a summary of the medical assistance eligibility rules laurie hanson long & reher, p.a. 5881...

TRANSCRIPT

A Summary of the Medical Assistance Eligibility Rules

LAURIE HANSON

Long & Reher, P.A.

5881 Cedar Lake Road

Minneapolis, Minnesota 55416

(952) 929-0622

www.longreher.com

•Private pay

•Medicare and supplemental insurance • Long-term care insurance

•Veterans Home

•Medicaid/Medical Assistance

Payment sources for long-term care services

What is Medicare? Federal health insurance program for Social

Security and Railroad Retirement recipients

who:

have reached age 65

have received SSDI for two years, OR

are suffering from chronic kidney disease.

Long-term care coverage under MedicareLong-term care coverage under Medicare: 3 days of hospitalization and admitted to NH

within 30 days of discharge

Skilled care only is covered

Maximum coverage: 100 days per spell of illness

After first 20 days, co-payment of $109.50/day in

2004

Medicare Supplemental Insurance policies

Must cover certain coinsurance payments under Medicare.

Will not cover care in nursing homes after the first 100 days, even if skilled.

Will not cover skilled care in nursing homes

if Medicare itself is not paying. If Medicare

doesn’t pay, neither does the supplemental

policy.

What is Medical Assistance? Medicaid -- A joint federal-state program created

to serve certain categories of lower income, disabled, and elderly persons. Eligibility is based on need.

Governed by federal law. To participate in the Medicaid program, states must comply with federal law.

An entitlement program: If you qualify for benefits, you get benefits.

Home and community-based care programs in MN

For persons 65 years old and older:

Elderly Waiver Program (EW)

Special Income Standard Elderly Waiver program (SIS EW)

Alternative Care program (AC) Not a Medical Assistance program

Home and community-based programs in MN

For persons under 65 years of age: Mental Retardation or Related Conditions

(MR/RC)

Community Alternative Care (CAC)

Community Alternatives for Disabled

Individuals (CADI)

Traumatic Brain Injury (TBI)

