beverages africa - wesgro africa beverages.pdf · beverages africa ... the united kingdom was the...

TRANSCRIPT

Beverages Africa

Executive Summary

This sector fact sheet provides key trade and investment related statistics for the beverages sector. Specifically, it

shows global trade and investment flows including an analysis of top markets and products for South Africa and

the Western Cape in relation to Africa for the beverages sector. The key highlights in Africa’s beverages sector are

provided below:

Trade

Largest Africa beverage exporters:

South Africa: ZAR13.8bn (59.67% share) of African beverage exports;

Zambia: ZAR2.1bn (8.98% share); and

Namibia: ZAR2bn (8.72% share).

Largest African beverage importers:

South Africa: ZAR6.3bn (17.11% share) of African beverage imports;

Angola: ZAR6.1bn (14.50% share); and

Nigeria: ZAR4.5bn (3.37% share).

Africa’s beverage trade in 2013 amounted to ZAR13.1bn, growing by 35%, the leading traded products were:

Wine of fresh grapes (38% share);

Spirits, liqueurs, other spirit beverages, alcoholic preparations (20% share); and

Non-alcoholic beverages (excl. water, fruit or vegetable juices) (13% share).

South Africa exported beverages to the value of ZAR3.6bn in 2013 to Africa, growing by 27% from the

previous year.

Spirits, liqueurs, other spirit beverages, alcoholic preparations (ZAR10.3bn) were the largest beverage import

into Africa and accounting for 28% of beverages. These were mainly exports of whiskies, rum, vodka and

liqueurs.

Grape wines (ZAR821.1m) were South Africa’s largest beverage export to Africa. The Western Cape was

responsible for 76% of this export.

The Western Cape was responsible for 40% of South Africa total exports of beverages to Africa. In 2013,

Africa was the province’s second largest beverage export market after Europe.

Foreign Direct investment

Between January 2003 and July 2014, Africa received a total of 115 FDI projects into its beverage sector.

These projects represent a total capital investment of ZAR65bn.

The United Kingdom was the largest investor into the African beverages sector, followed by the United States

and the Netherlands. These were also the leading nations into the global beverage sector. South Africa is

currently the 4th largest investor into the African beverages sector.

The majority of outward investment into the global beverages sector was from South Africa into other African

countries.

Outward investment from South Africa to the African beverages market was mainly concerned with

manufacturing activities.

Stellenbosch-based Distell was responsible for all beverage sector investment from the Western Cape. The

group invested into 4 projects since 2006 amounting to ZAR2.75bn and created a total of 670 jobs.

2

Contents

1. Sector Overview .................................................................................................................................. 3

1.1 Global overview .................................................................................................................................. 3

1.2 African beverage overview ................................................................................................................ 4

1.2.1 Beer ....................................................................................................................................................... 4

1.2.2 Wine ...................................................................................................................................................... 4

1.2.3 Recent developments in the African beverage industry ................................................................ 5

2. Trade ..................................................................................................................................................... 6

2.1 African trade of beverages ................................................................................................................ 6

2.2 South African beverage trade ........................................................................................................... 9

2.3 Western Cape beverage trade with Africa .................................................................................... 11

3. Foreign Direct Investment (FDI) ..................................................................................................... 13

3.1 Global FDI into the African beverages .......................................................................................... 13

3.2 African FDI in the global beverage sector ..................................................................................... 16

3.3 South African investment into the African beverages market .................................................... 17

3.3.1 Outward investment from South Africa to the African beverages market ................................. 17

3.4 Western Cape FDI ............................................................................................................................ 17

3.4.1 Outward investment Western Cape to the African beverages market ...................................... 17

3

1. Sector Overview

1.1 Global overview

Global beverage sales have been driven by alcoholic drinks followed closely by soft drinks, these two segments

are projected to grow at a considerable rate in the near future. America and Western Europe are drinking less

mainstream beer on average, the wider beer industry seems to have been re-invigorated by the success of craft

beer, which as an industry has had more success in capturing the evolution of consumers' tastes and preferences.

The ability of craft beer to register sales growth despite this trend reflects its favourable performance.

While commercial beer is on the decline in developed countries, beer has generally done quite well across most of

the big developing economies over recent years (with the exception of Russia), which has been supported

SABMiller's emerging-markets-centric business. While the average Sub-Saharan African and Asian consumer is

either drinking more beer or drinking more expensive beer, the average Western European is drinking less beer

than in recent years. Premium whisky has been alcohol's best performing global areas over the past few years. It

is no surprise that global spirits giants Diageo and Pernod Ricard are increasing their investment into whisky.

Premium blends of Scotch whisky are particularly popular in countries such as China and India.

Global Long-Term Beverage Outlook

Whisky, particularly Scotch whisky, will be outperformers in global premium spirits while energy drinks will

provide considerable opportunities globally, (Business Monitor International, 2014).

Bottled water, juices and energy drinks will be outperformers in global soft drinks.(Business Monitor

International, 2014).

Government legislation will play an increasing role in marginalising unhealthy beverage products.

Governments will increasingly pursue alcohol as an effective means of raising revenue through higher

taxes.

Companies with strong emerging market exposure will largely continue to outperform in sales growth,

although the best opportunities may now be beyond the BRIC countries of Brazil, Russia, India and China.

Emerging-market-based firms will increasingly pursue developed-market investments for the purposes of

diversification and access to stellar brands.

Source: Euromonitor, 2012

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Soft Drinks (USDm) 380 131 415 569 414 351 450 551 498 389 531 248 562 085 595 390 630 431 667 548

Hot Drinks (USDm) 88 614 98 866 98 774 109 143 125 920 133 972 141 533 149 761 158 260 167 470

Alcoholic Drinks (USDm) 491 924 539 475 526 444 564 820 612 416 644 415 677 054 714 096 754 851 802 004

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Valu

e (

US

Dbn)

GLOBAL BEVERAGE RETAIL VALUE RSP, 2007-2016

4

1.2 African beverage overview

1.2.1 Beer

Due to a predominantly young population, rising incomes across the region, and an increasing national self-

confidence, Africa is primed to be a huge target market for the beverage industry. Africa’s emerging middle class

will be the largest trade opportunity for the world’s beverage industry over the next two decades. Producers of

alcoholic beverages, brewers in particular, stand to benefit from the growing consumer market in Africa as more

people on the continent move into higher income groups where resultantly there is a strong growth potential in the

African market as more people move from home-brewed beer and spirits to commercially produced alcohol

(Moody’s 2013)

The beer market in Africa currently represents only 5% of worldwide volumes with four players controlling more

than 80% of the market ;SABMiller plc, Diageo plc, Heineken NV and Castel Group. They have all obtained a first-

mover advantage among brewers operating in the continent. Nigeria is one of the largest Guinness markets in the

world for Diageo, and Sub-Saharan Africa is SABMiller's fastest-growing region. In the premium segment, the

Heineken brand is showing a higher rate of organic growth in Africa and the Middle East than the company's total

volume growth in the region. The overall profitability of alcoholic beverage companies' African operations is high

and most should benefit from continued growth in the premium segment.

