bulgaria power-sector-rapid-assessment may27-final

TRANSCRIPT

Republic of Bulgaria

Power Sector Rapid Assessment

May 27, 2013

The World Bank

Europe and Central Asia Region

This note has been prepared by the World Bank in response to a request by the

Government of Bulgaria in March 2013 to conduct an assessment of the issues and

challenges in the Bulgarian power sector in the wake of the crisis in January 2013.

This note is intended to help inform the Government's deliberations on how to

improve public confidence and trust in the governance of the power sector, enhance

the sector’s financial standing, and provide adequate support to poor households so

that they can afford environmentally sustainable and reliable electricity service.

This assessment has been undertaken by the World Bank within a very short period

of time based on data provided by the Ministry of Economy, Energy and Tourism

(MEET), the State Water and Energy Regulatory Commission (SWERC), the National

Statistical Institute (NSI), and the Ministry of Labor and Social Policy (MLSP). This

rapid assessment is not a substitute for more detailed analysis that will inform and

guide specific implementation steps and sector reforms.

The World Bank will be available to continue the policy discussion on the findings of

this assessment and the suggested package of reforms with the Government to

develop and support a viable program of reforms that will help achieve reliable,

efficient, and affordable electricity and heating services for the citizens of Bulgaria.

Foreword

2

3

Public has lost confidence and trust in the management of energy companies and the

Government’s oversight of the electricity sector. Common believe that some State officials and

enterprise managers have investments in the energy sector has compromised public trust.

Bulgarian Energy Holding (BEH) is an unnecessary level of State oversight.

Sector has large financial deficits that are increasing contingent liabilities on the State. High

cost structure stemming from flat energy demand, poorly regulated growth in renewables, misuse of

incentives for cogeneration, long-term contracts, and inefficient trade/export incentives.

Declining level and coverage of social assistance benefits have made energy unaffordable

for the poor. Budget contribution for targeted social safety net programs is a third of levels in 2003.

Comprehensive package of actions needed to improve public confidence, financial viability

and affordability:

Enhance credibility, independence, and capacity of energy regulator.

Eliminate incentives that lead to inefficient investments and rent-seeking behaviour.

Address financial liabilities that arise from the off-take of renewable energy, co-generation,

long-term power purchase agreements, and failed investments in an equitable manner.

Increase budgetary funding to expand level and scope of targeted social assistance benefits

for vulnerable consumers.

Eliminate conflicts of interest of state officials and senior managers in having personal/family

financial interests in the power sector.

Synopsis of Diagnosis and Recommendations

4

I. Public distrust

II. Unsustainable cost structure

III. Affordability

IV. Future directions

Note Structure

I. Public distrust

5

Serious structural issues in the sector contributed to a political crisis

Public Distrust

Governance

Perception of deep

rooted corruption

Governance of State

Owned Enterprises

Undermined regulatory

framework

Unsustainable

cost structure

High cost generation mix

Inefficient operation of the

system

Poorly regulated growth in

renewables

Affordability

Inadequate social

protection

High and inefficient

electricity consumption

Unless these issues are comprehensively addressed, service delivery will

worsen and threaten economic stability 6

7

Consumers are frustrated by tariff hikes and the lack of

transparency in the sector

Electricity market performance (MPI): second lowest scoring country in the EU

The Market Performance Indicator (MPI) is a composite index based on the results of survey which information on consumer markets in terms

of comparability, trust, consumer problems and complaints, expectations, choice and switching.

Source: European Commission

Lowest scores for “trusting the provider” (to respect laws and regulations

protecting consumers) and “live up to what you wanted” (the service consumers

want is actually being delivered)

8

Overall, high perception of corruption

Bulgaria is the lowest scoring country in the EU area after Greece in terms of the

Corruption Perception Index (CPI) for 2012

A country or territory’s score indicates the perceived level of public sector corruption on a scale of 0 - 100,

where 0 means that a country is perceived as highly corrupt and 100 means it is CPI (2012) perceived as

very clean.

