a3 business forum aia, mcma, ria - vision online · pdf filea3 business forum . aia, mcma, ria...

TRANSCRIPT

Dr. Alan Beaulieu President

A Curve in the Road

A3 Business Forum AIA, MCMA, RIA

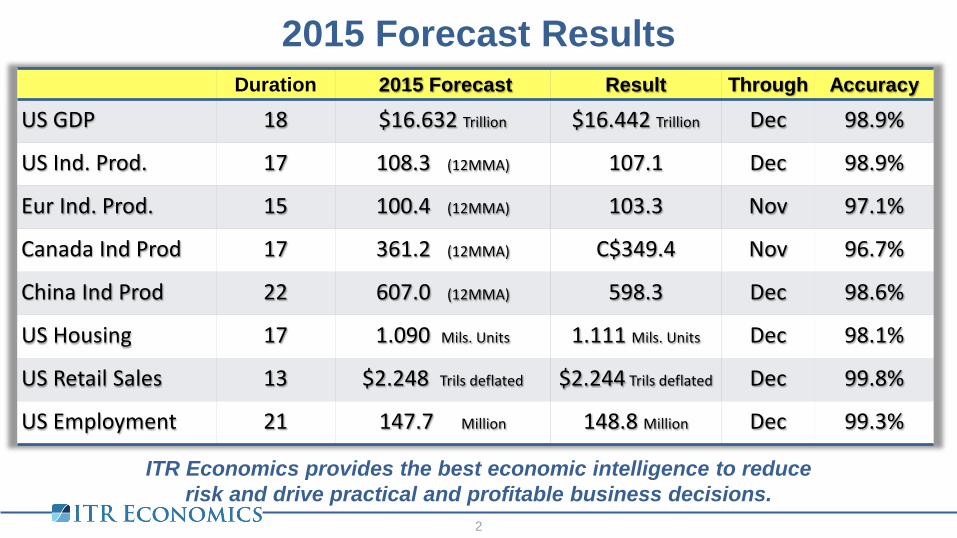

ITR Economics provides the best economic intelligence to reduce risk and drive practical and profitable business decisions.

Duration 2015 Forecast Result Through Accuracy

US GDP 18 $16.632 Trillion $16.442 Trillion Dec 98.9%

US Ind. Prod. 17 108.3 (12MMA) 107.1 Dec 98.9%

Eur Ind. Prod. 15 100.4 (12MMA) 103.3 Nov 97.1%

Canada Ind Prod 17 361.2 (12MMA) C$349.4 Nov 96.7%

China Ind Prod 22 607.0 (12MMA) 598.3 Dec 98.6%

US Housing 17 1.090 Mils. Units 1.111 Mils. Units Dec 98.1%

US Retail Sales 13 $2.248 Trils deflated $2.244 Trils deflated Dec 99.8%

US Employment 21 147.7 Million 148.8 Million Dec 99.3%

2015 Forecast Results 2

2

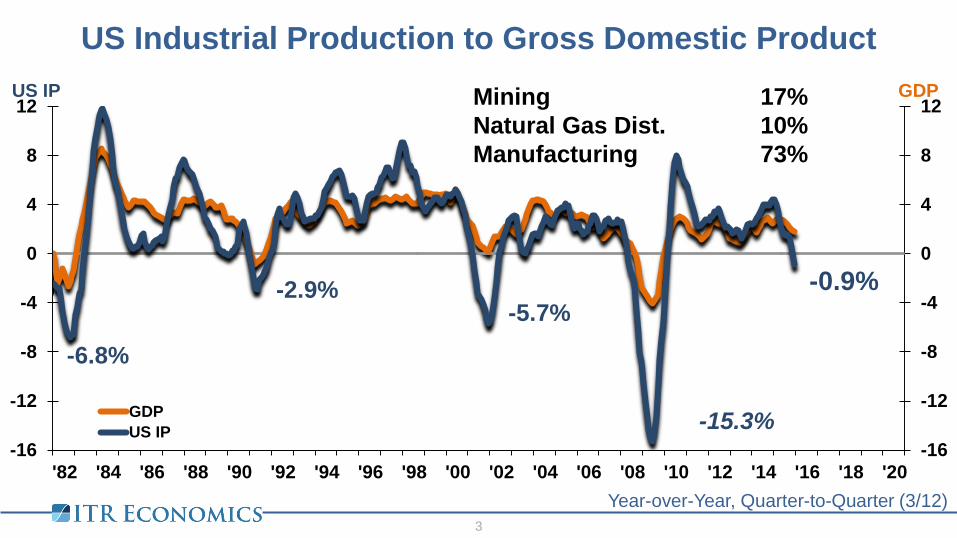

US Industrial Production to Gross Domestic Product

-6.8%

-2.9% -5.7%

-15.3%

-0.9%

-16

-12

-8

-4

0

4

8

12

-16

-12

-8

-4

0

4

8

12

'82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

GDP US IP

GDPUS IP

Year-over-Year, Quarter-to-Quarter (3/12) 3

Mining 17% Natural Gas Dist. 10% Manufacturing 73%

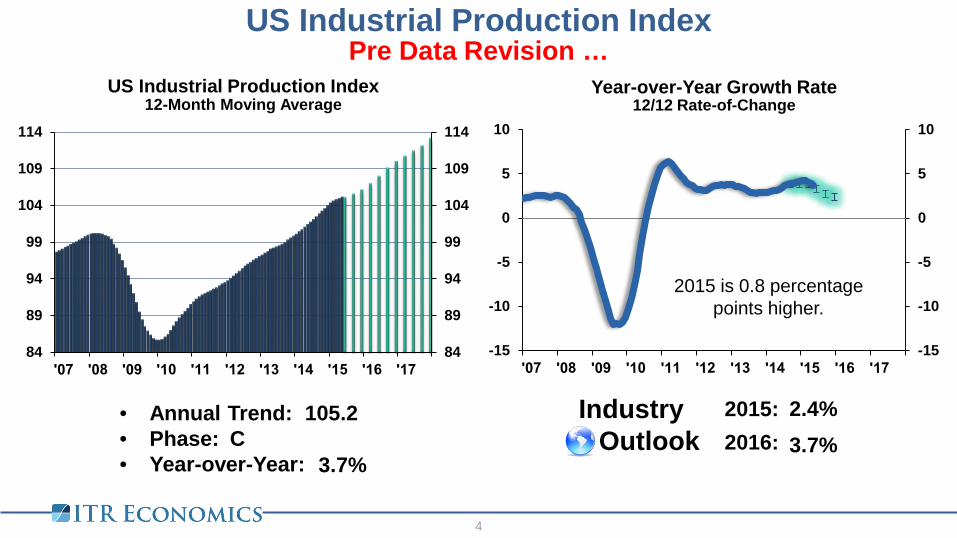

12-Month Moving Average 12/12 Rate-of-Change Year-over-Year Growth Rate

• Annual Trend: • Phase: • Year-over-Year:

Industry Outlook

2015: 2016: 2017:

US Industrial Production Index

4

US Industrial Production Index

105.2 C

3.7%

2.4% 3.7%

Pre Data Revision …

84

89

94

99

104

109

114

84

89

94

99

104

109

114

-15

-10

-5

0

5

10

-15

-10

-5

0

5

10

2015 is 0.8 percentage points higher.

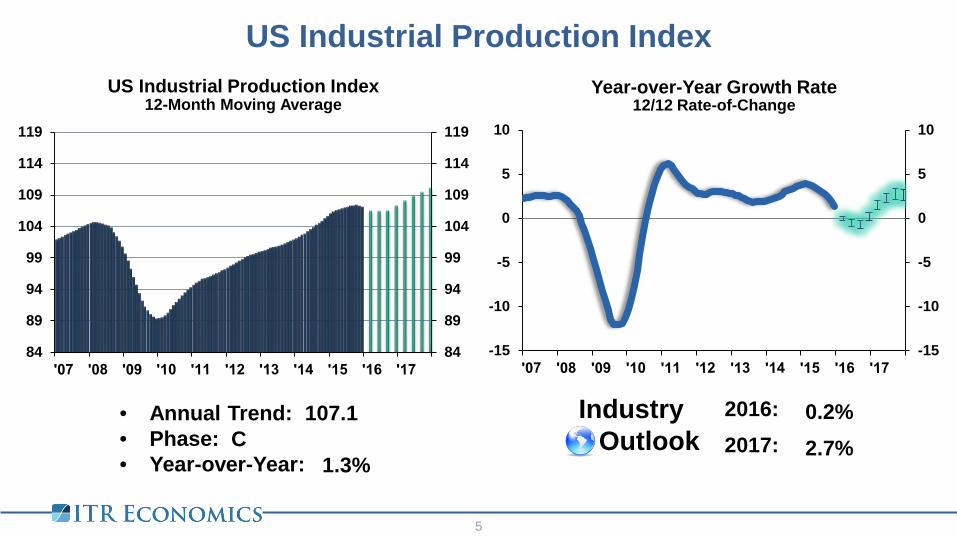

12-Month Moving Average 12/12 Rate-of-Change Year-over-Year Growth Rate

• Annual Trend: • Phase: • Year-over-Year:

Industry Outlook

2016: 2017:

US Industrial Production Index

5

84

89

94

99

104

109

114

119

84

89

94

99

104

109

114

119

-15

-10

-5

0

5

10

-15

-10

-5

0

5

10

US Industrial Production Index

107.1 C

1.3%

0.2% 2.7%

12-Month Moving Average 12/12 Rate-of-Change Year-over-Year Growth Rate

• Annual Trend: • Phase: • Year-over-Year:

Industry Outlook

2016: 2017:

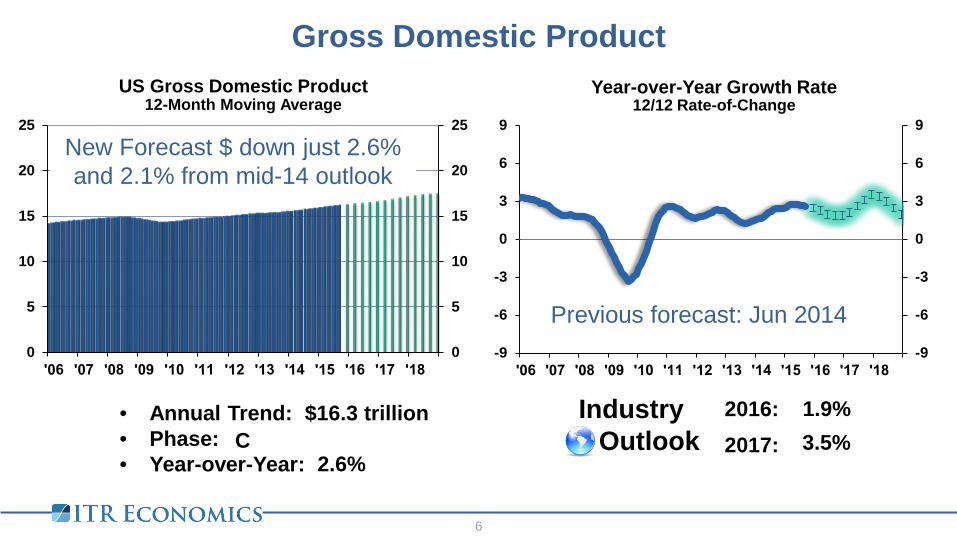

Gross Domestic Product

6

0

5

10

15

20

25

0

5

10

15

20

25

-9

-6

-3

0

3

6

9

-9

-6

-3

0

3

6

9

US Gross Domestic Product

$16.3 trillion C

2.6%

1.9% 3.5%

Previous forecast: Jun 2014

New Forecast $ down just 2.6% and 2.1% from mid-14 outlook

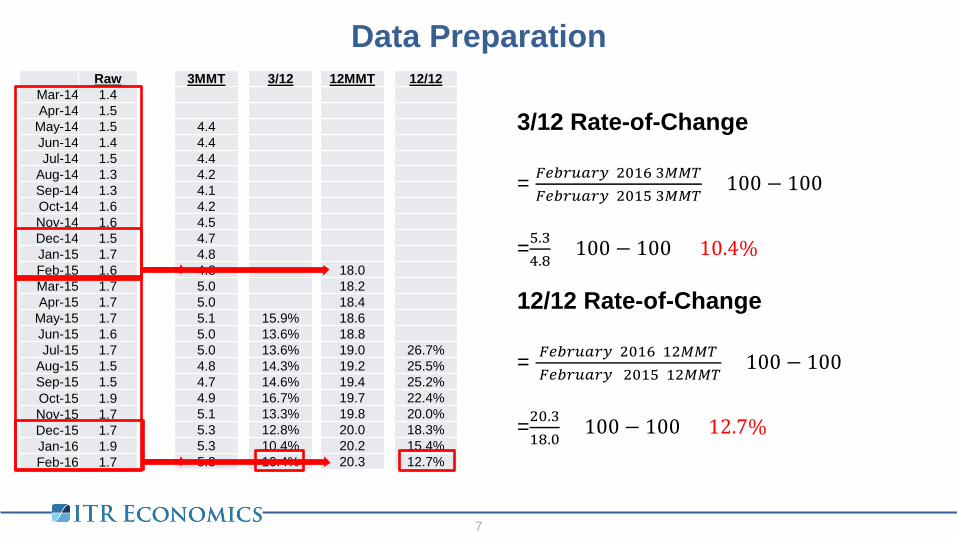

Raw Mar-14 1.4 Apr-14 1.5

May-14 1.5 Jun-14 1.4 Jul-14 1.5

Aug-14 1.3 Sep-14 1.3 Oct-14 1.6 Nov-14 1.6 Dec-14 1.5 Jan-15 1.7 Feb-15 1.6 Mar-15 1.7 Apr-15 1.7

May-15 1.7 Jun-15 1.6 Jul-15 1.7

Aug-15 1.5 Sep-15 1.5 Oct-15 1.9 Nov-15 1.7 Dec-15 1.7 Jan-16 1.9 Feb-16 1.7

3/12 Rate-of-Change = 𝐹𝐹𝐹𝐹𝐹𝐹𝐹𝐹 2016 3𝑀𝑀𝑀𝐹𝐹𝐹𝐹𝐹𝐹𝐹𝐹 2015 3𝑀𝑀𝑀

× 100 − 100 =5.34.8

× 100 − 100 = 10.4%

3MMT

4.4 4.4 4.4 4.2 4.1 4.2 4.5 4.7 4.8 4.8 5.0 5.0 5.1 5.0 5.0 4.8 4.7 4.9 5.1 5.3 5.3 5.3