Brewers are also using lower-priced alternatives to barley, such as sorghum or cassava, to produce beer tailored

to the local market. The use of locally grown raw materials has in some cases enabled companies to lower excise-

taxes, allowing them to reduce production costs and ensure affordability without lowering profit-margins.

Short term profits could however be limited by potential disruptions in the supply chain including a still-fragile

macroeconomic environment where countries may be subject to exogenous shocks, and regional droughts that

may severely hamper harvests. The large investment needed to run a number of small, regional breweries has

also led to significant cash outlays for brewers in the past. Furthermore, brewing capacity is a constraint and high

capital expenditure is likely to be a drag on free cash flow generation over the next 2-3 years (BancABC, 2013)

1.2.2 Wine

Wine producing regions in Africa

Central Africa

In Tanzania, organic wine is produced at 1100m above sea level, resulting in quality wines with intense bouquets

and personality. The wines are virtually free of acetic acidity, thanks to the optimal conditions in which the grapes

ripen.

Eastern Africa

Tej, also known as honey wine, is a unique drink only common to Ethiopia and Eritrea.

Northern Africa

Given Morocco and Tunisia’s Mediterranean climate, including abundant sun and dry air, it provides ideal

conditions for wine production. Following traditions in French winemaking, vintners have produced a unique and

flavourful assortment of wines. The countryside around Meknes, in the middle Atlas foothills of Morocco, produces

popular and impressive wines.

Western Africa

Palm wine is an incredibly important and popular beverage in West Africa that is consumed by more than 10 million

people. Most palm wine is made from raphia palms. It is normally consumed in a variety of flavours (ranging from

sweet to sour.) In Nigeria, these delicious wines are most popularly known as Emu or Ogogora while in Ghana,

palm wine is affectionately known as Nsafufuo.

Southern Africa

Southern Africa’s primary wine market, South Africa, the 8th largest wine producing country in the world, is the

continent’s leader in terms of quality and volume. Over 100,000 hectares of land is used for wine production. South

Africa’s wines come from the Western Cape region.

5

1.2.3 Recent developments in the African beverage industry

In 2014, beverage giant SABMiller, Gutsche Family Investments (GFI) and the Coca-Cola company have come to

an agreement to combine the bottling operations of their non-alcoholic ready-to-drink beverages businesses in

Southern and East Africa. This merger has led to the formation of Coca-Cola Beverages Africa. The newly formed

entity will service 12 high-growth countries that make up 40% of all Coca-Cola beverage volumes in Africa

(SABMiller, 2014).

In its initial stages Coca-Cola Beverages Africa will manufacture and distribute Coca-Cola beverages in nine

countries: South Africa, Kenya, Ethiopia, Mozambique, Tanzania, Uganda, Namibia, the Comoros and Mayotte.

SABMiller’s Swaziland soft drinks businesses and Zambia- and Botswana-based subsidiaries will be added. This

will also include the acquisition of or licensing rights for an additional 19 non-alcoholic ready-to-drink brands owned

by SABMiller and available in Africa and Latin America.

As one of the top 10 largest Coca-Cola bottling partners worldwide, Coca-Cola Beverages Africa can leverage the

scale, resources, capability and efficiency needed to accelerate Coca-Cola’s growth, and contribute to the

economic and social prosperity of African communities.

SABMiller Chief Executive Alan Clark said the soft drinks market is a significant part of the group’s growth strategy.

“This transaction increases our exposure to the total beverage market in Africa. The opportunity is significant, with

favourable demographics and economic development pointing to excellent growth prospects.”

According to Sharenet (2015), Ethiopian Greenfield brewer Habesha, majority-owned by Dutch brewer Bavaria NV,

said it plans to start selling beer in the second quarter of this year to tap rising domestic demand that has attracted

global brands. Bavaria NV is the latest beer maker lured by Ethiopia's expanding middle class over the last five

years and will compete with breweries owned by Heineken and Diageo.

The world’s leading brewers have turned their focus on emerging markets such as Africa as consumer demand in

Europe has stagnated and the United States offers limited expansion opportunities.

Ethiopia’s average annual beer consumption of less than five litres per capita is about half the average for sub-

Saharan Africa, excluding South Africa, offering scope for expansion among the population of 94 million. Bavaria

NV bought a stake in Habesha Breweries in 2012, and has since increased its holding to 60 percent. Habesha's

plant in Debre Birhan, will have a capacity to produce 350,000 hectolitres once it is completed, although production

will start before then. Heinekens USD130 million brewery near Addis Ababa is the largest in Ethiopia with a capacity

of 1.5 million hectolitres. The Dutch firm also owns the Bedele and Harar breweries it purchased from the state for

a combined USD163 million in 2011.

6

2. Trade

2.1 African trade of beverages

Since 2006 Africa has been a net importer of beverages and recovered successive trade deficits. These deficits

are the result of the lack of production capacity on the African continent to meet the growing demand. Demand is

set to continue to outstrip supply for the foreseeable future as countries’ young populations become more

developed and urbanized, leading to readymade beverages to be increasingly demanded. Africa showed

encouraging signs in its export potential with exports increasing by 35%.

Source: TradeMap, 2015

With its well developed and self-sufficient beverage market, South Africa is the largest exporter of beverages in

Africa and its exports amounted to 60% imports of African exports. Zambia’s beer market has experienced

considerable growth in the past few years. This is evident in Zambia’s ranking as the second largest exporter as

exports grew by a resounding 5000%. Namibia completed the top 3 export markets exporting beverages to the

value of ZAR2bn in 2015. The common denominator between the 3 markets is the presence of large brewing

companies namely South African breweries, Zambian Breweries and Namibian breweries.