Source: Transparency International

0

10

20

30

40

50

60

70

80

90

100

CP

I sco

re

9

Consumers upset over billing practices

Consumers are not sure what they

are being charged for

Bills do not make essential

information understandable

Past consumption is not explained

Billing cycles are irregular

State Ownership through Holding Company BEH compromises transparent

and professional management of the energy enterprises

State assets are being priced inefficiently. For example, some

hydroelectricity priced artificially low to accommodate high priced renewables

Growing Government liabilities hidden making it difficult to assess impact on

the State Budget

State governance of the sector is convoluted

10

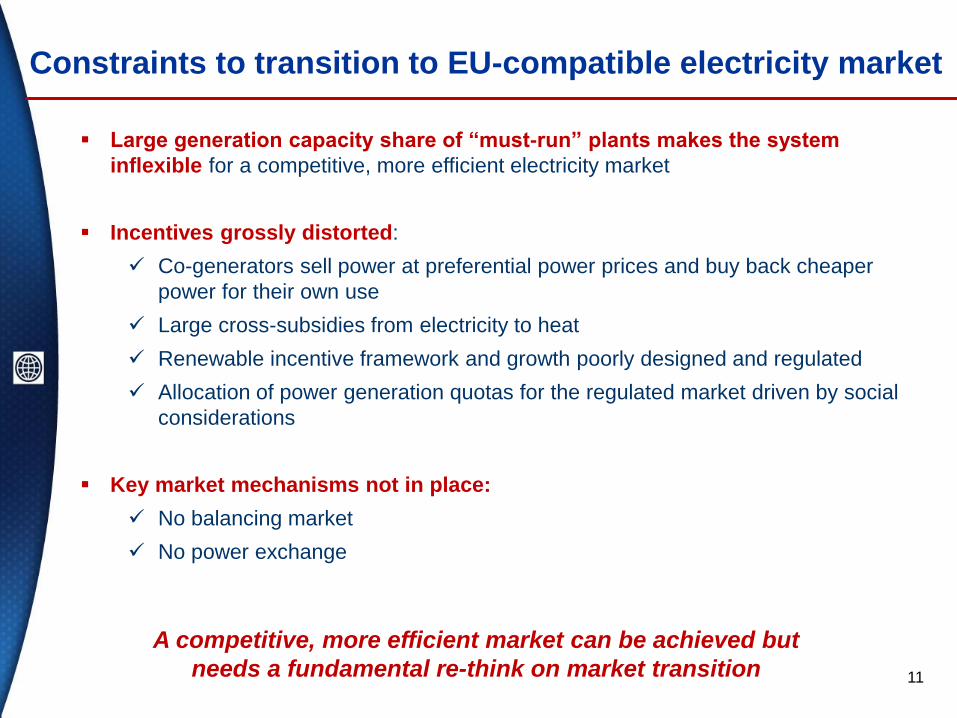

Constraints to transition to EU-compatible electricity market

Large generation capacity share of “must-run” plants makes the system

inflexible for a competitive, more efficient electricity market

Incentives grossly distorted:

Co-generators sell power at preferential power prices and buy back cheaper

power for their own use

Large cross-subsidies from electricity to heat

Renewable incentive framework and growth poorly designed and regulated

Allocation of power generation quotas for the regulated market driven by social

considerations

Key market mechanisms not in place:

No balancing market

No power exchange

A competitive, more efficient market can be achieved but

needs a fundamental re-think on market transition 11

Current market structure a good platform to facilitate

market transition

12

Well disaggregated sector - although transmission separation to be completed

The single buyer NEK can transition to a balancing market and power exchange

Active cross-border trade with neighbouring countries will help the transition

NEK(Single Buyer, Aggregator, Hydropower Generator, Supplier of Last Resort & Transmission Company)

State-owned Energy Suppliers (nuclear, coal,

gas)

CEZ

EVN

Energo Pro

System Operator

(owned by NEK; organizes the

balancing Market)

Coal Independent Power Producers

Cogeneration Suppliers

Renewable Energy Power Plants (under Feed in Tariffs)

