Currency Swap (CCS) transactions with banks.

The first and the biggest CCS transaction, exercised by SOE in Indonesia.• Garuda Indonesia, BII-Maybank, and NBAD/DIB carried signing of bridging loan facility with the principles of Sharia

facility of $ 500 million.

Second Quarter 2015• Garuda Indonesia launched the "New Mobile Apps“• Garuda Indonesia and Cardig Air signed a cooperation of air cargo management and business development• Garuda Indonesia exercised “Reprofiling Debt” of “Quick Wins” strategy by issuing sukuk amounted $500 mio with

4 times booking order.

Third Quarter 2015• Garuda Indonesia ends the Hajj Flights 2015 with 92.38% On-Time Performance Rates.• The Inaugurations of Garuda Maintenance Facilities AeroAsia (GMF-AA) 4th Hangar • President & CEO of Garuda Indonesia appointed as President of Indonesia Marketing Association (IMA) for the

period 2015-2017

Picture’s source: www.google.com

7

Garuda Indonesia Group Market Share – YTD August 2015

2014 2015

15%17%

44%37%

41%46%

Others

GA Group

Lion Group

Garuda domestic market share group (including Citilink)These market share were calculated based on all Garuda Indonesia’s routesSource: Company Data

Domestic Market Share

2014 2015

72%78%

28%22%

Others

GA Main Brand

International Market Share

Garuda main brand international market shareThese market share were calculated based on all Garuda Indonesia’s routesSource: Company Data

Picture’s source: www.google.com

Note: YTD September 2015Sumber: Airline Website and Asia Pacific Data for August 2015

Passenger carried growth (%) 2014-2015

ASK growth (%) 2014 vs 2015 RPK growth (%) 2014 vs 2015

Asia Pacific

Passenger carried of AAPA – 2015Passenger Carried Growth

Asia Pasific

Asia Pacific

8

6.4

11.4 10.9

5.5

0.6

8.9

-

5.0

10.0

15.0

20.0

25.0

SouthEast

South NorthEast

Oceania Central AsiaPacific

17.5

13.1 10.6

8.5

1.7 1.1

8.9

-

5.00

10.00

15.00

20.00

25.00

16.5 14.8

8.8 7.3 6.1

(0.9)

8.3

-5.00

0.00

5.00

10.00

15.00

20.0014.5

6.0 3.7 5.0

(0.2) (0.9)

6.4

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

Peers Comparison – Operational Performance YTD 9M2015

9

Operational Performance

Number of Fleets

5.85.0 4.5 4.7 4.3

2012 2013 2014 Sep-15 2015E

Average Age (year)

10

14-Dec Sep 15 Ops.lease Fin lease/

15-Decowned

Narrow body

• B737-500 4 1 - 1 -

• B737-800 NG 75 79 79 - 81

• CRJ - 1000 15 15 9 6 18

• ATR 72-600 8 10 10 - 11

Total narrow body 102 105 98 7 110

Wide Body

• B747-400 2 2 - 2 2

• B777-300 ER 6 8 8 - 9

• A330-200 11 10 10 - 9

• A330-300 11 12 6 6 13

Total wide body 30 32 24 8 33

Garuda main brand 132 137 122 15 143

Citilink

• B737-300 5 5 - 5 5

• B737-500 - 3 - 3 3

•A320-200 32 36 36 - 36

Total Citilink 37 44 36 8 44

Total fleets 169 181 158 23 187

Fleets per Dec 2014 169

In

* B737-800NG 5

* ATR 72-600 2

* B777-300 ER 2

* A320-200 4

* A330-300 1

Total 14

Out

* A330-200 1

* B737-800 1

Total 2

Fleets per Sept 2015 181

11

Operational Performance Garuda Group

Operational

Efficiency

Passenger & Cargo

Financial

9M-2014 9M-2015 ∆ %

Aircraft Utilization (Hours) 9:53 9:11 -0:42

Frequencies 165,642 186,105 12.4

On Time Performance - OTP (%) 89.6 88.2 (1.4)