As with imports, South Africa was Africa’s the largest import market, importing 18% of all Africa’s beverages which

equates to ZAR6.3bn. With the presence of most beverage segments in the South African markets, spirit imports

would constitute the majority of its imports. Angola was the second largest export market in 2013. With one of the

largest growing economies in Sub Saharan Africa, Angola has an ever growing demand for all basic food stuffs

due to shortage of manufacturing and bottling plants. The largest economy in Africa, Nigeria, was the third largest

import market, its imports however grew the least within the top import markets.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Exports (ZARm) 6 165,5 7 294,1 7 004,8 9 355,3 12 970,6 13 734,9 14 862,9 15 435,2 17 148,5 23 099,0

Imports (ZARm) 5 794,0 6 525,2 9 120,4 13 553,4 16 910,7 17 558,2 17 918,5 21 650,9 29 813,5 36 778,0

Trade Balance (ZARm) 371,5 769,0 -2 115,6 -4 198,1 -3 940,1 -3 823,3 -3 055,7 -6 215,7 -12 665,1 -13 679,0

-20 000

-10 000

0

10 000

20 000

30 000

40 000

Valu

e (

ZA

Rm

)

AFRICA'S BEVERAGE TRADE, 2004-2013

7

TOP 10 AFRICAN EXPORT MARKETS FOR BEVERAGES, 2013 TOP 10 AFRICAN IMPORT MARKETS FOR BEVERAGES, 2013

RANK

DESTINATION COUNTRY

VALUE 2013 (ZARm)

% GROWTH 2012-2013

% SHARE 2013

RANK DESTINATION

MARKETS

VALUE 2013

(ZARm)

% GROWTH 2012-2013

% SHARE

2013

1 South Africa 13 782.60 32.20% 59.67% 1 South Africa 6 292.5 17.97% 17.11%

2 Zambia 2 073.32 5029.57% 8.98% 2 Angola 6 080.9 14.50% 16.53%

3 Namibia 2 015.16 2.29% 8.72% 3 Nigeria 4 527.6 3.37% 12.31%

4 Uganda 576.64 20.14% 2.50% 4 Namibia 1 873.9 47.50% 5.10%

5 Ghana 467.36 99.94% 2.02% 5 Ghana 1 243.6 22.36% 3.38%

6 Tunisia 426.95 29.07% 1.85% 6 Equatorial Guinea 1 118.3 35.96% 3.04%

7 Kenya 419.08 -9.31% 1.81% 7 Democratic Republic of the Congo

1 058.9 128.85% 2.88%

8 Togo 372.90 116.76% 1.61% 8 Libya 1 010.6 34.00% 2.75%

9 Egypt 334.46 -12.07% 1.45% 9 Algeria 923.0 49.27% 2.51%

10 Algeria 330.72 24.67% 1.43% 10 Egypt 838.5 38.96% 2.28%

TOTAL EXPORTS 23 099.02 100.00% 34.70% TOTAL EXPORTS 36 778.0 23.36% 100.00%

Source: TradeMap, 2015

Largely due to South Africa’s prowess in viticulture and wine make, wine from fresh grapes (ZAR8.9bn) was the

largest beverage export from Africa. The wine exports were mainly of fortified wines and grape wines. Spirits,

liqueurs, other spirit beverages, alcoholic preparations (ZAR4.5bn) (mainly liqueurs and cordials) and non-alcoholic

beverages (excl. water, fruit or vegetable juices) were the second and third largest exports.

Spirits, liqueurs, other spirit beverages, alcoholic preparations (ZAR10.3bn) were the largest beverage import into

Africa and accounting for 28% of beverages. Non-alcoholic beverages (excl. water, fruit or vegetable juices)

(ZAR7.9bn) were the second largest import and the only beverage product to experience a decline in imports.

Growing by 17%, beer made from malt (ZAR6.8bn) was the 3rd largest import, as African consumers move from

home produced beers to commercially produced, this number is set to increase and South African brewers with its

footprint in most African countries, is perfectly placed to take advantage of this. South Africa also has a comparative

advantage in producing wines and would do well to forge relationships with local suppliers and reduce red tape to

expand its supply into African countries. In this instance, companies like Distell come to mind as incomes increase

and the middle class starts to swell there are opportunities for shift exports from bulk wine to premium brands.

AFRICA’S EXPORTS OF BEVERAGES, 2013 AFRICA’S IMPORTS OF BEVERAGES, 2013

RANK HS

CODE PRODUCT

VALUE 2013

(ZARm)

% GROWTH 2012-2013

RANK HS

CODE PRODUCT

VALUE 2013

(ZARm)

% GROWTH 2012-2013

1 2204 Wine of fresh grapes 8 887.3 34.39% 1 2208 Spirits, liqueurs, other spirit beverages, alcoholic preparations

10 266.4 50%

2 2208 Spirits, liqueurs, other spirit beverages, alcoholic preparations

4 546.9 114.84% 2 2202 Non-alcoholic beverages (excl. water, fruit or vegetable juices)

7 872.9 -1%

3 2202 Non-alcoholic beverages (excl. water, fruit or vegetable juices)

3 046.8 55.74% 3 2203 Beer made from malt 6 817.8 17%

4 2203 Beer made from malt 2 911.3 15.25% 4 2204 Wine of fresh grapes 6 455.7 47%

5 2207 Ethyl alcohol & other spirits (if undenatured then higher than 80% by

2 358.6

19.72% 5 2207 Ethyl alcohol & other spirits (if undenatured then higher than 80% by

3 476.5 9%

6 2206 Fermented beverages, nes

1 165.2 -5.70% 6 2206 Fermented beverages 1 268.9 12%

7 2201 Mineral & aerated waters 164.8 -77.00% 7 2201 Mineral & aerated waters

475.7 21%

8 2205 Vermouth & other grape wine flavoured with plants or aromatic substances

18.1

26.92% 8 2205 Vermouth & other grape wine flavoured with plants or aromatic substances

144.2

43%

TOTAL EXPORTS 23 099.0 34.70% TOTAL IMPORTS 36 778.0 23.3

Source: TradeMap, 2015

8

The top export products to each of the top 5 export markets are listed below:

South Africa

Wine of fresh grapes (ZAR1129.7m)

