141124 cash management cash forecasting

TRANSCRIPT

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

2.2. Cash Forecasting

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

1. Construct a cash forecast and automate the creation of some of the information contained within it;

2. Create a feedback loop for gradually increasing the accuracy of the forecast;

3. Describe several related topics, including the bullwhip effect and the integration of business cycle forecasting into the cash forecast.

Objectives

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

o Is used to estimate liquidity position of the company for periods ranging from the current day up to one year.

o Short term forecasts (0-3) months are used primarily for managing liquidity.

o Operational forecasts (1-12 months) are used for medium term working capital and financing requirements.

o Long-term forecasts (1-5 years) are used for planning strategic financial goals.

Cash Forecasting

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

o Combines what is known about expected receipts (e.g. collections form customers, interest, and maturing investments with expected disbursement (e.g. expected check presentments, payroll, taxes, interest payments, and loan repayments).

Cash Budgeting

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

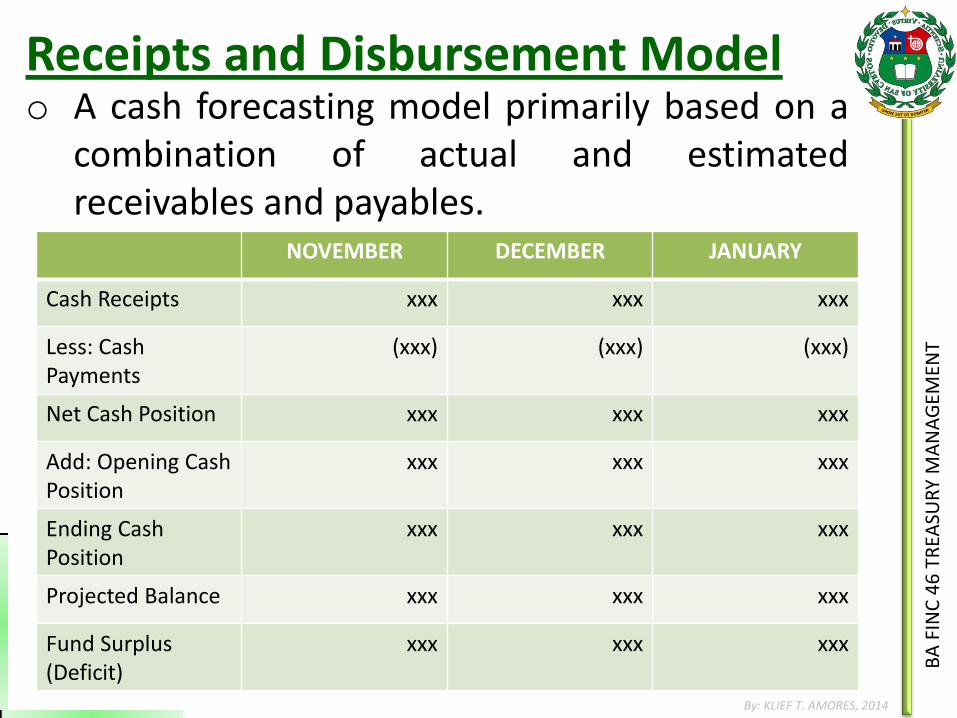

o A cash forecasting model primarily based on a combination of actual and estimated receivables and payables.

Receipts and Disbursement Model

NOVEMBER DECEMBER JANUARY

Cash Receipts xxx xxx xxx

Less: Cash Payments

(xxx) (xxx) (xxx)

Net Cash Position xxx xxx xxx

Add: Opening Cash Position

xxx xxx xxx

Ending Cash Position

xxx xxx xxx

Projected Balance xxx xxx xxx

Fund Surplus (Deficit)