ASK ('000) 36,902,810 38,748,407 5.0

Average Fuel Price (USD/L) 0.9 0.5 (37.9)

Fuel Burn/Blockhours 3,699 3,590 (2.9)

Passenger Carried 20,893,654 24,551,594 17.5

RPK ('000) 26,086,291 29,951,212 14.8

Seat Load Factor (%) 70.7 77.3 6.6

Passenger Yield (USc) 8.6 7.5 (13.7)

Cargo/Mail Uplifted (Ton) 292,888 257,304 (12.1)

CASK (Usc) 7.6 6.4 (15.3)

CASK-excl Fuel (Usc) 4.5 4.5 0.0

• The passenger yield decreased 13.7% due to IDR depreciation ±12.1% and lower international fares amidst unstable economic.

Yield decreased

• The utilization was going down to be 9:11 hours due to route restructuring of Quick Wins program, especially in international market.

Utilization decreased

• OTP decrease due to Mount Raung eruption and fire incident in SHIA Terminal 2

• Cargo capacity decrease due to the increase of passenger carried as Garuda Cargo is ‘belly cargo’ on Garuda Group.

Others

Operational Performance Domestic & International

Domestic

International

12

9M-2014 9M-2015 ∆ %

Passenger Carried 12,666,172 14,508,965 14.5

Frequency 106,581 118,607 11.3

ASK ('000) 14,779,378 16,448,716 11.3

RPK ('000) 10,915,976 12,675,797 16.1

Seat Load Factor (%) 73.9 77.1 3.20

Passenger Yield (Usc) 10.1 8.6 (14.5)

CASK (Usc) 8.6 7.1 (17.1)

CASK-excl Fuel (Usc) 5.3 5.0 (4.4)

Passenger Carried 2,897,051 3,176,986 9.7

Frequency 21,549 20,835 (3.3)

ASK ('000) 16,963,144 15,742,812 (7.2)

RPK ('000) 11,101,472 11,953,539 7.7

Seat Load Factor (%) 65.4 75.9 10.49

Passenger Yield (Usc) 8.0 6.9 (13.6)

CASK (Usc) 7.3 6.3 (13.6)

CASK-excl Fuel (Usc) 4.4 4.5 3.0

Garuda Indonesia main brand has 58 domestic destinations

17 international destinations

Picture’s source: www.google.com

Operational Performance Main Brand & Citilink

Main Brand

Citilink

13

9M-2014 9M-2015 ∆ %

Passenger Carried 15,563,223 17,685,951 13.6

Frequency 128,130 139,442 8.8

ASK ('000) 31,742,521 32,191,527 1.4

RPK ('000) 22,017,448 24,629,336 11.9

Seat Load Factor (%) 69.4 76.5 7.15

Passenger Yield (Usc) 9.1 7.8 (13.7)

CASK (Usc) 7.9 6.7 (14.9)

CASK-excl Fuel (Usc) 4.8 4.8 (0.2)

Passenger Carried 5,330,431 6,865,643 28.8

Frequency 37,512 46,663 24.4

ASK ('000) 5,160,289 6,556,880 27.1

RPK ('000) 4,068,844 5,321,876 30.8

Seat Load Factor (%) 78.9 81.2 2.31

Passenger Yield (Usc) 6.5 5.8 (10.7)

CASK (Usc) 5.7 5.0 (13.4)

CASK-excl Fuel (Usc) 2.9 3.2 11.2

14

Financial Performance

Summary of Consolidated Income Statement

Garuda GroupTop Line (USD, Bio)

Operating Revenue

Operating Expenses

Income

EBITDAR Margin 14.4% 32.3%

Garuda GroupNet Income (USD, Mio)