Generation Transmission Distribution

Purchased and Paid for by NEK under Law

Purchased and Paid for by NEK under Energy Law

Purchased and Paid for by NEK under PPAs

Purchased and Paid for by NEK under Energy Law

Distribution Entities collect on behalf of NEK

Regu

late

d Pr

ices

thr

ough

Ann

ual T

ariff

O

rder

s

Subsidiaries of BEH

Renewable and Efficient

~58%

15%

~12% of Energy

15%

~1%

High-Voltage Customers

13

Energy Regulator: lack of independence and capacity

Regulatory independence is insufficient

In the last 6 months there have been two changes of the Chairman of the Regulator

(SWERC)

Decision to decrease prices was pre-announced by the State officials and followed a

change in the Energy Law allowing price decreases

Regulator is blamed but unable to make the necessary political decisions to correct

problems in the electricity sector

Some regulatory decisions are unpredictable and not fully explained or supported by

transparent information

SEWRC has insufficient technical, financial capability to fulfil its

duties

Number of staff (128) is small considering scope of activities covering electricity, gas and

water

There are about 15 experts covering the electricity sector

The budget is insufficient and 2nd lowest per employee in Europe; it is part of the central

budget and not ring-fenced

Lack of key regulatory building blocks

No accounting standards framework for regulated utilities

No cost benchmarking of regulated utilities e.g. generation, transmission, and distribution

Allocation of quotas for the regulated market not based on efficiency principles

II. Unsustainable cost structure

14

Factors contributing to financial unsustainability

1. Adequate power capacity for domestic use, but administrative

constraints to exporting surplus power

2. Inefficient allocation of power generation quotas for the regulated

market and distortions in operational dispatch of power plants

3. Rapid build-up of renewable energy at high feed-in tariffs

4. High preferential tariffs paid to “cogeneration” plants imposed by law

5. Cost of long-term Power Purchase Agreements (PPAs)

6. Mismanagement of contingent liabilities in the sector

15

Adequate supply for exports

Even with rising demand for electricity, Bulgaria will continue to have a

supply surplus to maintain energy security and facilitate exports

Source: Generation mix projections MEET, alternative demand scenarios calculated by ECA 16

0

10

20

30

40

50

60

70

TW

h

Generation mix (2013-2030) Solar

Wind

Hydro

Factory Power Plants

CoGen

Thermal

Nuclear

Domestic Demand:25% price increase

Exports fall by 5%

Exports fall by 10%

17

Export- historic volumes (quarterly data)

Exports declined but not dramatically

0

0.5

1

1.5

2

2.5

3

3.5

4

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1

2006 2007 2008 2009 2010 2011 2012 2013

GW

h

TR

RS

RO

MK

GR

Exports to Western Balkans and Greece have fallen over the past two years

due to economic downturn. Turkey is now an important off-take market, but its

increase has not fully offset fall in other countries

Additional constraints to exports include:

Access to electricity priced at competitive

levels for the regional market

High transmission fees

Limited grid capacity for export

“Power costs from Bulgaria are

too high. I’m better off selling

power from Hungary to Turkey”

… Power trader

System not dispatched at least cost due to “must-run” plants

18

Supply curve* (least–average cost) Supply curve (with must-run plants)

Simplified supply curve on the left stacks generation options by least average cost order.

Without “must-run” plant constraints, average load could be covered mainly by the

operation of Kozloduy, Maritza 2, HPP, Varna, Bodov Dol and Maritza 3.

The curve on the right shows must-run plants (RES, PPAs and DH) stacked first in order

from the left. Lower cost plants (nuclear, thermal and hydro) are hardly dispatched.

This illustrates the impact of the must-run constraints; it is expensive for the system and

consumers.