xxx xxx xxx

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

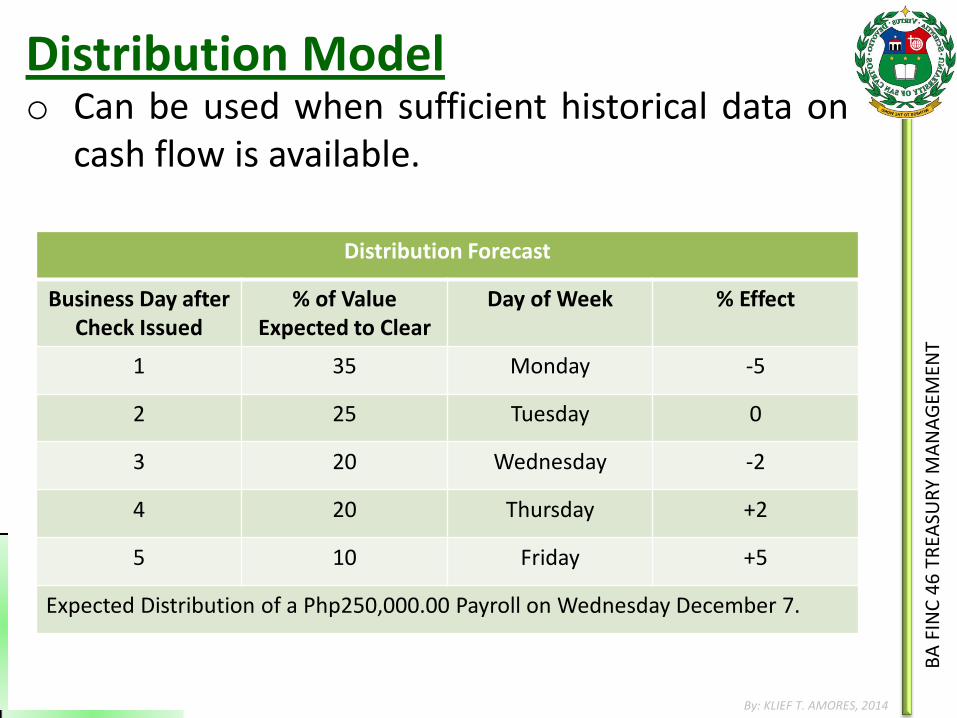

o Can be used when sufficient historical data on cash flow is available.

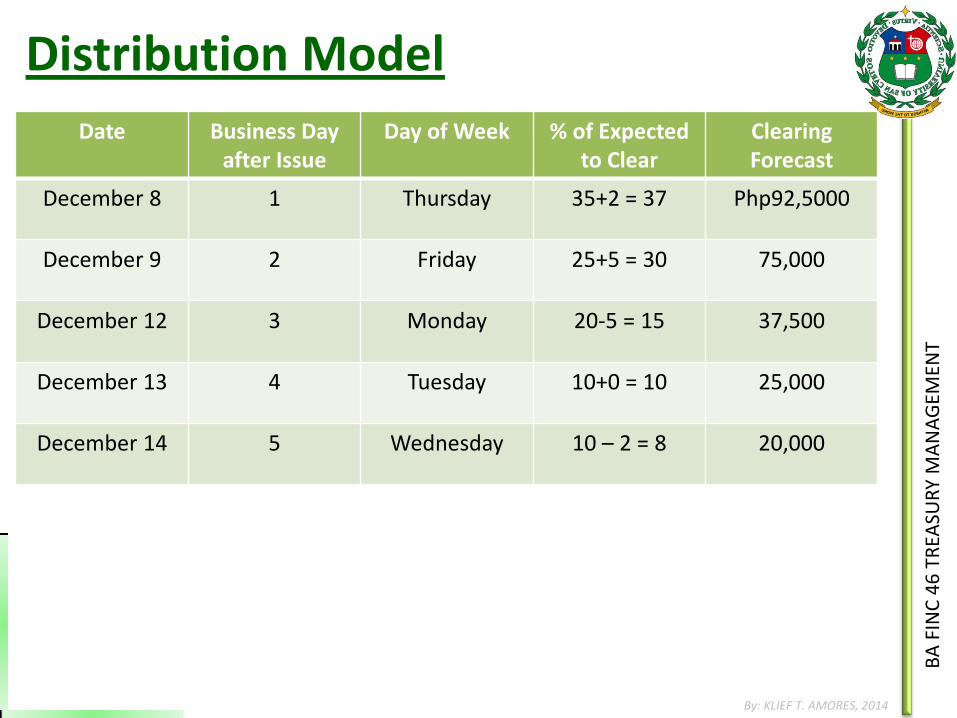

Distribution Model

Distribution Forecast

Business Day after Check Issued

% of Value Expected to Clear

Day of Week % Effect

1 35 Monday -5

2 25 Tuesday 0

3 20 Wednesday -2

4 20 Thursday +2

5 10 Friday +5

Expected Distribution of a Php250,000.00 Payroll on Wednesday December 7.

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

Distribution Model

Date Business Day after Issue

Day of Week % of Expected to Clear

Clearing Forecast

December 8 1 Thursday 35+2 = 37 Php92,5000

December 9 2 Friday 25+5 = 30 75,000

December 12 3 Monday 20-5 = 15 37,500

December 13 4 Tuesday 10+0 = 10 25,000

December 14 5 Wednesday 10 – 2 = 8 20,000

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

o Used for long-term forecast. Uses historical data thus, it is possible to extrapolate relationships between certain elements of the profit and loss statement and the balance sheet.

