cochilco mining in chile future y challenges rusia bielorrusia

DESCRIPTION

Cochilcos Sergio Hernandez presentation, dealing with the mining in Chile, investment situation and structural challenges in the sector. Enters in the reasons for attractive investments, copper production and forecast,TRANSCRIPT

Logo Gobierno:

160x162px.

Ministerio,

Subsecretaría,

Organismo,

etc.:160x145px

Sergio HernándezExecutive Vicepresident

Chilean Copper Commission

Mining in Chile: Future and

Challenges

Index

I. Mining in Chile and investments

II. Structural challenges

III. Final Comments

Imagen Referencial

I. Mining in Chile and investments

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

MUS$

Exportaciones nomineras

Otras exportacionesmineras

Exportaciones de cobre

Non-mining exports

Other miningexports

2014:

Mining 57%

Copper mining 50%

Source: Central Bank of Chile, COCHILCO

Tax revenue(2014)

•9% of total

•US$ 4.9 billion

Foreign Direct Investment(2009 – 2013)

•45%

•US$ 45.3 billion

GDP (2008 – 2014)

•13% nominal

Why Chile is attractive for mining investment?Economic Development

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Copper exports

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

1,0

7,0

Macroeconomía

Estabilidad política

Infraestructura paranegocios

Infraestructura generalMarco regulatorio

Mercado laboral

Potencial geológico

Países ingresos bajos y medios Países ingresos altos Chile

Source: COCHILCO, 2014

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Why Chile is attractive for mining investment?Competitive in comparison with other mining countries

Macroeconomics

Geological potential

Labour market

Regulatory framework General infrastructure

Business infrastructure

Political stability

Low and middle income countries High-income countries

Source: USGS Mineral Commodity Summaries (2014)

27.9%

10.3%

5.7%

4.4%

4.4%

4.1%

12.8%

5.6%

Chile

Peru

USA

Russia

China

Mexico

Other countries14%

Indonesia

Australia

Why Chile is attractive for mining investment?Geological potential

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Mining in Chile

World copper mining participation

Source: COCHILCO, WBMS and Wood Mackenzie

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

20.000

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

kt Cu

World total Chile

2014:Chile 31%

1950:Chile 14%

18%

Up to34%

Up to32-37%

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Source: COCHILCO Y WBMS

Country 2013 2014

Chile 5,776 5,745

China 1,707 1,632

Peru 1,376 1,380

USA 1,240 1,346

D.R. Congo 817 999

Australia 996 963

Zambia 839 759

Russia 720 720

Canada 632 696

Mexico 480 513

Others 3,705 3,677

World 18,288 18,428

Chile 31%

China 9%

Peru 8%USA

7%

D.R. Congo

5%

Australia 5%

Zambia 4%

Russia 4%

Canada 4%

Mexico 3%

Otros 20%

2014

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

World copper mine productionThousands of tons

The portfolio consists of investment projects in the mining of copper,

gold, industrial minerals and iron.

Consider initiatives with investments of over US $ 90 million.

Initiatives that companies have announced publicly.

At least they have started their pre-feasibility studies.

Its investment decision is expected no later than 2019.

9

Mining projects portfolio

General concepts - conditions for inclusion in the portfolio

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Investment

Risk

Engineeringprofile

Prefeasibility Feasibility Construction

Investment decision

Start up

Project Portfolio

Mining projects portfolio

General concepts – Project stages

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Levels of

certaintyType of project

Stage of

advancementEnvironmental licenses Start up

BASE Anyone Construction Approved 2015 - 2019

PROBABLE

Anyone Suspended construction Approved or legal claim 2015 - 2019

Anyone Feasibility Approved 2015 - 2019

Replacement or Expansion Feasibility In process 2015 - 2019

POSSIBLE

Replacement or Expansion Suspended Feasibility In process 2015 - 2019

Replacement or Expansion Feasibility Not submitted 2015 - 2019

New Feasibility In process or not submitted 2015 - 2019

Anyone Feasibility Approved 2020 - 2024

Replacement or Expansion Feasibility In process or not submitted 2020 - 2024

POTENTIAL

Anyone Suspended Feasibility Anyone 2020 - 2024

New Feasibility In process or not submitted 2020 - 2024

Anyone Prefeasibility Anyone Anyone

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Mining projects portfolio

General concepts – Levels of certainty

- Pampa Hermosa (MUS$ 1,033)