* Nuclear do not include costs for decommissioning of existing plants, long-term fuel storage, nor externality costs

19

Long Term Power Purchase Agreements, Cogeneration

and Renewables are a large share of the electricity output

Generation Structure in 2012 (TWh)

Long term power

purchase agreements,

15%

Nuclear power plant,

35% Thermal

plants, 23%

Cogeneration and factory plants, 12%

Renewable energy

sources, 15%

20

Rapid build-up of Renewable Energy (RE) and more

expected

Renewable Generation Capacity as of March 2013

682

980

2183

29

1596

753

214

93

0

500

1000

1500

2000

2500

3000

Wind Power Photovoltaics Hydro Power Bio Power

MW

In operation (as of March 2013) Contracted new capacitySource: MEET

Bulgaria has gone a long way in improving the sector’s environmental sustainability and is

in good track to meet its obligations specified in the EU 20/20 package.

Renewable capacity additions slowed down in 2013 given reductions in feed-in-tariffs. It is

unlikely that a significant amount of the contracted new capacity becomes on-stream.

Development of Renewables driven by high Feed-in-Tariffs

0

50

100

150

200

250

300

350

400

450F

ee

d-i

n-T

ari

ffs

\

EU

RO

/MW

h

Levelized cost per KWh*

FIT PV in Turkey:

104 EURO/MWh

FIT Wind in Turkey:

59 EURO/MWh

* Lower and upper level of the levelized cost of RES calculated assuming weighted average cost of

capital of 7% and 10%, respectively

Source: FIT from MEET and levelized costs calculated by Bank staff

Solar PV (capacity <

5MW)

Solar PV (capacity >

5MW) Onshore Wind

Installed capacity: 980 MW

Installed capacity: 682 MW

21

Worsening generation cost trend – putting pressure on

electricity prices

22

There has been an upward trend in generation costs (fixed+ variable costs) over the

past five years.

The cost of long term agreements and renewables is well above the generation cost of

the rest of State-owned power plants

This will puts pressure on electricity prices.

0

50

100

150

200

250

300

350

200

7

201

0

201

1

201

2

200

7

201

0

201

1

201

2

200

7

201

0

201

1

201

2

200

7

201

0

201

1

201

2

201

2

201

2

201

1

201

2

NPP Kozloduy Maritza East 2 Bobov Dol TPP Varna ME 1 ME 3 RES

BG

N /

MW

h

Evolution of Generation Costs

Variable costs Fixed costs Power Purchase Agreements Average FITs for RES

* Nuclear and do not include costs for decommissioning of existing plants, long-term fuel storage, nor externality

costs. Coal-fired plants do not include externality costs

2.27 1.67

2.26 2.04

8.42

5.34

1.16

0.81

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0

2

4

6

8

10

12

14

1 2

Fin

an

cia

l ga

p a

s %

of G

DP

Net P

rese

nt V

alu

e o

f fina

ncia

l ga

p B

GN

Bill

ion

Renewable Energy FITsHigh Efficiency CogenerationLong Term Power Purchase Agreements

23

NEK prices remain

constant

NEK prices increase by

5% once

Estimated net present value of financial gap until 2030 assuming that only 10 % of RES new contracted

capacity will go on stream and assuming a 5% discount rate.

Growing financial gaps threaten fiscal stability

Total financial gaps til 2030

projected to range from 5 to 20

Billion BGN

Financial deficit in the next 12

months is projected to be

between 800-1,200 Million BGN

Several measures will be

needed to address this gap --

increasing prices is not the only

solution.

% of GDP

% of GDP

Estimated financial gaps resulting from long-term agreements, high efficiency cogeneration, and

renewable energy Feed-in-tariffs (FTIs), net present value 2013-2030

24

Large debt accumulation if no action is taken

Estimated the level of financial gap until 2030 assuming that only 10 % of RES new contracted

capacity will go on stream

3.16

8.47

13.72

20.34

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Billi

on

s B

GN

Total financial gap in nominal termsLong-term Power Purchase AgreementsRenewable energy FITsHigh Efficient Cogeneration

Financial gaps per year resulting from long-term agreements, high efficiency cogeneration, and

renewable energy Feed-in-tariffs (FTIs) in nominal terms

Mismanagement of contingent liabilities

25

• NEK's precarious financial situation is the result of many state actions:

• Generous payments for service delivery for some technologies set by law

• Lack of planning of renewable additions

• Public investments in the power sector handled off budget

• Delays in introducing market reforms (e.g., balancing power market, export)

• No government entity monitoring arrears build-up to assess the consequences on

government finances and the economy.