Spirits, liqueurs, other spirit beverages, alcoholic preparations (ZAR1035.1m)

Non-alcoholic beverages (excl. water, fruit or vegetable juices) (ZAR813.8m)

Zambia

Spirits, liqueurs, other spirit beverages, alcoholic preparations (ZAR356.4m)

Non-alcoholic beverages (excl. water, fruit or vegetable juices) (ZAR189.4m)

Wine of fresh grapes (ZAR47.5m)

Namibia

Beer made from malt (ZAR1427.5m)

Fermented beverages, (ZAR266.4m)

Spirits, liqueurs, other spirit beverages, alcoholic preparations (ZAR202.8m)

Uganda

Beer made from malt (ZAR226.8m)

Non-alcoholic beverages (excl. water, fruit or vegetable juices) (ZAR218.9m)

Spirits, liqueurs, other spirit beverages, alcoholic preparations (ZAR64.8m)

Ghana

Spirits, liqueurs, other spirit beverages, alcoholic preparations (ZAR341.4m)

Ethyl alcohol & other spirits (if undenatured then higher than 80% ) (ZAR106.8m)

Non-alcoholic beverages (excl. water, fruit or vegetable juices ) (ZAR9.4m)

9

2.2 South African beverage trade

South Africa’s beverage trade has been characterised by a positive trade balance for the past ten years backed by

strong export performance. As the most developed economy in Africa, South Africa is globally competing and

established companies, manufacturing plants and distribution channels are represented in most beverage

segments. In 2014, South Africa recorded its largest export surplus as a result of a 27 % growth in exports with

imports remaining subdued.

Source: Quantec, 2015

The table below shows South Africa’s top African export destination markets for beverages. These markets

accounted for ZAR2.3bn of South Africa’s beverage exports equating to 65% of total exports to Africa. The amounts

shaded in grey represent the country that imported the largest amount of that particular product. Angola was the

largest importer of three of South Africa’s beverage products with Mozambique importing the largest amount of

malt made beer.

SOUTH AFRICA'S TOP 5 BEVERAGE AFRICAN EXPORT DESINATIONS AND PRODUCTS

PRODUCT (HS:4) ANGOLA (ZARm)

MOZAMBIQUE (ZARm)

NIGERIA (ZARm)

ZAMBIA (ZARm)

ZIMBABWE (ZARm)

Liqueur, spirits and undenatured ethyl alcohol <80%

223.18 46.25 58.24 83.42 45.11

Grape wines(including fortified), alcoholic grape must

161.81 113.28

86.70 58.25 34.37

Fermented beverages nes (eg cider, perry, mead) 139.77 45.47 6.23 41.33 25.47

Ethyl alcohol, undenatured and > 80%, or denatured

24.23 42.46 98.18 71.52 11.87

Waters, non-alcoholic sweetened or flavoured beverages

12.13 62.56 0.92 115.74 252.03

Unsweetened beverage waters, ice and snow 2.11 3.64 0.01 2.28 5.47

Beer made from malt 0.00 345.21 0.00 74.15 26.30

Vermouth and other flavoured grape wine - 0.10 0.99 0.06 0.06

TOTAL 563.22 658.96 251.28 446.75 400.68

Source: Quantec, 2015

Unsurprisingly grape wines (ZAR821.1m) were the largest exports from South Africa, this is mainly to the nation’s

prowess in production. Waters, non-alcoholic sweetened or flavoured beverages (ZAR745.5m) and ethyl alcohol,

undenatured and > 80%, or denatured (ZAR610.3m) were the second and third largest exports. Barring exports of

liqueur, spirits and undenatured ethyl alcohol <80% and fermented beverages, most of South Africa’s beverage

exports experience healthy growth. Exports of vermouth and other flavoured grape wine grew the strongest in

2013, Africa is currently South Africa’s second largest export market for this product. Nigeria, Kenya and Congo

imported the lion’s share of vermouth and other flavoured grape wine from South Africa.

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARm) 726,6 739,7 1 052,0 1 772,9 1 917,3 2 292,1 2 000,5 2 390,7 2 799,4 3 556,2

Imports (ZARm) 14,0 21,4 13,7 36,7 38,3 68,4 57,9 67,8 86,5 87,9

Trade Balance (ZARm) 712,6 718,3 1 038,3 1 736,2 1 879,0 2 223,7 1 942,6 2 322,9 2 712,9 3 468,3

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

Valu

e (

ZA

Rm

)