15

In USD Mio 9M14 9M15 ∆ % YoY

EBITDAR 406.3 918.4 126.0

Total revenues 2,831.3 2,845.7 0.5

Fuel 1,175.7 806.5 (31.4)

Aircraft rental and charter 530.1 659.9 24.5

Others 1,374.8 1,251.3 (9.0)

Total expenses 3,080.6 2,717.6 (11.8)

EBIT (249.3) 128.1 151.4

EBT (298.3) 81.3 127.3

Net income (220.1) 51.4 123.4

0.9 0.9

1.0

Q1 Q2 Q3

12.4 16.9

22.1

Q1 Q2 Q3

Operating Revenue

2,831.3

2,845.7

(2.4%)

2.4%0.5%

9M14 9M15

Schedule airline

Non Schedule Airline

Others

Operating Revenue Operating Revenue

• Lower yield due to IDR depreciation and unstable economic condition in regional

• Losing revenue potency due to challenging conditions such mount eruption, SHIA fire incident, and hazardous haze in indonesia surroundings

Scheduled airline decrease

• Sustainable increase of charter revenue to China market and Umrah (Middle East).

• Additional revenue from Hajj season

Non schedule airline increase

• Others revenue increased due to green performance of subsidiaries.

Others increase

In USD mio% Change

*PoT : Percentage of total

16

Operating Revenue *PoT

Schedule airline 84.60%

Non schedule airline 6.20%

Others 9.20%

Operating Expenses

2,717.6

3,080.6

(12.0%)

4.7% (1.6%)(0.3%)

(2.6%)

9M14 9M15Operating Expenses Operating Expenses

Fuel Fligh Ops + Maintenance +

User charge

Tickets + Passenger

Service

G&AOthers

In USD mio% change

*PoT : Percentage of total

• Fuel expenses decreased 31.4% to be USD 806.5miocompared to same period last year of USD 1.2bio due to fuel price declining 37.9% compare last year.

• Total operating expenses decreased 11.8% to be USD 2.7 bio compared to the same period last year USD 3.1bio.

• Fuel efficiency YTD 9M15 USD 369.3mio as impact of fuel price declining and fuel efficiency program

• Non fuel efficiency YTD 9M15 USD ±115.3mio

Decreasing expenses

• The rental cost increased 24.5% to be USD 659.9mio compared to the same period last year of USD 530.1 mio in line with the additional fleets.

• The maintenance cost increased by 9.5% to be USD 210.2mio compared to the same period last yearUSD 192.0mio in line with the additional fleets.

Increasing expenses

17

Operating Expenses PoT*

Fuel 28.97%

Flight ops + Rental + Maintenance + User charge 47.96%

Ticketing + Passenger Service 15.62%

G & A 5.89%

Others 1.55%

Summary of Consolidated Balance Sheet

Asset

Liability

Equity

Lease Adj. Net Debt/EBITDAR 10.1x 7.5x

18

FY14 9M15 ∆ % YoY

Current assets 810.5 843.5 4.1

Non current assets 2,302.6 2,238.5 (2.8)

Total Assets 3,113.1 3,082.0 (1.0)

Current liabilities 1,219.4 1,103.7 (9.5)

Non current liabilities 1,014.2 1,107.2 9.2

Total liabilities 2,233.6 2,210.9 (1.0)

Total equities 879.5 871.1 (0.9)

Total liabilities & Equities 3,113.1 3,082.0 (1.0)

Summary of Consolidated Cash Flow

Operating

Cash receipts from customers USD 2.8bio

Cash payments to suppliers USD 2.4bio

Payments of interest and financial expenses USD 45.2mio

Investing

Payments PDP & Maintenance Reserve Fund: USD 303.4mio

Security Deposit payment: USD 11.1mio Refund of PDP and Maintenance Reserve

Fund: USD 216.2mio Receipts of security Deposit : USD 9.0mio

Financing

Proceed of long term loan, bank loan, & financial institution and sukuk USD 1,4bio

Payment of long term loan, bank loan & financial institution: USD 1.3bio

19

Min 5% of Cash Ratio

Picture’s source: www.google.com

9M14 9M15 ∆ % YoY

Beginning cash 480.4 434.3 (9.6)

Cash from operating activities (180.9) 56.0 130.9

Cash from investing activities (189.6) (104.1) (45.1)

Cash from financing activities 271.2 44.8 (83.5)

Net increase (decrease) in cash (99.3) (3.1) n.a.