• Bulgaria lacks a system to properly manage contingent liabilities (e.g. a recording

system in the Ministry of Finance and established legal principles for approving

sub-sovereign liabilities and their provisioning).

• Contingent liabilities that have materialized could be managed more efficiently by

the Ministry of Finance rather than BEH.

25

III. Affordability

26

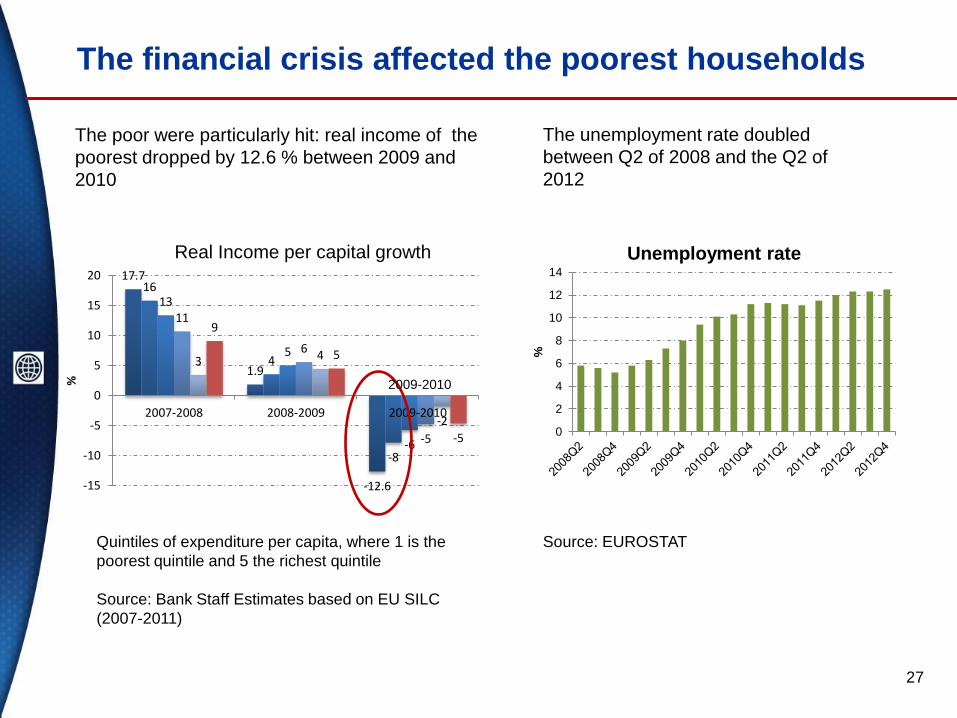

27

The poor were particularly hit: real income of the

poorest dropped by 12.6 % between 2009 and

2010

17.7

1.9

-12.6

16

4

-8

13

5

-6

11

6

-5

3 4

-2

9

5

-5

-15

-10

-5

0

5

10

15

20

2007-2008 2008-2009 2009-2010

%

Real Income per capital growth

Quintiles of expenditure per capita, where 1 is the

poorest quintile and 5 the richest quintile

Source: Bank Staff Estimates based on EU SILC

(2007-2011)

The financial crisis affected the poorest households

0

2

4

6

8

10

12

14

%

Unemployment rate

Source: EUROSTAT

The unemployment rate doubled

between Q2 of 2008 and the Q2 of

2012

2009-2010

28

The poorest spend the most on electricity (up to

9% of their total household expenditures)

Bulgarian households are more reliant on

electricity than households in other EU

Member States

Source: Bank staff estimates, ECAPOV database

Electricity is the most important energy source for households, especially for the poor