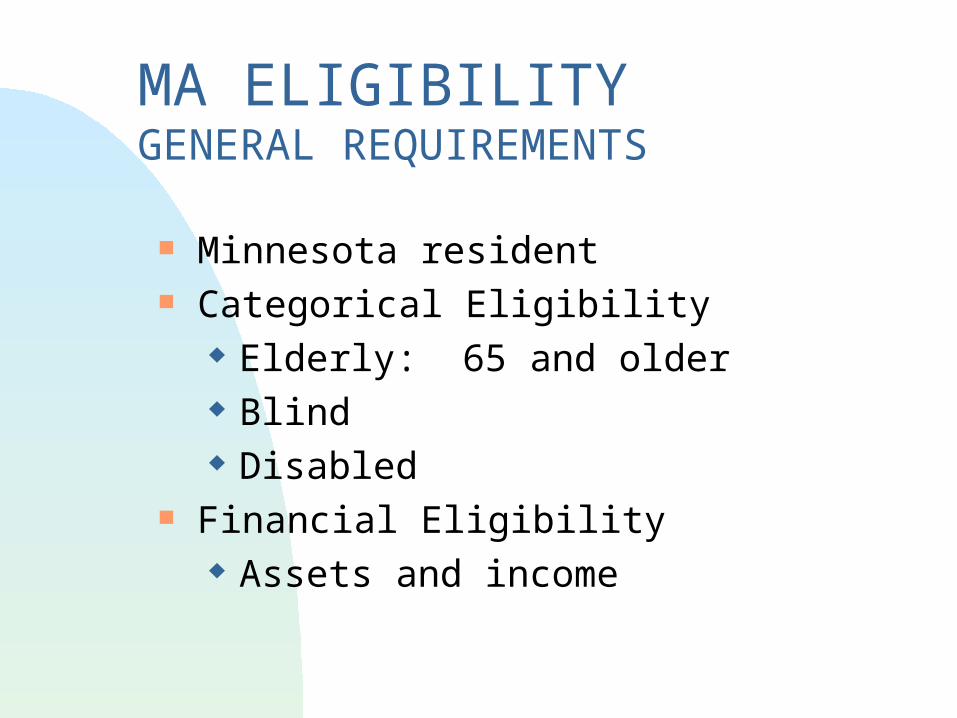

MA ELIGIBILITY GENERAL REQUIREMENTS

Minnesota resident Categorical Eligibility

Elderly: 65 and older Blind Disabled

Financial Eligibility Assets and income

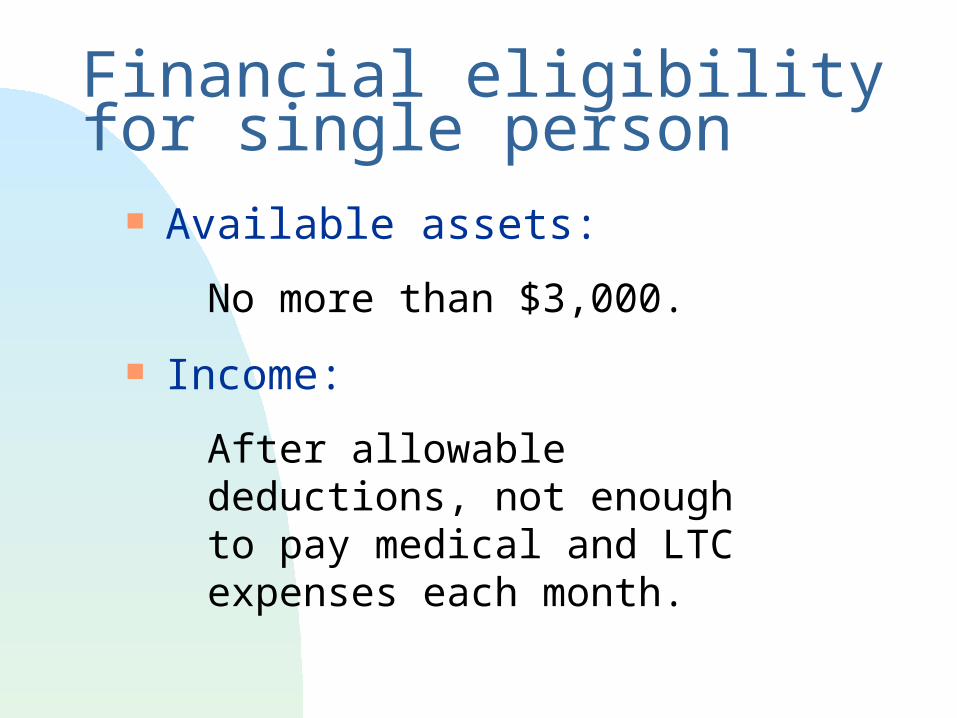

Financial eligibility for single person

Available assets:

No more than $3,000.

Income:

After allowable deductions, not enough to pay medical and LTC expenses each month.

Financial eligibility for married person with community spouse:

Available assets:

No more than community spouse asset allowance plus $3,000 for LTC spouse. Spousal impoverishment rules apply.

Income:

After allowable deductions, not enough to pay medical and LTC expenses each month.

Assets in general Real property, household furnishings and

wearing apparel, investments including savings and checking accounts, stocks, bonds, CDs, contracts for deed, mortgages, IRAs, collections, cash surrender value of life insurance policies, etc.

Kinds of assets: Available Assets Excluded Assets Unavailable assets

Available assets

Assets are available if the owner has both legal authority and actual

ability to use them for self-support and assets are not excluded or unavailable.

Premarital agreement has no effect.