Cash Modelling

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

Cash Modelling Pro Forma Financials

(Amount in Thousand of Pesos)

Profit and Loss

Actual Projected Balance Sheet Actual Projected

Sales 4,000 4,600 Cash 350 403

COGS -3,000 -3,450 Receivable 500 575

Selling / Admin Costs

-500 -575 Inventory 200 230

Depreciation -100 -85 Net Assets 650 565

Interest Exp. -31 -16 Total Assets 1,700 1,773

EBIT 369 474 Payables 650 748

Tax (40%) -148 -190 Long-Term Debt 350 200

Net Income 221 284 Equity 700 884

Dividends -100 Total Liabilities 1,700 1,832

Retained Earnings

184 Net Surplus 59

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

o A more complex statistical technique, usually performed using a computer.

Regression Analysis

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

Availability of Data. Using information that is readily available makes it possible for the cash manager to produce a timely forecast. Unfortunately, businesses typically do not maintain data in formats that allow easy access for statistical analysis.

Choosing a Forecasting Method

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

Reliability of Data. In producing the forecast, the cash manager will have to assess the probability of being correct about the timing of cash flows. Assured Cash Flows. (e.g. tax payments,

dividends, debt repayments, and maturing investments)

Reliable Cash Flows. (e.g. collection from credit sales, payroll, vendor payments)

Unreliable cash flows. (e.g. foreign currency collections, outcome of pending lawsuits, and costs of work stoppages.)

Choosing a Forecasting Method

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

Reliability of Data. Unanticipated Cash Flow. (e.g. cash

inflows or outflows resulting from totally unexpected circumstances such as outbreak of war in an area where company is involved, or the opportunity to buy up inventory due to a competitor going out of business)

Time Horizon. The more distant in time the forecast, the less accurate and the less useful it becomes to the cash manager.

Choosing a Forecasting Method

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

Reliability of Data. Sensitivity. Things change, and the cash

manager must be prepared to review, refine, and adjust the forecast frequently in light of internal and external amendments.

Choosing a Forecasting Method

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

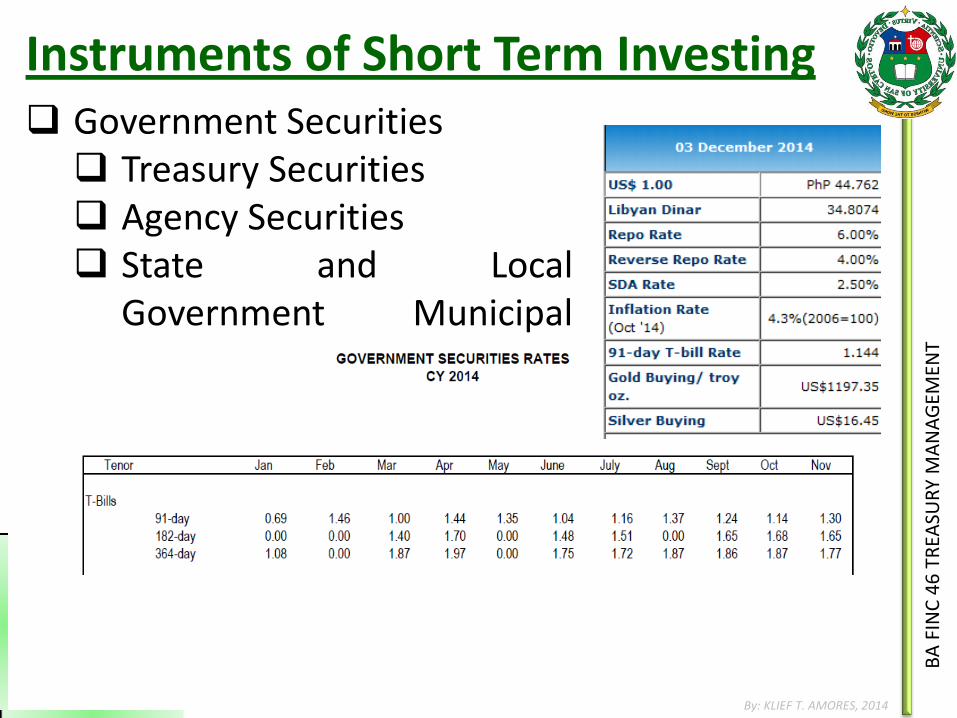

Government Securities Treasury Securities Agency Securities State and Local

Government Municipal Obligations

Instruments of Short Term Investing

BA

FIN

C 4

6 T

REA

SUR

Y M

AN

AG

EMEN

T

By: KLIEF T. AMORES, 2014

THANK YOU!