SOUTH AFRICAN TRADE OF BEVERAGES WITH AFRICA, 2005-2014

10

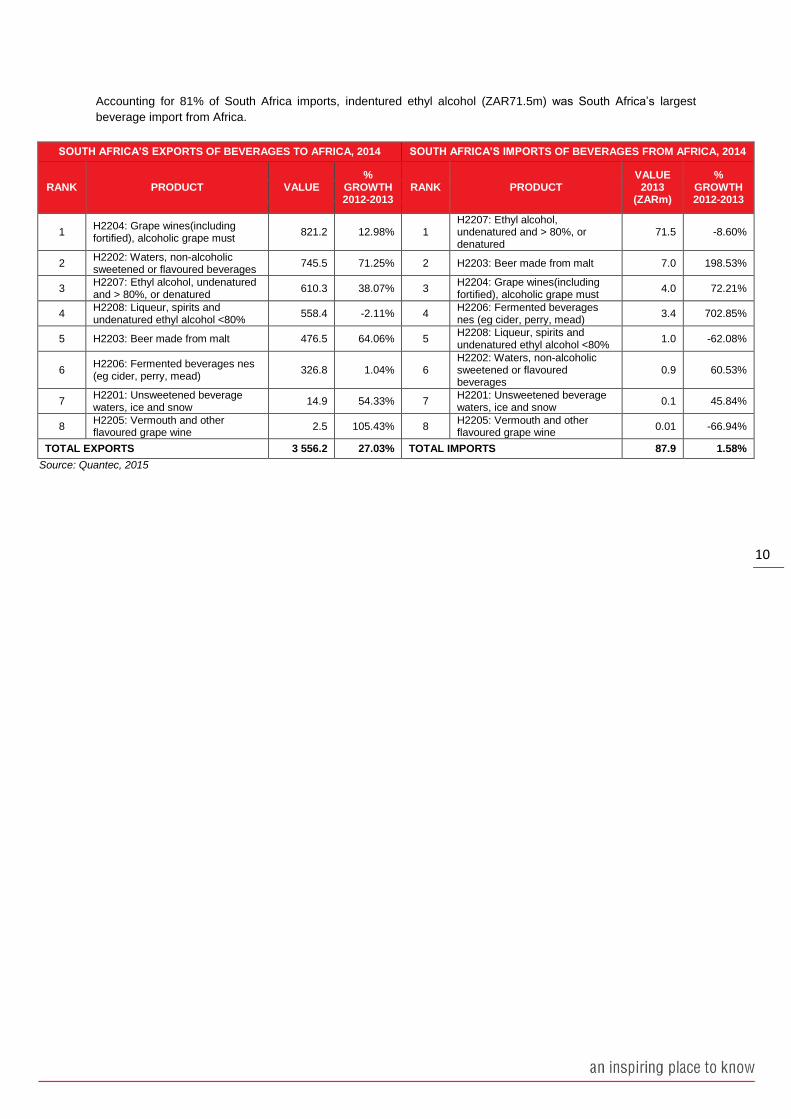

Accounting for 81% of South Africa imports, indentured ethyl alcohol (ZAR71.5m) was South Africa’s largest

beverage import from Africa.

SOUTH AFRICA’S EXPORTS OF BEVERAGES TO AFRICA, 2014 SOUTH AFRICA’S IMPORTS OF BEVERAGES FROM AFRICA, 2014

RANK PRODUCT VALUE %

GROWTH 2012-2013

RANK PRODUCT VALUE

2013 (ZARm)

% GROWTH 2012-2013

1 H2204: Grape wines(including fortified), alcoholic grape must

821.2 12.98% 1 H2207: Ethyl alcohol, undenatured and > 80%, or denatured

71.5 -8.60%

2 H2202: Waters, non-alcoholic sweetened or flavoured beverages

745.5 71.25% 2 H2203: Beer made from malt 7.0 198.53%

3 H2207: Ethyl alcohol, undenatured and > 80%, or denatured

610.3 38.07% 3 H2204: Grape wines(including fortified), alcoholic grape must

4.0 72.21%

4 H2208: Liqueur, spirits and undenatured ethyl alcohol <80%

558.4 -2.11% 4 H2206: Fermented beverages nes (eg cider, perry, mead)

3.4 702.85%

5 H2203: Beer made from malt 476.5 64.06% 5 H2208: Liqueur, spirits and undenatured ethyl alcohol <80%

1.0 -62.08%

6 H2206: Fermented beverages nes (eg cider, perry, mead)

326.8 1.04% 6 H2202: Waters, non-alcoholic sweetened or flavoured beverages

0.9 60.53%

7 H2201: Unsweetened beverage waters, ice and snow

14.9 54.33% 7 H2201: Unsweetened beverage waters, ice and snow

0.1 45.84%

8 H2205: Vermouth and other flavoured grape wine

2.5 105.43% 8 H2205: Vermouth and other flavoured grape wine

0.01 -66.94%

TOTAL EXPORTS 3 556.2 27.03% TOTAL IMPORTS 87.9 1.58%

Source: Quantec, 2015

11

2.3 Western Cape beverage trade with Africa

The province’s beverage trade mirrors that of South Africa. The Western Cape has been a strong exporter of

beverages to Africa for the past ten years and has continually maintained a trade surplus. In 2013, provincial

exports reached their peak by growing by 36% from 2012 while imports declined by 88%.

The Western Cape was responsible for 40% of South Africa’s total exports of beverages to Africa. In 2013, Africa

was the province’s second largest beverage export market after Europe.

Source: Quantec, 2015

The table below shows the Western Cape’s top African export destinations markets for beverages. These markets

accounted for ZAR1.1bn of the province’s beverage exports equating to 75% of total exports to Africa. With the

exception of Kenya, the province has the same top export destinations as South Africa. Western Cape beverages

seem to be well received by the Angolan market as it is the largest importer across most beverages categories.

The Western Cape has an export advantage with its proximity to the West African market, it is also encouraging to

see that the province is making inroads into east Africa.

WESTERN CAPE'S TOP 5 BEVERAGE AFRICANEXPORT DESTINATIONS AND PRODUCTS

PRODUCT (HS:4) ANGOLA (ZARm)

KENYA (ZARm)

MOZAMBIQUE (ZARm)

NIGERIA (ZARm)

ZIMBABWE (ZARm)

Grape wines(including fortified), alcoholic grape must 150.77 93.05 33.08 105.96 31.54

Liqueur, spirits and undenatured ethyl alcohol <80% 298.68 28.64 22.17 54.81 19.25

Fermented beverages nes (eg cider, perry, mead) 159.57 0.89 12.67 14.24 15.41

Waters, non-alcoholic sweetened or flavoured beverages

9.58 0.02 6.02 0.38 7.12

Beer made from malt 0.01 - 0.42 0.00 0.74

Unsweetened beverage waters, ice and snow 2.22 0.16 0.71 0.02 0.05

Vermouth and other flavoured grape wine 0.05 0.04 0.02 0.02 -

Ethyl alcohol, undenatured and > 80%, or denatured 0.00 - 0.10 - -

TOTAL 620.89 122.80 75.18 175.44 74.10

Source: Quantec, 2015

The Western Cape is South Africa’s largest grape producing region, it is thus unsurprising that grape wines were

the largest beverage export from the province and made up 44% of the province’s exports to Africa. With the

province’s prowess at wine production also comes its brandy and spirit production. The Western Cape is known

for making some of the best brandy’s which compete internationally and some premiums brands like Van Ryns

compete with French made cognac on the quality level.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Exports (ZARm) 170,6 235,1 266,4 400,6 671,8 692,8 850,5 1 084,6 1 134,9 1 412,5

Imports (ZARm) 4,5 10,7 7,1 6,0 11,1 17,4 8,2 9,4 18,6 2,2

Trade Balance (ZARm) 166,1 224,3 259,3 394,6 660,6 675,4 842,3 1 075,1 1 116,3 1 410,3

0

200

400

600

800

1 000

1 200

1 400

1 600

Valu

e (

ZA

Rm

)

WESTERN CAPE BEVERAGE TRADE WITH AFRICA, 2004-2013

12

Subsequently liqueur, spirits and undenatured ethyl alcohol <80% (ZAR474.5m) was the provinces second largest

export. Fermented beverages (ZAR267m) was the third largest exports, cider companies based in the Western

Cape benefit from their access for fresh produce.