12MMT

18.0 18.2 18.4 18.6 18.8 19.0 19.2 19.4 19.7 19.8 20.0 20.2 20.3

12/12

26.7% 25.5% 25.2% 22.4% 20.0% 18.3% 15.4% 12.7%

12/12 Rate-of-Change = 𝐹𝐹𝐹𝐹𝐹𝐹𝐹𝐹 2016 12𝑀𝑀𝑀

𝐹𝐹𝐹𝐹𝐹𝐹𝐹𝐹 2015 12𝑀𝑀𝑀× 100 − 100

=20.318.0

× 100 − 100 = 12.7%

3/12

15.9% 13.6% 13.6% 14.3% 14.6% 16.7% 13.3% 12.8% 10.4% 10.4%

Data Preparation

7

-21

-14

-7

0

7

14

21

-45

-30

-15

0

15

30

45

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

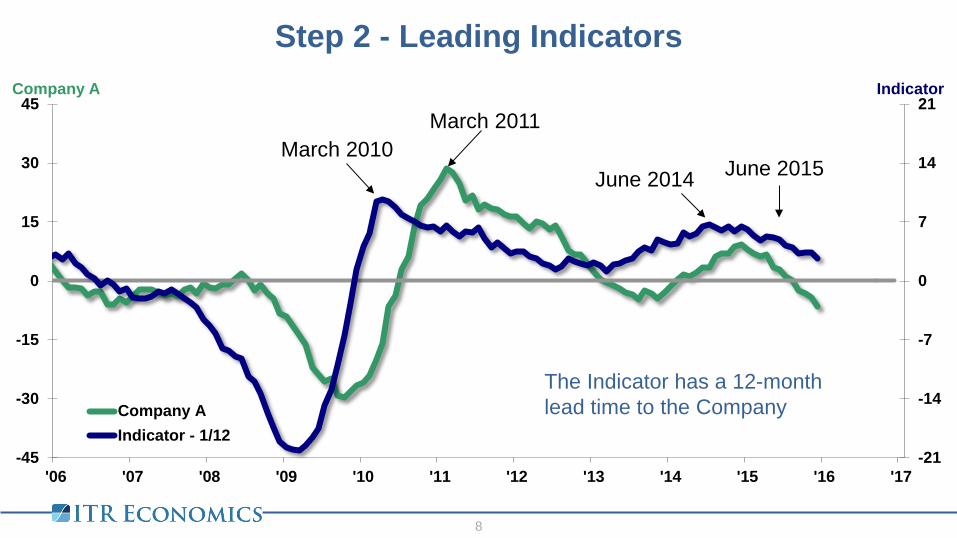

Indicator Company A

Company AIndicator - 1/12

Step 2 - Leading Indicators

8

8

March 2010 March 2011

The Indicator has a 12-month lead time to the Company

June 2014 June 2015

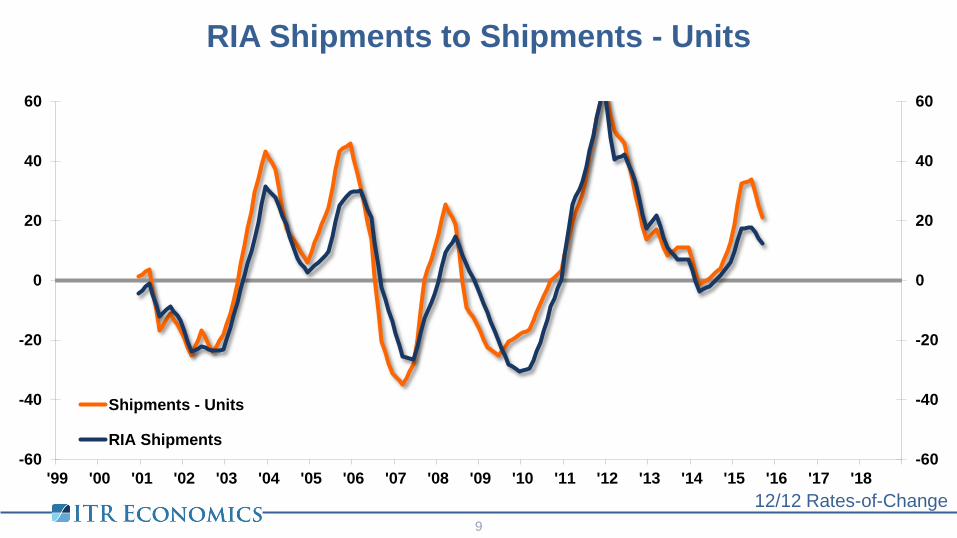

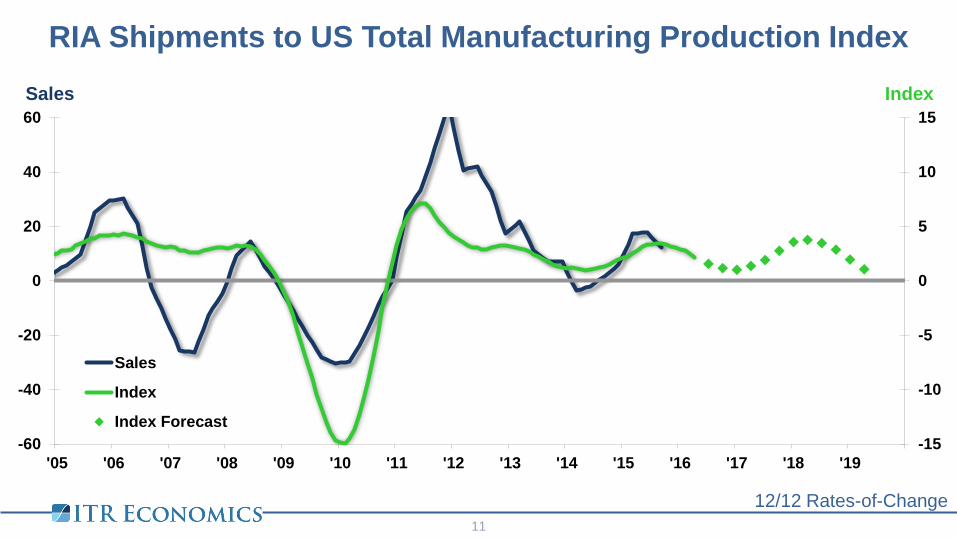

RIA Shipments to Shipments - Units

12/12 Rates-of-Change 9

-60

-40

-20

0

20

40

60

-60

-40

-20

0

20

40

60

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

Shipments - Units

RIA Shipments

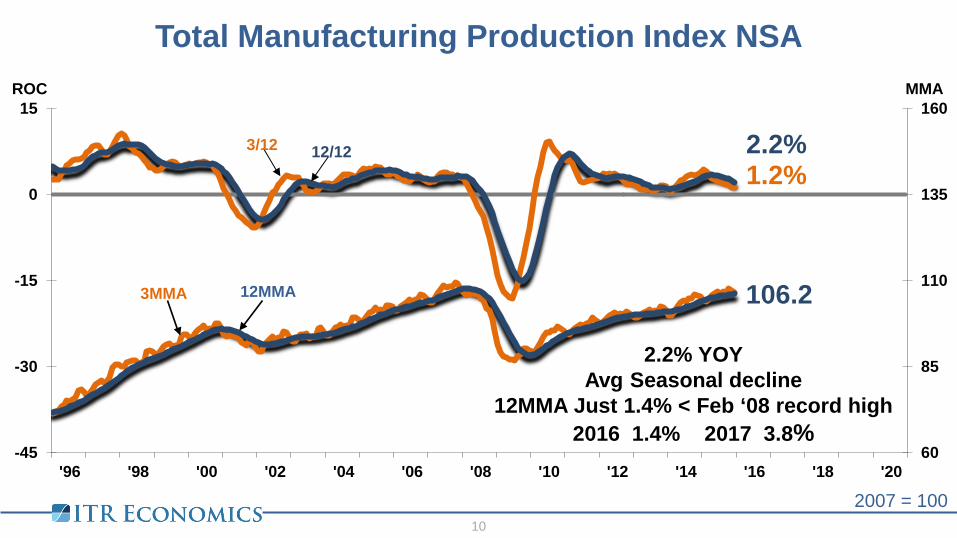

Total Manufacturing Production Index NSA

10

2007 = 100

1.2% 2.2%

106.2

60

85

110

135

160

-45

-30

-15

0

15

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMA ROC

12/12 3/12

3MMA 12MMA

2.2% YOY Avg Seasonal decline

12MMA Just 1.4% < Feb ‘08 record high 2016 1.4% 2017 3.8%

RIA Shipments to US Total Manufacturing Production Index

12/12 Rates-of-Change 11

-15

-10

-5

0

5

10

15

-60

-40

-20

0

20

40

60

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Sales

Index

Index Forecast

Index

Sales

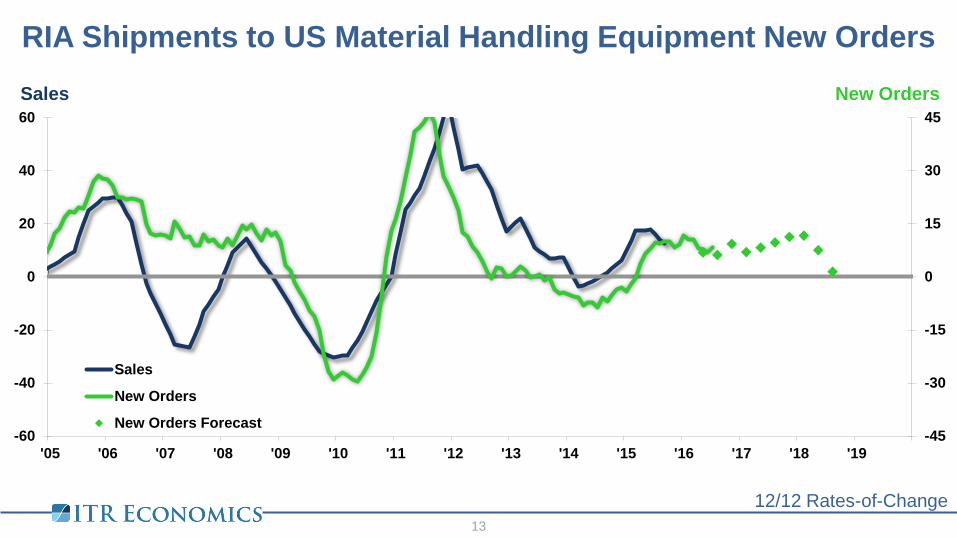

Material Handling Equipment New Orders

12

17.2 8.4

$33.1 Record high

10

20

30

40

50

60

-120

-80

-40

0

40

80

'94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMT R-O-C

3/12 12/12

3MMT 12MMT

Billions of Dollars

2016 9.7%

RIA Shipments to US Material Handling Equipment New Orders

12/12 Rates-of-Change 13

-45

-30

-15

0

15

30

45

-60

-40

-20

0

20

40

60

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Sales

New Orders

New Orders Forecast

New Orders

Sales

1.3% 2.9%

-60

-45

-30

-15

0

15

30

45

-16

-12

-8

-4

0

4

8

12

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Production US IP

US IPProduction

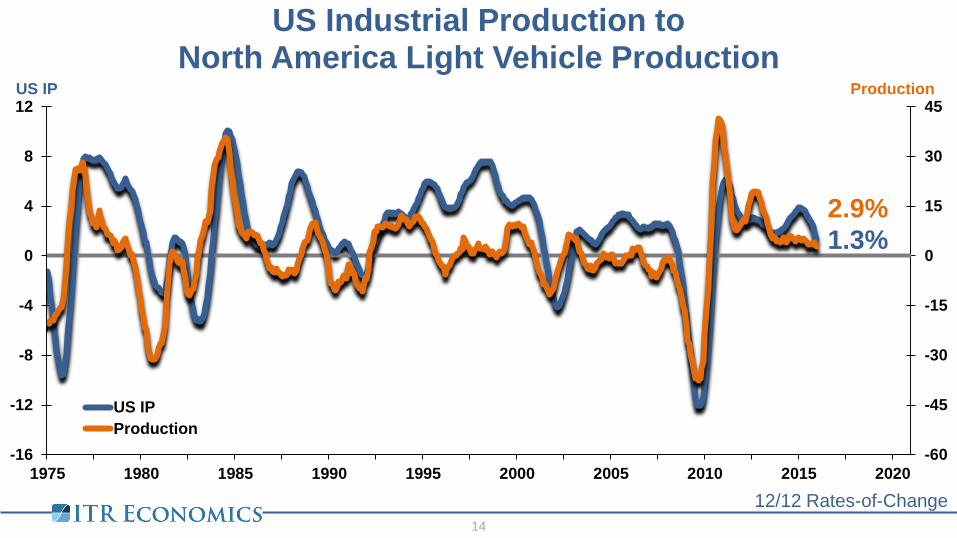

US Industrial Production to North America Light Vehicle Production

12/12 Rates-of-Change 14

North America Light Vehicle Production

2.2% 2.9%

17.4

5

10

15

20

25

30

35

40

-100

-75

-50

-25

0

25

50

75

'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMT R-O-C

3/12 12/12

3MMT

12MMT

2018 5.1% 18.3

Data Source: Wards Auto Millions of Units

15

3MMA seasonal decline is slightly steeper than average

(post Great Recession)

US Auto Exports

Thousands of Units 16

111.6

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Auto Exports

RIA Shipments to North America Light Vehicle Production

12/12 Rates-of-Change 17

-60

-40

-20

0

20

40

60

-60

-40

-20

0

20

40

60

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Sales

Production

Production Forecast

Production Page 6 of Manufacturing ITR Trends Report Sales

Crude Oil Futures Prices to Crude Oil Inventories Cushing, OK

-80

-40

0

40

80

120

-80

-40

0

40

80

120

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Price

Inventories

Inventories

Price

Data Sources: Wall Street Journal, EIA 12/12 Rates-of-Change

18

Copper Futures Tentative Dec ‘15 3/12 and 12/12 lows US Steel Futures Monthly up 14.3% since November Commodity Prices Tentative 1/12 and 3/12 lows