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Bu

lga

ria

Esto

nia

Hun

ga

ry

Latv

ia

Lith

uan

ia

Po

lan

d

Rom

an

ia

Sh

are

of e

ne

rgy e

xp

en

ditu

res b

y f

ue

l

Electricity Gas

LPG Wood

Coal District heat and hot water

Solid & Other Fuels

Source: Bank staff estimates, ECAPOV database

29

78% of the energy poor are located in urban areas

Bulgaria (61%) ranks second among countries in Europe and Central Asia, with the

highest rate of energy poor after Hungary (80%) and just before Tajikistan (60%)

* A conventional measure of high spending on energy is energy poverty, defined as spending more than 10 percent of household resources

to cover energy needs

Source: Bank staff estimates, ECAPOV database based on the 2007 HBS

61% of Bulgarian households considered energy poor*

90% 86%

78%

70%

46%

76%

62%

52% 48%

32%

73%

52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5

% o

f e

nerg

y

po

or

Rural Urban Average Rural Average Urban

Quintiles

30

Electricity tariffs hiked in 2012 but still below 2007 levels

Source: Bulgaria National Statistic Institute

Electricity tariffs for households by block of consumption, in real terms

Despite increases, tariffs lowest among EU Member States

31

0.08

0.11

0.13 0.14 0.15 0.15

0.16 0.17 0.17

0.19 0.20 0.21

0.23

0.26

0.30

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35 Retail electricity prices (€ per kWh)