As with national imports undenatured liqueur, spirits and ethyl alcohol (ZAR1.8m) was the province’s largest import

in 2013.

WESTERN CAPE’S EXPORTS OF BEVERAGES TO AFRICA, 2013 WESTERN CAPE’S IMPORTS OF BEVERAGES FROM AFRICA, 2013

RANK PRODUCT VALUE

2013 (ZAR)

% GROWTH 2012-2013

RANK PRODUCT VALUE

2013 (ZAR)

% GROWTH 2012-2013

1 H2204: Grape wines(including fortified), alcoholic grape must

620 381 243 27.75% 1 H2208: Liqueur, spirits and undenatured ethyl alcohol <80%

1 847 309 -15%

2 H2208: Liqueur, spirits and undenatured ethyl alcohol <80%

474 463 327 27.67% 2 H2204: Grape wines(including fortified), alcoholic grape must

289 642 -97%

3 H2206: Fermented beverages nes (eg cider, perry, mead)

267 532 373

14.59% 3 H2207: Ethyl alcohol, undenatured and > 80%, or denatured

46 340 -99%

4 H2202: Waters, non-alcoholic sweetened or flavoured beverages

41 409 388

20.51% 4 H2203: Beer made from malt 25 477 17470%

5 H2201: Unsweetened beverage waters, ice and snow

4 280 184 0.74% 5 H2202: Waters, non-alcoholic sweetened or flavoured beverages

18 382 -91%

6 H2203: Beer made from malt 4 178 031 5.41% 6 H2201: Unsweetened beverage waters, ice and snow

731 -3%

7 H2205: Vermouth and other flavoured grape wine

184 868 -85.37%

8 H2207: Ethyl alcohol, undenatured and > 80%, or denatured

117 924 -59.86%

TOTAL EXPORTS 1 412 547 338 24.47% TOTAL IMPORTS 2 227 881 -88%

Source: Quantec, 2015

Below are the Western Cape’s main exported beverages and their national export shares:

Grape wines (including fortified), alcoholic grape must,(ZAR620.4m) accounted for 44% of Western Cape

beverage exports and 76% of all the national exports were produced in Western Cape.

Liqueur, spirits and undenatured ethyl alcohol <80 %,( ZAR474.5m) accounted for 34% of Western Cape

beverage exports and 58% of all the national exports was produced in Western Cape.

Fermented beverages, (ZAR267.5m) accounted for 18.94% of Western Cape beverage exports and 33%

of all the national export was produced in Western Cape.

13

3. Foreign Direct Investment (FDI)

3.1 Global FDI into the African beverages

Between January 2003 and July 2014 a total of 115 FDI projects were recorded into the African beverage sector

from the world. These projects represent a total capital investment of ZAR64.96bn which is an average investment

of ZAR564.76m per project. During the period, a total of 22,755 jobs were created. Global investment into the

sector reached its peak in 2011. With the exception of 2012, Africa has received more than 10 projects since 2008.

Source: FDI Intelligence, 2015

The United Kingdom was the largest investor into the African beverages sector. Investments by British companies

into the sector accounted for 40% of capital expenditure (Capex) and 30% of projects. The United States (26

projects and ZAR9.3bn Capex) and the Netherlands (10 projects and ZAR11.5bn Capex) were the second and

third largest global investors respectively. The same markets were the largest investors into the global beverages

market. With 4 companies responsible for 8 projects and ZAR3.5bn, South Africa was the 4th largest investor in the

African beverage sector. For a country that is on the continent, more needs to be done to get a larger footprint and

influence in more African countries.

SOURCE MARKETS FOR GLOBAL FDI INTO THE AFRICAN BEVERAGES SECTOR JAN 2003-JULY 2014

RANK SOURCE COUNTRY PROJECTS %

PROJECTS CAPEX (ZARm)

% CAPEX

COMPANIES %

COMPANIES

1 United Kngdom 45 39.13% 26 262.60 40.43% 17 30.36%

2 United States 26 22.61% 9 329.10 14.36% 7 12.50%

3 Netherlands 10 8.70% 11 536.60 17.76% 4 7.14%

4 South Africa 8 6.96% 3 496.40 5.38% 4 7.14%

5 Portugal 6 5.22% 3 221.00 4.96% 5 8.93%

6 India 4 3.48% 1 209.20 1.86% 3 5.36%

7 UAE 3 2.61% 550.70 0.85% 3 5.36%

8 Saudi Arabia 3 2.61% 3 035.90 4.67% 3 5.36%

9 Mauritius 1 0.87% 653.80 1.01% 1 1.79%

10 Switzerland 1 0.87% 493.30 0.76% 1 1.79%

Other Countries 8 6.96% 5 171.80 7.96% 8 14.29%

TOTAL 115 100.00% 64 960.40 100.00% 56 100.00%

Source: FDI Intelligence, 2015

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Capex (ZARm) 7 937, 2 455, 3 940, 638,6 500,3 10 737 6 839, 4 075, 14 266 3 221, 4 359, 5 988,

Projects 10 5 4 4 2 19 13 11 21 8 11 7

0

5

10

15

20

25

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

Pro

jects

Valu

e (

ZA

Rm

)

