2015 - odin hosting & cloud automation platforms · • search engine optimization (seo) •...

TRANSCRIPT

SMB Cloud InsightsTM

2015

JAPAN

d

DEFINITIONS

Cloud Services DefinedThis research focuses on the cloud services that matter most to SMBs: IaaS, web presence and web applications, unified communications, and other general business applications.

Infrastructure-as-a-service (IaaS): • Cloud servers (previously not researched in our last study of Japan)

• Dedicated servers

• Virtual private servers (VPS)

• Managed hosting

• Add-on applications and services for hosted infrastructure:

• Control panels• Development platforms • LAMP stack • Security• Server backup

Web presence and web applications: • Third-party web hosting

• Domain registration

• Web applications:

• Content delivery networks (CDN)• Content management systems (CMS) • E-commerce • Health monitoring• Mobile optimization tools• Search engine optimization (SEO)• Site-building tools• SSL• Web server backup• Web server security

Unified communications: • Communication and collaboration applications:

• Web and phone conferencing• Instant collaboration • Mobile device management (MDM)

• Business-class email services:

• Email security and archiving

• Business voice services:

• Mobility and hosted phone services such as hosted PBX

General business applications:

• Major software applications accessible online:

• File sharing• Online accounting • Online backup and storage • Online customer relationship management (CRM)• Payroll and HR• Support and help desk• Virtual desktop (VDI)

SMB DefinedWe define SMBs – also known as small and medium enterprises (SMEs) – as companies with one to 250 employees. There are around 1.8 million SMBs in Japan today. SMB categories include micro (1-9 employees), small (10-49 employees), and medium (50-250 employees).

1

2

Odin SMB Cloud Insights™ has entered its fifth year of research into the consumption of cloud services by small and medium businesses (SMBs). After interviewing more than 400 IT decision makers at Japanese SMBs, we found many important trends in this market. Globally and locally, SMBs from a variety of sectors are moving business functions into the cloud. Tools and solutions previously reserved for enterprise-level organizations are being implemented in smaller firms as developers create services specifically for the SMB market.

Our research is intended to help cloud service providers take advantage of the trends outlined in this report in order to meet the evolving needs of their SMB customers. New to this year’s research is an exploration of the SMB’s journey of researching, purchasing, and using cloud services. This data will help service providers build successful relationships with their customers.

Note: This report uses a JPY-USD exchange rate of 118.21. This value is calculated using a one-year exponentially weighted rolling average.

Overall SMB Cloud Services Market in Japan

¥339B

($2.9B USD)

2015

Infrastructure-as-a-service

Web presence Unified communications

Business applications

($1,100M USD)

¥130B($451M USD)

¥53B ¥59B ¥97B($499M USD) ($818M USD)

3

INFRASTRUCTURE-AS-A-SERVICE (IaaS)

Top Barriers to Hosted Infrastructure

Buying IaaS

Japan’s infrastructure-as-a-service market has seen significant growth in recent years. Due to capital constraints and an increasing need for flexibility, Japanese SMBs are moving away from in-house to hosted infrastructure. More than half of SMBs with servers use a hosted server, and many of those with in-house servers are looking to move toward a hosted solution in coming years.

Total Server Add-ons by Industry54% of SMBs with servers use a hosted server

46% of SMBs with servers use an in-house server

Micro Small

Price Legacy systems and other tech concerns

Security or privacy concerns

36%39%25%41%38%92% 47%22%38%

Medium

4

IaaS Research Methods

Top Factors in Choosing Service Provider

Online

Price

Discuss with a trusted advisor

Ability to expand or contract quickly

From existing service providers

Ease of management

Business industry news

Existing relationship

Security or privacy concerns

16%

16%

15%

10%7%

17%

17%

46%

50%

Top IaaS Purchase Locations

Web hoster

Local IT resource (VAR)