- Cerro Negro Norte (MUS$ 1,200)

- Escondida Nueva Pila de Lix. De Óxidos (MUS$ 721)

- Planta Nitrato Potasio – Coya Sur (MUS$ 250)

- Sierra Gorda (MUS$ 4,240)

- Bellavista (MUS$ 143)

- Actualización Quebrada Blanca (2016 – MUS$ 165)

- Arbiodo (2017 – MUS$ 503)

- Los Bronces / Fase 7 (2017 – MUS$ 112)

- Spence Growth Option (2019 – MUS$ 3,300**)

SALEN(*)

ENTRAN

Source: COCHILCO, 2015.(*) in operation in 2014(**) Including desalination plant

Current status of investment portfolio

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

OUT

IN

- Jerónimo (Gold, MUS$ 423)

- Lomas Bayas III Sulfuros (Priv. mining - Cu, MUS$ 1,600)

- Tovaku (Mid. Min. – Cu, MUS$ 600)

- Lobo Marte (Gold, MUS$ 800)

- Inca de Oro (Mid. Min. – Cu, MUS$ 600)

- Volcán (Gold, MUS$ 800)

- Cerro Casale (Gold, MUS$ 6,000)

- El Morro (Gold, MUS$ 3,900)

- Collahuasi Expansión Fase III (Priv. mining – Cu, MUS$ 6,500)

- Ampliación Los Pelambres IV (Priv. mining – Cu, MUS$ 7,000)

REESTRUCTURADOS

Source: COCHILCO, 2015.(*) Projects out from the portfolio to be under review process without starting or investment decision clarified by companies

Projects under review*

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

UNDER REVIEW

Source: COCHILCO

The portfolio of mining projects 2015 - 2024 considered 42initiatives, broken down as follows, according to sector.

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Mining projects portfolio

Investment by the mining sector

Source: COCHILCO(*) CODELCO investment includes metallurgical plants, other development projects, information projects and five structural projects

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

*

Mining projects portfolio

Investment by type of company

Each project has considered attributes that give it a graduality associated

with greater or lesser certainty meet its deadlines of materialization.

Source: COCHILCO

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Mining projects portfolio

Levels of certainty

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

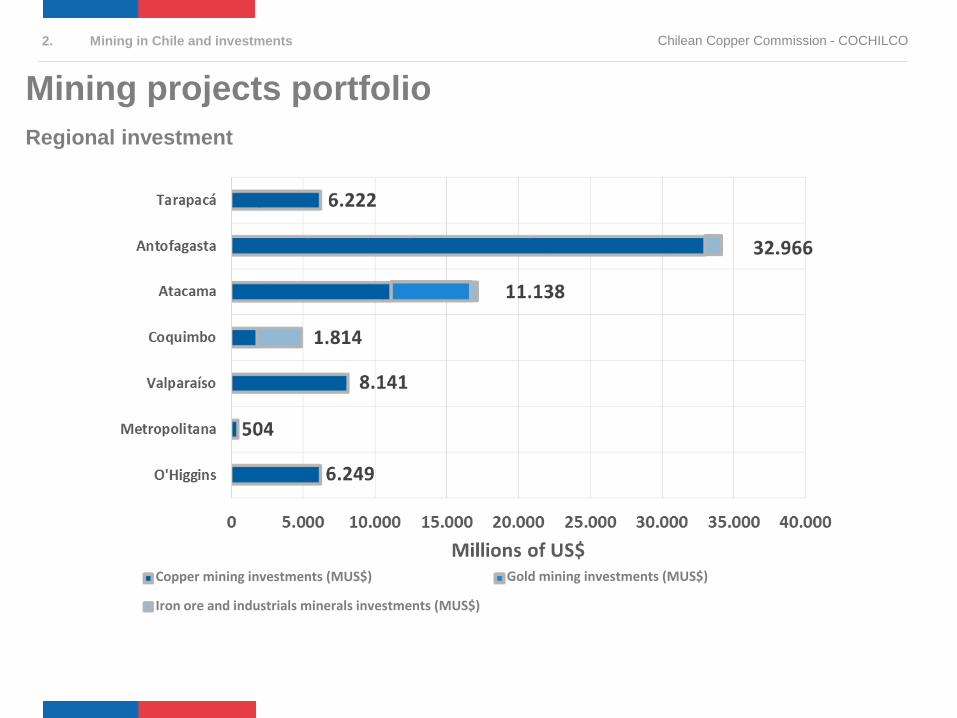

Mining projects portfolio

Regional investment

Copper mining investments (MUS$)