INWARD FDI INTO AFRICA'S BEVERAGE SECTOR, 2003-JULY 2014

14

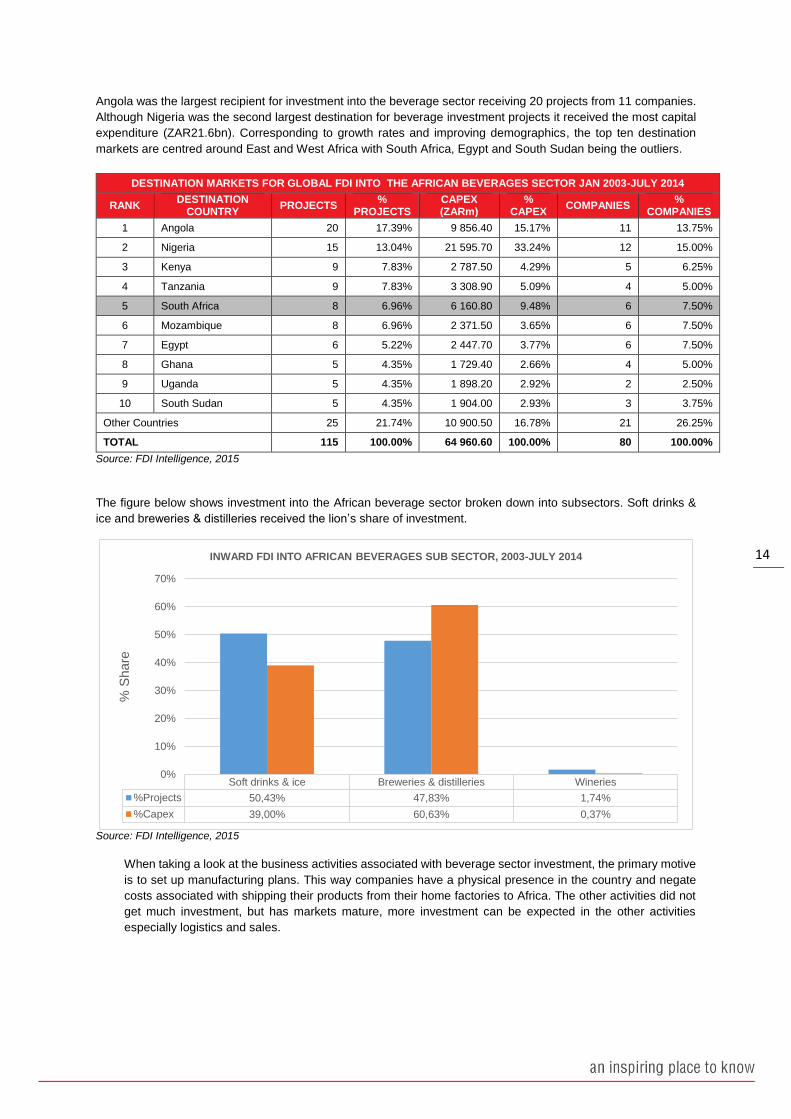

Angola was the largest recipient for investment into the beverage sector receiving 20 projects from 11 companies.

Although Nigeria was the second largest destination for beverage investment projects it received the most capital

expenditure (ZAR21.6bn). Corresponding to growth rates and improving demographics, the top ten destination

markets are centred around East and West Africa with South Africa, Egypt and South Sudan being the outliers.

DESTINATION MARKETS FOR GLOBAL FDI INTO THE AFRICAN BEVERAGES SECTOR JAN 2003-JULY 2014

RANK DESTINATION

COUNTRY PROJECTS

% PROJECTS

CAPEX (ZARm)

% CAPEX

COMPANIES %

COMPANIES

1 Angola 20 17.39% 9 856.40 15.17% 11 13.75%

2 Nigeria 15 13.04% 21 595.70 33.24% 12 15.00%

3 Kenya 9 7.83% 2 787.50 4.29% 5 6.25%

4 Tanzania 9 7.83% 3 308.90 5.09% 4 5.00%

5 South Africa 8 6.96% 6 160.80 9.48% 6 7.50%

6 Mozambique 8 6.96% 2 371.50 3.65% 6 7.50%

7 Egypt 6 5.22% 2 447.70 3.77% 6 7.50%

8 Ghana 5 4.35% 1 729.40 2.66% 4 5.00%

9 Uganda 5 4.35% 1 898.20 2.92% 2 2.50%

10 South Sudan 5 4.35% 1 904.00 2.93% 3 3.75%

Other Countries 25 21.74% 10 900.50 16.78% 21 26.25%

TOTAL 115 100.00% 64 960.60 100.00% 80 100.00%

Source: FDI Intelligence, 2015

The figure below shows investment into the African beverage sector broken down into subsectors. Soft drinks &

ice and breweries & distilleries received the lion’s share of investment.

Source: FDI Intelligence, 2015

When taking a look at the business activities associated with beverage sector investment, the primary motive

is to set up manufacturing plans. This way companies have a physical presence in the country and negate

costs associated with shipping their products from their home factories to Africa. The other activities did not

get much investment, but has markets mature, more investment can be expected in the other activities

especially logistics and sales.

Soft drinks & ice Breweries & distilleries Wineries

%Projects 50,43% 47,83% 1,74%

%Capex 39,00% 60,63% 0,37%

0%

10%

20%

30%

40%

50%

60%

70%

% S

hare

INWARD FDI INTO AFRICAN BEVERAGES SUB SECTOR, 2003-JULY 2014

15

Source: FDI Intelligence, 2015

The table below shows the companies making the most investments into the African beverage sector. Soft drinks

giant, Coca Cola lead the way with 18 projects. However it was the beer companies, SABMiller and Heineken that

there involved in the more capital intensive projects. In this regard Heineken made the largest investment per

project (ZAR1.3bn) amongst the top companies.

COMPANIES INVESTING INTO THE BEVERAGES SECTOR ,2003- JULY 2014

RANK INVESTING COMPANY SOURCE COUNTRY BUSINESS ACTIVITY

PROJECTS CAPEX (ZARm)

1 Coca-Cola United States Manufacturing 18 5 973.40

2 SABMiller UK Manufacturing 12 8 184.40

3 Heineken Netherlands Manufacturing 6 7 742.60

4 Tanzania Breweries Limited (TBL)

Tanzania Manufacturing 6 2 418.40

5 NILE Breweries (NBL) Uganda Manufacturing 4 1 675.50

6 Lonrho Springs UK Manufacturing 4 432.40

7 Distell Group South Africa Manufacturing 4 2 746.50

8 Guinness Nigeria UK Manufacturing 3 3 469.40

9 Coca-Cola Bottling (Luanda) United States Manufacturing 3 1 426.00

10 Zambian Breweries Plc Zambia Manufacturing 2 799.10

TOTAL 115 64 960.70

Source: FDI Intelligence, 2015

ManufacturingSales, Marketing &

Support

Logistics,Distribution &Transportation

HeadquartersDesign,

Development &Testing

%Projects 85,22% 6,96% 4,35% 2,61% 0,87%

%Capex 95,62% 2,58% 0,76% 0,94% 0,11%

0%

20%

40%

60%

80%

100%

% S

ha

reGLOBAL FDI INTO THE AFRICAN BEVERAGES SECTOR BY BUSINESS ACTIVITY 2003 - JULY

2014

16

3.2 African FDI in the global beverage sector

Between January 2003 and July 2014 a total of 14 FDI projects were recorded from Africa into the global beverages

sector. These projects represent a total capital investment of ZAR5.40bn which is an average investment of

ZAR385.49m per project. During the period, a total of 1,711 jobs were created. The majority of their investment

were from South Africa into other African countries. Most of the projects were concerned with manufacturing of

beverages.