Excluded assets Homestead Household goods and personal effects One motor vehicle Assets of trade or business Insurance payments to repair or replace

lost, damaged, or destroyed property CSV of certain insurance policies Burial funds

Unavailable assetsUnavailable assets are those that have a legal or

actual barrier to being liquidated. They can include:

Jointly held assets Share of estate that has not been probated Property involved in pending legal action Life estate interest in real property Real property not used as homestead:

reasonable effort to sell

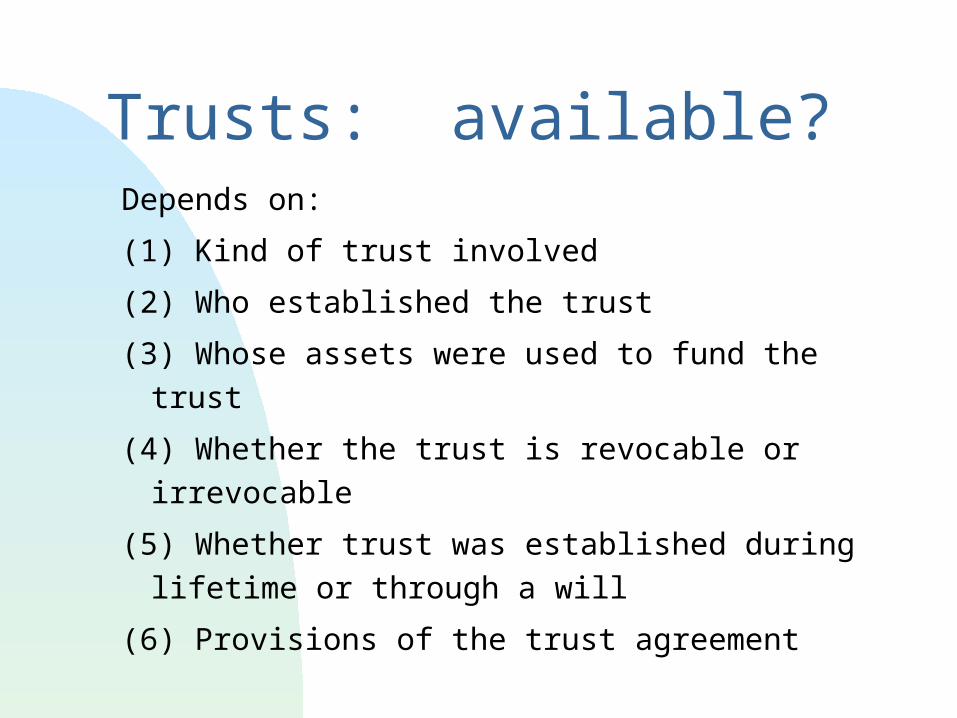

Trusts: available?Depends on:

(1) Kind of trust involved

(2) Who established the trust

(3) Whose assets were used to fund the trust

(4) Whether the trust is revocable or irrevocable

(5) Whether trust was established during

lifetime or through a will

(6) Provisions of the trust agreement

Kinds of trusts

Revocable trust

Medicaid qualifying trust

Trust with springing provisions

Supplemental needs trust

Special needs trust

Pooled trust

Jointly held assets General rule: Presumption that joint

tenants own pro rata share

Exception: Checking or savings account, time deposits owned by MA applicant

Savings bonds: Unavailable if owned jointly and in possession of person who is not applying for MA

Case Study: Single person

Assets owned:

Homestead (sole owner)

Farm property, owned with brother

Irrevocable burial fund

Checking account, joint with brother

Car, value $4,000

Household furnishings

Case Study: Single person

Assets owned:

Homestead (sole owner) Excluded

Farm property, owned with brother

Irrevocable burial fund

Checking account, joint with brother

Car, value $4,000

Household furnishings

Case Study: Single person

Assets owned:

Homestead (sole owner) Excluded

Farm property, owned with brother Unavailable

Irrevocable burial fund

Checking account, joint with brother

Car, value $4,000

Household furnishings

Case Study: Single person

Assets owned:

Homestead (sole owner) Excluded

Farm property, owned with brother Unavailable

Irrevocable burial fund Excluded

Checking account, joint with brother

Car, value $4,000

Household furnishings

Case Study: Single person

Assets owned:

Homestead (sole owner) Excluded

Farm property, owned with brother Unavailable

Irrevocable burial fund Excluded

Checking account, joint with brother Available

Car, value $4,000

Household furnishings

Case Study: Single person

Assets owned:

Homestead (sole owner) Excluded

Farm property, owned with brother Unavailable

Irrevocable burial fund Excluded

Checking account, joint with brother Available

Car, value $4,000 Excluded

Household furnishings

Case Study: Single person

Assets owned:

Homestead (sole owner) Excluded

Farm property, owned with brother Unavailable

Irrevocable burial fund Excluded

Checking account, joint with brother Available

Car, value $4,000 Excluded

Household furnishings Excluded

Income deductionsPay all income after following deductions made: Reparation and restitution payments Medicare premiums Personal needs allowance of $74, $90 for vets G/C fees, 5% of income up to $100 Community spouse income allocation Family member allocation Reasonable and necessary medical expenses

Balance must be paid to the nursing home.

Income Spenddown for Single Person: EXAMPLE

Income of Individual $1,000.60 less Medicare Part B -66.60 less personal needs allowance - 74.00 less insurance premium -100.00

Income applied to care $759.00

Cost of Care $5,440.00 less -759.00

MA pays: $4,681.00

What if the MA recipient is married?

Spousal Impoverishment Rules Apply LTC spouse in NH or Elderly Waiver Community spouse in community Asset Assessment Date:

NH/HH, completed only once Community spouse asset allowance Income allocation to community spouse

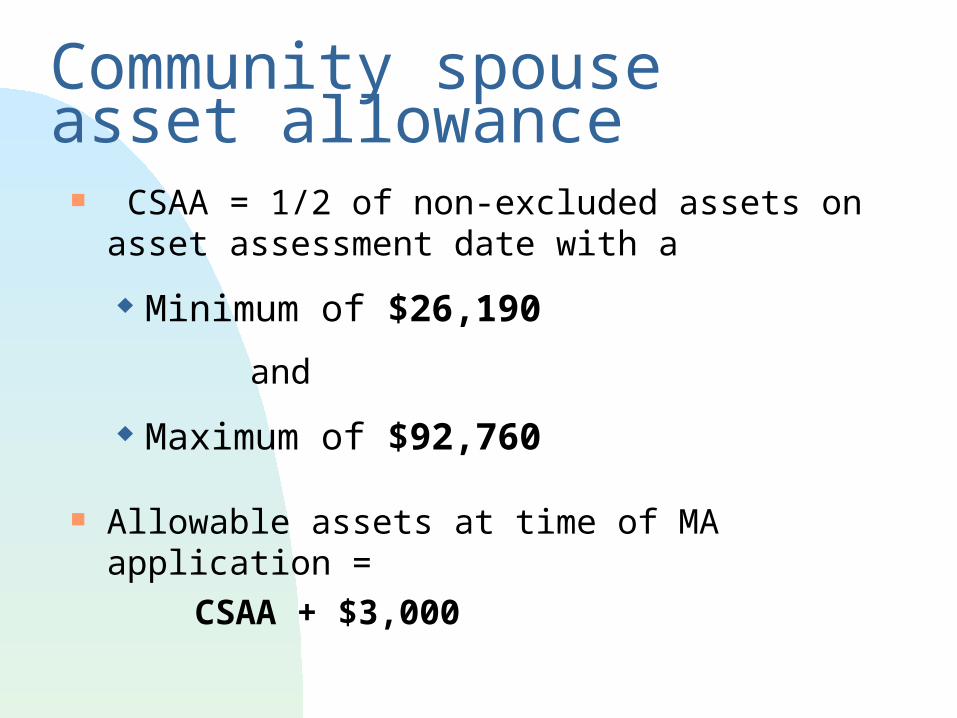

Community spouse asset allowance CSAA = 1/2 of non-excluded assets on asset

assessment date with a

Minimum of $26,190

and

Maximum of $92,760

Allowable assets at time of MA application =

CSAA + $3,000

Date of Institutionalization

Protected Assets: CSAA $26,190 MA limit $ 3,000

Excess Assets: $ 5,810

Date of MA application, if in 2004:

$26,190 $3,000

$35,000

Date of Institutionalization

Protected Assets: CSAA $50,000 MA limit $ 3,000

Excess Assets: $47,000

Date of MA application:

$50,000 $3,000

$100,000

Date of Institutionalization

Protected Assets: CSAA $ 92,760 MA limit $ 3,000

Excess Assets $104,240

Date of MA application, if in 2004:

$92,760 $3,000

$200,000

Income Spenddown for Married Recipient

Income of LTC spouse $2,000.60

Income of community spouse $ 700.00

CS is not required to pay any of her income for the care of the LTC spouse

BUT

How is CS going to live on $700/month?

Minimum income allowance for community spouse

Standard of $1,562 per month Increased by amount shelter expenses exceed

$469, up to cap of $2,319 Shelter expenses include:

Mortgage or rent Property taxes Utilities Fire insurance Association fee

Increased asset allowance based on income

If total income of both spouses is less than the CS’s minimum income allowance, the CSAA can be increased.

All retained assets must be income-producing.

Can occur when income is low and shelter expenses are relatively high.

IMPORTANT: ALWAYS REVIEW BOTH ASSETS AND INCOME

Assets

Eligible?

Income

Is reduction of assets necessary?

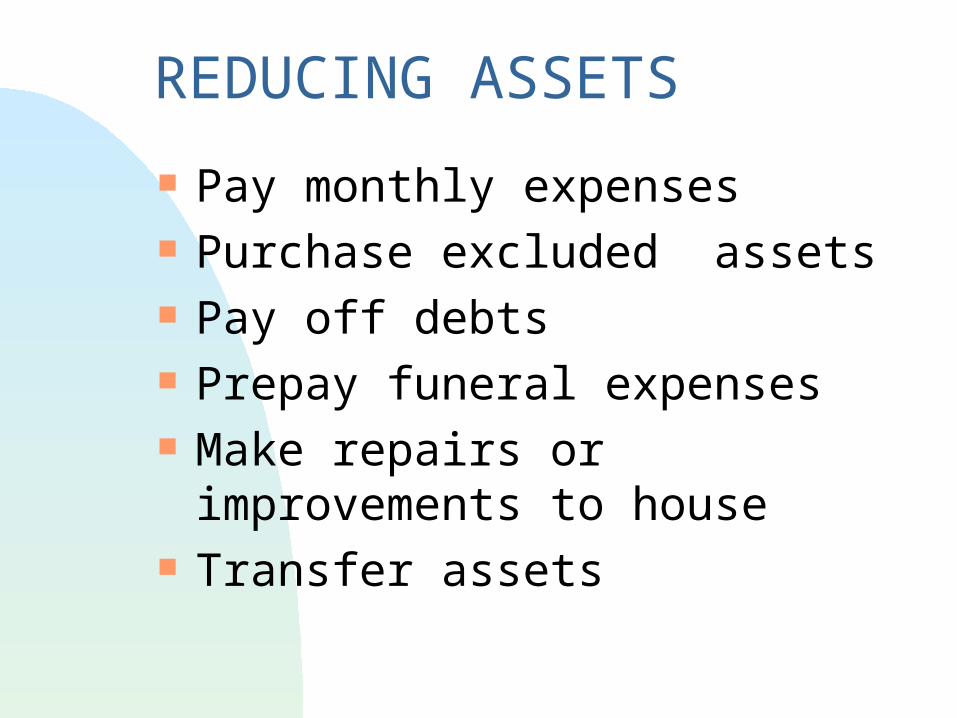

REDUCING ASSETS

Pay monthly expenses Purchase excluded assets Pay off debts Prepay funeral expenses Make repairs or improvements to

house Transfer assets

Transfer Warnings Federal law 1997: Makes it a misdemeanor

for paid advisor to counsel or assist in transfers if results in penalty period. Found to be unconstitutional.