Ending cash 396.6 409.5 3.2

Cash and Net Gearing

20

464.9 464.0 409.5 1,313.2 1,305.8 1,212.7 856.6 864.4 853.4

0.99

0.97

0.94

0.90

0.92

0.94

0.96

0.98

1.00

1.02

1.04

1.06

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

3M15 6M15 9M15

Cash Debt Equity Net Gearing

In USD Mio

31%

60%

9%

Debt Structure 9M2015

Shor term loan Long term loan Lease

Max 2.5x of Debt to Equity Ratio

Min capital USD 800mio

Picture’s source: www.google.com

21

Subsidiaries

Subsidiaries

22

Aero Wisata (in IDR bio) Citilink (in USD 000)

9M2014 9M2015 ∆ % YoY 9M2014 9M2015 ∆ % YoY

Operating Revenue 2,331.4 2,317.0 (0.6) Operating Revenue 287,853.0 351,728.0 22.2

Operating Income 82.3 98.4 19.5 Operating Income (11,208.0) 12,561.0 212.1

Net Income 64.1 77.0 20.0 Net Income (12,134.0) 5,888.0 148.5

EBITDA 167.5 189.9 13.4 EBITDA (4,747.1) 22,249.6 568.7

Dec14 Sept15 ∆ % YoY Dec14 Sept15 ∆ % YoY

Asset 2,735.5 2,830.9 3.5 Asset 166,019.0 218,420.0 31.6

Liability 937.2 952.1 1.6 Liability 209,441.0 199,902.0 (4.6)

Equity 1,798.3 1,878.8 4.5 Equity (43,422.0) 18,519.0 142.6

Gapura Angkasa (in IDR bio) GMF Aero Asia (in USD 000)