OUTWARD FDI FROM AFRICAN COMPANIES INTO THE GLOBAL BEVERAGE SECTOR, 2003- JULY 2014

DATE INVESTING COMPANY

SOURCE COUNTRY

DESTINATION STATE

SUB-SECTOR INDUSTRY ACTIVITY CAPEX (ZARm)

JOBS

Jun-14 Distell Group South Africa Angola Breweries & distilleries Manufacturing 616.3 222

Jun-14 Distell Group South Africa Nigeria Breweries & distilleries Manufacturing 1 713.0 222

Apr-14 Distell Group South Africa Ghana Breweries & distilleries Manufacturing 399.6 222

Sep-13 East Africa Bottling Share

South Africa Ethiopia Soft drinks & ice Manufacturing 152.3 52

Sep-13 East Africa Bottling Share

South Africa Ethiopia Soft drinks & ice Manufacturing 234.3 81

Feb-11 First National Choice South Africa Mozambique Soft drinks & ice Manufacturing 70.3 24

Apr-10 Kasapreko Ghana Nigeria Breweries & distilleries Manufacturing 117.2 40

Jul-08 Bright World South Africa Hong Kong Wineries Logistics, Distribution & Transportation

411.3 92

Apr-08 Phoenix Beverages Mauritius Madagascar Breweries & distilleries Manufacturing 653.8 225

May-06 Kenya Maltings Kenya Uganda Breweries & distilleries Sales, Marketing & Support

222.6 22

Mar-06 Distell Group South Africa Namibia Wineries Logistics, Distribution & Transportation

17.6 4

Feb-05 Lourensford Wines South Africa India Wineries Manufacturing 460.5 199

May-04 Coca-Cola Sabco South Africa Kenya Soft drinks & ice Manufacturing 292.9 300

Jun-03 Specialist Mechanical Engineers (SME)

South Africa UAE Soft drinks & ice Manufacturing 35.2 6

Source: FDI Intelligence, 2015

17

3.3 South African investment into the African beverages market

3.3.1 Outward investment from South Africa to the African beverages market

Between January 2003 and July 2014 a total of 8 FDI projects were recorded from South Africa into the African

beverages sector. These projects represent a total capital investment of ZAR3.50bn which is an average

investment of ZAR437.05m per project. During the period, a total of 1,127 jobs were created. The investment

projects were equally shared among the breweries & distilleries and soft drinks & ice sub sectors. The projects

were mainly concerned with manufacturing activities with the exception of logistics, distribution & transportation for

the investment into wineries.

OUTWARD FDI FROM SOUTH AFRICA TO THE AFRICAN BEVERAGES SECTOR, JANUARY 2003- JULY 2014

DATE INVESTING COMPANY

SOURCE STATE

DESTINATION COUNTRY

SUB-SECTOR INDUSTRY ACTIVITY CAPEX JOBS

Jun-14 Distell Group Western Cape Angola Breweries & distilleries Manufacturing 616.3 222

Jun-14 Distell Group Western Cape Nigeria Breweries & distilleries Manufacturing 1 713.0 222

Apr-14 Distell Group Western Cape Ghana Breweries & distilleries Manufacturing 399.6 222

Sep-13 East Africa Bottling Share

Eastern Cape Ethiopia Soft drinks & ice Manufacturing 152.3 52

Sep-13 East Africa Bottling Share

Eastern Cape Ethiopia Soft drinks & ice Manufacturing 234.3 81

Feb-11 First National Choice

Eastern Cape Mozambique Soft drinks & ice Manufacturing 70.3 24

Mar-06 Distell Group Western Cape Namibia Wineries Logistics, Distribution & Transportation

17.6 4

May-04 Coca-Cola Sabco Eastern Cape Kenya Soft drinks & ice Manufacturing 292.9 300

Source: FDI Intelligence, 2015

*There has not been any recorded fdi into South Africa from African countries

3.4 Western Cape FDI

3.4.1 Outward investment Western Cape to the African beverages market

Stellenbosch-based Distell was responsible of all beverage sector investment from the Western Cape. The group

invested into 4 projects since 2006 amounting to ZAR2.75bn and created a total of 670 jobs. The largest investment

was into Nigeria in 2014 as the company setting up a manufacturing plant for brewing and distilling.

OUTWARD FDI FROM THE WESTERN CAPE INTO AFRICAN BEVERAGES SECTOR, 2003- JULY 2014

DATE INVESTING COMPANY

SOURCE CITY

DESTINATION COUNTRY

SUB-SECTOR INDUSTRY ACTIVITY CAPEX (ZARm)

JOBS

Jun-14 Distell Group Stellenbosch Angola Breweries & distilleries Manufacturing 616.3 222

Jun-14 Distell Group Stellenbosch Nigeria Breweries & distilleries Manufacturing 1 713.0 222

Apr-14 Distell Group Stellenbosch Ghana Breweries & distilleries Manufacturing 399.6 222

Mar-06 Distell Group Stellenbosch Namibia Wineries Logistics, Distribution & Transportation

17.6 4

Source: FDI Intelligence, 2015

*There has not been any recorded fdi into Western Cape from African countries

Distell’s investments into Africa is part of a wider growth strategy which will see an additional facility established in

Angola, Nigeria and Ghana. The plant aims to produce a range of beverages for distribution in within the countries

themselves and neighbouring countries.

Distell has identified Ghana as a growth market and as a potential springboard for further penetration of its brands

in neighbouring Togo, Benin, Burkina Faso and Cote d'Ivoire. Distell Ghana, sees the South-African-based

producer of wines, spirits and ready-to-drinks (RTDs) partnering with Finatrade Group to establish a bottling plant

in Accra. “By pooling our respective skills, Finatrade and Distell is an example of how other African partners should

collaborate for the good of the continent” (Distell, 2014).

For more information on this publication and other Wesgro publications please contact [email protected]. For more

publications like this visit the Wesgro publications portal on our website at http://wesgro.co.za/publications