Retail computer store

Pure cloud infrastructure/

service provider

Telco or cable co

62%8%

8%8%

7%

5

Top Workloads in Production

Using IaaS

Content management

system

Database applications

Data mining/ analytics

Payroll, HR, and benefit

management

35% 31% 26% 21% 19% 11% 10%22% 36% 19% 23% 17%

Customer relationship

management (CRM)

Accounting/ financials

Micro/small (1-49 employees) Medium (50-249 employees)

Top Hosted Server Add-ons

Control panel Security Server backup

28% 36% 23% 17% 12% 11%40% 32% 23% 14%

Development platform

LAMP stack

2015 2018

6

Opinion of IaaS Service Provider

Areas for Improvement

Customer Experience

Positive40%

2 3 4 51

Performance (speed,

availability)

Support experience

Security vulnerabilities

Usability Self-service administration

31% 22% 21% 19% 7%

Total Server Add-ons by Industry36% of SMBs would pay an additional ¥1,000 per month for high availability

41% of SMBs would pay an additional ¥1,000 per month for unlimited storage

Neutral44%

Negative16%

7

How SMBs are Resolving Issues

Escalating with the vendor

Exploring alternative options

Cancelling the service

Moving in-house

47%33%

10%9%

IaaS Opportunities through 2018

7%CAGR

€487M €706M

2015 2018

¥161B($1,364M USD)

¥130B($1,100M USD)

8

Likelihood of Entering the Cloud Market

Cloud leapers (New adoption)

Cloud converters (Switch from in-house)

15% 29%

The Japanese IaaS market will see steady growth in coming years. Firms are finding value in moving to hosted services, but they also have concerns.

For example, price is a massive barrier for Japanese SMBs and will continue to be an important factor in future IaaS purchasing decisions. As a result, service providers with competitively priced packages will succeed in this market.

In terms of customer satisfaction, only 40% of SMBs have a positive view of their IaaS provider. While this number is low, SMBs would prefer to escalate their issue(s) with their service provider rather than move to a competitor. SMBs in other markets tend to be more willing to leave their service provider rather than escalate a problem. This means that service providers have the opportunity to answer their customers’ concerns and reduce churn. Overall, the IaaS market will continue to offer value to service providers working to gain SMB customers.

9

SMBs with a Company Website

Website Hosting Location

WEB PRESENCE

The web presence market has steadily expanded as firms increase their visibility online. Mobile optimization is becoming more important for SMBs as smartphone usage has skyrocketed in recent years. Additionally, businesses are finding site-building software to be an attractive substitute to costly web professionals. Although this market is relatively mature, there are still strong opportunities within the ¥53B ($451M USD) web presence market.

Micro Small Medium

75%

25% of websites are hosted in-house. Of those SMBs with in-house websites, 18% plan to add a third-party hosted website in three years.

75% of websites are hosted by a third-party.