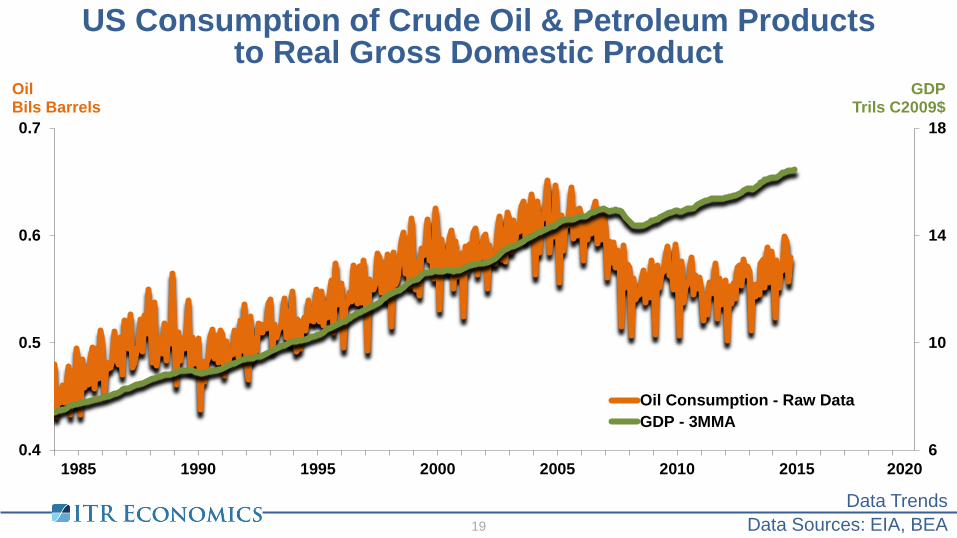

US Consumption of Crude Oil & Petroleum Products to Real Gross Domestic Product

19

Data Trends Data Sources: EIA, BEA

6

10

14

18

0.4

0.5

0.6

0.7

1985 1990 1995 2000 2005 2010 2015 2020

GDP Trils C2009$

Oil Bils Barrels

Oil Consumption - Raw DataGDP - 3MMA

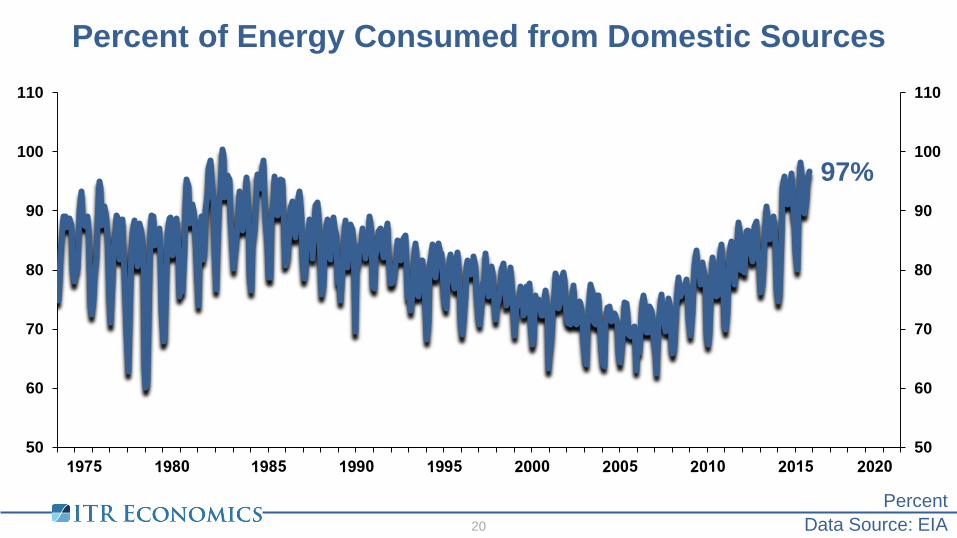

Percent of Energy Consumed from Domestic Sources

20 Data Source: EIA Percent

97%

50

60

70

80

90

100

110

50

60

70

80

90

100

110

Ongoing Concerns

21

China: Debt, Devaluation, Doubtful growth

Fear of instability from low oil prices

Non-defense capital goods new orders

South America

US Debt

World Demographics

China Industrial Production Index

2000 = 100 22

5.9% 6.2%

598.3

75

275

475

675

875

1075

1275

-30

-20

-10

0

10

20

30

'98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMA R-O-C

3/12 12/12

3MMA

12MMA

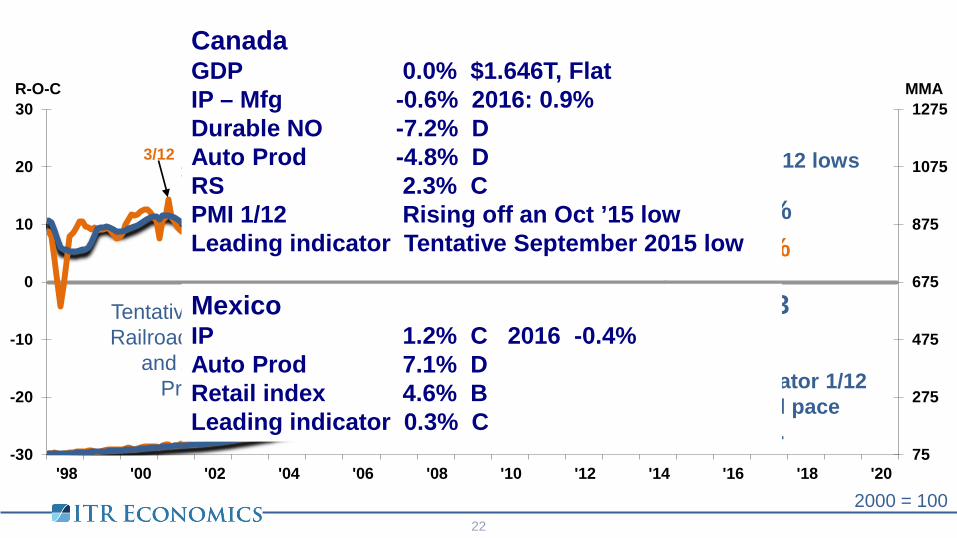

China leading indicator 1/12 is rising at a normal pace off a June 2015 low.

Tentative 1/12 and 3/12 lows

Tentative 12/12 rise in Railroad Freight Index

and Automobile Production.

Canada GDP 0.0% $1.646T, Flat IP – Mfg -0.6% 2016: 0.9% Durable NO -7.2% D Auto Prod -4.8% D RS 2.3% C PMI 1/12 Rising off an Oct ’15 low Leading indicator Tentative September 2015 low

Mexico IP 1.2% C 2016 -0.4% Auto Prod 7.1% D Retail index 4.6% B Leading indicator 0.3% C

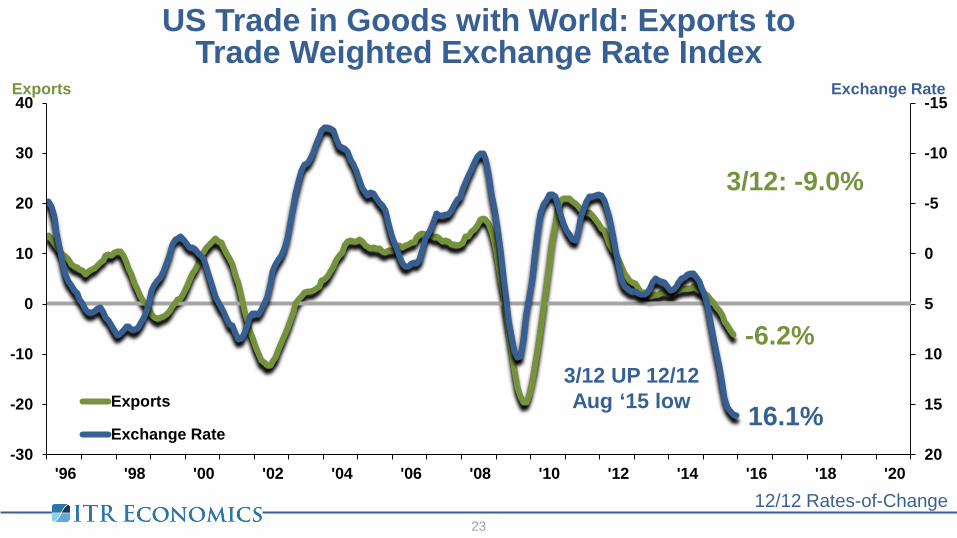

-6.2%

16.1%

-15

-10

-5

0

5

10

15

20-30

-20

-10

0

10

20

30

40

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Exchange Rate Exports

Exports

Exchange Rate

US Trade in Goods with World: Exports to Trade Weighted Exchange Rate Index

12/12 Rates-of-Change

3/12: -9.0%

23

3/12 UP 12/12 Aug ‘15 low

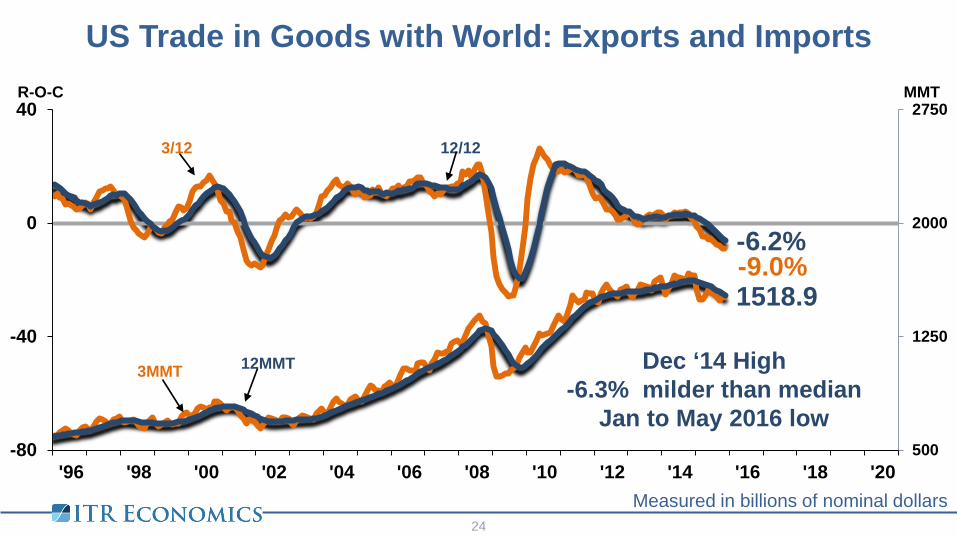

US Trade in Goods with World: Exports and Imports

Measured in billions of nominal dollars 24

-9.0% -6.2%

1518.9

500

1250

2000

2750

-80

-40

0

40

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMT R-O-C

3/12 12/12

3MMT 12MMT Dec ‘14 High -6.3% milder than median

Jan to May 2016 low

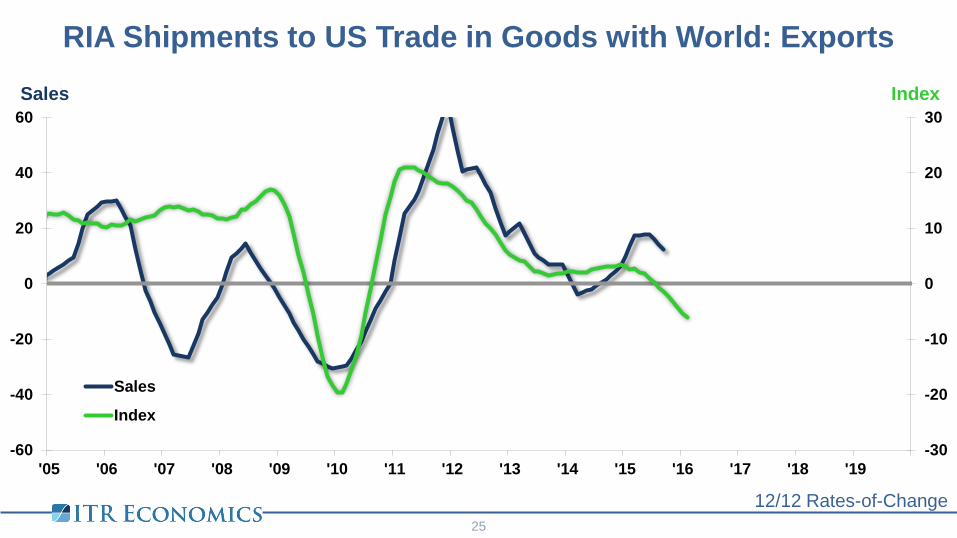

RIA Shipments to US Trade in Goods with World: Exports

12/12 Rates-of-Change 25

-30

-20

-10

0

10

20

30

-60

-40

-20

0

20

40

60

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Sales

Index

Index

Sales

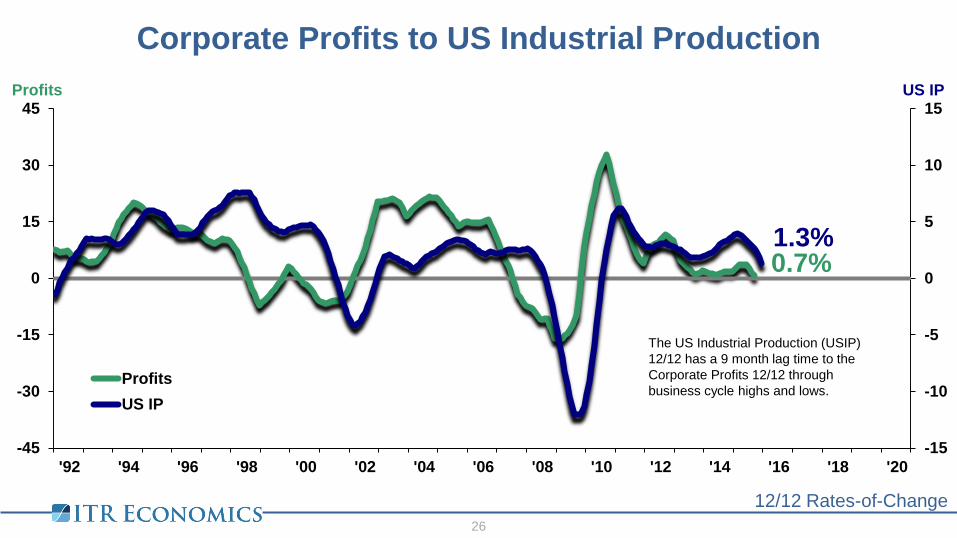

0.7% 1.3%

-15

-10

-5

0

5

10

15

-45

-30

-15

0

15

30

45

'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

US IP Profits

ProfitsUS IP

Corporate Profits to US Industrial Production

12/12 Rates-of-Change 26

The US Industrial Production (USIP) 12/12 has a 9 month lag time to the Corporate Profits 12/12 through business cycle highs and lows.