Minnesota law 2003: Not enforceable until federal waiver is given or federal law changes

Loss of ownership and control: once given away, assets are no longer yours.

Basic Transfer Rule Transfers of assets or income

By applicant or applicant’s spouse For less than FMV During “lookback period”:

36 months preceding MA application for transfers to people

60 months preceding MA application for transfers to and from certain trusts

Ineligible for LTC coverage for a specific period of time

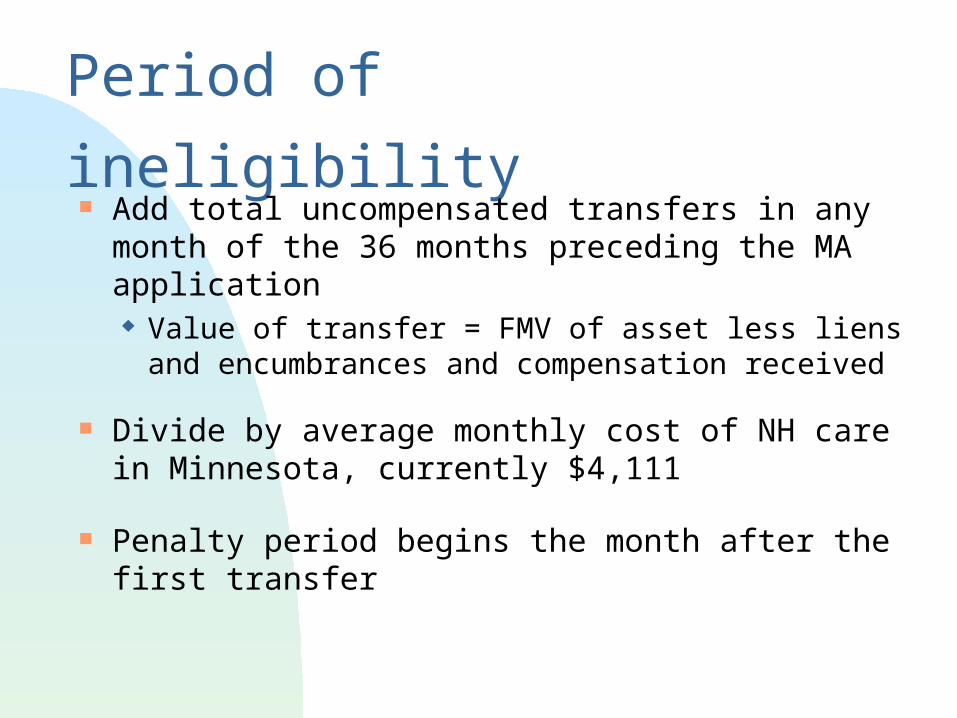

Period of ineligibility Add total uncompensated transfers in any month

of the 36 months preceding the MA application Value of transfer = FMV of asset less liens and

encumbrances and compensation received

Divide by average monthly cost of NH care in Minnesota, currently $4,111

Penalty period begins the month after the first transfer

Transfer $15,000 in June 2004

$15,000 ÷ $4,111 = 3.64 months

PERIOD OF INELIGIBILITY

Transfer made in June

7/04 ----------------------------------10/04 (.64)

Transfer $50,000 in June 2004$50,000 ÷ $4,111 = 12.16 months

PERIOD OF INELIGIBILITY

Transfer made in June

7/04 ----------------------------------7/05 (.16)

Transfer $200,000 in June 2004

$200,000 ÷ $4,111 = 48.64 months

Period of Ineligibility

If apply before July 2007 (within 36 months), full POI is imposed.

If wait to apply until after 36 months:

June 2004 --------------- July 2007The effective waiting period is 37 months.