third-party

92%79%54%

25%in-house

10

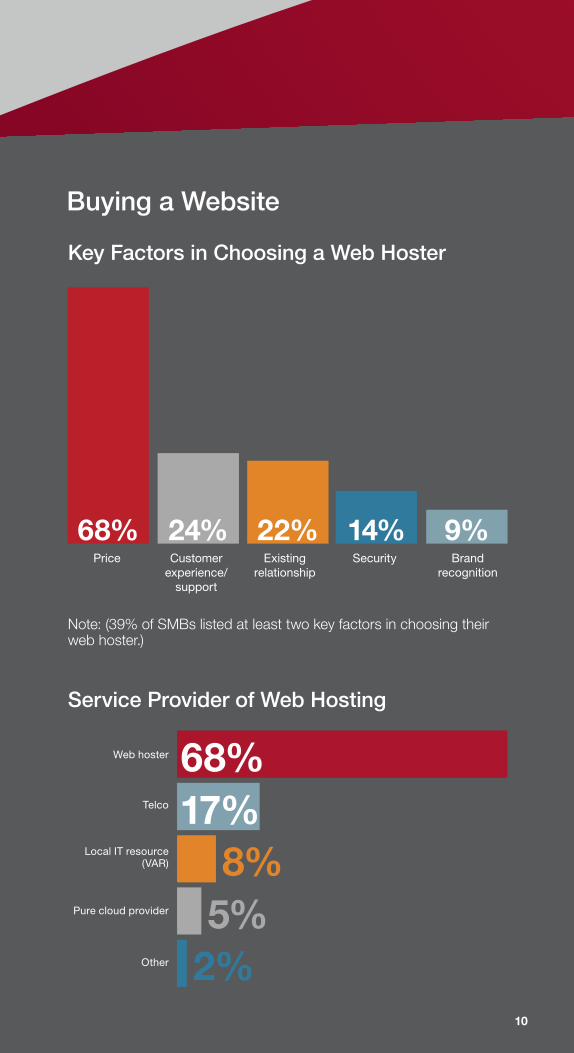

Buying a Website

Key Factors in Choosing a Web Hoster

Note: (39% of SMBs listed at least two key factors in choosing their web hoster.)

Price Customer experience/

support

Existing relationship

Security Brand recognition

22% 14% 9%24%68%

Service Provider of Web Hosting

Web hoster

Telco

Pure cloud provider

Local IT resource (VAR)

Other

68%17%

5%8%

2%10

11

Top Purchase Methods

Website Design

1 2 3 4

Online Face-to-face Over the phone

In a store74% 16% 10% 2%

of websites are designed by a third-party web designer

34%

of websites are designed

in-house

66%

Of in-house used a site builder

29%

Mobile Optimized Website

Only displays properly on a computer38%

Displays on mobile without optimization26%

Mobile optimized36%

12

Website Add-ons and Management

Purchase Location of Add-on

Top Website Add-ons

Web hoster: bundles with website

purchase

Directly from the application developer

Third-party provider

Web hoster: returned after website

purchase

45% 62%

25%13%

17%

Note: In total, 62% of add-ons are purchased from the web hoster.

Backup SSL SEO

19% 29% 17% 16% 14% 10%32% 33% 28% 22%

Security and health monitoring

E-commerce capabilities

2015 2018

13

Website Management

Customer Experience

In-house92%

Web hoster3%

Opinion of Web Provider

Positive38%

Neutral44%

Negative18%

Web designer5%

14

Top Areas for Improvement

How SMBs are Resolving Issues

Performance (speed, availability)

Escalating with the vendor

Security vulnerabilities

Exploring alternative options

Self-service administration

Canceling the service

Support experience

Moving in-house

Usability

43%

49%

23%

35%

6%

7%

22%

7%

5%

14

15

The Japanese web presence market is expected to grow to ¥61B ($529M USD) by 2018 at a CAGR of 4.8%. Drivers within this market will be the increased need for mobile optimization and the growing use of site builders. Web hosters remain the main sellers of websites and website add-ons. However, they are being challenged by telcos and cloud service providers that are edging into the market. Maintaining customer relationships while answering the growing importance of mobile optimization will be key to gaining ground in this competitive marketplace.

Web Presence Opportunities through 2018

4.8%CAGR

¥61B ($529M USD)

¥53B ($451M USD)

2015 2018

Likelihood of Entering the Cloud Market

Cloud leapers (New adoption)

Cloud converters (Switch from in-house)

15% 18%

16

UNIFIED COMMUNICATIONS

Hosted solutions for internal and external communications are growing in usage among SMBs. Hosted email is increasingly driven by the need for security while hosted business voice services are driven by cost savings. Although many SMBs currently use traditional landlines and free email services, we expect to see a sizeable number of cloud adopters in coming years.

Note: 14% of SMBs do not use email.