Consumer Prices

0 0

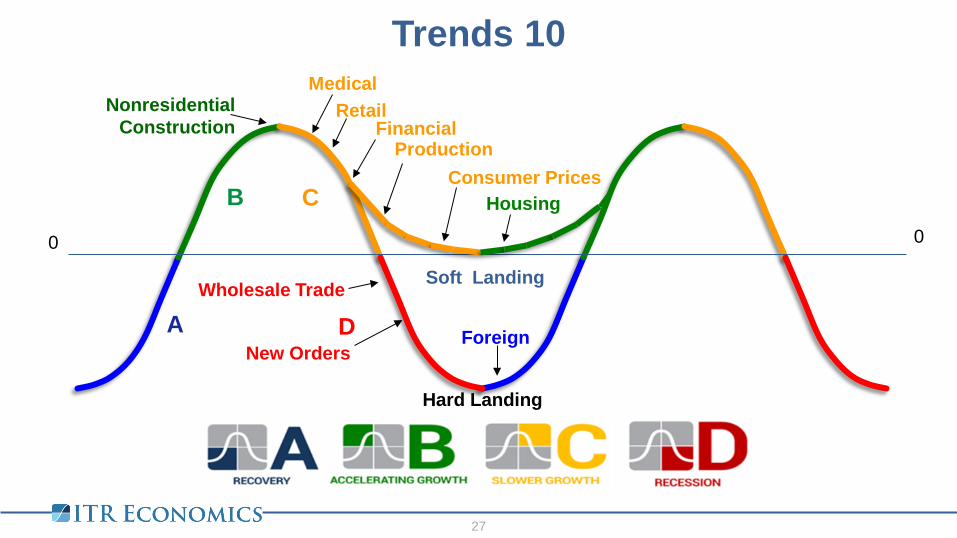

Soft Landing

A

B C

D

Trends 10

27

Housing

Production

Medical

New Orders

Financial Retail

Wholesale Trade

Foreign

Nonresidential Construction

Hard Landing

-10.6%

-50

-25

0

25

50

75

-50

-25

0

25

50

75

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

1/12

As seen in the

Leads US Economy by 9-14 months

Purchasing Managers Index

Data Source: Institute for Supply Management 1/12 Rate-of-Change

28

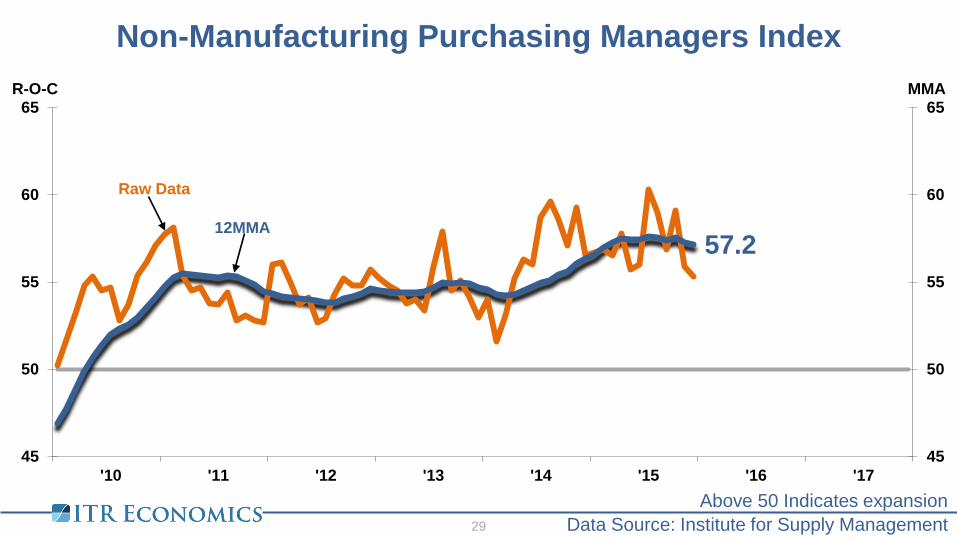

Non-Manufacturing Purchasing Managers Index

29

Above 50 Indicates expansion Data Source: Institute for Supply Management

57.2

45

50

55

60

65

45

50

55

60

65

'10 '11 '12 '13 '14 '15 '16 '17

MMA R-O-C

Raw Data

12MMA

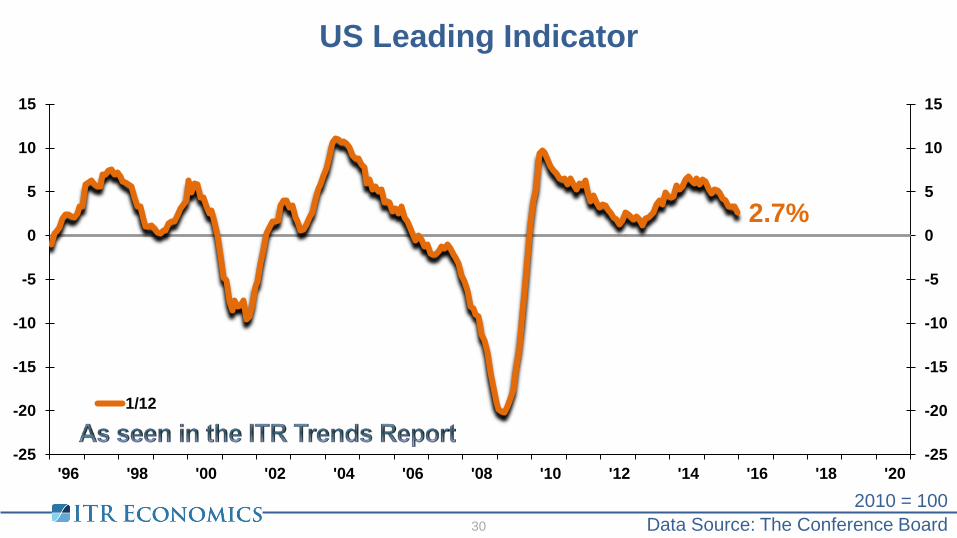

US Leading Indicator

2.7%

-25

-20

-15

-10

-5

0

5

10

15

-25

-20

-15

-10

-5

0

5

10

15

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

1/12

Data Source: The Conference Board 2010 = 100

30

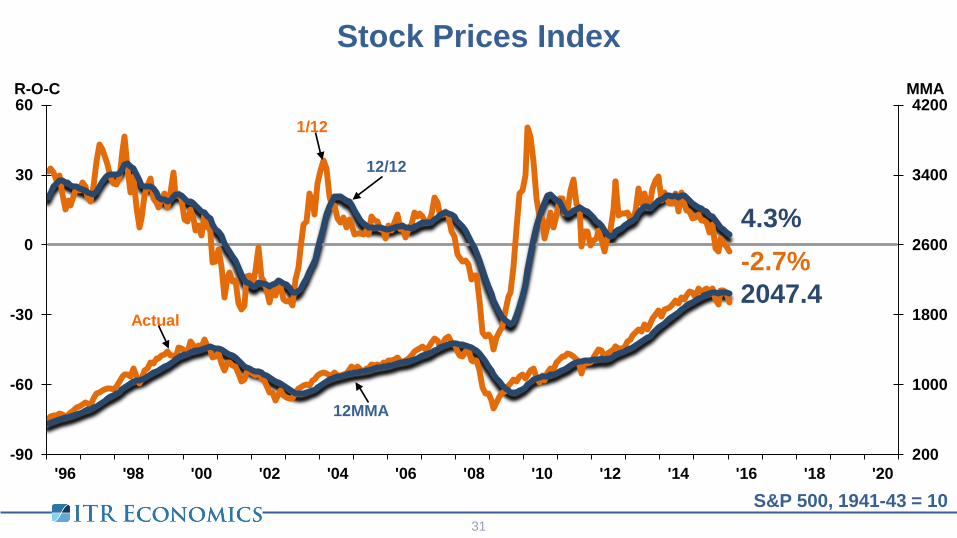

Stock Prices Index

S&P 500, 1941-43 = 10 31

31

-2.7% 4.3%

2047.4

200

1000

1800

2600

3400

4200

-90

-60

-30

0

30

60

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMA R-O-C

1/12

12/12

Actual

12MMA

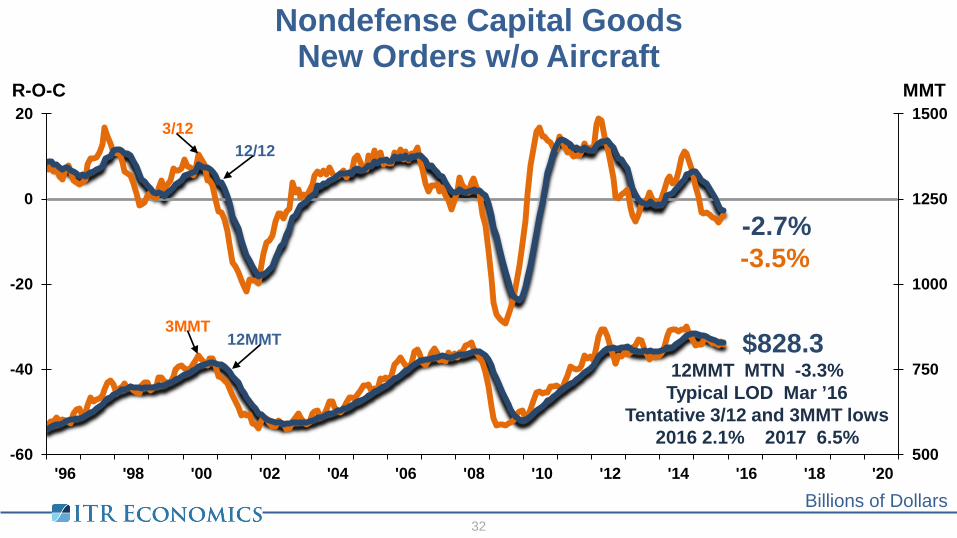

Nondefense Capital Goods New Orders w/o Aircraft

Billions of Dollars 32

-3.5% -2.7%

$828.3

500

750

1000

1250

1500

-60

-40

-20

0

20

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMT R-O-C

3/12 12/12

3MMT 12MMT

12MMT MTN -3.3% Typical LOD Mar ’16

Tentative 3/12 and 3MMT lows 2016 2.1% 2017 6.5%

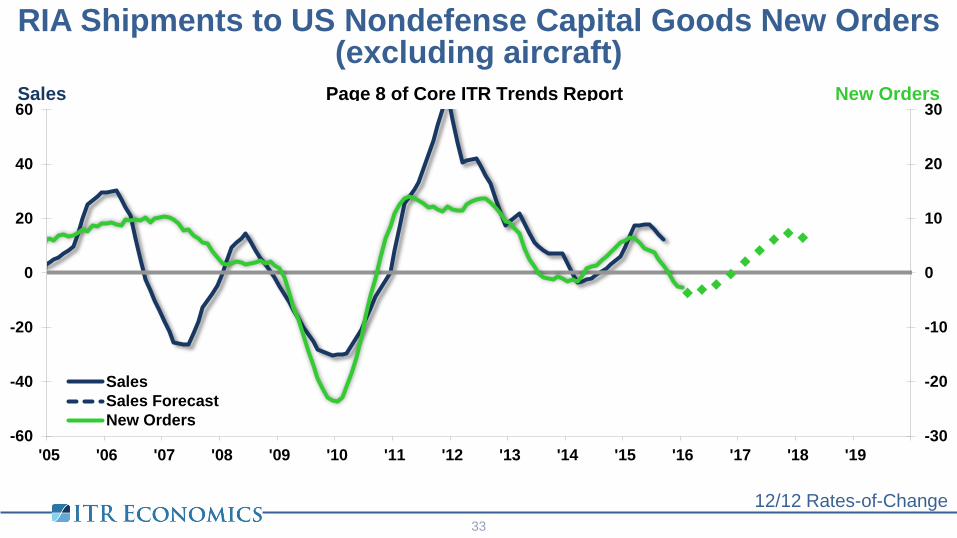

RIA Shipments to US Nondefense Capital Goods New Orders (excluding aircraft)