9M2014 9M2015 ∆ % YoY 9M2014 9M2015 ∆ % YoY

Operating Revenue 883.0 983.2 11.4 Operating Revenue 189,431.7 213,355.5 12.6

Operating Income 15.6 76.3 389.0 Operating Income 19,925.1 40,716.9 104.3

Net Income 8.7 57.8 565.1 Net Income 14,638.9 28,536.6 94.9

EBITDA 63.2 125.2 98.1 EBITDA 25,530.9 46,106.7 80.6

Dec14 Sept15 ∆ % YoY Dec14 Sept15 ∆ % YoY

Asset 787.0 842.9 7.1 Asset 251,351.9 284,929.7 13.4

Liability 422.0 449.6 6.6 Liability 146,760.0 170,429.4 16.1

Equity 365.0 393.2 7.7 Equity 104,592.0 114,500.3 9.5

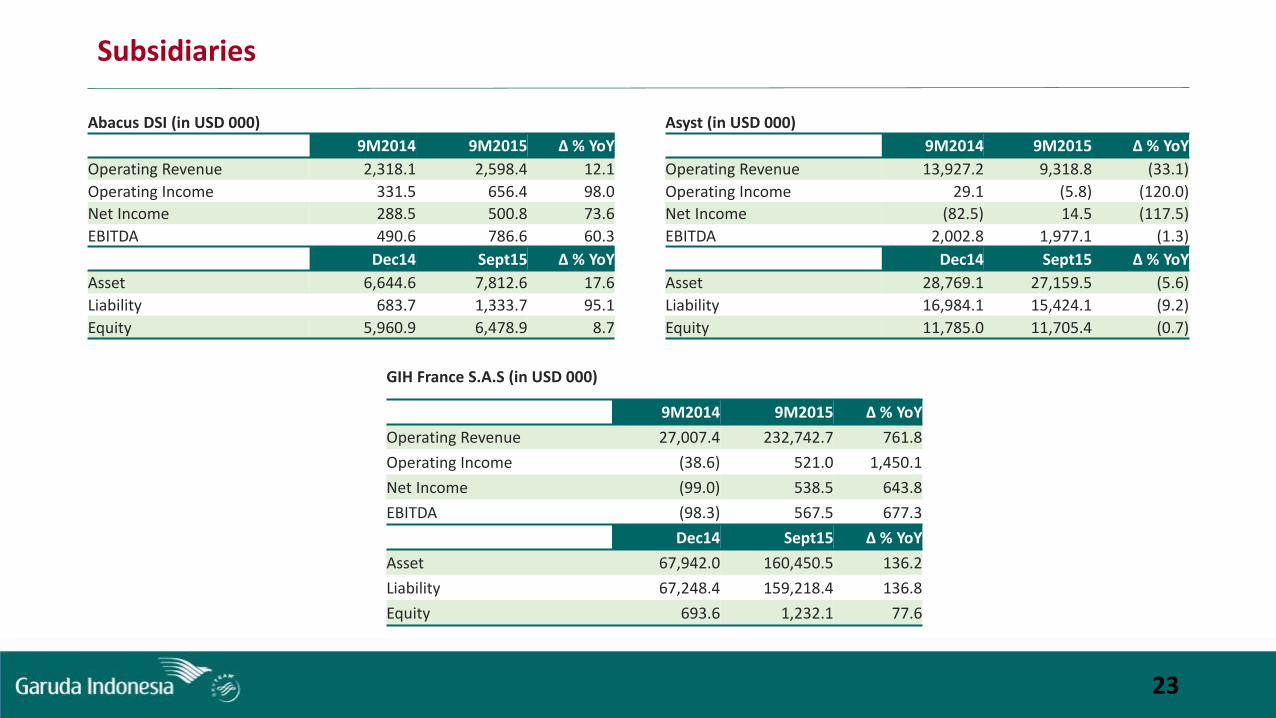

Subsidiaries

23

Abacus DSI (in USD 000) Asyst (in USD 000)

9M2014 9M2015 ∆ % YoY 9M2014 9M2015 ∆ % YoY

Operating Revenue 2,318.1 2,598.4 12.1 Operating Revenue 13,927.2 9,318.8 (33.1)

Operating Income 331.5 656.4 98.0 Operating Income 29.1 (5.8) (120.0)

Net Income 288.5 500.8 73.6 Net Income (82.5) 14.5 (117.5)

EBITDA 490.6 786.6 60.3 EBITDA 2,002.8 1,977.1 (1.3)

Dec14 Sept15 ∆ % YoY Dec14 Sept15 ∆ % YoY

Asset 6,644.6 7,812.6 17.6 Asset 28,769.1 27,159.5 (5.6)

Liability 683.7 1,333.7 95.1 Liability 16,984.1 15,424.1 (9.2)

Equity 5,960.9 6,478.9 8.7 Equity 11,785.0 11,705.4 (0.7)

GIH France S.A.S (in USD 000)

9M2014 9M2015 ∆ % YoY

Operating Revenue 27,007.4 232,742.7 761.8

Operating Income (38.6) 521.0 1,450.1

Net Income (99.0) 538.5 643.8

EBITDA (98.3) 567.5 677.3

Dec14 Sept15 ∆ % YoY

Asset 67,942.0 160,450.5 136.2

Liability 67,248.4 159,218.4 136.8

Equity 693.6 1,232.1 77.6

24

PT Garuda Indonesia (Persero) Tbk.Investor Relations Department

2nd Floor Management Building Garuda CitySoekarno-Hatta International AirportPhone: 62-21-2560 1201Email: [email protected]