Hosted on an in-house server

Free serviceHosted by a service provider

48% 34% 4%

Top Purchase Triggers for Premium Hosted Email

2 31

Increased need for security

Good price point

Need for professional look and feel

17

Opinion of Email Service Provider

Positive30%

Negative26%

Neutral44%

Total Server Add-ons by Industry54% of third-party hosted email is bundled with website hosting or a hosted server

Top Areas for Improvement

Performance (speed, availability)

Security vulnerabilities

Usability

Support experience

40%33%22%19%

18

How SMBs are Resolving Issues

Escalating with the vendor

Exploring alternative options

Cancelling the service

Moving in-house

39%27%

8%17%

Hosted Business Voice Services

Main Barriers to Hosted Business Voice Services

16%

14%

70% of SMBs do not have business voice services

of SMBs have in-house business voice services

of SMBs have hosted business voice services

Security and privacy concerns

Lack of knowledge about hosted business

voice services

Technical concerns

Price

16%42% 12%30%

Hosted

In-house

Do not have

19

Top Purchase Triggers for Hosted Business Voice Service

Top Features that Improve Productivity

Top Features that Improve Customer Satisfaction

2

2

1

1

Good price point

Single number reach

Automated attendant

30%Business has

explosive growth

Smartphone client

Integration with employee’s mobile devices

25%Major

change to business

20%

20

Opinion of Hosted Business Voice Services Provider

Neutral55%

Positive32%

Negative13%

Top Areas for Improvement

Performance (speed, availability)

Security vulnerabilities

Usability

Support experience

38%25%20%12%

21

How SMBs are Resolving Issues

Collaboration Applications

Escalating with the vendor

Exploring alternative options

Moving in-house

Cancelling the service

48%34%15%3%

Web conferencing Instant collaboration

Mobile device management

5% 12% 9% 3%16% 10%

2015 2018

22

Cloud leapers(New adoptions)

Cloud converters(Switch from in-house)

Likelihood of Entering the Cloud Market

8%19% 30%7%

Email Hosted PBX

Unified Communications Opportunities through 2018

8%CAGR

€487M €706M

2015 2018

¥74B($623M USD)

¥59B($499M USD)

The unified communications category will grow to ¥74B ($623M USD) by 2018. As noted earlier, price is a major barrier for cloud services. However, we expect many SMBs to purchase these services when presented with an affordable offering. Growth in the hosted email category will come significantly from SMBs without an email system while hosted business voice services will see growth from SMBs with traditional landlines. With an 8% CAGR and a strong interest by SMBs, service providers will derive significant value from the unified communications market in coming years.

23

BUSINESS APPLICATIONS

The business applications market is currently the second-largest category within the Japanese cloud market. Firms are deriving value from the flexibility and low overhead cost of hosted applications. Certain trends – particularly research methods – are different depending on firm size. Smaller firms rely heavily on online searching while larger firms are more likely to look toward trusted advisors and their existing service providers.