12/12 Rates-of-Change 33

-30

-20

-10

0

10

20

30

-60

-40

-20

0

20

40

60

'05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

SalesSales ForecastNew Orders

New Orders Page 8 of Core ITR Trends Report Sales

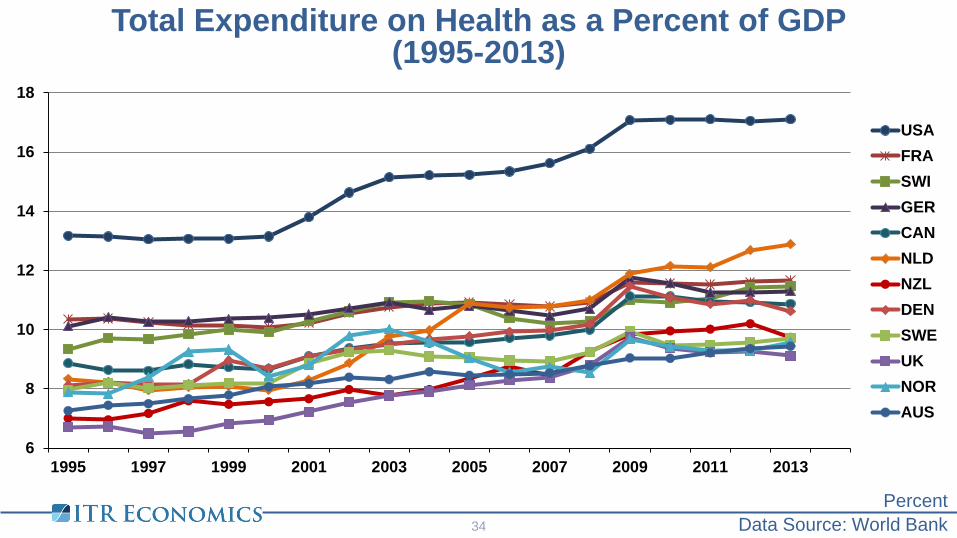

Total Expenditure on Health as a Percent of GDP (1995-2013)

Data Source: World Bank Percent

34

6

8

10

12

14

16

18

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

USAFRASWIGERCANNLDNZLDENSWEUKNORAUS

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

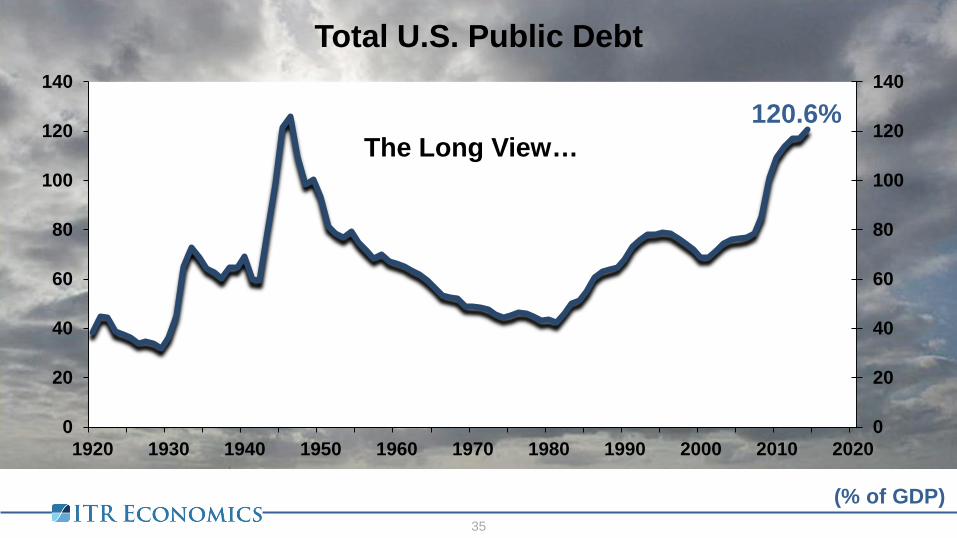

120.6%

Total U.S. Public Debt

35

(% of GDP)

The Long View…

The next Great Depression is coming.

Are you ready?

Order your copy today from Barnes & Noble.

Available in e-book and print format.

36

US/Global Recovery – Good Days Ahead

37

Consumers are in great shape

World is relatively calm

Employment rising

Banks are lending

Retail Sales are rising

Non-residential construction is improving

Deficit spending continues – no fear of austerity

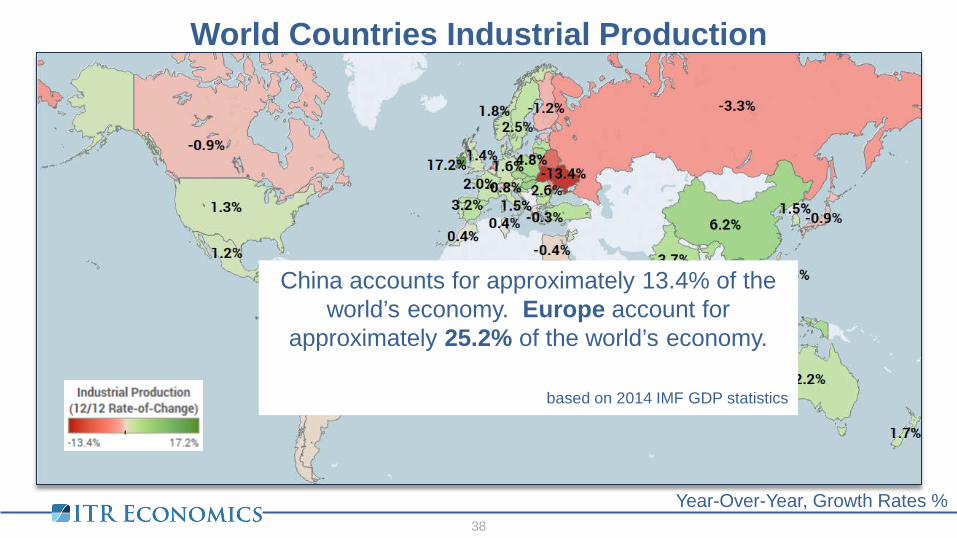

World Countries Industrial Production

Year-Over-Year, Growth Rates % 38

China accounts for approximately 13.4% of the world’s economy. Europe account for

approximately 25.2% of the world’s economy.