Iron ore and industrials minerals investments (MUS$)

Gold mining investments (MUS$)

In the last thirteen years (2002 - 2014) Copper mine production grew 25.5% at an average annual rate of 1.8%. The project portfolio has a potential production growth of 18.7%

copper mine at an average annual rate of 1.3%.

-4,6%

+11,0%

6,83 Mt

5,75 Mt

Copper production forecast

By levels of certainty, 2014 - 2026

2. Mining in Chile and investments Chilean Copper Commission - COCHILCOM

illio

nto

ns

of

cop

per

+1.8 Mt of copper in concentrates. (+70.5%)

-0.92 Mt of copper in SxEw cathodes (-50,1%)

2.55 Mt of copper in concentrate exported in 2014, 65.3% of concentrate production in the country. In 2026 would potentially be exported 4.4 million tons of concentrates, 73.6 % of the

chilean concentrate production that year.

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Copper production forecast

By products, 2014 - 2026

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Copper concentrate production forecast

Increased mineral processing

51.2%

90.5%

Daily production of tailings around 1.54 Mt, due to mining copper sulphide, the project portfolio will increase to 2.95 Mt of tailings daily production to 2026, a growth of 91%.

563,5

1.077,9

0,0

200,0

400,0

600,0

800,0

1.000,0

1.200,0

1.400,0

1.600,0

1.800,0

2005 2010 2015 2020 2025 2030 2035

Mill

ion

ton

so

gta

ilin

gs

2. Mining in Chile and investments Chilean Copper Commission - COCHILCO

Copper concentrate production forecast

Tailings, 2014 vs 2026

Imagen Referencial

III. Structural challenges

3. Structural challenges

Critical supplies

OPEX

Source: COCHILCO, 2014

Energía Eléctrica Chancado y Molienda (Conc)

Energía Eléctrica Sistema de Impulsión (Imp. Des)

Combustible (Petróleo y lubricantes) (mca)

M&R (Infraestructura, LHD, Camiones, Jumbo, Martillo, Chancador, Correas) (ms)

Requerimiento Agua Fresca (Desalada) (Conc)

Acido Sulfúrico (Sx-Lix-Ew)

Mantención y Reparación (M&R) (mca)Servicios de M&R Chancado yMolienda (Mec-Elec) (Conc)

Servicios de M&R Espesamiento Concentrado (Mec-Elec) (Conc)Bolas y Barras de Molino (Conc)

Cal (Conc)Espumante (Conc)Colector Primario (Conc)

Reactivos Sx-EW

Otros tronadura(mca)

Depresante Cobre (Conc)Floculante Relaves (Conc)

Energía Eléctrica Pta. Desaladora (Des)Servicios de M&R Desaladora(Mec-Elec) (Des)

Reactivo CO2 (Des)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

RIE

SG

O D

E D

ESA

BA

ST

EC

IMIE

NT

O

PESO RELATIVO EN LOS COSTOS DE OPERACIÓN(Por Subproceso)

Electricity

Sulphuric acid

Grinding balls

Lime

Water

Chilean Copper Commission - COCHILCO

Camiones (CAEX) (Mina Rajo)

Geomembrana (Lix)

Pala de Cable (Mina Rajo)

Insumos Eléctricos (Cables, conduit y

luminarias) (Lix)

Molino de Bolas y Barras (Pta. Concent.)

Bombas (Pta. Desal.)

Correas transportadoras (Lix)

Polín (correa)

(Lix)

Edificio Molienda (Pta. Concent.)

Celda Flotacion

(Pta. Concent.)