APPLY JULY 2007 AT THE EARLIEST

A transfer occurs when:An applicant or spouse Sells Gives away Reduces ownership interest Reduces control Disposes of asset or interest therein Waives right to or refuses inheritance

Refuses to claim elective share Disclaims

Allowable transfers of home To spouse To child under 21 To blind or disabled child To sibling with equity interest To caretaker child For value Denial of eligibility causes undue

hardship

Other exceptions to transfer rules $200 or less per month To spouse at any time, or to 3rd

person for sole benefit or spouse To disabled or blind child or SNT for

sole benefit of child Transfer into SNT for sole benefit of

any disabled person under age 65

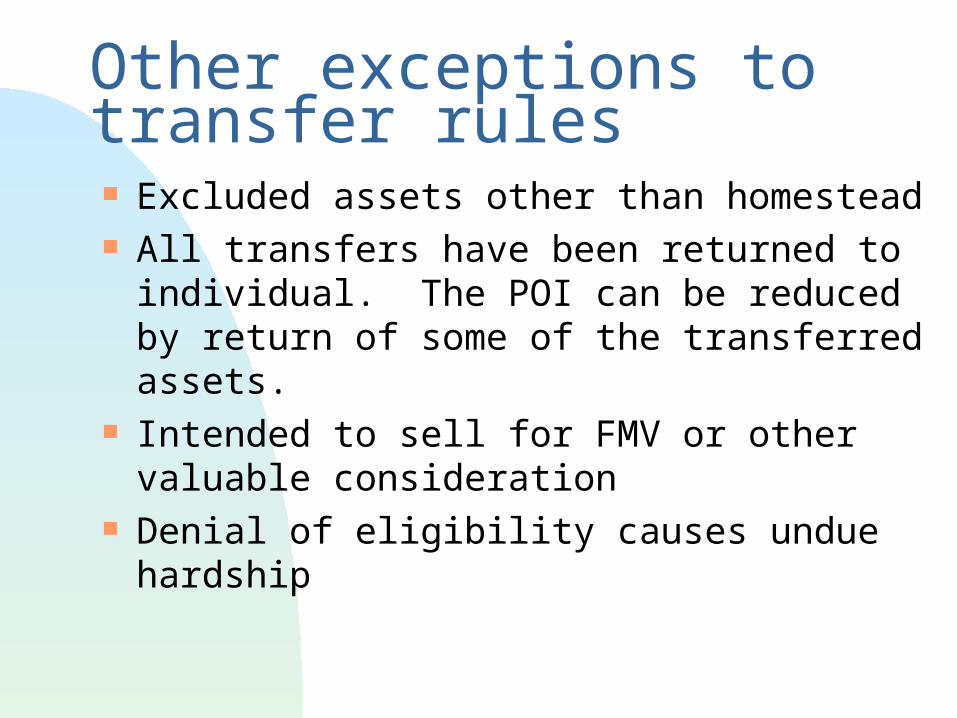

Other exceptions to transfer rules Excluded assets other than homestead All transfers have been returned to

individual. The POI can be reduced by return of some of the transferred assets.

Intended to sell for FMV or other valuable consideration

Denial of eligibility causes undue hardship

Proposed changes in transfer lawSee waiver request at http://www.dhs.state.mn.us/HealthCare/waivers/default.htm

72-month lookback period

Average payment used for divisor

POI begins in month person applies and is eligible for MA

Complete ineligibility for MA

Proposed changes to transfer law(cont.)

Homestead cannot be transferred to spouse,

sibling, caretaker child, disabled child, child under

21

No transfers to spouse after MA eligibility

No transfers to blind/disabled child

No transfers of excluded assets

DHS will decide permissible purposes of trusts

Liens and Estate Recovery Medical Assistance and Alternative

Care liens Notice of Potential Claim against real

estate interests Elective share claims Estate recovery, including claims

against life estate and joint tenancy interests

Thank you for your attention!

Long & Reher, P.A.

5881 Cedar Lake Road

Minneapolis, Minnesota 55416

(952) 929-0622

www.longreher.com