based on 2014 IMF GDP statistics

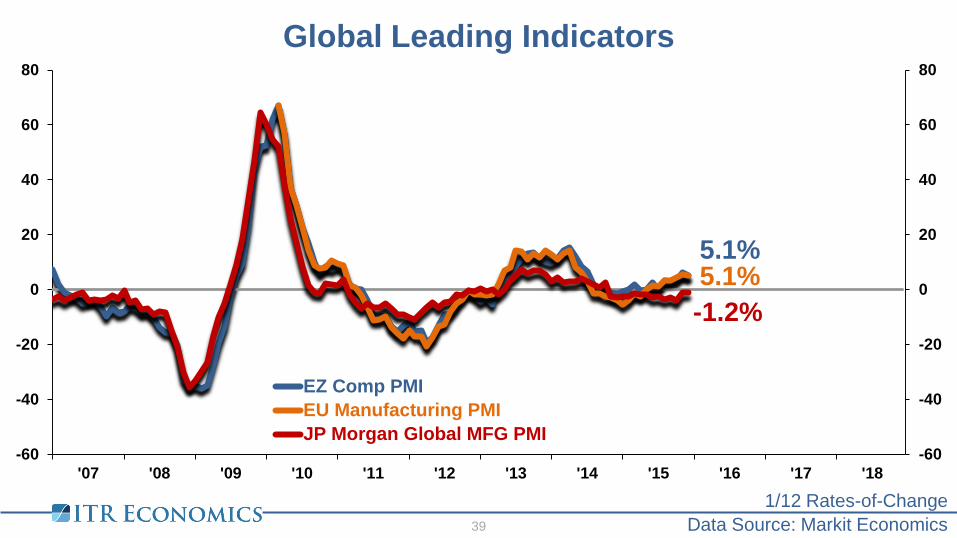

Global Leading Indicators

Data Source: Markit Economics 1/12 Rates-of-Change

39

-1.2% 5.1% 5.1%

-60

-40

-20

0

20

40

60

80

-60

-40

-20

0

20

40

60

80

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

EZ Comp PMIEU Manufacturing PMIJP Morgan Global MFG PMI

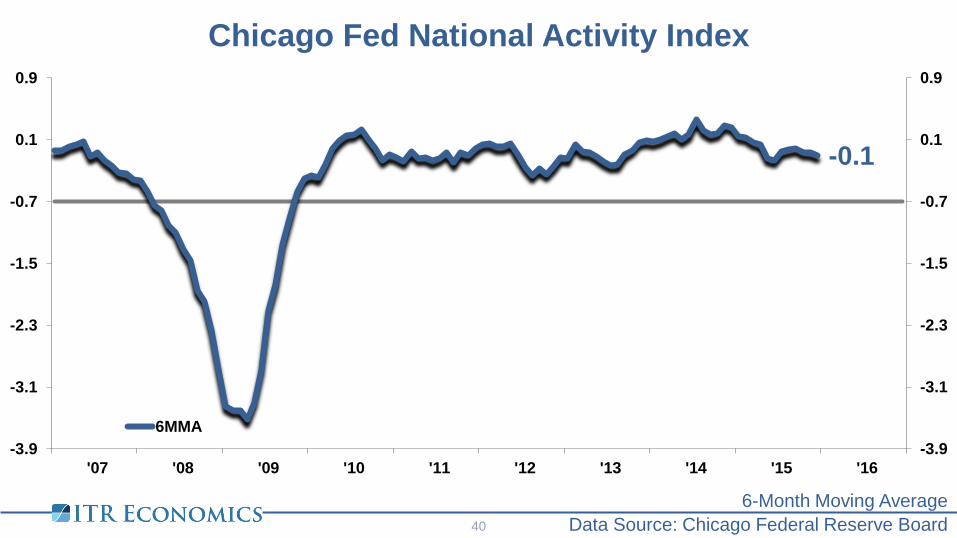

Chicago Fed National Activity Index

Data Source: Chicago Federal Reserve Board

6-Month Moving Average 40

40

-0.1

-3.9

-3.1

-2.3

-1.5

-0.7

0.1

0.9

-3.9

-3.1

-2.3

-1.5

-0.7

0.1

0.9

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16

6MMA

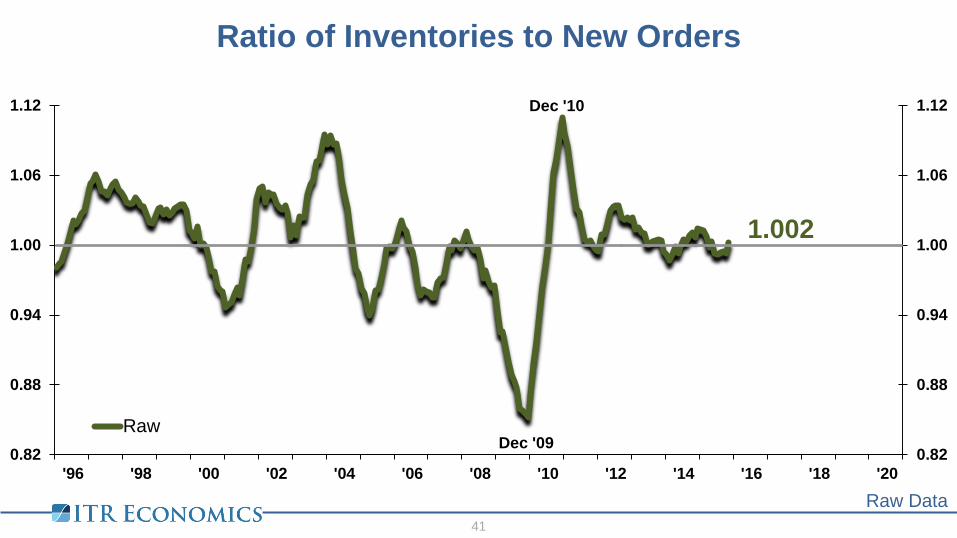

Ratio of Inventories to New Orders

Raw Data 41

1.002

0.82

0.88

0.94

1.00

1.06

1.12

0.82

0.88

0.94

1.00

1.06

1.12

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Raw

Dec '10

Dec '09

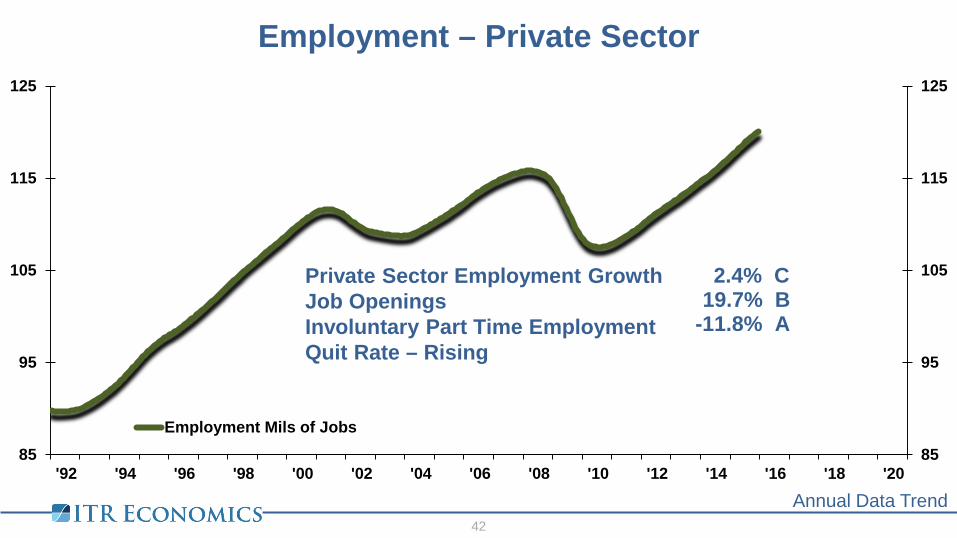

Employment – Private Sector

Annual Data Trend 42

85

95

105

115

125

85

95

105

115

125

'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Employment Mils of Jobs

Private Sector Employment Growth Job Openings Involuntary Part Time Employment Quit Rate – Rising

19.7% B 2.4% C

-11.8% A

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Consumer Loan Delinquency RateConsumer Credit Card Delinquency Rate

Percentage Percentage

10 Year Average

10 Year Average

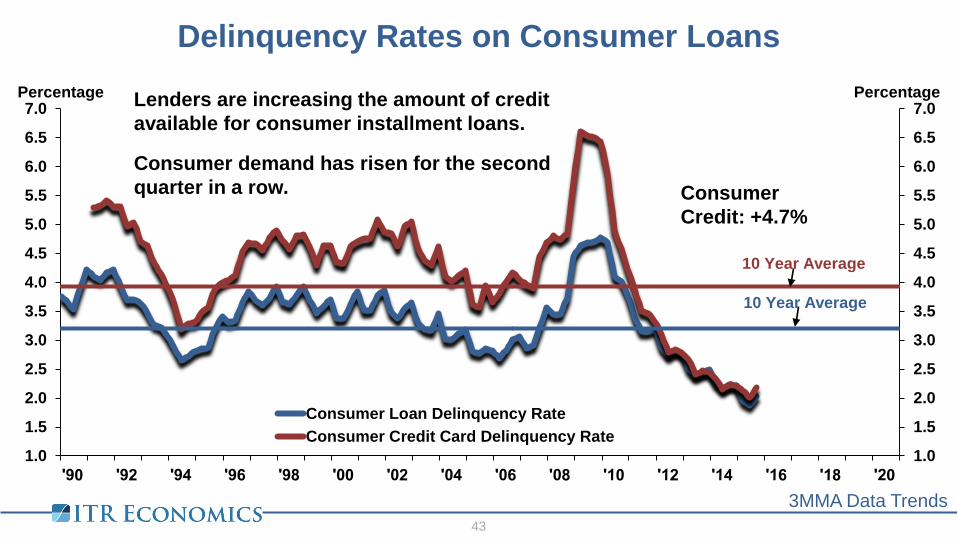

Delinquency Rates on Consumer Loans

3MMA Data Trends 43

Lenders are increasing the amount of credit available for consumer installment loans.

Consumer demand has risen for the second quarter in a row. Consumer

Credit: +4.7%

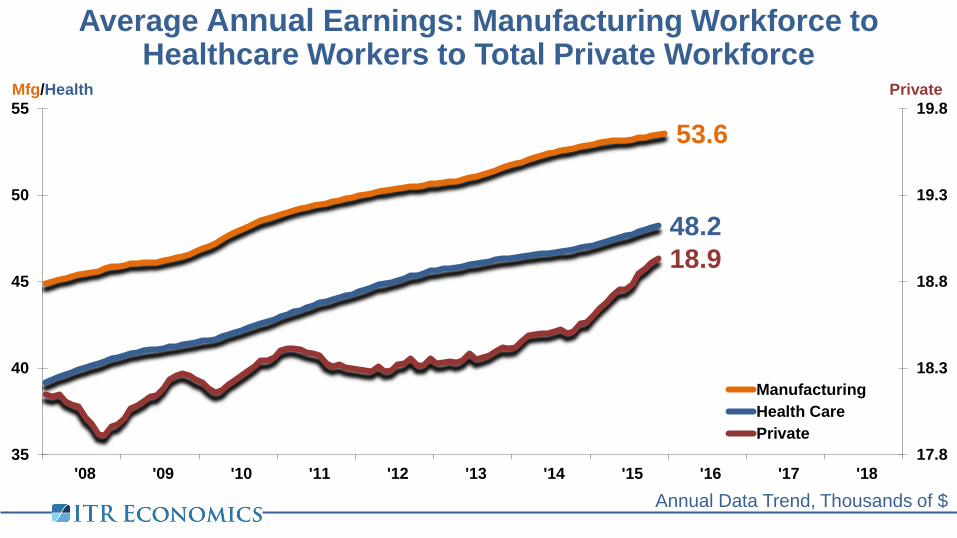

Average Annual Earnings: Manufacturing Workforce to Healthcare Workers to Total Private Workforce