Business Application Research Methods

Most Important Factors in Choosing Business Applications

Micro Small

Online research

Local IT resource

Industry news

Existing service provider

Trusted advisor

25%16%23%

15%

19%

9%

26%

12%

50%

5%

29%24%

12%

29%

6%

Medium

Price Features and capabilities

Business need

Customer experience

48% 31% 12% 9%

24

Trial Software

64% Purchased without a free trial

Purchasing

Bundling

Bundling

With bundle21

Hosted server

Broadband

88%Separate from bundle

12%With bundle

36% Purchased with a free trial

24

25

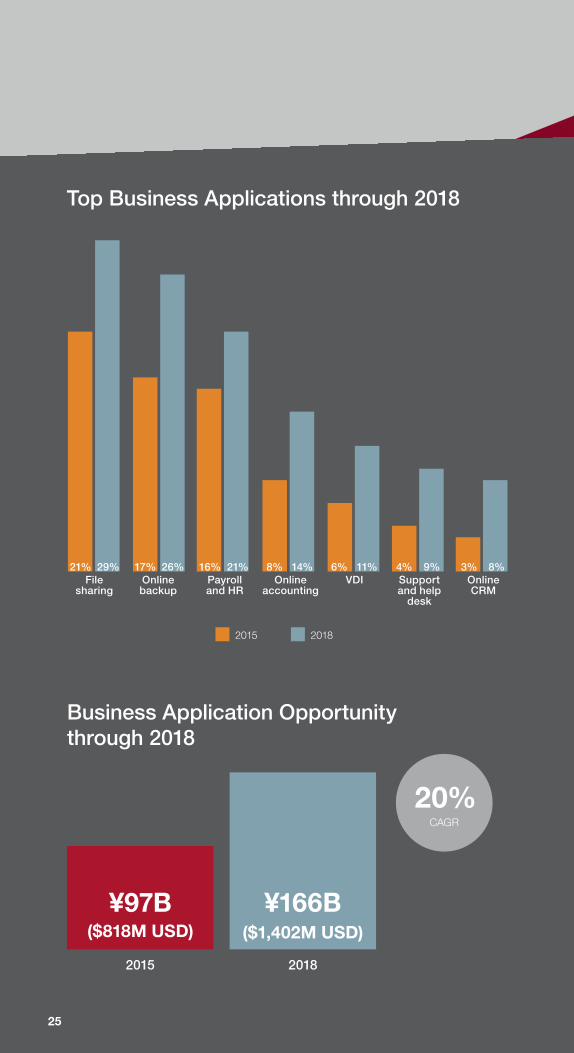

Top Business Applications through 2018

2015 2018

Business Application Opportunity through 2018

20%CAGR

¥166B ($1,402M USD)

¥97B ($818M USD)

2015 2018

File sharing

Online backup

Payroll and HR

Online accounting

VDI Support and help

desk

Online CRM

8%9% 3%4%6%8%16%17%21% 11%14%21%26%29%

26

Overall Cloud Services Opportunity through 2018

Business applications is slated to become the largest category over the next three years. This is a result of an increasingly crowded marketplace with high-quality offerings. SMBs are taking advantage of this trend since capital constraints make large in-house software purchases impossible. Service providers have the potential to grow their customer base but they must also offer best-in-breed services and transparent pricing. Overall, this expanding market will introduce SMBs to the many advantages of cloud services.

IaaS Web presence Unified communications

Business applications

¥161B

¥130B¥61B

¥74B

¥59B

¥97B

¥166B

¥53B

20182015

7% CAGR

5% CAGR8% CAGR

20% CAGR

26

27

11%CAGR

($2.9B USD)

¥339B

2015

($3.9B USD)

2018

¥462B

The Japanese cloud market will grow at a CAGR of 11% over the next three years. Business applications and communications tools will be the key drivers of this growth. Throughout this research, we have found that Japanese SMBs are extremely price-conscious and also place significant value on business relationships. Service providers who offer competitively priced products coupled with quality customer service will be in the best position to take advantage of the continued growth within this market.

28

Learn MoreOdin is committed to helping our partners understand the best opportunities in the SMB cloud market.

This report covers only a portion of the extensive data included in Odin SMB Cloud Insights™ research. Please contact [email protected] with questions.

About OdinOdin provides software that powers the cloud ecosystem, from small and local hosters to some of the world’s largest telecommunications providers. By partnering with Odin, service providers gain access to industry expertise, a catalog of the most in – demand cloud applications, and the most comprehensive selection of software including web server management, server virtualization, provisioning, and billing automation. With offices in 15 countries, Odin supports more than 10,000 service providers in delivering applications and cloud services to more than 10 million SMBs. For more information, visit www.odin.com, follow us on Twitter, or like us on Facebook.

© 2015 Parallels IP Holdings GmbH. All rights reserved. Odin and the Odin logo are trademarks of Parallels IP Holdings GmbH.

No part of this publication may be reproduced, photocopied, stored on a retrieval system, or transmitted without the express written consent of Parallels.

GLOBAL HEADQUARTERS500 SW 39th Street

Suite 200 Renton, WA 98057

USA main: +1 425 282 6400

EMEAWilly-Brandt-Platz 3

81829 Munich Germany

main: +49 89 450 80 86 -0 [email protected]

APAC 3 Anson Road, #36-01

Springleaf Tower 079909 Singapore

main: +65 6645 3290 [email protected]

For more office locations: www.odin.com/contact