Loop eléctrico(Mina Rajo)

Equipos de Bombeo (Bombas) (Lix)

Cañería Aceros (Lix)

Cañ

eria

s N

o M

etal

icas

(Pta

. Des

al.)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

0% 5% 10% 15% 20% 25% 30%

RIE

SGO

DE

DES

AB

AST

ECIM

IEN

TO

PESO RELATIVO EN EL CAPEX

(Por Subproceso)

Critical supplies

CAPEX

Source: COCHILCO, 2014

Mining Trucks

3. Structural challenges Chilean Copper Commission - COCHILCO

Energy (Electricity+Fuels)

Expected consumption forecast, 2014 - 2025

46,3

39,5

21,922,9

0

10

20

30

40

50

TWh

Consumomáximo

Consumoesperado

Mínimoesperado(Proyectos Base)

Minimumconsumption(Base projects)

It is expected that electricity demand

increase by 80.3% in the period 2014-2025.

Source: COCHILCO, 2014

3. Structural challenges Chilean Copper Commission - COCHILCO

Maximum consumption

Expected consumption

Water

Expected consumption forecast, 2014 - 2025

14,8 14,7 14,616,1 16,7 17,5

18,520,4 21,0

22,023,6

24,6

0

5

10

15

20

25

30

m3

/s An increase of 66.2% in water consumption in

mining is expected in the period 2014-2025

Source: “Proyección de consumo de agua en la minería del cobre 2014-2025”, COCHILCO, 2014.

3. Structural challenges Chilean Copper Commission - COCHILCO

Water

Expected consumption forecast of fresh water and sea water, by level of certainty

Source: “Proyección de consumo de agua en la minería del cobre 2014-2025”, COCHILCO, 2014.

0

2

4

6

8

10

12

14

16

18

m3

/se

g

Fresh Water

BASE PROBABLE POSIBLE POTENCIAL

0

2

4

6

8

10

12

14

16

18

m3

/se

g

Sea water

POTENCIAL POSIBLE PROBABLE BASE

3. Structural challenges Chilean Copper Commission - COCHILCO

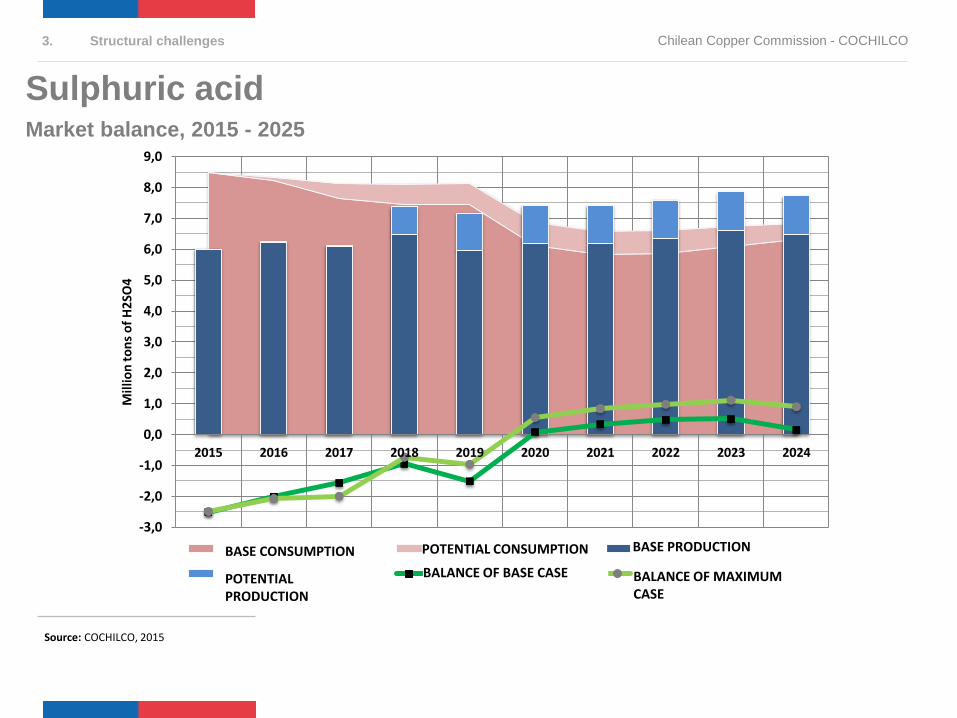

Sulphuric acidMarket balance, 2015 - 2025

Source: COCHILCO, 2015

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Mill

ion

ton

so

f H

2SO

4

CONSUMO BASE CONSUMO POTENCIAL PRODUCCIÓN BASE

PRODUCCIÓN POTENCIAL BALANCE CASO BASE BALANCE CASO MÁXIMO

3. Structural challenges Chilean Copper Commission - COCHILCO

BASE CONSUMPTION

POTENTIAL PRODUCTION

POTENTIAL CONSUMPTION

BALANCE OF BASE CASE

BASE PRODUCTION

BALANCE OF MAXIMUM CASE

• Starting in 2018, the entry into operation of new mining projects will push up the price of lime, as the domestic supply can not meet demand.