Annual Data Trend, Thousands of $

53.6

48.2 18.9

17.8

18.3

18.8

19.3

19.8

35

40

45

50

55

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

Private Mfg/Health

ManufacturingHealth CarePrivate

Data Sources: Federal Reserve Bank of St. Louis, U.S. Bureau of Labor Statistics

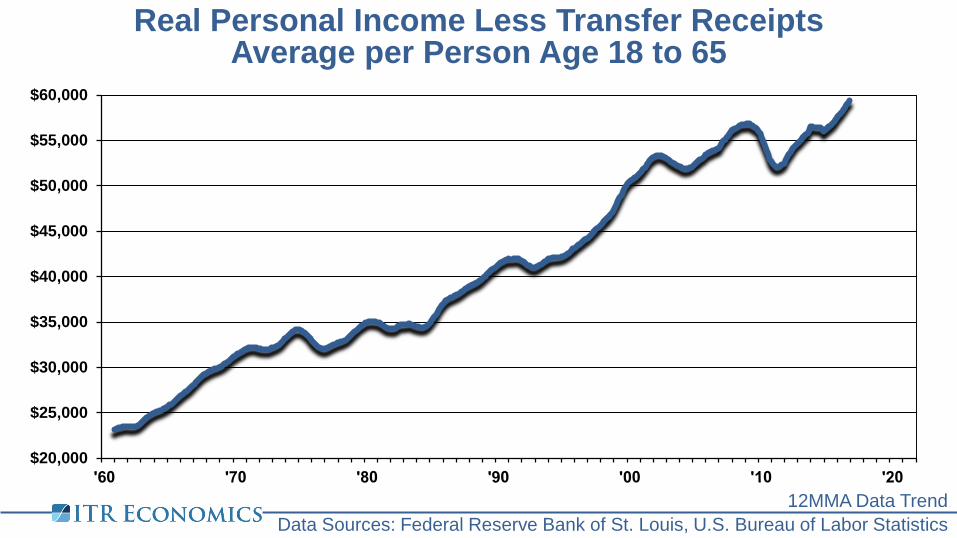

Real Personal Income Less Transfer Receipts Average per Person Age 18 to 65

12MMA Data Trend

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

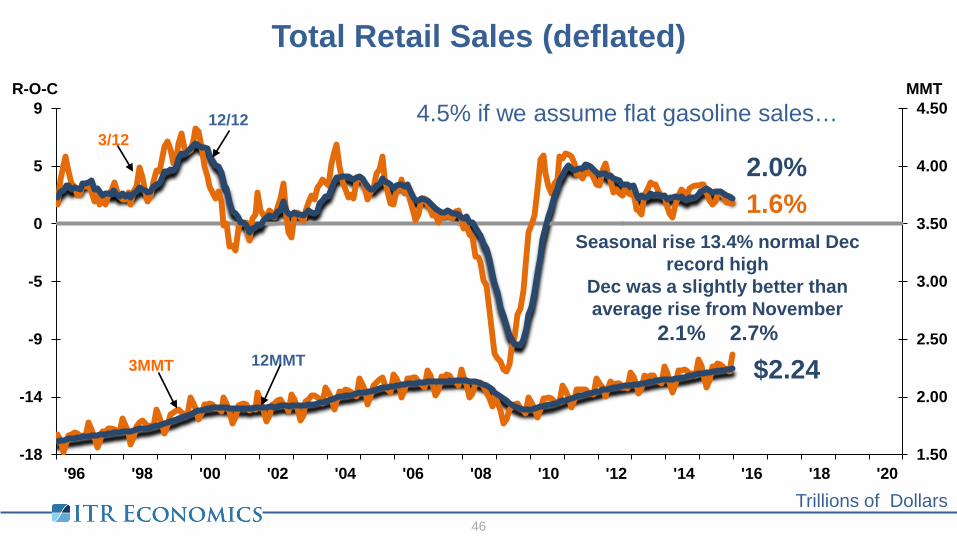

Total Retail Sales (deflated)

46

Trillions of Dollars

1.6% 2.0%

$2.24

1.50

2.00

2.50

3.00

3.50

4.00

4.50

-18

-14

-9

-5

0

5

9

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMT R-O-C

3/12 12/12

3MMT 12MMT

Seasonal rise 13.4% normal Dec record high

Dec was a slightly better than average rise from November

2.1% 2.7%

4.5% if we assume flat gasoline sales…

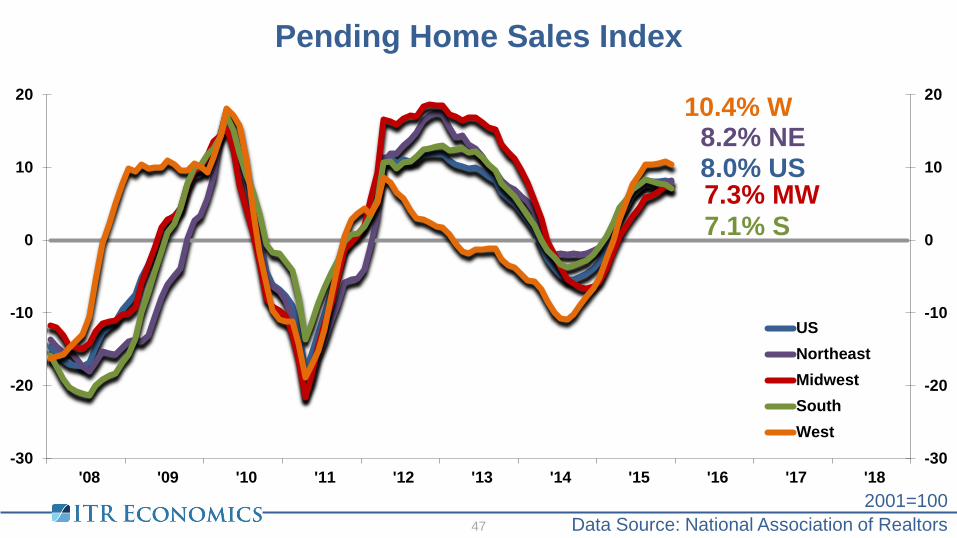

Pending Home Sales Index

Data Source: National Association of Realtors

2001=100 47

8.0% US 8.2% NE

7.1% S

10.4% W

7.3% MW

-30

-20

-10

0

10

20

-30

-20

-10

0

10

20

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

USNortheastMidwestSouthWest

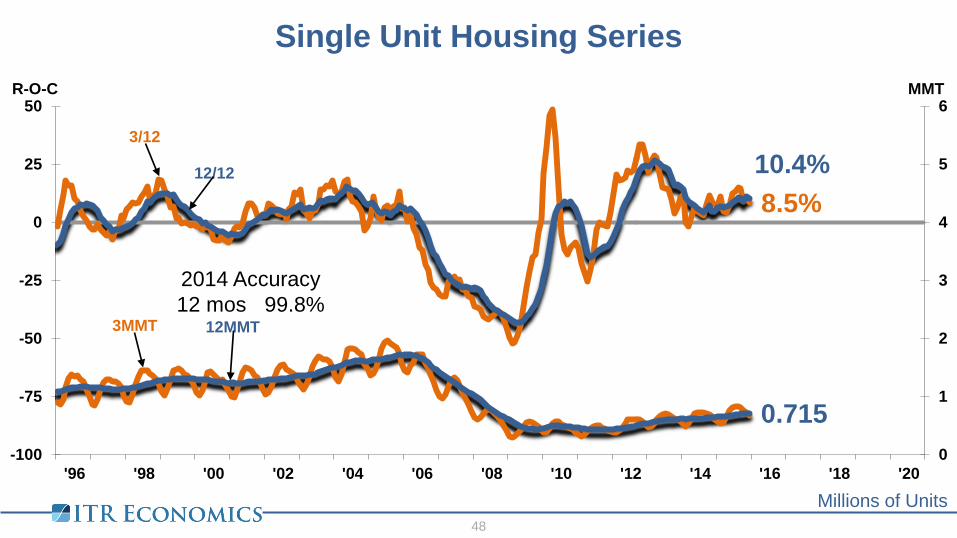

Single Unit Housing Series

Millions of Units 48

8.5% 10.4%

0.715 0

1

2

3

4

5

6

-100

-75

-50

-25

0

25

50

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

MMT R-O-C

3/12

12/12

3MMT 12MMT

2014 Accuracy 12 mos 99.8%

49 49

50 Source: Factset, FRB 50

0

2

4

6

8

10

12

14

16

'82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16

Yield on 10 Year Treasury Note

%

-1

0

1

2

3

4

5

6

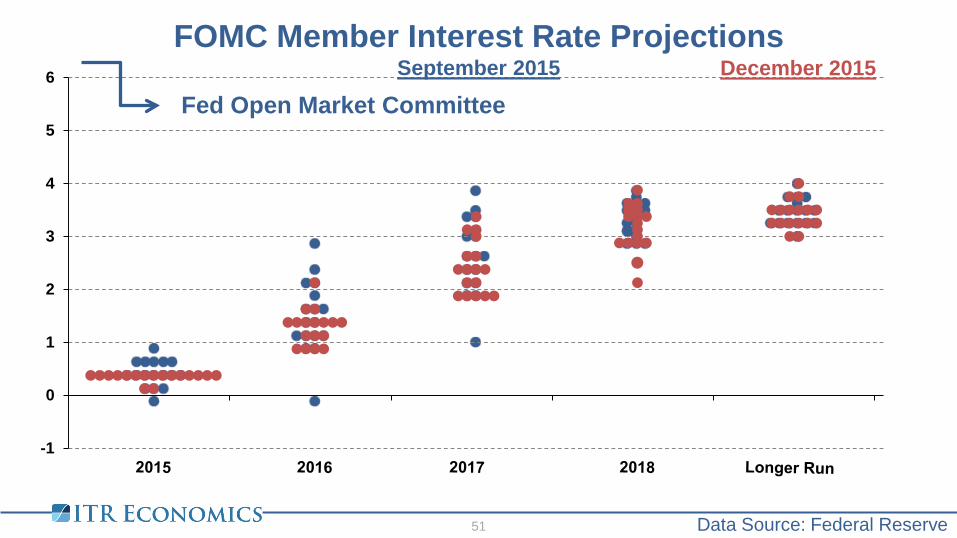

FOMC Member Interest Rate Projections

Data Source: Federal Reserve

51

Fed Open Market Committee December 2015 September 2015

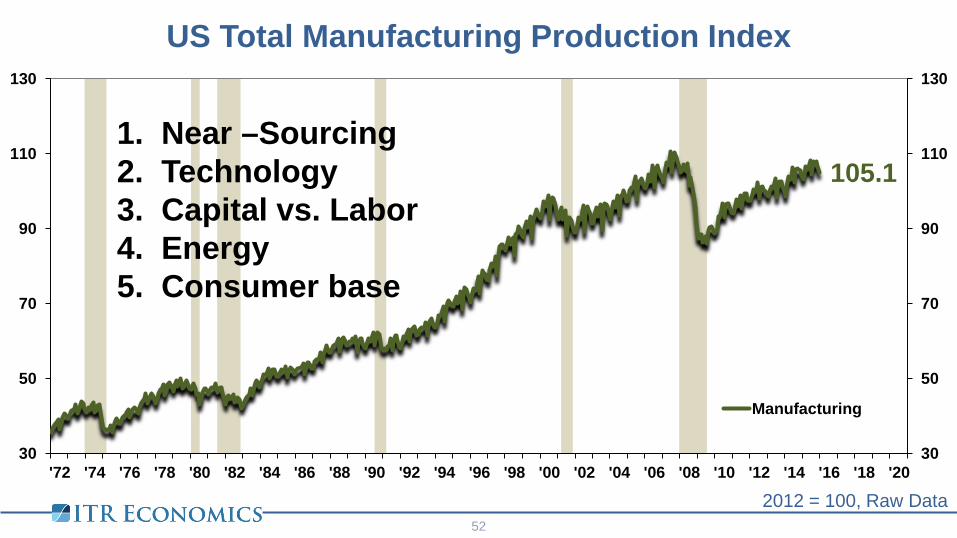

105.1

30

50

70

90

110

130

30

50

70

90

110

130

'72 '74 '76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Manufacturing

US Total Manufacturing Production Index

2012 = 100, Raw Data 52

1. Near –Sourcing 2. Technology 3. Capital vs. Labor 4. Energy 5. Consumer base

Actions to take in 2016

53

1. Budget for continued economic growth driven by the consumer

2. Invest in customer market research to reduce price sensitivity

3. Make sure your training and retention programs are top notch

4. Marketing and advertising spending increasingly effective

5. Drive efficiencies with technology

6. Hire sales people and leaders

7. Lock in costs in early 2016

8. Expand credit offerings to garner market share

9. Plan for higher wages and higher energy costs

Join our email list!

54

Want to hear more updates like you heard today?