32

0

20

40

60

80

100

120

140

160

2003 2004 2005 2006 2007 2008 2009 2010

Ind

ex

(20

03

=1

00

Expenditure on Social Assistance declined

Pensions Last Resort Social Assistance Housing & utility benefits

Source: World Bank ECA Social Protection Database

Targeted safety nets have been marginalized

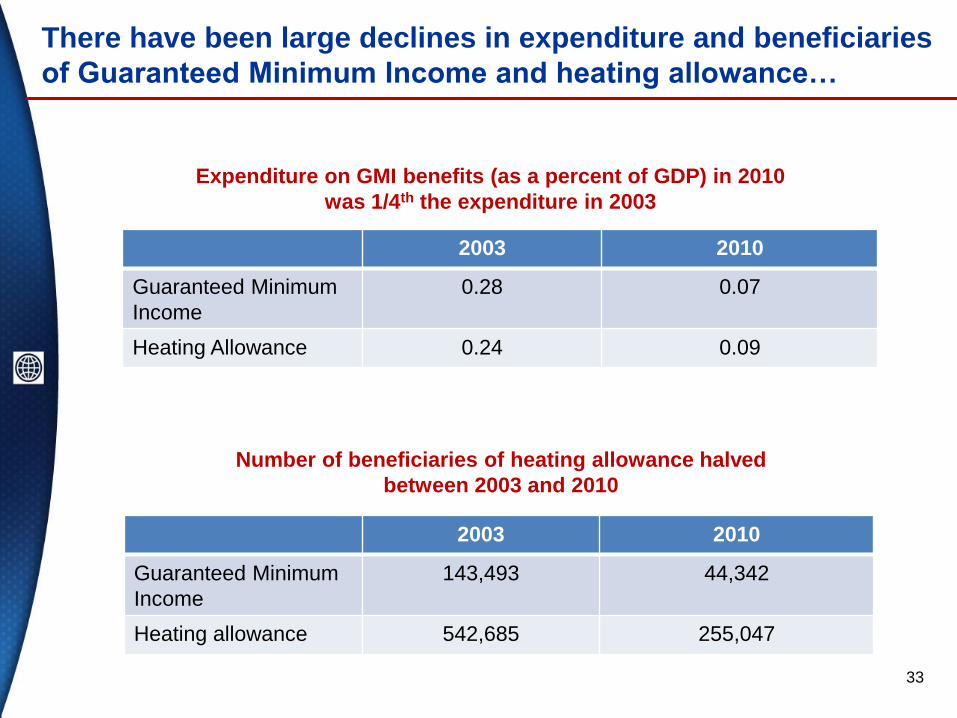

There have been large declines in expenditure and beneficiaries

of Guaranteed Minimum Income and heating allowance…

2003 2010

Guaranteed Minimum

Income

0.28 0.07

Heating Allowance 0.24 0.09

Expenditure on GMI benefits (as a percent of GDP) in 2010

was 1/4th the expenditure in 2003

2003 2010

Guaranteed Minimum

Income

143,493 44,342

Heating allowance 542,685 255,047

Number of beneficiaries of heating allowance halved

between 2003 and 2010

33

34

… as a result, more than 78% of the poor have not been

protected by targeted safety nets

Percentage receiving the Guaranteed

Minimum Income (GMI Benefits) Percentage receiving Heating Allowance

Source: Staff estimates from ECAPOV

Around 78% of the poor were not covered by

the main programs targeted to protect them

88% of the poor did not benefit from the

heating allowance

13%

4% 11%

87 96

89

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Poor Energy Poor Poor and EnergyPoor

88 96

89

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Poor Energy Poor Poor and EnergyPoor

13% 4%

11% 12% 4%

11%

To adequately protect the poor, at least restore budget allocation levels that existed in

the early 2000s

IV. Future Directions

35

Diagnosis and

objective

Package of actions

Immediate Follow-on

Public distrust:

Regain public

confidence by

emphasizing

transparency

Ensure that state officials and senior employees disclose

their financial interests in the energy sector

Dissolve BEH to increase transparency and accountability

of State Owned Enterprises (SOEs)

Grant financial and decision-making independence for the

Regulator as per EU Directives; Establish a plan to build

technical capacity

Eliminate conflicts of interest of state officials and senior

employees

Complete performance benchmarking and service audit in

the energy and mining sectors

Implement merit-based and competitive hiring of

new/replacement Board Members and Senior Management

of SOEs

Establish a power exchange to increase pricing

transparency and cost efficiency

Unsustainable

Cost Structure:

Address growing

deficits in the

sector

Eliminate abuse of preferential pricing for cogeneration

NEK and Ministry of Finance to equitably address

financial liabilities arising from preferential tariffs for

Renewable Energy, long-term agreements, and failed

investments such as Belene

Reduce costs by improving the allocation of generation

quotas in the regulated market and ensuring economic

dispatch

Facilitate exports to increase sector cash flows by

eliminating transmission surcharges and efficient allocation

of cross-border interconnection capacity

Regulator to define medium-term tariff adjustments to

reduce deficits in the sector

Affordability:

Make energy

services

affordable to the

poor

Increase budgetary funding to enhance coverage and

amount of the Guaranteed Minimum Income and Heating

Allowance programs

Scale-up Energy Efficiency (EE) program in the

residential buildings to make energy affordable

Reform the social protection system to improve incentives

to work and consolidate less effective programs

Improve mechanisms to utilize EU structural Funds for

national large-scale (EE) programs

Consult with citizens and other stakeholders to prepare and finalize a Policy Paper that sets the

strategic direction for the recovery and long-term development of the power sector

36

The full package of reforms needed to address the issues in the sector

Disclaimer:

This rapid assessment was conducted by staff of the International Bank for Reconstruction and Development/The World Bank. The findings, interpretations, and conclusions expressed in this assessment do not reflect the views of the Executive Directors of the World Bank or the governments they represent.

This assessment has been undertaken by the World Bank based on data provided by the Bulgarian Ministry of Economy, Energy and Tourism (MEET), the State Water and Energy Regulatory Commission (SWERC), the National Statistical Institute (NSI), and the Ministry of Labor and Social Policy (MLSP).

For questions please contact:

In Sofia: Ms. Ivelina Taushanova, World Bank; 359-2-969-7239; [email protected]

In Washington, DC: Ms. Heather Worley, World Bank; 1-202-458-4857; [email protected]

For more information:

http://www.worldbank.org/en/country/bulgaria

http://www.worldbank.org/content/dam/Worldbank/document/eca/Bulgaria-Snapshot.pdf

37