Source: “Análisis del mercado de insumos críticos en la minería del cobre”, Cochilco 2015

-

500.000

1.000.000

1.500.000

2.000.000

2014 2015 2016 2017 2018 2019 2020

(ton)

CaO otros usos (25% ) Esc. Base Esc. Probable Esc. Posible Esc. Potencial Oferta CaO Nacional

Lime

Consumption forecast, 2014 - 2020

3. Structural challenges Chilean Copper Commission - COCHILCO

• From 2019, the domestic supply fails to meet demand for a scenario in which all mininginvestments materialize, a situation that would push up the price of the grinding balls.

-

100

200

300

400

500

600

700

800

900

1.000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

(kto

no

f gr

ind

ing

bal

ls)

Base Probable Posible Potencial Oferta Nacional

Grinding balls

Consumption forecast, 2014 - 2020

Source: Análisis del mercado de insumos críticos en la minería del cobre, Cochilco 2015

3. Structural challenges Chilean Copper Commission - COCHILCO

Mining trucks

Current imports and additional quantity required by 2025

• For the period 2015 -2025 expected a need for 700 mining trucks, which is mainlyexplained by the replacement needs of existing units in operation for compliance with theestimated useful life.

Import models most used in the Private Mining, period 2002-2014

54 7950

104 94 68115

174208

7219

15

4058

90 103

48

85

152

180

87

84

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Caterpillar

(773-775-777-785-789-793-795)

Komatsu

(730E-830E-930E-960E-HD465-HD605-HD785)

Liebherr

(T282)

Source: “Análisis del mercado de insumos críticos en la minería del cobre”, Cochilco 2015

3. Structural challenges Chilean Copper Commission - COCHILCO

What is Chile doing to stay competitive?

CNID

• Research and Development Commission(Comisión de Investigación y Desarrollo)

• Advises the President of Chile on the identification, formulation and implementation of policies and actions to strengthen innovation and competitiveness in Chile.

CMDCh

• Mining and Development Commission of Chile (Comisión Minería y Desarrollo de Chile)

• Mining and Development Commission of Chile Team with representatives of public-private sector summoned to build a strategic vision of the challenges (gaps) facing copper mining development

Agenda

• Mining: A platform for the future of Chile (Minería: Una plataforma de futuro para Chile)

• Mining: A platform for the future of Chile Strategic agenda and guidance to bring the Chilean mining to a virtuous mining (competitive and productive), inclusive (communities) and sustainable (socially and environmentally).

• One of the strategic commitments, beginning in 2015, corresponding to generate collaborative initiatives and fund R & D + i.

3. Structural challenges Chilean Copper Commission - COCHILCO

ENABLINGELEMENTS/RESOURCES

What is Chile doing to stay competitive?

Roadmap

TENDENCIES/DRIVERS

BUSINESS OPPORTUNITIES

TECHNOLOGIES

PROJECTSR&D+i

TAILIN

GS

SMA

RT

MIN

ING

SMELTER

&

REFIN

ING

ENER

GY

&

WA

TER

OTH

ERS

DRIVING CORES

TODAY SHORT TERM MID TERM + 2035

ENABLING CORES

SUPPLIERS DEVELOPMENT

HUMAN CAPITAL

VISION AND OBJECTIVES

US$M 10.000 in exports

290 world-classsuppliers

80% of industrie in first costquartiles

3. Structural challenges Chilean Copper Commission - COCHILCO

Imagen Referencial

III. Final Comments

Ministerio de Minería| COCHILCO

Logo Gobierno:

160x162px.

Ministerio,

Subsecretaría,

Organismo,

etc.:160x145px

Sergio HernándezExecutive Vicepresident

Chilean Copper Commission

Mining in Chile: Future and

Challenges